The Impact of Corporate Social Responsibility as a Marketing Investment on Firms’ Performance: A Risk-Oriented Approach

Abstract

:1. Introduction

2. Relevant Literature and Hypothesis Development

2.1. CSR Initiatives and Firm Performance

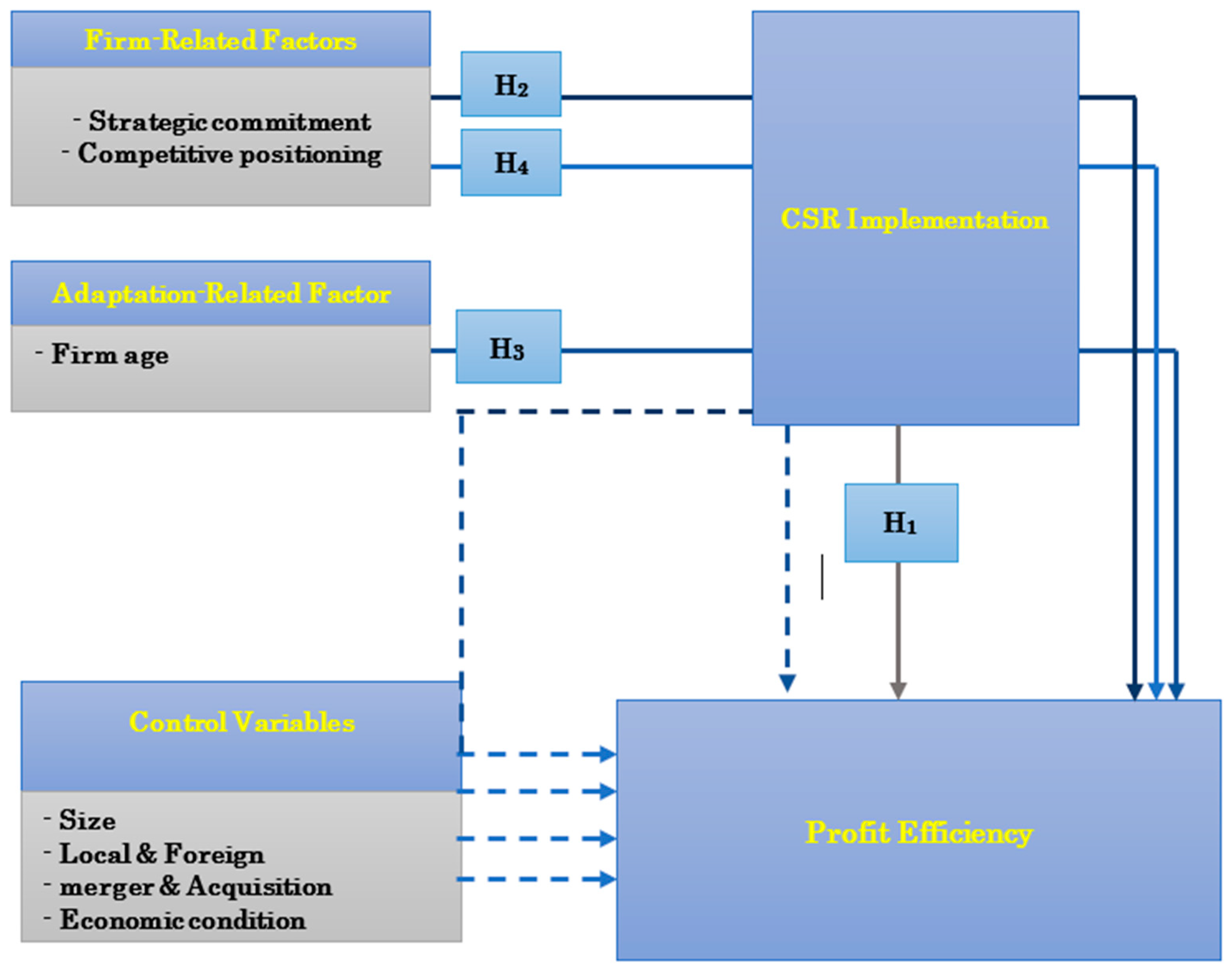

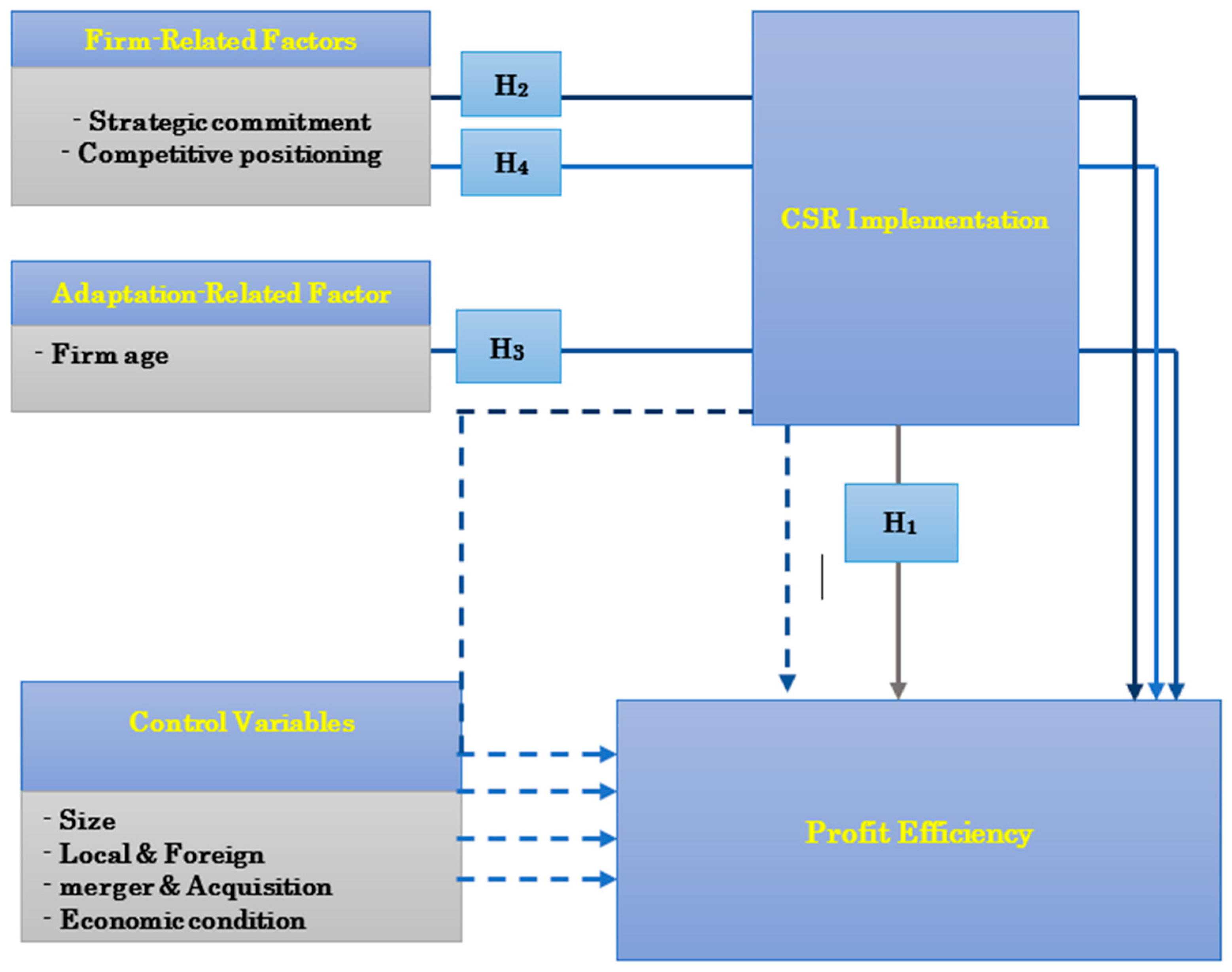

2.2. Moderating Factors of the Effect of CSR on Profit Efficiency

2.3. CSR Strategic Commitment (Firm-Related Factor)

2.4. Firm Age (Adoption-Related Factors)

2.5. Competitive Positioning (Firm-Related Factor)

3. Conceptual Model: Linking CSR Initiatives to Financial Performance

4. Research Method

4.1. Sample Selection and Data

4.2. Profit Efficiency Estimation

4.3. Using a Two-Level Hierarchical Linear Model

4.4. Computing Truncated Measures

5. Findings

5.1. Sensitivity Analysis

5.2. Profit Efficiency Scores Were Derived Using Equation (2)

6. Discussion

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Acharyya, Madhu. 2008. In Measuring the Benefits of Enterprise Risk Management in Insurance: An Integration of Economic Value Added and Balanced Score Card Approaches. ERM Monograph. Schaumburg: Society of Actuaries, pp. 1–25. [Google Scholar]

- Agudelo, Mauricio Andrés Latapí, Lára Jóhannsdóttir, and Brynhildur Davídsdóttir. 2019. A literature review of the history and evolution of corporate social responsibility. International Journal of Corporate Social Responsibility 4: 1–23. [Google Scholar] [CrossRef] [Green Version]

- Albuquerque, Rui, Yrjö Koskinen, and Chendi Zhang. 2019. Corporate social responsibility and firm risk: Theory and empirical evidence. Management Science 65: 4451–69. [Google Scholar] [CrossRef] [Green Version]

- Alexander, Gordon J., and Rogene A. Buchholz. 1978. Corporate social responsibility and stock market performance. Academy of Management Journal 21: 479–86. [Google Scholar] [CrossRef]

- Astara, Olga-Helen, Roido Mitoula, and E. Theodoropoulou. 2015. Corporate Social Responsibility: A marketing tool and/or a factor for the promotion of sustainable development for companies? An empirical examination of listed companies in the Athens Stock Exchange. International Journal of Strategic Innovative Marketing 2: 17–33. [Google Scholar] [CrossRef]

- Aupperle, Kenneth E., and Deane Van Pham. 1989. An expanded investigation into the relationship of corporate social responsibility and financial performance. Employee Responsibilities and Rights Journal 2: 263–74. [Google Scholar] [CrossRef]

- Badulescu, Alina, Daniel Badulescu, Tomina Saveanu, and Roxana Hatos. 2018. The relationship between firm size and age, and its social responsibility actions—Focus on a developing country (Romania). Sustainability 10: 805. [Google Scholar] [CrossRef] [Green Version]

- Bai, Xuan, and Jeanine Chang. 2015. Corporate social responsibility and firm performance: The mediating role of marketing competence and the moderating role of market environment. Asia Pacific Journal of Management 32: 505–30. [Google Scholar] [CrossRef]

- Bauer, Paul W., Allen N. Berger, Gary D. Ferrier, and David B. Humphrey. 1993. Consistency conditions for regulatory analysis of financial institutions: A comparison of frontier efficiency methods. Journal of Economics and Business 50: 85–114. [Google Scholar] [CrossRef] [Green Version]

- Belasri, Sanaa, Mathieu Gomes, and Guillaume Pijourlet. 2020. Corporate social responsibility and bank efficiency. Journal of Multinational Financial Management 54: 100612. [Google Scholar] [CrossRef]

- Berger, Allen N., Diana Hancock, and David B. Humphrey. 1993. Bank efficiency derived from the profit function. Journal of Banking & Finance 17: 317–47. [Google Scholar]

- Berger, Allen N., and Loretta J. Mester. 1997. Inside the black box: What explains differences in the efficiencies of financial institutions? Journal of Banking & Finance 21: 895–947. [Google Scholar]

- Berger, Allen N., and Robert De Young. 1997. Problem loans and cost efficiency in commercial banks. Journal of Banking & Finance 21: 849–70. [Google Scholar]

- Bhatnagar, Amit, and Sanjoy Ghose. 2004. Segmenting consumers based on the benefits and risks of Internet shopping. Journal of Business Research 57: 1352–60. [Google Scholar] [CrossRef]

- Bhattacharya, Chitra Bhanu, and Sankar Sen. 2004. Doing better at doing good: When, why, and how consumers respond to corporate social initiatives. California Management Review 47: 9–24. [Google Scholar] [CrossRef]

- Bogdanich, Walt. 2008. Heparin Is Now Suspected in 62 Fatalities across U.S. New York Times. Available online: http://www.nytimes.com/2008/04/10/health/policy/10heparin.html (accessed on 11 May 2008).

- Brammer, Stephen, Chris Brooks, and Stephen Pavelin. 2006. Corporate social performance and stock returns: UK evidence from disaggregate measures. Financial Management 35: 97–116. [Google Scholar] [CrossRef] [Green Version]

- Cegliński, Paweł, and Anna Wiśniewska. 2016. CSR as a source of competitive advantage: The case study of Polpharma group. Journal of Corporate Responsibility and Leadership 3: 9–25. [Google Scholar] [CrossRef] [Green Version]

- Chang, Kiyoung, Incheol Kim, and Ying Li. 2014. The heterogeneous impact of corporate social responsibility activities that target different stakeholders. Journal of Business Ethics 125: 211–34. [Google Scholar] [CrossRef]

- Chava, Sudheer, and Amiyatosh Purnanandam. 2010. Is default risk negatively related to stock returns? The Review of Financial Studies 23: 2523–59. [Google Scholar] [CrossRef] [Green Version]

- Cheng, Beiting, Ioannis Ioannou, and George Serafeim. 2014. Corporate social responsibility and access to finance. Strategic Management Journal 35: 1–23. [Google Scholar] [CrossRef]

- Commander, Cindy. 2008. Move Past Stereotypes and Connect with CIOs. (March 3). Available online: www.adage.com (accessed on 10 March 2020).

- Crane, Andrew, and John Desmond. 2002. Societal marketing and morality. European Journal of Marketing 36: 548–69. [Google Scholar] [CrossRef] [Green Version]

- Donaldson, Thomas, and Lee E. Preston. 1995. The stakeholder theory of the corporation: Concepts, evidence, and implications. Academy of Management Review 20: 65–91. [Google Scholar] [CrossRef]

- Du, Shuili, Chitrabhan B. Bhattacharya, and Sankar Sen. 2007. Reaping relational rewards from corporate social responsibility: The role of competitive positioning. International Journal of Research in Marketing 24: 224–41. [Google Scholar] [CrossRef]

- Du, Shuili, Chitrabhan B. Bhattacharya, and Sankar Sen. 2010. Maximizing business returns to corporate social responsibility (CSR): The role of CSR communication. International Journal of Management Reviews 12: 8–19. [Google Scholar] [CrossRef]

- Du, Shuili, Valérie Swaen, Adam Lindgreen, and Sankar Sen. 2013. The roles of leadership styles in corporate social responsibility. Journal of Business Ethics 114: 155–69. [Google Scholar] [CrossRef] [Green Version]

- Fiori, Giovanni, Francesca Di Donato, and Maria Federica Izzo. 2015. Corporate social responsibility and stock prices: A study on the italian market. Corporate Ownership & Control 12: 600–9. [Google Scholar]

- Fombrun, Charles J., Naomi A. Gardberg, and Joy M. Sever. 2000. The Reputation Quotient SM: A multi-stakeholder measure of corporate reputation. Journal of Brand Management 7: 241–55. [Google Scholar] [CrossRef]

- Gatti, Lucia, Peter Seele, and Lars Rademacher. 2019. Grey zone in–greenwash out. A review of greenwashing research and implications for the voluntary-mandatory transition of CSR. International Journal of Corporate Social Responsibility 4: 1–15. [Google Scholar] [CrossRef]

- Gautam, Richa, Anju Singh, and Debraj Bhowmick. 2016. Demystifying relationship between corporate social responsibility (CSR) and financial performance: An Indian business perspective. Independent Journal of Management & Production 7: 1034–62. [Google Scholar]

- Godfrey, Paul C. 2005. The relationship between corporate philanthropy and shareholder wealth: A risk management perspective. Academy of Management Review 30: 777–98. [Google Scholar] [CrossRef] [Green Version]

- Godfrey, Paul C., Craig B. Merrill, and Jared M. Hansen. 2009. The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Management Journal 30: 425–45. [Google Scholar] [CrossRef]

- Grewal, Rajdeep, and Rebecca J. Slotegraaf. 2007. Embeddedness of organizational capabilities. Decision Sciences 38: 451–88. [Google Scholar] [CrossRef]

- Gruca, Thomas S., and Lopo L. Rego. 2005. Customer satisfaction, cash flow, and shareholder value. Journal of Marketing 69: 115–30. [Google Scholar] [CrossRef]

- Hamidu, Ahmad, Md Haron, and Azlan Amran. 2015. Corporate social responsibility: A review on definitions, core characteristics and theoretical perspectives. Mediterranean Journal of Social Sciences 6: 83–95. [Google Scholar] [CrossRef] [Green Version]

- Han, Heesup, Xiaoting Chi, Chang-Sik Kim, and Hyungseo Bobby Ryu. 2020. Activators of airline customers’ sense of moral obligation to engage in pro-social behaviors: Impact of CSR in the Korean marketplace. Sustainability 12: 4334. [Google Scholar] [CrossRef]

- Hanssens, Dominique M., Daniel Thorpe, and Carl Finkbeiner. 2012. Marketing when customer equity matters”. International Journal of Communication Research 2: 9–16. [Google Scholar]

- Hategan, Camelia-Daniela, Nicoleta Sirghi, Ruxandra-Ioana Curea-Pitorac, and Vasile-Petru Hategan. 2018. Doing well or doing good: The relationship between corporate social responsibility and profit in Romanian companies. Sustainability 10: 1041. [Google Scholar] [CrossRef] [Green Version]

- Heugens, Pursey, and Nikolay Dentchev. 2007. Taming Trojan horses: Identifying and mitigating corporate social responsibility risks. Journal of Business Ethics 75: 151–70. [Google Scholar] [CrossRef] [Green Version]

- Hogan, John E., Donald R. Lehmann, Maria Merino, Rajendra K. Srivastava, Jacquelyn S. Thomas, and Peter C. Verhoef. 2002a. Linking customer assets to financial performance. Journal of Service Research 5: 26–38. [Google Scholar] [CrossRef]

- Hogan, John E., Katherine N. Lemon, and Roland T. Rust. 2002b. Customer equity management: Charting new directions for the future of marketing. Journal of service Research 5: 4–12. [Google Scholar] [CrossRef]

- Husted, Bryan W. 2005. Risk management, real options, corporate social responsibility. Journal of Business Ethics 60: 175–83. [Google Scholar] [CrossRef]

- Hyman, Michael R., and Ike Mathur. 2005. Retrospective and prospective views on the marketing/finance interface. Journal of the Academy of Marketing Science 33: 390–400. [Google Scholar] [CrossRef]

- Igalens, Jacques, and Jean-Pascal Gond. 2005. Measuring corporate social performance in France: A critical and empirical analysis of ARESE data. Journal of Business Ethics 56: 131–48. [Google Scholar] [CrossRef]

- Inoue, Yuhei, and Seoki Lee. 2011. Effects of different dimensions of corporate social responsibility on corporate financial performance in tourism-related industries. Tourism Management 32: 790–804. [Google Scholar] [CrossRef]

- Izzo, Maria Federica, and Francesca di Donato. 2012. The Relation between Corporate Social Responsibility and Stock Prices: An analysis of the Italian Listed Companies. Available online: https://ssrn.com/abstract=1986324 (accessed on 2 March 2021).

- Jayachandran, Satish, and Rajan Varadarajan. 2006. Does success diminish competitive responsiveness? Reconciling conflicting perspectives. Journal of the Academy of Marketing Science 34: 284–94. [Google Scholar] [CrossRef]

- Jensen, Michael C. 2010. Value maximization, stakeholder theory, and the corporate objective function. Journal of Applied Corporate Finance 22: 32–42. [Google Scholar] [CrossRef]

- Jia, Ixingping. 2020. Corporate social responsibility activities and firm performance:The moderating role of strategic emphasis and industry competition. Corporate Social Responsibility and Environmental Management 27: 65–73. [Google Scholar] [CrossRef]

- Jo, Hoje, and Maretno A. Harjoto. 2011. Corporate governance and firm value: The impact of corporate social responsibility. Journal of Business Ethics 103: 351–83. [Google Scholar] [CrossRef]

- Jones, Thomas M., and Andrew C. Wicks. 1999. Convergent stakeholder theory. Academy of Management Review 24: 206–21. [Google Scholar] [CrossRef]

- Joyner, Brenda E., and Dinah Payne. 2002. Evolution and implementation: A study of values, business ethics and corporate social responsibility. Journal of Business Ethics 41: 297–311. [Google Scholar] [CrossRef]

- Kalyar, Masood Nawaz, Nosheen Rafi, and Awais Nawaz Kalyar. 2013. Factors affecting corporate social responsibility: An empirical study. Systems Research and Behavioral Science 30: 495–505. [Google Scholar] [CrossRef]

- Kang, Charles, Frank Germann, and Rajdeep Grewal. 2016. Washing away your sins? Corporate social responsibility, corporate social irresponsibility, and firm performance. Journal of Marketing 80: 59–79. [Google Scholar] [CrossRef]

- Kjeldsen, Lisbeth. 2013. Strategic CSR and Performance—The Strategic Effect of CSR initiatives. Master’s thesis, International Business Copenhagen Business School, Copenhagen, Denmark. [Google Scholar]

- Koh, Ping-Sheng, Cuili Qian, and Heli Wang. 2014. Firm litigation risk and the insurance value of corporate social performance. Strategic Management Journal 35: 1464–82. [Google Scholar] [CrossRef]

- Kotler, Philip, and Gary Armstrong. 2016. Principles of Marketing. London: Pearson Education. [Google Scholar]

- Kotler, Philip, and Nancy Lee. 2005. Corporate Social Responsibility: Doing the Most Good for Your Company and Your Cause. Hoboken: John Wiley & Sons. [Google Scholar]

- Krasnikov, Alexander, Satish Jayachandran, and Anil Kumar. 2009. The impact of customer relationship management implementation on cost and profit efficiencies: Evidence from the US commercial banking industry. Journal of Marketing 73: 61–76. [Google Scholar] [CrossRef]

- Lacey, Justine, Richard Parsons, and Kieren Moffat. 2012. Exploring the Concept of a Social Licence to Operate in the Australian Minerals Industry: Results from Interviews with Industry Representatives. EP125553. Brisbane: CSIRO. [Google Scholar]

- Li, Beili, Xu Fan, Susana Álvarez-Otero, Muhammad Safdar Sial, Ubaldo Comite, Jacob Cherian, and László Vasa. 2021. CSR and Workplace Autonomy as Enablers of Workplace Innovation in SMEs through Employees: Extending the Boundary Conditions of Self-Determination Theory. Sustainability 13: 6104. [Google Scholar] [CrossRef]

- Li, Shaomin, Marc Fetscherin, Ilan Alon, Christoph Lattemann, and Kuang Yeh. 2010. Corporate social responsibility in emerging markets. Management International Review 50: 635–54. [Google Scholar] [CrossRef]

- Loose, Simone Mueller, and Hervé Remaud. 2013. Impact of corporate social responsibility claims on consumer food choice: A cross-cultural comparison. British Food Journal 115: 142–66. [Google Scholar] [CrossRef]

- Luo, Xueming, and Chitra Bhanu Bhattacharya. 2006. Corporate social responsibility, customer satisfaction, and market value. Journal of Marketing 70: 1–18. [Google Scholar] [CrossRef]

- Luo, Xueming, and Chitra Bhanu Bhattacharya. 2009. The debate over doing good: Corporate social performance, strategic marketing levers, and firm-idiosyncratic risk. Journal of Marketing 73: 198–213. [Google Scholar] [CrossRef] [Green Version]

- Luo, Xueming, and Naveen Donthu. 2006. Marketing’s credibility: A longitudinal investigation of marketing communication productivity and shareholder value. Journal of Marketing 70: 70–91. [Google Scholar] [CrossRef]

- Mahajan, Prashant, and Suresh Golahit. 2019. Service marketing mix as input and output of higher and technical education: A measurement model based on students’ perceived experience. Journal of Applied Research in Higher Education 12: 151–193. [Google Scholar] [CrossRef]

- Marcoux, Alexei. 2000. Balancing ac. Contemporary Issues in Business Ethics 4: 45–67. [Google Scholar]

- Margolis, Joshua D., and James P. Walsh. 2003. Misery loves companies: Rethinking social initiatives by business. Administrative Science Quarterly 48: 268–305. [Google Scholar] [CrossRef] [Green Version]

- Maudos, Joaquín, and Juan Fernandez De Guevara. 2004. Factors explaining the interest margin in the banking sectors of the European Union. Journal of Banking & Finance 28: 2259–81. [Google Scholar]

- McWilliams, Abagail, and Donald Siegel. 2001. Corporate social responsibility: A theory of the firm perspective. Academy of Management Review 26: 117–27. [Google Scholar] [CrossRef]

- McWilliams, Abagail, Donald S. Siegel, and Patrick M. Wright. 2006. Corporate social responsibility: Strategic implications. Journal of Management Studies 43: 1–18. [Google Scholar] [CrossRef] [Green Version]

- Michelon, Giovanna, Silvia Pilonato, and Federica Ricceri. 2015. CSR reporting practices and the quality of disclosure: An empirical analysis. Critical Perspectives on Accounting 33: 59–78. [Google Scholar] [CrossRef] [Green Version]

- Mints, Aleksey, Andrew Schumann, and Evelina Kamyshnykova. 2020. Stakeholders’ Rank of Reflexion Diagnostics in a Corporate Social Responsibility System. Economic Annals-XXI 181: 92–104. [Google Scholar]

- Mishra, Saurabh, and Sachin B. Modi. 2016. Corporate social responsibility and shareholder wealth: The role of marketing capability. Journal of Marketing 80: 26–46. [Google Scholar] [CrossRef]

- Morsing, Mette, and Majken Schultz. 2006. Corporate social responsibility communication: Stakeholder information, response and involvement strategies. Business Ethics: A European Review 15: 323–38. [Google Scholar] [CrossRef]

- Murray, Keith B., and John B. Montanari. 1986. Strategic management of the socially responsible firm: Integrating management and marketing theory. Academy of Management Review 11: 815–27. [Google Scholar] [CrossRef]

- Peloza, John, and Jingzhi Shang. 2011. How can corporate social responsibility activities create value for stakeholders? A systematic review. Journal of the academy of Marketing Science 39: 117–35. [Google Scholar] [CrossRef]

- Peloza, John. 2006. Using corporate social responsibility as insurance for financial performance. California Management Review 48: 52–72. [Google Scholar] [CrossRef]

- Porter, Michael E., and Mark R. Kramer. 2006. Strategy and society: The link between corporate social responsibility and competitive advantage. Harvard Business Review 84: 78–92. [Google Scholar] [PubMed]

- Preston, Lee E., and Douglas P. O’bannon. 1997. The corporate social-financial performance relationship: A typology and analysis. Business & Society 36: 419–29. [Google Scholar]

- Reinartz, Werner, Manfred Krafft, and Wayne D. Hoyer. 2004. The customer relationship management process: Its measurement and impact on performance. Journal of Marketing Research 41: 293–305. [Google Scholar] [CrossRef]

- Robbins, Stephen, Rolf Bergman, Ian Stagg, and Mary Colter. 2000. Management, 2nd ed. Frenchs Forest: Prentice Hall Australia Pty Ltd., pp. 10–12. [Google Scholar]

- Rust, Roland T., Katherine N. Lemon, and Valarie A. Zeithaml. 2004. Return on marketing: Using customer equity to focus marketing strategy. Journal of Marketing 68: 109–27. [Google Scholar] [CrossRef] [Green Version]

- Sanclemente-Téllez, Juan Carlos. 2017. Marketing and Corporate Social Responsibility (CSR). Moving between broadening the concept of marketing and social factors as a marketing strategy. Spanish Journal of Marketing-ESIC 21: 4–25. [Google Scholar] [CrossRef]

- Schnietz, Karen, and Marc Epstein. 2005. Exploring the financial value of a reputation for corporate social responsibility during a crisis. Corporate Reputation Review 7: 327–45. [Google Scholar] [CrossRef]

- Sharpe, William, Gordon Alexander, and Jeffery Bailey. 1998. Investments, 6th ed. Prentice Hall: International Edition. [Google Scholar]

- Singh, Ramendra, and Sharad Agarwal. 2011. CSR Orientation of Indian Banks and Stakeholder Relationship Marketing Orientation: An Empirical Analysis. Working Paper Series; Kolkata: Indian Institute of Management Calcutta. [Google Scholar]

- Slavova, Irena. 2013. Strategic perspective of corporate social responsibility. Economic Alternatives 7: 90–105. [Google Scholar]

- Srivastava, Rajendra K., Tasadduq A. Shervani, and Liam Fahey. 1998. Market-based assets and shareholder value: A framework for analysis. Journal of Marketing 62: 2–18. [Google Scholar] [CrossRef] [Green Version]

- Strotmann, Harald, Jürgen Volkert, and Melinda Schmidt. 2019. Multinational companies: Can they foster well-being in the eyes of the poor? Results from an empirical case study. International Journal of Corporate Social Responsibility 4: 1–14. [Google Scholar] [CrossRef] [Green Version]

- Sundaram, Anant K., and Andrew C. Inkpen. 2004. The corporate objective revisited. Organization Science 15: 350–63. [Google Scholar] [CrossRef] [Green Version]

- Tonin, Mirco, and Michael Vlassopoulos. 2015. Corporate philanthropy and productivity: Evidence from an online real effort experiment. Management Science 61: 1795–811. [Google Scholar] [CrossRef] [Green Version]

- Úbeda-García, Mercedes, Enrique Claver-Cortés, Bartolomé Marco-Lajara, and Patrocinio Zaragoza-Sáez. 2021. Corporate social responsibility and firm performance in the hotel industry. The mediating role of green human resource management and environmental outcomes. Journal of Business Research 123: 57–69. [Google Scholar] [CrossRef]

- Udayasankar, Krishna. 2008. Corporate social responsibility and firm size. Journal of Business Ethics 83: 167–75. [Google Scholar] [CrossRef]

- Uhlig, Marcela Rocha Haase, Emerson Wagner Mainardes, and Valcemiro Nossa. 2020. Corporate social responsibility and consumer’s relationship intention. Corporate Social Responsibility and Environmental Management 27: 313–24. [Google Scholar] [CrossRef]

- Van Doorn, Jenny, Marjolijn Onrust, Peter C. Verhoef, and Marnix S. Bügel. 2017. The impact of corporate social responsibility on customer attitudes and retention—the moderating role of brand success indicators. Marketing Letters 28: 607–19. [Google Scholar] [CrossRef] [Green Version]

- Vilanova, Marc, Josep Maria Lozano, and Daniel Arenas. 2009. Exploring the nature of the relationship between CSR and competitiveness. Journal of Business Ethics 87: 57–69. [Google Scholar] [CrossRef]

- Vogel, David. 2005. The Market for Virtue: The Potential and Limits of Corporate Social Responsibility. Washington, DC: Brookings Institution Press. [Google Scholar]

- Waddock, Sandra A., and Samuel B. Graves. 1997. The corporate social performance–financial performance link. Strategic Management Journal 18: 303–19. [Google Scholar] [CrossRef]

- Waluyo, Waluyo. 2017. Firm size, firm age, and firm growth on corporate social responsibility in Indonesia: The case of real estate companies. European Research Studies 20: 360–69. [Google Scholar] [CrossRef] [Green Version]

- Weber, Manuela. 2008. The business case for corporate social responsibility: A company-level measurement approach for CSR. European Management Journal 26: 247–61. [Google Scholar] [CrossRef]

- Werbel, James D., and Max S. Wortman. 2000. Strategic philanthropy: Responding to negative portrayals of corporate social responsibility. Corporate Reputation Review 3: 124–36. [Google Scholar] [CrossRef]

- Withisuphakorn, Pradit, and Pornsit Jiraporn. 2016. The effect of firm maturity on corporate social responsibility (CSR): Do older firms invest more in CSR? Applied Economics Letters 23: 298–301. [Google Scholar] [CrossRef]

- Wu, Meng-Wen, and Chung-Hua Shen. 2013. Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking & Finance 37: 3529–47. [Google Scholar]

- Wu, Qiang, Jacob Cherian, Sarminah Samad, Ubaldo Comite, Huajie Hu, Stefan B. Gunnlaugsson, Judit Oláh, and Muhammad Safdar Sial. 2021. The Role of CSR and Ethical Leadership to Shape Employees’ Pro-Environmental Behavior in the Era of Industry 4.0. A Case of the Banking Sector. Sustainability 13: 9773. [Google Scholar] [CrossRef]

{kind=link}

| Measure | Definition | Measurement |

|---|---|---|

| Institutional commitment to social initiatives (SI) | The extent to which the banks are committed to using CSR programs | Measured by accessing the percentage of the corporate budget allocated to CSR and using the average as a cutoff point; accordingly, we generated two categories of banks after checking all information: banks with high (above the average: SIi = 1) and low (under the average: SIi = 0) degrees of implementing CSR initiatives |

| Total assets of the listed banks | The order of banks according to the number of total assets | |

| Types of ownership | Local bank = 1; foreign bank = 0 | |

| The strength of the bank in comparison with the rest of its rivals in the marketplace | The rank of the banks according to their market share | |

| The number of years since bank inception in the marketplace | Measured in natural log of years: the younger the bank, the less entrenched its culture | |

| Mergers and acquisitions M&As | The merger-and-acquisition policies that affect bank profit structure if they occur in the previous period | Occurrence of mergers and acquisitions = 1; if not = 0 |

| The changes in economic conditions that affect bank profit structure if they occur in the previous period | The 30 day Egyptian treasury bill interest rate |

| Item | Description |

|---|---|

| 1. Profit | Difference between bank’s operating revenues and expenses |

| 2. Price of deposits | The ratio of interest paid/total deposits portfolio |

| 3. Price of labor | The ratio of salary expenses/total number of employees |

| 4. Price of purchased funds | The ratio of expenses of purchased funds (borrowed and federal funds)/total amount of purchased funds |

| 5. Price of marketing | The ratio of marketing and advertising expenses/total assets |

| 6. Amount of loans | The total amount of loan accounts |

| 7. Quantity of securities | Securities portfolio |

| 8. Amount of services | Revenues from service fees |

| 9. Price of loans | Interest income from loans/loans portfolio |

| 10. Price of securities | Revenues from securities/securities portfolio |

| 11. Price of services | Revenues from fees/total assets |

| 12. Financial equity capital | Total shareholder equity |

| 13. Fixed assets | Total fixed assets |

| 14. Nonperforming loans and advances | The proportion of loans past due >90 days |

| 15. Market risk | Value at risk (VaR) 95% confidence level |

| Variable | Mean | SD | CSR Initiatives Implementation | PEEF | Lambda | M&As | SI | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| CSR initiatives implementation | 225.27 | 998.12 | 1 | ||||||||

| PEEF | 6.51 | 3.47 | 0.062 | 1 | |||||||

| Lambda | 13.35 | 2.81 | −0.156 ** | −0.034 | 1 | ||||||

| M&As | 0.25 | 0.43 | 0.235 ** | 0.128 * | 0.000 | 1 | |||||

| 17.07 | 5.41 | 0.404 ** | 0.075 | 0.034 | 0.131 * | 1 | |||||

| 0.08 | 0.08 | 0.188 ** | 0.109 * | 0.000 | 0.781 ** | 0.082 | 1 | ||||

| 0.01 | 0.01 | −0.286 ** | −0.090 | 0.188 ** | 0.241 ** | −0.180 ** | 0.437 ** | 1 | |||

| SI | 0.51 | 0.501 | 0.385 ** | 0.067 | −0.128 * | 0.226 ** | 0.306 ** | 0.283 ** | −0.290 ** | 1 | |

| 0.17 | 0.373 | −0.375 ** | −0.026 | 0.000 | −0.236 ** | −0.714 ** | −0.175 ** | 0.070 | −0.249 ** | 1 |

| Predictor Variables | Hypotheses | β (t-Value) | Model with 1 Year Lagged Profit β (t-Value) | Model with 2 Year Lagged Profit β (t-Value) |

|---|---|---|---|---|

| (Intercept) | 5.94 (30.57) *** | 4.09 (19.45) *** | 6.67 (24.76) *** | |

| Loc ( | 0.505 (2.294) | 0.5687 (2.134) | 0.601 (2.345) | |

| Size | −0.13 (−0.25) | −0.09 (−0.14) | −0.15 (−0.34) | |

| Lagged profit efficiency | −0.00017 (−947) *** | −0.00023 (−9.67) *** | −0.00024 (−9.913) *** | |

| CSR initiatives implementation | H1 | −0.1753 (−5.349) ** | −0.1689 (−5.987) ** | −0.1654 (−5.067) ** |

| CPIT × CSR ( | H4 | −4.933 (−4.657) *** | −5.123 (−4.879) *** | −5.087 (−4.543) *** |

| SI × CSR | H2 | −13.792 (−0.812) | −14.098 (−0.982) | −13.675 (−0.798) |

| Size × CSR | 0.051 (1.063) | 0.067 (1.167) | 0.069 (1.145) | |

| FG × CSR ( | H3 | −0.12 (−23.506) *** | −0.143 (−22.987) *** | −0.156 (−23.034) *** |

| Mergers and acquisitions ( | 0.921 (13.62) *** | 0.879 (12.45) *** | 0.906 (13.453) *** | |

| Lambda ( | −0.069 (−7.905) *** | −0.071 (−8.234) *** | −0.089 (−7.876) *** |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ibrahim, M.M.; El Frargy, M.M.; Hussainey, K. The Impact of Corporate Social Responsibility as a Marketing Investment on Firms’ Performance: A Risk-Oriented Approach. J. Risk Financial Manag. 2021, 14, 515. https://doi.org/10.3390/jrfm14110515

Ibrahim MM, El Frargy MM, Hussainey K. The Impact of Corporate Social Responsibility as a Marketing Investment on Firms’ Performance: A Risk-Oriented Approach. Journal of Risk and Financial Management. 2021; 14(11):515. https://doi.org/10.3390/jrfm14110515

Chicago/Turabian StyleIbrahim, Mohamed M., Mohamed M. El Frargy, and Khaled Hussainey. 2021. "The Impact of Corporate Social Responsibility as a Marketing Investment on Firms’ Performance: A Risk-Oriented Approach" Journal of Risk and Financial Management 14, no. 11: 515. https://doi.org/10.3390/jrfm14110515

APA StyleIbrahim, M. M., El Frargy, M. M., & Hussainey, K. (2021). The Impact of Corporate Social Responsibility as a Marketing Investment on Firms’ Performance: A Risk-Oriented Approach. Journal of Risk and Financial Management, 14(11), 515. https://doi.org/10.3390/jrfm14110515