Towards True Climate Neutrality for Global Aviation: A Negative Emissions Fund for Airlines

Abstract

1. Introduction

1.1. The Urgency of Making Aviation Climate Neutral

1.2. Hypotheses and Methodology

2. Literature Review

2.1. Large and Growing Climate Impact of Aviation

2.2. Long-Term and Short-Term Climate Impacts

2.3. The Possible Contribution of Alternative Fuels

3. Reducing the Climate Impact of Aviation

4. Paying for Negative Emissions

4.1. From a Country to an International Air Transport Perspective

- Growth rate: aviation is projected to continue increasing emissions for decades unless the whole model changes, most likely as a result of change being imposed from outside. Rich countries’ territorial emissions have been falling since at least 2005 and some since 1990, and other countries are expected to peak soon and then start decreasing.

- Non-CO2 climate effects of aviation, on average, triple the climate impact. For countries, this impact is much smaller, a fraction of the impact of CO2, mainly due to methane and nitrous oxide. However, due to their short-lived nature, these non-CO2 effects will have a much lower impact if air travel starts declining, and a disproportionately large impact if current growth continues.

- Territoriality: it is unclear who is responsible for emissions in international airspace or when briefly flying over a third country.

- High-risk business/high default rate: due to high fixed costs, deregulation, cyclicality, and highly variable fuel costs, airlines are a very risky business. Additionally, due to the difficulty of getting creditors to pay across jurisdictions, any payment to a future negative emissions fund would need to happen almost immediately, possibly even as a pre-payment before flights.

4.2. Proposed Concept

- The contraction phase: airlines must contract flights by at least 2.5% p.a. until 2050, as a condition for continued participation in NEFA. The 2.5% figure is the minimum to ensure the short-lived non-CO2 effects balance the CO2 emitted (Klöwer et al. 2021). However, when the contraction phase ends, this effect stops and the long-lived CO2 must still be removed, which is the purpose of the payment into the fund.

- The steady-state phase: after a period of stabilization (which we do not model here), the short-lived non-CO2 effects will stop affecting the climate; only long-lived GHG (in our model only CO2) must be removed.

4.3. Model and Assumptions

- Fund launch 2025.

- 2025 CO2 aviation emissions: 1000 Mt.

- Flights (i.e., RPK) reduction of 7.3% p.a. from 2025 until 2050.

- Flight CO2 emissions reduction of 8.8% p.a. from 2025 until 2050, including efficiency gains of 1.5% p.a.

- Emissions stabilization in 2050 at 100 Mt CO2.

- CO2 payments increase by 5% per quarter from 2025 to 100% in 2030.

- First year of negative emissions: 1 Mt in 2026.

- Annual growth of negative emissions for 10 years: +50%.

- Annual growth of negative emissions after 10 years: +25%.

- Max annual negative emissions available for aviation (cap): 400 Mt.

- Negative emissions cost: $400/t CO2 including project governance, in 2025.

- Negative emissions cost: $250/t CO2 including project governance, from 2050.

- Interest rate: 2.00%.

- All prices and costs are adjusted for inflation (our model uses constant 2021 US dollars).

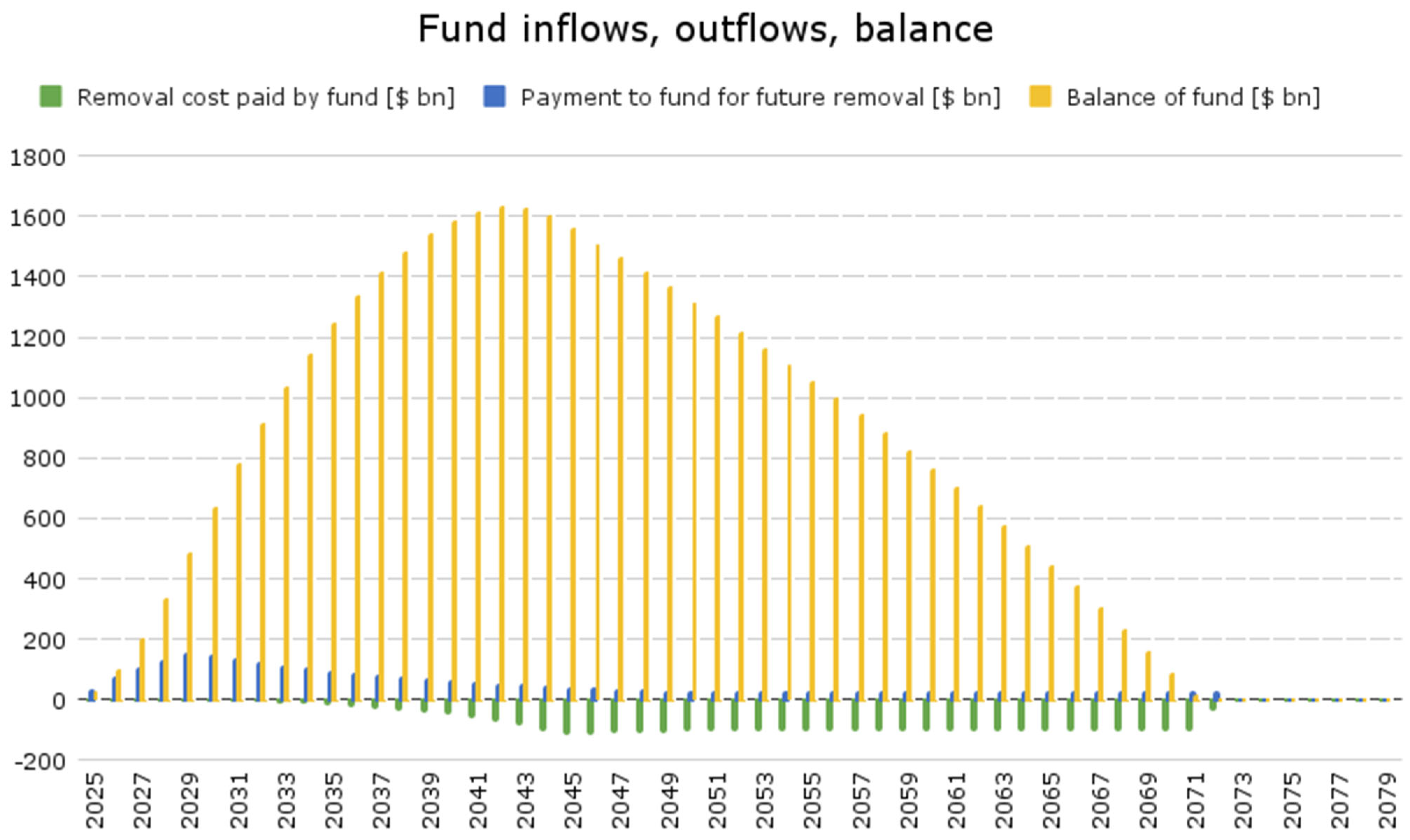

4.4. Results

4.5. Sensitivity Analysis and Robustness

5. Governance

5.1. Country vs. Airline Perspective, Nature of Risks, Role of Markets

5.2. Failure of CORSIA

5.3. History of Broken or Forgotten Promises

5.4. NEFA Governance and Participation Enforcement

6. Discussion and Conclusions

6.1. Can NEFA Be Implemented in the Real World?

6.2. Conclusions—A New Vision for Aviation

Supplementary Materials

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Airlines for America. 2022. World Airlines Traffic and Capacity, March 2022. Airlines For America. March. Available online: https://www.airlines.org/dataset/world-airlines-traffic-and-capacity/ (accessed on 23 October 2022).

- Air Transport Action Group—ATAG. 2021. “Waypoint 2050”. Air Transport Action Group—ATAG. Available online: https://aviationbenefits.org/environmental-efficiency/climate-action/waypoint-2050/ (accessed on 23 October 2022).

- Beevor, Jamie, and Keith Alexander. 2022. Missed Targets: A Brief History of Aviation Climate Change Targets. UK: Possible. Available online: www.wearepossible.org/latest-news/for-20-years-the-aviation-has-missed-all-but-one-of-their-sustainability-targets (accessed on 23 October 2022).

- Biofuelwatch. 2018. Neste: The Finnish Company Preparing to Put Palm Oil in Aircraft Fuel Tanks—Biofuelwatch. Available online: https://www.biofuelwatch.org.uk/2019/neste-aviation-biofuels/ (accessed on 23 October 2022).

- Brazzola, Nicoletta, Anthony Patt, and Jan Wohland. 2022. Definitions and Implications of Climate-Neutral Aviation. Nature Climate Change 12: 761–67. [Google Scholar] [CrossRef]

- Burkhardt, Ulrike, Lisa Bock, and Andreas Bier. 2018. Mitigating the Contrail Cirrus Climate Impact by Reducing Aircraft Soot Number Emissions. Npj Climate and Atmospheric Science 1: 1–7. [Google Scholar] [CrossRef]

- Climate Action Tracker. 2022. Climate Action Tracker: International Aviation. Available online: https://climateactiontracker.org/sectors/aviation/ (accessed on 23 October 2022).

- Cooper, Hannah V., Stephanie Evers, Paul Aplin, Neil Crout, Mohd Puat Bin Dahalan, and Sofie Sjogersten. 2020. Greenhouse Gas Emissions Resulting from Conversion of Peat Swamp Forest to Oil Palm Plantation. Nature Communications 11: 407. [Google Scholar] [CrossRef] [PubMed]

- EasyJet. 2021. EasyJet 2021 Annual Report and Accounts ‘Fast Track—The Recovery’. EasyJet plc. Available online: https://corporate.easyjet.com/~/media/Files/E/Easyjet/documents/easyjet-2021-annual-report-and-accounts.pdf (accessed on 23 October 2022).

- EasyJet. 2022. EasyJet Signs up to Support Breakthrough Carbon Removal Solutions. Available online: https://mediacentre.easyjet.com/story/15528/easyjet-signs-up-to-support-breakthrough-carbon-removal-solutions (accessed on 23 October 2022).

- German Federal Government. 2022. Speech by Olaf Scholz, Chancellor of the Federal Republic of Germany and Member of the German Bundestag, at the 13th Petersberg Climate Dialogue. Website of the Federal Government|Home Page. Available online: https://www.bundesregierung.de/breg-en/news/speech-by-olaf-scholz-chancellor-of-the-federal-republic-of-germany-and-member-of-the-german-bundestag-at-the-13th-petersberg-climate-dialogue-2064056 (accessed on 23 October 2022).

- Gössling, Stefan, and Andreas Humpe. 2020. The Global Scale, Distribution and Growth of Aviation: Implications for Climate Change. Global Environmental Change 65: 102194. [Google Scholar] [CrossRef]

- IATA. 2019. IATA—An Airline Handbook on CORSIA. IATA. Available online: https://www.iata.org/contentassets/fb745460050c48089597a3ef1b9fe7a8/corsia-handbook.pdf (accessed on 23 October 2022).

- IATA. 2021. IATA 77th AGM: Net-Zero Carbon Emissions by 2050. October 4. Available online: https://www.iata.org/en/pressroom/2021-releases/2021-10-04-03/ (accessed on 23 October 2022).

- IATA. 2022a. IATA—Air Passenger Numbers to Recover in 2024. Available online: https://www.iata.org/en/pressroom/2022-releases/2022-03-01-01/ (accessed on 23 October 2022).

- IATA. 2022b. IATA—Passenger Demand Recovery Continued in 2021 But Omicron Having Impact. Available online: https://www.iata.org/en/pressroom/2022-releases/2022-01-25-02/ (accessed on 23 October 2022).

- ICAO. 2021. CORSIA Default Life Cycle Emissions Values for CORSIA Eligible Fuels. Available online: https://www.icao.int/environmental-protection/CORSIA/Documents/ICAO%20document%2006%20-%20Default%20Life%20Cycle%20Emissions%20-%20March%202021.pdf (accessed on 23 October 2022).

- ICAO. 2022. ICAO: Countries’ Support Global ‘Net-Zero 2050′ Emissions Target to Achieve Sustainable Aviation. July 25. Available online: https://www.icao.int/Newsroom/Pages/Countries-highlevel-ICAO-emissions-talks-support-netzero.aspx (accessed on 23 October 2022).

- ICAO-CORSIA. 2022. Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA). Available online: https://www.icao.int/environmental-protection/CORSIA/Pages/default.aspx (accessed on 23 October 2022).

- IPCC. 2018. Global Warming of 1.5° C: An IPCC Special Report on the Impacts of Global Warming of 1.5° C above Pre-Industrial Levels and Related Global Greenhouse Gas Emission Pathways, in the Context of Strengthening the Global Response to the Threat of Climate Change, Sustainable Development, and Efforts to Eradicate Poverty. Cambridge and New York: Cambridge University Press. [Google Scholar]

- IPCC. 2021. IPCC. Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge and New York: Cambridge University Press. [Google Scholar]

- IPCC. 2022. IPCC. Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge and New York: Cambridge University Press. [Google Scholar]

- Jeswani, Harish K., Andrew Chilvers, and Adisa Azapagic. 2020. Environmental Sustainability of Biofuels: A Review. Proceedings of the Royal Society A: Mathematical, Physical and Engineering Sciences 476: 20200351. [Google Scholar] [CrossRef] [PubMed]

- Klöwer, Milan, Myles Allen, David Lee, Simon Proud, Leo Gallagher, and Agnieszka Skowron. 2021. Quantifying Aviation’s Contribution to Global Warming. Environmental Research Letters 16: 104027. [Google Scholar] [CrossRef]

- Lee, David S., David W. Fahey, Agnieszka Skowron, Myles R. Allen, Ulrike Burkhardt, Qi Chen, Sarah J. Doherty, S. Freeman, P. M. Forster, J. Fuglestvedt, and et al. 2021. The Contribution of Global Aviation to Anthropogenic Climate Forcing for 2000 to 2018. Atmospheric Environment 244: 117834. [Google Scholar] [CrossRef] [PubMed]

- MacKay, David J. C. 2011. Sustainable Energy—Without the Hot Air. Repr. Cambridge: UIT Cambridge. [Google Scholar]

- Meadows, Donella H. 1999. Leverage Points: Places to Intervene in a System. The Academy for Systems Change (blog). Available online: http://donellameadows.org/archives/leverage-points-places-to-intervene-in-a-system/ (accessed on 23 October 2022).

- Neu, Urs. 2021. The Impact of Emissions from Aviation on the Climate. Swiss Academies Communications 16. Available online: https://scnat.ch/en/id/cSx4y (accessed on 23 October 2022).

- Nick, Sascha, and Philippe Thalmann. 2021. Carbon Removal, Net Zero, and Implications for Switzerland. E4S Enterprise for Society. Available online: https://e4s.center/document/carbon-removal-net-zero-and-implications-for-switzerland (accessed on 23 October 2022).

- Nick, Sascha, and Philippe Thalmann. 2022. Swiss Negative Emissions Fund—Paying for Net Zero. E4S Enterprise for Society. Available online: https://e4s.center/document/swiss-negative-emissions-fund-paying-for-net-zero (accessed on 23 October 2022).

- Oreskes, Naomi, and Erik M. Conway. 2011. Merchants of Doubt: How a Handful of Scientists Obscured the Truth on Issues from Tobacco Smoke to Global Warming, Paperback ed. New York: Bloomsbury Press. [Google Scholar]

- Ritchie, Hannah, and Max Roser. 2021. Forests and Deforestation: Palm Oil. Our World in Data. Available online: https://ourworldindata.org/palm-oil (accessed on 23 October 2022).

- Ritchie, Hannah, Max Roser, and Pablo Rosado. 2020. CO2 Emissions from Aviation. Our World in Data. November 28. Available online: https://ourworldindata.org/co2-emissions-from-aviation (accessed on 23 October 2022).

- Sausen, Robert, and Ulrich Schumann. 2000. Estimates of the climate response to aircraft CO2 and NOx emissions scenarios. Climatic Change 44: 27–58. [Google Scholar] [CrossRef]

- Swiss Federal Council. 2021. Switzerland’s Long-Term Climate Strategy Long-Term Low Greenhouse Gas Emission Development Strategies (LT-LEDS) The Federal Council. Available online: https://www.bafu.admin.ch/bafu/en/home/topics/climate/info-specialists/emission-reduction/reduction-targets/2050-target/climate-strategy-2050.html (accessed on 23 October 2022).

- Teoh, Roger, Ulrich Schumann, Arnab Majumdar, and Marc E. J. Stettler. 2020. Mitigating the Climate Forcing of Aircraft Contrails by Small-Scale Diversions and Technology Adoption. Environmental Science & Technology 54: 2941–50. [Google Scholar] [CrossRef]

- Thalmann, Philippe, Fleance Cocker, Pallivathukkal Cherian Abraham, Marius Brülhart, Nikolai Orgland, Dominic Rohner, and Michael Yaziji. 2021. Introducing an Air Ticket Tax in Switzerland: Estimated Effects on Demand. Ecublens: E4S Enterprise for Society. Available online: https://infoscience.epfl.ch/record/285985/files/WP_aviation_en.pdf (accessed on 23 October 2022).

- UK Department for Transport. 2021. UK Department for Transport—Sustainable Aviation Fuels Mandate—Summary of Consultation Responses and Government Response; London: UK Department for Transport. Available online: https://www.gov.uk/government/consultations/mandating-the-use-of-sustainable-aviation-fuels-in-the-uk (accessed on 23 October 2022).

- Voigt, Christiane, Jonas Kleine, Daniel Sauer, Richard H. Moore, Tiziana Bräuer, Patrick Le Clercq, Stefan Kaufmann, Monika Scheibe, Tina Jurkat-Witschas, Manfred Aigner, and et al. 2021. Cleaner Burning Aviation Fuels Can Reduce Contrail Cloudiness. Communications Earth & Environment 2: 1–10. [Google Scholar] [CrossRef]

- World Economic Forum. 2021. Guidelines for a Sustainable Aviation Fuel Blending Mandate in Europe. Available online: https://www.weforum.org/reports/guidelines-for-a-sustainable-aviation-fuel-blending-mandate-in-europe/ (accessed on 23 October 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Sensitivity Analysis | Range of Parameter | CO2 Price [USD/t] | Σ CO2 Removal Payments [USD bn] | Removed All Excess CO2 by Year | |||||

|---|---|---|---|---|---|---|---|---|---|

| Simulation parameters | Baseline | Min. | Max. | Min. param. | Max. param. | Min. param. | Max. param. | Min. param. | Max. param. |

| Emission reductions p.a. | 8.8% | 2.5% | 10.0% | 160 | 239 | 9651 | 2953 | 2136 | 2069 |

| Reductions, narrower range, p.a. | 5.0% | 7.3% | 196 | 218 | 5177 | 3772 | 2091 | 2077 | |

| Final emissions [Mt/p.a.] | 100 | 50 | 150 | 231 | 227 | 2979 | 3717 | 2069 | 2076 |

| NE growth 2027-36 | 50.0% | 33% | 60% | 203 | 246 | 3326 | 3217 | 2078 | 2068 |

| NE growth 2037+ | 25.0% | 10% | 50% | 204 | 243 | 3401 | 3228 | 2080 | 2069 |

| Max removals [Mt p.a.] | 400 | 200 | 800 | 186 | 249 | 4629 | 2897 | 2128 | 2057 |

| Removal cost in 2025 [USD/t] | 400 | 300 | 600 | 222 | 245 | 3173 | 3422 | 2072 | 2072 |

| Removal cost from 2050 [USD/t] | 250 | 200 | 300 | 190 | 270 | 2671 | 3841 | 2072 | 2072 |

| Interest rate p.a. | 2% | 1% | 3% | 269 | 196 | 3256 | 3256 | 2072 | 2072 |

| Interest rate, extreme range | 0% | 4% | 314 | 168 | 3256 | 3256 | 2072 | 2072 | |

| Simulation results-baseline | 230 | 3256 | 2072 | ||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nick, S.; Thalmann, P. Towards True Climate Neutrality for Global Aviation: A Negative Emissions Fund for Airlines. J. Risk Financial Manag. 2022, 15, 505. https://doi.org/10.3390/jrfm15110505

Nick S, Thalmann P. Towards True Climate Neutrality for Global Aviation: A Negative Emissions Fund for Airlines. Journal of Risk and Financial Management. 2022; 15(11):505. https://doi.org/10.3390/jrfm15110505

Chicago/Turabian StyleNick, Sascha, and Philippe Thalmann. 2022. "Towards True Climate Neutrality for Global Aviation: A Negative Emissions Fund for Airlines" Journal of Risk and Financial Management 15, no. 11: 505. https://doi.org/10.3390/jrfm15110505

APA StyleNick, S., & Thalmann, P. (2022). Towards True Climate Neutrality for Global Aviation: A Negative Emissions Fund for Airlines. Journal of Risk and Financial Management, 15(11), 505. https://doi.org/10.3390/jrfm15110505