Value Co-Creation Behavior in Green Supply Chains: An Empirical Study

Abstract

1. Introduction

2. Literature Review

2.1. Cooperation in Green Supply Chain

2.2. Value Co-Creation Behavior in the Supply Chain

2.3. Value Co-Creation and Performance

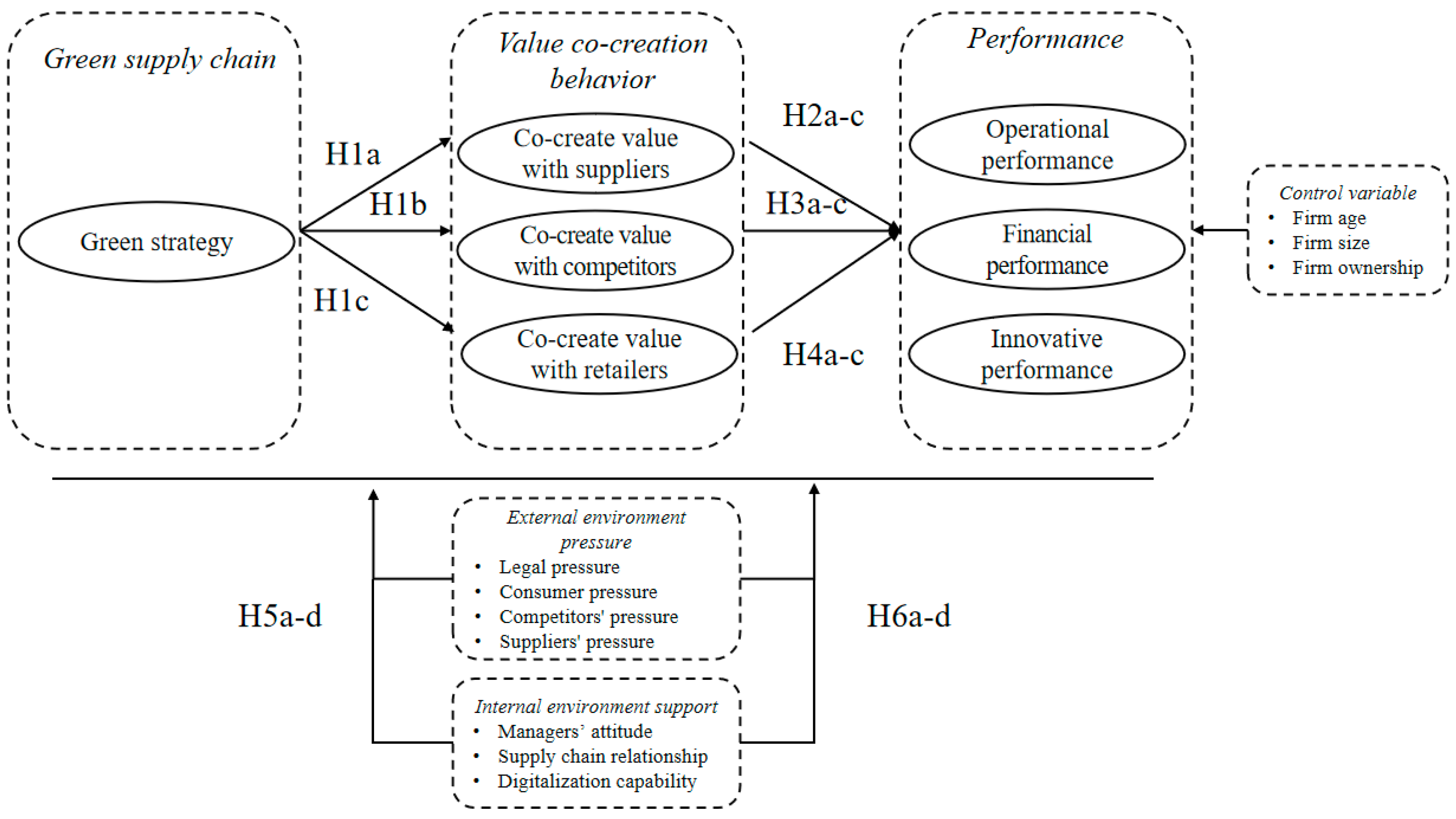

3. Hypotheses Development

3.1. The Relationship between Green Strategy and Value Co-Creation Behavior

3.2. The Impact of Value Co-Creation Behavior on Firm Performance

3.3. The Moderating Effect of External Environmental Pressure

3.4. The Moderating Effect of Internal Environmental Support

4. Methodology

4.1. Research Process

4.2. Survey Development

4.3. Sample Selection

5. Results

5.1. Preliminary Study

5.2. Exploratory Study

5.3. Confirmatory Study

5.4. Hypotheses Testing and Results

6. Discussion and Implications

6.1. Effects of Green Strategy on Value Co-Creation Behavior

6.2. Enablers of Performance

6.3. Effects of Moderators

6.4. Theoretical Implications

6.5. Managerial Implications

7. Limitations and Future Research Lines

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| Factor | Measured Variable | Item | |

|---|---|---|---|

| Green strategy (GS) | Managers are very willing to implement the green supply chain strategy. | GS1 | |

| Select environmentally friendly suppliers. | GS2 | ||

| Can carry out green design and green production for products. | GS3 | ||

| Can pay attention to the principle of resource conservation of environmental protection. | GS4 | ||

| Advocate that consumers choose green products that are not polluted or contribute to public health. | GS5 | ||

| Try to reduce the generation of harmful substances. | GS6 | ||

| Value co-creation with supplier (VCS) | Can adopt positive attitude and cooperative behavior with suppliers. | VCS1 | |

| Can jointly design products and systems to meet production requirements. | VCS2 | ||

| There are norms about the relationship of responsibility, right, interest and some behaviors. | VCS3 | ||

| Can establish the mechanism of interest distribution. | VCS4 | ||

| Value co-creation with competitor (VCC) | Can adopt positive attitude and cooperative behavior with competitors. | VCC1 | |

| Can share information, technology and resources to improve competitive advantage. | VCC2 | ||

| There are norms about the relationship of responsibility, right, interest and some behaviors. | VCC3 | ||

| Can establish the mechanism of interest distribution. | VCC4 | ||

| Value co-creation with retailer (VCR) | Can adopt positive attitude and cooperative behavior with retailers. | VCR1 | |

| Can receive retailers’ feedback in time and let retailers participate in product design and development. | VCR2 | ||

| There are norms about the relationship of responsibility, right, interest and some behaviors. | VCR3 | ||

| Can establish the mechanism of interest distribution. | VCR4 | ||

| External Environmental Pressure (EEP) | Legal Pressure (LP) | There are national laws, regulations and standards on environmental protection of manufacturing firms. | LP1 |

| There are local laws, regulations and standards on environmental protection of manufacturing firms. | LP2 | ||

| There are laws, regulations, and standards related to environmental protection in market. | LP3 | ||

| Relevant departments strengthen the supervision and management of firms’ compliance with laws, regulations and standards related to environmental protection. | LP4 | ||

| Law enforcement personnel increase the punishment for firms that violate relevant laws, regulations and standards. | LP5 | ||

| The government has increased financial subsidies to reduce the pollution and damage of firms to environmental resources. | LP6 | ||

| Relevant policies issued by the government strongly support the sustainable development. | LP7 | ||

| Consumers’ Pressure(CP) | Consumers’ social responsibility and awareness of environmental protection are enhanced. | CP1 | |

| Consumers’ expectations and requirements for green products and product safety increase. | CP2 | ||

| The export of products shall meet the environmental protection standards and safety standards. | CP3 | ||

| Consumers require us to have a good social and environmental image. | CP4 | ||

| Non-governmental organizations advocate social responsibility and environmental protection. | CP5 | ||

| Competitors’ Pressure (CmP) | Leading firms in the industry have begun to implement sustainable supply chain management. | CmP1 | |

| Firms in the industry that have implemented sustainable supply chain management perform well in terms of environment, society and economy. | CmP2 | ||

| Most firms in the industry have begun to implement sustainable supply chain management. | CmP3 | ||

| Suppliers’ Pressure (SP) | Suppliers pay more attention to environmental protection. | SP1 | |

| Suppliers put forward environmental protection requirements for the firms. | SP2 | ||

| The firm has reached certain environmental partnership with suppliers. | SP3 | ||

| Suppliers can provide environmentally friendly or recyclable raw materials. | SP4 | ||

| Suppliers can provide environmentally friendly or recyclable raw material packaging. | SP5 | ||

| Internal Environmental Support (IES) | Managers’ attitude (MA) | Top management believes that environmental protection is an important part of corporate strategy. | MA1 |

| Senior managers support activities to improve social responsibility and environmental performance. | MA2 | ||

| Top managers pay attention to corporate social responsibility and require corporate behavior to meet environmental requirements. | MA3 | ||

| Senior managers are directly responsible for the work of firm environment. | MA4 | ||

| Supply chain relationship (SCR) | Firms and government departments have established friendly relations at various levels. | SCR1 | |

| Firms and major suppliers have established friendly relations at multiple levels. | SCR2 | ||

| Different departments of the firms have established friendly relations at multiple levels. | SCR3 | ||

| Firms and distributors have established friendly relations at many levels. | SCR4 | ||

| Firms and retailers have established friendly relations at many levels. | SCR5 | ||

| Firms and suppliers have established friendly relations at multiple levels. | SCR6 | ||

| Digitalization capability (DC) | Managers have digital leadership. | DC1 | |

| Firms have more information professionals. | DC2 | ||

| Digital facilities and information systems are widely used. | DC3 | ||

| The business object of the enterprise has been digitized by means of mobile technology, etc. | DC4 | ||

| Can conduct digital contact analysis on the business of the enterprise. | DC5 | ||

| Business events and business decisions are driven by data analysis and algorithms. | DC6 | ||

| Firms have digital based business model innovation. | DC7 | ||

| Firms’ IT capability can support digital transformation. | DC8 | ||

| Operational performance (OP) | Customer service level of the company has been improved. | OP1 | |

| The company’s responsiveness has been improved. | OP2 | ||

| Decrease in customer complaints. | OP3 | ||

| Financial performance (FP) | Market share expansion. | FP1 | |

| Increase in revenue. | FP2 | ||

| Decrease in total operating costs. | FP3 | ||

| The return on assets of has been improved. | FP4 | ||

| The inventory turnover cycle is optimized. | FP5 | ||

| Innovative performance (IP) | Often take the lead in launching new products/services in the industry. | IP1 | |

| Often take the lead in applying new technologies in the industry. | IP2 | ||

| Cost increase of the manufacturer’s investment in product transformation and innovation. | IP3 | ||

| Increase in the manufacturer’s intellectual property (including application for patent, trademark and design, etc. | IP4 | ||

| The manufacturer’s innovative products have a good market response. | IP5 | ||

| Increase in sales revenue of innovative products. | IP6 | ||

| The manufacturer’s innovative products are highly irreplaceable. | IP7 | ||

References

- Bai, C.; Kusi-Sarpong, S.; Sarkis, J. An implementation path for green information technology systems in the Ghanaian mining industry. J. Clean. Prod. 2017, 164, 1105–1123. [Google Scholar] [CrossRef]

- Hong, Z.; Guo, X. Green product supply chain contracts considering environmental responsibilities. Omega 2018, 83, 155–166. [Google Scholar] [CrossRef]

- Kusi-Sarpong, S.; Gupta, H.; Sarkis, J. A supply chain sustainability innovation framework and evaluation methodology. Int. J. Prod. Res. 2019, 57, 1990–2008. [Google Scholar] [CrossRef]

- Lacoste, S. Sustainable value co-creation in business networks. Ind. Mark. Manag. 2016, 52, 151–162. [Google Scholar] [CrossRef]

- Isaksson, R.; Johansson, P.; Fischer, K. Detecting Supply Chain Innovation Potential for Sustainable Development. J. Bus. Ethics 2010, 97, 425–442. [Google Scholar] [CrossRef]

- Li, S.; Haney, M.H.; Lee, G.; Kang, M.; Ko, C. The effect of task conflict on outsourcers’ long-term orientation toward suppliers: The moderating role of formal control and Chinese guanxi. J. Bus. Ind. Mark. 2019, 35, 260–269. [Google Scholar] [CrossRef]

- Lo, S.M.; Zhang, S.; Wang, Z.; Zhao, X. The impact of relationship quality and supplier development on green supply chain integration: A mediation and moderation analysis. J. Clean. Prod. 2018, 202, 524–535. [Google Scholar] [CrossRef]

- Tariq, A.; Yuosre, F.; Badir, W.T.; Bhutta, U.S. Drivers and consequences of green product and process innovation: A systematic review, conceptual framework, and future outlook. Technol. Soc. 2017, 51, 8–23. [Google Scholar] [CrossRef]

- Liu, Y.; Luo, Y.; Liu, T. Governing buyer–supplier relationships through transactional and relational mechanisms: Evidence from China. J. Oper. Manag. 2009, 27, 294–309. [Google Scholar] [CrossRef]

- Somsuk, N.; Laosirihongthong, T. Prioritization of applicable drivers for green supply chain management implementation toward sustainability in Thailand. Taylor Fr. 2016, 24, 175–191. [Google Scholar] [CrossRef]

- Shi, X.; Chan, H.L.; Dong, C. Value of bargaining contract in a supply chain system with sustainability investment: An incentive analysis. IEEE Trans. Syst. Man Cybern. Syst. 2020, 50, 1622–1634. [Google Scholar] [CrossRef]

- Shi, X.; Dong, C.; Zhang, C.; Zhang, X. Who should invest in clean technologies in a supply chain with competition? J. Clean. Prod. 2019, 215, 689–700. [Google Scholar] [CrossRef]

- Dong, C.; Liu, Q.; Shen, B. To be or not to be green? Strategic investment for green product development in a supply chain. Transp. Res. Part E Logist. Transp. Rev. 2019, 131, 193–227. [Google Scholar] [CrossRef]

- Huang, X.X.; Hu, Z.P.; Liu, C.S.; Yu, D.J.; Yu, L.F. The relationships between regulatory and customer pressure, green organizational responses, and green innovation performance. J. Clean. Prod. 2016, 112, 3423–3433. [Google Scholar] [CrossRef]

- Schiederig, T.; Tietze, F.; Herstatt, C. Green innovation in technology and innovation management—An exploratory literature review. R&D Management 2012, 42, 180–192. [Google Scholar]

- Swami, S.; Shah, J. Channel coordination in green supply chain management. J. Oper. Res. Soc. 2013, 64, 339–351. [Google Scholar] [CrossRef]

- Wei, J.; Zhao, J. Pricing Decisions for Substitutable Products with Horizontal and Vertical Competition in Fuzzy Environments. Ann. Oper. Res. 2016, 242, 505–528. [Google Scholar] [CrossRef]

- Zu-Jun, M.; Zhang, N.; Dai, Y.; Hu, S. Managing channel profits of different cooperative models in closed-loop supply chains. Omega 2016, 59, 251–262. [Google Scholar] [CrossRef]

- Chen, R.R.; Roma, P. Group Buying of Competing Retailers. Prod. Oper. Manag. 2011, 20, 181–197. [Google Scholar] [CrossRef]

- Wei, J.; Zhao, J.; Li, Y. Price and warranty period decisions for complementary products with horizontal firms’ cooperation/noncooperation strategies. J. Clean. Prod. 2015, 105, 86–102. [Google Scholar] [CrossRef]

- Yang, L.; Zhang, Q.; Ji, J. Pricing and carbon emission reduction decisions in supply chains with vertical and horizontal cooperation. Int. J. Prod. Econ. 2017, 191, 286–297. [Google Scholar] [CrossRef]

- Li, H.; Wang, C.; Shang, M.; Ou, W. Pricing, Carbon Emission Reduction, Low-Carbon Promotion and Returning Decision in a Closed-Loop Supply Chain under Vertical and Horizontal Cooperation. Int. J. Environ. Res. Public Health 2017, 14, 1332. [Google Scholar] [CrossRef] [PubMed]

- Dai, R.; Zhang, J.; Tang, W. Cartelization or Cost-sharing? Comparison of cooperation modes in a green supply chain. J. Clean. Prod. 2017, 156, 159–173. [Google Scholar]

- Ge, Z.; Hu, Q. Collaboration in R&D activities: Firm-specific decisions. Eur. J. Oper. Res. 2007, 185, 864–883. [Google Scholar]

- Gupta, S. Research Note—Channel Structure with Knowledge Spillovers. Mark. Sci. 2008, 27, 247–261. [Google Scholar] [CrossRef]

- Ge, Z.; Hu, Q.; Xia, Y. Firms’ R&D Cooperation Behavior in a Supply Chain. Prod. Oper. Manag. 2014, 23, 599–609. [Google Scholar]

- Yenipazarli, A. To collaborate or not to collaborate: Prompting upstream eco-efficient innovation in a supply chain. Eur. J. Oper. Res. 2017, 260, 571–587. [Google Scholar] [CrossRef]

- Song, H.; Gao, X. Green supply chain game model and analysis under revenue-sharing contract. J. Clean. Prod. 2018, 170, 183–192. [Google Scholar] [CrossRef]

- Dong, C.; Shen, B.; Chow, P.S.; Yang, L.; Ng, C.T. Sustainability investment under cap-and-trade regulation. Ann. Oper. Res. 2016, 240, 509–531. [Google Scholar] [CrossRef]

- Heydari, J.; Govindan, K.; Aslani, A. Pricing and greening decisions in a three-tier dual channel supply chain. Int. J. Prod. Econ. 2019, 217, 185–196. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Strategy: Techniques for Analyzing Industries and Competitors; Social Science Electronic Publishing: New York, NY, USA, 1980; pp. 86–87. [Google Scholar]

- Huemer, L. Supply Management: Value Creation, Coordination and Positioning in Supply Relationships. Long Range Plan. 2006, 39, 133–153. [Google Scholar] [CrossRef]

- Ketchen, D.J.; Hult, G.T.M. Bridging Organization Theory and Supply Chain Management: The Case of Best Value Supply Chains. J. Oper. Manag. 2007, 25, 573–580. [Google Scholar] [CrossRef]

- Prahalad, C.K.; Ramaswamy, V. Co-creation experiences: The next practice in value creation. J. Interact. Mark. 2010, 18, 5–14. [Google Scholar] [CrossRef]

- Freeman, R.E. Managing for Stakeholders: Trade-offs or Value Creation. J. Bus. Ethics 2010, 96, 7–9. [Google Scholar] [CrossRef]

- Freudenreich, B.; Lüdeke-Freund, F.; Schaltegger, S. A Stakeholder Theory Perspective on Business Models: Value Creation for Sustainability. J. Bus. Ethics 2019, 8, 1–6. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Haslam, C.; Tsitsianis, N.; Andersson, T.; Gleadle, P. Accounting for business models: Increasing the visibility of stakeholders. J. Bus. Models 2015, 3, 62–80. [Google Scholar]

- Breuer, H.; Lüdeke-Freund, F. Values-based network and business model innovation. Int. J. Innov. Manag. 2017, 21, 1750028. [Google Scholar] [CrossRef]

- Dentoni, D.; Bitzer, V.; Pascucci, S. Cross-sector partnerships and the co-creation of dynamic capabilities for stakeholder orientation. J. Bus. Ethics 2016, 135, 35–53. [Google Scholar] [CrossRef]

- Vargo, S.L.; Lusch, R.F. Service-dominant logic: Continuing the evolution. J. Acad. Mark. Sci. 2008, 36, 1–10. [Google Scholar] [CrossRef]

- Cachon, G.P. Supply Chain Coordination with Contracts. Handb. Oper. Res. Manag. Sci. 2003, 11, 227–339. [Google Scholar]

- Anni-Kaisa, K.; Katrina, L. The Underlying Potential of Supply Management in Value Creation. J. Purch. Supply Manag. 2012, 18, 68–75. [Google Scholar]

- FitzPatrick, M.; Varey, R.J.; Grönroos, C.; Davey, J. Relationality in the service logic of value creation. J. Serv. Mark. 2015, 29, 463–471. [Google Scholar] [CrossRef]

- Yngfalk, F. ‘It’s not us, it’s them!’—Rethinking value co-creation among multiple actors. J. Mark. Manag. 2013, 29, 1163–1181. [Google Scholar] [CrossRef]

- Lei, M.; Liu, H.; Deng, H.; Huang, T.; Leong, G.K. Demand Information Sharing and Channel Choice in A Dual-channel Supply Chain with Multiple Retailers. Int. J. Prod. Res. 2014, 52, 6792–6818. [Google Scholar] [CrossRef]

- Mukhopadhyay, S.K.; Yao, D.Q.; Yue, X. Information Sharing of Value-adding Retailer in A Mixed Channel Hi-tech Supply Chain. J. Bus. Res. 2008, 61, 950–958. [Google Scholar] [CrossRef]

- D’Aspremont, C.; Jacquemin, A. Cooperative and Noncooperative R&D in Duopoly with Spillovers: Erratum. Am. Econ. Rev. 1990, 80, 641–642. [Google Scholar]

- Kamien, M.I.; Zang, M.I. Research Joint Ventures and R&D Cartels. Am. Econ. Rev. 1992, 82, 1293–1306. [Google Scholar]

- Luo, Z.; Chen, X.; Wang, X. The role of co-opetition in low carbon manufacturing. Eur. J. Oper. Res. 2016, 253, 392–403. [Google Scholar] [CrossRef]

- Gnyawali, D.R.; Park, B.R. Co-opetition Between Giants: Collaboration with Competitors for Technological Innovatio. Res. Policy 2011, 40, 650–663. [Google Scholar] [CrossRef]

- Yim, C.K.; Chan, K.W.; Lam, S.S.K. Do Customers and Employees Enjoy Service Participation? Synergistic Ef. J. Mark. 2012, 76, 121–140. [Google Scholar] [CrossRef]

- Xie, X.; Tsai, N.; Xu, S.; Zhang, B. Does customer co-creation value lead to electronic word-of-mouth? An empirical study on the short-video platform industry. Soc. Sci. J. 2019, 56, 401–416. [Google Scholar] [CrossRef]

- Lusch, R.F.; Vargo, S.L.; O’Brien, M. Competing through service: Insights from service-dominant logic. J. Retail. 2007, 83, 5–18. [Google Scholar] [CrossRef]

- Payne, A.F.; Storbacka, K.; Frow, P. Managing the co-creation of value. J. Acad. Mark. Sci. 2008, 36, 83–96. [Google Scholar] [CrossRef]

- Merz, M.A.; Zarantonello, L.; Grappi, S. How valuable are your customers in the brand value co-creation process? The development of a Customer Co-Creation Value (CCCV) scale. J. Bus. Res. 2018, 82, 79–89. [Google Scholar] [CrossRef]

- Navarro, S.; Llinares, C.; Garzon, D. Exploring the relationship between co-creation and satisfaction using qca. J. Bus. Res. 2016, 69, 1336–1339. [Google Scholar] [CrossRef]

- Franke, N.; Schreier, M. Why Customers Value Self-Designed Products: The Importance of Process Effort and Enjoyment. J. Prod. Innov. Manag. 2010, 27, 1020–1031. [Google Scholar] [CrossRef]

- Glassman, M.; Mcafee, R.B. Enthusiasm: The missing link in leadership. Sam Adv. Manag. J. 1990, 55, 4–6. [Google Scholar]

- Zhang, M.; Guo, L.; Hu, M.; Liu, W. Influence of customer engagement with company social networks on stickiness: Mediating effect of customer value creation. Int. J. Inf. Manag. 2017, 37, 229–240. [Google Scholar] [CrossRef]

- Tuli, K.R.; Kohli, A.K.; Bharadwaj, S.G. Rethinking Customer Solutions: From Product Bundles to Relational processes. J. Mark. 2007, 71, 1–17. [Google Scholar] [CrossRef]

- Kim, H.-S.; Kim, Y.-G. A CRM performance measurement framework: Its development process and application. Ind. Mark. Manag. 2007, 38, 477–489. [Google Scholar] [CrossRef]

- Butler, B.; Batt, P.J. Re-assessing value (co)-creation and cooperative advantage in international networks. Ind. Mark. Manag. 2014, 43, 538–542. [Google Scholar] [CrossRef]

- Kowalkowski, C.; Witell, L.; Gustafsson, A. Any way goes: Identifying value constellations for service infusion in SMEs. Ind. Mark. Manag. 2012, 42, 18–30. [Google Scholar] [CrossRef]

- Gummesson, E.; Nenonen, S.; Storbacka, K. Business model design: Conceptualizing networked value co-creation. Int. J. Qual. Serv. Sci. 2010, 2, 43–59. [Google Scholar]

- Ulaga, W.; Reinartz, W. Hybrid Offerings: How Manufacturing Firms Combine Goods and Services Successfully. J. Mark. A Q. Publ. Am. Mark. Assoc. 2011, 75, 5–23. [Google Scholar] [CrossRef]

- Zhu, Q.; Geng, Y.; Lai, K. Circular economy practices among Chinese manufacturers varying in environmental-oriented supply chain cooperation and the performance implications. Environ. Manag. 2010, 91, 1324–1331. [Google Scholar] [CrossRef]

- Green, K.W.; Zelbst, P.J.; Bhadauria, V.S.; Meacham, J. Do environmental collaboration and monitoring enhance organizational performance? Ind. Manag. Data Syst. 2012, 112, 186–205. [Google Scholar] [CrossRef]

- Ghosh, D.; Shah, J. A comparative analysis of greening policies across supply chain structures. Prod. Econ. 2012, 135, 568–583. [Google Scholar] [CrossRef]

- Grekova, K.; Calantone, R.J.; Bremmers, H.J.; Trienekens, J.H.; Omta, S.W.F. How environmental collaboration with suppliers and customers influences firm performance: Evidence from Dutch food and beverage processors. Clean. Prod. 2016, 112, 1861–1871. [Google Scholar] [CrossRef]

- Xu, X.; He, P.; Xu, H.; Zhang, Q. Supply chain coordination with green technology under cap-and-trade regulation. Int. J. Prod. Econ. 2017, 183, 433–442. [Google Scholar] [CrossRef]

- Hou, Y.; Zhang, S.; Hong, J. Study on the selection of enterprise suppliers under the green strategic alliance. China Bus. Theory 2017, 17, 73–75. [Google Scholar]

- Qiu, E. Research on Enterprise Green Management System; Harbin Engineering University: Harbin, China, 2006. [Google Scholar]

- Wang, M.; Gao, Q.; Liang, D. Stackelberg game model between retailers and two competitive manufacturers. Mod. Bus. 2014, 23, 17–18. [Google Scholar]

- Lee, H.L.; Padmanabhan, V.; Whang, S. Information distortion in a supply chain. Bullwhip Eff. Manag. Sci. 1997, 43, 546–558. [Google Scholar]

- Kang, Y.; Chen, J.; Tong, S. Service strategy and service performance: The regulatory effect of value co-creation. Soft Sci. 2016, 30, 103–107. [Google Scholar]

- Holweg, M.; Pil, F.K. Theoretical perspectives on the co-ordination of supply chains. J. Oper. Manag. 2008, 26, 389–406. [Google Scholar] [CrossRef]

- Liu, H.; Zhang, X. Influence of governance mechanism of online retail platform on opportunistic behavior of sellers-Taking perceived uncertainty as moderating variable. Bus. Econ. Manag. 2017, 04, 17–28. [Google Scholar]

- Zhu, Q.; Sun, Y.; Zhou, L. Research on the relationship between platform empowerment, value co-creation and enterprise performance. Sci. Res. 2019, 37, 2026–2033. [Google Scholar]

- Shi, H. Research on the Impact of Value Co-Creation among Firms on Innovation Cooperation Based on Resource Theory; Harbin University of Technology: Harbin, China, 2012. [Google Scholar]

- Roper, S.; Du, J.; Love, J.H. Modelling the innovation value chain. Res. Policy 2008, 37, 961–977. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why Companies Go Green: A Model of Ecological Responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar]

- Zhu, Q.H. An inter-sectoral comparison of GSC management in China: Drivers and practices. J. Clean. Prod. 2006, 14, 472–486. [Google Scholar] [CrossRef]

- Wu, F.; Gu, F.; Zhang, J. Factors influencing financial performance of Listed Companies. J. Syst. Manag. 2013, 022, 715–719. [Google Scholar]

- Jiang, Q.; Tan, Q. Research on the configuration path of enterprise innovation performance based on fuzzy qualitative analysis. China Sci. Technol. Forum 2019, 08, 67–76. [Google Scholar]

- Yang, J. The determinants of supply chain alliance performance: An empirical study. Int. J. Prod. Res. 2009, 47, 1055–1069. [Google Scholar] [CrossRef]

- Carter, C.R.; Carter, J.R. Interorganizational determinants of environmental purchasing: Initial evidence from the consumer products industries. Decis. Sci. 1998, 29, 659–685. [Google Scholar] [CrossRef]

- Ehrgott, M.; Reimann, F.; Kaufmann, L.; Carter, C.R. Social sustainability in selecting emerging economy suppliers. J. Bus. Ethics 2011, 98, 99–119. [Google Scholar] [CrossRef]

- Lee, J.N. The impact of knowledge sharing, organizational capability and partnership quality on IS outsourcing success. Inf. Manag. 2001, 38, 323–335. [Google Scholar] [CrossRef]

- Ngo, L.V.; O’Cass, A. Creating value offerings via operant resource-based capabilities. Ind. Mark. Manag. 2009, 38, 45–59. [Google Scholar] [CrossRef]

- Ren, S.J.; Hu, C.; Ngai, E.W.T.; Zhou, M. An empirical analysis of inter-organisational value co-creation in a supply chain: A process perspective. Prod. Plan. Control 2015, 26, 969–980. [Google Scholar] [CrossRef]

- Flynn, B.B.; Huo, B.; Zhao, X. The impact of supply chain integration on performance: A contingency and configuration approach. J. Oper. Manag. 2010, 28, 58–71. [Google Scholar] [CrossRef]

- Schruijer, S.G.; Curseu, P.L. Looking at the gap between social psychological and psychodynamic perspectives on group dynamics historically. J. Organ. Chang. Manag. 2014, 27, 232–245. [Google Scholar] [CrossRef]

| Characteristics | Percentage (%) |

|---|---|

| Respondent’s Position | |

| CEO | 12 |

| Middle manager | 42 |

| General staff | 46 |

| Age of the Firm (Number of Years) | |

| Less than 5 | 25 |

| 5–10 | 34 |

| 11–15 | 13 |

| 16–20 | 4 |

| More than 20 | 24 |

| Annual Revenue (Million RMB Yuan) | |

| Less than 50 | 23 |

| 50–100 | 27 |

| 100–200 | 10 |

| 200–2000 | 7 |

| More than 2000 | 33 |

| Ownership of the Firm | |

| State-owned | 9 |

| Local private | 58 |

| Foreign | 32 |

| Joint venture | 1 |

| Environmental Management System Certification | |

| Yes | 66 |

| No | 34 |

| Social Responsibility Management System Certification | |

| Yes | 54 |

| No | 46 |

| Quality Management System Certification | |

| Yes | 75 |

| No | 26 |

| Train Employees on Environmental Management | |

| Never | 16 |

| Sometimes | 58 |

| Always | 26 |

| Total Quality Management | |

| Yes | 75 |

| No | 25 |

| Item | Factor 1 | Factor 2 | Factor 3 | Factor 4 | Factor 5 | Factor 6 | Factor 7 | Factor 8 | Factor 9 |

|---|---|---|---|---|---|---|---|---|---|

| GS1 | 0.812 | - | - | - | - | - | - | - | - |

| GS2 | 0.764 | - | - | - | - | - | - | - | - |

| GS3 | 0.695 | - | - | - | - | - | - | - | - |

| GS4 | 0.703 | - | - | - | - | - | - | - | - |

| GS5 | 0.710 | - | - | - | - | - | - | - | - |

| GS6 | 0.693 | - | - | - | - | - | - | - | - |

| VCS1 | - | 0.785 | - | - | - | - | - | - | - |

| VCS2 | - | 0.778 | - | - | - | - | - | - | - |

| VCS3 | - | 0.790 | - | - | - | - | - | - | - |

| VCS4 | - | 0.811 | - | - | - | - | - | - | - |

| VCC1 | - | - | 0.828 | - | - | - | - | - | - |

| VCC2 | - | - | 0.813 | - | - | - | - | - | - |

| VCC3 | - | - | 0.830 | - | - | - | - | - | - |

| VCC4 | - | - | 0.802 | - | - | - | - | - | - |

| VCR1 | - | - | - | 0.793 | - | - | - | - | - |

| VCR2 | - | - | - | 0.727 | - | - | - | - | - |

| VCR3 | - | - | - | 0.847 | - | - | - | - | - |

| VCR4 | - | - | - | 0.835 | - | - | - | - | - |

| LP1 | - | - | - | - | 0.837 | - | - | - | - |

| LP2 | - | - | - | - | 0.809 | - | - | - | - |

| LP3 | - | - | - | - | 0.812 | - | - | - | - |

| LP4 | - | - | - | - | 0.811 | - | - | - | - |

| LP5 | - | - | - | - | 0.849 | - | - | - | - |

| LP6 | - | - | - | - | 0.811 | - | - | - | - |

| LP7 | - | - | - | - | 0.823 | - | - | - | - |

| CP1 | - | - | - | - | 0.806 | - | - | - | - |

| CP2 | - | - | - | - | 0.792 | - | - | - | - |

| CP3 | - | - | - | - | 0.763 | - | - | - | - |

| CP4 | - | - | - | - | 0.806 | - | - | - | - |

| CP5 | - | - | - | - | 0.769 | - | - | - | - |

| CmP1 | - | - | - | - | 0.857 | - | - | - | - |

| CmP2 | - | - | - | - | 0.878 | - | - | - | - |

| CmP3 | - | - | - | - | 0.860 | - | - | - | - |

| SP1 | - | - | - | - | 0.762 | - | - | - | - |

| SP2 | - | - | - | - | 0.789 | - | - | - | - |

| SP3 | - | - | - | - | 0.805 | - | - | - | - |

| SP4 | - | - | - | - | 0.803 | - | - | - | - |

| SP5 | - | - | - | - | 0.820 | - | - | - | - |

| MA1 | - | - | - | - | - | 0.821 | - | - | - |

| MA2 | - | - | - | - | - | 0.787 | - | - | - |

| MA3 | - | - | - | - | - | 0.814 | - | - | - |

| MA4 | - | - | - | - | - | 0.773 | - | - | - |

| SCR1 | - | - | - | - | - | 0.874 | - | - | - |

| SCR2 | - | - | - | - | - | 0.860 | - | - | - |

| SCR3 | - | - | - | - | - | 0.894 | - | - | - |

| SCR4 | - | - | - | - | - | 0.845 | - | - | - |

| SCR5 | - | - | - | - | - | 0.876 | - | - | - |

| SCR6 | - | - | - | - | - | 0.856 | - | - | - |

| DC1 | - | - | - | - | - | 0.863 | - | - | - |

| DC2 | - | - | - | - | - | 0.815 | - | - | - |

| DC3 | - | - | - | - | - | 0.830 | - | - | - |

| DC4 | - | - | - | - | - | 0.843 | - | - | - |

| DC5 | - | - | - | - | - | 0.850 | - | - | - |

| DC6 | - | - | - | - | - | 0.849 | - | - | - |

| DC7 | - | - | - | - | - | 0.855 | - | - | - |

| DC8 | - | - | - | - | - | 0.836 | - | - | - |

| OP1 | - | - | - | - | - | - | 0.881 | - | - |

| OP2 | - | - | - | - | - | - | 0.849 | - | - |

| OP3 | - | - | - | - | - | - | 0.838 | - | - |

| FP1 | - | - | - | - | - | - | - | 0.896 | - |

| FP2 | - | - | - | - | - | - | - | 0.888 | - |

| FP3 | - | - | - | - | - | - | - | 0.841 | - |

| FP4 | - | - | - | - | - | - | - | 0.855 | - |

| FP5 | - | - | - | - | - | - | - | 0.867 | - |

| IP1 | - | - | - | - | - | - | - | - | 0.862 |

| IP2 | - | - | - | - | - | - | - | - | 0.825 |

| IP3 | - | - | - | - | - | - | - | - | 0.823 |

| IP4 | - | - | - | - | - | - | - | - | 0.844 |

| IP5 | - | - | - | - | - | - | - | - | 0.915 |

| IP6 | - | - | - | - | - | - | - | - | 0.869 |

| IP7 | - | - | - | - | - | - | - | - | 0.840 |

| Mean | 4.250 | 4.202 | 3.940 | 4.178 | 4.079 | 4.010 | 4.140 | 3.953 | 4.075 |

| S.D. | 0.844 | 0.831 | 0.955 | 0.849 | 0.873 | 0.891 | 0.815 | 0.941 | 0.863 |

| Cumulative Percent of Variance | 0.602 | 0.643 | 0.677 | 0.722 | 0.750 | 0.775 | 0.800 | 0.812 | 0.827 |

| Cronbach’s α | 0.917 | 0.819 | 0.832 | 0.845 | 0.919 | 0.951 | 0.850 | 0.889 | 0.909 |

| Factor | Item | Standardized Factor Loading | t-Value | R2 |

|---|---|---|---|---|

| Factor1: Green strategy (GS) | GS1 | 0.869 | - | 0.594 |

| GS2 | 0.875 | 8.319 | 0.602 | |

| GS3 | 0.803 | 8.407 | 0.584 | |

| GS4 | 0.876 | 10.325 | 0.630 | |

| GS5 | 0.865 | 11.337 | 0.624 | |

| GS6 | 0.893 | 16.204 | 0.580 | |

| Factor 2: Value Co-creation with supplier (VCS) | VCS1 | 0.890 | - | 0.517 |

| VCS2 | 0.862 | 15.089 | 0.720 | |

| VCS3 | 0.819 | 13.730 | 0.690 | |

| VCS4 | 0.849 | 18.427 | 0.823 | |

| Factor 3: Value co-creation with competitor (VCC) | VCC1 | 0.831 | - | 0.785 |

| VCC2 | 0.907 | 16.082 | 0.723 | |

| VCC3 | 0.886 | 17.656 | 0.779 | |

| VCC4 | 0.850 | 21.299 | 0.712 | |

| Factor 4: Value co-creation with retailer (VCR) | VCR1 | 0.883 | - | 0.747 |

| VCR2 | 0.844 | 8.692 | 0.596 | |

| VCR3 | 0.864 | 8.670 | 0.598 | |

| VCR4 | 0.804 | 9.407 | 0.548 | |

| Factor 5: External environment pressure (EEP) | LE1 | 0.806 | - | 0.519 |

| LE2 | 0.874 | 10.873 | 0.566 | |

| LE3 | 0.865 | 11.940 | 0.575 | |

| LE4 | 0.882 | 10.684 | 0.581 | |

| LE5 | 0.889 | 10.467 | 0.843 | |

| LE6 | 0.893 | 10.556 | 0.849 | |

| LE7 | 0.918 | 8.769 | 0.701 | |

| CE1 | 0.921 | 8.692 | 0.940 | |

| CE2 | 0.837 | 8.670 | 0.898 | |

| CE3 | 0.970 | 9.407 | 0.917 | |

| CE4 | 0.948 | 9.949 | 0.787 | |

| CE5 | 0.957 | 10.873 | 0.716 | |

| IE1 | 0.887 | 9.548 | 0.832 | |

| IE2 | 0.846 | 8.470 | 0.765 | |

| IE3 | 0.912 | 8.484 | 0.946 | |

| PS1 | 0.875 | 8.687 | 0.892 | |

| PS2 | 0.973 | 30.232 | 0.838 | |

| PS3 | 0.944 | 9.465 | 0.740 | |

| PS4 | 0.916 | 9.653 | 0.710 | |

| PS5 | 0.815 | 9.428 | 0.858 | |

| Factor 6: Internal environment support (IES) | MA1 | 0.824 | - | 0.782 |

| MA2 | 0.815 | 19.425 | 0.536 | |

| MA3 | 0.899 | 17.367 | 0.527 | |

| MA4 | 0.858 | 18.739 | 0.525 | |

| SCR1 | 0.819 | 20.846 | 0.516 | |

| SCR2 | 0.898 | 17.436 | 0.607 | |

| SCR3 | 0.803 | 16.239 | 0.572 | |

| SCR4 | 0.827 | 13.285 | 0.755 | |

| SCR5 | 0.860 | 12.459 | 0.562 | |

| SCR6 | 0.843 | 19.048 | 0.584 | |

| DC1 | 0.926 | 18.475 | 0.567 | |

| DC2 | 0.884 | 22.532 | 0.572 | |

| DC3 | 0.661 | 20.604 | 0.858 | |

| DC4 | 0.654 | 21.204 | 0.892 | |

| DC5 | 0.652 | 20.791 | 0.736 | |

| DC6 | 0.818 | 22.841 | 0.965 | |

| DC7 | 0.879 | 20.873 | 0.890 | |

| DC8 | 0.856 | 19.023 | 0.901 | |

| Factor 7: Operational performance (OP) | OP1 | 0.869 | - | 0.754 |

| OP2 | 0.880 | 8.697 | 0.722 | |

| OP3 | 0.982 | 9.732 | 0.830 | |

| Factor 8: Financial performance (FP) | FP1 | 0.943 | - | 0.772 |

| FP2 | 0.949 | 20.620 | 0.961 | |

| FP3 | 0.868 | 21.703 | 0.871 | |

| FP4 | 0.849 | 24.339 | 0.812 | |

| FP5 | 0.911 | 21.661 | 0.578 | |

| Factor 9: Innovative performance (IP) | IP1 | 0.879 | - | 0.524 |

| IP2 | 0.980 | 30.314 | 0.511 | |

| IP3 | 0.933 | 27.233 | 0.639 | |

| IP4 | 0.901 | 22.583 | 0.575 | |

| IP5 | 0.843 | 21.490 | 0.670 | |

| IP6 | 0.926 | 21.963 | 0.637 | |

| IP7 | 0.884 | 18.806 | 0.594 |

| AVE | GS | VCS | VCC | VCR | EEP | ITE | OP | FP | IP | |

|---|---|---|---|---|---|---|---|---|---|---|

| GS | 0.625 | - | - | - | - | - | - | - | - | - |

| VCS | 0.661 | 0.004 | - | - | - | - | - | - | - | - |

| VCC | 0.725 | 0.021 | 0.021 | - | - | - | - | - | - | - |

| VCR | 0.682 | 0.003 | 0.152 | 0.160 | - | - | - | - | - | - |

| EEP | 0.816 | 0.038 | 0.199 | 0.256 | 0.065 | - | - | - | - | - |

| IES | 0.809 | 0.010 | 0.002 | 0.011 | 0.242 | 0.087 | - | - | - | - |

| OP | 0.811 | 0.025 | 0.116 | 0.106 | 0.007 | 0.039 | 0.145 | - | - | - |

| FP | 0.719 | 0.087 | 0.179 | 0.198 | 0.076 | 0.059 | 0.096 | 0.310 | - | - |

| IP | 0.842 | 0.203 | 0.214 | 0.236 | 0.157 | 0.095 | 0.208 | 0.178 | - | - |

| Model | VCS | VCC | VCR | OP | FP | IP | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | |

| Independent Variable | |||||||||||||||

| GS | 0.832 a | 0.355 b | 0.870 a | 0.150 | 0.778 a | 0.132 | - | - | - | - | - | - | - | - | - |

| VCS | - | - | - | - | - | - | - | 0.125 a | 0.849 | - | 0.177 | 1.168 | - | 0.189 | 1.650 c |

| VCC | - | - | - | - | - | - | - | 0.173 a | 0.356 | - | 0.520 a | 1.962 b | - | 0.321 a | 1.086 c |

| VCR | - | - | - | - | - | - | - | 0.187 a | 0.367 | - | 0.231 c | 0.773 | - | 0.368 a | 0.643 |

| Moderator Variable | |||||||||||||||

| EEP ∗ GS | - | 0.052 c | - | 0.149 c | 0.024 c | - | - | - | - | - | - | ||||

| IES ∗ GS | - | 0.023 | - | 0.011 | - | 0.079 | - | - | - | - | - | - | |||

| EEP ∗ VCS | - | - | - | - | - | - | - | 0.509 | - | - | 0.146 | 1.046 b | |||

| EEP ∗ VCC | - | - | - | - | - | - | - | 0.044 | - | - | 0.108 | 0.087 c | |||

| EEP ∗ VCR | - | - | - | - | - | - | - | 0.378 | - | - | 0.055 | 0.920 b | |||

| IES ∗ VCS | - | - | - | - | - | - | - | 0.274 | - | - | 0.200 c | 0.582 b | |||

| IES ∗ VCC | - | - | - | - | - | - | - | 0.284 | - | - | 0.333 c | 0.169 c | |||

| IES ∗ VCR | - | - | - | - | - | - | - | 0.569 | - | - | 0.165 c | 0.825 b | |||

| Control Variable | |||||||||||||||

| firm age | - | - | - | - | - | - | 0.126 | 0.024 | 0.048 | 0.174 c | 0.055 c | 0.081 c | 0.117 | 0.011 | 0.034 |

| firm size | - | - | - | - | - | - | 0.103 | 0.046 | 0.062 | 0.088 | 0.026 | 0.042 | 0.085 | 0.026 | 0.056 |

| firm ownership | - | - | - | - | - | - | 0.084 | 0.092 | 0.123 | 0.070 | 0.076 | 0.078 | 0.028 | 0.035 | 0.104 |

| Constant | 0.686 a | 1.386 a | 0.243 a | 1.741 a | 0.874 a | 1.819 a | 4.359 a | 0.454 a | 0.957 a | 0.052 | 0.209 | 0.372 | 0.575 b | 0.182 | 0.518 |

| Adjusted R2 | 0.696 | 0.744 | 0.539 | 0.692 | 0.581 | 0.689 | 0.737 | 0.704 | 0.776 | 0.552 | 0.711 | 0.817 | 0.528 | 0.717 | 0.812 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shi, X.; Li, G.; Dong, C.; Yang, Y. Value Co-Creation Behavior in Green Supply Chains: An Empirical Study. Energies 2020, 13, 3902. https://doi.org/10.3390/en13153902

Shi X, Li G, Dong C, Yang Y. Value Co-Creation Behavior in Green Supply Chains: An Empirical Study. Energies. 2020; 13(15):3902. https://doi.org/10.3390/en13153902

Chicago/Turabian StyleShi, Xianliang, Genzhu Li, Ciwei Dong, and Yefei Yang. 2020. "Value Co-Creation Behavior in Green Supply Chains: An Empirical Study" Energies 13, no. 15: 3902. https://doi.org/10.3390/en13153902

APA StyleShi, X., Li, G., Dong, C., & Yang, Y. (2020). Value Co-Creation Behavior in Green Supply Chains: An Empirical Study. Energies, 13(15), 3902. https://doi.org/10.3390/en13153902