Firm Complexity and the Accuracy of Auditors’ Going Concern Opinions in Emerging Markets: Does Auditor Work Stress Matter?

Abstract

1. Introduction

2. Egyptian Context

3. Literature Review and Hypotheses Development

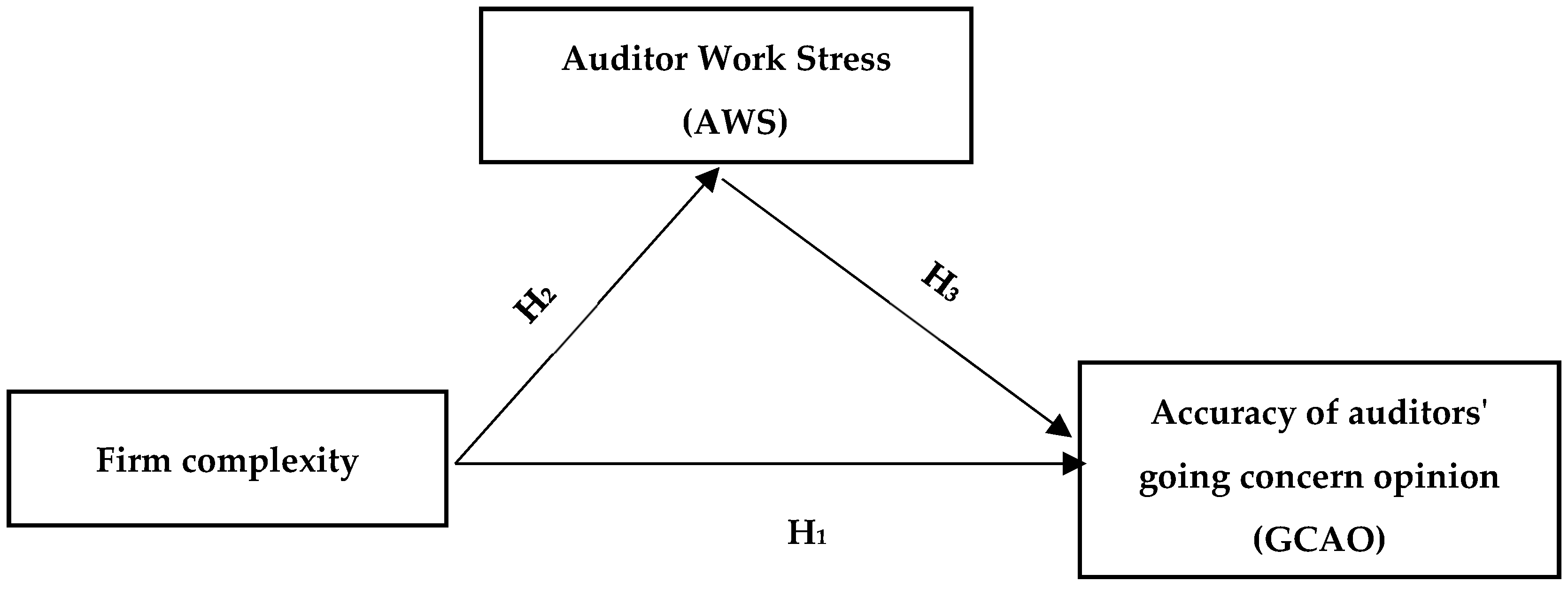

3.1. Firm Complexity and GCAO Accuracy

3.2. Firm Complexity and AWS

3.3. AWS and GCAO Accuracy

3.4. The Mediating Role of AWS

4. Research Design

4.1. Sample Selection

4.2. Variables’ Measurement

4.2.1. Dependent Variable

4.2.2. Independent Variable

4.2.3. Mediating Variable

4.2.4. Control Variables

4.3. Model Specification

4.3.1. Firm Complexity and the GCAO Accuracy Model

4.3.2. Firm Complexity and the AWS Model

4.3.3. AWS and GCAO Accuracy Model

4.3.4. The Mediating Role of AWS (Model 4—Indirect Effect)

5. Results and Discussion

5.1. Descriptive Statistics

5.2. Multicollinearity Diagnostics Test

5.3. Correlation

5.4. Main Findings

5.5. Robustness Checks

Using Alternative Measures of Main Variables

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abouelela, O., Diab, A., & Saleh, S. (2025). The determinants of the relationship between auditor tenure and audit report lag: Evidence from an emerging market. Cogent Business & Management, 12(1), 2444553. [Google Scholar] [CrossRef]

- Afzali, A., Afzali, M., & Ittonen, K. (2024). Distracted auditors, audit effort, and earnings quality. Accounting Forum, 48, 1–30. [Google Scholar] [CrossRef]

- Alsheikh, A. H., & Alsheikh, W. H. (2023). Does audit committee busyness impact audit report lag? International Journal of Financial Studies, 11(1), 48. [Google Scholar] [CrossRef]

- Amara, I., Khelil, I., El Ammari, A., & Khlif, H. (2023). Money laundering and infrastructure quality: The moderating effect of the strength of auditing and reporting standards. Pacific Accounting Review, 35(2), 249–264. [Google Scholar] [CrossRef]

- Amiruddin, A. (2019). Mediating effect of work stress on the influence of time pressure, work–family conflict and role ambiguity on audit quality reduction behavior. International Journal of Law and Management, 61(2), 434–454. [Google Scholar] [CrossRef]

- Aschauer, E., & Quick, R. (2024). Implementing shared service centres in Big 4 audit firms: An exploratory study guided by institutional theory. Accounting, Auditing & Accountability Journal, 37(9), 1–28. [Google Scholar] [CrossRef]

- Asnaashari, H., Safarzadeh, M. H., Kheirollahi, A., & Hashemi, S. (2023). The effect of auditors’ work stress and client participation on audit quality in the COVID-19 era. Journal of Facilities Management, 21(4), 1–28. [Google Scholar] [CrossRef]

- Awadallah, A. A., & Elsaid, H. M. (2020). Investigating the impact of macro-economic changes on auditors’ assessments of audit risk: A field study. Journal of Applied Accounting Research, 21(3), 345–361. [Google Scholar] [CrossRef]

- Bahtiar, A., Meidawati, N., Setyono, P., Putri, N. R., & Hamdani, R. (2021). Determinants of going concern audit opinion: An empirical study in Indonesia. Jurnal Akuntansi dan Auditing Indonesia, 25(2), 183–193. [Google Scholar] [CrossRef]

- Barinov, A., Park, S. S., & Yıldızhan, Ç. (2024). Firm complexity and post-earnings announcement drift. Review of Accounting Studies, 29(1), 527–579. [Google Scholar] [CrossRef]

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. [Google Scholar] [CrossRef]

- Blum, E. S., Hatfield, R. C., & Houston, R. W. (2022). The effect of staff auditor reputation on audit quality enhancing actions. The Accounting Review, 97(1), 75–97. [Google Scholar] [CrossRef]

- Chen, J. Z., Elemes, A., Hope, O. K., & Yoon, A. S. (2024). Audit-firm profitability: Determinants and implications for audit outcomes. European Accounting Review, 33(4), 1369–1396. [Google Scholar] [CrossRef]

- Chu, L., Fogel-Yaari, H., & Zhang, P. (2024). The estimated propensity to issue going concern audit reports and audit quality. Journal of Accounting, Auditing & Finance, 39(2), 589–613. [Google Scholar] [CrossRef]

- De Brabander, C. J., & Martens, R. L. (2014). Towards a unified theory of task-specific motivation. Educational Research Review, 11, 27–44. [Google Scholar] [CrossRef]

- Eldyasty, M. M., & Elamer, A. A. (2023). Audit (or) type and audit quality in emerging markets: Evidence from explicit vs. implicit restatements. Review of Accounting and Finance, 22(4), 489–507. [Google Scholar] [CrossRef]

- Farghaly, M., Basuony, M. A., Noureldin, N., & Hegazy, K. (2024). The antecedents of COVID-19 contagion on quality of audit evidence in Egypt. Journal of Accounting in Emerging Economies, 14(4), 717–746. [Google Scholar] [CrossRef]

- Fedyk, A., Hodson, J., Khimich, N., & Fedyk, T. (2022). Is artificial intelligence improving the audit process? Review of Accounting Studies, 27(3), 938–985. [Google Scholar] [CrossRef]

- Geiger, M. A., Gold, A., & Wallage, P. (2024). Practitioner perspectives on going concern opinion research and suggestions for further study: Part 1—Outcomes and consequences. Accounting Horizons, 38(2), 153–168. [Google Scholar] [CrossRef]

- Ghattas, P., Soobaroyen, T., & Marnet, O. (2021). Charting the development of the Egyptian accounting profession (1946–2016): An analysis of the State-Profession dynamics. Critical Perspectives on Accounting, 78, 102159. [Google Scholar] [CrossRef]

- Gontara, H., Khelil, I., & Khlif, H. (2023). The association between internal control quality and audit report lag in the French setting: The moderating effect of family directors. Journal of Family Business Management, 13(2), 261–271. [Google Scholar] [CrossRef]

- Hana, H., & Triani, N. N. A. (2024). The effect of company characteristics and audit firm on going concern audit opinion issued by audit firm. Journal of Economic, Bussines and Accounting (COSTING), 7(6), 5404–5411. [Google Scholar] [CrossRef]

- Handayani, T., Kusumaningtyas, M., Pratiwi, R., Suryanto, E., & Manurung, H. (2023). The influence of audit quality, profitability, liquidity, solvency on going concern audit opinions: A literature review. Jurnal Ilmiah Manajemen Kesatuan, 11(3), 783–790. [Google Scholar]

- Hutagalung, M., Hutagalung, M. T., Afrielza, O., Ndraha, P. A. Y., & Deliana, D. (2024). The influence of previous year audit opinions, company growth and leverage on going concern audit opinions. Prosiding Simposium Ilmiah Akuntansi, 1(1), 935–939. [Google Scholar]

- Jefferson, D. P., Andiola, L. M., & Hurley, P. J. (2024). Surviving busy season: Using the job demands-resources model to investigate coping mechanisms. Contemporary Accounting Research, 41, 1–30. [Google Scholar] [CrossRef]

- Kamal Hassan, M. (2008). The development of accounting regulations in Egypt: Legitimating the International Accounting Standards. Managerial Auditing Journal, 23(5), 467–484. [Google Scholar] [CrossRef]

- Kesimli, I., Karalar, S., & Tasdemir, Ö. (2018). Auditor stress: Literature review and classification. In Sustainability and social responsibility of accountability reporting systems: A global approach (pp. 317–346). Springer. [Google Scholar] [CrossRef]

- Khan, F., Abdul-Hamid, M. A. B., Fauzi Saidin, S., & Hussain, S. (2023). Organizational complexity and audit report lag in GCC economies: The moderating role of audit quality. Journal of Financial Reporting and Accounting, 21(5), 1–23. [Google Scholar] [CrossRef]

- Khelil, I., Guidara, A., & Khlif, H. (2023). The effect of the strength of auditing and reporting standards on infrastructure quality in Africa: Do ethical behaviour of firms and judicial independence matter? Journal of Financial Management of Property and Construction, 28(1), 145–160. [Google Scholar] [CrossRef]

- Li, H., Li, K. Y., Hu, X. R., Hong, X., He, Y. T., Xiong, H. W., & Zhang, Y. L. (2025). Development and validation of the Information Literacy Measurement Scale (ILMS-34) in Chinese public health practitioners. BMC Medical Education, 25(1), 75. [Google Scholar] [CrossRef] [PubMed]

- Li, X., & Sun, L. (2024). High-Quality auditor presence and informational influence: Evidence from firm investment decisions. Auditing: A Journal of Practice & Theory, 43(2), 189–218. [Google Scholar] [CrossRef]

- Lim, H. J., & Mali, D. (2024). An analysis of the effect of audit effort (hours) on stock price volatility: Evidence of increasing demand reducing uncertainty. International Journal of Disclosure and Governance, 21(3), 359–375. [Google Scholar] [CrossRef]

- Loughran, T., & McDonald, B. (2023). Measuring firm complexity. Journal of Financial and Quantitative Analysis, 58(3), 2487–2514. [Google Scholar] [CrossRef]

- Mannan, A., & Darwis, S. S. (2023). The Psychological impact of work stress on auditors: Exploring determinants and consequences. Journal for ReAttach Therapy and Developmental Diversities, 6(7s), 567–581. Available online: https://jrtdd.com/index.php/journal/article/view/833 (accessed on 20 December 2024).

- Moez, D. (2024). Does managerial power explain the association between agency costs and firm value? The French Case. International Journal of Financial Studies, 12(3), 94. [Google Scholar] [CrossRef]

- Mohd Sanusi, Z., Iskandar, T. M., Monroe, G. S., & Saleh, N. M. (2018). Effects of goal orientation, self-efficacy and task complexity on the audit judgement performance of Malaysian auditors. Accounting, Auditing & Accountability Journal, 31(1), 75–95. [Google Scholar] [CrossRef]

- Nelson, K., & Smith, A. P. (2023). Psychosocial work conditions as determinants of well-being in Jamaican police officers: The mediating role of perceived job stress and job satisfaction. Behavioral Sciences, 14(1), 1. [Google Scholar] [CrossRef] [PubMed]

- Nworie, G. O., & Obi, G. U. (2024). Audit firm physiognomies: A contrivance for mitigating corporate failures in listed consumer goods firms in Nigeria. IIARD International Journal of Economics, Business and Management, 10(5), 185–203. [Google Scholar]

- Ombati, R. M., & Karuti, J. K. (2024). Assessment of the influence of audit plan on the performance of internal auditors in the government ministries in Kenya. International Journal of Public Administration and Management Research, 10(4), 50–58. [Google Scholar]

- Peytcheva, M. (2014). Professional skepticism and auditor cognitive performance in a hypothesis-testing task. Managerial Auditing Journal, 29(1), 27–49. [Google Scholar] [CrossRef]

- Pham, D. H. (2022). Determinants of going-concern audit opinions: Evidence from Vietnam stock exchange-listed companies. Cogent Economics & Finance, 10(1), 1–13. [Google Scholar] [CrossRef]

- Pham, Q. T., Tan Tran, T. G., Pham, T. N. B., & Ta, L. (2022). Work pressure, job satisfaction and auditor turnover: Evidence from Vietnam. Cogent Business & Management, 9(1), 1–18. [Google Scholar] [CrossRef]

- Polo, O. C., Charris, N. N., Perez, E. B., Tovar, O. O., & Cantillo, I. F. C. (2023). Forensic audit: A case of automotive company, legal and accounting aspect. Journal of Law and Sustainable Development, 11(12), 1–34. [Google Scholar] [CrossRef]

- Proho, M. (2023). Going concern assessment: A literature review. Journal of Forensic Accounting Profession, 3(2), 48–62. [Google Scholar] [CrossRef]

- Saleh, S. A. (2023). Auditor’s effort following the implementation of 2015 revised Egyptian Accounting Standards: An evidence from the nonfinancial listed firms on the Egyptian Stock Exchange. Alexandria Journal of Accounting Research, 7(3), 131–172. [Google Scholar] [CrossRef]

- Salehi, M., Seyyed, F., & Farhangdoust, S. (2020). The impact of personal characteristics, quality of working life and psychological well-being on job burnout among Iranian external auditors. International Journal of Organization Theory & Behavior, 23(3), 189–205. [Google Scholar] [CrossRef]

- Shi, W., Connelly, B. L., & Hoskisson, R. E. (2017). External corporate governance and financial fraud: Cognitive evaluation theory insights on agency theory prescriptions. Strategic Management Journal, 38(6), 1268–1286. [Google Scholar] [CrossRef]

- Siahaan, L. E. J., Sihombing, J. T., Nasution, S. A., & Ginting, W. A. (2024). The influence of company size, profitability, solvency, current ratio, and capital structure on going concern audit opinions in consumer sector companies listed on the Indonesia stock exchange (BEI) 2019–2022. International Journal of Economics, Business and Innovation Research, 3(03), 339–358. [Google Scholar]

- Suhardianto, N., & Leung, S. C. (2020). Workload stress and conservatism: An audit perspective. Cogent Business & Management, 7(1), 1–19. [Google Scholar] [CrossRef]

- Talebkhah, Z. (2020). The relationship between auditor’s stress with audit quality and internal control weakness. Iranian Journal of Accounting, Auditing and Finance, 4(1), 99–112. [Google Scholar] [CrossRef]

- Tiron-Tudor, A., & Deliu, D. (2022). Reflections on the human-algorithm complex duality perspectives in the auditing process. Qualitative Research in Accounting & Management, 19(3), 255–285. [Google Scholar] [CrossRef]

- Umar, A., & Anandarajan, A. (2004). Dimensions of pressures faced by auditors and its impact on auditors’ independence: A comparative study of the USA and Australia. Managerial Auditing Journal, 19(1), 99–116. [Google Scholar] [CrossRef]

- Uthman, A. B., Salami, A. A., & Ajape, K. M. (2022). Impact of auditor industry specialization on the audit quality of listed non-financial firms in Nigeria. Nigerian Journal of Risk and Insurance, 12(1), 29–56. [Google Scholar]

- Van Hau, N., Hai, P. T., Diep, N. N., & Giang, H. H. (2023). Determining factors and the mediating effects of work stress to dysfunctional audit behaviors among Vietnamese auditors. Calitatea, 24(193), 164–175. [Google Scholar] [CrossRef]

- Wang, Y., Chiu, T., & Kogan, A. (2024). The effects of COVID-19 pandemic and auditor-client geographic proximity on auditors’ going concern opinions. International Journal of Disclosure and Governance, 21(2), 1–21. [Google Scholar] [CrossRef]

- Winoto, C. O., & Harindahyani, S. (2021). The effect of auditor’s work stress on audit quality of listed companies in Indonesia. Journal of Economics, Business, and Accountancy Ventura, 23(3), 361–374. [Google Scholar] [CrossRef]

- World Bank. (2023). World development indicators: Inflation, consumer prices (annual %). Available online: https://data.worldbank.org/indicator/FP.CPI.TOTL.ZG (accessed on 20 December 2024).

- Yan, H., & Xie, S. (2016). How does auditors’ work stress affect audit quality? Empirical evidence from the Chinese stock market. China Journal of Accounting Research, 9(4), 305–319. [Google Scholar] [CrossRef]

- Yang, Y., Simnett, R., & Carson, E. (2022). Auditors’ propensity and accuracy in issuing going concern modified audit opinions for charities. Accounting & Finance, 62, 1273–1306. [Google Scholar] [CrossRef]

{kind=link}

| Industry | Sample Firms (No.) | % |

|---|---|---|

| Basic Resources | 8 | 7.6% |

| Industrial Goods, Services, and Automobiles | 12 | 11.4% |

| Energy and Support Services | 7 | 6.7% |

| Health Care and Pharmaceuticals | 11 | 10.5% |

| Travel and Leisure | 8 | 7.6% |

| Building Materials | 17 | 16.2% |

| Food, Beverages, and Tobacco | 21 | 20% |

| Real Estate | 21 | 20% |

| Total | 105 | 100% |

| Variable | Minimum | Maximum | Mean | Std. Deviation |

|---|---|---|---|---|

| GCAO | 0 | 1 | 0.88 | 0.324 |

| Complex.Oper. | 0.080 | 4.121 | 1.539 | 1.115 |

| AWS | 2.76 | 9.99 | 7.76 | 1.95 |

| GROWTH | −0.99 | 0.511 | −0.022 | 0.213 |

| CURR. | 0.11 | 4.951 | 1.979 | 1.494 |

| CFO | −0.297 | 0.356 | 0.074 | 0.056 |

| DEBT | 0.008 | 0.9250 | 0.379 | 0.245 |

| ROA | −0.689 | 0.482 | 0.0849 | 0.016 |

| LOSS | 0 | 1 | 0.21 | 0.110 |

| AFR | 0.000 | 3.875 | 1.706 | 0.876 |

| N | 705 | |||

| Variable | Collinearity Statistics Tolerance | VIF |

|---|---|---|

| Complex.Oper. | 0.756 | 1.213 |

| AWS | 0.466 | 2.145 |

| GROWTH | 0.996 | 1.002 |

| CURR. | 0.746 | 1.230 |

| CFO | 0.981 | 1.017 |

| DEBT | 0.947 | 1.056 |

| ROA | 0.465 | 2.153 |

| LOSS | 0.886 | 1.129 |

| AFR | 0.371 | 2.693 |

| Correlation | Complex.Oper. | AWS | GROWTH | CURR. | CFO | DEBT | ROA | LOSS | AFR |

|---|---|---|---|---|---|---|---|---|---|

| Complex.Oper. | 1 | ||||||||

| AWS | 0.217 ** | 1 | |||||||

| GROWTH | −0.036 | 0.006 | 1 | ||||||

| CURR. | −0.263 ** | 0.112 ** | 0.019 | 1 | |||||

| CFO | 0.040 | 0.041 | 0.002 | 0.006 | 1 | ||||

| DEBT | 0.032 | 0.116 ** | −0.031 | −0.034 | 0.119 ** | 1 | |||

| ROA | −0.110 ** | 0.195 ** | −0.016 | 0.443 ** | −0.001 | −0.116 ** | 1 | ||

| LOSS | 0.027 | 0.157 ** | −0.013 | 0.106 ** | −0.034 | −0.031 | 0.268 ** | 1 | |

| AFR | −0.432 ** | −0.542 ** | −0.022 | 0.228 ** | −0.026 | −0.090 * | 0.421 ** | −0.063 | 1 |

| N = 705 | |||||||||

| Panel A: The effect of firm complexity and AWS on GCAO (H1 and H3) | ||||

| Variables | Model (1) | Model (3) | ||

| Complex.Oper. | −0.315 (0.029) * | −0.262 (0.105) * | ||

| AWS | −0.044 (0.072) * | |||

| Control Variables | ||||

| GROWTH | 0.824 (0.204) * | 0.418 (0.000) | ||

| CURR | 0.092 (21.942) * | 0.148 (0.075) * | ||

| CFO | 0.346 (1.767) | −0.130 (0.000) | ||

| DEBT | −1.155 (1.470) | −0.765 (0.032) | ||

| ROA | 0.387 (12.972) * | 0.535 (0.073) | ||

| LOSS | 0.297 (0.000) | −0.304 (0.000) * | ||

| Cox and Snell R Square | 0.287 | 0.324 | ||

| Chi-square | 248.563 | 287.383 | ||

| Sig. | 0.000 | 0.000 | ||

| N | 705 | 705 | ||

| Notes: Panel A summarizes the results of statistical analyses investigating the effect of firm complexity (Model 1) and AWS (Model 2) on GCAO. Definitions of all variables employed in the model specification. The coefficients for each variable are presented first, while Wald statistics are in parentheses. Asterisk (*) denotes statistical significance at the 5% level. | ||||

| Panel B: The effect of firm complexity on AWS (H2) | ||||

| Variables | Model (2) | |||

| Complex.Oper. | 1.207 (23.294) * | |||

| Control Variables | ||||

| GROWTH | −15.223 (−10.109) * | |||

| CFO | −16.092 (−5.653) * | |||

| DEBT | 0.836 (0.699) | |||

| LOSS | 0.127 (4.146) * | |||

| AFR | −1.187 (−7.397) * | |||

| Adjusted R2 | 0.435 | |||

| F-statistic | 542.604 | |||

| Sig. | 0.000 | |||

| N | 705 | |||

| Notes: Panel B summarizes the findings of statistical analyses investigating the influence of firm complexity on AWS. Definitions of all variables employed in the model specification. The coefficients for each variable are presented first, while t-statistics are in parentheses. Asterisk (*) denotes statistical significance at the 5% level. | ||||

| Panel C: The direct, indirect, and total effect of the mediating role of AWS in the relationship between firm complexity and GCAO (H4) | ||||

| The relationship between variables | Direct Effect | Indirect Effect | Total Effect | Path Number |

| Complex.Oper. → GCAO | −0.262 (0.000) | −0.053 (0.000) | −0.315 (0.000) | 1 |

| Complex.Oper. → AWS | 1.207 (0.000) | 1.207 (0.000) | 2 | |

| Complex.Oper. → AWS → GCAO | −0.044 (0.001) | −0.044 (0.001) | 3 | |

| Notes: Panel C summarizes the findings of statistical analyses investigating the direct, indirect, and total effect of the mediating role of AWS in the relationship between firm complexity and GCAO. Definitions of all variables employed in the model specification. The coefficients for each variable are presented first, while the P-values are in parentheses, denoting statistical significance at the 5% level. Finally, this table shows the path number when using path analysis to test the fourth hypothesis. | ||||

| Panel A: The effect of firm complexity and AWS on GCAO (H1n and H3) | ||||

| Variables | Model (1) | Model (3) | ||

| Complex.Oper. | −0.917 (0.036) * | −0.659 (010) | ||

| AWS | −0.154 (2.694) * | |||

| Control Variables | ||||

| GROWTH | 5.425 (0.000) | 1.952 (0.000) | ||

| CURR | −14.622 (0.001) | −9.883 (0.003) | ||

| CFO | 8.730 (0.000) | −7.512 (0.000) | ||

| DEBT | −7.559 (0.005) | 3.648 (0.002) | ||

| ROA | 12.817 (0.008) | −6.701 (0.073) | ||

| LOSS | 9.336 (0.003) | −.035 (0.004) | ||

| Cox and Snell R Square | 0.167 | 0.339 | ||

| Chi-square | 287.384 | 287.384 | ||

| Sig. | 0.000 | 0.000 | ||

| N | 705 | 705 | ||

| Notes: Panel A summarizes the results of statistical analyses investigating the effect of firm complexity and AWS on GCAO. Definitions of all variables employed in the model specification. The coefficients for each variable are presented first, while Wald statistics are in parentheses. Asterisks (*) denote statistical significance at the 5% level. | ||||

| Panel B: The effect of firm complexity on AWS (H2) | ||||

| Variables | Model (2) | |||

| Complex.Oper | 1.670 (44.006) * | |||

| Control Variables | ||||

| GROWTH | 0.004 (0.196) | |||

| CFO | 0.015 (0.787) | |||

| DEBT | 0.003 (0.132) | |||

| LOSS | −0.099 (−4.986) * | |||

| AFR | −0.048 (−2.439) * | |||

| Adjusted R2 | 0.734 | |||

| F-statistic | 338.677 | |||

| Sig. | 0.000 | |||

| N | 705 | |||

| Notes: Panel B summarizes the findings of statistical analyses investigating the influence of firm complexity on AWS. Definitions of all variables employed in the model specification. The coefficients for each variable are presented first, while t-statistics are in parentheses. Asterisks (*) denote statistical significance at the 5% level. | ||||

| Panel C: The direct, indirect, and total effect of the mediating role of AWS in the relationship between firm complexity and GCAO (H4) | ||||

| The relationship between variables | Direct Effect | Indirect Effect | Total Effect | Path Number |

| Complex.Oper. → GCAO | −0.659 (0.000) | −0.258 (0.000) | −0.917 (0.000) | 1 |

| Complex.Oper. → AWS | 1.670 (0.001) | 1.670 (0.001) | 2 | |

| Complex.Oper. → AWS → GCAO | −0.154 (0.001) | −0.154 (0.001) | 3 | |

| Notes: Panel C summarizes the findings of statistical analyses investigating the direct, indirect, and total effect of the mediating role of AWS in the relationship between firm complexity and GCAO. Definitions of all variables employed in the model specification. The coefficients for each variable are presented first, while the P-values are in parentheses, denoting statistical significance at the 5% level. Finally, this table shows the path number when using path analysis to test the fourth hypothesis. | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saleh, S.; Diab, A.; Abouelela, O. Firm Complexity and the Accuracy of Auditors’ Going Concern Opinions in Emerging Markets: Does Auditor Work Stress Matter? J. Risk Financial Manag. 2025, 18, 108. https://doi.org/10.3390/jrfm18030108

Saleh S, Diab A, Abouelela O. Firm Complexity and the Accuracy of Auditors’ Going Concern Opinions in Emerging Markets: Does Auditor Work Stress Matter? Journal of Risk and Financial Management. 2025; 18(3):108. https://doi.org/10.3390/jrfm18030108

Chicago/Turabian StyleSaleh, Safaa, Ahmed Diab, and Osama Abouelela. 2025. "Firm Complexity and the Accuracy of Auditors’ Going Concern Opinions in Emerging Markets: Does Auditor Work Stress Matter?" Journal of Risk and Financial Management 18, no. 3: 108. https://doi.org/10.3390/jrfm18030108

APA StyleSaleh, S., Diab, A., & Abouelela, O. (2025). Firm Complexity and the Accuracy of Auditors’ Going Concern Opinions in Emerging Markets: Does Auditor Work Stress Matter? Journal of Risk and Financial Management, 18(3), 108. https://doi.org/10.3390/jrfm18030108