FOMC Forecasts: Are They Useful for Understanding Monetary Policy?

Abstract

1. The Question

“Appropriate monetary policy is defined as the future policy most likely to foster outcomes for economic activity and inflation that best satisfy the participant’s interpretation of the Federal Reserve’s dual objectives of maximum employment and price stability.”2

The SEP, in my view, deserves a special place in the annals of obfuscation in the service of transparency. The SEP is the paradigm case of the second type of communication: it is purely a depiction of the policymakers’ different views on the outlook and appropriate policy, with no hints about how any differences may be resolved.(Faust 2016, p. 17)

2. FOMC Reaction Function

As noted above, the most important function to convey regards the reaction function of the policymakers. However, the SEP approach of providing separate variable-by-variable summaries of the 19 forecasts obscures any link between the paths of the federal funds rate as depicted in the dot-plot and the forecasts of the other variables.(Faust 2016, p. 18)

Wouldn’t it be easier if the FOMC just provided its reaction function, together with collective projections of key macroeconomic variables? In principle, yes; and in fact, in the course of expanding the SEP, the FOMC under my chairmanship experimented with developing a consensus committee forecast, together with alternative scenarios, that could be released to the public.(Bernanke 2016, p. 7)

And the question is, are we ever going to converge? I would feel my job is to get everybody to see that off-white is not a bad alternative. (Laughter) As brilliant as your choice was, maybe you could live with off-white, and it’s not so bad. And we can converge on that and it’s going to function just fine and maybe we can agree.

3. Empirical Taylor Rules

3.1. Single Equation

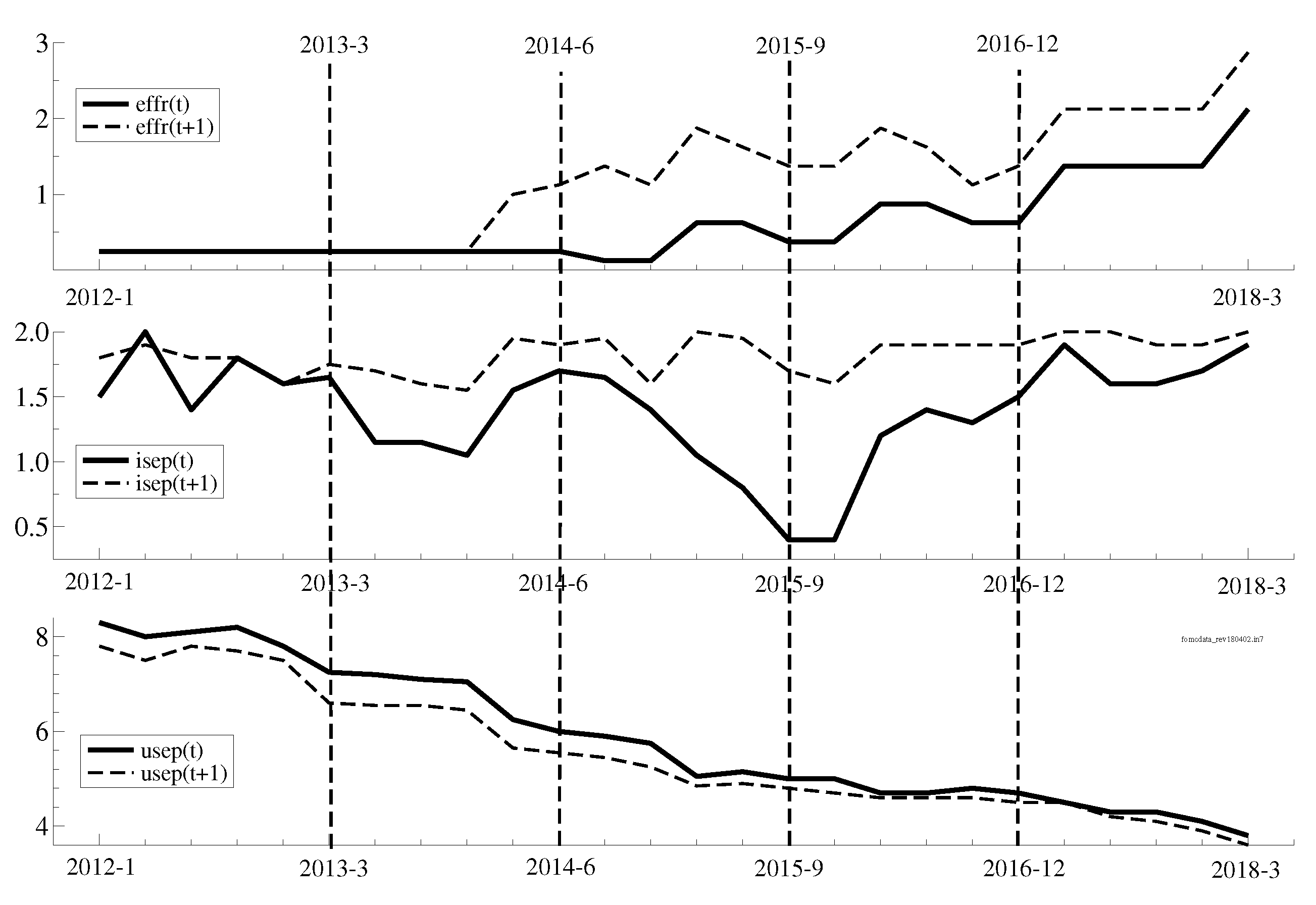

- is the median federal funds rate for the tth year made during the tth FOMC meeting

- is the median inflation projection for the tth year made during the tth FOMC meeting

- is the median unemployment projection for the tth year made during the tth FOMC meeting

- dummy variable equal to one for Bernanke’s tenure as Chair of the FOMC

- dummy variable equal to one for Yellen’s tenure as Chair of the FOMC

- dummy variable equal to one for Powell’s tenure as Chair of the FOMC

- and are projections from the Survey of Professional Forecasters for inflation and unemployment, respectively, available in real time prior to the FOMC meeting

- and are the actual values for inflation and unemployment prior to the FOMC meetings.11

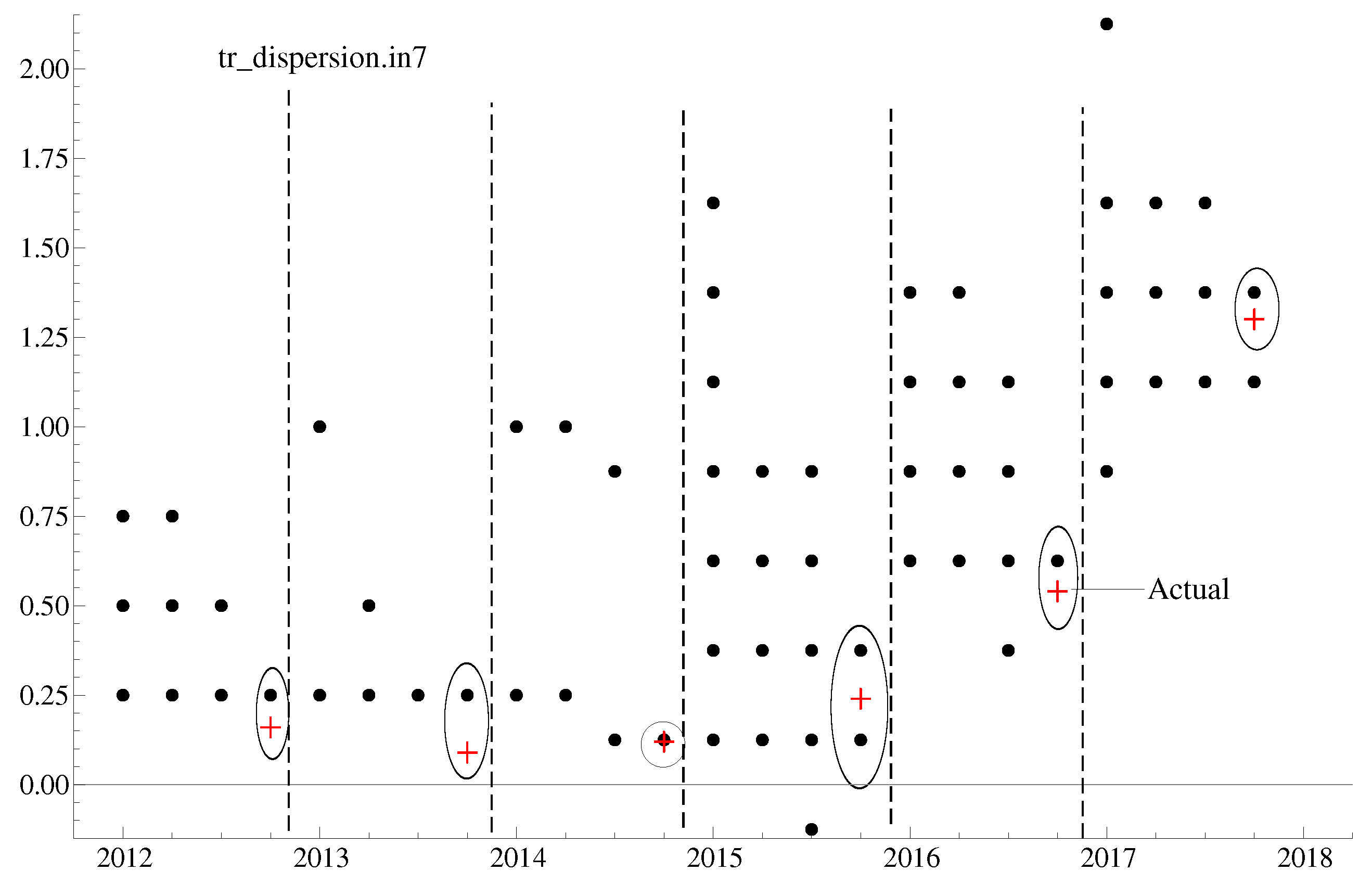

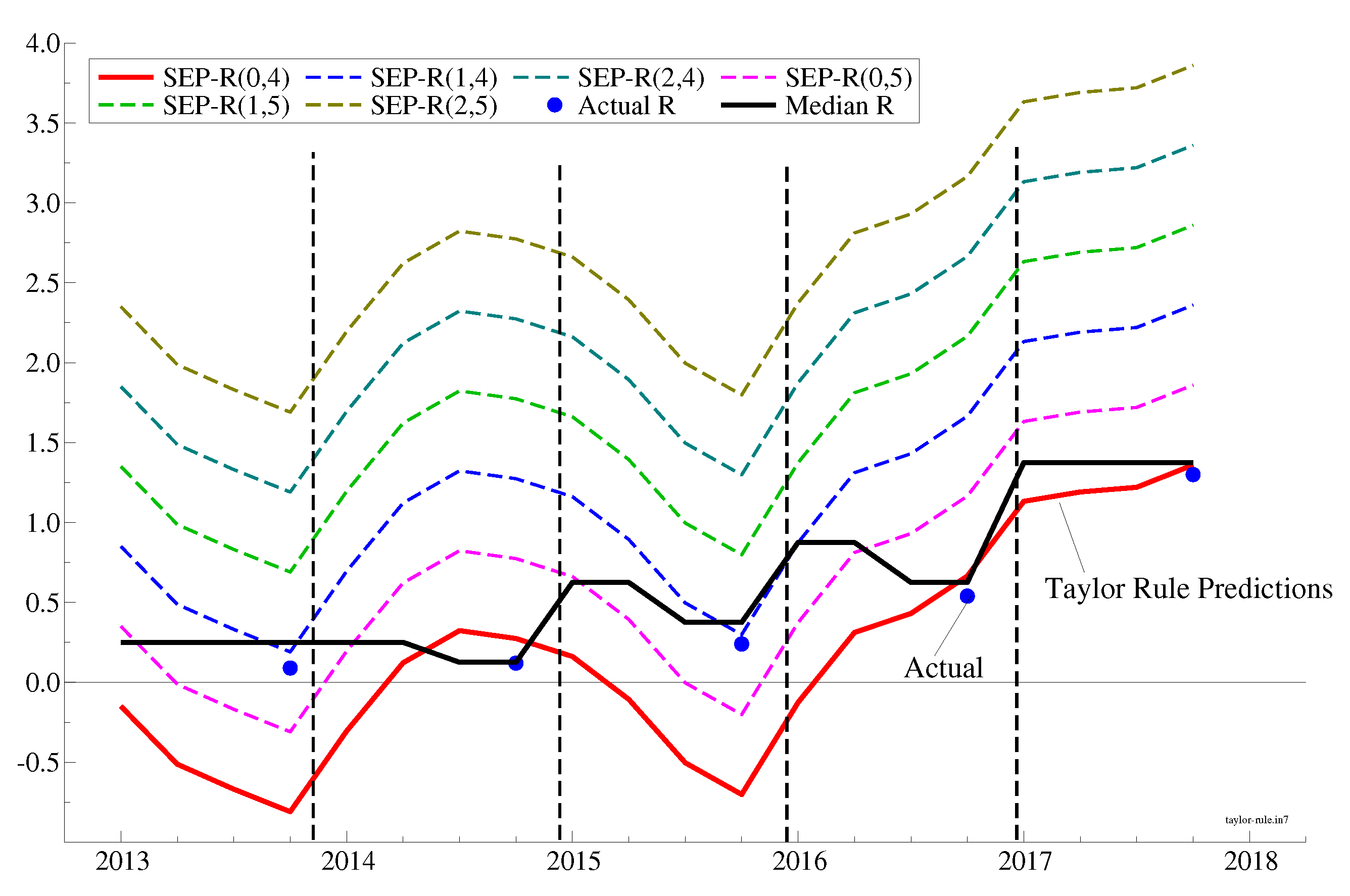

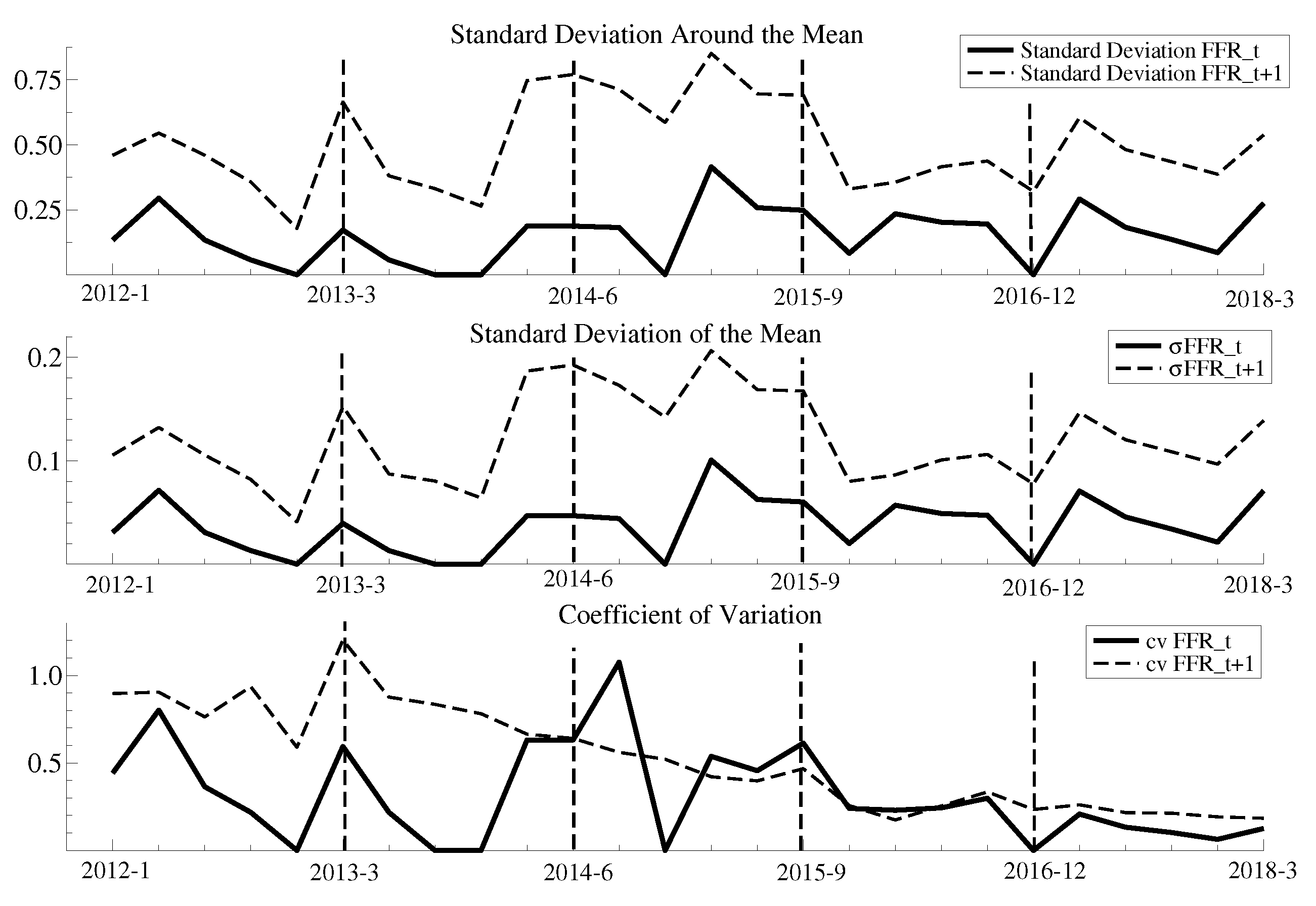

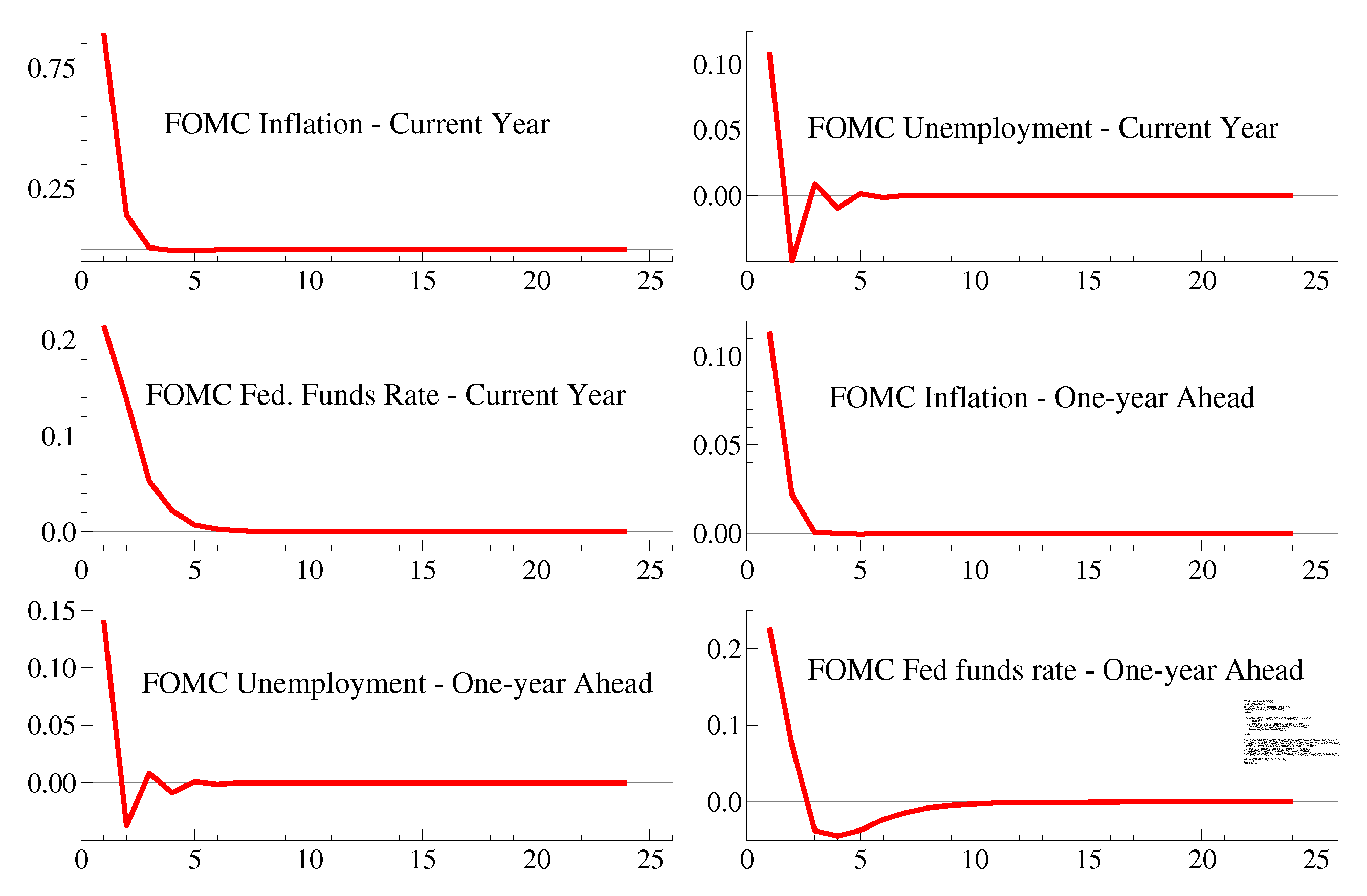

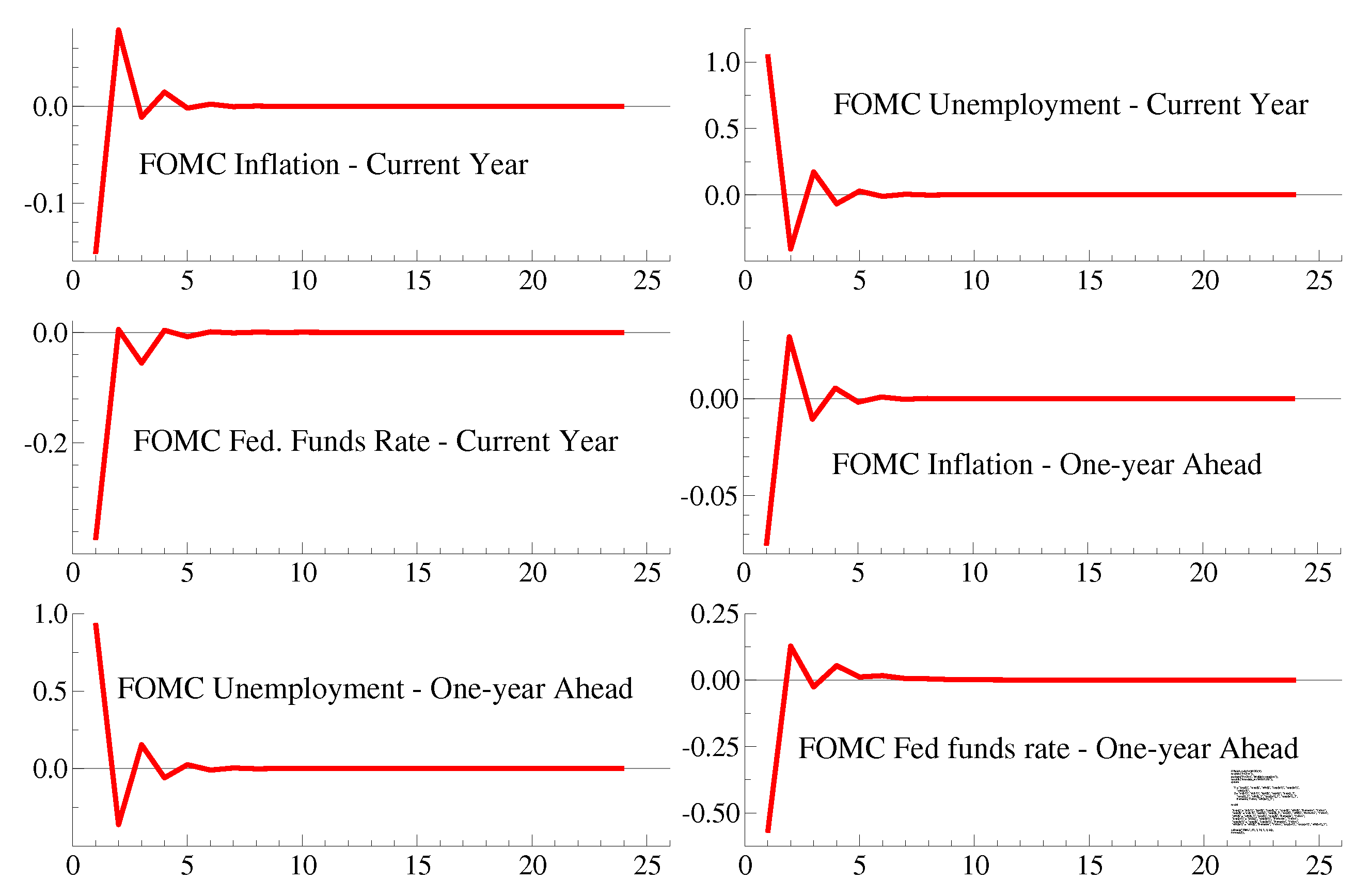

- and are coefficients of variation of the distribution of FOMC participants’ appropriate federal funds rate (Figure 5). Please note that we allow current and one-year-ahead uncertainty

- is a polynomial of degree one in the lag operator.

- Sole reliance on the GUM suggests that the previous value of the federal funds rate is the most important factor in explaining movements in that interest rate; neither FOMC Chair effects nor participants’ difference, nor economic data (FOMC’s or public) are statistically important.

- The implementation of Autometrics reveals that Chair effects are relevant and that their long-run values are robust to the choice of strategy.

- FOMC’s current-year forecasts of inflation and unemployment are not relevant for forecasting FOMC rate decisions. In other words, one cannot reject the null hypothesis that This confirms the relevancy of Faust’s critique.

- Estimates using a 0.01% significance level show that persistence is not relevant and that information about both inflation and unemployment play statistically important roles. The exclusion of persistence, odd at first, is reasonable once one realizes that persistence is already embodied in the FOMC Chair. However, the Chair embodies more than history: It embodies the power to persuade participants around the Chair’s view. Given this persuasive power, it is not surprising to find that one cannot reject the null hypothesis that In other words, heterogeneity among FOMC participants is not relevant for explaining the federal funds rate so long as the Chair is persuasive in reconciling differences among FOMC participants.

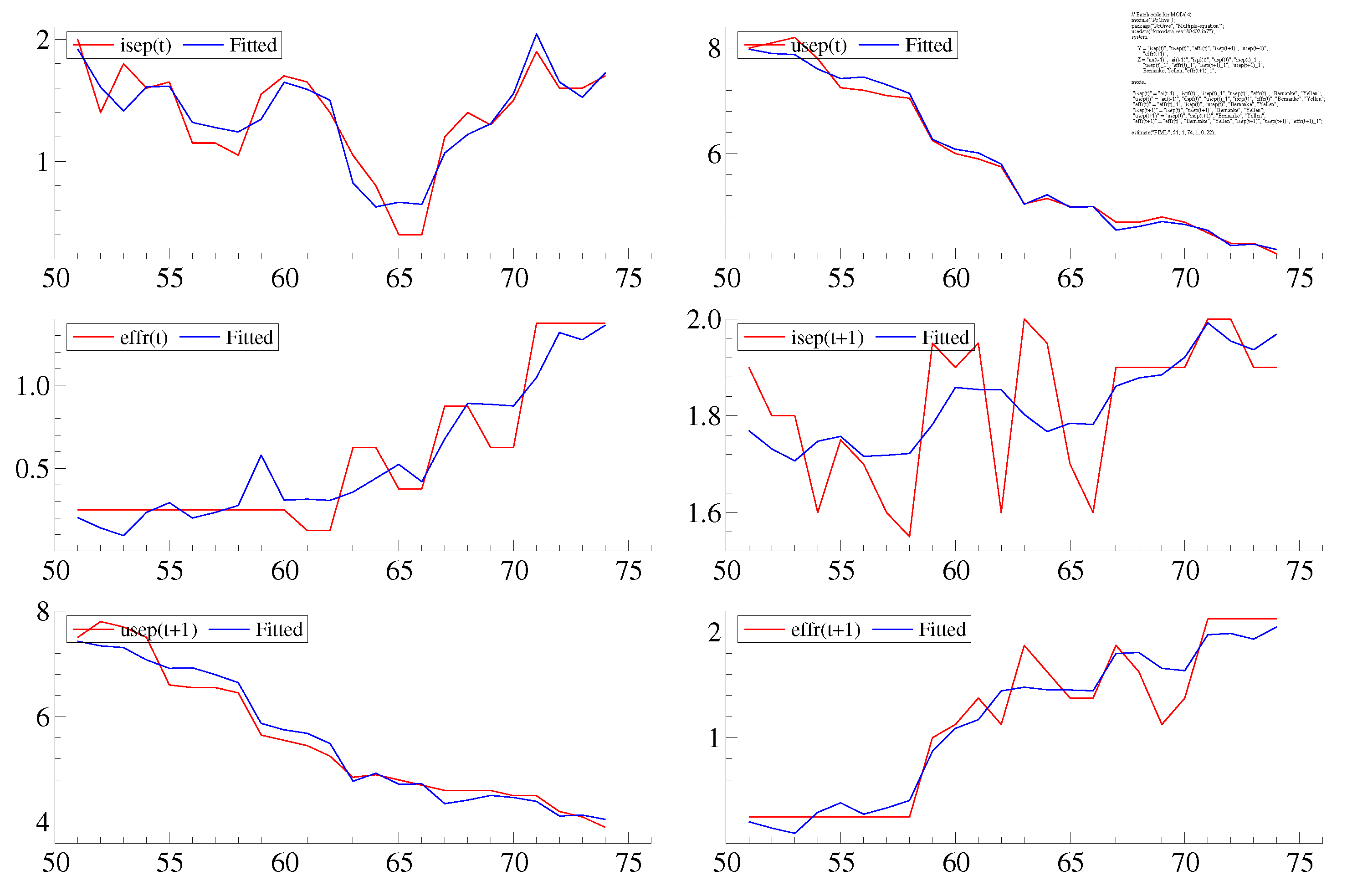

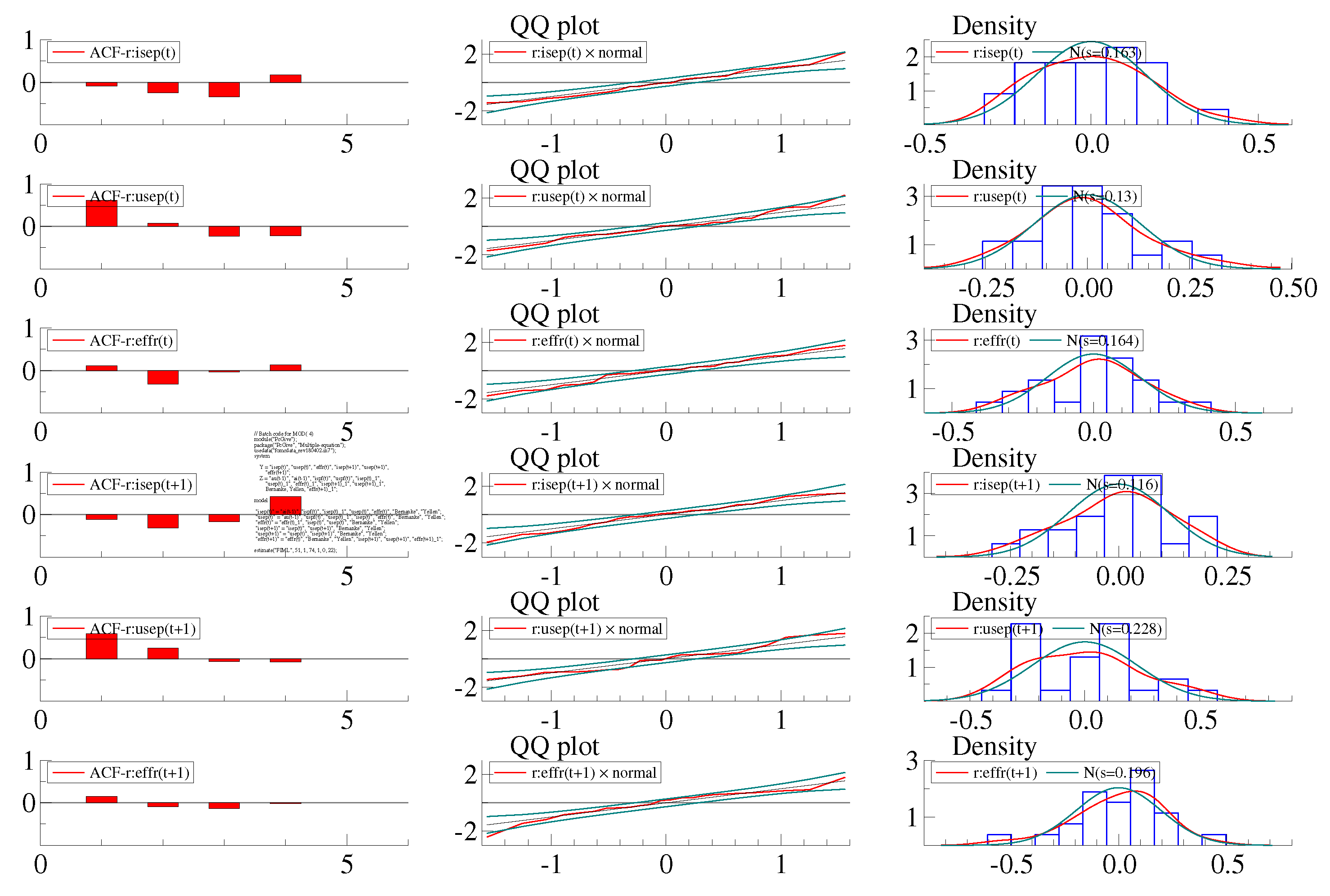

3.2. Sensitivity Analysis

3.2.1. Design

General Structure

- and are the inflation projections for the current year and one year ahead, respectively, made during the tth FOMC meeting

- and are the unemployment projections for the current year and one year ahead, respectively, made during the tth FOMC meeting

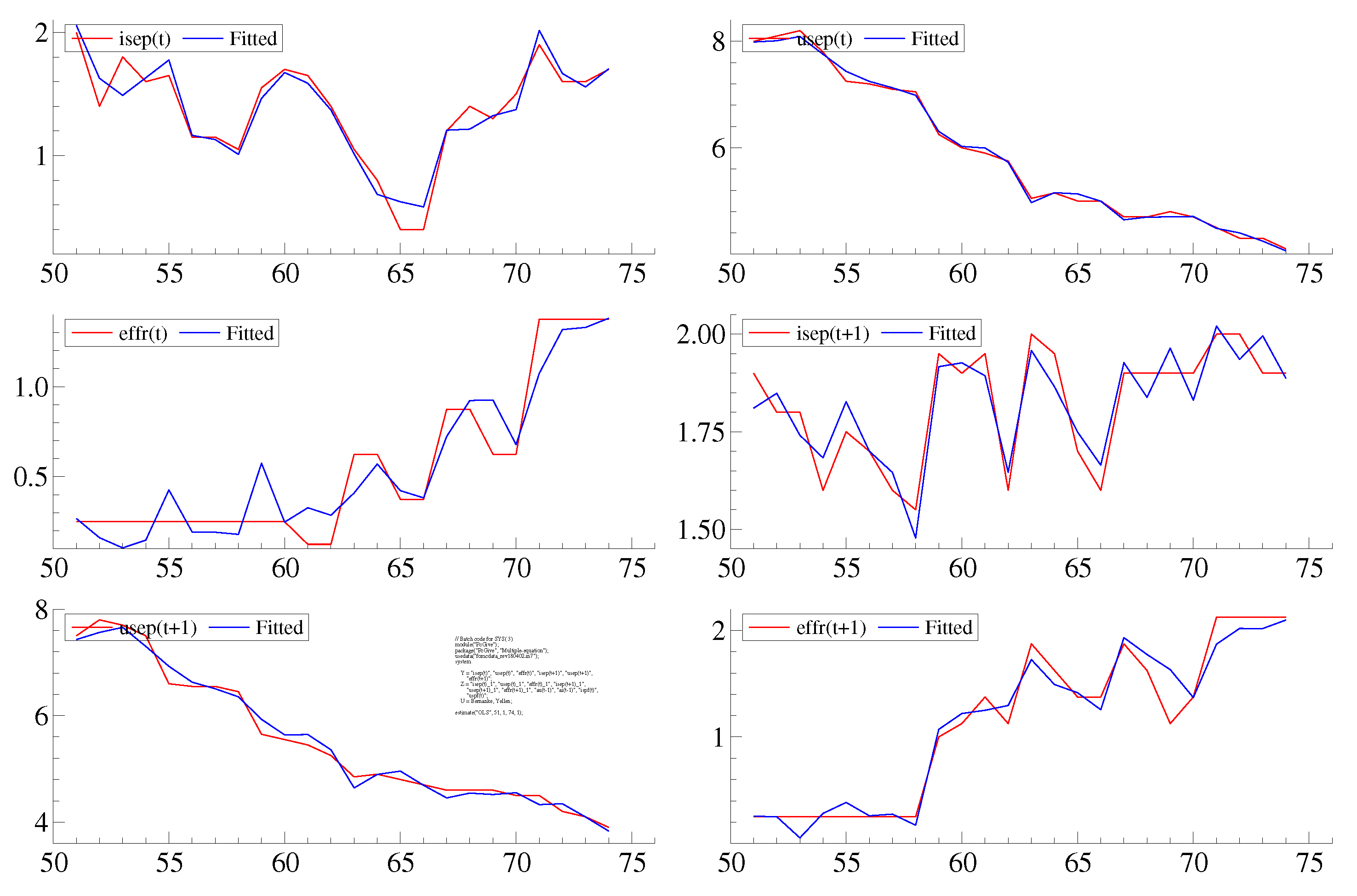

- and are the federal funds rate in the current and one-year-ahead projections, respectively, made during the tth FOMC meeting

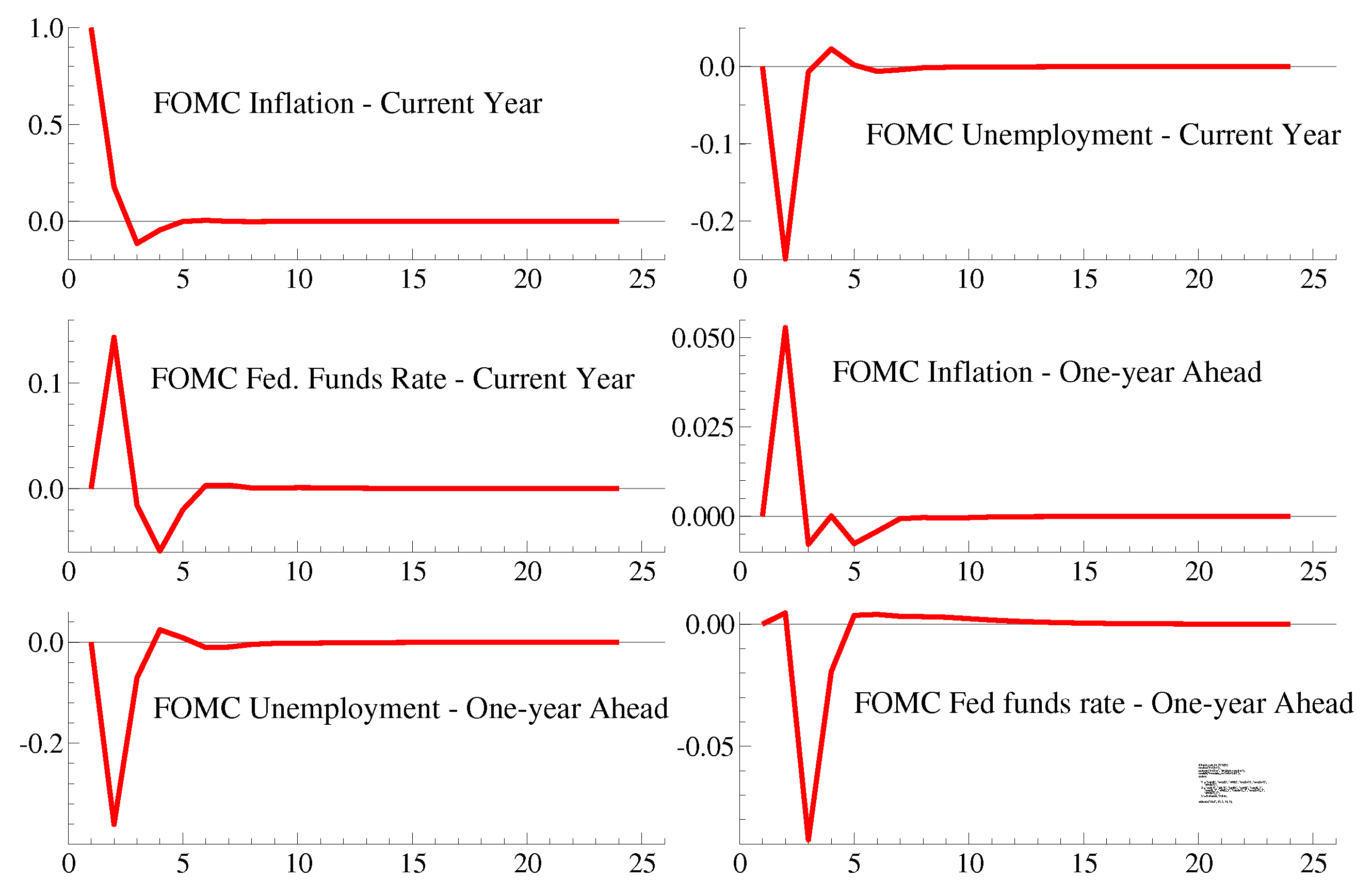

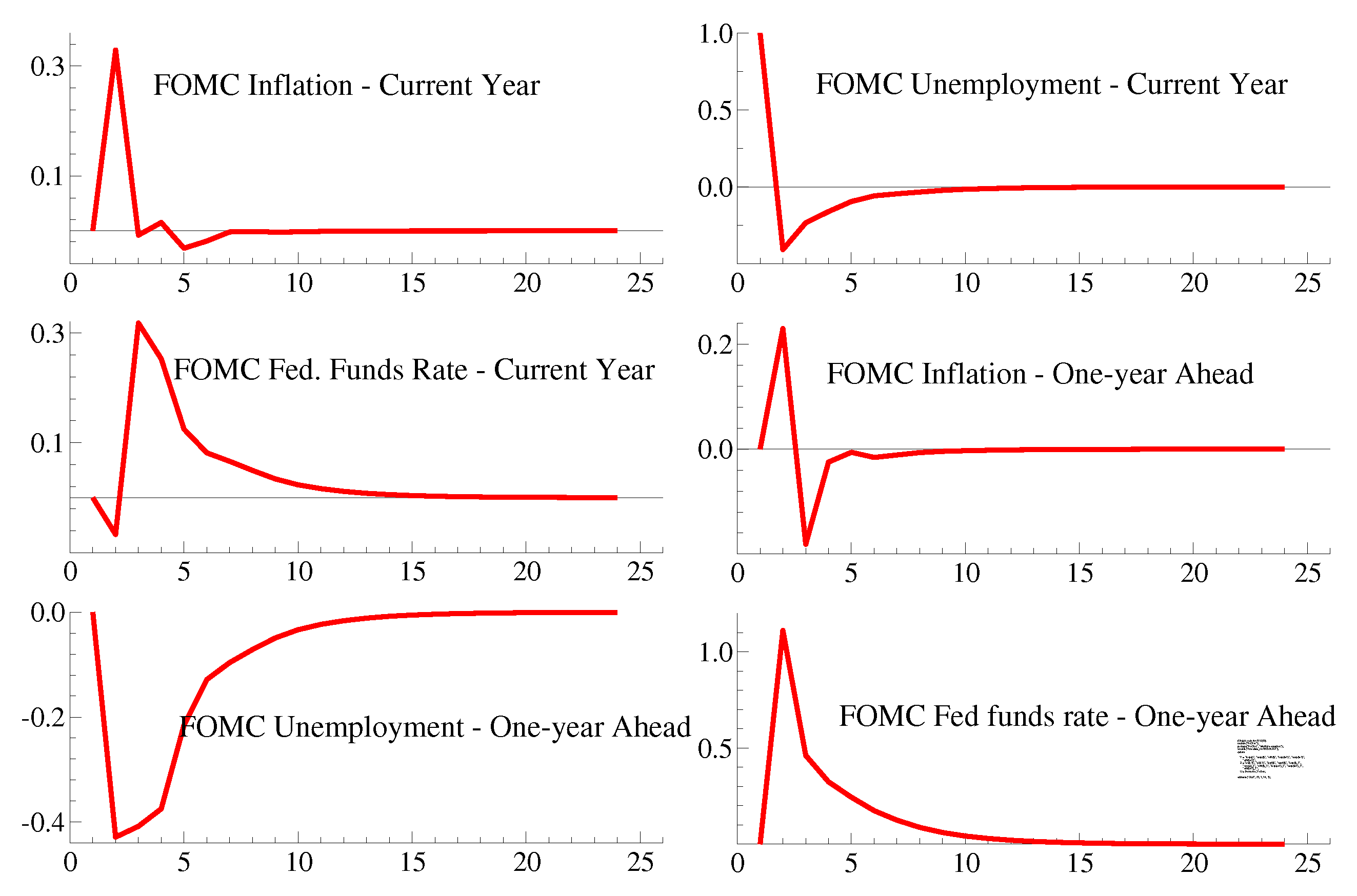

Vector Autoregresive Approach

“Incredible Restrictions” Formulation

3.2.2. Sensitivity Assessment

- Increases in the actual inflation rate raises the federal funds

- An increase of one percentage point in the SPF unemployment rate reduces the federal funds rate from 30 to 50 basis points.

- Chair-specific effects are significant and positive across models; the point estimates are somewhat sensitive to the estimation method. These effects reflect the power of persuasion of the FOMC Chair.

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Arai, Natsuki. 2015. Evaluating the Efficiency of FOMC’s New Economic Projections. Journal of Money, Credit and Banking 48: 1019–49. [Google Scholar] [CrossRef]

- Bernanke, Ben. 2016. Federal Reserve Economic Projections: What Are They Good for? Available online: https://www.brookings.edu/blog/ben-bernanke/2016/11/28/federal-reserve-economic-projections/ (accessed on 13 November 2018).

- Doornik, Jurgen A., and David F. Hendry. 2013. PcGive 14. 3 vols, London: Timberlake Consultants Press. [Google Scholar]

- Faust, Jon. 2016. Available online: https://www.brookings.edu/wp-content/uploads/2016/11/wp25_faust_monetarypolicytransparency_final1.pdf (accessed on 13 November 2018).

- Fendel, Ralf, and Jan-Christoph Rülke. 2012. Are Heterogenous FOMC Forecasts Consistent with the Fed’s Monetary Policy? Economic Letters 116: 5–7. [Google Scholar] [CrossRef]

- Granger, Clive, and David F. Hendry. 2004. A Dialogue Concerning a New Instrument for Econometric Modeling. Econometric Theory 21: 278–97. [Google Scholar] [CrossRef]

- Hendry, David F., and Hans-Martin Krolzig. 2003. New Developments in Automatic General-to-Specific Modeling. In Econometrics and the Philosophy of Economics. Edited by Bernt Stigum. Princeton: Princeton University Press. [Google Scholar]

- Nakazono, Yoshiyuki. 2013. Strategic Behavior of Federal Open Market Committee Board Members: Evidence from Member’s Forecasts. Journal of Economic Behavior & Organization 93: 62–70. [Google Scholar]

- Phillips, Peter. 2004. Automated Discovery in Econometrics. Cowles Foundation Discussion Paper No. 1469. New Haven: Yale University. [Google Scholar]

- Powell, Jerome. 2018. Monetary Policy in a Changing Economy. Available online: https://www.federalreserve.gov/newsevents/speech/files/powell20180824a.pdf (accessed on 13 November 2018).

- Romer, David. 2010. A New Data Set on Monetary Policy: The Economic Forecasts of Individual Members of the FOMC. Journal of Money, Credit, and Banking 42: 951–57. [Google Scholar] [CrossRef]

- Rülke, Jan-Christoph, and Peter Tillman. 2011. Do FOMC Members Herd? Economic Letters 11: 176–79. [Google Scholar] [CrossRef]

- Sheng, Simon. 2015. Evaluating the Economic Forecasts of FOMC Members. International of Forecasting 31: 165–75. [Google Scholar] [CrossRef]

- Tillman, Peter. 2011. Strategic Forecasting of the FOMC. European Journal of Political Economy 27: 547–53. [Google Scholar] [CrossRef][Green Version]

- Yellen, Janet. 2018. Interview. Available online: https://www.brookings.edu/wp-content/uploads/2018/03/es_20180227_yellen_bernanke_transcript.pdf (accessed on 13 November 2018).

| 1 | See also Page 3 of http://www.federalreserve.gov/mediacenter/files/FOMCpresconf20151216.pdf. Please note that FOMC participants are not picking just any value of the federal funds rate they deem appropriate. Rather, their values vary in steps of 0.125 percentage points; the steps might vary from meeting to meeting. Thus, their interpretation of the appropriate monetary policy is not unconstrained. |

| 2 | |

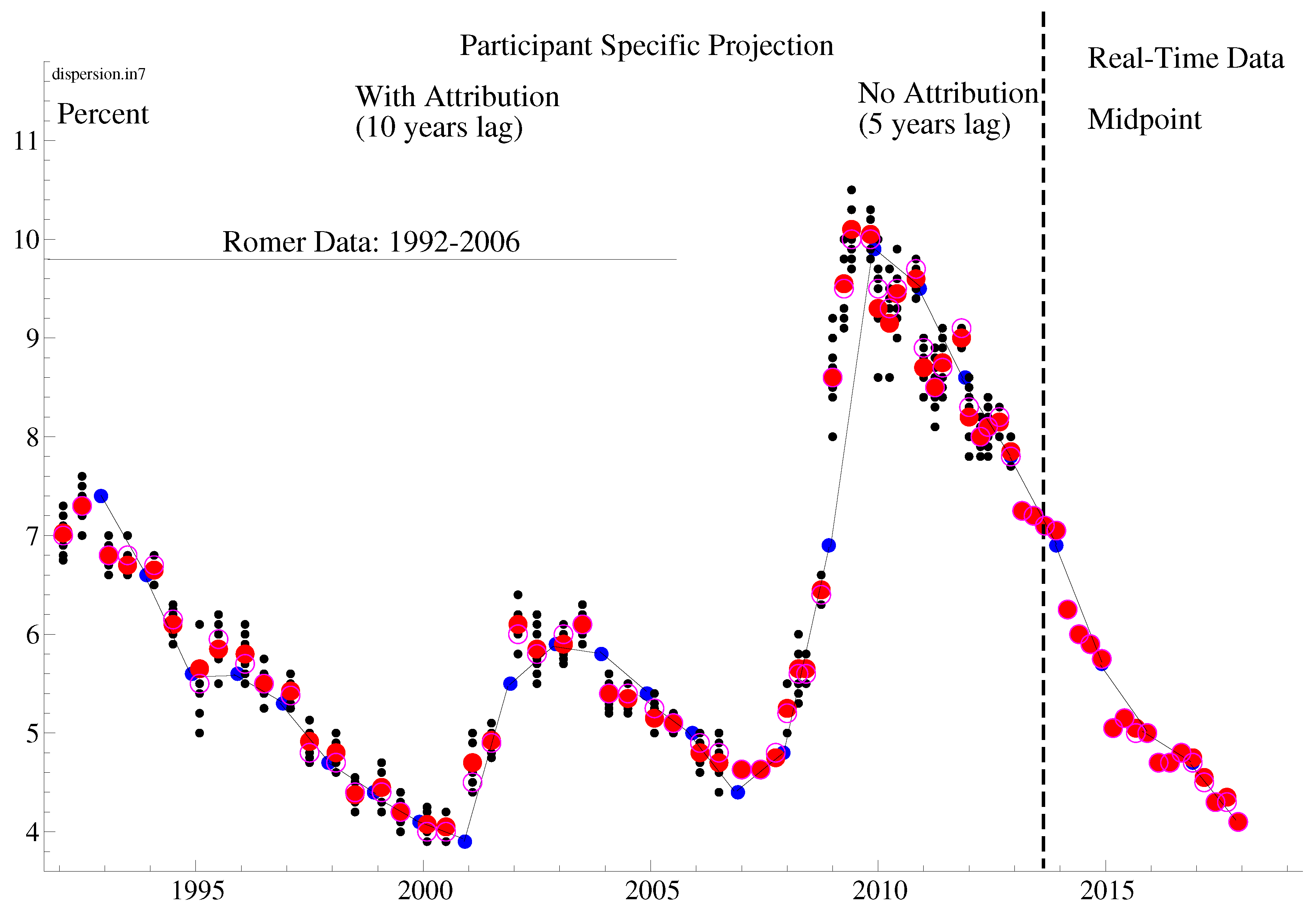

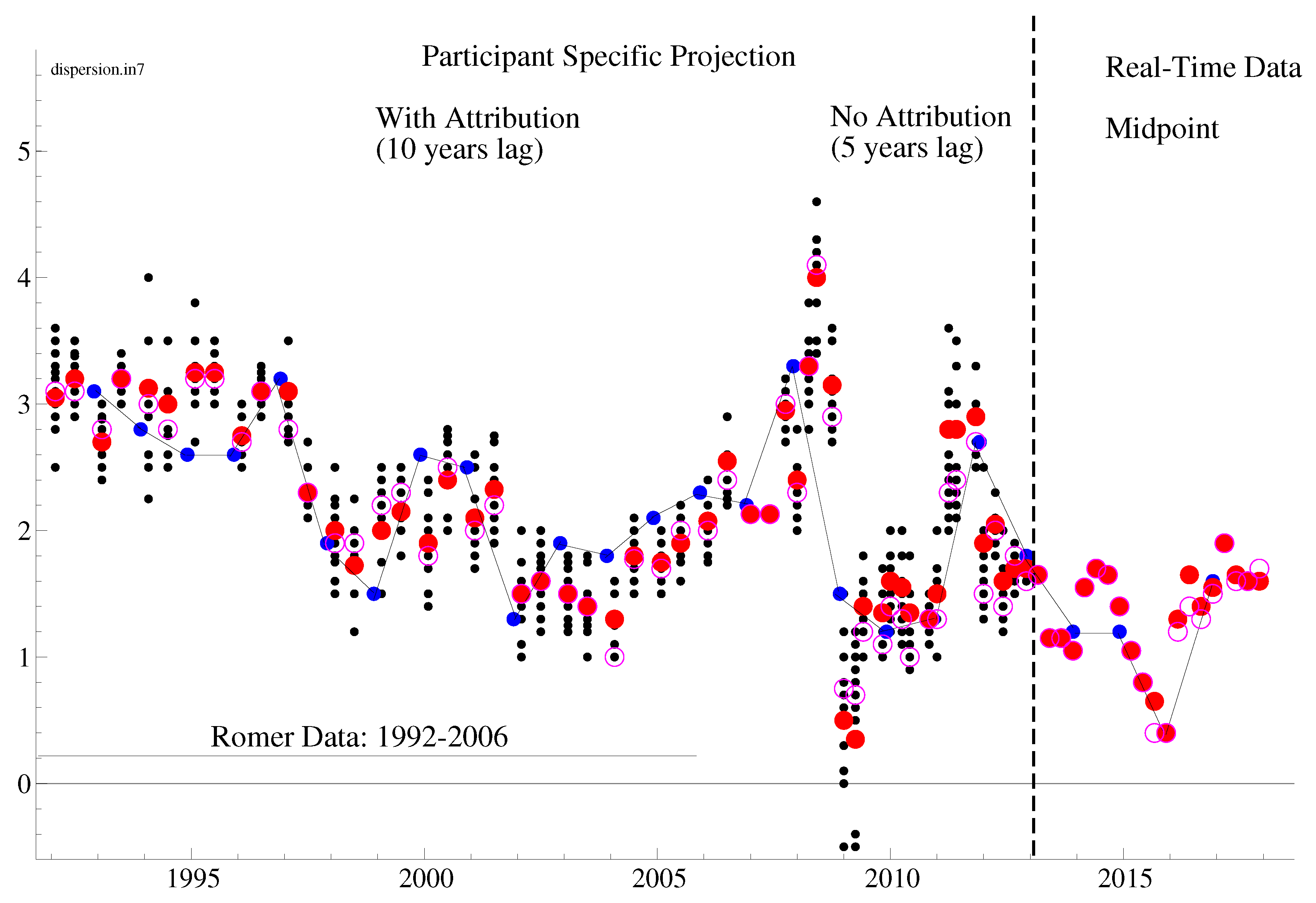

| 3 | The data assembled by Romer (2010) contains participant-specific projections for 1992 to 2006 with attribution. We replicated his data, added the observations for 2007 with attribution, and extended the data to include FOMC participants through 2012 but without attribution because they are not available. Please note that there are no comparable data for the interest rates. |

| 4 | Note, further, that forecast accuracy is not an FOMC mandate. Intuitively, FOMC participants are not impartial observers of their own forecasts but rather must influence the economy to meet their dual mandate. As a result, a narrow interpretation of forecast accuracy is not useful if that accuracy means high inflation and high unemployment. Furthermore, forecast revisions cannot be unambiguously interpreted as reactions to news. As indicated earlier, FOMC participants’ projections depend on their assessments of the appropriate monetary policy. Thus, even if FOMC participants had and released a shared knowledge of the economy, its usefulness to the public would be transitory because the makeup of the FOMC participants changes over time. New participants would bring their own interpretation of appropriate monetary policy which would translate into different interest-rate projections, even in the absence of economic news. |

| 5 | Previous work includes Arai (2015); Fendel and Rülke (2012); Nakazono (2013); Rülke and Tillman (2011), and Sheng (2015). |

| 6 | Please note that adherence to a single reaction function contradicts the FOMC directive embodied in the SEP. |

| 7 | The above remarks raise several questions. First, why do Faust and Bernanke use the singular when referring to the reaction function? Indeed, the FOMC directive associated with the SEP allows for the possibility of 19 reaction functions. Heuristically, the FOMC participant determines the appropriate interest rate that minimizes the welfare loss of deviations of inflation and unemployment from the dual mandate. Subject to the behavior of the economy, the FOMC participant would solve

|

| 8 | We focus on these two variables because the record of press releases of FOMC decisions and Bluebooks, documenting the alternative options over which FOMC members vote, indicates that the outlook for economic activity (i.e., unemployment) and inflation are the most important considerations for determining the outlook for interest rates. See page 52 of https://www.federalreserve.gov/monetarypolicy/files/FOMC20090128bluebook20090122.pdf. |

| 9 | Please note that the median of R need not correspond to a participant with the median of or Mismatch of medians can be solved if the FOMC released the participant-specific projections with attribution. |

| 10 | One way to detect extreme values is to see if the distributions of forecasts are asymmetric. Because normal distributions are symmetric, finding evidence of normality would reject the presence of fat-tails or extreme forecasts. |

| 11 | Please note that we do not include Greenbook/Teal book forecasts as an alternative to publicly available data in real time because they are released with a five-year delay. |

| 12 | For a discussion of the issues raised by automated specification, see Hendry and Krolzig (2003); Granger and Hendry (2004); and Phillips (2004). |

| 13 | The FOMC also provides projections for two and three years ahead but modeling those is beyond the scope of this paper. |

| 14 | Data sources and the associated time series properties are available on request. |

| 15 | The reduced form coefficients for Equation (1) above is

|

| 16 | Nevertheless, the Board of Governors posts the Eviews files needed to run the staff’s model FRB/US; see https://www.federalreserve.gov/econres/us-models-package.htm. This posting requires of the public an intimate familiarity with computer software. Even if that familiarity is present, one should not associate the views of the Board with the views of the FOMC as the dispersion of forecasts for the last 15 years demonstrates. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | GUM/OLS | Autometrics/Significance Level | ||||

|---|---|---|---|---|---|---|

| 1% | 0.01% | |||||

| Coeff | Std.Err | Coeff | Std.Err | Coeff | Std.Err | |

| 0.71 | 0.31 | 0.56 | 0.16 | – | – | |

| Yellen | −0.38 | 1.10 | 1.54 | 0.55 | 2.82 | 0.37 |

| Bernanke | −0.92 | 1.53 | 1.87 | 0.73 | 3.42 | 0.55 |

| Powell | 0.15 | 1.19 | 2.26 | 0.58 | 3.55 | 0.36 |

| −0.02 | 0.81 | −0.23 | 0.09 | −0.46 | 0.07 | |

| 0.42 | 0.50 | – | – | – | – | |

| 0.09 | 0.28 | – | – | 0.25 | 0.08 | |

| 0.84 | 0.44 | – | – | – | – | |

| −0.17 | 0.32 | – | – | – | – | |

| −0.18 | 0.28 | – | – | – | – | |

| −0.62 | 0.40 | – | – | – | – | |

| −0.04 | 0.26 | – | – | – | – | |

| −0.55 | 0.62 | – | – | – | – | |

| −0.44 | 0.61 | – | – | – | – | |

| −0.51 | 0.28 | – | – | – | – | |

| 0.072 | 0.61 | – | – | – | – | |

| SER | 0.18 | 0.20 | 0.21 | |||

| Adj.Rsqrd | 0.88 | 0.86 | 0.85 | |||

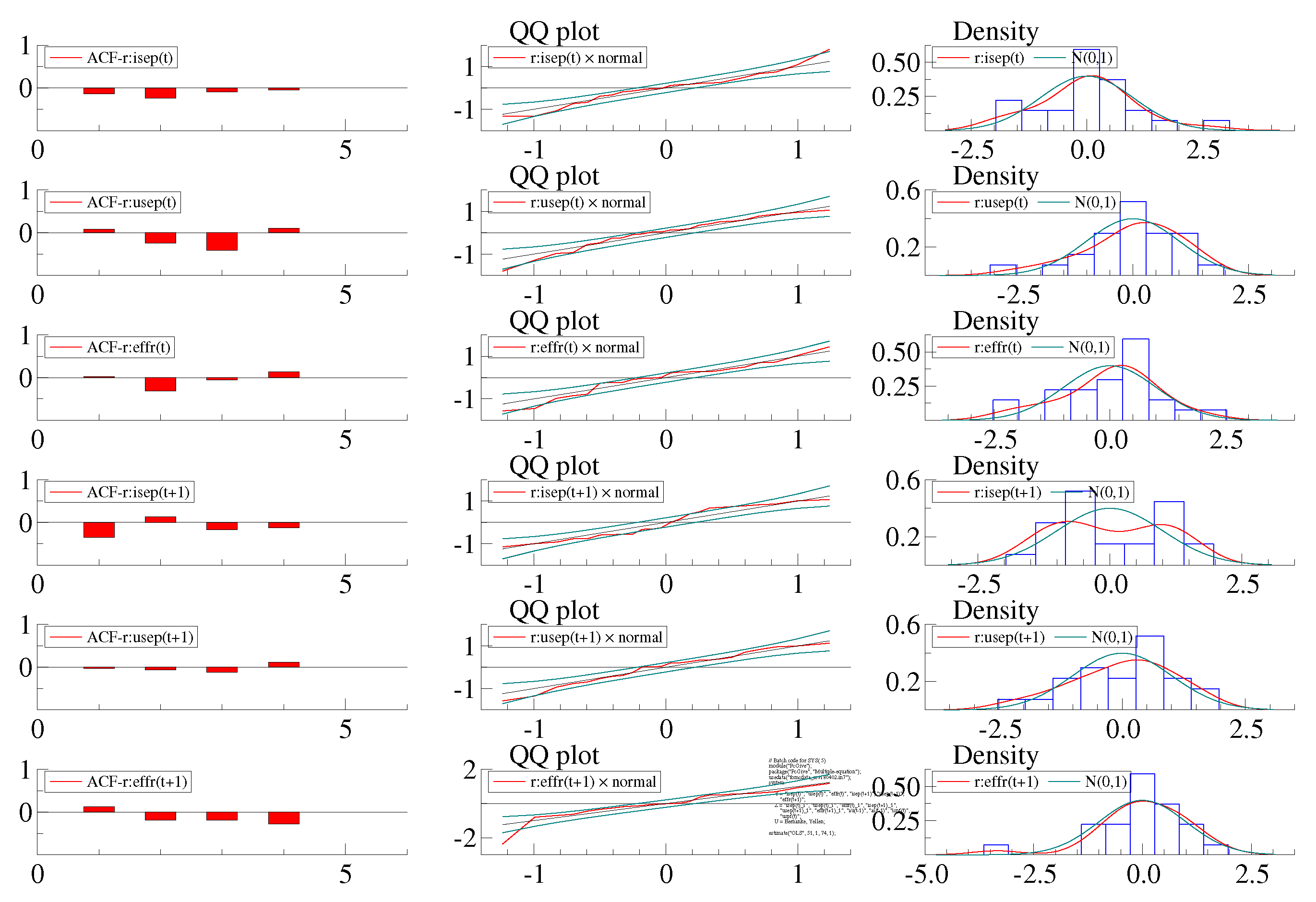

| Residual Properties | ||||||

| H Serial independence | 0.48 | 0.17 | 0.10 | |||

| H Homoskedasticity | 0.73 | 0.59 | 0.64 | |||

| H Normality | 0.45 | 0.05 | 0.31 | |||

| Parameters | 16 | 5 | 5 | |||

| Current Year Bloc | One-Year Ahead Bloc | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | ||||||

| 0.666 | 0.394 | 0.387 | 0.137 | 0.914 | −1.37 | ||||||

| 0.185 | 0.086 | 0.124 | 0.067 | 0.060 | 0.947 | ||||||

| 0.069 | 0.795 | 0.279 | −0.059 | 0.364 | 5.484 | ||||||

| 0.207 | 0.100 | 0.113 | 0.048 | 0.597 | 3.953 | ||||||

| 0.200 | −0.398 | −0.315 | −0.717 | ||||||||

| 0.15 | 0.082 | 0.085 | 0.42 | ||||||||

| −0.272 | 0.176 | 0.522 | |||||||||

| 0.281 | 0.109 | 0.241 | |||||||||

| −0.361 | −0.223 | ||||||||||

| 0.518 | 0.186 | ||||||||||

| 2.164 | 1.166 | 2.079 | 1.942 | −0.513 | −4.027 | ||||||

| 1.965 | 0.691 | 0.642 | 0.345 | 1.316 | 6.711 | ||||||

| 1.775 | 0.784 | 1.664 | 1.970 | −0.490 | −5.081 | ||||||

| 1.553 | 0.538 | 0.463 | 0.240 | 1.289 | 6.962 | ||||||

| Properties of Residuals | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| SER | Normality | Indep | Homosk | ||||||||

| Single/Autometrics | 0.25 * | - | - | −0.46 * | 3.42 * | 2.82 * | 3.55 * | 0.21 | 0.31 | 0.10 | 0.64 |

| VAR/OLS | 0.26 | 0.17 | −0.01 | −0.50 | 3.47 * | 2.81 * | 2.81 | 0.21 | 0.49 | 0.85 | 0.14 |

| Constrained VAR/FIML | 0.29 * | 0.03 | −0.17 * | −0.34 * | 3.63 * | 2.99 | 2.99 | 0.19 | 0.96 | 0.20 | 0.84 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kalfa, S.Y.; Marquez, J. FOMC Forecasts: Are They Useful for Understanding Monetary Policy? J. Risk Financial Manag. 2019, 12, 133. https://doi.org/10.3390/jrfm12030133

Kalfa SY, Marquez J. FOMC Forecasts: Are They Useful for Understanding Monetary Policy? Journal of Risk and Financial Management. 2019; 12(3):133. https://doi.org/10.3390/jrfm12030133

Chicago/Turabian StyleKalfa, S. Yanki, and Jaime Marquez. 2019. "FOMC Forecasts: Are They Useful for Understanding Monetary Policy?" Journal of Risk and Financial Management 12, no. 3: 133. https://doi.org/10.3390/jrfm12030133

APA StyleKalfa, S. Y., & Marquez, J. (2019). FOMC Forecasts: Are They Useful for Understanding Monetary Policy? Journal of Risk and Financial Management, 12(3), 133. https://doi.org/10.3390/jrfm12030133