The UK and German Low-Carbon Industry Transitions from a Sectoral Innovation and System Failures Perspective

, , , , ,

, , , , ,

Abstract

1. Introduction

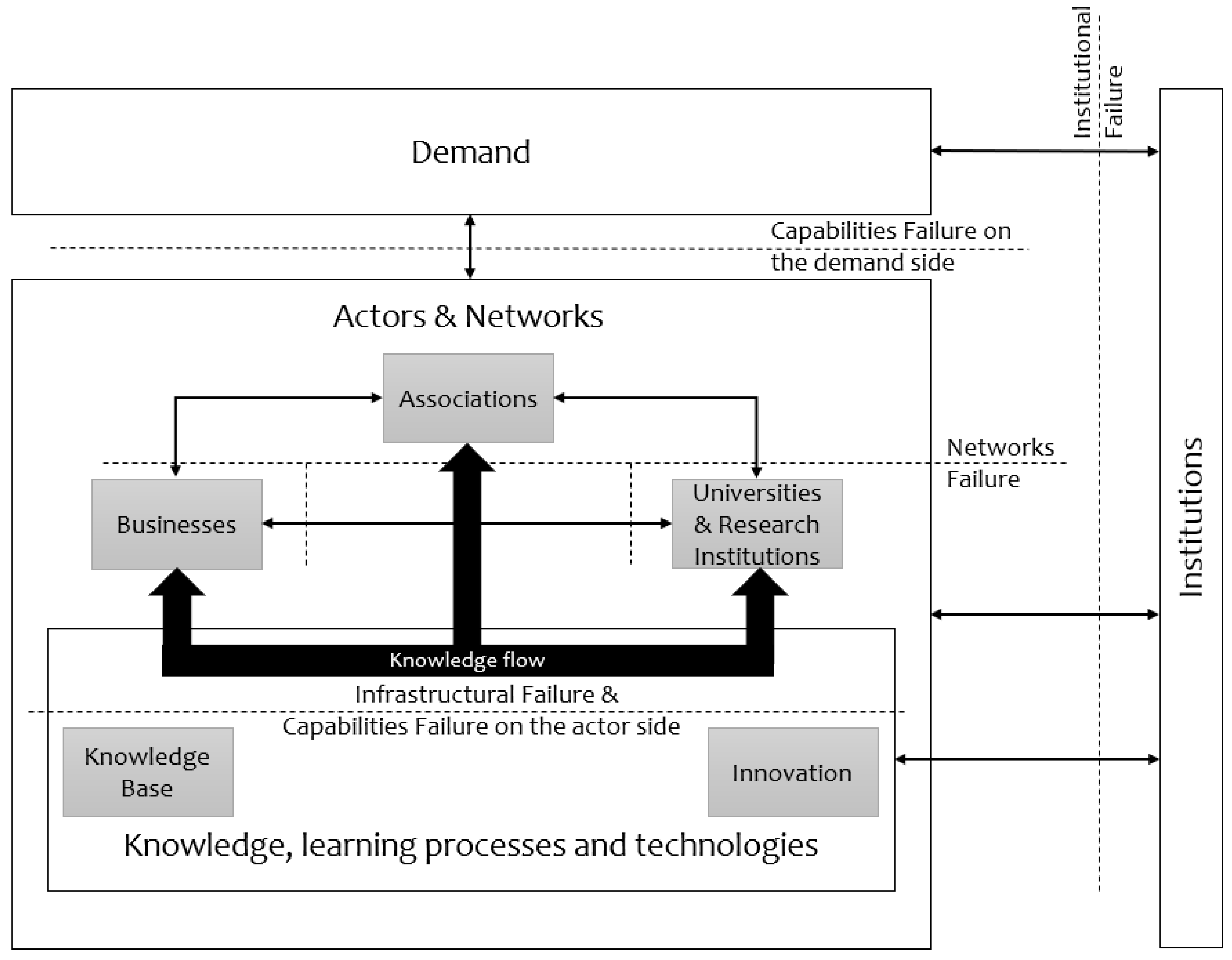

2. Background

3. Methodology

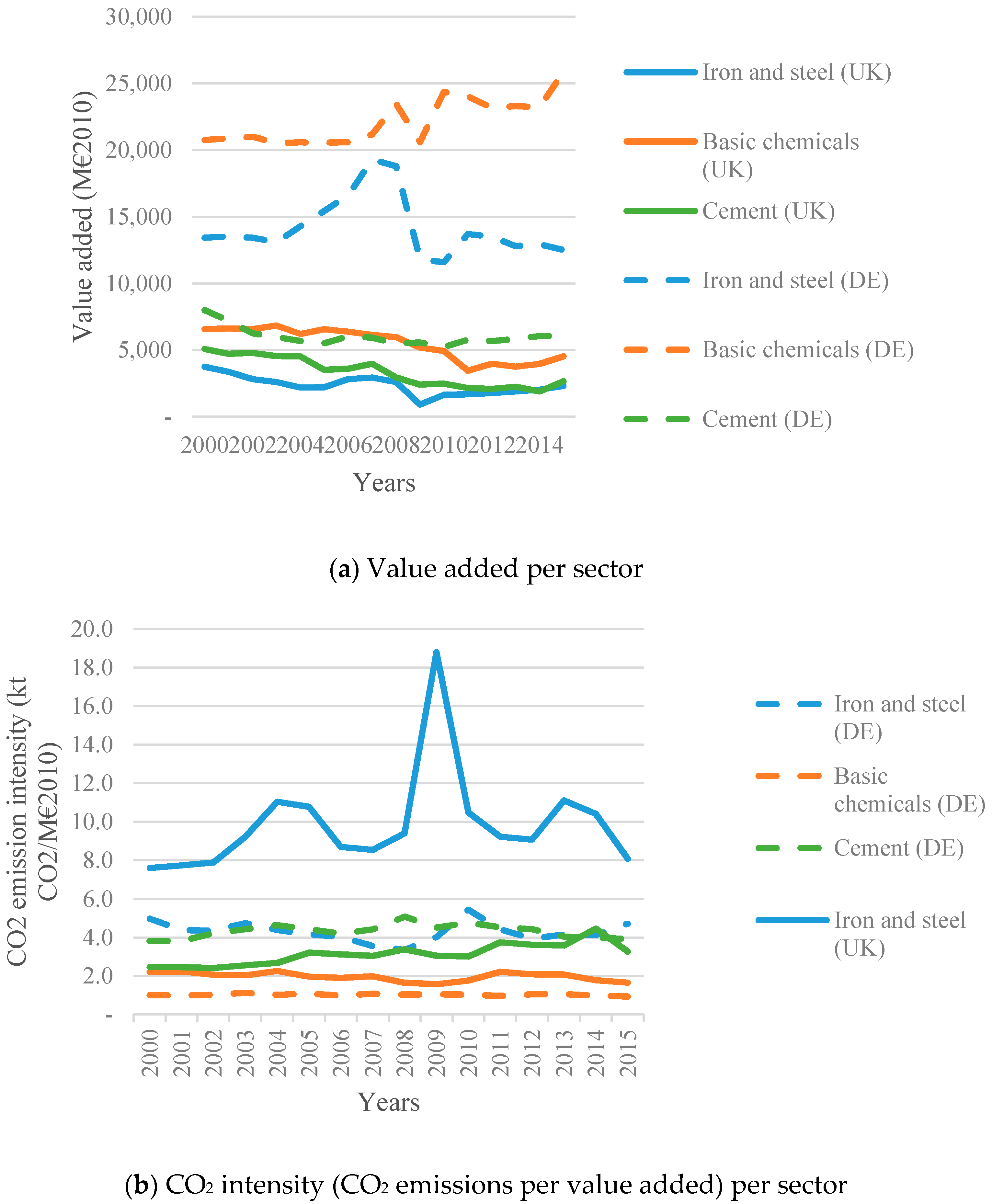

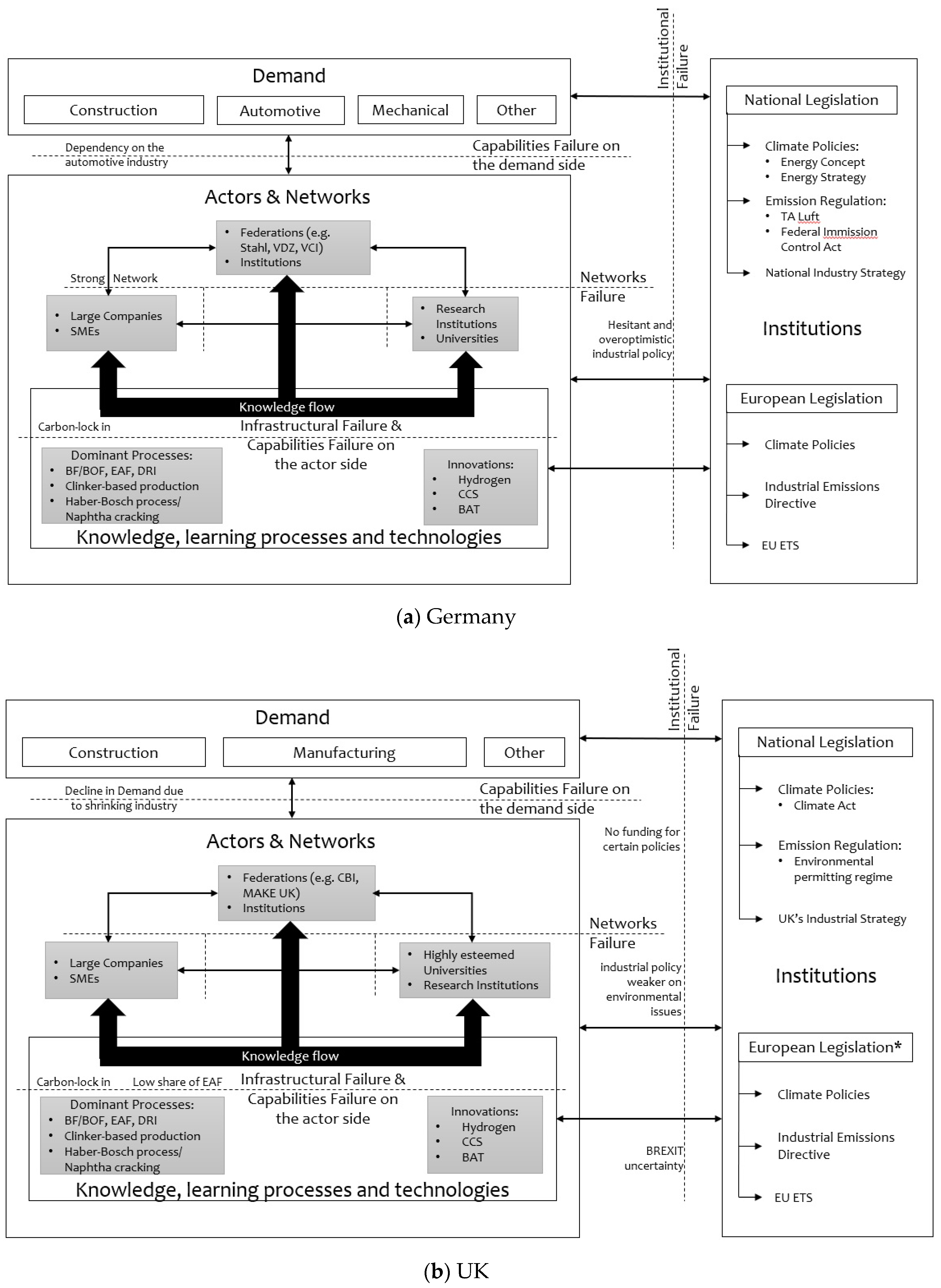

4. The German Industrial SIS

4.1. Actors and Networks

4.2. Institutions

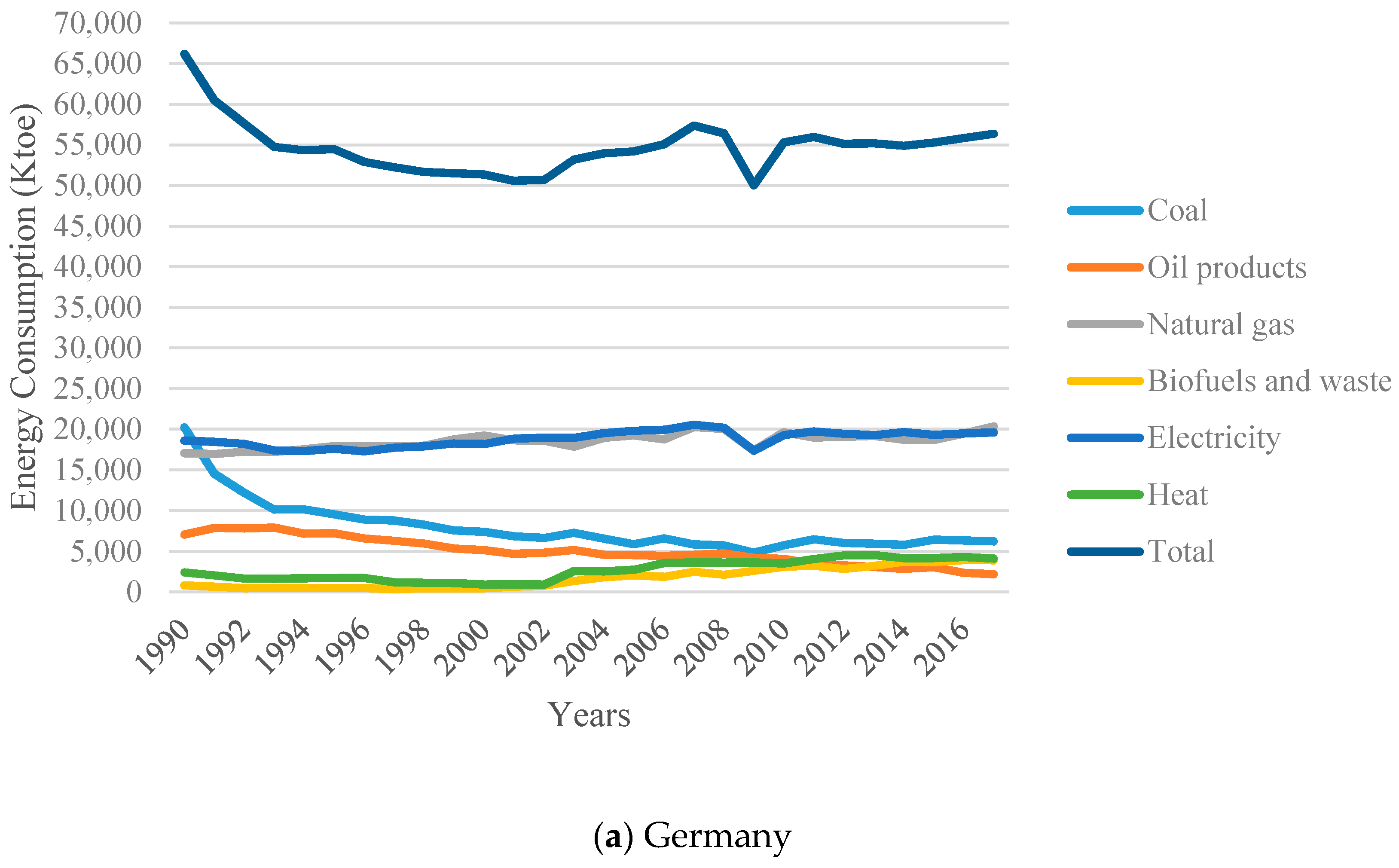

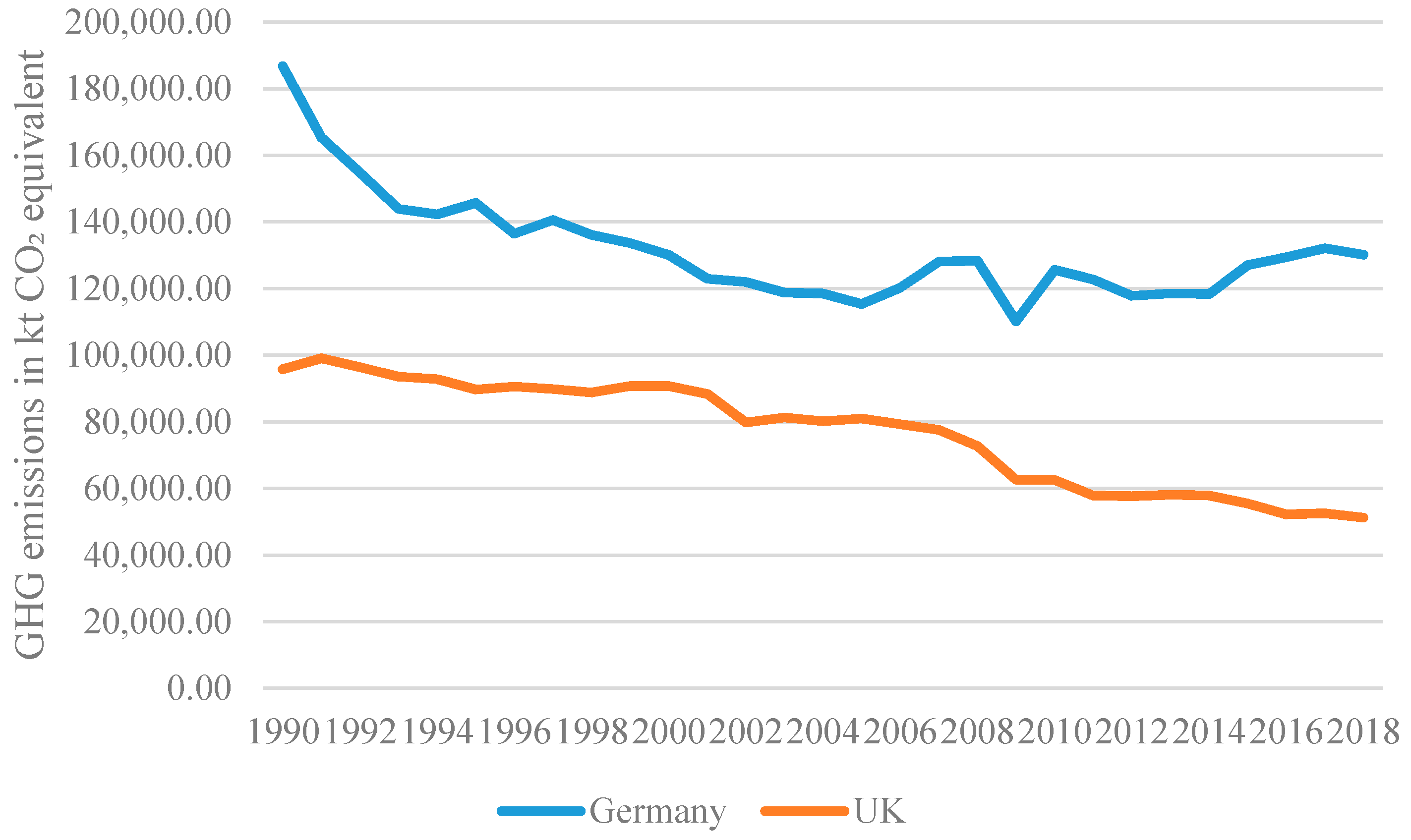

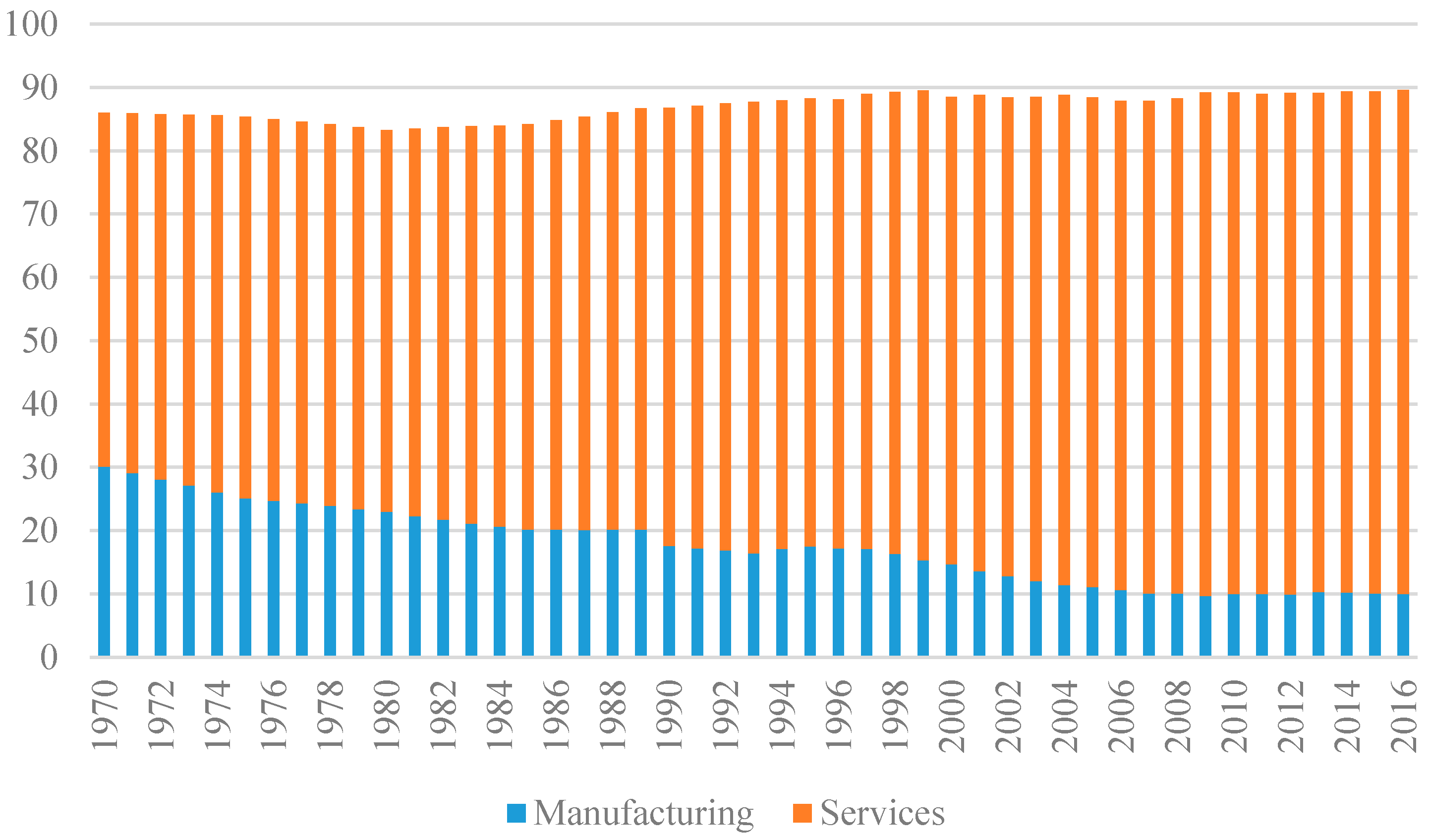

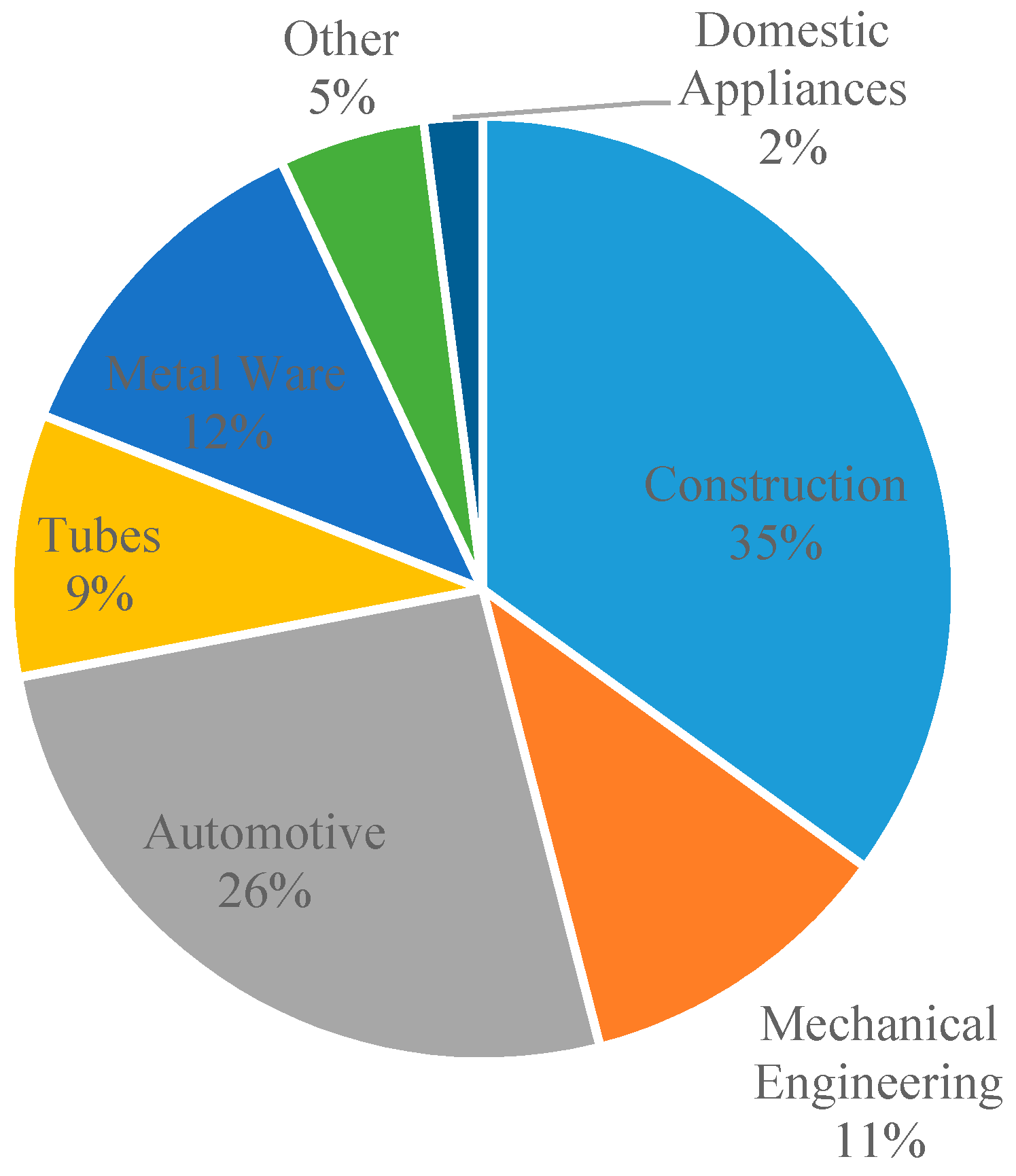

4.3. Demand

4.4. Knowledge, Learning Processes and Technologies

5. The UK Industrial SIS

5.1. Actors and Networks

5.2. Institutions

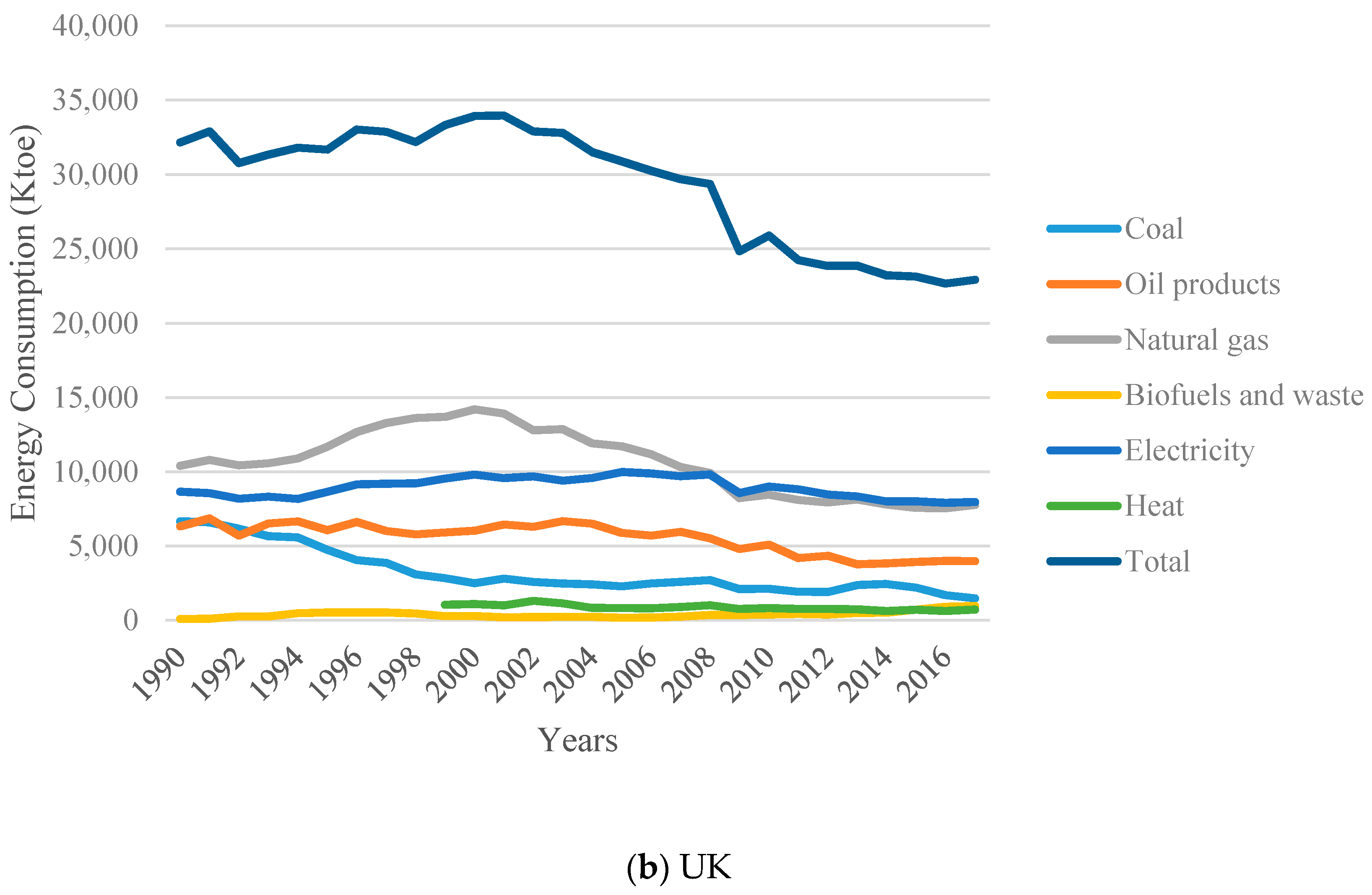

5.3. Demand

5.4. Knowledge, Learning Processes and Technologies

6. Comparative Analysis Based on the System Failures Framework

6.1. Interactions

6.2. Institutions

6.3. Capabilities

6.4. Infrastructure

7. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

References

- IPCC. Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. 2014. Available online: https://www.ipcc.ch/site/assets/uploads/2018/02/ipcc_wg3_ar5_chapter10.pdf (accessed on 19 March 2020).

- Åhman, M.; Nilsson, L.J. Decarbonizing industry in the EU: Climate, trade and industrial policy strategies. In Decarbonization in the European Union; Palgrave Macmillan: London, UK, 2015; pp. 92–114. [Google Scholar]

- Gerres, T.; Chaves Ávila, J.; Llamas, P.; San Román, T. A review of cross-sector decarbonisation potentials in the European energy intensive industry. J. Clean. Prod. 2019, 210, 585–601. [Google Scholar] [CrossRef]

- Pardo, N.; Moya, J.A. Prospective scenarios on energy efficiency and CO2 emissions in the European Iron & Steel industry. Energy 2013, 54, 113–128. [Google Scholar]

- Stefana, E.; Cocca, P.; Marciano, F.; Rossi, D.; Tomasoni, G. A Review of Energy and Environmental Management Practices in Cast Iron Foundries to Increase Sustainability. Sustainability 2019, 11, 7245. [Google Scholar] [CrossRef]

- Karakaya, E.; Nuur, C.; Assbring, L. Potential transitions in the iron and steel industry in Sweden: Towards a hydrogen-based future? J. Clean. Prod. 2018, 195, 651–663. [Google Scholar] [CrossRef]

- Wesseling, J.H.; Lechtenböhmer, S.; Åhman, M.; Nilsson, L.J.; Worrell, E.; Coenen, L. The transition of energy intensive processing industries towards deep decarbonisation: Characteristics and implications for future research. Renew. Sustain. Energy Rev. 2017, 79, 1303–1313. [Google Scholar] [CrossRef]

- Flichy, P. Understanding Technological Innovation: A Socio-technical Approach; Edward Elgar Publishing: Cheltenham, UK, 2008. [Google Scholar]

- Mokhtar, A.; Nasooti, M. A decision support tool for cement industry to select energy efficiency measures. Energy Strategy Rev. 2020, 28, 100458. [Google Scholar] [CrossRef]

- Avami, A.; Sattari, S. Energy conservation opportunities: Cement industry in Iran. Int. J. Energy 2007, 1, 65–71. [Google Scholar]

- Markewitz, P.; Zhao, L.; Ryssel, M.; Moumin, G.; Wang, Y.; Sattler, C.; Robinius, M.; Stolten, D. Carbon Capture for CO2 Emission Reduction in the Cement Industry in Germany. Energies 2019, 12, 2432. [Google Scholar] [CrossRef]

- Griffin, P.W.; Hammond, G.P.; Norman, J.B. Industrial energy use and carbon emissions reduction in the chemicals sector: A UK perspective. Appl. Energy 2018, 227, 587–602. [Google Scholar] [CrossRef]

- Allen, J. Towards a post-industrial economy. In The Economy in Question; Allen, J., Massey, D., Eds.; Sage: London, UK, 1998; pp. 91–135. [Google Scholar]

- Cunningham, I.; James, P. The outsourcing of social care in Britain: What does it mean for voluntary sector workers? Work Employ. Soc. 2009, 23, 363–375. [Google Scholar] [CrossRef]

- Edquist, C.; Hommen, L.; McKelvey, M.D. Innovation and Employment: Process versus Product Innovation; Edward Elgar Publishing: Cheltenham, UK, 2001. [Google Scholar]

- Fagerberg, J.; Mowery, D.C.; Nelson, R.R. (Eds.) The Oxford Handbook of Innovation; Oxford University Press: Oxford, UK, 2005. [Google Scholar]

- Song, L.; Lieu, J.; Nikas, A.; Arsenopoulos, A.; Vasileiou, G.; Doukas, H. Contested energy futures, conflicted rewards? Examining low-carbon transition risks and governance dynamics in China’s built environment. Energy Res. Soc. Sci. 2020, 59, 101306. [Google Scholar] [CrossRef]

- Edquist, C. Systems of Innovation: Perspectives and Challenges. In The Oxford Handbook of Innovation; Fagerberg, J., Mowery, D.C., Nelson, R.R., Eds.; Oxford University Press: Oxford, UK, 2005; pp. 181–208. [Google Scholar]

- Malerba, F. (Ed.) Sectoral Systems of Innovation: Concepts, Issues and Analyses of Six Major Sectors in Europe; Cambridge University Press: Cambridge, UK, 2004. [Google Scholar]

- Malerba, F. Sectoral systems of innovation and production. Res. Policy 2002, 31, 247–264. [Google Scholar] [CrossRef]

- Bosman, R.; Loorbach, D.; Rotmans, J.; Van Raak, R. Carbon lock-out: Leading the fossil port of Rotterdam into transition. Sustainability 2018, 10, 2558. [Google Scholar] [CrossRef]

- Woolthuis, R.K.; Lankhuizen, M.; Gilsing, V. A system failure framework for innovation policy design. Technovation 2005, 25, 609–619. [Google Scholar] [CrossRef]

- Marçal, E.F.; de Prince, D.; Zimmermann, B.; Merlin, G.; Simões, O. Assessing global economic activity linkages: The role played by United States, Germany and China. EconomiA 2020, 21, 38–56. [Google Scholar] [CrossRef]

- Statista. United Kingdom: Distribution of Gross Domestic Product (GDP) Across Economic Sectors from 2008 to 2018. 2018. Available online: https://www.statista.com/statistics/270372/distribution-of-gdp-across-economic-sectors-in-the-united-kingdom/ (accessed on 10 July 2020).

- Tamanini, J.; Bassi, A.; Hoffman, C.; Valeciano, J. The Global Green Economy Index GGEI 2014. In Measuring National Performance in the Green Economy 4th Edition–October; Dual Citizen: New York, NY, USA, 2014. [Google Scholar]

- OECD. Gross Domestic Spending on R&D. 2017. Available online: https://data.oecd.org/rd/gross-domestic-spending-on-r-d.htm (accessed on 15 May 2020).

- IEA. Data and Statistics. 2019. Available online: https://www.iea.org/data-and-statistics/data-tables?country=WORLD&energy=Balances&year=2017 (accessed on 10 April 2020).

- UNFCCC. Greenhouse Gas Inventory Data. 2018. Available online: https://di.unfccc.int/detailed_data_by_party (accessed on 18 July 2020).

- Zeng, B.; Zhu, L. Market Power and Technology Diffusion in an Energy-Intensive Sector Covered by an Emissions Trading Scheme. Sustainability 2019, 11, 3870. [Google Scholar] [CrossRef]

- BGS. Mineral Planning Factsheet: Cement Raw Materials. Available online: https://www.google.com.hk/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwiM2K-U4fvrAhVAy4sBHbHUA78QFjAAegQIAxAB&url=https%3A%2F%2Fwww.bgs.ac.uk%2Fdownloads%2Fstart.cfm%3Fid%3D1353&usg=AOvVaw2dVh6Sj35hxNqDdzplAFbP (accessed on 15 March 2020).

- Schettkat, R.; Yocarini, L. The shift to services employment: A review of the literature. Struct. Chang. Econ. Dyn. 2006, 17, 127–147. [Google Scholar] [CrossRef]

- Office for National Statistics. Changes in the Economy Since the 1970s. 2019. Available online: https://www.ons.gov.uk/economy/economicoutputandproductivity/output/articles/changesintheeconomysincethe1970s/2019-09-02 (accessed on 2 June 2020).

- Kaya, Y.; Yokobori, K. (Eds.) Environment, Energy, and Economy: Strategies for Sustainability; United Nations University Press: Tokyo, Japan, 1997. [Google Scholar]

- Wachsmuth, J.; Duscha, V. Achievability of the Paris targets in the EU—The role of demand-side-driven mitigation in different types of scenarios. Energy Effic. 2019, 12, 403–421. [Google Scholar] [CrossRef]

- Mantzos, L.; Matei, N.; Mulholland, E.; Rózsai, M.; Tamba, M.; Wiesenthal, T. JRC-IDEES 2015. European Commission, Joint Research Centre (JRC) [Dataset] PID. 2018. Available online: http://data.europa.eu/89h/jrc-10110-10001 (accessed on 30 May 2020).

- Hekkert, M.P.; Suurs, R.A.; Negro, S.O.; Kuhlmann, S.; Smits, R.E. Functions of innovation systems: A new approach for analysing technological change. Technol. Forecast. Soc. Chang. 2007, 74, 413–432. [Google Scholar] [CrossRef]

- Nelson, R.; Winter, S.G. An Evolutionary Theory of Economic Change; Harvard University Press: Cambridge, MA, USA, 1982. [Google Scholar]

- Nelson, R.R.; Nelson, K. Technology, institutions, and innovation systems. Res. Policy 2002, 31, 265–272. [Google Scholar] [CrossRef]

- Callon, M. Society in the making: The study of technology as a tool for sociological analysis. In The Social Construction of Technological Systems: New Directions in the Sociology and History of Technology; MIT Press: Cambridge, MA, USA, 1987; pp. 83–103. [Google Scholar]

- Freeman, C. Technology, Policy, and Economic Performance: Lessons from Japan; Pinter Publishers: London, UK, 1987. [Google Scholar]

- Lundvall, B.A. National Systems of Innovation: Towards a Theory of Innovation and Interactive Learning; Pinter Publishers: London, UK, 1992. [Google Scholar]

- Nelson, R.R. (Ed.) National Innovation Systems: A Comparative Analysis; Oxford University Press: Oxford, UK, 1993. [Google Scholar]

- Asheim, B.T.; Isaksen, A. Location, agglomeration and innovation: Towards regional innovation systems in Norway? Eur. Plan. Stud. 1997, 5, 299–330. [Google Scholar] [CrossRef]

- Cooke, P.; Uranga, M.G.; Etxebarria, G. Regional innovation systems: Institutional and organisational dimensions. Res. Policy 1997, 26, 475–491. [Google Scholar] [CrossRef]

- Cooke, P. Regional innovation systems, clusters, and the knowledge economy. Ind. Corp. Chang. 2001, 10, 945–974. [Google Scholar] [CrossRef]

- Breschi, S.; Malerba, F. Sectoral innovation systems: Technological regimes, Schumpeterian dynamics, and spatial boundaries. In Systems of Innovation: Technologies, Institutions and Organizations; Edquist, C., Ed.; Pinter Publisher: London, UK, 1997; pp. 130–156. [Google Scholar]

- Malerba, F. Sectoral systems of innovation: A framework for linking innovation to the knowledge base, structure and dynamics of sectors. Econ. Innov. New Technol. 2005, 14, 63–82. [Google Scholar] [CrossRef]

- Carlsson, B.; Stankiewicz, R. On the nature, function and composition of technological systems. J. Evol. Econ. 1991, 1, 93–118. [Google Scholar] [CrossRef]

- Asheim, B.T.; Smith, H.L.; Oughton, C. Regional innovation systems: Theory, empirics and policy. Reg. Stud. 2011, 45, 875–891. [Google Scholar] [CrossRef]

- Frenz, M.; Oughton, C. Innovation in the UK Regions and Devolved Administrations: A Review of the Literatura; Final Report for the Department of Trade and Industry and the Office of the Deputy Prime Minister; DTI: London, UK, 2005.

- Binz, C.; Truffer, B. Global Innovation Systems—A conceptual framework for innovation dynamics in transnational contexts. Res. Policy 2017, 46, 1284–1298. [Google Scholar] [CrossRef]

- Bergek, A.; Jacobsson, S.; Carlsson, B.; Lindmark, S.; Rickne, A. Analyzing the functional dynamics of technological innovation systems: A scheme of analysis. Res. Policy 2008, 37, 407–429. [Google Scholar] [CrossRef]

- Nikas, A.; Doukas, H.; Lieu, J.; Tinoco, R.A.; Charisopoulos, V.; van der Gaast, W. Managing stakeholder knowledge for the evaluation of innovation systems in the face of climate change. J. Knowl. Manag. 2017, 21, 1013–1034. [Google Scholar] [CrossRef]

- Albu, M.; Griffith, A. Mapping the Market: A Framework for Rural Enterprise Development Policy and Practice; Practical Action: Rugby, UK, 2005. [Google Scholar]

- Markard, J.; Truffer, B. Technological innovation systems and the multi-level perspective: Towards an integrated framework. Res. Policy 2008, 37, 596–615. [Google Scholar] [CrossRef]

- Rip, A.; Kemp, R. Technological change. Hum. Choice Clim. Chang. 1998, 2, 327–399. [Google Scholar]

- Geels, F.W. Technological transitions as evolutionary reconfiguration processes: A multi-level perspective and a case-study. Res. Policy 2002, 31, 1257–1274. [Google Scholar] [CrossRef]

- Chung, C.C. National, sectoral and technological innovation systems: The case of Taiwanese pharmaceutical biotechnology and agricultural biotechnology innovation systems (1945–2000). Sci. Public Policy 2012, 39, 271–281. [Google Scholar] [CrossRef]

- Rogge, K.S.; Hoffmann, V.H. The impact of the EU ETS on the sectoral innovation system for power generation technologies–Findings for Germany. Energy Policy 2010, 38, 7639–7652. [Google Scholar] [CrossRef]

- Siva, V.; Hoppe, T.; Jain, M. Green buildings in Singapore; analyzing a frontrunner’s sectoral innovation system. Sustainability 2017, 9, 919. [Google Scholar] [CrossRef]

- Kim, Y.Z.; Lee, K. Sectoral innovation system and a technological catch-up: The case of the capital goods industry in Korea. Glob. Econ. Rev. 2008, 37, 135–155. [Google Scholar] [CrossRef]

- Sæther, B.; Isaksen, A.; Karlsen, A. Innovation by co-evolution in natural resource industries: The Norwegian experience. Geoforum 2011, 42, 373–381. [Google Scholar] [CrossRef]

- Andersen, P.D.; Andersen, A.D.; Jensen, P.A.; Rasmussen, B. Sectoral innovation system foresight in practice: Nordic facilities management foresight. Futures 2014, 61, 33–44. [Google Scholar] [CrossRef]

- Balaguer, A.; Marinova, D. Sectoral Transformation in the Photovoltaics Industry in Australia, Germany and Japan: Contrasting the Co-evolution of Actors, Knowledge, Institutions and Markets. Prometheus 2006, 24, 323–339. [Google Scholar] [CrossRef]

- Chunhavuthiyanon, M.; Intarakumnerd, P. The role of intermediaries in sectoral innovation system: The case of Thailand’s food industry. Int. J. Technol. Manag. Sustain. Dev. 2014, 13, 15–36. [Google Scholar] [CrossRef]

- Faber, A.; Hoppe, T. Co-constructing a sustainable built environment in the Netherlands—Dynamics and opportunities in an environmental sectoral innovation system. Energy Policy 2013, 52, 628–638. [Google Scholar] [CrossRef]

- Lechtenböhmer, S.; Nilsson, L.J.; Åhman, M.; Schneider, C. Decarbonising the energy intensive basic materials industry through electrification–Implications for future EU electricity demand. Energy 2016, 115, 1623–1631. [Google Scholar] [CrossRef]

- Åhman, M.; Nikoleris, A.; Nilsson, L.J. Decarbonising Industry in Sweden; IMES/EES report no 77; Lund University: Lund, Sweden, 2012; Volume 77. [Google Scholar]

- Wesseling, J.H.; Van der Vooren, A. Lock-in of mature innovation systems: The transformation toward clean concrete in the Netherlands. J. Clean. Prod. 2017, 155, 114–124. [Google Scholar] [CrossRef]

- Coenen, L.; López, F.J.D. Comparing systems approaches to innovation and technological change for sustainable and competitive economies: An explorative study into conceptual commonalities, differences and complementarities. J. Clean. Prod. 2010, 18, 1149–1160. [Google Scholar] [CrossRef]

- Geels, F.W. From sectoral systems of innovation to socio-technical systems: Insights about dynamics and change from sociology and institutional theory. Res. Policy 2004, 33, 897–920. [Google Scholar] [CrossRef]

- Markusen, A. Des lieux-aimants dans un espace mouvant: Une typologie des districts industriels. La Rich. Des Régions 2000, 85–119. [Google Scholar]

- Esparcia, J. Innovation and networks in rural areas. Anal. Eur. Innov. Projects. J. Rural Stud. 2014, 34, 1–14. [Google Scholar] [CrossRef]

- Napp, T.A.; Gambhir, A.; Hills, T.P.; Florin, N.; Fennell, P.S. A review of the technologies, economics and policy instruments for decarbonising energy-intensive manufacturing industries. Renew. Sustain. Energy Rev. 2014, 30, 616–640. [Google Scholar] [CrossRef]

- Klepper, S.; Malerba, F. Demand, innovation and industrial dynamics: An introduction. Ind. Corp. Chang. 2010, 19, 1515–1520. [Google Scholar] [CrossRef]

- Turnbull, P.; Oliver, N.; Wilkinson, B. Buyer-supplier relations in the UK-automotive industry: Strategic implications of the Japanese manufacturing model. Strateg. Manag. J. 1992, 13, 159–168. [Google Scholar] [CrossRef]

- Mazur, C.; Contestabile, M.; Offer, G.J.; Brandon, N.P. Understanding the drivers of fleet emission reduction activities of the German car manufacturers. Environ. Innov. Soc. Transit. 2015, 16, 3–21. [Google Scholar] [CrossRef]

- Malerba, F.; Orsenigo, L. Technological regimes and sectoral patterns of innovative activities. Ind. Corp. Chang. 1997, 6, 83–118. [Google Scholar] [CrossRef]

- Unruh, G.C. Understanding carbon lock-in. Energy Policy 2000, 28, 817–830. [Google Scholar] [CrossRef]

- Zhang, J.; Liang, X.J. Promoting green ICT in China: A framework based on innovation system approaches. Telecommun. Policy 2012, 36, 997–1013. [Google Scholar] [CrossRef]

- Bento, N.; Fontes, M. Spatial diffusion and the formation of a technological innovation system in the receiving country: The case of wind energy in Portugal. Environ. Innov. Soc. Transit. 2015, 15, 158–179. [Google Scholar] [CrossRef]

- Andersen, A.D.; Markard, J. Multi-technology interaction in socio-technical transitions: How recent dynamics in HVDC technology can inform transition theories. Technol. Forecast. Soc. Chang. 2020, 151, 119802. [Google Scholar] [CrossRef]

- Janipour, Z.; de Nooij, R.; Scholten, P.; Huijbregts, M.A.; de Coninck, H. What are sources of carbon lock-in in energy-intensive industry? A case study into Dutch chemicals production. Energy Res. Soc. Sci. 2020, 60, 101320. [Google Scholar] [CrossRef]

- Åhman, M.; Nilsson, L.J.; Johansson, B. Global climate policy and deep decarbonisation of energy-intensive industries. Clim. Policy 2017, 17, 634–649. [Google Scholar] [CrossRef]

- Bataille, C.; Åhman, M.; Neuhoff, K.; Nilsson, L.J.; Fischedick, M.; Lechtenböhmer, S.; Solano-Rodriquez, B.; Denis-Ryan, A.; Stiebert, S.; Waisman, H.; et al. A review of technology and policy deep decarbonization pathway options for making energy-intensive industry production consistent with the Paris Agreement. J. Clean. Prod. 2018, 187, 960–973. [Google Scholar] [CrossRef]

- Dewald, U.; Achternbosch, M. Why more sustainable cements failed so far? Disruptive innovations and their barriers in a basic industry. Environ. Innov. Soc. Transit. 2016, 19, 15–30. [Google Scholar] [CrossRef]

- Luiten, E.E.; Blok, K. Stimulating R&D of industrial energy-efficient technology; the effect of government intervention on the development of strip casting technology. Energy Policy 2003, 31, 1339–1356. [Google Scholar]

- Foxon, T.; Pearson, P. Overcoming barriers to innovation and diffusion of cleaner technologies: Some features of a sustainable innovation policy regime. J. Clean. Prod. 2008, 16, S148–S161. [Google Scholar] [CrossRef]

- Brown, M.A. Market failures and barriers as a basis for clean energy policies. Energy Policy 2001, 29, 1197–1207. [Google Scholar] [CrossRef]

- Foxon, T.J.; Gross, R.; Chase, A.; Howes, J.; Arnall, A.; Anderson, D. UK innovation systems for new and renewable energy technologies: Drivers, barriers and systems failures. Energy Policy 2005, 33, 2123–2137. [Google Scholar] [CrossRef]

- Perel, M. One Point of View: Corporate Courage: Breaking the Barrier to Innovation. Res. Technol. Manag. 2002, 45, 9–17. [Google Scholar] [CrossRef]

- Koasidis, K.; Karamaneas, A.; Nikas, A.; Neofytou, H.; Hermansen, E.A.; Vaillancourt, K.; Doukas, H. Many Miles to Paris: A Sectoral Innovation System Analysis of the Transport Sector in Norway and Canada in Light of the Paris Agreement. Sustainability 2020, 12, 5832. [Google Scholar] [CrossRef]

- Carlsson, B.; Jacobsson, S. In search of useful public policies—Key lessons and issues for policy makers. In Technological Systems and Industrial Dynamics; Springer: Boston, MA, USA, 1997; pp. 299–315. [Google Scholar]

- Lundvall, B.A. Innovation as an interactive process. In The Learning Economy and the Economics of Hope; Anthem Press: London, UK, 2016; pp. 61–84. [Google Scholar]

- Jack, S.L. The role, use and activation of strong and weak network ties: A qualitative analysis. J. Manag. Stud. 2005, 42, 1233–1259. [Google Scholar] [CrossRef]

- Weber, K.M.; Rohracher, H. Legitimizing research, technology and innovation policies for transformative change: Combining insights from innovation systems and multi-level perspective in a comprehensive ‘failures’ framework. Res. Policy 2012, 41, 1037–1047. [Google Scholar] [CrossRef]

- Giugni, M. Social Protest and Policy Change: Ecology, Antinuclear, And Peace Movements in Comparative Perspective; Rowman & Littlefield: Lanham, MD, USA, 2004. [Google Scholar]

- Gutberlet, T. Mechanization, Transportation, and the Location of Industry in Germany 1846 to 1907. Ph.D. Thesis, University of Arizona, Tucson, AZ, USA, 2013. [Google Scholar]

- Fernihough, A.; O’Rourke, K.H. Coal and the European Industrial Revolution (No. w19802); National Bureau of Economic Research: Cambridge, MA, USA, 2014. [Google Scholar]

- Schuetze, A.; Seythal, T. German antitrust watchdog fines Thyssen, Salzgitter, Voestalpine. Reuters. 2019. Available online: https://www.reuters.com/article/us-germany-steel/german-antitrust-watchdog-fines-thyssen-salzgitter-voestalpine-idUSKBN1YG0UA (accessed on 12 December 2019).

- Hasanbeigi, A.; Arens, M.; Price, L. Alternative emerging ironmaking technologies for energy-efficiency and carbon dioxide emissions reduction: A technical review. Renew. Sustain. Energy Rev. 2014, 33, 645–658. [Google Scholar] [CrossRef]

- Schmidt, S.; Minssen, H. Accounting for international assignments: The case of the German chemical industry. J. Hum. Resour. Costing Account. 2007, 11, 214–228. [Google Scholar] [CrossRef]

- Kahl, R.; Desel, H. Germany: Toxicology information on the World Wide Web. Toxicology 2003, 190, 23–33. [Google Scholar] [CrossRef]

- Markussen, P.; Svendsen, G.T. Industry lobbying and the political economy of GHG trade in the European Union. Energy Policy 2005, 33, 245–255. [Google Scholar] [CrossRef]

- Liebmann, H.; Kuder, T. Pathways and strategies of urban regeneration—Deindustrialized cities in eastern Germany. Eur. Plan. Stud. 2012, 20, 1155–1172. [Google Scholar] [CrossRef]

- IEA. Electricity Feed-In Law of 1991 (“Stromeinspeisungsgesetz”). 2013. Available online: https://www.iea.org/policies/3477-electricity-feed-in-law-of-1991-stromeinspeisungsgesetz (accessed on 14 March 2020).

- Lauber, V.; Jacobsson, S. The politics and economics of constructing, contesting and restricting socio-political space for renewables–The German Renewable Energy Act. Environ. Innov. Soc. Transit. 2016, 18, 147–163. [Google Scholar] [CrossRef]

- Renn, O.; Marshall, J.P. Coal, nuclear and renewable energy policies in Germany: From the 1950s to the “Energiewende”. Energy Policy 2016, 99, 224–232. [Google Scholar] [CrossRef]

- Hartung, J. Rules and regulations related to preventing pollution from animal manure in the Federal Republic of Germany. Agric. Ecosyst. Environ. 1986, 16, 273–279. [Google Scholar] [CrossRef]

- Drotloff, H. Reduction of Emissions by Chemical Industry from the German Emission Control Act to the Industrial Emission Directive (IED). Procedia Technol. 2014, 12, 637–642. [Google Scholar] [CrossRef][Green Version]

- Roudier, S.; Sancho, L.D.; Remus, R.; Aguado-Monsonet, M. Best Available Techniques (BAT) Reference Document for Iron and Steel Production: Industrial Emissions Directive 2010/75/EU: Integrated Pollution Prevention and Control (No. JRC69967); Joint Research Centre (Seville site): Brussels, Belgium, 2013. [Google Scholar]

- Conti, M.E.; Ciasullo, R.; Tudino, M.B.; Matta, E.J. The industrial emissions trend and the problem of the implementation of the Industrial Emissions Directive (IED). Air Qual. Atmos. Health 2015, 8, 151–161. [Google Scholar] [CrossRef]

- Graichen, V.; Schumacher, K.; Matthes, F.C.; Mohr, L.; Duscha, V.; Schleich, J.; Diekmann, J. Impacts of the EU Emissions Trading Scheme on the Industrial Competitiveness in Germany; German Federal Environment Agency: Berlin, Germany, 2008.

- Naegele, H.; Zaklan, A. Does the EU ETS cause carbon leakage in European manufacturing? J. Environ. Econ. Manag. 2019, 93, 125–147. [Google Scholar] [CrossRef]

- European Commission. Free Allowances. 2020. Available online: https://ec.europa.eu/clima/policies/ets/allowances_en (accessed on 18 March 2020).

- Wehrmann, B. Germany’s Steel Industry Needs Political Support to Cope with CO2-Reduction–Opinion. 2020. Available online: https://www.cleanenergywire.org/news/germanys-steel-industry-needs-political-support-cope-co2-reduction-opinion (accessed on 10 February 2020).

- Kiel Institute of World Economics. Zeit für Eine Neue Industriepolitik? (Report No. 122). 2019. Available online: https://www.ifw-kiel.de/fileadmin/Dateiverwaltung/IfW-Publications/-ifw/Kiel_Policy_Brief/Kiel_Policy_Brief_122.pdf (accessed on 5 March 2020).

- American Institute for Contemporary German Studies. The German Industry Strategy 2030: Inconsistent and Dangerous! 2019. Available online: https://www.aicgs.org/2019/05/the-german-industry-strategy-2030-inconsistent-and-dangerous/ (accessed on 6 May 2019).

- Federal Statistical Office of Germany. Production in October 2019: −1.7% Seasonally Adjusted on the Previous Month. 2019. Available online: https://www.destatis.de/EN/Press/2019/12/PE19_463_421.html (accessed on 6 April 2020).

- Canzler, W. Market and Technology Trends for the Automotive Future in Germany. In The Ecological Modernization Capacity of Japan and Germany; Springer: Wiesbaden, Germany, 2020; pp. 155–169. [Google Scholar]

- Arnold, M. German Industry Hit by Biggest Downturn Since 2009. Financial Times. 2019. Available online: https://www.ft.com/content/a1a14220-1801-11ea-9ee4-11f260415385 (accessed on 15 March 2020).

- Malerba, F.; Pisano, G.P. Innovation, competition and sectoral evolution: An introduction to the special section on Industrial Dynamics. Ind. Corp. Chang. 2019, 28, 503–510. [Google Scholar] [CrossRef]

- Hummen, T.; Ostertag, K. Consumption trends of steel and aluminium in the context of decarbonization (No. S3/2015). Work. Pap. Sustain. Innov. 2015, 1–20. [Google Scholar]

- Stahl. Statistics|Stahl-Online.de—Part 2. 2020. Available online: https://en.stahl-online.de/index.php/statistics/2/ (accessed on 16 June 2020).

- International Trade Administration. Steel Exports Report: Germany. 2017. Available online: https://legacy.trade.gov/steel/countries/pdfs/2017/q2/exports-germany.pdf (accessed on 16 June 2020).

- Global Wind Energy Council. Global Wind Report 2018. 2019. Available online: https://gwec.net/wp-content/uploads/2019/04/GWEC-Global-Wind-Report-2018.pdf (accessed on 24 April 2019).

- VDZ. Cement Markets, Regional Markets and the International Environment. 2020. Available online: https://www.vdz-online.de/en/cement-industry/cement-sector/cementmarkets/ (accessed on 16 June 2020).

- Supino, S.; Malandrino, O.; Testa, M.; Sica, D. Sustainability in the EU cement industry: The Italian and German experiences. J. Clean. Prod. 2016, 112, 430–442. [Google Scholar] [CrossRef]

- Eurostat. Production and International Trade in Chemicals. 2019. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php/Production_and_international_trade_in_chemicals#Growing_trade_in_chemicals (accessed on 3 August 2020).

- Keller, F.; Lee, R.P.; Meyer, B. Life cycle assessment of global warming potential, resource depletion and acidification potential of fossil, renewable and secondary feedstock for olefin production in Germany. J. Clean. Prod. 2020, 250, 119484. [Google Scholar] [CrossRef]

- Alkousaa, R.; Martin, M. German Chemical Industry Body Slashes 2019 Revenue Forecast. 2019. Reuters. Available online: https://www.reuters.com/article/germany-economy-chemicals/german-chemical-industry-body-slashes-2019-revenue-forecast-idUSS8N23X00I (accessed on 3 July 2020).

- Stephan, D. Downward Trend Continues: German Chemical Industry Cuts its 2019 Forecast. 2019. Available online: https://www.process-worldwide.com/downward-trend-continues-german-chemical-industry-cuts-its-2019-forecast-a-845313/ (accessed on 7 June 2020).

- Kädtler, J.; Sperling, H.J. After globalisation and financialisation: Logics of bargaining in the German automotive industry. Compet. Chang. 2002, 6, 149–168. [Google Scholar] [CrossRef]

- Fischedick, M.; Marzinkowski, J.; Winzer, P.; Weigel, M. Techno-economic evaluation of innovative steel production technologies. J. Clean. Prod. 2014, 84, 563–580. [Google Scholar] [CrossRef]

- Khurana, S.; Banerjee, R.; Gaitonde, U. Energy balance and cogeneration for a cement plant. Appl. Therm. Eng. 2002, 22, 485–494. [Google Scholar] [CrossRef]

- Luis, P.; Van der Bruggen, B. Exergy analysis of energy-intensive production processes: Advancing towards a sustainable chemical industry. J. Chem. Technol. Biotechnol. 2014, 89, 1288–1303. [Google Scholar] [CrossRef]

- Thollander, P.; Ottosson, M. Energy management practices in Swedish energy-intensive industries. J. Clean. Prod. 2010, 18, 1125–1133. [Google Scholar] [CrossRef]

- Arens, M.; Worrell, E.; Eichhammer, W.; Hasanbeigi, A.; Zhang, Q. Pathways to a low-carbon iron and steel industry in the medium-term–the case of Germany. J. Clean. Prod. 2017, 163, 84–98. [Google Scholar] [CrossRef]

- Arens, M.; Worrell, E.; Schleich, J. Energy intensity development of the German iron and steel industry between 1991 and 2007. Energy 2012, 45, 786–797. [Google Scholar] [CrossRef]

- Brunke, J.C.; Blesl, M. Energy conservation measures for the German cement industry and their ability to compensate for rising energy-related production costs. J. Clean. Prod. 2014, 82, 94–111. [Google Scholar] [CrossRef]

- Usón, A.A.; López-Sabirón, A.M.; Ferreira, G.; Sastresa, E.L. Uses of alternative fuels and raw materials in the cement industry as sustainable waste management options. Renew. Sustain. Energy Rev. 2013, 23, 242–260. [Google Scholar] [CrossRef]

- Bühler, F.; Guminski, A.; Gruber, A.; Nguyen, T.V.; von Roon, S.; Elmegaard, B. Evaluation of energy saving potentials, costs and uncertainties in the chemical industry in Germany. Appl. Energy 2018, 228, 2037–2049. [Google Scholar] [CrossRef]

- Erisman, J.W.; Sutton, M.A.; Galloway, J.; Klimont, Z.; Winiwarter, W. How a century of ammonia synthesis changed the world. Nat. Geosci. 2008, 1, 636–639. [Google Scholar] [CrossRef]

- Kuntke, P.; Śmiech, K.; Bruning, H.; Zeeman, G.; Saakes, M.; Sleutels, T.H.J.A.; Hamelers, H.V.M.; Buisman, C.J.N. Ammonium recovery and energy production from urine by a microbial fuel cell. Water Res. 2012, 46, 2627–2636. [Google Scholar] [CrossRef]

- Hawkesford, M.J. Reducing the reliance on nitrogen fertilizer for wheat production. J. Cereal Sci. 2014, 59, 276–283. [Google Scholar] [CrossRef]

- Ghanta, M.; Fahey, D.; Subramaniam, B. Environmental impacts of ethylene production from diverse feedstocks and energy sources. Appl. Petrochem. Res. 2014, 4, 167–179. [Google Scholar] [CrossRef]

- Schorcht, F.; Kourti, I.; Scalet, B.M.; Roudier, S.; Sancho, L.D. Best available techniques (BAT) reference document for the production of cement, lime and magnesium oxide. In European Commission Joint Research Centre Institute for Prospective Technological Studies (Report EUR 26129 EN); Publications Office of the European Union: Luxembourg, 2013. [Google Scholar]

- Falcke, H.; Holbrook, S.; Clenahan, I.; Carretero, A.L.; Sanalan, T.; Brinkmann, T.; Joze, R.; Benoît, Z.; Serge, R.; Sancho, L.D. Best Available Techniques (BAT) Reference Document for the Production of Large Volume Organic Chemicals; Publications Office of the European Union: Luxembourg, 2017. [Google Scholar]

- Kopfle, J.; Hunter, R. Direct reduction’s role in the world steel industry. Ironmak. Steelmak. 2008, 35, 254–259. [Google Scholar] [CrossRef]

- Gassmann, O.; Zeschky, M.; Wolff, T.; Stahl, M. Crossing the industry-line: Breakthrough innovation through cross-industry alliances with ‘non-suppliers’. Long Range Plan. 2010, 43, 639–654. [Google Scholar] [CrossRef]

- Leeson, D.; Mac Dowell, N.; Shah, N.; Petit, C.; Fennell, P.S. A Techno-economic analysis and systematic review of carbon capture and storage (CCS) applied to the iron and steel, cement, oil refining and pulp and paper industries, as well as other high purity sources. Int. J. Greenh. Gas Control 2017, 61, 71–84. [Google Scholar] [CrossRef]

- Dütschke, E.; Wohlfarth, K.; Höller, S.; Viebahn, P.; Schumann, D.; Pietzner, K. Differences in the public perception of CCS in Germany depending on CO2 source, transport option and storage location. Int. J. Greenh. Gas Control 2016, 53, 149–159. [Google Scholar] [CrossRef]

- Dütschke, E. What drives local public acceptance–comparing two cases from Germany. Energy Procedia 2011, 4, 6234–6240. [Google Scholar] [CrossRef]

- Vögele, S.; Rübbelke, D.; Mayer, P.; Kuckshinrichs, W. Germany’s “No” to carbon capture and storage: Just a question of lacking acceptance? Appl. Energy 2018, 214, 205–218. [Google Scholar] [CrossRef]

- Lee, R.P. Alternative carbon feedstock for the chemical industry?-Assessing the challenges posed by the human dimension in the carbon transition. J. Clean. Prod. 2019, 219, 786–796. [Google Scholar] [CrossRef]

- Forsberg, C.W. Future hydrogen markets for large-scale hydrogen production systems. Int. J. Hydrogen Energy 2007, 32, 431–439. [Google Scholar] [CrossRef]

- Schwarze, K.; Posdziech, O.; Kroop, S.; Lapeña-Rey, N.; Mermelstein, J. Green industrial hydrogen via reversible high-temperature electrolysis. Ecs Trans. 2017, 78, 2943. [Google Scholar] [CrossRef]

- Vogl, V.; Åhman, M.; Nilsson, L.J. Assessment of hydrogen direct reduction for fossil-free steelmaking. J. Clean. Prod. 2018, 203, 736–745. [Google Scholar] [CrossRef]

- Amelang, S. German Industry Needs Policy Trigger for Deep Emission Cuts. 2020. Available online: https://www.cleanenergywire.org/news/german-industry-needs-policy-trigger-deep-emission-cuts (accessed on 24 April 2020).

- Spear, B. Iron and steel patents: The sinews of the GB Industrial Revolution. World Pat. Inf. 2019, 58, 101901. [Google Scholar] [CrossRef]

- Spear, B. Coal–Parent of the Industrial Revolution in Great Britain: The early patent history. World Pat. Inf. 2014, 39, 85–88. [Google Scholar] [CrossRef]

- Dobson, P.; Waterson, M. The competition effects of industry-wide vertical price fixing in bilateral oligopoly. Int. J. Ind. Organ. 2007, 25, 935–962. [Google Scholar] [CrossRef]

- Kim, J.W.; Lee, J.Y.; Kim, J.Y.; Lee, H.K. Sources of productive efficiency: International comparison of iron and steel firms. Resour. Policy 2006, 31, 239–246. [Google Scholar] [CrossRef]

- Sourisseau, S. The global iron and steel industry: From a bilateral oligopoly to a thwarted monopsony. Aust. Econ. Rev. 2018, 51, 232–243. [Google Scholar] [CrossRef]

- Burgess, T.; Hwarng, B.; Shaw, N.; De Mattos, C. Enhancing Value Stream Agility: The UK Speciality Chemical Industry. Eur. Manag. J. 2002, 20, 199–212. [Google Scholar] [CrossRef]

- Lampadarios, E. Critical challenges for SMEs in the UK chemical distribution industry. J. Bus. Chem. 2016, 13, 17–32. [Google Scholar]

- Department for Business; Energy & Industrial Strategy. International Comparison of the UK Research Base, 2019. 2019. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/815400/International_comparison_of_the_UK_research_base__2019._Accompanying_note.pdf (accessed on 26 July 2020).

- Her Majesty’s Treasury. Budget 2020. 2020. Available online: https://www.gov.uk/government/publications/budget-2020-documents/budget-2020#fn:62 (accessed on 26 July 2020).

- Centre for Global Higher Education. UK Universities Interacting with Industry: Patterns of Research Collaboration and Inter-sectoral Mobility of Academic Researchers. 2017. Available online: https://www.researchcghe.org/perch/resources/publications/wp14.pdf (accessed on 26 July 2020).

- European Commission. The Industrial Emissions Directive-Environment-European Commission. 2020. Available online: https://ec.europa.eu/environment/industry/stationary/ied/legislation.htm (accessed on 28 May 2020).

- Trew, A. Spatial takeoff in the first industrial revolution. Rev. Econ. Dyn. 2014, 17, 707–725. [Google Scholar] [CrossRef]

- Tradingeconomics. United Kingdom. 2020. Available online: https://tradingeconomics.com/united-kingdom (accessed on 28 May 2020).

- Shanks, W.; Dunant, C.; Drewniok, M.; Lupton, R.; Serrenho, A.; Allwood, J. How much cement can we do without? Lessons from cement material flows in the UK. Resour. Conserv. Recycl. 2019, 141, 441–454. [Google Scholar] [CrossRef]

- Singh, K. Chemistry in Daily Life; PHI Learning Pvt. Ltd.: New Delhi, India, 2012. [Google Scholar]

- USGS. Cement Statistics and Information. 2020. Available online: https://www.usgs.gov/centers/nmic/cement-statistics-and-information (accessed on 26 May 2020).

- Griffin, P.; Hammond, G. Analysis of the potential for energy demand and carbon emissions reduction in the iron and steel sector. Energy Procedia 2019, 158, 3915–3922. [Google Scholar] [CrossRef]

- Millward-Hopkins, J.; Zwirner, O.; Purnell, P.; Velis, C.; Iacovidou, E.; Brown, A. Resource recovery and low carbon transitions: The hidden impacts of substituting cement with imported ‘waste’ materials from coal and steel production. Glob. Environ. Chang. 2018, 53, 146–156. [Google Scholar] [CrossRef]

- Langley, K.F. Energy efficiency in the UK iron and steel industry. Appl. Energy 1986, 23, 73–107. [Google Scholar] [CrossRef]

- Griffin, P.; Hammond, G. Industrial energy use and carbon emissions reduction in the iron and steel sector: A UK perspective. Appl. Energy 2019, 249, 109–125. [Google Scholar] [CrossRef]

- WSP; Parsons Brinckerhoff; DNV-GL. Industrial Decarbonisation & Energy Efficiency Roadmaps to 2050 Cement. Report for the Department of Energy and Climate Change and the Department for Business, Innovation and Skills. 2015. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/416674/Cement_Report.pdf (accessed on 5 March 2020).

- WSP; Parsons Brinckerhoff; DNV-GL. Industrial Decarbonisation & Energy Efficiency Roadmaps to 2050 Cross-Sector Summary. Report for the Department of Energy and Climate Change and the Department for Business, Innovation and Skills. 2015. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/419912/Cross_Sector_Summary_Report.pdf (accessed on 20 March 2020).

- Mirasgedis, S.; Hontou, V.; Georgopoulou, E.; Sarafidis, Y.; Gakis, N.; Lalas, D.; Loukatos, A.; Gargoulas, N.; Mentzis, A.; Economidis, D.; et al. Environmental damage costs from airborne pollution of industrial activities in the greater Athens, Greece area and the resulting benefits from the introduction of BAT. Environ. Impact Assess. Rev. 2008, 28, 39–56. [Google Scholar] [CrossRef]

- He, K.; Wang, L. A review of energy use and energy-efficient technologies for the iron and steel industry. Renew. Sustain. Energy Rev. 2017, 70, 1022–1039. [Google Scholar] [CrossRef]

- Cormos, A.; Cormos, C. Reducing the carbon footprint of cement industry by post-combustion CO2 capture: Techno-economic and environmental assessment of a CCS project in Romania. Chem. Eng. Res. Des. 2017, 123, 230–239. [Google Scholar] [CrossRef]

- Stockford, C.; Brandon, N.; Irvine, J.; Mays, T.; Metcalfe, I.; Book, D.; Ekins, P.; Kucernak, A.; Molkov, V.; Steinberger-Wilckens, R.; et al. H2FC SUPERGEN: An overview of the Hydrogen and Fuel Cell research across the UK. Int. J. Hydrogen Energy 2015, 40, 5534–5543. [Google Scholar] [CrossRef]

- Stenberg, V.; Rydén, M.; Mattisson, T.; Lyngfelt, A. Exploring novel hydrogen production processes by integration of steam methane reforming with chemical-looping combustion (CLC-SMR) and oxygen carrier aided combustion (OCAC-SMR). Int. J. Greenh. Gas Control 2018, 74, 28–39. [Google Scholar] [CrossRef]

- Unruh, G.C. Escaping carbon lock-in. Energy Policy 2002, 30, 317–325. [Google Scholar] [CrossRef]

- Brown, M.A.; Chandler, J.; Lapsa, M.V.; Sovacool, B.K. Carbon Lock-in: Barriers to Deploying Climate Change Mitigation Technologies (No. ORNL/TM-2007/124); Oak Ridge National Lab. (ORNL): Oak Ridge, TN, USA; Georgia Inst. of Technology: Atlanta, GA, USA, 2008. [Google Scholar]

- Lehmann, P.; Creutzig, F.; Ehlers, M.H.; Friedrichsen, N.; Heuson, C.; Hirth, L.; Pietzcker, R. Carbon lock-out: Advancing renewable energy policy in Europe. Energies 2012, 5, 323–354. [Google Scholar] [CrossRef]

- Tvaronavičius, V.; Tvaronavičiene, M. Role of fixed investments in economic growth of country: Lithuania in European context. J. Bus. Econ. Manag. 2008, 9, 57–64. [Google Scholar] [CrossRef][Green Version]

- Haskel, J.; Wallis, G. Public support for innovation, intangible investment and productivity growth in the UK market sector. Econ. Lett. 2013, 119, 195–198. [Google Scholar] [CrossRef]

- Buschmann, P.; Oels, A. The overlooked role of discourse in breaking carbon lock-in: The case of the German energy transition. Wiley Interdiscip. Rev. Clim. Chang. 2019, 10, e574. [Google Scholar] [CrossRef]

- Bugeaud, F.; Pietyra, P.; Liger, V. From Service Design to Innovation through Services: Emergence of a Methodological and Systemic Framework. In Working Conference on Virtual Enterprises; Springer: Berlin/Heidelberg, Germany, 2013; pp. 431–438. [Google Scholar]

- Parker, R.; Cox, S. The state and the extractive industries in Australia: Growth for whose benefit? Extr. Ind. Soc. 2020, 7, 621–627. [Google Scholar] [CrossRef]

- García-Cabrera, A.; Durán-Herrera, J.; Suárez-Ortega, S. Multinationals’ political activity for institutional change: Evidence from Spain during the international crisis of 2008. Eur. Manag. J. 2019, 37, 541–551. [Google Scholar] [CrossRef]

- Pfeifer, S.; Gordon, S.; Pooler, M. Is the UK’s New Industrial Strategy Starting to Work? Financial Times. 2018. Available online: https://www.ft.com/content/bb242140-ef2b-11e8-89c8-d36339d835c0 (accessed on 26 May 2020).

- Partington, R. Watchdog Attacks Tories for ‘Neglecting Industrial Strategy’. The Guardian. 2020. Available online: https://www.theguardian.com/politics/2020/feb/19/watchdog-attacks-tories-for-neglecting-industrial-strategy-boris-johnson-uk-economy (accessed on 19 March 2020).

- Weng, Q.; Xu, H. A review of China’s carbon trading market. Renew. Sustain. Energy Rev. 2018, 91, 613–619. [Google Scholar] [CrossRef]

- Crompton, P.; Lesourd, J. Economies of scale in global iron-making. Resour. Policy 2008, 33, 74–82. [Google Scholar] [CrossRef]

- Worrell, E.; Biermans, G. Move over! Stock turnover, retrofit and industrial energy efficiency. Energy Policy 2005, 33, 949–962. [Google Scholar] [CrossRef]

- Dawood, F.; Anda, M.; Shafiullah, G.M. Hydrogen production for energy: An overview. Int. J. Hydrogen Energy 2020, 45, 3847–3869. [Google Scholar] [CrossRef]

- Mao, X.; He, C. A trade-related pollution trap for economies in transition? Evidence from China. J. Clean. Prod. 2018, 200, 781–790. [Google Scholar] [CrossRef]

- Latorre, M.C.; Olekseyuk, Z.; Yonezawa, H. Trade and foreign direct investment-related impacts of Brexit. World Econ. 2020, 43, 2–32. [Google Scholar] [CrossRef]

- Jafari, Y.; Britz, W. Brexit: An economy-wide impact assessment on trade, immigration, and foreign direct investment. Empirica 2020, 47, 17–52. [Google Scholar] [CrossRef]

- Davies, R. British Steel Rescue: UK Extends Funding ahead of Decision on Jingye. The Guradian. 2020. Available online: https://www.theguardian.com/business/2020/feb/28/british-steel-rescue-uk-extends-funding-ahead-of-decision-on-jingye (accessed on 28 March 2020).

- Johnson, B.H.; Charles, E.; Hommen, L.; Lemola, T.; Malerba, F.; Reiss, T.; Smith, K. The ISE Policy Statement: The Innovation Policy Implications of the ISE Research Project; VBN: Aalborg, Denmark, 1998. [Google Scholar]

- Pisano, G. Profiting from innovation and the intellectual property revolution. Res. Policy 2006, 35, 1122–1130. [Google Scholar] [CrossRef]

- Borghesi, S.; Cainelli, G.; Mazzanti, M. Linking emission trading to environmental innovation: Evidence from the Italian manufacturing industry. Res. Policy 2015, 44, 669–683. [Google Scholar] [CrossRef]

- Kuik, O.; Hofkes, M. Border adjustment for European emissions trading: Competitiveness and carbon leakage. Energy Policy 2010, 38, 1741–1748. [Google Scholar] [CrossRef]

- Vögele, S.; Grajewski, M.; Govorukha, K.; Rübbelke, D. Challenges for the European steel industry: Analysis, possible consequences and impacts on sustainable development. Appl. Energy 2020, 264, 114633. [Google Scholar] [CrossRef]

- Walz, R. Towards a dynamic understanding of innovation systems: An integrated TIS-MLP approach for wind turbines. In New Developments in Eco-Innovation Research; Springer: Cham, Switzerland, 2018; pp. 277–295. [Google Scholar]

- Mazur, C.; Contestabile, M.; Offer, G.J.; Brandon, N.P. Assessing and comparing German and UK transition policies for electric mobility. Environ. Innov. Soc. Transit. 2015, 14, 84–100. [Google Scholar] [CrossRef]

- Wagner, O.; Adisorn, T.; Tholen, L.; Kiyar, D. Surviving the Energy Transition: Development of a Proposal for Evaluating Sustainable Business Models for Incumbents in Germany’s Electricity Market. Energies 2020, 13, 730. [Google Scholar] [CrossRef]

- Bukovszki, V.; Magyari, Á.; Braun, M.K.; Párdi, K.; Reith, A. Energy Modelling as a Trigger for Energy Communities: A Joint Socio-Technical Perspective. Energies 2020, 13, 2274. [Google Scholar] [CrossRef]

- Miedema, J.H.; Van der Windt, H.J.; Moll, H.C. Opportunities and barriers for biomass gasification for green gas in the dutch residential sector. Energies 2018, 11, 2969. [Google Scholar] [CrossRef]

- Doukas, H.; Nikas, A. Decision support models in climate policy. Eur. J. Oper. Res. 2020, 280, 1–24. [Google Scholar] [CrossRef]

- Doukas, H.; Nikas, A.; González-Eguino, M.; Arto, I.; Anger-Kraavi, A. From integrated to integrative: Delivering on the Paris Agreement. Sustainability 2018, 10, 2299. [Google Scholar] [CrossRef]

- Nikas, A.; Lieu, J.; Sorman, A.; Gambhir, A.; Turhan, E.; Vienni Baptista, B.; Doukas, H. The desirability of transitions in demand: Incorporating behavioural and societal transformations into energy modelling. Energy Res. Soc. Sci. 2020, 70, 101780. [Google Scholar] [CrossRef]

- Van Sluisveld, M.A.; Hof, A.F.; Carrara, S.; Geels, F.W.; Nilsson, M.; Rogge, K.; Turnheim, B.; van Vuuren, D.P. Aligning integrated assessment modelling with socio-technical transition insights: An application to low-carbon energy scenario analysis in Europe. Technol. Forecast. Soc. Chang. 2018, 151, 119177. [Google Scholar] [CrossRef]

- Rogge, K.S.; Pfluger, B.; Geels, F.W. Transformative policy mixes in socio-technical scenarios: The case of the low-carbon transition of the German electricity system (2010–2050). Technol. Forecast. Soc. Chang. 2018, 151, 119259. [Google Scholar] [CrossRef]

- Geels, F.W.; McMeekin, A.; Pfluger, B. Socio-technical scenarios as a methodological tool to explore social and political feasibility in low-carbon transitions: Bridging computer models and the multi-level perspective in UK electricity generation (2010–2050). Technol. Forecast. Soc. Chang. 2018, 151, 119258. [Google Scholar] [CrossRef]

- Bachner, G.; Wolkinger, B.; Mayer, J.; Tuerk, A.; Steininger, K.W. Risk assessment of the low-carbon transition of Austria’s steel and electricity sectors. Environ. Innov. Soc. Transit. 2018, 35, 309–332. [Google Scholar] [CrossRef]

- Vögele, S.; Rübbelke, D.; Govorukha, K.; Grajewski, M. Socio-technical scenarios for energy-intensive industries: The future of steel production in Germany. Clim. Chang. 2019. [Google Scholar] [CrossRef]

- Nikas, A.; Stavrakas, V.; Arsenopoulos, A.; Doukas, H.; Antosiewicz, M.; Witajewski-Baltvilks, J.; Flamos, A. Barriers to and consequences of a solar-based energy transition in Greece. Environ. Innov. Soc. Transit. 2020, 35, 383–399. [Google Scholar] [CrossRef]

- Antosiewicz, M.; Nikas, A.; Szpor, A.; Witajewski-Baltvilks, J.; Doukas, H. Pathways for the transition of the Polish power sector and associated risks. Environ. Innov. Soc. Transit. 2020, 35, 271–291. [Google Scholar] [CrossRef]

- United Nations. International Standard Industrial Classification of All Economic Activities (Isic) Rev. 4; United Nations Publishing: New York, NY, USA, 2008. [Google Scholar]

- World Steel Association. About Steel. 2020. Available online: https://www.worldsteel.org/about-steel.html (accessed on 28 May 2020).

- Eurofer. European Steel in Figures 2019. 2019. Available online: http://www.eurofer.org/News%26Events/PublicationsLinksList/201907-SteelFigures.pdf (accessed on 10 April 2020).

- Razzaq, R.; Li, C.; Zhang, S. Coke oven gas: Availability, properties, purification, and utilization in China. Fuel 2013, 113, 287–299. [Google Scholar] [CrossRef]

- Geerdes, M.; Chaigneau, R.; Kurunov, I. Modern blast furnace ironmaking: An introduction (2015); Ios Press: Amsterdam, The Netherlands, 2015. [Google Scholar]

- Orth, A.; Anastasijevic, N.; Eichberger, H. Low CO2 emission technologies for iron and steelmaking as well as titania slag production. Miner. Eng. 2007, 20, 854–861. [Google Scholar] [CrossRef]

- Anameric, B.; Kawatra, S.K. Direct iron smelting reduction processes. Miner. Process. Extr. Metall. Rev. 2008, 30, 1–51. [Google Scholar] [CrossRef]

- Xiaoguang, Y.; Wanren, X.; Shaobo, Z. Theoretic Analysis on Using Top Gas-recycle and Coal-injection Technologies to Reduce Fuel Consumption of COREX/FINEX Process. Baosteel Technol. 2008, 6, 23–28. [Google Scholar]

- Yüksel, İ. A review of steel slag usage in construction industry for sustainable development. Environ. Dev. Sustain. 2017, 19, 369–384. [Google Scholar] [CrossRef]

- Proctor, D.M.; Fehling, K.A.; Shay, E.C.; Wittenborn, J.L.; Green, J.J.; Avent, C.; Bigham, R.D.; Connolly, M.; Lee, B.; Shepker, T.O.; et al. Physical and chemical characteristics of blast furnace, basic oxygen furnace, and electric arc furnace steel industry slags. Environ. Sci. Technol. 2000, 34, 1576–1582. [Google Scholar] [CrossRef]

- Worrell, E. Cement and Energy. Reference Module in Earth Systems and Environmental Sciences; Elsevier: Amsterdam, The Netherlands, 2014. [Google Scholar]

- Hurley, P.; Pritchard, R. CEMENT. Encycl. Anal. Sci. 2005, 21, 458–463. [Google Scholar]

- Hannant, D.; Venkata Siva, S.; Sreekanth, P.R. 5.15 Cement-Based Composites. In Comprehensive Composite Materials II; Elsevier: Amsterdam, The Netherlands, 2018; pp. 379–420. [Google Scholar]

- Oliveira, F.; Fernandes, J.; Galindo, J.; Rodríguez, J.; Cañadas, I.; Vermelhudo, V.; Nunes, A.; Rosa, L. Portland cement clinker production using concentrated solar energy—A proof-of-concept approach. Sol. Energy 2019, 183, 677–688. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Germany | UK | |||

|---|---|---|---|---|

| Resilience to Failures | Potential Causes of Failures | Resilience to Failures | Potential Causes of Failures | |

| Interactions | Network of active associations and companies A large number of SMEs especially for the chemical sector | Strong network interactions lead to lobbying practices and strategic decisions that threaten competition | Renowned universities that perform research activities A large number of SMEs especially for the chemical sector | |

| Institutional | Active environmental policy Optimistic targets and political will to achieve them | Industrial strategy hesitant and overoptimistic Industrial Policy not elaborated regarding high cost innovation Strict regulation causes fear of carbon leakage | Active environmental policy Optimistic targets and political will to achieve them | Industrial Policy focuses more on financial rather than environmental issues Limited funding for a vast number of policies Strict regulation cause fear of carbon leakage Uncertainty after withdrawing from the EU |

| Capabilities | Strong consumers (e.g., automotive industry for the iron and steel sector) Adequate operational capabilities High share of EAF compared to BF/BOF for steel production Existing DRI plant | Possible downturn when the automotive industry faces problems Problem supporting innovative processes due to high investment cost Consumers reluctant over higher cost of “green” products Carbon lock-into conservative dominant processes Difficulty in combining technologies like CCS, EAF | Adequate operational capabilities | Problem supporting innovative processes due to high investment cost The shrinking industry causes decline in demand Consumers reluctant over higher cost of “green” products Carbon lock-into conservative dominant processes Difficulty in combining technologies like CCS, EAF Low share of EAF compared to BF/BOF for steel production |

| Infrastructural | Strong Infrastructures | Strong Infrastructures | ||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Koasidis, K.; Nikas, A.; Neofytou, H.; Karamaneas, A.; Gambhir, A.; Wachsmuth, J.; Doukas, H. The UK and German Low-Carbon Industry Transitions from a Sectoral Innovation and System Failures Perspective. Energies 2020, 13, 4994. https://doi.org/10.3390/en13194994

Koasidis K, Nikas A, Neofytou H, Karamaneas A, Gambhir A, Wachsmuth J, Doukas H. The UK and German Low-Carbon Industry Transitions from a Sectoral Innovation and System Failures Perspective. Energies. 2020; 13(19):4994. https://doi.org/10.3390/en13194994

Chicago/Turabian StyleKoasidis, Konstantinos, Alexandros Nikas, Hera Neofytou, Anastasios Karamaneas, Ajay Gambhir, Jakob Wachsmuth, and Haris Doukas. 2020. "The UK and German Low-Carbon Industry Transitions from a Sectoral Innovation and System Failures Perspective" Energies 13, no. 19: 4994. https://doi.org/10.3390/en13194994

APA StyleKoasidis, K., Nikas, A., Neofytou, H., Karamaneas, A., Gambhir, A., Wachsmuth, J., & Doukas, H. (2020). The UK and German Low-Carbon Industry Transitions from a Sectoral Innovation and System Failures Perspective. Energies, 13(19), 4994. https://doi.org/10.3390/en13194994