A Multidimensional Comparative Analysis of Involvement in CSR Activities of Energy Companies in the Context of Sustainable Development Challenges: Evidence from Poland

Abstract

1. Introduction

- What is the importance of CSR in the energy industry in the context of sustainable development challenges?

- What factors motivating energy companies to engage in CSR have so far been identified by various researchers?

- What are the problems of assessing companies’ engagement in CSR on the basis of information contained in reports?

- What is the CSR commitment of Polish energy companies listed on the Warsaw Stock Exchange in general and broken down into individual dimensions/aspects?

2. Literature Review

2.1. The Importance of CSR in the Energy Industry

- social responsibility (personnel’s welfare, skills, and motivation; open interaction with stakeholders; the quality of energy supply; good practice of business and cooperation with the stakeholders, networking with other companies; and correct price for energy);

- environmental responsibility (measurement of environmental impact; awareness and reduction of environmental impacts of energy production and transfer; minimisation of use of fossil fuels; reduction of pollution and emissions; renewable sources development; and control systems for waste and pollution); and

- economic responsibility (cost-effective operations; fair prices and good service; investing in new technologies; reliability of energy supply; and financial risk management).

2.2. Motives of Energy Companies’ Involvement in CSR

- ethical and altruistic motives;

- the desire to obtain various benefits including financial ones; and

- to respond to social expectations and stakeholder pressure.

2.3. Dilemmas in Assessing Companies’ Involvement in CSR

- certification and accreditation, refering to the use of international standards: SA 8000, ISO26000, and ISO14001 [58];

- analysis of CSR content included in annual reports, financial statements (according to GRI guidelines or AccountAbility1000Standard), and websites; and

- measuring the attitudes and value system of individuals using a rating scale [67].

3. Materials and Methods

- xtj is the value of the j-th assessment criterion in the t-th test period

- and ztj is the normalised value of the j-th assessment criterion in the t-th test period (from 0 to 1).

4. Results

5. Discussion

5.1. The Importance of CSR in the Energy Sector

- social and ethical responsibility concerning the quality of the energy supply, cooperation with stakeholders, and interaction with partners in supply chains;

- environmental responsibility concerning primarily the reduction of pollution and CO2 emissions; and

- economic responsibility concerning the costs of energy production, energy transmission, and the reliability of the energy supply to all sectors of the economy.

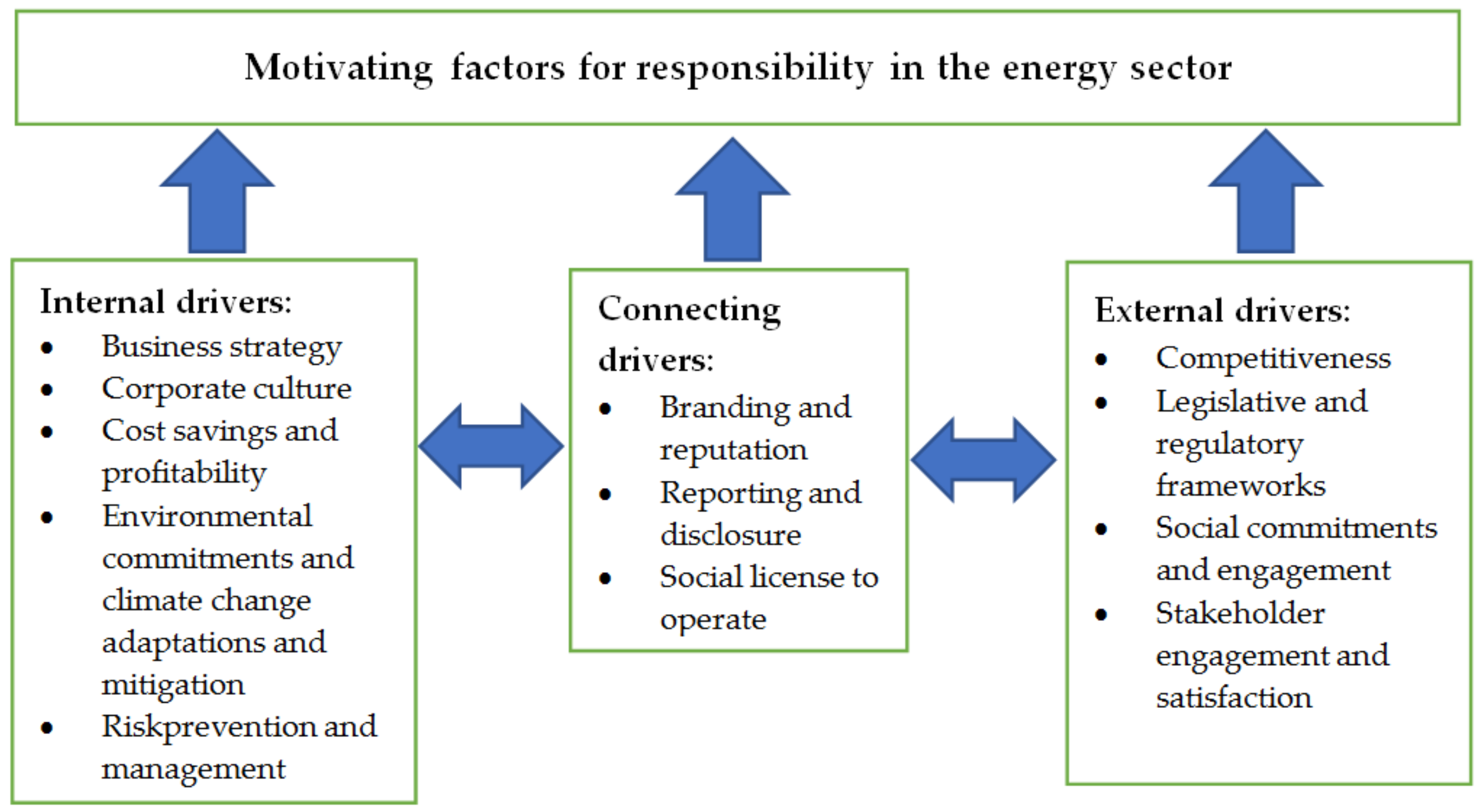

5.2. Factors Motivating Energy Companies to Engage in CSR Activities

- increasing competition in the industry, related to the use of renewable energy sources;

- the increasing number of national and international regulations introduced due to climate change (CO2 emission limits); and

- the pressure of different stakeholder groups and the need to obtain a kind of social license to operate [52].

5.3. The Problem of Assessing and Measuring Companies’ Involvement in CSR Activities on the Basis of Publicly Available Information Published in Periodic Reports

- the lack of a universal CSR reporting obligation and

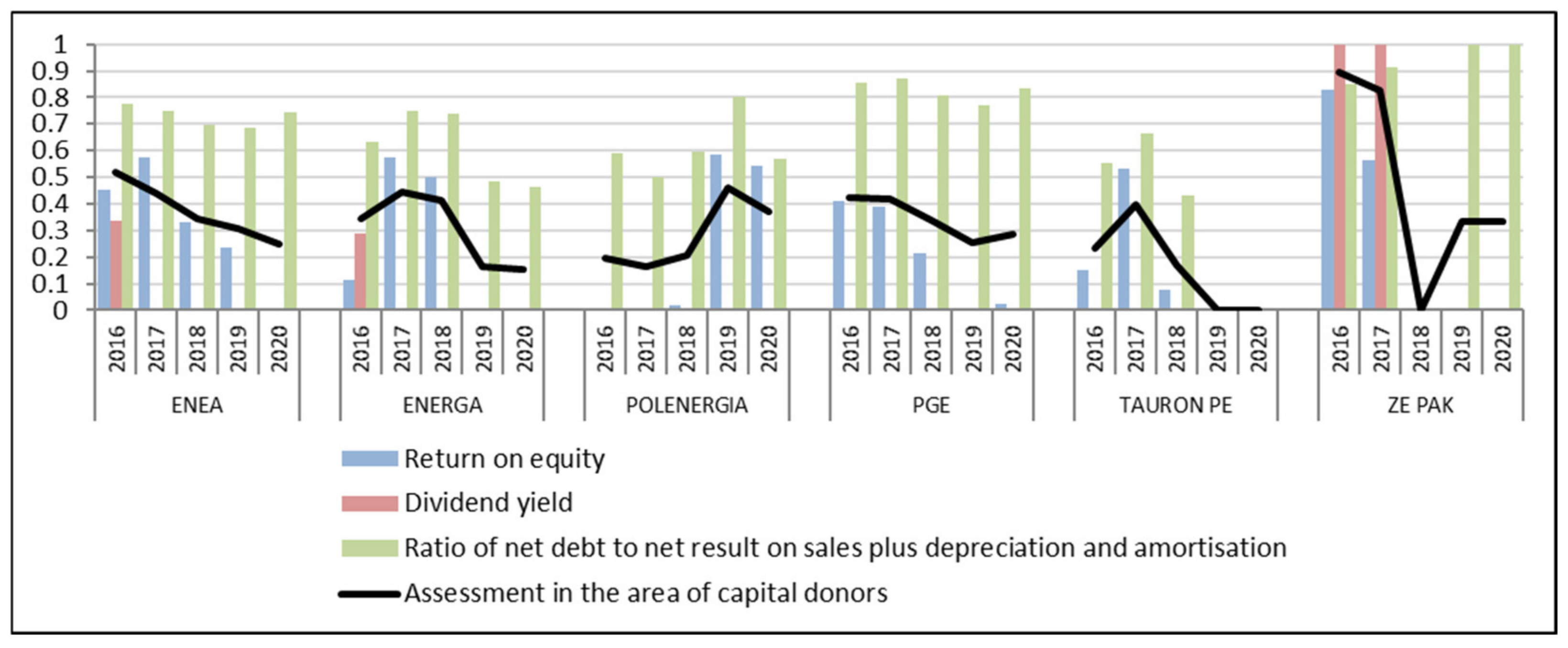

5.4. Assessment of the Involvement of Polish Energy Companies in CSR Activities

6. Conclusions and Policy Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wang, H.; Tong, L.; Takeuchi, R.; George, G. Corporate Social Responsibility: An overview and new research directions thematic issue on Corporate Social Responsibility. Acad. Manag. J. 2016, 59, 534–544. [Google Scholar] [CrossRef]

- Valente, M. Business sustainability embeddedness as a strategic imperative: A process framework. Bus. Soc. 2015, 54, 126–142. [Google Scholar] [CrossRef]

- Idowu, S.-O.; Dragu, I.-M.; Tiron-Tudor, A.; Farcas, T.-V. From CSR and sustainability to integrated reporting. Int. J. Soc. Entrep. Innov. 2016, 4, 134–151. [Google Scholar] [CrossRef]

- Kolk, A. The social responsibility of international business: From ethics and the environment to CSR and sustainable development. J. World Bus. 2016, 51, 23–34. [Google Scholar] [CrossRef]

- Zhang, D.; Morse, S.; Kambhampati, U. Sustainable Development and Corporate Social Responsibility; Routledge: New York, NY, USA, 2017; pp. 46–94. [Google Scholar]

- Jain, R.; Winner, L.H. CSR and sustainability reporting practices of top companies in India. Corp. Commun. Int. J. 2016, 21, 36–55. [Google Scholar] [CrossRef]

- Our Common Future: Report of the World Commission on Environment and Development. Available online: http://www.un-documents.net/ocf-02.htm (accessed on 7 April 2021).

- De Jong, M.D.T.; van der Meer, M. How Does It Fit? Exploring the Congruence Between Organizations and Their Corporate Social Responsibility (CSR) Activities. J. Bus. Ethics 2015, 143, 71–83. [Google Scholar] [CrossRef]

- Zieliński, M.; Jonek-Kowalska, I. Profitability of Corporate Social Responsibility Activities from the Perspective of Corporate Social Managers. Eur. Res. Stud. J. 2020, 13, 264–280. [Google Scholar] [CrossRef][Green Version]

- Yang, S.; Chen, W.; Kim, H. Building Energy Commons: Three Mini-PV Installation Cases in Apartment Complexes in Seoul. Energies 2021, 14, 249. [Google Scholar] [CrossRef]

- Stjepcevic, J.; Siksnelyte, I. Corporate Social Responsibility in Energy Sector. Transform. Bus. Econ. 2017, 16, 21–33. [Google Scholar]

- Lu, L.; Ren, L.; Qiao, J.; Yao, S.; Strielkowski, W.; Streimikis, J. Corporate Social Responsibility and Corruption: Implications for the Sustainable Energy Sector. Sustainability 2019, 11, 4128. [Google Scholar] [CrossRef]

- Clift, R. Climate change and energy policy: The importance of sustainability arguments. Energy 2007, 32, 262–268. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I. How do turbulent sectoral conditions sector influence the value of coal mining enterprises? Perspectives from the Central-Eastern Europe coal mining industry. Resour. Policy 2018, 55, 103–112. [Google Scholar] [CrossRef]

- García- Rodríguez, F.; García- Rodríguez, J.; Castilla- Gutiérrez, C.; Major, S. Corporate social responsibility of oil companies in developing countries: From altruism to business strategy. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 371–384. [Google Scholar] [CrossRef]

- Groza, M.D.; Pronschinske, M.R.; Walker, M. Perceived organizational motives and consumer responses to proactive and reactive CSR. J. Bus. Ethics 2011, 102, 639–652. [Google Scholar] [CrossRef]

- Garay, L.; Font, X. Doing good to do well? Corporate social responsibility reasons, practices and impacts in small and medium accommodation enterprises. Int. J. Hosp. Manag. 2012, 31, 329–337. [Google Scholar] [CrossRef]

- Morsing, M.; Schultz, M. Corporate social responsibility communication: Stakeholder information, response and involvement strategies. Bus. Ethics A Eur. Rev. 2006, 15, 323–338. [Google Scholar] [CrossRef]

- Becker-Olsen, K.L.; Cudmore, B.A.; Hill, R.P. The impact of perceived corporate social responsibility on consumer behavior. J. Bus. Res. 2006, 59, 46–53. [Google Scholar] [CrossRef]

- Izzo, M.F.; di Donato, F. The Relation between Corporate Social Responsibility and Stock Prices: An Analysis of the Italian Listed Companies. Available online: http://ssrn.com/abstract=1986324 (accessed on 4 May 2021). [CrossRef]

- Tang, Z.; Eiríkur Hull, C.; Rothenber, S. How Corporate Social Responsibility Engagement Strategy Moderates the CSR–Financial Performance Relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Serveas, H.; Tamayo, A. The Impact of Corporate Social Responsibility on Firm Value: The Role of Customer Awareness. Manag. Sci. 2013, 59, 1045–1061. [Google Scholar] [CrossRef]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate Social Responsibility and Access to Finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Flammer, C. Does corporate social responsibility lead to superior financial performance? A regression discontinuity approach. Manag. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef]

- Malik, M. Value-enhancing capabilities of CSR: A brief review of contemporary literature. J. Bus. Ethics 2015, 127, 419–438. [Google Scholar] [CrossRef]

- Zhao, X.; Murrell, A.J. Revisiting the corporate social performance-financial performance link: A replication of Waddock and Graves. Strateg. Manag. J. 2016, 37, 2378–2388. [Google Scholar] [CrossRef]

- Mattingly, J.E. Corporate social performance: A review of empirical research examining the corporation-society relationship using Kinder, Lydenberg, Domini social ratings data. Bus. Soc. 2017, 56, 796–839. [Google Scholar] [CrossRef]

- Shahzad, A.M.; Sharfman, M.P. Corporate social performance and financial performance sample-selection issues. Bus. Soc. 2017, 56, 889–918. [Google Scholar] [CrossRef]

- Pätäri, S.; Arminen, H.; Tuppura, A.; Jantunen, A. Competitive and responsible? The relationship between corporate social and financial performance in the energy sector. Renew. Sustain. Energy Rev. 2014, 37, 142–154. [Google Scholar] [CrossRef]

- Shahbazab, M.; Karaman, A.-S.; Kilic, M.; Uyar, A. Board attributes, CSR engagement, and corporate performance: What is the nexus in the energy sector? Energy Policy 2020, 143, 111582, 1–4. [Google Scholar] [CrossRef]

- Haigh, M.M.; Dardis, F. The impact of apology on organization–Public relationships and perceptions of corporate social responsibility. Public Relat. J. 2012, 6, 1–16. [Google Scholar]

- Fatma, M.; Rahman, Z.; Khan, I. Building company reputation and brand equity through CSR: The mediating role of trust. Int. J. Bank Mark. 2015, 33, 840–856. [Google Scholar] [CrossRef]

- Cheng, S.; Lin, K.Z.; Wong, W. Corporate Social Responsibility Reporting and Firm Performance: Evidence from China. J. Manag. Gov. 2016, 20, 503–523. [Google Scholar] [CrossRef]

- Aksak, E.O.; Ferguson, M.A.; Dumari, S.A. Corporate social responsibility and CSR fit as predictors of corporate reputation: A global perspective. Public Relat. Rev. 2016, 42, 79–81. [Google Scholar] [CrossRef]

- Cowan, K.; Guzman, F. How CSR reputation, sustainability signals, and country-of-origin sustainability reputation contribute to corporate brand performance: An exploratory study. J. Bus. Res. 2020, 117, 683–693. [Google Scholar] [CrossRef]

- Sparkes, R.; Cowton, C.J. The maturing of socially responsible investment: A review of the developing link with corporate social responsibility. J. Bus. Ethics 2004, 52, 45–57. [Google Scholar] [CrossRef]

- El Ghoul, S.; Guedhami, O.; Kwok, C.C.Y.; Mishra, D.R. Does corporate social responsibility affect the cost of capital? J. Bank. Financ. 2011, 35, 2388–2406. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I. Efficiency of Enterprise Risk Management (ERM) systems. Comparative analysis in the fuel sector and energy sector on the basis of Central-European companies listed on the Warsaw Stock Exchange. Resour. Policy 2019, 62, 405–415. [Google Scholar] [CrossRef]

- Choi, B.; La, S. The impact of corporate social responsibility (CSR) and customer trust on the restoration of loyalty after service failure and recovery. J. Serv. Mark. 2013, 27, 223–233. [Google Scholar] [CrossRef]

- Kim, S. What’s worse in times of product-harm crisis? Negative corporate ability or negative CSR reputation? J. Bus. Ethics 2014, 123, 157–170. [Google Scholar] [CrossRef]

- Lin, C.-P.; Chen, S.-C.; Chiu, C.-K.; Lee, W.-Y. Understanding purchase intention during product-harm crises: Moderating effects of perceived corporate ability and corporate social responsibility. J. Bus. Ethics 2011, 102, 455–471. [Google Scholar] [CrossRef]

- Sprinkle, G.B.; Maines, L.A. The benefits and costs of corporate social responsibility. Bus. Horiz. 2010, 53, 445–453. [Google Scholar] [CrossRef]

- Kim, S.-Y.; Park, H. Corporate social responsibility as an organizational attractiveness for prospective public relations practitioners. J. Bus. Ethics 2011, 103, 639–653. [Google Scholar] [CrossRef]

- Glavas, A.; Kelley, K. The effects of perceived Corporate Social Responsibility on employee attitudes. Bus. Ethics Q. 2014, 24, 165–202. [Google Scholar] [CrossRef]

- Jamali, D. A stakeholder approach to corporate social responsibility: A fresh perspective into theory and practice. J. Bus. Ethics 2008, 82, 213–231. [Google Scholar] [CrossRef]

- Yusoff, H.; Mohamad, S.S.; Darus, F. The influence of CSR disclosure structure on corporate financial performance: Evidence from stakeholders’ perspectives. Procedia Econ. Financ. 2013, 7, 213–220. [Google Scholar] [CrossRef]

- Zhang, A.; Moffat, K.; Lacey, J.; Wang, J.; Gonzalez, R.; Uribe, K.; Cui, L.; Dai, Y. Understanding the social license to operate of mining at the national scale: A comparative study of Australia, China and Chile. J. Clean Prod. 2015, 108, 1063–1072. [Google Scholar] [CrossRef]

- Lacey, J.; Lamont, J. Using social contract to inform social license to operate: An application in the Australian coal seam gas industry. J. Clean. Prod. 2014, 84, 831–839. [Google Scholar] [CrossRef]

- Liu, S.; Kasturiratne, D.; Moizer, J. A hub-and-spoke model for multi-dimensional integration of green marketing and sustainable supply chain management. Ind. Mark. Manag. 2012, 41, 581–588. [Google Scholar] [CrossRef]

- Dong, S.; Xu, L. The impact of explicit CSR regulation: Evidence from China’s mining firms. J. Appl. Account. Res. 2016, 17, 237–258. [Google Scholar] [CrossRef]

- Streimikiene, D.; Simanaviciene, Z.; Kovaliov, R. Corporate social responsibility for implementation of sustainable energy development in Baltic States. Renew. Sustain. Energy Rev. 2009, 13, 813–824. [Google Scholar] [CrossRef]

- Latapí Agudelo, M.-A.; Johannsdottir, L.; Davidsdottir, B. Drivers that motivate energy companies to be responsible. A systematic literature review of Corporate Social Responsibility in the energy sector. J. Clean. Prod. 2020, 274, 119094. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- Michel, N.; Buler, S. Maximizing the benefits of corporate social responsibility. How companies can derive benefits from corporate social responsibility. Eur. Sci. J. 2016, 1, 499–506. [Google Scholar]

- Lunenberg, K.; Gosselt, J.-F.; De Jong, M.-D.-T. Framing CSR fit: How corporate social responsibility activities are covered by news media. Public Relat. Rev. 2016, 42, 943–951. [Google Scholar] [CrossRef]

- Pfau, M.; Haigh, M.M.; Sims, J.; Wigley, S. The influence of corporate social responsibility campaigns on public opinion. Corp. Reput. Rev. 2008, 11, 145–154. [Google Scholar] [CrossRef]

- Frost, G.; Jones, S.; Lee, P. The Measurement and Reporting of Sustainability Information within the Organization: A Case Analysis. In Contemporary Issues in Sustainability Accounting, Assurance and Reporting; Jones, S., Ratnatunga, J., Eds.; Emerald Publishing: Bingley, UK, 2012; pp. 197–225. [Google Scholar]

- Szwajca, D.; Nawrocki, T.L. Możliwości oceny zaangażowania przedsiębiorstw w działania społecznie odpowiedzialne a ich polityka informacyjna w zakresie CSR. Przegląd Organizacji 2016, 4, 44–52. [Google Scholar] [CrossRef]

- Peloza, J. The challenge of measuring financial impacts from investments in corporate social performance. J. Manag. 2009, 35, 1518–1541. [Google Scholar] [CrossRef]

- Nowak, A. Problemy pomiaru społecznej odpowiedzialności przedsiębiorstwa. Pr. Nauk. Uniw. Ekon. We Wrocławiu 2014, 329, 232–240. [Google Scholar]

- Carroll, A.B. A commentary and an overview of key questions on corporate social performance measurement. Bus. Soc. 2000, 39, 466–478. [Google Scholar] [CrossRef]

- Hopkins, M. Measurement of social corporate responsibility. Int. J. Manag. Decis. Mak. 2005, 6, 213–231. [Google Scholar] [CrossRef]

- Marquez, A.; Fombrun, C.J. Measuring corporate social responsibility. Corp. Reput. Rev. 2005, 7, 304–308. [Google Scholar] [CrossRef]

- Fombrun, C.J. List of lists: A Compilation of International Corporate Reputation Ratings. Corp. Reput. Rev. 2007, 10, 144–153. [Google Scholar] [CrossRef]

- Turker, D. Measuring corporate social responsibility: A scale development study. J. Bus. Ethics 2009, 85, 411–427. [Google Scholar] [CrossRef]

- Wood, D.J. Measuring corporate social performance: A review. Int. J. Manag. Rev. 2010, 12, 50–84. [Google Scholar] [CrossRef]

- Maignan, I.; Ferrell, O.C. Measuring Corporate Citizenship in Two Countries: The Case of the United States and France. J. Bus. Ethics 2000, 23, 283–297. [Google Scholar] [CrossRef]

- Crane, A.; Henriques, I.; Husted, B.-W.; Matten, D. Measuring Corporate Social Responsibility and Impact: Enhancing Quantitative Research Design and Methods in Business and Society Research. Bus. Soc. 2017, 56, 787–795. [Google Scholar] [CrossRef]

- Ehsan, S.; Nazir, M.-S.; Nurunnabi, M.; Khan, O.-R.; Tahir, S.; Ahmed, I. A Multimethod Approach to Assess and Measure Corporate Social Responsibility Disclosure and Practices in a Developing Economy. Sustainability 2018, 10, 2995. [Google Scholar] [CrossRef]

- Capelle-Blancard, G.; Petit, A. The weighting of CSR dimensions: One size does not fit all. Bus. Soc. 2017, 56, 919–943. [Google Scholar] [CrossRef]

- Lulewicz-Sas, A. Społeczna odpowiedzialność biznesu w wybranych krajach Unii Europejskiej. Ekon. i Prawo 2013, 12, 537–550. [Google Scholar] [CrossRef]

- Tschopp, D.; Nastanski, M. The Harmonization and Convergence of Corporate Social Responsibility Reporting Standards. J. Bus. Ethics 2014, 125, 147–162. [Google Scholar] [CrossRef]

- Szczepankiewicz, E.I.; Mućko, P. CSR Reporting Practices of Polish Energy and Mining Companies. Sustainability 2016, 8, 126. [Google Scholar] [CrossRef]

- Sen, S.; Bhattacharya, C.B.; Korschun, D. The role of corporate social responsibility in strengthening multiple stakeholder relationships: A field experiment. J. Acad. Mark. Sci. 2006, 34, 158–166. [Google Scholar] [CrossRef]

- Hermann, S.P. Stakeholder Based Measuring and Management of CSR and Its Impact on Corporate Reputation. In From Customer Retention to a Holistic Stakeholder Management System; Huber, M., O‘Girman, S., Eds.; Springer-Verlag: Berlin/Heidelberg, Germany, 2008; pp. 51–61. [Google Scholar]

- Papania, L.; Shapiro, D.M.; Peloza, J. Social Impactas a Measure of Fit betweet Firm Activitiesand Stakeholder Expectations. Int. J. Bus. Gov. Ethics 2008, 4, 3–16. [Google Scholar] [CrossRef]

- Lex, A.; Streit, M.; Partl, C.; Kashofer, K.; Schmalsteig, D. Comparative Analysis of Multidimensional, Quantitative Data. IEEE Trans. Vis. Comput. Graph. 2010, 16, 1027–1035. [Google Scholar] [CrossRef] [PubMed]

- Panek, T.; Zwierzchowski, J. Statystyczne Metody Wielowymiarowej Analizy Porównawczej; Oficyna wydawnicza SGH: Warsaw, Poland, 2013. [Google Scholar]

- Dmitruk, J.; Gawinecki, J. Metody Wielowymiarowej Analizy Porównawczej—Budowa i Zastosowanie. Biuletyn WAT 2017, 66, 103–119. [Google Scholar]

- Walesiak, M. Podstawowe Zagadnienia Statystycznej Analizy Wielowymiarowej. In Metody Statystycznej Analizy Wielowymiarowej w Badaniach Marketingowych; Gatnar, E., Walesiak, M., Eds.; Wydaw. AE we Wrocławiu: Wrocław, Poland, 2004; pp. 17–59. [Google Scholar]

- Strahl, D. Propozycja konstrukcji miary syntetycznej. Przegląd Stat. 1978, 25, 205–215. [Google Scholar]

- Rozporządzenie Komisji (UE) nr 651/2014 z Dnia 17 Czerwca 2014 r. (Dz. Urz. UE L 187 z dnia 26.06.2014 r.). Available online: https://eur-lex.europa.eu/legal-content/PL/TXT/PDF/?uri=CELEX:32014R0651 (accessed on 18 July 2021).

- Sugino, T.; Mayrowani, H.; Kobayashi, H. Determinants for CSR in Developing Countries: The Case of Indonesian Palm Oil Companies. Jpn. J. Rural Econ. 2015, 17, 18–34. [Google Scholar] [CrossRef]

- Li, Z.F. Endogeneity in CEO power: A survey and experiment. Invest. Anal. J. 2016, 45, 149–162. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z.F. Managerial Attributes, Incentives, and Performance. Rev. Corp. Financ. Stud. 2020, 9, 256–301. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z.F. An Empirical Assessment of Empirical Corporate Finance. Available online: https://ssrn.com/abstract=1787143 (accessed on 12 July 2021).

- Dang, C.; Li, Z.F.; Yang, C. Measuring Firm Size in Empirical Corporate Finance. J. Bank. Financ. 2018, 86, 159–176. [Google Scholar] [CrossRef]

- Wolska, G. Zaangażowanie przedsiębiorstw w realizację koncepcji społecznej odpowiedzialności na podstawie badań empirycznych przeprowadzonych w Polsce. Studia Ekonomiczne. Zesz. Nauk. Uniw. Ekon. Katowicach 2015, 236, 85–95. [Google Scholar]

- GPW Uruchamia Indeks WIG-ESG. Available online: https://www.gpw.pl/aktualnosc?cmn_id=108700&title=GPW+uruchamia+indeks+WIG-ESG (accessed on 25 May 2021).

- Index Factsheet: WIG-ESG. Available online: https://gpwbenchmark.pl/karta-indeksu?isin=PL9999998955 (accessed on 25 May 2021).

- Ranking Odpowiedzialnych Firm. Available online: http://rankingodpowiedzialnychfirm.pl/ (accessed on 25 May 2021).

- Climate Change: Implications for the Energy Sector. Key Findings from the Intergovernmental Panel on Climate Change Fifth Assessment Report. University of Cambridge, World Energy Council, June 2014. Available online: https://www.worldenergy.org/assets/images/imported/2014/06/Climate-Change-Implications-for-the-Energy-Sector-Summary-from-IPCC-AR5-2014-Full-report.pdf (accessed on 16 July 2021).

- Źródła Energii w Polsce w 2020 Roku: Mniej Węgla, Więcej Gazu i OZE. Available online: https://wysokienapiecie.pl/35619-zrodla-energii-w-polsce-w-2020-mniej-wegla-wiecej-gazu-oze (accessed on 14 July 2021).

- Sustainable Europe investment Plan: European Green Deal Investment Plan. COM (2020) 21 Final. Brussels: European Commission. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52020DC0021 (accessed on 16 July 2021).

- Makarov, A.A.; Mitrova, T.A.; Kulagin, V.A. Long-term development of the global energy sector under the influence of energy policies and technological progres. Russ. J. Econ. 2020, 6, 347–357. [Google Scholar] [CrossRef]

- Hafner, M.; Raimondi, P.P. Priorities and challenges of the EU energy transition: From the European Green Package to the new Green Deal. Russ. J. Econ. 2020, 6, 374–389. [Google Scholar] [CrossRef]

- EEA. Trends and Projections in Europe 2019: Tracking Progress Towards Europe’s Climate and Energy Targets, EEA Report 15/2019; European Environment Agency: Luxembourg, 2019. [Google Scholar] [CrossRef]

- Sweden Is a Leader in the Energy Transition, According to Latest IEA Country Review. Available online: https://www.iea.org/news/sweden-is-a-leader-in-the-energy-transition-according-to-latest-iea-country-review (accessed on 12 July 2021).

- Hatipoglu, E.; Muhanna, S.A.; Efird, B. Renewables and the future of geopolitics: Revisiting main concepts of international relations from the lens of renewables. Russ. J. Econ. 2020, 6, 358–373. [Google Scholar] [CrossRef]

- Burke, M.J.; Stephens, J.C. Political power and renewable energy futures: A critical review. Energy Res. Soc. Sci. 2018, 35, 78–93. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Criterion Symbol | Criterion Name/Thematic Area | Criterion Nature * |

|---|---|---|

| Area of counterparties (suppliers/customers) | ||

| x1 | Repayment period of liabilities: average trade liabilities × 365 days/sales revenues | D |

| x2 | Receivables collection cycle: average receivables × 365 days/sales revenue | S |

| x3 | Ratio of reserves for lawsuits and compensations to equity | D |

| x4 | Ratio of compensations, penalties, and fines paid and received to sales revenue | D |

| Area of capital donors (investors/creditors) | ||

| x5 | Return on equity: 12-month net result/average equity | S |

| x6 | Dividend yield: dividend per share/market price of share | S |

| x7 | Ratio of net debt to net result on sales plus depreciation and amortisation | D |

| Area of employees | ||

| x8 | Salaries and benefits per employee | S |

| x9 | Ratio of salaries and employee benefits to sales revenue | S |

| x10 | Ratio of salaries and employee benefits to costs of external services | S |

| x11 | Percentage change in employment | S |

| Area of society | ||

| x12 | Relation of donations to sales revenue | S |

| x13 | Effective tax rate: income tax paid/gross financial result | S |

| x14 | Ratio of charges due to taxes (other than income taxes) and fees to sales revenue | S |

| Area of environment | ||

| x15 | Ratio of energy and materials consumption costs to sales revenues | D |

| x16 | Share of installed renewable energy capacity in total installed capacity | S |

| x17 | CO2 emissions per unit of energy produced | D |

| x18 | Share of renewable energy sources in total energy production | S |

| Criterion Symbol | Criterion Nature | cj = max(xj) | min(xj) |

|---|---|---|---|

| x1 | D | 150 | 0 |

| x2 | S | 45 | 0 |

| x3 | D | 0.150 | 0 |

| x4 | D | 0.010 | 0 |

| x5 | S | 0.150 | 0 |

| x6 | S | 0.050 | 0 |

| x7 | D | 8 | 0 |

| x8 | S | 150 | 0 |

| x9 | S | 0.140 | 0 |

| x10 | S | 2 | 0 |

| x11 | S | 0.100 | −0.100 |

| x12 | S | 0.001 | 0 |

| x13 | S | 0.190 | 0 |

| x14 | S | 0.060 | 0 |

| x15 | D | 0.700 | 0 |

| x16 | S | 1 | 0 |

| x17 | D | 1 | 0 |

| x18 | S | 1 | 0 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nawrocki, T.L.; Szwajca, D. A Multidimensional Comparative Analysis of Involvement in CSR Activities of Energy Companies in the Context of Sustainable Development Challenges: Evidence from Poland. Energies 2021, 14, 4592. https://doi.org/10.3390/en14154592

Nawrocki TL, Szwajca D. A Multidimensional Comparative Analysis of Involvement in CSR Activities of Energy Companies in the Context of Sustainable Development Challenges: Evidence from Poland. Energies. 2021; 14(15):4592. https://doi.org/10.3390/en14154592

Chicago/Turabian StyleNawrocki, Tomasz L., and Danuta Szwajca. 2021. "A Multidimensional Comparative Analysis of Involvement in CSR Activities of Energy Companies in the Context of Sustainable Development Challenges: Evidence from Poland" Energies 14, no. 15: 4592. https://doi.org/10.3390/en14154592

APA StyleNawrocki, T. L., & Szwajca, D. (2021). A Multidimensional Comparative Analysis of Involvement in CSR Activities of Energy Companies in the Context of Sustainable Development Challenges: Evidence from Poland. Energies, 14(15), 4592. https://doi.org/10.3390/en14154592