Factors Influencing the Green Bond Market Expansion: Evidence from a Multi-Dimensional Analysis

1

Public Accounting Unit, Financial Public Faculty, Academy of Finance, Hanio 10000, Vietnam

2

Department of Business Strategy and Innovation, Griffith Business School, Griffith University, Nathan, QLD 4111, Australia

3

Faculty of World Studies, University of Tehran, Tehran 1417466191, Iran

*

Author to whom correspondence should be addressed.

J. Risk Financial Manag. 2020, 13(6), 126; https://doi.org/10.3390/jrfm13060126

Submission received: 23 April 2020

/

Revised: 6 June 2020

/

Accepted: 10 June 2020

/

Published: 13 June 2020

(This article belongs to the Special Issue Challenges and Solutions of Green Finance in the Low Oil Price Era)

Abstract

:Expansion of green bond markets as an appropriate way to lower environmental pollution is one of the most debatable issues among scholars. However, the expansion of this market is not a simple matter and depends on several factors. The main purpose of this study is to carry out a multi-dimensional analysis using the analytic hierarchy process (AHP) method to find and prioritize factors influencing the development of green bond markets. As a case, we do our analysis for Vietnam that, since the last years, has been trying to expand green bond market as an effective investment channel to finance low-carbon projects. The main findings revealed that legal infrastructure, official interest rate of green bonds, and economic stability are the most important factors directly affecting green bond market expansion. Therefore, economic and legal requirements should be addressed by policy makers. As major policy implications, we recommend an affordable price of green bonds and improvement of economic and financial stability to accelerate the development of green bond markets.

1. Introduction

Green bonds (GBs) are an important financial tool used to raise capital for low-carbon projects that benefit the environment (World Bank 2019; Tu et al. 2020). According to Tolliver et al. (2020), this new financial tool is an applicable way to increase emissions reductions policies, long-run development, and improvement of ongoing eco-friendly projects to reach the goals of the Paris Agreement. Bachelet et al. (2019) define a green bond as a “plain-vanilla” fixed income product that opens sustainable doors for investors into financing green projects.

The first green bond was issued by the World Bank and the Swedish bank SEB in 2008, and its global market has expanded from $11 and $36 billion in 2013 and 2014 to nearly $167 billion in 2018 (Maltais and Nykvist 2020). Despite the rapid growth of the green bond market because of its remarkable impacts on debt financial expenses and financial performances (Curley 2014; Tang and Zhang 2018; Flammer 2018; DeSchryver and Mariz 2020), the market expansion of green bonds in countries is a debatable issue among scholars. A number of scholars such as Voica et al. (2015) and Partridge and Medda (2020) argue that private investors and public authorities are two important players in the green bond market, and these two players define the expansion level of green bond markets, while some studies believe in the impacts of different factors on development of green bond market. For instance, Ehlers and Packer (2017); Flammer (2018); Zerbib (2018); Reboredo and Ugolini (2019); and Broadstock and Cheng (2019) discuss the effect of financial markets and various macroeconomic factors on the green bond market, respectively. In addition, several studies (e.g., see Della Croce and Yermo 2013; Bhattacharya et al. 2015) declare that investment infrastructure can help the green bond market to expand. Therefore, it is clear that green bond market expansion depends on various factors having an interrelationship and makes the development of green bond market multi-dimensional.

In recent years, the green bond markets in different nations have been developed rapidly. Following Flammer (2019), this rapid development is characterized the “green bond boom” in the global financial market. According to the World Bank’s Emerging Market Green Bond Report 2018, East Asia and Pacific is the biggest green bond market among other geographical regions. South Asia, with 7.7 billion US $, has had the second biggest green bond market expansion over the period 2012–2018. Table 1 represents the green bonds issued in different regions during the 2012–2018 period.

Among Asian nations, Vietnam is one of the players in the green bond market with the most potential. Following the market reforms of this country carried out in 1986, Vietnam’s economic mechanisms are based on emerging systems. Nguyen and Gray (2016) express that Vietnam is facing two important issues of sustainability development and the green movement, which are accelerators of developing green economic instruments. One type of these green instruments is green bonds, which two Vietnamese local government entities—Ho Chi Minh City and Ba Ria Vung Tau—followed in their footsteps by issuing the first VND-denominated GBs and listing them on the Hanoi Stock Exchange in the last decade. Despite all Vietnam’s efforts to enter to this green market, it has not been developed and expand significantly owing to various reasons, such as inappropriate energy pricing policy, non-preferential feed-in tariff, and an undeveloped financial system (Nguyen et al. 2019).

Owing to the importance of green bond market expansion and the existence of various influencing factors on the expansion, it is a critical need to study and prioritize the influencing factors. In this paper, we seek to classify all important influencing factors on expansion of the green bond market in the case of Vietnam through a multi-dimensional analytic approach entitled analytic hierarchy process (AHP), and find out priorities of these factors based on judgments of a group of experts. Despite some fresh studies about green bond markets such as Cochu et al. (2016); Shishlov and Morel (2016); Jun et al. (2016); Hachenberg and Schiereck (2018); Hupart (2019); DeSchryver and Mariz (2020); and Tolliver et al. (2020), we did not find any academic study focusing on priority of factors affecting the expansion of the green bond market. Therefore, our paper will try to fill in this literature gap. Conducting this research help us to answer questions such as the following: What are the main factors in related to develop green bond market? Which influenced factors are more important than others? How can policy makers expand the green bond market?

2. Literature Review

The related literature can be divided into two different strands as follows.

The first strand of literature contains earlier studies with a focus on the green bond market. The characteristics of the green bond market have been debated by a vast number of scholars. Maltais and Nykvist (2020) discussed the role of green bond markets in economic sustainability for the case of Sweden. They identified the potential of the green bond market in economic participants’ engagement and sustainable economic and social development. Wang et al. (2020) and Baulkaran (2019) showed that a green bond is an interesting field for investors. They found that stock market investors in China have a positive response to green bond issuing news. This result has also been addressed by Pham and Huynh (2020), who revealed positive linkage between reactions of investors and green bond market performance. In addition, Wang and Zhi (2016) also proved the significant role of green bond markets in environmental protection and combating climate change. Banga (2019) investigated the key factors and barriers influencing the green bond market in developing nations. They found that climate-awareness from investors, inappropriate institutional arrangements, and high transactions costs with green bond issuance are major players in developing the green bond market. Wang et al. (2019) studied the factors influencing the risk premium of issuance in China’s green bond market. The major results revealed that debt credit rating, issue period, and issue size are three different factors that directly impact the risk premium of green bond issuance. In other study, Zhou and Cui (2019) made an attempt to find out the relationships between green bonds, corporate performance, and social responsibility in China’s green bond market. The findings showed that corporate performance and social responsibility to environmental issues positively affect the expansion of the green bond market. Agliardi and Agliardi (2019) argued that improvement in credit quality, lowering cost of capital for green bond issuers, and state support are three main drivers of green bond development. This finding is in line with Dou and Qi (2019), who investigated the factors affecting the choice of green bond issuing by state and private sectors. Flammer (2019) believes that certification is a main governance mechanism in the green bond market that motivates independent third parties in issuing green bonds. Tolliver et al. (2020) investigated drivers of green bond market growth in 49 countries and found out the positive influence of capital market, macroeconomic, and institutional factors on developing green bond markets. Broadstock and Cheng (2019) argued that the development of the green bond market depends on various factors. Using the dynamic conditional correlations (DCC) revealed that economic policy instability, energy price, and financial market uncertainty (the effect of financial market has also been proven by Reboredo and Ugolini (2019)) are major drivers to accelerate growth of the green bond market. Febi et al. (2018) evaluated the impact of liquidity uncertainty on green bonds. They concluded that liquidity risk is an important factor for green bonds’ development. In a study, Tu et al. (2020) argued that the existence of an efficient legal framework is a pioneer need for expansion of green bond markets. Jin et al. (2020) focused on the relationship between the hedging effect and the efficiency of green bond markets. They proved that the green bond market is one of the most efficient markets for future emissions reductions. Zerbib (2019) analyzes the relationship between pro-environmental preferences and green bond market development. The major results showed the significant investors’ pro-environmental preferences effect on the green bond market expansion. Wang and Zhi (2016) argued that appropriate regulation framework and state support can improve the mechanism efficient of green bond market, which leads to better environmental protections. Voica et al. (2015) proved that an appropriate legal and institutional framework may shape a better atmosphere to expand green bond markets in countries by encouraging investors to have a more efficient participation.

The second strand of literature concentrates on earlier studies that used the AHP method to solve an economic problem. Saaty (1987) introduced AHP as a new technique for macroeconomic forecasting considering policies of monetarist, Keynesian, and supply-side. Byun (2001) provided a model based on the AHP approach to prioritize automobile purchase models. Bozbura and Beskese (2007) employed the AHP approach to study organizational capital measurement indicators. In another study, Gerdsri and Kocaoglu (2007) conducted the AHP method in the problem of technology road mapping in a knowledge-based economy. Podvezko (2009) discussed advantages of the AHP technique in solving economic and social matters. Lin et al. (2011) applied a mixed model of AHP and DEA (data envelopment analysis) to study the economic activities of local Chinese governments. Sadeghi and Ameli (2012) tried to study energy subsidy in several economic sectors in Iran through the AHP method. In other study, Alizadeh et al. (2014) investigated factors affecting the expansion of wooden commodities exports from Iran. To this end, they conducted the AHP method to prioritize the influencing factors. Oztaysi (2014) used the AHP method to study IT (information technology) selection in a knowledge-based economic framework. Longaray et al. (2015) conducted academic research on services’ qualities in the Brazilian retail sector using the AHP method. Hadadian and Rasoulian (2017) used the AHP method to prioritize trade partners for Iran with the goal of economic integration. Lotti and Caetano (2018) evaluated the appropriate airports for fruit exports from Brazil using analytic hierarchy process. In other study, Sharma (2018) explained the capabilities of the AHP method to make decisions in economic problems. Roh et al. (2019) and Lee and Hwang (2010) used the AHP technique to model nuclear power plant export competitiveness in Korea. Ortiz-Barrios et al. (2019) applied a comparison with AHP to study efficiencies of food supply chain management. Mahdiloo et al. (2019) and Jabalameli and Rasoulinezhad (2012) applied the AHP technique to find out the solutions of lowering negative effects of sanctions against Iran. Ren and Ding (2019) performed an analytic hierarchy process to investigate the impacts of high-speed rail on regional economic development in China. Jurík et al. (2020) applied the AHP method to select projects related to the three dimensions of economic, social, and environmental for sustainable development.

Overall, it can be concluded from the earlier studies that the expansion of the green bond market is affected by various factors. The literature gap that will be filled in with our research is the lack of academic study gathering all factor influencing green bond market expansion and ranking them through a logical multi-dimensional method.

3. Methodology

To determine the importance of various factors influencing GB market development in Vietnam, we employed a multi-criteria decision making (MCDM) method called the analytic hierarchy process (AHP) method. This method, proposed by T.L. Saaty in the 1970s, is commonly used as a structured approach to analyze complex decisions. Albayrak and Erensal (2004) express that the AHP method can help researchers to solve qualitative problems that involve multiple criteria. Kwong and Bai (2002) and Russo and Camanho (2015) argue that the AHP method is a simple technique to face a multi-dimensional problem. The main reasons for selecting the AHP method in this study are the increasing complexity of the problem of green bond market expansion and the capability of AHP to define the problem in detail and rank the criteria and sub-criteria according to their importance.

To conduct the AHP method, we needed to state the main problem (GB market development in Vietnam) and determine the framework of the problem based on all actors and objectives. Mahmudova and Jabrailova (2020) and Mandić et al. (2017) expressed that construction of the AHP structure addresses all dimensions of the problem, and so we can make the best solutions in an easier way.

Next, we identified the criteria and used the hierarchy structure to design the relationship between purpose, criteria, and factors. Subsequently, pairwise comparisons were conducted to evaluate the weights of the criteria and factors. To this end, we asked ten Asian energy and economy experts to carry out the comparisons through an AHP questionnaire that was distributed to the experts during February 2020 through email. It should be noted that the number of experts in the multi-criteria dimensional model is flexible. However, Tsyganok et al. (2012) proved that the large expert group size would decrease the importance of being an expert in these models. Furthermore, many earlier studies (e.g., see Peterson et al. 1994; Al-Harbi 2001; Armacost et al. 1994; Mawapanga and Debertin 1996; Huang and Yeh 2011; Kil et al. 2016) have considered a small group of experts to conduct the AHP method. Therefore, we decided to select only 10 experts who have advanced experience in or study green bond markets. Table 2 represents the demographic characteristics of our panel of experts.

Next, we performed calculations to determine the maximum value of eigenvector, consistency index (CI), consistency ratio (CR), and normalized values for each criterion.

Here, indicates the principal eigenvector; n is the matrix size; aij denotes an element of the pairwise comparison matrix; and wj and wi represent the jth and ith element of values of eigenvector, respectively. As a rule, if the maximum value of eigenvector, CI, and CR are satisfactory, then the decision is made based on the normalized values; otherwise, the last procedure is conducted again until these values fall within a desired range. If CI > 0.1, we can interpret the relative weights of factors and also conduct a global ranking of factors related to the goal (Rasolinezhad 2009).

4. Results and Discussion

At the first stage, we determine the objective of our decision making as green bond market expansion in Vietnam. Then, we gather several criteria and factors related to our goal from the earlier literature and ask the panel of our experts to help us finalizing the most important and relevant criteria and sub-criteria. Finally, using a brainstorm method, 4 criteria and 23 factors associated with each criterion were finalized by the group of experts, as expressed in Table 3.

Next, we used the judgments of the group of experts to make pairwise comparisons to calculate the relative priority of each criterion. This would help us to find the weights of each criterion and factor related to our model’s goal. The results, expressed in Table 4, reveal that, among the four criteria, the experts emphasized the importance of financial (A) and infrastructural criteria (D), while they thought the economic and political (B) and social criteria (C) are the least influential for GB market expansion in Vietnam. The major roles of financial and infrastructural aspects have also been expressed by Ketterer et al. (2019) and Climatebonds (2015), respectively.

After pairwise comparison of the criteria, the group of experts conducted judgments to determine the importance of sub-criteria associated with each criterion (Table 5, Table 6, Table 7 and Table 8). The judgments in this step help us to prioritize the importance of factors related to the criteria.

The results, represented in Table 5, show that the most important sub-criteria of financial criterion (A) based on the experts’ judgments are monetary policy (A5) applied by the State Bank of Vietnam and inflation rate (A1), respectively, while investment risk (A4) has the lowest priority among these sub-criteria. The importance of monetary policy on expansion of bond market has also been declared by Nishat and Matsuda (2016). Furthermore, increasing price levels of goods and commodities as inflation rate negatively impact green bond investors. Hence, the factor of inflation rate is one of the most important financial factors related to green bond market expansion (Sabov and Murphy (1999) and Macchiarelli (2014) proved the importance of the inflation rate in bond markets).

Regarding economic and politics sub-criteria (B), the pairwise comparisons show evidence of the importance of political stability (B1), whereas CO2 emissions level (B7) and market-based economic system (B3) play a small role in green bond market expansion for Vietnam. The results are in line with Perry and Robertson (1998) and McGee (2007), who showed the relationship between political stability and bond markets. Moreover, our finding about the importance of CO2 emissions level in the expansion of green bond market is in line with Sartzetakis (2020).

The experts’ judgments about sub-criteria of social criterion (C) reveal that social support (C1) and income inequality (C5) are more important priorities compared with social–environmental linkage (C2), urbanization growth (C3), and unemployment rate (C4) in the green bond market expansion of Vietnam.

Finally, the results, represented in Table 8, depict the high importance of institutional infrastructure (D3) and legal framework (D1), respectively. In addition, limited application to international standard (D2) with a priority of 0.052 is the least important sub-criterion among others.

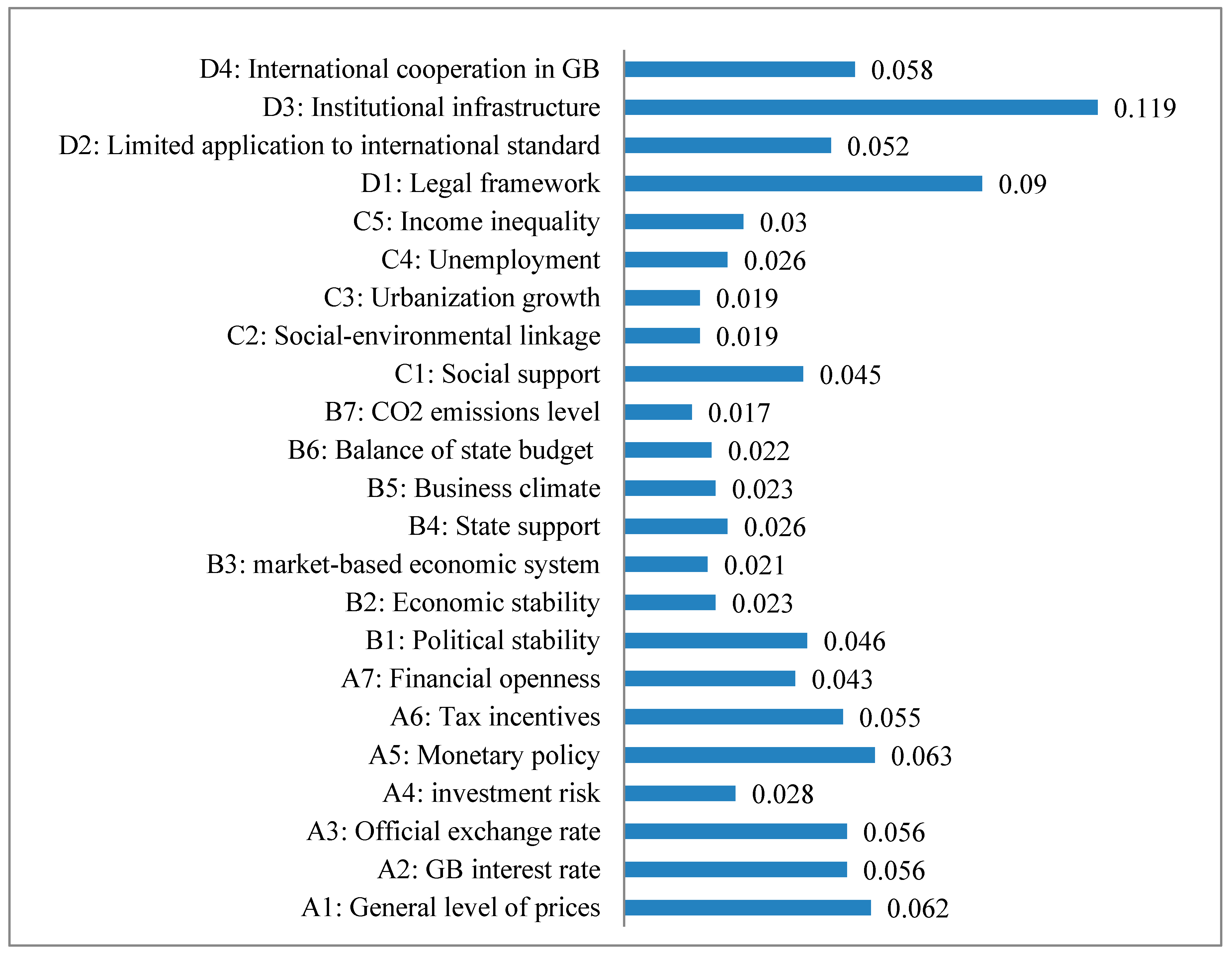

In the above, the relative weights of sub-criteria associated with each criterion are achieved, and we now calculate the overall ranking of these factors with respect to the goal of the GB market expansion in Vietnam. The ranking of factors influencing the green bond market expansion in Vietnam is shown in Figure 1.

As shown in Figure 1, institutional infrastructure (D3), legal framework (D1), and monetary policy (A5) of the State Bank of Vietnam are considered the three most important influential factors on Vietnam’s GB market expansion, while CO2 emissions level (B7) with a weight of 0.017 and social–environmental linkage (C2) and urbanization growth (C3) with 0.019 are the least important influencing factors for expanding the GB market expansion in Vietnam. It can be expressed that the factors included in the infrastructural criterion play the major role in developing GB market, while the social criterion is not as important compared with other criteria. This finding is in contrast with Zhou and Cui (2019), who emphasize the role of the social factor, while it is in line with Voica et al. (2015), who prove that an appropriate legal and institutional framework may shape a better atmosphere to expand green bond markets in countries by encouraging investors to have a more efficient participation.

5. Robustness Check

To ensure the reliability and viability of our results from the AHP technique, we follow the method of robust partial least squares (R-PLS) regression applied by Marcarelli et al. (2013) to re-calculate the weights of comparison matrices. Using a PLS regression estimator helps us to make priorities from pairwise comparison matrices via correlation coefficient maximizing (Wang et al. 2007).

Table 9 reports the final priorities of factors based on R-PLS regression.

The estimated weights by the R-PLS regression, listed in Table 8, reveal quite similar results with the AHP, indicating the robust of our results.

6. Conclusions and Policy Implications

The issue of green bond market expansion for Vietnam is necessary owing to the fossil-fuel intensive nature of the economy of this country and its high potential abundant sources of green energy resources. Expansion of green bond market as a useful instrument of emissions reductions has been considered by many scholars. This study was an academic attempt to determine and find priorities of factors influencing green bond (GB) market expansion in Vietnam. To this end, a multi-dimensional decision making method called analytic hierarchy process (AHP) was conducted in software Expert Decision 10. To apply the AHP, we asked ten Asian energy and economy experts to judge the importance levels of 4 criteria and 23 sub-criteria gathered based on the earlier literature review and consultation with the group of experts. The major highlights from the findings of the AHP method are as follows: (i) among the four major criteria, financial (which has been discussed by Sun et al. (2020) and Mohsin et al. (2020)) and infrastructural criteria play the most important role in the expansion of the green bond market in Vietnam. (ii) The presence of an efficient monetary policy and a controlled inflation rate is necessary for sustainable expansion of the GB market in Vietnam. (iii) Vietnam’s political stability is the most important political factor (in line with Freeman (1992), who argues that the reform in Vietnam was a movement to political stability that ensures the sustainable development in the country). (iv) Societal concern for the environment is not an important factor compared with financial and infrastructural criteria to expand the green bond market in Vietnam. (v) Considering all 23 influential sub-criteria revealed that the most important influencing factors among them are institutional infrastructure and the legal framework for GB operations, the monetary policies of the State Bank of Vietnam, and the general level of prices of goods and services. In other words, financial and infrastructural factors are more important to the growth and expansion of the current Vietnamese GB market than economic-political or social criteria.

Regarding policy, improving financial issues related to the green bond market is recommended. Despite several issued policies related to the green bond market in Vietnam, such as National Power Development Plan (2011), Vietnam Renewable Energy Development Strategy 2050 (2016), and Revised National Power Development Plan 7 (2016), the market needs more relevant regulations to support local and foreign private sectors who can play a big role in developing the green bond market in this country. Ensuring protection for investors in green bond markets, financial transparency, and regulating prices in different markets are highlighted policies in this field. Bessembinder et al. (2006); Bessembinder and Maxwell (2008); and Schultz (2012) show that transparency has a remarkable impact on investors’ performances in bond markets. Moreover, according to Taghizadeh-Hesary and Yoshino (2020) and Pham and Huynh (2020), an insufficient rate of return and the existence of several risks are two major challenges for financing green projects. Moreover, lowering different risks such as legal risk, default risk, liquidity risk, inflation risk, political risk, interest rate risk, and investment risk should be considered by the state to create an appropriate climate for private investors. The uni-directional relationship of different risks and the efficiency of bond markets has been discussed by many scholars such as Helberg and Lindset (2016); Duyvesteyn et al. (2016); Febi et al. (2018); Fendel and Neumann (2019); and Reboredo and Ugolini (2019). In addition, there is a potential threat to the growth of green projects owing to the current oil price reduction in the base of the Russia–Saudi Arabia oil war and the Coronavirus outbreak. Currently, owing to low oil prices, the competitiveness of green energy projects compared with fossil fuel projects is reduced, which would endanger their growth post-Covid-19. Hence, wider state support for the green energy projects would be required in the near future.

In fact, considering the need for green financing, public investment will be not sufficient to finance low-carbon projects. A significant contribution from private financial sources (e.g., Taghizadeh-Hesary and Yoshino 2019) is needed in Vietnam and other emerging economies. Green bond market integrity, enhancing green infrastructure, and improving risk–return profiles are two vital GB expansion policies in emerging nations such as Vietnam.

Author Contributions

Data curation, T.S.; Formal analysis, E.R.; Investigation, C.A.T. and E.R.; Resources, T.S.; Software, E.R. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgments

The authors thank Taghizadeh-Hesary and the reviewers for comments that greatly improved the manuscript.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Agliardi, Elettra, and Rossella Agliardi. 2019. Financing environmentally-sustainable projects with green bonds. Environment and Development Economics 24: 608–23. [Google Scholar] [CrossRef] [Green Version]

- Albayrak, Esra, and Yasemin Claire Erensal. 2004. Using analytic hierarchy process (AHP) to improve human performance: An application of multiple criteria decision making problem. Journal of Intelligent Manufacturing 15: 491–503. [Google Scholar] [CrossRef]

- Al-Harbi, Kamal M. Al-Subhi. 2001. Application of the AHP in project management. International Journal of Project Management 19: 19–27. [Google Scholar] [CrossRef]

- Alizadeh, Hassan, Mehdi Faezipour, Majid Azizi, and Mohsen Ziaie. 2014. Determine the parameters affecting the development of Iran’s exports of wooden furniture using Analytic Hierarchy Process (AHP). Journal of Forest and Wood Products 66: 477–91. [Google Scholar]

- Armacost, Robert L., Paul J. Componation, Michael A. Mullens, and William W. Swart. 1994. An AHP framework for prioritizing customer requirements in QFD: An industrialized housing application. IIE Transactions 26: 72–79. [Google Scholar] [CrossRef]

- Bachelet, Maria Jua, Leonardo Becchetti, and Stefano Manfredonia. 2019. The Green Bonds Premium Puzzle: The Role of Issuer Characteristics and Third-Party Verification. Sustainability 11: 1098. [Google Scholar] [CrossRef] [Green Version]

- Banga, Josué. 2019. The green bond market: A potential source of climate finance for developing countries. Journal of Sustainable Finance & Investment 9: 17–32. [Google Scholar]

- Baulkaran, Vishaal. 2019. Stock market reaction to green bond issuance. Journal of Asset Management 20: 331–40. [Google Scholar] [CrossRef]

- Bessembinder, Hendrik, and William Maxwell. 2008. Markets: Transparency and the corporate bond market. The Journal of Economic Perspectives 22: 217–34. [Google Scholar] [CrossRef]

- Bessembinder, Hendrik, William Maxwell, and Kumar Venkataraman. 2006. Market transparency, liquidity externalities, and institutional trading costs in corporate bonds. Journal of Financial Economics 82: 251–88. [Google Scholar] [CrossRef]

- Bhattacharya, Amar, Jeremy Oppenheim, and Nicholas Stern. 2015. Driving Sustainable Development through Better Infrastructure: Key Elements of a Transformation Program. Brookings Global Working Paper Series. No.91; Washington, DC: Brookings. [Google Scholar]

- Bozbura, F. Tunc, and Ahmet Beskese. 2007. Prioritization of organizational capital measurement indicators using fuzzy AHP. International Journal of Approximate Reasoning 44: 124–47. [Google Scholar] [CrossRef] [Green Version]

- Broadstock, David C., and Louis T. W. Cheng. 2019. Time-varying relation between black and green bond price benchmarks: Macroeconomic determinants for the first decade. Finance Research Letters 29: 17–22. [Google Scholar] [CrossRef]

- Byun, Dae-Ho. 2001. The AHP approach for selecting an automobile purchase model. Information & Management 38: 289–97. [Google Scholar]

- Climatebonds. 2015. Scaling up Green Bond Markets for Sustainable Development. Consultation Paper. Available online: https://www.climatebonds.net/files/files/Guide%2030Nov15%20FINAL.pdf (accessed on 11 April 2020).

- Cochu, Annica, Carsten Glenting, Dominic Hogg, Ivo Georgiev, Julija Skolina, Frederik Elsinger, Malene Jespersen, Rainer Agster, Steven Fawkes, and Tanzir Chowdury. 2016. Study on the Potential of Green Bond Finance for Resource-Efficient Investments. Brussels: European Comission, pp. 1–174. [Google Scholar]

- Curley, Michael. 2014. Finance Policy for Renewable Energy and a Sustainable Environment. Boca Raton: CRC Press/Taylor and Francis. [Google Scholar]

- Della Croce, Raffaele, and Juan Yermo. 2013. Institutional Investors and Infrastructure Financing. OECD Working Paper No. 36. Available online: https://www.oliverwyman.com/our-expertise/insights/2014/mar/oecd-institutional-investors-and-infrastructure-financing.html (accessed on 11 April 2020).

- DeSchryver, Pauline, and Frederic De Mariz. 2020. What Future for the Green Bond Market? How Can Policymakers, Companies, and Investors Unlock the Potential of the Green Bond Market? Journal of Risk and Financial Management 13: 61. [Google Scholar] [CrossRef] [Green Version]

- Dou, Xiangsheng, and Shuxiu Qi. 2019. The choice of green bond financing instruments. Cogent Business and Management 6: 1–19. [Google Scholar] [CrossRef]

- Duyvesteyn, Johan, Martin Martens, and Patrick Verwijmeren. 2016. Political risk and expected government bond returns. Journal of Empirical Finance 38: 498–512. [Google Scholar] [CrossRef]

- Ehlers, Torsten, and Frank Packer. 2017. Green Bond Finance and Certification. BIS Quarterly Review. Available online: https://www.bis.org/publ/qtrpdf/r_qt1709h.htm (accessed on 17 February 2020).

- Febi, Wulandari, Dorothea Schäfer, Andreas Stephan, Chen Sun, and Febi Wulandari. 2018. The impact of liquidity risk on the yield spread of green bonds. Finance Research Letters 27: 53–59. [Google Scholar] [CrossRef]

- Fendel, Ralf, and Christian Neumann. 2019. Tail risk in the European sovereign bond market during the financial crises: Detecting the influence of the European Central Bank. Global Finance Journal. [Google Scholar] [CrossRef]

- Flammer, Caroline. 2018. Green Bonds Benefit Companies, Investors, and the Planet. Available online: https://hbr.org/2018/11/green-bonds-benefit-companies-investors-and-the-planet (accessed on 15 February 2020).

- Flammer, Caroline. 2019. Green Bonds: Effectiveness and Implications for Public Policy. NBER Working Paper, No. w25950. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Freeman, Nick J. 1992. International economic responses to reform in Vietnam: An overview of obstacles and progress. Studies in Comparative Communism 25: 287–302. [Google Scholar] [CrossRef]

- Gerdsri, Nathasit, and Dundar F. Kocaoglu. 2007. Applying the Analytic Hierarchy Process (AHP) to build a strategic framework for technology roadmapping. Mathematical and Computer Modelling 46: 1071–81. [Google Scholar] [CrossRef]

- Hachenberg, Britta, and Dirk Schiereck. 2018. Are green bonds priced differently from conventional bonds? Journal of Asset Management 19: 371–83. [Google Scholar] [CrossRef]

- Hadadian, Alireza, and Ali Rasoulian. 2017. Using Analytic Hierarchy Process for selecting the appropriate country for economic integration. International Research Journal of Finance and Economics 162: 24–32. [Google Scholar]

- Helberg, Stig, and Snorre Lindset. 2016. Risk protection from risky collateral: Evidence from the euro bond market. Journal of Banking and Finance 70: 193–213. [Google Scholar] [CrossRef]

- Huang, Rong-Yau, and Cheng-Hung Yeh. 2011. Development of an assessment framework for green highway construction. Journal of the Chinese Institute of Engineers 31: 573–85. [Google Scholar] [CrossRef]

- Hupart, Ruth. 2019. Cracking Open the Green Bond Market—What’s Next? Available online: https://blogs.worldbank.org/climatechange/cracking-open-green-bond-market-what-s-next (accessed on 18 February 2020).

- Jabalameli, Farkhonde, and Ehsan Rasoulinezhad. 2012. Iran solutions against the economic sanctions: Analytic hierarchy process approach. American Journal of Business and Management 1: 23–29. [Google Scholar] [CrossRef]

- Jin, Jiayu, Liyan Han, Lei Wu, and Hongchao Zeng. 2020. The hedging effect of green bonds on carbon market risk. International Review of Financial Analysis. [Google Scholar] [CrossRef]

- Jun, Ma, Christopher Kaminker, Sean Kidney, and Nicholas Pfaff. 2016. Green Bonds: Country Experiences, Barriers and Options. Available online: http://unepinquiry.org/wp-content/uploads/2016/09/6_Green_Bonds_Country_Experiences_Barriers_and_Options.pdf (accessed on 15 February 2020).

- Jurík, Lukáš, Natália Horňáková, Eva Šantavá, Dagmar Caganova, and Jozef Sablik. 2020. Application of AHP method for project selection in the context of sustainable development. Wireless Networks 8: 1–10. [Google Scholar] [CrossRef]

- Ketterer, Juan Antonio, Gabriela Andrade, Maria Netto, and Maria Isabel Haro. 2019. Transforming Green Bond Markets: Using Financial Innovation and Technology to Expand Green Bond Issuance in Latin America and the Caribbean. Inter-American Development Bank. Available online: https://publications.iadb.org/publications/english/document/Transforming_Green_Bond_Markets_Using_Financial_Innovation_and_Technology_to_Expand_Green_Bond_Issuance_in_Latin_America_and_the_Caribbean_en.pdf (accessed on 3 March 2020).

- Kil, Sung-Ho, Joongku Lee, Jun-Hyun Kim, Ming-Han Li, and Galen Newman. 2016. Utilizing the Analytic Hierarchy Process to Establish Weighted Values for Evaluating the Stability of Slope Revegetation based on Hydroseeding Applications in South Korea. Sustainability 8: 58. [Google Scholar] [CrossRef] [Green Version]

- Kwong, Chun-Kit, and Hao Bai. 2002. A fuzzy AHP approach to the determination of importance weights of customer requirements in quality function deployment. Journal of Intellingent Manufacturing 13: 367–77. [Google Scholar] [CrossRef]

- Lee, Deok Joo, and Jooho Hwang. 2010. Decision support for selecting exportable nuclear technology using the analytic hierarchy process: A Korean case. Energy Policy 38: 161–67. [Google Scholar] [CrossRef]

- Lin, Ming-Ian, Yuan-Duen Lee, and Tsai-Neng Ho. 2011. Applying integrated DEA/AHP to evaluate the economic performance of local governments in China. European Journal of Operational Research 209: 129–40. [Google Scholar] [CrossRef]

- Longaray, André Andrade, João De Deus Rodrigues Gois, and Paulo Roberto Da Silva Munhoz. 2015. Proposal for using AHP method to evaluate the quality of services provided by outsourced companies. Procedia Computer Science 55: 715–24. [Google Scholar] [CrossRef] [Green Version]

- Lotti, Raoni, and Mauro Caetano. 2018. The airport choice of exporters for fruit from Brazil. Journal of Air Transport Management 70: 104–12. [Google Scholar] [CrossRef]

- Macchiarelli, Corrado. 2014. Bond Market Co-Movements, Expected Inflation and the GBP-USD Equilibrium Real Exchange Rate. The Quarterly Review of Economics and Finance 54: 242–56. [Google Scholar] [CrossRef]

- Mahdiloo, Ali, Asghar Abolhasani, and Mohsen Rezaei. 2019. Ranking of economic sanctions and estimating hazard of sanctions index using fuzzy analytical hierarchy process. Quarterly Journal of Applied Theories of Economics 6: 47–72. [Google Scholar]

- Mahmudova, Shafagat Jabrail, and Zarifa Jabrailova. 2020. Development of an algorithm using the AHP method for selecting software according to its functionality. Soft Computing 24: 8495–502. [Google Scholar] [CrossRef]

- Maltais, Aaron, and Björn Nykvist. 2020. Understanding the role of green bonds in advancing sustainability. Journal of Sustainable Finance & Investment 2: 1–20. [Google Scholar] [CrossRef] [Green Version]

- Mandić, Ksenija, Boris Delibašić, Snežana Knežević, and Sladjana Benković. 2017. Analysis of the efficiency of insurance companies in Serbia using the fuzzy AHP and TOPSIS methods. Economic Research 30: 550–65. [Google Scholar]

- Marcarelli, Gabriella, Biagio Simonetti, and Viviana Ventre. 2013. Analyzing AHP matrix by Robust Regression. In Advanced Dynamic Modeling of Economic and Social Systems. Springer: Berlin/Heidelberg, Germany, vol. 448. [Google Scholar]

- Mawapanga, Mwana N., and David L. Debertin. 1996. Choosing between alternative farming systems: An application of the analytic hierarchy process. Review of Agricultural Economics 18: 385–401. [Google Scholar] [CrossRef]

- McGee, Christopher Dylan. 2007. Sovereign bond markets with political risk and moral hazard. International Review of Economics & Finance 16: 186–201. [Google Scholar]

- Mohsin, Muhammad, Farhad Taghizadeh-Hesary, Nisit Panthamit, Saba Anwar, Qaiser Abbas, and Xuan Vinh Vo. 2020. Developing Low Carbon Finance Index: Evidence from Developed and Developing Economies. Finance Research Letters 5: 101520. [Google Scholar] [CrossRef]

- Nguyen, Hong-Trang, and Matthew Gray. 2016. A Review on Green Building in Vietnam. Procedia Engineering 142: 314–21. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, Trong Co, Anh Tu Chuc, and Le Ngoc Dang. 2019. Green finance in Vietnam: Barriers and solutions. In Handbook of Green Finance: Energy Security and Sustainable Development. Edited by Jeffrey Sachs, Wing Thye Woo, Naoyuki Yoshino and Farhad Taghizadeh-Hesary. Tokyo: Springer. [Google Scholar]

- Nishat, Mohammed, and Yasumasa Matsuda. 2016. Analysis of the Government Bond Market and Monetary Policy. International Growth Center. Available online: https://www.theigc.org/project/analysis-of-the-government-bond-market-and-monetary-policy/ (accessed on 15 February 2020).

- Ortiz-Barrios, Miguel Angel, Carlos Miranda-De La Hoz, Pedro López-Meza, Antonella Petrillo, and Fabio De Felice. 2019. A case of food supply chain management with AHP, DEMATEL, and TOPSIS. Journal of Multi-Criteria Decision Analysis 27: 104–28. [Google Scholar] [CrossRef]

- Oztaysi, Basar. 2014. A decision model for information technology selection using AHP integrated TOPSIS-Grey: The case of content management systems. Knoweldge-Based Systems 70: 44–54. [Google Scholar] [CrossRef]

- Partridge, Candace, and Francesca Romana Medda. 2020. The evolution of pricing performance of green municipal bonds. Journal of Sustainable Finance and Investment 10: 44–64. [Google Scholar] [CrossRef]

- Perry, Robert L., and John D. Robertson. 1998. Political Markets, Bond Markets, and the Effects of Uncertainty: A Cross-National Analysis. International Studies Quarterly 42: 131–59. [Google Scholar] [CrossRef]

- Peterson, David L., David G. Silsbee, and Daniel L. Schmoldt. 1994. A case study of resources management planning with multiple objectives and projects. Environmental Management 18: 729–42. [Google Scholar] [CrossRef]

- Pham, Linh, and Toan Luu Duc Huynh. 2020. How does investor attention influence the green bond market? Finance Research Letters 5: 101533. [Google Scholar] [CrossRef]

- Podvezko, Valentinas. 2009. Application of AHP technique. Journal of Business Economics and Management 10: 181–89. [Google Scholar] [CrossRef] [Green Version]

- Rasolinezhad, Ehsan. 2009. Evaluating electronic banking systems in developing nations through Analytic Hierarchy Process model: A case study. International Journal of Electronic Finance 3: 325–38. [Google Scholar] [CrossRef]

- Reboredo, Juan C., and Andrea Ugolini. 2019. Price connectedness between green bond and financial markets. Economic Modelling 88: 25–38. [Google Scholar] [CrossRef]

- Ren, Xiangju, and Qi Ding. 2019. The effect of high-speed rail on regional economy in China using AHP. International Journal of Transportation Engineering 5: 111–17. [Google Scholar]

- Roh, SeungKook, Jae Young Choi, and Soon Heung Chang. 2019. Modeling of nuclear power plant export competitiveness and its implications: The case of Korea. Energy 166: 157–69. [Google Scholar] [CrossRef]

- Russo, Rosaria, and Roberto Camanho. 2015. Criteria in AHP: A Systematic Review of Literature. Procedia Computer Science 55: 1123–32. [Google Scholar] [CrossRef] [Green Version]

- Saaty, Thomas L. 1987. A new macroeconomic forecasting and policy evaluation method using the Analytic Hierarchy Process. Mathematical Modelling 9: 219–31. [Google Scholar] [CrossRef] [Green Version]

- Sabov, Z., and A. Murphy. 1999. The Relationship between Bond Returns and Inflation in a Controlled Economy. Economics of Planning 32: 89–102. [Google Scholar] [CrossRef]

- Sadeghi, Mehdi, and Ahmad Ameli. 2012. An AHP decision making model for optimal allocation of energy subsidy among socio-economic subsectors in Iran. Energy Policy 45: 24–32. [Google Scholar] [CrossRef]

- Sartzetakis, Eftichios S. 2020. Green bonds as an instrument to finance low carbon transition. Economic Change and Restructuring 2: 1–25. [Google Scholar] [CrossRef]

- Schultz, Paul. 2012. The market for new issues of municipal bonds: The roles of transparency and limited access to retail investors. Journal of Financial Economics 106: 492–512. [Google Scholar] [CrossRef]

- Sharma, Jitendra. 2018. Economics of decision making: Exploring Analytical Hierarchical Process. Theoretical Economics Letters 8: 3141–56. [Google Scholar] [CrossRef] [Green Version]

- Shishlov, Igor, and Romain Morel. 2016. Beyond Transparency: Unlocking the Full Potential of Green Bonds. Available online: https://www.cbd.int/financial/greenbonds/i4ce-greenbond2016.pdf (accessed on 15 February 2020).

- Sun, Yu, Lizhen Chen, Huaping Sun, and Farhad Taghizadeh-Hesary. 2020. Low-carbon financial risk factor correlation in the belt and road PPP project. Finance Research Letters 3: 101491. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, Farhad, and Naoyuki Yoshino. 2019. The way to induce private participation in green finance and investment. Finance Research Letters 31: 98–103. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, Farhad, and Naoyuki Yoshino. 2020. Sustainable Solutions for Green Financing and Investment in Renewable Energy Projects. Energies 13: 788. [Google Scholar] [CrossRef] [Green Version]

- Tang, Dragon Yongjun, and Yupu Zhang. 2018. Do shareholders benefit from green bonds? Journal of Corporate Finance 61: 101427. [Google Scholar] [CrossRef]

- Tolliver, Clarence, Alexander Ryota Keeley, and Shunsuke Managi. 2020. Drivers of green bond market growth: The importance of Nationally Determined Contributions to the Paris Agreement and implications for sustainability. Journal of Cleaner Production 244: 118643. [Google Scholar] [CrossRef]

- Tsyganok, Vitaliy, Sergii Kadenko, and Oleh Andriichuk. 2012. Significance of expert competence consideration in group decision making using AHP. International Journal of Production Research 50: 4785–92. [Google Scholar] [CrossRef]

- Tu, Chuc Anh, Ehsan Rasoulinezhad, and Tapan Sarker. 2020. Investigating solutions for the development of a green bond market: Evidence from analytic hierarchy process. Finance Research Letters 2: 101457. [Google Scholar] [CrossRef]

- Voica, Marian Catalin, Mirela Panait, and Irina Radulescu. 2015. Green Investments—Between Necessity, Fiscal Constraints and Profit. Procedia Economics and Finance 22: 72–79. [Google Scholar] [CrossRef] [Green Version]

- Wang, Yao, and Qiang Zhi. 2016. The role of green finance in environmental protection: Two aspects of market mechanism and policies. Energy Procedia 104: 311–16. [Google Scholar] [CrossRef]

- Wang, Ying-Ming, Celik Parkan, and Ying Luo. 2007. Priority estimation in the AHP through maximization of correlation coefficient. Applied Mathematical Modelling 31: 2711–18. [Google Scholar] [CrossRef]

- Wang, Qinghua, Yaning Zhou, Li Luo, and Junping Ji. 2019. Research on the Factors Affecting the Risk Premium of China’s Green Bond Issuance. Sustainability 11: 6394. [Google Scholar] [CrossRef] [Green Version]

- Wang, Jiazhen, Xin Chen, Xiaoxia Li, Jing Yu, and Rui Zhong. 2020. The market reaction to green bond issuance: Evidence from China. Pacific-Basin Finance Journal 60: 101294. [Google Scholar] [CrossRef]

- World Bank. 2019. 10 Years of Green Bonds: Creating the Blueprint for Sustainability Across Capital Markets. Washington, DC: World Bank. [Google Scholar]

- Zerbib, Oliver David. 2018. Is There a Green Bond Premium? The Yield Differential between Green and Conventional Bonds. CEP Working Paper. Available online: https://www.cepweb.org/ (accessed on 15 February 2020).

- Zerbib, Olivier David. 2019. The effect of pro-environmental preferences on bond prices: Evidence from green bonds. Journal of Banking & Finance 98: 39–60. [Google Scholar]

- Zhou, Xiaoguang, and Yadi Cui. 2019. Green Bonds, Corporate Performance, and Corporate Social Responsibility. Sustainability 11: 6881. [Google Scholar] [CrossRef] [Green Version]

Figure 1.

Overall weights of sub-criteria with respect to the goal. Note: consistency index is 0.01. Source: Export Choice output. GB, green bond.

Figure 1.

Overall weights of sub-criteria with respect to the goal. Note: consistency index is 0.01. Source: Export Choice output. GB, green bond.

{kind=link}

Table 1.

Green bonds issued by different regions from 2012 to 2018.

| Geographical Regions | Number of Countries | Number of Green Bonds Issuers | Volume ($ Billion) |

|---|---|---|---|

| Africa | 4 | 8 | 1.5 |

| East Asia and Pacific | 7 | 160 | 112.3 |

| Europe and Central Asia | 5 | 9 | 3.2 |

| Latin America and the Caribbean | 8 | 32 | 14.1 |

| Middle East and North Africa | 3 | 6 | 1.0 |

| South Asia | 1 | 20 | 7.7 |

| Total | 28 | 235 | 139.7 |

Source: authors’ compilation from the International Finance Cooperation (IFC).

Table 2.

Characteristics of panel of experts.

| Characteristics | Items | % |

|---|---|---|

| Gender | Male | 70 |

| Female | 30 | |

| Age | 30–40 | 20 |

| 41–50 | 70 | |

| 51 years + | 10 | |

| Position | Financial director | 20 |

| Senior manager | 30 | |

| Researcher/analyst | 50 | |

| Education | PhD | 80 |

| MSc/MBA | 20 |

Source: authors’ compilation from SPSS software 10.

Table 3.

Network structure of our model. GB, green bond.

| Objective of Decision Making | Criterion | Factors |

|---|---|---|

| Green bond market expansion in Vietnam | A: Financial | A1: General level of prices A2: GB interest rate A3: Official exchange rate A4: Investment risk A5: Monetary policy A6: Tax incentives A7: Financial openness |

| B: Economic and Political | B1: Political stability B2: Economic stability B3: Market-based economic system B4: State support B5: Business climate B6: Balance of state budget B7: CO2 emissions level | |

| C: Social | C1: Social support C2: Social–environmental linkage C3: Urbanization growth C4: Unemployment C5: Income inequality | |

| D: Infrastructural | D1: Legal framework D2: Limited application to international standard D3: Institutional infrastructure D4: International cooperation in GB |

Source: authors’ compilation from expert opinions.

Table 4.

Compare the relative importance with respect to the goal: GB market development.

| Criterion | A: Financial | B: Economic and Political | C: Social | D: Infrastructural | Priorities |

|---|---|---|---|---|---|

| A: Financial | 3.0 | 2.0 | 1.0 | 0.363 | |

| B: Economic and Political | 2.0 | −2.0 | 0.179 | ||

| C: Social | −2.0 | 0.138 | |||

| D: Infrastructural | 0.320 |

Note: inconsistency rate is 0.03. Source: authors’ compilation from Expert Choice 10.

Table 5.

Compare the relative importance with respect to financial criterion (A).

| Factor | A1 | A2 | A3 | A4 | A5 | A6 | A7 | Priorities |

|---|---|---|---|---|---|---|---|---|

| A1 | 2 | 1 | 2 | 2 | −2 | 1 | 0.062 | |

| A2 | 2 | 2 | −3 | 2 | 1 | 0.056 | ||

| A3 | 3 | 1 | 1 | 2 | 0.056 | |||

| A4 | 1 | −2 | −2 | 0.028 | ||||

| A5 | 1 | 2 | 0.063 | |||||

| A6 | 1 | 0.055 | ||||||

| A7 | 0.043 |

Note: inconsistency rate is 0.01. Source: authors’ compilation from Expert Choice 10.

Table 6.

Compare the relative importance with respect to economic and political criterion (B).

| Factor | B1 | B2 | B3 | B4 | B5 | B6 | B7 | Priorities |

|---|---|---|---|---|---|---|---|---|

| B1 | 3 | 3 | 1 | 2 | 2 | 3 | 0.046 | |

| B2 | 2 | 1 | −2 | 1 | 2 | 0.023 | ||

| B3 | 1 | 1 | 2 | 1 | 0.021 | |||

| B4 | 1 | 1 | 2 | 0.026 | ||||

| B5 | −2 | 1 | 0.023 | |||||

| B6 | 1 | 0.022 | ||||||

| B7 | 0.017 |

Note: inconsistency rate is 0.06. Source: authors’ compilation from Expert Choice 10.

Table 7.

Compare the relative importance with respect to social criterion (C).

| Factor | C1 | C2 | C3 | C4 | C5 | Priorities |

|---|---|---|---|---|---|---|

| C1 | 3 | 3 | 2 | 1 | 0.045 | |

| C2 | −2 | 1 | 1 | 0.019 | ||

| C3 | −2 | −2 | 0.019 | |||

| C4 | 1 | 0.026 | ||||

| C5 | 0.030 |

Note: inconsistency rate is 0.06. Source: authors’ compilation from Expert Choice 10.

Table 8.

Compare the relative importance with respect to infrastructural criterion (D).

| Factor | D1 | D2 | D3 | D4 | Priorities |

|---|---|---|---|---|---|

| D1 | 2 | 1 | 1 | 0.090 | |

| D2 | −2 | 1 | 0.052 | ||

| D3 | 3 | 0.119 | |||

| D4 | 0.058 |

Note: inconsistency rate is 0.04. Source: authors’ compilation from Expert Choice 10.

Table 9.

Robustness check (robust partial least squares (R-PLS) regression).

| Rank | Factor | R-PLS Weight | Rank | Factor | R-PLS Weight |

|---|---|---|---|---|---|

| 1 | D3 | 0.639 | 14 | C5 | 0.163 |

| 2 | D1 | 0.611 | 15 | B4 | 0.152 |

| 3 | A5 | 0.419 | 16 | A4 | 0.150 |

| 4 | A1 | 0.403 | 17 | B3 | 0.132 |

| 5 | D4 | 0.382 | 18 | B2 | 0.127 |

| 6 | A6 | 0.359 | 19 | B5 | 0.110 |

| 7 | D2 | 0.329 | 20 | B6 | 0.103 |

| 8 | A3 | 0.218 | 21 | C2 | 0.093 |

| 9 | A2 | 0.210 | 22 | C3 | 0.042 |

| 10 | A6 | 0.202 | 23 | B7 | 0.020 |

| 11 | B1 | 0.193 | |||

| 12 | C1 | 0.178 | |||

| 13 | A7 | 0.172 |

Source: authors’ compilation from Software R.

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Anh Tu, C.; Sarker, T.; Rasoulinezhad, E. Factors Influencing the Green Bond Market Expansion: Evidence from a Multi-Dimensional Analysis. J. Risk Financial Manag. 2020, 13, 126. https://doi.org/10.3390/jrfm13060126

AMA Style

Anh Tu C, Sarker T, Rasoulinezhad E. Factors Influencing the Green Bond Market Expansion: Evidence from a Multi-Dimensional Analysis. Journal of Risk and Financial Management. 2020; 13(6):126. https://doi.org/10.3390/jrfm13060126

Chicago/Turabian StyleAnh Tu, Chuc, Tapan Sarker, and Ehsan Rasoulinezhad. 2020. "Factors Influencing the Green Bond Market Expansion: Evidence from a Multi-Dimensional Analysis" Journal of Risk and Financial Management 13, no. 6: 126. https://doi.org/10.3390/jrfm13060126