Evidence of Economic Policy Uncertainty and COVID-19 Pandemic on Global Stock Returns

Abstract

:1. Introduction

2. Literature Review

3. Data

4. Research Methodology

5. Empirical Evidence

5.1. Impact of EPU on Stock Returns

5.2. Impact of the COVID-19 Pandemic

5.3. Nonlinear Estimations

- (i)

- Uncertainty premium hypothesis—A rise in has a negative effect on stock returns, that is, which implies = , where . This expression suggests that some investors tend to sell off stocks as higher uncertainty hits market; this selloff will lead current stock prices to fall, which is reflected by a negative sign of . < 0; however, a market rebound will result in .

- (ii)

- COVID-19 uncertainty hypothesis—Increased spread of COVID-19 will provoke fears in investors, leading to a decline in stock returns. That is, < 0, which is a direct effect from

- (iii)

- Interactive uncertainty hypothesis—A rise in COVID-19 from the last period will induce uncertainty, exacerbating the current level of EPU, which will produce more uncertainty about the direction of stock returns; thus, the constitutes an indirect negative effect, that is < 0.

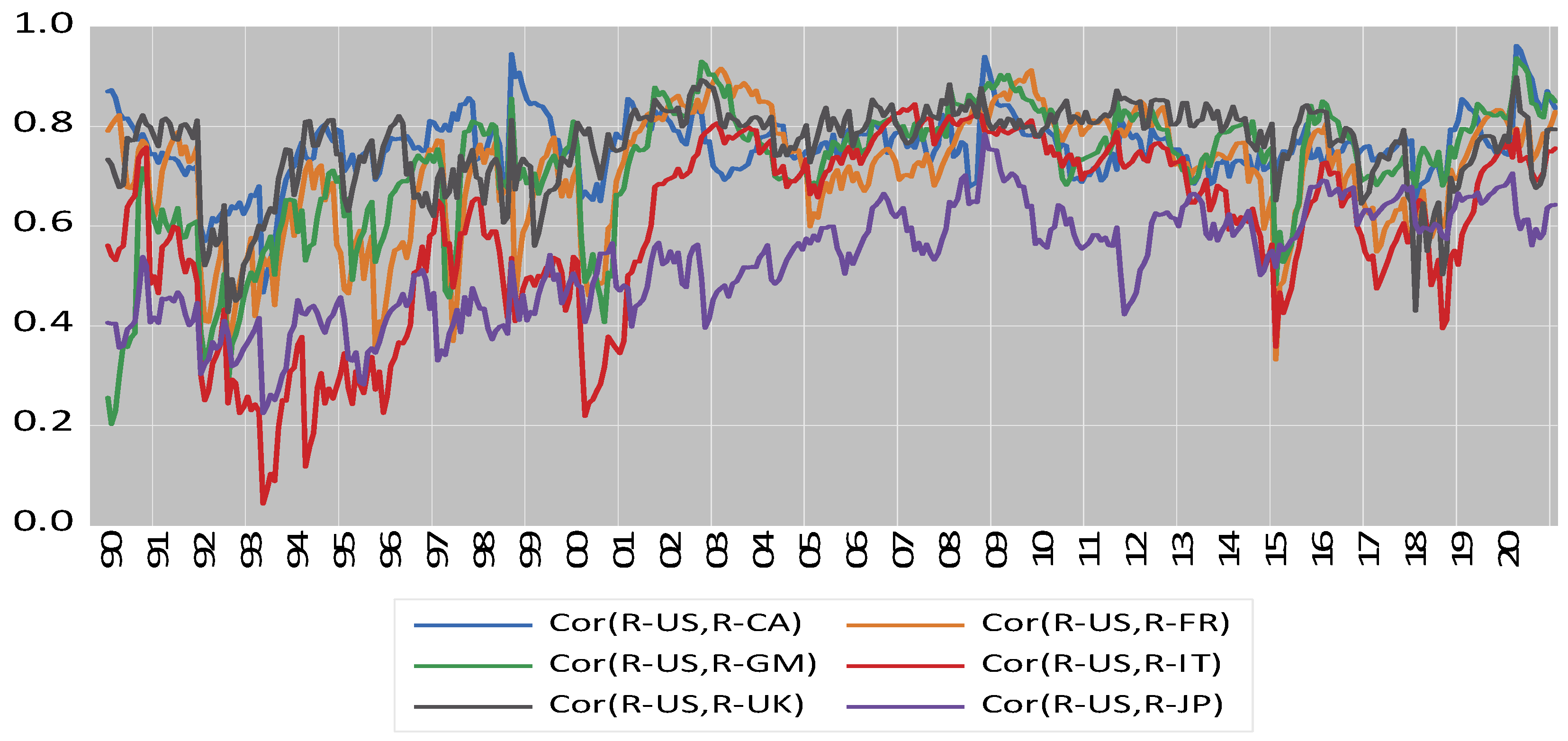

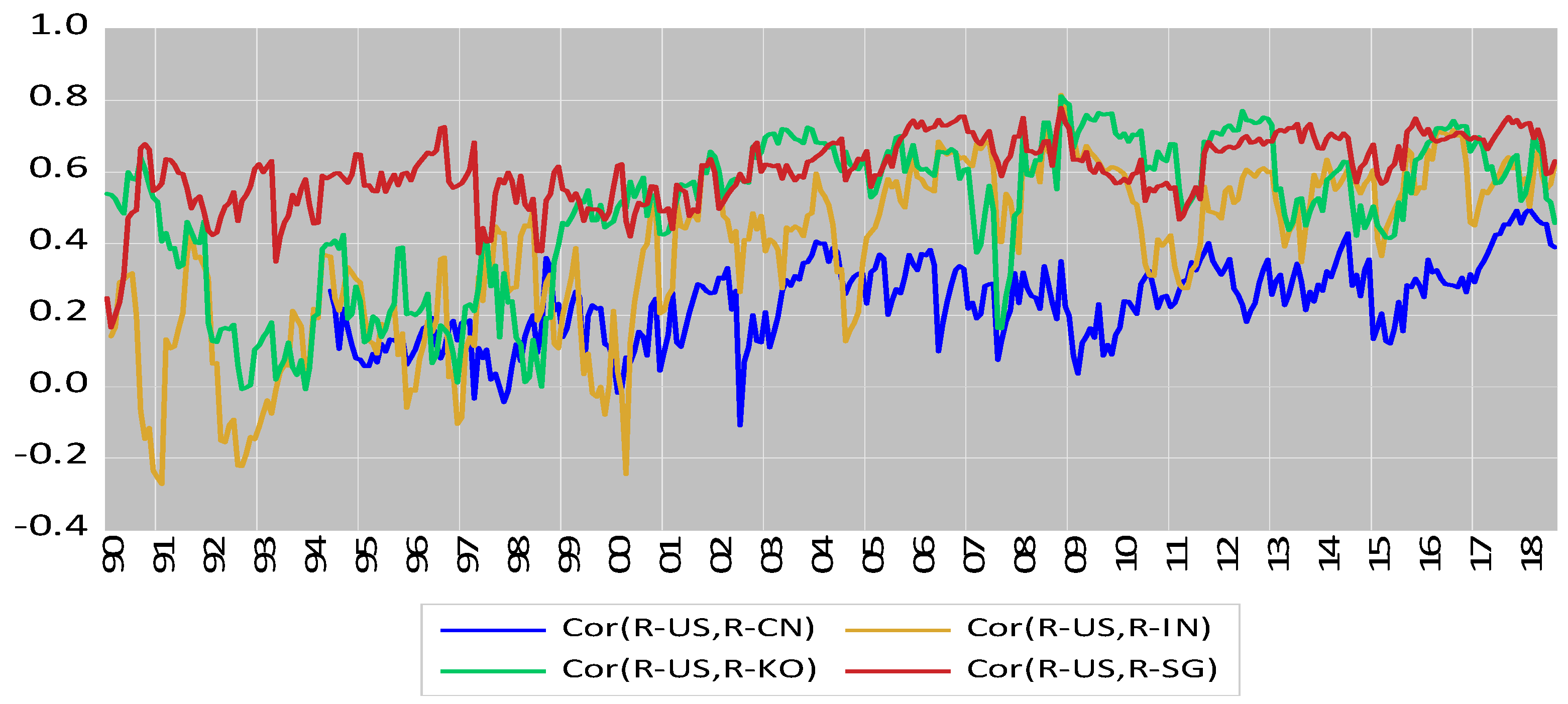

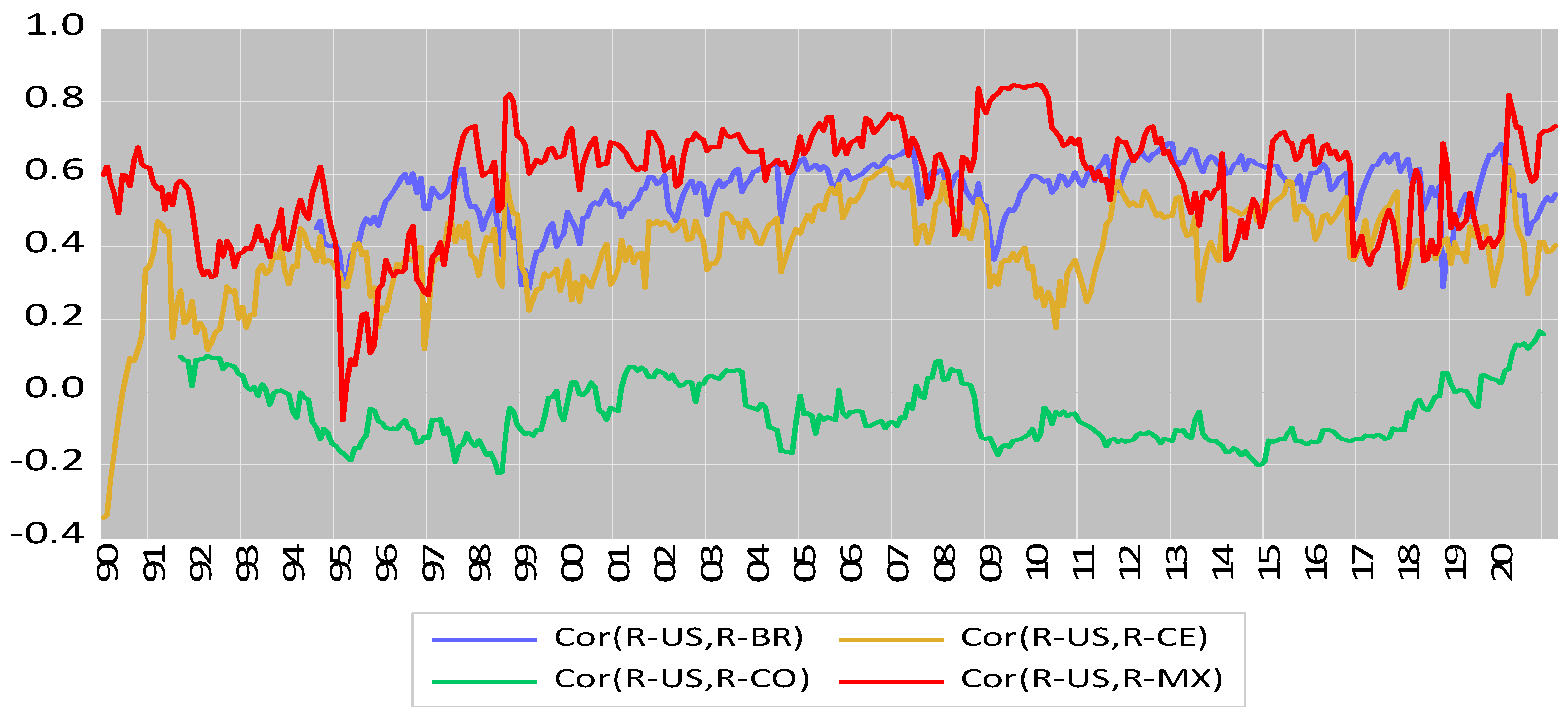

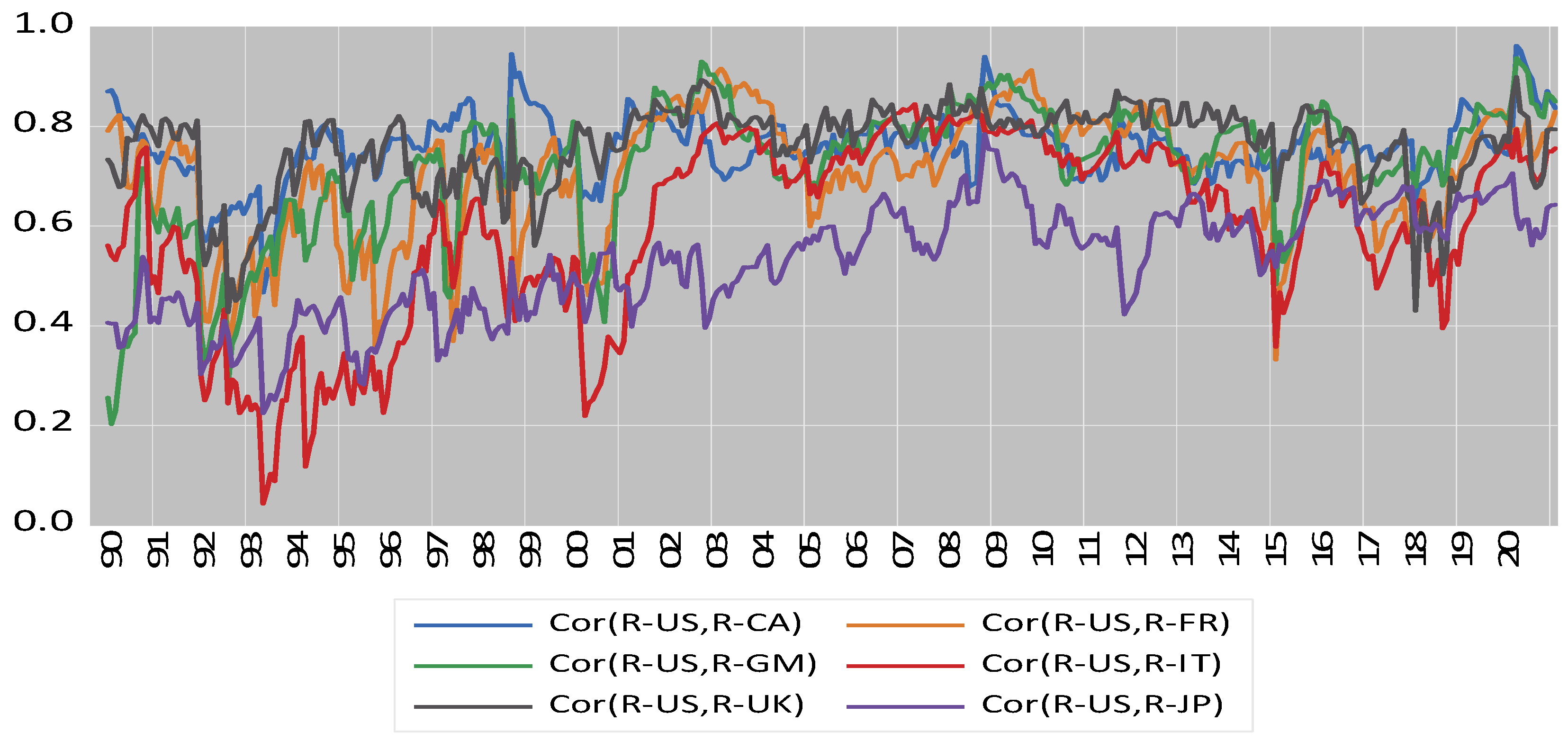

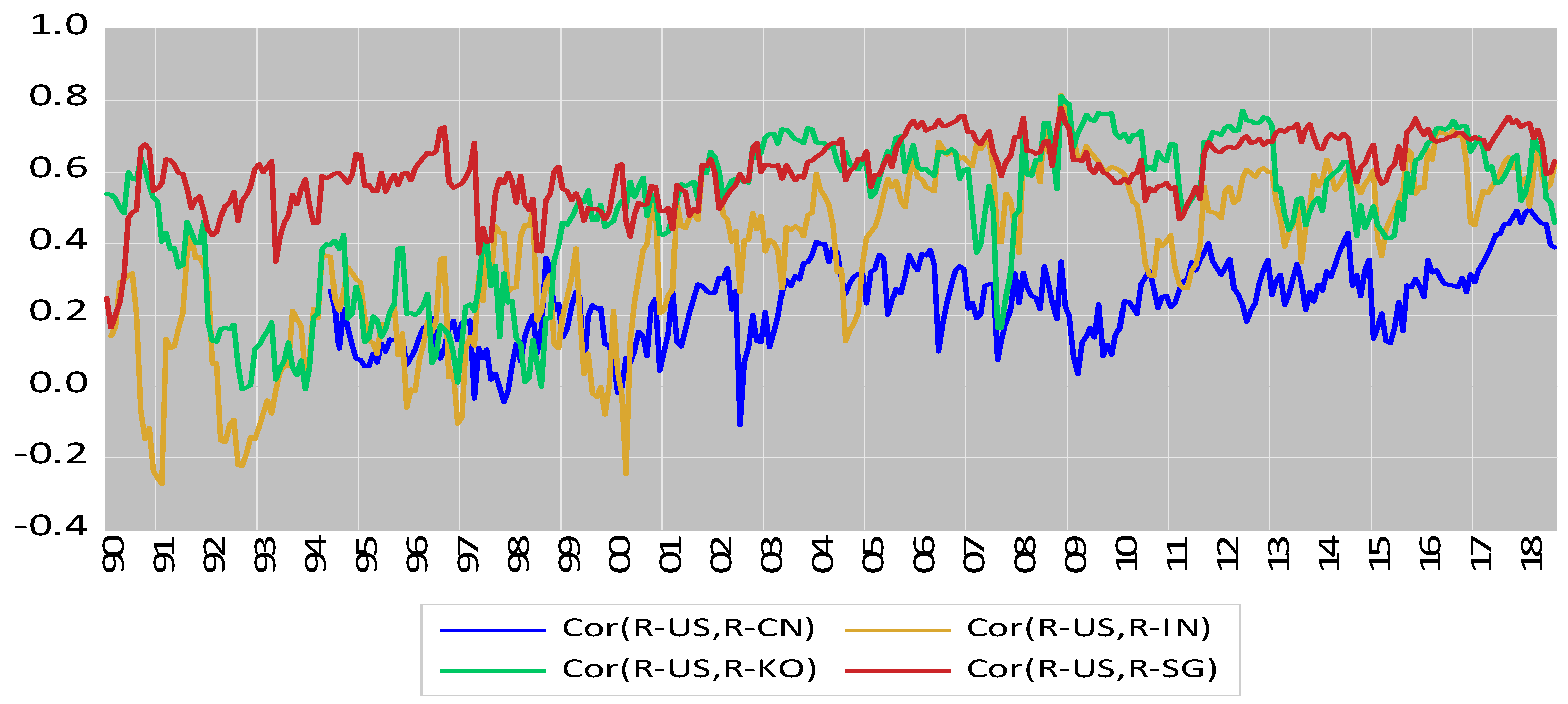

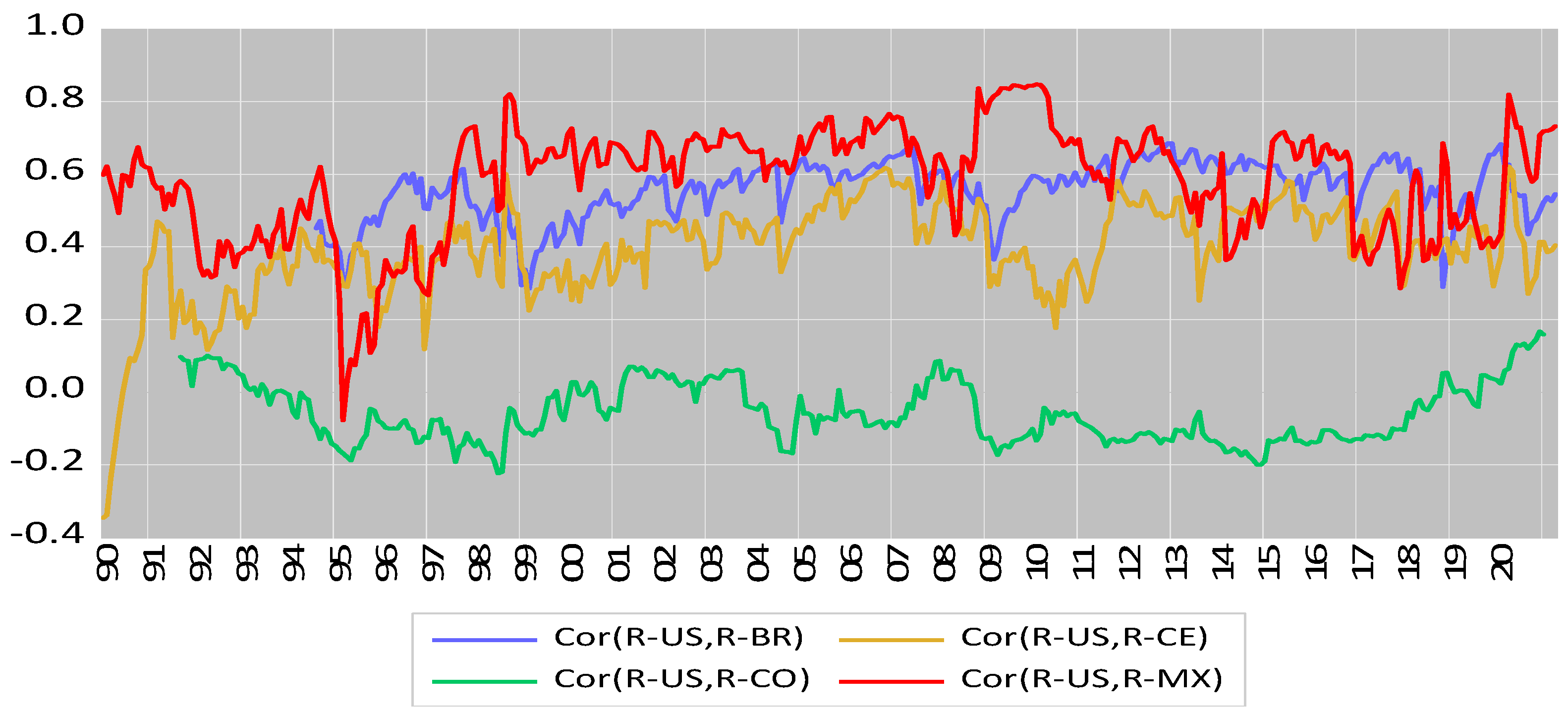

6. Time-Varying Stock–Return Correlation

6.1. Dynamic Conditional Correlation Model

6.2. EPU and COVID-19 on Time-Varying Return Correlations

7. Conclusions and Implications

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. Estimating the Time-Varying Correlations

| 1 | |

| 2 | Knight differentiated risk from uncertainty by the measurability vs. immeasurability. Knight (1921) defined only quantifiable uncertainty to be risk. However, the EPU indices provided by Baker et al. (2016) help to quantify the measurability of uncertainty. |

| 3 | Hillen et al. (2017) emphasize the concept that uncertainty provokes fear and perceptions of vulnerability. |

| 4 | Global indices are from: http://www.policyuncertainty.com/media/Global_Annotated_Series.pdf (accessed on 6 June 2021). |

| 5 | Baker et al. (2020a) use the following terms (term variants): E: {economic, economy, financial}; M: {“stock market”, equity, equities, “Standard and Poors”}; V: {volatility, volatile, uncertain, uncertainty, risk, risky};ID:{epidemic, pandemic, virus, flu, disease, coronavirus, mers, sars, ebola, H5N1, H1N1}. |

| 6 | A model that incorporates an asymmetry shock (Nelson 1991) is not considered, since this information will be captured by a lag of the COVID disease shock at a later point. The use of GARCH (1,1) was popularized by Bollerslev et al. (1992) as a way to achieve a better fit of the stock return equation. Bollerslev (2010) provides a summary of different specification of GARCH-type models. |

| 7 | A kurtosis above 3 indicates “fat tails,” or leptokurtosis, relative to the normal, or Gaussian, distribution. Platykurtosis refers to a distribution that has a negative excess kurtosis with a relatively flatter peak than a normal distribution. |

| 8 | Bollerslev (2010) provides alternative specifications of the GARCH-type model. |

| 9 | As arrival of COVID-19 in U.S. on early 2020, the Dow Jones Industrial Average (DJIA) was down 3.56%, S&P 500 decreased 3.35%, and NASDAQ dropped 3.71%. Recently, as COVID-19 variant emerged from news, the DJIA fell 2.53%, while the S&P 500 and NASDAQ Composite declined 2.27% and 2.23%, respectively. causing a big sell-off on Friday, November 26. Specifically, Futures on the DJIA dropped 415 points or 1.18% S&P 500 futures were down 0.78%, and Nasdaq 100 futures fell 0.4% as reported by Yun Li for CNBC on November 30, 2021, 03:30 AM EST. |

| 10 | IMF provides a report with respect to various key policy responses for different countries (See Policy response to COVID-19–International Monetary Fund, www.imf.org (accessed on 6 June 2021)). |

| 11 | + + + + . |

| 12 | |

| 13 | Canada, India and Singapore are thought much heighted connected with U.S., both on the economic and political aspects, that renders a positive respond to the The same argument apply to Japan for the coefficient of |

| 14 | Some researcers alternatively use a factor model by specifying size and value factors and other style factors as exogenous variables in their mean equation. |

References

- Antonakakis, Nikolaos, Ioannis Chatziantoniou, and George Filis. 2013. Dynamic co-movements of stock market returns, implied volatility and policy uncertainty. Economics Letters 120: 87–92. [Google Scholar] [CrossRef]

- Arouri, Mohamed, Christophe Estay, Christophe Rault, and David Roubaud. 2016. Economic policy uncertainty and stock markets: Long run evidence from the US. Finance Research Letters 18: 136–41. [Google Scholar] [CrossRef]

- Bahrini, Raéf, and Assaf Filfilan. 2020. Impact of the novel coronavirus on stock market returns: Evidence from GCC countries. Quantitative Finance and Economics 4: 640–52. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, and Steven J. Davis. 2016. Measuring economic policy uncertainty. Quarterly Journal of Economics 131: 1593–636. [Google Scholar] [CrossRef]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, and Kyle Kost. 2019. Policy News and Stock Market Volatility. Available online: https://www.policyuncertainty.com/media/Policy%20News%20and%20Stock%20Market%20Volatility.pdf (accessed on 12 October 2021).

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, and Stephen J. Terry. 2020a. COVID-Induced Economic Uncertainty. NBER Working Paper No. 26983. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Baker, Scott R., Nicholas Bloom, Steven J. Davis, Kyle Kost, Marco Sammon, and Tasaneeya Viratyosin. 2020b. The Unprecedented stock market reaction to COVID-19. The Review of Asset Pricing Studies 10: 742–58. [Google Scholar] [CrossRef]

- Bhattarai, Saroj, Arpita Chatterjee, and Woong Yong Park. 2020. Global spillover effects of US uncertainty. Journal of Monetary Economics 114: 71–89. [Google Scholar] [CrossRef] [Green Version]

- Bloom, Nicholas. 2009. The impact of uncertainty shocks. Econometrica 77: 623–685. [Google Scholar]

- Bloom, Nicholas. 2014. Fluctuations in Uncertainty. Journal of Economic Perspectives 28: 153–76. [Google Scholar] [CrossRef] [Green Version]

- Bollerslev, Tim. 2010. Glossary to ARCH (GARCH) in Volatility and Time Series Econometrics: Essays in Honor of Robert Engle. Edited by Tim Bollerslev, Jeffrey Russell and Mark Watson. Oxford: Oxford University Press. [Google Scholar]

- Bollerslev, Tim, Ray Y. Chou, and Kenneth F. Kroner. 1992. ARCH modeling in finance: A review of the theory and empirical evidence. Journal of Econometrics 52: 5–59. [Google Scholar] [CrossRef]

- Bora, Debakshi, and Daisy Basistha. 2021. The outbreak of COVID-19 and its impact on stock market volatility: Evidence from a worst affected economy. Journal of Public Affairs 2021: e2623. [Google Scholar] [CrossRef]

- Bouoiyour, Jamal, Refk Selmi, and Mark E. Wohar. 2018. Measuring the response of gold prices to uncertainty: An analysis beyond the mean. Economic Modeling 75: 1–12. [Google Scholar] [CrossRef] [Green Version]

- Brogaard, Jonathan, and Andrew Detzel. 2015. The Asset Pricing Implications of Government Economic Policy Uncertainty. Management Science 61: 3–18. [Google Scholar] [CrossRef] [Green Version]

- Caggiano, Giovanni, Efrem Castelnuovo, and Nicolas Groshenny. 2014. Uncertainty shocks and unemployment dynamics in U.S. recessions. Journal of Monetary Economics 67: 78–92. [Google Scholar] [CrossRef] [Green Version]

- Chatjuthamard, Pattanaporn, Pavitra Jindahra, Pattarake Sarajoti, and Sirimon Treepongkaruna. 2021. The effect of COVIC-19 on the global stock market. Accounting & Finance 61: 4923–53. [Google Scholar]

- Chatziantoniou, Ioannis, David Duffy, and George Filis. 2013. Stock market response to monetary and fiscal policy shocks: Multi-country evidence. Economic Modelling 30: 754–69. [Google Scholar] [CrossRef] [Green Version]

- Chen, Cathy W. S., Thomas C. Chiang, and Mike K. P. So. 2003. Asymmetrical reaction to US stock-return news: Evidence from major stock markets based on a double-threshold model. Journal of Economics and Business 55: 487–502. [Google Scholar] [CrossRef]

- Chen, Cathy Yi-Hsuan, and Thomas C. Chiang. 2016. Empirical analysis of the intertemporal relation between downside risk and expected returns: Evidence from time-varying transition probability models. European Financial Management 22: 749–96. [Google Scholar] [CrossRef]

- Chen, Cathy Yi-Hsuan, Thomas C. Chiang, and Wolfgang Karl Härdle. 2018. Downside risk and stock returns in the G7 countries: An empirical analysis of their long-run and short-run dynamics. Journal of Banking & Finance 93: 21–32. [Google Scholar]

- Chen, Jian, Fuwei Jiang, and Guoshi Tong. 2017. Economic policy uncertainty in China and stock market expected returns. Accounting & Finance 57: 1265–86. [Google Scholar]

- Chiang, Thomas C. 2019. Economic policy uncertainty, risk and stock returns: Evidence from G7 stock markets. Finance Research Letters 29: 41–49. [Google Scholar] [CrossRef]

- Chiang, Thomas C. 2020. US policy uncertainty and stock returns: Evidence in the US and its spillovers to European Union, China, and Japan. Journal of Risk Finance 21: 621–57. [Google Scholar] [CrossRef]

- Chiang, Thomas C. 2021. Spillovers of U.S. market volatility and monetary policy uncertainty to global stock markets. North American Journal of Economics and Finance 58: 474–501. [Google Scholar] [CrossRef]

- Chiang, Thomas C., Bang Nam Jeon, and Huimin Li. 2007. Dynamic correlation analysis of financial contagion: Evidence from Asian markets. Journal of International Money and Finance 26: 1206–28. [Google Scholar] [CrossRef]

- Chiang, Thomas C., Lanjun Lao, and Qingfeng Xue. 2016. Comovements between Chinese and global stock markets: Evidence from aggregate and sectoral data. Review of Quantitative Finance and Accounting 47: 1003–42. [Google Scholar] [CrossRef]

- Chiang, Thomas C., and Yuanqing Zhang. 2018. An Empirical Investigation of Risk-Return Relations in Chinese Equity Markets: Evidence from Aggregate and Sectoral Data. International Journal of Financial Studies 6: 35. [Google Scholar] [CrossRef] [Green Version]

- Christou, Christina, Juncal Cunado, Rangan Gupta, and Christis Hassapis. 2017. Economic policy uncertainty and stock market returns in Pacific-Rim countries: Evidence based on a Bayesian panel VAR model. Journal of Multinational Financial Management 40: 92–102. [Google Scholar] [CrossRef]

- Connolly, Robert, Chris Stivers, and Licheng Sun. 2005. Stock market uncertainty and the stock-bond return relation. Journal of Financial and Quantitative Analysis 40: 161–94. [Google Scholar] [CrossRef] [Green Version]

- Davis, Steven. 2016. An Index of Global Economic Policy Uncertainty. NBER Working Paper 22740. Available online: https://ideas.repec.org/p/nbr/nberwo/22740.html (accessed on 1 October 2021).

- Davis, Steven J., Dingqian Liu, and Xuguang Simon Sheng. 2021. Stock prices and economic activity in the time of coronavirus. IMF Economic Review. [Google Scholar] [CrossRef]

- Ding, Zhuanxin, Clive W. J. Granger, and Robert F. Engle. 1993. A long memory property of stock market returns and a new model. Journal of Empirical Finance 1: 83–106. [Google Scholar] [CrossRef]

- Engle, Robert F. 2002. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business and Economic Statistics 20: 339–50. [Google Scholar] [CrossRef]

- Engle, Robert F. 2009. Anticipating Correlations: A New Paradigm for Risk Management. Princeton: Princeton University Press. [Google Scholar]

- Forbes, Kristin J., and Roberto Rigobon. 2002. No contagion, only Interdependence: Measuring stock market co-movements. Journal of Finance 57: 2223–62. [Google Scholar] [CrossRef]

- French, Kenneth R., G. William Schwert, and Robert F. Stambaugh. 1987. Expected stock returns and volatility. Journal of Financial Economics 19: 3–29. [Google Scholar] [CrossRef] [Green Version]

- Guo, Hui, and Robert F. Whitelaw. 2006. Uncovering the risk-return relation in the stock market. Journal of Finance 61: 1433–63. [Google Scholar] [CrossRef] [Green Version]

- Hillen, Marij A., Caitlin M. Gutheil, Tania D. Strout, Ellen M. A. Smets, and Paul K. J. Han. 2017. Tolerance of uncertainty: Conceptual analysis, integrative model, and implications for healthcare. Social Science & Medicine 180: 62–75. [Google Scholar]

- Hong, Hui, Zhicun Bian, and Chien-Chiang Lee. 2021. COVID-19 and instability of stock market performance: Evidence from the U.S. Financial Innovation 7: 12. [Google Scholar] [CrossRef]

- Hung, Dao Van, Nguyen Thi Minh Hue, and Vu Thuy Duong. 2021. The impact of COVID-19 on stock market returns in Vietnam. Journal of Risk Financial Management 14: 441. [Google Scholar] [CrossRef]

- Indrayono, Yohanes. 2021. What factors affect stocks’ abnormal return during the COVID-19 pandemic: Data from the Indonesia stock exchange. European Journal of Business & Management Research 6: 1–11. [Google Scholar] [CrossRef]

- Jones, Lora, Daniele Palumbo, and David Brown. 2021. Coronavirus: How the pandemic has changed the world economy. BBC News. March 4. Available online: www.bbc.com (accessed on 30 November 2021).

- Karolyi, G. Andrew, and René M. Stulz. 1996. Why do markets move together? An investigation of US-Japanese stock return comovements. Journal of Finance 51: 951–86. [Google Scholar] [CrossRef]

- Kenourgios, Dimitris, Aristeidis Samitas, and Nikos Paltalidis. 2011. Financial crises and stock market contagion in a multivariate time-varying asymmetric framework. Journal of International Financial Markets, Institutions and Money 21: 92–106. [Google Scholar] [CrossRef]

- Khatatbeh, Ibrahim N., Mohammad Bani Hani, and Mohammed N. Abu-Alfoul. 2020. The impact of COVID-19 pandemic on global stock markets: An event study. International Journal of Economics and Business Administration 8: 505–14. [Google Scholar] [CrossRef]

- Knight, Frank H. 1921. Risk, Uncertainty, and Profit, 5th ed. New York: Dover Publications. [Google Scholar]

- Latif, Yousaf, Ge Shunqi, Shahid Bashir, Wasim Iqbal, Salman Ali, and Muhammad Ramzan. 2021. COVID-19 and stock exchange return variation: Empirical evidence from econometric estimation. Environmental Science and Pollution Research 28: 60019–31. [Google Scholar] [CrossRef] [PubMed]

- Lee, Kelvin Yong-Ming, Mohamad Jais, and Chia-Wen Chan. 2020. Impact of Covid-19: Evidence from Malaysian stock market. International Journal of Business and Society 21: 607–28. [Google Scholar]

- Li, Qi, Jian Yang, Cheng Hsiao, and Young-Jae Chang. 2005. The relationship between stock returns and volatility in international stock markets. Journal of Empirical Finance 12: 650–65. [Google Scholar] [CrossRef]

- Li, Xiao-Ming. 2017. New evidence on economic policy uncertainty and equity premium. Pacific-Basin Finance Journal 46: 41–56. [Google Scholar] [CrossRef]

- Liow, Kim Hiang, Wen-Chi Liao, and Yuting Huang. 2018. Dynamics of international spillovers and interaction: Evidence from financial market stress and economic policy uncertainty. Economic Modelling 68: 96–116. [Google Scholar] [CrossRef]

- Liu, Li, and Tao Zhang. 2015. Economic policy uncertainty and stock market volatility. Finance Research Letter 15: 99–105. [Google Scholar] [CrossRef] [Green Version]

- Liu, Zhifeng, Toan Luu Duc Huynh, and Peng-Fei Dai. 2021. The impact of COVID-19 on the stock market crash risk in China. Research in International Business and Finance 57: 101419. [Google Scholar] [CrossRef]

- Longin, Francois, and Bruno Solnik. 1995. Is the correlation in international equity returns constant: 1960–1990? Journal of International Money and Finance 14: 3–26. [Google Scholar] [CrossRef]

- Menzly, Lior, Tano Santos, and Pietro Veronesi. 2004. Understanding predictability. Journal of Political Economy 112: 1–47. [Google Scholar] [CrossRef] [Green Version]

- Merton, Robert C. 1973. An intertemporal capital asset pricing model. Econometrica 41: 867–87. [Google Scholar] [CrossRef]

- Merton, Robert C. 1980. On estimating the expected return on the market: An exploratory investigation. Journal of Financial Economics 8: 323–61. [Google Scholar] [CrossRef]

- Moore, Tomoe, and Ping Wang. 2014. Dynamic linkage between real exchange rates and stock prices: Evidence from developed and emerging Asian markets. International Review of Economics & Finance 29: 1–11. [Google Scholar]

- Mugiarni, Ajeng, and Permata Wulandari. 2021. The Effect of Covid-19 Pandemic on Stock Returns: An evidence of Indonesia stock exchange. Journal of International Conference Proceedings 4: 28–37. [Google Scholar] [CrossRef]

- Nelson, Daniel B. 1991. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 59: 347–370. [Google Scholar] [CrossRef]

- Nian, Rui, Yijin Xu, Qiang Yuan, Chen Feng, and Amaury Lendasse. 2021. Quantifying time-frequency co-movement impact of COVID-19 on U.S. and China stock market toward investor sentiment index. Frontiers in Public Health 9: 727047. [Google Scholar] [CrossRef] [PubMed]

- Ozoguz, Arzu. 2009. Good times or bad times? Investors’ uncertainty and stock returns. Review of Financial Studies 22: 4377–422. [Google Scholar] [CrossRef]

- Rapach, David E., Jack K. Strauss, and Guofu Zhou. 2013. International stock return predictability: What is the role of the United States? Journal of Finance 68: 1633–22. [Google Scholar] [CrossRef]

- Rubbaniy, Ghulame, Ali Awais Khalid, Muhammad Umar, and Nawazish Mirza. 2021. European Stock Markets’ Response to COVID-19, Lockdowns, Government Response Stringency and Central Banks’ Interventions. Available online: https://ssrn.com/abstract=3785598 (accessed on 8 December 2021).

- Shahzad, Syed Jawad Hussain, Elie Bouri, Ladislav Kristoufek, and Tareq Saeed. 2021. Impact of the COVID-19 outbreak on the US equity sectors: Evidence from quantile return spillovers. Financial Innovation 7: 1–23. [Google Scholar] [CrossRef]

- Singh, Gurmeet, and Muneer Shaik. 2021. The short-term impact of COVID-19 on global stock market indices. Contemporary Economics 15: 1–18. [Google Scholar] [CrossRef]

- Trung, Nguyen Ba. 2019. The Spillover Effect of the US Uncertainty on Emerging Economies: A panel VAR approach. Applied Economics Letters 26: 210–16. [Google Scholar] [CrossRef]

- Wątorek, Marcin, Jarosław Kwapień, and Stanisław Drożdż. 2021. Financial return distributions: Past, present, and COVID-19. Entropy 23: 884. [Google Scholar] [CrossRef]

- Yan, Chao. 2020. COVID-19 outbreak and stock prices: Evidence from China. SSRN 3574374. Available online: https://ssrn.com/abstract=3574374 (accessed on 1 October 2021).

- Youssef, Manel, Khaled Mokni, and Ahdi Noomen Ajmi. 2021. Dynamic connectedness between stock markets in the presence of the COVID-19 pandemic: Does economic policy uncertainty matter? Financial Innovation 7: 13. [Google Scholar] [CrossRef]

- Zehri, Chokri. 2021. Stock market comovements: Evidence from the COVID-19 pandemic. The Journal of Economic Asymmetries 24: e00228. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

| Market | C | ||||||

|---|---|---|---|---|---|---|---|

| Panel A | 9.2456 | −1.7804 | 2.6838 | 0.9218 | 0.7993 | 0.021 | |

| 43.49 | −48.97 | 0.42 | 1.02 | 4.19 | |||

| 3.4020 | −0.6431 | 1.0573 | 0.5141 | 0.7975 | 0.024 | ||

| 17.20 | −14.66 | 0.52 | 0.95 | 3.73 | |||

| 1.3583 | −0.2260 | 2.2151 | 0.5312 | 0.7394 | 0.004 | ||

| 13.55 | −9.22 | 0.60 | 0.81 | 2.46 | |||

| 3.8502 | −0.7652 | 1.6395 | 0.5014 | 0.7888 | 0.020 | ||

| 7.00 | −6.68 | 0.60 | 0.81 | 3.54 | |||

| 3.5922 | −0.7206 | 1.5669 | 0.4706 | 0.8151 | 0.007 | ||

| 8.26 | −8.04 | 0.41 | 0.81 | 3.58 | |||

| 2.0566 | −0.3813 | 2.2151 | 0.5564 | 0.6991 | 0.007 | ||

| 9.66 | −9.59 | 0.60 | 0.78 | 1.91 | |||

| 3.9755 | −0.8276 | 0.0511 | 0.3896 | 0.8899 | 0.007 | ||

| 58.64 | −68.16 | 0.10 | 1.10 | 9.10 | |||

| Panel B | 2.8454 | −0.5234 | 5.8669 | 0.3606 | 0.7421 | 0.005 | |

| 24.65 | −13.54 | 0.73 | 0.70 | 2.78 | |||

| 7.3318 | −1.5870 | 7.4521 | 0.3243 | 0.6930 | 0.066 | ||

| 11.41 | −10.98 | 0.42 | 0.45 | 1.08 | |||

| 1.7588 | −0.3586 | 1.4725 | 0.5531 | 0.8223 | 0.002 | ||

| 7.02 | −7.73 | 0.51 | 1.07 | 5.39 | |||

| 5.7930 | −1.1537 | 1.8871 | 0.7118 | 0.6663 | 0.037 | ||

| 13.47 | −13.04 | 0.67 | 0.89 | 2.01 | |||

| Panel C | 2.0072 | −0.3629 | 36.6671 | 1.1989 | 0.0902 | 0.006 | |

| 22.85 | −10.82 | 1.55 | 1.04 | 0.26 | |||

| 5.6974 | −1.1701 | 1.4079 | 0.1244 | 0.7470 | 0.034 | ||

| 5.34 | −5.01 | 0.79 | 1.02 | 2.97 | |||

| 0.6241 | −0.1306 | 1.6867 | 0.2400 | 0.8058 | 0.003 | ||

| 4.09 | −3.90 | 0.57 | 1.01 | 3.81 | |||

| 1.3676 | −0.2215 | 3.2422 | 0.4435 | 0.7712 | 0.002 | ||

| 6.57 | −4.22 | 0.55 | 0.66 | 2.53 |

| Market | C | ||||||

|---|---|---|---|---|---|---|---|

| Panel A | 6.4605 | −1.3264 | 0.8016 | 0.5987 | 0.7981 | 0.040 | |

| 57.44 | −47.31 | 0.47 | 1.01 | 4.18 | |||

| 5.9379 | −1.2225 | 1.2473 | 0.5324 | 0.7963 | 0.030 | ||

| 17.59 | −16.43 | 0.52 | 0.88 | 3.60 | |||

| 6.2713 | −1.2989 | 1.8783 | 0.5175 | 0.7660 | 0.032 | ||

| 12.56 | −12.08 | 0.65 | 0.90 | 3.43 | |||

| 6.3616 | −1.3085 | 1.7092 | 0.5683 | 0.8006 | 0.023 | ||

| 19.95 | −19.06 | 0.49 | 0.89 | 3.77 | |||

| 6.2653 | −1.3144 | 1.2556 | 0.5127 | 0.7665 | 0.040 | ||

| 27.52 | −28.94 | 0.55 | 0.82 | 2.88 | |||

| 3.9773 | −0.8238 | 0.0081 | 0.3093 | 0.9167 | 0.011 | ||

| 49.59 | −56.61 | 0.02 | 0.96 | 10.52 | |||

| Panel B | 9.6793 | −2.0053 | 3.0395 | 0.2010 | 0.8253 | 0.027 | |

| 26.58 | −25.54 | 0.97 | 0.79 | 5.92 | |||

| 5.0161 | −1.0040 | 4.2392 | 0.3231 | 0.8167 | 0.007 | ||

| 6.62 | −6.04 | 0.63 | 0.86 | 3.98 | |||

| 2.3167 | −0.4624 | 4.1761 | 1.0240 | 0.7989 | 0.001 | ||

| 3.08 | −2.89 | 0.52 | 0.85 | 3.79 | |||

| 3.1397 | −0.6311 | 1.4576 | 0.6254 | 0.7357 | 0.012 | ||

| 16.81 | −14.19 | 0.84 | 1.29 | 4.46 | |||

| Panel C | 8.0327 | −1.6380 | 23.6677 | 0.9735 | 0.0763 | 0.020 | |

| 11.35 | −10.04 | 1.98 | 1.38 | 0.32 | |||

| 2.5995 | −0.4680 | 4.7147 | 0.2519 | 0.6236 | 0.003 | ||

| 5.13 | −3.96 | 0.58 | 0.74 | 1.18 | |||

| 3.9392 | −0.7955 | 2.7380 | 0.2189 | 0.7791 | 0.008 | ||

| 14.20 | −17.37 | 0.60 | 0.84 | 2.92 | |||

| 6.7019 | −1.2737 | 1.2727 | 0.1398 | 0.8808 | 0.005 | ||

| 23.06 | −21.50 | 0.65 | 0.89 | 6.81 |

| US Return | C | ||||||

|---|---|---|---|---|---|---|---|

| Panel A | 1.4823 | −0.0410 | 1.7913 | 0.4462 | 0.7776 | −0.014 | |

| 2.08 | −0.28 | 0.71 | 1.30 | 4.92 | |||

| 1.3583 | −0.2260 | 2.2151 | 0.5312 | 0.7394 | 0.004 | ||

| 13.55 | −9.22 | 0.60 | 0.81 | 2.46 | |||

| 3.8502 | −0.7652 | 1.6395 | 0.5014 | 0.7888 | 0.020 | ||

| 7.00 | −6.68 | 0.60 | 0.81 | 3.54 | |||

| 0.9425 | −0.0016 | 0.8612 | 0.2214 | 0.7576 | −0.005 | ||

| 0.32 | −0.00 | 1.60 | 3.34 | 11.56 | |||

| 2.0944 | −0.1447 | 1.5580 | 0.3939 | 0.7585 | −0.022 | ||

| 3.88 | −1.30 | 0.82 | 1.47 | 5.09 | |||

| 2.5850 | −0.2717 | 1.2028 | 0.3072 | 0.7937 | −0.013 | ||

| 1.37 | −0.65 | 0.78 | 1.44 | 6.05 | |||

| Panel B | 1.3617 | 0.0137 | 1.3341 | 0.3512 | 0.7839 | −0.024 | |

| 2.95 | 0.12 | 0.78 | 1.30 | 5.59 | |||

| −1.0616 | 0.6082 | 1.5865 | 0.3688 | 0.7283 | −0.069 | ||

| −1.50 | 3.92 | 0.76 | 1.29 | 3.90 | |||

| 2.1825 | −0.1852 | 1.0027 | 0.2614 | 0.7718 | −0.013 | ||

| 1.99 | −0.76 | 1.04 | 1.86 | 6.97 | |||

| 3.2477 | −0.4153 | 1.2270 | 0.2543 | 0.7457 | −0.012 | ||

| 1.96 | −1.17 | 0.83 | 1.51 | 4.55 | |||

| Panel C | 1.7224 | −0.0890 | 1.8999 | 0.4008 | 0.7283 | −0.012 | |

| 4.50 | −1.05 | 0.87 | 1.43 | 4.16 | |||

| 3.5865 | −0.4809 | 1.1412 | 0.2811 | 0.7581 | −0.012 | ||

| 2.57 | −1.54 | 1.11 | 1.78 | 6.35 | |||

| 1.2896 | 0.0484 | 2.1000 | 0.4208 | 0.7244 | −0.032 | ||

| 16.11 | 4.59 | 0.77 | 1.29 | 3.80 | |||

| 2.0597 | −0.1390 | 1.4469 | 0.4134 | 0.7528 | −0.028 | ||

| 3.73 | −1.19 | 0.85 | 1.41 | 5.04 |

| Market | C | |||||||

|---|---|---|---|---|---|---|---|---|

| Panel A: World and G7 markets | ||||||||

| 0.1096 | −0.0823 | −0.0028 | 1.3127 | 15.9656 | 1.2466 | 0.6377 | 0.11 | |

| 0.63 | −21.24 | −5.87 | 5.79 | 0.50 | 0.73 | 1.65 | ||

| −0.0839 | −0.0484 | −0.0021 | 1.5487 | 4.7491 | 0.7632 | 0.7438 | 0.05 | |

| −6.18 | −14.19 | −3.33 | 25.89 | 0.58 | 1.04 | 3.04 | ||

| 0.7429 | −0.0280 | −0.0064 | 0.0416 | 5.8430 | 0.6865 | 0.8821 | 0.05 | |

| 18.75 | −28.69 | −16.71 | 5.45 | 0.41 | 0.73 | 5.21 | ||

| 0.9777 | −0.0173 | −0.0007 | 0.5220 | 13.6361 | 1.2435 | 0.6199 | 0.01 | |

| 3.00 | −12.45 | −7.00 | 1.94 | 0.68 | 1.08 | 1.99 | ||

| 0.7105 | −0.0261 | −0.0079 | 0.7383 | 21.5563 | 0.8452 | 0.7126 | 0.04 | |

| 4.01 | −24.01 | −8.46 | 3.27 | 0.56 | 0.67 | 1.82 | ||

| 0.0662 | −0.0136 | −0.0094 | 0.9067 | 9.7415 | 0.3312 | 0.5585 | 0.01 | |

| 0.15 | −2.27 | −2.99 | 2.13 | 1.23 | 1.33 | 2.13 | ||

| −0.8786 | −0.0328 | −0.0065 | 1.1210 | 10.3997 | 0.6916 | 0.7248 | 0.07 | |

| −3.39 | −23.49 | −6.02 | 5.25 | 0.45 | 0.67 | 1.74 | ||

| −0.1842 | −0.0472 | −0.0008 | 1.4395 | 52.7483 | 0.7716 | 0.4179 | 0.05 | |

| −3.36 | −15.82 | −2.10 | 13.81 | 0.66 | 0.71 | 0.59 | ||

| Panel B: Asia markets | ||||||||

| −0.2908 | −0.0178 | −0.0036 | 1.3856 | 8.7601 | 0.3511 | 0.7873 | 0.01 | |

| −3.56 | −4.13 | −1.89 | 5.15 | 0.61 | 0.89 | 3.51 | ||

| −1.0237 | −0.0408 | −0.0068 | 5.8629 | 13.1608 | 0.3215 | 0.8048 | 0.12 | |

| −5.37 | −10.08 | −5.30 | 11.50 | 0.48 | 0.61 | 2.56 | ||

| −0.7663 | −0.0307 | −0.0079 | 3.3599 | 0.3126 | 0.1178 | 0.8994 | 0.03 | |

| −1.68 | −5.57 | −3.21 | 3.91 | 0.75 | 2.08 | 20.98 | ||

| 0.3059 | −0.0634 | −0.0062 | 0.3909 | 12.5017 | 0.6833 | 0.8094 | 0.06 | |

| 5.90 | −23.05 | −14.83 | 4.48 | 0.44 | 0.52 | 2.34 | ||

| Panel C: Latin America markets | ||||||||

| 0.3825 | −0.0100 | −0.0023 | 0.3879 | 36.5546 | 0.5042 | 0.6726 | 0.01 | |

| 2.51 | −6.21 | −2.67 | 2.65 | 0.57 | 0.58 | 1.66 | ||

| −3.0494 | −0.0355 | −0.0041 | 2.7365 | 28.9737 | 1.4632 | 0.3697 | 0.06 | |

| −7.11 | −22.13 | −6.03 | 7.32 | 0.77 | 1.13 | 1.81 | ||

| −0.6681 | −0.0008 | −0.0012 | 1.3985 | 3.3979 | 0.2179 | 0.8829 | 0.01 | |

| −1.70 | −2.68 | −2.27 | 4.31 | 0.39 | 0.84 | 5.51 | ||

| 0.8966 | −0.0161 | −0.0024 | 0.1039 | 6.4867 | 1.3228 | 0.8434 | 0.02 | |

| 14.47 | −10.34 | −4.46 | 3.79 | 0.33 | 0.61 | 3.45 | ||

| Market | C | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Panel A: G7 markets | |||||||||

| −0.4936 | −0.0618 | −0.0149 | −0.0091 | 2.2303 | 8.2510 | 0.7452 | 0.6858 | 0.10 | |

| −2.47 | −13.58 | −4.97 | −10.22 | 7.13 | 0.56 | 0.85 | 1.88 | ||

| 0.8576 | −0.0184 | −0.0477 | −0.0018 | 0.0461 | 9.9053 | 0.5323 | 0.8620 | 0.08 | |

| 23.62 | −17.85 | −22.46 | −3.09 | 1.68 | 0.38 | 0.53 | 3.10 | ||

| 0.7859 | −0.0040 | −0.0824 | −0.0004 | −0.0321 | 20.227 | 0.4334 | 0.9629 | 0.09 | |

| 48.71 | −5.07 | −33.21 | −2.69 | −1.73 | 0.31 | 0.24 | 14.35 | ||

| 0.4541 | −0.0177 | −0.0804 | −0.0028 | 0.3509 | 15.991 | 0.6042 | 0.7989 | 0.11 | |

| 15.00 | −12.23 | −28.50 | −25.73 | 9.18 | 0.43 | 0.59 | 2.34 | ||

| −1.2045 | −0.0163 | −0.0657 | −0.0071 | 1.7698 | 11.254 | 0.4195 | 0.4336 | 0.07 | |

| −1.43 | −2.68 | −5.56 | −2.36 | 2.47 | 1.55 | 1.60 | 1.77 | ||

| −0.8806 | −0.0222 | −0.0588 | −0.0032 | 1.1739 | 16.255 | 0.9641 | 0.8259 | 0.13 | |

| −1.76 | −11.61 | −16.43 | −4.52 | 2.72 | 0.38 | 0.46 | 2.46 | ||

| −0.2502 | −0.0620 | −0.0432 | −0.0053 | 1.7913 | 20.959 | 0.6388 | 0.6953 | 0.08 | |

| −3.51 | −14.33 | −17.38 | −5.35 | 12.84 | 0.52 | 0.70 | 1.63 | ||

| Panel B: Asia markets | |||||||||

| −0.1900 | −0.0032 | −0.0233 | −0.0007 | 2.0995 | 19.892 | 0.5917 | 0.8048 | 0.01 | |

| −1.63 | −2.00 | −4.27 | −6.81 | 10.67 | 0.48 | 0.59 | 2.66 | ||

| −1.0011 | −0.0412 | −0.0312 | −0.0052 | 6.5639 | 15.748 | 0.2838 | 0.7944 | 0.12 | |

| −7.88 | −11.51 | −5.57 | −3.34 | 26.45 | 0.46 | 0.55 | 2.22 | ||

| −0.3448 | −0.0279 | −0.0260 | −0.0105 | 1.8926 | 0.4865 | 0.2136 | 0.9106 | 0.04 | |

| −1.49 | −9.40 | −4.18 | −9.70 | 4.92 | 0.36 | 1.29 | 14.51 | ||

| 0.2641 | −0.0450 | −0.0236 | −0.0057 | 0.3953 | 15.656 | 0.3323 | 0.8634 | 0.06 | |

| 4.34 | −7.42 | −61.89 | −10.91 | 3.30 | 0.38 | 0.35 | 2.56 | ||

| Panel C: Latin America markets | |||||||||

| 0.398 | −0.0093 | 0.0000 | −0.0023 | 0.3901 | 3.341 | 0.1727 | 0.9452 | 0.01 | |

| 3.74 | −6.69 | −3.13 | −2.14 | 3.77 | 0.28 | 0.68 | 9.67 | ||

| −3.059 | −0.0288 | −0.0348 | −0.0062 | 2.7591 | 33.388 | 2.0449 | 0.3889 | 0.07 | |

| −6.62 | −16.22 | −12.55 | −12.51 | 6.61 | 0.74 | 1.00 | 0.77 | ||

| −0.659 | −0.0005 | 0.0208 | 0.0009 | 1.4933 | 22.417 | 1.3826 | 0.8156 | 0.01 | |

| −2.12 | −4.58 | 12.11 | 2.78 | 5.96 | 0.34 | 0.61 | 2.67 | ||

| 0.974 | −0.0126 | −0.0349 | −0.0035 | 0.1662 | 18.008 | 0.2596 | 0.9059 | 0.02 | |

| 17.51 | −19.13 | −13.34 | −5.43 | 4.17 | 0.38 | 0.40 | 4.18 | ||

| Market | C | |||||||

|---|---|---|---|---|---|---|---|---|

| Panel A: World and G7 markets | ||||||||

| −0.1066 | −0.0766 | −0.0002 | 1.1601 | 20.0148 | 1.1905 | 0.5434 | 0.11 | |

| −2.30 | −32.13 | −2.21 | 15.54 | 0.54 | 0.76 | 1.93 | ||

| −0.1935 | −0.0246 | −0.0003 | 1.5758 | 3.7192 | 0.6748 | 0.7811 | 0.06 | |

| −1.48 | −4.60 | −5.61 | 10.07 | 0.55 | 1.02 | 3.79 | ||

| 0.6387 | −0.0039 | −0.0003 | 0.1833 | 9.9606 | 1.3638 | 0.7925 | 0.05 | |

| 9.34 | −6.89 | −12.64 | 3.07 | 0.50 | 0.73 | 2.98 | ||

| 1.0833 | −0.0178 | −0.0001 | 0.3694 | 19.1867 | 0.8490 | 0.6324 | 0.02 | |

| 11.37 | −9.60 | −3.81 | 7.46 | 0.64 | 0.86 | 1.66 | ||

| 0.5641 | −0.0259 | −0.0001 | 0.7442 | 17.9196 | 0.6773 | 0.7096 | 0.04 | |

| 2.57 | −16.14 | −6.16 | 2.95 | 0.61 | 0.71 | 1.98 | ||

| 1.7170 | −0.0248 | −0.0001 | −1.0795 | 31.8163 | 0.7747 | 0.6716 | 0.02 | |

| 5.34 | −14.95 | −18.50 | −4.68 | 0.46 | 0.52 | 1.19 | ||

| −0.4147 | −0.0284 | −0.0001 | 1.3179 | 10.0024 | 0.9075 | 0.6651 | 0.03 | |

| −1.61 | −20.99 | −7.08 | 5.77 | 0.58 | 0.83 | 1.79 | ||

| −0.2556 | −0.0326 | −0.0009 | 1.4338 | 4.5136 | 0.1219 | 0.8214 | 0.06 | |

| −1.55 | −3.85 | −2.66 | 4.67 | 0.63 | 0.82 | 3.68 | ||

| Panel B: Asia markets | ||||||||

| 0.1207 | −0.0094 | −0.0001 | 0.5103 | 6.9450 | 0.3314 | 0.7879 | 0.02 | |

| 2.12 | −2.56 | −2.19 | 2.94 | 0.65 | 1.01 | 3.95 | ||

| −1.0216 | −0.0442 | −0.0002 | 6.4460 | 32.0478 | 0.2750 | 0.9500 | 0.12 | |

| −11.15 | −23.74 | −4.50 | 20.96 | 0.44 | 0.28 | 10.56 | ||

| −0.7236 | −0.0336 | 0.0000 | 3.4093 | 0.4263 | 0.1135 | 0.9000 | 0.03 | |

| −1.61 | −5.82 | 0.61 | 4.01 | 0.81 | 2.03 | 20.63 | ||

| 0.2860 | −0.0603 | −0.0004 | 0.4074 | 13.0539 | 0.9830 | 0.7781 | 0.06 | |

| 4.19 | −12.09 | −5.39 | 3.33 | 0.48 | 0.60 | 2.36 | ||

| Panel C: Latin America markets | ||||||||

| 0.5163 | −0.0164 | −0.0001 | 0.5717 | 6.4776 | 0.2463 | 0.9144 | 0.01 | |

| 2.16 | −7.02 | −4.65 | 3.17 | 0.34 | 0.58 | 5.73 | ||

| −3.0950 | −0.0347 | −0.0002 | 2.7405 | 31.0225 | 2.3343 | 0.3746 | 0.05 | |

| −7.63 | −16.44 | −18.50 | 6.62 | 0.73 | 1.08 | 0.78 | ||

| −0.6656 | −0.0005 | 0.0000 | 1.4695 | 32.2105 | 0.4877 | 0.9732 | 0.01 | |

| −12.83 | −2.04 | 1.39 | 42.70 | 0.30 | 0.21 | 22.08 | ||

| 0.8966 | −0.0164 | −0.0001 | 0.2713 | 1.4323 | 0.8697 | 0.8173 | 0.01 | |

| 13.69 | −12.74 | −2.13 | 3.49 | 0.25 | 0.83 | 4.01 | ||

| Market | C | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Panel A. World and G7 markets | |||||||||

| −0.1956 | −0.0490 | −0.0025 | −0.0002 | 1.6683 | 4.9411 | 0.7551 | 0.7382 | 0.06 | |

| −5.65 | −13.46 | −6.18 | −7.90 | 20.97 | 0.61 | 1.04 | 3.05 | ||

| 0.6146 | −0.0219 | −0.0099 | −0.0001 | 0.6372 | 9.4522 | 0.4954 | 0.7279 | 0.06 | |

| 3.72 | −12.69 | −11.55 | −3.86 | 3.41 | 0.56 | 0.65 | 1.84 | ||

| 1.0427 | −0.0151 | −0.0032 | −0.0001 | 0.0877 | 20.3605 | 1.5996 | 0.5976 | 0.01 | |

| 20.08 | −7.44 | −5.58 | −6.38 | 3.48 | 0.55 | 0.91 | 1.44 | ||

| 0.7044 | −0.0309 | −0.0061 | −0.0001 | 0.7191 | 25.5986 | 0.8744 | 0.7027 | 0.03 | |

| 4.93 | −34.17 | −9.23 | −6.26 | 4.79 | 0.55 | 0.65 | 1.72 | ||

| 1.7508 | −0.0217 | −0.0111 | −0.0001 | −1.0915 | 23.5601 | 0.2525 | 0.8586 | 0.03 | |

| 7.92 | −20.60 | −8.97 | −11.23 | −5.62 | 0.35 | 0.33 | 2.49 | ||

| −0.8170 | −0.0332 | −0.0063 | 0.0001 | 1.1227 | 12.5512 | 0.7267 | 0.6820 | 0.06 | |

| −1.68 | −15.50 | −5.19 | −2.36 | 2.78 | 0.49 | 0.66 | 1.45 | ||

| 0.1867 | −0.0140 | −0.0455 | −0.0006 | 1.1887 | 5.6923 | 0.1482 | 0.7280 | 0.10 | |

| 1.10 | −1.66 | −7.98 | −2.15 | 3.59 | 0.88 | 1.10 | 3.03 | ||

| −0.1956 | −0.0490 | −0.0025 | −0.0002 | 1.6683 | 4.9411 | 0.7551 | 0.7382 | 0.06 | |

| −5.65 | −13.46 | −6.18 | −7.90 | 20.97 | 0.61 | 1.04 | 3.05 | ||

| Panel B: Asia markets | |||||||||

| −0.3387 | −0.0155 | −0.0032 | −0.0001 | 1.2814 | 17.7666 | 0.7268 | 0.7689 | 0.01 | |

| −1.67 | −4.15 | −2.11 | −6.57 | 4.35 | 0.51 | 0.70 | 2.56 | ||

| −0.9896 | −0.0432 | −0.0071 | −0.0001 | 6.3692 | 66.7758 | 2.0890 | 0.8414 | 0.12 | |

| −8.23 | −17.72 | −3.99 | −2.72 | 16.25 | 0.32 | 0.42 | 2.59 | ||

| −0.7436 | −0.0306 | −0.0077 | 0.0000 | 3.2097 | 0.3139 | 0.1099 | 0.8933 | 0.03 | |

| −1.38 | −4.59 | −2.63 | 0.53 | 3.18 | 0.98 | 2.58 | 23.77 | ||

| 0.2991 | −0.0613 | −0.0069 | −0.0004 | 0.4483 | 14.5963 | 0.5164 | 0.8470 | 0.06 | |

| 2.44 | −13.43 | −8.97 | −6.04 | 3.42 | 0.41 | 0.45 | 2.65 | ||

| Panel C: Latin America markets | |||||||||

| 0.4713 | −0.0132 | −0.0030 | −0.0001 | 0.4692 | 25.2113 | 0.4703 | 0.7741 | 0.01 | |

| 2.36 | −6.41 | −7.03 | −12.28 | 3.15 | 0.50 | 0.54 | 2.13 | ||

| −3.1065 | −0.0359 | −0.0048 | −0.0001 | 2.7365 | 13.1636 | 1.0070 | 0.3709 | 0.06 | |

| −4.58 | −19.23 | −3.10 | −3.08 | 4.43 | 1.06 | 1.48 | 1.08 | ||

| −0.2194 | 0.0014 | −0.0003 | −0.0001 | 1.1443 | 1.6039 | 0.1039 | 0.8855 | 0.01 | |

| −0.61 | 1.63 | −0.11 | −2.29 | 3.23 | 0.56 | 1.23 | 8.29 | ||

| 0.9026 | −0.0182 | −0.0037 | −0.0001 | 0.2543 | 1.9193 | 0.6885 | 0.8396 | 0.01 | |

| 9.74 | −14.62 | −3.42 | −3.16 | 1.96 | 0.33 | 0.81 | 4.48 | ||

| Mean | Median | Maximum | Minimum | Std. Dev. | Skewness | Kurtosis | Observations | |

|---|---|---|---|---|---|---|---|---|

| Panel A | ||||||||

| 0.7599 | 0.7592 | 0.9626 | 0.4668 | 0.0650 | −0.4153 | 5.2704 | 380 | |

| 0.7098 | 0.7305 | 0.9169 | 0.3101 | 0.1212 | −0.7925 | 3.1743 | 380 | |

| 0.7196 | 0.7490 | 0.9377 | 0.2030 | 0.1324 | −1.2736 | 4.6736 | 380 | |

| 0.5984 | 0.6500 | 0.8452 | 0.0433 | 0.1823 | −0.8441 | 2.7822 | 380 | |

| 0.7616 | 0.7894 | 0.8994 | 0.4273 | 0.0836 | −1.3870 | 5.0310 | 380 | |

| 0.5307 | 0.5473 | 0.7848 | 0.2251 | 0.1095 | −0.3409 | 2.3949 | 380 | |

| Panel B | ||||||||

| 0.2455 | 0.2651 | 0.4955 | −0.1083 | 0.1102 | −0.3254 | 2.7438 | 327 | |

| 0.3956 | 0.4421 | 0.8556 | −0.2723 | 0.2371 | −0.7024 | 2.8191 | 379 | |

| 0.5141 | 0.5690 | 0.8507 | −0.0075 | 0.2136 | −0.8048 | 2.6565 | 380 | |

| 0.6077 | 0.6150 | 0.7789 | 0.1657 | 0.0947 | −1.0525 | 5.2400 | 380 | |

| Panel C | ||||||||

| 0.5565 | 0.5742 | 0.6860 | 0.2852 | 0.0796 | −1.0028 | 3.8424 | 325 | |

| 0.3911 | 0.4086 | 0.6213 | −0.3459 | 0.1327 | −1.6380 | 8.9068 | 380 | |

| −0.0573 | −0.0755 | 0.1674 | −0.2240 | 0.0821 | 0.4818 | 2.3176 | 353 | |

| 0.5820 | 0.6234 | 0.8478 | −0.0773 | 0.1549 | −0.9141 | 3.9936 | 380 |

| EPU_CA | EPU_FR | EPU_GM | EPU_IT | EPU_UK | EPU_JP | |

|---|---|---|---|---|---|---|

| EPU_US | 0.75 | 0.60 | 0.72 | 0.54 | 0.43 | 0.46 |

| 19.59 | 12.88 | 17.95 | 10.92 | 8.20 | 8.82 | |

| EPU_CN | EPU_IN | EPU_KO | EPU_SG | |||

| EPU_US | 0.57 | 0.49 | 0.58 | 0.75 | ||

| 10.05 | 8.27 | 10.38 | 16.73 | |||

| EPU_BR | EPU_CE | EPU_CO | EPU_MX | |||

| EPU_US | 0.27 | 0.19 | −0.04 | 0.01 | ||

| 4.44 | 3.09 | −0.64 | 0.20 |

| Correlation | ||||||||

|---|---|---|---|---|---|---|---|---|

| 0.3082 | 0.0540 | 0.0214 | 0.0572 | 0.0013 | 1.7428 | 0.1414 | 0.15 | |

| 14.64 | 12.15 | 6.30 | 9.65 | 2.08 | 2.06 | 0.74 | ||

| 0.3529 | 0.0661 | 0.0446 | 0.0135 | 0.0012 | 2.1691 | 0.0570 | 0.07 | |

| 12.28 | 10.77 | 15.30 | 2.01 | 1.53 | 2.19 | 0.27 | ||

| 0.1359 | 0.1280 | 0.0100 | 0.0035 | 0.0067 | 3.7468 | 0.0504 | 0.08 | |

| 3.83 | 17.05 | 4.34 | 0.37 | 0.92 | 1.58 | 0.22 | ||

| 0.3709 | 0.0881 | 0.0200 | −0.0252 | 0.0011 | 3.9813 | 0.0546 | 0.11 | |

| 20.82 | 33.51 | 5.25 | −5.91 | 1.30 | 1.54 | 0.19 | ||

| 0.7733 | 0.0001 | 0.0002 | 0.0104 | 0.0001 | 0.4253 | 0.5873 | 0.14 | |

| 116.38 | 3.18 | 4.50 | 3.95 | 2.56 | 4.37 | 10.45 | ||

| −0.2949 | 0.1565 | 0.0421 | 0.0163 | 0.0034 | 2.5370 | 0.0474 | 0.15 | |

| −22.56 | 71.34 | 17.99 | 14.70 | 1.79 | 2.08 | 0.30 | ||

| 0.0437 | 0.1389 | 0.0811 | −0.1321 | 0.0019 | 1.6032 | 0.1353 | 0.35 | |

| 0.97 | 14.33 | 15.48 | −9.34 | 1.41 | 1.82 | 0.56 | ||

| 0.1419 | 0.0132 | 0.0505 | 0.0366 | 0.0028 | 3.6815 | −0.0009 | 0.11 | |

| 6.37 | 2.49 | 10.77 | 4.04 | 1.05 | 1.43 | −0.01 | ||

| −0.3811 | 0.1441 | 0.1680 | 0.0769 | 0.0135 | 2.5987 | 0.0766 | 0.21 | |

| −8.91 | 12.55 | 20.43 | 4.53 | 1.33 | 1.56 | 0.30 | ||

| 0.4040 | −0.0143 | 0.0081 | 0.1124 | 0.0017 | 2.5554 | 0.0895 | 0.12 | |

| 21.49 | −2.91 | 2.82 | 14.39 | 1.99 | 2.28 | 0.44 | ||

| −0.2211 | 0.0141 | 0.0214 | 0.1649 | 0.0428 | 1.9290 | −0.1092 | 0.05 | |

| −3.89 | 1.78 | 6.66 | 15.73 | 2.81 | 1.90 | −1.38 | ||

| −0.0275 | 0.0680 | 0.0706 | 0.0629 | 0.0055 | 2.9306 | 0.0574 | 0.13 | |

| −0.67 | 7.49 | 10.33 | 6.85 | 1.02 | 1.50 | 0.20 | ||

| −0.0488 | 0.0877 | 0.0069 | −0.0168 | 0.0011 | 2.3848 | 0.2668 | 0.05 | |

| −3.14 | 14.20 | 37.91 | −3.03 | 0.91 | 1.41 | 0.91 | ||

| −0.2679 | 0.1921 | 0.0406 | 0.0210 | 0.0019 | 1.7879 | 0.1860 | 0.01 | |

| −8.79 | 21.44 | 8.67 | 2.18 | 1.66 | 2.18 | 1.38 |

| Correlation | ||||||||

|---|---|---|---|---|---|---|---|---|

| 0.7527 | −0.0001 | −0.0001 | 0.0041 | 0.0006 | 1.4384 | 0.4245 | 0.11 | |

| 48.58 | −3.85 | −4.03 | 21.38 | 1.11 | 1.60 | 1.81 | ||

| 0.6756 | −0.0003 | 0.0008 | −0.0041 | 0.0009 | 1.1234 | 0.1216 | 0.02 | |

| 87.59 | −9.71 | 11.56 | −6.81 | 4.53 | 5.68 | 2.03 | ||

| 0.6976 | 0.0000 | 0.0008 | −0.0006 | 0.0019 | 1.1669 | 0.2340 | 0.02 | |

| 95.73 | −3.20 | 19.98 | −3.59 | 1.98 | 3.25 | 2.46 | ||

| 0.5955 | −0.0003 | 0.0010 | −0.0014 | 0.0016 | 4.0129 | 0.0697 | 0.05 | |

| 109.28 | −10.86 | 23.64 | −3.53 | 0.99 | 1.72 | 0.32 | ||

| 0.7351 | −0.0001 | 0.0007 | −0.0014 | 0.0014 | 3.1169 | 0.0965 | 0.03 | |

| 76.94 | −17.96 | 25.99 | −9.75 | 1.43 | 1.74 | 0.48 | ||

| 0.4487 | 0.0001 | 0.0009 | −0.0022 | 0.0016 | 4.5319 | 0.0904 | 0.05 | |

| 129.54 | 3.79 | 114.14 | −5.36 | 1.19 | 1.74 | 0.46 | ||

| 0.2810 | 0.0004 | −0.0004 | −0.0011 | 0.0079 | 3.8101 | 0.1116 | 0.14 | |

| 80.30 | 20.79 | −12.32 | −4.57 | 1.08 | 1.21 | 0.37 | ||

| 0.5689 | 0.0003 | −0.0006 | 0.0109 | 0.0081 | 5.3505 | 0.0813 | 0.03 | |

| 94.98 | 12.87 | −7.76 | 27.61 | 0.99 | 1.25 | 0.27 | ||

| 0.4079 | 0.0005 | 0.0014 | −0.0023 | 0.0053 | 4.3679 | −0.0254 | 0.02 | |

| 57.36 | 12.46 | 19.16 | −4.65 | 2.52 | 2.31 | −1.53 | ||

| 0.6785 | 0.0003 | −0.0004 | 0.0011 | 0.0007 | 0.4594 | 0.3534 | 0.04 | |

| 57.29 | 2.79 | −3.04 | 2.48 | 2.52 | 3.57 | 3.11 | ||

| 0.5954 | 0.0001 | −0.0001 | −0.0033 | 0.0005 | 1.1062 | 0.1413 | 0.02 | |

| 84.64 | 3.64 | −2.03 | −5.65 | 2.80 | 3.03 | 1.01 | ||

| 0.4192 | 0.0001 | −0.0001 | −0.0006 | 0.0100 | 5.3182 | −0.0499 | 0.01 | |

| 90.98 | 3.13 | −2.29 | −7.72 | 1.29 | 1.33 | −0.17 | ||

| −0.0954 | 0.0001 | −0.0002 | −0.0052 | 0.0003 | 0.7585 | 0.1739 | 0.02 | |

| −13.36 | 2.61 | −2.84 | −0.99 | 3.92 | 5.05 | 2.03 | ||

| 0.4171 | 0.0005 | 0.0012 | −0.0139 | 0.0007 | 0.0941 | 0.8695 | 0.04 | |

| 17.17 | 4.76 | 4.48 | −1.77 | 2.58 | 3.86 | 30.75 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chiang, T.C. Evidence of Economic Policy Uncertainty and COVID-19 Pandemic on Global Stock Returns. J. Risk Financial Manag. 2022, 15, 28. https://doi.org/10.3390/jrfm15010028

Chiang TC. Evidence of Economic Policy Uncertainty and COVID-19 Pandemic on Global Stock Returns. Journal of Risk and Financial Management. 2022; 15(1):28. https://doi.org/10.3390/jrfm15010028

Chicago/Turabian StyleChiang, Thomas Chinan. 2022. "Evidence of Economic Policy Uncertainty and COVID-19 Pandemic on Global Stock Returns" Journal of Risk and Financial Management 15, no. 1: 28. https://doi.org/10.3390/jrfm15010028

APA StyleChiang, T. C. (2022). Evidence of Economic Policy Uncertainty and COVID-19 Pandemic on Global Stock Returns. Journal of Risk and Financial Management, 15(1), 28. https://doi.org/10.3390/jrfm15010028