Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation

Abstract

1. Introduction

2. Studies about Trade Policy Uncertainty

2.1. Linkages between Trade Policy Uncertainty and the Macro Economy

2.2. The Nexus between Trade Policy Uncertainty and Institutions

2.3. Trade Policy Uncertainty and Migration

2.4. The Connection between Trade Policy Uncertainty and Financial Markets

3. Data and Methodology

4. Econometric Results

5. Conclusions and Avenues for Further Research

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors | Journal | Variables | Data Source | Period | Country | Methodology | Findings |

|---|---|---|---|---|---|---|---|

| Caldara et al. (2020) | JME | Three measures of US Trade Policy Uncertainty Tariff rates Firm-level and aggregate macroeconomic data | 11 newspapers (Boston Globe, Chicago Tribune, Guardian, Los Angeles Times, New York Times, Wall Street Journal, Washington Post) Compustat | 1960–2018 | USA | Open-economy New Keynesian DSGE model with a discrete choice of entering and exiting the export market Calibration Regressions Vector Autoregressions (VAR) | Higher TPU results in lower US business investment by 1% while VAR outcomes present even greater reduction |

| Crowley et al. (2018) | JIE | Chinese trade transactions Tariffs Macroeconomic data on real GDP and exchange rates | Chinese Customs Database (CCD) by China’s General Administration of Customs Global Antidumping Database (GAD) by Chad Bown and maintained by the World Bank World Bank’s Development Indicators database USDA Economic Research Service | 2000–2009 | China 33 countries (20 largest export destinations and countries with antidumping duties against China) | Model based on Handley and Limao (2015) Panel regressions | High trade policy uncertainty urges Chinese firms to exit established foreign markets and become more hesitant towards entering new foreign markets. |

| Facchini et al. (2019) | JIE | US Trade Policy Uncertainty Internal migration Exports (firm-level data) Industry skill-intensity data Tariffs Pervasiveness of barriers to investment in China US Multi Fiber Agreement (MFA) quota Availability of production subsidies to Chinese firms | China’s Population Census China Custom Data (CCD) (also called “China Import and Export data”) from World Integrated Trading Solution (WITS) database 2004 China’s Annual Survey of Industrial Firms (CASIF) (also known as “Chinese Industrial Enterprises Database”) | 2000–2005 | USA China | Panel estimations | Higher migrationin China by 24% due to lower TPU. The migrants most responsive are “non-hukou”, skilled and in their prime working age |

| Feng et al. (2017) | JIE | Firm-product level dataset Fixed export costs (measured as fixed assets of exporting firms or as the intermediary share of exports) Tariffs New entrant and exiter margins | China’s manufacturing survey data | 2000–2006 | China connected to USA and European Union | Heterogeneous firm model based on Handley and Limao (2015) Panel regressions | Lower Chinese tariff policy uncertainty determined aggregate reallocation of Chinese exports and encouraged participation by exporters with higher-quality and lower-price products |

| Gozgor et al. (2019) | FRL | Bitcoin price index USA Trade Policy Uncertainty (TPI) | www.coindesk.com www.policyuncertainty.com | July 2010–August 2018 | USA | Wavelet Power Spectrum (WPS) methodology by Torrence and Compo (1998) Cross Wavelet Transform (CWT) method by Grinsted et al. (2004) Wavelet Coherency (WTC) method by Grinsted et al. (2004) VAR-based frequency domain Granger causality by Breitung and Candelon (2006) | USA TPU positively and significantly affects Bitcoin returns but exert a negative impact on these returns during extreme events (regime change) |

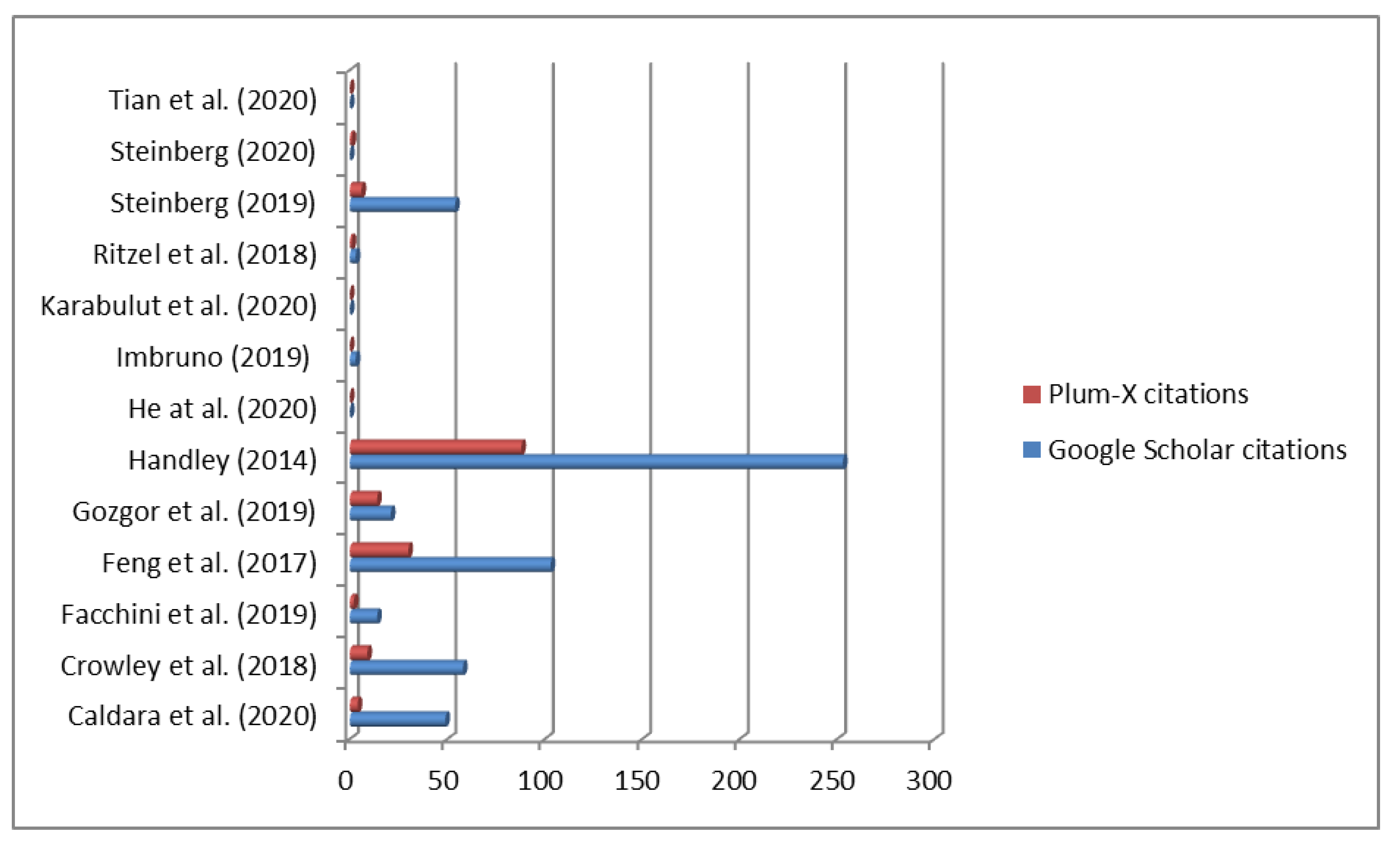

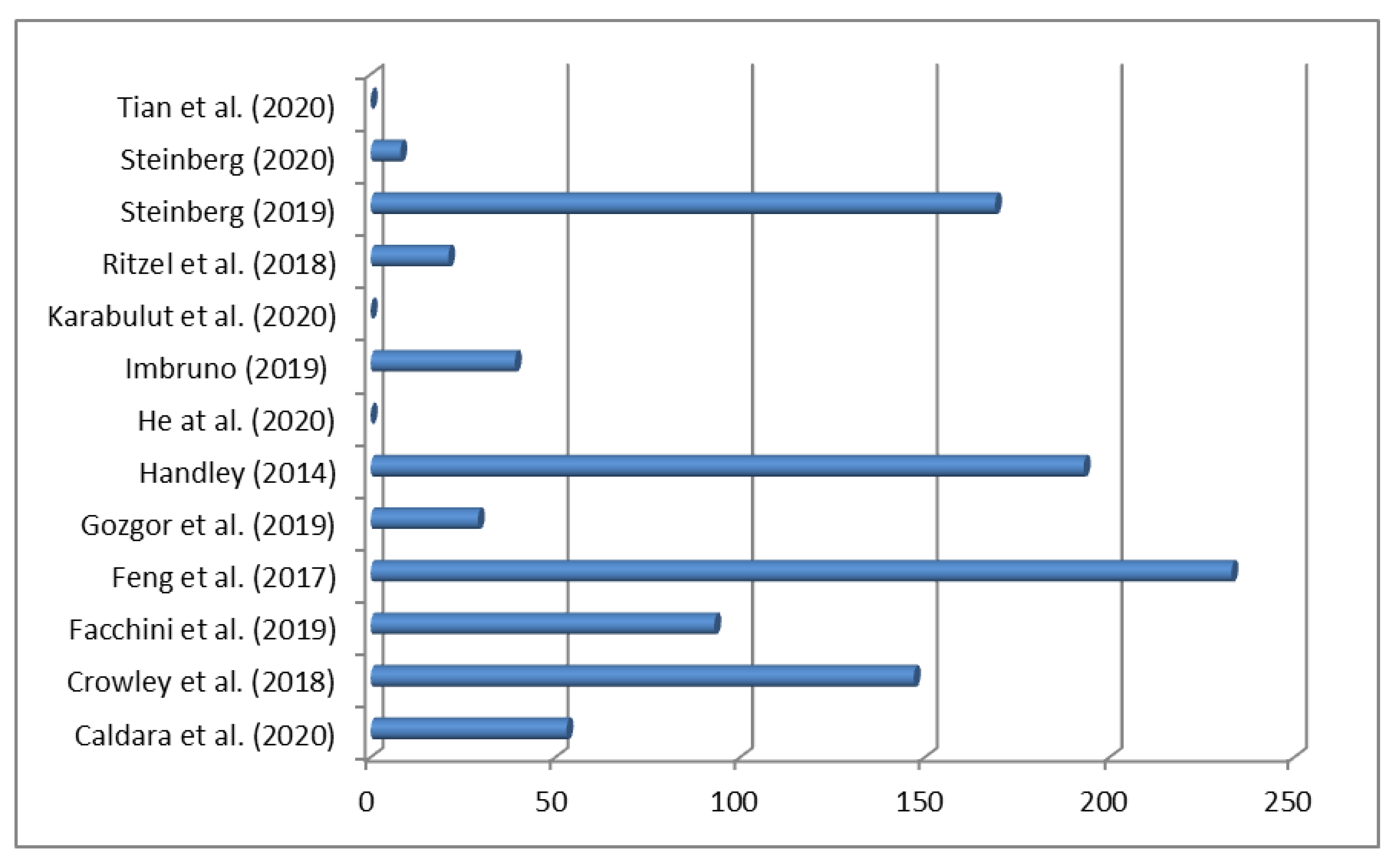

| Handley (2014) | JIE | Tariffs Bindings for Australia’s Uruguay Round Commitments Import data | UNCTAD TRAINS database via the World Integrated Trade Solution (WITS) WTO’s consolidated tariff schedules (CTS) by the Tariff Analysis On-line database Australian Bureau of Statistics | 1993–2001 | Australia | Dynamic heterogeneous firms model | Growth of exporter-product varieties would have been 7% lower if no binding commitments took place by the WTO after 1996 If no tariffs and bindings existed, over 50% of predicted product growth would be linked with uncertainty WTO commitments could lead to lower uncertainty and higher product entry |

| He et al. (2020) | FRL | S&P500 Shanghai Composite Index | - | January 2000–April 2019 | USA China | TVP-SV-VAR by Nakajima (2011) | US–China trade conflicts generate positive effects on the US stock market whereas negative impacts on the Chinese stock market |

| Imbruno (2019) | JCE | Imports at the country/product/firm level Applied tariffs Bound tariffs Non-tariff trade barriers | Chinese Customs Trade Statistics (CCTS) World Bank’s World Integrated Trade Solution (WITS) database WTO’s Consolidated Tariff Schedules (CTS) database China’s Protocol of the WTO accession | 2000–2006 | China | Panel regression with dummies Linear probability model | Lower Chinese TPU leads to multinationals relocating the downstreame stages of global value chains in China more than the upstream stages. So they are market-seeking rather than resource-seeking in China. |

| Karabulut et al. (2020) | EAP | World Trade Uncertainty Index by Ahir et al. (2018) US Commodity Price Index (CPI) | IMF database | January 1996–September 2019 | USA | VAR based on Breitung and Candelon (2006) Granger causality by Granger (1969) Continuous Wavelet Transform (CWT), Wavelet Coherency (WC), Wavelet Power Spectrum (WPS) based on Ramsey (1999) | Strong noises concerning world trade uncertainty between 2009–2010 and 2015–2016 as well as for CPI between 2008–2009 and 2015–2016 and between 2008–2009 and 2017–2018. Co-movements linked with important political and economic events |

| Steinberg (2019) | JIE | Macroeconomic variables Prices | World Input Output Database (Timmer et al. 2015) EFIGE dataset (Altomonte and Aquilante 2012) World Bank Exporter Dynamics Database (Fernandes et al. 2016) | Since 2011 | UK European Union Rest of the world | Dynamic General Equilibrium Model with heterogeneous firms, endogenous export participation and stochastic trade costs Regime construction Calibration | The total consumption-equivalent welfare cost due to Brexit is between 0.4% and 1.2% but uncertainty is repsonsible for less than 25% of this cost |

| Steinberg (2020) | JME | Firm-level TPU dataset of Caldara et al. (2020) linked to the US input–output accounts Trade exposure (export exposure, imported input exposure) | US Bureau of Economic Analysis Compustat | 1960–2018 | USA | DSGE model with sticky prices and sunk exporting costs Simple model of price- setting under nominal rigidities | A number of issues arise concerning Caldara et al. (2020) |

| Tian et al. (2020) | EM | 3-year and 5-year uncertainty measures based on Jurado et al. (2015) Polity2score (democracy) | Data from Glick and Rose (2016) Data from Marshall et al. (2015) | 1960–2013 | 194 countries | Ordinary Least Squares (OLS) Generalized Method of Moments (GMM) by Blundell and Bond (1998) | Higher income leads to democratic transitions but mainly in developing countries |

References

- Ahir, Hites, Nicholas Bloom, and Davide Furceri. 2018. The World Uncertainty Index. Available online: http://dx.doi.org/10.2139/ssrn.3275033 (accessed on 10 September 2020).

- Akaike, Hirotugu. 1974. A new look at the statistical model identification. IEEE Transactions on Automatic Control 19: 716–23. [Google Scholar] [CrossRef]

- Altomonte, Carlo, and Tommaso Aquilante. 2012. The EU-EFIGE/Bruegel-Unicredit Dataset (No. 2012/13). Bruegel Working Paper. Brussels: Bruegel. Available online: https://www.bruegel.org/2012/10/the-eu-efigebruegel-unicredit-dataset/ (accessed on 10 September 2020).

- Baier, Scott L., and Jeffrey H. Bergstrand. 2004. Economic determinants of free trade agreements. Journal of international Economics 64: 29–63. [Google Scholar] [CrossRef]

- Baur, Dirk G., Thomas Dimpfl, and Konstantin Kuck. 2018. Bitcoin, gold and the US dollar—A replication and extension. Finance Research Letters 25: 103–10. [Google Scholar] [CrossRef]

- Ben-David, Dan. 1993. Equalizing exchange: Trade liberalization and income convergence. The Quarterly Journal of Economics 108: 653–79. [Google Scholar] [CrossRef]

- Bhagwati, Jagdish, and Vangal K. Ramaswami. 1963. Domestic distortions, tariffs and the theory of optimum subsidy. Journal of Political Economy 71: 44–50. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Glossary to ARCH (GARCH). In Volatility and Time Series Econometrics Essays in Honor of Robert Engle. MarkWatson, Tim Bollerslev and Jerey. Oxford: University Press. [Google Scholar]

- Breitung, Jörg, and Bertrand Candelon. 2006. Testing for short-and long-run causality: A frequency-domain approach. Journal of Econometrics 132: 363–78. [Google Scholar] [CrossRef]

- Burstein, Ariel, and Javier Cravino. 2015. Measured aggregate gains from international trade. American Economic Journal: Macroeconomics 7: 181–218. [Google Scholar] [CrossRef][Green Version]

- Caldara, Dario, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo. 2020. The economic effects of trade policy uncertainty. Journal of Monetary Economics 109: 38–59. [Google Scholar] [CrossRef]

- Capie, Forrest, Terence C. Mills, and Geoffrey Wood. 2005. Gold as a hedge against the dollar. Journal of International Financial Markets, Institutions and Money 15: 343–52. [Google Scholar] [CrossRef]

- Crowley, Meredith, Ning Meng, and Huasheng Song. 2018. Tariff scares: Trade policy uncertainty and foreign market entry by Chinese firms. Journal of International Economics 114: 96–115. [Google Scholar] [CrossRef]

- Dasgupta, Partha, and Joseph Stiglitz. 1977. Tariffs vs. quotas as revenue raising devices under uncertainty. The American Economic Review 67: 975–81. [Google Scholar]

- Ding, Zhuanxin, Clive W. J. Granger, and Robert F. Engle. 1993. A long memory property of stock market returns and a new model. Journal of Empirical Financ 1: 83–106. [Google Scholar] [CrossRef]

- Dyhrberg, Anne Haubo. 2016. Bitcoin, gold and the dollar—A GARCH volatility analysis. Finance Research Letters 16: 85–92. [Google Scholar] [CrossRef]

- Edmond, Chris, Virgiliu Midrigan, and Daniel Yi Xu. 2015. Competition, markups, and the gains from international trade. American Economic Review 105: 3183–221. [Google Scholar] [CrossRef]

- Edwards, Sebastian. 1997. Trade policy, growth, and income distribution. The American Economic Review 87: 205–10. [Google Scholar]

- Engle Robert, F. 1982. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica: Journal of the Econometric Society 50: 987–1007. [Google Scholar] [CrossRef]

- Facchini, Giovanni, Maggie Y. Liu, Anna Maria Mayda, and Minghai Zhou. 2019. China’s “Great Migration”: The impact of the reduction in trade policy uncertainty. Journal of International Economics 120: 126–44. [Google Scholar] [CrossRef]

- Feenstra, Robert C. 1992. How costly is protectionism? Journal of Economic Perspectives 6: 159–78. [Google Scholar] [CrossRef]

- Feng, Ling, Zhiyuan Li, and Deborah L. Swenson. 2017. Trade policy uncertainty and exports: Evidence from China’s WTO accession. Journal of International Economics 106: 20–36. [Google Scholar] [CrossRef]

- Fernandes, Ana M., Caroline Freund, and Martha Denisse Pierola. 2016. Exporter Behavior, Country Size and Stage of Development: Evidence from the Exporter Dynamics Database. Washington, DC: The World Bank. [Google Scholar]

- Findlay, Ronald, and Stanislaw Wellisz. 1982. Endogenous tariffs, the political economy of trade restrictions, and welfare. In Import Competition and Response. Chicago: University of Chicago Press, pp. 223–44. [Google Scholar]

- Foellmi, Reto, and Manuel Oechslin. 2010. Market imperfections, wealth inequality, and the distribution of trade gains. Journal of International Economics 81: 15–25. [Google Scholar] [CrossRef]

- Glick, Reuven, and Andrew K. Rose. 2016. Currency unions and trade: A post-EMU reassessment. European Economic Review 87: 78–91. [Google Scholar] [CrossRef]

- Glosten, Lawrence R., Ravi Jagannathan, and David E. Runkle. 1993. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance 48: 1779–801. [Google Scholar]

- Gozgor, Giray, Aviral Kumar Tiwari, Ender Demir, and Sagi Akron. 2019. The relationship between Bitcoin returns and trade policy uncertainty. Finance Research Letters 29: 75–82. [Google Scholar] [CrossRef]

- Granger, Clive W. J. 1969. Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society 37: 424–38. [Google Scholar] [CrossRef]

- Grinsted, Aslak, John C. Moore, and Svetlana Jevrejeva. 2004. Application of the cross wavelet transform and wavelet coherence to geophysical time series. Nonlinear Processes in Geophysics 11: 561–66. [Google Scholar] [CrossRef]

- Grossman, Gene M., and Elhanan Helpman. 1993. The Politics of free Trade Agreements (No. w4597). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Handley, Kyle. 2014. Exporting under trade policy uncertainty: Theory and evidence. Journal of International Economics 94: 50–66. [Google Scholar] [CrossRef]

- Handley, Kyle, and Nuno Limao. 2015. Trade and investment under policy uncertainty: Theory and firm evidence. American Economic Journal: Economic Policy 7: 189–222. [Google Scholar] [CrossRef]

- He, Feng, Brian Lucey, and Ziwei Wang. 2020. Trade Policy Uncertainty and its Impact on the Stock Market-evidence from China-US trade conflict. Finance Research Letters. [Google Scholar] [CrossRef]

- Higgins, Matthew L., and Anil K. Bera. 1992. A class of nonlinear ARCH models. International Economic Review 33: 137–58. [Google Scholar] [CrossRef]

- Imbruno, Michele. 2019. Importing under trade policy uncertainty: Evidence from China. Journal of Comparative Economics 47: 806–26. [Google Scholar] [CrossRef]

- Jurado, Kyle, Sydney C. Ludvigson, and Serena Ng. 2015. Measuring uncertainty. American Economic Review 105: 1177–216. [Google Scholar] [CrossRef]

- Karabulut, Gokhan, Mehmet Huseyin Bilgin, and Asli Cansin Doker. 2020. The relationship between commodity prices and world trade uncertainty. Economic Analysis and Policy. [Google Scholar] [CrossRef]

- Kimbrough, Kent P. 1985. Tariffs, quotas and welfare in a monetary economy. Journal of International Economics 19: 257–77. [Google Scholar] [CrossRef]

- Krueger, Anne O. 1980. Trade Policy as an Input to Development (No. w0466). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Krueger, Anne O. 1997. Trade Policy and Economic Development: How We Learn (No. w5896). Cambridge: National Bureau of Economic Research. [Google Scholar]

- Krugman, Paul. 1991. The move toward free trade zones. Economic Review 76: 5. [Google Scholar]

- Kyriazis, Nikolaos A. 2019. A survey on efficiency and profitable trading opportunities in cryptocurrency markets. Journal of Risk and Financial Management 12: 67. [Google Scholar] [CrossRef]

- Kyriazis, Nikolaos, Stephanos Papadamou, and Shaen Corbet. 2020. A Systematic Review of the Bubble Dynamics of Cryptocurrency Prices. Research in International Business and Finance 54: 101254. [Google Scholar] [CrossRef]

- Levy, Philip I. 1997. A political-economic analysis of free-trade agreements. The American Economic Review 87: 506–19. [Google Scholar]

- Li, Chunding, Chuantian He, and Chuangwei Lin. 2018. Economic impacts of the possible China–US trade war. Emerging Markets Finance and Trade 54: 1557–77. [Google Scholar] [CrossRef]

- Li, Minghao, Edward J. Balistreri, and Wendong Zhang. 2020. The US–China trade war: Tariff data and general equilibrium analysis. Journal of Asian Economics 69: 101216. [Google Scholar] [CrossRef]

- Lindé, Jesper, and Andrea Pescatori. 2019. The macroeconomic effects of trade tariffs: Revisiting the lerner symmetry result. Journal of International Money and Finance 95: 52–69. [Google Scholar] [CrossRef]

- Marshall, Monty G., G. Ted Robert, and Keith Jaggers. 2015. Polity IV Project: Political Regime Characteristics and Transitions, 1800–2015. Available online: http://www.systemicpeace.org/inscr/p4manualv2016.pdf (accessed on 10 September 2020).

- Myint, Hla. 1954. The gains from international trade and the backward countries. The Review of Economic Studies 22: 129–42. [Google Scholar] [CrossRef]

- Nakajima, Jouchi. 2011. Time-Varying Parameter VAR Model with Stochastic Volatility: An Overview of Methodology and Empirical Applications. Monetary and Economic Studies 29: 107–42. [Google Scholar]

- Ossa, Ralph. 2014. Trade wars and trade talks with data. American Economic Review 104: 4104–46. [Google Scholar] [CrossRef]

- Ramsey, James B. 1999. The Contribution of Wavelets to the Analysis of Economic and Financial Data. Philosophical Transactions: Mathematical, Physical and Engineering Sciences 357: 2593–606. [Google Scholar] [CrossRef]

- Rodriguez, Francisco, and Dani Rodrik. 2000. Trade policy and economic growth: A skeptic’s guide to the cross-national evidence. NBER Macroeconomics Annual 15: 261–325. [Google Scholar] [CrossRef]

- Samuelson, Paul A. 1939. The gains from international trade. The Canadian Journal of Economics and Political Science/Revue Canadienne d’Economique Et De Science Politique 5: 195–205. [Google Scholar] [CrossRef]

- Samuelson, Paul Anthony. 1962. The gains from international trade once again. The Economic Journal 72: 820–29. [Google Scholar] [CrossRef]

- Schwarz, Gideon. 1978. Estimating the dimension of a model. The Annals of Statistics 6: 461–64. [Google Scholar] [CrossRef]

- Sharif, Arshian, Chaker Aloui, and Larisa Yarovaya. 2020. COVID-19 pandemic, oil prices, stock market, geopolitical risk and policy uncertainty nexus in the US economy: Fresh evidence from the wavelet-based approach. International Review of Financial Analysis 70: 101496. [Google Scholar] [CrossRef]

- Steinberg, Joseph B. 2019. Brexit and the macroeconomic impact of trade policy uncertainty. Journal of International Economics 117: 175–95. [Google Scholar] [CrossRef]

- Steinberg, Joseph B. 2020. Comment on: “The economic effects of Trade Policy Uncertainty” by Dario Caldara, Matteo Iacoviello, Patrick Molligo, Andrea Prestipino, and Andrea Raffo. Journal of Monetary Economics 109: 60–64. [Google Scholar] [CrossRef]

- Tian, Jilin, Nicholas Sim, Wenshou Yan, and Yanyun Li. 2020. Trade uncertainty, income, and democracy. Economic Modelling. [Google Scholar] [CrossRef]

- Timmer, Marcel P., Erik Dietzenbacher, Bart Los, Robert Stehrer, and Gaaitzen J. De Vries. 2015. An illustrated user guide to the world input–output database: The case of global automotive production. Review of International Economics 23: 575–605. [Google Scholar] [CrossRef]

- Torrence, Christopher, and Gilbert P. Compo. 1998. A practical guide to wavelet analysis. Bulletin of the American Meteorological Society 79: 61–78. [Google Scholar] [CrossRef]

- Zakoian, Jean-Michel. 1994. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18: 931–55. [Google Scholar] [CrossRef]

| 1 |

| (a) | |||||

| ARCH | GARCH | Threshold ARCH | GJR-Form of Threshold ARCH | ||

| Mean equation | TPU | 2.2595 (0.000) *** | 0.3661 (0.000) *** | 0.4434 (0.000) *** | 0.259 (0.000) *** |

| Oil | −0.1069 (0.000) *** | −0.6985 (0.000) *** | −0.3336 (0.000) *** | −0.1059 (0.000) *** | |

| constant | 5.513 (0.000)*** | 7.2684 (0.000)*** | 5.578 (0.000)*** | 5.5132 (0.000) *** | |

| Variance equation | Arch | 1.0375 (0.000) *** | 0.9683 (0.000) *** | 0.9585 (0.005) *** | |

| Abarch | 0.9272 (0.000) *** | ||||

| Atarch | 0.0452 (0.843) | ||||

| Tarch | 0.1435 (0.746) | ||||

| Garch | 0.0988 (0.224) | ||||

| Constant | 0.01 (0.000) *** | 0.0082 (0.145) | 0.0761 (0.001) *** | 0.0099 (0.000) *** | |

| AIC | 986.262 | 1034.152 | 1014.299 | 987.516 | |

| BIC | 1006.054 | 1057.903 | 1038.05 | 1011.267 | |

| (b) | |||||

| Simple Asymmetric ARCH | Power ARCH | Non-linear ARCH | Non-linear GARCH | ||

| Mean equation | TPU | 0.2478 (0.000) *** | 0.5553 (0.000) *** | 0.5477 (0.000) *** | 0.501 (0.000) *** |

| Oil | −0.0702 (0.018) ** | −1.134 (0.000) *** | −1.1087 (0.000) *** | −1.1499 (0.000) *** | |

| constant | 5.42 (0.000) *** | 8.0777 (0.000) *** | 8.0137 (0.000) *** | 8.3442 (0.000) *** | |

| Variance equation | Arch | 1.036 (0.000) *** | |||

| Saarch | 0.0663 (0.147) | ||||

| Parch | 0.9905 (0.002) *** | ||||

| Narch | 0.9793 (0.000) *** | 0.7593 (0.001) *** | |||

| Narch_k | −0.0391 (0.356) | −0.0619 (0.084) * | |||

| Garch | 0.2157 (0.001) *** | ||||

| Constant | 0.0096 (0.000) *** | 0.0341 (0.601) | 0.0253 (0.000) *** | 0.0129 (0.000) *** | |

| Power | 1.7719 (0.122) | ||||

| AIC | 985.013 | 1033.445 | 1032.704 | 1028.214 | |

| BIC | 1008.764 | 1057.196 | 1056.455 | 1055.923 | |

| (c) | |||||

| Non-linear ARCH with one shift | Non-linear GARCH with one shift | Asymmetric Power ARCH | Asymmetric Power GARCH | ||

| Mean equation | TPU | 0.5476 (0.000) *** | 0.501 (0.000) *** | 0.5596 (0.000) *** | 0.7517 (0.000) *** |

| Oil | −1.1087 (0.000) *** | −1.1499 (0.000) *** | −1.1351 (0.000) *** | 0.7271 (0.000) *** | |

| constant | 8.0137 (0.000) *** | 8.3442 (0.000) *** | 8.0702 (0.000) *** | 0.4941 (0.199) | |

| Narch | 0.9793 (0.000) *** | 0.7593 (0.001) *** | |||

| Narch_k | −0.0391 (0.356) | −0.0619 (0.084) * | |||

| Aparch | 0.9505 (0.002) *** | 1.0525 (0.001) *** | |||

| Aparch_e | 0.0569 (0.702) | 0.0368 (0.725) | |||

| Garch | 0.2157 (0.001) *** | −0.0286 (0.737) | |||

| Constant | 0.0253 (0.000) *** | 0.0129 (0.000) *** | 0.0453 (0.532) | 0.0472 (0.423) | |

| Power | 1.5837 (0.1) | 2.5123 (0.014) ** | |||

| AIC | 1032.704 | 1028.214 | 1035.267 | 1022.707 | |

| BIC | 1056.455 | 1055.923 | 1062.976 | 1054.374 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kyriazis, N.A. Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation. J. Risk Financial Manag. 2021, 14, 41. https://doi.org/10.3390/jrfm14010041

Kyriazis NA. Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation. Journal of Risk and Financial Management. 2021; 14(1):41. https://doi.org/10.3390/jrfm14010041

Chicago/Turabian StyleKyriazis, Nikolaos A. 2021. "Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation" Journal of Risk and Financial Management 14, no. 1: 41. https://doi.org/10.3390/jrfm14010041

APA StyleKyriazis, N. A. (2021). Trade Policy Uncertainty Effects on Macro Economy and Financial Markets: An Integrated Survey and Empirical Investigation. Journal of Risk and Financial Management, 14(1), 41. https://doi.org/10.3390/jrfm14010041