Bank Competition and Credit Risk in Euro Area Banking: Fragmentation and Convergence Dynamics

Abstract

1. Introduction

2. Evolution of Competitive Conditions in EU Banking

2.1. Before the Introduction of the Euro

2.2. Around the Introduction of the Euro

2.3. After the Introduction of the Euro

3. Bank Competition in the Euro Area

3.1. Measuring Bank Competition through Market Power

3.2. Calculation of a Lerner Index Using a Stochastic Frontier Methodology

3.3. Evolution of the Lerner Index of Bank Market Power

4. Bank Concentration in the Euro Area

4.1. The Evolution of the Herfindahl–Hirschman Index (HHI)

4.2. The Evolution of the CR5 Concentration Ratio

5. Credit Risk in the Euro Area

6. Theil Inequality for Bank Competition, Concentration, and Credit Risk

6.1. Theil Inequality Index

6.2. Theil Inequality for Market Power

6.3. Theil Inequality for Concentration

6.4. Theil Inequality for Credit Risk (NPL Ratio)

7. Convergence Analysis

8. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Al-Eyd, Ali, and Pelin Berkmen. 2013. Fragmentation and Monetary Policy in the Euro Area. Working Paper No. 13/208. Washington, DC, USA: International Monetary Fund. [Google Scholar]

- Anastasiou, Dimitrios, Helen Louri, and Mike Tsionas. 2019. Non-Performing Loans in the Euro-area: Are Core-Periphery Banking Markets Fragmented? International Journal of Finance and Economics 24: 97–112. [Google Scholar] [CrossRef]

- Angelini, Paolo, and Nicola Cetorelli. 2003. The Effects of Regulatory Reform on Competition in the Banking Industry. Journal of Money, Credit and Banking 35: 663–84. [Google Scholar] [CrossRef]

- Apergis, Nicholas, Irene Fafaliou, and Michael L. Polemis. 2016. New evidence on assessing the level of competition in the European Union banking sector: A panel data approach. International Business Review 25: 395–407. [Google Scholar] [CrossRef]

- Baele, Lieven, Annalisa Ferrando, Peter Hördahl, Elizaveta Krylova, and Cyril Monnet. 2004. Measuring Financial Integration in the Euro Area. Occasional Paper No. 14. Frankfurt: European Central Bank. [Google Scholar]

- Barro, Robert J., and Xavier Sala-i-Martin. 1991. Convergence across states and regions. Brookings Papers on Economic Activity 1: 107–82. [Google Scholar] [CrossRef]

- Berenberg-Gossler, Paul, and Henrik Enderlein. 2016. Financial Market Fragmentation in the Euro Area: State of Play. Policy Paper No. 177. Berlin: Jacques Delors Institut. [Google Scholar]

- Bikker, Jacob A., and Katharina Haaf. 2002. Competition, concentration and their relationship: An empirical analysis of the banking industry. Journal of Banking and Finance 26: 2191–214. [Google Scholar] [CrossRef]

- Bikker, Jacob A., and Laura Spierdijk. 2008. How Banking Competition Changed over Time. Working Paper No. 167. Amsterdam, The Netherlands: De Netherlandsche Bank. [Google Scholar]

- Boone, Jan. 2008. A new way to measure competition. Economic Journal 118: 1245–61. [Google Scholar] [CrossRef]

- Casu, Barbara, and Claudia Girardone. 2009. Competition issues in European banking. Journal of Financial Regulation and Compliance 17: 119–33. [Google Scholar] [CrossRef]

- Claessens, Stijn. 2019. Fragmentation in Global Financial Markets: Good or Bad for Financial Stability? BIS Working Papers No. 815. Basel, Switzerland: Bank for International Settlements. [Google Scholar]

- Coccorese, Paolo. 2004. Banking competition and macroeconomic conditions: A disaggregate Analysis. Journal of International Financial Markets, Institutions and Money 14: 203–19. [Google Scholar] [CrossRef]

- Cruz-Garcia, Paula, Juan Fernandez de Guevara, and Joaquin Maudos. 2017. The evolution of market power in European banking. Finance Research Letters 23: 257–62. [Google Scholar] [CrossRef]

- De Bandt, Olivier, and E. Philip Davis. 2000. Competition, contestability and market structure in European banking sectors on the eve of EMU. Journal of Banking and Finance 24: 1045–66. [Google Scholar] [CrossRef]

- De Sola Perea, Maite, and Christophe Van Nieuwenhuyze. 2014. Financial integration and fragmentation in the euro area. Economic Review, 99-125, June. Brussels: National Bank of Belgium. [Google Scholar]

- ECB. 2003. The Integration of Europe’s Financial Markets. European Central Bank Monthly Bulletin. Frankfurt: European Central Bank. [Google Scholar]

- ECB. 2016. Report on Financial Structures. Frankfurt: European Central Bank. [Google Scholar]

- ECB. 2018. Financial integration in Europe. Frankfurt: European Central Bank. [Google Scholar]

- ECB. 2019a. Statistical Data Warehouse: Balance Sheet Items Statistics. Available online: https://sdw.ecb.europa.eu/browse.do?node=1491 (accessed on 3 September 2019).

- ECB. 2019b. Statistical Data Warehouse: Banking Structural Financial Indicators Statistics. Available online: https://sdw.ecb.europa.eu/browseSelection.do?node=9689719 (accessed on 3 September 2019).

- ECB. 2020. Supervisory Banking Statistics—Third Quarter 2019. Frankfurt: European Central Bank. [Google Scholar]

- Fernandez de Guevara, Juan, Joaquin Maudos, and Francisco Perez. 2007. Integration and competition in the European financial markets. Journal of International Money and Finance 26: 26–45. [Google Scholar] [CrossRef]

- FSB. 2019. FSB Report on Market Fragmentation. Basel: Financial Stability Board. [Google Scholar]

- Gischer, Horst, and Mike Stiele. 2008. Competition Tests with a Non-Structural Model: The Panzar–Rosse Method Applied to Germany’s Savings Banks. German Economic Review 10: 50–70. [Google Scholar] [CrossRef]

- Goddard, John, Hong Liu, Phil Molyneux, and John O. S. Wilson. 2013. Do Bank Profits Converge? European Financial Management 19: 345–65. [Google Scholar] [CrossRef]

- Hondroyiannis, George, Sarantis Lolos, and Evangelia Papapetrou. 1999. Assessing competitive conditions in the Greek banking system. Journal of International Financial Markets, Institutions and Money 9: 377–91. [Google Scholar] [CrossRef]

- Jondrow, James, C. A. Knox Lovell, Ivan S. Materov, and Peter Schmidt. 1982. On the estimation of technical inefficiency in the stochastic frontier production function model. Journal of Econometrics 19: 233–38. [Google Scholar] [CrossRef]

- Karadima, Maria, and Helen Louri. 2019. Non-Performing Loans in the Euro Area: Does Market Power Matter? Working Paper No. 271. Athens, Greece: Bank of Greece. [Google Scholar]

- Kumbhakar, Subal C., Sjur Baardsen, and Gudbrand Lien. 2012. A new method for estimating market power with an application to Norwegian sawmilling. Review of Industrial Organization 40: 109–29. [Google Scholar] [CrossRef]

- Lapteacru, Ion. 2018. Convergence of bank competition in Central and Eastern European countries: do foreign and domestic banks go hand in hand? Post-Communist Economies 30: 588–616. [Google Scholar] [CrossRef]

- Lerner, Abba P. 1934. The concept of monopoly and the measurement of monopoly power. Review of Economic Studies 1: 157–75. [Google Scholar] [CrossRef]

- Louri, Helen, and Petros Migiakis. 2019. Bank lending margins in the euro area: Funding conditions, fragmentation and ECB’s policies. Review of Financial Economics 37: 482–505. [Google Scholar] [CrossRef]

- Lucotte, Yannick. 2015. Euro area banking fragmentation in the aftermath of the crisis: A cluster analysis. Applied Economics Letters 22: 1046–50. [Google Scholar] [CrossRef]

- Magnus, Marcel, Alienor Margerit, Benoit Mesnard, and Christina Katopodi. 2017. Non-Performing Loans in the Banking Union—Stocktaking and Challenges. European Parliament Briefing, 13 July. Brussels: European Parliament. [Google Scholar]

- Maudos, Joaquin, and Xavier Vives. 2019. Competition Policy in Banking in the European Union. Review of Industrial Organization 55: 27–54. [Google Scholar] [CrossRef]

- Moch, Nils. 2013. Competition in fragmented markets: New evidence from the German banking industry in the light of the subprime crisis. Journal of Banking and Finance 37: 2908–19. [Google Scholar] [CrossRef]

- Panzar, John C., and James N. Rosse. 1987. Testing for “monopoly” equilibrium. Journal of Industrial Economics 35: 443–56. [Google Scholar] [CrossRef]

- Phillips, Peter, and Donggyu Sul. 2007. Transition modeling and econometric convergence tests. Econometrica 75: 1771–855. [Google Scholar] [CrossRef]

- Staikouras, Christos K., and Anastasia Koutsomanoli-Filippaki. 2006. Competition and Concentration in the New European Banking Landscape. European Financial Management 12: 443–82. [Google Scholar] [CrossRef]

- Sun, Yu. 2009. Recent Developments in European Bank Competition. Working Paper No. 11/146. Washington, DC, USA: International Monetary Fund. [Google Scholar]

- Weill, Laurent. 2013. Bank competition in the EU: How has it evolved? Journal of International Financial Markets, Institutions and Money 26: 100–12. [Google Scholar] [CrossRef]

- World Bank. 2019a. World Development Indicators Database. Available online: https://databank.worldbank.org/source/world-development-indicators (accessed on 28 October 2019).

- World Bank. 2019b. Global Financial Development Database. Available online: https://datacatalog.orldbank.org/dataset/global-financial-development (accessed on 28 October 2019).

| 1 | While Italy should in principle be considered as a core country since it has been one of the EU founding members, it is classified in this study as a periphery country because of its high levels of NPLs during the crisis. A classification of Italy as a periphery country has also been made in other studies (see Al-Eyd and Berkmen 2013; Anastasiou et al. 2019; Louri and Migiakis 2019). |

| 2 | In the case of competition, for example, β-convergence would apply if countries with lower levels of competition were found to tend to catch up with countries characterized by higher levels of competition, while σ-convergence would apply if the dispersion of competition levels across countries showed a tendency to decline over time. |

| 3 | Ιn this study, we preferred the weighted euro area averages to unweighted ones, because it is only the weighted averages that can take into account the large differences between euro area countries with regard to total banking assets. |

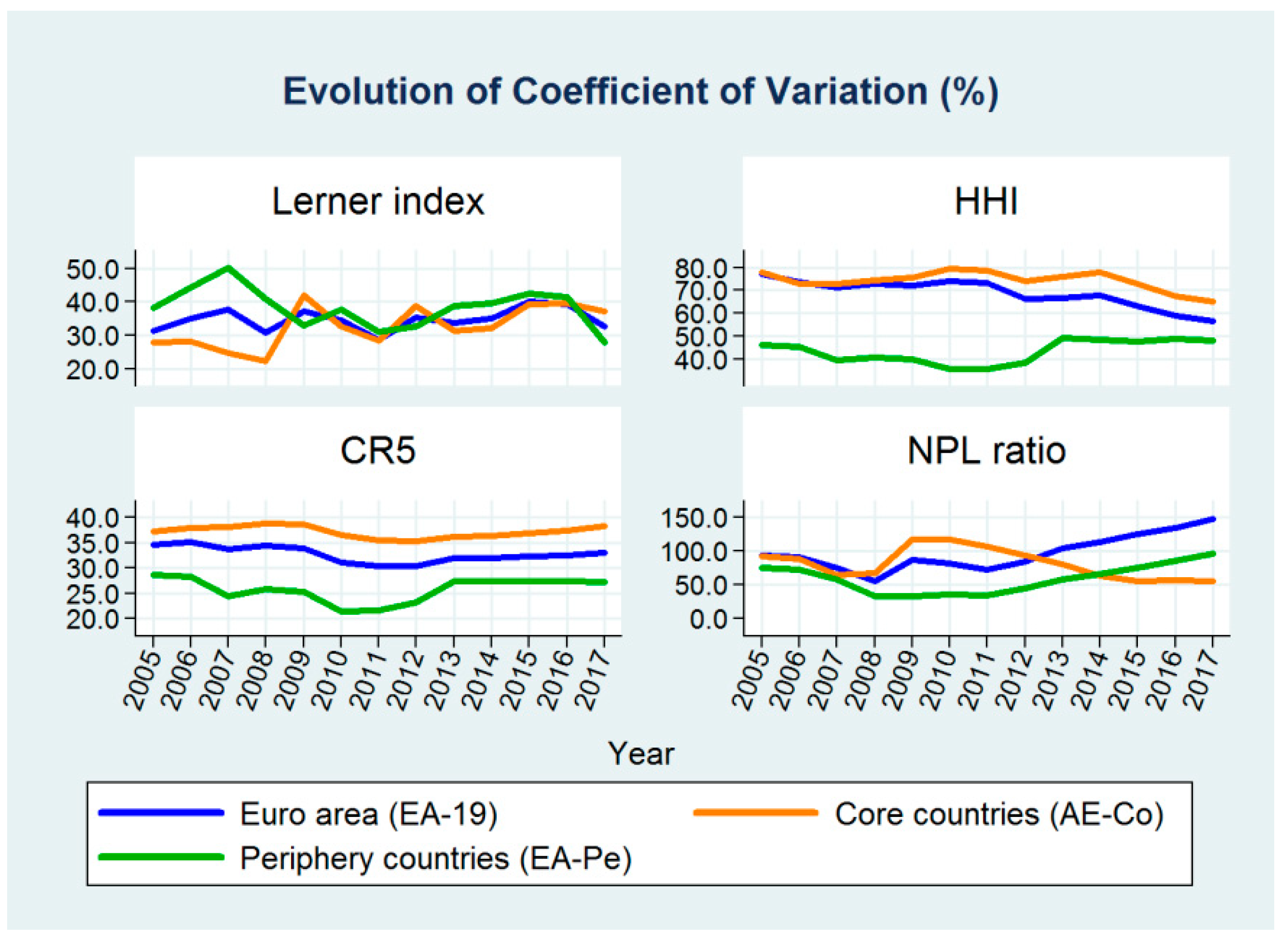

| 4 | The coefficient of variation is defined as the ratio of the standard deviation to the mean. It shows the degree of variability in relation to the mean. |

| 5 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Total Change | Coeff. Var (%) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Euro Area Core Countries (EA-Co) | |||||||||||||||

| Austria | 0.142 | 0.112 | 0.096 | 0.096 | 0.117 | 0.128 | 0.125 | 0.116 | 0.139 | 0.133 | 0.150 | 0.136 | 0.189 | 0.047 | 18.9 |

| Belgium | 0.194 | 0.213 | 0.129 | 0.099 | 0.113 | 0.159 | 0.153 | 0.112 | 0.135 | 0.123 | 0.170 | 0.146 | 0.147 | −0.047 | 22.6 |

| Estonia | 0.107 | 0.133 | 0.201 | 0.110 | 0.046 | 0.090 | 0.114 | 0.137 | 0.223 | 0.167 | 0.205 | 0.240 | 0.242 | 0.135 | 40.4 |

| Finland | 0.129 | 0.165 | 0.135 | 0.124 | 0.225 | 0.255 | 0.220 | 0.257 | 0.199 | 0.209 | 0.285 | 0.321 | 0.174 | 0.045 | 29.7 |

| France | 0.185 | 0.177 | 0.119 | 0.100 | 0.190 | 0.154 | 0.138 | 0.168 | 0.162 | 0.137 | 0.178 | 0.200 | 0.141 | −0.044 | 18.7 |

| Germany | 0.111 | 0.085 | 0.085 | 0.071 | 0.100 | 0.113 | 0.131 | 0.128 | 0.121 | 0.118 | 0.115 | 0.108 | 0.108 | −0.003 | 16.5 |

| Latvia | 0.211 | 0.182 | 0.166 | 0.158 | 0.183 | 0.163 | 0.165 | 0.196 | 0.218 | 0.215 | 0.232 | 0.243 | 0.185 | −0.026 | 14.4 |

| Lithuania | 0.164 | 0.162 | 0.128 | 0.097 | 0.121 | 0.118 | 0.071 | 0.108 | 0.137 | 0.178 | 0.112 | 0.193 | 0.186 | 0.022 | 27.3 |

| Luxembourg | 0.160 | 0.175 | 0.143 | 0.145 | 0.245 | 0.250 | 0.215 | 0.260 | 0.296 | 0.298 | 0.329 | 0.287 | 0.253 | 0.093 | 26.5 |

| Netherlands | 0.084 | 0.088 | 0.121 | 0.100 | 0.101 | 0.166 | 0.153 | 0.091 | 0.153 | 0.155 | 0.108 | 0.071 | 0.068 | −0.016 | 30.3 |

| Slovakia | 0.116 | 0.126 | 0.109 | 0.105 | 0.137 | 0.157 | 0.168 | 0.118 | 0.126 | 0.128 | 0.146 | 0.174 | 0.080 | −0.036 | 20.3 |

| Coeff. Var (%) | 27.8 | 28.0 | 24.7 | 22.3 | 41.9 | 32.7 | 28.5 | 38.7 | 31.4 | 32.0 | 39.3 | 39.5 | 37.1 | ||

| EA-Co average | 0.140 | 0.130 | 0.107 | 0.091 | 0.142 | 0.144 | 0.142 | 0.145 | 0.149 | 0.139 | 0.154 | 0.153 | 0.128 | −0.012 | 13.4 |

| Euro Area Periphery Countries (EA-Pe) | |||||||||||||||

| Cyprus | 0.102 | 0.236 | 0.233 | 0.103 | 0.146 | 0.167 | 0.103 | 0.154 | 0.184 | 0.295 | 0.331 | 0.318 | 0.216 | 0.114 | 40.4 |

| Greece | 0.159 | 0.127 | 0.086 | 0.085 | 0.091 | 0.075 | 0.101 | 0.119 | 0.056 | 0.067 | 0.080 | 0.111 | 0.128 | −0.031 | 29.2 |

| Ireland | 0.036 | 0.016 | 0.016 | 0.068 | 0.153 | 0.224 | 0.209 | 0.140 | 0.217 | 0.224 | 0.285 | 0.141 | 0.194 | 0.158 | 60.1 |

| Italy | 0.142 | 0.138 | 0.109 | 0.098 | 0.110 | 0.117 | 0.109 | 0.129 | 0.126 | 0.145 | 0.142 | 0.103 | 0.138 | −0.004 | 13.5 |

| Malta | 0.178 | 0.192 | 0.215 | 0.209 | 0.217 | 0.196 | 0.161 | 0.237 | 0.219 | 0.224 | 0.212 | 0.251 | 0.166 | −0.012 | 12.9 |

| Portugal | 0.163 | 0.193 | 0.147 | 0.128 | 0.154 | 0.179 | 0.118 | 0.109 | 0.088 | 0.130 | 0.192 | 0.159 | 0.233 | 0.070 | 25.9 |

| Slovenia | 0.120 | 0.128 | 0.142 | 0.074 | 0.121 | 0.158 | 0.145 | 0.172 | 0.156 | 0.154 | 0.122 | 0.145 | 0.106 | −0.014 | 19.4 |

| Spain | 0.207 | 0.202 | 0.181 | 0.143 | 0.237 | 0.295 | 0.207 | 0.251 | 0.187 | 0.240 | 0.264 | 0.202 | 0.231 | 0.024 | 18.1 |

| Coeff. Var (%) | 38.1 | 44.4 | 50.3 | 40.8 | 32.9 | 37.7 | 30.9 | 32.5 | 38.7 | 39.7 | 42.5 | 41.5 | 27.9 | ||

| EA-Pe average | 0.150 | 0.144 | 0.122 | 0.111 | 0.163 | 0.196 | 0.155 | 0.174 | 0.151 | 0.181 | 0.196 | 0.145 | 0.179 | 0.030 | 16.4 |

| All Euro Area Countries (EA-19) | |||||||||||||||

| Coeff. Var (%) | 31.4 | 35.1 | 37.6 | 30.7 | 37.2 | 34.5 | 28.7 | 35.2 | 33.8 | 35.0 | 40.0 | 39.3 | 32.6 | ||

| EA-19 average | 0.143 | 0.134 | 0.112 | 0.097 | 0.149 | 0.160 | 0.146 | 0.154 | 0.150 | 0.151 | 0.166 | 0.151 | 0.142 | −0.001 | 13.3 |

| Country | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Total Change | Coeff. Var (%) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Euro Area Core Countries (EA-Co) | |||||||||||||||

| Austria | 560 | 534 | 527 | 454 | 414 | 383 | 423 | 395 | 405 | 412 | 397 | 358 | 374 | −186 | 18.9 |

| Belgium | 2112 | 2041 | 2079 | 1881 | 1622 | 1439 | 1294 | 1061 | 979 | 981 | 998 | 1017 | 1102 | −1010 | 22.6 |

| Estonia | 4039 | 3593 | 3410 | 3120 | 3090 | 2929 | 2613 | 2493 | 2483 | 2445 | 2409 | 2406 | 2419 | −1620 | 40.4 |

| Finland | 3130 | 3010 | 2970 | 3490 | 3480 | 3830 | 3880 | 3250 | 3410 | 3630 | 3160 | 2300 | 1700 | −1430 | 29.7 |

| France | 727 | 726 | 679 | 681 | 605 | 610 | 600 | 545 | 568 | 584 | 589 | 572 | 574 | −153 | 18.7 |

| Germany | 174 | 178 | 183 | 191 | 206 | 301 | 317 | 307 | 266 | 300 | 273 | 277 | 250 | 76 | 16.5 |

| Latvia | 1176 | 1270 | 1158 | 1205 | 1181 | 1005 | 929 | 1027 | 1037 | 1001 | 1033 | 1080 | 1235 | 59 | 14.4 |

| Lithuania | 1838 | 1913 | 1827 | 1714 | 1693 | 1545 | 1871 | 1749 | 1892 | 1818 | 1939 | 1938 | 2189 | 351 | 27.3 |

| Luxembourg | 373 | 333 | 316 | 309 | 310 | 343 | 346 | 345 | 357 | 330 | 321 | 260 | 256 | −117 | 26.5 |

| Netherlands | 1796 | 1822 | 1928 | 2167 | 2034 | 2049 | 2067 | 2026 | 2105 | 2131 | 2104 | 2097 | 2087 | 291 | 30.3 |

| Slovakia | 1076 | 1131 | 1082 | 1197 | 1273 | 1239 | 1268 | 1221 | 1215 | 1221 | 1250 | 1264 | 1332 | 256 | 20.3 |

| Coeff. Var (%) | 77.8 | 73.0 | 72.9 | 74.3 | 75.7 | 79.5 | 78.5 | 73.9 | 75.9 | 78.1 | 73.1 | 67.3 | 65.0 | ||

| EA-Co average | 711 | 714 | 733 | 757 | 713 | 742 | 767 | 713 | 705 | 746 | 724 | 695 | 663 | −48 | 3.8 |

| Euro Area Periphery Countries (EA-Pe) | |||||||||||||||

| Cyprus | 1029 | 1056 | 1089 | 1017 | 1085 | 1125 | 1030 | 1007 | 1645 | 1445 | 1443 | 1366 | 1962 | 933 | 40.4 |

| Greece | 1096 | 1101 | 1096 | 1172 | 1183 | 1214 | 1278 | 1487 | 2136 | 2195 | 2254 | 2332 | 2307 | 1211 | 29.2 |

| Ireland | 600 | 600 | 700 | 661 | 714 | 700 | 645 | 630 | 671 | 673 | 672 | 636 | 658 | 58 | 60.1 |

| Italy | 230 | 220 | 328 | 307 | 298 | 410 | 407 | 410 | 406 | 424 | 435 | 452 | 519 | 289 | 13.5 |

| Malta | 1330 | 1171 | 1177 | 1236 | 1250 | 1181 | 1203 | 1313 | 1458 | 1648 | 1620 | 1602 | 1599 | 269 | 12.9 |

| Portugal | 1154 | 1134 | 1098 | 1114 | 1150 | 1207 | 1206 | 1191 | 1197 | 1164 | 1215 | 1181 | 1220 | 66 | 25.9 |

| Slovenia | 1369 | 1300 | 1282 | 1268 | 1256 | 1160 | 1142 | 1115 | 1045 | 1026 | 1077 | 1147 | 1133 | −236 | 19.4 |

| Spain | 487 | 442 | 459 | 497 | 507 | 528 | 596 | 654 | 719 | 839 | 896 | 937 | 965 | 478 | 18.1 |

| Coeff. Var (%) | 46.0 | 45.4 | 39.6 | 40.6 | 40.0 | 35.8 | 35.9 | 38.4 | 49.4 | 48.6 | 47.9 | 48.7 | 48.0 | ||

| EA-Pe average | 480 | 462 | 520 | 526 | 540 | 594 | 604 | 626 | 681 | 726 | 754 | 765 | 812 | 332 | 18.6 |

| All Euro Area Countries (EA-19) | |||||||||||||||

| Coeff. Var (%) | 77.2 | 73.5 | 71.3 | 72.8 | 72.2 | 74.1 | 73.2 | 66.5 | 66.6 | 67.9 | 63.4 | 58.9 | 56.6 | ||

| EA-19 average | 647 | 640 | 669 | 685 | 657 | 696 | 717 | 686 | 698 | 740 | 733 | 714 | 703 | 56 | 4.5 |

| Country | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Total Change | Coeff. Var (%) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Euro Area Core Countries (EA-Co) | |||||||||||||||

| Austria | 0.450 | 0.438 | 0.428 | 0.390 | 0.372 | 0.359 | 0.384 | 0.365 | 0.367 | 0.368 | 0.358 | 0.345 | 0.361 | −0.089 | 8.8 |

| Belgium | 0.853 | 0.844 | 0.834 | 0.808 | 0.771 | 0.749 | 0.708 | 0.663 | 0.640 | 0.658 | 0.655 | 0.662 | 0.688 | −0.165 | 10.9 |

| Estonia | 0.981 | 0.971 | 0.957 | 0.948 | 0.934 | 0.923 | 0.906 | 0.896 | 0.897 | 0.899 | 0.886 | 0.880 | 0.903 | −0.078 | 3.6 |

| Finland | 0.871 | 0.868 | 0.861 | 0.877 | 0.875 | 0.892 | 0.869 | 0.859 | 0.871 | 0.897 | 0.880 | 0.805 | 0.735 | −0.136 | 5.0 |

| France | 0.519 | 0.523 | 0.518 | 0.512 | 0.472 | 0.474 | 0.483 | 0.446 | 0.467 | 0.476 | 0.472 | 0.460 | 0.454 | −0.065 | 5.5 |

| Germany | 0.216 | 0.220 | 0.220 | 0.227 | 0.250 | 0.326 | 0.335 | 0.330 | 0.306 | 0.321 | 0.306 | 0.314 | 0.297 | 0.081 | 16.8 |

| Latvia | 0.673 | 0.692 | 0.672 | 0.702 | 0.693 | 0.604 | 0.596 | 0.641 | 0.641 | 0.636 | 0.645 | 0.665 | 0.735 | 0.062 | 6.0 |

| Lithuania | 0.806 | 0.825 | 0.809 | 0.813 | 0.805 | 0.788 | 0.847 | 0.836 | 0.871 | 0.857 | 0.868 | 0.871 | 0.901 | 0.095 | 4.0 |

| Luxembourg | 0.345 | 0.315 | 0.306 | 0.297 | 0.293 | 0.311 | 0.312 | 0.331 | 0.337 | 0.320 | 0.313 | 0.276 | 0.262 | −0.083 | 7.5 |

| Netherlands | 0.845 | 0.851 | 0.863 | 0.867 | 0.851 | 0.842 | 0.836 | 0.821 | 0.838 | 0.850 | 0.846 | 0.847 | 0.838 | −0.007 | 1.4 |

| Slovakia | 0.677 | 0.669 | 0.682 | 0.716 | 0.721 | 0.720 | 0.722 | 0.707 | 0.703 | 0.707 | 0.723 | 0.727 | 0.745 | 0.068 | 3.1 |

| Coeff. Var (%) | 37.3 | 37.9 | 38.1 | 38.8 | 38.7 | 36.5 | 35.4 | 35.4 | 36.3 | 36.4 | 36.9 | 37.5 | 38.3 | ||

| EA-Co average | 0.442 | 0.447 | 0.454 | 0.452 | 0.445 | 0.468 | 0.477 | 0.459 | 0.457 | 0.472 | 0.464 | 0.460 | 0.447 | 0.005 | 2.4 |

| Euro Area Periphery Countries (EA-Pe) | |||||||||||||||

| Cyprus | 0.598 | 0.639 | 0.649 | 0.638 | 0.647 | 0.642 | 0.607 | 0.626 | 0.641 | 0.634 | 0.675 | 0.658 | 0.842 | 0.244 | 9.2 |

| Greece | 0.656 | 0.663 | 0.677 | 0.696 | 0.692 | 0.706 | 0.720 | 0.795 | 0.940 | 0.941 | 0.952 | 0.973 | 0.970 | 0.314 | 16.7 |

| Ireland | 0.478 | 0.490 | 0.504 | 0.503 | 0.526 | 0.499 | 0.467 | 0.464 | 0.478 | 0.476 | 0.459 | 0.443 | 0.455 | −0.023 | 4.9 |

| Italy | 0.268 | 0.262 | 0.331 | 0.312 | 0.310 | 0.398 | 0.395 | 0.397 | 0.396 | 0.410 | 0.410 | 0.430 | 0.434 | 0.166 | 16.6 |

| Malta | 0.753 | 0.709 | 0.702 | 0.728 | 0.728 | 0.713 | 0.720 | 0.744 | 0.765 | 0.815 | 0.813 | 0.803 | 0.809 | 0.056 | 5.6 |

| Portugal | 0.688 | 0.679 | 0.678 | 0.691 | 0.701 | 0.709 | 0.708 | 0.699 | 0.703 | 0.692 | 0.723 | 0.712 | 0.731 | 0.043 | 2.3 |

| Slovenia | 0.630 | 0.620 | 0.595 | 0.591 | 0.597 | 0.593 | 0.593 | 0.584 | 0.571 | 0.556 | 0.592 | 0.610 | 0.615 | −0.015 | 3.3 |

| Spain | 0.420 | 0.404 | 0.410 | 0.424 | 0.433 | 0.443 | 0.481 | 0.514 | 0.544 | 0.583 | 0.602 | 0.618 | 0.637 | 0.217 | 17.3 |

| Coeff. Var (%) | 28.6 | 28.3 | 24.4 | 25.8 | 25.4 | 21.5 | 21.7 | 23.2 | 27.4 | 27.4 | 27.3 | 27.3 | 27.3 | ||

| EA-Pe average | 0.398 | 0.395 | 0.424 | 0.425 | 0.432 | 0.467 | 0.473 | 0.486 | 0.502 | 0.519 | 0.526 | 0.537 | 0.549 | 0.151 | 11.3 |

| All Euro Area Countries (EA-19) | |||||||||||||||

| Coeff. Var (%) | 34.7 | 35.1 | 33.8 | 34.5 | 33.9 | 31.2 | 30.5 | 30.4 | 32.0 | 32.0 | 32.3 | 32.6 | 33.1 | ||

| EA-19 average | 0.431 | 0.433 | 0.446 | 0.445 | 0.442 | 0.469 | 0.477 | 0.469 | 0.472 | 0.487 | 0.483 | 0.483 | 0.476 | 0.045 | 4.4 |

| Country | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | Total change | Coeff. Var (%) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Euro area core countries (EA-Co) | |||||||||||||||

| Austria | 2.60 | 2.74 | 2.24 | 1.90 | 2.25 | 2.83 | 2.71 | 2.81 | 2.87 | 3.47 | 3.39 | 2.70 | 2.37 | −0.23 | 16.3 |

| Belgium | 2.00 | 1.28 | 1.16 | 1.65 | 3.08 | 2.80 | 3.30 | 3.74 | 4.24 | 4.18 | 3.79 | 3.43 | 2.92 | 0.92 | 36.6 |

| Estonia | 0.20 | 0.20 | 0.50 | 1.94 | 5.20 | 5.38 | 4.05 | 2.62 | 1.47 | 1.39 | 0.98 | 0.87 | 0.70 | 0.50 | 92.6 |

| Finland | 0.30 | 0.20 | 0.30 | 0.40 | 0.60 | 0.60 | 0.50 | 0.50 | 0.67 | 1.30 | 1.34 | 1.52 | 1.67 | 1.37 | 66.7 |

| France | 3.50 | 3.00 | 2.70 | 2.82 | 4.02 | 3.76 | 4.29 | 4.29 | 4.50 | 4.16 | 3.98 | 3.64 | 3.08 | −0.42 | 16.5 |

| Germany | 4.05 | 3.41 | 2.65 | 2.85 | 3.31 | 3.20 | 3.03 | 2.86 | 2.70 | 2.34 | 1.97 | 1.71 | 1.50 | −2.55 | 26.2 |

| Latvia | 0.70 | 0.50 | 0.80 | 2.10 | 14.28 | 15.93 | 14.05 | 8.72 | 6.41 | 4.60 | 4.64 | 6.26 | 5.51 | 4.81 | 82.0 |

| Lithuania | 0.60 | 1.00 | 1.00 | 6.08 | 23.99 | 23.33 | 18.84 | 14.80 | 11.59 | 8.19 | 4.95 | 3.66 | 3.18 | 2.58 | 90.4 |

| Luxembourg | 0.20 | 0.10 | 0.40 | 0.60 | 0.67 | 0.25 | 0.38 | 0.15 | 0.21 | 0.21 | 0.21 | 0.90 | 0.79 | 0.59 | 67.7 |

| Netherlands | 1.20 | 0.80 | 1.50 | 1.68 | 3.20 | 2.83 | 2.71 | 3.10 | 3.23 | 2.98 | 2.71 | 2.54 | 2.31 | 1.11 | 34.2 |

| Slovakia | 5.00 | 3.20 | 2.50 | 2.49 | 5.29 | 5.84 | 5.61 | 5.22 | 5.14 | 5.35 | 4.87 | 4.44 | 3.70 | −1.30 | 25.6 |

| Coeff. Var (%) | 92.4 | 88.5 | 65.4 | 67.3 | 117.2 | 117.1 | 106.6 | 93.2 | 81.0 | 64.0 | 55.6 | 56.7 | 55.2 | ||

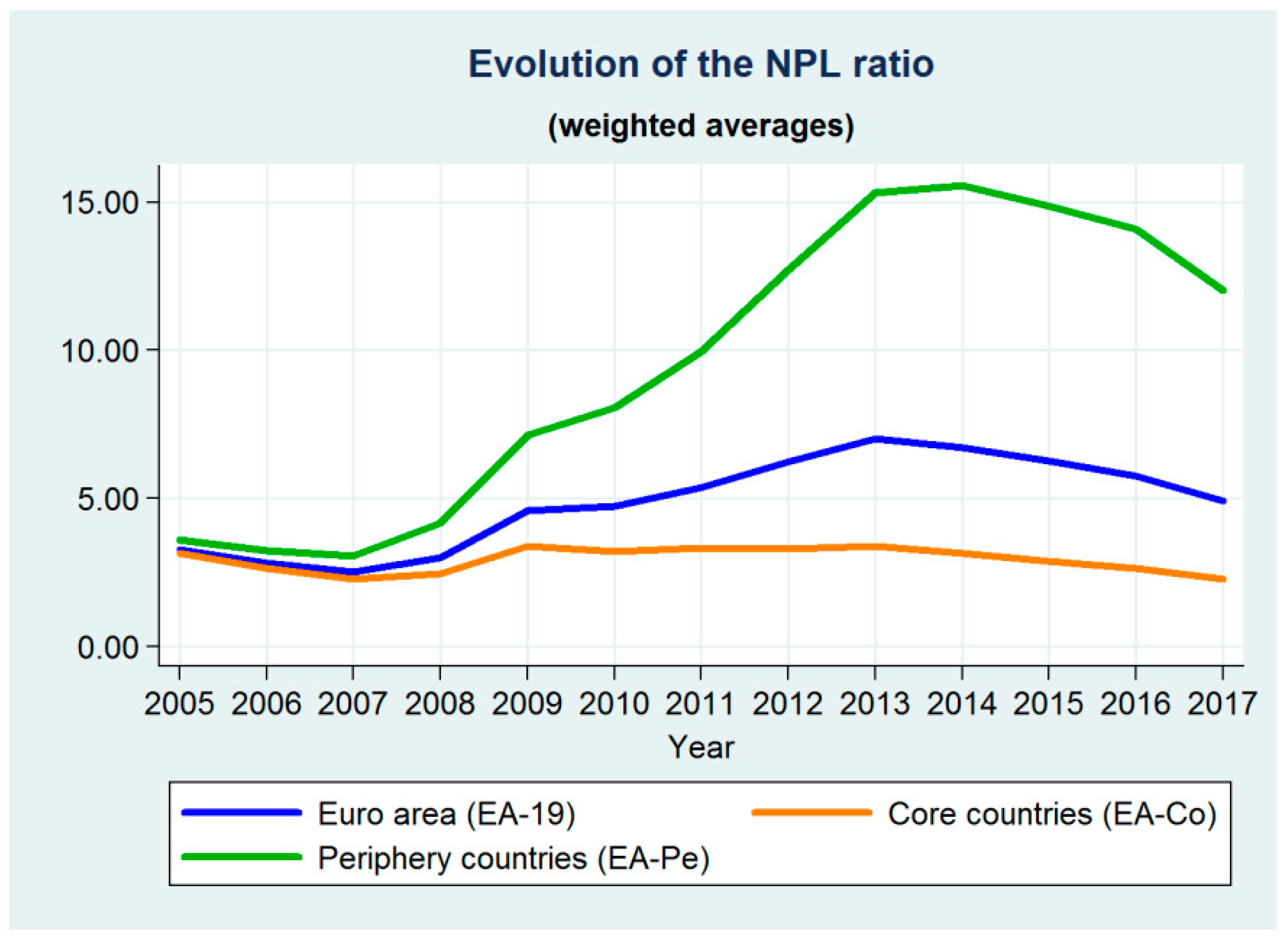

| EA-Co average | 3.15 | 2.63 | 2.28 | 2.45 | 3.38 | 3.20 | 3.32 | 3.30 | 3.38 | 3.14 | 2.88 | 2.62 | 2.28 | −0.87 | 14.4 |

| Euro area periphery countries (EA-Pe) | |||||||||||||||

| Cyprus | 7.10 | 5.40 | 3.40 | 3.59 | 4.51 | 5.82 | 9.99 | 18.37 | 38.56 | 44.97 | 47.75 | 48.68 | 40.17 | 33.07 | 89.5 |

| Greece | 6.30 | 5.40 | 4.60 | 4.67 | 6.95 | 9.12 | 14.43 | 23.27 | 31.90 | 33.78 | 36.65 | 36.30 | 45.57 | 39.27 | 75.7 |

| Ireland | 0.48 | 0.53 | 0.63 | 1.92 | 9.80 | 13.05 | 16.12 | 24.99 | 25.71 | 20.65 | 14.93 | 13.61 | 11.46 | 10.98 | 75.6 |

| Italy | 7.00 | 6.57 | 5.78 | 6.28 | 9.45 | 10.03 | 11.74 | 13.75 | 16.54 | 18.03 | 18.06 | 17.12 | 14.38 | 7.38 | 39.5 |

| Malta | 8.21 | 6.47 | 5.31 | 5.01 | 5.78 | 7.02 | 7.09 | 7.75 | 8.95 | 9.05 | 6.77 | 5.32 | 4.07 | −4.14 | 23.2 |

| Portugal | 1.50 | 1.30 | 2.85 | 3.60 | 5.13 | 5.31 | 7.47 | 9.74 | 10.62 | 11.91 | 17.48 | 17.18 | 13.27 | 11.77 | 67.7 |

| Slovenia | 2.50 | 2.50 | 2.50 | 4.22 | 5.79 | 8.21 | 11.81 | 15.18 | 13.31 | 11.73 | 9.96 | 5.07 | 3.20 | 0.70 | 61.7 |

| Spain | 0.79 | 0.70 | 0.90 | 2.81 | 4.12 | 4.67 | 6.01 | 7.48 | 9.38 | 8.45 | 6.16 | 5.64 | 4.46 | 3.67 | 60.4 |

| Coeff. Var (%) | 75.9 | 72.5 | 58.9 | 33.7 | 33.3 | 35.4 | 34.2 | 44.7 | 58.4 | 66.2 | 75.5 | 85.5 | 97.0 | ||

| EA-Pe average | 3.58 | 3.22 | 3.05 | 4.15 | 7.14 | 8.07 | 9.95 | 12.71 | 15.32 | 15.56 | 14.86 | 14.08 | 12.03 | 8.45 | 51.6 |

| All euro area countries (EA-19) | |||||||||||||||

| Coeff. Var (%) | 93.4 | 91.7 | 75.6 | 55.9 | 87.4 | 82.6 | 72.7 | 84.1 | 103.7 | 113.6 | 126.0 | 134.6 | 147.3 | ||

| EA-19 average | 3.27 | 2.80 | 2.51 | 2.98 | 4.59 | 4.72 | 5.35 | 6.23 | 7.02 | 6.72 | 6.26 | 5.76 | 4.90 | 1.63 | 32.0 |

| Year | Market Power (Lerner Index) | Concentration (HHI) | Concentration (CR5) | Credit Risk (NPL Ratio) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Inequality | Inequality | Inequality | Inequality | |||||||||

| Total | Within -Group | Between-Group | Total | Within -Group | Between-Group | Total | Within -Group | Between-Group | Total | Within -Group | Between-Group | |

| 2005 | 0.099 | 0.097 (98%) | 0.002 (2%) | 0.365 | 0.350 (96%) | 0.015 (4%) | 0.116 | 0.115 (99%) | 0.001 (1%) | 0.280 | 0.278 (99%) | 0.002 (1%) |

| 2006 | 0.136 | 0.133 (98%) | 0.003 (2%) | 0.354 | 0.336 (95%) | 0.018 (5%) | 0.112 | 0.110 (98%) | 0.002 (2%) | 0.322 | 0.318 (99%) | 0.004 (1%) |

| 2007 | 0.105 | 0.100 (95%) | 0.005 (5%) | 0.323 | 0.311 (96%) | 0.012 (4%) | 0.102 | 0.101 (99%) | 0.001 (1%) | 0.194 | 0.185 (95%) | 0.009 (5%) |

| 2008 | 0.099 | 0.092 (93%) | 0.007 (7%) | 0.331 | 0.318 (96%) | 0.013 (4%) | 0.097 | 0.096 (99%) | 0.001 (1%) | 0.108 | 0.077 (71%) | 0.031 (29%) |

| 2009 | 0.121 | 0.119 (98%) | 0.002 (2%) | 0.299 | 0.291 (97%) | 0.008 (3%) | 0.081 | 0.080 (99%) | 0.001 (1%) | 0.135 | 0.069 (51%) | 0.066 (49%) |

| 2010 | 0.110 | 0.101 (92%) | 0.009 (8%) | 0.229 | 0.224 (98%) | 0.005 (2%) | 0.049 | 0.048 (98%) | 0.001 (2%) | 0.187 | 0.087 (47%) | 0.100 (53%) |

| 2011 | 0.095 | 0.094 (99%) | 0.001 (1%) | 0.227 | 0.221 (97%) | 0.006 (3%) | 0.045 | 0.044 (98%) | 0.001 (2%) | 0.229 | 0.088 (38%) | 0.141 (62%) |

| 2012 | 0.103 | 0.102 (99%) | 0.001 (1%) | 0.218 | 0.216 (99%) | 0.002 (1%) | 0.045 | 0.044 (98%) | 0.001 (2%) | 0.325 | 0.110 (34%) | 0.215 (66%) |

| 2013 | 0.112 | 0.111 (99%) | 0.001 (1%) | 0.249 | 0.247 (99%) | 0.002 (1%) | 0.054 | 0.053 (98%) | 0.001 (2%) | 0.372 | 0.102 (27%) | 0.270 (73%) |

| 2014 | 0.134 | 0.126 (94%) | 0.008 (6%) | 0.243 | 0.241 (99%) | 0.002 (1%) | 0.053 | 0.052 (98%) | 0.001 (2%) | 0.400 | 0.100 (25%) | 0.300 (75%) |

| 2015 | 0.124 | 0.119 (96%) | 0.005 (4%) | 0.249 | 0.247 (99%) | 0.002 (1%) | 0.059 | 0.057 (97%) | 0.002 (3%) | 0.437 | 0.123 (28%) | 0.314 (72%) |

| 2016 | 0.153 | 0.152 (99%) | 0.001 (1%) | 0.237 | 0.235 (99%) | 0.002 (1%) | 0.057 | 0.055 (96%) | 0.002 (4%) | 0.423 | 0.097 (23%) | 0.326 (77%) |

| 2017 | 0.164 | 0.162 (99%) | 0.002 (1%) | 0.236 | 0.232 (98%) | 0.004 (2%) | 0.062 | 0.058 (94%) | 0.004 (6%) | 0.421 | 0.104 (25%) | 0.317 (75%) |

| Total change | 0.065 | 0.065 | 0.000 | −0.129 | −0.118 | −0.011 | −0.054 | −0.057 | 0.003 | 0.141 | −0.174 | 0.315 |

| Year | Euro Area (EA-19) | Core Countries (EA-Co) | Periphery Countries (EA-Pe) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Inequality | Inequality | Inequality | |||||||

| Total | Within-Country | Between-Country | Total | Within-Country | Between-Country | Total | Within-Country | Between-Country | |

| 2005 | 0.099 | 0.064 (65%) | 0.035 (35%) | 0.096 | 0.063 (66%) | 0.033 (34%) | 0.105 | 0.072 (69%) | 0.033 (31%) |

| 2006 | 0.135 | 0.063 (47%) | 0.072 (53%) | 0.137 | 0.067 (49%) | 0.070 (51%) | 0.117 | 0.051 (44%) | 0.066 (56%) |

| 2007 | 0.105 | 0.068 (65%) | 0.037 (35%) | 0.084 | 0.065 (77%) | 0.019 (23%) | 0.158 | 0.079 (50%) | 0.079 (50%) |

| 2008 | 0.099 | 0.071 (72%) | 0.028 (28%) | 0.096 | 0.076 (79%) | 0.020 (21%) | 0.078 | 0.053 (68%) | 0.025 (32%) |

| 2009 | 0.122 | 0.061 (50%) | 0.061 (50%) | 0.107 | 0.052 (49%) | 0.055 (51%) | 0.161 | 0.090 (56%) | 0.071 (44%) |

| 2010 | 0.110 | 0.055 (50%) | 0.055 (50%) | 0.081 | 0.054 (67%) | 0.027 (33%) | 0.163 | 0.058 (36%) | 0.105 (64%) |

| 2011 | 0.094 | 0.073 (78%) | 0.021 (22%) | 0.084 | 0.074 (88%) | 0.010 (12%) | 0.122 | 0.072 (59%) | 0.050 (41%) |

| 2012 | 0.103 | 0.069 (67%) | 0.034 (33%) | 0.079 | 0.055 (70%) | 0.024 (30%) | 0.170 | 0.112 (66%) | 0.058 (34%) |

| 2013 | 0.111 | 0.079 (71%) | 0.032 (29%) | 0.105 | 0.080 (76%) | 0.025 (24%) | 0.130 | 0.078 (60%) | 0.052 (40%) |

| 2014 | 0.135 | 0.094 (70%) | 0.041 (30%) | 0.120 | 0.097 (81%) | 0.023 (19%) | 0.144 | 0.087 (61%) | 0.057 (39%) |

| 2015 | 0.124 | 0.071 (57%) | 0.053 (43%) | 0.106 | 0.064 (60%) | 0.042 (40%) | 0.155 | 0.090 (58%) | 0.065 (42%) |

| 2016 | 0.152 | 0.102 (67%) | 0.050 (33%) | 0.149 | 0.102 (68%) | 0.047 (32%) | 0.158 | 0.103 (65%) | 0.055 (35%) |

| 2017 | 0.163 | 0.126 (77%) | 0.037 (23%) | 0.153 | 0.131 (86%) | 0.022 (14%) | 0.143 | 0.112 (78%) | 0.031 (22%) |

| Total change | 0.064 | 0.062 | 0.002 | 0.057 | 0.068 | −0.011 | 0.038 | 0.040 | −0.002 |

| Variable | Period | EA-19 | EA-Co | EA-Pe | |||

|---|---|---|---|---|---|---|---|

| β | σ | β | σ | β | σ | ||

| Lerner index | 2008–2012 | −0.9976 *** (0.1001) | 0.0031 * (0.0017) | −1.0405 *** (0.1450) | 0.0043 * (0.0022) | −0.9490 *** (0.1367) | 0.0016 (0.0028) |

| 2013–2017 | −0.8851 *** (0.1436) | 0.0012 (0.0022) | −0.9229 *** (0.2177) | 0.0026 (0.0026) | −0.8542 *** (0.1930) | −0.0014 (0.0035) | |

| 2005–2017 | −0.4072 *** (0.0548) | 0.0018 *** (0.0005) | −0.5367 *** (0.0834) | 0.0023 *** (0.0006) | −0.3551 *** (0.0781) | 0.0011 (0.0008) | |

| HHI | 2008–2012 | −0.4009 *** (0.1003) | −0.0018 ** (0.0008) | −0.4112 *** (0.1203) | −0.0022 * (0.0012) | −0.3711 * (0.1924) | −0.0004 (0.0007) |

| 2013–2017 | −0.1257 (0.1524) | −0.0025 * (0.0014) | 0.1707 (0.1714) | −0.0048 ** (0.0022) | −0.8280 *** (0.2513) | 0.0007 (0.0010) | |

| 2005–2017 | −0.1210 *** (0.0363) | −0.0005 (0.0004) | −0.1531 *** (0.0478) | −0.0018 *** (0.0005) | −0.0914 (0.0558) | 0.0013 *** (0.0004) | |

| CR5 | 2008–2012 | −0.4466 *** (0.0953) | −0.0056 *** (0.0020) | −0.4785 *** (0.1099) | −0.0070 *** (0.0024) | −0.3822 ** (0.1805) | −0.0027 (0.0029) |

| 2013–2017 | −0.1709 (0.1672) | 0.0030 (0.0022) | 0.0201 (0.1848) | 0.0042 (0.0026) | −0.4191 (0.3000) | 0.0035 (0.0033) | |

| 2005–2017 | −0.1415 *** (0.0356) | −0.0002 (0.0009) | −0.2044 *** (0.0486) | −0.0008 (0.0008) | −0.0941 * (0.0530) | 0.0017 (0.0013) | |

| NPL ratio | 2008–2012 | −0.7191 *** (0.0829) | 1.0584 *** (0.1872) | −1.0430 *** (0.0974) | 0.2944 (0.2230) | −0.3218 *** (0.0927) | 0.9931 *** (0.1779) |

| 2013–2017 | −0.2679 ** (0.1012) | 0.2008 * (0.1771) | −0.3747 *** (0.1347) | −0.2758 *** (0.0910) | −0.0174 (0.1426) | 0.8723 ** (0.3450) | |

| 2005–2017 | −0.2009 *** (0.0325) | 0.7479 *** (0.0793) | −0.2817 *** (0.0519) | −0.0245 (0.0545) | −0.1304 *** (0.0369) | 1.0566 *** (0.1243) | |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Karadima, M.; Louri, H. Bank Competition and Credit Risk in Euro Area Banking: Fragmentation and Convergence Dynamics. J. Risk Financial Manag. 2020, 13, 57. https://doi.org/10.3390/jrfm13030057

Karadima M, Louri H. Bank Competition and Credit Risk in Euro Area Banking: Fragmentation and Convergence Dynamics. Journal of Risk and Financial Management. 2020; 13(3):57. https://doi.org/10.3390/jrfm13030057

Chicago/Turabian StyleKaradima, Maria, and Helen Louri. 2020. "Bank Competition and Credit Risk in Euro Area Banking: Fragmentation and Convergence Dynamics" Journal of Risk and Financial Management 13, no. 3: 57. https://doi.org/10.3390/jrfm13030057

APA StyleKaradima, M., & Louri, H. (2020). Bank Competition and Credit Risk in Euro Area Banking: Fragmentation and Convergence Dynamics. Journal of Risk and Financial Management, 13(3), 57. https://doi.org/10.3390/jrfm13030057