Mini-Grids for the Base of the Pyramid Market: A Critical Review

Abstract

1. Introduction

2. Brief Overview of Mini-Grids

2.1. Meaning of Mini-Grids

2.2. Technical Configuration

2.3. Service Delivery Models

3. Market at the Base of the Pyramid

- (1)

- One successful adaptation has been to provide the service in small, affordable units [32]. Taking advantage of LED lighting, many mini-grid businesses are offering extremely low wattage level supplies (less than 5 W in the case of lighting only services) that were unthinkable in the era of the central grids. Even those suppliers providing lighting plus services or higher tier services are also packaging their supplies quite differently from the standard utility supplies, thereby adapting to the customer needs.

- (2)

- Privately-owned and commercially motivated supply providers are setting tariffs for their services considering expenditure on alternative options that compete with mini-grid based electricity. To ensure attractiveness of their supply, the tariff is being set lower than expenses on monthly kerosene consumption or payments to diesel generator-based supplies.

- (3)

- Businesses are using innovative billing and collection systems using smart meters, prepaid meters, and mobile payment systems to improve revenue collection efficiency and reduce defaults.

- (4)

- To mitigate business environment-related risks, innovative contractual arrangements are being used: for example, joint liability groups have been used to manage credit and payment risks. Similarly, flexible bill collection approaches (daily or weekly collection) have tried to align billing cycle to consumer characteristics [33].

- (5)

- To support financing their electricity access, micro-credit facilities are being used. The supply provider working with the consumers organise such credits so that the market is created. The example of Grameen Bank in Bangladesh appears in the literature widely but such credit systems are being used in other countries as well [31]. However, Reference [33] remarks that poor consumers are paying high interest rates (2 to 3% per month) for the credit remains a major issue.

4. Challenges Facing Mini-Grid Based Electricity Supply in BoP Markets

4.1. Regulatory and Policy Environment

- (1)

- Coverage: The service area of a mini-grid based supply may not be clearly demarcated avoiding overlaps with the service area of the central grid utility. In many countries, the national electricity company or a distribution licensee may already have the jurisdiction over the area and unless a service area for the mini-grid is carved out legally, the legal basis for the mini-grid can be problematic. Moreover, this leads to the other issue, which [37] calls the gateway problem—the threat of grid extension by the central grid. In the absence of clarity over jurisdiction of service area, the threat of grid extension acts as a major deterrent for private sector investment in mini-grids. The possibility of an aggressive grid extension effort by the incumbent and the potential for stranded mini-grid assets in the absence of a defined exit mechanism is a major investment risk. This can also be an issue when two or more mini-grid operators appear in the same area—which can duplicate the system and lead to non-optimal resource use. Accordingly, a non-overlapping service area is essential.

- (2)

- Permission for doing business: Electricity generation and supply is a regulated activity in most countries around the world but the legal provisions do not often recognise the decentralised models of supply. This may be due to old legal provisions or may be deliberately left out to avoid overburdening of the regulatory system. In the absence of a proper approval system, legitimising mini-grid businesses may be difficult. Ambiguity in the legal area breeds confusion and alternative interpretations cause business uncertainty, which reduces attractiveness of the market to potential investors. A simple, transparent and low cost approval system is a must [38].

- (3)

- Eligibility requirements: Being an emerging opportunity, many new entrants are entering the business but unless they meet certain capacity requirements (in technical, financial and organisational terms), the development of the business is likely to be affected through reduced credibility, loss of trust and perhaps misuse of resources. Lack of clear eligibility requirements opens the door to everyone, making it difficult for the serious businesses to establish themselves.

- (4)

- Conditions of supply: A business engaged in electricity supply has to satisfy a certain conditions. For example, the supply has to be safe and secure. The service has to offer non-discriminatory supply to all eligible consumers. Similarly, conditions for connection/disconnection, prevention of market abuse, minimum performance targets, etc. are other conditions normally applied. Lack of clarity about business engagement and expectations can reduce effectiveness of the businesses [35].

- (5)

- Tariff-related issues: Any confusion regarding tariffs or any potential for disagreement in this area can be fatal for the viability of a mini-grid business. While businesses aim for cost recovery, high cost of supply can limit the consumer base due to affordability issues. On the other hand price parity with the central grid or a uniform tariff for all mini-grids can create viability issues for the investors [13]. Balancing this trade-off is a demanding challenge as favouring one will affect the other party adversely. For example, in the Uttar Pradesh Mini-grid Policy in India, if the mini-grid developer adopts the capital subsidy route where 30% of the capital cost will be subsidised, then the tariff has been prescribed for the basic service level (serving a load of 100 W for 8 h per day). The prescribed tariff aims parity with grid-based supply but this is unlikely to make the mini-grid business viable [37]. An overly prescriptive approach is likely to be less acceptable to the investors while a very lenient approach can lead to abuse of market power by the supplier. Negotiated solutions are allowed in some countries but as the supplier tends to have a higher bargaining power, the decision-making can be highly influenced by them.

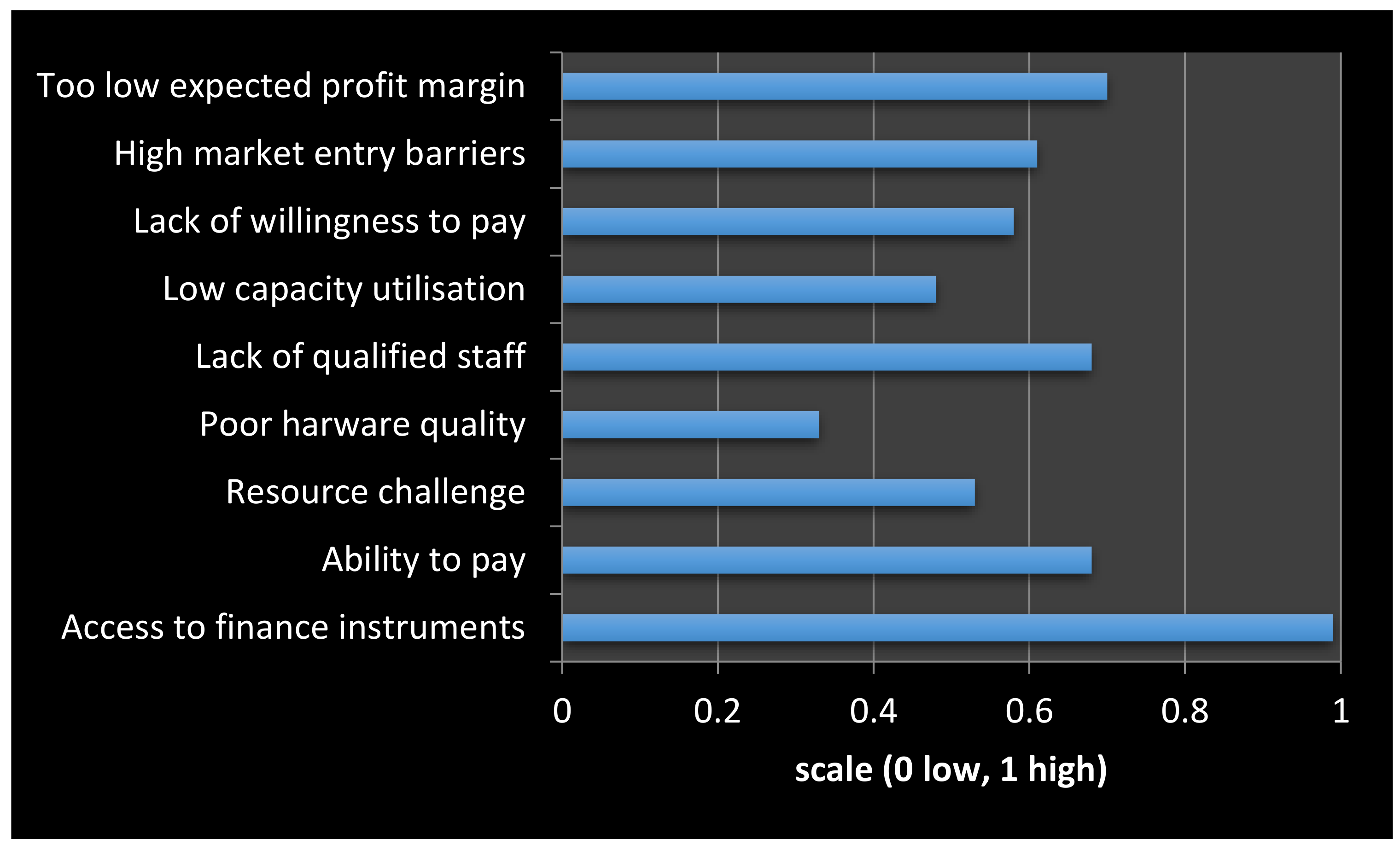

4.2. Viability and Affordability Issues

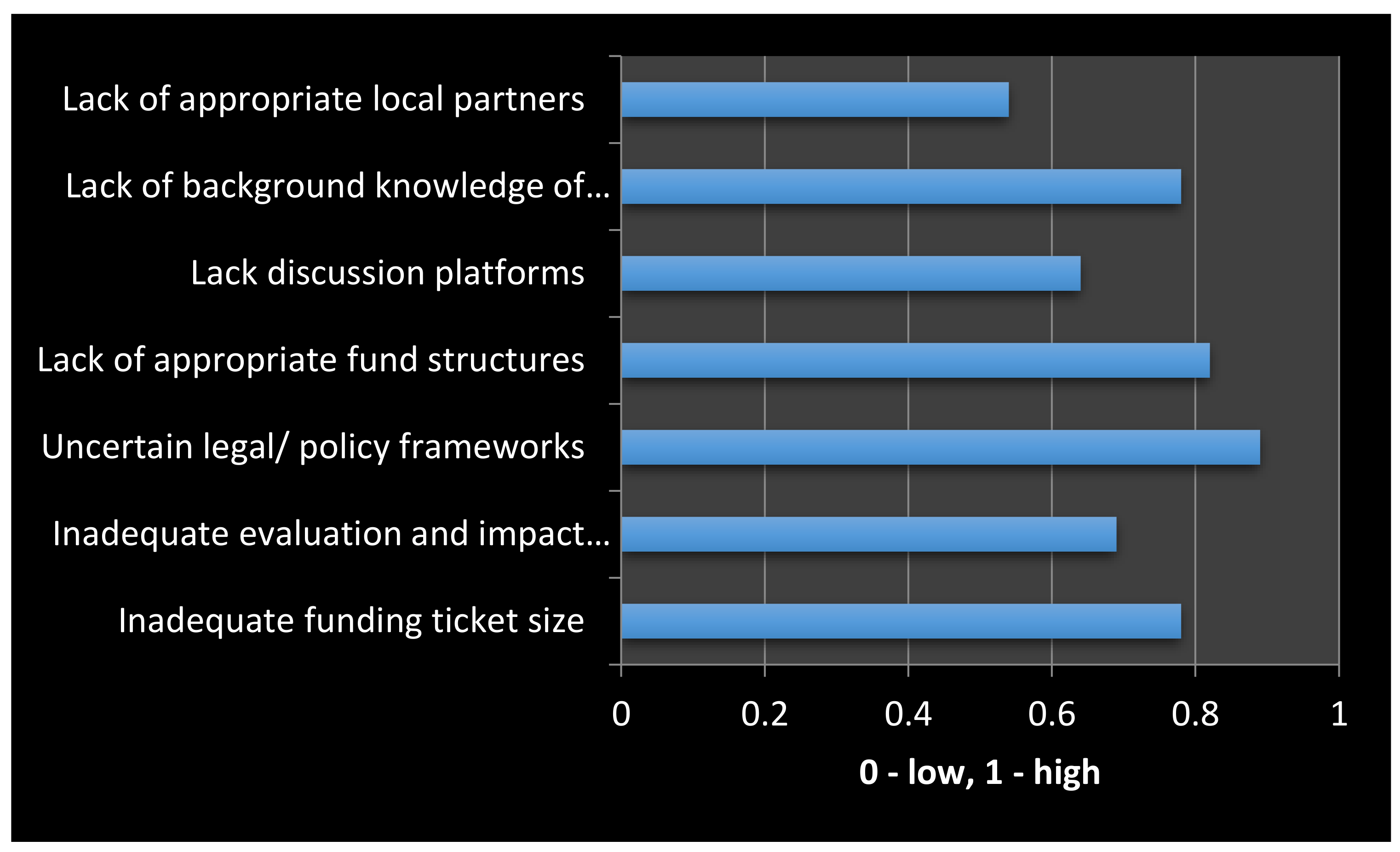

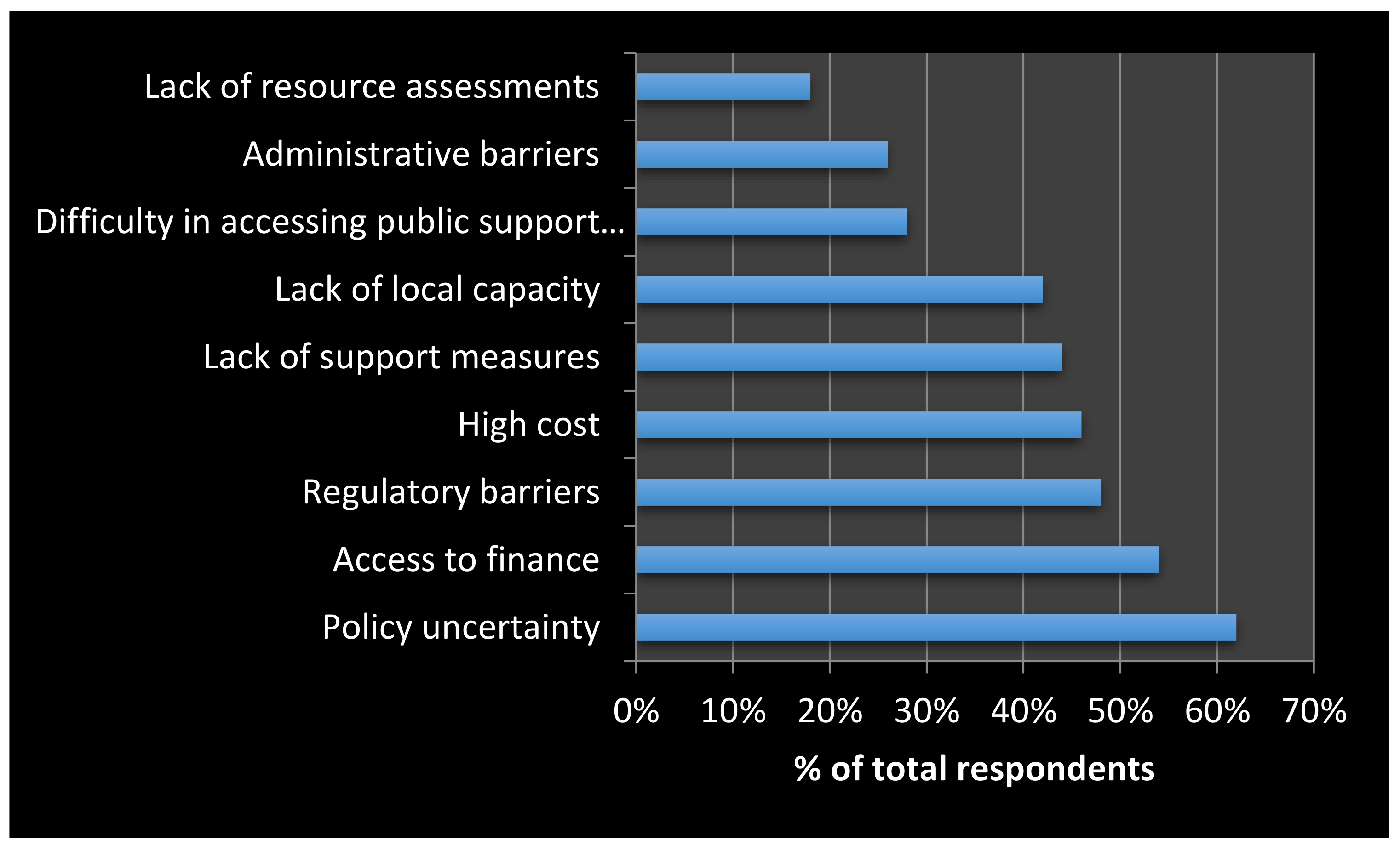

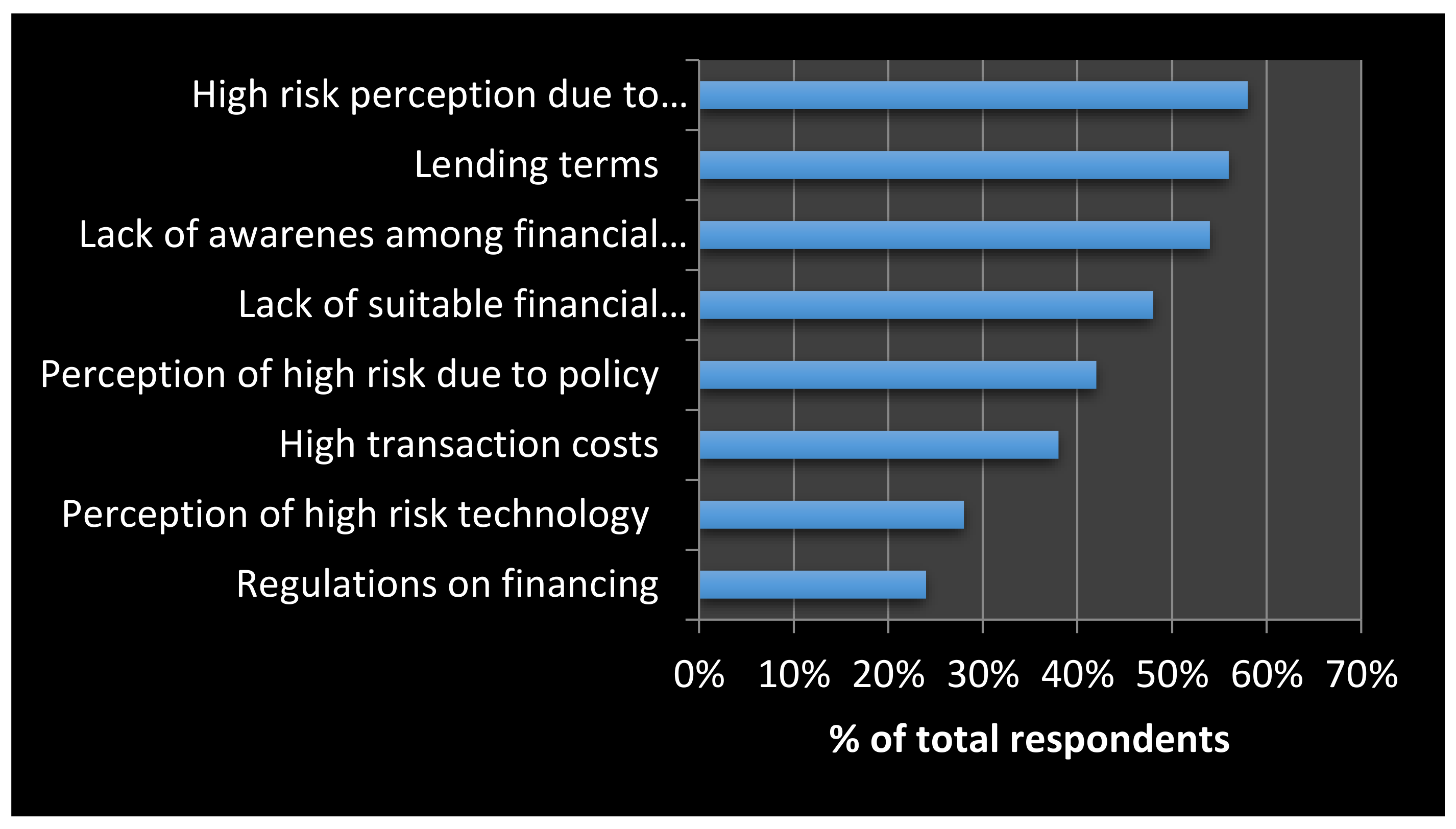

4.3. Financing Challenges

4.4. Other Issues

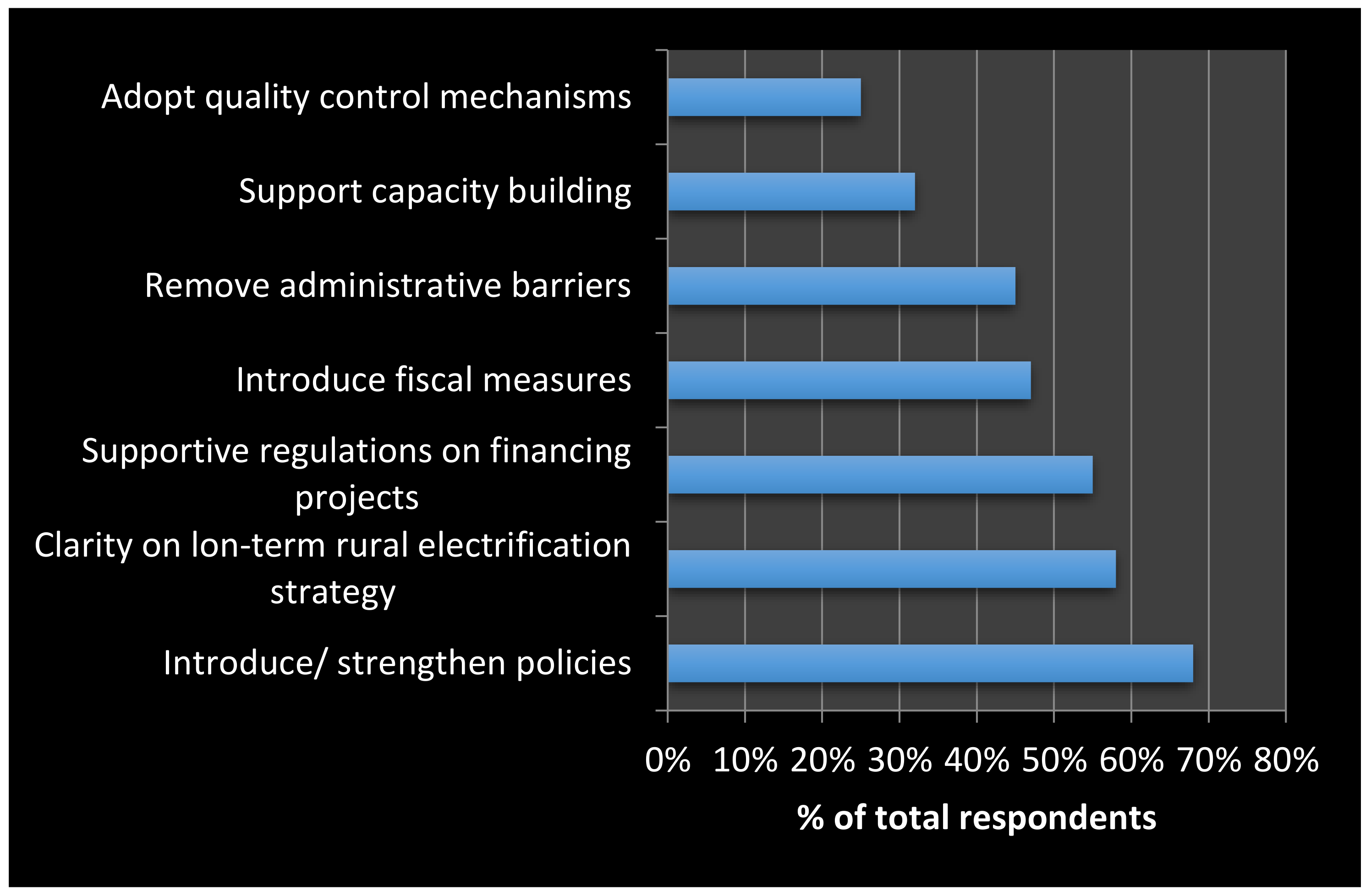

5. Supports and Interventions for Mini-Grid Business Development

- (1)

- Giving a legal status to mini-grid business: defining the mini-grid space legally in the electricity acts and clarifying the scope of the business is essential to create the activity;

- (2)

- Defining the regulatory framework: formulating appropriate regulatory arrangements for managing mini-grids, defining standards of service for mini-grids, and policies for entry/ exit and coordination of grid and mini-grid based electrification are some aspects of regulatory and electricity planning that are essential.

- (3)

- Tariff and financial support policy: A generic framework for tariff and subsidy for mini-grids and its delivery mechanism can bring clarity to the business activity.

- (4)

- Fiscal incentives: Tax breaks and tax holidays for businesses, waiver of import duties and reductions in value added tax or service tax are possible ways of incentivising the activities.

- (5)

- Risk mitigation measures: Because mini-grids are considered as high risk low return investment propositions, risk mitigation measures to minimise impacts on the investors can be designed at the national level.

- (6)

- Consumer support mechanisms: Arrangements for supporting the BoP consumers to enable them access electricity will also be important.

6. Conclusions

Conflicts of Interest

References

- IEA. Energy Access Outlook, Special Report of World Energy Outlook 2017; International Energy Agency: Paris, France, 2017. [Google Scholar]

- Bhattacharyya, S. Energy access programmes and sustainable development: A critical review and analysis. Energy Sustain. Dev. 2012, 16, 260–271. [Google Scholar] [CrossRef]

- IEA and the World Bank. Sustainable Energy for All—Global Tracking Framwork: Progress toward Sustainable Energy; The World Bank: Washington, DC, USA, 2017. [Google Scholar]

- World Bank. State of Electricity Access Report; The World Bank: Washington, DC, USA, 2017. [Google Scholar]

- IRENA. Off-grid Renewable Energy Systems: Status and Methodological Issues; International Renewable Energy Agency: Abu Dhabi, UAE, 2015. [Google Scholar]

- IFC. From Gap to Opportunity: Business Models for Scaling up Energy Access; International Finance Corporation: Washington, DC, USA, 2012. [Google Scholar]

- Schnitzer, D.; Lounsbury, D.D.S.; Carvallo, J.; Deshmukh, R.; Apt, J.; Kammen, D. Microgrids for Rural Electrification: A Critical Review of Best Practices on Seven Case Studies; United Nations Foundation: Washington, DC, USA, 2014. [Google Scholar]

- Draeck, M.; Kottasz, E. Renewable Energy-Based Mini-Grids: The UNIDO Experience; United Nations Industrial Development Organisation: Vienna, Austria, 2017. [Google Scholar]

- Panos, E.; Densing, M.; Volkart, K. Access to electricity in the World Energy Council’s global energy scenarios: An outlook for developing regions until 2030. Energy Strategy Rev. 2016, 9, 28–49. [Google Scholar] [CrossRef]

- Yan, J.; Zhai, Y.; Wijayatunga, P.; Mohamed, A.; Campana, P. Renewable energy integration with mini/micro-grids. Appl. Energy 2017, 201, 241–244. [Google Scholar] [CrossRef]

- Mandelli, S.; Barbieri, J.; Mereu, R.; Colombo, E. Off-grid systems for rural electrification in developing countries: Definitions, classification and a comprehensive literature review. Renew. Sustain. Energy Rev. 2016, 58, 1621–1648. [Google Scholar] [CrossRef]

- International Energy Agency. The Role of Energy Storage for Mini-Grid Stabilisation, PVPS T11-02; International Energy Agency: Paris, France, 2011. [Google Scholar]

- EUEI-PDF. Mini-Grid Policy Toolkit: Policy and Business Frameworks for Successful Mini-Grid Rollouts; European Union Energy Initiative Partnership Dialogue Facility: Eschborn, Germany, 2014. [Google Scholar]

- Knuckles, J. Business models for mini-grid electricity in base of the pyramid markets. Energy Sustain. Dev. 2016, 31, 67–82. [Google Scholar] [CrossRef]

- Cloke, J.; Mohr, A.; Brown, E. Imagining renewable energy: Towards a Social Energy Systems approach to community renewable energy projects in the Global South. Energy Res. Soc. Sci. 2017, 31, 263–272. [Google Scholar] [CrossRef]

- Pedersen, M.B. Deconstructing the concept of renewable energy-based mini-grids for rural electrification in East Africa. WIREs Energy Environ. 2016, 5, 570–587. [Google Scholar] [CrossRef]

- Chaurey, A.; Kandpal, T. A techno-economic comparison of rural electrification based on solar home systems and PV microgrids. Energy Policy 2010, 38, 3118–3129. [Google Scholar] [CrossRef]

- Boait, P. Technical aspects of mini-grids for rural electrification. In Mini-Grids for Rural Electrification of Developing Countries; Bhattacharyya, S., Palit, D., Eds.; Springer: London, UK, 2014; pp. 37–61. [Google Scholar]

- Boait, P.; Advani, V.; Gammon, R. Estimation of demand diversity and daily demand profile for off-grid electrification in developing countries. Energy Sustain. Dev. 2015, 29, 135–141. [Google Scholar] [CrossRef]

- Blum, N.U.; Wakeling, R.S.; Schmidt, T.S. Rural electrification through village grids—Assessing the cost competitiveness of isolated renewable energy technologies in Indonesia. Renew. Sustain. Energy Rev. 2013, 22, 482–496. [Google Scholar] [CrossRef]

- ARE. Hybrid Mini-Grids for Rural Electrification: Lessons Learned; Alliance for Rural Electrification: Brussels, Belgium, 2014. [Google Scholar]

- Safdar, T. Business Models for Mini-Grids; Technical Report 9; Smart Villages: Cambridge, UK, 2017. [Google Scholar]

- Krithika, P.; Palit, D. Participatory business models for off-grid electrification. In Rural Electrification through Decentralised Off-Grid Systems in Developing Countries; Bhattacharyya, S., Ed.; Springer: London, UK, 2013; pp. 187–225. [Google Scholar]

- Bhattacharyya, S. Business issues for mini-grid based electrification in developing countries. In Mini-Grids for Rural Electrification of Developing Countries; Bhattacharyya, S., Palit, D., Eds.; Springer: London, UK, 2014; pp. 145–164. [Google Scholar]

- Contejean, A.; Verin, L. Making Mini-Grids Work: Productive Uses of Electricity in Tanzania; IIED Working Paper; International Institute for Environment and Development: London, UK, 2017. [Google Scholar]

- IRENA. Innovation Outlook: Renewable Mini-Grids; International Renewable Energy Agency: Abu Dhabi, UAE, 2016. [Google Scholar]

- Prahalad, C.; Hart, S. The fortune at the Bottom of the Pyramid. Strategy Bus. 2002, 26, 1–14. [Google Scholar] [CrossRef]

- Prahalad, C.; Hammond, A. Serving the World’s poor, profitably. Harvard Bus. Review. 2002, 80, 48–59. [Google Scholar]

- Bhattacharyya, S. Renewable energies and the poor: Niche or nexus? Energy Policy 2006, 34, 659–663. [Google Scholar] [CrossRef]

- Cook, P. Infrastructure, rural electrification and developmen. Energy Sustain. Dev. 2011, 15, 304–313. [Google Scholar] [CrossRef]

- Ausrod, V.; Sinha, V.; Widding, O. Business model design at the base of the pyramid. J. Clean. Prod. 2017, 162, 982–996. [Google Scholar] [CrossRef]

- Alam, M.; Bhattacharyya, S. Are the off-grid customers ready to pay for electricity from the decentralized renewable hybrid mini-girds? A study of willingness to pay in rural Bangladesh. Energy 2017, 139, 433–446. [Google Scholar]

- Bhattacharyya, S.; Palit, D. Mini-grid based electrification to enhance electricity access in developing countries: What policies may be required? Energy Policy 2016, 94, 166–178. [Google Scholar] [CrossRef]

- Manetsgruber, D.; Wagemann, B.; Kondev, B.; Dziergwa, K. Risk Management for Mini-Grids: A New Approach to Guide Mini-Grid Development; Alliance for Rural Electrification: Brussels, Belgium, 2015. [Google Scholar]

- Tenenbaum, B.; Greacen, C.; Siyambalapitiya, T.; Knuckles, J. From the Bottom Up: How Small Power Producers and Mini-Grids Can Deliver Electrification and Renewable Energy in Africa; Directions in Development—Energy and Mining; The World Bank: Washington, DC, USA, 2014. [Google Scholar]

- Bhattacharyya, S. To regulate or not to regulate off-grid electricity access in developing countries. Energy Policy 2013, 63, 494–503. [Google Scholar] [CrossRef]

- Comello, S.; Reichelstein, S.J.; Sahoo, A.; Schmidt, T. Enabling mini-grid development in India. World Dev. 2017, 93, 94–107. [Google Scholar] [CrossRef]

- IRENA. Policies and Regulations for Private Sector Renewable Energy Mini-Grids; International Renewable Energy Agency: Abu Dhabi, UAE, 2016. [Google Scholar]

- Doukas, A.; Ballesteros, A. Clean Energy Access in Developing Countries: Perspectives on Policy and Regulation; World Resources Institute: Washington, DC, USA, 2015. [Google Scholar]

- Palit, D.; Bandopadhyay, K. Rural electricity access in India in retrospect: A critical rumination. Energy Policy 2017, 109, 109–120. [Google Scholar] [CrossRef]

- Attigah, B.; Mayer-Tasch, L. The Impact of Electricity Access on Economic Development—A Literature Review; Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH: Eschborn, Germany, 2013. [Google Scholar]

- Banerjee, S.G.; Moreno, A.; Sinton, J.; Primiani, T.; Seong, J. Regulatory Indicators for Sustainable Energy: A Global Scorecard for Policy Makers; The World Bank: Washington, DC, USA, 2016. [Google Scholar]

- Solar Energy Foundation. OBIN—Global Off-Grid Business Indicator; Stiftung Solarenergie—Solar Energy Foundation: Merzhausen, Germany, 2014. [Google Scholar]

- IRENA. Accelerating Off-Grid Renewable Energy, IOREC 2014, Key Findings and Recommendations; International Renewable Energy Agency: Abu Dhabi, UAE, 2015. [Google Scholar]

- Urmee, T.; Anisuzzaman, M. Social, cultural and political dimensions of off-grid renewable energy programs in developing countries. Renew. Energy 2016, 93, 159–167. [Google Scholar] [CrossRef]

- ESMAP. Technical and Economic Assessment of Off-Grid, Mini-Grid and Grid Electrification Technologies; ESMAP Technical Paper 121/07; The World Bank: Washington, DC, USA, 2007. [Google Scholar]

- Nouni, M.; Mullick, S.; Kandpal, T. Providing electricity access to remote areas in India: An approach towards identifying potential areas for decentralised electricity supply. Renew. Sustain. Energy Rev. 2008, 12, 1187–1220. [Google Scholar] [CrossRef]

- Banerjee, R. Comparison of options for distributed generation in India. Energy Policy 2006, 34, 101–111. [Google Scholar] [CrossRef]

- Bhattacharyya, S. Viability of off-grid electricity supply using rice-husk: A case study of Bangladesh. Biomass Bioenergy 2014, 68, 44–54. [Google Scholar] [CrossRef]

- Bhattacharyya, S. Mini-grid based electrification in Bangladesh: Technical configuration and business analysis. Renew. Energy 2015, 75, 745–761. [Google Scholar] [CrossRef]

- Ramamurthi, P.; Fernandes, M.; Nielsen, P.; Nunes, C. Utilisation of rice residues for decentralised electricity generation in Ghana: An economic analysis. Energy 2016, 111, 620–629. [Google Scholar] [CrossRef]

- Sandwell, P.; Chan, N.; Foster, S.; Nagpal, D.; Emmott, C.; Candelise, C.; Buckle, S.; Ekins-Daukes, N.; Gambhir, A.; Nelson, J. Off-grid solar photovoltaic systems for rural electrification and emissions mitigation in India. Sol. Energy Mater. Sol. Cells 2016, 156, 147–156. [Google Scholar] [CrossRef]

- Alam, M.; Bhattacharyya, S. Decentralized Renewable Hybrid Mini-Grids for Sustainable Electrification of the Off-Grid Coastal Areas of Bangladesh. Energies 2016, 9, 268. [Google Scholar] [CrossRef]

- Himri, Y.; Stambouli, A.B.; Draoui, B.; Himri, S. Techno-economical study of hybrid power system for a remote village in Algeria. Energy 2008, 33, 1128–1136. [Google Scholar] [CrossRef]

- Nandi, S.; Ghosh, H. Prospect of wind-PV-battery hybrid system as an alternative to grid extension in Bangladesh. Energy 2010, 35, 3040–3047. [Google Scholar] [CrossRef]

- Dalton, G.; Lockington, D.; Baldock, T. Feasibility analysis of stand-alone renewable energy supply options for a large hotel. Renew. Energy 2008, 33, 1475–1490. [Google Scholar] [CrossRef]

- Sen, R.; Bhattacharyya, S. Off-grid electricity generation with renewable energy technologies in India: An application of HOMER. Renew. Energy 2014, 62, 388–398. [Google Scholar] [CrossRef]

- Blechinger, P.; Cader, C.; Bertheau, P.; Huyskens, H.; Seguin, R.; Breyer, C. Global analysis of the techno-economic potential of renewable energy hybrid systems on small islands. Energy Policy 2016, 98, 674–687. [Google Scholar] [CrossRef]

- Das, B.; Hoque, N.; Mandal, S.; Pal, T.; Raihand, M. A techno-economic feasibility of a stand-alone hybrid power generation for remote area application in Bangladesh. Energy 2017, 134, 775–788. [Google Scholar] [CrossRef]

- Chauhan, A.; Saini, R. Techno-economic feasibility study on Integrated Renewable Energy System for an isolated community of India. Renew. Sustain. Energy Rev. 2016, 59, 388–405. [Google Scholar] [CrossRef]

- Azimoh, C.; Klintenberg, P.; Wallin, F.; Karlsson, B.; Mbohwa, C. Electricity for development: Mini-grid solution for rural electrification in South Africa. Energy Convers. Manag. 2016, 10, 268–277. [Google Scholar] [CrossRef]

- Kolhe, M.; Ranaweera, K.; Gunawardana, A. Techno-economic sizing of off-grid hybrid renewable energy system for rural electrification in Sri Lanka. Sustain. Energy Technol. Assess. 2015, 11, 53–64. [Google Scholar] [CrossRef]

- Akpan, U. Technology options for increasing electricity access in areas with low electricity access rate in Nigeria. Socio-Econ. Plan. Sci. 2015, 51, 1–12. [Google Scholar] [CrossRef]

- Chakrabarti, S.; Chakrabarti, S. Rural electrification programme with solar energy in remote region—A case study in an island. Energy Policy 2002, 30, 33–42. [Google Scholar] [CrossRef]

- Roche, O.; Blanchard, R. Design of a solar energy centre for providing lighting and income-generating activities for off-grid rural communities in Kenya. Renew. Energy 2018, 118, 685–694. [Google Scholar] [CrossRef]

- Babatunde, O.; Akinyele, D.; Akinbulire, T.; Oluseyi, P. valuation of grid-independent solar photovoltaic system for primary health centres (PHCs) in developing countries. Renew. Energy Focus 2018, 24, 16–27. [Google Scholar] [CrossRef]

- Zubi, G.; Dufo-Lopez, R.; Pasaoglu, G.; Pardo, N. Techno-economic assessment of an off-grid PV system for developing regions to provide electricity for basic domestic needs: A 2020–2040 scenario. Appl. Energy 2016, 176, 309–319. [Google Scholar] [CrossRef]

- Chattopadhyay, D.; Bazilian, M.; Lilienthal, P. More power less cost: Transitioning up the solar energy ladder from home systems to mini-grids. Electr. J. 2015, 28, 41–50. [Google Scholar] [CrossRef]

- Graber, S.; Narayanan, T.; Alfaro, J.; Palit, D. Solar microgrids in rural India: Consumers’ willingness to pay for attributes of electricity. Energy Sustain. Dev. 2018, 42, 32–43. [Google Scholar] [CrossRef]

- Asian Development Bank (ADB). The Future of Mini-Grids: From Low Cost to High Value: Using Demand Driven Design to Maximise Revenue and Impact; CAT Projects; Asian Development Bank: Metro Manila, Philippines, 2013. [Google Scholar]

- cKinetics. Financing Decentralised Renewable Energy Mini-grids in India: Opportunities, Gaps and Directions; cKinetics: New Delhi, India, 2013. [Google Scholar]

- Domenech, B.; Ferrer-Martí, L.; Pastor, R. Hierarchical methodology to optimize the design of stand-alone electrification systems for rural communities considering technical and social criteria. Renew. Sustain. Energy Rev. 2015, 51, 182–196. [Google Scholar] [CrossRef][Green Version]

- Dufo-López, R.; Bernal-Agustín, J.L.; Yusta-Loyo, J.M.; Domínguez-Navarro, J.A.; Ramírez-Rosado, I.J.; Lujano, J.; Aso, I. Multi-objective optimization minimizing cost and life cycle emissions of stand-alone PV–wind–diesel systems with batteries storage. Appl. Energy 2011, 88, 4033–4041. [Google Scholar] [CrossRef]

- Henao, F.; Cherni, JA.; Jaramillo, P.; Dyner, I. A multicriteria approach to sustainable energy supply for the rural poor. Eur. J. Oper. Res. 2012, 218, 801–809. [Google Scholar] [CrossRef]

- Bhattacharyya, S.C.; Mishra, A.; Sarangi, G.K. Analytical frameworks and an integrated approach for mini-grid based electrification. In Mini Grids for Rural Electrification of Developing Countries; Bhattacharyya, S., Palit, D., Eds.; Springer International Publishing: Cham, Switzerland, 2014; pp. 95–134. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Local Grid Systems | Commonly Used Size Definitions | IRENA Proposed Categorisation [5] |

|---|---|---|

| Mini-grids | 10 to few MW | 0–100 MW |

| Micro-grids | 1–10 kW | 5–100 kW |

| Nano-grid | 0.5–1 kW | 0–5 kW |

| Pico-grid | 0–0.5 kW | 0–1 kW |

| Country | Total | Electrification Plan | Scope of Plan | Grid Electrification Framework | Framework for Mini-Grids | Framework for Stand Alone Systems | Affordability | Utility Transparency | Utility Credit Worthiness |

|---|---|---|---|---|---|---|---|---|---|

| Top Ranking Countries | |||||||||

| India | 84 | 80 | 75 | 100 | 77 | 69 | 100 | 96 | 76 |

| Kenya | 82 | 100 | 50 | 67 | 66 | 93 | 100 | 96 | 86 |

| Philippines | 82 | 100 | 75 | 67 | 85 | 62 | 100 | 87 | 82 |

| Uganda | 78 | 100 | 63 | 67 | 64 | 93 | 100 | 79 | 59 |

| Tanzania | 75 | 100 | 50 | 100 | 96 | 73 | 100 | 83 | 0 |

| Bangladesh | 68 | 80 | 25 | 33 | 74 | 80 | 100 | 100 | 54 |

| Bottom Ranking Countries | |||||||||

| Sierra Leone | 17 | 0 | 0 | 0 | 35 | 40 | 50 | 8 | 0 |

| Chad | 14 | 0 | 0 | 17 | 30 | 11 | 50 | 4 | 0 |

| Haiti | 13 | 0 | 0 | 0 | 43 | 11 | 50 | 0 | 0 |

| Central African Republic | 11 | 0 | 0 | 0 | 10 | 11 | 0 | 17 | 50 |

| Somalia | 3 | 0 | 0 | 0 | 5 | 22 | 0 | 0 | 0 |

| Cost of Supply Studies | Techno-Economic Studies | Case Studies |

|---|---|---|

| [20]; [46,47,48,49,50,51,52]. | [53,54,55,56,57,58,59,60,61,62,63]. | [7], [64,65,66]. |

| Characteristics | Mini-Grids Supported by Financiers | Mini-Grids Developed by Supply Chain Entities | NGO/Community Supported Mini-Grids |

|---|---|---|---|

| Capacity to aggregate demand to achieve financial viability | Low | Low | Moderate |

| Flexibility to tailor technical solutions to variable demand and environmental conditions | Low/NA | Moderate | High |

| Flexibility to adapt programmes across geographic and environmental conditions and different consumer behaviour | Low/NA | Moderate | High |

| Capability to manage O&M risks and optimise O&M service delivery | Low | High | Low |

| Ability to optimise supply chain | Low | High | Low |

| Technical capacity to deliver high quality service throughout the project life | Low | High | Low |

| Capacity to aggregate demand to reduce administration costs significantly | Low | Moderate | Moderate |

| Characteristics | Mini-Grids Supported by Financiers | Mini-Grids Developed by Supply Chain Entities | NGO/Community Supported Mini-Grids |

|---|---|---|---|

| Knowledge of fund creation | High | Moderate | Low |

| Ability to optimise finance structure to specific local contexts | High | Low | Low |

| Ability to mobilise finances to scale at low transaction costs | High | Low | Low |

| Ability to access support finance to guarantee high risk consumer base | High | Low | High |

| Community Type | Strong Economic Linkages | Poor Economic Linkages |

|---|---|---|

| Vibrant community | Vibrant community with strong economic linkages | Vibrant community but poor economic linkages |

| Poor community strength | Poor community structure/ strength but strong economic linkages | Poor community strength and poor economic linkages |

© 2018 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bhattacharyya, S.C. Mini-Grids for the Base of the Pyramid Market: A Critical Review. Energies 2018, 11, 813. https://doi.org/10.3390/en11040813

Bhattacharyya SC. Mini-Grids for the Base of the Pyramid Market: A Critical Review. Energies. 2018; 11(4):813. https://doi.org/10.3390/en11040813

Chicago/Turabian StyleBhattacharyya, Subhes C. 2018. "Mini-Grids for the Base of the Pyramid Market: A Critical Review" Energies 11, no. 4: 813. https://doi.org/10.3390/en11040813

APA StyleBhattacharyya, S. C. (2018). Mini-Grids for the Base of the Pyramid Market: A Critical Review. Energies, 11(4), 813. https://doi.org/10.3390/en11040813