Green Production Planning and Control for the Textile Industry by Using Mathematical Programming and Industry 4.0 Techniques

Abstract

1. Introduction

2. Research Background

2.1. Brief of Industry 4.0

2.2. The Influence of Industry 4.0 and Green Production on the Textile Industry

3. Green Production Planning Model under ABC by Using Mathematical Programming

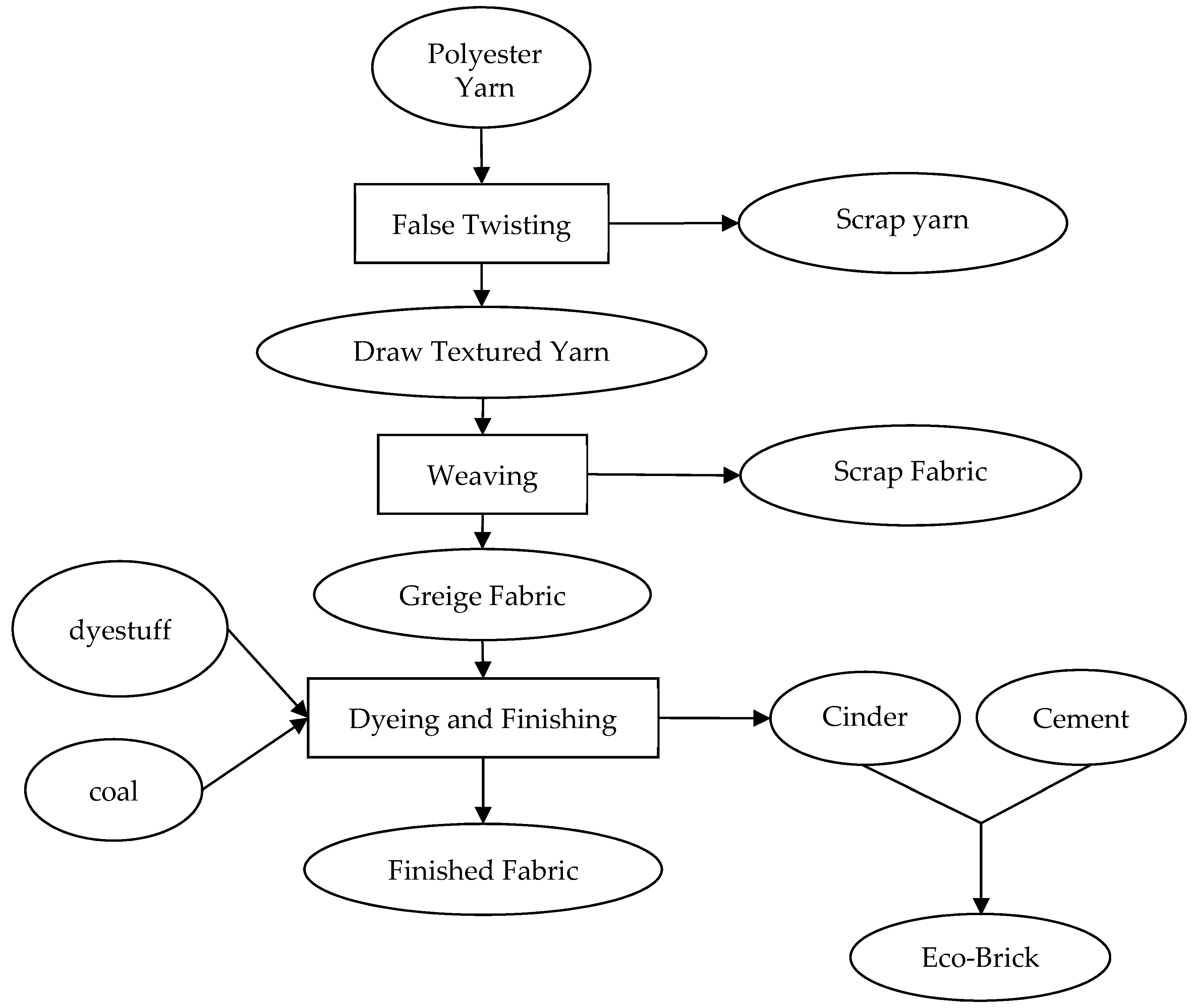

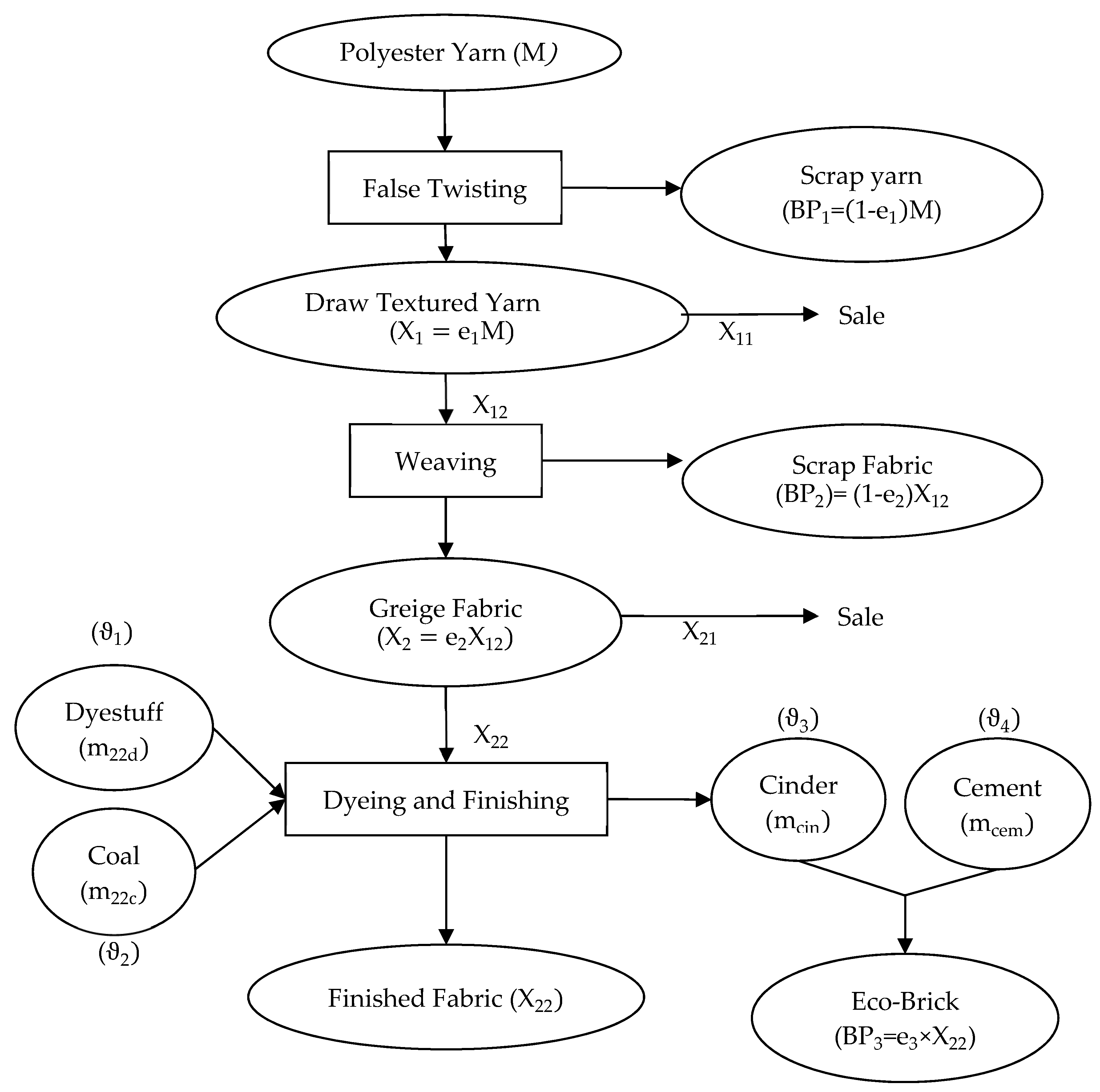

3.1. A Production Process for a Typical Textile Company

3.2. Assumptions

3.3. Objective Function

| Maximize π = Total Revenue of main product + Revenue of by product − Total material cost − Total direct labor cost − Carbon tax − Energy recycling cost saving − Total other fixed cost |

| The unit selling price of i product | |

| The selling quantities of drawn textured yarn | |

| The future processing quantities of drawn textured yarn | |

| The selling quantities of greige fabric | |

| The selling quantities of finished fabric | |

| The unit selling price of i by-product | |

| The input-output coefficient from POY to drawn textured yarn and scrap yarn | |

| The input-output coefficient from textured yarn to greige fabric and scrap fabric | |

| The input-output coefficient of Eco-Brick | |

| , , , | The unit material cost of , , and |

| , | The unit recycle saving cost of heat and water |

| The material quantities of POY | |

| The material quantities of dye | |

| The material quantities of cinder | |

| The material quantities of cement | |

| The direct labor cost of available normal hours | |

| Special ordered sets of type 1 (SOS1) of 0/1 variables, where only one variable will be 1 | |

| The wage rate of the total direct labor hours in overtime work situations | |

| The overtime working hours (extend working hours to 2 hours per worker) | |

| The limit of the normal direct labor hour | |

| Special ordered sets of type 1 (SOS1) of 0/1 variables, where only one variable will be 1 | |

| The carbon tax rate of available normal CO2 emission quantities | |

| The carbon tax rate that produces excessive CO2 emission quantities | |

| The total CO2 emission quantities in normal production | |

| The total CO2 emission quantities that produces excessive CO2 emission quantities | |

| No charge for CO2 emission quantities | |

| , | Green energy recycling saving quantities of heat and water |

| Fixed cost |

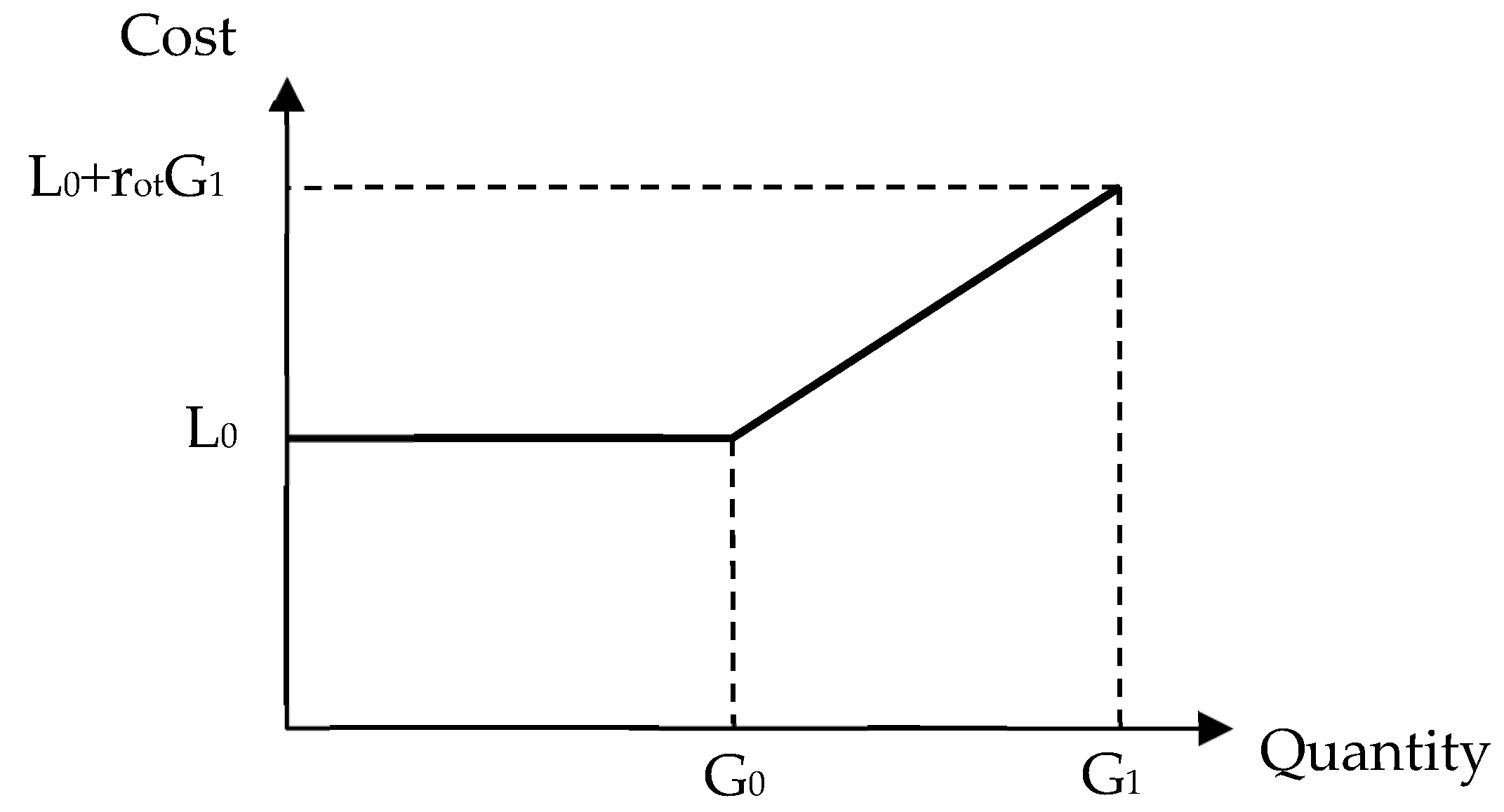

3.4. Unit-Level Direct Labor Cost Function

| The direct labor hours required by | |

| The direct labor hours required by | |

| The direct labor hours required by | |

| The direct labor hours of the handling of each batch-level activity from start to finish | |

| The product of shipping from start to finish in terms of quantities needed at each batch-level | |

| Each batch of direct labor hours of setup | |

| The setup product in terms of quantities of each batch-level | |

| The total direct labor hours in the normal working hour | |

| The overtime working hours (extend working hours to 2 h per worker) | |

| G0 | The limit of the normal direct labor hour |

| G1 | The limit of the overtime work direct labor hour |

| Special ordered sets of type 1 (SOS1) of 0/1 variables. |

3.5. Batch-Level Activity Cost Function for Material Handling and Setup Activities

| The quantity of handling of each batch-level activity from start to finish | |

| The quantity of setup of batch-level activity |

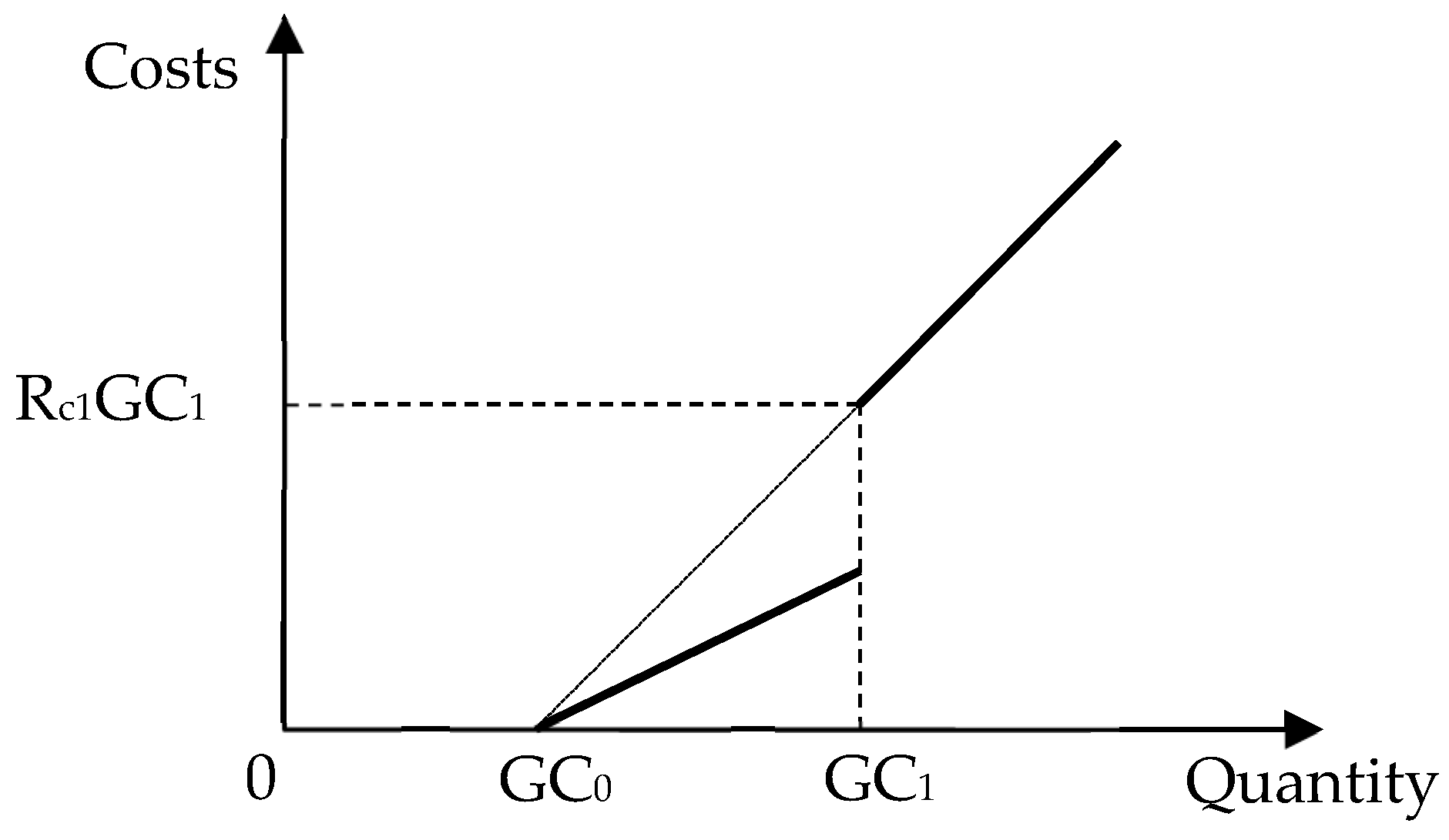

3.6. Carbon Tax Function

| The total CO2 emission quantities in the dyeing and finishing process | |

| The total CO2 emission quantities where there is no charge in standard range | |

| The total CO2 emission quantities in normal production | |

| The total CO2 emission quantities that produces excessive CO2 emission quantities | |

| No charge for CO2 emission quantities | |

| Carbon tax cost of normal capacity | |

| Carbon tax cost for over emission capacity | |

| Special ordered sets of type 1 (SOS1). The summation of 0/1 variables is 1 |

3.7. Energy Recycling

| The relation coefficient between energy recycling of heat and | |

| The relation coefficient between energy recycling of water and |

3.8. Input-Output Relationship

| The quantities of i byproduct | |

| The relation coefficient between and | |

| The relation coefficient between and | |

| The relation coefficient between and | |

| The relation coefficient between and |

3.9. Other Sale and Production Constraints

| the resources of machine hours of false twisting | |

| the resources of machine hours of weaving | |

| the resources of machine hours of dyeing and finishing | |

| The limited machine hours of false twisting | |

| The limited machine hours of weaving | |

| The limited machine hours of dyeing and finishing |

4. Illustrative Case

4.1. Illustrative Data and Optimal Decision Analysis

4.2. Optimal Solution Analysis

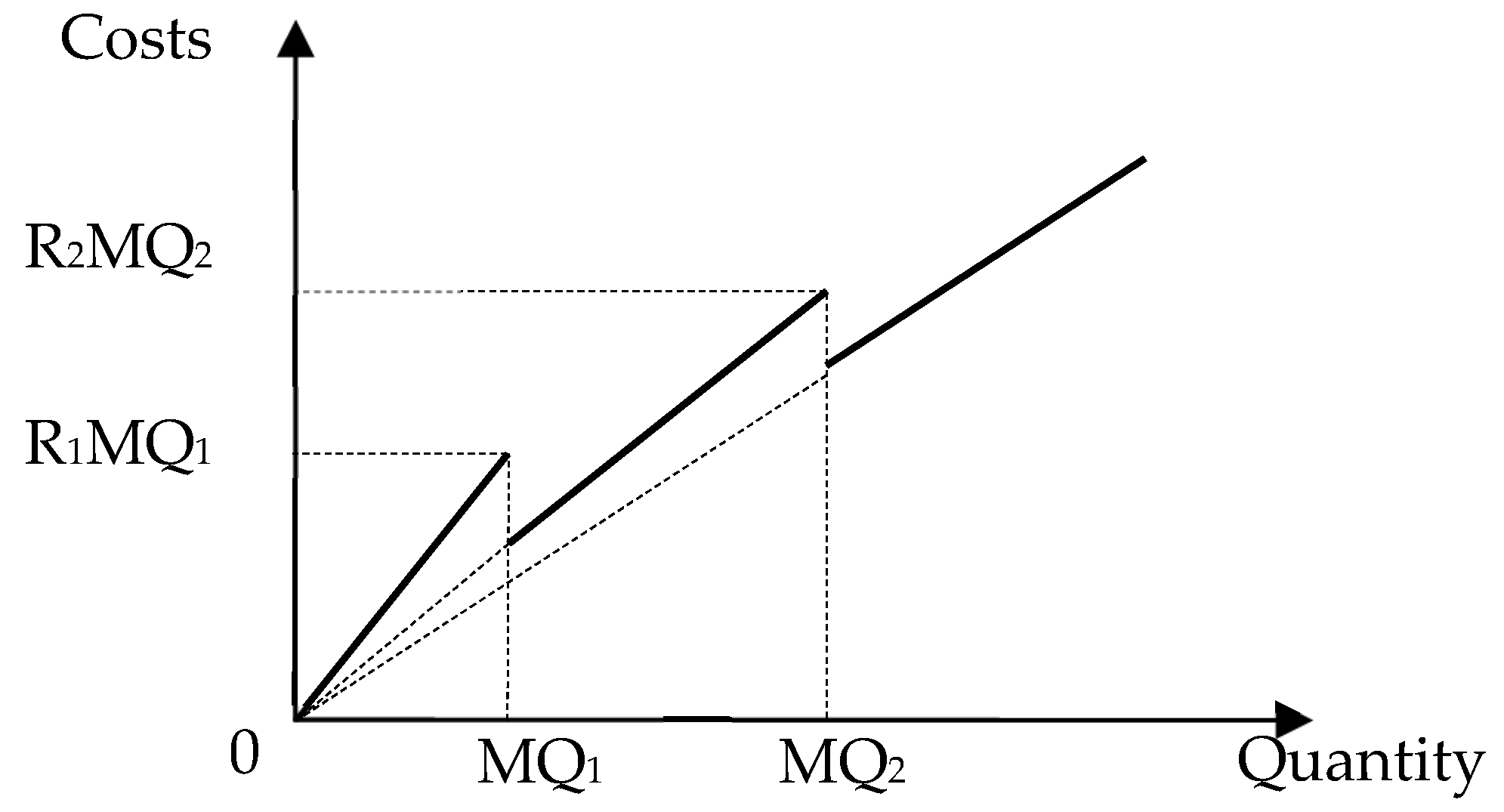

4.3. Sensitivity Analysis of the Quantity Discount of Direct Material

| The original price of the amount of material | |

| The amount of material in the first gradation of the price discount | |

| The amount of material in the second gradation of the price discount | |

| The original price of the maximum amount of material | |

| The maximum amount of material in the first gradation of the price discount | |

| Special ordered sets of type 1 (SOS1). The summation of 0/1 variables is 1. |

5. Manufacturing Execution System for Production Control under Industry 4.0 in the Textile Industry

5.1. Status Monitoring and Predictive Maintenance

5.2. Work-in-Process Tracking

5.3. Quality Control

6. Discussion

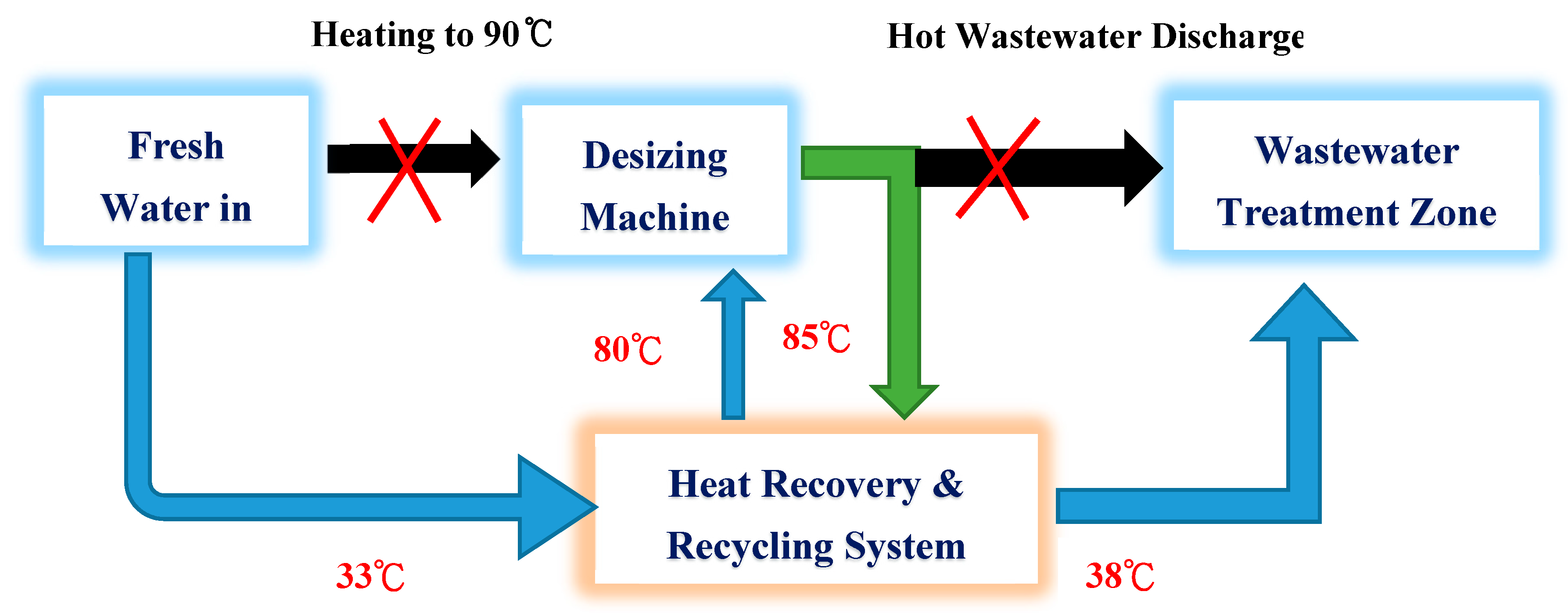

6.1. Energy Saving Method for the Case Company

6.2. From Waste Cinder to Eco-Brick

6.3. Labor Skills and Job Losses Due to the Introduction of Industry 4.0

7. Conclusions

Acknowledgments

Conflicts of Interest

References

- Choudhury, A.R. Environmental impacts of the textile industry and its assessment through life cycle assessment. In Roadmap to Sustainable Textiles and Clothing; Springer: Berlin, Germany, 2014; pp. 1–39. [Google Scholar]

- Bullon, J.; González Arrieta, A.; Hernández Encinas, A.; Queiruga Dios, A. Manufacturing processes in the textile industry. Expert Systems for fabrics production. Adv. Distrib. Comput. Articial Intell. J. 2017, 6, 41–50. [Google Scholar]

- Brettel, M.; Friederichsen, N.; Keller, M.; Rosenberg, M. How virtualization, decentralization and network building change the manufacturing landscape: An industry 4.0 perspective. Int. J. Mech. Ind. Sci. Eng. 2014, 8, 37–44. [Google Scholar]

- Rüßmann, M.; Lorenz, M.; Gerbert, P.; Waldner, M.; Justus, J.; Engel, P.; Harnisch, M. Industry 4.0: The Future of Productivity and Growth in Manufacturing Industries; Boston Consulting Group: Boston, MA, USA, 2015. [Google Scholar]

- Lee, J.; Kao, H.-A.; Yang, S. Service innovation and smart analytics for industry 4.0 and big data environment. Procedia Cirp 2014, 16, 3–8. [Google Scholar] [CrossRef]

- Awad, M.I.; Hassan, N.M. Joint decisions of machining process parameters setting and lot-size determination with environmental and quality cost consideration. J. Manuf. Syst. 2018, 46, 79–92. [Google Scholar] [CrossRef]

- Rojko, A. Industry 4.0 Concept: Background and Overview. Int. J. Inf. Manag. 2017, 11, 77–90. [Google Scholar] [CrossRef]

- Park, S.; Huh, J.-H. Effect of Cooperation on Manufacturing IT Project Development and Test Bed for Successful Industry 4.0 Project: Safety Management for Security. Processes 2018, 6. [Google Scholar] [CrossRef]

- Küsters, D.; Praß, N.; Gloya, Y.-S. Textile up 4.0—Preparing Germany’s Textile Industry for the Digital Future. Procedia Manuf. 2017, 9, 214–221. [Google Scholar] [CrossRef]

- Chen, Z.; Xing, M. Upgrading of textile manufacturing based on Industry 4.0. In Proceedings of the 5th International Conference on Advanced Design and Manufacturing Engineering (ICADME 2015), Shenzhen, China, 19–20 September 2015; pp. 2143–2146. [Google Scholar]

- Dujin, A.; Blanchet, M.; Rinn, T.; Von Thaden, G.; De Thieullo, G. Industry 4.0—The New Industrial Revolution: How Europe Will Succeed; Roland Berger Strategy Consultants: Munich, Germany, 2014. [Google Scholar]

- Jerzembeck, J. Industry 4.0 Potential in Textile Production (Dyeing and Finishing). Melliand Int. 2016, 4, 220–222. [Google Scholar]

- RINA Consulting. Industry 4.0: The New Challenge for the ITALIAN TEXTILE MACHINERY INDUSTRY. Executive Summary, Italian Textile Machinery, 2017. Available online: http://www.acimit.it/DOC/Executive17-Ing.pdf (accessed on 20 July 2018).

- Lee, H.-G.; Huh, J.-H. A Cost-Effective Redundant Digital Excitation Control System and Test Bed Experiment for Safe Power Supply for Process Industry 4.0. Processes 2018, 6. [Google Scholar] [CrossRef]

- Huh, J.-H. Smart Grid Test Bed Using OPNET and Power Line Communication; IGI Global: Hershey, PA, USA, 2017. [Google Scholar]

- Kamal Abd Rahman, I.; Omar, N.; Zainal Abidin, Z. The applications of management accounting techniques in Malaysian companies: An industrial survey. J. Financ. Rep. Account. 2003, 1, 1–12. [Google Scholar] [CrossRef]

- Holmen, J.S. ABC vs. TOC: It’s a matter of time. Strat. Financ. 1995, 76, 37. [Google Scholar]

- Kee, R. Integrating activity-based costing with the theory of constraints to enhance production-related decision-making. Account. Horiz. 1995, 9, 48–61. [Google Scholar]

- Lockhart, J.; Taylor, A. Environmental considerations in product mix decisions using ABC and TOC: As environmental issues increasingly influence corporate performance, they need to be a standard part of management accounting systems. Manag. Account. Q. 2007, 9, 13. [Google Scholar]

- Turney, P.B.B. Common Cents: The ABC Performance Breakthrough—How to Succeed with Activity-Based Costing, Revised ed.; McGraw-Hill: New York, NY, USA, 2005. [Google Scholar]

- Luebbe, R.; Finch, B. Theory of constraints and linear programming: A comparison. Int. J. Prod. Res. 1992, 30, 1471–1478. [Google Scholar] [CrossRef]

- Plenert, G. Optimizing theory of constraints when multiple constrained resources exist. Eur. J. Oper. Res. 1993, 70, 126–133. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Lin, T.-M. Nonlinear multiproduct CVP analysis with 0–1 mixed integer programming. Eng. Costs Prod. Econ. 1990, 20, 81–91. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Lee, K.-C.; Liu, J.-Y.; Lin, H.-L.; Chou, Y.-W.; Lin, S.-J. A mixed activity-based costing decision model for green airline fleet planning under the constraints of the European Union Emissions Trading Scheme. Energy 2012, 39, 218–226. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Lin, S.-J.; Liu, J.-Y.; Lin, W.-R.; Lee, K.-C. Incorporating life cycle assessments into building project decision-making: An energy consumption and CO2 emission perspective. Energy 2011, 36, 3022–3029. [Google Scholar] [CrossRef]

- Jaedicke, R.K. Improving breakeven analysis by linear programming techniques. NAA Bull. 1961, 5–12. [Google Scholar]

- Entezaminia, A.; Heydari, M.; Rahmani, D. A multi-objective model for multi-product multi-site aggregate production planning in a green supply chain: Considering collection and recycling centers. J. Manuf. Syst. 2016, 40, 63–75. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Yang, C.-H.; Chang, J.-C.; Lee, H.-L. An activity-based costing decision model for life cycle assessment in green building projects. Eur. J. Oper. Res. 2014, 238, 607–619. [Google Scholar] [CrossRef]

- Williams, H.P. Model Building in Mathematical Programming; John Wiley & Sons: West Sussex, UK, 2013. [Google Scholar]

- Cohon, J.L. Multiobjective Programming and Planning; Dover Publications: Mineola, NY, USA, 2003. [Google Scholar]

- Hanasusanto, G.A.; Kuhn, D.; Wallace, S.W.; Zymler, S. Distributionally robust multi-item newsvendor problems with multimodal demand distributions. Math. Program. 2015, 152, 1–32. [Google Scholar] [CrossRef]

- Correa, J.; Marchetti-Spaccamela, A.; Matuschke, J.; Stougie, L.; Svensson, O.; Verdugo, V.; Verschae, J. Strong LP formulations for scheduling splittable jobs on unrelated machines. Math. Program. 2015, 154, 305–328. [Google Scholar] [CrossRef]

- Elamvazuthi, I.; Ganesan, T.; Vasant, P.; Webb, J.F. Application of a Fuzzy Programming Technique to Production Planning in the Textile Industry. Int. J. Comput. Sci. Inf. Secur. 2009, 6, 238–243. [Google Scholar]

- Teke, Ç.; Okutkan, C.; Erden, C. Determining the Production Amounts in Textile Industry with Fuzzy Linear Programming. Int. J. Eng. Technol. Res. 2017, 2, 1–6. [Google Scholar]

- Waidner, M.; Kasper, M. Security in industrie 4.0: Challenges and solutions for the fourth industrial revolution. In Proceedings of the 2016 Conference on Design, Automation & Test in Europe, Dresden, Germany, 14–18 March 2016; pp. 1303–1308. [Google Scholar]

- Schmidt, R.; Möhring, M.; Härting, R.-C.; Reichstein, C.; Neumaier, P.; Jozinović, P. Industry 4.0—Potentials for creating smart products: Empirical research results. In Proceedings of the International Conference on Business Information Systems, Poznań, Poland, 24–26 June 2015; Springer: Berlin, Germany, 2015; pp. 16–27. [Google Scholar]

- Wang, S.; Wan, J.; Zhang, D.; Li, D.; Zhang, C. Towards smart factory for industry 4.0: A self-organized multi-agent system with big data based feedback and coordination. Comput. Netw. 2016, 101, 158–168. [Google Scholar] [CrossRef]

- Lee, J.; Bagheri, B.; Kao, H.-A. A cyber-physical systems architecture for industry 4.0-based manufacturing systems. Manuf. Lett. 2015, 3, 18–23. [Google Scholar] [CrossRef]

- Kagermann, H. Change through digitization—Value creation in the age of Industry 4.0. In Management of Permanent Change; Springer: Berlin, Germany, 2015; pp. 23–45. [Google Scholar]

- Karre, H.; Hammer, M.; Kleindienst, M.; Ramsauer, C. Transition towards an Industry 4.0 State of the LeanLab at Graz University of Technology. Procedia Manuf. 2017, 9, 206–213. [Google Scholar] [CrossRef]

- Jazdi, N. Cyber physical systems in the context of Industry 4.0. In Proceedings of the 2014 IEEE International Conference on Automation, Quality and Testing, Robotics, Cluj-Napoca, Romania, 22–24 May 2014; pp. 1–4. [Google Scholar]

- Schoeberl, P.; Brik, M.; Braun, R.; Fuchs, W. Treatment and recycling of textile wastewater—Case study and development of a recycling concept. Desalination 2005, 171, 173–183. [Google Scholar] [CrossRef]

- Gorecky, D.; Schmitt, M.; Loskyll, M.; Zühlke, D. Human-Machine-Interaction in the industry 4.0 era. In Proceedings of the 2014 12th IEEE International Conference on Industrial Informatics (INDIN), Porto Alegre, Brazil, 27–30 July 2014; pp. 289–294. [Google Scholar]

- Lethbridge, T.C. What knowledge is important to a software professional? Computer 2000, 33, 44–50. [Google Scholar] [CrossRef]

- Valdeza, A.C.; Braunera, P.; Schaara, A.K.; Holzingerb, A.; Zieflea, M. Reducing complexity with simplicity-usability methods for industry 4.0. In Proceedings of the 19th Triennial Congress of the IEA, Melbourne, Australia, 9–14 August 2015; pp. 1–8. [Google Scholar]

- Lary, H.B. Trade in Labor-Intensive Manufactures. In Imports of Manufactures from Less Developed Countries; NBER: Cambridge, MA, USA, 1968; pp. 86–115. [Google Scholar]

- Leamer, E.E. Wage inequality from international competition and technological change: Theory and country experience. Am. Econ. Rev. 1996, 86, 309–314. [Google Scholar]

- Kletti, J. Manufacturing Execution System—MES; Springer: Berlin, Germany, 2007. [Google Scholar]

- Saenz de Ugarte, B.; Artiba, A.; Pellerin, R. Manufacturing execution system—A literature review. Prod. Plan. Control 2009, 20, 525–539. [Google Scholar] [CrossRef]

- Arik Ragowsky, T.M.S. Enterprise resource planning. J. Manag. Inf. Syst. 2002, 19, 11–15. [Google Scholar]

- Leon, A. Enterprise Resource Planning; McGraw-Hill Education: New York, NY, USA, 2008. [Google Scholar]

- Sumner, M. Enterprise Resource Planning; Pearson Education Inc.: New Jersey, NJ, USA, 2005. [Google Scholar]

- O’Leary, D.E. Enterprise Resource Planning Systems: Systems, Life Cycle, Electronic Commerce, and Risk; Cambridge University Press: Cambridge, UK, 2000. [Google Scholar]

- Umble, E.J.; Haft, R.R.; Umble, M.M. Enterprise resource planning: Implementation procedures and critical success factors. Eur. J. Oper. Res. 2003, 146, 241–257. [Google Scholar] [CrossRef]

- Lasi, H.; Fettke, P.; Kemper, H.-G.; Feld, T.; Hoffmann, M. Industry 4.0. Bus. Inf. Syst. Eng. 2014, 6, 239–242. [Google Scholar] [CrossRef]

- Choi, B.K.; Kim, B.H. MES (manufacturing execution system) architecture for FMS compatible to ERP (enterprise resource planning). Int. J. Comput. Integr. Manuf. 2002, 15, 274–284. [Google Scholar] [CrossRef]

- Liu, W.; Chua, T.J.; Larn, J.; Wang, F.-Y.; Yin, X. APS, ERP and MES systems integration for semiconductor backend assembly. In Proceedings of the 7th International Conference on Control, Automation, Robotics and Vision, Singapore, 2–5 December 2002; pp. 1403–1408. [Google Scholar]

- Saggiomo, M.; Wischnowski, M.; Winkel, B.; Nierhaus, M.; Gloy, Y.-S.; Gries, T. Industry 4.0 in the field of textile machinery-first steps of implementation. Melliand Int. 2015, 1, 49–50. [Google Scholar]

- Ramanathan, V.; Feng, Y. Air pollution, greenhouse gases and climate change: Global and regional perspectives. Atmos. Environ. 2009, 43, 37–50. [Google Scholar] [CrossRef]

- Dodman, D. Blaming cities for climate change? An analysis of urban greenhouse gas emissions inventories. Environ. Urban. 2009, 21, 185–201. [Google Scholar] [CrossRef]

- Keohane, N.O.; Olmstead, S.M. Introduction. In Markets and the Environment; Springer: Berlin, Germany, 2016; pp. 1–10. [Google Scholar]

- Davis, S.J.; Caldeira, K. Consumption-based accounting of CO2 emissions. Proc. Natl. Acad. Sci. USA 2010, 107, 5687–5692. [Google Scholar] [CrossRef] [PubMed]

- Guan, D.; Peters, G.P.; Weber, C.L.; Hubacek, K. Journey to world top emitter: An analysis of the driving forces of China’s recent CO2 emissions surge. Geophys. Res. Lett. 2009, 36, 1–5. [Google Scholar] [CrossRef]

- Steinberger, J.K.; Friot, D.; Jolliet, O.; Erkman, S. A spatially explicit life cycle inventory of the global textile chain. Int. J. Life Cycle Assess. 2009, 14, 443–455. [Google Scholar] [CrossRef]

- Elahee, K. Heat recovery in the textile dyeing and finishing industry: Lessons from developing economies. J. Energy S. Afr. 2010, 21, 9–15. [Google Scholar]

- Oǧulata, R.T. Utilization of waste-heat recovery in textile drying. Appl. Energy 2004, 79, 41–49. [Google Scholar] [CrossRef]

- Lopez, A.; Ricco, G.; Ciannarella, R.; Rozzi, A.; Di Pinto, A.; Passino, R. Textile wastewater reuse: Ozonation of membrane concentrated secondary effluent. Water Sci. Technol. 1999, 40, 99–105. [Google Scholar] [CrossRef]

- Chequer, F.M.D.; de Oliveira, G.A.R.; Ferraz, E.R.A.; Cardoso, J.C.; Zanoni, M.V.B.; de Oliveira, D.P. Textile dyes: Dyeing process and environmental impact. In Eco-Friendly Textile Dyeing and Finishing; InTech: London, UK, 2013. [Google Scholar]

- Li, K.; Zhang, X.; Leung, J.Y.-T.; Yang, S.-L. Parallel machine scheduling problems in green manufacturing industry. J. Manuf. Syst. 2016, 38, 98–106. [Google Scholar] [CrossRef]

- Monahan, J.P. A quantity discount pricing model to increase vendor profits. Manag. Sci. 1984, 30, 720–726. [Google Scholar] [CrossRef]

- Kee, R. The sufficiency of product and variable costs for production-related decisions when economies of scope are present. Int. J. Prod. Econ. 2008, 114, 682–696. [Google Scholar] [CrossRef]

- Sinha, A.; Rämö, J.; Malo, P.; Kallio, M.; Tahvonen, O. Optimal management of naturally regenerating uneven-aged forests. Eur. J. Oper. Res. 2017, 256, 886–900. [Google Scholar] [CrossRef]

- Koh, S.; Saad, S. A holistic approach to diagnose uncertainty in ERP-controlled manufacturing shop floor. Prod. Plan. Control. 2003, 14, 273–289. [Google Scholar] [CrossRef]

- Lin, G.Y.; Solberg, J.J. Integrated shop floor control using autonomous agents. IIE Trans. 1992, 24, 57–71. [Google Scholar] [CrossRef]

- Park, H.-S.; Tran, N.-H. An autonomous manufacturing system for adapting to disturbances. Int. J. Adv. Manuf. Technol. 2011, 56, 1159–1165. [Google Scholar] [CrossRef]

- Zhong, R.Y.; Dai, Q.; Qu, T.; Hu, G.; Huang, G.Q. RFID-Enabled real-time manufacturing execution system for mass-customization production. Robot. Comput. Integr. Manuf. 2013, 29, 283–292. [Google Scholar] [CrossRef]

- Hua, J.; Liang, T.; Lei, Z. Study and design real-time manufacturing execution system based on RFID. In Proceedings of the 2008 Second International Symposium on Intelligent Information Technology Application, Shanghai, China, 20–22 December 2008; pp. 591–594. [Google Scholar]

- Almada-Lobo, F. The Industry 4.0 revolution and the future of manufacturing execution systems (MES). J. Innov. Manag. 2016, 3, 16–21. [Google Scholar]

- Wang, W.Y.; Chan, H.K. Virtual organization for supply chain integration: Two cases in the textile and fashion retailing industry. Int. J. Prod. Econ. 2010, 127, 333–342. [Google Scholar] [CrossRef]

- Kuhn, W. Digital factory-simulation enhancing the product and production engineering process. In Proceedings of the 2006 Winter Simulation Conference, Monterey, CA, USA, 3–6 December 2006; pp. 1899–1906. [Google Scholar]

- Tajima, M. Strategic value of RFID in supply chain management. J. Purch. Supply Manag. 2007, 13, 261–273. [Google Scholar] [CrossRef]

- Spekman, R.E.; Kamauff, J.W., Jr.; Myhr, N. An empirical investigation into supply chain management: A perspective on partnerships. Supply Chain Manag. Int. J. 1998, 3, 53–67. [Google Scholar] [CrossRef]

- Johnson, H.T. Early cost accounting for internal management control: Lyman Mills in the 1850’s. Bus. Hist. Rev. 1972, 46, 466–474. [Google Scholar] [CrossRef]

- Abernathy, F.H.; Dunlop, J.T.; Hammond, J.H.; Weil, D. Globalization in the apparel and textile industries: What is new and what is not? In Locating Global Advantage: Industry Dynamics in the International Economy; Stanford University Press: Stanford, CA, USA, 2004. [Google Scholar]

- Lummus, R.R.; Vokurka, R.J.; Alber, K.L. Strategic supply chain planning. Prod. Invent. Manag. J. 1998, 39, 49–58. [Google Scholar]

- Montgomery, D.C. Introduction to Statistical Quality Control; John Wiley & Sons: Hoboken, NJ, USA, 2007. [Google Scholar]

- Stojanovic, R.; Mitropulos, P.; Koulamas, C.; Karayiannis, Y.; Koubias, S.; Papadopoulos, G. Real-Time vision-based system for textile fabric inspection. Real-Time Imaging 2001, 7, 507–518. [Google Scholar] [CrossRef]

- Esmaeilian, B.; Behdad, S.; Wang, B. The evolution and future of manufacturing: A review. J. Manuf. Syst. 2016, 39, 79–100. [Google Scholar] [CrossRef]

- Aulbur, W.; Arvind, C.J.; Bigghe, R. Whitepaper: Skill Development for Industry 4.0; BRICS Skill Development Group: Roland Berger, India, 2016. [Google Scholar]

- Gehrke, L.; Kühn, A.; Rule, D.; Moore, P.; Bellmann, C.; Siemes, S.; Dawood, D.; Singh, L.; Kulik, J.; Standle, M. Industry4.0: A Discussion of Qualifications and Skills in the Factory of the Future: A German and American Perspective; The Association of German Engineers (VDI): Düsseldorf, Germany; American Society of Mechanical Engineers (ASME): Washington, DC, USA, 2015. [Google Scholar]

- Hartmann, E.; Bovenschulte, M. Skills Needs Analysis for “Industry 4.0” Based on Roadmaps for Smart Systems. In SKOLKOVO Moscow School of Management & International Labour Organization: Using Technology Foresights for Identifying Future Skills Needs; Global Workshop Proceedings, Moscow; Institute for Innovation and Technology: Berlin, Germany, 2013; pp. 24–36. [Google Scholar]

- Lowman, S. WEF 2016: 4th Industrial Revolution. 5 mn Jobs, Women in the Firing Line. BIZNEWS. 18 January 2016. Available online: https://www.biznews.com/wef/davos-2016/2016/01/18/wef-2016-4th-industrial-revolution-5mn-jobs-women-in-the-firing-line/ (accessed on 20 July 2018).

- Team, M. Five Million Jobs by 2020: The Real Challenge of the Fourth Industrial Revolution. World Economic Forum, 18 January 2016. Available online: https://www.weforum.org/press/2016/01/five-million-jobs-by-2020-the-real-challenge-of-the-fourth-industrial-revolution/ (accessed on 20 July 2018).

- Flynn, J.; Dance, S.; Schaefer, D. Industry 4.0 and Its Potential Impact on Employment Demographics in the UK. In Advanced in Manufacturing Technology XXXI, Proceedings of the 15th International Conference on Manufacturing Research, incorporating the 32nd National Conference on Manufacturing Research, London, UK, 5–7 September 2017; Gao, J., El Souri, M., Keates, S., Eds.; IOS Press: Amsterdam, The Netherlands, 2017. [Google Scholar]

- Matovcikova, D. Industry 4.0 as the Culprit of Unemployment. In Proceedings of the 12th International Workshop on Knowledge Management, Trenčín, Slovakia, 12–13 October 2017. [Google Scholar]

- Tsai, W.-H.; Hung, S.-J. A fuzzy goal programming approach for green supply chain optimisation under activity-based costing and performance evaluation with a value-chain structure. Int. J. Prod. Res. 2009, 47, 4991–5017. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Chen, H.-C.; Leu, J.-D.; Chang, Y.-C.; Lin, T.W. A product-mix decision model using green manufacturing technologies under activity-based costing. J. Clean. Prod. 2013, 57, 178–187. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Hung, S.-J. Treatment and recycling system optimisation with activity-based costing in WEEE reverse logistics management: An environmental supply chain perspective. Int. J. Prod. Res. 2009, 47, 5391–5420. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Chen, H.-C.; Liu, J.-Y.; Chen, S.-P.; Shen, Y.-S. Using activity-based costing to evaluate capital investments for green manufacturing systems. Int. J. Prod. Res. 2011, 49, 7275–7292. [Google Scholar] [CrossRef]

- Wang, S.; Wan, L.; Li, T.; Luo, B.; Wang, C. Exploring the effect of cap-and-trade mechanism on firm’s production planning and emission reduction strategy. J. Clean. Prod. 2018, 172, 591–601. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Activity Resources | Process 1 | Process 2 | Process 3 | Capacity | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Draw Textured Yarn | Scrap yarn | Greige Fabric | Scrap Fabric | Finished Fabric | Eco-Brick | ||||||

| Price of per selling unit | $97,000 | $570 | $135,000 | $2,100 | $202,500 | $2,300 | |||||

| Production coefficient | ei | 0.96 | 0.95 | 0.14 | |||||||

| (1 − ei) | 0.04 | 0.05 | |||||||||

| Direct material cost | M, | $65,000 | $7,000 | ||||||||

| $1,800 | $1,500 | ||||||||||

| Machine hours constraint | Activity driver | ||||||||||

| Machine 1 | Machine hrs. | hi | 3 | 120,000 | |||||||

| Machine 2 | 4 | 100,000 | |||||||||

| Machine 3 | 5 | 130,000 | |||||||||

| li | 3 | 2 | 1 | ||||||||

| Direct Labor constraint | Carbon tax constraint | qc | 7 | ||||||||

| Cost | L0 = 47,840,000 | L1 = 101,660,000 | Cost | PC0 = 0 | PC1 = 170,000,000 | PC2 = 270,000,000 | |||||

| Labor hours | G0 = 368,000 | G1 = 598,000 | Emission Quantities | GC0 = 50,000 | GC1 = 170,000 | GC2 = 180,000 | |||||

| Wage Rate | wr0 = $130/h | wr1 = 170/h | Tax Rate | Tr0 = $0/ton | Tr1 = $1,000/ton | Tr2 = $1,500/ton | |||||

| Batch-Level Activity | Starting Location (s) | End Location (e) | Draw Textured Yarn | Greige Fabric | Finished Fabric | |

|---|---|---|---|---|---|---|

| Handling | σse, μse | 0 | 1 | 5, 2 | ||

| 1 | 2 | 1, 1 | ||||

| 1 | 0 | 0.5, 1 | ||||

| 2 | 3 | 1, 1 | ||||

| 2 | 0 | 2, 1 | ||||

| 2 | 3 | 3, 2 | ||||

| Set-up | λ, ω | 3, 2 |

| Max = (97,000 × + 135,000 × + 202,500 × + 570 × 0.04 × + 2100 × 0.05 × + 2300 × 0.14 × ) − (65,000 × M + 7000 × + 1800 × + 1500 × ) − [47,840,000 + (170 × − 62,560,000 × )] − (1000 × − 50,000,000 × + 1500 × − 75,000,000 × ) + (60 × + 120 × ) − 500,000 | |

| Subject to Input-Output Relationship: − 0.96 × M = 0 = + − 0.95 × = 0 = + = 0.04 × M = 0.05 × = 0.14 × = 0.65 × = 0.1 × = 0.2 × = 6 × = 0.95 × = 0.85 × | Subject to Direct Labor: 3 × + 2 × + 1 × + 2 × + 1 × + 1 × + 1 × + 1 × + 2 × + 2 × − − ≤ 0 ≤ × 368,000 × 368,000 < ≤ × 598,000 + = 1 |

| Subject to Machine Hour: 3 × − 120,000 ≤ 0 4 × − 100,000 ≤ 0 5 × − 130,000 ≤ 0 | |

| Subject to Batch-Level: M ≤ 5 × ≤ 1 × + 0.04 × M ≤ 0.5 × ≤ 1 × + 0.05 × ≤ 2 × + 0.14 × ≤ 3 × ≤ 3 × | |

| Subject to Carbon Tax Function: 7 × ≤ + + ≤ × 50,000 50,000 × < ≤ × 170,000 × 170,000 < ≤ × 0.1E + 10 + + = 1 | |

| = 3,361,133,000 | = 40,000 | = 13,684.21 | = 26,315.79 |

| = 25,000 | = 714.2857 | = 24,285.71 | = 1666.667 |

| = 1315.789 | = 2695.714 | M = 41,666.67 | = 15,785.71 |

| = 2428.571 | = 485.7143 | = 2914.286 | = 0 |

| = 327,455.7 | = 0.746149 | = 0.9253851 | = 0 |

| = 170,000 | = 0 | = 0 | = 1 |

| = 0 | = 23,071.43 | = 20,642.86 | = 8334 |

| = 26,316 | = 30,702 | = 24,286 | = 13,158 |

| = 9229 | = 8334 |

| Cost variation Ratio (%) | Normal | Price Discount | ||

|---|---|---|---|---|

| Profit (Thousands) | Profit Variation Ratio (%) | Profit (Thousands) | Profit Variation Ratio (%) | |

| 20% | 2,819,466 | −16.12% | 3,144,466 | −13.42% |

| 15% | 2,954,883 | −12.09% | 3,266,341 | −10.07% |

| 10% | 3,090,299 | −8.06% | 3,388,216 | −6.71% |

| 5% | 3,225,716 | −4.03% | 3,510,091 | −3.36% |

| 0% | 3,361,133 | 0.00% | 3,631,966 | 0.00% |

| −5% | 3,496,549 | 4.03% | 3,753,841 | 3.36% |

| −10% | 3,631,966 | 8.06% | 3,875,716 | 6.71% |

| −15% | 3,767,383 | 12.09% | 3,997,591 | 10.07% |

| −20% | 3,902,799 | 16.12% | 4,119,466 | 13.42% |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tsai, W.-H. Green Production Planning and Control for the Textile Industry by Using Mathematical Programming and Industry 4.0 Techniques. Energies 2018, 11, 2072. https://doi.org/10.3390/en11082072

Tsai W-H. Green Production Planning and Control for the Textile Industry by Using Mathematical Programming and Industry 4.0 Techniques. Energies. 2018; 11(8):2072. https://doi.org/10.3390/en11082072

Chicago/Turabian StyleTsai, Wen-Hsien. 2018. "Green Production Planning and Control for the Textile Industry by Using Mathematical Programming and Industry 4.0 Techniques" Energies 11, no. 8: 2072. https://doi.org/10.3390/en11082072

APA StyleTsai, W.-H. (2018). Green Production Planning and Control for the Textile Industry by Using Mathematical Programming and Industry 4.0 Techniques. Energies, 11(8), 2072. https://doi.org/10.3390/en11082072