Are GARCH and DCC Values of 10 Cryptocurrencies Affected by COVID-19?

Abstract

:1. Introduction

2. Literature Review

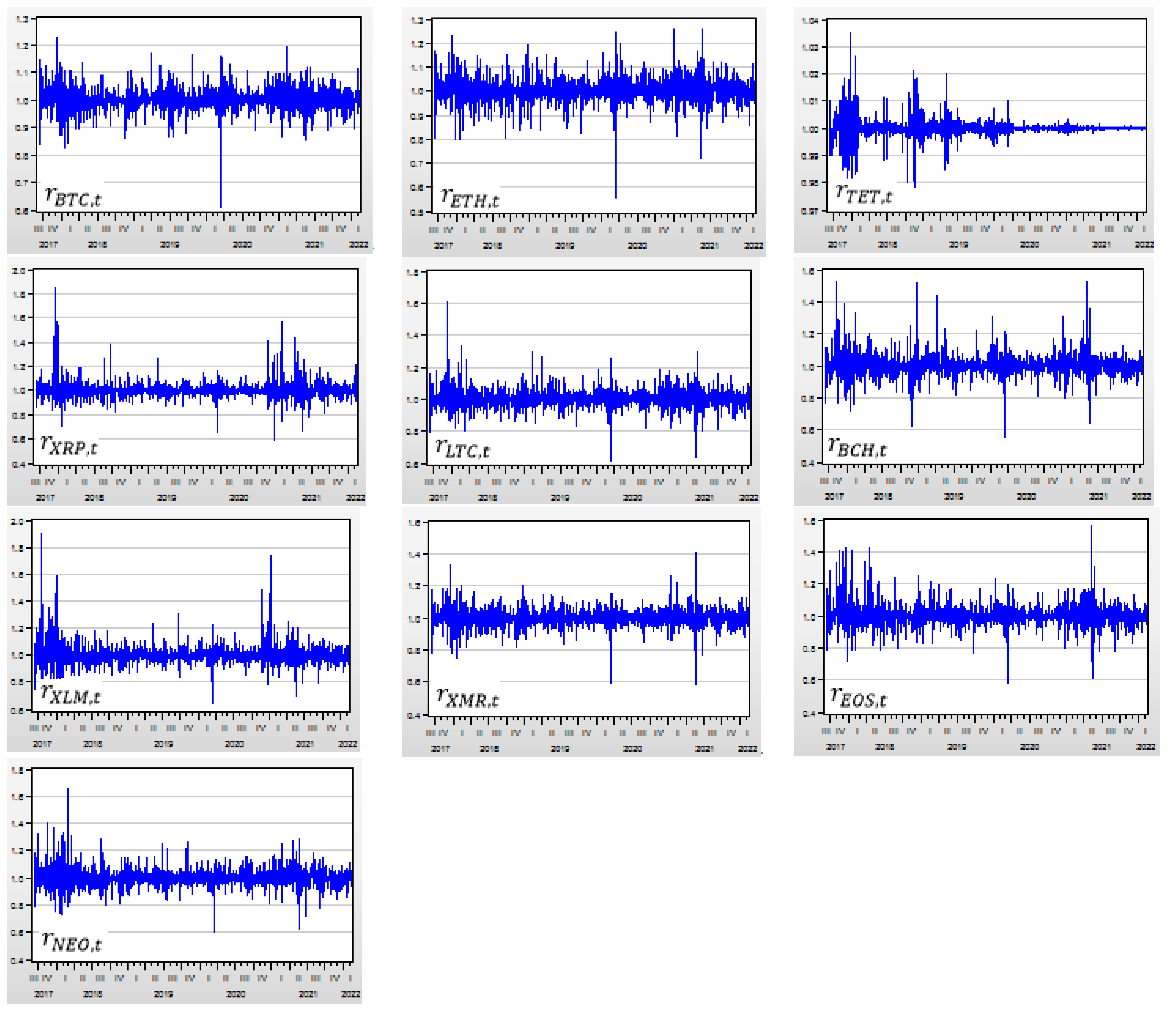

3. Data

4. Methodology

4.1. Ljung–Box Autocorrelation Test

4.2. ADF Unit Root Test

4.3. AR(1)-GARCH(1,1) Model

4.4. DCC(1,1) Model

4.5. Maximum Likelihood Estimation of Parameters

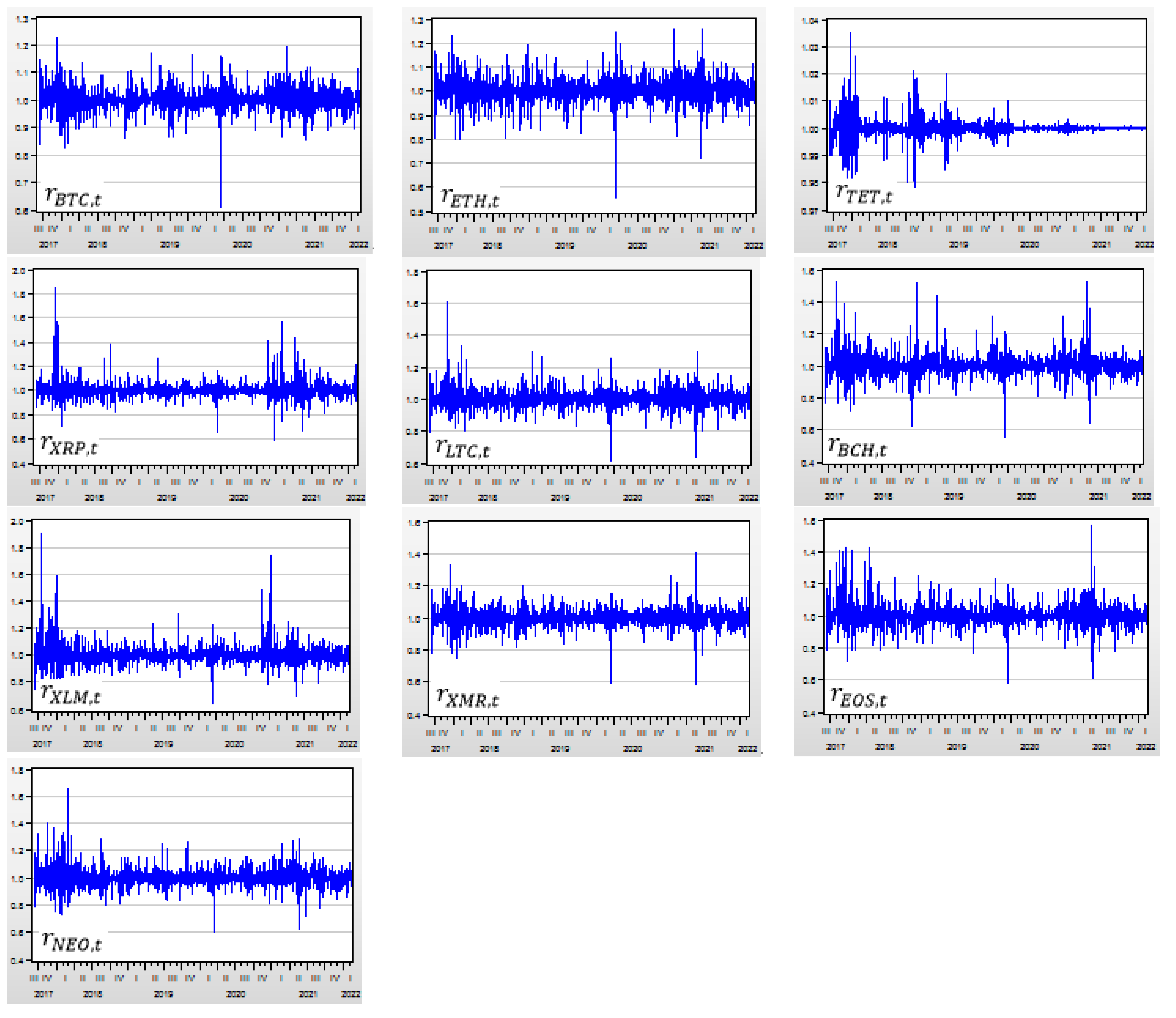

5. Descriptive Statistics and Tests

5.1. Average Growth Rates of the 10 Cryptocurrencies for the Three Periods

5.2. Ljung and Box Test for Autocorrelation

5.3. ADF Unit Root Tests

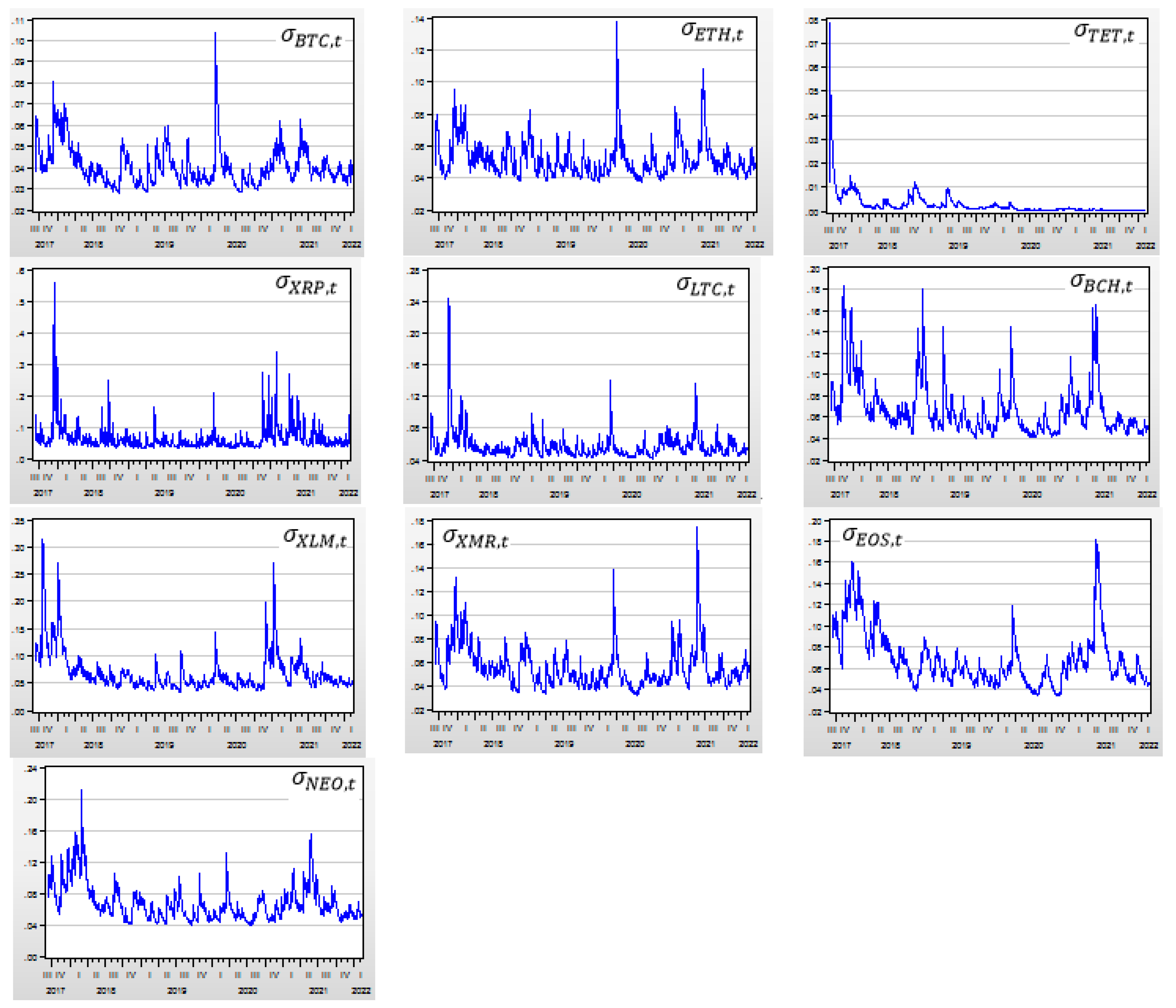

6. Empirical Analysis

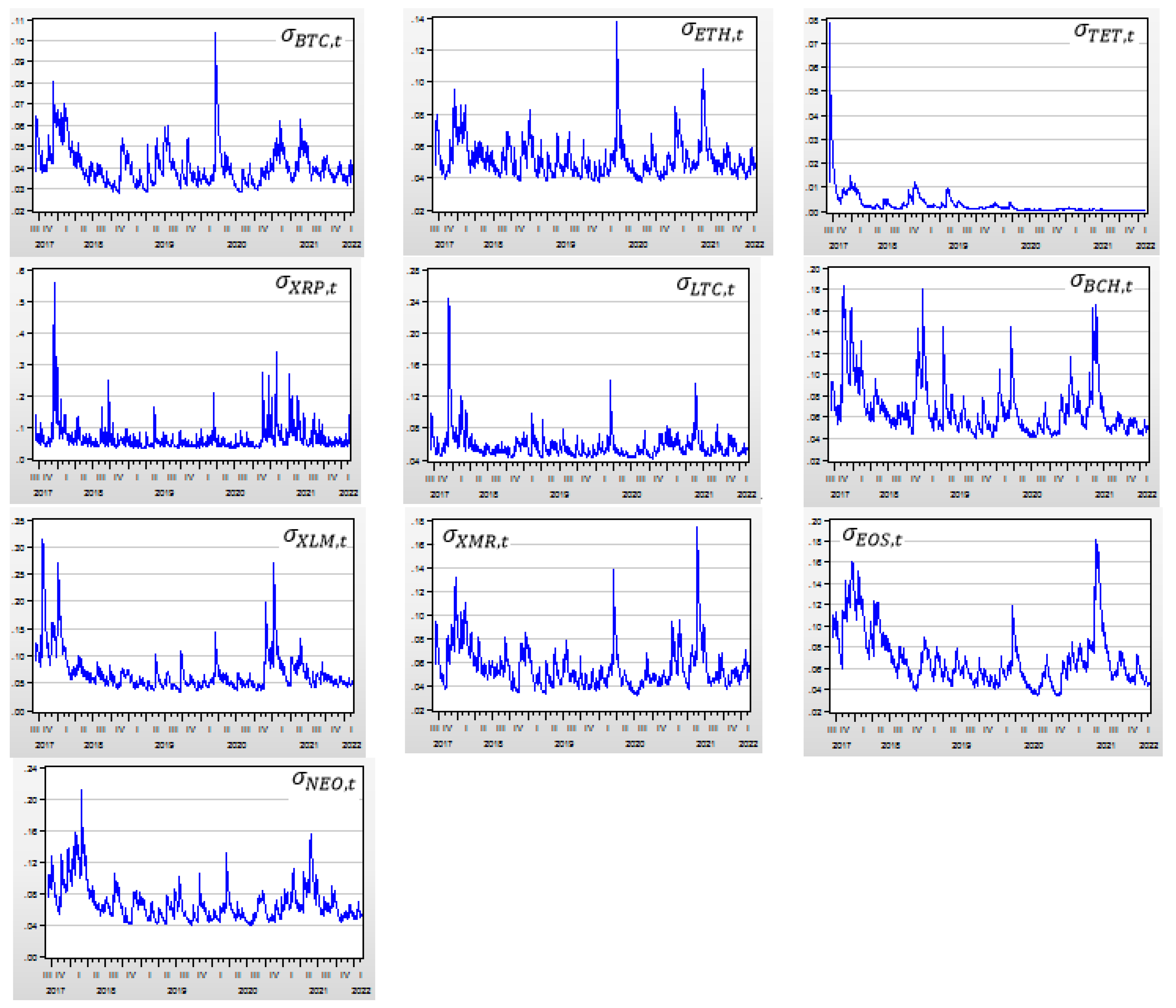

6.1. AR(1) and GARCH(1,1) Models

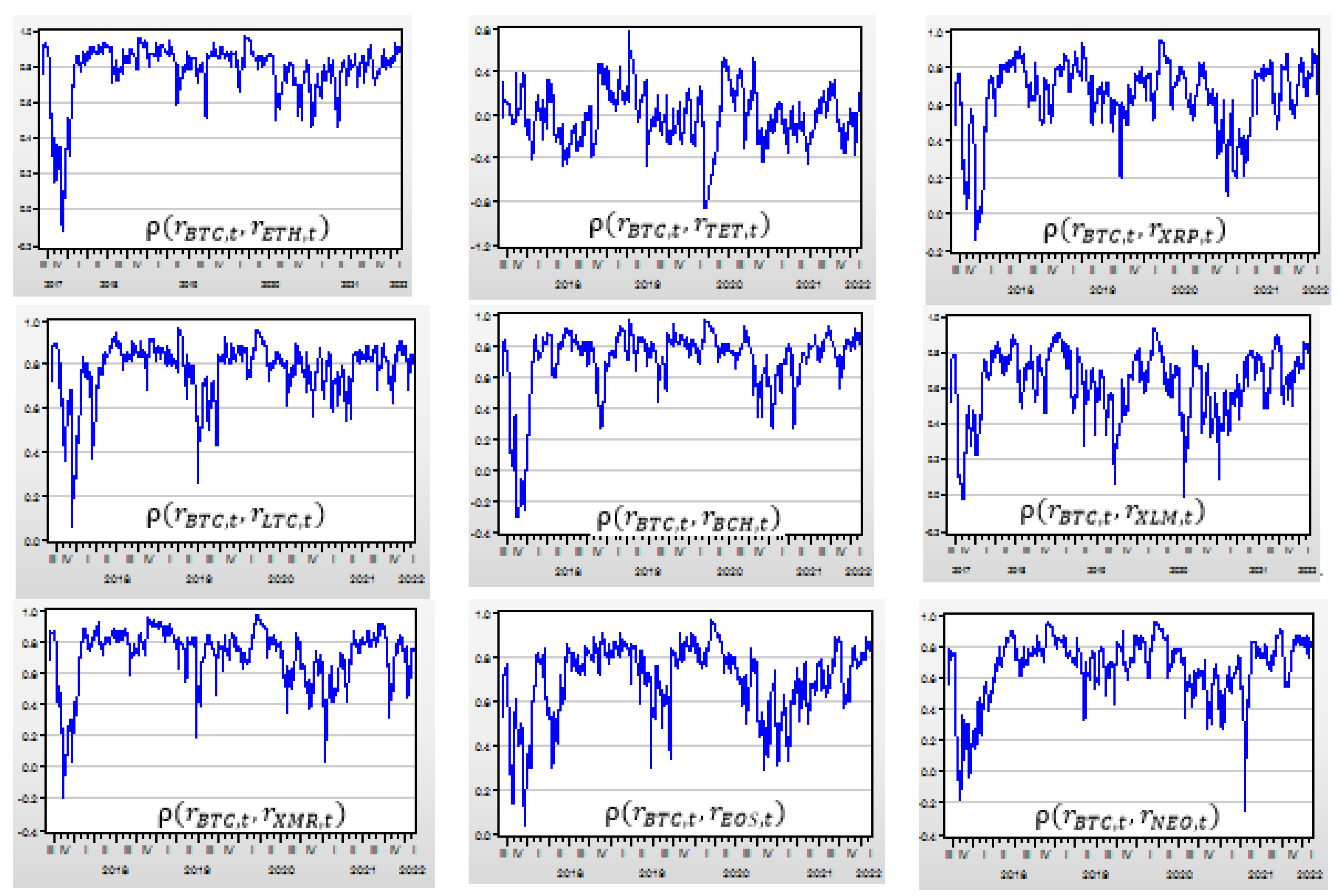

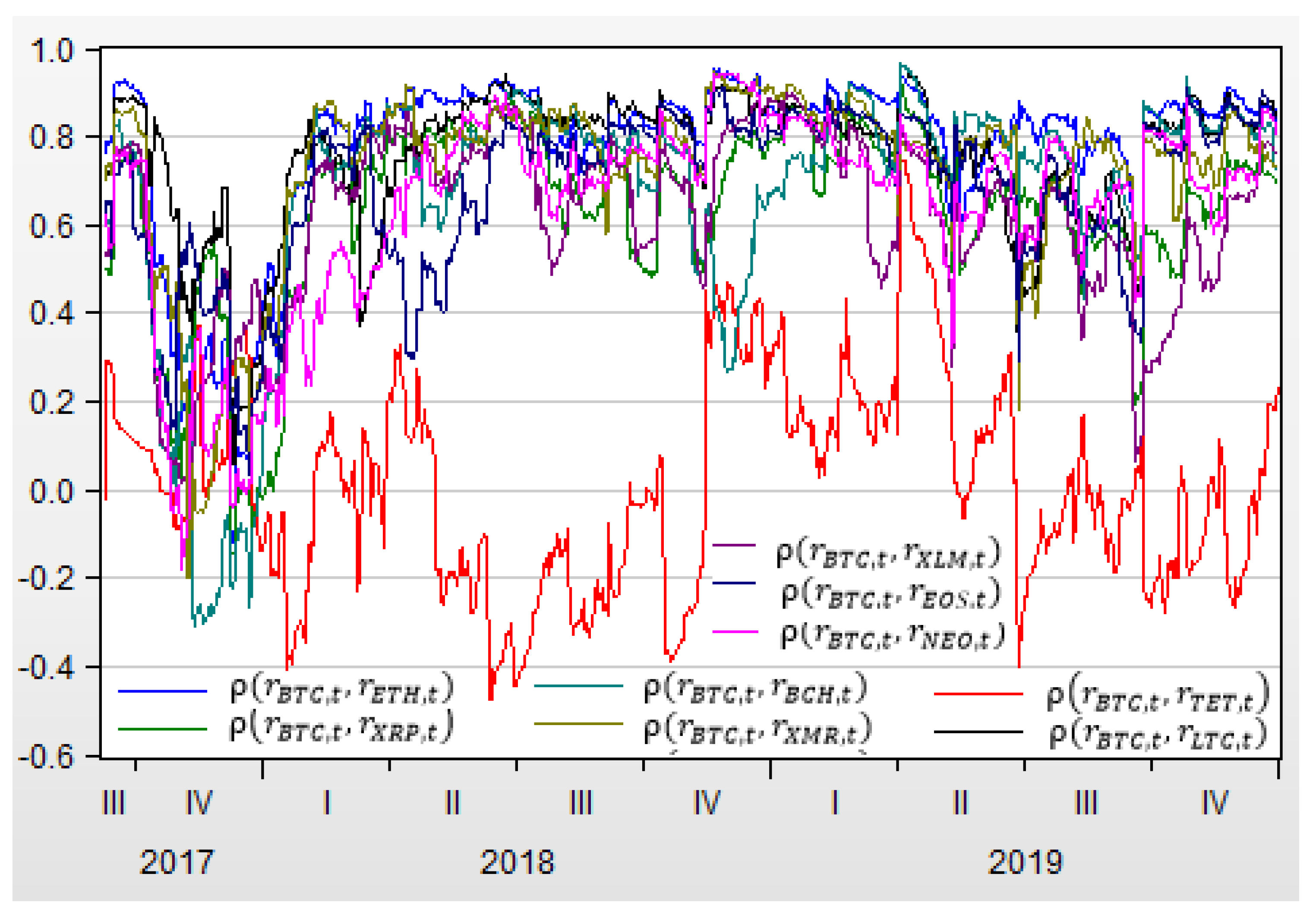

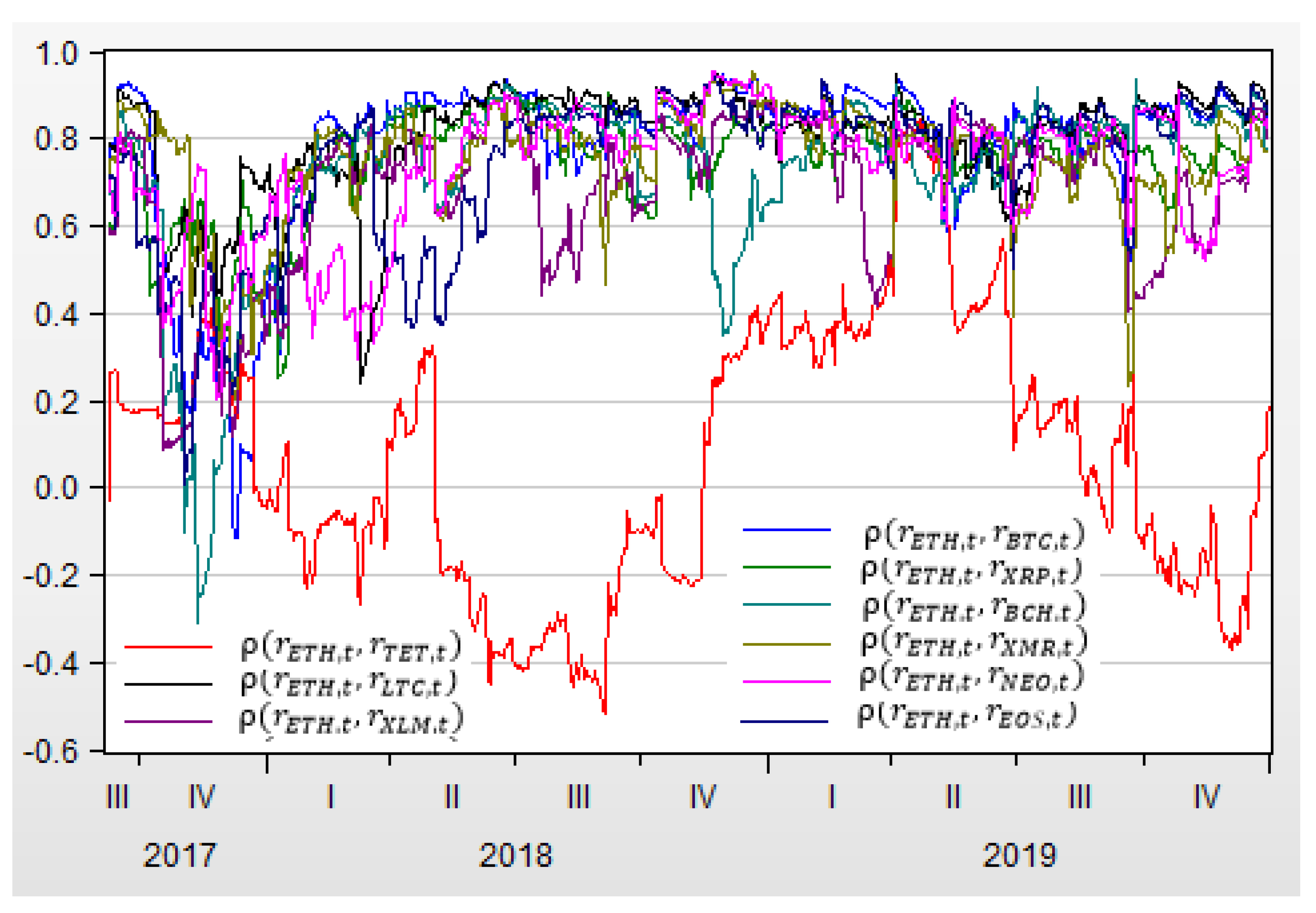

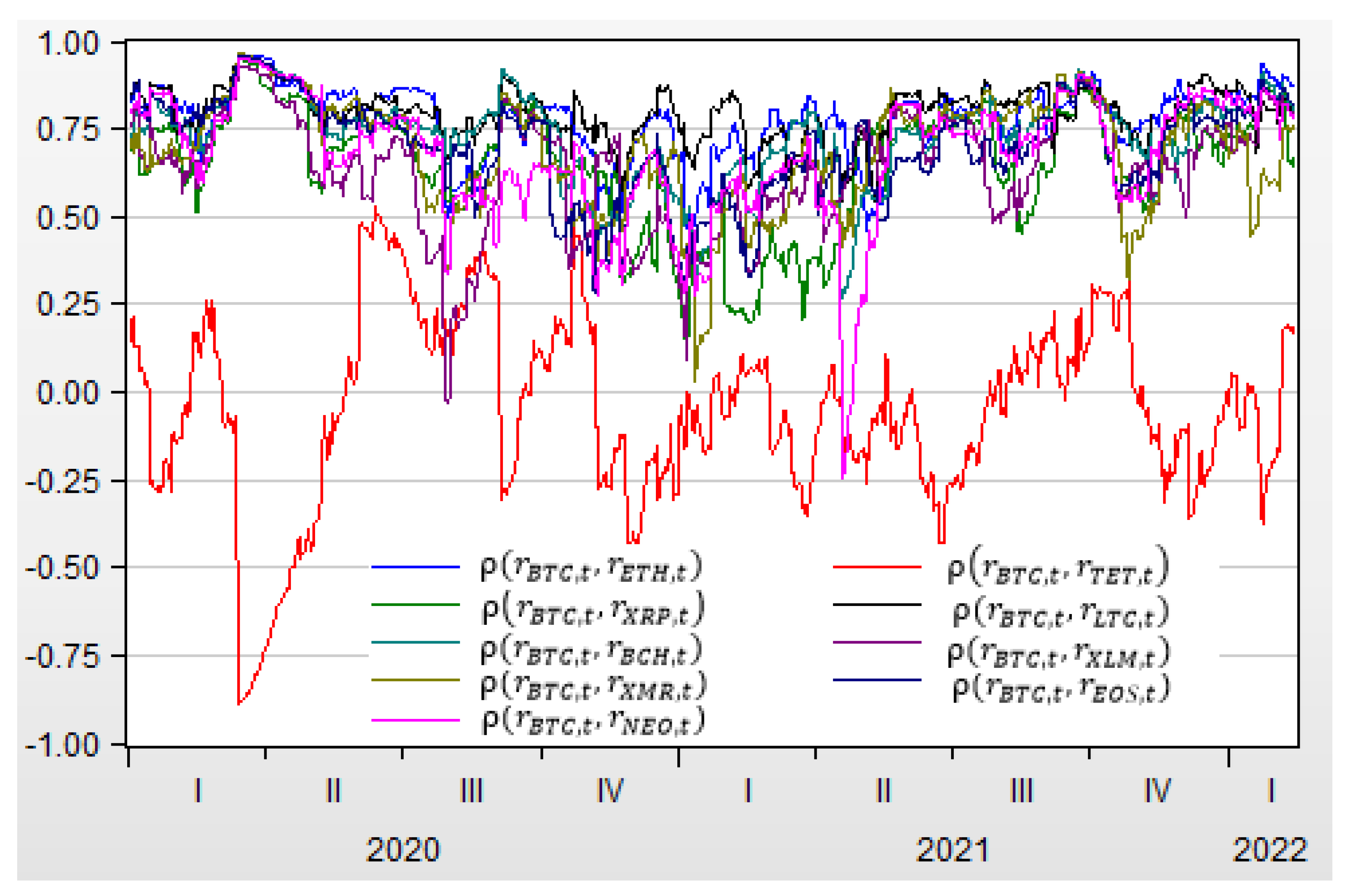

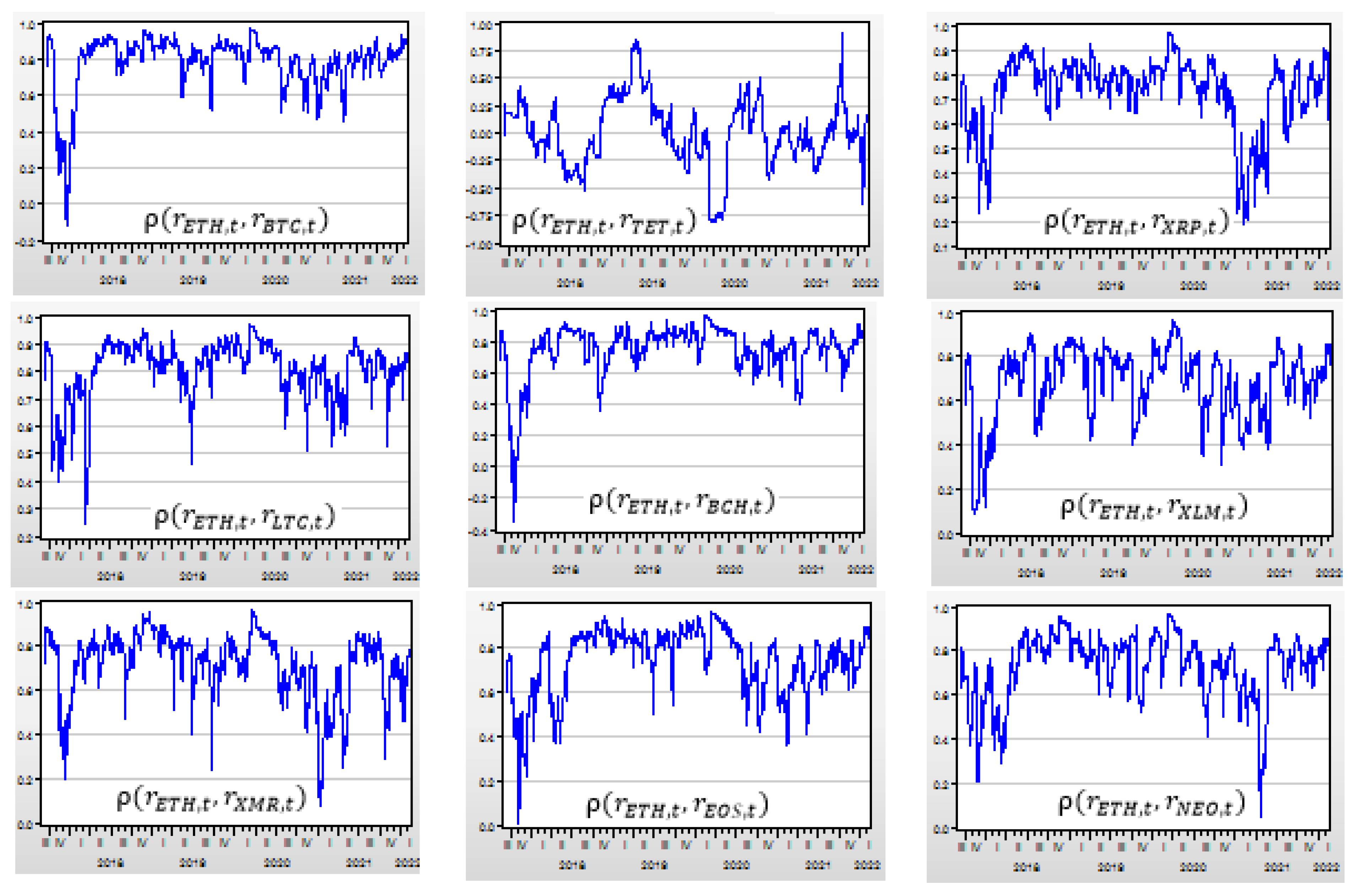

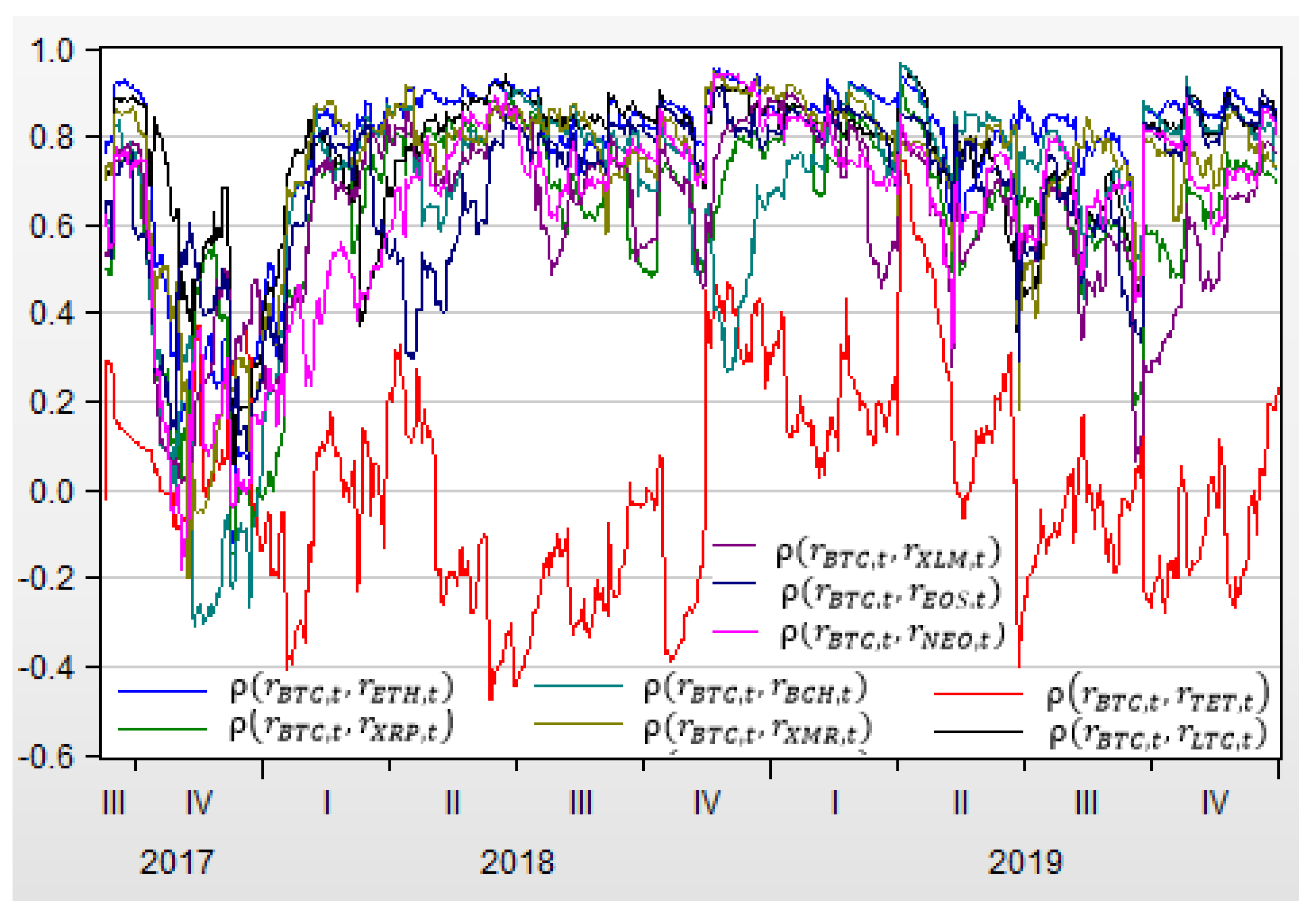

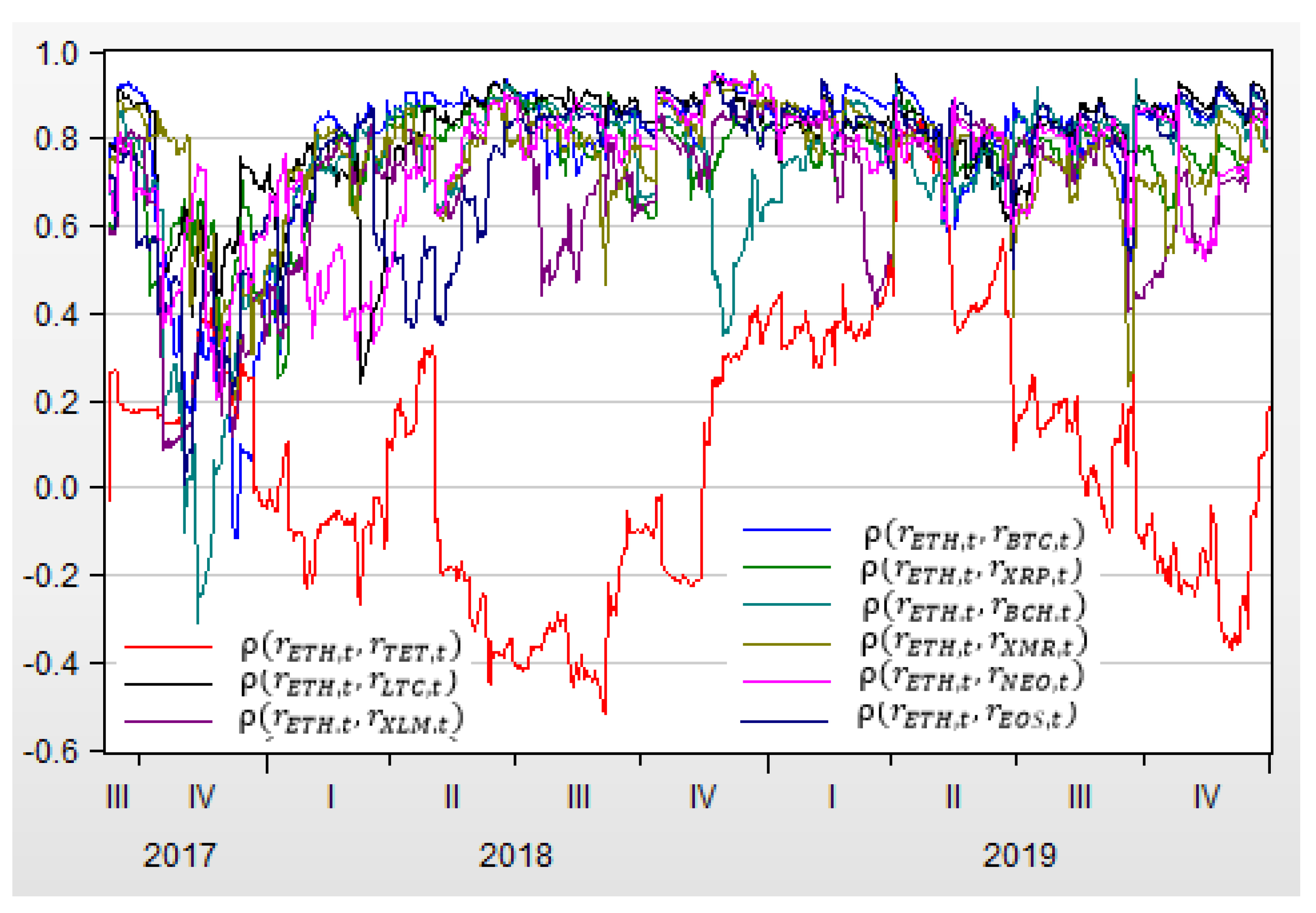

6.2. DCC(1,1) Models

7. Summary and Further Studies

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abakah, Emmanuel Joel Aikins, Luis Alberiko Gil-Alana, Godfrey Madigu, and Fatima Romero-Rojo. 2020. Volatility persistence in cryptocurrency markets under structural breaks. International Review of Economics and Finance 69: 680–91. [Google Scholar] [CrossRef]

- Ardia, David, Keven Bluteau, and Maxime Rüede. 2019. Regime changes in Bitcoin GARCH volatility dynamics. Finance Research Letters 29: 266–71. [Google Scholar]

- Będowska-Sójka, Barbara, Tomasz Hinc, and Agata Kliber. 2019. Causality between Volatility and Liquidity in Cryptocurrency Market. Working Paper. [Google Scholar] [CrossRef]

- Box, George E. P., and David A. Pierce. 1970. Distribution of residual correlations in autoregressive-integrated moving average time series models. Journal of the American Statistical Association 65: 1509–26. [Google Scholar] [CrossRef]

- Caporale, Guglielmo Maria, and Timur Zekokh. 2019. Modelling volatility of cryptocurrencies using Markov Switching GARCH models. Research in International Business and Finance 48: 143–55. [Google Scholar] [CrossRef]

- Ciaian, Pavel, Miroslava Rajcaniova, and Artis Kancs. 2018. Virtual relationships: Short- and long-run evidence from BitCoin and altcoin markets. Journal of International Financial Markets, Institutions & Money 52: 173–95. [Google Scholar]

- Corbet, Shaen, Yang Hou, Yang Hu, Charles Larkin, and Larkin Oxley. 2020. Any port in a storm: Cryptocurrency safe-havens during the COVID-19 pandemic. Economics Letters 194: 109377. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the estimators for time series with a unit root. Journal of the American Statistical Association 74: 427–31. [Google Scholar]

- Dickey, David A., and Wayne A. Fuller. 1981. Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 49: 1057–72. [Google Scholar] [CrossRef]

- Dilek, Teker, Teker Suat, and Ozyesil Mustafa. 2020. Macroeconomic determinants of cryptocurrency volatility: Time series analysis. Journal of Business & Economic Policy 7: 65–77. [Google Scholar] [CrossRef]

- Engle, Robert F. 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflations. Econometria 50: 987–1007. [Google Scholar] [CrossRef]

- Engle, Robert. 2002. Dynamic Conditional Correlation—A Simple Class of Multivariate GARCH models. Journal of Business and Economic Statistics 20: 339–50. [Google Scholar] [CrossRef]

- Enoksen, F. A., C. J. Landsnes, K. Lucivjanská, and P. Molnár. 2020. Understanding risk of bubbles in cryptocurrencies. Journal of Economic Behavior and Organization 176: 129–44. [Google Scholar] [CrossRef]

- García-Medina, Andrés, and José B. Hernández C. 2020. Network analysis of multivariate transfer entropy of cryptocurrencies in times of turbulence. Entropy 22: 760. [Google Scholar] [CrossRef] [PubMed]

- Huynh, Toan Luu Duc, Muhammad Ali Nasir, Xuan Vinh Vo, and Thong Trung Nguyen. 2020. Small things matter most: The spillover effects in the cryptocurrency market and gold as a silver bullet. North American Journal of Economics and Finance 54: 101277. [Google Scholar] [CrossRef]

- İçellioğlu, Cansu Şarkaya, and Selma Öner. 2019. An investigation on the volatility of cryptocurrencies by means of heterogeneous panel data Analysis. Procedia Computer Science 158: 913–20. [Google Scholar] [CrossRef]

- IFRSIC. 2019. Committee’s Tentative Agenda Decisions on Holdings of Cryptocurrencies. IFRS Interpretations Committee (IC), Update March 2019. Available online: https://www.ifrs.org/news-and-events/updates/IFRSIC-updates/march-2019/#1 (accessed on 9 September 2020).

- Investing. 2022. Today’s Cryptocurrency Prices. Available online: https://cn.investing.com/crypto/currencies (accessed on 18 February 2022).

- Iqbal, Najaf, Zeeshan Fareed, Guangcai Wan, and Farruskh Shahzad. 2021. Asymmetric nexus between COVID-19 outbreak in the world and cryptocurrency market. International Review of Financial Analysis 73: 101613. [Google Scholar] [CrossRef]

- James, Nick, Max Menzies, and Jennifer Chan. 2021. Changes to the extreme and erratic behaviour of cryptocurrencies during COVID-19. Physica A 565: 125581. [Google Scholar] [CrossRef]

- Kyriazis, Nikolaos A., Kalliopi Daskalou, Marios Arampatzis, Paraslevi Prassa, and Evangelia Papaioannou. 2019. Estimating the volatility of cryptocurrencies during bearish markets byemploying GARCH models. Heliyon 5: e02239. [Google Scholar] [CrossRef]

- Lahajnar, Sebastian, and Alenka Rozanec. 2020. The correlation strength of the most important cryptocurrencies in the bull and bear market. Investment Management and Financial Innovations 17: 67–81. [Google Scholar] [CrossRef]

- Le, TN-Lan, Emmanuel Joel Aikins Abakah, and Aviral Kumar Tiwari. 2021. Time and frequency domain connectedness and spill-over among fintech, green bonds and cryptocurrencies in the age of the fourth industrial revolution. Technological Forecasting & Social Change 162: 120382. [Google Scholar]

- Ljung, Greta Marianne, and George Edward Pelham Box. 1978. On a measure of lack of fit in time series models. Biometrika 66: 67–72. [Google Scholar] [CrossRef]

- Palamalai, Srinivasan, K. Krishna Kumar, and Bipasha Maity. 2020. Testing the random walk hypothesis for leading cryptocurrencies. Borsa Istanbul Review 21: 256–68. [Google Scholar] [CrossRef]

- Sensoy, Ahmet, Thiago Christiano Silva, Shaen Corbet, and Benjamin Miranda Tabak. 2020. High-Frequency Return and Volatility Spillovers among Cryptocurrencies. Researchgate, June. Available online: https://www.researchgate.net/publication/341820733 (accessed on 30 November 2020).

- Siswantoro, Dpdik, Rangga Handika, and Aria Farah Mita. 2020. The requirements of cryptocurrency for money, an Islamic view. Heliyon 6: e03235. [Google Scholar] [CrossRef] [Green Version]

- Soylu, Pinar Kaya, Mustafa Okur, Ozgur Çatıkkaş, and Ayca Altintig. 2020. Long memory in the volatility of selected cryptocurrencies: Bitcoin, Ethereum and Ripple. Journal of Risk and Financial Management 13: 107. [Google Scholar] [CrossRef]

- Wooldridge, Jeffrey M. 2000. Introductory Econometrics: A Modern Approach. Chula Vista: South Western College, ISBN 0-538-85013-2. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Ranking | Cryptocurrency | Abbreviation | Price (USD) | Market Capitalization | 24 h Trading Volume | ||

|---|---|---|---|---|---|---|---|

| Market Cap (USD) | Ratio (%) | 24 h Volume (USD) | Ratio (%) | ||||

| 1 | Bitcoin | 40782 | 771.32B | 41.69% | 17.460000B | 30.68% | |

| 2 | Ethereum | 2899.3 | 347.288B | 18.77% | 13.210000B | 23.21% | |

| 3 | Tether (USDT) | 1.009 | 78.73B | 4.26% | 2.616600B | 4.60% | |

| 6 | Ripple | 0.78793 | 37.74B | 2.04% | 0.139910B | 0.25% | |

| 20 | Litecoin | 117 | 8.15B | 0.44% | 0.115070B | 0.20% | |

| 28 | Bitcoin Cash | 313.8 | 5.96B | 0.32% | 0.077834B | 0.14% | |

| 31 | Stellar | 0.20498 | 5.11B | 0.28% | 0.034826B | 0.06% | |

| 45 | Monero | 164.38 | 2.98B | 0.16% | 0.028847B | 0.05% | |

| 48 | EOS | 2.3559 | 2.31B | 0.12% | 0.051469B | 0.09% | |

| 58 | NEO | 24.59 | 1.73B | 0.09% | 0.020801B | 0.04% | |

| Sum of the 10 cryptocurrencies | 1261.318B | 68.18% | 33.755357B | 59.32% | |||

| Total 10,707 cryptocurrencies | 1850B | 100.00% | 56.906B | 100.00% | |||

| Stats | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 1.0023 | 1.0028 | 1.0000 | 1.0031 | 1.0021 | 1.0020 | 1.0041 | 1.0018 | 1.0031 | 1.0023 |

| Growth | 0.2295% | 0.2813% | −0.0006% | 0.3111% | 0.2097% | 0.2007% | 0.4058% | 0.1835% | 0.3116% | 0.2299% |

| Median | 1.0015 | 1.0015 | 1.0000 | 1.0001 | 0.9995 | 0.9988 | 1.0000 | 1.0026 | 1.0000 | 1.0010 |

| Maximum | 1.2255 | 1.2596 | 1.0352 | 1.8558 | 1.6106 | 1.5291 | 1.8977 | 1.4080 | 1.5618 | 1.6605 |

| Minimum | 0.6082 | 0.5545 | 0.9787 | 0.5822 | 0.6146 | 0.5501 | 0.6438 | 0.5854 | 0.5801 | 0.5996 |

| Std. Dev. | 0.0418 | 0.0527 | 0.0034 | 0.0705 | 0.0601 | 0.0699 | 0.0745 | 0.0558 | 0.0713 | 0.0701 |

| Skewness | −0.2508 | −0.2809 | 0.7773 | 2.6610 | 1.0338 | 1.1259 | 2.6139 | −0.1714 | 1.0374 | 0.8436 |

| Kurtosis | 10.23 | 8.77 | 22.64 | 28.64 | 15.55 | 14.29 | 27.45 | 10.46 | 11.95 | 11.87 |

| Jarque–Bera | 3544 | 2268 | 26,225 | 46,333 | 10,935 | 8947 | 42,217 | 3767 | 5696 | 5501 |

| Probability | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Obs | 1621 | 1621 | 1621 | 1621 | 1621 | 1621 | 1621 | 1621 | 1621 | 1621 |

| Stats | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 1.0015 | 1.0003 | 1.0000 | 1.0021 | 1.0012 | 1.0015 | 1.0040 | 1.0005 | 1.0041 | 1.0015 |

| Growth | 0.1523% | 0.0338% | −0.0007% | 0.2064% | 0.1154% | 0.1482% | 0.3983% | 0.0465% | 0.4067% | 0.1468% |

| Median | 1.0007 | 0.9989 | 1.0000 | 0.9987 | 0.9964 | 0.9962 | 0.9972 | 0.9993 | 0.9985 | 0.9974 |

| Maximum | 1.2255 | 1.2322 | 1.0352 | 1.8558 | 1.6106 | 1.5291 | 1.8977 | 1.3268 | 1.4275 | 1.6605 |

| Minimum | 0.8295 | 0.7982 | 0.9787 | 0.7019 | 0.7350 | 0.6193 | 0.7226 | 0.7471 | 0.7202 | 0.7347 |

| Std. Dev. | 0.0430 | 0.0519 | 0.0046 | 0.0704 | 0.0626 | 0.0760 | 0.0805 | 0.0566 | 0.0759 | 0.0762 |

| Skewness | 0.2694 | 0.0319 | 0.5858 | 3.9068 | 2.1114 | 1.3783 | 2.8195 | 0.1439 | 1.3027 | 1.4692 |

| Kurtosis | 6.0744 | 5.5172 | 12.6270 | 40.0922 | 19.2643 | 12.3852 | 26.7278 | 6.1820 | 9.4422 | 12.7413 |

| Jarque–Bera | 343.01 | 223.23 | 3311.42 | 50,590.19 | 9941.45 | 3368.73 | 20,942.07 | 359.40 | 1700.21 | 3645.00 |

| Probability | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Observations | 845 | 845 | 845 | 845 | 845 | 845 | 845 | 845 | 845 | 845 |

| Stats | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 1.0031 | 1.0055 | 1.0000 | 1.0043 | 1.0031 | 1.0026 | 1.0041 | 1.0033 | 1.0021 | 1.0032 |

| Growth | 0.3134% | 0.5493% | −0.0015% | 0.4251% | 0.3114% | 0.2580% | 0.4130% | 0.3292% | 0.2071% | 0.3179% |

| Median | 1.0024 | 1.0043 | 1.0000 | 1.0020 | 1.0027 | 1.0021 | 1.0026 | 1.0054 | 1.0012 | 1.0034 |

| Maximum | 1.1941 | 1.2596 | 1.0102 | 1.5667 | 1.2923 | 1.5283 | 1.7395 | 1.4080 | 1.5618 | 1.2893 |

| Minimum | 0.6082 | 0.5545 | 0.9933 | 0.5822 | 0.6146 | 0.5501 | 0.6438 | 0.5854 | 0.5801 | 0.5996 |

| Std. Dev. | 0.0403 | 0.0534 | 0.0009 | 0.0707 | 0.0572 | 0.0627 | 0.0674 | 0.0549 | 0.0660 | 0.0629 |

| Skewness | −0.9294 | −0.6023 | 0.3948 | 1.3228 | −0.5074 | 0.6062 | 2.1484 | −0.5412 | 0.5645 | −0.3788 |

| Kurtosis | 16.0985 | 12.0773 | 37.5916 | 16.5720 | 9.6452 | 17.1891 | 26.4363 | 15.8050 | 15.9871 | 8.6374 |

| Jarque–Bera | 5659.13 | 2711.08 | 38,709.61 | 6182.08 | 1461.10 | 6557.19 | 18,356 | 5339.53 | 5494.72 | 1046.1 |

| Probability | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Observations | 776 | 776 | 776 | 776 | 776 | 776 | 776 | 776 | 776 | 776 |

| Return Index | Pre_COVID-19 (1) | COVID-19 (2) | Full Period (3) | (2)–(1) | (2)–(3) |

|---|---|---|---|---|---|

| 0.1523% | 0.3134% | 0.2295% | 0.1611% | 0.0839% | |

| 0.0338% | 0.5493% | 0.2813% | 0.5155% | 0.2680% | |

| −0.0007% | −0.0015% | −0.0006% | −0.0008% | −0.0009% | |

| 0.2064% | 0.4251% | 0.3111% | 0.2187% | 0.1140% | |

| 0.1154% | 0.3114% | 0.2097% | 0.1960% | 0.1017% | |

| 0.1482% | 0.2580% | 0.2007% | 0.1098% | 0.0573% | |

| 0.3983% | 0.4130% | 0.4058% | 0.0147% | 0.0072% | |

| 0.0465% | 0.3292% | 0.1835% | 0.2827% | 0.1457% | |

| 0.4067% | 0.2071% | 0.3116% | −0.1996% | −0.1045% | |

| 0.1468% | 0.3179% | 0.2299% | 0.1711% | 0.0880% |

| Stats | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 4.7359 ** (p = 0.030) | 8.3473 *** (p = 0.004) | 0.0433 (p = 0.835) | 63.684 *** (p = 0.000) | 3.7614 ** (p = 0.052) | 0.3933 (p = 0.531) | 3.9499 ** (p = 0.047) | 0.0831 (p = 0.773) | 23.998 *** (p = 0.000) | 5.2118 ** (p = 0.022) | |

| 18.859 ** (p = 0.042) | 23.930 *** (p = 0.008) | 22.130 ** (p = 0.014) | 134.12 *** (p = 0.000) | 11.800 (p = 0.299) | 15.459 (p = 0.116) | 19.479 ** (p = 0.035) | 10.483 (p = 0.399) | 35.206 *** (p = 0.000) | 17.362 * (p = 0.067) | |

| 28.199 (p = 0.105) | 32.332 ** (p = 0.040) | 49.436 *** (p = 0.000) | 248.79 *** (p = 0.000) | 21.156 (p = 0.378) | 22.316 (p = 0.324) | 33.926 ** (p = 0.027) | 33.627 ** (p = 0.029) | 44.897 *** (p = 0.001) | 43.686 *** (p = 0.002) | |

| 32.880 (p = 0.328) | 43.626 ** (p = 0.052) | 57.666 *** (p = 0.002) | 329.07 *** (p = 0.000) | 29.663 (p = 0.483) | 38.154 (p = 0.146) | 41.192 * (p = 0.084) | 48.984 ** (p = 0.016) | 55.703 *** (p = 0.003) | 52.581 *** (p = 0.007) |

| Variables | Level Variable | 1st Difference Variable | 2nd Difference Variable | ||||||

|---|---|---|---|---|---|---|---|---|---|

| t-Statistics | |||||||||

| −36.329 *** (p = 0.000) | −36.343 *** (p = 0.000) | −0.1193 (p = 0.6424) | −18.606 *** (p = 0.000) | −18.615 *** (p = 0.000) | −18.624 *** (p = 0.000) | −17.139 *** (p = 0.000) | −17.146 *** (p = 0.000) | −17.153 *** (p = 0.000) | |

| −23.199 *** (p = 0.000) | −23.197 *** (p = 0.000) | −0.0611 (p = 0.6622) | −15.692 *** (p = 0.000) | −15.699 *** (p = 0.000) | −15.706 *** (p = 0.000) | −17.146 *** (p = 0.000) | −17.154 *** (p = 0.000) | −17.162 *** (p = 0.000) | |

| −22.005 *** (p = 0.000) | −22.006 *** (p = 0.000) | −0.0189 (p = 0.6763) | −15.911 *** (p = 0.000) | −15.918 *** (p = 0.000) | −15.925 *** (p = 0.000) | −16.347 *** (p = 0.000) | −16.354 *** (p = 0.000) | −16.361 *** (p = 0.000) | |

| −12.528 *** (p = 0.000) | −12.534 *** (p = 0.000) | −0.0823 (p = 0.7087) | −14.809 *** (p = 0.000) | −14.815 *** (p = 0.000) | −14.821 *** (p = 0.000) | −15.445 *** (p = 0.000) | −15.452 *** (p = 0.000) | −15.459 *** (p = 0.000) | |

| −36.055 *** (p = 0.000) | −36.070 *** (p = 0.000) | −0.0532 (p = 0.6996) | −16.328 *** (p = 0.000) | −16.335 *** (p = 0.000) | −16.341 *** (p = 0.000) | −16.740 *** (p = 0.000) | −16.745 *** (p = 0.000) | −16.753 *** (p = 0.000) | |

| −33.465 *** (p = 0.000) | −33.480 *** (p = 0.000) | −0.2165 (p = 0.6996) | −18.101 *** (p = 0.000) | −18.109 *** (p = 0.000) | −18.118 *** (p = 0.000) | −17.499 *** (p = 0.000) | −17.507 *** (p = 0.000) | −17.515 *** (p = 0.000) | |

| −22.922 *** (p = 0.000) | −22.866 *** (p = 0.000) | −0.0022 (p = 0.6825) | −16.153 *** (p = 0.000) | −16.159 *** (p = 0.000) | −16.166 *** (p = 0.000) | −16.893 *** (p = 0.000) | −16.901 *** (p = 0.000) | −16.907 *** (p = 0.000) | |

| −34.442 *** (p = 0.000) | −34.391 *** (p = 0.000) | −0.0319 (p = 0.6720) | −15.726 *** (p = 0.000) | −15.732 *** (p = 0.000) | −15.739 *** (p = 0.000) | −16.948 *** (p = 0.000) | −16.956 *** (p = 0.000) | −16.964 *** (p = 0.000) | |

| −39.382 *** (p = 0.000) | −39.393 *** (p = 0.000) | −0.0077 (p = 0.6850) | −17.256 *** (p = 0.000) | −17.263 *** (p = 0.000) | −17.270 *** (p = 0.000) | −17.041 *** (p = 0.000) | −17.049 *** (p = 0.000) | −17.056 *** (p = 0.000) | |

| −36.447 *** (p = 0.000) | −36.461 *** (p = 0.000) | −0.0675 (p = 0.6850) | −16.137 *** (p = 0.000) | −16.145 *** (p = 0.000) | −16.152 *** (p = 0.000) | −17.097 *** (p = 0.000) | −17.102 *** (p = 0.000) | −17.109 *** (p = 0.000) | |

| AR(1) | GARCH | LLH | AIC | SIC | HIC | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1.054122 *** (p = 0.0000) | −0.051714 *** (p = 0.0080) | 0.0000775 *** (p = 0.0000) | 0.060582 *** (p = 0.0000) | 0.895008 *** (p = 0.0000) | 2925 | −3.60 | −3.58 | −3.59 | ||

| 1.075821 *** (p = 0.0000) | −0.072808 *** (p = 0.0006) | 0.000160 *** (p = 0.0000) | 0.073061 *** (p = 0.0000) | 0.869725 *** (p = 0.0000) | 2538 | −3.12 | −3.10 | −3.11 | ||

| 1.224324 *** (p = 0.0000) | −0.224454 *** (p = 0.0116) | 6.82E−09 *** (p = 0.0004) | 0.118990 *** (p = 0.0000) | 0.880962 *** (p = 0.0000) | 8066 | −9.94 | −9.92 | −9.94 | ||

| 1.050704 *** (p = 0.0000) | −0.051973 ** (p = 0.0454) | 0.000392 *** (p = 0.0000) | 0.337334 *** (p = 0.0000) | 0.641374 *** (p = 0.0000) | 2322 | −2.85 | −2.84 | −2.85 | ||

| 1.039144 *** (p = 0.0000) | −0.037239 (p = 0.1543) | 0.000271 *** (p = 0.0000) | 0.089293 *** (p = 0.0000) | 0.833616 *** (p = 0.0000) | 2380 | −2.93 | −2.91 | −2.92 | ||

| 1.031207 *** (p = 0.0000) | −0.030796 (p = 0.3473) | 0.000129 *** (p = 0.0000) | 0.077802 *** (p = 0.0000) | 0.901260 *** (p = 0.0000) | 2161 | −2.66 | −2.64 | −2.65 | ||

| 1.029506 *** (p = 0.0000) | −0.029788 (p = 0.2788) | 9.69E−05 *** (p = 0.0000) | 0.110921 *** (p = 0.0000) | 0.882065 *** (p = 0.0000) | 2175 | −2.67 | −2.66 | −2.67 | ||

| 1.113165 *** (p = 0.0000) | −0.110605 *** (p = 0.0000) | 9.07E−05 *** (p = 0.0000) | 0.092967 *** (p = 0.0000) | 0.887105 *** (p = 0.0000) | 2498 | −3.07 | −3.05 | −3.07 | ||

| 1.084713 *** (p = 0.0000) | −0.083321 *** (p = 0.0000) | 4.36E−05 *** (p = 0.0000) | 0.056496 *** (p = 0.0000) | 0.938592 *** (p = 0.0000) | 2161 | −2.66 | −2.64 | −2.65 | ||

| 1.059275 *** (p = 0.0000) | −0.057302 ** (p = 0.0375) | 0.000113 *** (p = 0.0000) | 0.081906 *** (p = 0.0000) | 0.899729 *** (p = 0.0000) | 2153 | −2.65 | −2.63 | −2.64 |

| Return Index | Pre_COVID-19 (1) | COVID-19 (2) | Full Period (3) | (2)–(1) | (2)–(3) |

|---|---|---|---|---|---|

| 0.041508 | 0.039749 | 0.040666 | −0.001759 | −0.000917 | |

| 0.051479 | 0.051481 | 0.051480 | 0.000002 | 0.000001 | |

| 0.004809 | 0.000730 | 0.002857 | −0.004079 | −0.002127 | |

| 0.062983 | 0.064909 | 0.063905 | 0.001926 | 0.001004 | |

| 0.058295 | 0.056452 | 0.057413 | −0.001843 | −0.000961 | |

| 0.072249 | 0.062369 | 0.067519 | −0.009880 | −0.005150 | |

| 0.073247 | 0.064930 | 0.069265 | −0.008317 | −0.004335 | |

| 0.056321 | 0.053340 | 0.054894 | −0.002981 | −0.001554 | |

| 0.073962 | 0.063003 | 0.068715 | −0.010959 | −0.005712 | |

| 0.071897 | 0.063170 | 0.067719 | −0.008727 | −0.004549 |

| Correlation | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1.000000 | 0.776808 | 0.281069 | 0.424849 | 0.689947 | 0.634587 | 0.523330 | 0.792656 | 0.653542 | 0.693236 | |

| 0.776808 | 1.000000 | 0.215460 | 0.502605 | 0.716635 | 0.659216 | 0.467497 | 0.814021 | 0.656849 | 0.616062 | |

| 0.281069 | 0.215460 | 1.000000 | 0.134521 | 0.208981 | 0.282569 | 0.292132 | 0.260092 | 0.292969 | 0.265776 | |

| 0.424849 | 0.502605 | 0.134521 | 1.000000 | 0.630485 | 0.394366 | 0.490050 | 0.439728 | 0.466209 | 0.382584 | |

| 0.689947 | 0.716635 | 0.208981 | 0.630485 | 1.000000 | 0.578735 | 0.438103 | 0.676326 | 0.615683 | 0.549046 | |

| 0.634587 | 0.659216 | 0.282569 | 0.394366 | 0.578735 | 1.000000 | 0.493803 | 0.739067 | 0.746646 | 0.586670 | |

| 0.523330 | 0.467497 | 0.292132 | 0.490050 | 0.438103 | 0.493803 | 1.000000 | 0.466423 | 0.564658 | 0.460194 | |

| 0.792656 | 0.814021 | 0.260092 | 0.439728 | 0.676326 | 0.739067 | 0.466423 | 1.000000 | 0.764007 | 0.768529 | |

| 0.653542 | 0.656849 | 0.292969 | 0.466209 | 0.615683 | 0.746646 | 0.564658 | 0.764007 | 1.000000 | 0.736894 | |

| 0.693236 | 0.616062 | 0.265776 | 0.382584 | 0.549046 | 0.586670 | 0.460194 | 0.768529 | 0.736894 | 1.000000 | |

| Minimum | 0.281069 | 0.215460 | 0.134521 | 0.134521 | 0.208981 | 0.282569 | 0.292132 | 0.260092 | 0.292969 | 0.265776 |

| Maximum | 0.792656 | 0.814021 | 0.292969 | 0.630485 | 0.716635 | 0.746646 | 0.564658 | 0.814021 | 0.764007 | 0.768529 |

| Average | 0.6470024 | 0.6425153 | 0.3233569 | 0.4865397 | 0.6103941 | 0.6115659 | 0.519619 | 0.6720849 | 0.6497457 | 0.6058991 |

| Correlation | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1.000000 | 0.707955 | 0.330240 | 0.509360 | 0.675031 | 0.603496 | 0.533173 | 0.819559 | 0.686039 | 0.708381 | |

| 0.707955 | 1.000000 | 0.318743 | 0.630937 | 0.677730 | 0.591474 | 0.402037 | 0.805435 | 0.651593 | 0.565191 | |

| 0.330240 | 0.318743 | 1.000000 | 0.196235 | 0.228384 | 0.274286 | 0.317141 | 0.339486 | 0.320246 | 0.253864 | |

| 0.509360 | 0.630937 | 0.196235 | 1.000000 | 0.701694 | 0.387791 | 0.437912 | 0.536644 | 0.554319 | 0.388788 | |

| 0.675031 | 0.677730 | 0.228384 | 0.701694 | 1.000000 | 0.454941 | 0.357114 | 0.597625 | 0.561834 | 0.455023 | |

| 0.603496 | 0.591474 | 0.274286 | 0.387791 | 0.454941 | 1.000000 | 0.409046 | 0.711409 | 0.644365 | 0.463473 | |

| 0.533173 | 0.402037 | 0.317141 | 0.437912 | 0.357114 | 0.409046 | 1.000000 | 0.462733 | 0.614799 | 0.428417 | |

| 0.819559 | 0.805435 | 0.339486 | 0.536644 | 0.597625 | 0.711409 | 0.462733 | 1.000000 | 0.750222 | 0.739181 | |

| 0.686039 | 0.651593 | 0.320246 | 0.554319 | 0.561834 | 0.644365 | 0.614799 | 0.750222 | 1.000000 | 0.674533 | |

| 0.708381 | 0.565191 | 0.253864 | 0.388788 | 0.455023 | 0.463473 | 0.428417 | 0.739181 | 0.674533 | 1.000000 | |

| Minimum | 0.330240 | 0.318743 | 0.196235 | 0.196235 | 0.228384 | 0.274286 | 0.317141 | 0.339486 | 0.320246 | 0.253864 |

| Maximum | 0.819559 | 0.805435 | 0.339486 | 0.701694 | 0.701694 | 0.711409 | 0.614799 | 0.819559 | 0.750222 | 0.739181 |

| Average | 0.6573234 | 0.6351095 | 0.3578625 | 0.534368 | 0.5709376 | 0.5540281 | 0.4962372 | 0.6762294 | 0.645795 | 0.5676851 |

| Correlation | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1.000000 | 0.858839 | 0.477586 | 0.329774 | 0.728852 | 0.673157 | 0.508551 | 0.767655 | 0.610086 | 0.688878 | |

| 0.858839 | 1.000000 | 0.449101 | 0.392509 | 0.828315 | 0.785365 | 0.594386 | 0.827712 | 0.699520 | 0.774880 | |

| 0.477586 | 0.449101 | 1.000000 | 0.105073 | 0.341076 | 0.409906 | 0.243316 | 0.307797 | 0.138836 | 0.156834 | |

| 0.329774 | 0.392509 | 0.105073 | 1.000000 | 0.531854 | 0.435479 | 0.601903 | 0.350426 | 0.391736 | 0.414526 | |

| 0.728852 | 0.828315 | 0.341076 | 0.531854 | 1.000000 | 0.812879 | 0.601509 | 0.820240 | 0.724326 | 0.762379 | |

| 0.673157 | 0.785365 | 0.409906 | 0.435479 | 0.812879 | 1.000000 | 0.624312 | 0.790189 | 0.864738 | 0.789139 | |

| 0.508551 | 0.594386 | 0.243316 | 0.601903 | 0.601509 | 0.624312 | 1.000000 | 0.487252 | 0.479866 | 0.498825 | |

| 0.767655 | 0.827712 | 0.307797 | 0.350426 | 0.820240 | 0.790189 | 0.487252 | 1.000000 | 0.785721 | 0.872285 | |

| 0.610086 | 0.699520 | 0.138836 | 0.391736 | 0.724326 | 0.864738 | 0.479866 | 0.785721 | 1.000000 | 0.844125 | |

| 0.688878 | 0.774880 | 0.156834 | 0.414526 | 0.762379 | 0.789139 | 0.498825 | 0.872285 | 0.844125 | 1.000000 | |

| Minimum | 0.329774 | 0.392509 | 0.105073 | 0.105073 | 0.341076 | 0.409906 | 0.243316 | 0.307797 | 0.138836 | 0.156834 |

| Maximum | 0.858839 | 0.858839 | 0.477586 | 0.601903 | 0.828315 | 0.864738 | 0.624312 | 0.872285 | 0.864738 | 0.872285 |

| Average | 0.6643378 | 0.7210627 | 0.3629525 | 0.455328 | 0.715143 | 0.7185164 | 0.563992 | 0.7009277 | 0.6538954 | 0.6801871 |

| DCC(1,1) | LLH | SIC | DCC(1,1) | LLH | SIC | ||||

|---|---|---|---|---|---|---|---|---|---|

| 0.059207 *** (0.0000) | 0.931559 *** (0.0000) | −2771815 | 3419 | 0.059192 *** (0.0000) | 0.931558 *** (0.0000) | −2770250 | 17 | ||

| 0.058019 *** (0.0000) | 0.927671 *** (0.0000) | −752884 | 928 | 0.039144 *** (0.0000) | 0.975561 *** (0.0000) | −5206703 | 6424 | ||

| 0.059859 *** (0.0000) | 0.932308 *** (0.0000) | −22687280 | 27991 | 0.059832 *** (0.0000) | 0.932277 *** (0.0000) | −19675829 | 24276 | ||

| 0.059641 *** (0.0000) | 0.932072 *** (0.0000) | −8820785 | 10883 | 0.058988 *** (0.0000) | 0.931386 *** (0.0000) | −2816160 | 3474 | ||

| 0.059800 *** (0.0000) | 0.932236 *** (0.0000) | −14754445 | 18204 | 0.059671 *** (0.0000) | 0.932067 *** (0.0000) | −8867302 | 10940 | ||

| 0.059763 *** (0.0000) | 0.932193 *** (0.0000) | −14013995 | 17290 | 0.059753 *** (0.0000) | 0.932179 *** (0.0000) | −4032724 | 17313 | ||

| 0.058533 *** (0.0000) | 0.930968 *** (0.0000) | −1154885 | 1424 | 0.060000 *** (0.0000) | 0.932472 *** (0.0000) | −765969 | 945 | ||

| 0.59694 *** (0.0000) | 0.932117 *** (0.0000) | −10202643 | 12588 | 0.059535 *** (0.0000) | 0.931893 *** (0.0000) | −6670654 | 8230 | ||

| 0.059659 *** (0.0000) | 0.932085 *** (0.0000) | −8168736 | 10078 | 0.059562 *** (0.0000) | 0.931949 *** (0.0000) | −6566249 | 8101 |

| DCC(1,1) | Full Period | Pre-COVID | COVID | DCC(1,1) | Full Period | Pre-COVID | COVID |

|---|---|---|---|---|---|---|---|

| 0.778316 | 0.77948 | 0.777049 | 0.778307 | 0.779468 | 0.777042 | ||

| −0.017080 | 0.013162 | −0.050011 | 0.005532 | 0.072424 | −0.067308 | ||

| 0.639410 | 0.633941 | 0.645365 | 0.725803 | 0.747717 | 0.70194 | ||

| 0.773738 | 0.754496 | 0.794691 | 0.803866 | 0.801298 | 0.806663 | ||

| 0.699301 | 0.672014 | 0.729014 | 0.740293 | 0.722064 | 0.760142 | ||

| 0.624351 | 0.615718 | 0.633752 | 0.681546 | 0.677399 | 0.686063 | ||

| 0.708394 | 0.727672 | 0.687401 | 0.714453 | 0.753233 | 0.672226 | ||

| 0.690766 | 0.685013 | 0.69703 | 0.740066 | 0.744708 | 0.735012 | ||

| 0.658295 | 0.642678 | 0.675301 | 0.730576 | 0.731375 | 0.729706 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yan, K.; Yan, H.; Gupta, R. Are GARCH and DCC Values of 10 Cryptocurrencies Affected by COVID-19? J. Risk Financial Manag. 2022, 15, 113. https://doi.org/10.3390/jrfm15030113

Yan K, Yan H, Gupta R. Are GARCH and DCC Values of 10 Cryptocurrencies Affected by COVID-19? Journal of Risk and Financial Management. 2022; 15(3):113. https://doi.org/10.3390/jrfm15030113

Chicago/Turabian StyleYan, Kejia, Huqin Yan, and Rakesh Gupta. 2022. "Are GARCH and DCC Values of 10 Cryptocurrencies Affected by COVID-19?" Journal of Risk and Financial Management 15, no. 3: 113. https://doi.org/10.3390/jrfm15030113

APA StyleYan, K., Yan, H., & Gupta, R. (2022). Are GARCH and DCC Values of 10 Cryptocurrencies Affected by COVID-19? Journal of Risk and Financial Management, 15(3), 113. https://doi.org/10.3390/jrfm15030113