Quanto Pricing beyond Black–Scholes

Abstract

1. Introduction

2. The NTS Framework for Quanto Options

3. Data on Retail Structured Products

- (i)

- Credit risk: All products are basically a type of bearer bonds and, thus, are expected to include counterparty risk. Therefore, one would assume, considering only this effect, tradable prices to be somewhat lower than those coming from classical option pricing models as investors would want to be compensated for taking on default risk.

- (ii)

- Issuer’s PnL: Issuers intend to profit from structuring and pricing RSPs which is reflected in the overpricing- and the lifecycle-hypothesis. Overpricing means a certain margin is charged on top of the model price (see Chen and Kensinger (1990) and Chen and Sears (1990) for the US retail market and Wilkens et al. (2003) for Germany). According to the lifecycle-hypothesis, this charge tends to decrease over time as the issuer presumably wants to profit from initial investors selling back later (see Stoimenov and Wilkens (2005)).

- (iii)

- Dividends: The Nikkei 225 is a price index and, thus, does not account for dividends. Therefore, all else being equal, the index would decrease over time through this effect. The chosen market setups (Black–Scholes and NTS alike) do not account for such dividends.

4. Naive Model Calibration Using Quanto Options

- Step 1:

- Draw , and , with U, and E being independent.

- Step 2:

- Calculate

- Step 3:

- If , return V. Otherwise return to Step 1.

- (1)

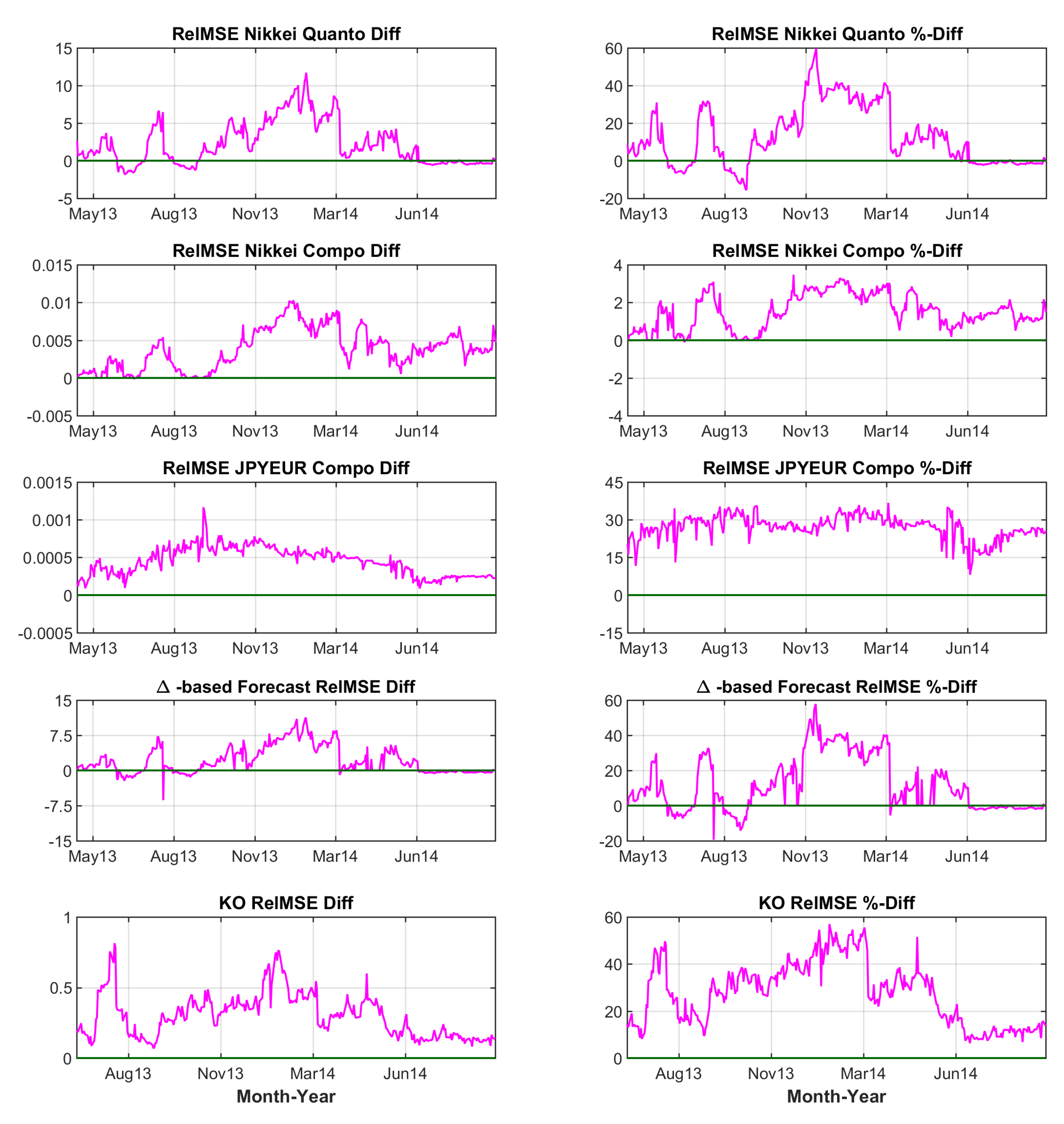

- As the Black–Scholes model is contained in the NTS framework, RelMSE differences are non-negative and positive values support the NTS model. While on some days both models seem to fit equally well, the NTS setup generally outperforms.

- (2)

- Although parameter stability seems to be an issue for the NTS model, the use of yesterday’s parameter values still produces more realistic model prices than the Black–Scholes setup. This is of practical relevance as traders have to resort to readily available parameter values.

- (3)

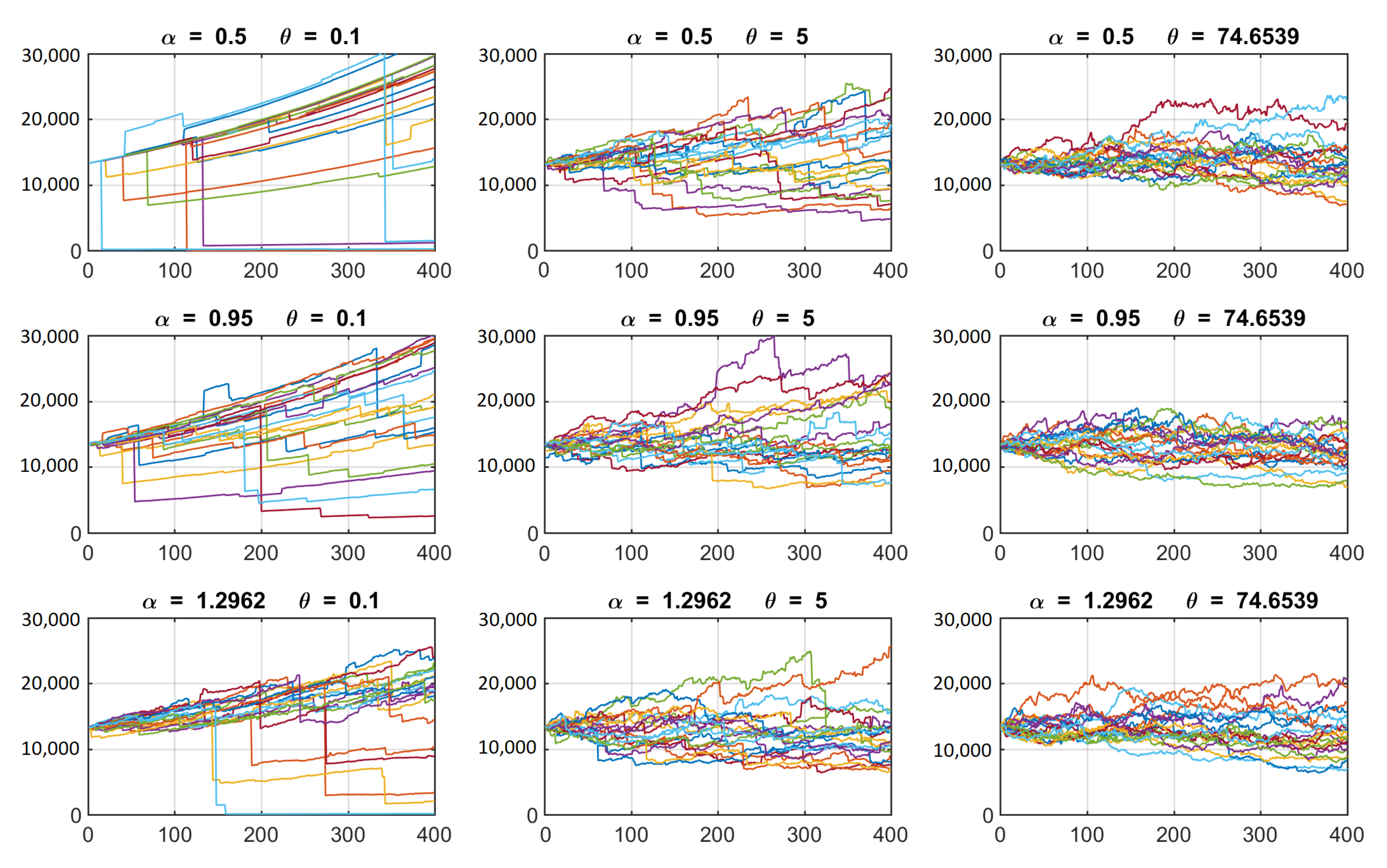

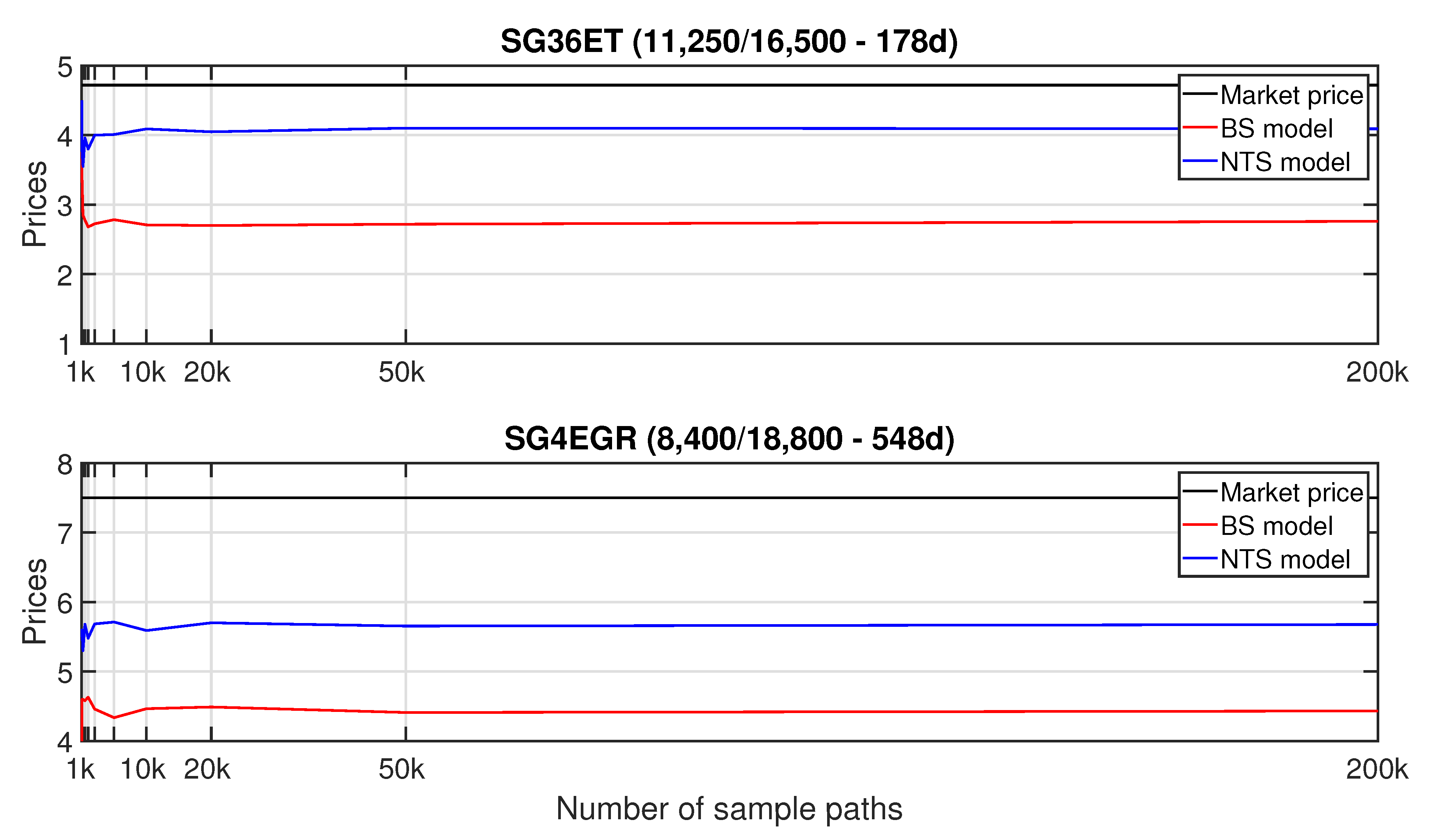

- Concerning barrier risk, the NTS model clearly dominates the Gaussian version. The main reason for this follows from Figure 2. To accommodate fat tails, the Gaussian setup generally produces distributions that are flatter in the center. However, when the barriers of KO warrants are close enough to the current underlying level, significant overestimation of knock-out risk and, thus, lower prices will result. Moreover, we may – in some heuristic sense – relate our findings to hedging strategies. Since perfect delta-hedging is impossible, due to the unremovable jump risk in the NTS setup16, we can expect prices to be higher.

5. Compo Options and a New Calibration Algorithm

- Step 1:

- Calibrate via compo options on .

- Step 2:

- Take the historical correlation (based on the roughly 12-year sample in Section 2) and calibrate via compo options on N.

- Step 3:

- Use the implied volatilities and obtained in Step 2 and calibrate via quanto options on N.

- Step 1:

- Step 2:

- Calibrate the Y-parameters via compo options on .

- Step 3:

- Calibrate the X-parameters and the correlation via compo options on N.

- Step 4:

- Calibrate the quanto option formula using the Y-parameters obtained in Step 2, but let the X-parameters and the correlation, , vary under the restriction that the relative Nikkei compo fit is not worse than that of the Black–Scholes model (see Algorithm BS).

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Proofs

Appendix B. Identifier Numbers (WKNs) of All RSPs Used in Empirical Analysis

References

- Baeumer, Boris, and Mark M. Meerschaert. 2010. Tempered stable Lévy motion and transit super-diffusion. Journal of Computational and Applied Mathematics 233: 2438–48. [Google Scholar] [CrossRef]

- Ballotta, Laura, Griselda Deelstra, and Grégory Rayée. 2015. Quanto Implied Correlation in a Multi-Lévy Framework. Available online: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2569015 (accessed on 10 October 2020).

- Barndorff-Nielsen, Ole Eiler, and Sergei Z. Levendorskii. 2001. Feller processes of normal inverse Gaussian type. Quantitative Finance 1: 318–31. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2001. Normal Modified Stable Processes. Department of Economics, Discussion Paper Series; Oxford: University of Oxford, p. 72. [Google Scholar]

- Baxter, Martin, and Andrew Rennie. 1996. Calculus: An Introduction to Derivative Pricing. Cambridge: Cambridge University Press. [Google Scholar]

- Bianchi, Michele L., Svetlozar R. Rachev, Young S. Kim, and Frank J. Fabozzi. 2010. Tempered stable distributions and processes in finance: Numerical analysis. In Mathematical and Statistical Methods for Actuarial Sciences and Finance. Edited by Marco Corazza and Claudio Pizzi. Berlin and Heidelberg: Springer. [Google Scholar]

- Branger, Nicole, and Matthias Muck. 2012. Keep on smiling? The pricing of Quanto options when all covariances are stochastic. Journal of Banking & Finance 36: 1577–91. [Google Scholar]

- Brigo, Damiano, and Aurélien Alfonsi. 2005. Credit default swap calibration and derivatives pricing with the SSRD stochastic intensity model. Finance and Stochastics 9: 29–42. [Google Scholar] [CrossRef]

- Broadie, Mark, and Paul Glasserman. 1997. A continuity correction for discrete barrier options. Mathematical Finance 7: 325–48. [Google Scholar] [CrossRef]

- Carr, Peter, and Dilip Madan. 1999. Option pricing and the Fast Fourier Transform. Journal of Computational Finance 2: 61–73. [Google Scholar] [CrossRef]

- Chen, Andrew H., and John W. Kensinger. 1990. An analysis of market-index certificates of deposit. Journal of Financial Services Research 4: 93–110. [Google Scholar] [CrossRef]

- Chen, Kuang C., and R. Stephen Sears. 1990. Pricing the SPIN. Financial Management 19: 36–47. [Google Scholar] [CrossRef]

- Delbaen, Freddy, and Walter Schachermayer. 1994. A general version of the fundamental theorem of asset pricing. Mathematische Annalen 312: 463–520. [Google Scholar] [CrossRef]

- Derman, Emanuel, Piotr Karasinski, and Jeffrey Wecker. 1990. Understanding guaranteed exchange-rate contracts in foreign stock investments. In Goldman Sachs Quantitative Strategies Research Notes. New York: Goldman Sachs. [Google Scholar]

- Dimitroff, Georgi, Alexander Szimayer, and Andreas Wagner. 2009. Quanto Option Pricing in the Parsimonious Heston Model. Available online: https://ssrn.com/abstract=1477387 (accessed on 23 September 2009).

- Eberlein, Ernst, and Kathrin Glau. 2014. Variational solutions of the pricing PIDEs for European options in Lévy models. Applied Mathematical Finance 21: 417–50. [Google Scholar] [CrossRef]

- Eberlein, Ernst, Kathrin Glau, and Antonis Papapantoleon. 2009. Analyticity of the Wiener-Hopf factors and valuation of exotic options in Lévy models. In Advanced Mathematical Methods for Finance. Berlin and Heidelberg: Springer, pp. 223–45. [Google Scholar]

- Eberlein, Ernst, Kathrin Glau, and Antonis Papapantoleon. 2010. Analysis of Fourier transform valuation formulas and applications. Applied Mathematical Finance 17: 211–40. [Google Scholar] [CrossRef]

- Eberlein, Ernst, and Ulrich Keller. 1995. Hyperbolic distributions in finance. Bernoulli 1: 281–99. [Google Scholar] [CrossRef]

- Eberlein, Ernst, Ulrich Keller, and Karsten Prause. 1998. New insights into smile, mispricing and value at risk: the hyperbolic model. Journal of Business 71: 371–405. [Google Scholar] [CrossRef]

- Eberlein, Ernst, Antonis Papapantoleon, and Albert N. Shiryaev. 2009. Esscher transform and the duality principle for multidimensional semimartingales. Annals of Applied Probability 19: 1944–71. [Google Scholar] [CrossRef]

- Escobar, Marcos, Peter Hieber, and Matthias Scherer. 2014. Efficiently pricing double barrier derivatives in stochastic volatility models. Review of Derivatives Research 17: 191–216. [Google Scholar] [CrossRef]

- Fink, Holger, Sebastian Geissel, Jörn Sass, and Frank T. Seifried. 2019. Implied risk aversion: an alternative rating system for retail structured products. Review of Derivatives Research 22: 357–87. [Google Scholar] [CrossRef]

- Geman, Hélyette, and Marc Yor. 1996. Pricing and hedging double-barrier options: a probabilistic approach. Mathematical Finance 6: 365–78. [Google Scholar] [CrossRef]

- Gerber, Hans. U., and Elias S. W. Shiu. 1994. Option pricing by Esscher transforms. Transactions of Society of Actuaries 48: 99–191. [Google Scholar]

- Guillaume, Florence. 2013. The αVG model for multivariate asset pricing: calibration and extension. Review of Derivatives Research 16: 25–52. [Google Scholar] [CrossRef]

- Guillaume, Florence, and Wim Schoutens. 2012. Calibration risk: Illustrating the impact of calibration risk under the Heston model. Review of Derivatives Research 15: 57–79. [Google Scholar] [CrossRef][Green Version]

- Kawai, Reiichiro, and Hiroki Masuda. 2012. Infinite variation tempered stable Ornstein-Uhlenbeck processes with discrete observations. Communications in Statistics-Simulation and Computation 41: 125–39. [Google Scholar] [CrossRef][Green Version]

- Kim, Young S., Rosella Giacometti, Svetlozar T. Rachev, Frank J. Fabozzi, and Domenico Mignacca. 2012. Measuring financial risk and portfolio optimization with a non-Gaussian multivariate model. Annals of Operations Research 201: 325–43. [Google Scholar] [CrossRef]

- Kim, Young S., Jaesung Lee, Stefan Mittnik, and Jiho Park. 2015. Quanto option pricing in the presence of fat tails and asymmetric dependence. Journal of Econometrics 187: 512–20. [Google Scholar] [CrossRef]

- Kunitomo, Naoto, and Masayuki Ikeda. 1992. Pricing options with curved boundaries. Mathematical Finance 2: 275–98. [Google Scholar] [CrossRef]

- Park, Jiho, Youngrok Lee, and Jaesung Lee. 2013. Pricing of quanto option under the Hull and White stochastic volatility model. Communications of the Korean Mathmatical Society 28: 615–33. [Google Scholar] [CrossRef]

- Sato, Ken-Iti. 1999. Lévy Processes and Infinitely Divisible Distributions. Cambridge: Cambridge University Press. [Google Scholar]

- Schoutens, Wim, and Geert Van Damme. 2011. The β-variance gamma model. Review of Derivatives Research 14: 263–82. [Google Scholar] [CrossRef]

- Stoimenov, Pavel A., and Sascha Wilkens. 2005. Are structured products ’fairly’ priced? An analysis of the german market for equity-linked instruments. Journal of Banking and Finance 29: 2971–93. [Google Scholar] [CrossRef]

- Teng, Long, Matthias Ehrhardt, and Michael Günther. 2015. The pricing of quanto options under dynamic correlation. Journal of Computational and Applied Mathematics 275: 304–10. [Google Scholar] [CrossRef]

- Wilkens, Sascha, Carsten Erner, and Klaus Röder. 2003. The pricing of structured products in germany. Journal of Derivatives 11: 55–69. [Google Scholar] [CrossRef]

- Wilmott, Paul. 2006. Paul Wilmott on Quantitative Finance. Hoboken: John Whiley & Sons, Ltd. [Google Scholar]

| 1 | All proofs are given in Appendix A. Appendix B identifies all RSPs used in our empirical study. |

| 2 | To avoid confusion, we will state the specific asset or currency in question in parentheses. |

| 3 | |

| 4 | Our option data set starts on 16 April 2013, cf. Section 3. |

| 5 | As discussed below, for the maximization procedure we imposed the restrictions and . |

| 6 | CME options on its Nikkei 225 USD futures being one of the few exceptions. |

| 7 | Note, we focus only on simple option types and ignore more complex structures, like bonus-, lookback- or rainbow-certificates, which are left for future research. |

| 8 | The data were obtained from the data provider ARIVA.DE AG which also supplies the Frankfurt retail exchange Börse Frankfurt Zertifikate AG. |

| 9 | The identifiers (WKNs) of these tracker and the above plain vanilla as well as KO options are provided in Appendix B. |

| 10 | The main input factor (apart from time to maturity and interest rates) that changes is the price of the underlying, hence the term delta-based due to the Black–Scholes Greek delta. |

| 11 | The minimization is carried out in MATLAB using the routine fmincon. For this procedure the pricing formulas from Section 2 are invoked. |

| 12 | A very good overview and description of the various techniques can be found in Eberlein et al. (2009, 2010), or Eberlein and Glau (2014) and references therein. |

| 13 | The latter rely on the so-called Wiener-Hopf factorization, providing approximations of the characteristic functions of the running minimum and maximum and have been successfully applied to variance-gamma-type Lévy models (see Schoutens and Van Damme (2011)). |

| 14 | It should be mentioned that, for tax purposes, even in the case of a knock-out these types of products usually still pay a fixed amount of EUR. For the sake of simplicity, we ignore this feature. |

| 15 | For all considerations, riskless rates were taken to be the lending rates from the European Central Bank and the Bank of Japan, respectively, at each trading day of the observation period. |

| 16 | See the discussion in the concluding section in Kim et al. (2015) |

| 17 | This and all other proof are presented in Appendix A. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Black–Scholes | NTS | |||

|---|---|---|---|---|

| Parameters | ||||

| 2 | − | |||

| − | − | |||

| − | − | |||

| − | − | |||

| Nikkei 225 in EUR | ||||

| log-likelihood | 8834 | 8962 | ||

| AIC | ||||

| BIC | ||||

| JPYEUR | ||||

| log-likelihood | ||||

| AIC | ||||

| BIC | ||||

| Bivariate Model | ||||

| log-likelihood | ||||

| AIC | ||||

| BIC | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fink, H.; Mittnik, S. Quanto Pricing beyond Black–Scholes. J. Risk Financial Manag. 2021, 14, 136. https://doi.org/10.3390/jrfm14030136

Fink H, Mittnik S. Quanto Pricing beyond Black–Scholes. Journal of Risk and Financial Management. 2021; 14(3):136. https://doi.org/10.3390/jrfm14030136

Chicago/Turabian StyleFink, Holger, and Stefan Mittnik. 2021. "Quanto Pricing beyond Black–Scholes" Journal of Risk and Financial Management 14, no. 3: 136. https://doi.org/10.3390/jrfm14030136

APA StyleFink, H., & Mittnik, S. (2021). Quanto Pricing beyond Black–Scholes. Journal of Risk and Financial Management, 14(3), 136. https://doi.org/10.3390/jrfm14030136