Impact of Elimination of Dividend Distribution Tax on Indian Corporate Firms Amid COVID Disruptions

Abstract

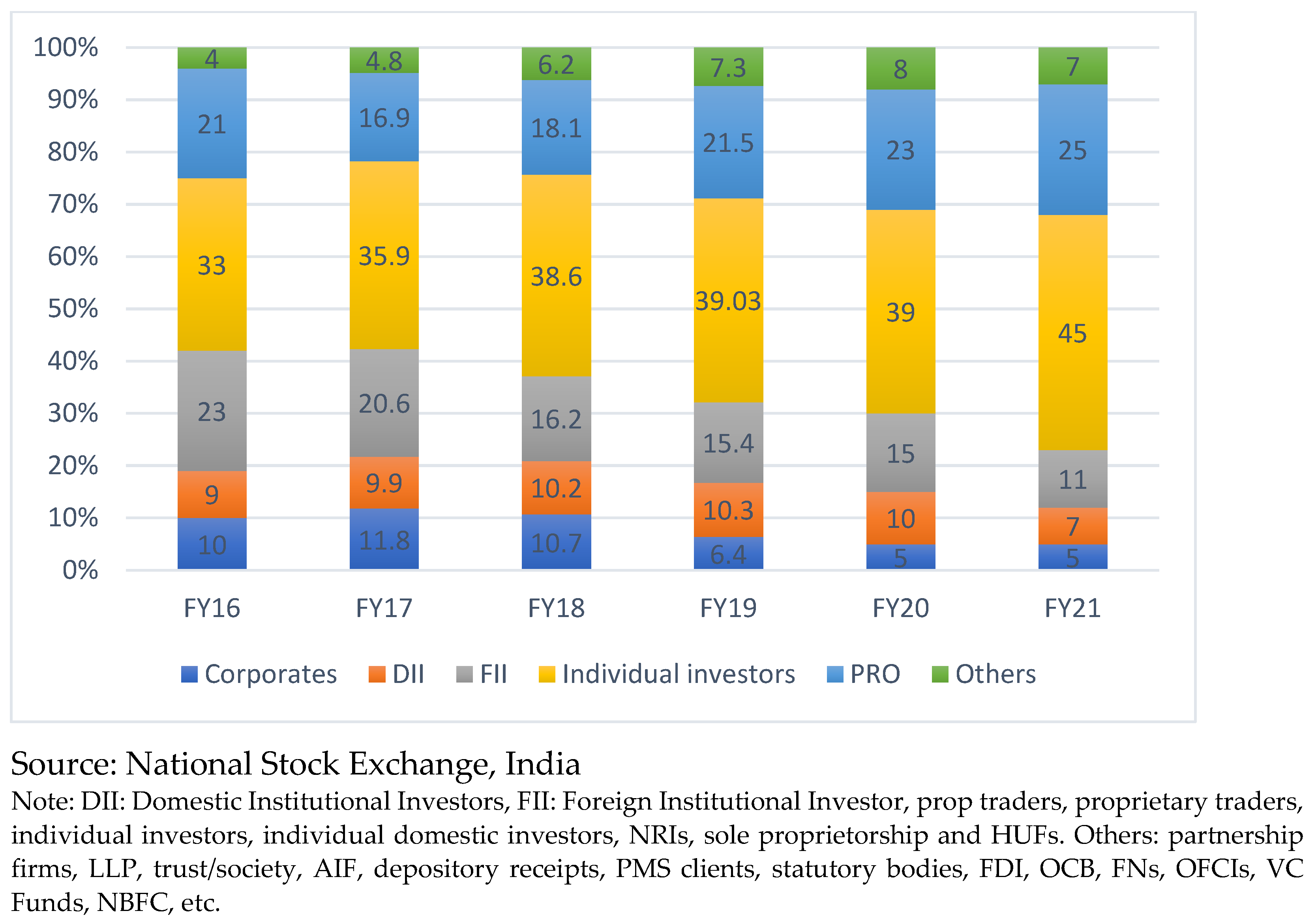

1. Introduction

2. Literature Review

2.1. Profitability

2.2. Free Cash Flow

2.3. Financing and Investment Decisions

2.4. Growth Rate

2.5. Leverage

2.6. Investors’ Expectation

2.7. Environment

2.8. Taxes

2.9. DDT Elimination in India and Dividend-Payout

3. Research Methodology

3.1. Objectives

3.2. Sample Firms and Data

3.3. Variables of the Study

3.3.1. Dependent Variables and the Proxy Measures Used

3.3.2. Independent Variables

3.4. Research Model

- Dummy2020 = Dummy variable for year 2020;

- Dummy2021 = Dummy variable for year 2021;

- DivPeri,t = Dividend payout percentage of firm i at time period t;

- EBITDAi,t = Earnings before interest, taxes, depreciation and amortization;

- LogTAi,t = Natural log of total assets;

- BVSi,t = Book value per share;

- CFi,t = EBITDA interest taxes dividend;

- FCFi,t = CF*1/Total assets;

- ROTAi,t = EBITDA/Total assets;

- MBVRi,t = Proxy of market premium = Market cap/Net worth;

- DEi,t = Debt–equity ratio = Total debt/Equity funds;

- EBITDARi,t = EBITDA/Net sales;

- Taxi,t = Corporate tax rate = Provision for taxes/Earnings before taxes;

- LagDivi,t = DivPert−1;

- ɛi,t = Error term;

- DivCut = Dummy variable for dividend cut;

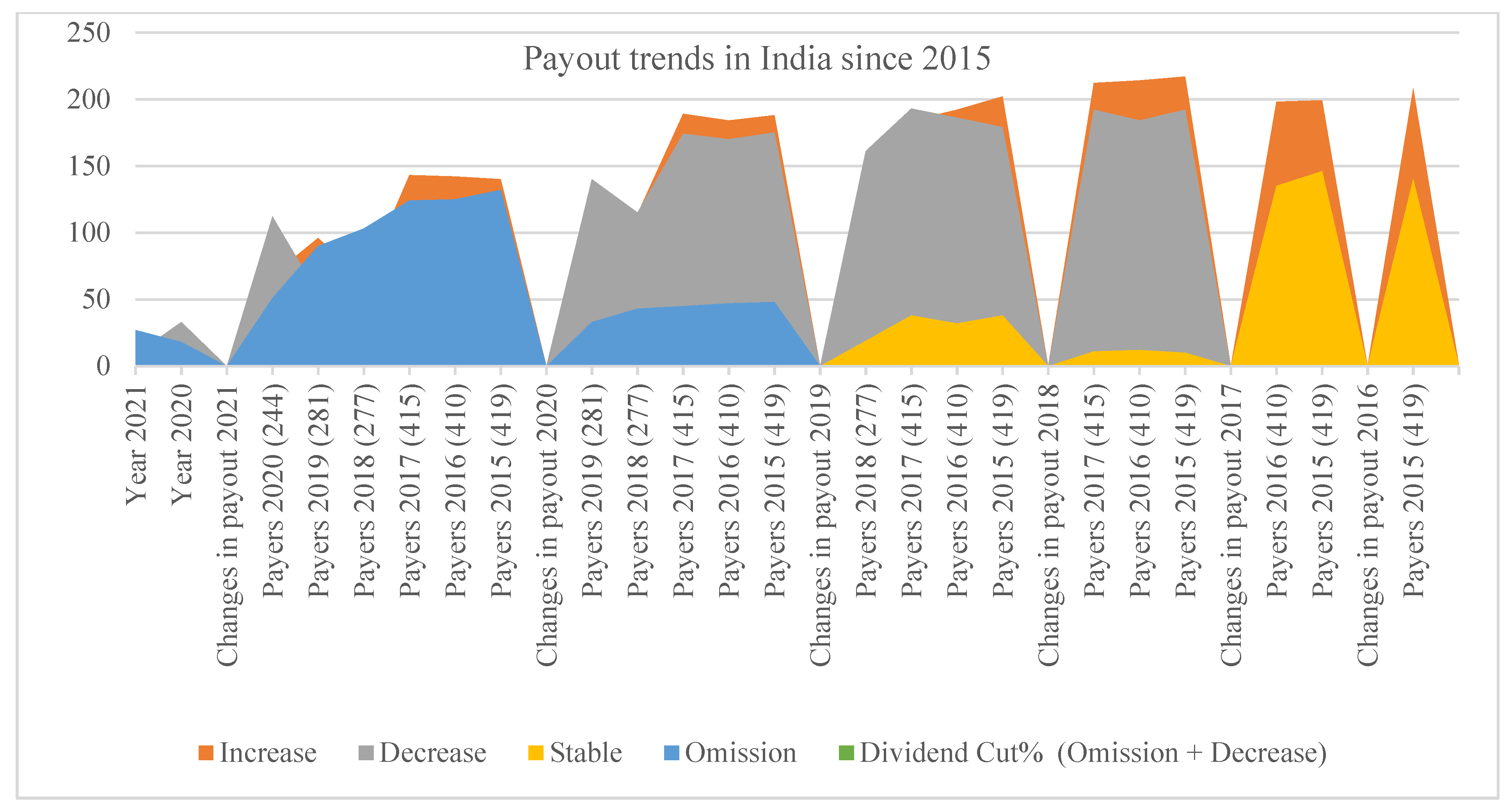

4. Empirical Findings

4.1. Impact of the DDT Elimination under Finance Act 2020 on the Corporate Dividend Behavior

4.2. Determinants of Changing Dividend Behavior

4.2.1. Determinants of Dividend Payout

4.2.2. Determinants of Changing Dividend Payouts and Dividend Cuts

5. Discussion

6. Concluding Observation

Funding

Institutional Review Board Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Sample Firms Analyzed

| 1 | Carborundum Universal Ltd. |

| 2 | Grindwell Norton Ltd. |

| 3 | Bombay Burmah Trading Corporation Ltd. |

| 4 | Gujarat Ambuja Exports Ltd. |

| s5 | Tata Coffee Ltd. |

| 6 | GM Breweries Ltd. |

| 7 | United Breweries Ltd. |

| 8 | Alicon Castalloy Ltd. |

| 9 | Apollo Tyres Ltd. |

| 10 | Atul Auto Ltd. |

| 11 | Automotive Axles Ltd. |

| 12 | Bajaj Auto Ltd. |

| 13 | Banco Products (India) Ltd. |

| 14 | Endurance Technologies Ltd. |

| 15 | Escorts Ltd. |

| 16 | Exide Industries Ltd. |

| 17 | Gabriel India Ltd. |

| 18 | GP Petroleums Ltd. |

| 19 | Hindustan Composites Ltd. |

| 20 | Hi-Tech Gears Ltd. |

| 21 | Jamna Auto Industries Ltd. |

| 22 | JK Tyre & Industries Ltd. |

| 23 | JTEKT India Ltd. |

| 24 | LG Balakrishnan & Brothers Ltd. |

| 25 | Lumax Auto Technologies Ltd. |

| 26 | Maharashtra Scooters Ltd. |

| 27 | Mahindra & Mahindra Ltd. |

| 28 | Man Industries (India) Ltd. |

| 29 | Panama Petrochem Ltd. |

| 30 | Rico Auto Industries Ltd. |

| 31 | Sandhar Technologies Ltd. |

| 32 | Shanthi Gears Ltd. |

| 33 | Sterling Tools Ltd. |

| 34 | Swaraj Engines Ltd. |

| 35 | Tide Water Oil Company (India) Ltd. |

| 36 | Timken India Ltd. |

| 37 | TVS Srichakra Ltd. |

| 38 | Wabco India Ltd. |

| 39 | AIA Engineering Ltd. |

| 40 | Alphageo (India) Ltd. |

| 41 | Apar Industries Ltd. |

| 42 | Bharat Electronics Ltd. |

| 43 | Engineers India Ltd. |

| 44 | GMM Pfaudler Ltd. |

| 45 | Graphite India Ltd. |

| 46 | Ingersoll-Rand (India) Ltd. |

| 47 | Kirloskar Brothers Ltd. |

| 48 | Orient Abrasives Ltd. |

| 49 | Orient Refractories Ltd. |

| 50 | Rites Ltd. |

| 51 | Thermax Ltd. |

| 52 | Vesuvius India Ltd. |

| 53 | Aarti Industries Ltd. |

| 54 | Akzo Nobel India Ltd. |

| 55 | Alkyl Amines Chemicals Ltd. |

| 56 | Apcotex Industries Ltd. |

| 57 | Balaji Amines Ltd. |

| 58 | BASF India Ltd. |

| 59 | Bhansali Engineering Polymers Ltd. |

| 60 | Bharat Rasayan Ltd. |

| 61 | Chambal Fertilisers & Chemicals Ltd. |

| 62 | Coromandel International Ltd. |

| 63 | Deepak Fertilisers & Petrochemicals Corporation Ltd. |

| 64 | Dhanuka Agritech Ltd. |

| 65 | Dhunseri Ventures Ltd. |

| 66 | Gujarat State Fertilizers & Chemicals Ltd. |

| 67 | Kansai Nerolac Paints Ltd. |

| 68 | Nocil Ltd. |

| 69 | Oriental Carbon & Chemicals Ltd. |

| 70 | PI Industries Ltd. |

| 71 | Privi Speciality Chemicals Ltd. |

| 72 | Rallis India Ltd. |

| 73 | Rashtriya Chemicals & Fertilizers Ltd. |

| 74 | Sharda Cropchem Ltd. |

| 75 | Supreme Petrochem Ltd. |

| 76 | UPL Ltd. |

| 77 | Vidhi Specialty Food Ingredients Ltd. |

| 78 | Vinati Organics Ltd. |

| 79 | Ambuja Cements Ltd. |

| 80 | Century Plyboards (India) Ltd. |

| 81 | Everest Industries Ltd. |

| 82 | Greenply Industries Ltd. |

| 83 | JK Cement Ltd. |

| 84 | JK Lakshmi Cement Ltd. |

| 85 | Pokarna Ltd. |

| 86 | Ramco Industries Ltd. |

| 87 | Shree Cement Ltd. |

| 88 | Somany Ceramics Ltd. |

| 89 | The Ramco Cements Ltd. |

| 90 | Ultratech Cement Ltd. |

| 91 | Dixon Technologies (India) Ltd. |

| 92 | KDDL Ltd. |

| 93 | Symphony Ltd. |

| 94 | Hindustan Petroleum Corporation Ltd. |

| 95 | Indian Oil Corporation Ltd. |

| 96 | Oil & Natural Gas Corporation Ltd. |

| 97 | Oricon Enterprises Ltd. |

| 98 | Reliance Industries Ltd. |

| 99 | Rajesh Exports Ltd. |

| 100 | Titan Company Ltd. |

| 101 | Birla Corporation Ltd. |

| 102 | Century Textiles & Industries Ltd. |

| 103 | DCM Shriram Ltd. |

| 104 | SRF Ltd. |

| 105 | Surya Roshni Ltd. |

| 106 | Texmaco Infrastructure & Holdings Ltd. |

| 107 | Centum Electronics Ltd. |

| 108 | Maithan Alloys Ltd. |

| 109 | Avanti Feeds Ltd. |

| 110 | AVT Natural Products Ltd. |

| 111 | Bajaj Consumer Care Ltd. |

| 112 | Britannia Industries Ltd. |

| 113 | Emami Ltd. |

| 114 | Galaxy Surfactants Ltd. |

| 115 | Gillette India Ltd. |

| 116 | Godfrey Phillips India Ltd. |

| 117 | Hatsun Agro Products Ltd. |

| 118 | Heritage Foods Ltd. |

| 119 | Hindustan Unilever Ltd. |

| 120 | Jyothy Labs Ltd. |

| 121 | KRBL Ltd. |

| 122 | Marico Ltd. |

| 123 | Mirza International Ltd. |

| 124 | Relaxo Footwears Ltd. |

| 125 | Tasty Bite Eatables Ltd. |

| 126 | Tata Consumer Products Ltd. |

| 127 | VST Industries Ltd. |

| 128 | Mahanagar Gas Ltd. |

| 129 | Aarti Drugs Ltd. |

| 130 | Alembic Ltd. |

| 131 | Alembic Pharmaceuticals Ltd. |

| 132 | Aurobindo Pharma Ltd. |

| 133 | Caplin Point Laboratories Ltd. |

| 134 | Cipla Ltd. |

| 135 | Divis Laboratories Ltd. |

| 136 | Dr. Lal Pathlabs Ltd. |

| 137 | Hester Biosciences Ltd. |

| 138 | Hikal Ltd. |

| 139 | Jubilant Pharmova Ltd. |

| 140 | Lupin Ltd. |

| 141 | Natco Pharma Ltd. |

| 142 | Nectar Lifesciences Ltd. |

| 143 | Pfizer Ltd. |

| 144 | Piramal Enterprises Ltd. |

| 145 | RPG Life Sciences Ltd. |

| 146 | SMS Pharmaceuticals Ltd. |

| 147 | Strides Pharma Science Ltd. |

| 148 | Torrent Pharmaceuticals Ltd. |

| 149 | Indraprastha Gas Ltd. |

| 150 | GE Power India Ltd. |

| 151 | Indian Hume Pipe Company Ltd. |

| 152 | Ircon International Ltd. |

| 153 | J Kumar Infraproject Ltd. |

| 154 | KEC International Ltd. |

| 155 | KNR Construction Ltd. |

| 156 | Larsen & Toubro Ltd. |

| 157 | Power Mech Projects Ltd. |

| 158 | Vindhya Telelinks Ltd. |

| 159 | Maharashtra Seamless Ltd. |

| 160 | Sarda Energy & Minerals Ltd. |

| 161 | Tata Steel Ltd. |

| 162 | Tinplate Company Of India Ltd. |

| 163 | Welspun Corp Ltd. |

| 164 | Accelya Solutions India Ltd. |

| 165 | Aptech Ltd. |

| 166 | Cyient Ltd. |

| 167 | eClerx Services Ltd. |

| 168 | Hinduja Global Solutions Ltd. |

| 169 | Info Edge (India) Ltd. |

| 170 | Infosys Ltd. |

| 171 | Larsen & Toubro Infotech Ltd. |

| 172 | Mastek Ltd. |

| 173 | Mphasis Ltd. |

| 174 | Nucleus Software Exports Ltd. |

| 175 | Persistent Systems Ltd. |

| 176 | Quick Heal Technologies Ltd. |

| 177 | Sasken Technologies Ltd. |

| 178 | Adani Ports and Special Economic Zone Ltd. |

| 179 | Gateway Distriparks Ltd. |

| 180 | DB Corp Ltd. |

| 181 | Entertainment Network (India) Ltd. |

| 182 | NXT Digital Ltd. |

| 183 | Sandesh Ltd. |

| 184 | Saregama India Ltd. |

| 185 | Zee Entertainment Enterprises Ltd. |

| 186 | Coal India Ltd. |

| 187 | Gujarat Mineral Development Corporation Ltd. |

| 188 | NMDC Ltd. |

| 189 | Gravita India Ltd. |

| 190 | Hindustan Zinc Ltd. |

| 191 | National Aluminium Company Ltd. |

| 192 | Seshasayee Paper & Boards Ltd. |

| 193 | Tamil Nadu Newsprint & Papers Ltd. |

| 194 | Astral Ltd. |

| 195 | Cosmo Films Ltd. |

| 196 | EPL Ltd. |

| 197 | Mold-Tek Packaging Ltd. |

| 198 | Polyplex Corporation Ltd. |

| 199 | Time Technoplast Ltd. |

| 200 | NTPC Ltd. |

| 201 | SJVN Ltd. |

| 202 | Tata Power Company Ltd. |

| 203 | Torrent Power Ltd. |

| 204 | Care Ratings Ltd. |

| 205 | DLF Ltd. |

| 206 | JMC Projects (India) Ltd. |

| 207 | PSP Projects Ltd. |

| 208 | Sobha Ltd. |

| 209 | Sunteck Realty Ltd. |

| 210 | Cochin Shipyard Ltd. |

| 211 | Bombay Dyeing & Manufacturing Company Ltd. |

| 212 | Himatsingka Seide Ltd. |

| 213 | Jindal Worldwide Ltd. |

| 214 | Kewal Kiran Clothing Ltd. |

| 215 | Kitex Garments Ltd. |

| 216 | KPR Mill Ltd. |

| 217 | Mayur Uniquoters Ltd. |

| 218 | Page Industries Ltd. |

| 219 | Ruby Mills Ltd. |

| 220 | Swan Energy Ltd. |

| 221 | Trident Ltd. |

| 222 | Welspun India Ltd. |

| 223 | Zodiac Clothing Company Ltd. |

| 224 | Adani Enterprises Ltd. |

| 225 | Gujarat Gas Ltd. |

| 226 | Redington (India) Ltd. |

| 227 | Sakuma Exports Ltd. |

| 228 | Zuari Global Ltd. |

| 229 | Monsanto India Ltd.—(Amalgamated) |

| 230 | Wendt (India) Ltd. |

| 231 | Bannari Amman Sugars Ltd. |

| 232 | CCL Products (India) Ltd. |

| 233 | Radico Khaitan Ltd. |

| 234 | Amara Raja Batteries Ltd. |

| 235 | Balkrishna Industries Ltd. |

| 236 | Ceat Ltd. |

| 237 | Cummins India Ltd. |

| 238 | Fiem Industries Ltd. |

| 239 | Gandhi Special Tubes Ltd. |

| 240 | HBL Power Systems Ltd. |

| 241 | Hero MotoCorp Ltd. |

| 242 | India Nippon Electricals Ltd. |

| 243 | Jay Bharat Maruti Ltd. |

| 244 | JBM Auto Ltd. |

| 245 | Lumax Industries Ltd. |

| 246 | Maruti Suzuki India Ltd. |

| 247 | Menon Bearings Ltd. |

| 248 | Minda Corporation Ltd. |

| 249 | Minda Industries Ltd. |

| 250 | MM Forgings Ltd. |

| 251 | Motherson Sumi Systems Ltd. |

| 252 | Munjal Showa Ltd. |

| 253 | NRB Bearings Ltd. |

| 254 | Precision Camshafts Ltd. |

| 255 | Rane Brake Lining Ltd. |

| 256 | Savita Oil Technologies Ltd. |

| 257 | Srikalahasthi Pipes Ltd. |

| 258 | Subros Ltd. |

| 259 | Sundaram-Clayton Ltd. |

| 260 | Suprajit Engineering Ltd. |

| 261 | TVS Motor Company Ltd. |

| 262 | VST Tillers Tractors Ltd. |

| 263 | Wheels India Ltd. |

| 264 | Hindustan Aeronautics Ltd. |

| 265 | Ador Welding Ltd. |

| 266 | BEML Ltd. |

| 267 | Bharat Dynamics Ltd. |

| 268 | Elgi Equipments Ltd. |

| 269 | Genus Power Infrastructures Ltd. |

| 270 | Havells India Ltd. |

| 271 | Hercules Hoists Ltd. |

| 272 | Honda India Power Products Ltd. |

| 273 | HPL Electric & Power Ltd. |

| 274 | Igarashi Motors India Ltd. |

| 275 | Kirloskar Industries Ltd. |

| 276 | Kirloskar Oil Engines Ltd. |

| 277 | Nesco Ltd. |

| 278 | Praj Industries Ltd. |

| 279 | Shriram Pistons & Rings Ltd. |

| 280 | Siemens Ltd. |

| 281 | Skipper Ltd. |

| 282 | TD Power Systems Ltd. |

| 283 | V-Guard Industries Ltd. |

| 284 | Voltamp Transformers Ltd. |

| 285 | Asian Paints Ltd. |

| 286 | Atul Ltd. |

| 287 | Berger Paints India Ltd. |

| 288 | Bhageria Industries Ltd. |

| 289 | Deepak Nitrite Ltd. |

| 290 | Excel Industries Ltd. |

| 291 | GHCL Ltd. |

| 292 | GOCL Corporation Ltd. |

| 293 | Gujarat Alkalies & Chemicals Ltd. |

| 294 | Insecticides (India) Ltd. |

| 295 | Manali Petrochemicals Ltd. |

| 296 | Meghmani Organics Ltd. |

| 297 | Navin Fluorine International Ltd. |

| 298 | Pidilite Industries Ltd. |

| 299 | Plastiblends India Ltd. |

| 300 | Solar Industries (India) Ltd. |

| 301 | Sudarshan Chemical Industries Ltd. |

| 302 | Tata Chemicals Ltd. |

| 303 | ACC Ltd. |

| 304 | Cera Sanitaryware Ltd. |

| 305 | Deccan Cements Ltd. |

| 306 | HIL Ltd. |

| 307 | HSIL Ltd. |

| 308 | Kajaria Ceramics Ltd. |

| 309 | KCP Ltd. |

| 310 | La Opala RG Ltd. |

| 311 | Mangalam Cement Ltd. |

| 312 | Orient Cement Ltd. |

| 313 | Visaka Industries Ltd. |

| 314 | Blue Star Ltd. |

| 315 | Control Print Ltd. |

| 316 | Voltas Ltd. |

| 317 | Bharat Petroleum Corporation Ltd. |

| 318 | Oil India Ltd. |

| 319 | Thangamayil Jewellery Ltd. |

| 320 | Andhra Sugars Ltd. |

| 321 | Balmer Lawrie & Company Ltd. |

| 322 | Grasim Industries Ltd. |

| 323 | Finolex Cables Ltd. |

| 324 | KEI Industries Ltd. |

| 325 | Precision Wires India Ltd. |

| 326 | Agro Tech Foods Ltd. |

| 327 | Colgate-Palmolive (India) Ltd. |

| 328 | Dabur India Ltd. |

| 329 | Godrej Consumer Products Ltd. |

| 330 | ITC Ltd. |

| 331 | LT Foods Ltd. |

| 332 | Procter & Gamble Hygiene & Health Care Ltd. |

| 333 | VIP Industries Ltd. |

| 334 | Zydus Wellness Ltd. |

| 335 | Gujarat State Petronet Ltd. |

| 336 | Advanced Enzyme Technologies Ltd. |

| 337 | Alkem Laboratories Ltd. |

| 338 | Amrutanjan Health Care Ltd. |

| 339 | Apollo Hospitals Enterprise Ltd. |

| 340 | Bliss GVS Pharma Ltd. |

| 341 | Cadila Healthcare Ltd. |

| 342 | Dr. Reddys Laboratories Ltd. |

| 343 | Granules India Ltd. |

| 344 | Gufic Biosciences Ltd. |

| 345 | Indoco Remedies Ltd. |

| 346 | JB Chemicals & Pharmaceuticals Ltd. |

| 347 | Lincoln Pharmaceuticals Ltd. |

| 348 | Marksans Pharma Ltd. |

| 349 | Poly Medicure Ltd. |

| 350 | Shalby Ltd. |

| 351 | Shilpa Medicare Ltd. |

| 352 | Sun Pharmaceutical Industries Ltd. |

| 353 | TTK Healthcare Ltd. |

| 354 | Unichem Laboratories Ltd. |

| 355 | Advani Hotels & Resorts (India) Ltd. |

| 356 | Wonderla Holidays Ltd. |

| 357 | GAIL (India) Ltd. |

| 358 | IRB Infrastructure Developers Ltd. |

| 359 | Kalpataru Power Transmission Ltd. |

| 360 | Man InfraConstruction Ltd. |

| 361 | NCC Ltd. |

| 362 | Om Infra Ltd. |

| 363 | PNC Infratech Ltd. |

| 364 | Reliance Industrial Infrastructure Ltd. |

| 365 | Jindal Saw Ltd. |

| 366 | JSW Steel Ltd. |

| 367 | Mishra Dhatu Nigam Ltd. |

| 368 | Ratnamani Metals & Tubes Ltd. |

| 369 | Shankara Building Products Ltd. |

| 370 | 63 Moons Technologies Ltd. |

| 371 | Birlasoft Ltd. |

| 372 | HCL Technologies Ltd. |

| 373 | Mindtree Ltd. |

| 374 | Newgen Software Technologies Ltd. |

| 375 | Onmobile Global Ltd. |

| 376 | Sonata Software Ltd. |

| 377 | Tata Consultancy Services Ltd. |

| 378 | Tata Elxsi Ltd. |

| 379 | Tech Mahindra Ltd. |

| 380 | Vakrangee Ltd. |

| 381 | Wipro Ltd. |

| 382 | Zen Technologies Ltd. |

| 383 | Zensar Technologies Ltd. |

| 384 | Aegis Logistics Ltd. |

| 385 | Allcargo Logistics Ltd. |

| 386 | Container Corporation Of India Ltd. |

| 387 | The Great Eastern Shipping Company Ltd. |

| 388 | Transport Corporation Of India Ltd. |

| 389 | Balaji Telefilms Ltd. |

| 390 | Navneet Education Ltd. |

| 391 | PVR Ltd. |

| 392 | Sun TV Network Ltd. |

| 393 | TV Today Network Ltd. |

| 394 | MOIL Ltd. |

| 395 | Delta Corp Ltd. |

| 396 | Hindalco Industries Ltd. |

| 397 | Vedanta Ltd. |

| 398 | Orient Paper & Industries Ltd. |

| 399 | Finolex Industries Ltd. |

| 400 | Jai Corp Ltd. |

| 401 | Jindal Poly Films Ltd. |

| 402 | Nilkamal Ltd. |

| 403 | Responsive Industries Ltd. |

| 404 | Supreme Industries Ltd. |

| 405 | Uflex Ltd. |

| 406 | CESC Ltd. |

| 407 | Gujarat Industries Power Company Ltd. |

| 408 | India Power Corporation Ltd. |

| 409 | Nava Bharat Ventures Ltd. |

| 410 | NHPC Ltd. |

| 411 | NLC India Ltd. |

| 412 | Power Grid Corporation Of India Ltd. |

| 413 | CRISIL Ltd. |

| 414 | Ajmera Realty & Infra India Ltd. |

| 415 | Anant Raj Ltd. |

| 416 | Ashiana Housing Ltd. |

| 417 | Brigade Enterprises Ltd. |

| 418 | Dilip Buildcon Ltd. |

| 419 | Prestige Estate Projects Ltd. |

| 420 | Trent Ltd. |

| 421 | Garden Reach Shipbuilders & Engineers Ltd. |

| 422 | Astra Microwave Products Ltd. |

| 423 | Bharti Airtel Ltd. |

| 424 | Indus Towers Ltd. |

| 425 | Tata Communications Ltd. |

| 426 | Century Enka Ltd. |

| 427 | Ganesha Ecosphere Ltd. |

| 428 | Garware Technical Fibres Ltd. |

| 429 | Lakshmi Machine Works Ltd. |

| 430 | Lux Industries Ltd. |

| 431 | Nitin Spinners Ltd. |

| 432 | Rupa & Company Ltd. |

| 433 | Siyaram Silk Mills Ltd. |

| 434 | Sutlej Textiles & Industries Ltd. |

| 435 | Weizmann Ltd. |

| 436 | India Motor Parts & Accessories Ltd. |

| 437 | Sundram Fasteners Ltd. |

| 438 | VenkyS (India) Ltd. |

| 439 | Som Distilleries & Breweries Ltd. |

| 440 | Castrol India Ltd. |

| 441 | Greaves Cotton Ltd. |

| 442 | Harita Seating Systems Ltd. |

| 443 | Nelcast Ltd. |

| 444 | Ramkrishna Forgings Ltd. |

| 445 | Rane (Madras) Ltd. |

| 446 | Schaeffler India Ltd. |

| 447 | Setco Automotive Ltd. |

| 448 | SML Isuzu Ltd. |

| 449 | Steel Strips Wheels Ltd. |

| 450 | Titagarh Wagons Ltd. |

| 451 | Ucal Fuel Systems Ltd. |

| 452 | Varroc Engineering Ltd. |

| 453 | Interglobe Aviation Ltd. |

| 454 | ABB India Ltd. |

| 455 | Bharat Heavy Electricals Ltd. |

| 456 | Elecon Engineering Company Ltd. |

| 457 | GE T&D India Ltd. |

| 458 | KSB Ltd. |

| 459 | Foseco India Ltd. |

| 460 | Godrej Industries Ltd. |

| 461 | Jayant Agro-Organics Ltd. |

| 462 | Vikas EcoTech Ltd. |

| 463 | Bajaj Electricals Ltd. |

| 464 | Johnson Controls—Hitachi Air Conditioning India Ltd. |

| 465 | Deep Energy Resources Ltd. |

| 466 | Rain Industries Ltd. |

| 467 | Bhartiya International Ltd. |

| 468 | DFM Foods Ltd. |

| 469 | Glaxosmithkline Consumer Healthcare Ltd.—(Amalgamated) |

| 470 | Vadilal Industries Ltd. |

| 471 | Biocon Ltd. |

| 472 | Glenmark Pharmaceuticals Ltd. |

| 473 | Indraprastha Medical Corporation Ltd. |

| 474 | Sanofi India Ltd. |

| 475 | Suven Life Sciences Ltd. |

| 476 | Asian Hotels (West) Ltd. |

| 477 | EIH Associated Hotels Ltd. |

| 478 | EIH Ltd. |

| 479 | India Tourism Development Corporation Ltd. |

| 480 | Linde India Ltd. |

| 481 | Petronet LNG Ltd. |

| 482 | Sadbhav Engineering Ltd. |

| 483 | Simplex Infrastructures Ltd. |

| 484 | APL Apollo Tubes Ltd. |

| 485 | Gallantt Ispat Ltd. |

| 486 | Tata Steel Long Products Ltd. |

| 487 | Genesys International Corporation Ltd. |

| 488 | Hexaware Technologies Ltd. |

| 489 | Take Solutions Ltd. |

| 490 | Blue Dart Express Ltd. |

| 491 | GATI Ltd. |

| 492 | HT Media Ltd. |

| 493 | Shemaroo Entertainment Ltd. |

| 494 | Crest Ventures Ltd. |

| 495 | Huhtamaki India Ltd. |

| 496 | Jain Irrigation Systems Ltd. |

| 497 | Kolte Patil Developers Ltd. |

| 498 | Mahindra Lifespace Developers Ltd. |

| 499 | Oberoi Realty Ltd. |

| 500 | Omaxe Ltd. |

| 501 | Phoenix Mills Ltd. |

| 502 | Puravankara Ltd. |

| 503 | Future Lifestyle Fashions Ltd. |

| 504 | Shoppers Stop Ltd. |

| 505 | V-Mart Retail Ltd. |

| 506 | Arvind Ltd. |

| 507 | Raymond Ltd. |

| 508 | Vardhman Textiles Ltd. |

| 509 | MMTC Ltd. |

Appendix B. Regular Payer Firms

| 6 | GM Breweries Ltd. |

| 7 | United Breweries Ltd. |

| 12 | Bajaj Auto Ltd. |

| 18 | GP Petroleums Ltd. |

| 74 | Sharda Cropchem Ltd. |

| 75 | Supreme Petrochem Ltd. |

| 136 | Dr. Lal Pathlabs Ltd. |

| 146 | SMS Pharmaceuticals Ltd. |

| 153 | J Kumar Infraproject Ltd. |

| 163 | Welspun Corp Ltd. |

| 212 | Himatsingka Seide Ltd. |

| 213 | Jindal Worldwide Ltd. |

| 227 | Sakuma Exports Ltd. |

| 232 | CCL Products (India) Ltd. |

| 233 | Radico Khaitan Ltd. |

| 240 | HBL Power Systems Ltd. |

| 247 | Menon Bearings Ltd. |

| 250 | MM Forgings Ltd. |

| 273 | HPL Electric & Power Ltd. |

| 274 | Igarashi Motors India Ltd. |

| 279 | Shriram Pistons & Rings Ltd. |

| 283 | V-Guard Industries Ltd. |

| 295 | Manali Petrochemicals Ltd. |

| 300 | Solar Industries (India) Ltd. |

| 313 | Visaka Industries Ltd. |

| 319 | Thangamayil Jewellery Ltd. |

| 324 | KEI Industries Ltd. |

| 336 | Advanced Enzyme Technologies Ltd. |

| 338 | Amrutanjan Health Care Ltd. |

| 344 | Gufic Biosciences Ltd. |

| 347 | Lincoln Pharmaceuticals Ltd. |

| 358 | IRB Infrastructure Developers Ltd. |

| 371 | Birlasoft Ltd. |

| 375 | Onmobile Global Ltd. |

| 384 | Aegis Logistics Ltd. |

| 400 | Jai Corp Ltd. |

| 401 | Jindal Poly Films Ltd. |

| 403 | Responsive Industries Ltd. |

| 405 | Uflex Ltd. |

| 410 | NHPC Ltd. |

| 414 | Ajmera Realty & Infra India Ltd. |

| 417 | Brigade Enterprises Ltd. |

| 421 | Garden Reach Shipbuilders & Engineers Ltd. |

| 427 | Ganesha Ecosphere Ltd. |

| 430 | Lux Industries Ltd. |

| 431 | Nitin Spinners Ltd. |

| 432 | Rupa & Company Ltd. |

| 434 | Sutlej Textiles & Industries Ltd. |

| 435 | Weizmann Ltd. |

| 438 | VenkyS (India) Ltd. |

| 439 | Som Distilleries & Breweries Ltd. |

| 452 | Varroc Engineering Ltd. |

| 462 | Vikas EcoTech Ltd. |

| 464 | Johnson Controls—Hitachi Air Conditioning India Ltd. |

| 465 | Deep Energy Resources Ltd. |

| 467 | Bhartiya International Ltd. |

| 468 | DFM Foods Ltd. |

| 482 | Sadbhav Engineering Ltd. |

| 494 | HT Media Ltd. |

| 495 | Shemaroo Entertainment Ltd. |

| 498 | Jain Irrigation Systems Ltd. |

| 501 | Oberoi Realty Ltd. |

| 502 | Omaxe Ltd. |

| 505 | Future Lifestyle Fashions Ltd. |

| 506 | Shoppers Stop Ltd. |

Appendix C. Result of Factor Analysis Used for Extracting the Dependent Variables for the Study

{kind=link}

{kind=link}

| Components | ||||||||

|---|---|---|---|---|---|---|---|---|

| Factors | 1. Profitability | 2. Firm Size | 3. Book Value | 4.Cash Flows | 5.Investment Opportunity and Growth Rate | 6. Leverage | 7.Operating Profit | 8. Tax Rate |

| ShareholdersFunds | 0.933 | |||||||

| Networth | 0.931 | |||||||

| EBITDA | 0.898 | |||||||

| Netsales | 0.767 | |||||||

| Interest | 0.746 | |||||||

| EAT | 0.731 | 0.444 | ||||||

| LogTA | 0.375 | 0.894 | ||||||

| LogNetworth | 0.367 | 0.879 | ||||||

| LogSales | 0.333 | 0.840 | ||||||

| LogMcap | 0.834 | 0.327 | ||||||

| BVS | 0.972 | |||||||

| AdjBVS | 0.972 | |||||||

| EPS | 0.644 | 0.441 | ||||||

| Currentratio | 0.635 | 0.381 | ||||||

| C.F. | −0.889 | |||||||

| FCF | −0.810 | −0.354 | ||||||

| NetCA | −0.537 | 0.603 | ||||||

| LagDiv | 0.588 | |||||||

| ROTA | 0.811 | |||||||

| MBVratio | 0.776 | |||||||

| Debtequity | 0.943 | |||||||

| ROE | 0.506 | 0.769 | ||||||

| EBITDAmargin | 0.857 | |||||||

| Taxrate | 0.942 | |||||||

| IntCovergae | 0.313 | |||||||

Appendix D. Segregated Year-Wise Regression Results of Dividend Payout Determinants

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | ||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Model | B | Std. Error | Beta | B | Std. Error | Beta | B | Std. Error | Beta | B | Std. Error | Beta | B | Std. Error | Beta | B | Std. Error | Beta | B | Std. Error | Beta | |||||||

| (Constant) | −116.46 | 31.01 | *** | −68.78 | 34.68 | ** | −84.17 | 41.63 | ** | 77.38 | 48.98 | −20.6 | 59.9 | −46.52 | 96.94 | −404.66 | 114.05 | *** | ||||||||||

| BVS | 0.06 | 0.01 | 0.1 | *** | 0.01 | 0.01 | 0.02 | 0.01 | 0.01 | 0.02 | 0.05 | 0.02 | 0.04 | 0.07 | 0.02 | 0.07 | *** | 0.28 | 0.04 | 0.2 | *** | 0.2 | 0.09 | 0.05 | ** | |||

| CF | 0 | 0 | 0.11 | *** | 0 | 0 | 0.19 | *** | 0 | 0 | 0.01 | 0 | 0 | 0.13 | *** | 0 | 0 | 0.23 | *** | 0 | 0 | 0.36 | *** | 0 | 0 | 0.05 | ||

| Debtequity | 36.16 | 7.15 | 0.05 | *** | −29.19 | 10.17 | −0.04 | *** | −14.69 | 10.59 | −0.02 | −7.5 | 10.84 | −0.01 | −3.95 | 7.02 | −0.01 | −3.13 | 4.19 | −0.02 | −72.06 | 32.94 | −0.05 | ** | ||||

| EBITDA | 0 | 0.01 | −0.03 | 0 | 0.01 | −0.04 | −0.01 | 0.01 | −0.08 | −0.01 | 0 | −0.05 | 0 | 0 | 0.01 | 0 | 0.01 | −0.04 | −0.01 | 0.01 | −0.06 | |||||||

| FCF | −3.56 | 0.09 | −0.94 | *** | −3.15 | 0.1 | −0.81 | *** | −2.73 | 0.09 | −0.69 | *** | −3.28 | 0.1 | −0.76 | *** | −2.55 | 0.13 | −0.57 | *** | −5.25 | 0.21 | −1.18 | *** | −404.64 | 13.81 | −0.9 | *** |

| MBVratio | 0.52 | 0.96 | 0.01 | 2.77 | 1.49 | 0.03 | 1.71 | 1.61 | 0.02 | −5.45 | 1.84 | −0.05 | *** | 3.01 | 2.11 | 0.03 | 2.55 | 3.59 | 0.02 | 7.46 | 3.01 | 0.06 | ** | |||||

| ROTA | 48.77 | 75.54 | 0.01 | −137.2 | 84.98 | −0.03 | −254.54 | 94.62 | −0.05 | *** | −418.38 | 99.95 | −0.08 | *** | −452.85 | 135.95 | −0.08 | *** | −881.26 | 222.82 | −0.11 | *** | −329.33 | 165.43 | −0.05 | ** | ||

| Networth | 0 | 0 | 0.02 | 0 | 0 | 0.03 | 0 | 0 | 0.07 | 0 | 0 | 0.05 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | −0.02 | |||||||

| Taxrate | 1.87 | 2.43 | 0.01 | 3.27 | 22.01 | 0 | −0.59 | 1.95 | 0 | 0.44 | 2.44 | 0 | −1.75 | 41.52 | 0 | 7.69 | 10.14 | 0.02 | −0.69 | 25.13 | 0 | |||||||

| LogTA | 18.5 | 3.89 | 0.06 | *** | 19.51 | 4.23 | 0.08 | *** | 21.19 | 5.13 | 0.07 | *** | 4.2 | 6.05 | 0.01 | 10.98 | 6.98 | 0.03 | 26.64 | 11.85 | 0.06 | ** | 72.21 | 13.7 | 0.17 | *** | ||

| EBITDAR | −4.9 | 3.11 | −0.02 | −4.25 | 1.52 | −0.04 | *** | −4.32 | 3.7 | −0.02 | −12.52 | 12.98 | −0.02 | −14.03 | 10.95 | −0.02 | −126.03 | 31.15 | −0.12 | *** | 0.84 | 5.88 | 0 | |||||

| LagDiv | 0.15 | 0.02 | 0.13 | *** | 0.24 | 0.02 | 0.31 | *** | 0.4 | 0.02 | 0.35 | *** | 0.42 | 0.02 | 0.39 | *** | 0.63 | 0.03 | 0.59 | *** | 0 | 0.03 | 0 | 0.08 | 0.03 | 0.07 | *** | |

| R Square | 0.961 | 0.925 | 0.92 | 0.905 | 0.87 | 0.804 | 0.846 | |||||||||||||||||||||

| N | 508 | 507 | 507 | 507 | 504 | 451 | 331 |

| 1 | https://www.ceicdata.com/en/indicator/india/market-capitalization--nominal-gdp, (accessed on 31 December 2020). |

| 2 | https://www.rbi.org.in/Scripts/PublicationReportDetails.aspx?UrlPage=&ID=1167REPORTS, (accessed on 25 July 2021). |

| 3 | https://fortune.com/2021/01/27/india-fdi-foreign-investment-2020/, (accessed on 15 July 2021). |

| 4 | https://www.financialexpress.com/budget/finance-bill-2018-all-you-need-to-know/1045506/, (accessed on 2 June 2021). |

References

- Abdulkadir, Rihanat Idowu, Nur Adiana Hiau Abdullah, and Woei-Chyuan Wong. 2016. Dividend Payment Behaviour and Its Determinants: The Nigerian Evidence. African Development Review 28: 53–63. [Google Scholar] [CrossRef]

- Adehi, Mary U., and Bilkisu Maijamaa. 2020. COVID-19, Learning & Dividends. African Journal of Education and Practice 6: 79. [Google Scholar] [CrossRef]

- Aggarwal, Shobhit, and Mrityunjay Kumar Tiwary. 2019. Do Stock Markets Witness Instantaneous Reactions to Changes in Dividend Tax Laws: Evidence from India. International Journal of Indian Culture and Business Management 19: 226. [Google Scholar] [CrossRef]

- Agrawal, Anshu. 2020. Modified Total Interpretive Structural Model of Corporate Financial Flexibility. Global Journal of Flexible Systems Management 21: 369–88. [Google Scholar] [CrossRef]

- Aivazian, Varouj, Laurence Booth, and Sean Cleary. 2003. Do Emerging Market Firms Follow Different Dividend Policies From U.S. Firms? Journal of Financial Research 26: 371–87. [Google Scholar] [CrossRef]

- Ajay, Ranjitha, and R. Madhumathi. 2015. Institutional Ownership and Earnings Management in India. Indian Journal of Corporate Governance 8: 119–36. [Google Scholar] [CrossRef]

- Alam, M. D. Zahangir. 2012. Dividend Policy: A Comparative Study of UK and Bangladesh Based Companies. IOSR Journal of Business and Management 1: 57–67. [Google Scholar] [CrossRef]

- Alekneviciene, Vilija, Povilas Domeika, and Dalia Jatkunaite. 2015. The Development of Company Dividend Policy in Respect of Profit Distribution. Engineering Economics 50: 5. [Google Scholar]

- Al-Kuwari, Duha. 2010. To Pay or Not to Pay: Using Emerging Panel Data to Identify Factors Influencing Corporate Dividend Payout Decisions. International Research Journal of Finance and Economics 42: 19–36. [Google Scholar]

- Allen, Franklin, Antonio E. Bernardo, and Ivo Welch. 2000. A Theory of Dividends Based on Tax Clienteles. The Journal of Finance 55: 2499–536. [Google Scholar] [CrossRef]

- Al-Najjar, Basil, and Erhan Kilincarslan. 2017. Corporate Dividend Decisions and Dividend Smoothing. International Journal of Managerial Finance 13: 304–31. [Google Scholar] [CrossRef]

- Al-Najjar, Basil, and Erhan Kilincarslan. 2019. What Do We Know about the Dividend Puzzle?—A Literature Survey. International Journal of Managerial Finance 15: 205–35. [Google Scholar] [CrossRef]

- Anand, Manoj. 2004. Factors Influencing Dividend Policy Decisions of Corporate India. ICFAI Journal of Applied Finance 10: 5–16. [Google Scholar]

- Anil, Kanwal. 2008. Determinants of Dividend Payout Ratios-A Study of Indian Information Technology Sector. International Research Journal of Finance and Economics 15: 63–71. [Google Scholar]

- Anjali, Rane, and Guntur Anjana Raju. 2017. Dividend Announcement and Market Efficiency-An Empirical Study on Service Sector Companies Listed In BSE. SDMIMD Journal of Management 8: 1–10. [Google Scholar] [CrossRef]

- Ardestani, Hananeh Shahteimoori, Siti Zaleha Abdul Rasid, Rohaida Basiruddin, and Mohammadghorban Mehri. 2013. Dividend Payout Policy, Investment Opportunity Set and Corporate Financing in the Industrial Products Sector of Malasya. Journal of Applied Finance & Banking 3: 123. [Google Scholar]

- Baker, H. Kent, and Rob Weigand. 2015. Corporate Dividend Policy Revisited. Edited by Professor H. Kent Baker and Dr Rob Weigand. Managerial Finance 41: 126–44. [Google Scholar] [CrossRef]

- Baker, Malcolm, and Jeffrey Wurgler. 2004. A Catering Theory of Dividends. The Journal of Finance 59: 1125–65. [Google Scholar] [CrossRef]

- Baker, H. Kent, Gail E. Farrelly, and Richard B. Edelman. 1985. A Survey of Management Views on Corporate Dividend Policy in Portugal. Financial Management 14: 78–84. [Google Scholar] [CrossRef]

- Baker, Malcolm, Brock Mendel, and Jeffrey Wurgler. 2016. Dividends as Reference Points: A Behavioral Signaling Approach. The Review of Financial Studies 29: 697–738. [Google Scholar]

- Baker, H. Kent, N. Jayantha Dewasiri, Weerakoon Banda Yatiwelle Koralalage, and Athambawa Abdul Azeez. 2019. Dividend Policy Determinants of Sri Lankan Firms: A Triangulation Approach. Managerial Finance 45: 2–20. [Google Scholar] [CrossRef]

- Banerjee, Arindam, and Anupam De. 2015. Capital Structure Decisions and Its Impact on Dividend Payout Ratio during the Pre- and Post-Period of Recession in Indian Scenario: An Empirical Study. Vision: The Journal of Business Perspective 19: 366–77. [Google Scholar] [CrossRef]

- Baskin, Jonathan. 1989. Dividend Policy and the Volatility of Common Stocks. The Journal of Portfolio Management 15: 19–25. [Google Scholar] [CrossRef]

- Basu, Debarati, and Kaustav Sen. 2015. Financial Decisions by Business Groups in India: Is It ‘Fair and Square’? Journal of Contemporary Accounting & Economics 11: 121–37. [Google Scholar] [CrossRef]

- Batabyal, Sourav, and Richard Robinson. 2017. Capital Change and Stability When Dividends Convey Signals. The Quarterly Review of Economics and Finance 65: 158–67. [Google Scholar] [CrossRef]

- Benavides, Julian, Luis Berggrun, and Hector Perafan. 2016. Dividend Payout Policies: Evidence from Latin America. Finance Research Letters 17: 197–210. [Google Scholar] [CrossRef]

- Bhattacharya, Sudipto. 1979. The Bird in the Hand. The Bell Journal of Economics 10: 259–70. [Google Scholar] [CrossRef]

- Bhattacharya, Debarati, Chia-Wen Chang, and Wei-Hsien Li. 2020. Stages of Firm Life Cycle, Transition, and Dividend Policy. Finance Research Letters 33: 101226. [Google Scholar] [CrossRef]

- Bilel, Hadfi, and Kouki Mondher. 2020. Catering Theory and Dividend Policy: A Study of MENA Region. Corporate Ownership and Control 17. [Google Scholar] [CrossRef]

- Bilel, Hadfi, and Kouki Mondher. 2021. What Can Explain Catering of Dividend? Environment Information and Investor Sentiment. Journal of Economics and Finance 45: 428–50. [Google Scholar] [CrossRef]

- Black, Fischer. 1996. The Dividend Puzzle. The Journal of Portfolio Management 23: 8–12. [Google Scholar] [CrossRef]

- Blouin, Jennifer L., Jana S. Raedy, and Douglas A. Shackelford. 2011. Dividends, Share Repurchases, and Tax Clienteles: Evidence from the 2003 Reductions in Shareholder Taxes. The Accounting Review 86: 887–914. [Google Scholar] [CrossRef]

- Bostanci, Faruk, Eyup Kadioglu, and Guven Sayilgan. 2018. Determinants of Dividend Payout Decisions: A Dynamic Panel Data Analysis of Turkish Stock Market. International Journal of Financial Studies 6: 93. [Google Scholar] [CrossRef]

- Brav, Alon, John R. Graham, Campbell R. Harvey, and Roni Michaely. 2005. Payout Policy in the 21st Century. Journal of Financial Economics 77: 483–527. [Google Scholar] [CrossRef]

- Brennan, Michael J. 1970. Taxes, Market Valuation and Corporate Financial Policy. National Tax Journal 23: 417–27. [Google Scholar] [CrossRef]

- Budagaga, Akram. 2018. Factors Affecting Dividend Payment Decisions: The Case of Libya. Archives of Business Research 6. [Google Scholar] [CrossRef]

- Budagaga, Akram Ramadan. 2020. Determinants of Banks’ Dividend Payment Decisions: Evidence from MENA Countries. International Journal of Islamic and Middle Eastern Finance and Management 13: 847–71. [Google Scholar] [CrossRef]

- Bulan, Laarni T., and Narayanan Subramanian. 2011. The Firm Life Cycle Theory of Dividends. In Dividends and Dividend Policy. Hoboken: John Wiley & Sons, Inc., pp. 201–13. [Google Scholar] [CrossRef]

- Cejnek, Georg, Otto Randl, and Josef Zechner. 2020. The COVID-19 Pandemic and Corporate Dividend Policy. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Chadha, Saurabh, and Anil K. Sharma. 2015. Determinants of Capital Structure: An Empirical Evaluation from India. Journal of Advances in Management Research 12: 3–14. [Google Scholar] [CrossRef]

- Chaleeda, Md. Aminul Islam, Tunku Salha Tunku Ahmad, and Anas Najeeb Mosa Ghazalat. 2019. The Effects of Corporate Financing Decisions on Firm Value in Bursa Malaysia. International Journal of Economics and Finance 11: 127. [Google Scholar] [CrossRef][Green Version]

- Chang, Rosita P., and S. Ghon Rhee. 1990. The Impact of Personal Taxes on Corporate Dividend Policy and Capital Structure Decisions. Financial Management 19: 21. [Google Scholar] [CrossRef]

- Chevalier, Etienne, Vathana Ly Vath, and Alexandre Roch. 2020. Optimal Dividend and Capital Structure with Debt Covenants. Journal of Optimization Theory and Applications 187: 535–65. [Google Scholar] [CrossRef]

- Daas, Abdullah Al, Moid U. Ahmad, and Suleiman Jamal Mohammad. 2020. The Dynamics between Dividends, Financing and Investments: Evidence From Jordanian Companies. International Journal of Financial Research 11: 231. [Google Scholar] [CrossRef]

- Daniels, Kenneth, Tai S. Shin, and Cheng F. Lee. 1997. The Information Content of Dividend Hypothesis: A Permanent Income Approach. International Review of Economics & Finance 6: 77–86. [Google Scholar] [CrossRef]

- Danil, Nevi, Umara Noreen, Noor Azlinna Azizan, Muhammad Farid, and Zaheer Ahmed. 2020. Growth Opportunities, Capital Structure and Dividend Policy in Emerging Market: Indonesia Case Study. The Journal of Asian Finance, Economics and Business 7: 1–8. [Google Scholar] [CrossRef]

- Datta, Debabrata, Santanu K. Ganguli, and Manu Chaturvedi. 2014. Announcement Effect of Dividend in Presence of Dividend Tax: Possible Agency Problem and Macro Level Inefficiency? South Asian Journal of Macroeconomics and Public Finance 3: 195–220. [Google Scholar] [CrossRef]

- DeAngelo, Harry, and Linda DeAngelo. 2007. Capital Structure, Payout Policy, and Financial Flexibility. SSRN Electronic Journal, 2–6. [Google Scholar] [CrossRef]

- DeAngelo, Harry, Linda DeAngelo, and René M. Stulz. 2006. Dividend Policy and the Earned/Contributed Capital Mix: A Test of the Life-Cycle Theory. Journal of Financial Economics 81: 227–54. [Google Scholar] [CrossRef]

- Deslandes, Manon, Suzanne Landry, and Anne Fortin. 2015. The Effects of a Tax Dividend Cut on Payout Policies: Canadian Evidence. International Journal of Managerial Finance 11: 2–22. [Google Scholar] [CrossRef]

- Dewasiri, N. Jayantha, Weerakoon Banda Yatiwelle Koralalage, Athambawa Abdul Azeez, P. G. S. A. Jayarathne, Duminda Kuruppuarachchi, and V. A. Weerasinghe. 2019. Determinants of Dividend Policy: Evidence from an Emerging and Developing Market. Managerial Finance 45: 413–29. [Google Scholar] [CrossRef]

- Dewasiri Narayanage, Jayantha, and Weerakoon Banda Yatiwella. 2016. Why Do Companies Pay Dividends?: A Comment. Corporate Ownership and Control 13: 443–53. [Google Scholar] [CrossRef]

- Dickinson, Victoria. 2011. Cash Flow Patterns as a Proxy for Firm Life Cycle. The Accounting Review 86: 1969–94. [Google Scholar] [CrossRef]

- Dinh, Nguyen Van, and Nguyen Thi Hai Yen. 2018. Testing Effects of Changes in Earning to Dividend Actions of Listing Firms on Vietnamese Stock Exchanges Using the Multinomial Logistic Regression Model. VNU Journal of Science: Economics and Business 34: 2. [Google Scholar] [CrossRef]

- Dionne, Georges, and Karima Ouederni. 2011. Corporate Risk Management and Dividend Signaling Theory. Finance Research Letters 8: 188–95. [Google Scholar] [CrossRef]

- Dixit, Bipin Kumar, Nilesh Gupta, and Suman Saurabh. 2020. Dividend Policy in India: Reconciling Theory and Evidence. Managerial Finance 46: 1437–53. [Google Scholar] [CrossRef]

- Driver, Ciaran, Anna Grosman, and Pasquale Scaramozzino. 2020. Dividend Policy and Investor Pressure. Economic Modelling 89: 559–76. [Google Scholar] [CrossRef]

- Drobetz, Wolfgang, Michael Halling, and Henning Schrrder. 2015. Corporate Life-Cycle Dynamics of Cash Holdings. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Edgerton, Jesse. 2013. Four Facts about Dividend Payouts and the 2003 Tax Cut. International Tax and Public Finance 20: 769–84. [Google Scholar] [CrossRef]

- El-Ansary, Osama, and Tasneem Gomaa. 2012. The Life Cycle Theory of Dividends: Evidence from Egypt. International Research Journal of Finance and Economics 97: 72–80. [Google Scholar]

- Elayan, Fayez A., Jingyu Li, Maureen E. Donnelly, and Allister W. Young. 2009. Changes to Income Trust Taxation in Canada: Investor Reaction and Dividend Clientele Theory. Journal of Business Finance & Accounting 36: 725–53. [Google Scholar] [CrossRef]

- Endri, Endri, and Moch Fathony. 2020. Determinants of Firm’s Value: Evidence from Financial Industry. Management Science Letters 10: 111–20. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 1998. Taxes, Financing Decisions, and Firm Value. The Journal of Finance 53: 819–43. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2001. Disappearing Dividends: Changing Firm Characteristics or Lower Propensity to Pay? Journal of Financial Economics 60: 3–43. [Google Scholar] [CrossRef]

- Fama, Eugene F., and Kenneth R. French. 2002. Testing Trade-Off and Pecking Order Predictions About Dividends and Debt. Review of Financial Studies 15: 1–33. [Google Scholar] [CrossRef]

- Fliers, Philip T. 2019. What Is the Relation between Financial Flexibility and Dividend Smoothing? Journal of International Money and Finance 92: 98–111. [Google Scholar] [CrossRef]

- Floyd, Eric, Nan Li, and Douglas J. Skinner. 2015. Payout Policy through the Financial Crisis: The Growth of Repurchases and the Resilience of Dividends. Journal of Financial Economics 118: 299–316. [Google Scholar] [CrossRef]

- Franc-Dąbrowska, Justyna, Magdalena Mądra-Sawicka, and Magdalena Ulrichs. 2020. Determinants of Dividend Payout Decisions—The Case of Publicly Quoted Food Industry Enterprises Operating in Emerging Markets. Economic Research-Ekonomska Istraživanja 33: 1108–29. [Google Scholar] [CrossRef]

- Frankfurter, George M., and Bob G. Wood. 2002. Dividend Policy Theories and Their Empirical Tests. International Review of Financial Analysis 11: 111–38. [Google Scholar] [CrossRef]

- Gakumo, Samuel Thuo, and C. Nanjala. 2017. Factors Influencing Dividend Payout Decision of Financial and Non-Financial Companies Listed on Nairobi Securities Exchange. American Journal of Finance 1: 16. [Google Scholar] [CrossRef]

- Gangil, Ritu, and Navita Nathani. 2018. Determinants of Dividend Policy: A Study of FMCG Sector in India. Journal of Business and Managemnet 20: 40–46. [Google Scholar]

- Ghose, Biswajit, and Kailash Chandra Kabra. 2016. What Determines Firms’ Zero-Leverage Policy in India? Managerial Finance 42: 1138–58. [Google Scholar] [CrossRef]

- Gordon, Myron J. 1959. Dividends, Earnings, and Stock Prices. The Review of Economics and Statistics 41: 99. [Google Scholar] [CrossRef]

- Goyal, Shreyansh. 2019. The Dividend Puzzle Misspecification—Why the Role of Dividends Is Not What People Think. Cogent Economics & Finance 7: 1649000. [Google Scholar] [CrossRef]

- Hadian, Niki. 2019. The Influence of Profitability and Leverage on Dividend Policy in the Banking Sector. International Journal of Innovation, Creativity and Change 6: 1–23. [Google Scholar]

- Hamed Al-Yahyaee, Khamis, Toan Pham, and Terry Walter. 2010. Dividend Stability in a Unique Environment. Managerial Finance 36: 903–16. [Google Scholar] [CrossRef]

- Higgins, Robert C. 1972. The Corporate Dividend-Saving Decision. The Journal of Financial and Quantitative Analysis 7: 1527. [Google Scholar] [CrossRef]

- Ismail, Ida Suriya, Mohd Rizal Palil, Rosiati Ramli, and Mara Ridhuan Che Abdul Rahman. 2018. Effects of Dividend Tax Reform on Dividend Behavior: A Clientele Theory Approach. Jurnal Pengurusan 54: 165–79. [Google Scholar] [CrossRef]

- Iyer, Subramanian Rama, Harry Feng, and Ramesh P. Rao. 2017. Payout Flexibility and Capital Expenditure. Review of Quantitative Finance and Accounting 49: 633–59. [Google Scholar] [CrossRef]

- Jensen, Michael. 1986. American Economic Association Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. American Economic Review 76: 323–29. [Google Scholar]

- Jensen, Michael C. 1996. Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. In Corporate Bankruptcy. Edited by Jagdeep S. Bhandari and Lawrence A. Weiss. Cambridge: Cambridge University Press, pp. 11–16. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1999. Agency Cost of Free Cash Flow, Corporate Finance, and Takeovers. SSRN Electronic Journal 76: 323–29. [Google Scholar] [CrossRef]

- Jensen, Gerald R., Leonard L. Lundstrum, and Robert E. Miller. 2010. What Do Dividend Reductions Signal? Journal of Corporate Finance 16: 736–47. [Google Scholar] [CrossRef]

- Jiang, Wei, and Andrew W. Stark. 2013. Dividends, Research and Development Expenditures, and the Value Relevance of Book Value for UK Loss-Making Firms. The British Accounting Review 45: 112–24. [Google Scholar] [CrossRef]

- Jiraporn, Pornsit, and Pandej Chintrakarn. 2009. Staggered Boards, Managerial Entrenchment, and Dividend Policy. Journal of Financial Services Research 36: 1–19. [Google Scholar] [CrossRef]

- John, Kose, and Anzhela Knyazeva. 2006. Payout Policy, Agency Conflicts, and Corporate Governance. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Juhmani, Omar Issa. 2020. Corporate Boards, Ownership Structure and Dividend Payout: Evidence from Bahrain. Journal of Critical Reviews 7: 37–43. [Google Scholar] [CrossRef]

- Kajola, Sunday O., Ajibola A. Desu, and Tobechi F. Agbanike. 2015. Factors Influencing Dividend Payout Policy Decisions of Nigerian Listed Firms. International Journal of Economics, Commerce and Management 3: 539–57. [Google Scholar]

- Kapoor, Sujata, Anil Mishra, and Kanwal Anil. 2010. Dividend Policy Determinants of Indian Services Sector: A Factorial Analysis. Paradigm 14: 24–41. [Google Scholar] [CrossRef]

- Karjalainen, Jussi, Eero Kasanen, Juha Kinnunen, and Jyrki Niskanen. 2020. Dividends and Tax Avoidance as Drivers of Earnings Management: Evidence from Dividend-Paying Private SMEs in Finland. Journal of Small Business Management 18: 1–33. [Google Scholar] [CrossRef]

- Krieger, Kevin, Nathan Mauck, and Stephen W. Pruitt. 2020. The Impact of the COVID-19 Pandemic on Dividends. Finance Research Letters, 101910. [Google Scholar] [CrossRef]

- Kumar, Sanjeev, and K. S. Ranjani. 2019. Dividend Behaviour of Indian-Listed Manufacturing and Service Sector Firms. Global Business Review 20: 179–93. [Google Scholar] [CrossRef]

- Labhane, Nishant B. 2017. Disappearing and Reappearing Dividends in Emerging Markets: Evidence from Indian Companies. Journal of Asia-Pacific Business 18: 46–80. [Google Scholar] [CrossRef]

- Labhane, Nishant B. 2018. Why Do Firms Smooth Dividends? Empirical Evidence from an Emerging Economy India. Afro-Asian J. of Finance and Accounting 8: 237. [Google Scholar] [CrossRef]

- Labhane, Nishant. 2019a. Impact of Catering Incentives on Dividend Payment Decisions: Evidence from Indian Firms. Asian Journal of Business and Accounting 12: 93–120. [Google Scholar] [CrossRef]

- Labhane, Nishant B. 2019b. Dividend Policy Decisions in India: Standalone Versus Business Group-Affiliated Firms. Global Business Review 20: 133–50. [Google Scholar] [CrossRef]

- Labhane, Nishant B. 2020. A Test of the Catering Theory of Dividends: Empirical Evidence from an Emerging Economy India. Asian Academy of Management Journal of Accounting and Finance 15: 29–52. [Google Scholar] [CrossRef]

- Labhane, Nishant B., and Ramesh Chandra Das. 2015. Determinants of Dividend Payout Ratio: Evidence from Indian Companies. Business and Economic Research 5: 217. [Google Scholar] [CrossRef]

- Labhane, Nishant B., and Jitendra Mahakud. 2018. Dividend Smoothing and Business Groups: Evidence from Indian Companies. Global Business Review 19: 690–706. [Google Scholar] [CrossRef]

- Labhane, Nishant, and Jitendra Mahakud. 2019. Impact of Business Group Size and Diversification on Dividend Policy and Payouts: Evidence from Indian Companies. South Asian Journal of Management 26: 50–75. [Google Scholar]

- Lahiri, Poulomi, and Indrani Chakraborty. 2014. Explaining Dividend Gap between R&D and Non-R&D Indian Companies in the Post-Reform Period. Research in International Business and Finance 30: 268–83. [Google Scholar] [CrossRef]

- Laing, Timothy. 2020. The Economic Impact of the Coronavirus 2019 (Covid-2019): Implications for the Mining Industry. The Extractive Industries and Society 7: 580–82. [Google Scholar] [CrossRef]

- Lambrecht, Bart M., and Stewart C. Myers. 2012. A Lintner Model of Payout and Managerial Rents. The Journal of Finance 67: 1761–810. [Google Scholar] [CrossRef]

- Lang, Larry H. P., and Robert H. Litzenberger. 1989. Dividend Announcements. Cash Flow Signalling vs. Free Cash Flow Hypothesis? Journal of Financial Economics 24: 191–91. [Google Scholar] [CrossRef]

- Le, Thi Thai Ha, Xuan Hung Nguyen, and Manh Dung Tran. 2019. Determinants of Dividend Payout Policy in Emerging Markets: Evidence from the ASEAN Region. Asian Economic and Financial Review 9: 531–46. [Google Scholar] [CrossRef]

- Lin, James Juichia, and Cheng-Few Lee. 2021. Does Managerial Reluctance of Dividend Cuts Signal Future Earnings? Review of Quantitative Finance and Accounting 56: 453–78. [Google Scholar] [CrossRef]

- Lintner, John. 1956. Distribution of Incomes of Corporations among Dividends, Retained Earnings, and Taxes. The American Economic Review 46: 97–113. [Google Scholar]

- Livoreka, Besnik, Alban Hetemi, Albulena Shala, Arta Hoti, and Rrustem Asllanaj. 2014. Theories on Dividend Policy Empirical Research in Joint Stock Companies in Kosovo. Procedia Economics and Finance 14: 387–96. [Google Scholar] [CrossRef]

- Lotto, Josephat. 2020a. On an Ongoing Corporate Dividend Dialogue: Do External Influences Also Matter in Dividend Decision? Edited by David McMillan. Cogent Business & Management 7: 1787734. [Google Scholar] [CrossRef]

- Lotto, Josephat. 2020b. Towards Extending Dividend Puzzle Debate: What Motivates Distribution of Corporate Earnings in Tanzania? International Journal of Financial Studies 8: 18. [Google Scholar] [CrossRef]

- Loukil, Nadia. 2020. Does Political Instability Influence Dividend Payout Policy: Evidence from Tunisian Stock Exchange? EuroMed Journal of Business 15: 253–67. [Google Scholar] [CrossRef]

- Lu, Xiaoguang, Yiran Xi, and Diqian Lu. 2014. An Empirical Study about Catering Theory of Dividends: The Proof from Chinese Stock Market. Journal of Industrial Engineering and Management 7: 506–17. [Google Scholar] [CrossRef]

- Lumapow, Lihard Stevanus, and Ramon Arthur Ferry Tumiwa. 2017. The Effect of Dividend Policy, Firm Size, and Productivity to The Firm Value. Research Journal of Finance and Accounting 8: 20–24. [Google Scholar]

- MacKIE-Mason, Jeffrey K. 1990. Do Taxes Affect Corporate Financing Decisions? The Journal of Finance 45: 1471–93. [Google Scholar] [CrossRef]

- Mahenthiran, Sakthi, David Cademartori, and Tom Gjerde. 2020. Mandatory Dividend Policy, Growth, Liquidity and Corporate Governance: Evidence from Chile. Review of Pacific Basin Financial Markets and Policies 23: 2050025. [Google Scholar] [CrossRef]

- Martono, S., Arief Yulianto, Rini Setyo Witiastuti, and Angga Pandu Wijaya. 2020. The Role of Institutional Ownership and Industry Characteristics on the Propensity to Pay Dividend: An Insight from Company Open Innovation. Journal of Open Innovation: Technology, Market, and Complexity 6: 74. [Google Scholar] [CrossRef]

- Mehta, Anupam. 2012. An Empirical Analysis of Determinants of Dividend Policy—Evidence from the UAE Companies. Global Review of Accounting and Finance 3: 19–31. [Google Scholar]

- Mehta, Chhavi, P. K. Jain, and Surendra S. Yadav. 2014. Market Reaction to Stock Dividends: Evidence from India. Vikalpa: The Journal for Decision Makers 39: 55–74. [Google Scholar] [CrossRef]

- Miklus, Matjaz, and Zan Jan Oplotnik. 2016. Capital Market Response to the Change in the Dividend Policy: The Case of Slovenian Stock Market. Research in Applied Economics 8: 42. [Google Scholar] [CrossRef][Green Version]

- Miler, Merton H., and Kevin Rock. 1985. Dividend Policy under Asymmetric Information. The Journal of Finance 40: 1031–51. [Google Scholar] [CrossRef]

- Miller, Merton H., and Franco Modigliani. 1961. Dividend Policy, Growth, and the Valuation of Shares. The Journal of Business 34: 411. [Google Scholar] [CrossRef]

- Modigliani, Franco, and Merton H. Miller. 1958. American Economic Association the Cost of Capital, Corporation Finance and the Theory of Investment. Source: The American Economic Review 48: 261–97. [Google Scholar]

- Mohd, Kamarun Nisham Taufil, and Khairul Zharif Zaharudin. 2019. Future Earnings Growth and Dividend Payout: Evidence from Malaysia. Management Science Letters 9: 347–56. [Google Scholar] [CrossRef]

- Moon, Joonho, Won Seok Lee, and John Dattilo. 2015. Determinants of the Payout Decision in the Airline Industry. Journal of Air Transport Management 42: 282–88. [Google Scholar] [CrossRef]

- Nguyen, Ha Viet, Hung Ngoc Dang, and Hung Hoang Dau. 2021. Influence of Corporate Governance on Dividend Policy in Vietnam. Journal of Asian Finance, Economics and Business 8: 893–902. [Google Scholar] [CrossRef]

- Pahi, Debasis, and Inder Sekhar Yadav. 2021. Dividend Behavior of Indian Firms: New Evidence from Large Data Set. Journal of Asia-Pacific Business 22: 4–38. [Google Scholar] [CrossRef]

- Pandey, I. M. 2007. Dividend Behaviour of Indian Companies under Monetary Policy Restrictions. Managerial Finance 33: 14–25. [Google Scholar] [CrossRef]

- Pettenuzzo, Davide, Riccardo Sabbatucci, and Allan Timmermann. 2020. Dividend Suspensions and Cash Flow Risk during the COVID-19 Pandemic. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Pieloch-Babiarz, Aleksandra. 2020. Managerial Ownership and Catering to Investor Sentiment for Dividends: Evidence from the Electromechanical Industry Sector on the Warsaw Stock Exchange. Oeconomia Copernicana 11: 467–83. [Google Scholar] [CrossRef]

- Pinto, Geetanjali, and Shailesh Rastogi. 2019. Sectoral Analysis of Factors Influencing Dividend Policy: Case of an Emerging Financial Market. Journal of Risk and Financial Management 12: 110. [Google Scholar] [CrossRef]

- Poulsen, Michael, Robert Faff, and Stephen Gray. 2013. Financial Inflexibility and the Value Premium. International Review of Finance 13: 327–44. [Google Scholar] [CrossRef]

- Pruitt, Stephen W., and Lawrence J. Gitman. 1991. The Interactions between the Investment, Financing, and Dividend Decisions of Major U.S. Firms. The Financial Review 26: 409–30. [Google Scholar] [CrossRef]

- Qamar, Saima, Zuhaib Ahmed Bazaz, and Zuhaib Ahmed Bazaz. 2014. Factors Influencing Dividend Decision: A Study of Listed Companies in India. International Journal of Scientific Research and Reviews 3: 40–66. [Google Scholar]

- Rajesh Kumar, B., and K. S. Sujit. 2018. Determinants of Dividends among Indian Firms—An Empirical Study. Edited by Andrew Vivian. Cogent Economics & Finance 6: 1423895. [Google Scholar] [CrossRef]

- Rajput, Monika, and Shital Jhunjhunwala. 2019. Corporate Governance and Payout Policy: Evidence from India. Corporate Governance: The International Journal of Business in Society 19: 1117–32. [Google Scholar] [CrossRef]

- Rajverma, Abhinav Kumar, Rakesh Arrawatia, Arun Kumar Misra, and Abhijeet Chandra. 2019. Ownership Structure Influencing the Joint Determination of Dividend, Leverage, and Cost of Capital. Cogent Economics & Finance 7: 1600462. [Google Scholar] [CrossRef]

- Ramaratnam, M., R. Jayaraman, and G. Vasanthi. 2012. Impact of Investors’ Ratios on Dividend Decisions with Special Reference to Select Cement Companies in India: An Analytical Study. South Asian Journal of Management 19: 68. [Google Scholar]

- Ranajee, Ranajee, Rajesh Pathak, and Akanksha Saxena. 2018. To Pay or Not to Pay: What Matters the Most for Dividend Payments? International Journal of Managerial Finance 14: 230–44. [Google Scholar] [CrossRef]

- Rifat, Afrin, Anika Bushra, and Nabila Nisha. 2020. Factors That Drive Dividend Payout Decisions: An Investigation in the Context of Bangladesh. Afro-Asian J. of Finance and Accounting 10: 380. [Google Scholar] [CrossRef]

- Rochmah, Hidayati Nur, and Ardianto Ardianto. 2020. Catering Dividend: Dividend Premium and Free Cash Flow on Dividend Policy. Edited by Collins G. Ntim. Cogent Business & Management 7: 1812927. [Google Scholar] [CrossRef]

- Rój, Justyna. 2019. The Determinants of Corporate Dividend Policy in Poland. Ekonomika 98: 96–110. [Google Scholar] [CrossRef]

- Rozeff, Michael S. 1982. Growth, Beta and Agency Costs as Determinants of Dividend Payout Ratios. Journal of Financial Research 5: 249–59. [Google Scholar] [CrossRef]

- Santhosh Kumar, S., and C. Bindu. 2018. Determinants of Capital Structure: An Exclusive Study of Passenger Car Companies in India. Indian Journal of Finance 12. [Google Scholar] [CrossRef]

- Saraswat, Saloni. 2018. Strategies v/s Consumer Perception of Brand Zara—India. IITM Journal of Management and IT 9: 68–80. [Google Scholar]

- Sharma, Rakesh Kumar. 2020. Factors Influencing Dividend Decisions of Indian Construction, Housing and Real Estate Companies: An Empirical Panel Data Analysis. International Journal of Finance & Economics, 1–18. [Google Scholar] [CrossRef]

- Shetty, Rajalakshmi, and Sajeevan Rao. 2020. Dividend Policy and Its Impact on Share Price of Listed Nationalised Banks in Bse. European Journal of Molecular and Clinical Medicine 7: 259–69. [Google Scholar]

- Simoes Vieira, Elisabete. 2011. Investor Sentiment and the Market Reaction to Dividend News: European Evidence. Managerial Finance 37: 1213–45. [Google Scholar] [CrossRef]

- Singhania, Monica, and Akshay Gupta. 2012. Determinants of Corporate Dividend Policy: A Tobit Model Approach. Vision: The Journal of Business Perspective 16: 153–62. [Google Scholar] [CrossRef]

- Singla, Harish Kumar, and Pradeepta Kumar Samanta. 2019. Determinants of Dividend Payout of Construction Companies: A Panel Data Analysis. Journal of Financial Management of Property and Construction 24: 19–38. [Google Scholar] [CrossRef]

- Smith, Deborah Drummond, and Anita K. Pennathur. 2019. Signaling Versus Free Cash Flow Theory: What Does Earnings Management Reveal About Dividend Initiation? Journal of Accounting, Auditing & Finance 34: 284–308. [Google Scholar] [CrossRef]

- Smith, Clifford W., and Ross L. Watts. 1992. The Investment Opportunity Set and Corporate Financing, Dividend, and Compensation Policies. Journal of Financial Economics 32: 263–92. [Google Scholar] [CrossRef]

- Stern, Joel M., and Joseph T. Willett. 2019. A Look Back at the Beginnings of EVA and Value-Based Management. Journal of Applied Corporate Finance 31: 95–102. [Google Scholar] [CrossRef]

- Suliman Al-Fasfus, Fuad. 2020. Impact of Free Cash Flows on Dividend Pay-Out in Jordanian Banks. Asian Economic and Financial Review 10: 547–58. [Google Scholar] [CrossRef]

- Sulistiono, Sugeng, and Yusna Yusna. 2020. Analysis of the Effect of Funding Decision and Dividend Policy on the Firm Value and Investment Decision as Mediation (Study on Manufacturing Companies in Indonesia Stock Exchange). Paper presented at the 1st Annual Management, Business and Economic Conference (AMBEC 2019), Batu, Indonesia, August 29–30; Paris: Atlantis Press. [Google Scholar]

- Tahir, Hussain, Mahfuzur Rahman, and Ridzuan Masri. 2020. Do Board Traits Influence Firms’ Dividend Payout Policy? Evidence from Malaysia. The Journal of Asian Finance, Economics and Business 7: 87–99. [Google Scholar] [CrossRef]

- Taleb, Lotfi. 2019. Dividend Policy, Signaling Theory: A Literature Review. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Thaiyalnayaki, M., and G. Divakara Reddy. 2018. A Brief Analysis on Dividend Payout vs. Promoters Share in Corporate Firms. Indian Journal of Public Health Research & Development 9: 19. [Google Scholar] [CrossRef]

- Tiwari, Shamik, and Debajyoti Pal. 2020. Dividend Policy Decisions and Share Prices Relationship. Finance & Accounting Research Journal 2: 76–81. [Google Scholar] [CrossRef]

- Tran, Quoc Trung. 2020. Corruption, Agency Costs and Dividend Policy: International Evidence. The Quarterly Review of Economics and Finance 76: 325–34. [Google Scholar] [CrossRef]

- Tse, Alex S. L. 2020. Dividend Policy and Capital Structure of a Defaultable Firm. Mathematical Finance 30: 961–94. [Google Scholar] [CrossRef]

- Utami, Siti Rahmi, and Eno L. Inanga. 2011. Agency Costs of Free Cash Flow, Dividend Policy, and Leverage of Firms in Indonesia. European Journal of Economics, Finance and Administrative Sciences 33: 7–24. [Google Scholar]

- Walter, James E. 1956. Dividend Policies and Common Stock Prices. The Journal of Finance 11: 29–41. [Google Scholar] [CrossRef]

- Walter, James E. 1963. Dividend Policy: Its Influence on the Value of the Enterprise. The Journal of Finance 18: 280–91. [Google Scholar] [CrossRef]

- Wang, George Yungchih. 2010. The Impacts of Free Cash Flows and Agency Costs on Firm Performance. Journal of Service Science and Management 3: 408–18. [Google Scholar] [CrossRef]

- Wang, Wenjing, and Arthur S. Guarino. 2020. The Impact of the Covid-19 Crisis on Common Stock Dividend Payout Policy. Research in Economics and Management 5: 68. [Google Scholar] [CrossRef]

- Wang, Ming-Hui, Mei-Chu Ke, Feng-Yu Lin, and Yen-Sheng Huang. 2016. Dividend Policy and the Catering Theory: Evidence from the Taiwan Stock Exchange. Managerial Finance 42: 999–1016. [Google Scholar] [CrossRef]

- Wooldridge, Jeffrey M. 2013. Panel Data Models with Heterogeneity and Endogeneity. Programme Evaluation for Policy Analysis. East Lansing: Michigan State University. [Google Scholar]

- Wu, Yufeng. 2018. What’s behind Smooth Dividends? Evidence from Structural Estimation. The Review of Financial Studies 31: 3979–4016. [Google Scholar] [CrossRef]

- Yousef, Ibrahim, Sailesh Tanna, and Sudip Patra. 2021. Testing Dividend Life-Cycle Theory in the Islamic and Conventional Banking Sectors of GCC Countries. Journal of Islamic Accounting and Business Research 12: 276–300. [Google Scholar] [CrossRef]

| Variables | Underlying Theories | Proxy Measures | Formula | References | Factor Loadings |

|---|---|---|---|---|---|

| Profitability | Studies by (Lintner 1956; Fama and French 2001); Residual dividend theory; Modigliani Irrelevance theory (Miller and Modigliani 1961); Walter Theory (Walter 1963); Gordon Theory (Gordon 1959) | EBITDA | Earnings before interest, taxes, depreciation and amortization | (Jiraporn and Chintrakarn 2009; Edgerton 2013) | 0.898 |

| EBITDAMargin | EBITDA margin = EBITDA/Net sales | 0.847 | |||

| ROTA | Return on total assets = EBIT/Total assets | (Labhane and Mahakud 2018; Fama and French 2001) | |||

| Liquidity | Free cash flow theory signaling (Lang and Litzenberger 1989) | C.F. | Cash flows = EBITDA Interest Taxes Dividend paid | (Dewasiri et al. 2019; Labhane and Das 2015) | 0.889 |

| FCF | Free cash flows = Cashflows*(1/Total Assets) | (Dewasiri et al. 2019; Lang and Litzenberger 1989; Suliman Al-Fasfus 2020) | 0.810 | ||

| Leverage | Residual theory (Lintner 1956; Baker and Weigand 2015) | Debt-equity | Debt–equity ratio = Total debt/Total equity | (Singla and Samanta 2019; Dewasiri et al. 2019; Banerjee and De 2015; Danil et al. 2020) | 0.943 |

| Size/tangibility | Agency theory; studies by (Endri and Fathony 2020; Lumapow and Tumiwa 2017) | LogTA | Natural log of total assets | (Dewasiri et al. 2019; Le et al. 2019) | 0.894 |

| Networth BVS | Net worth Book value per share | (Jiang and Stark 2013) | 0.972 | ||

| Growth rate | Walter theory (Walter 1963; Ismail et al. 2018) | ROTA | EBITDA/TA | (Jensen et al. 2010) | 0.811 |

| MBV | Market-to-book value ratio = Market capitalization/Net worth | (Labhane 2019b; Smith and Watts 1992; Benavides et al. 2016; Walter 1963; Lahiri and Chakraborty 2014) | 0.776 | ||

| Tax rate | Clientele effect (Blouin et al. 2011; Allen et al. 2000) | Tax | Provision for tax/Profit before tax | (Labhane 2019a; Allen et al. 2000; Blouin et al. 2011; Ismail et al. 2018) | 0.947 |

| Dividend premium | Catering theory (Baker and Wurgler 2004; Bilel and Mondher 2021) | MBV | Market capitalization/Net worth | (Baker and Wurgler 2004; Labhane 2019a; Stern and Willett 2019) | |

| Lag dividend | Signaling theory (Labhane 2018; Wu 2018) | LagDiv | LagDiv = DivPert−1 | (Dewasiri et al. 2019; Dinh and Yen 2018; Qamar et al. 2014; Baker et al. 2019; DeAngelo et al. 2006) |

| Paired Differences | t | df | Sig. (2-Tailed) | |||||

|---|---|---|---|---|---|---|---|---|

| Pairs | Mean | Std. Deviation | Std. Error Mean | 95% Confidence Interval of the Difference | ||||

| Lower | Upper | |||||||

| DivPer21–DivPer20 | 29.06 | 896.32 | 48.33 | −66.00 | 124.11 | 0.60 | 343 | |

| DivPer21–Pre2020DivPer | 87.87 | 529.86 | 28.20 | 32.40 | 143.33 | 3.12 | 352 | *** |

| DivPer20–Pre2020DivPer | 72.05 | 707.07 | 33.26 | 6.69 | 137.41 | 2.17 | 451 | ** |

| DivY21–DivY20 | −1.21 | 3.71 | 0.16 | −1.54 | −0.89 | −7.37 | 507 | *** |

| DivY21–Pre2020DivY | −0.04 | 1.79 | 0.08 | −0.20 | 0.12 | −0.50 | 471 | |

| DivY20–Pre2020DivY | 1.17 | 3.56 | 0.16 | 0.85 | 1.49 | 7.13 | 470 | *** |

| Increase | Decrease | Stable | Omission | Dividend Cut% (Omission + Decrease) | |

|---|---|---|---|---|---|

| Consistent payers post 2015 (65) | |||||

| Year 2021 | 14 | 9 | 15 | 27 | 55.38% |

| Year 2020 | 13 | 33 | 1 | 18 | 78.46% |

| Changes in payouts 2021 | |||||

| Payers 2020 (244) | 68 | 112 | 13 | 51 | 48.77% |

| Payers 2019 (281) | 96 | 54 | 41 | 90 | 66.19% |

| Payers 2018 (277) | 64 | 65 | 45 | 103 | 60.29% |

| Payers 2017 (415) | 143 | 93 | 55 | 124 | 64.34% |

| Payers 2016 (410) | 142 | 88 | 55 | 125 | 65.12% |

| Payers 2015 (419) | 140 | 87 | 60 | 132 | 64.92% |

| Changes in payouts 2020 | |||||

| Payers 2019 (281) | 106 | 140 | 2 | 33 | 49.47% |

| Payers 2018 (277) | 114 | 115 | 5 | 43 | 56.68% |

| Payers 2017 (415) | 189 | 174 | 7 | 45 | 56.39% |

| Payers 2016 (410) | 184 | 170 | 9 | 47 | 56.34% |

| Payers 2015 (419) | 188 | 175 | 8 | 48 | 56.32% |

| Changes in payouts 2019 | |||||

| Payers 2018 (277) | 97 | 161 | 19 | 0 | 58.12% |

| Payers 2017 (415) | 184 | 193 | 38 | 0 | 46.51% |

| Payers 2016 (410) | 192 | 186 | 32 | 0 | 45.37% |

| Payers 2015 (419) | 202 | 179 | 38 | 0 | 42.72% |

| Changes in payouts 2018 | |||||

| Payers 2017 (415) | 212 | 192 | 11 | 0 | 46.27% |

| Payers 2016 (410) | 214 | 184 | 12 | 0 | 44.88% |

| Payers 2015 (419) | 217 | 192 | 10 | 0 | 45.82% |

| Changes in payouts 2017 | |||||

| Payers 2016 (410) | 198 | 77 | 135 | 0 | 18.78% |

| Payers 2015 (419) | 199 | 74 | 146 | 0 | 17.66% |

| Changes in payouts 2016 | |||||

| Payers 2015 (419) | 208 | 71 | 140 | 0 | 16.95% |

| Years | Number of Firms | % | Change in Dividend–Cut Percentage | ||||

|---|---|---|---|---|---|---|---|

| Minimum | Maximum | Mean | Std. Deviation | Variance | |||

| 2021 | 164 | 32.22% | −0.99 | −0.04 | −0.65 | 0.27 | 0.70 |

| 2020 | 280 | 55.00% | −1.00 | −0.07 | −0.74 | 0.27 | 0.07 |

| 2019 | 228 | 44.80% | −1.00 | −0.04 | −0.64 | 0.27 | 0.07 |

| 2018 | 232 | 45.60% | −0.99 | −0.02 | −0.68 | 0.25 | 0.06 |

| 2017 | 94 | 18.50% | −0.91 | −0.02 | −0.45 | 0.23 | 0.05 |

| 2016 | 99 | 19.40% | −0.97 | −0.04 | −0.39 | 0.24 | 0.06 |

| 2015 | 90 | 17.70% | −0.97 | −0.01 | −0.39 | 0.24 | 0.06 |

| Industry | Number of Companies | Dividend Cuts | ||||||

|---|---|---|---|---|---|---|---|---|

| 2021 | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | ||

| Manufacturing | 298 | 157 | 134 | 135 | 137 | 57 | 53 | 50 |

| Service sector | 108 | 57 | 63 | 47 | 45 | 27 | 27 | 21 |

| FMCG | 32 | 19 | 12 | 18 | 20 | 2 | 4 | 6 |

| Infrastructure | 18 | 11 | 9 | 8 | 6 | 5 | 1 | 2 |

| Realty | 17 | 10 | 11 | 5 | 6 | 2 | 6 | 4 |

| Diversified | 9 | 5 | 3 | 6 | 6 | 1 | - | 2 |

| Trading | 9 | 4 | 3 | 2 | 4 | - | 4 | - |

| Agri | 7 | 3 | 3 | 2 | 3 | - | 2 | 2 |

| Diamond & Jewellery | 3 | 2 | 1 | 1 | 1 | - | 1 | - |

| Electricals | 4 | 2 | 3 | 1 | 1 | - | - | 1 |

| Aviation | 2 | 1 | 2 | 1 | 2 | - | - | 1 |

| Miscellaneous | 2 | 1 | 1 | 2 | - | - | - | - |

| Total | 509 | 272 | 245 | 228 | 231 | 94 | 98 | 89 |

| DivCut% | 53% | 48% | 45% | 45% | 18% | 19% | 17% | |

| Variable | Coefficient | Std. Error | Significance |

|---|---|---|---|

| C | −282.12 | 54.864 | *** |

| EBITDA | −0.004 | 0.002 | * |

| LOGTA | 44.558 | 6.89 | *** |

| BVS | 0.076 | 0.046 | * |

| CFS | −0.001 | 0.001 | |

| FCFS | −2.807 | 0.346 | *** |

| MBVRATIO | 10.973 | 4.061 | *** |

| DEBTEQUITY | −4.263 | 3.319 | |

| EBITDAMARGIN | −5.692 | 1.559 | *** |

| TAXRATE | 0.479 | 0.568 | |

| LAGDIV | 0.092 | 0.035 | *** |

| Effects Specification | |||

| Cross-section fixed (dummy variables) | |||

| Root MSE | 254.141 | R-Squared | 0.75 |

| Mean dependent var. | 209.583 | Adj. R-Squared | 0.71 |

| S.D. dependent var. | 508.104 | S.E. of regression | 274.95 |

| Akaike into criterion | 14.205 | Sum squared resid | 230,125,535.8 |

| Schwarz criterion | 15.205 | Log likelihood | −24,787.18 |

| Hannan–Quinn criterion | 14.526 | F-statistic | 17.61 |

| Durbin–Watson stat. | 1.913 | Prob(F-statistic) | 0 |

| Dependent Variable: DIVPER | |||

| Method: Panel Least Squares | |||

| Sample 2015–2021 | |||

| Periods included: 7 | |||

| Cross-sections included: 509 | |||

| Total panel (balanced) observations: 3563 | |||

| White period standard errors & covariance (d.f. corrected) | |||

| Variable | Coefficient | Std. Error | Sig. |

|---|---|---|---|

| C | 114.311 | 86.793 | |

| EBITDA | 0.006 | 0.006 | |

| LOGTA | −8.939 | 14.81 | |

| BVS | 0.036 | 0.023 | |

| CFS | 0.004 | 0.001 | *** |

| FCFS | −294.114 | 134.497 | ** |

| MBVRATIO | −0.156 | 0.121 | |

| DEBTEQUITY | −19.681 | 11.395 | * |

| EBITDAMARGIN | −23.265 | 13.185 | * |

| TAXRATE | −18.859 | −18.954 | |

| LAGDIV | 0.672 | 0.265 | ** |

| Effects Specification | |||

| Cross-section fixed (dummy variables) | |||

| Root MSE | 99.342 | R-Squared | 0.956 |

| Mean dependent var. | 172.501 | Adj. R-Squared | 0.946 |

| S.D dependent var. | 472.029 | S.E. of regression | 109.841 |

| Akaike into criterion | 12.399 | Sum squared resid | 4,065,918.282 |

| Schwarz criterion | 13.131 | Log likelihood | −2479.211 |

| Hannan–Quinn criter. | 12.689 | F-statistic | 98.016 |

| Durbin–Watson stat. | 2.285 | Prob(F-statistic) | 0 |

| Dependent Variable: DIVPER | |||

| Method: Panel Least Squares | |||

| Sample 2015–2021 | |||

| Periods included: 7 | |||

| Cross-sections included: 65 | |||

| Total panel (balanced) observations: 412 | |||

| White period standard errors & covariance (d.f. corrected) | |||

| All Firms | Regular Payers | |||||

|---|---|---|---|---|---|---|

| Variable | Coefficient | Std. Error | Sig. | Coefficient | Std. Error | Sig. |

| C | −290.686 | 62.049 | *** | 223.549 | 210.142 | |

| DUMMY2020 | 44.167 | 16.95 | *** | 20.938 | 22.475 | ** |

| DUMMY2021 | 49.717 | 27.817 | * | −35.076 | 17.433 | *** |

| FCFS | −3.236 | 0.228 | *** | −541.842 | 90.132 | |

| EBITDAMARGIN | −6.065 | 2.577 | ** | 33.176 | 33.437 | |

| ROTA | 231.836 | 179.373 | −538.501 | 406.11 | ||

| LOGTA | 45.83 | 12.061 | *** | −51.485 | 51.005 | |

| LOGMCAP | −7.63 | 4.753 | 10.912 | 5.094 | ** | |

| LOGSALES | 5.693 | 7.891 | 40.636 | 36.002 | ||

| MBVRATIO | 8.685 | 4.184 | ** | −0.065 | 0.092 | |

| DEBTEQUITY | −4.12 | 3.094 | −56.928 | 30.335 | * | |

| Effects Specification | ||||||

| Cross-section fixed (dummy variables) | ||||||

| Root MSE | 258.320 | 173.823 | ||||

| Mean dependent var. | 209.583 | 172.495 | ||||

| S.D. dependent var. | 508.104 | 471.456 | ||||

| Akaike into criterion | 14.238 | 13.517 | ||||

| Schwarz criterion | 15.138 | 14.248 | ||||

| Hannan–Quinn criter. | 14.558 | 13.806 | ||||

| Durbin–Watson stat. | 1.878 | 2.628 | ||||

| R-Squared | 0.741 | 0.864 | ||||

| Adj. R-Squared | 0.697 | 0.834 | ||||

| S.E.of regression | 279.475 | 192.143 | ||||

| Sum squared resid | 237,755,377.389 | 12,487,548.679 | ||||

| Log likelihood | −24,845.283 | −2716.291 | ||||

| F-statistic | 16.853 | 28.952 | ||||

| Prob(F-statistic) | 0.000 | 0.000 | ||||

| Cross-sections included | 509 | 65 | ||||

| Total panel (balanced) observations: | 3563 | 413 | ||||

| Dependent Variable: DIVPER | ||||||

| Method: Panel Least Squares | ||||||

| Sample 2015–2021 | ||||||

| Periods included: 7 | ||||||

| White period standard errors & covariance (d.f. corrected) | ||||||

| All Firms | Regular Payers | |||||

|---|---|---|---|---|---|---|

| Variable | Coefficient | Std. Error | Coefficient | Std. Error | ||

| C | 1.177 | 0.063 | *** | 0.079 | 0.115 | |

| DUMMY2020 | 0.015 | 0.026 | 0.798 | 0.055 | *** | |

| DUMMY2021 | 0.037 | 0.046 | 0.548 | 0.069 | *** | |

| FCFS | 0.000 | 0.000 | ** | 0.039 | 0.028 | |

| EBITDAMARGIN | 0.004 | 0.005 | 0.029 | 0.018 | ||

| ROTA | −1.41 | 0.179 | *** | −0.237 | 0.345 | |

| LOGTA | −0.033 | 0.015 | ** | −0.036 | 0.025 | |

| LOGMCAP | −0.012 | 0.006 | * | 0.004 | 0.007 | |

| LOGSALES | −0.017 | 0.013 | 0.026 | 0.02 | ||

| MBVRATIO | −0.005 | 0.002 | * | 0.000 | 0.001 | |

| DEBTEQUITY | 0.008 | 0.005 | 0.017 | 0.029 | ||

| Effects Specification | ||||||

| Cross-section fixed (dummy variables) | ||||||

| Root MSE | 0.450 | 0.229 | ||||

| Mean dependent var. | 0.524 | 0.191 | ||||

| S.D. dependent var. | 0.499 | 0.394 | ||||

| Akaike into criterion | 1.531 | 0.215 | ||||

| Schwarz criterion | 2.431 | 0.894 | ||||

| Hannan–Quinn criter. | 1.852 | 0.483 | ||||

| Durbin–Watson stat. | 2.354 | 2.182 | ||||

| R-Squared | 0.189 | 0.662 | ||||

| Adj. R-Squared | 0.051 | 0.597 | ||||

| S.E. of regression | 0.487 | 0.250 | ||||

| Sum squared resid | 720.517 | 23.760 | ||||

| Log likelihood | −2208.147 | 26.032 | ||||

| F-statistic | 1.372 | 10.073 | ||||

| Prob(F-statistic) | 0.000 | 0.000 | ||||

| Cross-sections included | 509 | 65 | ||||

| Total panel (balanced) observations: | 3563 | 455 | ||||

| Dependent Variable: DIVCUT | ||||||

| Method: Panel Least Squares | ||||||

| Sample: 2015–2021 | ||||||

| Periods included: 7 | ||||||

| White period standard errors & covariance (d.f. corrected) | ||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Agrawal, A. Impact of Elimination of Dividend Distribution Tax on Indian Corporate Firms Amid COVID Disruptions. J. Risk Financial Manag. 2021, 14, 413. https://doi.org/10.3390/jrfm14090413

Agrawal A. Impact of Elimination of Dividend Distribution Tax on Indian Corporate Firms Amid COVID Disruptions. Journal of Risk and Financial Management. 2021; 14(9):413. https://doi.org/10.3390/jrfm14090413

Chicago/Turabian StyleAgrawal, Anshu. 2021. "Impact of Elimination of Dividend Distribution Tax on Indian Corporate Firms Amid COVID Disruptions" Journal of Risk and Financial Management 14, no. 9: 413. https://doi.org/10.3390/jrfm14090413

APA StyleAgrawal, A. (2021). Impact of Elimination of Dividend Distribution Tax on Indian Corporate Firms Amid COVID Disruptions. Journal of Risk and Financial Management, 14(9), 413. https://doi.org/10.3390/jrfm14090413