2.1. The Sharing Economy

Airbnb, and home-sharing platforms more generally, operate within the broader sharing economy. Whilst the sharing economy is a term often used to describe a number of different platforms, it is best defined as a ‘set of peer-to-peer online marketplaces that facilitate matching between demanders and suppliers of various goods and services’ (

Barron et al. 2020, p. 2). Common examples of platforms that operate within the sharing economy include Airbnb, Uber, HomeAway, Lyft, Deliveroo, Fiverr, Doordash, and TaskRabbit. Despite the economy spanning such a vast range of industries, each characterised by different features, the platforms often share common components. On all platforms, the suppliers of products and services look to share excess capacity that might otherwise go underutilised with people that want to use them for a short period of time (

Ferreri and Sanyal 2018). Additionally, the platforms do not own any of the assets that they are advertising, but instead facilitate sharing between participants for a fee, often relying on spot-transactions rather than long contracts (

Einav et al. 2016;

Proserpio and Tellis 2017). With many of the marketplaces being app-based, developers often utilise advancements in technology to improve the matching between buyers and sellers and have implemented reputation and rating systems in order to create a sense of trust on the platforms (

Einav et al. 2016). In theory, there are two main segments that operate in the ‘pure’ peer-to-peer economy. The first are decentralised platforms. These are services that bridge the gap between demanders and suppliers, but leave the searching, matching, and price setting to the participants (

Proserpio and Tellis 2017). Examples in this segment include Airbnb, Stashbee, and TaskRabbit. On the other hand, centralised platforms take control and centrally match buyers and sellers, setting prices using tested algorithms. Examples include Uber, Lyft, and Doordash.

The sharing economy, which is projected to generate more than

$335 bn of revenue worldwide by 2025, has seen tremendous growth in recent years and is rapidly changing the ways in which we consume products and services (

Proserpio and Tellis 2017). There are numerous reasons as to why this growth has occurred. Firstly, the 2008/09 financial crisis left many without steady incomes or employment opportunities and created a group of people that were unable to pay for assets and services. The sharing economy thus created an opportunity for these groups to turn to alternative platforms that compensated them for providing underused assets. Additionally, the flexibility of these platforms allows users to decide between working on these marketplaces full-time or to use it as a supplement to their regular income. Secondly, a wave of technological advancements, including smartphones, apps, and WiFi has allowed for greater connectivity and has reduced search costs and the time it takes to connect buyers and suppliers. Finally, globalisation has blurred the lines between local and global economies. This has meant that resources that are underutilised in a local economy can now be accessed by users on a global scale (

Proserpio and Tellis 2017).

The sharing economy is celebrated by many as an innovation that improves economic efficiencies by reducing the frictions caused by excess capacity whilst also being capable of disrupting established industries (

Barron et al. 2020;

Proserpio and Tellis 2017). Proponents of these marketplaces applaud the platforms’ ability to provide consumers with a better matching and use of resources, lower prices, better offerings, and an overall increase in welfare (

Barron et al. 2020). Additionally, the economy’s flexibility mentioned previously is argued to foster micro-entrepreneurialism as individuals are able to monetise their assets whilst still contributing to the GDP through their regular occupations (

Ferreri and Sanyal 2018). This being said, however, there are many that argue that these platforms’ negatives outweigh their benefits. More specifically, recent evidence has shown that the sharing economy may increase societal inequality (

Schor 2017) and lower city centre affordability whilst displacing lower income populations to nearby communities (

Lee 2016). Furthermore, academics, including

Ferreri and Sanyal (

2018), contend that the sharing economy has moved away from a forum that allows the exchange of goods and services and towards one where ‘venture capital firms come to intervene and influence these processes’ (p. 3357).

2.2. Airbnb and Short-Term Rentals

After renting out air mattresses on their apartment floor to attendees of a conference in San Francisco, Brian Chesky and Joe Gebbia founded Airbnb in 2008, which is now recognised as the pioneer of not just the home-sharing industry, but the sharing economy as a whole. Airbnb operates as a peer-to-peer marketplace for short-terms rentals, connecting tourists with suppliers of various kinds of accommodations. It is important to note that in most academic literature, short-term rentals (STRs) are defined as ‘lettings of up to 30 consecutive days’ (

Koster et al. 2018, p. 8). The website allows its users to advertise three different types of listings: a shared room, a private room, or an entire unit. Local authorities and academics often distinguish between two types of short-term rentals. ‘Home-sharing’, which includes Airbnb’s shared and private room listings, is usually defined as a STR where at least one of the primary residents lives on-site during the tourists’ stay. ‘Vacation rentals’, on the other hand, are where the tourist occupies the entirety of the letting (

Koster et al. 2018). Seeing as Airbnb operates in both segments, the platform has essentially created a new category of rental housing which blur the lines between traditional rentals and hotel accommodation.

Furthermore, the platform’s business model is simple: hosts list their offerings on the marketplace for a price set by themselves, while Airbnb takes a commission of anywhere from 7% to 18% per booking (

Wachsmuth and Weisler 2018). This being said, Airbnb takes great pains in order to hide its operations from public view and has been claimed to bypass regulations and ‘undermine policies aimed at protecting the supply of affordable housing’ (

Wachsmuth and Weisler 2018, p. 5). It is often argued that Airbnb has moved away from a sharing platform to one that incentivises large scale operators to accumulate additional properties in search for profit. For example, in Los Angeles, researchers found that these large-scale property developers earn huge revenues; just 6% of hosts list more than one property and yet they earn 35% of all Airbnb revenue (

Lee 2016).

DiNatale et al. (

2018) surveyed the Airbnb markets in 237 cities in Oregon, USA. They found that nearly 40% of Airbnbs are whole homes that are rented more than 30 days in a year, which potentially has significant impacts on long-term rental supply in those cities.

Airbnb’s rapid growing in many cities raised serious concerns in a wide range of areas such as anti-social behaviour (noise, disruption), public health, safety, fire risk, availability and affordability of permanent rental housing, impacts on local services and tax revenue, and impacts on the tourism industry (

Gurran and Phibbs 2017;

Gurran et al. 2018). Although Airbnb position itself as the poster child of sharing economy by providing temporary supplies to the tourism sector, evidence is found that Airbnb actually removes residential units from housing market permanently (

Crommelin et al. 2018;

Schäfer and Braun 2016;

Vinogradov et al. 2020). There are growing concerns about Airbnb’s role in the financialization of housing (

Cocola-Gant and Gago forthcoming;

Grisdale 2019), displacement (

Cocola-Gant and Gago forthcoming;

Yrigoy 2019), and tourism-led gentrification (

Robertson et al. 2020;

Wachsmuth and Weisler 2018).

Despite these criticism and concerns, Airbnb has seen tremendous rates of growth since its incubation in 2008. Airbnb now has over seven million properties on its platform, listed by over two million hosts in 81,000 cities and 191 countries worldwide, more than twice as many as its closest competitor, HomeAway (

Airbnb Newsroom 2020;

Barron et al. 2020;

Wachsmuth and Weisler 2018). Additionally, Airbnb has provided accommodation to over 500 million guests, allowing it to gain a monopolistic position in many of the cities in which it operates (

Airbnb Newsroom 2020;

Ferreri and Sanyal 2018). Despite attempts at regulation in order to protect local markets and curb Airbnb’s growth (

Cassell and Deutsch forthcoming), these numbers are still expected to rise. While Airbnb has yet to have its IPO, the platform’s market penetration and profitability figures has resulted in a valuation of over

$31 bn, making it larger than some of the World’s leading accommodation chains including the Marriot and Hilton groups (

Proserpio and Tellis 2017).

2.3. The Effects of Airbnb on Rental Real Estate Markets

It is often theorised that Airbnb has two competing effects on local rental property markets. On the one hand, the extra rental income earned by local residents is argued to enable some citizens to continue living in ‘booming’ housing markets. On the other hand, the high revenues earnt from short-term rentals mean that property owners of all types have an incentive to shift their supply from the long-term market to the tourist market, which increases rents for long-term tenants. In support of the latter argument, recent research by academics in both Europe and the USA have found that Airbnb often distorts rental markets through either a supply effect or a demand shift.

Perhaps the leading theory on Airbnb’s effect on residential markets is that the expansion of the platform has caused a supply shift from the long-term to the short-term rental market, decreasing total supply in the long-term and increasing rents for local tenants. Academics suggest that the market for long and short-term rentals is segmented on both the demand and supply side. This segmentation is argued to exist for many reasons. On the demand side, tenants will have different needs depending on the length of their stay: the potential tenants of short-term accommodation are usually tourists, business travellers, and other visitors who may only be looking for a bed and bathroom. Local residents seeking a more comprehensive dwelling, on the other hand, create the demand for long-term accommodation (

Barron et al. 2020). On the supply side, there may be legal restrictions which do not allow for the transfer of accommodations from different term structures; additionally, landlords may prefer one length of letting to another or may be unable to switch due to contractual obligations.

This segmentation has created a term structure of rents, with the rents coming from short-term accommodation typically being much higher than the rents coming from long-term lettings. The gap between the two term structures is often referred to as the ‘home-sharing premium’. The expansion of home-sharing platforms like Airbnb have reduced the frictions between the two segments and has allowed for the transfer of accommodation from the long-term to the short (

Horn and Merante 2017). Furthermore, seeing as the supply of housing is fixed or highly inelastic in the short-run, this transition results in a decreased supply of long-term rental properties and puts tourists in direct competition with local renters, raising prices for all long-term accommodations (

Lee 2016). This issue is exacerbated by the fact that, in many cities, both private and public developers are already unable to build enough new homes for their residents.

There is substantial evidence that a supply side factor has contributed to the rising rental prices in many cities. Focusing on U.S. metropolitan areas,

Barron et al. (

2020) engaged in regression analysis to discover a causal relationship between Airbnb penetration and rental rates. More specifically, they found that, on average, a 1% increase in Airbnb listings led to a 0.018% increase in indexed rental rates. Consistent with the supply side theory, they found that higher rates of Airbnb listings resulted in fewer dwellings being vacant and available for rent. This, together with the fact that there was no effect on the total housing supply, led to their conclusion that Airbnb affects rental real estate markets through a supply side effect (

Barron et al. 2020).

In a research journal published at a similar time,

Horn and Merante (

2017) focused more closely on Boston, a single city in the U.S. Their initial analysis had found that in Boston, while 82% of the hosts had only one simultaneous listing on Airbnb, the 18% of hosts that did have multiple listings represented nearly 50% of all dwellings. This suggests that Airbnb may have evolved into an operation that is dominated by profit-seeking commercial operators. Their main piece of analysis involved an examination of whether Airbnb presence is associated with higher rents in the following time period. The researchers found that a one standard deviation increase in Airbnb listings relative to the total units of housing within a census tract increased listed asking rents by 0.4% and decreased the number of rental units offered by 5.9% (

Horn and Merante 2017). Once again, these results support the supply side theory mentioned previously.

Outside of the U.S., few studies have estimated the effects of Airbnb on the supply of rental housing. However, a working paper published by Garcia-López et al. in 2019 used similar processes in order to analyse markets in Barcelona. Having access to individual-level data on transactions of second hand apartments sold in the city, as well as a summary of all advertised rental listings, they were able to conclude that rent levels were higher in areas with more Airbnb activity; specifically, their results suggested that, on average, an increase of 54 active listings in a neighbourhood increased rents by 1.9% (

Garcia-López et al. 2019).

Another prominent theory argues that Airbnb affects rents by creating a rent gap in the markets in which it operates, which then leads to gentrification. Neil Smith’s original rent gap model, which was proposed to explain the gentrification trends occurring in American inner-cities, is underpinned by two key theoretical concepts: ‘actual’ and ‘potential’ economic returns, or ground rents (

Smith 1979). Actual ground rent refers to the rent currently received by the landlord, given the present use of land whilst potential ground rents are the ‘amount that could be capitalised under the land’s highest and best use’ (

Smith 1979, p. 543).

Smith (

1979) argues that rent gaps are created when there is a divergence between actual and potential ground rents, often resulting in real estate investment flowing in. This increase in investment will likely ‘drive up rents, attract more affluent residents and displace the neighbourhood’s existing residents’ to nearby communities (

Wachsmuth and Weisler 2018, p. 7). Airbnb, and the home-sharing premium associated with the platform, is argued to create a new highest and best use of residential properties, resulting in the creation of a new potential ground rent.

This technologically driven rent gap, however, is different to those proposed by

Smith (

1979). In the case of Airbnb, there is no dramatic decrease in actual ground rents due to capital depreciation prior to the gap emerging. Rather, the expansion of Airbnb acts as an exogenous shock to the market, instantaneously creating a divergence between actual and potential ground rents. Additionally, in the standard rent gap theory, in order for gentrification to occur, the gap must become wide enough to justify the cost of renovations or new construction; however, with the little to no cost involved with listing a dwelling on Airbnb, the gap does not have to pass a certain threshold before gentrification occurs. In practice, however, it is difficult to prove that the technologically driven rent gap exists due to the difficulty in measuring the highly theoretical concepts of actual and potential ground rents.

Focusing on New York City, researchers

Wachsmuth and Weisler (

2018) find that Airbnb has created new potential revenue streams for landlords and has had geographically uneven effects. The paper is able to find clear evidence of a rent gap by investigating empirical indicators of actual and potential ground rents. More specifically, the researchers discover that some areas offer Airbnb hosts revenues of 200–300% higher than from median rents. Furthermore, the platform’s greatest disruption has been on affluent neighbourhoods that have already been gentrified, leading to wealthy landowners capturing many of Airbnb’s economic benefits at the expense of local residents.

Additionally, after noticing the lack of empirical studies that address the rent gap in the context of Europe,

Yrigoy (

2019) looked to quantify the gap between rental income vis-à-vis tourist rentals in the Old Quarter of Palma de Mallorca. By estimating a yearly potential revenue from Airbnb listings, he found that the income generated by tourist rentals more than tripled that earned by dwellings rented to local residents despite there being far fewer units available. Once again, this is clear evidence of the rent gap. The paper also argues that the rent gap has contributed to tourism-gentrification, whereby the capital flows toward real estate, as well as a boost in the urban tourism market, pushes out local residents in favour of more affluent newcomers (

Yrigoy 2019). The researcher concludes that, despite the gradual decrease in revenues generated from individual tourist lettings, landlords will continue switching from the long to the short-term market until rents equalise and the rent gap disappears.

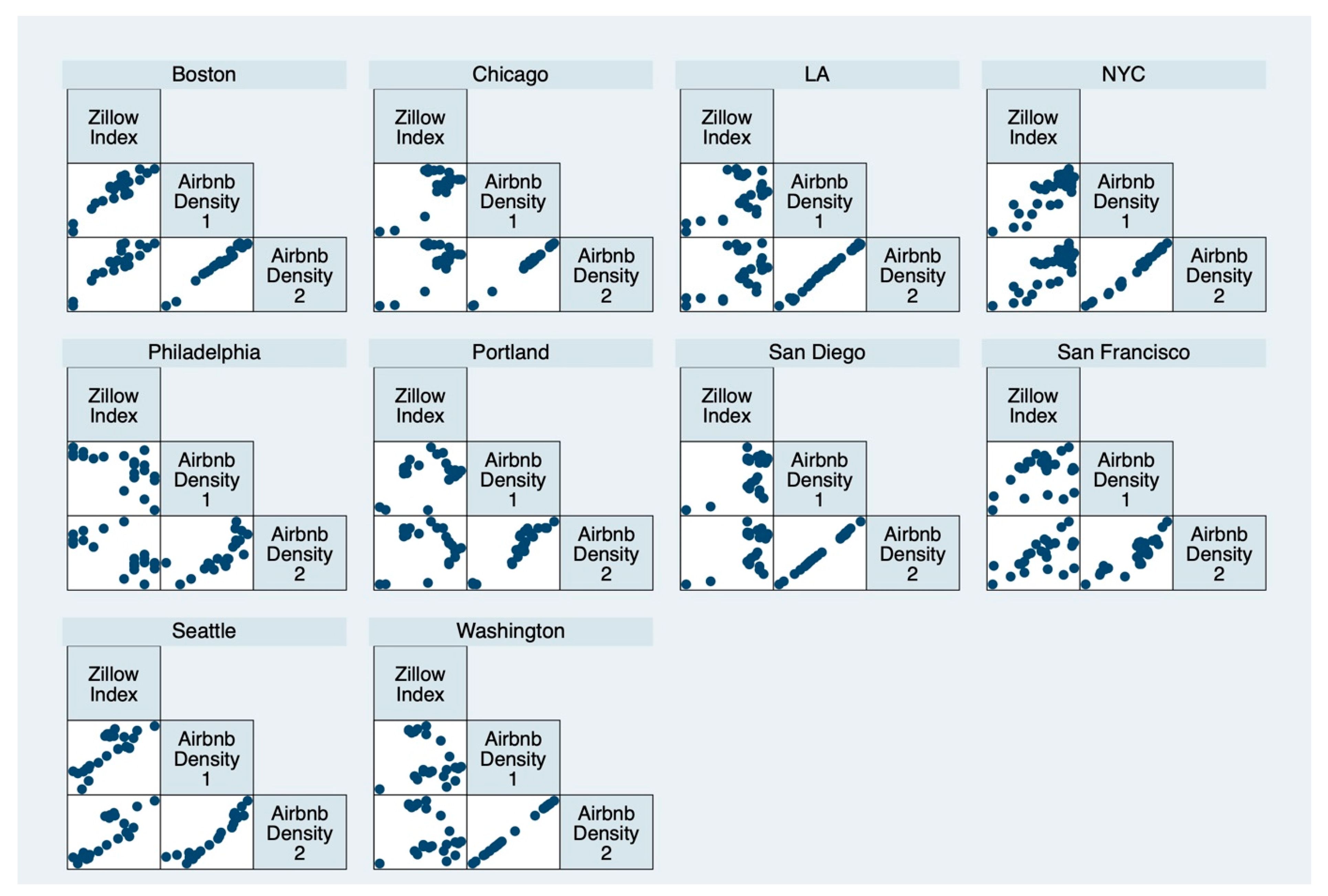

The majority of the literature cited here offers an over-simplistic view of the dynamics through which Airbnb operates. More specifically, the papers often rely on analysing the relationship between home-sharing and rental rates at an aggregate scale and fail to examine the many discrepancies present between specific rental markets. This paper looks to supplement the literature by examining Airbnb’s effects at a neighbourhood, or zip code level.

{kind=link}