Cognitive User Interface for Portfolio Optimization

Abstract

1. Introduction

2. Related Work

2.1. Chatbot and the IBM Watson Assistant

2.2. SS&C Algorithmics Portfolio Optimization Service

- sectors, such as IT, health care, energy, real estate, and consumer staples;

- environmental, sustainability, controversy, governance, and social priorities (in many cases referred to as ESG preferences);

- excluding sin investments from consideration such as fossil fuels, military, gambling, tobacco, or alcohol;

- allocating to domestic investments vs. foreign investments; and,

- diversification preferences and no-short-sales restriction.

3. Methods

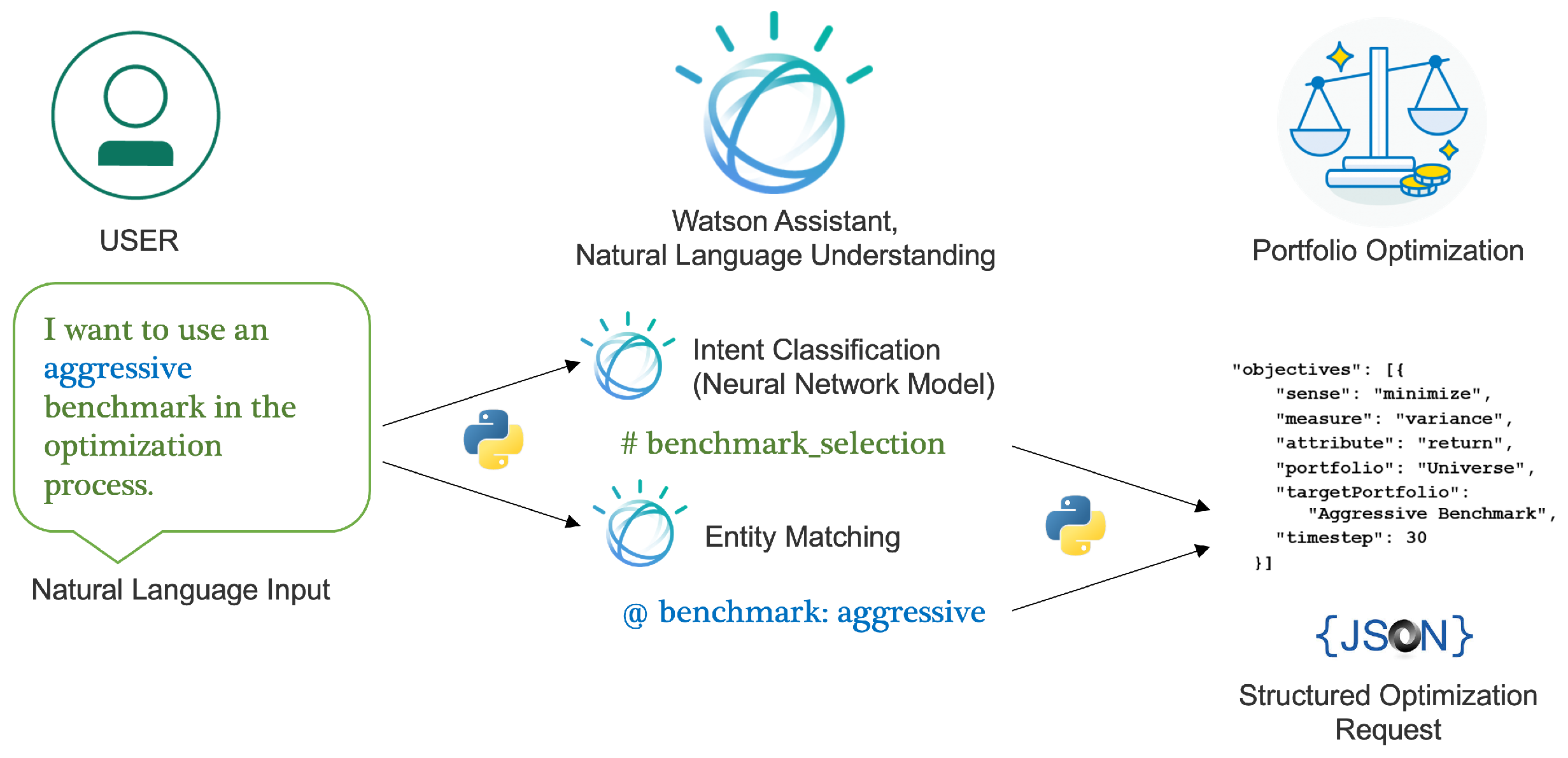

3.1. Intent Classification

3.2. Entity Matching

3.3. Global Variables and Optimization Problem Formulation

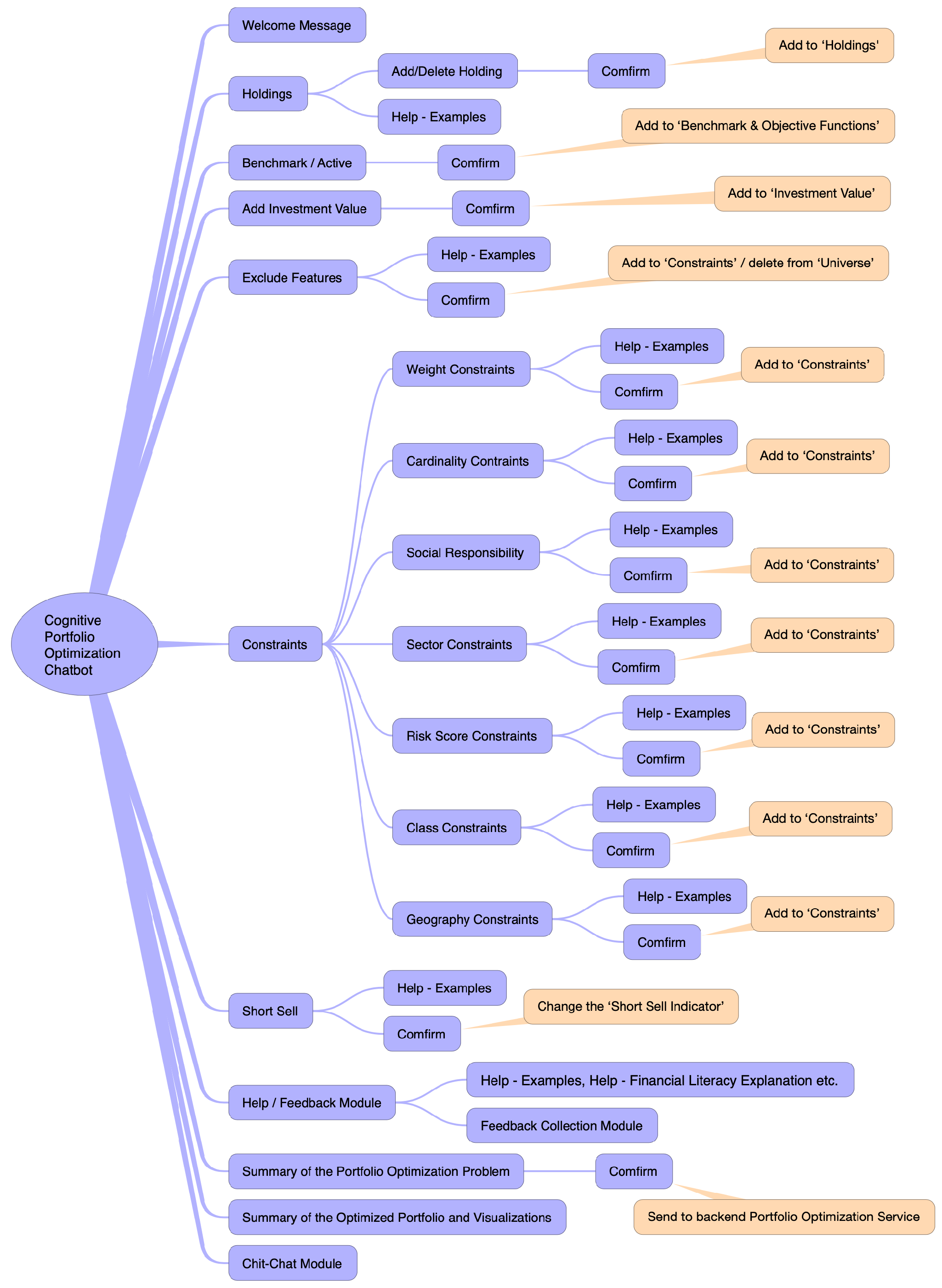

3.4. Conversation Management

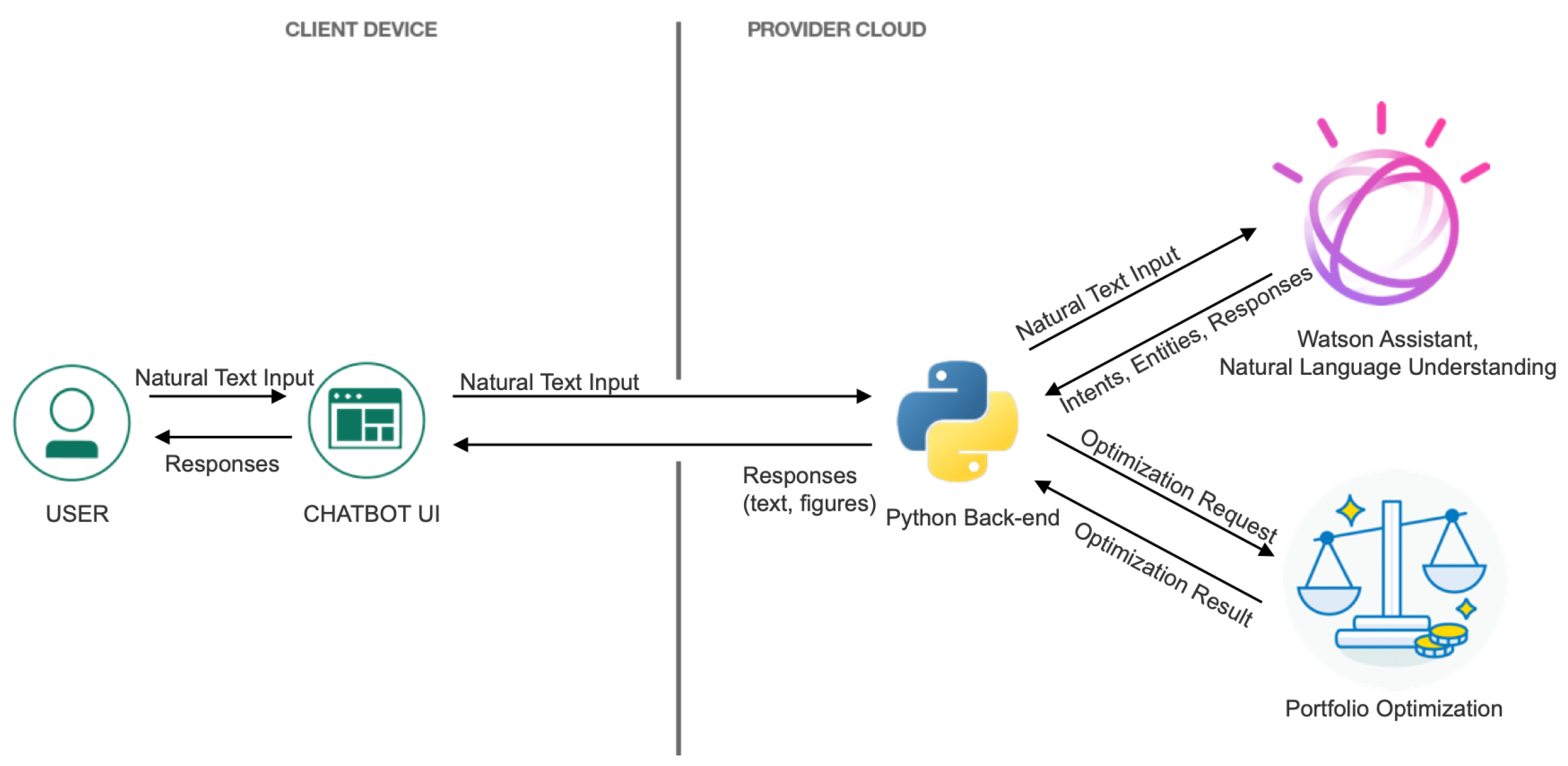

3.5. System Design

3.6. Paragraph Handling

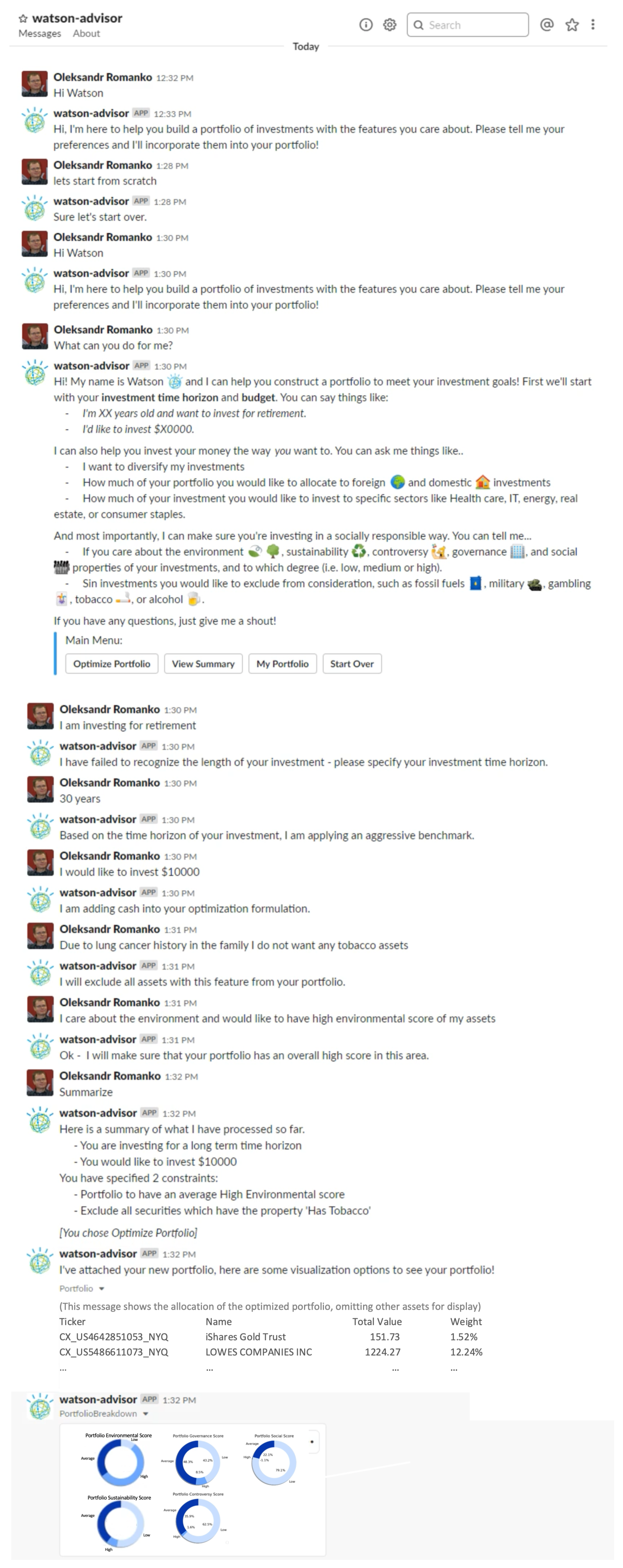

4. Implementation

5. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Brandtzaeg, Petter Bae, and Asbjørn Følstad. 2017. Why people use chatbots. In International Conference on Internet Science. New York: Springer, pp. 377–92. [Google Scholar]

- Burmeister, Curt, Helmut Mausser, and Oleksandr Romanko. 2010. Using trading costs to construct better replicating portfolios. In 2010 Enterprise Risk Management Symposium Monograph. Schaumburg: Society of Actuaries, pp. 1–24. [Google Scholar]

- Cameron, Gillian, David Cameron, Gavin Megaw, Raymond Bond, Maurice Mulvenna, Siobhan O’Neill, Cherie Armour, and Michael McTear. 2017. Towards a chatbot for digital counselling. Paper presented at the 31st International BCS Human Computer Interaction Conference, Sunderland, UK, 3–6 July; pp. 1–7. [Google Scholar]

- Chen, Ying, JD Elenee Argentinis, and Griff Weber. 2016. Ibm watson: How cognitive computing can be applied to big data challenges in life sciences research. Clinical Therapeutics 38: 688–701. [Google Scholar] [CrossRef] [PubMed]

- Clarizia, Fabio, Francesco Colace, Marco Lombardi, Francesco Pascale, and Domenico Santaniello. 2018. Chatbot: An education support system for student. In International Symposium on Cyberspace Safety and Security. New York: Springer, pp. 291–302. [Google Scholar]

- Cocca, Teodoro. 2016. Potential and limitations of virtual advice in wealth management. Journal of Financial Transformation 44: 45–57. [Google Scholar]

- Colby, Kenneth Mark, Sylvia Weber, and Franklin Dennis Hilf. 1971. Artificial paranoia. Artificial Intelligence 2: 1–25. [Google Scholar] [CrossRef]

- Collins, J Michael. 2012. Financial advice: A substitute for financial literacy? Financial Services Review 21: 307. [Google Scholar] [CrossRef]

- Cornuejols, Gerard, and Reha Tütüncü. 2006. Optimization Methods in Finance. 5 vols. Cambridge: Cambridge University Press. [Google Scholar]

- Cui, Lei, Shaohan Huang, Furu Wei, Chuanqi Tan, Chaoqun Duan, and Ming Zhou. 2017. Superagent: A customer service chatbot for e-commerce websites. Paper presented at ACL 2017, System Demonstrations, Vancouver, BC, Canada, 30 July–4 August; pp. 97–102. [Google Scholar]

- da Silva Oliveira, Jeferson, Danubia Bueno Espíndola, Regina Barwaldt, Luciano Maciel Ribeiro, and Marcelo Pias. 2019. Ibm watson application as faq assistant about moodle. Paper presented at the 2019 IEEE Frontiers in Education Conference, Cincinnati, OH, USA, 16–19 October; pp. 1–8. [Google Scholar]

- Ferrucci, David A. 2012. Introduction to “this is watson”. IBM Journal of Research and Development 56: 1. [Google Scholar] [CrossRef]

- Fischer, Rene, and Ralf Gerhardt. 2007. Investment mistakes of individual investors and the impact of financial advice. Paper presented at 20th Australasian Finance & Banking Conference, Sydney, Australia, 12–14 December. [Google Scholar]

- Goel, Ashok, Tory Anderson, Jordan Belknap, Brian Creeden, William Hancock, Mithun Kumble, Shanu Salunke, Bradley Sheneman, Abhinaya Shetty, and B Wilden. 2016. Using watson for constructing cognitive assistants. Advances in Cognitive Systems 4: 1–16. [Google Scholar]

- Harlow, WV, Keith C Brown, and Stephen E Jenks. 2020. The use and value of financial advice for retirement planning. The Journal of Retirement 7: 46–79. [Google Scholar] [CrossRef]

- Hoy, Matthew B. 2018. Alexa, siri, cortana, and more: An introduction to voice assistants. Medical Reference Services Quarterly 37: 81–88. [Google Scholar] [CrossRef]

- Jenkins, Marie-Claire, Richard Churchill, Stephen Cox, and Dan Smith. 2007. Analysis of user interaction with service oriented chatbot systems. In International Conference on Human-Computer Interaction. New York: Springer, pp. 76–83. [Google Scholar]

- Kelly, John E, III, and Steve Hamm. 2013. Smart Machines: IBM’s Watson and the Era of Cognitive Computing. Columbia: Columbia University Press. [Google Scholar]

- Lee, Chih-Wei, Yau-Shian Wang, Tsung-Yuan Hsu, Kuan-Yu Chen, Hung-yi Lee, and Lin-shan Lee. 2018. Scalable sentiment for sequence-to-sequence chatbot response with performance analysis. Paper presented at 2018 IEEE International Conference on Acoustics, Speech and Signal Processing, Calgary, AB, Canada, 15–20 April; pp. 6164–8. [Google Scholar]

- Lui, Alison, and George William Lamb. 2018. Artificial intelligence and augmented intelligence collaboration: regaining trust and confidence in the financial sector. Information & Communications Technology Law 27: 267–283. [Google Scholar]

- Markowitz, Harry. 1952. Portfolio selection. The Journal of Finance 7: 77–91. [Google Scholar]

- Martin, Alistair, Jama Nateqi, Stefanie Gruarin, Nicolas Munsch, Isselmou Abdarahmane, Marc Zobel, and Bernhard Knapp. 2020. An artificial intelligence-based first-line defence against covid-19: Digitally screening citizens for risks via a chatbot. Scientific Reports 10: 1–7. [Google Scholar] [CrossRef] [PubMed]

- Mausser, Helmut, and Oleksandr Romanko. 2014. Computing equal risk contribution portfolios. IBM Journal of Research and Development 58: 5:1–5:12. [Google Scholar] [CrossRef]

- Memeti, Suejb, and Sabri Pllana. 2018. Papa: A parallel programming assistant powered by ibm watson cognitive computing technology. Journal of computational science 26: 275–84. [Google Scholar] [CrossRef]

- Miner, Adam S, Liliana Laranjo, and A Baki Kocaballi. 2020. Chatbots in the fight against the covid-19 pandemic. NPJ Digital Medicine 3: 1–4. [Google Scholar] [CrossRef]

- Montmarquette, Claude, and Nathalie Viennot-Briot. 2019. The gamma factors and the value of financial advice. Annals of Economics and Finance 20: 387–411. [Google Scholar]

- Murtaza, Syed Shariyar, Paris Lak, Ayse Bener, and Armen Pischdotchian. 2016. How to effectively train ibm watson: Classroom experience. Paper presented at 2016 49th Hawaii International Conference on System Sciences, Koloa, HI, USA, 5–8 January; pp. 1663–70. [Google Scholar]

- Nuruzzaman, Mohammad, and Omar Khadeer Hussain. 2018. A survey on chatbot implementation in customer service industry through deep neural networks. Paper presented at 2018 IEEE 15th International Conference on e-Business Engineering, Xi’An, China, 12–14 October; pp. 54–61. [Google Scholar]

- Okuda, Takuma, and Sanae Shoda. 2018. Ai-based chatbot service for financial industry. Fujitsu Scientific and Technical Journal 54: 4–8. [Google Scholar]

- Przegalinska, Aleksandra, Leon Ciechanowski, Anna Stroz, Peter Gloor, and Grzegorz Mazurek. 2019. In bot we trust: A new methodology of chatbot performance measures. Business Horizons 62: 785–97. [Google Scholar] [CrossRef]

- Ranoliya, Bhavika R, Nidhi Raghuwanshi, and Sanjay Singh. 2017. Chatbot for university related faqs. Paper presented at 2017 International Conference on Advances in Computing, Communications and Informatics, Udupi, India, 13–16 September; pp. 1525–30. [Google Scholar]

- Rese, Alexandra, Lena Ganster, and Daniel Baier. 2020. Chatbots in retailers’ customer communication: How to measure their acceptance? Journal of Retailing and Consumer Services 56: 102176. [Google Scholar] [CrossRef]

- Romanko, Oleksandr, and Helmut Mausser. 2016. Robust scenario-based value-at-risk optimization. Annals of Operations Research 237: 203–18. [Google Scholar] [CrossRef]

- Romanko, Oleksandr, and Helmut Mausser. 2017. Applications of conic linear optimization in financial engineering. In Advances and Trends in Optimization with Engineering Applications. Edited by Tamas Terlaky, Miguel F. Anjos and Shabbir Ahmed. Philadelphia: SIAM, Chapter 12. pp. 149–60. [Google Scholar]

- Su, Ming-Hsiang, Chung-Hsien Wu, Kun-Yi Huang, Qian-Bei Hong, and Hsin-Min Wang. 2017. A chatbot using lstm-based multi-layer embedding for elderly care. Paper presented at 2017 International Conference on Orange Technologies, Singapore, 8–10 December; pp. 70–74. [Google Scholar]

- Wallace, Richard S. 2009. The anatomy of alice. In Parsing the Turing Test. New York: Springer, pp. 181–210. [Google Scholar]

- Weizenbaum, Joseph. 1966. Eliza—A computer program for the study of natural language communication between man and machine. Communications of the ACM 9: 36–45. [Google Scholar] [CrossRef]

- Xu, Anbang, Zhe Liu, Yufan Guo, Vibha Sinha, and Rama Akkiraju. 2017. A new chatbot for customer service on social media. Paper presented at Proceedings of the 2017 CHI Conference on Human Factors in Computing Systems, Denver, CO, USA, 6–11 May; pp. 3506–10. [Google Scholar]

- Zhou, Li, Jianfeng Gao, Di Li, and Heung-Yeung Shum. 2020. The design and implementation of xiaoice, an empathetic social chatbot. Computational Linguistics 46: 53–93. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Intent Name | Optimization Problem Formulation |

|---|---|

| active_invest | rejects the usage of any benchmark and tries to identify the objective function. |

| passive_invest | add benchmark by attempting to identify the proper benchmark of investment based on investment time horizon and risk preferences. |

| add_current_holding | add/delete the entity describing holdings details (stock, etc.). |

| add_investment_value | increase or decrease the total value of portfolio. |

| exclude_asset_features | add constraints on excluding assets with certain features in universe |

| social_responsible_value | add constraints on assets with certain overall social responsibility scores and identify the requirement as low, medium or high. |

| constrain_asset_weight | add constraints on the weight of assets. |

| constrain_cardinality | add constraints on the cardinality of asset weights. |

| constrain_sector | add constraints on certain sectors. |

| constrain_risk_score | add constraints on risk level, measured by asset risk score. |

| constrain_asset_class | add constraints on asset classes. |

| constrain_geography | add constraints based on geography (i.e. domestic, foreign). |

| allow_short_sell | add indicator to allow short selling. |

| max_investment_weight | add maximum weight allowed for each asset allocation. |

| help | supplementary intent to provide help and instructions for using the chatbot. |

| Entity Type | Description and Role in Formulating Optimization Problem |

|---|---|

| asset_name | the code and name of assets in the trading universe |

| benchmark | the name of the benchmark portfolios |

| portfolio_measurement | metric used in formulating the objective function such as return rate, variance and tracking error. |

| optimizing_direction | minimize and maximize in the optimization objective. |

| time_unit | time unit measurement in investment horizon such as years, months, days. |

| inequality_relationship | equal to, less than or equal, more than or equal used to formulate constraints. |

| asset_features | used to construct constraints to include or exclude assets with the target features, such as alcohol, fossil fuels, gambling, tobacco, military etc. |

| social_responsibility | used to construct constraints on the social responsibility level of assets, the social responsibility criteria included are sustainability, environmental-friendliness, and governance. |

| asset_sector | used to identify the asset sector that the constraints apply to, such as information technology, finance etc. |

| asset_class | used to identify the asset class that the constraints apply to, such as stocks, bonds etc. |

| asset_geography | used to identify the asset geographical features that the constraints apply to, such as domestic, foreign etc. |

| constrain_geography | add constraints on geography (domestic, foreign) assets in constraints. |

| attitude | used to distinguish the attitude from positive, negative and ambiguous. |

| add_or_delete | distinguish the processing of adding or deleting. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

He, Y.; Romanko, O.; Sienkiewicz, A.; Seidman, R.; Kwon, R. Cognitive User Interface for Portfolio Optimization. J. Risk Financial Manag. 2021, 14, 180. https://doi.org/10.3390/jrfm14040180

He Y, Romanko O, Sienkiewicz A, Seidman R, Kwon R. Cognitive User Interface for Portfolio Optimization. Journal of Risk and Financial Management. 2021; 14(4):180. https://doi.org/10.3390/jrfm14040180

Chicago/Turabian StyleHe, Yuehuan, Oleksandr Romanko, Alina Sienkiewicz, Robert Seidman, and Roy Kwon. 2021. "Cognitive User Interface for Portfolio Optimization" Journal of Risk and Financial Management 14, no. 4: 180. https://doi.org/10.3390/jrfm14040180

APA StyleHe, Y., Romanko, O., Sienkiewicz, A., Seidman, R., & Kwon, R. (2021). Cognitive User Interface for Portfolio Optimization. Journal of Risk and Financial Management, 14(4), 180. https://doi.org/10.3390/jrfm14040180