Technoeconomic and Policy Drivers of Project Performance for Bioenergy Alternatives Using Biomass from Beetle-Killed Trees

Abstract

:1. Introduction

Technoeconomic Analysis of Woody Biomass Energy

2. Methods

2.1. The Production Scenarios

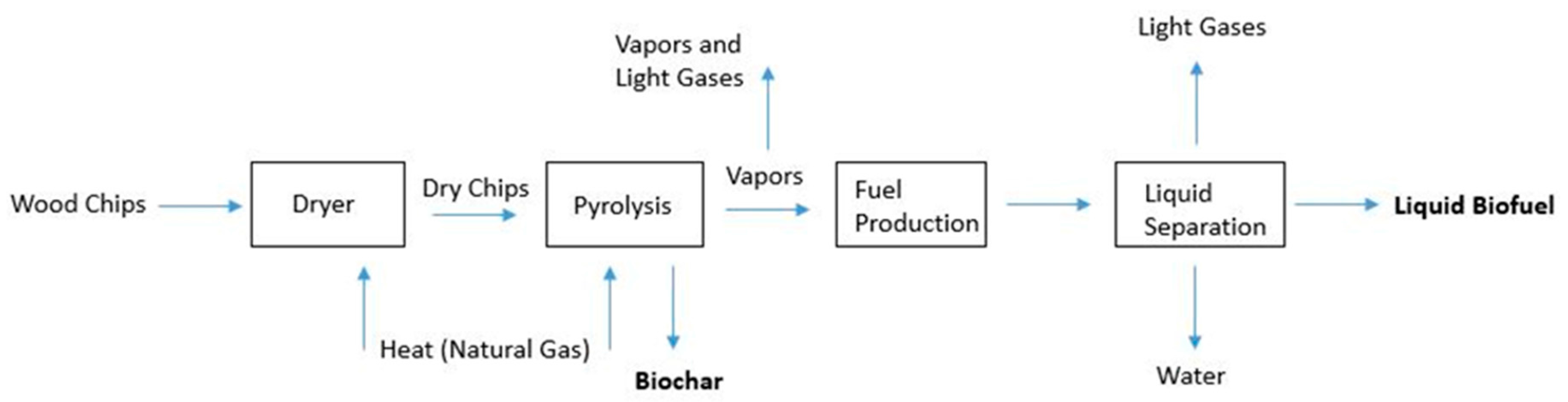

2.1.1. Biofuel with Biochar Scenario

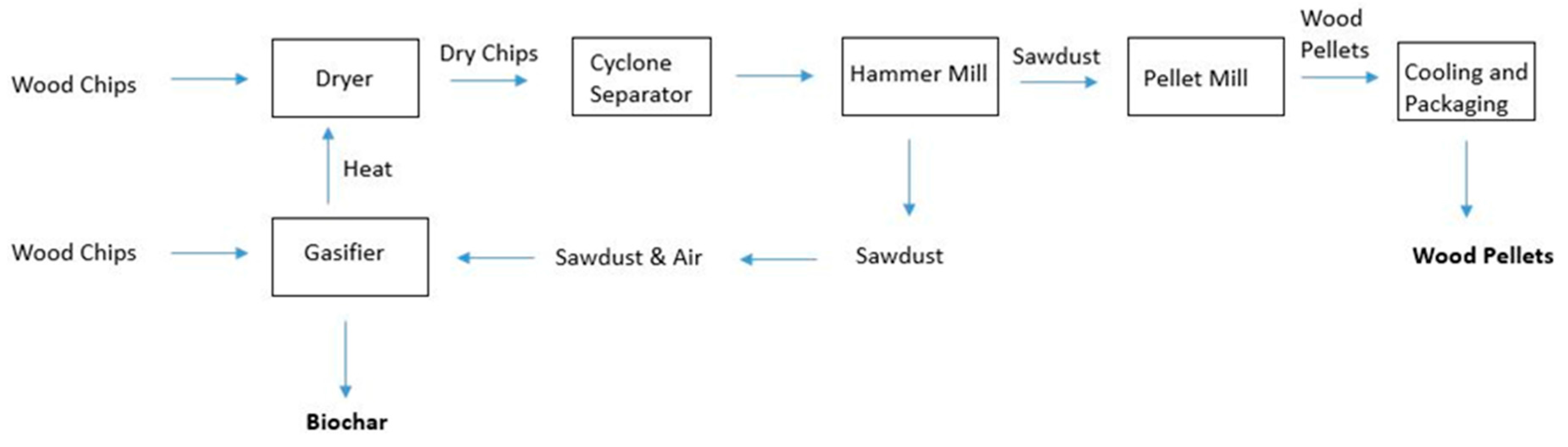

2.1.2. Pellet Scenario

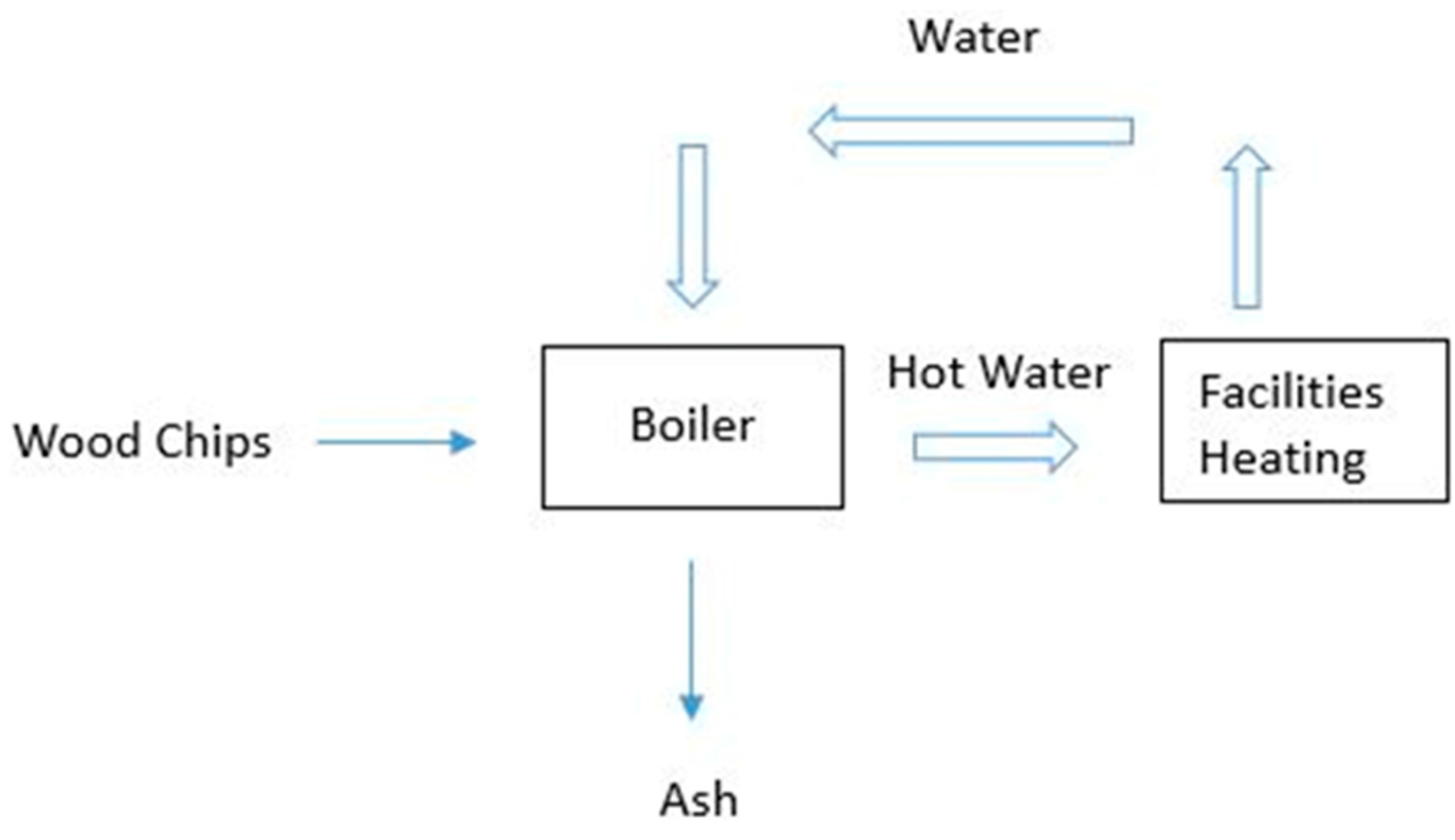

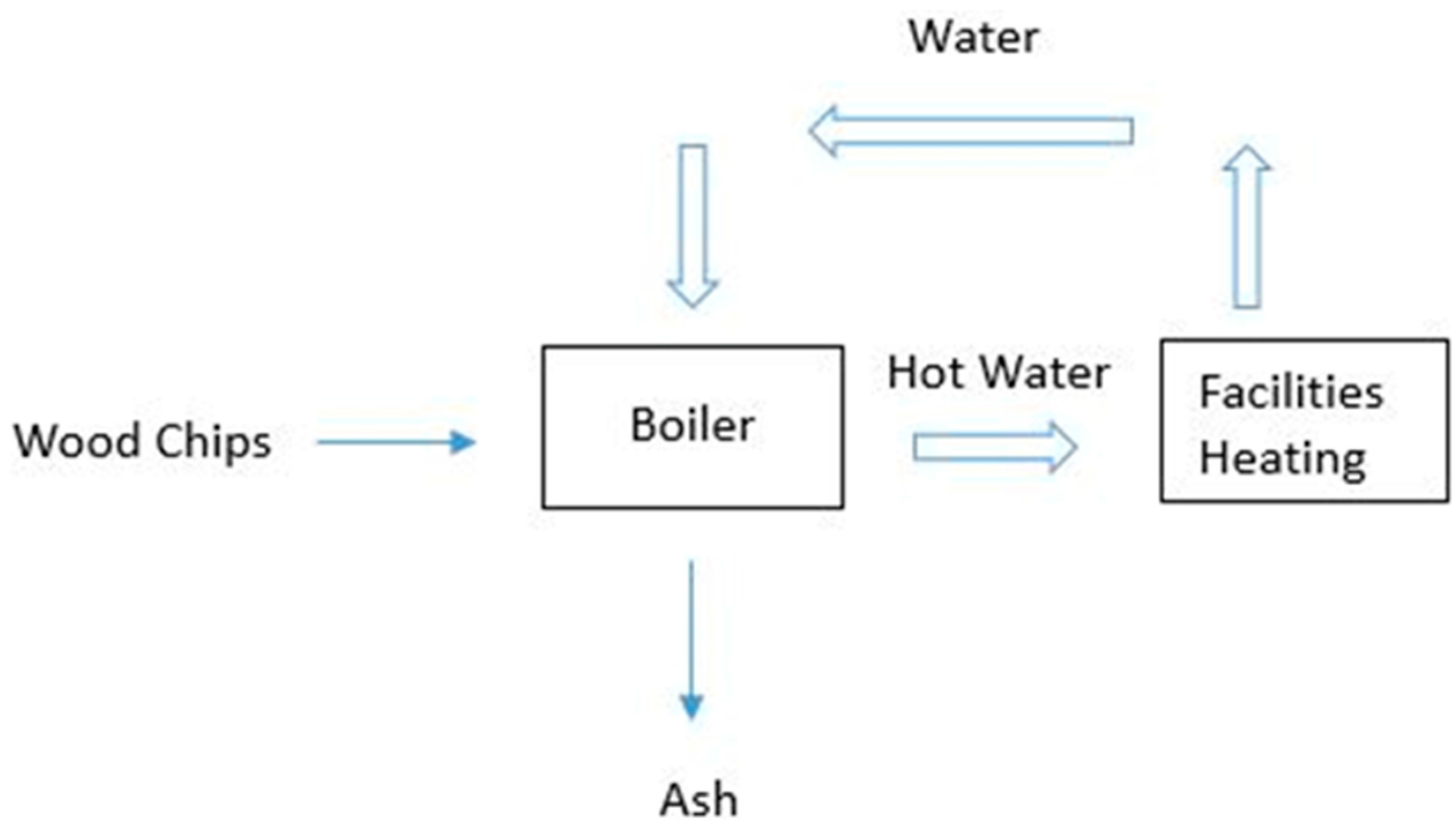

2.1.3. Heat Scenario

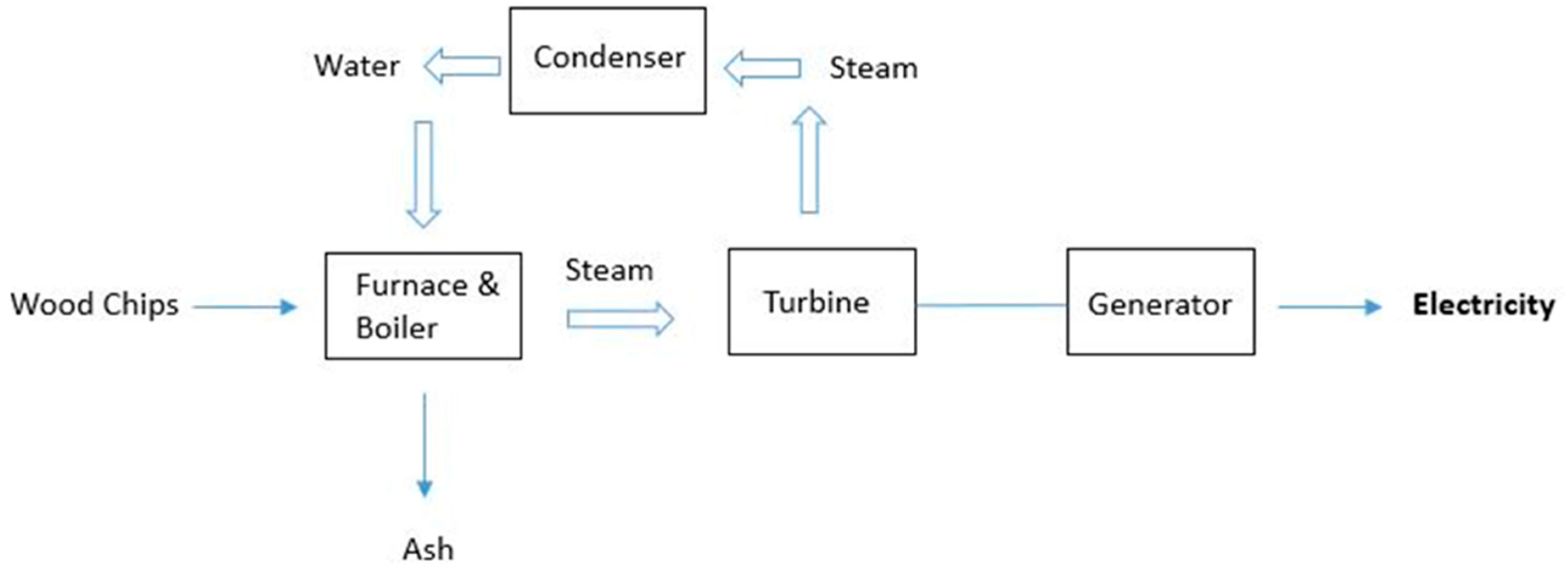

2.1.4. Power Scenario

2.2. Economic Analysis

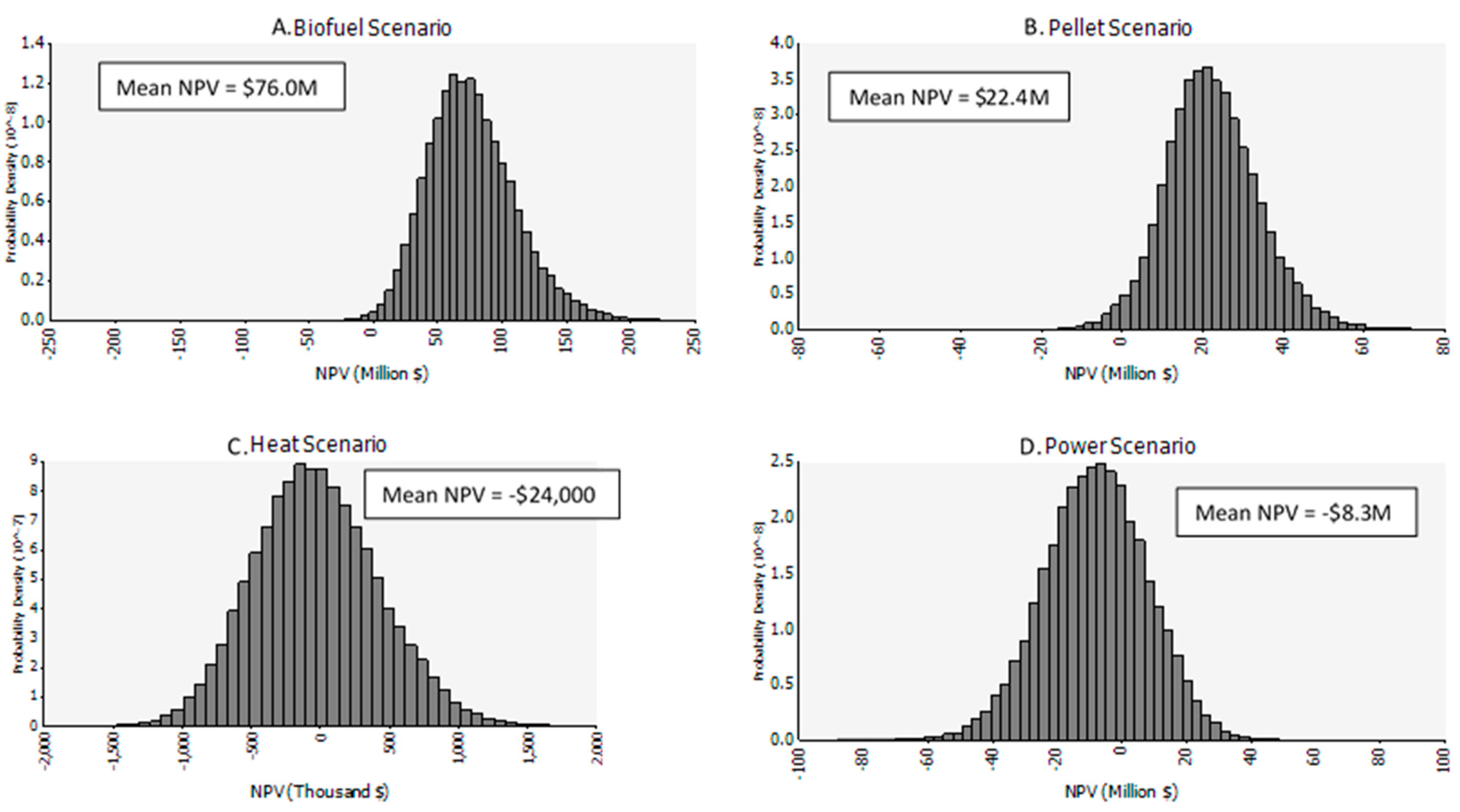

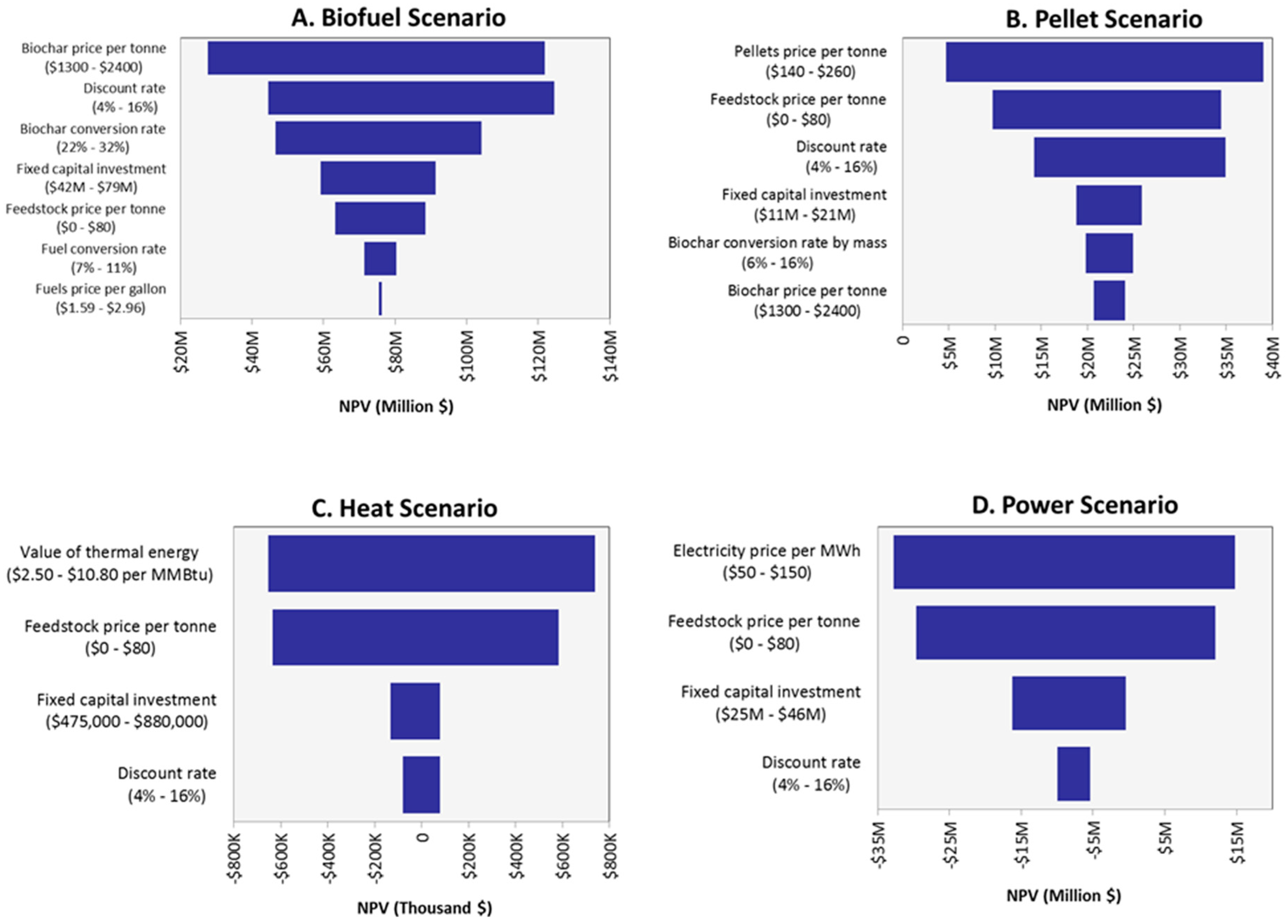

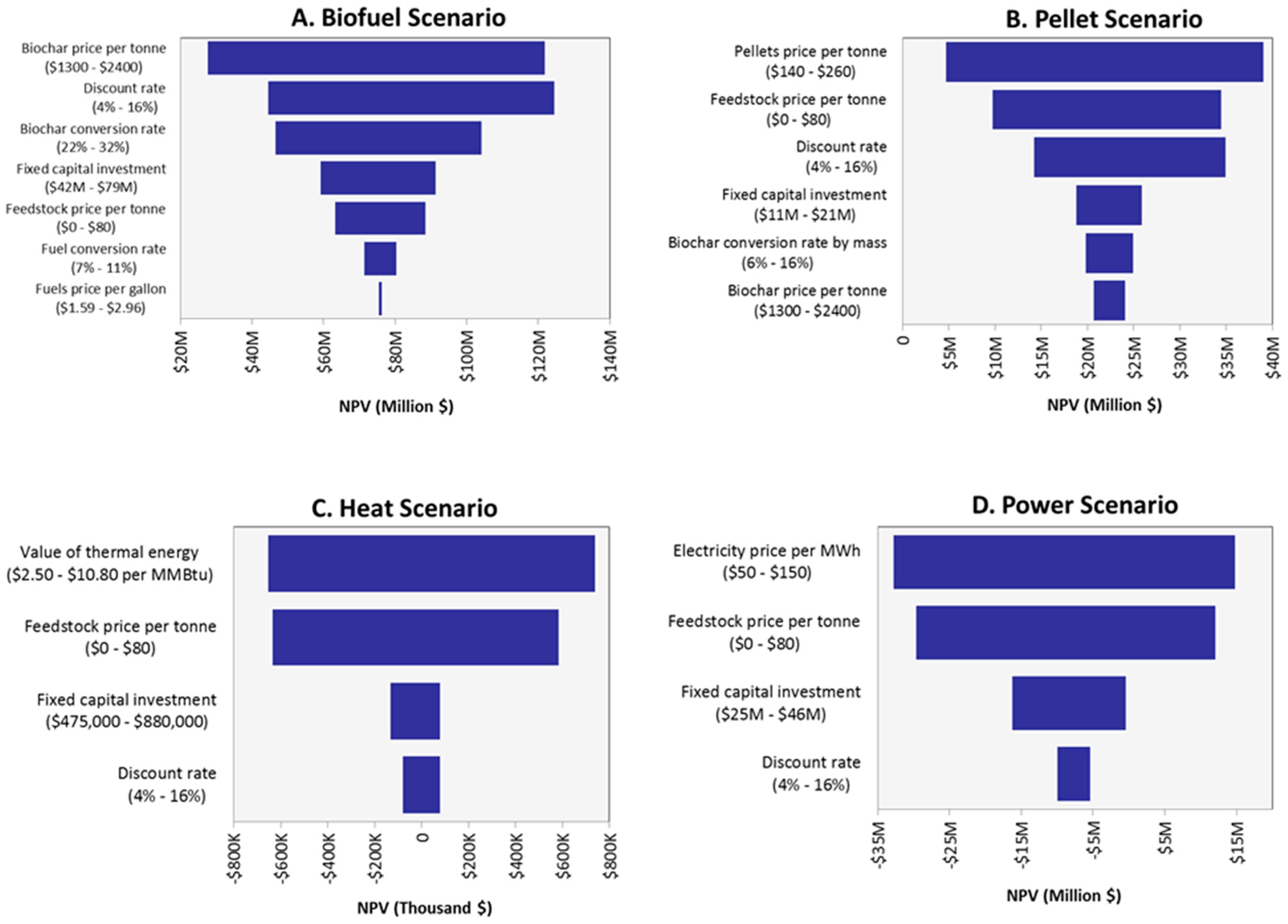

3. Results

4. Discussion

4.1. Industry Implications

4.2. Policy Implications

4.3. Forest Management Implications

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- US Energy Information Administration. Monthly Energy Review; Table 1.3; US Energy Information Administration: Washington, DC, USA, 2017.

- United States Congress. Energy Independence and Security Act of 2007. In Public Law; United States Congress: Washington, DC, USA, 2007; pp. 110–140. [Google Scholar]

- Becker, D.; Moseley, C.; Lee, C. A supply chain analysis framework for assessing state-level forest biomass utilization policies in the United States. Biomass Bioenergy 2011, 35, 1429–1439. [Google Scholar] [CrossRef]

- Ebers, A.; Malmsheimer, R.; Volk, T.; Newman, D. Inventory and classification of United States federal and state forest biomass electricity and heat policies. Biomass Bioenergy 2016, 84, 67–75. [Google Scholar] [CrossRef]

- U.S. Department of Energy. 2016 Billion-Ton Report: Advancing Domestic Resources for a Thriving Bioeconomy, Volume 1: Economic Availability of Feedstocks; Langholtz, M.H., Stokes, B.J., Eaton, L.M., Eds.; ORNL/TM-2016/160; Oak Ridge National Laboratory: Oak Ridge, TN, USA, 2016.

- Zanchi, G.; Pena, N.; Bird, N. Is woody bioenergy carbon neutral? A comparative assessment of emissions from consumption of woody bioenergy and fossil fuel. Glob. Chang. Biol. Bioenergy 2012, 4, 761–772. [Google Scholar] [CrossRef]

- Buchholz, T.; Hurteau, M.D.; Gunn, J.; Saah, D. A global meta-analysis of forest bioenergy greenhouse gas emission accounting studies. GCB Bioenergy 2016, 8, 281–289. [Google Scholar] [CrossRef]

- Wienk, C.L.; Sieg, C.H.; McPherson, G.R. Evaluating the role of cutting treatments, fire and soil seed banks in an experimental framework in ponderosa pine forests of the Black Hills, South Dakota. For. Ecol. Manag. 2004, 192, 375–393. [Google Scholar] [CrossRef]

- Hutto, R.L. The ecological importance of severe wildfires: Some like it hot. Ecol. Appl. 2008, 18, 1827–1834. [Google Scholar] [CrossRef] [PubMed]

- Westerling, A.L.; Hidalgo, H.G.; Cayan, D.R.; Swetnam, T.W. Warming and earlier spring increase western U.S. forest wildfire activity. Science 2006, 313, 940–943. [Google Scholar] [CrossRef] [PubMed]

- Littell, J.S.; McKenzie, D.; Peterson, D.L.; Westerling, A.L. Climate and wildfire area burned in western U.S. ecoprovinces, 1916–2003. Ecol. Appl. 2009, 19, 1003–1021. [Google Scholar] [CrossRef] [PubMed]

- Miller, J.; Safford, H.; Crimmins, M.; Thode, A. Quantitative evidence for increasing forest fire severity in the Sierra Nevada and southern Cascade Mountains, California and Nevada, USA. Ecosystems 2009, 12, 16–32. [Google Scholar] [CrossRef]

- Cansler, C.A.; McKenzie, D. Climate, fire size, and biophysical setting control fire severity and spatial pattern in the northern Cascade Range, USA. Ecol. Appl. 2014, 24, 1037–1056. [Google Scholar] [CrossRef] [PubMed]

- Bentz, B.J.; Regniere, J.; Fettig, C.J.; Hansen, E.M.; Hicke, J.; Hayes, J.L.; Kelsey, R.; Negron, J.; Seybold, S. Climate change and bark beetles of the western U.S. and Canada: Direct and indirect effects. BioScience 2010, 60, 602–613. [Google Scholar] [CrossRef]

- Chapman, T.B.; Veblen, T.T.; Schoennagel, T. Spatiotemporal patterns of mountain pine beetle activity in the southern Rocky Mountains. Ecology 2012, 93, 2175–2185. [Google Scholar] [CrossRef] [PubMed]

- United States Department of Agriculture Forest Service. Western Bark Beetle Strategy. 2011. Available online: https://www.fs.fed.us/restoration/Bark_Beetle/ (accessed on 24 January 2018).

- Hart, S.J.; Veblen, T.T.; Eisenhart, K.S.; Jarvis, D.; Kulakowski, D. Drought induces spruce beetle (Dendroctonus rufipennis) outbreaks across northwestern Colorado. Ecology 2014, 95, 930–939. [Google Scholar] [CrossRef] [PubMed]

- Gan, J.; Smith, C.T. Availability of logging residues and potential for electricity production and carbon displacement in the USA. Biomass Bioenergy 2006, 30, 1011–1020. [Google Scholar] [CrossRef]

- Keefe, R.; Anderson, N.; Hogland, J.; Muhlenfeld, K. Woody Biomass Logistics: Cellulosic Energy Cropping Systems; Karlen, D., Ed.; John Wiley & Sons: Hoboken, NJ, USA, 2014. [Google Scholar]

- McKendry, P. Energy production from biomass (part 2): Conversion technologies. Bioresour. Technol. 2002, 83, 47–54. [Google Scholar] [CrossRef]

- Patel, M.; Kumar, X. Techno-economic and life cycle assessment on lignocellulosic biomass thermochemical conversion technologies: A review. Renew. Sustain. Energy Rev. 2016, 53, 1486–1499. [Google Scholar] [CrossRef]

- Zhao, X.; Yao, G.; Tyner, W. Quantifying breakeven price distributions in stochastic techno-economic analysis. Appl. Energy 2016, 183, 318–326. [Google Scholar] [CrossRef]

- Bridgwater, A.; Toft, A.; Brammer, J. A techno-economic comparison of power production by biomass fast pyrolysis with gasification and combustion. Renew. Sustain. Energy Rev. 2002, 6, 181–248. [Google Scholar] [CrossRef]

- Sarkar, S.; Kumar, A.; Sultana, A. Biofuels and biochemical production from forest biomass in Western Canada. Energy 2011, 36, 6251–6262. [Google Scholar] [CrossRef]

- Shabangu, S.; Woolf, D.; Fisher, E.; Angenent, L.; Lehmann, J. Techno-economic assessment of biomass slow pyrolysis into different biochar and methanol concepts. Fuel 2014, 117, 742–748. [Google Scholar] [CrossRef]

- Beagle, E.; Belmont, E. Technoeconomic assessment of beetle kill biomass co-firing in existing coal fired power plants in the Western United States. Energy Policy 2016, 97, 429–438. [Google Scholar] [CrossRef]

- Jones, S.; Meyer, P.; Snowden-Swan, L.; Padmaperuma, A.; Tan, E.; Dutta, A.; Jacobson, J.; Cafferty, K. Process Design and Economics for the Conversion of Lignocellulosic Biomass to Hydrocarbon Fuels; PNNL-23053; NREL/TP-5100-61178; Pacific Northwest National Laboratory: Richland, WA, USA; National Renewable Energy Laboratory: Golden, CO, USA; Idaho National Laboratory: Idaho Falls, ID, USA, 2013.

- Pirraglia, A.; Gonzalez, R.; Saloni, D. Techno-economical analysis of wood pellets production for U.S. manufacturers. BioResources 2010, 5, 2374–2390. [Google Scholar]

- Qian, Y.; McDow, W. The Wood Pellet Value Chain; U.S. Endowment for Forestry and Communities: Greenville, SC, USA, 2013. [Google Scholar]

- US Energy Information Administration. Electric Power Annual: Average Price of Electricity to Ultimate Customers by End-Use Sector. 2016. Available online: https://www.eia.gov/electricity/annual/html/epa_02_10.html (accessed on 24 January 2018).

- De Jong, S.; Hoefnagels, R.; Faaij, A.; Slade, R.; Mawhood, R.; Junginger, M. The feasibility of short-term production strategies for renewable jet fuels—A comprehensive techno-economic comparison. Biofuels Bioprod. Biorefin. 2015, 9, 778–800. [Google Scholar] [CrossRef]

- Wright, M.; Daugaard, D.; Satrio, J.; Brown, R. Techno-economic analysis of biomass fast pyrolysis to transportation fuels. Fuel 2010, 89, S2–S10. [Google Scholar] [CrossRef]

- Towler, G.; Sinnott, R. Chemical Engineering Design: Principles, Practice and Economics of Plant and Process Design; Butterworth-Heinemann: Oxford, UK, 2013. [Google Scholar]

- Swanson, R.; Platon, A.; Satrio, J.; Brown, R. Techno-economic analysis of biomass-to-liquids production based on gasification. Fuel 2010, 89, S11–S19. [Google Scholar] [CrossRef]

- Peters, M.; Timmerhaus, K.; West, R. Plant Design and Economics for Chemical Engineers, 5th ed.; McGraw Hill: Boston, MA, USA, 2003. [Google Scholar]

- US Bureau of Labor Statistics. Occupational Employment Statistics. 2017. Available online: https://www.bls.gov/oes/ (accessed on 24 January 2018).

- Bergman, R.; Maker, T. Fuels for Schools: Case Study in Darby, Montana; General Technical Report FPL-GTR-173; Madison, W.I., Ed.; U.S. Department of Agriculture, Forest Service, Forest Products Laboratory: Madison, WI, USA, 2007; 21p.

- Sprow, F. Evaluation of research expenditures using triangular distribution functions and Monte Carlo methods. Ind. Eng. Chem. 1967, 59, 35–38. [Google Scholar] [CrossRef]

- Kim, D.; Anderson, N.; Chung, W. Financial performance of a mobile pyrolysis system used to produce biochar from sawmill residues. For. Prod. J. 2015, 65, 189–197. [Google Scholar] [CrossRef]

- U.S. Energy Information Administration. Petroleum and Other Liquids Data: New York Harbor No. 2 Heating Oil Future Contract 1. 2017. Available online: https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=EER_EPD2F_PE1_Y35NY_DPG&f=A (accessed on 24 January 2018).

- U.S. Energy Information Administration. Petroleum and Other Liquids Data: New York Harbor Reformulated RBOB Regular Gasoline Future Contract 1. 2017. Available online: https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=EER_EPMRR_PE1_Y35NY_DPG&f=A (accessed on 24 January 2018).

- U.S. Energy Information Administration. Henry Hub Natural Gas Spot Price. 2017. Available online: http://tonto.eia.gov/dnav/ng/hist/rngwhhdm.htm (accessed on 24 January 2018).

- U.S. Environmental Protection Agency. Biomass Combined Heat and Power Catalog of Technologies; U.S. Environmental Protection Agency Combined Heat and Power Partnership: Washington, DC, USA, 2007.

- Fantozzi, F.; Bartocci, P.; D’Alessandro, B.; Arampatzis, S.; Manos, B. Public-private partnerships value in bioenergy projects: Economic feasibility analysis based on two case studies. Biomass Bioenergy 2014, 66, 387–397. [Google Scholar] [CrossRef]

- U.S. Department of Agriculture. USDA Awards Funds to Expand, Accelerate Wood Energy and Wood Products Markets in 19 States. USDA Press Release No. 0115.16; 2016. Available online: https://www.usda.gov/media/press-releases/2016/05/13/usda-awards-funds-expand-accelerate-wood-energy-and-wood-products (accessed on 24 January 2018).

- U.S. Department of Energy. Loan Programs Office: Bioenergy and Biofuels Projects. 2017. Available online: https://energy.gov/lpo/bioenergy-biofuels-projects (accessed on 24 January 2018).

- Aguilar, F.; Song, N.; Shifley, S. Review of consumption trends and public policies promoting woody biomass as an energy feedstock in the US. Biomass Bioenergy 2011, 35, 3708–3718. [Google Scholar] [CrossRef]

- Couture, T.; Cory, K.; Kreycik, C.; Williams, E. A Policymaker’s Guide to Feed-in Tariff Policy Design; Technical Report: NREL/TP-6A2-44849; National Renewable Energy Laboratory: Golden, CO, USA, 2010.

- O’Shaughnessy, E.; Heeter, J.; Liu, C.; Nobler, E. Status and Trends in the U.S. Voluntary Green Power Market (2014 Data); Technical Report: NREL/TP-6A20-65252; National Renewable Energy Laboratory: Golden, CO, USA, 2015.

- US Federal Register. Biomass Crop Assistance Program; Final Rule. 7 CFR Part 1450; USDA: Washington, DC, USA, 2010; Volume 75, pp. 66202–66243.

- NC Clean Energy Technology Center. Database of State Incentives for Renewables and Efficiency; North Carolina State University: Raleigh, NC, USA, 2018. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Alternative Scenarios | ||||

|---|---|---|---|---|

| 1. Biofuel | 2. Pellet | 3. Heat | 4. Power | |

| Production technology | Pyrolysis | Pellet mill with gasifier | Commercial boiler | Combustion with steam turbine |

| Primary product | Biofuel | Wood pellets | Thermal energy | Electricity |

| Co-product | Biochar | Biochar | None | None |

| Feedstock processing capacity | 10 t h−1 | 9 t h−1 | 0.4 t h−1 | 10 t h−1 |

| Primary product yield | 1.8 MM gal | 56,500 t | 22,400 MMBtu | 89,100 MWh |

| Co-product yield | 17,700 t | 620 t | NA | NA |

| Total Capital Investment | $80.0 MM | $18.3 MM | $680,000 | $39.3 MM |

| Annual operating costs | $11.3 MM | $6.2 MM | $84,000 | $5.1 MM |

| Annual labor costs | $2.6 MM | $1.0 MM | $11,000 | $0.9 MM |

| Annual operating time | 6570 h | 7446 h | 5256 h | 7884 h |

| Variable | Value | Source |

|---|---|---|

| Discount rate | 10% | [24,31,32] |

| Loan financing | 80% loan financed | [31] |

| Loan interest rate | 8% APR a | [22,27] |

| Loan term | 10 year payback period | [22,27] |

| Federal income tax rate | 35% a | [33] |

| Plant life | 20 years | [32,34] |

| Depreciation | Straight-line method, 10 years, zero salvage value | [33] |

| Insurance and local taxes | 2% of TCI b | [33] |

| Variable | Scenarios | Minimum | Base-Case | Maximum | Source |

|---|---|---|---|---|---|

| Discount Rate | All | 4% | 10% | 16% | [24,31,32] |

| Feedstock price | All | $0 t−1 | $40 t−1 | $80 t−1 | Industry Partners; [24] |

| Fixed Capital Investment | All | −30% | Scenario-specific | +30% | Table 2 |

| Biochar conversion rate | Biofuel | 22% | 27% | 32% | Industry Partners |

| Biochar conversion rate | Pellet | 6% | 11% | 16% | Industry Partners |

| Biofuel conversion rate | Biofuel | 7% | 9% | 11% | Industry Partners |

| Pellets price | Pellet | $178 t−1 | $200 t−1 | $222 t−1 | Industry Partners; [28] |

| Biochar price | Biofuel, Pellet | $899 t−1 | $1834 t−1 | $2,778 t−1 | Industry Partners; [39] |

| Biofuel price | Biofuel | $1.59 gal−1 | $2.36 gal−1 | $2.96 gal−1 | [40,41] |

| Electricity price | Power | $50 MWh−1 | $100 MWh−1 | $150 MWh−1 | Industry Partners |

| Heat price | Heat | $2.52 MMBtu−1 | $5.35 MMBtu−1 | $10.83 MMBtu−1 | [42] |

| Biofuel Scenario | Pellet Scenario | Heat Scenario | Power Scenario | |

|---|---|---|---|---|

| Mean NPV at $40 t−1 feedstock price | $76.0M | $22.4 M | −$24,000 | −$8.3 M |

| Maximum feedstock price for NPV = 0 | $227 t−1 | $97 t−1 | $39 t−1 | $26 t−1 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Campbell, R.M.; Anderson, N.M.; Daugaard, D.E.; Naughton, H.T. Technoeconomic and Policy Drivers of Project Performance for Bioenergy Alternatives Using Biomass from Beetle-Killed Trees. Energies 2018, 11, 293. https://doi.org/10.3390/en11020293

Campbell RM, Anderson NM, Daugaard DE, Naughton HT. Technoeconomic and Policy Drivers of Project Performance for Bioenergy Alternatives Using Biomass from Beetle-Killed Trees. Energies. 2018; 11(2):293. https://doi.org/10.3390/en11020293

Chicago/Turabian StyleCampbell, Robert M., Nathaniel M. Anderson, Daren E. Daugaard, and Helen T. Naughton. 2018. "Technoeconomic and Policy Drivers of Project Performance for Bioenergy Alternatives Using Biomass from Beetle-Killed Trees" Energies 11, no. 2: 293. https://doi.org/10.3390/en11020293

APA StyleCampbell, R. M., Anderson, N. M., Daugaard, D. E., & Naughton, H. T. (2018). Technoeconomic and Policy Drivers of Project Performance for Bioenergy Alternatives Using Biomass from Beetle-Killed Trees. Energies, 11(2), 293. https://doi.org/10.3390/en11020293