Mapping the Literature on Social Responsibility and Stakeholders’ Pressures in the Mining Industry

Abstract

1. Introduction

2. Literature Review

2.1. CSR Theories

2.2. CSR in the Mining Industry

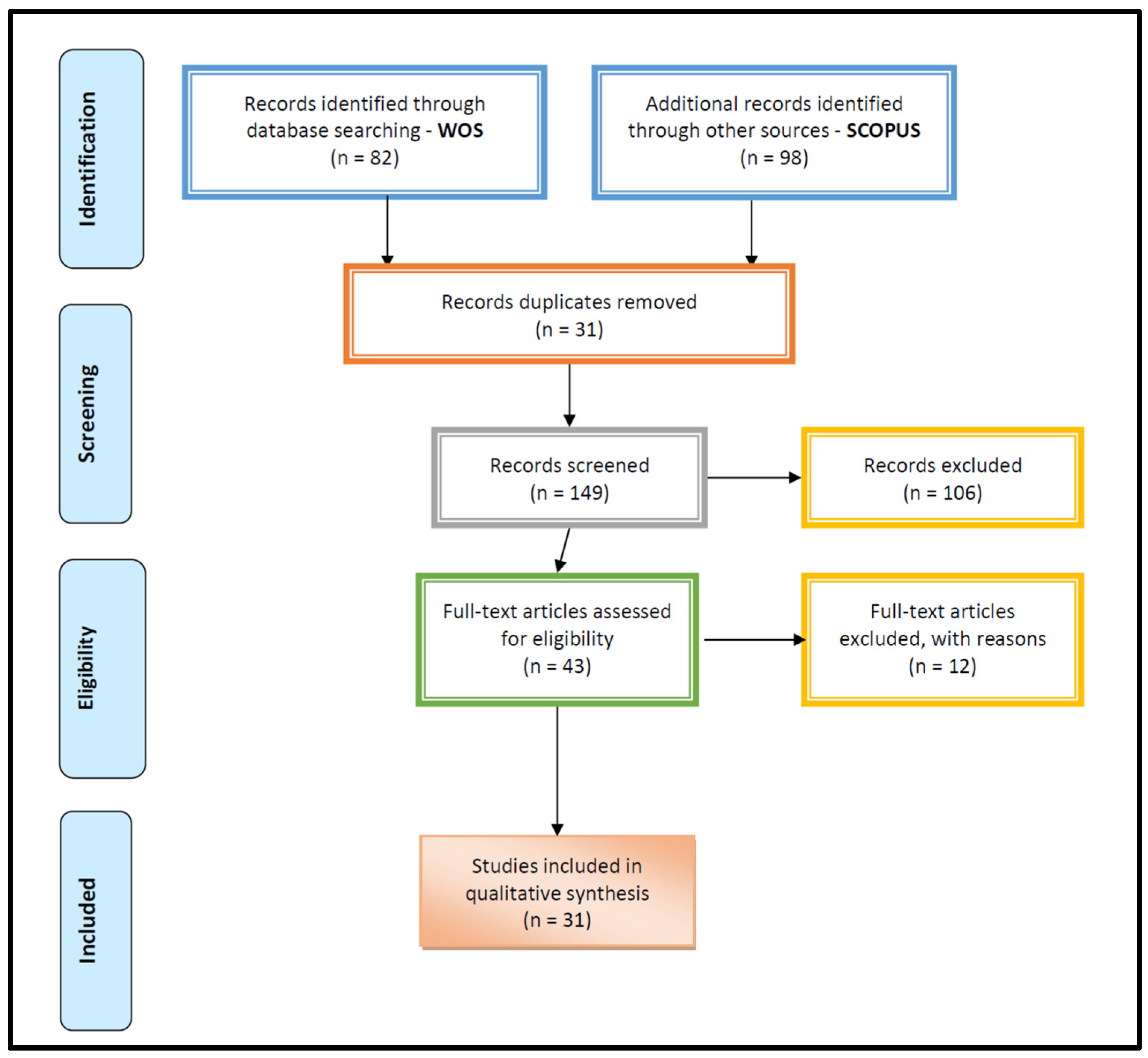

3. Methodology

4. Results

4.1. Descriptive Analysis

4.2. Content Analysis

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Adiyarta, Krisna, Darmawan Napitupulu, Mohammad Syafrullah, Deni Mahdiana, and Rushdah Rusdah. 2020. Analysis of smart city indicators based on prisma: Systematic review. IOP Conference Series: Materials Science and Engineering 725: 012113. [Google Scholar] [CrossRef]

- Adler, Ralph, Mansi Mansi, Rakesh Pandey, and Carolyn Stringer. 2017. United Nations decade on biodiversity: A study of the reporting practices of the Australian mining industry. Accounting, Auditing and Accountability Journal 30: 1711–45. [Google Scholar] [CrossRef]

- Altman, Barbara W., and Deborah Vidaver-Cohen. 2000. A framework for understanding corporate citizenship: Introduction to the special edition of Business and Society Review “Corporate citizenship and the new millennium”. Business and Society Review 105: 1–7. [Google Scholar] [CrossRef]

- Alves, Maria-Ceu, and Margarida Rodrigues. 2017. Corporate Social Responsibility: An Integrative Approach in the Mining Industry. International Journal of Social Ecology and Sustainable Development 8: 19–37. [Google Scholar] [CrossRef]

- Alves, Maria-Ceu, and Margarida Rodrigues. 2019. Corporate Social Responsibility: An Integrative Approach in the Mining Industry. In Corporate Social Responsibility: Concepts, Methodologies, Tools, and Applications. Hershey: IGI Global, pp. 1135–54. [Google Scholar] [CrossRef]

- Amoako, Kwame Oduro, Beverley R. Lord, and Keith Dixon. 2017. Sustainability reporting: Insights from the websites of five plants operated by Newmont Mining Corporation. Meditari Accountancy Research 25: 186–215. [Google Scholar] [CrossRef]

- Amponsah-Tawiah, Kwesi, and Justice Mensah. 2015. Exploring the link between Corporate Social Responsibility and health and safety in the mines. Journal of Global Responsibility 6: 65–79. [Google Scholar] [CrossRef]

- Ansu-Mensah, Peter, Emmanuel Opoku Marfo, Lyon Salia Awuah, and Kwame Oduro Amoako. 2021. Corporate social responsibility and stakeholder engagement in Ghana’s mining sector: A case study of Newmont Ahafo mines. International Journal of Corporate Social Responsibility 6: 1. [Google Scholar] [CrossRef]

- Asmeri, Rina, Tika Alvionita, and Ardi Gunardi. 2017. CSR Disclosures in the Mining Industry: Empirical Evidence from Listed Mining Firms in Indonesia. Indonesian Journal of Sustainability Accounting and Management 1: 16–22. [Google Scholar] [CrossRef]

- Bansal, Pratima. 2005. Evolving sustainably: A longitudinal study of corporate sustainable development. Strategic Management Journal 26: 197–218. [Google Scholar] [CrossRef]

- Boiral, Olivier. 2016. Accounting for the Unaccountable: Biodiversity Reporting and Impression Management. Journal of Business Ethics 135: 751–68. [Google Scholar] [CrossRef]

- Carroll, Archie B. 1979. A Three-Dimensional Conceptual Model of Corporate Performance. The Academy of Management Review 4: 497–505. [Google Scholar] [CrossRef]

- Claasen, Cyrlene, and Julia Roloff. 2012. The Link Between Responsibility and Legitimacy: The Case of De Beers in Namibia. Journal of Business Ethics 107: 379–98. [Google Scholar] [CrossRef]

- Coetzee, Charmaine M., and Chris J. van Staden. 2011. Disclosure responses to mining accidents: South African evidence. Accounting Forum 35: 232–46. [Google Scholar] [CrossRef]

- Dashwood, Helvina S. 2013. Sustainable Development and Industry Self-Regulation: Developments in the Global Mining Sector. Business and Society 53: 551–82. [Google Scholar] [CrossRef]

- Deegan, Craig. 2002. Introduction. Accounting, Auditing & Accountability Journal 15: 282–311. [Google Scholar] [CrossRef]

- Deng, Ping. 2012. The Internationalization of Chinese Firms: A Critical Review and Future Research*. International Journal of Management Reviews 14: 408–27. [Google Scholar] [CrossRef]

- Devenin, Veronica, and Constanza Bianchi. 2018. Soccer fields? What for? Effectiveness of corporate social responsibility initiatives in the mining industry. Corporate Social Responsibility and Environmental Management 25: 866–79. [Google Scholar] [CrossRef]

- Dobele, Angela R., Kate Westberg, Marion Steel, and Kris Flowers. 2014. An Examination of Corporate Social Responsibility Implementation and Stakeholder Engagement: A Case Study in the Australian Mining Industry. Business Strategy and the Environment 23: 145–59. [Google Scholar] [CrossRef]

- Donaldson, Thomas, and Lee E. Preston. 1995. The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications. Academy of Management Review 20: 65–91. [Google Scholar] [CrossRef]

- Donato, Helena, and Mariana Donato. 2019. Stages for undertaking a systematic review. Acta Medica Portuguesa 32: 227–35. [Google Scholar] [CrossRef]

- Dong, Shidi, Roger Burritt, and Wei Qian. 2014. Salient stakeholders in corporate social responsibility reporting by Chinese mining and minerals companies. Journal of Cleaner Production 84: 59–69. [Google Scholar] [CrossRef]

- Duarte, Fernanda. 2010. Corporate social responsibility in a Brazilian mining company: “official” and divergent narratives. Social Responsibility Journal 6: 4–17. [Google Scholar] [CrossRef]

- European Commission. 2001. Economic Impact of Occupational Safety and Health in the Member States of the European Union. European Agency for Safety and Health at Work. Available online: https://osha.europa.eu/en/publications/report-economic-impact-occupational-safety-and-health-member-states-european-union/view (accessed on 30 August 2021).

- Fitzpatrick, Patricia, Alberto Fonseca, and Mary Louise McAllister. 2011. From the whitehorse mining initiative towards sustainable mining: Lessons learned. Journal of Cleaner Production 19: 376–84. [Google Scholar] [CrossRef]

- Freeman, R. Edward. 1984. Strategic Management: A Stakeholder Approach. Cambridge: Cambridge University Press. [Google Scholar]

- Freeman, R. Edward, Jeffrey S. Harrison, Andrew C. Wicks, Bidhan Parmar, and Simone de Colle. 2010. Stakeholder Theory: The State of the Art. The Academy of Management Annals 4: 403–45. [Google Scholar] [CrossRef]

- Garriga, Elisabet, and Domenec Melé. 2004. Corporate Social Responsibility Theories: Mapping the Territory. Journal of Business Ethics 53: 51–71. [Google Scholar] [CrossRef]

- Garvin, Theresa, Tara K. McGee, Karen E. Smoyer-Tomic, and Emmanuel Ato Aubynn. 2009. Community-company relations in gold mining in Ghana. Journal of Environmental Management 90: 571–86. [Google Scholar] [CrossRef]

- Gaweł, Ewelina, Anna Jałoszyńska, Mateusz Orłowski, Emilia Ratajczak, Joanna Ratajczak, and Begona Riera. 2015. Corporate social responsibility as an instrument of sustainable development of production enterprises. Management Systems in Production Engineering 3: 152–55. [Google Scholar] [CrossRef]

- Gifford, Blair, and Andrew Kestler. 2008. Toward a theory of local legitimacy by MNEs in developing nations: Newmont mining and health sustainable development in Peru. Journal of International Management 14: 340–52. [Google Scholar] [CrossRef]

- Govindan, Kannan, Devika Kannan, and K. Mandan Shankar. 2014. Evaluating the drivers of corporate social responsibility in the mining industry with multi-criteria approach: A multi-stakeholder perspective. Journal of Cleaner Production 84: 214–32. [Google Scholar] [CrossRef]

- Grácio, Cabrini Maria Cláudia. 2016. Acoplamento bibliográfico e análise de cocitação: Revisão teórico-conceitual. Encontros Bibli 21: 82–99. [Google Scholar] [CrossRef]

- Guz, Aleksander N., and Jeremiah J. Rushchitsky. 2009. Scopus: A system for the evaluation of scientific journals. International Applied Mechanics 45: 351–62. [Google Scholar] [CrossRef]

- Hąbek, Patrycja, and Rodoslaw Wolniak. 2016. Assessing the quality of corporate social responsibility reports: The case of reporting practices in selected European Union member states. Quality and Quantity 50: 399–420. [Google Scholar] [CrossRef] [PubMed]

- Hąbek, Patrycja, Wiltold Biały, and Galina Livenskaya. 2019. Stakeholder engagement in corporate social responsibility reporting. The case of mining companies. Acta Montanistica Slovaca 24: 25–34. Available online: https://actamont.tuke.sk/pdf/2019/n1/3habek.pdf (accessed on 30 August 2021).

- Hirsch, Jorge E. 2005. An index to quantify an individual’s scientific research output. Proceedings of the National Academy of Sciences of the United States of America 102: 16569–72. [Google Scholar] [CrossRef]

- Hopper, Trevor, and Andrew Powell. 1985. Making sense of research into the organizational and social aspects of management accounting: A review of its underlying assumptions. Journal of Management Studies 22: 429–65. [Google Scholar] [CrossRef]

- Horisch, Jacob, R. Edward Freeman, and Stefan Schaltegger. 2014. Applying Stakeholder Theory in Sustainability Management. Organization and Environment 27: 328–46. [Google Scholar] [CrossRef]

- Humphreys, David. 2000. A business perspective on community relations in mining. Resources Policy 26: 127–31. [Google Scholar] [CrossRef]

- ICMM—International Council on Mining and Metals. 2015. Sustainable Development Framework: ICMM Principles. London: International Council on Mining and Metals (ICMM). [Google Scholar]

- Imbun, Benedict Young. 2007. Cannot manage without the ,significant other’: Mining, corporate social responsibility and local communities in Papua New Guinea. Journal of Business Ethics 73: 177–92. [Google Scholar] [CrossRef]

- Jenkins, Heledd. 2004. Responsibility and the Mining Industry. Corporate Social Responsibility and Environmental Management 34: 23–34. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Jonek-Kowalska, Izabela. 2016. Sustainable development as a challenge for polish coal mining enterprises. Zeszyty Naukowe. Organizacja i Zarządzanie/Politechnika Śląska 95: 131–45. [Google Scholar] [CrossRef]

- Jones, Marc T., and Mattheus Haigh. 2007. The Transnational Corporation and New Corporate Citizenship Theory. Journal of Corporate Citizenship 2007: 51–69. [Google Scholar] [CrossRef]

- Kemp, Deanna. 2010. Community Relations in the Global Mining Industry: Exploring the Internal Dimensions of Externally Orientated Work. Corporate Social Responsibility and Environmental Management 17: 1–14. [Google Scholar] [CrossRef]

- Kemp, Deanna, John R. Owen, Nora Gotzmann, and Carol J. Bond. 2011. Just Relations and Company-Community Conflict in Mining. Journal of Business Ethics 101: 93–109. [Google Scholar] [CrossRef]

- Kepore, Kevin P., and Benedict Y. Imbun. 2011. Mining and stakeholder engagement discourse in a Papua New Guinea mine. Corporate Social Responsibility and Environmental Management 18: 220–33. [Google Scholar] [CrossRef]

- Kroon, Nanja, Maria-Ceu Alves, and Isabel Martins. 2021. The Impacts of Emerging Technologies on Accountants’ Role and Skills: Connecting to Open Innovation—A Systematic Literature Review. Journal of Open Innovation: Technology, Market, and Complexity 7: 163. [Google Scholar] [CrossRef]

- Liberati, Alessandro, Douglas G. Altman, Jennifer Tetzlaff, Cynthia Mulrow, Peter C. Gøtzsche, John P. A. Ioannidis, Mike Clarke, Philip J. Devereaux, Jos Kleijnen, and David Moher. 2009. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate health care interventions: Explanation and elaboration. Journal of Clinical Epidemiology 62: e1–e34. [Google Scholar] [CrossRef]

- Lopez-Morales, Jose Satsumi. 2018. Multilatinas: A systematic literature review. Review of International Business and Strategy 28: 331–57. [Google Scholar] [CrossRef]

- Lorenc, Sylwia, and Olena Sorokina. 2015. Sustainable development of mining enterprises as a strategic direction of growth of value for stakeholders. Mining Science 22: 67–78. [Google Scholar] [CrossRef]

- Magness, Vanessa. 2006. Strategic posture, financial performance and environmental disclosure: An empirical test of legitimacy theory. Accounting. Auditing and Accountability Journal 19: 540–63. [Google Scholar] [CrossRef]

- Magness, Vanessa. 2008. Who are the stakeholders now? An empirical examination of the Mitchell, Agle, and Wood theory of stakeholder salience. Journal of Business Ethics 83: 177–92. [Google Scholar] [CrossRef]

- Mallett, Richard, Jessica Hagen-Zanker, Rachel Slater, and Maren Duvendack. 2012. The benefits and challenges of using systematic reviews in international development research. Journal of Development Effectiveness 4: 445–55. [Google Scholar] [CrossRef]

- Matikainen, Lotta Sihvo. 2022. Addressing Sustainability in the Mining Industry Through Stakeholder Engagement. South Asian Journal of Business and Management Cases 11: 35–48. [Google Scholar] [CrossRef]

- Matten, Dirk, and Andrew Crane. 2005. Corporate Citizenship: Toward an Extended Theoretical Conceptualization. The Academy of Management Review 30: 166–79. [Google Scholar] [CrossRef]

- McDonald, Sharyn, and Suzanne Young. 2012. Cross-sector collaboration shaping Corporate Social Responsibility best practice within the mining industry. Journal of Cleaner Production 37: 54–67. [Google Scholar] [CrossRef]

- Melé, Domenèc. 2009. Corporate Social Responsibility Theories. In The Oxford Handbook of Corporate Social Responsibility. Oxford: Oxford University Press, pp. 47–82. [Google Scholar] [CrossRef]

- Moomen, Abdul-Wadood, and Ashraf Dewan. 2017. Probing the Perspectives of Stakeholder Engagement and Resistance Against Large-Scale Surface Mining in Developing Countries. Corporate Social Responsibility and Environmental Management 24: 85–95. [Google Scholar] [CrossRef]

- Morales, Osvaldo, Andrew N. Kleit, and Gareth H. Rees. 2018. Mining and community relations in Peru: Can agreement be reached? Academia Revista Latinoamericana de Administracion 31: 605–24. [Google Scholar] [CrossRef]

- Mutti, Diana, Natalia Yakovleva, Diego Vazquez-Brust, and Martín H. Di Marco. 2012. Corporate social responsibility in the mining industry: Perspectives from stakeholder groups in Argentina. Resources Policy 37: 212–22. [Google Scholar] [CrossRef]

- Mzembe, Andrew Ngawenja. 2016. Doing Stakeholder Engagement Their Own Way: Experience from the Malawian Mining Industry. Corporate Social Responsibility and Environmental Management 23: 1–14. [Google Scholar] [CrossRef]

- Mzembe, Andrew Ngawenja, and Julia Meaton. 2014. Driving Corporate Social Responsibility in the Malawian Mining Industry: A Stakeholder Perspective. Corporate Social Responsibility and Environmental Management 21: 189–201. [Google Scholar] [CrossRef]

- O’Dwyer, Brendan. 2002. Managerial perceptions of corporate social disclosure: An Irish story. Accounting, Auditing and Accountability Journal 15: 406–36. [Google Scholar] [CrossRef]

- Orlikowski, Wanda J., and Jack J. Baroudi. 1991. Studying Information Technology in Organizations: Research Approaches and Assumptions. Information Systems Research 2: 1–28. [Google Scholar] [CrossRef]

- Owen, John R., and Deanna Kemp. 2012. Assets, Capitals, and Resources: Frameworks for Corporate Community Development in Mining. Business and Society 51: 382–408. [Google Scholar] [CrossRef]

- Pfajfar, Gregor, Aviv Shoham, Agnieszka Małecka, and Maja Zalaznik. 2022. Value of corporate social responsibility for multiple stakeholders and social impact—Relationship marketing perspective. Journal of Business Research 143: 46–61. [Google Scholar] [CrossRef]

- Pons, Adria, Carla Vintrò, Josep Rius, and Jordi Vilaplana. 2021. Impact of Corporate Social Responsibility in mining industries. Resources Policy 72: 102117. [Google Scholar] [CrossRef]

- Ranängen, Helena, and Åsa Lindman. 2018. Exploring corporate social responsibility practice versus stakeholder interests in Nordic mining. Journal of Cleaner Production 197: 668–77. [Google Scholar] [CrossRef]

- Ranängen, Helena, and Thomas Zobel. 2014. Revisiting the “how” of corporate social responsibility in extractive industries and forestry. Journal of Cleaner Production 84: 299–312. [Google Scholar] [CrossRef]

- Raufflet, Emmanuel, Luciano Barin Cruz, and Luc Bres. 2014. An assessment of corporate social responsibility practices in the mining and oil and gas industries. Journal of Cleaner Production 84: 256–70. [Google Scholar] [CrossRef]

- Rodrigues, Margarida, and Luis Mendes. 2018. Mapping of the literature on social responsibility in the mining industry: A systematic literature review. Journal of Cleaner Production 181: 88–101. [Google Scholar] [CrossRef]

- Rodrigues, Margarida, Maria do Céu Alves, Cidália Oliveira, Vera Vale, José Vale, and Rui Silva. 2021. Dissemination of Social Accounting Information: A Bibliometric Review. Economies 9: 41. [Google Scholar] [CrossRef]

- Ross, Stephen A. 1973. The Economic Theory of Agency: The Principal’s Problem. The American Economic Review 63: 134–39. [Google Scholar]

- Rowley, Jennifer, and Frances Slack. 2004. Conducting a literature review. Management Research News 27: 31–39. [Google Scholar] [CrossRef]

- Saenz, Cesar. 2019. Creating shared value using materiality analysis: Strategies from the mining industry. Corporate Social Responsibility and Environmental Management 26: 1351–60. [Google Scholar] [CrossRef]

- Segura-Salazar, Juliana, and Luis Marcelo Tavares. 2018. Sustainability in the Minerals Industry: Seeking a Consensus on Its Meaning. Sustainability 10: 1429. [Google Scholar] [CrossRef]

- Selmier, W. Travis, and Aloysius Newenham-Kahindi. 2017. Under African skies-Mining TNCs in Africa and the sustainable development goals. Transnational Corporations 24: 119–33. [Google Scholar] [CrossRef]

- Sethi, S. Prakash, Terrence F. Martell, and Mert Demir. 2016. Building Corporate Reputation Through Corporate Social Responsibility (CSR) Reports: The Case of Extractive Industries. Corporate Reputation Review 19: 219–43. [Google Scholar] [CrossRef]

- Sharma, Deepankar, and Priya Bhatnagar. 2015. Corporate social responsibility of mining industries. International Journal of Law and Management 57: 367–72. [Google Scholar] [CrossRef]

- Song, Baobao, and Jing Taylor Wen. 2020. Online corporate social responsibility communication strategies and stakeholder engagements: A comparison of controversial versus noncontroversial industries. Corporate Social Responsibility and Environmental Management 27: 881–96. [Google Scholar] [CrossRef]

- Strand, Robert, R. Edward Freeman, and Kai Hockerts. 2015. Corporate Social Responsibility and Sustainability in Scandinavia: An Overview. Journal of Business Ethics 127: 1–15. [Google Scholar] [CrossRef]

- Sutantoputra, Aries. 2022. Do stakeholders’ demands matter in environmental disclosure practices? Evidence from Australia. Journal of Management and Governance 26: 449–78. [Google Scholar] [CrossRef]

- Turker, Duygu. 2009. Measuring corporate social responsibility: A scale development study. Journal of Business Ethics 85: 411–27. [Google Scholar] [CrossRef]

- Ventura, Jose, and Cesar Sandro Saenz. 2015. Beyond corporate social responsibility. Towards a model for managing sustainable mining operations, Qualitative research based upon best practices. Social Responsibility Journal 11: 605–21. [Google Scholar] [CrossRef]

- Vintró, Carla, Luis Sanmiquel, and Modesto Freijo. 2014. Environmental sustainability in the mining sector: Evidence from Catalan companies. Journal of Cleaner Production 84: 155–63. [Google Scholar] [CrossRef]

- Viveros, Hector. 2016. Examining Stakeholders’ Perceptions of Mining Impacts and Corporate Social Responsibility. Corporate Social Responsibility and Environmental Management 23: 50–64. [Google Scholar] [CrossRef]

- Wood, Donna J. 1991. Corporate Social Performance Revisited. The Academy of Management Review 16: 691–718. [Google Scholar] [CrossRef]

- Wozniak, Justyna, and Weronika Jurczyk. 2022. SLO in CSR perspective—A comparative case study from Poland (2018–2020). Resources Policy 77: 102654. [Google Scholar] [CrossRef]

- Yakovleva, Natalia, and Diego Vazquez-Brust. 2012. Stakeholder Perspectives on CSR of Mining MNCs in Argentina. Journal of Business Ethics 106: 191–211. [Google Scholar] [CrossRef]

- Yang, Xiaohua, and Cheryl Rivers. 2009. Antecedents of CSR practices in MNCs’ subsidiaries: A stakeholder and institutional perspective. Journal of Business Ethics 86: 155–69. [Google Scholar] [CrossRef]

- Yang, Yu, and Dongjing Chen. 2022. Issues of corporate social responsibility in the mining industry: The case of China. Resources Policy 76: 102648. [Google Scholar] [CrossRef]

- Yin, Robert K. 2015. Case Study Research: Design and Methods—Applied Social Research Methods Series, 6th ed. Thousand Oaks: Sage Publications, Inc. [Google Scholar]

- Yudarwati, Gregoria Arum, and Fandy Tjiptono. 2017. An enactment theory perspective of corporate social responsibility and public relations. Marketing Intelligence & Planning 35: 626–40. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Items | |

|---|---|

| Eligibility Criteria 1 | |

| Period: | No chronological filter |

| Online databases | WoS (Web of Science) and Scopus |

| Keywords: | (“social responsibility” and “stakeholders” and “mining industry”) |

| Systematisation by category: | BUSINESS OR MANAGEMENT OR BUSINESS FINANCE OR MINING MINERAL PROCESSING |

| Systematisation by type of document: | Articles and Review |

| Language: | English |

| Eligibility Criterion 2 | |

| Keywords: | Only articles whose keywords include the exact search term were selected |

| Authors | Keywords | Goal | Theory Used | Type of Study | Methodology | Research Paradigm |

|---|---|---|---|---|---|---|

| 1. Magness (2006) | Social responsibility, Accounting, Mining industry, Financial performance, Disclosure, Canada | Examine the reactions of stakeholders when accidents occur. | Stakeholders Theory | Empirical | Quantitative | Positivism |

| 2. Magness (2008) | Stakeholder theory, corporate social responsibility, legitimacy perspective | To test Ullmann’s hypothesis in light of stakeholders and inherent disclosure of social responsibility reports. | Legitimacy Theory | Empirical | Quantitative | Positivism |

| 3. Kemp (2010) | stakeholder engagement, community relations, mining, sustainable development; corporate social responsibility, public relations, community development | Exploration of a conceptual and pedagogical framework for community-business interaction, with distinct constructs. | Does not mention | Empirical | Qualitative | Interpretivism |

| 4. Yakovleva and Vazquez-Brust (2012) | Corporate social responsibility, Corporate social responsibility orientation, Mining Stakeholders | Investigate the conceptualisation of corporate social responsibility in the context of multinationals in Argentina. | Stakeholders Theory | Empirical | Quantitative | Positivism |

| 5. Mzembe and Meaton (2014) | Corporate social responsibility (CSR), Malawi, mining, sustainable development, stakeholder engagement | To examine the predictors of the corporate social responsibility agenda pursued by Paladin (Africa), a subsidiary of an Australian multinational mining company, operator of the first uranium mine in Malawi. | Stakeholders Theory | Empirical | Qualitative | Interpretivism |

| 6. Dong et al. (2014) | China Mining and Minerals Industry, CSR, Reports, Stakeholder, Theory Stakeholder Salience | To investigate the influence of key stakeholder groups on CSR disclosure in mining and mineral companies in China. | Stakeholders Theory | Empirical | Quantitative | Positivism |

| 7. Dobele et al. (2014) | Corporate social responsibility, mining, environment, stakeholder engagement, case study | To explore the efforts of a company in a sector with significant environmental impacts to implement a socially responsible way of operating and associated actions. | Stakeholders Theory | Empirical | Qualitative | Interpretivism |

| 8. McDonald and Young (2012) | Corporate social responsibility, cross-sector collaboration, Environmental partnerships, Nonprofits | To explore the 30-year journey undertaken by the giant mining company Alcoa of Australia’ in terms of its approach to social and environmental issues. | Legitimacy Theory | Empirical | Qualitative | Interpretivism |

| 9. Fitzpatrick et al. (2011) | Sustainability, Policy, Learning, Mining Association of Canada, Mining, minerals | Investigation of changes in the sustainable development approach undertaken by the Mining Association of Canada over a 20-year period. | Does not mention | Empirical | Qualitative | Interpretivism |

| 10. Viveros (2016) | Corporate social responsibility; sustainable development; stakeholder engagement; stakeholder perceptions; mining; Chile | Provide a better understanding of the perceptions of multiple stakeholders on CSR. | Legitimacy Theory, Stakeholders Theory | Empirical | Qualitative | Interpretivism |

| 11. Kepore and Imbun (2011) | Community engagement discourse; corporate social responsibility; environmental impact; indigenous local communities; multinational mining companies | Assessment of the effectiveness of voluntary social responsibility in Papua New Guinea. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| 12. Coetzee and van Staden (2011) | Safety, disclosure Social, responsibility, Mining Accidents, Legitimacy Stakeholder theory | Observation of safety disclosures in annual sustainability reports and corporate lobbying in mining industries. | Media-agenda Theory, Legitimacy Theory, Stakeholders Theory | Empirical | Quantitative | Positivism |

| 13. Mzembe (2016) | Corporate social responsibility; Malawi; mining; stakeholder engagement; sustainable development | To test stakeholders’ perspectives on responses to shareholder requests for accountability in developing countries in mining companies. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| 14. Rodrigues and Mendes (2018) | Corporate social responsibility, Mining industry, Bibliometric analysis, Systematic literature review, Content analysis | To identify the most researched topics in academia on social responsibility in mining operations, from 1998 to 2017, through a bibliometric review. | Stakeholder Theory, Legitimacy Theory | Theoretical | Qualitative | Interpretivism |

| 15. Song and Wen (2020) | Communication strategy, controversial industry, corporate social responsibility, social media, stakeholder engagement | This study attempts to reveal the corporate social responsibility (CSR) programming and communication strategies of companies from controversial versus noncontroversial industry sectors and stakeholders’ responses to these online CSR communications. | Stakeholder Theory | Empirical | Quantitative | Positivism |

| 16. Ranängen and Zobel (2014) | CSR, sustainability management systems, ISSO 26000, stakeholder management, mining industry | Obtain evidence on whether the adoption of integrated management systems is useful for putting stakeholder management into practice. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| 17. Asmeri et al. (2017) | Corporate social responsibility disclosure, profitability, environmental performance, Indonesia. | To obtain empirical evidence on the effect of profitability and environmental performance on corporate social responsibility disclosure. | Legitimacy Theory | Empirical | Quantitative | Positivism |

| 18. Adler et al. (2017) | Biodiversity, Disclosure, Mining, Reporting, Environment, Australia | To explore the practices and trends in the biodiversity reporting of the top 50 Australian mining companies before and after the United Nations declared the period 2011–2020 as the “Decade of Biodiversity. | Legitimacy Theory | Empirical | Qualitative | Interpretivism |

| 19. Pons et al. (2021) | CSR, Mining, Twitter, Big data, Sentiment analysis | This paper aims to examine CSR communication in the mining sector on Twitter and identify the main topics of CSR and the main participants in the creation of content. | Dialogic theory of public relations | Empirical | Quantitative | Positivism |

| 20. Amoako et al. (2017) | Mining industry, Content analysis, Sustainability reporting, Mining plants, Triple bottom line reporting, Website reporting | Identify and account for the content of sustainability reports disclosed by the mining industry. | Institutional isomorphism | Empirical | Qualitative | Interpretivism |

| 21. Selmier and Newenham-Kahindi (2017) | Corporate social responsibility, Sustainable Development Goals, mining industry, business ethics, Africa, communities as stakeholders. | Illustration of the progress of the problems of two mining multinationals in Africa. | Does not mention | Empirical | Qualitative | Interpretivism |

| 22. Sutantoputra (2022) | Environmental reporting, Environmental disclosure, Environmental performance, Stakeholder management, Australia | This exploratory qualitative study investigates the possible reasons for the environmental disclosures of nine companies listed in the top 200 Australian Securities Exchange (ASX) companies. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| 23. Devenin and Bianchi (2018) | Collaborative adaptive management, copper mining, corporate social responsibility, effectiveness, legitimacy, stakeholder engagement | To examine the perceptions of stakeholders in the mining sector concerning intended results from social responsibility initiatives. | Legitimacy Theory, Stakeholders Theory | Empirical | Qualitative | Interpretivism |

| 24. Lorenc and Sorokina (2015) | Sustainable development (SD), corporate social responsibility (CSR), value of mining enterprise | Discussion of the concept of sustainable development and the need for its implementation in the mining industries. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| 25. Duarte (2010) | Corporate image, Social responsibility, Organisational culture, Mining industry, Brazil | Study two distinct narratives about social responsibility in Brazil | Does not mention | Empirical | Qualitative | Interpretivism |

| 26. Yudarwati and Tjiptono (2017) | Corporate Social Responsibility, Public Relations, enactment theory, mining industry, community, Indonesia | Gauging on: (1) how companies perceive Corporate Social Responsibility and Public Relations; (2) how companies perceive the interconnectedness between these functions; and (3) what factors contribute to their perceptions. | Enactment Theory | Empirical | Qualitative | Interpretivism |

| 27. Ranängen and Lindman (2018) | Mining, Corporate sustainability, CSR, Corporate social responsibility, Stakeholder interests, Social licence to operate | Study the Nordic mining industry and its stakeholders to find out whether their interests are taken into account. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| 28. Amponsah-Tawiah and Mensah (2015) | Social Responsibility, mining | To conclude about the meaning of the concept of social responsibility to stakeholders in Ghana’s mining industries and whether there is a link between social responsibility and health and safety. | Social License Theory | Empirical | Qualitative | Interpretivism |

| 29. Morales et al. (2018) | Social conflict, Culture, Mining, Corporate social responsibility, Peru, Foreign direct investment | Presentation of a country’s mixed history of colonialism and cultural heritage as a backdrop for managing community engagement in a mining company. | Does not mention | Empirical | Qualitative | Interpretivism |

| 30. Hąbek et al. (2019) | Corporate social responsibility, stakeholders, CSR report, communication, mining industry | Assess how stakeholders are involved in the process of disclosure of social responsibility reports in the mining industry. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| 31. Saenz (2019) | Creating shared value, materiality, mining, social responsibility, strategy | Explain how the material issues of the mining industry are intertwined with issues of social responsibility and co-shared value creation. | Stakeholder Theory | Empirical | Qualitative | Interpretivism |

| Authors | Conclusions | Limitations | Future Clues |

|---|---|---|---|

| Magness (2006) | Faced with the occurrence of accidents, the responses of company executives were quicker than those of shareholders. On the other hand, accidents led to increased disclosure of social responsibility practices | n.a. | n.a. |

| Magness (2008) | Companies that use press-release disclose more information than others, but there is no evidence that the content of the information disclosed is mediated by financial performance. | No assessment of social performance; The press release is just one form of strategic posture | Use of other measures that provide something more about the decision-making process. |

| Kemp (2010) | Conceptually, community relations must be dissociated from public relations in order to have strength as an area of professional work | n.a. | n.a. |

| Yakovleva and Vazquez-Brust (2012) | The analysis suggested that environmental obligations are the critical element of social responsibility in Argentina’s mining sector | Not all stakeholders were interviewed | Study social responsibility strategies, stakeholder engagement, social performance, corporate image and why conflicts differ between domestic and foreign companies |

| Mzembe and Meaton (2014) | The social responsibility agenda in the mining sector in Malawi is strongly influenced by externally generated pressures, such as civil society organisation activism and community expectations; although it is clear that other factors, such as public and private regulations and pressure from financial markets, also play a role in coercing Paladin to adopt a social responsibility agenda | Single case study, which does not allow the generalisation of the results; | Empirical studies at the remaining Paladin energy subsidiaries. |

| Dong et al. (2014) | In addition to local government, key stakeholders have a significant impact on reporting disclosure in China, specifically foreign stakeholders over domestic stakeholders | Failure to take into account possible conflicts between stakeholders. Short time coverage (4 years); Non-generalisation of results | Filling of the abovementioned limitations |

| Dobele et al. (2014) | The results highlight that managers committed to social responsibility, play a crucial role in guiding operations in a socially responsible manner. | n.a. | More studies are still needed on the extensions of the social responsibility model; Explore how managers’ personal traits affect the success of social responsibility initiatives. |

| McDonald and Young (2012) | Identification of a successful and long-term environmental partnership; highlighting the role of employees in achieving legitimacy; there is a positive effect of the evaluation of social practices | n.a. | n.a. |

| Fitzpatrick et al. (2011) | Recognition of the importance of sustainability of mining companies in Canada | n.a. | |

| Viveros (2016) | The results reveal that shareholders perceive negative social and environmental impacts in contrast to positive perception about economic impacts. Corporate social responsibility is addressed in terms of social and environmental responsibilities but is also perceived negatively as mere rhetoric or simply as a marketing campaign. These perceptions reflect an anti-trade-off sentiment, revealing that CSR cannot be used as a tool to offset the negative impacts of mining. | A single case study in Chile; Heterogeneity of communities with different cultures; | Replication of studies in other geographical contexts (Argentina, Peru), in the same sector and in different sectors; Control the cultural heterogeneity of communities |

| Kepore and Imbun (2011) | Importance of communities as a vehicle, particularly to facilitate socially responsible actions | n.a. | n.a. |

| Coetzee and van Staden (2011) | Organisations show reactive attitudes to threats to their perceived legitimacy. Thus, there is an increase in the disclosure of data on safety in the mining industry after the accidents, so that there is no loss of legitimacy in the eyes of stakeholders | Small sample size; Non-generalization of results; No consideration of information additional to that disclosed on the websites; | Increase the sample size by using other companies with a similar reputation to those of this study; Use of other available information; |

| Mzembe (2016) | More attention needs to be paid to factors specific to business, community and civil society if there is an effective engagement of mining industry stakeholders in developing countries. | Single case study (Malawi); Non-generalization of results; | Studies at other Ashford’s subsidiary mines to conduct a comparative investigation. |

| Rodrigues and Mendes (2018) | Identifies two main lines of research: (i) relationships with local communities and (ii) CSR reporting. | Use of the WoS database only | A social network analysis would be a promising approach to studying collaborative and multilevel governance configurations due to its ability to understand structural patterns of stakeholders, thus allowing to address research questions that cannot be adequately explored through traditional stakeholder analysis. |

| Song and Wen (2020) | Generally, various CSR communication strategies are not strongly associated with the volume of stakeholder comments but the valences of their attitudes. Specifically, CSR videos that (a) use an information strategy, (b) take a company-dominant perspective, and (c) describe high fit CSR programs are more likely to receive negative and skeptical comments. | Although the purposive sampling procedure was carried out properly and the researchers had reliable coding, it is necessary to point out certain limitations of the study. | Future research can examine different platforms to determine how messages fit in with the company’s social media repertoire as well as their entire communications program. A more comprehensive analysis of the entire organizational picture would truly reveal insights into how a company communicates its CSR programs. |

| Ranängen and Zobel (2014) | Certified tools can be effective in implementing social responsibility management, although they do not cover all operational issues and fair practices with the surrounding community | Use of ISSO 26000; The interviewees were only in strategic roles; Difficulty in obtaining documentation from subsidiaries | n.a. |

| Asmeri et al. (2017) | Environmental performance is a determinant of the degree of social responsibility disclosure in Indonesia, and this is a way to gain organisational legitimacy. | Use of only annual social responsibility disclosure reports | Use of other types of media |

| Adler et al. (2017) | The aggregate reporting typically conducted by the mining industry produces obscure information that is not useful to stakeholders affected by their activities or to policymakers responsible for protecting and maintaining the world’s biodiversity. | Focus on voluntary disclosures; | n.a. |

| Pons et al. (2021) | The results show the CSR debate is increasingly growing in developing countries and in countries with a bad reputation of environmental and health mining conditions. | Our research has some practical limitations, since it only considered the Tweets collected within a specific period of time and the Tweets written in English and Spanish. | it would be interesting for further research to include more languages and more filters in order to extend the list of initial words to search within the Tweets. |

| Amoako et al. (2017) | Sustainability reports are scarce in financial information; in addition, there is no similarity between the contents. Thus, standardised templates are needed to see improvements. | The theoretical framework (coercive isomorphic pressure) is vulnerable to misinterpretation. | Empirical on-site study to understand the disparities in the reports; Understand why extractive industry reports are produced, how and by whom they are used, and how they should be improved. |

| Selmier and Newenham-Kahindi (2017) | Many improvements are needed for the industries in Minas Gerais to reach the desirable level of social responsibility and legitimacy | n.a. | n.a. |

| Sutantoputra (2022) | The fndings in this study have revealed that the frms attempted to address the issues of concern from their stakeholders. Although it is impossible for frms to be responsible for all environmental issues, the companies could be seen to be responsible for minimizing and rectifying the environmental problems that they have caused directly from their operations and that indirectly relate to their business operations and products | The small sample size in this study should be taken into account in generalizing the disclosure behaviours of firms in Australia. | Perform further case study analysis on an industry-specifc basis. |

| Devenin and Bianchi (2018) | The results show three ineffective situations that emerged from empirical contrasts of social responsibility initiatives declared by industries in sustainability reports and the real impact on beneficiaries in the communities, which are: (1) failure of initiatives to contribute to the real needs of beneficiaries in the community; (2) failure of initiatives adjusted to the socio-cultural characteristics of the beneficiary group; and (3) failure of initiatives to ensure long-term sustainability. | Analysis of only companies located in Chile and Australia; Some interviewees from the companies were also part of the local community | Replication of the study in other geographical contexts; Inclusion of other mining industries, particularly those in natural resources; |

| Lorenc and Sorokina (2015) | Mining companies should focus on seeking economic benefits in their operations without neglecting social and environmental issues. | n.a. | n.a. |

| Duarte (2010) | The study revealed that the official narrative emerging from the key informant’s ‘corporate performances’ was consistently positive. The divergent narrative portrayed the company negatively and was revealed through web searches and further reflection in the post-fieldwork period. | The selection of participants was not fully controlled by the investigator | n.a. |

| Yudarwati and Tjiptono (2017) | Social responsibility and public relations are perceived as forms of community relations to obtain and maintain organisational legitimacy from communities and shareholders. Three factors shape these forms: (1) social and political changes in Indonesia, (2) the collective culture of communities, and (3) the nature of the mining industry. | Only focused on companies and their organisational environment | More studies with communities and other stakeholders for the understanding of their interpretation about the company: Replication of the study in other sectors of activity |

| Ranängen and Lindman (2018) | The practice of social responsibility fulfils to some extent the interests of stakeholders. However, the sustainable use of resources and other components still need improvements at the legal level. | n.a. | Continued studies on this topic, based on the argument that creating value for stakeholders is important for the social license to operate. |

| Amponsah-Tawiah and Mensah (2015) | Most mines operating in Ghana are beginning to commit to social responsibility and some programs have already outlined with the community. However, it is important to have a balance between the internal and external dimensions of social responsibility. | Semi-structured interviews, which may have promoted consistency of responses; Different responses on some issues by different stakeholders | Conducting an empirical study on the mediation of social responsibility in employees’ perceptions of quality of life, health, safety and well-being. |

| Morales et al. (2018) | Conflict in mining industries is a complex issue and a strategic problem that requires an analysis of causal variables and a deeper understanding of underlying historical and cultural forces. The transactional responses of community engagement are not always adequate to maintain the social license of a mining project. | n.a. | n.a. |

| Hąbek et al. (2019) | The involvement of stakeholders in the preparation of social responsibility reports is positive since it opens space for their improvement. However, the feedback mechanism is still underused. | Immense unavailability of data; Heterogeneity of the content and format of reports; | Analyse the stakeholder groups taking into account the cultural context of the reporting companies. |

| Saenz (2019) | It points out which strategies for creating shared value can be used given materiality in the mining industry as an aid for managers to identify priority social issues and the correct allocation of resources to them. | Survey only focused on one sector of activity; | Identify other strategies with other theoretical frameworks (e.g., bottom-of-the-pyramid theory or triple-bottom-line theory); Extend research to other sectors of activity |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rodrigues, M.; Alves, M.-C.; Silva, R.; Oliveira, C. Mapping the Literature on Social Responsibility and Stakeholders’ Pressures in the Mining Industry. J. Risk Financial Manag. 2022, 15, 425. https://doi.org/10.3390/jrfm15100425

Rodrigues M, Alves M-C, Silva R, Oliveira C. Mapping the Literature on Social Responsibility and Stakeholders’ Pressures in the Mining Industry. Journal of Risk and Financial Management. 2022; 15(10):425. https://doi.org/10.3390/jrfm15100425

Chicago/Turabian StyleRodrigues, Margarida, Maria-Ceu Alves, Rui Silva, and Cidália Oliveira. 2022. "Mapping the Literature on Social Responsibility and Stakeholders’ Pressures in the Mining Industry" Journal of Risk and Financial Management 15, no. 10: 425. https://doi.org/10.3390/jrfm15100425

APA StyleRodrigues, M., Alves, M.-C., Silva, R., & Oliveira, C. (2022). Mapping the Literature on Social Responsibility and Stakeholders’ Pressures in the Mining Industry. Journal of Risk and Financial Management, 15(10), 425. https://doi.org/10.3390/jrfm15100425