Renewable and Sustainable Energy Transitions for Countries with Different Climates and Renewable Energy Sources Potentials

Abstract

1. Introduction

2. General Comparison of the Climate Conditions and Populations of Italy and Finland

3. Energy System Modeling for Italy

3.1. Demand Data

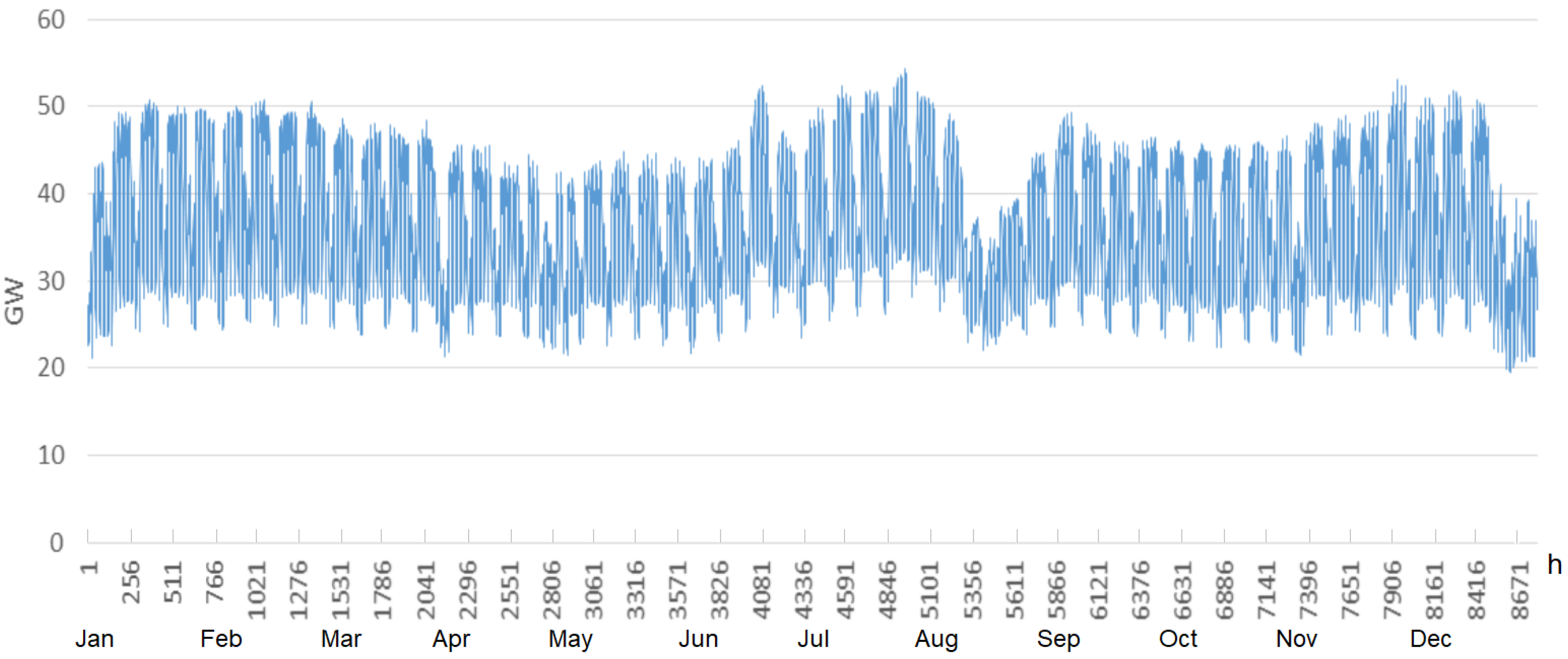

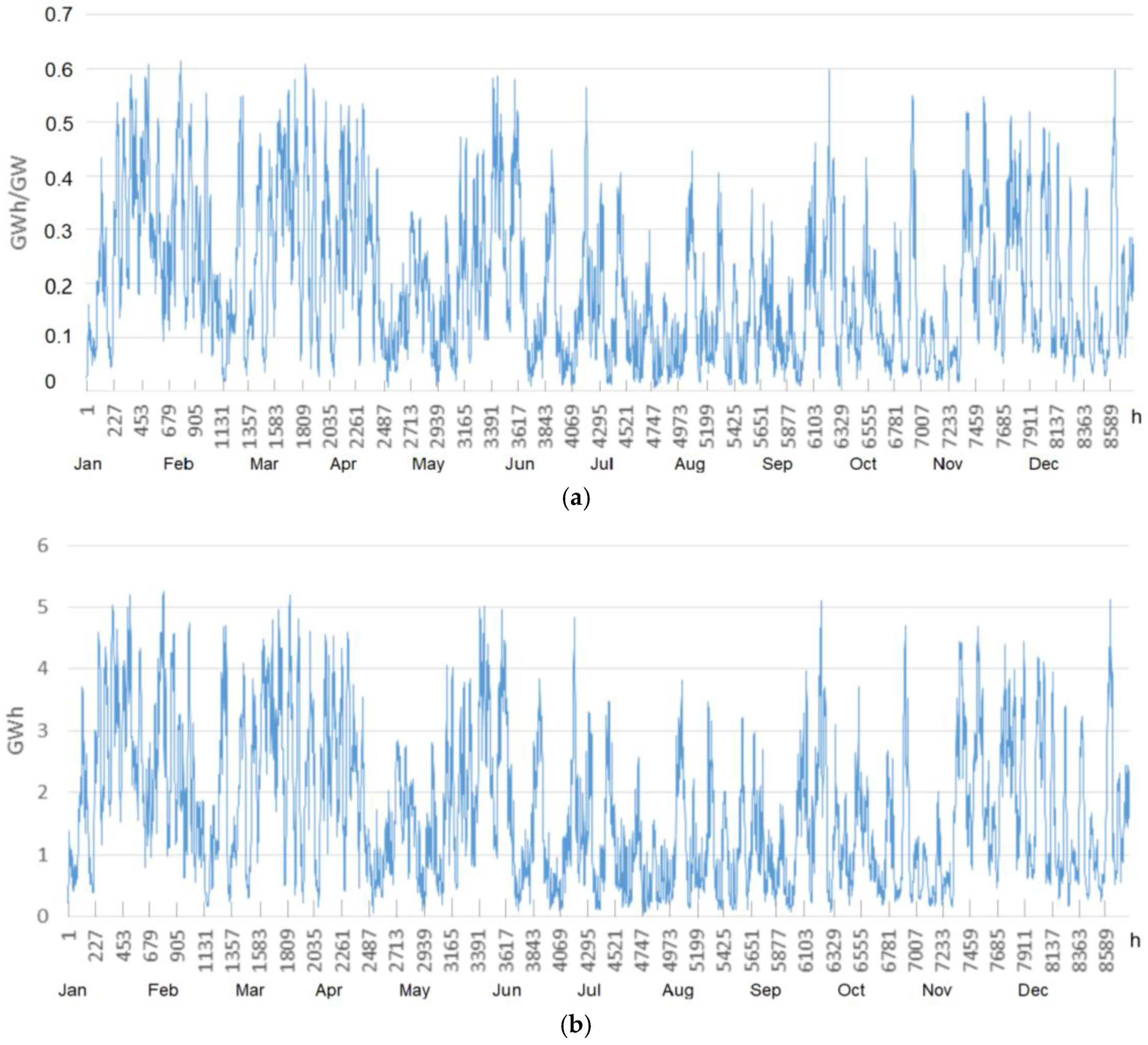

3.1.1. Electricity Demand

3.1.2. Heat Demand

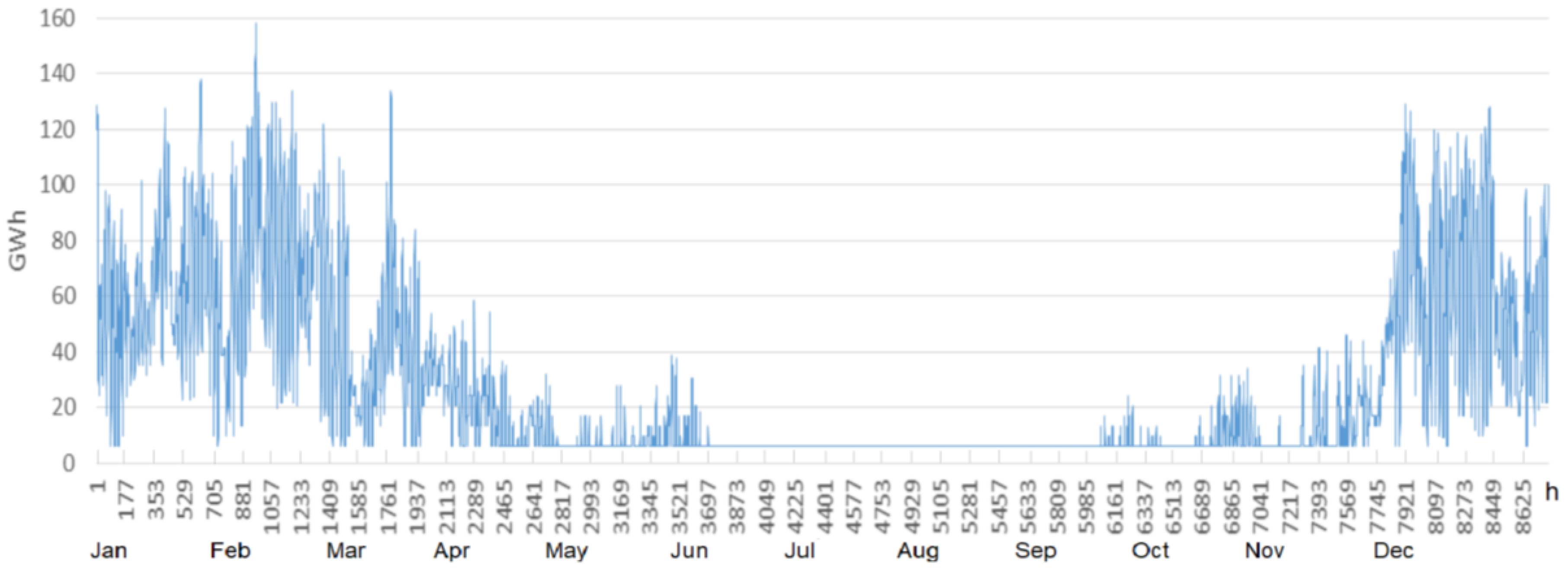

3.1.3. Cooling Demand

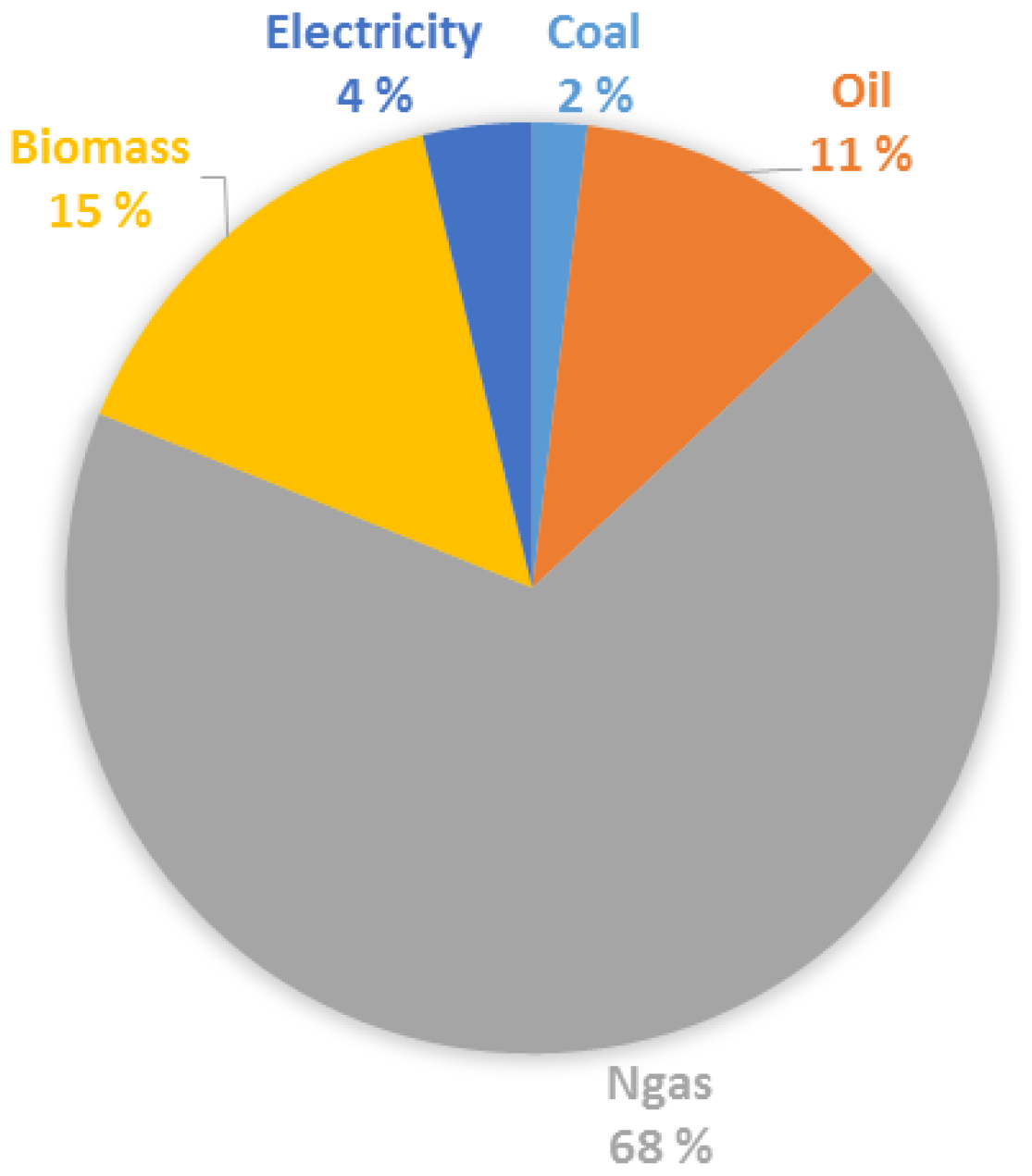

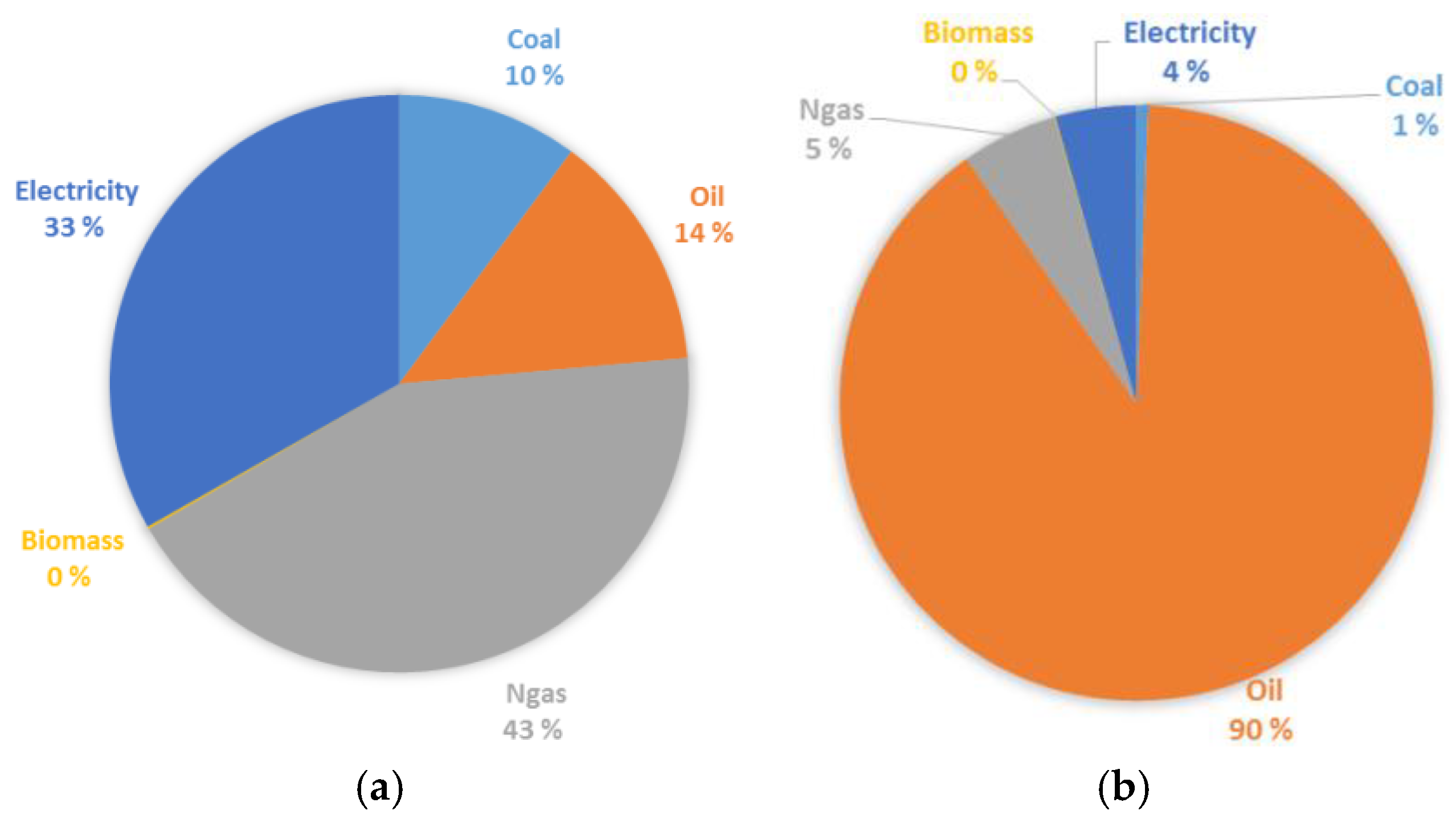

3.1.4. Industry and Other Fuel Consumption

3.1.5. Transport

3.2. Supply Data

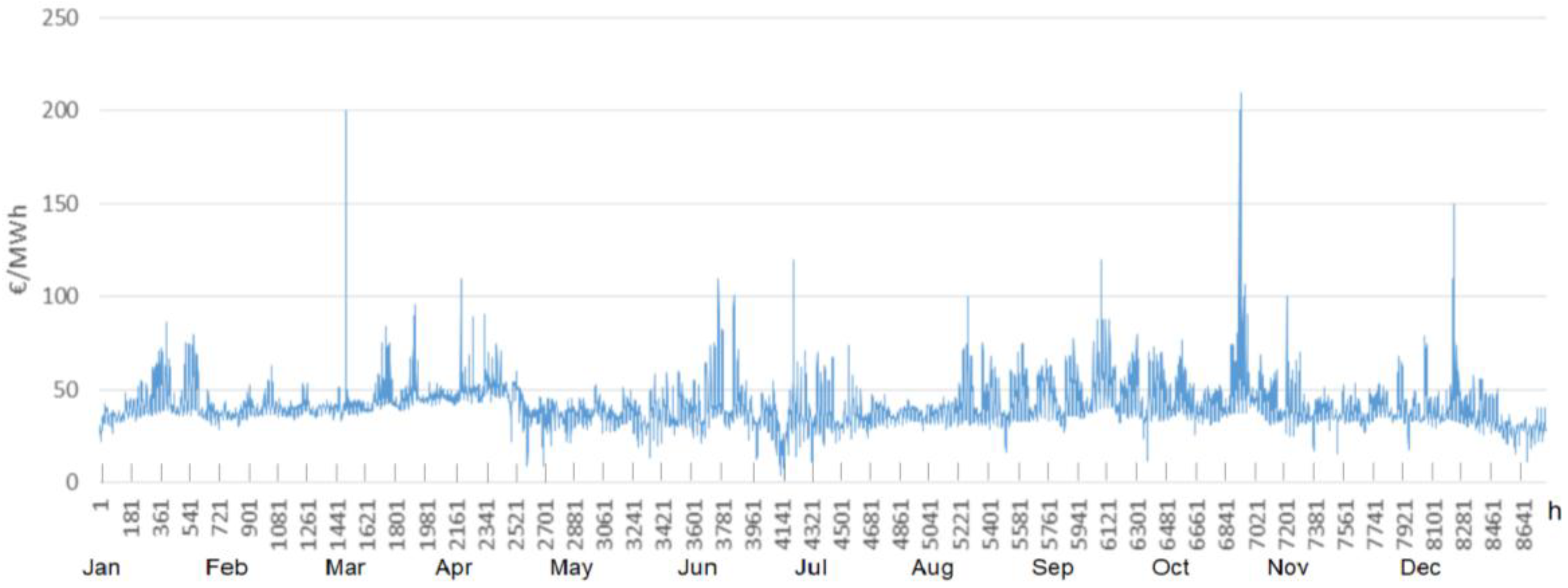

3.2.1. Electricity Supply

Solar

Wind

Geothermal

Nuclear Power

Hydropower

Condensing Power

3.2.2. Combined Heat and Power Supply

- (1)

- Cogeneration power plants fed by fossil fuels: 851 MW;

- (2)

- Cogeneration power plants fed by biomass: 78 MW;

- (3)

- Auxiliary boilers fed by fossil fuels: 4726 MW (thermal);

- (4)

- Auxiliary boilers fed by biomass: 336 MW (thermal);

- (5)

- Geothermal: 240 GWh as heat production;

- (6)

- Waste treatments;

- (7)

- HPs.

3.2.3. Thermal Plant Supply and Fuel Mix

3.2.4. CO2 Emission Data

3.3. Model Results for the Base Case of Italy

- (1)

- Electricity consumption: 318.5 TWh [39];

- (2)

- Electricity production: (a) condensing power plants: 94.9 TWh; (b) CHP power plants: 88.52 TWh; (c) RES: 93 TWh;

- (3)

- Import: 44.4 TWh;

- (4)

- Export: 2.37 TWh.

4. Energy System Modeling for Finland

4.1. Demand Data

4.1.1. Electricity Demand

4.1.2. Heat Demand

4.1.3. Cooling Demand

4.1.4. Industry and Other Fuel Consumption

4.1.5. Transport

4.2. Supply Data

4.2.1. Electricity Supply

Nuclear Power

Wind

Hydropower

Solar

4.2.2. Combined Heat and Power Supply

4.2.3. Thermal Plant Supply and Fuel Mix

4.2.4. CO2 Emission Data

4.3. Model Results for the Base Case of Finland

- (1)

- Electricity demand: 84 TWh [57];

- (2)

- Electricity production: (a) CHP power plants: 23.33 TWh; (b) nuclear: 22.67 TWh; (c) RES: 13.44 TWh; (d) condensing power plants: 8.9 TWh;

- (3)

- Import: 17.6 TWh;

- (4)

- Export: 1.87 TWh.

- (1)

- District heating Demand: 33.2 TWh [57];

- (2)

- District heating Production: 36.8 TWh, including: (a) CHP plants produced 26.1 TWh; (b) Auxiliary boilers supplied 10.7 TWh.

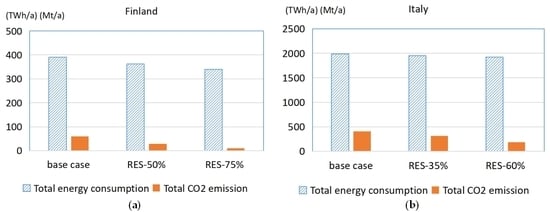

5. Model Optimization Results from Different Renewable Energy Sources Scenarios for Energy Transition

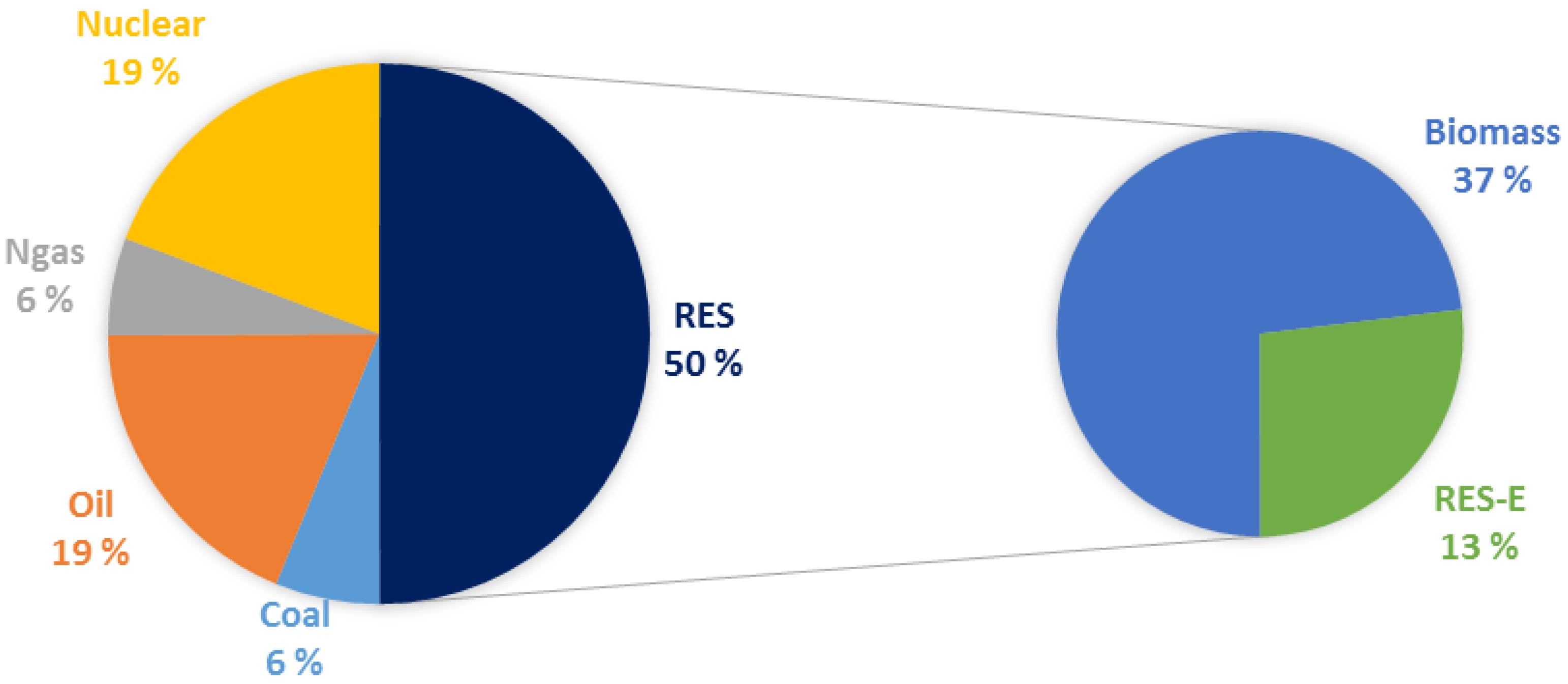

5.1. Italian Scenarios and Model Results

- (1)

- Improving energy efficiency in buildings because of the large number of old houses;

- (2)

- Introducing energy savings in industrial processes;

- (3)

- Developing the district heating network in all the municipalities in climate Zones E and F;

- (4)

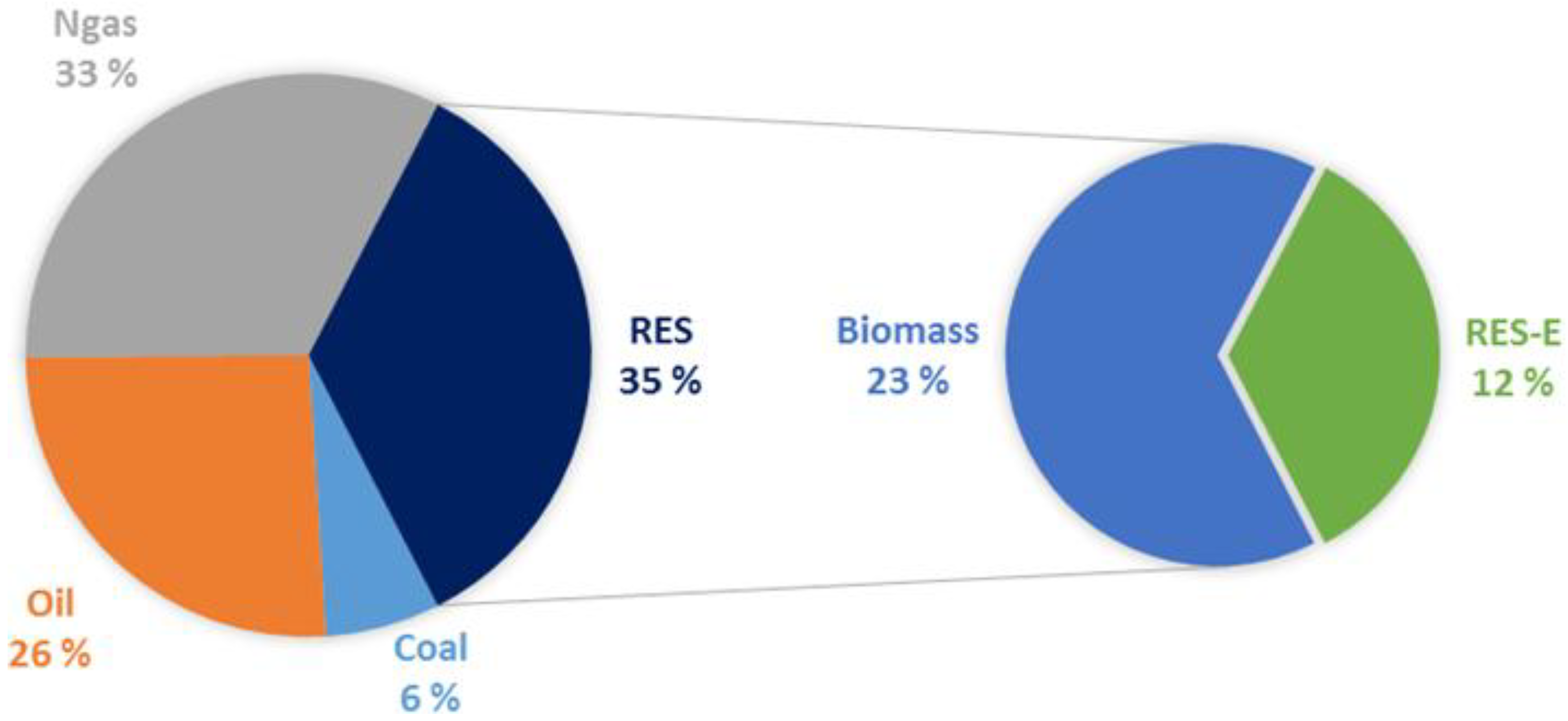

- Ensuring the highest share of RES in district heating production, approximately 37%;

- (5)

- Increasing the use of biomass throughout the whole system, especially biofuels.

5.2. Finnish Scenarios and Model Results

- (1)

- Wind power production will rise to 6 TWh, compared to 0.7 TWh in 2013;

- (2)

- Hydropower will increase to 14 TWh, compared to 12.67 TWh in 2013;

- (3)

- CHP production from wood chips will be equivalent to at least 28 TWh of fuel;

- (4)

- Renewable energy production by HP should be increased to 8 TWh;

- (5)

- The use of biofuels in the transport sector will be increased to 7 TWh and biogas to 0.7 TWh.

5.3. Results and Discussion

6. Possible Power Transmission and Discussion

7. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Lin, B.; Omoju, O.E. Focusing on the right targets: Economic factors driving non-hydro renewable energy transition. Renew. Energy 2017, 113, 52–63. [Google Scholar] [CrossRef]

- European Commission. Progress towards Completing the Internal Energy Market; European Commission: Brussels, Belgium, 2014. [Google Scholar]

- European Commission. Making the Internal Energy Market Work; European Commission: Brussels, Belgium, 2012. [Google Scholar]

- Gourvitch, N. Merit Order Effect; Green Giraffe Energy Bankers: London, UK, 2013. [Google Scholar]

- European Commission. Launching the Public Consultation Process on a New Energy Market Design; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- Zipp, A. The marketability of variable renewable energy in liberalized electricity markets—An empirical analysis. Renew. Energy 2018, 113, 1111–1121. [Google Scholar] [CrossRef]

- European Environment Agency. Share of Renewable Energy in Gross Final Energy Consumption. 2016. Available online: http://www.eea.europa.eu/data-and-maps/indicators/renewable-gross-final-energy-consumption-3/assessment#tab-news-and-articles (accessed on 8 August 2018).

- European Commission. A Policy Framework for Climate and Energy in the Period from 2020 to 2030; European Commission: Brussels, Belgium, 2014. [Google Scholar]

- European Commission. Energy Roadmap 2050; European Commission: Brussels, Belgium, 2011. [Google Scholar]

- European Commission. The EU Emissions Trading System (EU ETS); European Commission: Brussels, Belgium, 2013. [Google Scholar]

- Child, C.; Breyer, C. Transition and transformation: A review of the concept of change in the progress towards future sustainable energy systems. Energy Policy 2017, 107, 11–26. [Google Scholar] [CrossRef]

- Pye, S.; Sabio, N.; Strachan, N. An integrated systematic analysis of uncertainties in UK energy transition pathways. Energy Policy 2015, 87, 673–684. [Google Scholar] [CrossRef]

- Bonneuil, N.; Boucekkine, R. Optimal transition to renewable energy with threshold of irreversible pollution. Eur. J. Oper. Res. 2016, 248, 257–262. [Google Scholar] [CrossRef]

- Ruppert-Winkel, C.; Hussain, W.; Hauber, J. Understanding the regional process of energy transition in Marin County, California: Applying a Three-Phase-Model based on case studies from Germany. Energy Res. Soc. Sci. 2016, 14, 33–45. [Google Scholar] [CrossRef]

- Lange, M.; O’Hagan, M.; Devoy, R.R.N.; Martin, T.L.; Cummins, V. Governance barriers to sustainable energy transitions—Assessing Ireland’s capacity towards marine energy futures. Energy Policy 2018, 113, 623–632. [Google Scholar] [CrossRef]

- Lind, A.; Espegren, K. The use of energy system models for analyzing the transition to low-carbon cities—The case of Oslo. Energy Strat. Rev. 2017, 15, 44–56. [Google Scholar] [CrossRef]

- Guidolin, M.; Guseo, R. The German energy transition: Modeling competition and substitution between nuclear power and Renewable Energy Technologies. Renew. Sustain. Energy Rev. 2016, 60, 1498–1504. [Google Scholar] [CrossRef]

- Anil, K.; Dmitrii, B.; Onur, P.; Upeksha, C.; Arman, A.; Christian, B. An energy transition pathway for Turkey to achieve 100% renewable energy powered electricity, desalination and non-energetic industrial gas demand sectors by 2050. Sol. Energy 2017, 158, 218–235. [Google Scholar]

- Mediavilla, M.; Castro, C.D.; Capellán, I.; Miguel, L.J.; Arto, I.; Frechoso, F. The transition towards renewable energies: Physical limits and temporal conditions. Energy Policy 2013, 52, 297–311. [Google Scholar] [CrossRef]

- Zakeri, B.; Virasjoki, V.; Syri, S.; Connolly, D.; Mathiesen, B.V.; Welsch, M. Impact of Germany’s energy transition on the Nordic power market—A market-based multi-region energy system model. Energy 2016, 115, 1640–1662. [Google Scholar] [CrossRef]

- Vidadili, N.; Suleymanov, E.; Bulut, C.; Mahmudlu, C. Transition to renewable energy and sustainable energy development in Azerbaijan. Renew. Sustain. Energy Rev. 2017, 80, 1153–1161. [Google Scholar] [CrossRef]

- Chai, Q.; Zhang, X. Technologies and policies for the transition to a sustainable energy system in China. Energy 2010, 35, 3995–4002. [Google Scholar] [CrossRef]

- Sun, X.Y.; Zhang, B.A.; Tang, X.; Benjamin, C.M.; Mikael, H. Sustainable Energy Transitions in China: Renewable Options and Impacts on the Electricity System. Energies 2016, 9, 980. [Google Scholar] [CrossRef]

- Sun, X.Y.; Zhang, B.A.; Zou, L.P.; Wang, R.Z. The Role of Renewable Energy in China’s Sustainable Energy Transition. In Proceedings of the 2nd International Conference on Sustainable Development (ICSD 2016), Xi’an, China, 2–4 December 2016; pp. 327–332. [Google Scholar]

- Amrutha, A.A.; Balachandra, P.; Mathirajan, M. Model-based approach for planning renewable energy transition in a resource-constrained electricity system—A case study from India. Int. J. Energy Res. 2018, 42, 1023–1039. [Google Scholar] [CrossRef]

- Thapar, S.; Sharma, S.; Verma, A. Local community as shareholders in clean energy projects: Innovative strategy for accelerating renewable energy deployment in India. Renew. Energy 2017, 101, 873–885. [Google Scholar] [CrossRef]

- Bundit, F.; Atit, T.; Takashi, O.; Cecilia, T. Transition pathways for a sustainable low-carbon energy system in Thailand. J. Renew. Sustain. Energy 2017, 9, 021405. [Google Scholar]

- Mah, N.Y.; Wu, Y.Y.; Ip, C.M.; Hills, P.R. The role of the state in sustainable energy transitions: A case study of large smart grid demonstration projects in Japan. Energy Policy 2013, 63, 726–737. [Google Scholar] [CrossRef]

- Mohammad, A.S.; Khan, S.A. Transition towards sustainable energy production—A review of the progress for solar energy in Saudi Arabia. Energy Explor. Exploit. 2018, 36, 3–27. [Google Scholar]

- Dóci, G.; Vasileiadou, E.; Petersen, A.C. Exploring the transition potential of renewable energy communities. Futures 2015, 66, 85–95. [Google Scholar] [CrossRef]

- Steg, L.; Perlaviciute, G.; van der Werff, E. Understanding the human dimensions of a sustainable energy transition. Front. Psychol. 2015, 6, 805. [Google Scholar] [CrossRef] [PubMed]

- Dumas, M.; Rising, J.; Urpelainen, J. Political competition and renewable energy transitions over long time horizons: A dynamic approach. Ecol. Econ. 2016, 124, 175–184. [Google Scholar] [CrossRef]

- International Energy Agency (IEA). Energy Policies of IEA Countries—Italy 2009 Review; OECD/IEA2009; IEA: Paris, France, 2010. [Google Scholar]

- ISTAT—Istituto Nazionale di Statistiche. Popolazione Residente al 1° Gennaio. 2017. Available online: http://dati.istat.it/Index.aspx?DataSetCode=DCIS_POPRES1 (accessed on 29 May 2018). (In Italian).

- International Energy Agency (IEA). Energy Policies of IEA Countries—Finland 2013 Review; OECD/IEA 2013; IEA: Paris, France, 2013. [Google Scholar]

- Lund, H. EnergyPLAN—Advanced Energy Systems Analysis Computer Model. 2015. Available online: www.EnergyPLAN.eu (accessed on 29 May 2018).

- TERNA—Rete Elettrica Nazionale. Dati Statistici Sull’Energia Elettrica in Italia; TERNA Group: Roma, Italy, 2013. (In Italian) [Google Scholar]

- ENTSO-E—European Network of Transmission System Operators for Electricity. 2017. Available online: https://www.entsoe.eu/db-query/country-packages/production-consumption exchange-package (accessed on 29 May 2018).

- ISTAT—Istituto Nazionale di Statistiche. I Consumi Energetici Delle Famigli; Istat Ufficio Stampa: Roma, Italy, 2013. (In Italian) [Google Scholar]

- ENEA—Agenzia Nazionale per le Nuove Tecnologie, L’energia e lo Sviluppo Economico Sostenibile. 2010. Available online: http://www.enea.it/it/pubblicazioni/rapporto-energia-e-ambiente-1/rapporto-energia-eambiente-2009-2010/i-dati-2009-2010/statistiche-nazionali (accessed on 29 May 2018). (In Italian).

- GSE—Gestore Servizi Energetici. Energia da Fonti Rinnovabili—Anno 2013; GSE–Unita Studi e Statistiche: Roma, Italy, 2015. (In Italian) [Google Scholar]

- Braccio, G.; Mario, F.D.; Marano, D.; Sabatelli, V. Solare Termico a Bassa e Media Temperatura; ENEA—Agenzia Nazionale per le Nuove Tecnologie, L’energia e lo Sviluppo Economico Sostenibile: Roma, Italy, 2011. (In Italian) [Google Scholar]

- Caleffi. Gli Impianti a Pannelli Solari; Idraulica Caleffi: Novara, Italy, 2005. (In Italian) [Google Scholar]

- AIRU—Associazione Italiana Teleriscaldamento Urbano. Il Teleriscaldamento Urbano—Annuario 2015; AIRU: Milano, Italy, 2017. (In Italian) [Google Scholar]

- Giordano, R.; Allione, C.; Clos, A.; Montacchini, E.; Tedesco, S. The integrated design of building services by an equipped and eco-efficient module (MOTE2). Int. J. Arch. Technol. Sustain. 2016, 2, 13–23. [Google Scholar] [CrossRef]

- Frederiksen, S.; Werner, S. District Heating and Cooling; Studentlitteratur: Lund, Sweden, 2013. [Google Scholar]

- EuroMeteo. Zone Climatiche Italiane. 2017. Available online: http://www.eurometeo.com/italian/read/doc_zone-climatiche (accessed on 11 October 2017). (In Italian).

- Wunderground. 2017. Available online: https://www.wunderground.com/ (accessed on 6 March 2018).

- TERNA—Rete Elettrica Nazionale. Individuazione Zone Della Rete Rilevante; TERNA: Roma, Italy, 2008. (In Italian) [Google Scholar]

- Pardo, N.; Vatopoulos, K.; Krook-Riekkola, A.; Moya, J.A.; Perez, A. Heating and Cooling Demand and Market Perspective; European Union: Petten, The Netherlands, 2012. [Google Scholar]

- ENEA—Agenzia Nazionale per le Nuove Tecnologie, L’energia e lo Sviluppo Economico Sostenibile. Rapporto Annuale Efficienza Energetica; ENEA: Roma, Italy, 2015. (In Italian) [Google Scholar]

- TERNA—Rete Elettrica Nazionale. Ex Post Data on the Actual Generation; TERNA: Roma, Italy, 2016. [Google Scholar]

- TERNA—Rete Elettrica Nazionale. Impianti di Generazione; TERNA: Roma, Italy, 2013. (In Italian) [Google Scholar]

- TERNA—Rete Elettrica Nazionale. Produzione; TERNA: Roma, Italy, 2013. (In Italian) [Google Scholar]

- GME—Gestore Mercati Energetici. Dati Storici. 2017. Available online: http://www.mercatoelettrico.org/it/Download/DatiStorici.aspx (accessed on 6 March 2018). (In Italian).

- GME—Gestore Mercati Energetici. Vademecum della Borsa Elettrica; GME: Roma, Italy, 2009. [Google Scholar]

- Statistics Finland. Use of Fossil Fuels Grew in Electricity and Heat Production in 2013. 2014. Available online: http://www.stat.fi/til/salatuo/2013/salatuo_2013_2014-10-16_tie_001_en.html (accessed on 6 March 2018).

- NordPool. Historical Market Data. 2017. Available online: http://www.nordpoolspot.com/historical-market-data/ (accessed on 6 March 2018).

- Finnish Energy. District Heating. 2017. Available online: http://energia.fi/en/home-and-heating/district-heating (accessed on 6 March 2018).

- Statistics Finland. Statistics Finland Web Databases Energy; Statistics Finland: Helsinki, Finland, 2017. [Google Scholar]

- Finnish Meteorological Institute. Heating Degree Days. 2017. Available online: https://en.ilmatieteenlaitos.fi/heating-degree-days (accessed on 14 December 2018).

- VTT Technical Research Centre of Finland. High-Efficiency CHP, District Heating and District Cooling in Finland 2010–2015; VTT—Tecnical Research Centre of Finland: Helsinki, Finland, 2015. [Google Scholar]

- Ministry of Employment and the Economy. Nuclear Energy in Finland; Ministry of Employment and the Economy: Helsinki, Finland, 2011. [Google Scholar]

- Motiva. Electricity Supply and Demand. 2017. Available online: https://www.motiva.fi/en/solutions/energy_use_in_finland/electricity_supply_and_demand (accessed on 14 December 2018).

- Italian Ministry for Economic Development. Italian National Renewable Energy Action Plan; Italian Ministry for Economic Development: Roma, Italy, 2010.

- Hoesen, J.V.; Letendre, S. Evaluating potential renewable energy resources in Poultney, Vermont: A GIS-based approach to supporting rural community energy planning. Renew. Energy 2010, 35, 2114–2122. [Google Scholar] [CrossRef]

- Energoclub. Potenziale Nazionale Delle Fonti Energetiche Rinnovabili. 2017. Available online: http://www.energoclub.org/page/potenziale-nazionale-fer (accessed on 17 December 2018). (In Italian).

- Ministry of Employment and the Economy Energy Department. Finland’s National Action Plan for Promoting Energy from Renewable Sources; Ministry of Employment and the Economy Energy Department: Helsinki, Finland, 2010. [Google Scholar]

- Motiva. Hydropower. 2017. Available online: http://www.motiva.fi/en/areas_of_operation/renewable_energy/hydropower (accessed on 6 March 2018).

- VTT. Wind Energy Statistics in Finland. 2017. Available online: https://www.vttresearch.com/services/low-carbon-energy/wind-energy/wind-energy-statistics-in-finland (accessed on 14 December 2018).

- Zakeri, B.; Syri, S.; Rinne, S. Higher renewable energy integration into the existing energy system of Finland—Is there any maximum limit? Energy 2015, 92, 244–259. [Google Scholar] [CrossRef]

- Faninger-Lund, H. Road-Map for Solar Energy Technology and Markets in Finland; Solpros: Helsinki, Finland, 2002. [Google Scholar]

- Abdollahi, E.; Wang, H.; Lahdelma, R. An optimization method for multi-area combined heat and power production with power transmission network. Appl. Energy 2016, 168, 248–256. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Zone | HDD | Typical City |

|---|---|---|

| A | <600 | / |

| B | 601–900 | Messina |

| C | 901–1400 | Napoli |

| D | 1401–2100 | Rome |

| E | 2101–3000 | Milan |

| F | >3001 | / |

| Zone | City | HDD | Heat Demand (TWh/Year) |

|---|---|---|---|

| B | Messina | 707 | 15.34 |

| C | Naples | 1034 | 12.64 |

| D | Rome | 1415 | 6.8 |

| E | Milan | 2402 | 1.0 |

| Country | Neighboring Countries | Maximum Import/Export (MW) |

|---|---|---|

| Italy | Switzerland | 3850 |

| France | 2650 | |

| Greece | 500 | |

| Slovenia | 430 | |

| Austria | 220 |

| Country | Neighboring Countries | Maximum Import/Export (MW) |

|---|---|---|

| Finland | Sweden (Northern) | 1500/1100 |

| Sweden (Central) | 1200/1200 | |

| Estonia | 1016/1000 | |

| Russia | 1100/- |

| Item | Electricity (TWh) | Share of Electricity Production (%) | District Heat (TWh) | Share of Heat Production (%) | |

|---|---|---|---|---|---|

| Separate production of electricity | Hydro power | 12.7 | 16.1 (RES) | - | - |

| Wind power | 0.8 | - | - | ||

| Nuclear power | 22.7 | 27.0 | - | - | |

| Condensing power | 8.9 | 10.6 | - | - | |

| Combined heat and power production | 23.3 | 27.7 | 26.1 | 75.7 | |

| Separate heat production | - | - | 8.4 | 24.3 | |

| Total production | 68.3 | 81.3 | 34.5 | 100 | |

| Net imports of electricity | 15.7 | 18.7 | - | - | |

| Total | 84 | 100.0 | 34.5 | 100 | |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, H.; Di Pietro, G.; Wu, X.; Lahdelma, R.; Verda, V.; Haavisto, I. Renewable and Sustainable Energy Transitions for Countries with Different Climates and Renewable Energy Sources Potentials. Energies 2018, 11, 3523. https://doi.org/10.3390/en11123523

Wang H, Di Pietro G, Wu X, Lahdelma R, Verda V, Haavisto I. Renewable and Sustainable Energy Transitions for Countries with Different Climates and Renewable Energy Sources Potentials. Energies. 2018; 11(12):3523. https://doi.org/10.3390/en11123523

Chicago/Turabian StyleWang, Haichao, Giulia Di Pietro, Xiaozhou Wu, Risto Lahdelma, Vittorio Verda, and Ilkka Haavisto. 2018. "Renewable and Sustainable Energy Transitions for Countries with Different Climates and Renewable Energy Sources Potentials" Energies 11, no. 12: 3523. https://doi.org/10.3390/en11123523

APA StyleWang, H., Di Pietro, G., Wu, X., Lahdelma, R., Verda, V., & Haavisto, I. (2018). Renewable and Sustainable Energy Transitions for Countries with Different Climates and Renewable Energy Sources Potentials. Energies, 11(12), 3523. https://doi.org/10.3390/en11123523