3. Mandates and Health Spending

While previous research identified this tradeoff and has documented many specific ways in which the reactions of insurers and employers at least partly undermine the effectiveness of mandates, it remains unclear whether the net effect of mandates is to increase or to reduce the affordability of health care. Two key pieces of information needed to fully evaluate the effect of mandates have been missing: their effect on out-of-pocket healthcare spending and on overall healthcare spending. We must understand these outcomes in order to quantify the overall costs and benefits of mandates.

The mechanism by which mandates are expected to make care more affordable is by reducing out-of-pocket costs. If patients have been spending directly out-of-pocket on health care because it is not covered by insurance, then when a state mandate causes insurers to begin covering that care, we would generally expect out-of-pocket spending on that care to fall dramatically for insured patients. This has been found to be the case for the one mandate where out-of-pocket spending has been studied, mental health parity (

Barry et al. 2006). To date, however, no previous study has measured whether state benefit mandates in general reduce out-of-pocket spending.

In this project, I evaluate the net effect of mandates on health care affordability using data on out-of-pocket and overall health care spending from the Medical Expenditure Panel Survey—Household Component (MEPS-HC). The MEPS-HC surveys approximately 30,000 households each year and collects extensive information on demographics, health status, health insurance, and health expenditures. Out-of-pocket costs are an important outcome in their own right for patients and policymakers. Knowing how state health insurance benefit mandates affect out-of-pocket costs is also crucial for evaluating mandates more broadly. Reducing out-of-pocket costs is a necessary condition for mandates to have positive effects on the affordability of care.

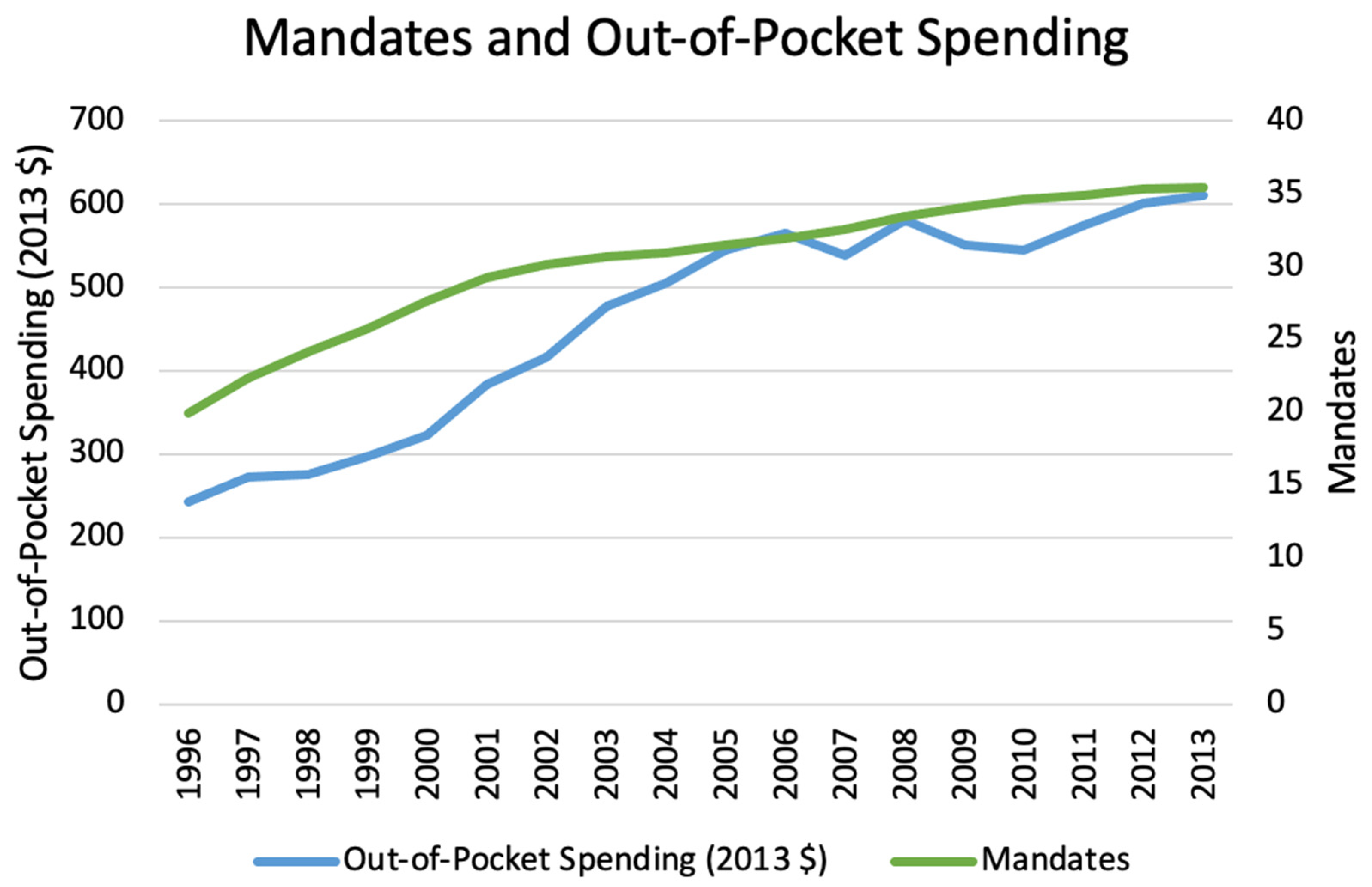

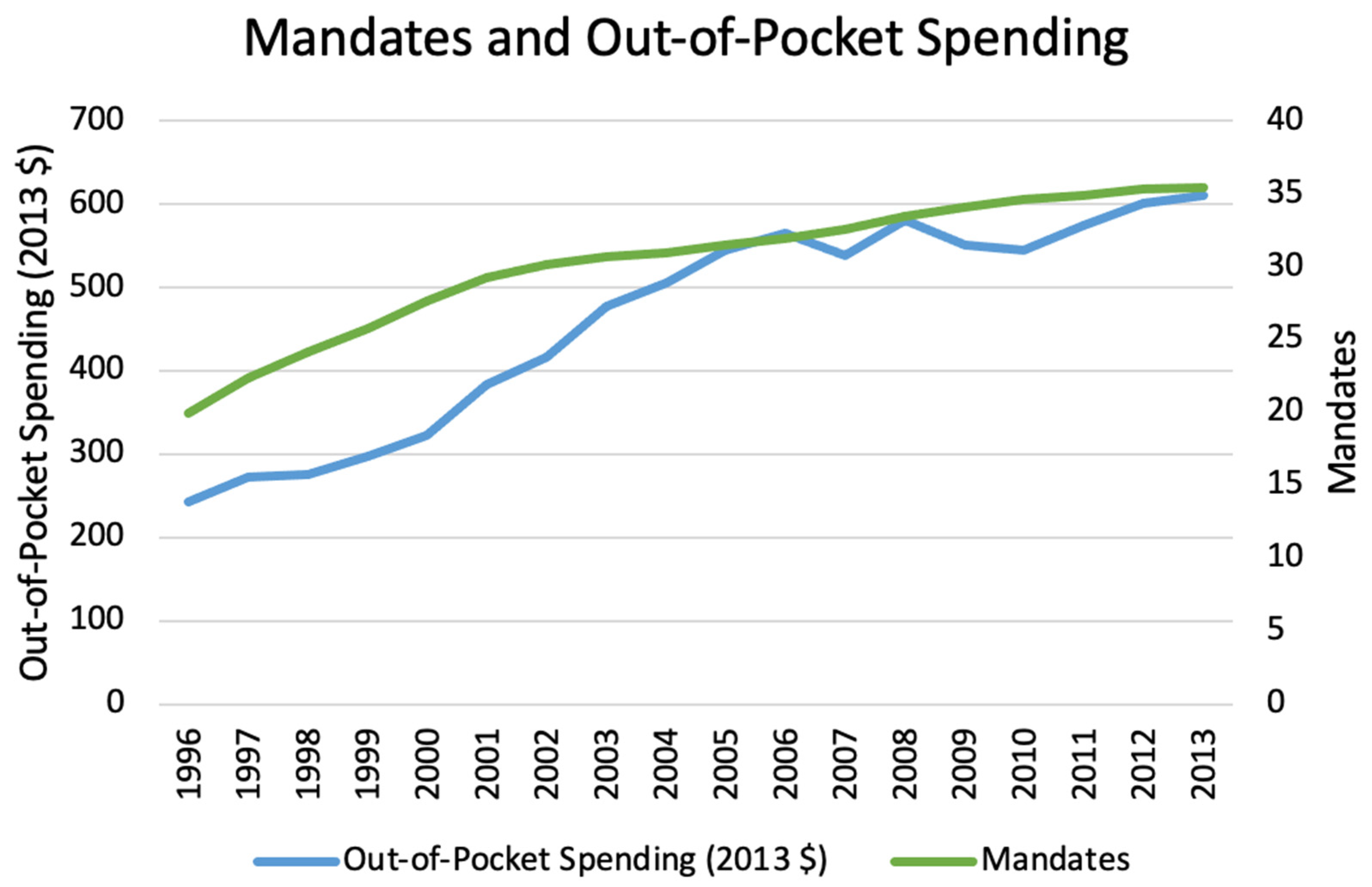

Figure 1 shows that out-of-pocket spending nationally has generally risen over time along with the average number of state mandates, but our regression analysis using individual- and state-level data suggests that if mandates have any causal effect it is to reduce out-of-pocket spending. In the next section, I consider more fully how mandates might affect out-of-pocket and overall health spending.

4. Affordability Framework

If mandates reduce household medical expenditure risk and promote affordability, we would expect them to work by reducing out-of-pocket spending on mandated services, being paid for by increased premiums and/or reduced insurer profits. If mandates are not working, we would expect to observe either that they are non-binding, with no effect on out-of-pocket spending on mandated services, or that they do reduce out-of-pocket costs of mandated services but that negative reactions (e.g., rising deductibles or coinsurance, insurers ceasing to cover non-mandated services, employers or individuals dropping coverage in response to rising premiums) prevent this from translating into more affordable care or more comprehensive insurance overall. I will assess how changes along many such margins together affect health care affordability, taking care to distinguish between its effect on average health care spending and its effect on risk reduction through insurance coverage.

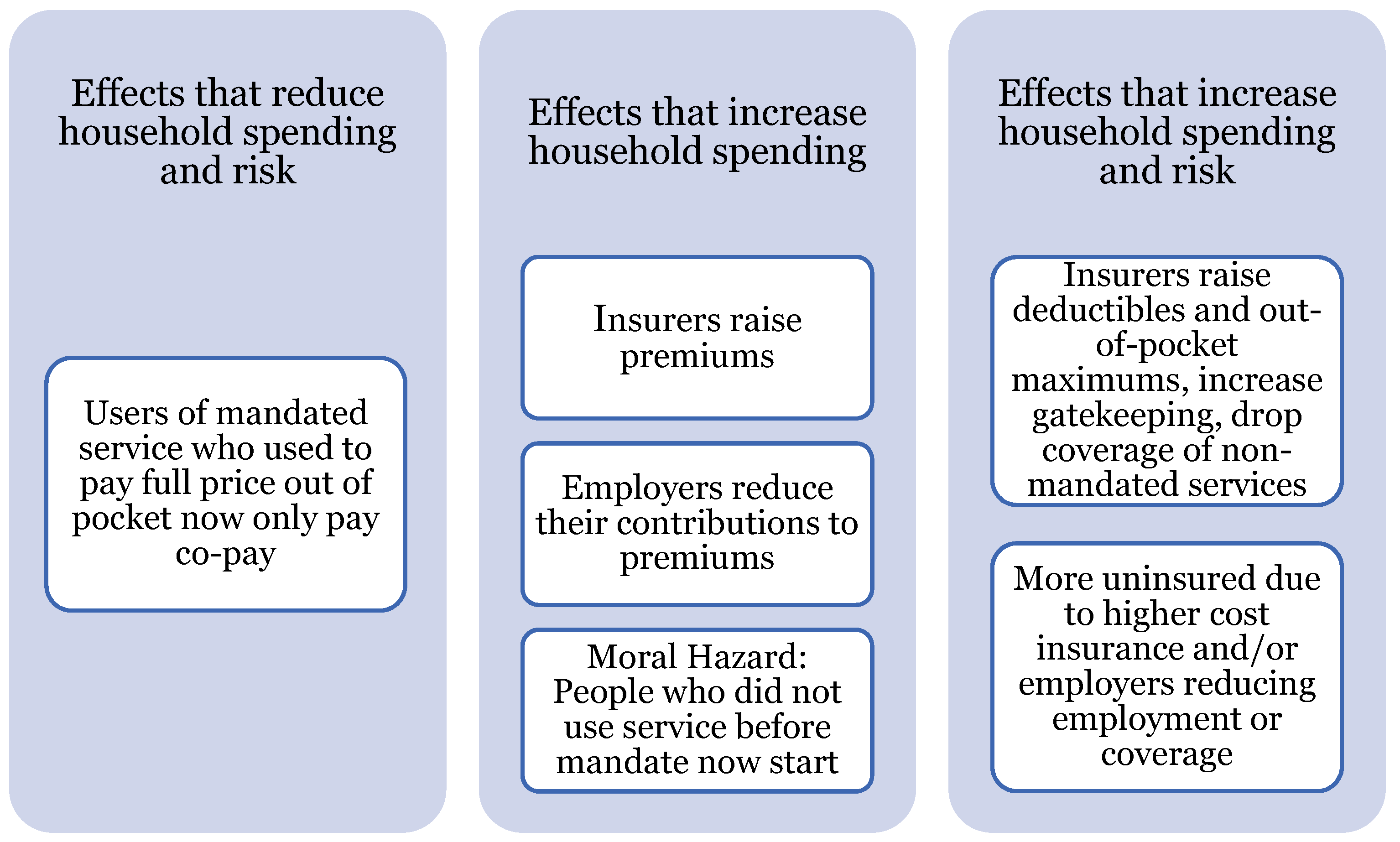

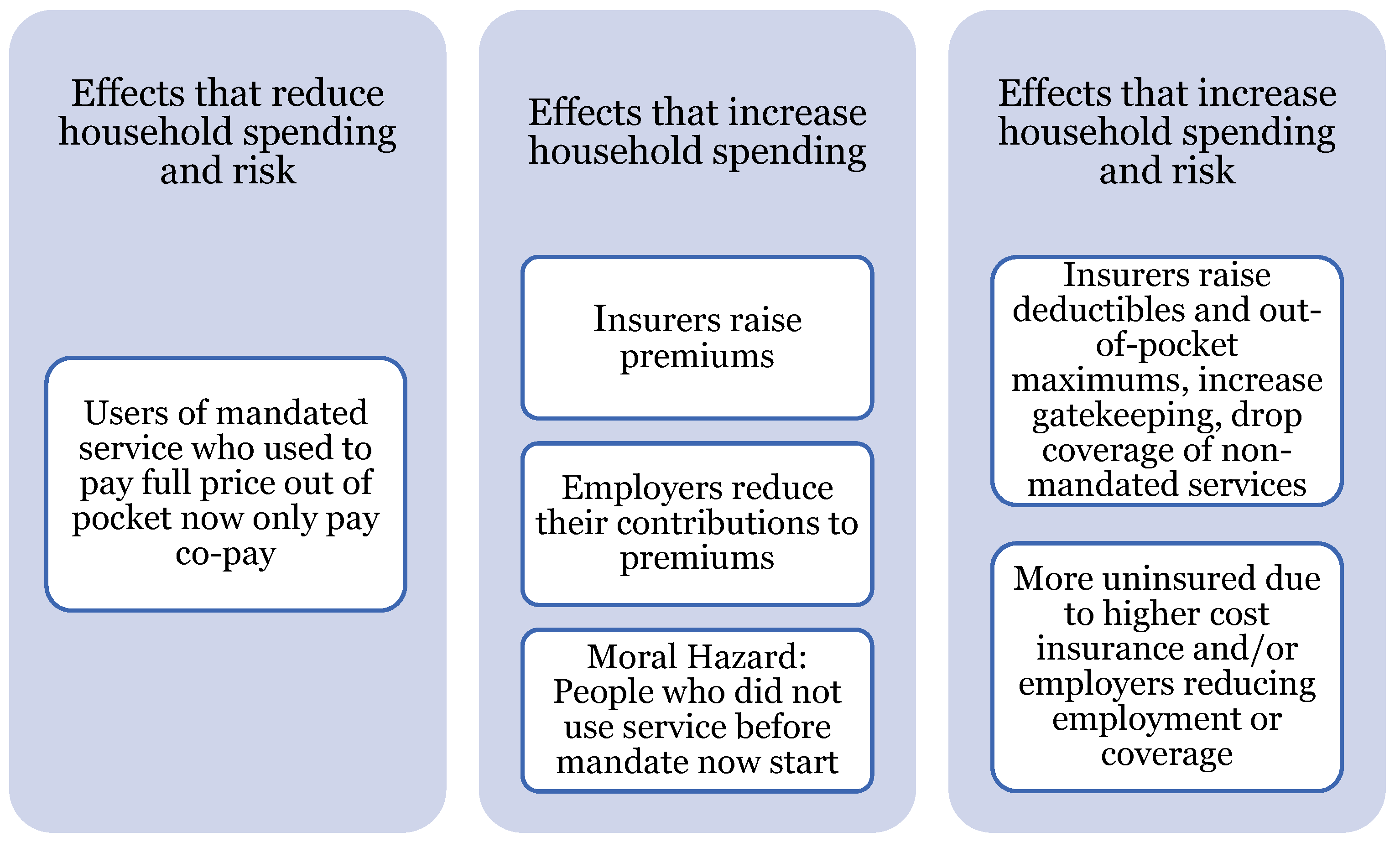

Figure 2 categorizes the main possible effects of mandates. The first-stage effect of mandates is that they actually lead insurers to cover services they previously did not; if mandates are non-binding we would not expect any follow-on effects. Presuming that mandates are at least sometimes binding, as seems likely given that the literature has often found follow-on effects, we can then categorize those effects.

The left branch illustrates the effect that policymakers likely hope for: the mandate leads insurers to cover a service they otherwise would not, so that insured patients who use the service now pay less out-of-pocket; barring any countervailing effects, this reduction in out-of-pocketing spending leads to lower overall health spending by households and reduces their risk of suddenly incurring a large expense. This could be achieved if the mandate does not increase insurer costs, or if insurers do not pass cost increases on to patients.

The center branch illustrates ways in which the mandate could lead to increased average health spending by households, though without directly increasing their risk of large unexpected out-of-pocket costs. These are primarily ways that insurers, or employers offering insurance, could attempt to pass on the cost of the mandate to households: higher premiums or employee contributions to premiums. It also includes the possibility of moral hazard: households who did not use the service before the mandate begin to use it after it is covered by insurance. Even though they only pay a fraction of the cost of the service, their observed spending still rises because they now pay co-pays where previously they paid (and received) nothing.

The right branch illustrates ways in which the mandate could lead households to take on more risk of unexpected out-of-pocket costs while also likely increasing average health spending. Insurers could lower the quality of their coverage by raising deductibles and out-of-pocket maximums or by reducing coverage of non-mandated services; this would lead to higher out-of-pocket spending and more risk for households. Finally, the sum of all these attempts to pass on the cost of the mandate to households could lead households to choose not to purchase insurance at all, or the higher cost of insurance could lead employers to reduce employment or drop insurance coverage.

The previous literature has tried to evaluate the extent to which mandates cause some of these costly countervailing effects. However, previous work has not attempted to evaluate whether mandates have benefits that exceed their costs. Most papers on mandates only attempt to quantify the extent of one or two of the costs described above. However, showing that one hypothesized cost is zero does not imply mandates are a good policy, and showing that one hypothesized cost is high does not imply mandates are a bad policy. To fully evaluate the policy, we either need to complete the arduous work of measuring all costs and benefits separately and summing them, or to find a few “sufficient statistics” that once measured can tell the full story themselves.

There has been one “sufficient statistic” for welfare analysis proposed in previous literature. In the

Summers (

1989) model, employers attempt to pass the costs of a mandate back to employees. If employees value the mandate at least as much as its cost, then this cost-shifting attempt succeeds at lowering wages; if employees value the mandate below its cost, the cost-shifting attempt leads to lower employment.

Gruber (

1994a) found that employees fully valued a mandate for maternity care, while

Lahey (

2012) and

Bailey (

2014b) found that employees did not fully value mandates for infertility treatment or prostate cancer screening, respectively. While this welfare analysis is valuable, it makes strong assumptions (e.g., competitive labor markets and perfect information), can only be applied to employer-sponsored insurance, and only tracks some of the margins of adjustment.

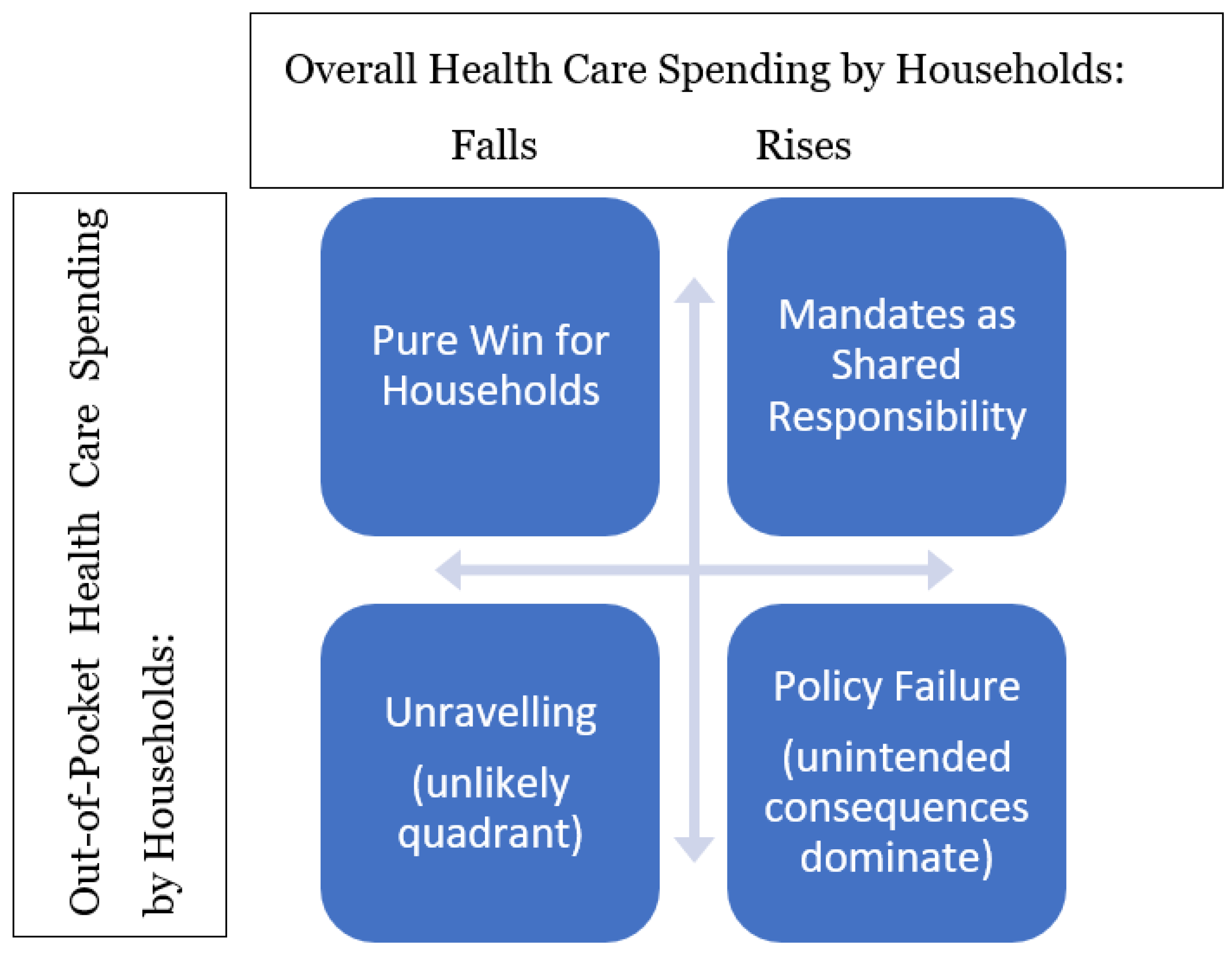

I propose a new set of sufficient statistics, as shown in

Figure 3: out-of-pocket health care spending and overall health care spending (including out-of-pocket spending and premiums). Mandates could move these either up or down, and knowing which direction each moves allows us to characterize the net effect of the mandate.

The top left quadrant of the figure shows the case where out-of-pocket and overall spending both fall. In this case, mandates caused a service to be covered, which led households who use the service to pay less out-of-pocket and overall; the negative countervailing effects were either zero or not enough to overwhelm this benefit. This is the case mandate advocates hope for, where the benefits of the mandate are clear and the costs are either non-existent, or small relative to benefits, or at least borne by insurers rather than households.

The top right quadrant shows the case where out-of-pocket costs fall but overall health spending by households rise. This case would occur if the benefit of the mandate reducing out-of-pocket costs is realized, but is more than offset by rising premiums, so that overall health care spending rises (premiums rise more than out-of-pocket spending falls). In this case, the benefit mandates take on the character of the ACA’s “shared responsibility” mandate to buy insurance: households spend more overall on average but their risk is reduced as insurance pools it. This case is closest to a judgement call: households pay higher costs to get more insurance. This could be worth it if policymakers think that households systematically underestimate the need for insurance, or if adverse selection problems loom large.

The bottom two quadrants see out-of-pocket costs rise, undermining the case for mandates as a policy. Most likely this occurs if insurance quality falls, with insurers raising cost-sharing and reducing what they cover. Along with increases in premiums this could lead to increases in total health spending by households (bottom right quadrant). Alternatively, out-of-pocket spending could increase while total health spending falls (bottom left). This could indicate an unravelling of insurance markets, where rising premiums lead households or employers to drop insurance coverage entirely; this lack of coverage would increase out-of-pocket spending, but not by as much as spending on premiums fall. The demand for insurance would need to be quite elastic for the coverage-dropping effects to dominate, which is why I consider this quadrant unlikely.

4.1. Data Sources

Data on state health insurance benefit mandates is available through 2013 from the Blue Cross Blue Shield Association (

Laudicina et al. 2013). The data provide the total number of mandates in each state, as well as the exact mandated conditions, treatments, providers, or persons, and the year each mandate came into effect. These data have been used frequently in previous research on benefit mandates. Here I use it to create a variable that counts the total number of benefit mandates in effect in each state in each year 1996–2013.

The MEPS-HC provides the other key variables. Since 1996, the Agency for Healthcare Research and Quality has conducted the MEPS-HC annually by surveying approximately 30,000 households each year. They collect data on out-of-pocket health care expenditures as well as insurance coverage, demographics, and medical conditions. For privacy reasons, the public MEPS-HC does not include geographic information, so I use the restricted MEPS-HC that includes each respondent’s state of residence, which allows me to merge in the state-level data on mandates. The MEPS-HC provides specific detail for many variables, breaking down expenditures both by source (e.g., out-of-pocket, Medicare, Medicaid, private insurance) and by type of care (e.g., hospital, office-based, prescription drug, dental). I adjust all expenditure variables for inflation in all regressions, reporting all results in 2012 dollars. The individual-level demographic control variables used are age (indicator variables for each year of age), gender, race (Black or Asian), ethnicity (Hispanic), education (indicators for high school degree and college degree), and health status (indicators for self-reported health that is good/very good and fair/poor, excellent health is the omitted category).

4.2. Econometric Strategies

4.2.1. Fixed Effects

The primary econometric approaches will be fixed effects and difference-in-difference, similar to most recent work on mandates. The initial baseline fixed effects specification is:

where Spending

ist represents an individual’s health spending in a given year (out-of-pocket or total, depending on the regression), Mandates

st−1 is a count of health insurance benefit mandates in place in the individual’s state in the previous year, X

ist is a vector of individual-level controls (age, gender, race, ethnicity, education, and health status), and

s and

t represent state and year fixed effects.

Endogeneity is certainly a significant concern, as states do not simply pass mandates at random. Among the many political and policy considerations that could influence the passage of mandates, one is particularly concerning: mandates could be passed in response to changes in out-of-pocket costs. For instance, rising out-of-pocket costs could spur patients or providers to lobby for a mandate that insurance cover them. If costs continued to rise after the mandate, the estimation strategy described above might estimate that mandates increase out-of-pocket costs even if they have no effect on costs or slightly reduce them. To some extent this issue could be tested for directly and controlled for using state-specific time trends. However, a better solution is to identify a control group that is subject to the same conditions before the mandate but that is not covered by the mandate. This group can be used as part of difference-in-difference estimation to more accurately identify the causal effect of the mandate.

4.2.2. Difference-in-Difference

The difference-in-difference strategy takes advantage of the fact that benefit mandates do not apply to everyone, but only to private insurance companies and those whom they cover. State mandates by their nature do not directly affect the uninsured, and due to federal pre-emption do not affect Medicare, Medicaid, or self-insured employer plans. Each of these could therefore provide a control group for those covered by the mandate, though we must be careful to select treatment and control groups that are similar enough to provide an appropriate match. For instance, Medicare recipients are on average older and might be expected to have different trends in out-of-pocket costs from privately insured individuals generally.

The most appropriate control group available is self-insured plans, as these are also private and cover a population most similar in income, age, and employment to those with non-mandate-exempt private plans. While MEPS-HC does not track which employer plans are self-insured, they do track a reasonable proxy: employer size. It is rare for firms with fewer than 50 employees to self-insure, and rare for firms with more than 50 employees not to. Because self-insured plans are exempt from mandates, we should expect mandates to have much larger effects on employees of small firms than those of large firms; previous work has found this to be the case (

Bailey 2014a).

where β

3, the coefficient of interest, measures the effect of mandates on the out-of-pocket spending of employees of small firms. X

it is a vector of individual-level controls (such as age, race, and health status), and

s and

t represent state and year fixed effects.

6. Conclusions

Using fixed effects and difference-in-difference econometric strategies and restricted MEPS-HC data, I provide the first estimates of how health insurance benefit mandates affect out-of-pocket and overall health care spending. Both strategies find that mandates reduce out-of-pocket spending, while they are divided on whether mandates also reduce overall health care spending and spending by private insurers.

Simply summing the total number of state mandates in a given year has the drawback that we do not expect all mandates to have the same effect on costs. Some mandates target treatments, conditions, or providers that are common and/or expensive (e.g., dentists, chiropractors, autism therapy) and so might have large effects, while others would be expected to be have smaller effects due to covering inexpensive things and/or rare conditions (e.g., lead screening for children or wigs for cancer patients). There are two main alternatives to this simple summation. One is to create an index that weights mandates by their predicted costs, or to use only mandates actuarially predicted to have high costs, as in

Gruber (

1994b). Another is to study mandates individually. Studying single mandates would allow for superior identification strategies that better address concerns over endogeneity; but studying all of the 100+ mandates individually would be challenging, while focusing on a few may tell us little about the rest if the few studied are unrepresentative.

Another limitation of the data is that it does not include health insurance premiums. In the “affordability framework” I discuss, I am interested in households’ overall spending on healthcare- including health insurance premiums. However, the “total health care spending” variable in MEPS includes spending BY health insurers on behalf of their enrollees, not the households’ spending on premiums. Therefore, lower “total health spending” as measured by this variable does not necessarily indicate that health care is more affordable for households.

Due to these divided results and the limitations of the data and econometric strategies, I am unable to determine whether or not health insurance benefit mandates represent a win for households. Yet, while I cannot say for sure whether the benefits of these mandates exceed the costs, I can say that the benefits exist. Mandates on average do lead to lower out-of-pocket costs for households. Policymakers should weigh this benefit of mandates alongside the costs of mandates identified by the previous literature, such as higher premiums, as they consider whether to pass additional mandates or repeal previous ones.

{kind=link}

{kind=link}

{kind=link}