In order to better understand the MSCI of China A-shares, we further decomposed the related 236 stocks into 10 sectors and examined the performance of each sector in the same sample period. Moreover, we analyzed the predictability of sector returns on MCASI’s return and present a re-portfolio analysis for these 10 sectors with different allocation methods.

3.3.1. Sector Portfolios

In this section, we mainly classify and analyze the MSCI China A-share constituents to distinguish the performances of different industries and analyze whether there is a sector portfolio that performs better than others.

We divided the 236 stocks of MSCI China A-shares into 10 categories by their industry properties, forming 10 sector portfolios. The specific sector codes and names are in Panel A of

Table 8, where the sector

O includes all stocks that do not belong to other nine sectors. Each sector portfolio is constructed by all stocks of this sector with equal weight. For a given month

t, the return of the sector portfolio

k is

where

denotes the return of stock

i in the sector

k in month

t, and

is the number of all stocks in sector

k. The cumulative return of the sector portfolio

k is calculated as

.

Table 8 shows sector information of MSCI China A-shares. Panel A shows that sector code tags of MSCI China A-shares. Panel B show basic data statistics of corresponding sector portfolios. The sample period extends from January 2010 to December 2018.

Panel B of

Table 8 gives basic statistics for these sector portfolios. These results show that the manufacturing sector (Code: C) and the finance sector (Code: J) have the most stocks, with 94 and 49, respectively. For the average of portfolio returns (monthly), the sector portfolio of the information transfer, software and information technology services (Code: I), with 14 stocks, has the largest monthly average return of 2.06%, and the sector portfolio of the mining and quarrying (Code: B) has the lowest monthly average return. The minimum monthly returns of these sector portfolios are concentrated around −20% in the interval range (−26.23%, −18.15%). The maximum monthly returns of the sector portfolios of the construction (Code: E) and the transportation, storage and postal services (Code: G) are outstanding in all portfolios, reaching 57.08% and 47.78%, respectively. Sector portfolio I and sector portfolio O have the best annualized returns of 48.47% and 36.80%, respectively, and the annualized return of the sector portfolio B is the only negative value of −2.71% in all sector portfolios. For the performance of the Sharpe ratio, sector portfolios I, O, and C have the highest values of 0.64, 0.59, and 0.54, respectively; the sector portfolio of mining and quarrying (Code: B) has the lowest Sharpe ratio, −0.07. The standard deviation of the returns of the sector portfolios indicates that the portfolio of the manufacturing (C) has lower risk exposure; sector portfolios E, I, J and K (construction sector, IT sector, finance sector and Real estate sector) have the highest risk exposure. In order to further measure the risk attribution of the portfolios, we also calculated the maximum drawdown of their net values, which can be used to measure the maximum loss of the portfolio net value during the investment period. The results of the maximum drawdown show that the portfolio of the manufacturing (C) has the lowest historical maximum drawdown (the lowest risk exposure) in all sector portfolios, and the portfolio of constructions (E) has the maximum risk exposure. Both mining and quarrying (B), transportation (G), utilities (D) and information technology (I) are sectors with relatively higher maximum drawdown.

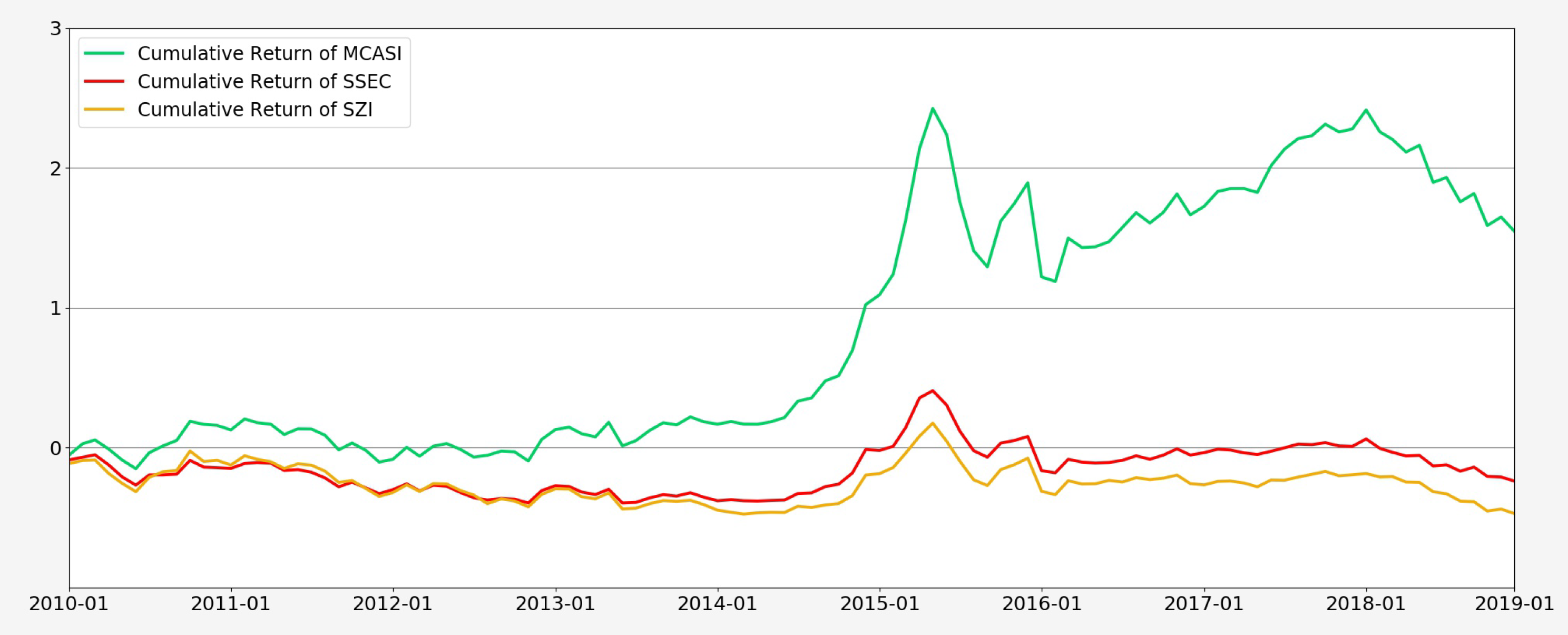

Figure 3 shows the time-series cumulative returns of all sector portfolios and MCASI. Portfolios C, I, and O have higher cumulative returns relative to MCASI, while other portfolios perform poorly relatively. At the same time, the synergy among the cumulative return curves of these portfolios is very clear and high, and the exhibited performances are mainly due to the financial crash during 2015. From 2010 to 2014, there is no obviously outstanding performance in these portfolios, and the market situation is relatively sluggish. From 2016 to 2018, there is no obvious advance for any portfolio, and all sector portfolios have been basic in the concussion period. One of the reasons for the poor performance of these portfolios during this period is that the Chinese stock market performed poorly and the Chinese financial environment was relatively unstable due to the ongoing US–China trade negotiations in 2018.

Figure 3 shows that the cumulative return of portfolio B is basically maintained below the 0 scale, and investing in the mining and quarrying sector of MSCI China A-shares is not a good plan for investors.

To further analyze the high synergy shown in

Figure 3, we conducted a Pearson correlation analysis for the returns of all sector portfolios.

Table 9 shows that all correlation coefficients are statistically significant and positive, and all these values are large.

Table 9 indicates that the constituents of MSCI China A-shares have a high synergy of return performance under the industry classification. Therefore, these portfolios cannot satisfy investors’ hedging needs with the condition of short-selling constraints from the hedging perspective.

Table 9 shows the correlation analysis of sector portfolios of MSCI China A-shares.

We further conducted a seasonality analysis of these sector portfolios.

Table 10 shows that the results of the monthly aggregation analysis in Panel A show that January and June have negative aggregated average returns in all portfolios, indicating that investors need to pay extra attention to these two months when making investment decisions. In February, March, April, July, October, November, and December, each sector has a better return performance than other months. Almost all sectors exhibit poor performances in June, which suggests a better investment strategy in each month in different sectors, as well as avoiding trading in June. The quarterly aggregation analysis in Panel B shows that the first and the fourth quarters have relatively better average returns, and considering the results in Panel A, the good performances of these portfolios in the first quarter are mainly caused by returns in February and March. The average monthly returns of portfolios C, I, and O are positive in all four quarters. Portfolio O has the best average return in the second quarter, but the averages of other many portfolios are negative in this quarter. Both the first and fourth quarters have positive average returns for all sectors in the MSCI of China A-shares. In Panel C, each portfolio performs well in 2014 and performs poorly in 2011 and 2018. In 2018, the Chinese stock market fluctuated more. Under such circumstances, the average monthly return loss of the portfolio D during the year is the least in all portfolios, only −0.44%. The losses of portfolios C, F and G are more serious, reaching −2.36%, −2.59%, −2.57% per month, respectively. The different losses of these sector portfolios in 2018 are directly related to the US–China trade negotiations in 2018.

Table 10 introduces seasonal analysis of sector portfolios of MSCI China A-shares, which are grouped and averaged for the months, quarters, and years. The sample period extends from January 2010 to December 2018.

In summary, among these sector portfolios, the manufacturing, information transfer, software and information technology services sectors, and sector O, have better investment attributes, such as higher returns, lower risk exposure, and larger Sharpe ratios, and the synergy of returns is high for these sector portfolios. In terms of seasonality, February, March, April, July, October, November, and December are the best months for all sector portfolios, and January and June are the worst months. The year 2018 is the bad year for all sector portfolios in the sample period.

3.3.2. Sector Return and MCASI’s Return

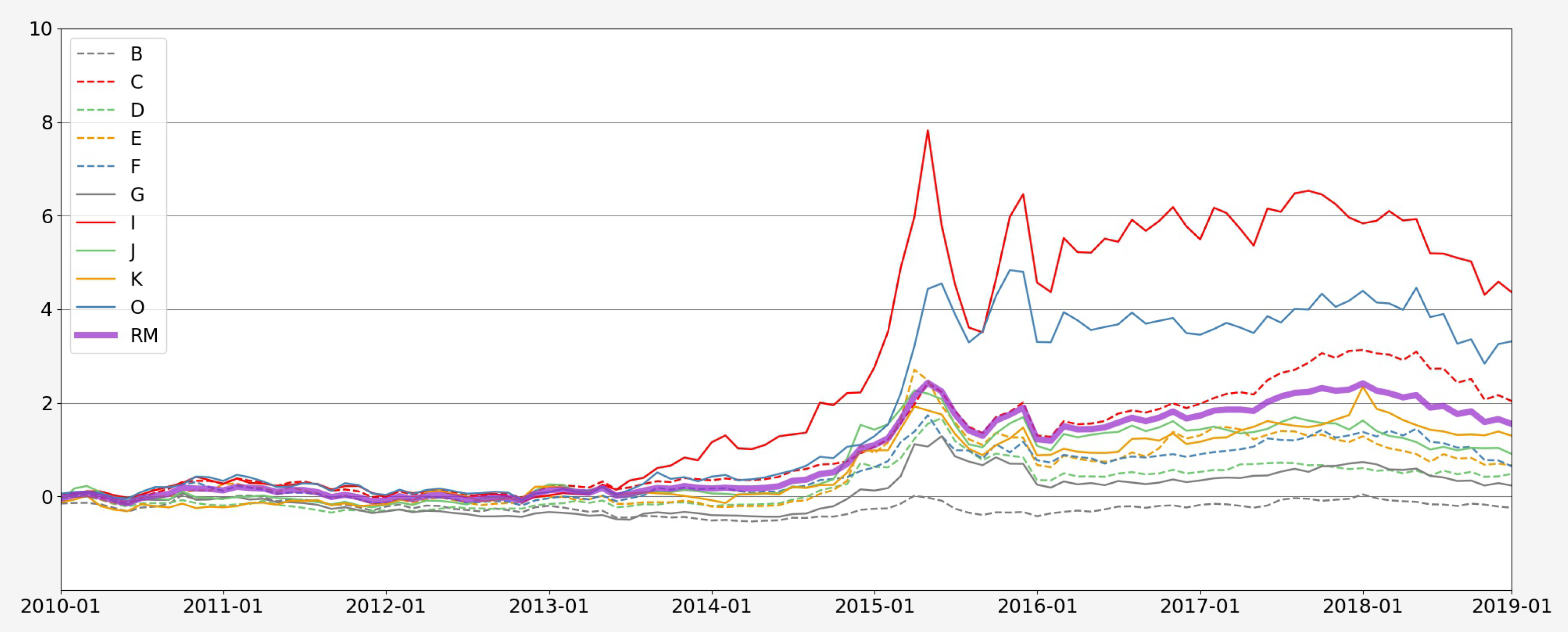

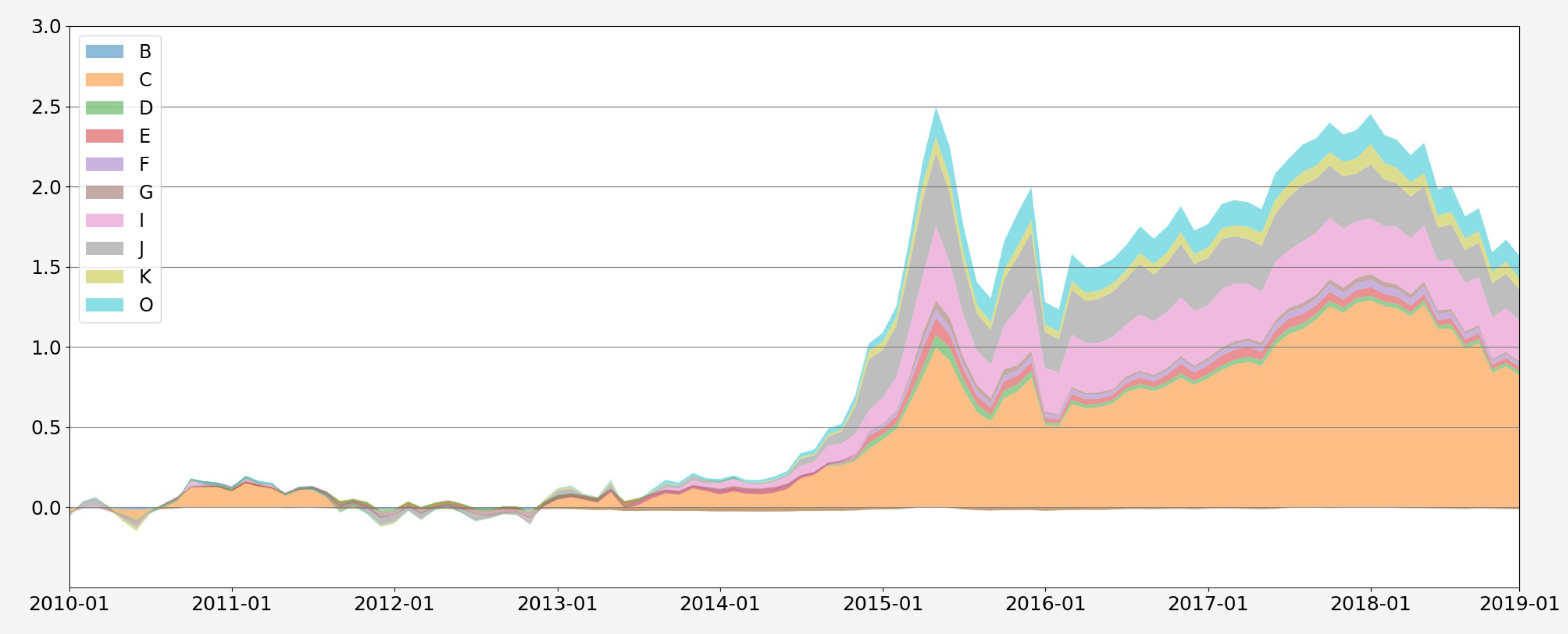

In this section, we analyze the relations between the return of the sector portfolios and MCASI’s return. First, we combined the returns of these sector portfolios with their weights and plotted the dynamic contribution of each sector portfolio to MCASI’s return in

Figure 4. The weight of the return of each sector portfolio on MCASI’s return depends on the number of stocks in this sector, and the sectors’ weights on MCASI’s return are presented in Panel A of

Table 11. Portfolio C (Manufacturing) has the largest weight of 41.10%, followed by portfolio J (Finance), which has a weight of 20.76%. The weights of other sector portfolios are basically around 5% with the smallest weight of 3.39% for portfolio F (wholesale and retail trades).

The relation between MCASI’s return and the sector portfolio’s return is

where

denotes the weight of the sector portfolio

k on MCASI’s return;

is the return of the sector portfolio

k for month

t;

S represents the set of all sector portfolios. In

Figure 4, portfolio C has an absolute contribution to MCASI’s return, followed by the portfolio J, and portfolios I and O also have some contribution. Compared with portfolios C and J, which have high contributions on MCASI’s return caused by their high weights, portfolios I and J have high contributions due to their respective high returns. Therefore, from the investment perspective, and regarding MCASI’s return with higher investment weights in portfolio I, J will perform better, and investors need to pay more attention to sectors I and J.

Since MCASI’s return constructed by all constituents belongs to different sectors, do the sector portfolios have predictive effects on MCASI’s return? In order to answer this question, we use the sector-weighted returns of sector portfolios to predict the future MCASI returns. First, we conducted a univariate analysis to simply judge the effect of the returns of a single sector portfolio on MCASI’s return. Then, we conducted a multivariate analysis using the returns of all sector portfolios to forecast the future MCASI returns.

Table 11 introduces the coefficients of the regressions for forecasting MCASI’s return with returns of sector portfolios. Panel A presents the weights of these sectors of MSCI China A-shares, which were calculated according to the number of stocks in each sector. Panel B shows the specific results of regressions, where

indicates the return of sector portfolio

i for month

t.

Panel B of

Table 11 introduces the specific results of all regressions. For the univariate regressions, the returns of portfolios B, E, G, I, and J all have a significantly positive impact on MCASI’s return. For the multivariate regression of the last column of Panel B, the returns of portfolios C and D become significant and have a negative impact on the future MCASI return while they are insignificant for the results of the univariate regressions. The returns of portfolios E and I remain significant and have positive impact on the future MCASI return in the multivariate regression results. Due to the high synergy between sector portfolios which is showed in the correlation analysis of

Table 9 and

Figure 3, there may be multicollinearity in the multivariate regression to make the coefficients of these variables unreliable. However, considering the results of both univariate and multivariate models, we also conclude that the return of the sector construction and the return of the sector of information transfer, software and information technology services have significant and positive effects on the future MCASI return.

3.3.3. Portfolio Analysis for Sectors

Investors are interested in how to allocate cash among different sectors to ensure lower risk exposure or a larger Sharpe ratio. In this section, we provide various types of portfolio analyses for the sector return of MSCI China A-shares.

The first type of portfolio is just concerned with MCASI’s return (RM), mentioned above, which serves as our benchmark. The second one is an equal-weighted portfolio (EWP) for these sector returns, and the third one is return-weighted portfolio (RWP), which focuses on the past returns of sectors. Specifically, for the next period, RWP allocates the cash weight of each sector to

where

is the average excess return of sector

k over the past 36 months for month

. The condition that the average excess return is greater than zero is due to the short-selling constraints in the Chinese stock market.

The fourth portfolio is the Sharpe ratio-weighted portfolio (SRWP), and the weight for each sector is

where

is the same definition as above and

is the standard deviation of monthly returns over the past 36 months for sector

k in month

.

The fifth portfolio is a volatility-weighted portfolio (VWP), the weight of which is calculated by

where

is the same definition as above. The fifth portfolio type is just a rough way to avoid risks without considering the covariance among sectors’ returns. So, the sixth is the minimum-variance portfolio (MVP) according to

Markowitz (

1952) with the goal of minimizing portfolio risk exposure, and the weights of sectors need to solve a quadratic programming as

where the condition of

is due to the same reason of short-selling constraints as RWP. We use sectors’ returns over the past 36 months to solve the quadratic programming and obtain the optimal weights for any month

t.

Considering the dynamic mean and volatility for the sectors’ returns, the last portfolio type is the AR-GARCH minimum-variance portfolio (AGMVP). Based on

Hu et al. (

2019), we used the AR(1)-GARCH(1,1) model for each sector portfolio’s time-series returns instead of ARMA-GARCH models in

Hu et al. (

2019), where they fit ARMA(1,1)-GARCH(1,1) for the returns of crypto assets. Then, we also approached the joint distribution of the sample innovations from AR(1)-GARCH(1,1) models by the multivariate Copula method, where the Copula function is based on the multivariate normal distribution. For each one-step forecast, we generated 1000 joint sample innovations and calculated 1000 simulated returns for each sector based on the coefficients of the AR-GARCH models. Then, we followed MVP’s procedure to obtain the optimal weights with the simulated returns. The initial 36 observations were utilized to generate the first one-step optimal sector weights and each of the next optimal sector weights, and, consistent with the constructed portfolios above, we used the recent 36 observations to fit the AR-GARCH models.

Our sample period extends from January 2010 to December 2018, and the observation period of our six portfolios is from January 2013 to December 2018, and we used the previous 36 data to compute related measures.

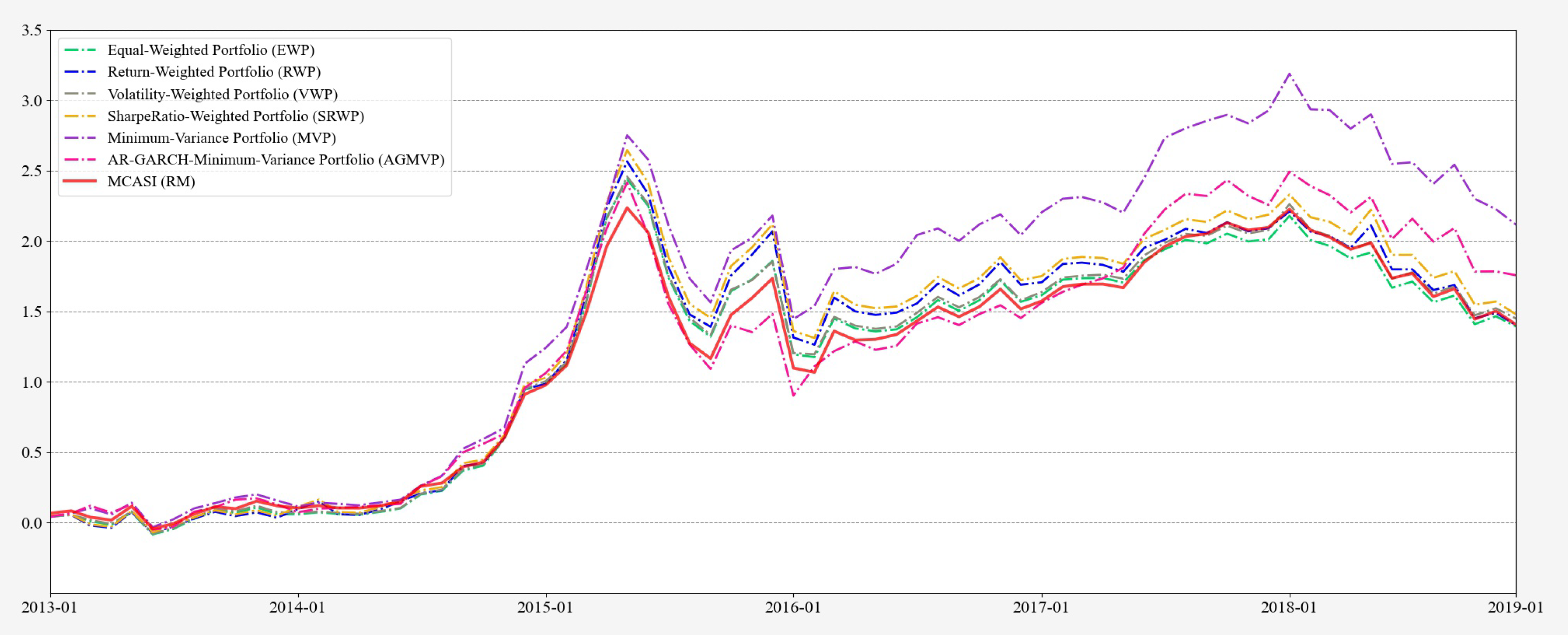

Table 12 shows the information of these seven portfolios. We refreshed our portfolios’ weights every month and there are 72 observations to compare these portfolios’ performances. MVP has the highest average of 1.9% and maximum of 27.21% for monthly returns, and the corresponding values for MCASI (RM) are the lowest, at 1.49% and 19.42%. All portfolios have approximate minimums in their monthly returns. MVP has the highest annualized return of 36.22%, followed by AGMVP, which has the annualized return of 29.29%. The results of the Sharpe ratio also show that the MVP exhibits the best performance in our sample. In terms of a risk measure worthy of investors’ attention, the maximum drawdown results suggest that MVP has an advantage among the seven portfolios, and the AGMVP performs poorly. EWP, RWP, VWP and SRWP are not particularly prominent compared to MCASI in almost all respects.

Figure 5 also shows the cumulative return curves for all six portfolios, and MVP has an obvious advantage in terms of performance.

Table 12 introduces portfolios’ information for sector return of MSCI China A-shares. These portfolios are described in the text, including the basic portfolio with respect to MCASI’s return (RM), equal-weighted portfolio (EWP), return-weighted portfolio (RWP), volatility-weighted portfolio (VWP), Sharpe ratio-weighted portfolio (SRWP), minimum-variance portfolio (MVP), and AR-GARCH-minimum-variance portfolio (AGMVP). Our sample period extends from January 2010 to December 2018, and the observation period of our six portfolios is from January 2013 to December 2018 considering we used the previous 36 data to compute related measures.

Investors can use the classic Markowitz portfolio approach to allocate their money in these sectors of MSCI China A-shares and achieve a better investment performance in terms of average return, standard deviation, annualized return, the Sharpe ratio, and maximum drawdown.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}