Abstract

Solid biofuels have the potential of making a major contribution to achieving the objectives of the Paris Climate Agreement if they are used more extensively for covering the heat demand of the industry and the trade, commerce, and service (TCS) sector. To unlock this potential, a holistic analysis of the supply chain from producer to end customer was performed, involving consultants, planners, and financial institutions. The focus is on the deployment of larger biomass heating boilers (with heat loads spanning several 100 kW to several MW). The study identifies the most important barriers for expanding the use of solid biofuels for heat in the German TCS sector as well as in the industry sector. Nine sets of measures were identified for overcoming the most critical barriers, among others, by drawing on best practice approaches and solutions from other German and European contexts. Based on these measures, political recommendations were derived to shape the regulatory framework conditions accordingly. These recommendations can in turn offer a stimulus for other countries to foster a more efficient and climate-effective use of biomass.

1. Introduction

Heating and cooling is the dominating energy sector in final energy consumption, in the European Union (EU) with almost 50% [1], and in Germany with over 50% as well [2]. The heat demand of industry, households, and the trade, commerce, and service (TCS) sector is used at different temperature levels (process heat and space heating). For Germany, around 57% of the heat is used by industry and the TCS sector. Households use the remaining 43% of heat.

Thus, the heat sector plays a crucial role in achieving the climate goals, signed on to the Paris Climate Agreement [3]. An analysis of climate change scenarios reveals that between 2008 and 2030 the heat sector could, and must, contribute to cutting CO2 emissions (by 62%) in a similar fashion to the electricity sector (by 57%) [4]. According to internal calculations by the German Federal Ministry for the Environment, this will only be possible if greater efforts are made to create appropriate framework conditions and incentives for further emission reductions [5,6].

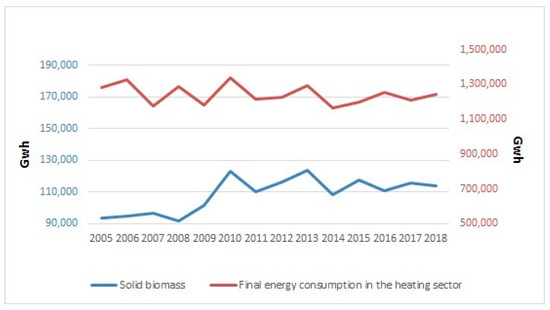

The energy supplied for heating and cooling is still dominated by fossil fuels in Germany. In 2019, the share of renewable energies in the gross final consumption of energy for heating and cooling (excluding the biogenic content of municipal waste) was 14.5% [7]. For comparison: in the EU, the share of renewable energy of the gross final consumption in the heating sector is slightly higher at 21.1% [8]. Solid biomass, with a share of 9.6% in 2019 of the final energy consumption in the heating sector, is the most important renewable fuel in Germany [7] (in the EU, average is much higher at 16.9% (2019) [9]. After a strong increase in the use of solid biofuels for heating purposes between 2008 and 2010, subsequent years saw no growth tendency (see Figure 1) [10].

Figure 1.

Final energy consumption for heating purposes in Germany, total and covered by solid biomass (data from [10,11]).

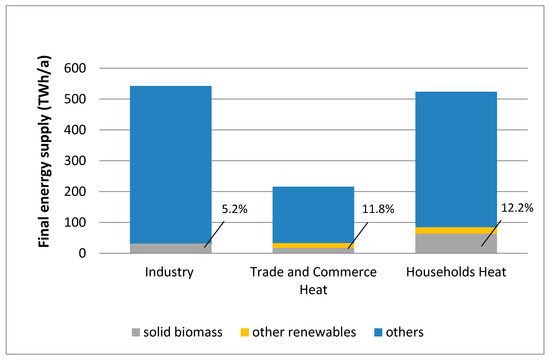

Most solid biofuels are used in the domestic sector for space heating and hot water supply. In contrast, significantly less solid biomass fuels are applied in the industrial sector to provide process heat (see Figure 2) [11,12,13].

Figure 2.

Contribution of different energy sources to meet sectors’ final heat demand in Germany (based on [11,12,13]).

A review of 155 German energy scenarios [14], as well as a comprehensive study of the German industry association (BDI) for future developments in the energy system, came to the conclusion that, for reasons of cost-effectiveness and in view of achieving the German climate protection targets, the use of solid biofuels has to drastically shift in the future, away from the residential sector. Instead, it should predominantly be used in the industrial sector as replacement of fossil fuels in industrial low- and medium-temperature [15] or in the high heat [12] generation. The recommendations refer not only to Germany, but also to industrialized countries in general [12].

Different studies on biomass potentials and scenarios have indicated that there are still significant untapped biomass potentials in the field of solid biofuels in Germany, which could be mobilized without risking to endanger sustainability principles [16,17,18]. At the European level, however, the picture is different. Despite increasing solid biofuel production in the EU28, supply and demand are already almost balanced. To maintain this situation in a sustainable manner, it is recommended to establish a monitoring program [19]. These limited opportunities for expansion of solid biofuel production at EU level reinforce the need for using available resources as efficiently as possible.

These scientific findings have already been incorporated into policy planning in Germany. The German Integrated National Energy and Climate Plan (NECP) is an important roadmap for the years 2021–2030 to achieve the EU’s renewable energy and energy efficiency targets for 2030. The projections up to 2030 foresee a stable to increasing role of biomass in district heating, decentralized heating, and process heat generation [20]. The Climate Protection Plan 2050 [21] on the other hand, reflects the long-term plans of the German government. Accordingly, biomass is to be used in parts of industry and will also continue to play an important role in the heating sector as a whole. Due to limited resources, however, cascading biomass uses will be increasingly necessary in the future.

To tap the potentials for bioheat in the most promising market segments, the analysis of existing barriers and the development of incentives was performed during the project Bioenergy4Business, notably focusing on the deployment of larger biomass heating boilers (with heat loads spanning several 100 kW to several MW).

While the publication mentioned [12,15] aiming at a long-term market shift of biomass fuels in order to achieve the climate goals of 2050, the intention of this approach is a short term solution for an efficient use of the currently available biomass potentials for greenhouse gas (GHG) reduction and thus also include the TSC sector.

As a current study on the status and future perspectives for energy production from solid biomass in the European industry, [18] shows solid biofuels are—similar to Germany—mainly used in the residential sector in the majority of European countries, particularly in Eastern and Southern Europe. Another study on the development of heat supply and consumption in the EU28 [22] highlights that biomass as a fuel for heat supply is the second largest source of emissions in the residential sector. The GHG emissions from this source more than doubled between 1990 and 2015; thus, preventing a significant reduction of emissions in the residential sector. This is due to untapped decarbonization opportunities, such as heat pumps and heating networks. Thus, a shift in the use of solid biofuels from the residential to the industry and TSC sector leads to a more efficient biomass use with lower CO2 emissions.

The aims of this study are to identify the obstacles that are slowing down this necessary development and to point out approaches for their removal. The focus here is on the market, technical, and regulatory framework conditions in Germany. In view of identifying enabling concepts, promising examples from other EU countries, participating in the EU project (Bioenergy4Business) were also taken into account. In turn, the approaches outlined here for the German context can and should also provide other EU countries with the basis for examining their specific situation with regard to solid biomass use practices, so that they can take further steps to reduce CO2 emissions and achieve their own climate protection goals.

2. Materials and Methods

2.1. General Approach

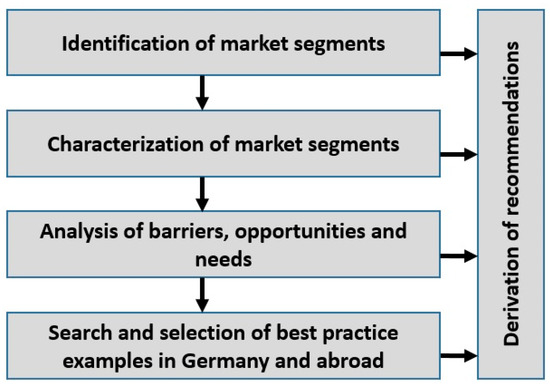

In order to tap the potentials for bioenergy in the most promising market segments in the industry and TCS sector, a stepwise approach was developed (see Figure 3) that identifies the most important hurdles for the future deployment of solid biofuel, and helps to develop policy recommendation for an enabling regulatory and market environment.

Figure 3.

Methodical approach.

First, promising market segments were identified where a switch from a fossil fuel-based to biomass-based heat supply is most likely to be achieved (see Section 2.2). Then, these identified markets were analyzed and characterized with respect to assess the existing heat requirements (see Section 2.3). In addition, framework legislation and current support and financing schemes were examined in view of removing existing barriers to a potential fuel switch. The thus identified barriers, opportunities, and needs of promising market segments were further consolidated through interviews with stakeholders in the respective market segments and their upstream suppliers (see Section 2.4). In a next step, examples of good practices within the promising market segments were selected to serve as blueprints for solutions to overcome existing barriers. Similarly, the enabling framework conditions and best practice examples identified in the other partner countries were examined for their transferability to Germany (see Section 2.5). Finally, the results were consolidated to provide recommendations for national and European policymakers in order to support the development of these markets (see Section 2.6).

2.2. Identification of Market Segments with Unexploited Potential and Relevant Key Factors for Implementing Bioheat Concepts

In order to detect the most promising market segments in industry and TCS sectors, a literature analysis was performed and interviews were conducted with experts who have a good understanding of both the current sales market and future market opportunities for biomass boilers. The interviewees included:

- three major German biomass plant manufacturers;

- one stakeholder in contracting and energy services who has extensive experience with the implementation of biomass-based projects;

- an engineering office that has already implemented several biomass heating plants in the industry, and TCS commerce, trade and services sector, and which offers neutral and independent planning services (see also Appendix A, Table A1).

The methodology of a guided interview via phone was chosen for all surveys since it sets a thematic priority that allows for a comparison of different experts. At the same time, the guided interview also contains narrative elements, in other words the interviewees are able to go into more detail about a specific situation based on their practical experience. This enables additional information to be gathered and new aspects to be included. Thus, during the telephone call, the subject areas can be processed in a structured manner. At the same time, relevant yet unexpected supplementary information can be added by the interview partner [23].

The analysis included the following consecutive work steps:

- paraphrasing: a factual reiteration of the content of the interview;

- thematic structure: divided into individual thematic sections;

- thematic comparison: comparison of the text passages of the various expert interviews, formation of thematic categories;

- comprehensive presentation of the expert assessment.

The interviewees were asked to name the most promising market segments in the district heating sector and for “on-site” boiler applications. Then, they had to state which criteria they used in choosing these markets segments. The pre-selection and classification of factors was done based on existing approaches, mainly existing studies and documents [24,25]. A summary of the interviews revealed the most promising market segments, which served as basis for the further investigations detailed below.

2.3. Characterization of Market Segments

The market segments were characterized in order to assess the existing heat requirements in the respective application fields. This included estimating the annual final energy consumption, especially for heating purposes. The data to assess the heat requirements of the promising market segments were collected by surveying existing statistics and reports that contain energy consumption data. The characteristics of heat demand (space heating, water heating, process heat, low/high temperature) were also defined.

In cases of insufficient data available to calculate the final energy consumption in the heating sector, such lack was compensated by own data from Deutsche Biomasseforschungszentrum gGmbh (DBFZ), which has previously developed a method for determining the heat demand in the TCS sectors [26].

2.4. Analysis of Barriers, Opportunities, and Needs

Various business models and the general regulatory, institutional, legal, and administrative conditions regarding bioenergy heating in the specific business sectors were investigated with respect to the uptake of solid biomass heating. The legal and supporting framework conditions, pertaining to the planning, implementation, and operation of biomass heating plants, which affect these market segments, were also considered. This included pricing policies, the cost of licensing procedures, environmental and emission standards, certification programs for renewable energy systems (RES) installations, and building regulations related to RES heating. Moreover, institutions and authorities involved in the approval of processes or other interested representatives on the topic of biomass and bioenergy were identified and described. Even relevant training programs e.g., for installers were included [27].

Relevant stakeholders in the market segments were also identified, and biomass suppliers, community interest organizations, and policy stakeholders were consulted in order to ascertain the existing barriers in the market segments and supply chains, as well as to increase cooperation between different actors. Finally, in the course of a literature analysis, it was examined whether further complementary information on barriers and options to overcome these could be found.

2.4.1. Interview of Financing Institutions

In order to obtain a clear picture of the banks’ practical experience and the resulting requirements and procedures for granting credit, four banks were selected, which have trained staff to analyze and assess project plans of biomass heating systems (see Appendix A, Table A1).

2.4.2. Interview with Relevant Stakeholders in the Promising Market Segments and their Upstream Supply Chain

Drawing upon the findings of the previous steps, the relevant stakeholders on the supply and demand side, as well as relevant sector representatives and their communication channels were identified in order to determine supporting and harming factors for using more solid biofuels in the business sector. These were stakeholders in the most promising commercial market segments: district heating operators, developers and planners, biomass suppliers and users, political decision-makers, as well as agricultural, forestry and community interest organizations that play a key role as multipliers of information (see Appendix A, Table A2). By including all relevant stakeholders, the entire supply chain could be analyzed.

The interviews allow for a proper understanding of the relevant target groups, and their positions with regard to bioenergy heating. The results of the interviews were analyzed in light of existing barriers, opportunities, and needs of the respective market segments, broken down into the supply and demand side as well as by policy stakeholder.

2.4.3. Classification of Barriers and Solutions

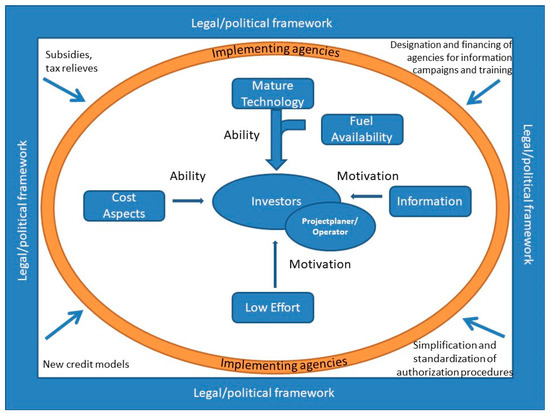

Investors and construction project planners play a key role in the further expansion of solid biofuels. Their decision for a biomass heating system depends on a number of enabling and motivating conditions. The basic requirement is a market-ready technology. This is supplemented by enabling framework conditions, which can be divided into three elements (Figure 4, inner circle):

Figure 4.

The system supporting the implementation of biomass for heat technologies (source: own illustration, based on [28] modified from [29].

- cost aspects: competitiveness in comparison with fossil (and other renewable) plant concepts;

- information: e.g., awareness of the target groups on the possible economic advantages and climate protection contribution of biomass heating systems; and

- low effort: the least possible expenditure of time and effort for planning, authorization, and construction of the plants.

The obstacles and solutions identified in the course of the interviews and within additional literature studies were assigned to these three elements.

2.5. Search and Selection of Best Practice Examples in Germany and Abroad

Operators of economically successful solid biomass heating plants in the relevant target markets were selected and interviewed to identify the difficulties they have experienced, as well as their viable solutions and factors for success. Emphasis was put on understanding the solutions reached to overcome difficulties/barriers encountered during project implementation and plant operation (see also Appendix A, Table A2).

Furthermore, the results of another 10 EU countries participating in the EU project Bioenergy4Business were evaluated, regarding their transferability to the German context and their ability to provide solutions for fostering the use of solid biomass in the heat sector.

2.6. Derivation of Recommendations

A comprehensive picture of the barriers and necessary actions was obtained based on previous steps. This allowed to identify key players that are crucial for removing the barriers and to draw conclusions and recommendations for action to be taken by decision-makers in the policy and market sphere by providing the necessary framework and setting financial incentives. Finally, these recommendations for action were discussed with a German expert board of the Fachverband Holzenergie (Association of German wood energy industry) in order to verify the results.

3. Results

3.1. Selection and Characterization of Promising Market Segments

The demands on biomass heating systems regarding efficiency and emission behavior are constantly increasing, notably for plants in the power segment of 100 kW up to several MW. Compliance with the increasingly stringent emission limit values is only possible by using high-quality fuel assortments and/or cost-intensive filters. In view of the higher investment costs of biomass heating plants compared to plant concepts operated with fossil fuels, only comparatively favorable fuel costs can compensate for this. A high annual heat quantity requirement is, therefore, an important factor in shortening the payback period and allowing a competitive use.

The interviewees in Germany stated that hospitals, the hospitality sector, industries requiring process heat, indoor and outdoor swimming pools, as well as nursing homes are promising market segments, i.e., offering yet untapped potentials for biomass use. Table 1 shows the estimated heat demand and the respective number of properties in the respective target groups. The interviewees stated in the surveys (conducted in the Bioenergy4Business project) that the wood and woodworking industries were suitable. However, due to the direct availability of an inexpensive fuel, these industries already cover a high proportion of their heat requirements on the basis of solid biomass and were, therefore, not included further in the detailed analysis.

Table 1.

Heat demand for the most promising branches, projections for 2016/2019 in TWh/year. Detailed information about the results of the in-depth market analysis and best practice models can be found in [30,31].

Recent publications show a nuanced picture of the promising industrial sectors with regard to the use of solid biofuels. Based on findings of a review performed for 155 German energy system scenarios [12], the identification of future promising sectors was focused on those with a constant or growing demand for high temperature, including steam supply at 200–500/600 °C and direct firing with temperature above 500/600 °C. With regard to the increasing demand for wood in the course of a growing bio-economy, and a preferably climate-efficient use of wood biomass, the holistic study [12] comes—among others—to the following conclusions: the wood and wood product sectors, as well as the pulp and paper or food sector, have only low heat requirements in the temperature range >200 °C. The solid biofuels used so far to cover the heat demand in the low temperature range could be replaced by other renewable energies, so that the biomass could be released to cover the high temperature demand of other sectors.

The subsector “chemical and petrochemical” has been identified as one promising future market with regard to an increasing use of biomass (and a corresponding amount of residues) in the course of a developing bio-economy. In the short term, however, the subsector “non-metal minerals” (cement, clinker, glass, and ceramics) promise the greatest market potential.

3.2. Barriers Identified in the Promising Markets

The primary barriers in Germany, identified in the interviews and workshop are assigned to three categories: cost aspects, deficits in knowledge, and workload (see Section 2.4). For each of the obstacles, the solutions named by the participants were listed (Table 2, Table 3 and Table 4).

Table 2.

Economic hurdles and approaches to further expand of bioheat concepts (partly cited and revised from [42]).

Table 3.

Deficits in knowledge and approaches to further expand of bioheat concepts (partly cited and revised from [42]).

Table 4.

Deficits in planning and approval processes and approaches to further expand of bioheat concepts (based on [42], including some modification).

3.3. Nine Sets of Measures for Improvement

Finally, nine sets of recommendations for political action were derived from the suggestions made by the stakeholders. Wherever possible, reference was made to best practice examples from other EU countries and to institutions in Germany that could a play a decisive role in implementing and/or monitoring the proposed measures.

Good examples found within Germany or in the other EU countries participating in the Bioenergy4Business project were directly included in the nine sets of measures below Section 3.3.1. Improving competitiveness of biomass heating plants.

Solid biomass heating plants can compete with oil-fired boilers, but struggle against natural gas. The construction of new bioheat facilities and fuel switches primarily occurred in the years when the price for fossil fuels was high. When heating oil prices crashed in October 2014, it became increasingly more difficult to absorb the financial disadvantages through public funding. For this reason, interest in switching fuel sources decreased. It is often argued that prices for coal, oil, and gas are low because they do not include the cost of environmental damage and their CO2 load [35]. To overcome this obstacle, fair pricing for fossil CO2 emissions has to be introduced, which could relieve pressure on citizens and the economy by means of an intelligent allocation of income. To avoid competitive disadvantages for individual countries, however, the G20 countries (international forum for the governments and central bank governors from 19 countries and the EU) would have to agree on a minimum price for CO2. The Mercator Research Institute on Global Commons and Climate Change (MCC) and the Potsdam Institute for Climate Impact Research (PIK) have calculated how high the price of CO2 would have to be in order to achieve the climate targets to which Germany committed itself in the Paris Climate Convention. According to these calculations, the starting price in 2020 should be 50 euros per ton CO₂ in 2020 and rise to around 80 euros per ton by 2025. In 2030, the price should already be between 70 and 180 euros per ton CO₂. At the same time, the energy tax is to be abolished for the heating sector. In order to avoid a fragmentation of CO2 costs and a resulting uneven burden on companies in Europe, an integrated Europe-wide CO2 pricing system should be implemented as soon as possible [44].

Another approach to improve the competitiveness of solid biofuels is the introduction of tax relief, which takes greater account of external costs for environmental impacts. A similar approach has already been implemented for the biomethane in the transport sector, because of its lower CO2 and NOx emissions [45,46]. Tax relief on solid biomass fuels provides plant operators with a cost-competitive fuel and makes the long-term benefits of the plants more likely.

Another obstacle is the granting of credits. Banks usually lack the necessary expertise to be able to carry out an evaluation of large-scale biomass heating plant projects. However, long payback periods and thus longer credit repayment periods generally increase the risk of default, whereas banks protect themselves against this risk by charging higher interest rates on loans. The higher interest costs compared to fossil plant concepts reduce the attractiveness of biomass heating plants for investors.

As liquidity and operational requirements are tied together, companies mostly accept only short amortization periods. Thus, even investments that are profitable under the aspects of life cycle costs are given too little consideration.

The German Engineering Association (VDMA) has already outlined what such a credit model would look like [43]: it proposes that investing companies, which invest in low-emission heating technologies, receive a loan for 100% of the investment volume as well as a prepayment on upcoming energy saving costs. The actual annual amounts saved are then used to repay the loan. The new credit model requires key performance indicators for energy-efficient investments, which could be set up by the VDMA in cooperation with plant manufactures as well as qualified energy consultants in order to assess efficiency investments. Lending above 100% of the loan amount exceeds conventional bank lending limits. Even collateralizing the loan with the energy cost savings is not possible, according to the Banking Act. Therefore, combining the 100% investment loan with a dedicated revolving fund is recommended. The 100% investment loan and a revolving fund from the federal government for the energy cost savings, requires state aid approval from the EU Commission, which only can be obtained with the support of the federal government.

3.3.1. Prioritization of Renewable Heat Supply at Different Policy Levels

The interviewed stakeholders wanted clearer political signals for the use of solid biofuels. Political advocacy could encourage potential investors who have been unsettled to date.

A first step could be to emphasize the importance of the use of solid fuels for energy in the Charter for Wood 2.0 Charter and to compile the contents separately as an information package. The Charter, promoted by the Federal Ministry of Food and Agriculture, sets the framework for action to strengthen climate protection by using wood from sustainable forestry, to increase resource efficiency and benefit, and to maintain and improve the competitiveness of the domestic forestry and timber industry.

At the municipal level, there are also opportunities for greater support of biomass combustion plants. Municipalities have a very important role in the planning and implementation of a climate-friendly heating infrastructure: they are responsible for spatial planning, have the relevant knowledge and data on the building stock, and are usually the holders of rights of way and owners of the infrastructure facilities. In addition, by providing climate-friendly heating for the municipal buildings, it can serve as a role model and win the support of citizens and companies for the issue.

Biomass heating systems can be used efficiently in heating networks that ensure continuous heat consumption. Further expansion of heating networks and early assessment of the suitability of biomass heating systems for a cost-effective and climate-friendly heat supply is, therefore, a key. For this purpose, the preparation of a detailed energy concept, e.g., in the form of an energy use plan is useful. An energy use plan is a strategic planning instrument that provides an overview of the current and future energy demand and energy supply situation in the municipality.

In Bavaria, energy usage plans are funded [47]. Even in the federal state of Baden-Württemberg, there is a development program for efficient heating grids. A competence center has also been established, which provides information and is an initial booster for new projects.

Federal states such as Bavaria and Lower Saxony offer additional working aids and guidelines for the development of municipal heat planning [48,49]. For the best possible integration of biomass heating systems into the municipal planning concept, however, further special working aids and/or training of planners are necessary.

At present, planners already have at their disposal a tool for an initial assessment of the profitability and climate contribution of biomass heating systems, provided by the Austrian Energy Agency [50]. In addition, from October 2020, an updated online tool for assessing the impact of renewable energies on regional value added will be made available by the Renewable Energy Agency [48].

Finally, the expansion of solid biomass plants (as well as other renewable energy plants) can also be promoted by banning fossil plant concepts. For example, the Danish government aims to have all of its heat supplied by renewable energies. Since 1 January 2016, oil-fired boilers may no longer be installed in existing buildings [47]. Moreover, the Dutch government regulates energy system transformation on the basis of the Dutch building regulations (bouwbesluit). This defines, that since 1 July 2018, no new buildings will be connected to the gas supply and these homes and buildings will be supplied with renewable energy sources or a connection to a district heating network [48].

In Germany, a ban on the new installation of oil heating systems is planned from 2026. Exceptional regulations are planned, however. For example, the installation of modern oil condensing boilers will continue to be permitted if they are combined with renewable energies such as solar thermal energy for domestic hot water or to support heating systems. The minimum share of renewable energies has not yet been determined [49].

3.3.2. Support for Introducing Clean Technologies to the Market

Another barrier to cost competitiveness is the tightening of emission limit values. To implement the legal requirements of the European “Medium Combustion Plants Directive” (MCPD) Germany’s federal government plans to re-launch the Technical Instructions on Air Quality Control “TA Luft”, which sets the emission limit values for biomass heating installations in the capacity range between 1 and 50 MW. This directive includes emission limit values for the biomass sector but does not differentiate between the various capacity classes, plant categories, and biomass fuels used. As a result, comparatively small biomass heating plants that use residual forest wood and have a rated thermal output of 1 MWth have to fulfill the same emission requirements as e.g., industrial waste wood power plants in the upper-performance category (50 MWth).

Based on this strict emission regulation, it is doubtful that municipalities will implement bioheat concepts in the future to supply residential and business premises. However, the tightened regulation not only prevents new plants but also affects existing biomass plants. The significant expenditures related to technology and construction remove the economic basis of existing biomass plants.

As a result, the Federal Bioenergy Association published a common statement in conjunction with other interest groups [45]. In that it point out that retrofitting required when the tightened emission limits come into force would pose major economic problems for many existing plants. In addition, individual requirements could not be implemented technically or without undesirable side effects (e.g., temporarily increased ammonia emissions). In summary, the Association therefore calls for a mission limit value an adjustment of the limit values to the current technological state of the art and pleads for appropriate investigations in order to create a valid basis for the definition of reduction targets.

The implementing agency could be the Federal Ministry for the Environment, Nature Conservation and Nuclear Safety (BMU) or the Federal Ministry of Economics and Technology (BMWI). In order to avoid an economic overload of the plant operators and to maintain the competitiveness of the plants, additional subsidies for the installation of the expensive filter system (e.g., via the Market Incentive Program) can also be expedient.

3.3.3. Establishment of Energy Performance Contracting and Leasing

The advantages of energy contracting agreements have so far been insufficiently exploited due to knowledge deficits among companies and public administrations. For this reason, standard procedures (self-build solutions) instead of contracting solutions are often still implemented by the municipalities for suitable properties and quarters [51]. The conclusion of energy-contracting agreements offers especially small and medium-sized enterprises (SMEs) the following benefits:

- they reduce the effort for planning and organizational implementation of energy efficiency measures;

- the technical and economic risk is transferred to the energy service company (ESCO);

- the heat consumers save the high investment costs and can use the liquid funds that remain free for their core business.

A special form is the energy saving contract. In this case, an energy service company carries out energy saving measures on behalf of the customer and in return receives performance-related remuneration from the contractual partner. Thus, the energy service company only benefits if the actual energy cost savings can be realized. The bundling and joint tendering of several objects results in work efficiency gains for the tendering party and the energy service company, which makes this constellation very interesting for ESCOs.

Finance contracting (leasing) can be another attractive concept for companies. For example, an hotelier has leased a biomass boiler, including the wood chip bunker, from a local machinery ring or biomass facility. The leasing rates are recognized in full as operating expenses at the time of payment and reduce the profit of the hotel owner, and thus, the tax burden of the lessee in the year of payment. In addition to the leasing contract, a long-term supply contract for the fuel is agreed between the lessee and the lessor, which ensures for both partners a long-term planning security.

Municipalities are often unable to tap existing energy efficiency potentials due to a lack of personnel, expertise, or insufficient budgetary resources. Innovative energy service companies can close this gap.

In principle, the tendering authority cannot describe the services of the contractors fully and clearly. The EU negotiated procedure with a preliminary competition (in the upper threshold area) or the direct award of contracts with a preliminary competition (in the lower threshold area) offers energy service companies the opportunity to propose and have their individual solution proposals evaluated. However, public authorities inviting tenders are often uncertain whether the prerequisites for a negotiated procedure or a direct award of contract, are met. This prevents the development of existing potential for contracting.

In addition to these gaps in knowledge, legal hurdles also hamper the implementation of contracting solutions. The expenditure (contracting rate) is credited to the local authority credit line and reduces it, although corresponding savings in energy costs counterbalance the expenditure in energy-saving contracting. As a rule, it is also not possible to use contracting for municipalities subject to budgetary supervision.

In order to better inform the relevant groups of actors at state and municipal level, such as the municipal treasurers (responsible for the financial affairs of municipalities), a working group mandated with the analysis and optimization of the contracting situation recommends a training offensive for these groups [51].

The focus of this training offensive should be on the presentation of contracting models, the effects on the municipal budget and the differences between contracting and self-build solutions for the municipality (advantages/risks).

Several guidance documents have already been developed to assist businesses and public administrations [52,53].

The visibility of these guides can be improved by dissemination and promotion through Chambers of Industry and Commerce, energy agencies, and the German association of cities and towns. The selection of exemplary consulting concepts as well as the facilitation of visits by interested target groups can be a further building block to increase the visibility and interest.

As part of the “Energy Performance Contracting Consultation” funding program, the Federal Office of Economics and Export Control supports municipalities as well as small and medium-sized enterprises (SMEs), which can apply for funding in 2018 for professional support in the planning and implementation of energy performance contracting. The evaluation and selection of the proposals submitted by the ESCOs could also be carried out in a holistic monetary evaluation by including the energy efficiency by pricing in the saved external costs for environmental impacts with a cost factor (€/t CO2), which is yet to be determined. For this purpose, the average value of 80 €/t, calculated by the Federal Environment Agency from best-practice examples, can be taken as a reference value [54].

3.3.4. Quality Standards for Planning and Maintenance

Further weaknesses identified were operational disruptions and insufficient maintenance in some cases. Plant malfunctions and high repair and maintenance costs (e.g., due to slagging) are often due to the use of incorrect fuel qualities and plant design errors.

To ensure the reliable operation of the biomass combustion plants, the investors should only commission planners and installers that are sufficiently trained and experienced in this area. Appropriate training should be provided to ensure that the installers are highly qualified.

To avoid long downtimes, it is necessary to ensure fast delivery of spare parts and fast arrival of the service company. The planners must consider this at an early stage when planning the system and include the costs for service contracts in the calculation.

A certification of qualified planners and installers could facilitate the selection for the potential investors. One example of good practice has been developed in Austria. There, biomass installers undergo certified training. The Austrian Biomass Association organized courses, which are carried in nine federal states of Austria. In 2014, already one-third of all Austrian installers (1300) have received training, which covers the demand of the whole country. After an examination and, if necessary, with adaptation of the training contents, this course system could possibly be applied in Germany. A nationwide agreement on equal standards in plant design and construction could simplify the transfer.

The Federal Bioenergy Association or Central Agrarian Raw Material Marketing and Development Network could organize and carry out the training activities. Information about suitable installers and service companies as well as experienced ESCOs for large-scale biomass heating plants could be collected and provided on the websites of the German Central Association of Plumbing, Heating, and Air Conditioning, the German Pellet Institute as well as on the websites of the energy agencies and the Chamber of Industry and Commerce.

3.3.5. Better Information about Tailored Supply Concepts Especially in the Woodchip Sector

Due to the higher space requirement of woodchips, limited storage space often causes problems when there is a planned switch in fuels. Often the potential storage areas cannot even be accessed by truck. The storage areas are often quite small due to cost and space.

Through suitable supply concepts, obstacles such as limited storage capacities on site can be overcome. Many fuel suppliers already offer a just-in-time delivery service and, thus, guarantee supply security.

In order to be able to reach storage units that are difficult to access by truck, many suppliers have also equipped their delivery vehicles with special technology, such as a woodchip suction blower or a woodchip blower.

To enable plant concepts even under the above-mentioned unfavorable conditions, investors and plant designers need a good overview of the fuel suppliers and their product ranges as well as their service offers, to include suitable delivery concepts in the planning process at an early stage.

Therefore, the focus should be on improving the information basis. For instance, the Federal Bioenergy Association could publish an online list of fuel suppliers and their services. The website should also provide a proximity search (e.g., based on postal code) for quickly locating suppliers in case of a need for information. To increase the visibility of this site for the target groups, energy agencies, and chambers of industry and commerce could link to this website.

3.3.6. Reducing Uncertainties in Fuel Quality

Consistent fuel quality allows the plant technology to be finely tuned to fuel and, thus, a more efficient use of the biomass. However, for reasons of cost, some of the operators, who are unaware of the negative effects, also purchased low quality, which is not specific to the plant. This leads to shorter maintenance intervals and, thus, higher operating costs.

To ensure a constant fuel quality, expensive processing and laboratory technology is required.

The processing technology enables the production of homogenous fuel qualities from various sources such as nature conservation, landscape management, roadside greenery, used construction timber, and green waste. However, this is only profitable with a large volume turnover, which is why smaller fuel suppliers does not use this. Thus, a fusion of several small suppliers for a joint fuel procession could have a positive effect on the quality and security of supply and leady to additional sorting gains for higher value products.

Long-term supply contracts between supplier and plant operator offer a secure planning basis for the biomass plant. In addition to the delivery quantities and delivery intervals, the contracts also specify the fuel quality parameters. Model contracts provide assistance with the contractual design of supply contracts and the adjustment of fuel prices in long-term contracts [55].

Possible provider of this information are the Federal Bioenergy Association or Central Agrarian Raw Material Marketing and Development Network. Again, Energy Agencies and Chambers of Industry and Commerce could link to this website.

3.3.7. Reducing Uncertainty in the Sustainability Debate of Solid Biomass Fuels

Often potential customers are worried that the use of solid biofuels may jeopardize the sustainability of wood use. To close this knowledge gap and to increase confidence in the sustainable use of energy wood, appropriate quality labels must be created or better publicized. Joint public relations work by state forestry administrations, fuel manufacturers, and suppliers is recommended. A stronger development and use of short rotation plantations on polluted soils or uneconomic agricultural areas could also contribute to the solution. In this context, the possible positive effects on regional value creation should also be considered.

The Charter for Wood 2.0 aims to use more wood from sustainable forestry—for the benefit of climate protection, jobs, and value creation in rural areas, and to conserve finite resources. The Federal Ministry for Food and Agriculture, which has set up a steering group and several working groups for this purpose, highlights that the German forest is richer than any other country in the European Union in terms of its stock, structure, and species. In 2015 only about two-thirds of the 120 million m3 annual increment was harvested for material and energy use (76 million m3). Other publications point out, however, that wood potentials identified in the forest inventory are not fully usable. About 5% of the wood stock cannot be activated due to various restrictions on use and because parts of the forest are under nature conservation or are being used by the military. In addition, the usable wood potentials are not evenly distributed across all types of property. In the state-owned forests and, to some degree, in the corporate forests, the growth rates are mostly exploited to a much greater extent than in private forests. For this reason, the focus of wood mobilization is on private forests, especially micro and small private forests.

Crown wood, with a diameter of less than 7 cm is used in large wood-fired heating plants. Since, crown wood contains important nutrients, its intensive use could endanger the nutrient balance when the soil is poor. In [56], an example of some provincial forests shows that nutrient sustainability is already taken into account in timber harvesting and that nutrient management systems are constantly being enhanced. In order to boost consumer confidence, a common public campaign with political backing is needed. State forestry administrations, fuel manufacturers and suppliers should work together to support the wood campaign and should emphasize the criteria of wood supply sustainability as part of existing certificates.

3.3.8. Acceleration and Standardization of Approval Procedures

Additional effort for conversion work and approval of storage spaces leads to an increasing workload. In addition, due to the federal system, each federal state has its own building code (Bauordnung—BauO). Based on these building codes, the respective state ministries make provisions in the Ordinance on Firing Installations (Feuerungsverordnung—FeuVO), forming the legal basis for setting up and operating combustion plants. Differences in the building codes and in the Ordinance on Firing Installations requirements make the work of planners with cross-border activities more difficult.

The model building code (MBO) is a central instrument for harmonizing the building regulations of the federal states. All building regulations are based on this model building code and, therefore, essentially contain identical legal provisions, differing only in minor details. A further revision of the MBO by the Conference of Construction Ministers is needed to pave the way for the harmonization of the Ordinance on Firing Installations in the respective federal states.

Even during the respective application procedures, difficulties are encountered due to insufficient communication, as there are great differences in the legal and technical expertise of both the respective authorities and the applicants with regard to biomass combustion plants.

The authorization bodies, in turn, complain that the applicants are unaware of the legal requirements and do not take the chance of clarifying discussions with the authorities in advance of the application. To speed up the application procedures, the Chambers of Industry and Commerce could offer support through a coordination office that advises the applicant in the licensing procedure and identifies possible problems at an early stage (building plans, protected areas, and citizen protests). In addition, a digital building application also accelerates the approval process. For instance, there is a cooperation between the federal states Brandenburg, Lower Saxony, Mecklenburg-Western Pomerania, and Schleswig-Holstein Saxony to optimize the digital data exchange between the municipalities belonging to the districts. The example of the electronic transmission of applications and the experience already gained should be transferred to other federal states.

4. Discussion

The analysis results presented are based on the conviction that the stakeholders involved in plant design and construction and the energy supply chain are interlinked like links in a chain. In order to be able to tap the still available potential for solid biofuel plants to the greatest extent possible, it is not enough to simply repair individual chinks in this chain, but must ensure continuous stability.

Against this background, various representatives of the groups of stakeholders (wood producers, plant manufacturers, plant designers, wood and fuel producers, fuel suppliers, and industries well suited for further expansion) were interviewed and the most important obstacles were identified in joint workshops. A further breakdown of these obstacles showed that the implementation of solid biofuel plants (or even their consideration at an early planning stage) often fails due to a lack of awareness on the part of investors and planners/installers, the high investment costs compared to fossil plants, as well of the higher bureaucratic effort and expenses associated with plant planning and plant construction. In addition, many potential buyers of biomass heating plants fear of high maintenance and repair costs during operation. This is due to known negative examples in which planning and operating errors lead to longer plant downtimes.

Nine sets of measures have been formulated to minimize or eliminate the existing weaknesses and to point out possible approaches for politicians and interest groups, to create supportive framework conditions.

A central obstacle to a fuel switch is the low price for coal, oil, and gas and lack of CO2 emission certificates. Without supports, climate-friendly alternatives, such as solid biofuel would therefore not be economical on their own in most cases. Especially in the industrial sector, the challenge is to shorten the amortization period for biofuel-fired plants to make them more competitive with fossil fuel-fired plants.

Companies are reluctant to accept long payback periods for two main reasons: firstly, their liquid funds are tied up for a long period of time, which limits their future scope for action in their core business. On the other hand, there is an increasing risk that the political framework conditions and the conditions necessary for the economic operation of the plant will change. One example for this is the planned tightening of emission limits, also for existing plants, which poses major economic challenges for many plant operators. Politicians can therefore help to shorten the payback period by providing subsidies to lower the high investment costs. At the same time, it must be also ensured that reliable long-term framework conditions are in place. This can be achieved, for example, by ensuring that sufficient subsidies are made available in the event of stricter environmental regulations in order to avoid a financial overload of the plant operators.

The Federal Government has already taken important measures in this respect. Since the beginning of 2020, a percentage subsidy has been provided for biomass heating plants. This makes higher subsidies possible. In addition, not only the boilers but also the entire components of the biomass heating plant, as well as the installation costs of the system components, are subsidized. Existing installations also benefit, as retrofitting of secondary components for particle separation or condensing boiler utilization is promoted. The subsidy amounts to up to 35% of the eligible costs. If an old oil heating system is replaced by a biomass heating system, the subsidy even increases to 45% [57].

A further supporting measure is the increase in the price of fossil fuels by taking greater account of their external costs. As a reaction to the ever-increasing protests of the climate strike movement, the German government decided to introduce a CO2 price. However, the introductory price of €25 remains significantly below the required introductory price calculated by the scientific community for achieving the national climate protection targets. It will only be become clear in the next years to what extent the combination of these two new incentives will affect the demand for biomass heating systems. A suitable monitoring system is needed to measure the effectiveness of the incentives and to be able to adjust them if necessary.

In order to avoid competitive disadvantages for the domestic economy and to prevent national “island solutions” of financial funding, a concerted approach at an international level is necessary. An agreement by the G20 countries regarding a minimum price for CO2 would be a big step forward.

In addition to direct incentives, there is also a need to improve the expertise of all actors (investors and operators, planners, and licensing authorities). As the analysis showed, a large number of guidelines and tools, as well as training programs, have already been developed in the past to support and accelerate planning processes and to ensure a reliable plant operation. However, the oversupply with varying degrees of topicality can also lead to confusion among potential investors in the target groups. In this case, the coordination, updating and compilation of information for the target groups mentioned would be an important step towards improving the necessary level of knowledge of the actors along the supply chain and of potential investors from the promising sectors. Their visibility should be increased and their content should be integrated into mandatory training activities for the target group in question.

In training courses, authority representatives should also be informed of ways to integrate renewable energy into the municipal energy supply. Heating networks offer a good basis for the cost-effective integration of renewable energies. To ensure a climate-neutral heat supply, municipalities should build their strategic planning on energy usage plans. As part of these energy usage plans, heat plans allow suitable locations for the integration of bioheat concepts to be identified.

Local structural conditions, as well as the regionally available suppliers and the (sustainably) available fuel qualities offered by them, must already be taken into account at the planning stage. The barrier of limited storage space can be overcome by tailored supply logistics. Information about the supplier, their services, and the delivery area should be collected and accessible online for generally known contact points (i.e., energy agencies).

Finally, the increasing uncertainty of the public as to whether solid fuels originate from sustainable sources must also be countered by appropriate evidence. The European Commission already considered these concerns in the proposed update to the Renewable Energy Directive for the period 2021–2030 (RED II), wherein the member states are encouraged to develop voluntary international or national schemes that set standards for the production of sustainable biofuels. In order to avoid double certification for wood and the associated higher costs, current, internationally known voluntary certification systems should be strengthened and their visibility to the public should be improved. Based on reliable information and clear management guidelines, these certificates guarantee to the consumers that the biomass comes from a sustainable source, which should also ensure a sustainable soil nutrient balance.

Solid biofuels make an important contribution for achieving climate protection targets not only in Germany, but throughout Europe. Since the potential that can be exploited here has already been exhausted at European level, the focus is on increasing efficiency rather than on further expanding the use of biomass. In combination with other renewable energies, they can achieve a high level of efficiency, especially in the industrial and commercial sector. However, as in Germany, solid biofuels are still predominantly used in the private household sector in most other European countries.

Similarly, in the other partner countries involved in the study Bionergy4Business, hotels, hospitals, and nursing homes, as well as several industry branches are among the most mentioned market segments. Besides these, public buildings and existing district heating plants were also considered as promising sales areas [58]. The packages of measures described here for Germany can also offer approaches and transfer possibilities for other countries and the promising sectors there; thus, contribute to further tapping the existing climate protection potential in Europe.

The focus of this paper is the development of existing potentials for the climate-efficient use of solid biofuels. Last, but not least, it should not be ignored that the sustainable energetic use of biomass can also have positive economic and social effects on regional value creation. However, the evaluation of these effects always requires a case-by-case assessment of a specific region. This issue was thus not considered in detail because the present study focused on potential investors and the criterion of “regional value added” was not identified as a decisive factor by them. However, it must be emphasized that this criterion should always be taken into account when planning heat supply concepts for public buildings.

Author Contributions

Conceptualization, T.S.-B. and D.T.; methodology, T.S.-B.; validation, T.S.-B., D.T.; formal analysis, T.S.-B.; investigation, T.S.-B.; data curation, T.S.-B.; writing—original draft preparation, T.S.-B., D.T.; writing—review and editing, T.S.-B., D.T.; visualization, T.S.-B.; supervision, D.T.; project administration, T.S.-B.; funding acquisition, T.S.-B. All authors have read and agreed to the published version of the manuscript.

Funding

The research was funded by the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program, grant number 646495”.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Overview of key stakeholders interviewed to identify promising market segments (see also [28]).

Table A1.

Overview of key stakeholders interviewed to identify promising market segments (see also [28]).

| Role | Company | Type of Business |

|---|---|---|

| Energy system planner | IDEE-Seeger | Planner of biomass district heating plant |

| Managing director | HDG-Bavaria | Biomass boiler manufacturer |

| Managing director | Heizomat | Biomass boiler manufacturer |

| Managing director | Viessmann Germany Industry GmbH | Biomass boiler manufacturer |

| Division manager for heating contract services | GBH Mieterservice Vahrenheide GmbH | Contractor |

Table A2.

Person/organization interviewed in the second phase.

Table A2.

Person/organization interviewed in the second phase.

| Organization/ Person Interviewed (PI) | Scope/Function |

|---|---|

| Biomass Suppliers | |

| Biomassehof Borlinghausen (biomass treatment plant) PI: Managing Director | Important biofuel supplier (12,000 tons per year). Product portfolio encompasses woodchips, DIN plus pellets (DIN—German Institute for Standardization) and briquettes for energetic use. |

| German Forestry Council (DFWR) PI: Managing Director | Represents forest management and all stakeholders in forests in Germany. Members are state forest management agencies, representatives of the German Association of Towns and Municipalities (DStGB), and the working group of the German Forest Owners Association (AGDW) for private forests. The association represents the interests of sustainable forest management and 2 million private and public forest owners. |

| Biomassehof Achental PI: CEO | The convincing economic concept of Biomassehof Achental gained the political support of the municipalities of Achental Valley. Approximately 8000 m³of premium woodchips are delivered annually to hotels, restaurants, and the health center. In addition, the Biomassehof train a large number of heating engineers as a preparation to play a key role in the implementation of heat concepts based on solid biomass fuels. Facility managers and heating engineers are trained on wood fuels and renewable energies, plant construction, energy saving measures, etc. |

| Demand Side | |

| Adelphie (consulting company) PI: Project Manager | Implements the national energy campaign for the German Hotel and Restaurant Association (DEHOGA). DEHOGA represents the interests of the German hospitality industry. |

| Sportbäder Leipzig GmbH PI: Technical Director | Operates 8 indoor swimming pools, 6 outdoor swimming pools, and 2 saunas. |

| Helios clinics PI: Manager of Central Technical Services | A member of the Fresenius Group, one of the largest hospital groups in Europe. In Germany, HELIOS operates 112 acute care hospitals and post-acute care clinics, representing 5% of all German hospitals. The Helios clinics operate 13 pellet plants. |

| Interest Organization/Policy Authority | |

| Ministry for the Environment of the federal state of Baden-Wuerttemberg PI: Member of the “energy industry” department, “renewable energies” unit | The department deals with the fundamental issues of energy politics, energy efficiency of buildings, energy efficiency in households and companies, renewable energies, and transport and storage networks. |

| The Wood Energy Association as a subunit of the German Bioenergy Association (BBE): PI: Managing Director | Holding organization of the German bioenergy market, representing the energy market in comprehensive areas (electricity, heat, and transportation). The Wood Energy Association represents the interest of energetic wood use. |

| Federal Ministry of Economic Affairs and Energy PI: Expert in the topic Bioenergy | Central priority is to lay the foundations for economic prosperity in Germany; one subtask is the realization and strategic planning of the transformation of the German energy system. |

| Regional Planning Association of West Saxony PI: Director | Body responsible for regional planning in Western Saxony. |

| Energy Agency of Saxony (SAENA): PI: Contact Person in “Energy” Service Center | Independent competence and information center for energy for the federal state of Saxony. |

| Financial Institutions [28] | |

| Commerzbank | Focuses specifically on the requirements of medium-sized companies, the public sector, and institutional clients. Focus is primarily on financing biomass-based heat concepts of medium-sized companies (with own substrate resources). |

| Volks- und Raiffeisenbank PI: Representative from the business field “Energy and Environment” | Has offered financing options for renewable energy projects for more than 25 years. Usually long-term investment loans are provided, whereby low-interest loans are primarily from KfW Bank and Landwirtschaftliche Rentenbank. |

| Investitionsbank Schleswig-Holstein PI: Head of Energy Agency | The SH investment bank is the only development bank that also has an energy agency. As part of the country’s energy and climate change initiative, free initial consultations are offered for municipal stakeholders and municipalities.Consortium partner of local banks – co-financing of projects. |

| Wirtschafts- und Infrastrukturbank Hessen | Up to 30% of the investment costs of woodchip and pellet-fired bioenergy plants are subsidized through a special agricultural support program of the federal state of Hesse. |

| Examples of Good Practice | |

| VILA VITA Holiday Resort Anneliese Pohl Seedorf PI: Plant Operator | The holiday resort has 160 beds in small apartment buildings, a restaurant, a multifunctional hall, and a spa area. All of its heating requirements are covered by a high-efficiency 400 kW base load (+500 kW backup and for further extension) cogeneration pellet plant, which supply the resort by a heating network. |

| Weißenstadt Health Resort PI: Plant operator | The health resort is supplied by the company Biomasseheizung Weißenstadt GmbH. There are two woodchip-fired biomass boilers, one for base load with an output of 550 KW, and one for peak load with an output of 300 KW. Local farmers ensure the fuel supply of the plant. |

| Clinical Center of Erlangen PI: Plant Operator | The Clinical Center of Erlangen has in total about 700 beds. Since 2004, approximately 97% of the heat demand has been supplied by a biomass heating plant, which is located next to the clinical center. Net capacity of the biomass boiler is 4.3 MW base load. Investor and operator of the system is the biomass treatment works (Kompostier Betriebs GmbH Erlangen-Höchstadt). |

| Obernsees Thermal Bath PI: Plant operator | The Obernsees Thermal Bath and has a thermal pool and an adventure area. Since November 1997, a biomass heating plant, which was built next to the water park, covers the heat demand of the bath. The investor and operator of the system is the Biomasse Heizanlage Obernsees GmbH (BHO). Shareholders are the MR Agrarservice GmbH, the Bayernwerke Natur (energy provider), which develop individualized energy solutions on the basis of renewable sources. Net capacity of the biomass boiler(s) 1.25 MW base load (400 kW + 850 kW). |

References

- Bertram, R.; Primova, R. Energy Atlas 2018: Facts and Figures about Renewables in Europe. Available online: https://www.boell.de/sites/default/files/energyatlas2018_facts-and-figures-renewables-europe.pdf.pdf (accessed on 12 July 2019).

- Bundesministerium für Wirtschaft und Energie (BMWi). Energieeffizienz in Zahlen: Entwicklungen und Trends in Deutschland 2019. Available online: www.bmwi.de/Redaktion/DE/Publikationen/Energie/energieeffizienz-in-zahlen-2019.pdf?__blob=publicationFile&v=72 (accessed on 28 July 2020).

- Bundesministerium für Umwelt, Naturschutz, Bau und Reaktorsicherheit (BMUB). Klimaschutzplan 2050. Klimaschutzplan 2050 Klimaschutzpolitische Grundsätze und Ziele der Bundesregierung. 2016. Available online: https://www.bmu.de/fileadmin/Daten_BMU/Download_PDF/Klimaschutz/klimaschutzplan_2050_bf.pdf (accessed on 3 September 2020).

- Matthes, F.C.; Busche, J.; Döring, U.; Emele, L.; Gores, S.; Harthan, R.O.; Hermann, H.; Jörß, W.; Loreck, C.; Scheffler, M.; et al. Politikszenarien für den Klimaschutz IV. Climate Change. 2013. Available online: http://www.uba.de/uba-info-medien/4412.html (accessed on 3 September 2020).

- Bauchmüller, M. Deutschland Hinkt Seinem Klimaziel Hinterher. Süddeutsche, 11 October 2017. Available online: http://www.spiegel.de/wissenschaft/natur/klimaschutz-deutschland-produziert-zu-viel-co2-ziele-in-gefahr-a-1172368.html (accessed on 30 January 2018).

- Stryi-Hipp, G.; Baur, F.; Borggrefe, F.; Gerhardt, N.; Hauer, A.; Horst, J.; Huenges, E.; Kastner, O.; Lenz, V.; Martin, N.; et al. Erneuerbare Energien im Wärmesektor–Aufgaben, Empfehlungen und Perspektiven. Positionspapier des Forschungsverbunds Erneuerbare Energien. 2015. Available online: http://www.fvee.de/fileadmin/publikationen/Politische_Papiere_FVEE/15.EEWaerme/15_FVEE-Positionspapier_EE-Waerme.pdf (accessed on 3 September 2020).

- Umweltbundesamt AGEE-Stat. Erneuerbare Energien in Zahlen. Available online: https://www.umweltbundesamt.de/themen/klima-energie/erneuerbare-energien/erneuerbare-energien-in-zahlen#uberblick (accessed on 28 July 2020).

- Eurostat. Renewable Energy Statistics. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php/Renewable_energy_statistics#Share_of_renewable_energy_almost_doubled_between_2004_and_2018 (accessed on 28 July 2020).

- Sustainable Agribusiness Forum. Biomass for Heat. Bioenergy Europe Statistical Report 2019. Available online: https://saf.org.ua/en/news/722/ (accessed on 28 July 2020).

- Bundesministerium für Wirtschaft und Energie. Erneuerbare Energien in Zahlen 2015. Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Energie/erneuerbare-energien-in-zahlen-2018.pdf?__blob=publicationFile&v=22 (accessed on 3 September 2020).

- Bundesministerium für Wirtschaft und Energie (BMWi). Erneuerbare Energien in Zahlen. Nationale und Internationale Entwicklungen im Jahr 2017. 2018. Available online: https://www.bmwi.de/Redaktion/DE/Publikationen/Energie/erneuerbare-energien-in-zahlen-2017.pdf?__blob=publicationFile&v=29 (accessed on 28 July 2020).

- Lenz, V.; Szarka, N.; Jordan, M.; Thrän, D. Status and Perspectives of Biomass Use for Industrial Process Heat for Industrialized Countries. Chem. Eng. Technol. 2020, 43, 1469–1484. [Google Scholar] [CrossRef]

- Frauenhofer ISI. Erstellung von Anwendungsbilanzen für die Jahre 2018 bis 2020 für die Sektoren Industrie und GHD. Studie für die Arbeitsgemeinschaft Energiebilanzen e.V. (AGEB)—Entwurf. 2019. Available online: https://ag-energiebilanzen.de/8-0-Anwendungsbilanzen.html (accessed on 3 September 2020).

- Jordan, M.; Lenz, V.; Millinger, M.; Oehmichen, K.; Thrän, D. Future competitive bioenergy technologies in the German heat sector: Findings from an economic optimization approach. Energy 2019, 189, 116194. [Google Scholar] [CrossRef]

- Herhold, P.; Burchardt, J.; Schönberger, S.; Rechenmacher, F.; Kirchner, A.; Kemmler, A.; Wuensch, M.; Gerbert, P. Climate Paths for Germany. 2018. Available online: https://www.bcg.com/de-de/publications/2018/climate-paths-for-germany (accessed on 3 September 2020).

- Thrän, D.; Arendt, O.; Ponitka, J.; Braun, J.; Millinger, M.; Wolf, V.; Banse, M.; Schaldach, R.; Schüngel, J.; Gärtner, S.; et al. Meilensteine 2030. Elemente und Meilensteine für die Entwicklung Einer Tragfähigen und Nachhaltigen Bioenergiestrategie; Endbericht zu FKZ 03KB065, FKZ 03MAP230; DBFZ: Leipzig, Germany, 2015. [Google Scholar]

- Mantau, U. Holzrohstoffbilanzen und Stoffströme des Holzes–Entwicklungen in Deutschland 1987 bis 2016; Final Report; Hamburg: Gülzow-Prüzen, Germany, 2018. [Google Scholar]

- Oehmichen, K.; Röhling, S.; Dunger, K.; Gerber, K.; Klatt, S. Ergebnisse und Bewertung der Alternativen WEHAM-Szenarien. Available online: https://www.weham-szenarien.de/fileadmin/weham/Ergebnisse/AFZ_13_17_2_Ergebnisse_und_Bewertung_der_alternativen_WEHAM-Szenarien.pdf (accessed on 3 September 2020).

- Malico, I.; Nepomuceno Pereira, R.; Gonçalves, A.C.; Sousa, A.M.O. Current status and future perspectives for energy production from solid biomass in the European industry. Renew. Sustain. Energy Rev. 2019, 112, 960–977. [Google Scholar] [CrossRef]

- Bundesministerium für Wirtschaft und Energie (BMWi). Integrierter Nationaler Energie-und Klimaplan. Available online: https://www.bmwi.de/Redaktion/DE/Textsammlungen/Energie/necp.html (accessed on 28 July 2020).

- Bundesministerium für Naturschutz und Nukleare Sicherheit (BMU) 2019 Klimaschutzplan 2050. Klimaschutzpolitische Grundsätze und Ziele der Bundesregierung. Available online: https://www.bmu.de/fileadmin/Daten_BMU/Download_PDF/Klimaschutz/klimaschutzplan_2050_bf.pdf (accessed on 3 September 2020).

- Bertelsen, N.; Mathiesen, B.V. EU-28 Residential Heat Supply and Consumption: Historical Development and Status. Energies 2020, 13, 1894. [Google Scholar] [CrossRef]

- Baur, N.; Blasius, J. Handbuch Methoden der Empirischen Sozialforschung; Springer Fachmedien Wiesbaden: Wiesbaden, Germany, 2014; ISBN 978-3-531-18939-0. [Google Scholar]

- CrossBorder Bioenergy Working Group on District Heating. SECTOR HANDBOOK DISTRICT HEATING: Prepared by the CrossBorder Bioenergy Working Group on District Heating. Available online: http://www.crossborderbioenergy.eu/fileadmin/user_upload/Sector_Handbook_DH.pdf (accessed on 3 September 2020).

- Uslu, A.; van Stralen, J. Bioenergy Markets: The Policy Demand for Heat, Electricity and Biofuels, and Sustainable Biomass Supply: Results from Alternative Bioenergy Demand Scenarios for 2020 and 2030. Available online: https://www.ecn.nl/publications/PdfFetch.aspx?nr=ECN-L--12-004 (accessed on 19 December 2018).

- Viehmann, C.; Westerkamp, T.; Schwenker, A.; Schenker, M.; Thrän, D.; Lenz, V.; Ebert, M. Ermittlung des Verbrauchs Biogener Festbrennstoffe im Sektor Gewerbe, Handel, Dienstleistungen (GHD-Sektor); Endbericht; DBFZ: Leipzig, Germany, 2012. [Google Scholar]

- Romanian Association of Biomass and Biogas (ARBIO). Report on Bioenergy Business Models and Financing Conditions for Selected Countries. 2015. Available online: http://www.bioenergy4business.eu/wp-content/uploads/2015/06/D3.4-Report-on-bioenergy-business-models-and-financing-conditions-for-selected-countries.pdf (accessed on 12 July 2019).

- Rogers, E.M. Diffusion of Innovations, 4th ed.; Free Press: New York, NY, USA, 1995; ISBN 0028740742. [Google Scholar]

- Schmidt-Baum, T. Report on Frame Conditions for Realizing Bioenergy Heat Projects in Promising Market Segments. Available online: https://ec.europa.eu/research/participants/documents/downloadPublic?documentIds=080166e5b5d96471&appId=PPGMS (accessed on 3 September 2020).

- Bloche, K.; Schmidt-Baum, T. Germany’s Promising Market Segments for Heating with Solid Biomass (>100 kW). Country Summary Report of Promising Market Segments for Use of Bioenergy. Available online: https://ec.europa.eu/research/participants/documents/downloadPublic?documentIds=080166e5ad8cb0f0&appId=PPGMS (accessed on 3 September 2020).

- Romanian Association of Biomass and Biogas (ARBIO). Report Summarizing Best Practice Examples and Conclusions. 2015. Available online: https://ec.europa.eu/research/participants/documents/downloadPublic?documentIds=080166e5a33ed958&appId=PPGMS (accessed on 3 September 2020).

- Geiger, B.; Kleeberger, H.; Hardi, L. Erstellen der Anwendungsbilanzen 2013 bis 2017 für den Sektor Gewerbe, Handel, Dienstleistungen (GHD). 2019. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=&ved=2ahUKEwjN7IfrgcLqAhWEfZoKHdb5AksQFjABegQIAhAB&url=https%3A%2F%2Fag-energiebilanzen.de%2Findex.php%3Farticle_id%3D29%26fileName%3Dgeiger_ife_-_einzelbericht_gewerbe__handel__dienstleistungen_2013_-_2017.pdf&usg=AOvVaw19C2LE6a3vyAEcF1w3pbIX (accessed on 28 July 2020).

- Deutschen Gesellschaft für das Badewesen e.V. Bäderatlas. Available online: http://www.baederatlas.com/ (accessed on 28 July 2020).

- Statistisches Bundesamt. Statistisches Jahrbuch: Gastgewerbe und Tourismus. Available online: https://www.destatis.de/DE/Themen/Querschnitt/Jahrbuch/jb-gastgewerbe-tourismus.pdf?__blob=publicationFile (accessed on 28 July 2020).

- Kirschbaum, S. Branchenenergiekonzept Alten-und Pflegeheime NRW Energiekennzahlen. Available online: https://docplayer.org/19478057-Branchenenergiekonzept-alten-und-pflegeheime-nrw-energiekennzahlen.html (accessed on 28 July 2020).

- Gesundheitsberichtserstattung des Bundes (GBE). Pflegeheime und Verfügbare Plätze in Pflegeheimen. Gliederungsmerkmale: Jahre, Region, Art der Einrichtungen/Plätze, Träger. Available online: http://www.gbe-bund.de/oowa921-install/servlet/oowa/aw92/dboowasys921.xwdevkit/xwd_init?gbe.isgbetol/xs_start_neu/&p_aid=i&p_aid=35086526&nummer=570&p_sprache=D&p_indsp=-&p_aid=22910504 (accessed on 28 July 2020).

- Statistisches Bundesamt. Pflegeheime und Verfügbare Plätze in Pflegeheimen. Gliederungsmerkmale: Jahre, Region, Art der Einrichtungen/Plätze, Träger. 2017. Available online: http://www.gbe-bund.de/oowa921-install/servlet/oowa/aw92/WS0100/_XWD_PROC?_XWD_2/1/XWD_CUBE.DRILL/_XWD_30/D.100/10101#SOURCES (accessed on 12 July 2019).

- Statistisches Bundesamt. Krankenhäuser. 2017. Available online: http://www.gbe-bund.de/oowa921-install/servlet/oowa/aw92/dboowasys921.xwdevkit/xwd_init?gbe.isgbetol/xs_start_neu/&p_aid=3&p_aid=73227620&https://www.destatis.de/DE/Themen/Gesellschaft-Umwelt/Gesundheit/Krankenhaeuser/Tabellen/gd-krankenhaeuser-jahre.html (accessed on 12 July 2019).

- Verein Deutscher Zementwerke, e.V. (VDZ). Zementindustrie im Überblick 2017/2018. Berlin. 2017. Available online: https://www.vdz-online.de/fileadmin/gruppen/vdz/3LiteraturRecherche/Zementindustie_im_Ueberblick/VDZ_Zementindustrie_im_Ueberblick_2017_2018.pdf (accessed on 28 July 2020).

- Datenbasis zur Bewertung von Energieeffizienzmaßnahmen in der Zeitreihe 2005–2014; Umwelt, B., Ed.; Endbericht; Umwelt Bundesamt: Dessau-Roßlau, Germany, 2017. [Google Scholar]

- Hohmann, H. Anzahl der Unternehmen in der Branche Herstellung von Glas-, Keramik- und Steinwaren in Deutschland in den Jahren 2005 bis 2019. 2020. Available online: https://de.statista.com/statistik/daten/studie/259512/umfrage/unternehmen-in-der-branche-herstellung-von-glas-keramik-und-steinwaren/ (accessed on 28 July 2020).

- Schmidt-Baum, T. Country Specific Recommendations to Support the Implementation of Bioenergy Heat Projects in the Promising Markets. 2017. Available online: http://www.bioenergy4business.eu/wp-content/uploads/2015/06/D6.5-Country-specific-recommendations-to-support-the-implementation-of-bioenergy-heat-projects-in-the-promising-markets.pdf (accessed on 12 July 2019).

- Verband Deutscher Maschinen und Anlagenbau e.V. Beschleunigung von Energieeffizienzinvestitionen in Deutschland. das VDMA-Kreditmodell. 2012. Available online: http://www.vdma.org/article/-/articleview/4725526?cachedLR61051178=de_DE (accessed on 3 September 2020).

- Edenhofer, O.; Flachsland, C.; Kalkuhl, M.; Knopf, B.; Pahle, M. Optionen für Eine CO2-Preisreform. MCC-PIK-Expertise für den Sachverständigenrat zur Begutachtung der Gesamtwirtschaftlichen Entwicklung, Berlin. 2019. Available online: https://www.mcc-berlin.net/fileadmin/data/B2.3_Publications/Working%20Paper/2019_MCC_Optionen_f%C3%BCr_eine_CO2-Preisreform_final.pdf (accessed on 3 September 2020).

- Bundesverband der Deutschen Industrie e.V. (BDI); German Watch; Mercator Research Institute on Global Commons and Climate Change (MCC). G20-Staaten Sollen Bepreisung von CO2 Beschließen. Available online: https://bdi.eu/media/presse/presse/downloads/20160901_Pressemitteilung_CO2_Bepreisung.pdf (accessed on 3 September 2020).