Abstract

Our knowledge of discount rates plays an important role both in the discounted cash flow decision-making process and in the later phases of a project’s lifetime. It is useful than both for management and cash-flow monitoring purposes at operating stages. Investors putting money into power generation projects expect an appropriate rate of return to compensate them for a minimum acceptable real return available in the market (risk-free rate of interest) and the project’s specific risk. Due to its essential nature in the financial and economic evaluation of projects (it is the only parameter that reflects the risk), it is reasonable to assume that investors would also be interested in constituent components of that indicator. The discount rate is one parameter in the discounted cash flow analysis that takes into account the risk of a venture. Further, the previous research in this area has focused mainly on the dimension of this variable, and the structure of this parameter has not been dealt with any other studies. The proposed idea of this study met the expectations of the industry—it aimed to present a typical project implemented in the energy industry, a relatively simple methodology that allowed estimating the components within the cost of equity capital of the enterprise. In the power generation sector, one can find various types of discount rates—assessed for multiple technologies, at different development stages, and expressed differently. Owing to the know-how and decades-long experience, coal-fired power projects’ remarks may be a good benchmark for alternative low carbon technologies. That is why, in this work, a discount rate for valuing investment in new coal-fired power projects was evaluated. This assessment was made on the “bare-bones” assumption, meaning evaluations at 100% equity, after-tax, in constant (real) currency units. The analysis of the discount rate structure was performed by applying the procedure of the classical sensitivity analysis having the accuracy of key input parameters. Finally, the risk factors within the risk-adjusted discount rate were calculated. The obtained results showed the importance of individual risk factors within the risk-adjusted discount rate used in coal energy projects, which would enable a more pragmatic approach to controlling this parameter by decision-makers and understanding the risk.

1. Introduction

Despite the existence of alternative methods of assessing the effectiveness of investment projects, e.g., real options valuation (ROV), discounted cash-flow analysis (DCF) remains an essential tool in the fuel and energy sector, allowing for making investment decisions and, consequently, effective management of projects (for example “Guidelines for Economic Analysis of Power Sector Projects” [1] or Dranka et al. [2], Hemerlink, de Jager [3], etc.). This method is based on money as a universal medium of exchange, assuming that making an investment decision is only rational if sufficiently a high return is expected on the invested cash over a certain period. It should be stressed that the DCF analysis requires a broad set of reliable data in terms of forecasts of investment outlays, prices, costs, and production volumes. Therefore, this method is used at the planning stage to assess the effectiveness of projects analyzed in the pre-feasibility, feasibility, and operational phases.

It should be asserted that the DCF methodology tacitly assumes that the project will be implemented according to the most probable (for the moment of assessment) scenario of events in which the expected statistical sense and values of input variables will occur, as presented by Bliński [4]. The parameter that expresses the risk that the situation may develop differently from what is expected is the cost of capital, also called the discount rate, as presented by Andrén and Jankensgård [5].

Decision-making on projects is based on the investment criteria defined in the DCF analysis, which are related to defined economic performance indicators, which are:

- −

- net present value (NPV)

- −

- internal rate of return (IRR)

- −

- discounted payback period (DPP)

The decision criteria say that the project under consideration should be undertaken if the NPV > 0 or IRR > than the cost of capital involved at the discount rate. An adopted discount rate is, therefore, a reference point in the IRR criterion and an integral part of the formula determining the value scale. It plays a vital role in all the processes of assessing the economic efficiency of business ventures, being the key that constitutes an attempt both for making decisions and controlling operations at the operational stage [6].

Since the level of the discount rate is closely related to the risk level of the project under consideration, in industrial practice, there is an unresolved problem of analytical determination of the discount rate [7,8]. This practice recommends using the weighted average cost of capital (WACC)—a discount rate calculated based on the cost of equity and debt in proportion to their shares in the pool of capital expenditures. Cost of equity, often referred to the risk-adjusted discount rate (RADR), is calculated analytically most often in the procedure of the capital asset pricing model (CAPM), as a result of the analysis of linear regression of returns on shares of the company under consideration and returns on the securities market (determination of the so-called beta coefficient). RADR rates vary by industry and company, and it means, if there is a higher risk, then there will be a higher cost of equity. In recent years, the cost of capital in the power generation sector has been analyzed in many of the studies, as cited below. The studies depend on the country, technology, project advancement, and time. In this paper, despite current efforts to decarbonize energy, the focus was on the analysis of discount rates of companies using coal-fired power stations. This choice was made for three reasons. Firstly, due to the possession of new units, the Polish power industry will be based on coal for several decades to come [9,10]. Secondly, because of the established knowledge of this type of generation, it can be a kind of benchmark for other low-carbon technologies. Thirdly, in some regions, even despite environmental conditions, power generation from modern coal-based sources remains the cheapest way to produce power, so knowledge about the discount rate can be valuable and needed.

None of the quoted sources deals with the subject of the in-depth structure of the discount rate “adjusted to the risk”—an answer to the question to what extent the risk of key parameters of investment projects implemented in the coal sector affects the level of the cost of equity. It is worth noting that investors from the power generation industry, particularly in the coal-using sector, are generally well versed in terms of sources and risks [11,12,13,14,15]. However, their opinions, expressed in terms of the cost of equity, differ.

In light of these considerations, the purpose of this paper was to determine the components of the risk-adjusted discount rate. Knowledge of the scope of risk related to particular variables is important for planning, but first of all—making decisions on launching the investment and then managing the risk of the project [16,17]. This paper proposed the selection of the discount rate for projects as a degressive rate concerning the extent of risk involved. The first part presents the generally accepted approach to the setting of discount rates, with concepts for estimating these indicators for investment projects. The following parts present current practice in the selection of discount factors for projects, followed by a proposal to modify this approach using a degressive rate. At the end of the paper, the proposed concept has been verified on a concrete example from the industry.

2. Methods and Data

While speaking about the discount rate, it is worth noting that there are two ways of discounting in the power generation industry—from the position of a private investor and the social point of view. The first discloses the discount rate, as a behavioral parameter, linked to the rates that market participants apply to their daily investment decisions. In economic theory, they reflect the cost of capital, which is the expected rate of return required by investors on shares or other securities with the same risks as the project [18,19]. The second approach uses the so-called social discount rate, considering the long-term social interest [20,21]. It differs from the classic discount rate in that it is time-varying in hyperbolic mode. The rate “weighs” the intergenerational benefit and is, therefore, used to assess the total costs and benefits of power generation systems [22,23]. This paper, however, focused on the classic financial discount rate, which is used to assess the economic efficiency of projects by individual investors.

Most of the studies on the a/m topics focus mainly on determining the corporate discount rate (WACC) in nominal or real terms, without taking into account the sophistication and risk of individual projects. As mentioned, the WACC “weighs” the cost of equity and debt according to the formula:

where:

RE, RD—the cost of equity and debt, respectively,

VE, VD—the size of equity and debt capital in financing the project, respectively,

TAX—corporate tax rate.

As stated before, RE (≡ RADR) rate is usually calculated using the CAPM model, according to the formula:

where:

RADR—the cost of equity—expected return on shares q,

Rf—expected risk-free rate,

Rm—expected market return,

Β—risk-determining factor related to shares q.

Of course, WACC is lower than RADR, as the cost of debt is usually lower than the cost of equity.

It is worth noting the recurring adjective “expected”—the calculation should refer to the future, while all variables in the formula are usually determined from historical data. This is obvious but has rarely raised the theoretical dissonance. The data acquired from the past is indeed reflected in the future. Thus, the model reflects the future.

In order to remove the financial leverage effect, the RADR is expressed in an unlevered form. Unlevered beta (βUL) refers to differences between companies concerning capital structure. This indicator shows how much of the observed risk of shares of a given company is specific, directly related to the business model of the company:

where:

TAX, VE, VD—as above.

Thus, in the RADR calculation, the debt component is removed from all asset risk.

- −

- At this point, it is necessary to mention an important attribute of the capital asset valuation model. The cost of equity obtained in this algorithm is a discount rate for the whole company, not for the individual project. Therefore, concerning a given country, an industry (here: the power generation sector) in the literature, we can find different values depending on the company, its advancement, age of the technology used, the period, and the way it is expressed. For example, for companies using coal-fired power plants, the following figures can be recognized:

- −

- According to Organisation for Economic Co-operation and Development data (2010) [24], the real cost of equity calculated for years 2003–2004 after-tax is 8.7%;

- −

- According to World Energy Council (2013) [25], it is 10% with a comment that at present (i.e., in 2013), in case of construction of new coal-fired units, investors can expect as much as 18% and more (there is no information whether this is a pre- or post-tax rate and whether in nominal or real terms);

- −

- Surface Transportation Board (2015) [26] gave the cost of equity, real, after-tax for regulated electric companies (without specifying the fuel used) at 6.4%, while coal companies at 9.7%;

- −

- According to National Economic Research Associates (NERA) (2015) [27], hurdle rates for newly built modern coal-fired sources for 2015 (after-tax, real) are 7.75% (reference scenario; 6.18%—low scenario, and 9.31%—high scenario); and for 2030 (after-tax, real) are 8.57% (reference scenario, 7.48%—low scenario, 16.3%—high scenario);

- −

- Nine percent gives Nalbandian-Sugden (2016) [28], but without any other additional information;

- −

- Zamasz [29] gave the real RADR of several dozen companies from the traditional U.S. power generation sector, according to Damodaran data [30], at the level of 8.52% (average for 2001–2015) (however, it is not known what sources we are talking about);

- −

- Saługa and Kamiński [31] reported, for the years 2013–2017, the cost of equity—nominal, after-tax, of the companies separated from the Damodaran Coal & Related Energy group at 9.7%, which after taking into account, the inflation is 9% in real terms;

- −

- Kozieł, Pawłowski, and Kustra [32], on the other hand, gave the cost of equity (2016–2017) of 5.52% for Tauron Polska Energia (TPE) (hard coal) and 5.33% for PGE (Polska Grupa Energetyczna) (lignite)—probably in nominal values; it is worth mentioning that both these companies have geological-mining assets in their portfolios, in addition to power generation assets;

- −

- Bachner, Mayer, and Steininger [33] estimated the cost of capital for investments in coal-fired units in Eastern Europe at just over 10% (approximately 10.3%), in nominal terms.

As we can see, the costs of equity for coal projects, often combined with mining investments, are quite diverse. It should be noted that in the power generation industry, the concept of the hurdle rate is often used, which means that the minimum acceptable rate of return (MARR) is most often associated with the IRR indicator, and it should not be equated with the cost of equity.

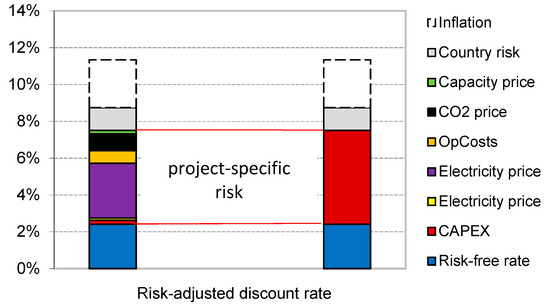

Analyzing the values mentioned above and based on own experience, resulting from economic analyses and conversations with managers of national energy companies, for the purposes of this article, it was assumed that in Polish conditions, a reasonable cost of equity capital while considering investments in coal blocks should be 7.5% (real, after-tax). The presented 7.5 percent rate includes a risk-free rate. The latter is the rate of return on zero-risk financial assets (State guarantee), which means a full return on the original capital plus accrued interest. The risk-free rate has been calculated based on the average yield of 10-year State Treasury bonds with the longest maturity, listed on the Treasury BondSpot Market from 2011–2020 [34,35,36]. Taking the average yield of 10-year bonds as a basis for forecasting the future has economic justification, and since the power generating plants are long-term investments, so there is a legitimate expectation that long-term periods remain in relationship with each other. The inflation for the a/m period has been taken from the Statistics Poland [37]. After actualizing the nominal values and averaging the results, a risk-free rate of 2.41% has been obtained.

Therefore, the specific risk within the RADR rate covers about 5.1%; the 7.5% RADR rate in question does not include the percentage of country risk that would be considered by foreign investors. Based on historical data (2011–2019) provided on Damodaran’s website [30,38], the average risk for Poland in the long-term can be estimated at 1.24%.

As said, the cost of equity or the risk-adjusted discount rate (real, after-tax) includes the following components:

- (1)

- risk-free rate

- (2)

- the rate related to the specific risk of the company/project

- (3)

- percentage of country risk

The nominal rate additionally includes an inflation element.

In the case of projects using coal combustion technology, the share related to specific risk includes such main risk factors like:

- (1)

- capital expenditures

- (2)

- power generation

- (3)

- electricity price

- (4)

- operating costs—mainly fuel (coal) costs

- (5)

- costs of CO2 emission allowances

- (6)

- an auction price in the capacity market

This raises the question—What is the percentage of these risk factors within the 5.1% set? As already mentioned, this is important for planning a project, making decisions about launching the investment, and, consequently, effective risk management at the strategic and operational stage.

In order to answer this question, the methodology used by Smith [39] has been adopted. The starting point is the concept that risk is the product of uncertainty and consequence:

Uncertainty means a lack of knowledge and can be reduced by obtaining more information [40]. In the statistical sense, uncertainty can be understood as a range of variability of a parameter. Naturally, if highly volatile parameters have a strong impact on the economics of a project, we can say that they are important risk factors. If, on the other hand, the impact is not large, or if the range of volatility is small, then the risk associated with these parameters will not be high.

Uncertainty (UnCrnty) can be expressed by the range of error or by the accuracy of the parameter estimate. Consequences (CnSqnce), on the other hand, can be presented as the effect of a variable on the effectiveness of the project, measured by the tangent of the angle of slope of the sensitivity curve in a classical spider chart. The sensitivity analysis includes an examination of the impact of individual uncertain variables on IRR changes. This choice is related to the fact that this indicator has a percentage form and can be referred directly to the cost of equity.

As the interaction of the individual risk factors is cumulative, all tangents of the slope angles of the sensitivity curves are taken as absolute values.

3. Discussion of Results

In order to achieve the set research objectives, a cash-flow sheet for a typical project carried out in Polish conditions has been prepared. The construction of a new 500 MW unit in an existing coal-fired power plant with a 22-year lifetime (including a 4-year investment cycle) has been assumed. Total initial capital expenditure has been estimated at PLN 2.3 billion (with a margin of ±15%), spent in, respectively, 0.32, 0.34, 0.23, and 0.11 portions. It has been assumed that the project will be financed entirely from its own resources. Power generation (in a total of 108,872.7 GWh) has been estimated with an accuracy of ±10%. It has been assumed that the planned unit will successfully participate in the capacity market, which will allow it to obtain revenues on this account, from the 5th year of its existence, in the amount of 224 thousand PLN/MW. The accuracy of this forecast has been estimated at ±20%. Wholesale electricity prices (avg 251.22 PLN/MWh) and the price of coal (avg 334.34 PLN/Mg) have been taken according to Pöyry’s forecasts [41], central scenario. The variability of these parameters has been estimated by averaging the gaps between the values of the high and low forecast scenarios, rounded to integers. The prices of CO2 emission allowances (avg 114.95 PLN/Mg) have been based on Polish Ministry of State Assets data [42], assuming the estimation accuracy of ±40%. All values have been expressed in fixed money.

In such defined base case conditions of the project, the value of NPV is at the level of PLN 856.86 million, while interesting for us, the IRR rate is 11.91% (this rate is higher than the assumed discount rate of 7.5%, therefore, together with the information that NPV > 0, this is an argument for making a decision on launching the investment).

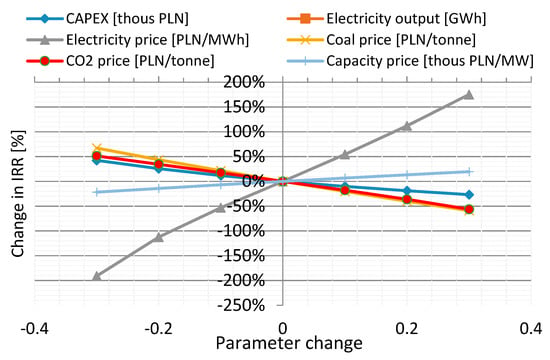

According to the ceteris paribus assumption, the sensitivity analysis has been carried out in relation to the base case by examining the influence of changes in individual key parameters on IRR, each time by ±10%, 20%, and 30%, and by plotting the results on a spider chart. The results (Figure 1) indicate that the project is most sensitive to electricity price changes, while the least sensitive to changes in investment outlays and capacity price. In order to compute for individual variables, the CnSqnce values of the tangents of the slope angles of the sensitivity curves to the abscissae have been calculated. By multiplying UnCrnty and CnSqnce values for each key variable, the risk value has been obtained, and then by calculating the relative risk, it has been obtained by the risk component in the RADR rate. The results of the analysis of risk factors within the cost of equity are presented in Table 1 and Figure 2.

Figure 1.

The sensitivity of the internal rate of return (IRR) to key coal-fired power project parameters in Poland.

Table 1.

Analysis of risk components within a risk-adjusted discount rate of coal-fired power projects in Polish conditions.

Figure 2.

Key risk factors portions of the equity rate of coal-fired power projects under Polish conditions.

The obtained results indicate that, with the adopted assumptions, the highest share in the specific risk of the real risk-adjusted discount rate, occurring in the conditions of evaluation of investments in coal-fired power units, has the electricity price almost 3%, followed by the price of CO2 emission allowances, which is about 0.9%, and operational cost (in which coal costs are the most significant) is about 0.7%. The impact of other risk factors is small. The risk factors are capital expenditure, power generation volume, and capacity price, and together they account for approximately 0.5% of the risk within the cost of equity.

Regarding the obtained results, an attempt has been made to analyze the scope of the discount rate at the operational stage of the power plant operation. It has been assumed that at this stage, the risk of the capacity price and investment outlays would be resolved. At the same time, the accuracy of the estimation of UnCrntly operating costs decrease to ±10%, and the discount rate will then decrease to the level of 6.7%. Consequently, the shares of production and electricity factors, as well as CO2 prices, will not change, while the share of the operating cost factor in the rate will drop to 0.3%. Innovative solutions in the power industry concern both the development and introduction of new technologies and the application of an appropriate organization. Changes also occur very dynamically in the search for new concepts of operation and management. Therefore, making the right decision should be preceded by:

- −

- formulating a long-term goal to be achieved through investment

- −

- determining the options of possible solutions

- −

- calculation of investment outlays and future cash-flows from investments

Obtained results provide essential information for decision-makers in the management of coal technology projects. The most significant attention must be paid to tracking electricity prices and responding appropriately to its changes. A second concern must be related to cost control, in particular, concerning the risk of changes in CO2 emission allowance prices. It should be borne in mind that over time, the level of the RADR applied for current purposes will decrease, as the risks related to the capital expenditure and capacity price will be solved, and the risk associated with operating costs will decrease significantly.

4. Summary and Final Conclusions

For both investment decision-making and subsequent project management, the issue arose in this paper for choosing a risk-adjusted rate and estimating its components are essential. The cost of equity is the only element considering risk (understood in this paper as the product of uncertainty and consequences) in the analysis of discounted cash-flows, which is the most frequently used methodology for assessing the effectiveness of projects.

In the process of economic assessment of investment projects, the key issue, which is the choice of the discount rate, is usually resolved using the equity valuation model. This model, despite many critical opinions, forms the basis for determining the cost of equity, also by large mining companies. This is mainly because of its relative simplicity and transparency and because, until today, no better analytical method has been developed. Because of the above, in practice, to assess raw material projects, modifications to the discount rate are often used. The companies start from the cost of estimated capital and then adjust this rate considering the state of progress and category of the project. This process involves each time:

- −

- risk factor identification

- −

- scale estimation development

- −

- assessing the risk portion

- −

- calculation of the importance of individual risks

- −

- determining the risk value

The above process takes place with significant involvement of the subjective factor. However, since project evaluations are usually carried out by analysts and managers with many years of practice and experience, their estimates can be considered authoritative.

This paper describes the methodology of discount rates selection and then, focusing on the cost of equity, determines a priori its level at the stage of making investment decisions and then the individual components analytically.

The projects mentioned above were carried out for investments in coal-fired units in the power generation sector, being aware of the twilight of this technology. However, it has been recognized that coal-fired power plants using well-known and mastered technology can be an excellent point for comparing new and renewable investments. However, there are many more factors influencing the increase in the cost of equity. The observed trends to the rise in the cost of equity of enterprises in the markets should be the direction of further research in this area. Therefore, the obtained and exciting results indicating that the most critical risk factors in coal projects are the price of electricity and CO2. In contrast, the least important is the volume of power production; the direction of further work may be considered to conduct similar analyses for other power generation technologies. It also causes some crucial implications for national energy policy because of the fact that resolving the problem of CO2 is very difficult. To come out of the issues related to CO2 emission, the country must redefine and update its energy strategy and policy. The study in this area may be of great utilitarian importance. A wider knowledge of the structure of the cost of equity capital will allow for proper undertaking and provide more rational management of investment projects, as well as pave the way to a better understanding of the assessment of cash flows and effective risk control.

Author Contributions

Conceptualization, P.W.S.; data curation, P.W.S.; formal analysis, P.W.S., K.S.-W. and M.C.; investigation, P.W.S.; methodology, P.W.S.; project administration, P.W.S. and K.S.-W.; resources, P.W.S. and R.M.; writing—original draft, P.W.S., K.S.-W., M.C. and R.M.; writing—review and editing, P.W.S. and M.C.; data curation, P.W.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Conflicts of Interest

The authors declare no conflict of interest.

References

- World Bank. Guidelines for Economic Analysis of Power Sector Projects; Technical Notes; World Bank: Washington, DC, USA, 2015; Volume 2, p. 99506, Public Disclosure Authorized; Available online: http://documents1.worldbank.org/curated/en/267971468000014869/pdf/99506-WP-v2-PUBLIC-Box393204B-Guidelines-Economic-Analysis-Power-Projects-Volume-2-Final.pdf (accessed on 28 March 2020).

- Dranka, G.G.; Cunha, J.; de Lima, J.D.; Fereira, P. Economic Evaluation Methodologies for Renewable Energy Projects. Research article. AIMS Energy 2020, 8, 339–364. [Google Scholar] [CrossRef]

- Hermelink, A.H.; de Jager, D. Evaluating Our Future—The Crucial Role of Discount Rates in European Commission Energy System Modelling; European Council for an Energy Efficient Economy & Ecofys: Stockholm, Sweden, 2015; Available online: https://www.eceee.org/static/media/uploads/site-2/policy-areas/discount-rates/evaluating-our-future-report.pdf (accessed on 6 April 2020).

- Blinski, P. Do Analyst Disclose Cash Flow Forecast with Earnings Estimates when Earnings Quality is Low? J. Bus. Financ. Account. 2014, 41, 401–434. [Google Scholar] [CrossRef]

- Andrén, N.; Jankensgård, H. Disappearing investment-cash flow sensitivities: Earnings have not become a worse proxy for cash flow. J. Bus. Financ. Account. 2020, 47, 760–785. [Google Scholar] [CrossRef]

- Daroń, M.; Górska, M. Challenges and Problems of Transport. Management in the Mining Sector. In 33rd IBIMA Conference proceedings: Education Excellence and Innovation Management through Vision 2020; Soliman Khalid, S., Ed.; International Business Information Management (IBIMA): Granada, Spain, 2019; pp. 2357–2372. [Google Scholar]

- Aliu, F.; Pavelkova, D.; Dehning, B. Portfolio risk-return analysis: The case of the automotive industry in the Czech Republic. J. Int. Stud. 2017, 10, 72–83. [Google Scholar] [CrossRef] [PubMed]

- Pietrzak, M.B.; Fałdziński, M.; Balcerzak, A.P.; Meluzín, T.; Zinecker, M. Short-term Shocks and Long-term Relationships of Interdependencies Among Central European Capital Markets. Econ. Sociol. 2017, 10, 61–77. [Google Scholar] [CrossRef] [PubMed]

- Jonek-Kowalska, I. Transformation of energy balances with dominant coal consumption in European economies and Turkey in the years 1990–2017. Oeconomia Copernic. 2019, 10, 627–647. [Google Scholar] [CrossRef]

- Jonek-Kowalska, I. Coal mining in Central-East Europe in perspective of industrial risk. Oeconomia Copernicana. 2017, 8, 131–143. [Google Scholar] [CrossRef]

- Amadi, C.W. Estimation of the Cost of Equity: A Chance of a Loss Approach; “Business Quest”; Richards College of Business; University of West Georgia: Carrollton, GA, USA, 2010. [Google Scholar]

- Mohutsiwa, M. Estimation of Capital Costs for Establishing Coal Mines in South Africa; a Research Report; Faculty of Engineering and the Built Environment, University of the Witwatersrand: Johannesburg, South Africa, 2015; Available online: http://wiredspace.wits.ac.za/jspui/bitstream/10539/18378/2/Moshe_Mohutsiwa_Estimation%20of%20Capital%20Costs%20for%20Establishing%20Coal%20Mines%20in%20South%20Africa.pdf (accessed on 26 July 2020).

- Oláh, J.; Kovács, S.; Virglerova, Z.; Lakner, Z.; Popp, J. Analysis and Comparison of Economic and Financial Risk Sources in SMEs of the Visegrad Group and Serbia. Sustainability 2019, 11, 1853. [Google Scholar] [CrossRef]

- Oláh, J.; Virglerova, Z.; Klieštiková, J.; Popp, J.; Kovács, S. The Assessment of Non-Financial Risk Sources of SMES in the V4 Countries and Serbia. Sustainability 2019, 11, 4806. [Google Scholar] [CrossRef]

- Rabe, M.; Streimikiene, D.; Bilan, Y. EU carbon emissions market development and its impact on penetration of renewables in the power sector. Energies 2019, 12, 2961. [Google Scholar] [CrossRef]

- Michalski, G. Relation Between Cash Levels and Debt in Small and Medium Wood and Furniture Industry Enterprises with Full Operating Cycle. Procedia Econ. Financ. 2015, 34, 469–476. [Google Scholar] [CrossRef]

- Hussain, H.I.; Slusarczyk, B.; Kamarudin, F.; Thaker, H.M.T.; Szczepańska-Woszczyna, K. An investigation of an adaptive neuro-fuzzy inference system to predict the relationship among energy intensity, globalization, and financial development in major ASEAN economies. Energies 2020, 13, 850. [Google Scholar] [CrossRef]

- Brealey, R.A.; Myers, S.C.; Allen, F. Principles of Corporate Finance; McGraw-Hill/Irwin: New York, NY, USA, 2008. [Google Scholar]

- Kolupaieva, I.; Pustovhar, S.; Suprun, O.; Shevchenko, O. Diagnostics of systemic risk impact on the enterprise capacity for financial risk neutralization: The case of Ukrainian metallurgical enterprises. Oeconomia Copernic. 2019, 10, 471–491. [Google Scholar] [CrossRef]

- Gollier, C.; Koundouri, P.; Pantelidis, T. Declining Discount Rates: Economic Justifications and Implications for Long-Run Policy. Econ. Policy 2008, 23, 757–795. [Google Scholar] [CrossRef]

- Lind, R.C. A Primer on the Major Issues Relating to the Discount Rate for Evaluating National Energy Options, Resources for the Future; Lind, R.C., Ed.; Discounting for Time and Risk in Energy Policy: Washington, DC, USA, 1982; pp. 21–94. [Google Scholar]

- García-Gusano, D.; Kari, E.; Lind, A.; Kirkengen, M. The Role of the Discount Rates in Energy Systems Optimisation Models. Renew. Sustain. Energy Rev. 2016, 59, 56–72. [Google Scholar] [CrossRef]

- Śliwiński, P.; Łobza, M. The impact of global risk on the performance of socially responsible and conventional stock indices. Equilibrium. Q. J. Econ. Econ. Policy 2017, 12, 657–674. [Google Scholar] [CrossRef]

- OECD. Projected Costs of Generation Electricity–2010, Edition, OECD Publications. 2010. Available online: https://www.oecd-nea.org/ndd/pubs/2010/6819-projected-costs.pdf (accessed on 28 August 2020).

- WEC. World Energy Perspective: Cost of Energy Technologies; Project Partner: Bloomberg New Energy Finance; World Energy Council (WEC): London, UK, 2013; p. 48. Available online: https://www.worldenergy.org/assets/downloads/WEC_J1143_CostofTECHNOLOGIES_021013_WEB_Final.pdf (accessed on 5 March 2020).

- STB, Surface Transportation Board. Draft Environmental Impact Statement for the Tongue River Railroad. 2015, Appendix C, Coal Production and Markets, April 2015. Available online: https://www.stb.gov/decisions/readingroom.nsf/UNID/E7DE39D1F6FD4A9A85257E2A0049104D/$file/AppC_CoalProduction.pdf (accessed on 17 February 2020).

- NERA Economic Consulting. Electricity Generation Costs and Hurdle Rates–Lot 1: Hurdle Rates Update for Generation Technologies, Prepared for the Department of Energy and Climate Change (DECC). 2015. Available online: https://www.nera.com/content/dam/nera/publications/2016/,NERA_Hurdle_Rates_for_Electricity_Generation_Technologies.pdf (accessed on 8 March 2020).

- Nalbandian-Sugden, H. Operating Ratio and Cost of Coal Power Generation; IEA Clean Coal Centre: London, UK, 2016; p. 107. Available online: https://www.usea.org/sites/default/files/ (accessed on 19 February 2020).

- Zamasz, K. Discount Rates for the Evaluation of Energy Projects–Rules and Problems. Sci. J. Sil. Univ. Technol. Ser. Organ. Manag. (Zesz. Nauk. Politech. ŚląskiejSer. Organ. I Zarządzanie) 2017, 101, 571–584. [Google Scholar]

- Damodaran Online: Data. Costs of Capital by Industry (Europe). Website of Aswath Damodaran. Available online: http://pages.stern.nyu.edu/~adamodar (accessed on 15 March 2020).

- Saługa, P.W.; Kamiński, J. The Cost of Equity in the Energy Sector. Polityka Energetyczna-Energy Policy J. 2018, 21, 81–96. [Google Scholar] [CrossRef]

- Kozieł, D.; Pawłowski, S.; Kustra, A. Cost of Equity Estimation in Fuel and Energy Sector Companies Based on CAPM. Scientific-Research Cooperation between Vietnam and Poland POL-VIET 2017. In E3S Web of Conferences; EDP Sciences: Les Ulis, France, 2018; Volume 35, p. 1008. [Google Scholar] [CrossRef]

- Bachner, G.; Mayer, J.; Steininger, K.W. Costs or Benefits? Assessing the Economy-Wide Effects of the Electricity Sector’s Low Carbon Transition–The Role of Capital Costs, Divergent Risk Perceptions and Premiums. Energy Strategy Rev. 2019, 26, 100373. [Google Scholar] [CrossRef]

- Škare, M.; Tomić, D.; Stjepanović, S. Energy Consumption and Green GDP in Europe: A Panel Cointegration Analysis 2008–2016. Acta Montan. Slovaca 2020, 25, 46–56. [Google Scholar] [CrossRef]

- Energy Regulatory Office (URE). Methodology for Determining the Rate of Return on Capital Engaged, for Power System Operators for 2016–2020. 2015. Available online: www.ure.gov.pl (accessed on 16 March 2020).

- Energy Regulatory Office (URE). Risk-Free Rate for the Purpose of Determining the Cost of Capital Engaged, Used for the Calculation of Infrastructure Tariffs of Gas and District Heating Companies as well as Power System Operators, CIRE.pl. 2020. Available online: https://www.cire.pl/item,144479,5,0,0,0,0,0,stopa-wolna-od-ryzyka-.html (accessed on 16 March 2020).

- Statistics Poland (GUS). Annual Indices of Consumer Prices of Goods and Services Since 1950. 2020. Available online: https://stat.gov.pl/obszary-tematyczne/ceny-handel/wskazniki-cen/wskazniki-cen-towarow-i-uslug-konsumpcyjnych-pot-inflacja-/roczne-wskazniki-cen-towarow-i-uslug-konsumpcyjnych/ (accessed on 15 March 2020).

- Oxford University; The Oxford Institute for Energy Studies, Energy Transition. Uncertainty, and the Implications of Change in the Risk Preferences of Fossil Fuels Investors; University of Oxford: Oxford, UK, 2019; p. 13. Available online: https://www.oxfordenergy.org/wpcms/wp-content/uploads/2019/01/Energy-Transition-Uncertainty-and-the-Implications-of-Change-in-the-Risk-Preferences-of-Fossil-Fuel-Investors-Insight-45.pdf (accessed on 18 February 2019).

- Smith, L.D. Discount Rates and Risk Assessment in Mineral Project Evaluations. Can. Inst. Min. Metall. Bull. 1995, 88, 34–43. [Google Scholar]

- Hudáková, M.; Dvorský, J. Assessing the risks and their sources in dependence on the rate of implementing the risk management process in the SMEs. Equilib. Q. J. Econ. Econ. Policy 2018, 13, 543–567. [Google Scholar] [CrossRef]

- Pöyry. Independent Market. Report for Poland (Q3 2019 Update). Available online: https://www.poyry.com/sites/default/files/pimrflyer_poland19_v100.pdf (accessed on 18 February 2019).

- Ministry of State Assets (MAP). Updated Draft Energy Policy of Poland Until 2040–Conclusions from Prognostic Analyses for the Fuel and Energy Sector. Available online: https://www.gov.pl/web/aktywa-panstwowe/zaktualizowany-projekt-polityki-energetyczna-polski-do-2040-r (accessed on 15 March 2019).

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).