1. Introduction

The Renewable Energy Roadmap 21 settles for 2020 and for the whole European Union a share of energy from renewable sources of 20% [

1]. Some countries, such as Portugal, have already reached or surpassed such a target [

2,

3]; in fact, the current energy situation in the country has significantly changed in the last decade, when renewable energy deployment strategies were still under debate [

4]. Portugal was the fourth country of the European Union with a higher incorporation of renewable electricity in 2015 (44.6%) after Denmark (50.2%), Austria (62.6%), and Sweden (72.1%) [

3]. The Portuguese renewable annual electricity production has increased almost fourfold since 2005 and reached 33.3 TWh in 2016, relying mostly on hydro (16.9 TWh) and wind (12.5 TWh) sources, together representing 88% of the total renewable power production [

3].

In Portugal, an annual surplus of renewable power production in the range of 800–1200 GWh is estimated for 2020 [

5,

6]. As renewable power relevance increases within the energy sector, developing a way to efficiently and economically store its surpluses in periods of low demand becomes an urgent problem to be tackled [

7]. Among the systems available or under development for such a purpose (pumped hydroelectric storage, compressed air energy storage, electrochemical and flow batteries) [

8], power-to-gas technologies (PtG) are receiving increased attention, particularly in Europe [

9,

10,

11], and a storage potential of at least 500 GWh has been foreseen in Portugal [

6]. One PtG option could be to use the surplus electricity for H

2O electrolysis to obtain H

2 (PtH), but its storage remains a challenge and lacks a dedicated infrastructure for its distribution [

2]. Another way is to use that “green” H

2 and blend it in natural gas, but only up to 10% without major effect in the gas grid and end-use equipment, or further convert it to methane (PtM), also called substitute/synthetic natural gas (SNG), through the Sabatier reaction (Equation (1)) [

9]. Methane is far simpler to store and transport than pure H

2 using the well-established natural gas infrastructure and therefore enabling the connection between the power and natural gas grids [

12,

13].

Synthetic natural gas can be later reconverted to electricity in periods of high demand or used as feedstock or fuel. Thus, SNG can be seen as a secure and efficient supply of renewable energy, while simultaneously reducing the dependence on (imported) fossil fuels and supporting the transition towards a low-carbon economy [

14,

15,

16].

Bailera et al. [

10] reported the existence of 43 PtG projects worldwide taking place in 11 countries, with most initiatives occurring in Germany (16 projects), Denmark (7 projects), and Switzerland (6 projects) as a result of strong governmental support. In the review by Quarton and Samsatli [

13], these results were updated, with Germany standing out among other countries with 45 projects, either finished, planned, operating, or under construction. The main drivers towards PtG in Germany are the existence of geographic advantages for PtG implementation, like the availability of enough suitable underground gas storage capacity and a sufficient gas network development for gas distribution [

11,

17], as well as the country targets to increase its power generation with origin in renewable sources from 32% (in 2015) to 50% and 80% in 2030 and 2050, respectively [

18]. In Portugal, despite being a pioneering country regarding the adoption and massive diffusion of wind power parks across its territory, the first national research project in the country dedicated to the topic was launched in mid-2018 [

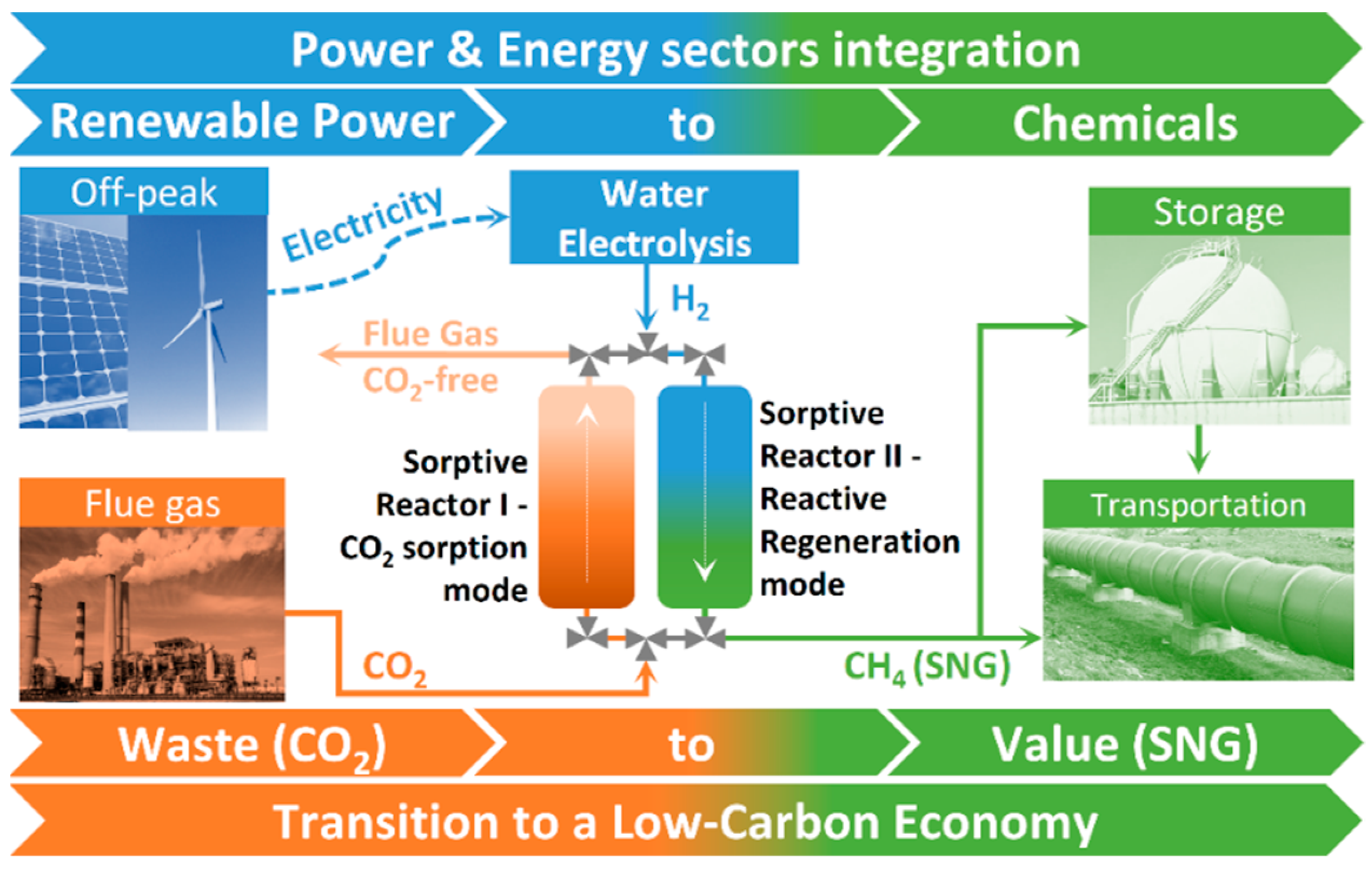

19], dealing with the development of a cyclic sorption-reaction process for simultaneous CO

2 capture and conversion to methane to be coupled in PtG applications (cf.

Figure 1).

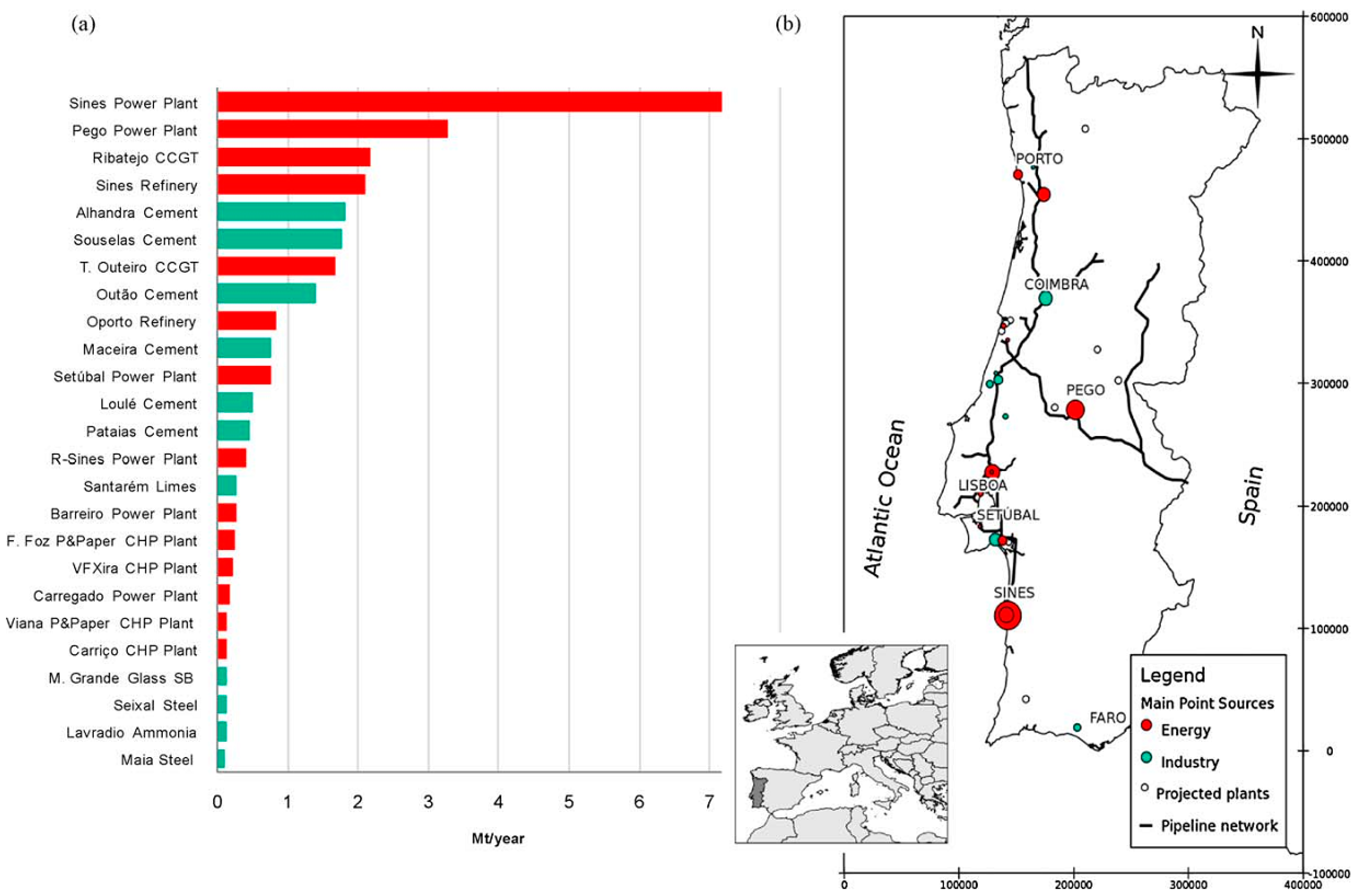

There are few studies concerning the assessment of power-to-gas implementation potential in Portugal. The first work was by Heymann and Bessa [

6], who estimated the cost of PtG products in the country as a function of the distance to wind power parks and gas storage facilities. The levelized cost of energy when considering SNG as a final product ranged between 0.05–0.10 €/kWh. Recently, Carneiro et al. [

20] presented the opportunities for large-scale energy storage in geological formations in mainland Portugal.

While PtG demonstration activities are growing fast, particularly in Europe, the current situation in Portugal supports the findings by Bento and Fontes [

21] that, typically, Portugal has an average adoption of energy-related technologies lag of one to two decades relative to “core” countries (i.e., energy technology developers/leaders, generally from the OECD-Organization for Economic Co-operation and Development) [

21]. Hence, the present work aims to contribute to the current state-of-art by providing a background image of the Portuguese energy sector (

Section 2), presenting the main facts and figures, such as the country energy dependence evolution with time (

Section 2.1), the consumption of fossil fuels (

Section 2.2), and renewable power production (

Section 2.3). Afterwards, in

Section 3, requirements for power-to-gas implementation are described, namely the availability of renewable power surpluses (

Section 3.1), carbon dioxide sources for the methanation (

Section 3.2), and access to the natural gas grid for SNG storage and distribution (

Section 3.3). In

Section 3.4, needs for future research are identified and, finally, in

Section 4, the main conclusions and the most important steps that all interested parties should take to raise awareness regarding deployment of PtG in Portugal are presented.

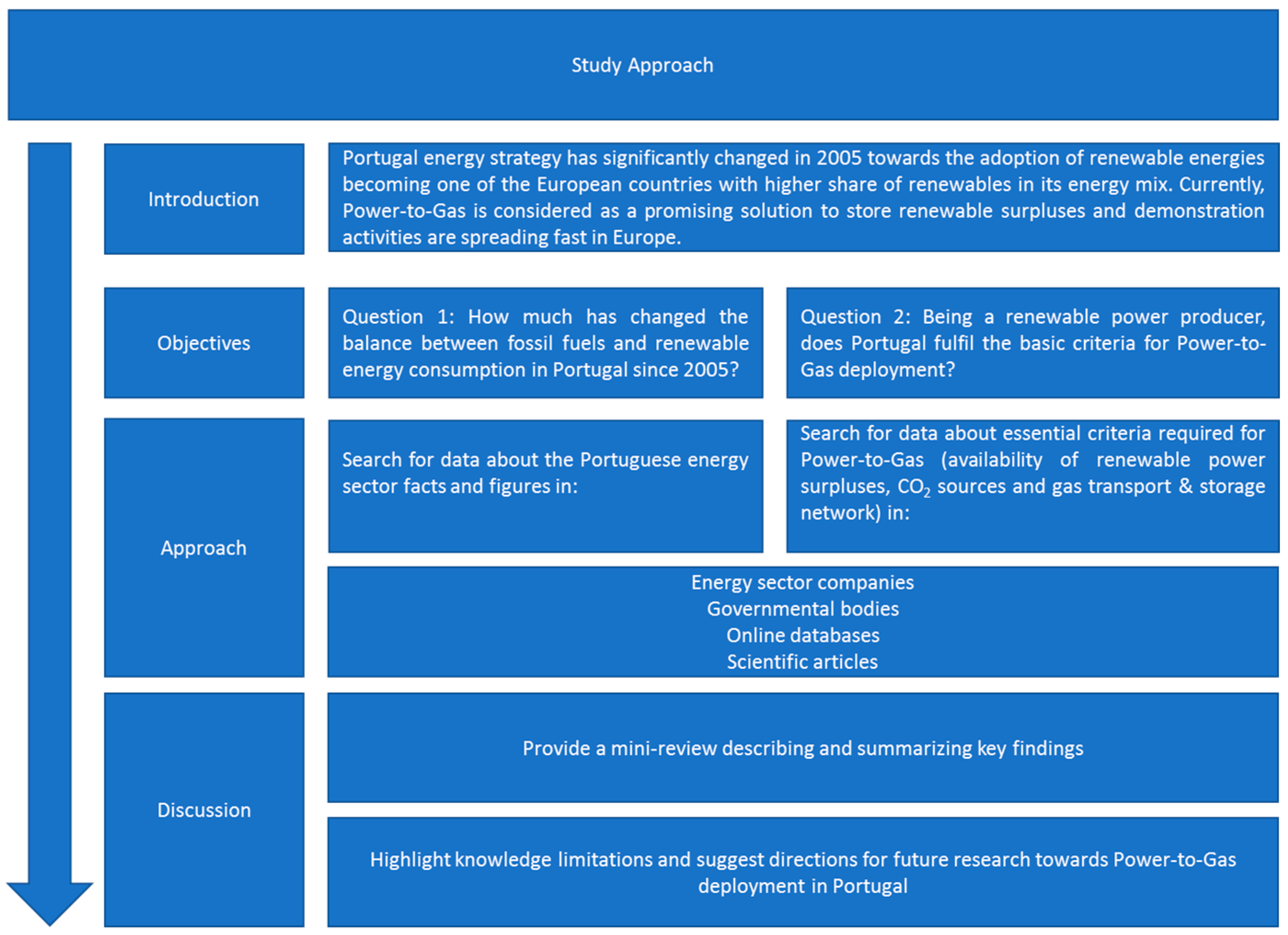

Figure 2 shows a diagram presenting the approach adopted in this work.

4. Conclusions

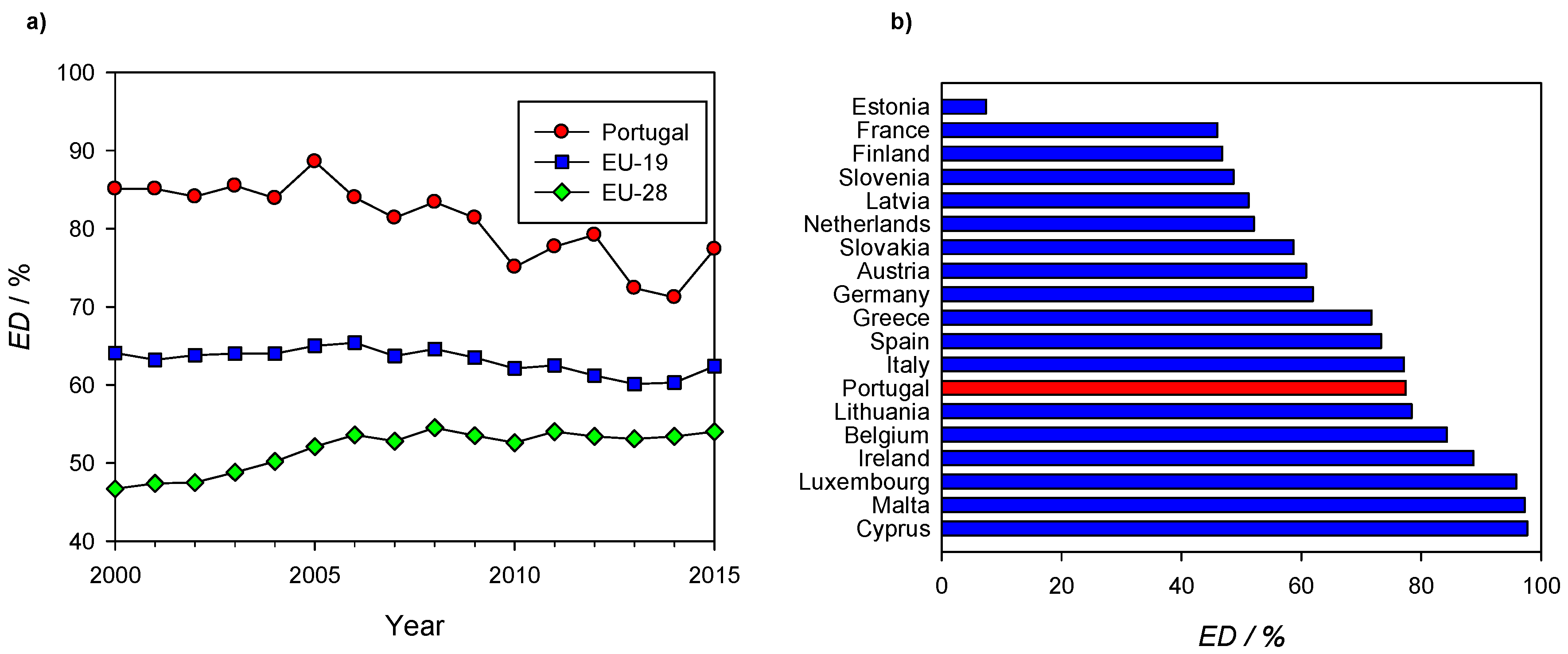

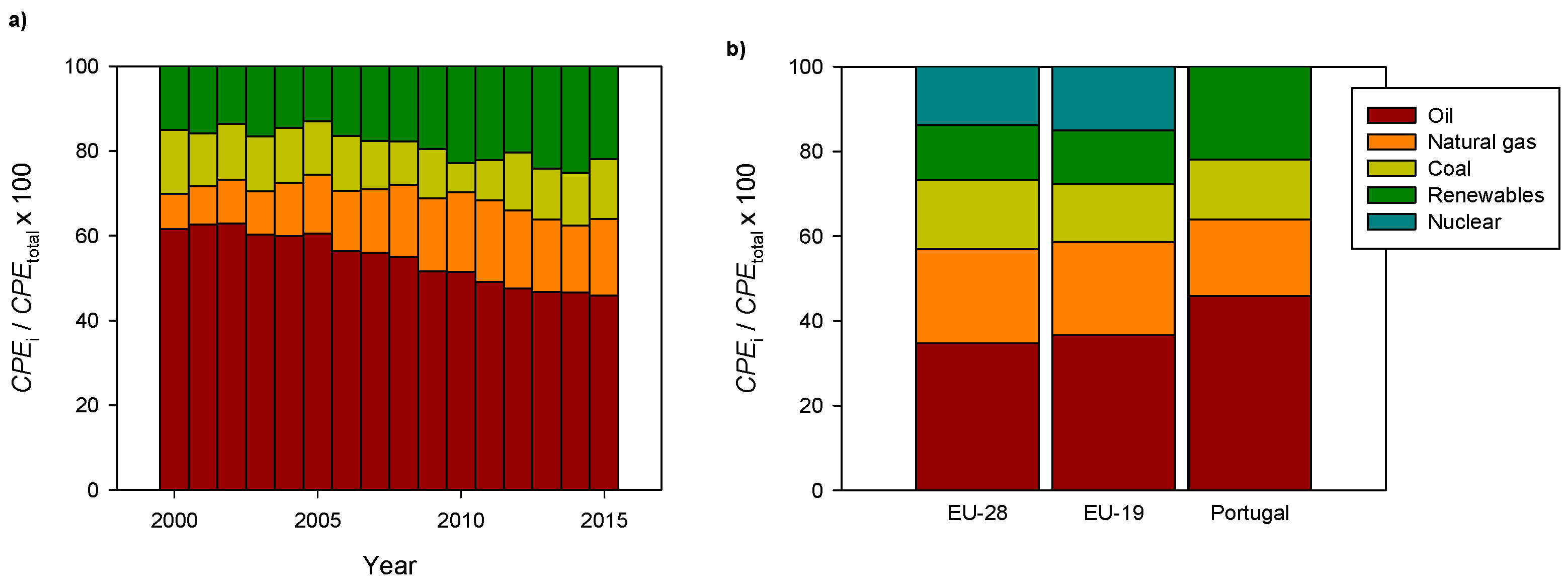

The present analysis of the Portuguese energy sector highlights the country’s intense dependence on fossil fuels to afford its energetic needs, although, despite this, it was the fourth EU-18 member with the highest incorporation of renewables in power production in 2015 (i.e., 44.6%), a value that reached 57% in 2016 [

36]. So far, the country’s options to manage the energy surpluses generated by electricity from renewable sources relies on pumped hydro storage plants or power exportation to Spain. Hence, decentralized power-to-methane applications can be of strategic relevance for the country, since power production from natural gas will increase following the decommissioning of the Sines and Pego coal power plants by 2021. Storing surplus renewable electricity as methane would also allow the diversification of natural gas provision, minimizing the dependence and risk of shortage supply from foreign countries, as it is advised by the Portuguese Directorate-General for Energy and Geology [

47]. Additionally, a significant increase of natural gas consumption in the 2005–2015 decade (ca. 19%) by several and important industry sectors was also shown.

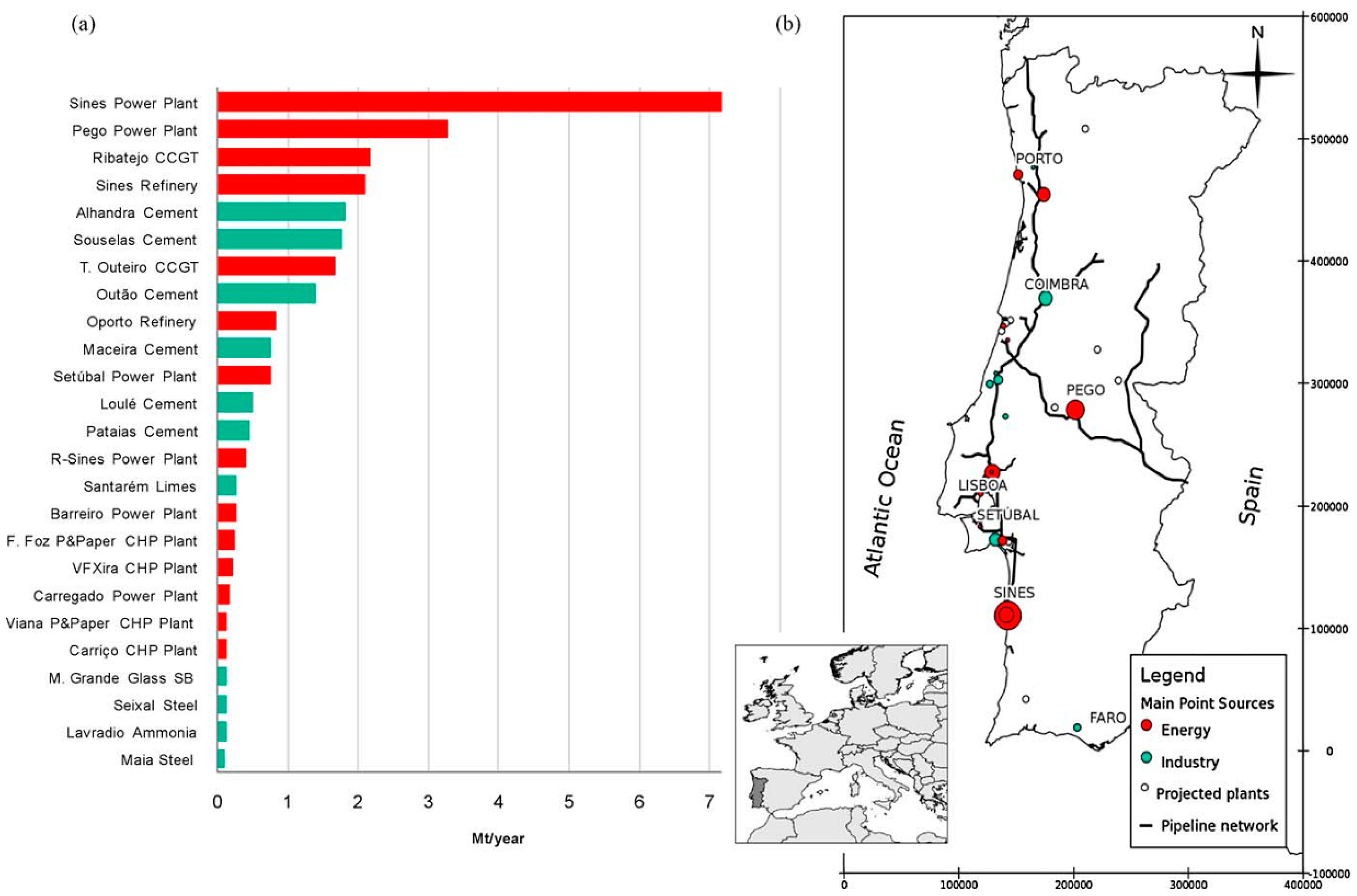

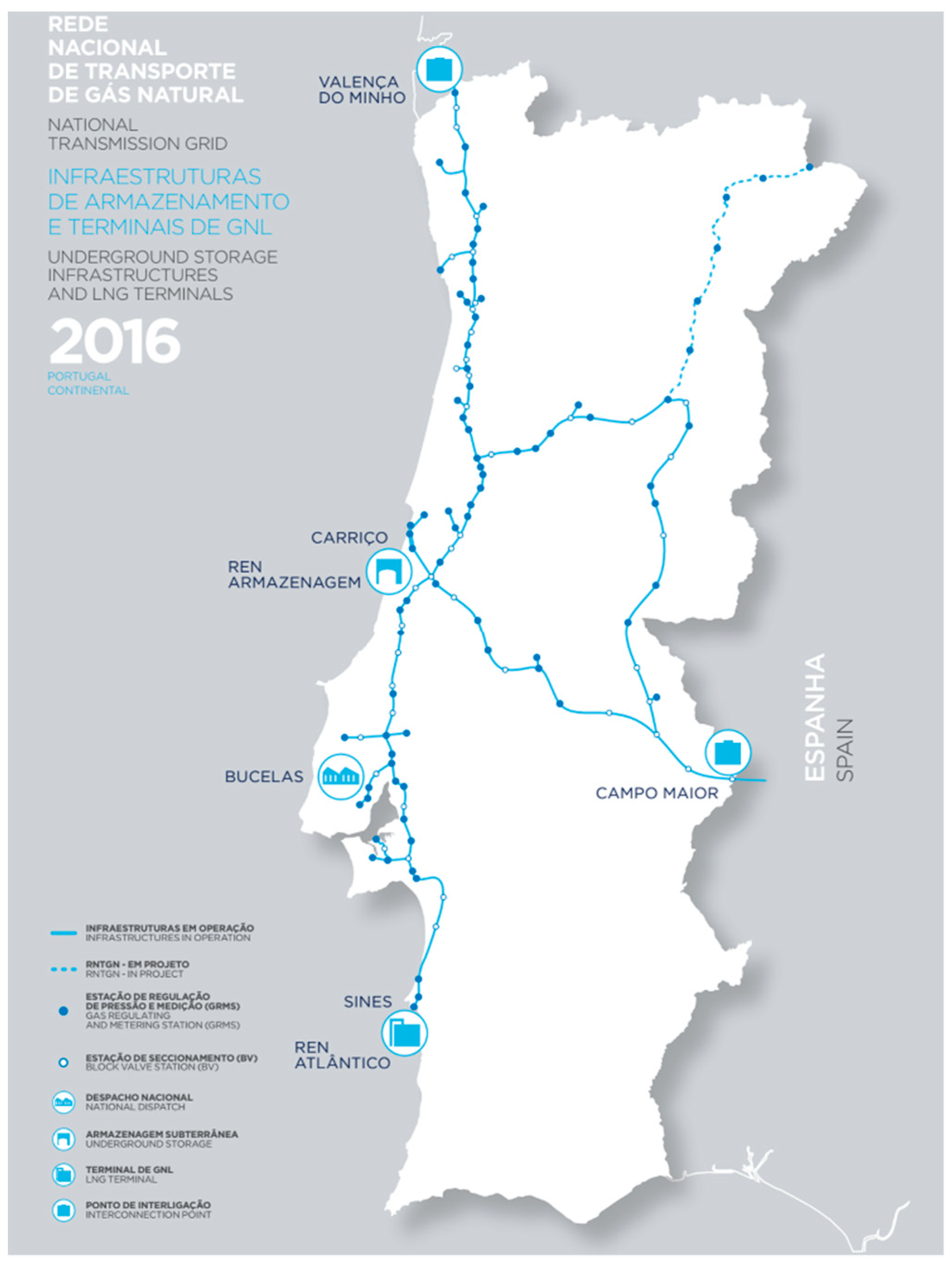

Portugal has important geographic advantages in favor of PtM demonstration projects, such as a well-developed natural gas network near wind parks and CO2 sources, as well as a promising underground storage potential yet to be explored. For such a purpose, the engagement of all stakeholders (namely, academics, governmental bodies, technology and energy providers, major CO2 polluting companies, and natural gas consumers) will be crucial for establishing national and/or regional research and development roadmaps, where the barriers (e.g., technical, legal, and regulatory), challenges, and opportunities for fast PtG deployment should be identified for coordinated actions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}