What Drives the Declining Wealth Effect of Subsequent Share Repurchase Announcements?

Abstract

1. Introduction

2. Hypothesis Development

3. Sample

4. Methods and Results

β5LEVERAGE + β6STDEV + β7ROA + β8OPTION + Industry and Year Control + ε

Robustness Tests

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Aktas, Nihat, Eric de Bodt, and Richard Roll. 2013. Learning from repetitive acquisitions: Evidence from the time between deals. Journal of Financial Economics 108: 99–117. [Google Scholar] [CrossRef]

- Aktas, Nihat, Eric De Bodt, Hellen Bollaert, and Richard Roll. 2016. CEO narcissism and the takeover process: From private initiation to deal completion. Journal of Financial and Quantitative Analysis 51: 113–37. [Google Scholar] [CrossRef]

- Bagwell, Laurie Simon. 1991. Share repurchase and takeover deterrence. Rand Journal of Economics 22: 72–88. [Google Scholar] [CrossRef]

- Bagwell, Laurie Simon, and John B. Shoven. 1988. Share repurchase and acquisitions: An analysis of which firms participate. In Corporate Takeovers: Causes and Consequences. Edited by A. J. Auerbach. Chicago: University of Chicago Press. [Google Scholar]

- Bayat, Ali, Reza Salehnejad, and Peter Kawalek. 2016. Does CEO’s Holding of Vested Options Measure Overconfidence? Working Paper. Manchester: Alliance Manchester Business School. [Google Scholar]

- Ben-David, Itzhak, John R. Graham, and Campbell R. Harvey. 2007. Managerial Overconfidence and Corporate Policies No. w13711. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Billett, Matthew T., and Yiming Qian. 2008. Are overconfident CEOs born or made? Evidence of self-attribution bias from frequent acquirers. Management Science 54: 1037–51. [Google Scholar] [CrossRef]

- Bonaimé, Alice A. 2012. Repurchases, reputation and returns. Journal of Financial and Quantitative Analysis 47: 469–91. [Google Scholar] [CrossRef]

- Busch, Pascal, and Stefan Obernberger. 2017. Actual share repurchases, price efficiency, and the information content of stock prices. The Review of Financial Studies 30: 324–32. [Google Scholar] [CrossRef]

- Cai, Jie, Moon H. Song, and Ralph A. Walkling. 2011. Anticipation, acquisitions, and bidder returns: Industry shocks and the transfer of information across rivals. Review of Financial Studies 24: 2242–85. [Google Scholar] [CrossRef]

- Campbell, T. Colin, Michael Gallmeyer, Shane A. Johnson, Jessica Rutherford, and Brooke W. Stanley. 2011. CEO optimism and forced turnover. Journal of Financial Economics 101: 695–712. [Google Scholar] [CrossRef]

- Chang, Shao-Chi, Sheng-Syan Chen, and Li-Yu Chen. 2010. Does prior record matter in the wealth effect of open market share repurchase announcements? International Review of Economics and Finance 19: 427–35. [Google Scholar] [CrossRef]

- Chatterjee, Arijit, and Donald C. Hambrick. 2007. It’s all about me: Narcissistic chief executive officers and their effects on company strategy and performance. Administrative Science Quarterly 52: 351–86. [Google Scholar] [CrossRef]

- Chen, Chao C., and James R. Meindl. 1991. The construction of leadership images in the popular press: The case of Donald Burr and People Express. Administrative Science Quarterly 36: 521–55. [Google Scholar] [CrossRef]

- De Ridder, Adri, and Jonas Rasbrandt. 2014. Share repurchases: Does frequency matter? Studies in Economics and Finance 31: 88–105. [Google Scholar] [CrossRef]

- Dittmar, Amy. K. 2000. Why do firms repurchase stock? Journal of Business 73: 331–55. [Google Scholar] [CrossRef]

- Fenn, George W., and Nellie Liang. 2001. Corporate payout policy and managerial stock incentives. Journal of Financial Economics 60: 1–44. [Google Scholar] [CrossRef]

- Finkelstein, Sydney. 1992. Power in top management teams: Dimensions, measurement and validation. Academy of Management Journal 3: 505–38. [Google Scholar]

- Fu, Fangjian, and Sheng Huang. 2016. The persistence of long-run abnormal reruns following stock repurchases and offerings. Management Science 62: 964–84. [Google Scholar] [CrossRef]

- Hayward, Matthew L. A., and Donald C. Hambrick. 1997. Explaining the premiums paid for large acquisitions: Evidence of CEO hubris. Administrative Science Quarterly 42: 103–27. [Google Scholar] [CrossRef]

- Howe, Keith M., Jia He, and G. Wenchi Kao. 1992. One-Time Cash Flow Announcements and Free Cash-Flow Theory: Share Repurchases and Special Dividends. Journal of Finance 47: 1963–75. [Google Scholar] [CrossRef]

- Ikenberry, David, Josef Lakonishok, and Theo Vermaelen. 1995. Market underreaction to open market share repurchases. Journal of Financial Economics 39: 181–208. [Google Scholar] [CrossRef]

- Jagannathan, Murali, and Clifford P. Stephens. 2003. Motives for multiple open market repurchase programs. Financial Management 32: 71–91. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1986. Agency costs of free cash flow, corporate finance and takeover. American Economic Review 76: 323–29. [Google Scholar]

- Kahle, Kathleen M. 2002. When a buyback isn’t a buyback: Open market repurchases and employee options. Journal of Financial Economics 63: 235–61. [Google Scholar] [CrossRef]

- Karolyi, G. Andrew, Rose C. Liao, and Gilberto Loureiro. 2015. The Decreasing Returns of Serial Acquirers around the World. Working Paper. Ithaca: Cornell University. New Brunswick: Rutgers University. Braga: University of Minho. [Google Scholar]

- Kim, Jeong-Bon, Zheng Wang, and Liandong Zhang. 2016. CEO overconfidence and stock price crash risk. Contemporary Accounting Research 33: 1720–49. [Google Scholar] [CrossRef]

- Lakonishok, Josef, and Theo Vermaelen. 1990. Anomalous price behavior around repurchase tender offers. Journal of Finance 45: 455–77. [Google Scholar] [CrossRef]

- Lehn, Kenneth, and Annette Poulsen. 1989. Free Cash Flow and Stockholder Gains in Going Private Transactions. Journal of Finance 44: 771–87. [Google Scholar] [CrossRef]

- Liu, Harrison, and Edward P. Swanson. 2016. Is price support a motive for increasing share repurchases? Journal of Corporate Finance 38: 77–91. [Google Scholar] [CrossRef]

- Malmendier, Ulrike, and Geoffrey Tate. 2005. CEO overconfidence and corporate investment. Journal of Finance 60: 2661–700. [Google Scholar] [CrossRef]

- Malmendier, Ulrike, and Geoffrey Tate. 2008. Who makes acquisitions? CEO overconfidence and the market’s reaction. Journal of Financial Economics 89: 20–43. [Google Scholar] [CrossRef]

- Malmendier, Ulrike, and Geoffrey Tate. 2015. Behavioral CEOs: The role of managerial overconfidence. Journal of Economic Perspectives 29: 37–60. [Google Scholar] [CrossRef]

- Manfred, F. R., Kets de Vries, and Danny Miller. 1984. Neurotic style and organizational pathology. Strategic Management Journal 5: 35–55. [Google Scholar]

- Meindl, James R., Sanford B. Ehrlich, and Janet M. Dukerich. 1985. The romance of leadership. Administrative Science Ouarterly 30: 78–102. [Google Scholar] [CrossRef]

- Miller, Danny, and Cornelia Droge. 1986. Psychological and traditional determinants of structure. Administrative Science Quarterly 31: 539–60. [Google Scholar] [CrossRef]

- Mishra, Dev, Marie D. Racine, and Luke Schmidt. 2011. Credibility of Corporate Announcements and Market Reaction: Evidence from Canadian Share Repurchase Programs. Canadian Journal of Administrative Sciences 28: 83–100. [Google Scholar] [CrossRef]

- Peyer, Urs, and Theo Vermaelen. 2009. The Nature and Persistence of Buyback Anomalies. Review of Financial Studies 22: 1693–745. [Google Scholar] [CrossRef]

- Roll, Richard. 1986. The hubris hypothesis of corporate takeovers. Journal of Business 59: 197–216. [Google Scholar] [CrossRef]

- Salancik, Gerald R., and James R. Meindl. 1984. Corporate attributions as strategic illusions of management control. Administrative Science Quarterly 29: 238–54. [Google Scholar] [CrossRef]

- Skinner, Douglas J. 2008. The evolving relation between earnings, dividends, and stock repurchases. Journal of Financial Economics 87: 582–609. [Google Scholar] [CrossRef]

- Snyder, C. R., Randee Jae Shenkel, and Carol R. Lowery. 1977. Acceptance of personality interpretations: The “Barnum effect” and beyond. Journal of Consulting and Clinical Psychology 45: 104–14. [Google Scholar] [CrossRef]

- Song, Moon H., and Ralph A. Walkling. 2000. Abnormal Returns to Rivals of Acquisition Targets: A Test of the “Acquisition Probability Hypothesis”. Journal of Financial Economics 55: 143–72. [Google Scholar] [CrossRef]

- Stephens, Clifford P., and Michael S. Weisbach. 1998. Actual share reacquisition in open market repurchase programs. Journal of Finance 53: 313–33. [Google Scholar] [CrossRef]

- Swann, William B., and Stephen J. Read. 1981. Acquiring self-knowledge: The search for feedback that fits. Journal of Personality and Social Psychology 41: 1119–28. [Google Scholar] [CrossRef]

- Taylor, Shelley E., and Peter M. Gollwitzer. 1995. Effects of mindset on positive illusions. Journal of Personality and Social Psychology 69: 213–26. [Google Scholar] [CrossRef] [PubMed]

- Vermaelen, Theo. 1981. Common stock repurchases and market signaling. Journal of Financial Economics 9: 139–83. [Google Scholar] [CrossRef]

- Yook, Ken C., and Partha Gangopadhyay. 2011. A comprehensive examination of the wealth effects of recent stock repurchase announcements. Review of Quantitative Finance and Accounting 37: 509–29. [Google Scholar] [CrossRef]

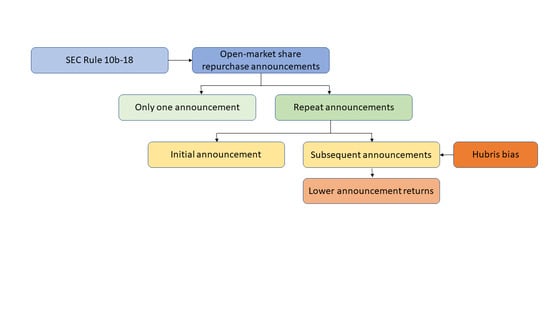

| 1 | The main motive for open market share repurchases is mainly either to buy back undervalued stocks (Lakonishok and Vermaelen 1990; Peyer and Vermaelen 2009), or to distribute temporary free cash flows, in lieu of dividends, to shareholders (Stephens and Weisbach 1998; Dittmar 2000; Skinner 2008). Other theories used to explain repurchases are: (1) to improve their leverage ratios (Bagwell and Shoven 1988); (2) to discourage takeover attempts (Bagwell 1991); and (3) to counter the dilution effect of stock option plans (Fenn and Liang 2001; Kahle 2002). |

| 2 | Another possible explanation could be due to lower past repurchase completion rates. (Bonaimé 2012; Mishra et al. 2011; Chang et al. 2010) argue that when a firm launches an open market share repurchase program but does not follow it through or repurchase less than the number of shares announced in the program, the market considers the firm as having a bad reputation. Consequently, the market will react less favourably when the firm announces a subsequent open market share repurchase program. Low past completion rates, however, cannot explain why some firms keep repeating open market repurchase programs. If the motivation to repurchase is related to stock undervaluation, which is one of the most common motives to launch an open market repurchase program, a positive market reaction to the repurchase announcement may be sufficient for the announcing firm to not fully follow through on its announced repurchase plan, and therefore may explain its lower repurchase completion rate. Similarly, if a firm’s subsequent open market repurchase program is motivated by distributing excess cash flows or stock options, it should not have a low repurchase completion rate. |

| 3 | A similar pattern has also been observed in the Swedish stock market. De Ridder and Rasbrandt (2014) find that repeat repurchasers make two out of three Swedish share repurchase announcements. |

| 4 | For the purposes of the current research work, we refer to hubris as an individual’s personal attribute of self- or over-confidence. We define the term managerial hubris as the over-confident behavior of corporate managers. |

| 5 | The finance literature documents that some managers are prone to self-attribution bias, which leads them to be hubristic. Ben-David et al. (2007) find that among other corporate actions, these managers are more likely to be associated with less efficient investments. Hayward and Hambrick (1997) find that CEO’s hubris (or exaggerated self-confidence) is strongly positively associated with the size of premiums paid for acquisitions. Malmendier and Tate (2008) find evidence consistent with the view that hubristic CEOs overestimate their ability to generate returns. Hence, they overpay for target companies and undertake value-destroying mergers. Another managerial trait—CEO narcissism—has also been shown to be positively related to the number and size of acquisitions. (Chatterjee and Hambrick 2007; Billett and Qian 2008; Karolyi et al. 2015) find evidence consistent with hubristic managers explaining the declining returns of serial acquirers. Recent work by Aktas et al. (2016) show that both acquirer and target CEO narcissism affect the characteristics of the takeover process. No prior studies have studied stock repurchases using the lens of managerial hubris. |

| 6 | Drops only in 1998 and 1999 to less than half of the total announcements in a year (48% and 45%, respectively). |

| 7 | Lehn and Poulsen (1989) find that firms with undistributed free cash flows tend to pay a significant premium for stock repurchases related to going private transactions. Howe et al. (1992) investigate whether Jensen’s (1986) free cash flow theory explains the market reaction to tender offer share repurchases and specially designated dividends where the cash distribution is not expected to be repeated. They find that free cash flows do not explain the announcement returns very well and conclude that their results are inconsistent with Jensen’s free cash flow hypothesis but consistent with the information-signaling hypothesis. They offer the entrenchment hypothesis as a possible explanation for their conflicting findings with those of Jensen’s. |

| 8 | |

| 9 | This methodology is also used in studies on repeat acquisitions, such as (Karolyi et al. 2015; Billett and Qian 2008). |

{kind=link}

| Panel A. Number of Repurchases | ||||||

| YEAR | ONLY ONE | REPEAT | TOTAL | % REPEAT | ||

| 1996 | 94 | 133 | 227 | 59% | ||

| 1997 | 122 | 128 | 250 | 51% | ||

| 1998 | 211 | 194 | 405 | 48% | ||

| 1999 | 147 | 122 | 269 | 45% | ||

| 2000 | 96 | 112 | 208 | 54% | ||

| 2001 | 43 | 82 | 125 | 66% | ||

| 2002 | 57 | 109 | 166 | 66% | ||

| 2003 | 23 | 79 | 102 | 77% | ||

| 2004 | 25 | 132 | 157 | 84% | ||

| 2005 | 47 | 156 | 203 | 77% | ||

| 2006 | 47 | 1474 | 194 | 76% | ||

| 2007 | 41 | 142 | 183 | 78% | ||

| 2008 | 32 | 92 | 124 | 74% | ||

| 2009 | 12 | 59 | 71 | 83% | ||

| 2010 | 30 | 97 | 127 | 76% | ||

| 2011 | 28 | 106 | 134 | 79% | ||

| 2012 | 12 | 24 | 36 | 67% | ||

| 2013 | 16 | 43 | 59 | 73% | ||

| 2014 | 36 | 46 | 82 | 56% | ||

| Panel B. Cumulative Abnormal Announcement Returns | ||||||

| YEAR | 2-day Cumulative Abnormal Returns [CAR (0, +1)] | SIZE OF PROGRAM (%) (SIZEPROG) | ||||

| 1996 | 0.024 | 6.656 | ||||

| 1997 | 0.020 | 6.538 | ||||

| 1998 | 0.030 | 7.358 | ||||

| 1999 | 0.047 | 7.917 | ||||

| 2000 | 0.045 | 7.631 | ||||

| 2001 | 0.023 | 7.413 | ||||

| 2002 | 0.040 | 6.617 | ||||

| 2003 | 0.016 | 6.826 | ||||

| 2004 | 0.013 | 6.465 | ||||

| 2005 | 0.019 | 7.010 | ||||

| 2006 | 0.004 | 7.459 | ||||

| 2007 | 0.022 | 8.649 | ||||

| 2008 | 0.025 | 8.025 | ||||

| 2009 | 0.020 | 7.441 | ||||

| 2010 | 0.015 | 8.753 | ||||

| 2011 | 0.010 | 8.201 | ||||

| 2012 | 0.020 | 9.407 | ||||

| 2013 | 0.008 | 8.177 | ||||

| 2014 | 0.014 | 7.055 | ||||

| PERIOD | First Announcement | Subsequent Announcements | Difference |

|---|---|---|---|

| Average Total period | 0.026 *** | 0.016 *** | 0.010 ** |

| Average 1996–2002 | 0.037 *** | 0.022 *** | 0.015 ** |

| Average 2003–2014 | 0.020 *** | 0.013 *** | 0.007 ** |

| Difference | 0.017 *** | 0.009 ** |

| Panel A. Only One Repurchase vs. Repeat Repurchases | ||

| ONLY ONE | REPEAT | Difference |

| 3.56% *** | 1.83% *** | −1.73% *** |

| Panel B. Cumulative announcement abnormal returns of repeat repurchasers | ||

| Initial announcement | Second announcement | Difference |

| 2.51% *** | 1.77% *** | −0.73% ** |

| Second announcement | Third announcement | Difference |

| 1.77% *** | 1.25% *** | −0.53% * |

| Third announcement | ≥5 announcements | Difference |

| 1.25% *** | 0.89% *** | −0.36% |

| Panel A. Negative Past Announcement Returns | |||

| CAR (0, +1) | |||

| 2nd Announcement | >2 Announcements | Difference | |

| Mean | 1.59% | 0.16% | −1.43% *** |

| Median | 1.29% | −0.16% | −1.45% † |

| Panel B. Positive past announcement returns | |||

| CAR (0, +1) | |||

| 2nd announcement | >2 announcements | Difference | |

| Mean | 1.39% | 2.12% | 0.74% ** |

| Median | 0.90% | 1.50% | 0.60% † |

| Repeat Repurchasers | |||||

|---|---|---|---|---|---|

| Mean Values | Total | ONLY ONE | Initial Announcement | ≥2 Announcements | ≥3 Announcements |

| CASHFLOW | 0.120 | 0.092 | 0.133 | 0.137 | 0.140 |

| B/M | 0.561 | 0.671 | 0.519 | 0.492 | 0.436 |

| DIVYIELD | 0.008 | 0.005 | 0.007 | 0.009 | 0.011 |

| LEVERAGE | 0.178 | 0.180 | 0.172 | 0.179 | 0.183 |

| SIZE ($000) | 741,760 | 273,773 | 770,361 | 1,654,712 | 2,770,892 |

| ΔSALES | 0.022 | 0.018 | 0.035 | 0.019 | 0.023 |

| ROA | 0.049 | 0.016 | 0.064 | 0.068 | 0.079 |

| ROA+1 | 0.048 | 0.009 | 0.068 | 0.069 | 0.076 |

| RUNUP | −0.063 | −0.092 | −0.073 | −0.035 | −0.024 |

| STDEV | 0.028 | 0.034 | 0.028 | 0.023 | 0.020 |

| SIZEPROG | 7.420 | 7.702 | 6.780 | 7.496 | 7.689 |

| Coeff. | (p-Values) | |

|---|---|---|

| RUNUP | 0.600 *** | (0.001) |

| CASHFLOW | 3.629 *** | (0.000) |

| SIZE | 0.287 *** | (0.000) |

| B/M | 0.226 * | (0.061) |

| ΔSIZEPROG | 0.038 *** | (0.006) |

| LEVERAGE | −0.123 | (0.670) |

| STDEV | −7.744 ** | (0.026) |

| ROA | −0.014 | (0.959) |

| OPTION | 0.492 | (0.614) |

| INTERCEPT | −3.168 ** | (0.029) |

| Year effect | Y | |

| Industry effect | Y | |

| LR chi2 | 616.11 | |

| Pseudo R2 | 0.1599 | |

| Number of obs. | 2981 |

| (1) | (p-Values) | (3) | (p-Values) | |

|---|---|---|---|---|

| ENDWHUBRIS | −0.008 ** | (0.037) | ||

| TBD (×10,000) | 0.0288 * | (0.083) | ||

| RUNUP | −0.031 *** | (0.000) | −0.01768 | (0.125) |

| SIZE | −0.002 | (0.306) | −0.00173 | (0.393) |

| B/M | 0.003 | (0.394) | 0.002276 | (0.672) |

| LEVERAGE | −0.018 | (0.042) | −0.00916 | (0.399) |

| STDEV | 0.627 *** | (0.000) | 0.485303 *** | (0.003) |

| ΔSIZEPROG | 0.001 * | (0.055) | 0.000679 * | (0.066) |

| OPTION | −0.026 | (0.421) | −0.08596 | (0.111) |

| CASHFLOW | 0.029 | (0.280) | 0.054924 * | (0.091) |

| Pr(Repeat repurchase) | −0.026 | (0.420) | 0.002167 | (0.954) |

| INTERCEPT | 0.033 | (0.462) | −0.13531 ** | (0.022) |

| Year effect | Y | Y | ||

| Industry effect | Y | Y | ||

| Adj. R2 | 0.0679 | 0.0214 | ||

| Number of obs. | 2972 | 1311 |

| Coeff. | p-Value | Coeff. | p-Value | |

|---|---|---|---|---|

| ENDWHUBRIS | −0.007 * | (0.053) | ||

| TBD (×10,000) | 0.031 * | (0.061) | ||

| RUNUP | −0.033 *** | (0.000) | −0.018 * | (0.099) |

| SIZE | −0.002 | (0.080) | −0.001 | (0.504) |

| B/M | 0.004 | (0.281) | 0.005 | (0.291) |

| LEVERAGE | −0.016 * | (0.065) | −0.008 | (0.429) |

| STDEV | 0.700 *** | (0.000) | 0.530 *** | (0.000) |

| ΔSIZEPROG | 0.001 ** | (0.045) | 0.001 ** | (0.012) |

| OPTION | −0.028 | (0.384) | −0.091 * | (0.087) |

| CASHFLOW | 0.028 | (0.133) | 0.072 *** | (0.004) |

| Pr(Repeat repurchase) | −0.020 | (0.181) | −0.012 | (0.489) |

| TREND | 0.000 | (0.298) | 0.000 | (0.445) |

| INTERCEPT | 0.020 | (0.648) | −0.155 *** | (0.006) |

| Industry effect | Y | Y | ||

| Adj. R2 | 0.0681 | 0.0279 | ||

| Number of obs. | 2972 | 1311 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ding, D.K.; Koerniadi, H.; Krishnamurti, C. What Drives the Declining Wealth Effect of Subsequent Share Repurchase Announcements? J. Risk Financial Manag. 2020, 13, 176. https://doi.org/10.3390/jrfm13080176

Ding DK, Koerniadi H, Krishnamurti C. What Drives the Declining Wealth Effect of Subsequent Share Repurchase Announcements? Journal of Risk and Financial Management. 2020; 13(8):176. https://doi.org/10.3390/jrfm13080176

Chicago/Turabian StyleDing, David K., Hardjo Koerniadi, and Chandrasekhar Krishnamurti. 2020. "What Drives the Declining Wealth Effect of Subsequent Share Repurchase Announcements?" Journal of Risk and Financial Management 13, no. 8: 176. https://doi.org/10.3390/jrfm13080176

APA StyleDing, D. K., Koerniadi, H., & Krishnamurti, C. (2020). What Drives the Declining Wealth Effect of Subsequent Share Repurchase Announcements? Journal of Risk and Financial Management, 13(8), 176. https://doi.org/10.3390/jrfm13080176