Deciphering DeFi: A Comprehensive Analysis and Visualization of Risks in Decentralized Finance

Abstract

:1. Introduction

2. Decentralized Finance

- Decentralization: DeFi is based on decentralized networks, notably blockchain, which is a decentralized and distributed ledger technology that records transactions across multiple computers securely, transparently, and immutably, as well as peer-to-peer networks. These technologies function without a central authority or intermediaries.

- Smart contracts: DeFi relies on smart contracts, defined as self-executing contracts, where the terms are directly written into code and run on a blockchain, ensuring that they are not only tamper-proof but also automatically enforceable without the need for a centralized authority. These blockchain-encoded, self-executing, and enforceable computer programs enable DeFi to automate complex operations, remove the need for intermediaries, and increase efficiency and trust;

- Crypto assets: DeFi makes use of crypto assets, such as cryptocurrencies and tokens, as a means of exchanging and storing wealth. Crypto assets provide DeFi products with higher liquidity, flexibility, increased speed and accessibility than conventional assets, allowing DeFi to offer innovative financial products and services;

- Open finance: Open finance is the use of open protocols, standards, and networks to facilitate financial innovation and interoperability. Open finance enables DeFi to offer more inclusive, interoperable, and decentralized financial services than traditional finance;

- DeFi applications: Decentralized applications, also known as dApps, provide the user interface for financial services that run on blockchain systems. DeFi-powered decentralized applications include decentralized exchanges, lending systems, stablecoins, insurance, and prediction markets;

- DeFi ecosystem: The DeFi ecosystem includes blockchain technology and cryptocurrencies, platforms, and communities. Developers, users, investors, academics, regulators, and other stakeholders all contribute to the development and evolution of DeFi.

2.1. Stablecoins

- Fiat-backed stablecoins: Stablecoins are backed by fiat currencies, such as the US dollar, the euro, or other currencies. They are issued and maintained by centralized entities that hold reserves of the corresponding fiat currency;

- Commodity-backed stablecoins: Stablecoins backed by a commodity, like gold or oil. They are also issued and maintained by centralized entities and are supported by reserves of the respective commodity;

- Algorithmic stablecoins: These stablecoins use computer algorithms to keep their value stable. They are not backed by real-world assets but rely on tech solutions instead. Decentralized systems, such as MakerDAO1 and Frax2, issue and control algorithmic stablecoins (Kjäer et al. 2021).

2.2. Liquidity Pools

2.3. Lending Pools

2.4. Automated Market Makers

3. Risks in Traditional Finance and DeFi

3.1. Risk Categories in TradFi

- Credit risk: This is the risk of default or loss on a loan or investment due to the borrower’s or issuer’s inability or reluctance to make regular payments. Credit risk is the primary risk category in traditional finance. It is managed through the establishment of appropriate capital requirements, implementing credit rules and processes, and conducting thorough credit risk assessments;

- Market risk: This is the risk of loss resulting from changes in market pricing or conditions, including interest rates, exchange rates, and stock prices. Market risk is controlled by imposing limitations on market exposure, developing frameworks for market risk management, and conducting routine stress testing;

- Operational risk: This is the risk associated with inadequate or failing internal processes, people, and systems, or external occurrences. Operational risk is managed by creating robust risk management frameworks, conducting regular internal audits, and executing effective contingency plans;

- Liquidity risk: This risk addresses the danger of incurring a loss or being unable to meet financial obligations owing to a lack of liquid assets or finances. Liquidity risk is managed by setting appropriate liquidity ratios, performing liquidity stress tests, and maintaining adequate funding sources;

- Concentration risk: This is the risk of loss resulting from a concentration of exposures to a single counterparty, sector, or geographic region. To manage concentration risk, diversification techniques are implemented, concentration limits are established, and exposures are regularly reviewed and monitored.

3.2. Qualitative Analysis of Risks in DeFi

3.2.1. Technology Risks

Risks from Smart Contracts

- Creation risks: Contract creation is an important step to implement smart contracts. Developers have to code their own contracts and then deploy them in various blockchain platforms. Translating the smart contract using the programming languages, can introduce exploitable vulnerabilities or errors. There might also be arithmetic vulnerabilities, which are types of vulnerabilities caused by flaws or errors in the contract’s arithmetic computations. Other vulnerabilities in this category are re-entrancy vulnerability (Li et al. 2020), block randomness vulnerability (Bonneau et al. 2015), and overcharging (Chen et al. 2017).

- Deployment risks: Smart contracts need to be checked carefully before deploying on blockchain platforms to avoid potential bugs that can be exploited by malicious behaviors. However, it is challenging to verify the correctness of smart contracts due to the complexity of modeling smart contracts, it is of vital importance to evaluate the correctness of smart contracts before the formal deployment (Luu et al. 2016).

- Execution risks: The execution phase is pivotal to smart contracts, as it determines the final state of smart contracts. Since smart contracts cannot work without real-world information, it is necessary to rely on a trustworthy oracle (Al-Breiki et al. 2020). Also, the dependence of the order of transactions is challenging to solve it in smart contracts, and developers should be aware to mitigate potential losses (Mavridou and Laszka 2017). Finally, smart contracts are executed in serialization, which limits the system performance. There are some software transactional memory systems that help to improve the execution efficiency of smart contracts (Bragagnolo et al. 2018), but more work needs to be performed.

- Completion risks: The proliferation of smart contracts brings additional concerns. Most current smart contract and blockchain platforms lack privacy-preserving mechanisms, especially concerning transactional privacy. Consequently, all the transactions are visible to everyone in the networks. Although some blockchain systems use pseudonymous public keys to improve the anonymity of the transactions, most transaction data are still publicly visible (Ron and Shamir 2013).

Risks from the Blockchain Protocol

- Changes to the protocol: Changes to the blockchain protocol can happen via hard forks, soft forks, protocol upgrades, or modifications from a governance process. A hard fork is a modification to the blockchain protocol that is not backward-compatible, requiring all network participants to update to the latest version of the program. A soft fork is a backward-compatible update to the blockchain protocol that may be executed without needing all users to upgrade their software. Some blockchain protocols, including Ethereum, have a method for executing protocol upgrades. Depending on the nature of the modifications being made, these enhancements may be introduced via a hard fork or a soft fork. Some blockchain networks provide a governance procedure that enables users to propose and vote on protocol modifications. The execution method for these modifications depends on the specific network, the type of proposed change, and the community’s social structure. They can be implemented through a hard fork, a soft fork, or another method. There is the risk of fraud or sub-optimal outcomes of these change processes, as described in Barrera and Hurder (2018).

- Centralization: Consensus protocols, such as proof-of-work (PoW) or proof-of-stake (PoS), might be susceptible to centralization, which occurs when a small number of users control a considerable majority of the network’s computational capacity (Gencer et al. (2018)). This is called a 51% attack. PoS protocols depend on a limited set of validators to validate transactions and establish consensus on the blockchain’s state. If these validators are hacked or do not function in the best interests of the network, it might pose a risk to DeFi users. Further risks specific to the used consensus protocols are: selfish mining, pool hopping attack, Sybil attack, or nothing at stake attack.

- Performance and scalability: DeFi products can also be affected by the speed and scalability of a consensus mechanism. If the protocol cannot manage a huge amount of transactions or has a high latency, it might cause DeFi users to experience delays and other issues.

- Front running: Front running is a method of trading that includes profiting on knowledge of a future deal. This risk already existed in traditional finance (Cai 2003). A person or entity can engage in front running in the context of decentralized finance (DeFi) if they are able to monitor a trade that is about to be performed on a blockchain and then arrange their own trade ahead of it to gain an advantage. Often, the transaction pool (mempool) is used for front running. We also include attacks like sandwich attacks this category.

Risks from the Use of Oracles

Risks from the Use of Liquidity Pools

- Impermanent loss: During extreme market fluctuations, liquidity pools risk impermanent loss. In simple terms, impermanent loss means that the FIAT value of a user’s crypto assets deposited to a pool could decline over time.

- Smart contract vulnerabilities: Once assets have been added to a liquidity pool, they are controlled exclusively by a smart contract, with no central authority or custodian. So, if a bug or some vulnerability is exploited, they could lose the coins for good.

- Liquidation risk: As liquidity pools are often leveraged, there is a risk of forced liquidation if the price of the assets devalues. The highly volatile market of the crypto-currencies and the vulnerabilities can lead to liquidity problems. Recently, the missing payments on USD 17.7 million of loans from lending pools after a sudden implosion of FTX percolated to creditors on lending protocols (Sandor 2022). Solend, a decentralized lending protocol on the Solana network, has narrowly avoided having 95% of the SOL deposits in its lending pool liquidated (Elliot 2022). As the price of SOL continued to drop and the collateral is used for liquidation, Solend almost ended with no SOL.

- Flash loan attack: Flash loans are unlimited and non-collateralized loans in which a user borrows funds and returns them in the same transaction. Malicious actors use flash loans to manipulate the price of the market, resulting in the theft of assets. In 2021, a flash loan attack caused the value of the token to drop 95% (Crawley 2021). The attacker profited USD 3 million and left the company to adapt their strategy to prioritize security instead of product release. These attacks are becoming a serious problem in cryptocurrency and are increasing yearly. In 2021, attackers gained over USD 3.2 billion in various attacks, hacks, and scams. In 2022, this value raised to USD 3.7 billion (Malwa 2022).

- Vampire attack: Although unusual, vampire attacks can lead to the depletion of a liquidity pool. This attack drains the liquidity from one exchange to another source. Uniswap has become a victim of a vampire attack when a cloned exchange called SushiSwap siphoned USD 1.2 billion in liquidity (Kelly and Balakrishnan 2020). Although SushiSwap returned USD 14 million in Ether, this attack cast a shadow on the confidence of DeFi’s community in this DEX.

Risks from the Use of Lending Pools

- Liquidity risk: Currently, the main depositors contribute to most liquidity in LPs (Gudgeon et al. 2020) and a small group of borrowers account for most loans. For instance, when dual-role users supply stablecoins, they can launch illiquidity risks by withdrawing their deposits and not repay the loans. Aave protocol benefit from more revenue when potential risks are higher. This is consistent with the logic around LPs. LPs rely on users to provide liquidity. Therefore, these dual-role users can booster the growth of Aave by depositing their stablecoins. In contrast, this protocol faces negative consequences when the risk of potential illiquidity increases, because it can lead to devaluations of Aave protocol.

- Counterparty risk: Counterparty risk happens when one party in a financial transaction cannot fulfill their commitments. A reentrancy attack can be used as a tool to drain the liquidity. Since blockchain allows smart contracts to work without the need to trust any party except the smart contract itself, the untrusted contract then calls back to the original function in an attempt to drain funds. To avoid this risk, the security of a smart contract is a vital in DeFi.

Risks from Internet and Online Access

3.2.2. Market and Financial Risks

- Counterparty risk: Since DeFi depends on an interconnected network of smart contracts and other applications, the failure of a single component can have cascading effects on the entire system. The term for this is counterparty risk.

- Volatility and leverage: The values of cryptocurrencies and other assets utilized in DeFi often have an enormous leverage effect and can be extremely volatile, meaning that users may incur substantial losses if the value of their assets declines.

- Liquidity risk: Some DeFi systems and protocols may have restricted liquidity, making it challenging for users to purchase or sell particular assets. This can generate liquidity risk, since consumers may be unable to readily transfer their assets into cash or other kinds of value.

- Credit risk: Certain DeFi products, including decentralized exchanges (DEXs) and lending platforms, extend credit to customers. This can create credit risk, as there is a chance that borrowers will default on their loans or that the value of the collateralized assets would drop. Credit risks in DeFi differ from traditional finance because loans are typically overcollateralized.

3.2.3. Operational Risks

- Governance risks: Governance risks in DeFi relate to the uncertainties associated with the procedures and mechanisms that are used to make decisions concerning the operation and development of DeFi platforms and protocols. This could be the lack of transparency, making it difficult for consumers to comprehend how and by whom decisions are made Makridis et al. (2023). Also, some DeFi governance organizations may not be responsible to users, meaning that consumers may have few options if anything goes wrong or if they disagree with the decisions made. If a small number of persons or entities has disproportionate control over DeFi governance procedures, this might pose hazards for DeFi users, since these individuals or businesses may be able to make choices that are not in the best interests of the larger community. These decision-making processes utilized by DeFi governing bodies may be inefficient or susceptible to bias, which might result in subpar decision-making and cause hazards for DeFi users.

- Inappropriate key management: One aspect of governance risk involves the mishandling of private keys. The vast majority of DeFi smart contracts permit an update or even a trade halt. These transactions are performed using the product administrators’ wallet and private keys. Any unauthorized use or theft of these private keys might lead to the loss of all funds. These may occur both intentionally and accidentally.

- Prospectus risks: “Depending on the country and legal structure of the underlying tokens, DeFi products might fall in the category of securities or asset tokens. For example, in Switzerland this token category result in prospectus requirements under the Swiss Code of Obligations” (FINMA 2018, pp. 6/11). This means that missing prospectus or errors in the descriptions can have legal consequences for the issuer.

3.2.4. Legislative, Regulatory and Governance Risks

- Legal status of smart contracts: Since smart contracts are self-executing, there is typically no legal redress when anything goes wrong. This implies that it may be difficult or impossible to remedy the issue if a contract is abused or a mistake is made in the code.

- Legal, regulatory, and compliance risk: DeFi is a very new and mostly unregulated field, which implies that there is a lack of legal and regulatory control. This can pose dangers for DeFi users, since they may have little options if something goes wrong. These risks can arise if either already existing legal requirements are not complied with or if the legal framework changes but the DeFi product is not or cannot be adapted.

3.2.5. Strategic and Reputational Risks

- Changes in technology: the DeFi area is characterized by fast technical development, and platforms and protocols that do not keep up with these changes risk becoming obsolete or less appealing to consumers;

- Reputational risk: the reputation of a DeFi platform or protocol is crucial to its success, and any unfavorable press or security breaches might harm its reputation and reduce its appeal to users;

- Leave risk: if a DeFi platform or protocol encounters substantial issues or loses the confidence of its users, there is a danger that users would “exit” the platform, which might result in a loss of value or the platform’s demise.

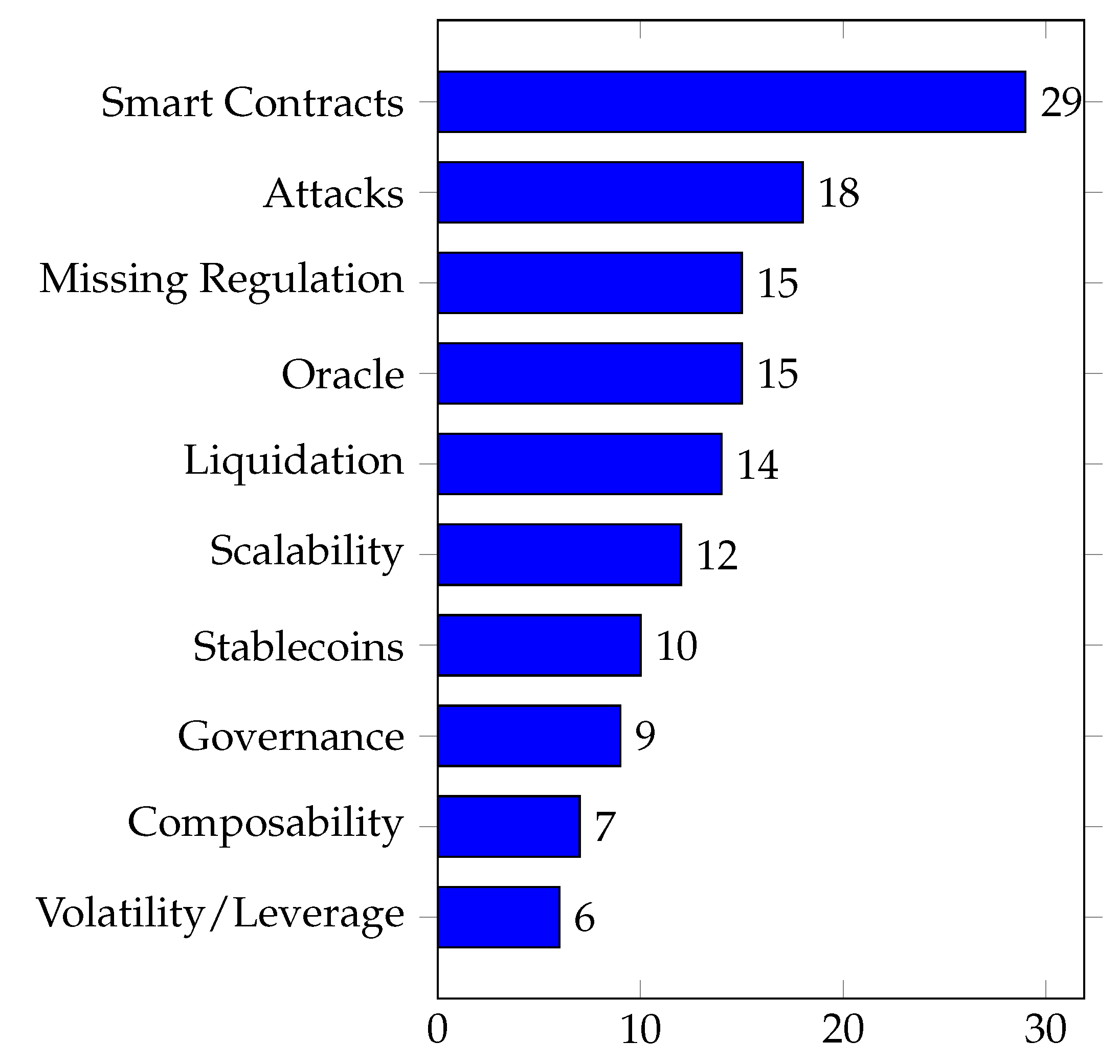

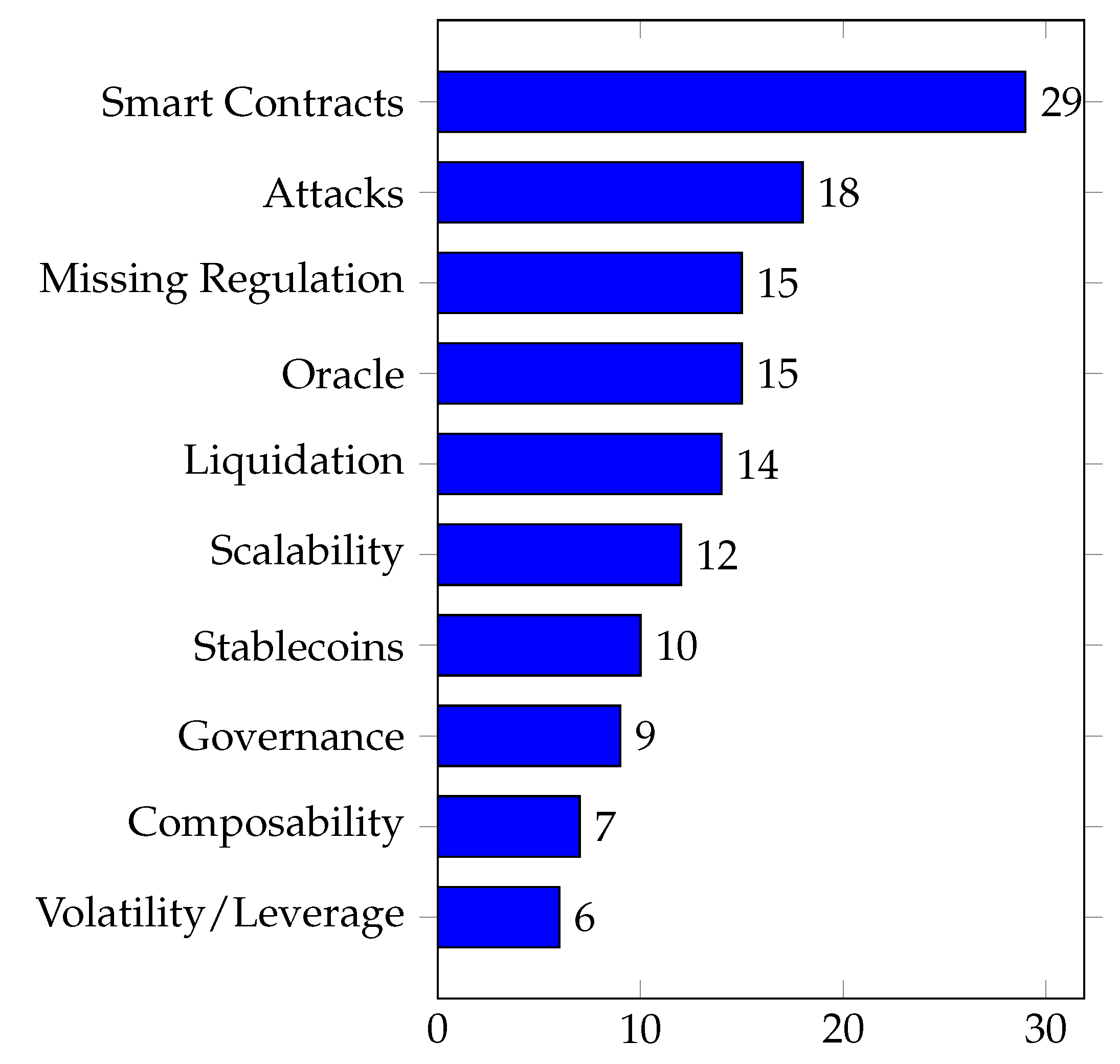

3.3. Quantitative Literature Review of DeFi Risks

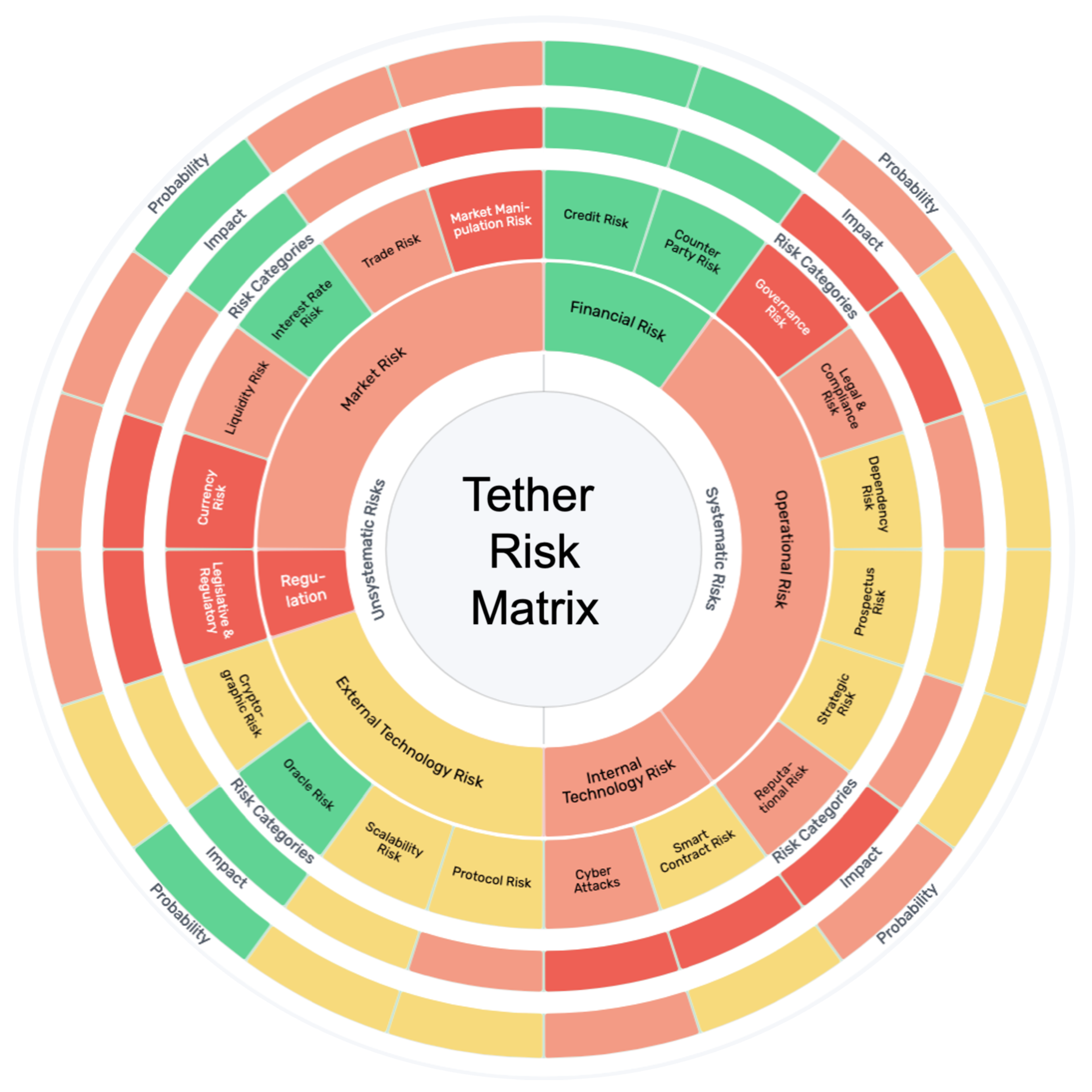

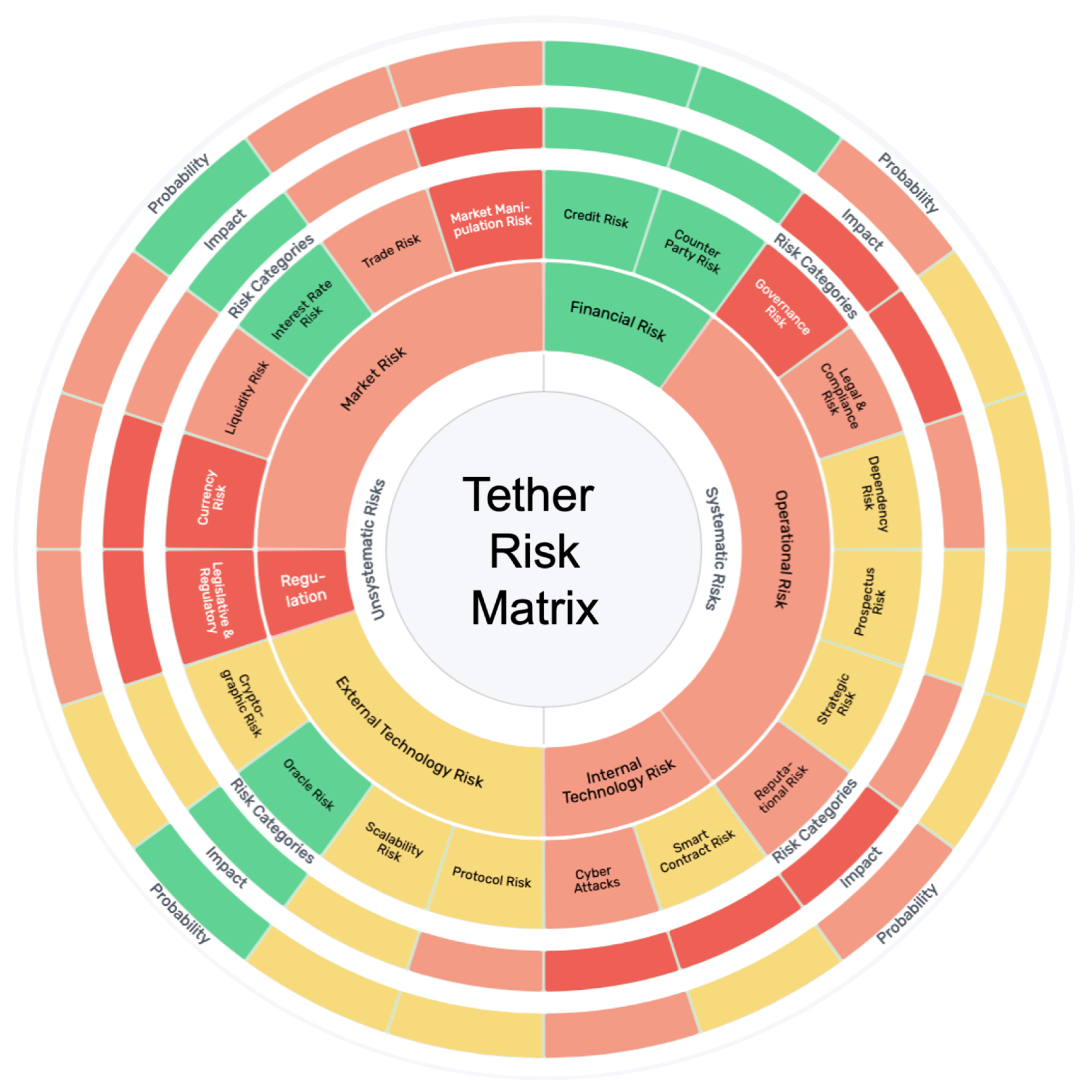

4. Classification of Risks in DeFi

5. Assessing Risks in DeFi

5.1. Static Risk Assessment

5.2. Continuous Risk Monitoring

5.3. Risk-Based Comparison of DeFi Products

5.4. Subsequent Analysis of Risk Incidents

5.5. Educational Tool

6. Discussion

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Title | Reference | Year | DeFi | DeFi Risks | DeFi Protocol | TradFi | Total | Smart Contracts | Attacks | Missing Regulation | Oracle | Liquidation | Scalability | Stablecoins | Governance | Composability | Volatility/Leverage | Other Risks |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DeFi protocol risks: the paradox of DeFi | Carter and Jeng (2021) | 2021 | 2 | 2 | 2 | 2 | 8 | X | X | X | X | Operational Risk | ||||||

| DeFi risks and the decentralisation illusion | Aramonte et al. (2021) | 2021 | 2 | 2 | 1 | 2 | 7 | X | X | X | ||||||||

| A Risk Classification Framework for Decentralized Finance Protocols | Chang et al. (2022) | 2022 | 2 | 2 | 2 | 1 | 7 | X | X | MEV, network effect | ||||||||

| Decentralized Finance (DeFi): Foundations, Applications, Potentials, and Challenges | Gramlich et al. (2022) | 2022 | 2 | 2 | 2 | 1 | 7 | X | X | X | X | X | ||||||

| Security and efficiency of collateral in decentralized finance | Harz (2022) | 2022 | 2 | 2 | 2 | 1 | 7 | X | X | X | Governance, technical security | |||||||

| Risks in DeFi-Lending Protocols-An Exploratory Categorization and Analysis of Interest Rate Differences | Huber and Treytl (2022) | 2022 | 2 | 2 | 2 | 1 | 7 | X | X | X | X | Operational risk | ||||||

| A Survey of DeFi Security: Challenges and Opportunities | Li et al. (2022) | 2022 | 2 | 2 | 2 | 1 | 7 | X | X | Cybersecurity, design issues | ||||||||

| An empirical study of DeFi liquidations: Incentives, risks, and instabilities | Qin et al. (2021) | 2021 | 2 | 2 | 2 | 1 | 7 | X | Flash loans | |||||||||

| Deceptive Assurance? A Conceptual View on Systemic Risk in Decentralized Finance (DeFi) | Bekemeier (2021) | 2021 | 1 | 2 | 1 | 2 | 6 | X | X | X | X | X | X | X | ||||

| DeFi Potential, Advantages and Challenges | Borisov (2022) | 2022 | 1 | 2 | 2 | 1 | 6 | X | X | X | X | X | Infrastructure risk | |||||

| Decentralized Finance (DeFi): Transformative Potential & Associated Risks | Carapella et al. (2022) | 2022 | 1 | 2 | 2 | 1 | 6 | X | X | X | X | X | X | X | X | |||

| Security analysis of DeFi: Vulnerabilities, attacks and advances | Li et al. (2022) | 2022 | 1 | 2 | 2 | 1 | 6 | X | X | |||||||||

| Cryptocurrencies and decentralized finance (DeFi) | Makarov and Schoar (2022) | 2022 | 2 | 1 | 1 | 2 | 6 | X | X | Leverage | ||||||||

| Flash crash for cash: Cyber threats in decentralized finance | Oosthoek (2021) | 2021 | 2 | 2 | 2 | 0 | 6 | X | X | |||||||||

| Speculative multipliers on DeFi: Quantifying on-chain leverage risks | Wang et al. (2022) | 2022 | 2 | 2 | 2 | 0 | 6 | X | X | X | ||||||||

| Centralized and decentralized finance: Coexistence or convergence? | Wieandt and Heppding (2023) | 2023 | 2 | 1 | 1 | 2 | 6 | X | X | X | X | X | ||||||

| Defining DeFi: Challenges & pathway | Amler et al. (2021) | 2021 | 1 | 1 | 1 | 2 | 5 | X | X | X | X | X | Data protection, infrastructure | |||||

| Embedded Supervision: How to Build Regulation Into Decentralized Finance | Auer (2022) | 2022 | 1 | 1 | 1 | 2 | 5 | X | Exchanges | |||||||||

| DeFi Survival Analysis: Insights into Risks and User Behavior | Green et al. (2022) | 2023 | 1 | 2 | 2 | 0 | 5 | X | Lending protocol | |||||||||

| SoK: Preventing Transaction Reordering Manipulations in Decentralized Finance | Heimbach and Wattenhofer (2022) | 2022 | 1 | 2 | 2 | 0 | 5 | X | ||||||||||

| Advantages and disadvantages of decentralized financial (DeFi) services | Kirvesoja (2022) | 2022 | 2 | 1 | 0 | 2 | 5 | X | X | X | Flash loans, illegal activities, systemic risk | |||||||

| Stablecoins and Their Risks to Financial Stability | MacDonald and Zhao (2022) | 2022 | 1 | 1 | 2 | 1 | 5 | X | ||||||||||

| Risks and benefits of centralized and decentralized cryptocurrency exchanges and services | Nummelin (2022) | 2022 | 2 | 2 | 0 | 1 | 5 | X | Fraud, scams | |||||||||

| Decentralized finance (DeFi)–the lego of finance | Popescu (2020) | 2020 | 2 | 1 | 2 | 0 | 5 | X | X | Fraud | ||||||||

| Decentralized finance: On blockchain-and smart contract-based financial markets | Schär (2021) | 2021 | 2 | 2 | 1 | 0 | 5 | X | X | X | X | |||||||

| Decentralized finance (DeFi) | Zetzsche et al. (2020) | 2020 | 2 | 1 | 0 | 2 | 5 | X | Lack of support in times of crisis, technological dependency, price manipulation | |||||||||

| SoK: lending pools in decentralized finance | Bartoletti et al. (2021) | 2021 | 1 | 2 | 1 | 0 | 4 | X | X | X | ||||||||

| Governing Decentralized Finance (Defi) | Bhambhwani (2023) | 2022 | 1 | 1 | 2 | 0 | 4 | X | ||||||||||

| A deep dive into crypto financial risks: stablecoins, DeFi and climate transition risk | Born et al. (2022) | 2022 | 0 | 1 | 2 | 1 | 4 | X | X | X | X | Risk appetite, spillover effect | ||||||

| Risk Analysis of Crypto Assets | Botte and Nigro (2021) | 2021 | 0 | 2 | 1 | 1 | 4 | Correlation, complexability, | ||||||||||

| Flashot: a snapshot of flash loan attack on DeFi ecosystem | Cao et al. (2021) | 2021 | 2 | 1 | 1 | 0 | 4 | X | X | Flash loans | ||||||||

| Blockchain disruption and decentralized finance: The rise of decentralized business models | Chen and Bellavitis (2020) | 2020 | 2 | 1 | 1 | 0 | 4 | X | X | Data protection | ||||||||

| Decentralized finance (DeFi): an emergent alternative financial architecture | Chohan (2021) | 2021 | 1 | 1 | 1 | 1 | 4 | X | X | X | Arbitrage, manipulationen, money laundry | |||||||

| Do we still need financial intermediation? The case of decentralized finance–DeFi | Grassi et al. (2022) | 2022 | 1 | 1 | 1 | 1 | 4 | X | X | Technology risks | ||||||||

| Manage Risk in DeFi Portfolio | Inzirillo and De Quénetain (2022) | 2022 | 1 | 2 | 1 | 0 | 4 | X | X | X | X | Double Spending attack | ||||||

| An introduction to decentralized finance (DeFi) | Jensen et al. (2021) | 2021 | 1 | 2 | 1 | 0 | 4 | X | X | X | X | |||||||

| Stablecoins 2.0: Economic foundations and risk-based models | Klages-Mundt et al. (2020) | 2020 | 1 | 1 | 1 | 1 | 4 | X | X | X | X | Stability, counterparty risk | ||||||

| MiCA and DeFi (‘Proposal for a Regulation on Market in Crypto-Assets’ and ‘Decentralised Finance’) | Maia and Vieira dos Santos (2021) | 2021 | 2 | 1 | 1 | 0 | 4 | X | X | |||||||||

| DeFi Risk Transfer: Towards A Fully Decentralized Insurance Protocol | Nadler et al. (2022) | 2022 | 1 | 1 | 2 | 0 | 4 | X | X | X | X | |||||||

| Decentralized Finance & Centralized Finance Analogy | Pardhi et al. (2022) | 2 | 1 | 0 | 1 | 4 | X | Missing customer service | ||||||||||

| Liquidations: DeFi on a Knife-edge | Perez et al. (2021) | 2021 | 1 | 1 | 2 | 0 | 4 | X | ||||||||||

| Attacking the DeFi ecosystem with flash loans for fun and profit | Qin et al. (2021) | 2021 | 1 | 2 | 1 | 0 | 4 | X | ||||||||||

| Challenges and approaches to regulating decentralized finance | Salami (2021) | 2021 | 1 | 1 | 1 | 1 | 4 | X | X | Know-Your-Customer Challenge | ||||||||

| Decentralized finance (DeFi) compliance and operations | Scharfman and Scharfman (2022) | 2022 | 2 | 1 | 1 | 0 | 4 | X | X | |||||||||

| DeFi: decentralized finance-an introduction and overview | Schueffel (2021) | 2021 | 2 | 0 | 1 | 1 | 4 | X | X | X | ||||||||

| P2P-The Key Behind Regulatory Framework of DeFi Services | Shalini et al. (2023) | 2023 | 1 | 2 | 0 | 1 | 4 | X | X | X | X | X | ||||||

| Liquidity Risks in Lending Protocols (LPs): Evidence from Aave Protocol | Sun (2022) | 2022 | 1 | 1 | 2 | 0 | 4 | X | ||||||||||

| Rethinking the Rule and Role of Law in Decentralized Finance | Wang (2022) | 2022 | 1 | 1 | 1 | 1 | 4 | X | Unstable loss, arbitrage | |||||||||

| Blockeye: Hunting for DeFi attacks on blockchain | Wang et al. (2021) | 2021 | 1 | 2 | 1 | 0 | 4 | X | X | |||||||||

| Sok: Decentralized finance (DeFi) incidents | Zhou et al. (2023) | 2023 | 1 | 1 | 2 | 0 | 4 | X | X | X | Cyber risks, front running | |||||||

| 50 sources | 29 | 18 | 15 | 15 | 14 | 12 | 10 | 9 | 7 | 6 |

| 1 | https://makerdao.com/ (accessed on 20 December 2022). |

| 2 | https://frax.finance/ (accessed on 20 December 2022). |

| 3 | https://plandisc.com/ (accessed on 3 October 2023). |

References

- Al-Breiki, Hamda, Muhammad Habib Ur Rehman, Khaled Salah, and Davor Svetinovic. 2020. Trustworthy blockchain oracles: Review, comparison, and open research challenges. IEEE Access 8: 85675–85. [Google Scholar] [CrossRef]

- Amler, Hendrik, Lisa Eckey, Sebastian Faust, Marcel Kaiser, Philipp Sandner, and Benjamin Schlosser. 2021. Defi-ning DeFi: Challenges & pathway. Paper presented at the 2021 3rd Conference on Blockchain Research & Applications for Innovative Networks and Services (BRAINS), Paris, France, September 27–30; pp. 181–84. [Google Scholar]

- Aramonte, Sirio, Wenqian Huang, and Andreas Schrimpf. 2021. Defi Risks and the Decentralisation Illusion. BIS Quarterly Review. December 6. Available online: https://www.bis.org/publ/qtrpdf/r_qt2112b.htm (accessed on 29 January 2023).

- Auer, Raphael. 2022. Embedded supervision: How to build regulation into decentralized finance. Cryptoeconomic Systems 2: 1–48. [Google Scholar] [CrossRef]

- Barrera, Cathy, and Stephanie Hurder. 2018. Blockchain Upgrade as a Coordination Game. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3192208 (accessed on 29 January 2023).

- Bartoletti, Massimo, James Hsin-yu Chiang, and Alberto Lluch Lafuente. 2021. Sok: Lending pools in decentralized finance. In Financial Cryptography and Data Security. FC 2021 International Workshops: CoDecFin, DeFi, VOTING, and WTSC, Virtual Event, March 5, Revised Selected Papers 25. Berlin and Heidelberg: Springer, pp. 553–78. [Google Scholar]

- Basel Committee on Banking Supervision. 2011. Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems. [Revised Version: June 2011; Online]. Available online: https://www.bis.org/publ/bcbs189.pdf (accessed on 29 January 2023).

- Bekemeier, Felix. 2021. Deceptive assurance? a conceptual view on systemic risk in decentralized finance (DeFi). Paper presented at the 2021 4th International Conference on Blockchain Technology and Applications, Xi’an, China, December 17–19; pp. 76–87. [Google Scholar]

- Bhambhwani, Siddharth M. 2023. Governing Decentralized Finance (DeFi). Available online: https://ssrn.com/abstract=4513325 (accessed on 17 July 2023).

- Bonneau, Joseph, Jeremy Clark, and Steven Goldfeder. 2015. On Bitcoin as a Public Randomness Source. Cryptology ePrint Archive, Paper 2015/1015. Available online: https://eprint.iacr.org/2015/1015 (accessed on 1 October 2023).

- Borisov, Svetoslav. 2022. Defi–potential, advantages and challenges. Economic Studies 31: 33–54. [Google Scholar]

- Born, Alexandra, and Josep M. Vendrell Simón. 2022. A Deep Dive into Crypto Financial Risks: Stablecoins, DeFi and Climate Transition Risk. Macroprudential Bulletin. Available online: https://ideas.repec.org/a/ecb/ecbmbu/20221.html (accessed on 1 October 2023).

- Botte, Alex, and Mike Nigro. 2021. Risk Analysis of Crypto Assets. TwoSigma. July. Available online: https://www.twosigma.com/wp-content/uploads/2021/07/Using-Factors-to-Explain-Risk-in-Crypto-Assets-3.pdf (accessed on 1 October 2023).

- Bragagnolo, Santiago, Henrique Rocha, Marcus Denker, and Stephane Ducasse. 2018. Smartinspect: Solidity smart contract inspector. Paper presented at the 2018 International Workshop on Blockchain Oriented Software Engineering (IWBOSE), Campobasso, Italy, March 20; pp. 9–18. [Google Scholar] [CrossRef]

- Cai, Fang. 2003. Was There Front Running during the Ltcm Crisis? Available online: https://ssrn.com/abstract=385560 (accessed on 19 October 2023).

- Caldarelli, Giulio. 2020. Understanding the blockchain oracle problem: A call for action. Information 11: 509. [Google Scholar] [CrossRef]

- Cao, Yixin, Chuanwei Zou, and Xianfeng Cheng. 2021. Flashot: A snapshot of flash loan attack on DeFi ecosystem. arXiv arXiv:2102.00626. [Google Scholar]

- Carapella, Francesca, Edward Dumas, Jacob Gerszten, Nathan Swem, and Larry Wall. 2022. Decentralized Finance (DeFi): Transformative Potential & Associated Risks. August 2022. FEDS Working Paper No. 2022-57. Available online: https: //www.federalreserve.gov/econres/feds/decentralized-finance-defi-transformative-potential-and-associated-risks.htm (accessed on 19 October 2023).

- Carter, Nic, and Linda Jeng. 2021. Defi protocol risks: The paradox of DeFi. Regtech, Suptech and Beyond: Innovation and Technology in Financial Services” RiskBooks–Forthcoming Q 3 2021. Available online: https://ssrn.com/abstract=3866699 (accessed on 19 October 2023).

- Chang, Tara, Joe Ho, Zachary Tirrell, Gwen Weng, and Jo You. 2022. A Risk Classification Framework for Decentralized Finance Protocols. Available online: https://www.soa.org/resources/research-reports/2022/decentralized-finance-protocols/ (accessed on 6 January 2023).

- Chen, Ting, Xiaoqi Li, Xiapu Luo, and Xiaosong Zhang. 2017. Under-optimized smart contracts devour your money. Paper presented at the 2017 IEEE 24th International Conference on Software Analysis, Evolution and Reengineering (SANER), Klagenfurt, Austria, February 20–24; pp. 442–46. [Google Scholar] [CrossRef]

- Chen, Yan, and Cristiano Bellavitis. 2020. Blockchain disruption and decentralized finance: The rise of decentralized business models. Journal of Business Venturing Insights 13: e00151. [Google Scholar] [CrossRef]

- Chohan, Usman W. 2021. Decentralized finance (DeFi): An emergent alternative financial architecture. Critical Blockchain Research Initiative (CBRI) Working Papers. Available online: https://ssrn.com/abstract=3791921 (accessed on 19 October 2023).

- Crawley, Jamie. 2021. Flash Loan Attack Causes DeFi Token Bunny to Crash over 95%. Available online: https://www.coindesk.com/markets/2021/05/20/flash-loan-attack-causes-defi-token-bunny-to-crash-over-95/ (accessed on 20 December 2022).

- Elliot, Stacy. 2022. How a Solend Whale with a $108 M Loan Nearly Crashed the Solana Network. Available online: https://decrypt.co/103489/solend-whale-108m-loan-nearly-crashed-solana (accessed on 22 December 2022).

- FINMA, Swiss Financial Market Supervisory Authority. 2018. Guidelines for Enquiries Regarding the Regulatory Framework for Initial Coin Offerings (icos). Available online: https://www.finma.ch/en/~/media/finma/dokumente/dokumentencenter/myfinma/1bewilligung/fintech/wegleitung-ico.pdf (accessed on 20 January 2023).

- Gencer, Adem Efe, Soumya Basu, Ittay Eyal, Robbert Van Renesse, and Emin Gün Sirer. 2018. Decentralization in bitcoin and ethereum networks. In Financial Cryptography and Data Security: 22nd International Conference, FC 2018, Nieuwpoort, Curaçao, February 26–March 2, Revised Selected Papers 22. Berlin and Heidelberg: Springer, pp. 439–57. [Google Scholar]

- Gramlich, Vincent, Marc Principato, Benjamin Schellinger, Johannes Sedlmeir, Julia Amend, Jan Stramm, Till Zwede, Jens Strüker, and Nils Urbach. 2022. Decentralized Finance DeFi: Foundations, Applications, Potentials, and Challenges. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4535868 (accessed on 20 January 2023).

- Grassi, Laura, Davide Lanfranchi, Alessandro Faes, and Filippo Maria Renga. 2022. Do we still need financial intermediation? the case of decentralized finance–DeFi. Qualitative Research in Accounting & Management 19: 323–47. [Google Scholar]

- Green, Aaron, Christopher Cammilleri, John Erickson, Oshani Seneviratne, and Kristin Bennett. 2022. DeFi survival analysis: Insights into risks and user behavior. In The International Conference on Mathematical Research for Blockchain Economy. Cham: Springer International Publishing. [Google Scholar]

- Gudgeon, Lewis, Sam Werner, Daniel Perez, and William J Knottenbelt. 2020. Defi protocols for loanable funds: Interest rates, liquidity and market efficiency. Paper presented at the 2nd ACM Conference on Advances in Financial Technologies, New York, NY, USA, October 21–23; pp. 92–112. [Google Scholar]

- Handfield, Robert, and Kevin P. McCormack. 2007. Supply Chain Risk Management: Minimizing Disruptions in Global Sourcing. Boca Raton: CRC Press. [Google Scholar]

- Harz, Dominik Lucas. 2022. Security and Efficiency of Collateral in Decentralized Finance. Dissertation. Available online: http://hdl.handle.net/10044/1/101394 (accessed on 2 January 2023). [CrossRef]

- Heimbach, Lioba, and Roger Wattenhofer. 2022. Sok: Preventing transaction reordering manipulations in decentralized finance. arXiv arXiv:2203.11520. [Google Scholar]

- Hines, Richard. 2022. Attackers Hijack $1.26 Million from Solend Lending Platform. Available online: https://heraldsheets.com/attackers-hijack-1-26-million-from-solend-lending-platform/ (accessed on 2 January 2023).

- Huber, Marco, and Vinzenz Treytl. 2022. Risks in DeFi-lending protocols-an exploratory categorization and analysis of interest rate differences. In Database and Expert Systems Applications-DEXA 2022 Workshops: 33rd International Conference, DEXA 2022, Vienna, Austria, 22–24 August 2022, Proceedings. Berlin and Heidelberg: Springer, pp. 258–69. [Google Scholar]

- Inzirillo, Hugo, and Stanislas De Quénetain. 2022. Manage risk in DeFi portfolio. arXiv arXiv:2205.14699. [Google Scholar]

- Jensen, Johannes Rude, Victor von Wachter, and Omri Ross. 2021. An introduction to decentralized finance (DeFi). Complex Systems Informatics and Modeling Quarterly 26: 46–54. [Google Scholar] [CrossRef]

- Kelly, Liam, and Ashwath Balakrishnan. 2020. All You Need to Know about DeFi’s SushiSwap Saga. Available online: https://cryptobriefing.com/all-you-need-know-about-defis-sushiswap-saga/ (accessed on 14 January 2023).

- King, Peter, and Heath Tarbert. 2011. Basel iii: An overview. Banking & Financial Services Policy Report 30: 1–18. [Google Scholar]

- Kirvesoja, Ville. 2022. Advantages and Disadvantages of Decentralized Financial (DeFi) Services. Master’s Thesis, University of Jyväskylä, Jyväskylä, Finland. Available online: http://urn.fi/URN:NBN:fi:jyu-202206153332 (accessed on 20 February 2023).

- Kjäer, Martin, Monika Di Angelo, and Gernot Salzer. 2021. Empirical evaluation of makerdao’s resilience. Paper presented at the 2021 3rd Conference on Blockchain Research & Applications for Innovative Networks and Services (BRAINS), Paris, France, September 27–30; pp. 193–200. [Google Scholar]

- Klages-Mundt, Ariah, Dominik Harz, Lewis Gudgeon, Jun-You Liu, and Andreea Minca. 2020. Stablecoins 2.0: Economic foundations and risk-based models. Paper presented at the 2nd ACM Conference on Advances in Financial Technologies, New York, NY, USA, October 21–23; pp. 59–79. [Google Scholar]

- Li, Wenkai, Jiuyang Bu, Xiaoqi Li, and Xianyi Chen. 2022. Security analysis of DeFi: Vulnerabilities, attacks and advances. Paper presented at the 2022 IEEE International Conference on Blockchain (Blockchain), Espoo, Finland, August 22–25; pp. 488–93. [Google Scholar]

- Li, Wenkai, Jiuyang Bu, Xiaoqi Li, Hongli Peng, Yuanzheng Niu, and Xianyi Chen. 2022. A Survey of DeFi Security: Challenges and Opportunities. arXiv arXiv:2206.11821. [Google Scholar] [CrossRef]

- Li, Xiaoqi, Peng Jiang, Ting Chen, Xiapu Luo, and Qiaoyan Wen. 2020. A survey on the security of blockchain systems. Future Generation Computer Systems 107: 841–53. [Google Scholar] [CrossRef]

- Luu, Loi, Duc-Hiep Chu, Hrishi Olickel, Prateek Saxena, and Aquinas Hobor. 2016. Making smart contracts smarter. In CCS ’16: Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security. New York: Association for Computing Machinery, pp. 254–69. [Google Scholar] [CrossRef]

- MacDonald, Cameron, and Laura Zhao. 2022. Stablecoins and Their Risks to Financial Stability. Bank of Canada Staff Discussion Paper 2022-20. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4466522 (accessed on 20 February 2023).

- Maia, Guilherme C., and João Vieira dos Santos. 2021. MiCA and DeFi (‘Proposal for a Regulation on Market in Crypto-Assets’ and ‘Decentralised Finance’). In Blockchain and the Law: Dynamics and Dogmatism, Current and Future. N. 2, Vol. 28. Available online: https://ssrn.com/abstract=3875355 (accessed on 17 July 2023).

- Makarov, Igor, and Antoinette Schoar. 2022. Cryptocurrencies and Decentralized Finance (DeFi). Technical Report. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Makridis, Christos A., Michael Fröwis, Kiran Sridhar, and Rainer Böhme. 2023. The rise of decentralized cryptocurrency exchanges: Evaluating the role of airdrops and governance tokens. Journal of Corporate Finance 79: 102358. [Google Scholar] [CrossRef]

- Malwa, Shaurya. 2022. 2022 Crypto Attacks Were Least in December, with $62 M Lost in Heists, Certik Says. Available online: https://www.msn.com/en-us/money/markets/2022-crypto-attacks-were-least-in-december-with-62m-lost-in-heists-certik-says (accessed on 3 January 2023).

- Markowitz, Harry. 1952. Portfolio selection. Journal of Finance 7: 77–91. [Google Scholar]

- Mavridou, Anastasia, and Aron Laszka. 2017. Designing secure ethereum smart contracts: A finite state machine based approach. arXiv arXiv:1711.09327. [Google Scholar]

- Meegan, Xavier. 2020. Identifying Key Non-Financial Risks in Decentralised Finance on Ethereum Blockchain. Milano: MIP Politecnico di Milano. [Google Scholar]

- Meyer, Eva, Isabell M. Welpe, and Philipp G. Sandner. 2022. Decentralized finance—A systematic literature review and research directions. ECIS 2022 Research Papers. 25. Available online: https://ssrn.com/abstract=4016497 (accessed on 19 October 2023).

- Mohan, Vijay. 2020. Automated market makers and decentralized exchanges: A DeFi primer. Financial Innovation 8: 1–48. [Google Scholar]

- Nadler, Matthias, Felix Bekemeier, and Fabian Schär. 2022. Defi risk transfer: Towards a fully decentralized insurance protocol. arXiv arXiv:2212.10308. [Google Scholar]

- Nummelin, Sami. 2022. Risks and Benefits of Centralized and Decentralized Cryptocurrency Exchanges and Services. Bachelor Thesis. Available online: https://www.theseus.fi/bitstream/handle/10024/786568/Nummelin_Sami.pdf (accessed on 20 February 2023).

- Oosthoek, Kris. 2021. Flash crash for cash: Cyber threats in decentralized finance. arXiv arXiv:2106.10740. [Google Scholar]

- Pardhi, Sarika, Sakshi Mohale, Nikhil Ganorkar, Aman Jadhao, and Sonal V. Sawarkar. Decentralized finance & centralized finance analogy. In 2022 IJCSPUB, Volume 12, Issue 1 January 2022. Available online: https://ijcspub.org/papers/IJCSP22A1008.pdf (accessed on 22 March 2023).

- Perez, Daniel, Sam M. Werner, Jiahua Xu, and Benjamin Livshits. 2021. Liquidations: Defi on a knife-edge. In Financial Cryptography and Data Security: 25th International Conference, FC 2021, Virtual Event, March 1–5, 2021, Revised Selected Papers, Part II 25. Berlin and Heidelberg: Springer, pp. 457–76. [Google Scholar]

- Peterson, Jack, Joseph Krug, Micah Zoltu, Austin K. Williams, and Stephanie Alexander. 2018. Augur: A Decentralized Oracle and Prediction Market Platform. arXiv arXiv:1501.01042. [Google Scholar] [CrossRef]

- Popescu, Andrei-Dragoş. 2020. Decentralized finance (DeFi)—The lego of finance. Social Sciences and Education Research Review 7: 321–49. [Google Scholar]

- Pourpouneh, Mohsen, Kurt Nielsen, and Omri Ross. 2020. Automated Market Makers. IFRO Working Paper No. 2020/08. Available online: https://www.econstor.eu/handle/10419/222424 (accessed on 3 March 2023).

- Qin, Kaihua, Liyi Zhou, Pablo Gamito, Philipp Jovanovic, and Arthur Gervais. 2021. An empirical study of DeFi liquidations: Incentives, risks, and instabilities. Paper presented at the 21st ACM Internet Measurement Conference, Virtual, November 2–4; pp. 336–50. [Google Scholar]

- Qin, Kaihua, Liyi Zhou, Benjamin Livshits, and Arthur Gervais. 2021. Attacking the DeFi ecosystem with flash loans for fun and profit. In International Conference on Financial Cryptography and Data Security. Berlin and Heidelberg: Springer, pp. 3–32. [Google Scholar]

- Rivas, Ricardo. 2022. DeFi Algorand Based Platform Tinyman Lost $3 Million During an Exploit. Available online: https://www.fxempire.com/news/article/defi-platform-tinyman-lost-3-million-during-an-exploit-855009 (accessed on 6 January 2023).

- Ron, Dorit, and Adi Shamir. 2013. Quantitative analysis of the full bitcoin transaction graph. In International Conference on Financial Cryptography and Data Security. Berlin and Heidelberg: Springer, pp. 6–24. [Google Scholar]

- Rorot. 2013. The BREACH Attack. Available online: https://resources.infosecinstitute.com/topic/the-breach-attack/ (accessed on 7 January 2023).

- Rorot. 2014. Padding Oracle Attack. Available online: https://resources.infosecinstitute.com/topic/padding-oracle-attack-2/ (accessed on 25 July 2014).

- Salami, Iwa. 2021. Challenges and approaches to regulating decentralized finance. American Journal of International Law 115: 425–29. [Google Scholar] [CrossRef]

- Sandor, Krisztian. 2022. Crypto Trading Firm Auros, Hit by FTX Collapse, Discloses Provisional Liquidation. Available online: https://www.coindesk.com/markets/2022/12/20/crypto-trading-firm-auros-hit-by-ftx-collapse-discloses-provisional-liquidation/ (accessed on 20 December 2022).

- Schär, Fabian. 2021. Decentralized finance: On blockchain-and smart contract-based financial markets. FRB of St. Louis. Review. Available online: https://ssrn.com/abstract=3843844 (accessed on 19 October 2023).

- Scharfman, Jason, and Jason Scharfman. 2022. Decentralized finance (DeFi) compliance and operations. In Cryptocurrency Compliance and Operations: Digital Assets, Blockchain and DeFi. Cham: Palgrave Macmillan, pp. 171–86. [Google Scholar]

- Schueffel, Patrick. 2021. Defi: Decentralized finance-an introduction and overview. Journal of Innovation Management 9: I–XI. [Google Scholar] [CrossRef]

- Shakdwipee, Pushpkant, and Masuma Mehta. 2017. From basel i to basel ii to basel iii. International Journal of New Technology and Research (IJNTR) 3: 66–70. [Google Scholar]

- Shalini, H. S., K. Ravichandran, and P. V. Raveendra. 2023. P2p-the key behind regulatory framework of DeFi services. In Recent Advances in Blockchain Technology: Real-World Applications. Berlin and Heidelberg: Springer, pp. 267–79. [Google Scholar] [CrossRef]

- Sovryn. 2022. October 2022 Lending Pool Exploit Postmortem. Available online: https://www.sovryn.app/blog/october-2022-lending-pool-exploit-postmortem (accessed on 20 December 2022).

- Sun, Xiaotong. 2022. Liquidity risks in lending protocols (lps): Evidence from aave protocol. arXiv arXiv:2206.11973. [Google Scholar]

- Szalachowski, Pawel. 2019. Padva: A blockchain-based tls notary service. Paper presented at the 2019 IEEE 25th International Conference on Parallel and Distributed Systems (ICPADS), Tianjin, China, December 4–6; pp. 836–43. [Google Scholar] [CrossRef]

- Wang, Andre. 2022. Rethinking the rule and role of law in decentralized finance. Paper presented at the 2022 IEEE 24th Conference on Business Informatics (CBI), Amsterdam, The Netherlands, June 5–17; vol. 2, pp. 118–25. [Google Scholar]

- Wang, Bin, Han Liu, Chao Liu, Zhiqiang Yang, Qian Ren, Huixuan Zheng, and Hong Lei. 2021. Blockeye: Hunting for DeFi attacks on blockchain. Paper presented at the 2021 IEEE/ACM 43rd International Conference on Software Engineering: Companion Proceedings (ICSE-Companion), Madrid, Spain, May 25–28; pp. 17–20. [Google Scholar]

- Wang, Zhipeng, Kaihua Qin, Duc Vu Minh, and Arthur Gervais. 2022. Speculative multipliers on DeFi: Quantifying on-chain leverage risks. In Financial Cryptography and Data Security: 26th International Conference, FC 2022, Grenada, 2–6 May 2022, Revised Selected Papers. Berlin and Heidelberg: Springer, pp. 38–56. [Google Scholar]

- Werner, Sam M., Daniel Perez, Lewis Gudgeon, Ariah Klages-Mundt, Dominik Harz, and William J. Knottenbelt. 2021. Sok: Decentralized finance (DeFi). arXiv arXiv:2101.08778. [Google Scholar]

- Wieandt, Axel, and Laurenz Heppding. 2023. Centralized and decentralized finance: Coexistence or convergence? In The Fintech Disruption: How Financial Innovation Is Transforming the Banking Industry. Berlin and Heidelberg: Springer, pp. 11–51. [Google Scholar]

- Xu, Jiahua, Krzysztof Paruch, Simon Cousaert, and Yebo Feng. 2022. SoK: Decentralized exchanges (DEX) with automated market maker (AMM) protocols. ACM Computing Surveys 55: 1–50. [Google Scholar] [CrossRef]

- Zetzsche, Dirk A., Douglas W. Arner, and Ross P. Buckley. 2020. Decentralized finance (DeFi). Journal of Financial Regulation 6: 172–203. [Google Scholar] [CrossRef]

- Zhang, Fan, Ethan Cecchetti, Kyle Croman, Ari Juels, and Elaine Shi. 2016. Town crier: An authenticated data feed for smart contracts. In CCS ’16: Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security. New York: Association for Computing Machinery, pp. 270–82. [Google Scholar] [CrossRef]

- Zhao, Xiangfu, Zhongyu Chen, Xin Chen, Yanxia Wang, and Changbing Tang. 2017. The DAO attack paradoxes in propositional logic. Paper presented at the 2017 4th International Conference on Systems and Informatics (ICSAI), Hangzhou, China, November 11–13; pp. 1743–746. [Google Scholar] [CrossRef]

- Zhou, Liyi, Xihan Xiong, Jens Ernstberger, Stefanos Chaliasos, Zhipeng Wang, Ye Wang, Kaihua Qin, Roger Wattenhofer, Dawn Song, and Arthur Gervais. 2023. Sok: Decentralized finance (DeFi) attacks. Paper presented at the 2023 IEEE Symposium on Security and Privacy (SP), San Francisco, CA, USA, May 22–24; pp. 2444–61. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Weingärtner, T.; Fasser, F.; Reis Sá da Costa, P.; Farkas, W. Deciphering DeFi: A Comprehensive Analysis and Visualization of Risks in Decentralized Finance. J. Risk Financial Manag. 2023, 16, 454. https://doi.org/10.3390/jrfm16100454

Weingärtner T, Fasser F, Reis Sá da Costa P, Farkas W. Deciphering DeFi: A Comprehensive Analysis and Visualization of Risks in Decentralized Finance. Journal of Risk and Financial Management. 2023; 16(10):454. https://doi.org/10.3390/jrfm16100454

Chicago/Turabian StyleWeingärtner, Tim, Fabian Fasser, Pedro Reis Sá da Costa, and Walter Farkas. 2023. "Deciphering DeFi: A Comprehensive Analysis and Visualization of Risks in Decentralized Finance" Journal of Risk and Financial Management 16, no. 10: 454. https://doi.org/10.3390/jrfm16100454

APA StyleWeingärtner, T., Fasser, F., Reis Sá da Costa, P., & Farkas, W. (2023). Deciphering DeFi: A Comprehensive Analysis and Visualization of Risks in Decentralized Finance. Journal of Risk and Financial Management, 16(10), 454. https://doi.org/10.3390/jrfm16100454