Turkmenistan’s Gas Sector Development Scenarios Based on Econometric and SWOT Analysis

Abstract

1. Introduction

2. Background

2.1. Turkmenistan on the Global Gas Market

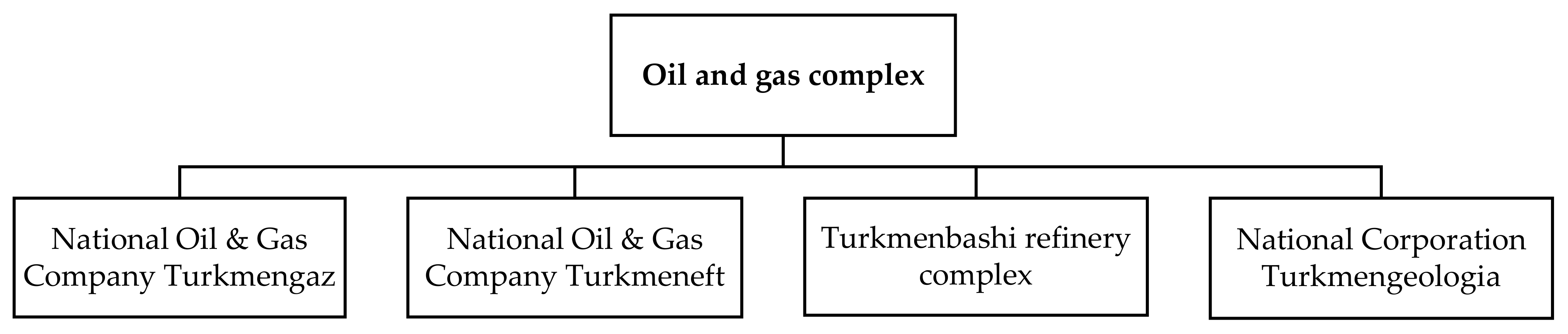

2.2. Turkmenistan Oil and Gas Complex

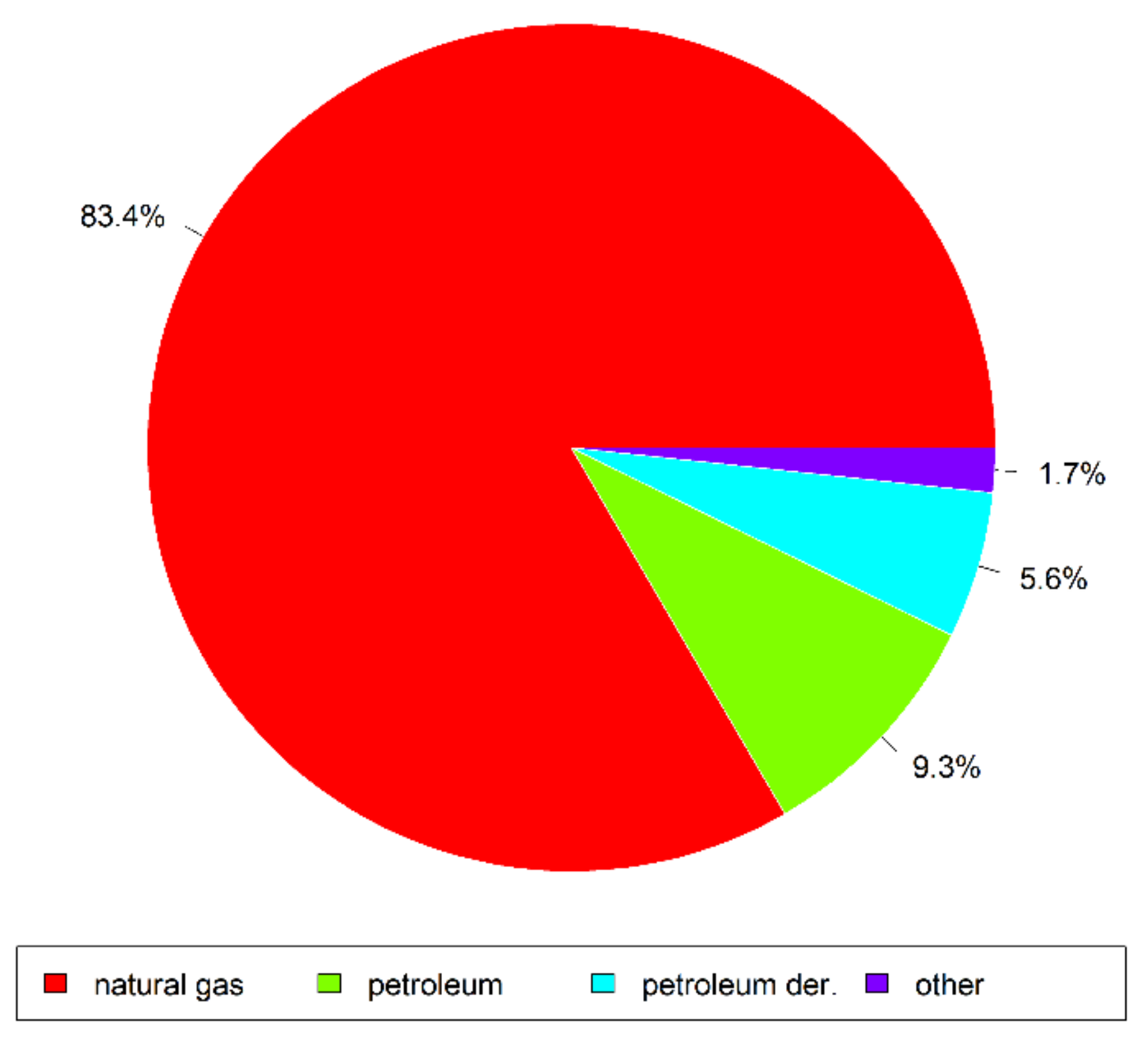

2.3. Share of Hydrocarbons in Turkmenistan’s Exports

3. Theoretical Concept and Methods

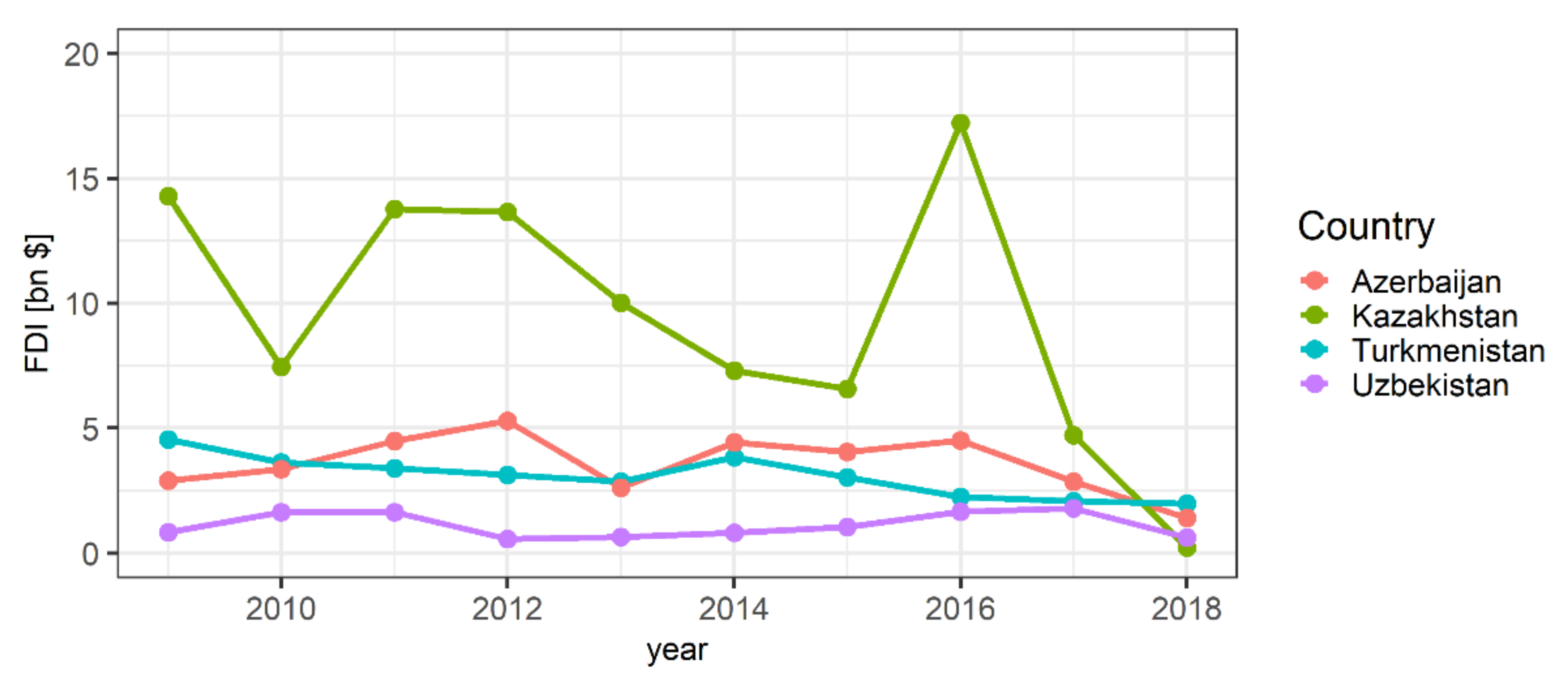

3.1. Relationship between FDI and GDP

3.2. Granger Causality and VAR Methodology

3.3. SWOT and Scenario Analysis

4. Results and Discussion

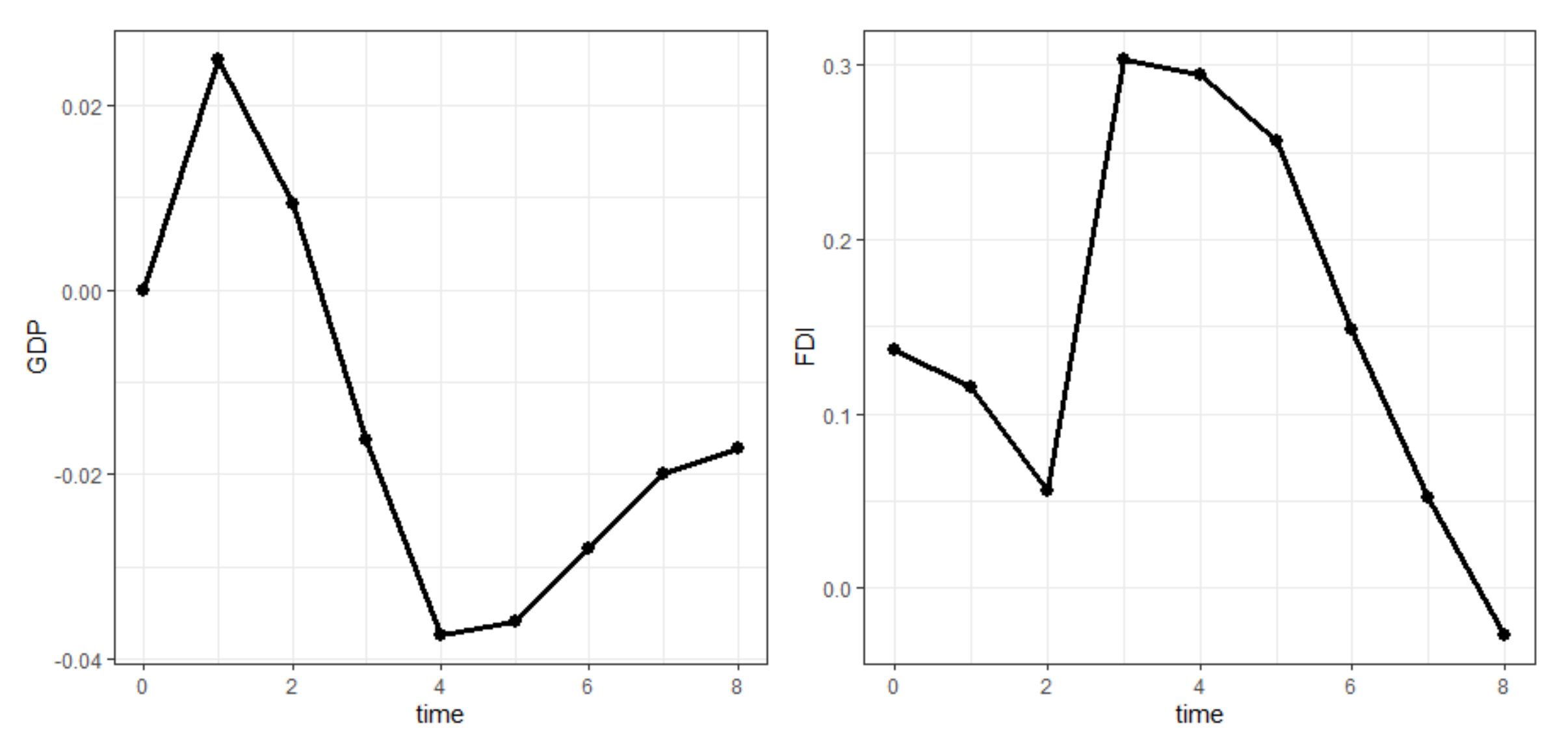

4.1. Causality Relationship between Foreign Direct Investment and GDP in Turkmenistan

4.2. SWOT Analysis of Turkmenistan’s Gas Sector

4.2.1. Strengths

4.2.2. Weaknesses

4.2.3. Opportunities

4.2.4. Threats

4.3. Scenario Analysis

- pessimistic;

- realistic;

- optimistic.

5. Summary

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- British Petroleum. BP Statistical Review of World Energy 2002. Available online: https://www.griequity.com/resources/industryandissues/Energy/bp2002statisticalreview.pdf (accessed on 15 June 2020).

- British Petroleum. BP Statistical Review of World Energy 2019. Available online: https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2019-full-report.pdf (accessed on 15 June 2020).

- Population City. Available online: http://populacja.population.city/turkmenistan/ (accessed on 15 June 2020).

- Bilgin, M. New prospects in the political economy of inner-Caspian hydrocarbons and western energy corridor through Turkey. Energy Policy 2007, 35, 6383–6394. [Google Scholar] [CrossRef]

- Bilgin, M. Geopolitics of European natural gas demand: Supplies from Russia, Caspian and the Middle East. Energy Policy 2009, 37, 4482–4492. [Google Scholar] [CrossRef]

- Cobanli, O. Central Asian Gas in Eurasian Power Game. Energy Policy 2014, 68, 348–370. [Google Scholar] [CrossRef]

- Lee, Y. Opportunities and risks in Turkmenistan’s quest for diversification of its gas export routes. Energy Policy 2014, 74, 330–339. [Google Scholar] [CrossRef]

- Heinrich, A.; Pleines, H. Mixing geopolitics and business: How ruling elites in the Caspian states justify their choice of export pipelines. J. Eurasian Stud. 2015, 6, 107–113. [Google Scholar] [CrossRef]

- Esen, V.; Oral, B. Natural gas reserve/production ratio in Russia, Iran, Qatar and Turkmenistan: A political and economic perspective. Energy Policy 2016, 93, 101–109. [Google Scholar] [CrossRef]

- Azam, M. Economic Determinants of Foreign Direct Investment in Armenia, Kyrgyz Republic and Turkmenistan: Theory and Evidence. Eurasian J. Bus. Econ. 2010, 3, 27–40. [Google Scholar]

- Toda, H.Y.; Yamamoto, T. Statistical Inference in Vector Autoregressions with Possibly Integrated Processes. J. Econom. 1995, 66, 225–250. [Google Scholar] [CrossRef]

- World Bank Open Data. Available online: https://data.worldbank.org/indicator/BX.KLT.DINV.WD.GD.ZS?locations=HU-TM (accessed on 10 January 2021).

- Neftegaz.RU. Available online: https://neftegaz.ru/analisis/world_market/328583-turkmenistan-istochnik-energii-shelkovogo-puti/ (accessed on 12 February 2020).

- Neftegaz.RU. Available online: https://neftegaz.ru/news/dobycha/479557-turkmenistan-dobyl-35-6-mlrd-m3-gza-za-1-e-polugodie-2019-g (accessed on 14 March 2020).

- British Petroleum. BP Statistical Review of World Energy 2020. Available online: https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2020-full-report.pdf?utm_source=BP_Global_GroupCommunications_UK_external&utm_medium=email&utm_campaign=11599394_Statistical%20Review%202020%20-%20on%20the%20day%20reminder&dm_i=1PGC%2C6WM5E%2COV0LQ4%2CRQW75%2C1 (accessed on 23 January 2021).

- Nebit Gaz1. Available online: https://www.oilgas.gov.tm/m/page/page/22 (accessed on 30 July 2020).

- Nebit Gaz2. Available online: https://www.oilgas.gov.tm/ (accessed on 30 August 2020).

- Nebit Gaz3. Available online: https://oilgas.gov.tm/compositions/28 (accessed on 22 July 2020).

- Sputnik. Uzbekistan. Available online: https://uz.sputniknews.ru/economy/20190719/12045250/Uzbekistan-i-Kitay-namereny-uskorit-stroitelstvo-IV-nitki-gazoprovoda.html (accessed on 22 July 2020).

- Neftegaz.RU. Available online: https://neftegaz.ru/news/transport-and-storage/651439-stroitelstvo-gazoprovoda-tapi-na-territorii-afganistana-nachnetsya-v-2021-g/ (accessed on 26 November 2020).

- Neft Capital. Available online: https://oilcapital.ru/article/general/02-08-2019/turkmenistan-bez-nefti-no-s-gazom (accessed on 30 August 2020).

- Lamasz, B.; Iwaszczuk, N. The impact of implied volatility fluctuations on vertical spread option strategies: The case of WTI crude oil market. Energies 2020, 13, 5323. [Google Scholar] [CrossRef]

- Lamasz, B.; Iwaszczuk, N. Crude oil option market parameters and their impact on the cost of hedging by long strap strategy. Int. J. Energy Econ. Policy 2020, 10, 471–480. [Google Scholar] [CrossRef]

- Chu, A.M.; Lv, Z.; Wagner, N.F.; Wong, W.K. Linear and nonlinear growth determinants: The case of Mongolia and its connection to China. Emerg. Mark. Rev. 2020, 43, 100693. [Google Scholar] [CrossRef]

- Tekin, R.B. Economic growth, exports and foreign direct investment in Least Developed Countries: A panel Granger causality analysis. Econ. Model. 2012, 29, 868–878. [Google Scholar] [CrossRef]

- Azam, M.; Ibrahim, Y.; Bakhtyar, B. Foreign direct investment and economic growth in Asia. Actual Probl. Econ. 2014, 11, 58–67. [Google Scholar]

- Chowdhury, A.; Mavrotas, G. FDI and growth: A causal relationship. WIDER Res. Pap. 2005, 25, 1–10. [Google Scholar]

- Sharma, A.; Rishad, A.; Gupta, S. Relationship between FDI, export and economic growth in India: Evidence from Toda and Yamamoto approach. J. Acad. Res. Econ. 2018, 10, 17–29. [Google Scholar]

- Frimpong, J.M.; Oteng-Abayie, E.F. Bivariate causality analysis between FDI inflows and economic growth in Ghana. In Proceedings of the 3rd African Finance Journal Conference, Accra, Ghana, 12–13 July 2006. [Google Scholar]

- Kosztowniak, A. Verification of the relationship between FDI and GDP in Poland. Acta Oeconomica 2016, 66, 307–332. [Google Scholar] [CrossRef]

- Ibrahim, O.A.; Abdel-Gadir, S.E.M. Motives and Determinants of FDI: A VECM Analysis for Oman. Glob. Bus. Rev. 2015, 16, 936–946. [Google Scholar] [CrossRef]

- Hsiao, F.S.; Hsiao, M.C.W. FDI, exports, and GDP in East and Southeast Asia—Panel data versus time-series causality analyses. J. Asian Econ. 2006, 17, 1082–1106. [Google Scholar] [CrossRef]

- Gherghina, Ș.C.; Simionescu, L.N.; Hudea, O.S. Exploring Foreign Direct Investment–Economic Growth Nexus—Empirical Evidence from Central and Eastern European Countries. Sustainability 2019, 11, 5421. [Google Scholar] [CrossRef]

- Baltagi, B.H. Econometrics, 4th ed.; Springer: New York, NY, USA, 2008; ISBN 978-3-540-76515-8. [Google Scholar]

- Jeleński, T.; Dendys, M.; Tomaszewska, B.; Pająk, L. The Potential of RES in the Reduction of Air Pollution: The SWOT Analysis of Smart Energy Management Solutions for Krakow Functional Area (KrOF). Energies 2020, 13, 1754. [Google Scholar] [CrossRef]

- Ervural, B.C.; Zaim, S.; Demirel, O.F.; Aydin, Z.; Delen, D. An ANP and fuzzy TOPSIS-based SWOT analysis for Turkey’s energy planning. Renew. Sustain. Energy Rev. 2018, 82, 1538–1550. [Google Scholar] [CrossRef]

- Ishola, F.A.; Olatunji, O.O.; Ayo, O.O.; Akinlabi, S.A.; Adedeji, P.A.; Inegbenebor, A.O. Sustainable Nuclear Energy Exploration in Nigeria–A SWOT Analysis. Procedia Manuf. 2019, 35, 1165–1171. [Google Scholar] [CrossRef]

- Haque, H.M.E.; Dhakal, S.; Mostafa, S.M.G. An assessment of opportunities and challenges for cross-border electricity trade for Bangladesh using SWOT-AHP approach. Energy Policy 2020, 137, 111118. [Google Scholar] [CrossRef]

- Agyekum, E.B.; Ansah, M.N.S.; Afornu, K.B. Nuclear energy for sustainable development: SWOT analysis on Ghana’s nuclear agenda. Energy Rep. 2020, 6, 107–115. [Google Scholar] [CrossRef]

- Nezhad, M.M.; Shaik, R.U.; Heydari, A.; Razmjoo, A.; Arslan, N.; Garcia, D.A. A SWOT Analysis for Offshore Wind Energy Assessment Using Remote-Sensing Potential. Appl. Sci. 2020, 10, 6398. [Google Scholar] [CrossRef]

- Alvarez, D.B.; Sugiyama, M. A SWOT Analysis of Utility-Scale Solar in Myanmar. Energies 2020, 13, 884. [Google Scholar] [CrossRef]

- Lei, Y.; Lu, X.; Shi, M.; Wang, L.; Lv, H.; Chen, S.; Hu, C.; Yu, Q.; da Silveira, S.D.H. SWOT analysis for the development of photovoltaic solar power in Africa in comparison with China. Environ. Impact Assess. Rev. 2019, 77, 122–127. [Google Scholar] [CrossRef]

- Kamran, M.; Fazal, M.R.; Mudassar, M. Towards empowerment of the renewable energy sector in Pakistan for sustainable energy evolution: SWOT analysis. Renew. Energy 2020, 146, 543–558. [Google Scholar] [CrossRef]

- Elavarasan, R.M.; Afridhis, S.; Vijayaraghavan, R.R.; Subramaniam, U.; Nurunnabi, M. SWOT analysis: A framework for comprehensive evaluation of drivers and barriers for renewable energy development in significant countries. Energy Rep. 2020, 6, 1838–1864. [Google Scholar] [CrossRef]

- Irfan, M.; Hao, Y.; Panjwani, M.K.; Khan, D.; Chandio, A.A.; Li, H. Competitive assessment of South Asia’s wind power industry: SWOT analysis and value chain combined model. Energy Strategy Rev. 2020, 32, 100540. [Google Scholar] [CrossRef]

- Agyekum, E.B. Energy poverty in energy rich Ghana: A SWOT analytical approach for the development of Ghana’s renewable energy. Sustain. Energy Technol. Assess. 2020, 40, 100760. [Google Scholar] [CrossRef]

- Lustenberger, P.; Schumacher, F.; Spada, M.; Burgherr, P.; Stojadinovic, B. Assessing the Performance of the European Natural Gas Network for Selected Supply Disruption Scenarios Using Open-Source Information. Energies 2019, 12, 4685. [Google Scholar] [CrossRef]

- Hafezi, R.; Wood, D.A.; Akhavan, A.N.; Pakseresht, S. Iran in the emerging global natural gas market: A scenario-based competitive analysis and policy assessment. Resour. Policy 2020, 68, 101790. [Google Scholar] [CrossRef]

- Scharf, H.; Arnold, F.; Lencz, D. Future natural gas consumption in the context of decarbonization–A meta-analysis of scenarios modeling the German energy system. Energy Strategy Rev. 2021, 33, 100591. [Google Scholar] [CrossRef]

- Kolb, S.; Plankenbühler, T.; Frank, J.; Dettelbacher, J.; Ludwig, R.; Karl, J.; Dillig, M. Scenarios for the integration of renewable gases into the German natural gas market–A simulation-based optimisation approach. Renew. Sustain. Energy Rev. 2021, 139, 110696. [Google Scholar] [CrossRef]

- Zhou, I.; Jin, B.; Du, S.; Zhang, P. Scenario Analysis of Carbon Emissions of Beijing-Tianjin-Hebei. Energies 2018, 11, 1489. [Google Scholar] [CrossRef]

- Wu, Q.; Peng, C. Scenario Analysis of Carbon Emissions of China’s Electric Power Industry Up to 2030. Energies 2016, 9, 988. [Google Scholar] [CrossRef]

- Kim, S.H.; Lee, S.; Han, S.Y.; Kim, J.H. Scenario Analysis for GHG Emission Reduction Potential of the Building Sector for New City in South Korea. Energies 2020, 13, 5514. [Google Scholar] [CrossRef]

- Yao, X.; Lei, H.; Yang, I.; Shao, S.; Ahmed, D.; Ismaail, M.G.A. Low-carbon transformation of the regional electric power supply structure in China: A scenario analysis based on a bottom-up model with resource endowment constraints. Resour. Conserv. Recycl. 2021, 167, 105315. [Google Scholar] [CrossRef]

- Leo, S.D.; Pietrapertosa, F.; Salvia, M.; Cosmi, C. Contribution of the Basilicata region to decarbonisation of the energy system: Results of a scenario analysis. Renew. Sustain. Energy Rev. 2021, 138, 110544. [Google Scholar] [CrossRef]

- Facchini, F.; Mummolo, G.; Vitti, M. Scenario Analysis for Selecting Sewage Sludge-to-Energy/Matter Recovery Processes. Energies 2021, 14, 276. [Google Scholar] [CrossRef]

- Lederer, J.; Gassner, A.; Fellner, J.; Mollay, U.; Schremmer, C. Raw materials consumption and demolition waste generation of the urban building sector 2016-2050: A scenario-based material flow analysis of Vienna. J. Clean. Prod. 2021, 288, 125566. [Google Scholar] [CrossRef]

- Tosoni, E.; Salo, A.; Govaerts, J.; Zio, E. Definition of the data for comprehensiveness in scenario analysis of near-surface nuclear waste repositories. Data Brief 2020, 31, 105780. [Google Scholar] [CrossRef] [PubMed]

- Westgaard, S.; Fleten, S.E.; Negash, A.; Botterud, A.; Bogaard, K.; Verling, T.H. Performing price scenario analysis and stress testing using quantile regression: A case study of the Californian electricity market. Energy 2021, 214, 118796. [Google Scholar] [CrossRef]

- Cieplinski, A.; D’Alessandro, S.; Marghella, F. Assessing the renewable energy policy paradox: A scenario analysis for the Italian electricity market. Renew. Sustain. Energy Rev. 2021, 142, 110838. [Google Scholar] [CrossRef]

- Javed, M.S.; Ma, T.; Jurasz, J.; Mikulik, J. A hybrid method for scenario-based techno-economic-environmental analysis of off-grid renewable energy systems. Renew. Sustain. Energy Rev. 2021, 139, 110725. [Google Scholar] [CrossRef]

- Li, T.; Li, Z.; Li, W. Scenarios analysis on the cross-region integrating of renewable power based on a long-period cost-optimization power planning model. Renew. Energy 2020, 156, 851–863. [Google Scholar] [CrossRef]

- Salvucci, R.; Petrović, S.; Karlsson, K.; Wråke, M.; Uteng, T.P.; Balyk, O. Energy Scenario Analysis for the Nordic Transport Sector: A Critical Review. Energies 2019, 12, 2232. [Google Scholar] [CrossRef]

- Song, Y.; Li, G.; Wang, Q.; Meng, X.; Wang, H. Scenario analysis on subsidy policies for the uptake of electric vehicles industry in China. Resour. Conserv. Recycl. 2020, 161, 104927. [Google Scholar] [CrossRef]

- Keseru, I.; Coosemans, T.; Macharis, C. Stakeholders’ preferences for the future of transport in Europe: Participatory evaluation of scenarios combining scenario planning and the multi-actor multi-criteria analysis. Futures 2021, 127, 102690. [Google Scholar] [CrossRef]

- Dzikuć, M.; Piwowar, A.; Szufa, S.; Adamczyk, J.; Dzikuć, M. Potential and Scenarios of Variants of Thermo-Modernization of Single-Family Houses: An Example of the Lubuskie Voivodeship. Energies 2021, 14, 191. [Google Scholar] [CrossRef]

- Alshammari, Y.M. Scenario analysis for energy transition in the chemical industry: An industrial case study in Saudi Arabia. Energy Policy 2021, 150, 112128. [Google Scholar] [CrossRef]

- Borghino, N.; Corson, M.; Nitschelm, L.; Wilfart, A.; Fleuet, J.; Moraine, M.; Breland, T.A.; Lescoat, P.; Godinot, O. Contribution of LCA to decision making: A scenario analysis in territorial agricultural production systems. J. Environ. Manag. 2021, 287, 112288. [Google Scholar] [CrossRef] [PubMed]

- UNCTAD. World Investment Report 2014. United Nations Conference on Trade and Development. Available online: https://unctad.org/system/files/official-document/wir2014_en.pdf (accessed on 12 March 2020).

- UNCTAD. World Investment Report 2020, United Nations Conference on Trade and Development. Available online: https://unctad.org/system/files/official-document/wir2020_overview_en.pdf (accessed on 10 January 2021).

- Santander Trade Markets. Available online: https://santandertrade.com/en/portal/establish-overseas/turkmenistan/investing-3 (accessed on 28 December 2020).

- Borowski, P.F. Nexus between Water, Energy, Food and Climate Change as Challenges Facing the Modern Global, European and Polish economy. AIMS Geosci. 2020, 6, 397–421. [Google Scholar] [CrossRef]

- Borowski, P.F. Zonal and Nodal Models of Energy Market in European Union. Energies 2020, 13, 4182. [Google Scholar] [CrossRef]

- ÓhAiseadha, C.; Quinn, G.; Connolly, R.; Connolly, M.; Soon, W. Energy and Climate Policy–An Evaluation of Global Climate Change Expenditure 2011–2018. Energies 2020, 13, 4839. [Google Scholar] [CrossRef]

- Gouel, C.; Laborded, D. The crucial role of domestic and international market-mediated adaptation to climate change. J. Environ. Econ. Manag. 2021, 106, 102408. [Google Scholar] [CrossRef]

- Chen, X.; Fu, Q.; Chang, C.P. What are the shocks of climate change on clean energy investment: A diversified exploration. Energy Econ. 2021, 95, 105136. [Google Scholar] [CrossRef]

- Dovì, V.; Battaglini, A. Energy Policy and Climate Change: A Multidisciplinary Approach to a Global Problem. Energies 2015, 8, 13473–13480. [Google Scholar] [CrossRef]

- Jiang, S.; Deng, X.; Liu, G.; Zhang, F. Climate change-induced economic impact assessment by parameterizing spatially heterogeneous CO2 distribution. Technol. Forecast. Soc. Chang. 2021, 167, 120668. [Google Scholar] [CrossRef]

- Scott, C.A.; Sugg, Z.P. Global Energy Development and Climate-Induced Water Scarcity–Physical Limits, Sectoral Constraints, and Policy Imperatives. Energies 2015, 8, 8211–8225. [Google Scholar] [CrossRef]

- Krishna, A. Understanding the differences between climate change deniers and believers’ knowledge, media use, and trust in related information sources. Public Relat. Rev. 2021, 47, 101986. [Google Scholar] [CrossRef]

- Silveira, I.H.; Cortes, T.R.; de Oliveira, B.F.A.; Junger, W.L. Projections of excess cardiovascular mortality related to temperature under different climate change scenarios and regionalized climate model simulations in Brazilian cities. Environ. Res. 2021, 197, 110995. [Google Scholar] [CrossRef] [PubMed]

- Jones, C.A.; Davison, A. Disempowering emotions: The role of educational experiences in social responses to climate change. Geoforum 2021, 118, 190–200. [Google Scholar] [CrossRef]

- Lupi, V.; Marsiglio, S. Population growth and climate change: A dynamic integrated climate-economy-demography model. Ecol. Econ. 2021, 184, 107011. [Google Scholar] [CrossRef]

- Yang, Y.; Xu, H.; Wang, J.; Liu, T.; Huanzhi, W. Integrating climate change factor into strategic environmental assessment in China. Environ. Impact Assess. Rev. 2021, 89, 106585. [Google Scholar] [CrossRef]

- Poitras, G. Rhetoric, epistemology and climate change economics. Ecol. Econ. 2021, 184, 106985. [Google Scholar] [CrossRef]

- Herzer, D. How Does Foreign Direct Investment Really Affect Developing Countries’ Growth? Rev. Int. Econ. 2012, 20, 396–414. [Google Scholar] [CrossRef]

- Sothan, S. Causality between foreign direct investment and economic growth for Cambodia. Cogent Econ. Financ. 2017, 5, 1277860. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | 2018 | 2019 | ||||

|---|---|---|---|---|---|---|

| Production (bcm) | Consumption (bcm) a | Production/ Consumption (%) | Production (bcm) | Consumption (bcm) | Production/ Consumption (%) | |

| Norway | 120.6 | 4.5 | 2680.00 | 114.4 | 4.5 | 2542.22 |

| Qatar | 175.5 | 41.4 | 423.91 | 178.1 | 41.1 | 433.33 |

| Turkmenistan | 61.5 | 28.5 | 215.79 | 63.2 | 31.5 | 200.64 |

| Total World | 3867.9 | 3848.9 | 3989.3 | 3929.2 | ||

| Period of Operation | Authority |

|---|---|

| 23.04.1993–30.06.1996 | Ministry of Oil and Gas of Turkmenistan |

| 01.07.1996–07.01.2016 | Ministry of oil and gas industry and mineral resources of Turkmenistan |

| 08.01.2016–14.07.2016 | Ministry of Oil and Gas of Turkmenistan |

| Until 15.07.2016 | Department of the Cabinet of Ministers of Turkmenistan |

| Variable | N | Mean | Sd | Min | Max | Skew | Kurtosis |

|---|---|---|---|---|---|---|---|

| GDP | 24 | 23.098 | 1.119 | 21.590 | 24.497 | −0.124 | −1.705 |

| FDI | 24 | 20.106 | 1.493 | 17.947 | 22.239 | 0.127 | −1.666 |

| Variable | Value | ADF Test | KPSS Test | ||

|---|---|---|---|---|---|

| Levels | Diff. | Levels | Diff. | ||

| GDP | Statistic | −2.214 | −3.208 | 0.865 | 0.191 |

| p-value | 0.460 | 0.033 a | <0.01 a | >0.10 | |

| FDI | Statistic | −0.988 | −5.218 | 0.825 | 0.125 |

| p-value | 0.740 | <0.01 a | <0.01 a | >0.10 | |

| Lag | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| AIC | −6.204 | −5.912 | −6.270 a | −6.033 | −6.141 |

| Variable | Wald Statistics | p-Value | Causality |

|---|---|---|---|

| GDP causes FDI | 14.1 a | 0.0028 | GDP → FDI |

| FDI causes GDP | 1.4 | 0.71 | - |

| Strengths | Weaknesses |

|---|---|

| Large deposits of natural gas. Low domestic demand. Oil deposits—an alternative to gas. FExistence of an extensive gas pipeline network. Construction of new gas pipelines—a way to expand export markets. Financial support from the state—subsidies, legal regulations, cheap loans. National fiscal policy favoring the sector. Favorable investment climate—for selected foreign investors. Activity of representatives of the gas sector and government—to promote the sector and attract potential buyers of natural gas and investors. Production of other products from hydrocarbons. Overproduction of cheap electric energy, which is used in the technological process of gas liquefaction (LNG). | State budget dependence on hydrocarbon exports. Lack of internal resources to implement investment projects. Dependence on foreign creditors from a single country (China). Poorly developed gas pipeline network. Lack of access to open sea routes, resulting in a more expensive way of LNG delivery—by land. Outdated technologies and faulty machinery in the extraction sector, which require modernization and new investments. High energy consumption of gas liquefaction technologies Weak development of other sectors of the economy, which makes it a resource-based economy. High volatility of the exchange rate. Lack of structures compliant with international trade standards to support foreign investors. Political and economic instability of the country. |

| Opportunities | Threats |

| Increase in global gas demand due to rise in energy demand. Climate policy that prioritizes the development of RES and the use of less carbon-intensive fossil fuels. Gas is a greener fuel compared to other fossil fuels Construction of new facilities for liquefying natural gas LNG. Cheap domestic electricity means lower costs of LNG production. Decrease in LNG transportation costs due to increased competition in the carrier market. Selection of a gas liquefaction technology adapted to climatic conditions. Establishing cooperation with transit countries. Finding new gas customers. Developing the domestic economy with a focus on investments in other sectors of the domestic economy. Commissioning of new gas pipelines. Increasing investment in the oil and gas sector. National energy policy focused on the development of the gas sector. | Increase in global gas production, especially from non-traditional sources (shale gas). Economic downturn on the gas market and decline in gas prices. Reduced costs of shale gas production—risk of competition. Increase in LNG transportation costs—given the limited number of carriers. Increase in prices of raw materials and materials used in the gas liquefaction technology. Increase in the cost of gas transport through foreign territories (transit costs). Development of alternative and renewable energy sources. Decrease in costs of green energy production. Increase in the share of power generation from nuclear power plants. Low rate of return on investment. Supply risks due to the unstable political and economic situation in the transit and destination countries. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Iwaszczuk, N.; Wolak, J.; Iwaszczuk, A. Turkmenistan’s Gas Sector Development Scenarios Based on Econometric and SWOT Analysis. Energies 2021, 14, 2740. https://doi.org/10.3390/en14102740

Iwaszczuk N, Wolak J, Iwaszczuk A. Turkmenistan’s Gas Sector Development Scenarios Based on Econometric and SWOT Analysis. Energies. 2021; 14(10):2740. https://doi.org/10.3390/en14102740

Chicago/Turabian StyleIwaszczuk, Natalia, Jacek Wolak, and Aleksander Iwaszczuk. 2021. "Turkmenistan’s Gas Sector Development Scenarios Based on Econometric and SWOT Analysis" Energies 14, no. 10: 2740. https://doi.org/10.3390/en14102740

APA StyleIwaszczuk, N., Wolak, J., & Iwaszczuk, A. (2021). Turkmenistan’s Gas Sector Development Scenarios Based on Econometric and SWOT Analysis. Energies, 14(10), 2740. https://doi.org/10.3390/en14102740