1. Introduction

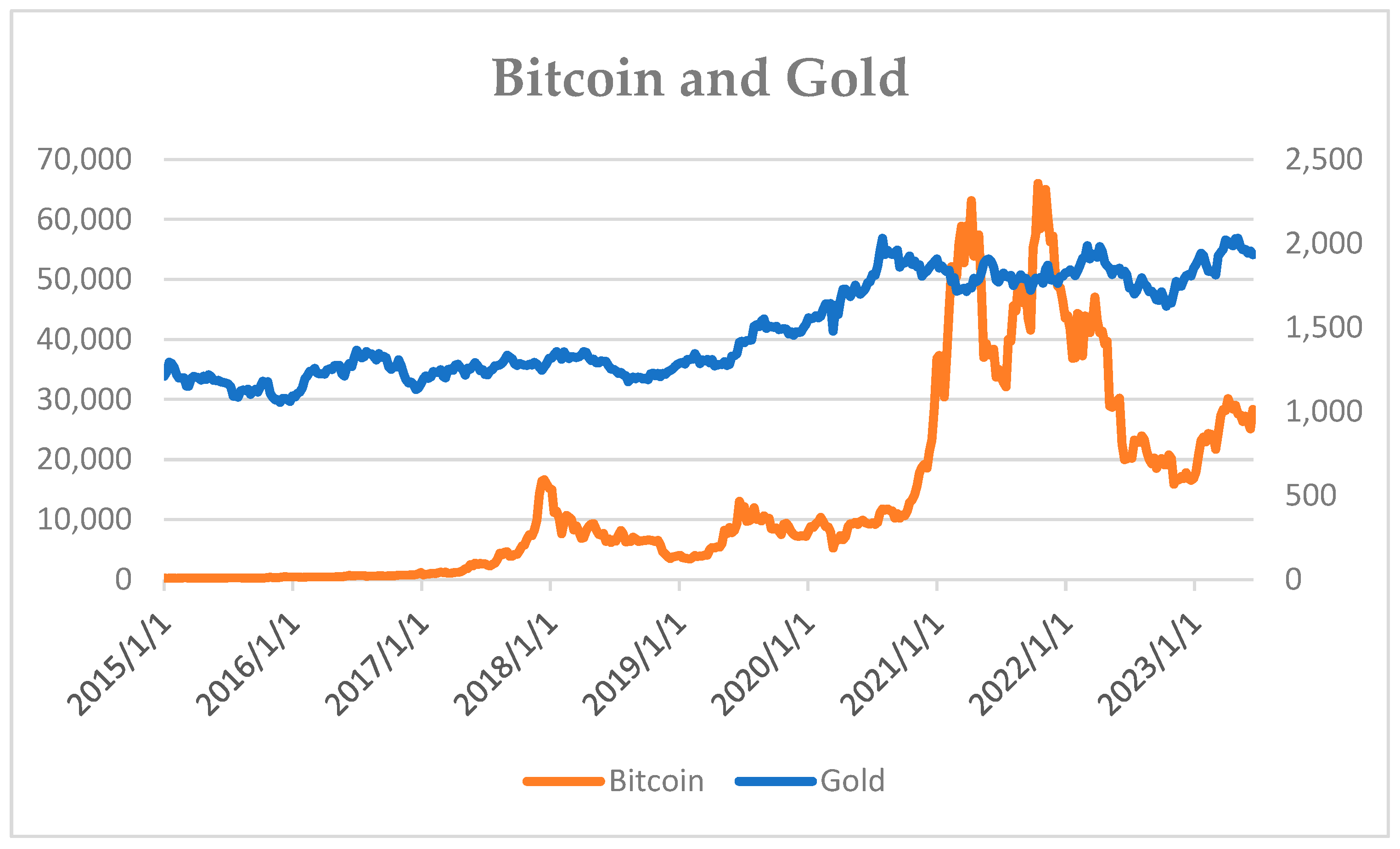

Bitcoin, as well as traditional gold, crude oil, and the US dollar, are globally important financial assets that have received widespread attention from financial investors, financial institutions, and economists (

Li et al. 2021). It seems that Bitcoin is more sought after by investors as a new financial asset. Bitcoin is favored due to its independence from central banks, with its value dependent on scarcity and mining costs (

Dyhrberg 2016a;

Abdullah and Mutawa 2023). As it were, Bitcoin is a product of the distrust and uncertainty in the existing financial system. With the opening of the Bitcoin market, its trading volume and value have been increased, attracting more investors and financial institutions. Bitcoin has similar characteristics to gold, and many scholars believe that Bitcoin is also a safe-haven asset (

Long et al. 2021). As a result, Bitcoin is often referred to as digital gold (

Selmi et al. 2018).

In recent years, scholars have studied Bitcoin from many aspects, such as the hedging ability of Bitcoin (

Wei et al. 2023;

Madichie et al. 2023;

Wang et al. 2019), factors influencing Bitcoin price (

Bouoiyour and Selmi 2015), Bitcoin price predictions (

Zhu et al. 2023;

Chen 2023;

Detzel et al. 2021), and spillover effect of Bitcoin (

Fasanya et al. 2021). Although Bitcoin is a new investment product, it brings substantial investment returns. The price of Bitcoin fell below USD 5000 in the early days of the COVID-19 pandemic, but by November 2021, it almost reached USD 65,000 (

Long et al. 2021). The impact of the COVID-19 pandemic on the Bitcoin market is significant (

Khan et al. 2023). The COVID-19 pandemic and Bitcoin not only had a positive correlation, but also caused the rise of Bitcoin (

Goodell and Goutte 2021). A few studies showed that Bitcoin, stock markets, and the global financial assets had different volatility and co-movement during the COVID-19 pandemic (

Abdul-Rahim et al. 2022;

Chan et al. 2023). This shows that Bitcoin has become a very popular investment asset. High returns inevitably come with high risks. More Bitcoin investors are paying attention to the relationship between Bitcoin and global financial assets, namely gold, crude oil, and the US dollar. Among them, gold has long been considered a safe-haven asset (

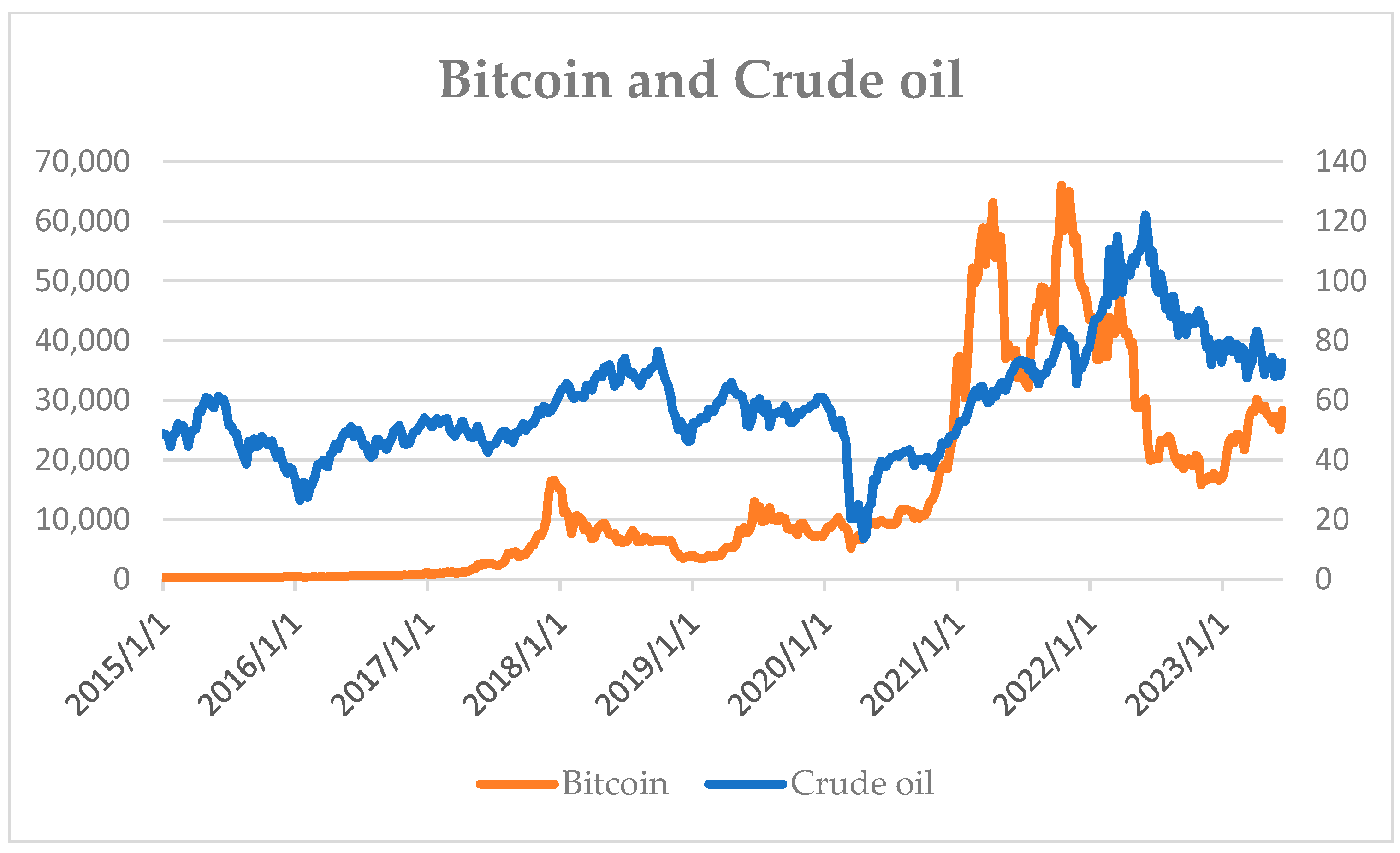

Cunado et al. 2019). Crude oil is also commonly used to hedge against the risks brought by the rise in commodity financialization (

Chen et al. 2018;

Tang and Xiong 2012). And the US dollar is a store of value. Studying the relationships between Bitcoin and global financial assets helps diversify the investment risk of Bitcoin and ensure return on investment.

The purpose of this paper is to examine whether there is a co-integration relationship, especially asymmetric co-integration, between Bitcoin and global financial assets, namely gold, crude oil, and the US dollar. Through co-integration analysis, the causality, particularly asymmetric causality, between Bitcoin and global financial assets is further determined. The other objective of this study is to investigate whether the co-integration relationship and causality changes before and after the COVID-19 outbreak. The findings of this study will help investors and financial institutions understand the relationships between Bitcoin and gold, crude oil, and the US dollar, providing valuable insights for Bitcoin investment decision making and risk management.

The reminder of this study is as follows:

Section 2 is a literature review that evaluates the relevant studies on Bitcoin and gold, Bitcoin and crude oil, and Bitcoin and the US dollar.

Section 3 provides a detailed description of the data.

Section 4 introduces the asymmetric co-integration test and asymmetric Granger causality test.

Section 5 demonstrates the empirical results and discussions, and

Section 6 draws a conclusion.

5. Empirical Results

This study aims to solve two problems concerning the asymmetric long-term relationship between Bitcoin and global financial assets, namely crude oil, gold, and the US dollar, as well as the asymmetric causality between them. To answer the above two questions, we first take the natural logarithm of Bitcoin and global financial assets and perform unit root tests. Second, we employ the Engle–Granger method to test the long-term relationship between Bitcoin and crude oil, Bitcoin and gold, and Bitcoin and the US dollar, respectively. Based on this, we examine the asymmetric long-term relationship between Bitcoin and global financial assets. Last, we test the asymmetric causality between Bitcoin and global financial assets.

5.1. Results of Unit Root Tests

Table 1 shows the unit root test results of Bitcoin, crude oil, gold and the US dollar. ADF and PP methods are used for the unit root test. The null hypothesis of ADF and PP methods is that the sequence has a Root of unity. It can be observed that neither Bitcoin nor crude oil, gold, or the US dollar challenge the null hypothesis at a 5% confidence level, indicating that the level data are all non-stationary. The unit root test results of first-order difference data show that all first-order difference data challenge the null hypothesis at a 1% confidence level, indicating that all first-order difference data are stationary. Many scholars including

Zhang et al. (

2022) and

Dyhrberg (

2016a) have also proved that the logarithmic return of financial assets is stationary. On this basis, the ADF, PP, and KPSS methods are employed to examine the stationarity of the residuals with logbitcoin as the dependent variable and global financial assets as independent variables for regression analysis. If the test result is stationary, it indicates the presence of a co-integration relationship between Bitcoin and global financial assets.

Table 2 shows the unit root test results of the residuals. In the ADF test, the Akaike information criterion (AIC) is used to select the appropriate lag length for dependent variables. In the PP and KPSS tests, the Newey–West automatic method is adopted to determine the bandwidth parameters (

Newey and West 1994). The null hypothesis of ADF and PP tests is that there is a unit root, while that of the KPSS test is that data are stationary. It is evident that the null hypothesis cannot be challenged in both ADF and PP tests, while it is challenged in the KPSS test. That is to say, the three residual sequences are not stationary. Therefore, there is no co-integration or long-term relationship between Bitcoin and the said three global financial assets. First, some scholars support this viewpoint, too. For example, the long-term relationships between Bitcoin and crude oil and between Bitcoin and the US dollar were refuted, respectively, by

Ciaian et al. (

2016) and Ünvana (

Ünvan 2021). The relationship between Bitcoin and global financial assets is not long-lasting but close, including, for example, time-varying correlation (

Liu and Li 2022), nonlinear correlation (

Wei et al. 2023), and the spillover effect (

Liu and Li 2022).

5.2. Results of Asymmetric Co-Integration and Causality Tests

Although no co-integration relationship exists between Bitcoin and global financial assets, positive (negative) fluctuation of global financial assets may affect Bitcoin and the impact may last for a long time.

Table 3 shows the results of the asymmetric co-integration test between the positive/negative fluctuation of global financial assets and the positive fluctuation of Bitcoin. First, in ADF and PP tests, only the US dollar - and Bitcoin + are significant when the confidence level is set to 5%, while in the KPSS test, only the residual sequence of the US dollar - is non-significant. Therefore, a nonlinear long-term relationship exists between the negative fluctuation of the US dollar and the positive fluctuation of Bitcoin. The negative fluctuation of the US dollar represents an appreciation of the currency, which is the base currency of Bitcoin. Therefore, a lower USDX causes a positive fluctuation of Bitcoin (

Oad Rajput et al. 2022). Second, no co-integration relationship exists between the impact on gold and crude oil, positive or negative, and the positive impact on Bitcoin.

Table 4 shows the results of the asymmetric co-integration test between the positive/negative fluctuation of global financial assets and the negative fluctuation of Bitcoin. ADF and PP test results show that all the residual sequences are significant at least when the confidence level is set to 10%. None of the KPSS tests challenge the null hypothesis. Therefore, an asymmetric co-integration relationship exists between global financial assets (gold, crude oil, the US dollar) and negatively fluctuating Bitcoin. That is to say, when Bitcoin depreciates, there is a co-integration relationship between gold, crude oil or the US dollar, regardless of whether they appreciate or depreciate, and Bitcoin.

Table 5 shows the estimation of the long-term relationship. As variables consist of the accumulation of positive or negative impacts, the slope coefficient has no economic significance. However, the operators and values of the slope coefficients still indicate something. First, all the slope coefficients are significant when the confidence level is set to 1%, supporting the existence of asymmetry. Second, compared with gold and crude oil, the asymmetric impact of USDX on Bitcoin is high. The decline in USDX, equivalent to the appreciation of the US dollar, has the strongest impact on the appreciation of Bitcoin. This may be because Bitcoin is denominated in the US dollar. It could also be found that, compared with the positive impact, the negative impact on global financial assets has a strong influence on the depreciation of Bitcoin. As expected, the appreciation and depreciation of gold, crude oil and the US dollar have opposite impacts on the depreciation of Bitcoin.

Table 6 and

Table 7 display the asymmetric co-integration of Bitcoin and the global financial assets before and after the outbreak of the COVID-19 pandemic, respectively.

Table 6 shows that the rise of gold has a long-run relationship with the rise of Bitcoin, and the rise of the US dollar has a long-run relationship with the fall of Bitcoin. Overall, we cannot reject the null hypothesis in all ADF and PP tests and reject the null hypothesis in the KPSS test. Clearly, this implies that there is no asymmetric cointegration between Bitcoin and the global financial assets during the COVID-19 pandemic. Then, again, for negative shocks to crude oil and Bitcoin, the ADF statistic is significant at the 10% credit level, while the KPSS test is insignificant at the 5% level. However, we cannot reject the null hypothesis of the PP test. The results of the PP test are not consistent with the results of the ADF and PP tests. We may not be able to determine whether there is a long-run relationship between crude oil and Bitcoin for negative shocks.

The multivariate normality test and the ARCH test were first conducted to determine whether the Granger causality test is applicable. Test results are shown in

Table 8. The Jarque–Bera test showed a non-binary normal distribution of Bitcoin and all the other assets. Most multivariate ARCH tests challenged the null hypothesis, too, indicating a potential ARCH fluctuation of Bitcoin and most financial assets. Therefore, standard test methods are not applicable to the causality.

Table 9 shows the results of tests for causality using the bootstrap simulations. First, there is a Granger causality between crude oil (but not gold or the US dollar) and Bitcoin. Second, an asymmetric causality exists between Bitcoin and crude oil, too. There is a causality between the negative impact on crude oil and the positive/negative fluctuation of Bitcoin. Second, there is no causality between gold/US dollar, regardless of whether a positive or negative impact is suffered, and Bitcoin fluctuation. Is there any difference in the asymmetric causality between Bitcoin and global financial assets before and after the COVID-19 outbreak?

Table 10 and

Table 11, respectively, show the asymmetric causality test results between Bitcoin and global financial assets before and after the COVID-19 outbreak. The COVID-19 pandemic did cause changes in the causality between Bitcoin and the global financial assets. Before the pandemic, a negative impact on gold would cause a positive impact on Bitcoin. There is neither Granger nor asymmetric causality between crude oil/US dollar and Bitcoin. Regarding the data on the time after the outbreak of the pandemic, however,

Table 11 shows results in line with those of

Table 9.

5.3. Further Analysis

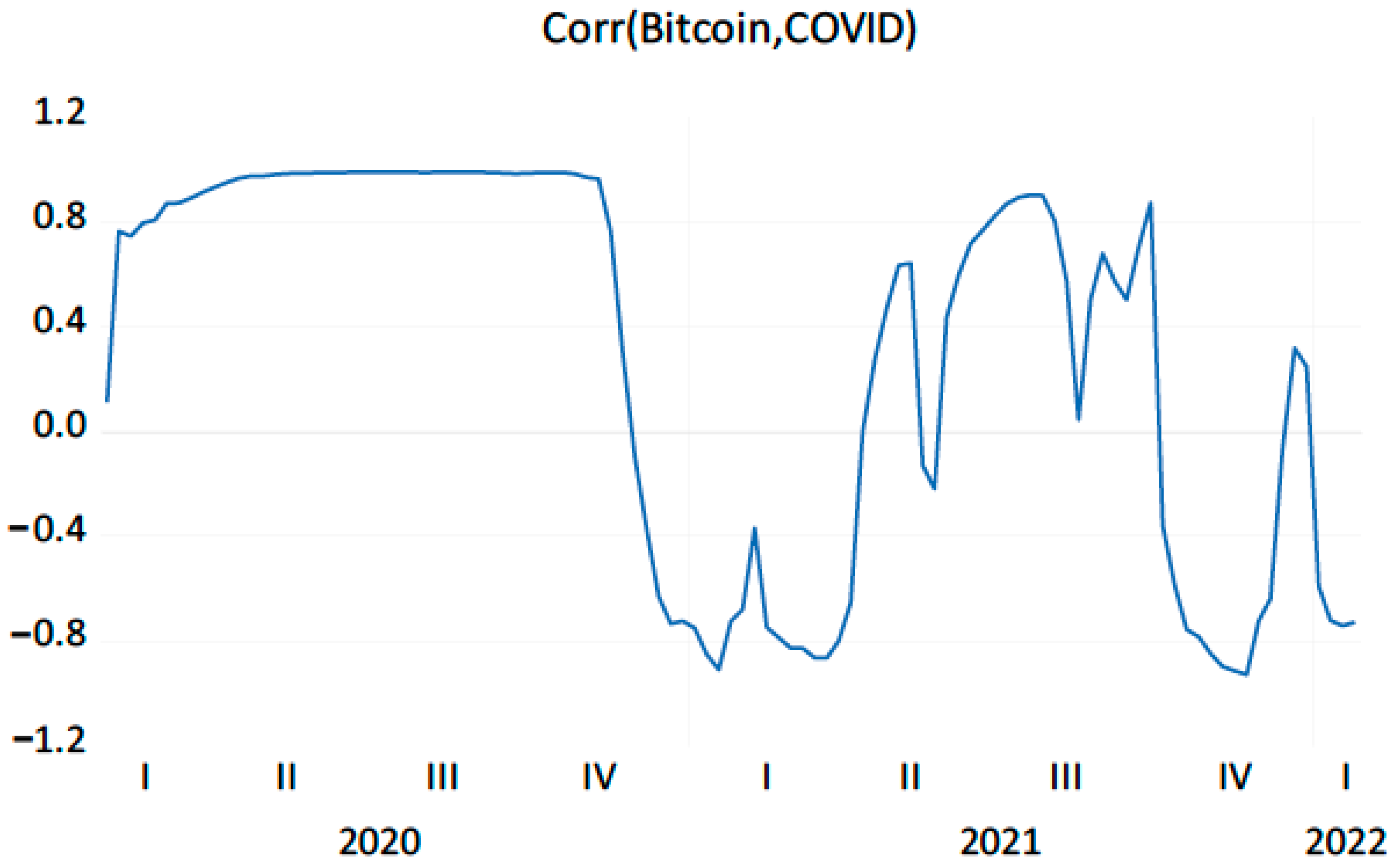

The above empirical results confirm that the asymmetric cointegration and causality between Bitcoin and the global financial assets before and after the COVID-19 pandemic outbreak are significantly different. This suggests that the COVID-19 pandemic has some relationship with such changes at least. Therefore, we need to further investigate the co-movement between Bitcoin and the COVID-19 pandemic. We measured the co-movement between Bitcoin and the global weekly number of confirmed cases using the DCC-GARCH model. The global weekly number of confirmed cases was derived from the Coronavirus Government Response Tracker (OxCGRT) produced by researchers at the Blavatnik School of Government, University of Oxford (

Hasell et al. 2020). The DCC-GARCH model is a common measure of co-movement. For this reason, we did not provide a detailed description of the DCC-GARCH models in this paper. We ran the DCC-GARCH model using Eviews version 10 software.

Figure 4 shows the dynamic correlation between Bitcoin and the COVID-19 pandemic from January 2020 to January 2022. We found a high time-varying correlation between Bitcoin and the COVID-19 pandemic. Bitcoin has a high positive correlation of over 0.9 with the COVID-19 pandemic, especially in the first year of the COVID-19 pandemic. It is safe to say that the price of Bitcoin rose rapidly with the number of confirmed cases in 2020. The high correlation between Bitcoin and the COVID-19 pandemic aptly indicates that Bitcoin was affected by the COVID-19 pandemic, and the COVID-19 pandemic changed the causal relationship between Bitcoin and global financial assets. In addition, we tested for Granger causality between Bitcoin and the COVID-19 pandemic using a VAR model. The results showed that the Chi-square statistic was 8.798 in the Wald test, which rejects the null hypothesis that the COVID-19 pandemic does not Granger-cause Bitcoin at the 5% level. This implies that the COVID-19 pandemic does Granger-cause Bitcoin, which again indirectly supports the suspicion that the COVID-19 pandemic changes the causality of Bitcoin with the global financial assets.

5.4. Discussion

The empirical results have identified the asymmetric co-integration relationship and causality between Bitcoin and the global financial assets. Only a better understanding of these phenomena and findings could help the investors and financial institutions make more informed decisions. First, the relationship between Bitcoin and global financial assets changed somewhat before and after the COVID-19 pandemic. The fall of Bitcoin had a long-run relationship with the rise and fall of gold, crude oil, and the US dollar, but this relationship ceased to exist during the COVID-19 pandemic. There are studies confirming that the New Crown epidemic caused an upward movement of Bitcoin’s price (

Goodell and Goutte 2021), and also revealing a huge volatility change in the relationship between the New Crown epidemic and the energy market (

Maneejuk et al. 2021). This may all indirectly confirm our view. On the one hand, this suggests that the COVID-19 pandemic hit global economic development, leading to a more complex relationship between Bitcoin and global financial assets. On the other hand, during the COVID-19 pandemic, because Bitcoin did not have a long-term relationship with gold, crude oil, and the US dollar, financial institutions and investors could no longer make investment decisions based on the fact that they had a long-term relationship due to the fact that the relevance of Bitcoin and traditional financial assets during tranquil and turbulent periods is significantly different (

Elsayed et al. 2022). Second, the causality between Bitcoin and the global financial assets also changed significantly before and after the outbreak of the COVID-19 pandemic. Before the COVID-19 pandemic, only the fall in the price of gold was a Granger causality for Bitcoin’s rise. No other global financial assets were Granger causality for Bitcoin. During periods of economic tranquility, the price of gold falls if there is a drop in market demand, which causes some investors to look for higher returns on Bitcoin, which causes the price of Bitcoin to rise (

Kyriazis 2020). After the outbreak of the COVID-19 pandemic, crude oil was the Granger causality for the rise and fall of Bitcoin price.

Li et al. (

2021) substantially supported the view that there is an asymmetric Granger causality between crude oil and Bitcoin.

Bitcoin investors can benefit from following fluctuations in the price of gold and crude oil over time, which can be used to make Bitcoin investment decisions. In periods of economic stability, Bitcoin seekers can refer to movements in the price of gold to formulate investment strategies. In a turbulent economy, movements in the price of crude oil become more important. The US dollar has the lowest reference value compared to gold and crude oil. However, in the long run, when the dollar falls, the risk of Bitcoin falling is higher, and investors and financial institutions need to keep an eye on it frequently.

6. Conclusions

Bitcoin is always popular among investors. A clear understanding of the relationship between Bitcoin and global financial assets is essential to investors and financial institutions. Based on existing studies, asymmetric co-integration and causality tests are adopted to explore the asymmetric co-integration and causality between Bitcoin and gold, Bitcoin and crude oil and Bitcoin and gold. The test results are shown as below: first, using Engle–Granger co-integration test, we found that there is no co-integration relationship between Bitcoin and the global financial assets. Second, there is a significant co-integration relationship between the negative impact on the US dollar and the positive impact on Bitcoin. Third, there is a co-integration relationship between a positive (negative) impact on the global financial assets and a negative impact on Bitcoin. Fourth, there is a Granger causality between crude oil and Bitcoin, wherein a negative impact on crude oil causes a negative impact on Bitcoin too. Fifth, there is no causality between gold/US dollar and Bitcoin. These findings identify the relationship between Bitcoin and global financial assets from an asymmetric perspective, and may facilitate decision making and risk avoidance for investments in Bitcoin and the global financial assets.

The results of this paper are not only supported by other literature, but also further extend previous research. The relationship between Bitcoin and crude oil became stronger during the COVID-19 pandemic (

Yousaf et al. 2022), which just shows that the epidemic changed the relationship between Bitcoin and crude oil. This finding also validates the idea that the relationship between Bitcoin and the global financial assets changed before and after the COVID-19 pandemic in this paper. Similarly, the relationship between Bitcoin and gold, and Bitcoin and the US dollar increased during the epidemic (

González et al. 2021). It may not be accurate to test the cointegration and causality between Bitcoin and the global financial assets using data from the early stages of the outbreak.

Ibrahim and Ali Basah (

2022) found no causal relationship between Bitcoin and gold, crude oil, and the US dollar. Instead, we further analyze their asymmetric causality and cointegration.

This paper, despite its findings in the asymmetric relationship between Bitcoin and global financial assets, has its limitations. Both the asymmetric co-integration test and asymmetric Granger causality test are static and unable to reflect the dynamic relationship between Bitcoin and global financial assets. Also, the trends of Bitcoin and global financial assets may have their own cycles. The co-integration relationship or causality may vary with the economic cycles. In addition, the Engle–Granger method leads to severe downward bias in the long-run (cointegration) parameter, and the Johansen Cointegration Test is preferable to the Engle and Granger procedures (

Bilgili 1998). Therefore, future studies require us to explore the dynamic relationship between Bitcoin and global financial assets, as well as the co-integration and causality in different time periods. How to use the Johansen approach in the asymmetric cointegration test is also worth exploring.

{kind=link}

{kind=link}

{kind=link}

{kind=link}