Testing Stylized Facts of Bitcoin Limit Order Books

Abstract

:1. Introduction

- Structured framework for analyzing limit order book data: First, following the literature, we establish a structured framework for the extraction of empirical properties from LOB data and trade flows. The substantial body of literature addressing LOB data from established exchanges serves as a baseline for our work as well as other studies addressing cryptocurrencies.

- Recovery of common qualitative facts: Second, using a large-scale limit order data set, we can confirm that many empirical observations from more mature markets also transfer to major exchanges for the BTC/USD currency pair, most notably:

- Symmetric average limit order book: We recover the commonly observed symmetry between the bid and the ask side of the time-averaged LOB.

- Dispersion of liquidity: Liquidity is dispersed over many levels of the order book, and small values of depth at the best bid and ask occur with highest probability.

- No autocorrelation in lower-frequency returns: We do not observe significant autocorrelation in the series of returns on time scales from minutes to days.

- Negative autocorrelation in tick-level returns (bid-ask bounce): The series of trade-to-trade price changes exhibits negative autocorrelation in the first lags.

- Volatility clustering: The autocorrelation of volatility measures exhibits significant positive values even after multiple days.

- Non-normality of returns: The distribution of returns on different time scales shows heavy tails and deviates strongly from the normal distribution.

- Timing of large trades: Trades of large size seem to be executed when liquidity costs are relatively low.

- Power tails in trade size distribution: For trades larger than the minimum order size, we recover a power tail in the distribution of trade size.

- Idiosyncratic observations: Third, we can identify the following key idiosyncrasies:

- Relatively shallow limit order book: Despite narrow bid-ask spreads, liquidity costs increase rapidly once higher volumes are traded. This finding is consistent with Bitcoin traders being retail traders rather than institutional investors.

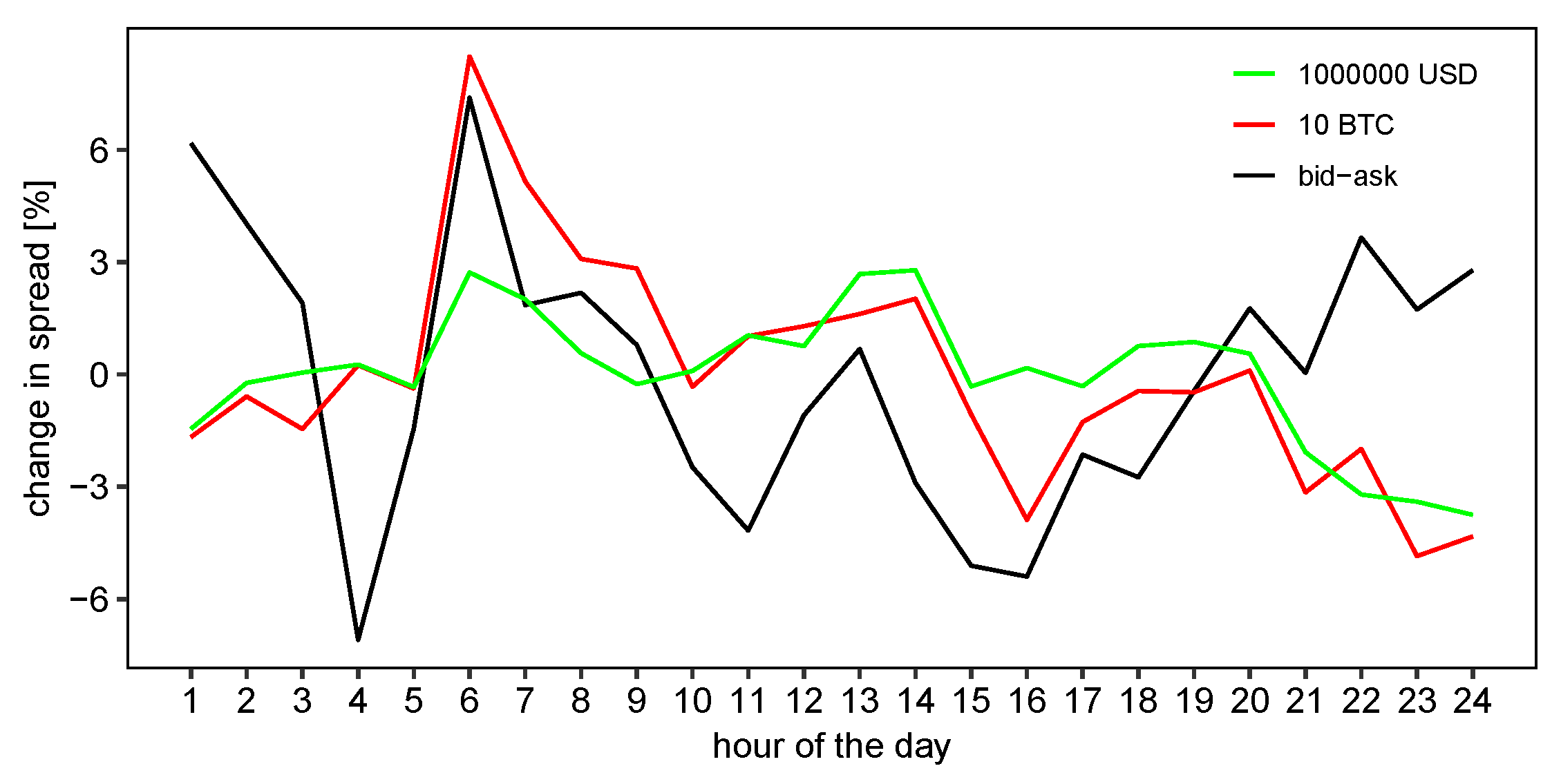

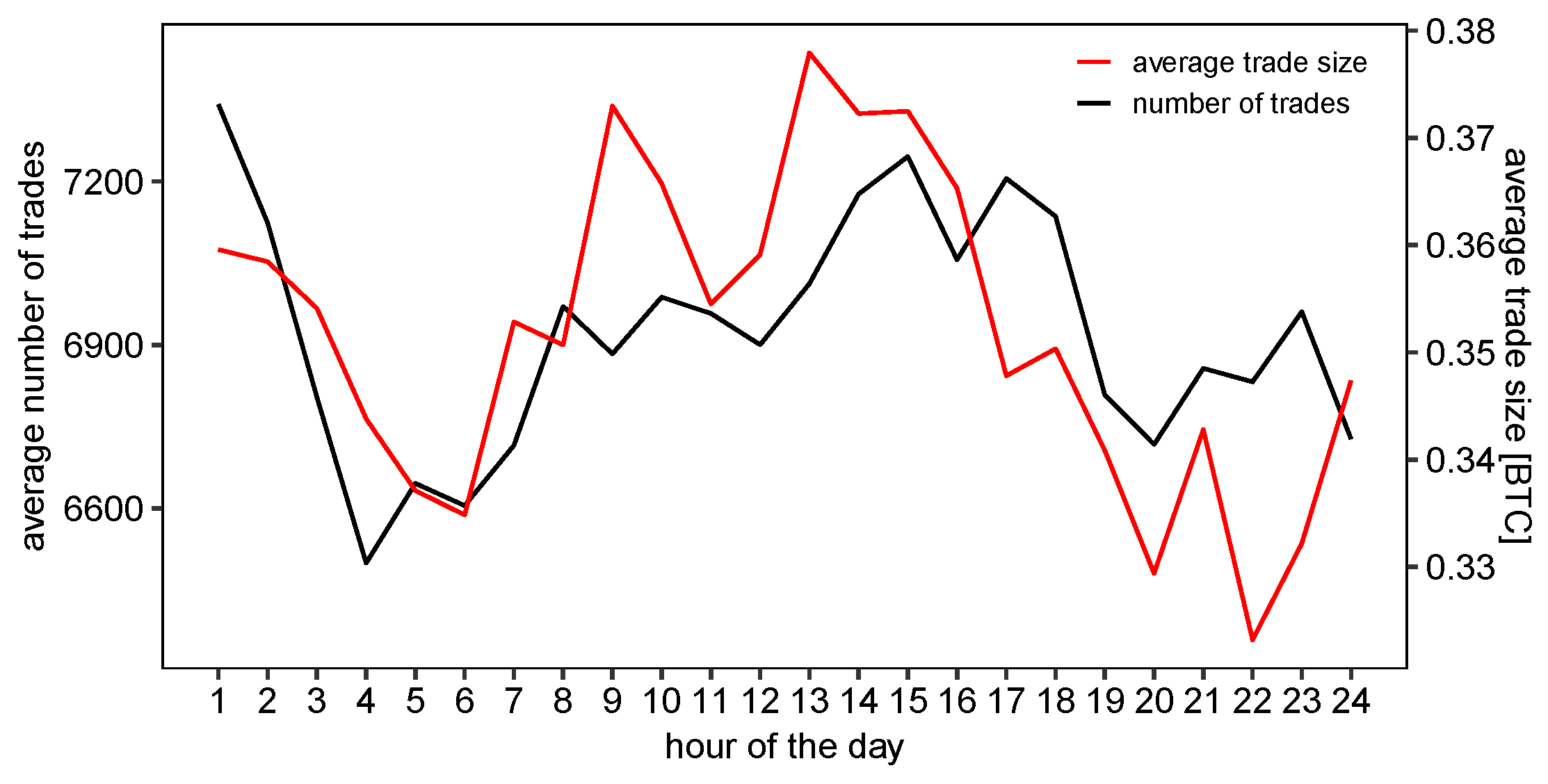

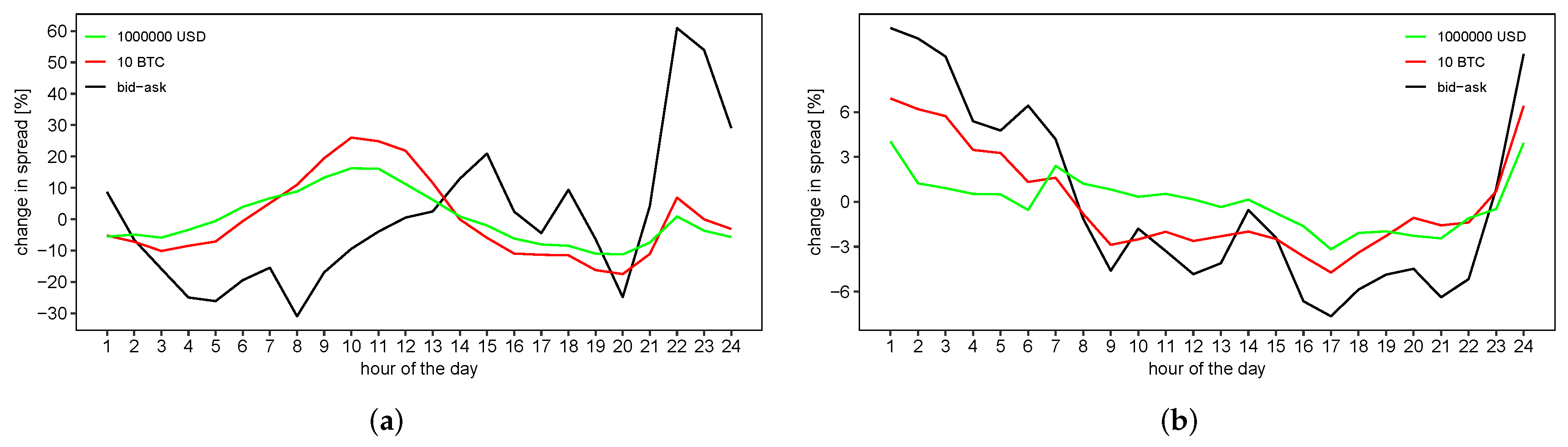

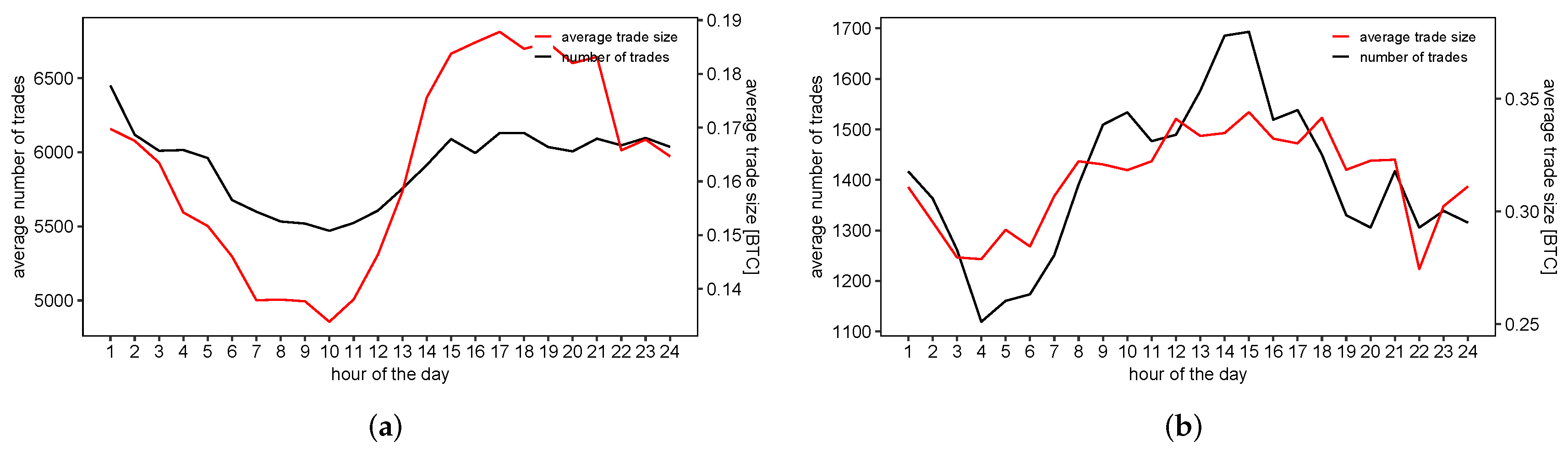

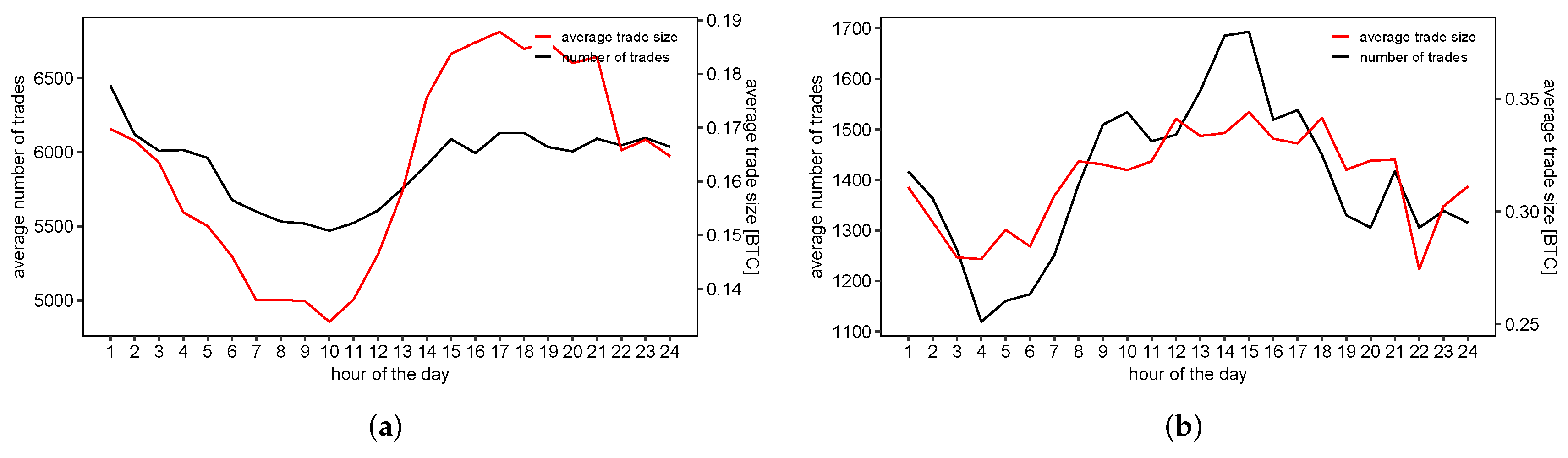

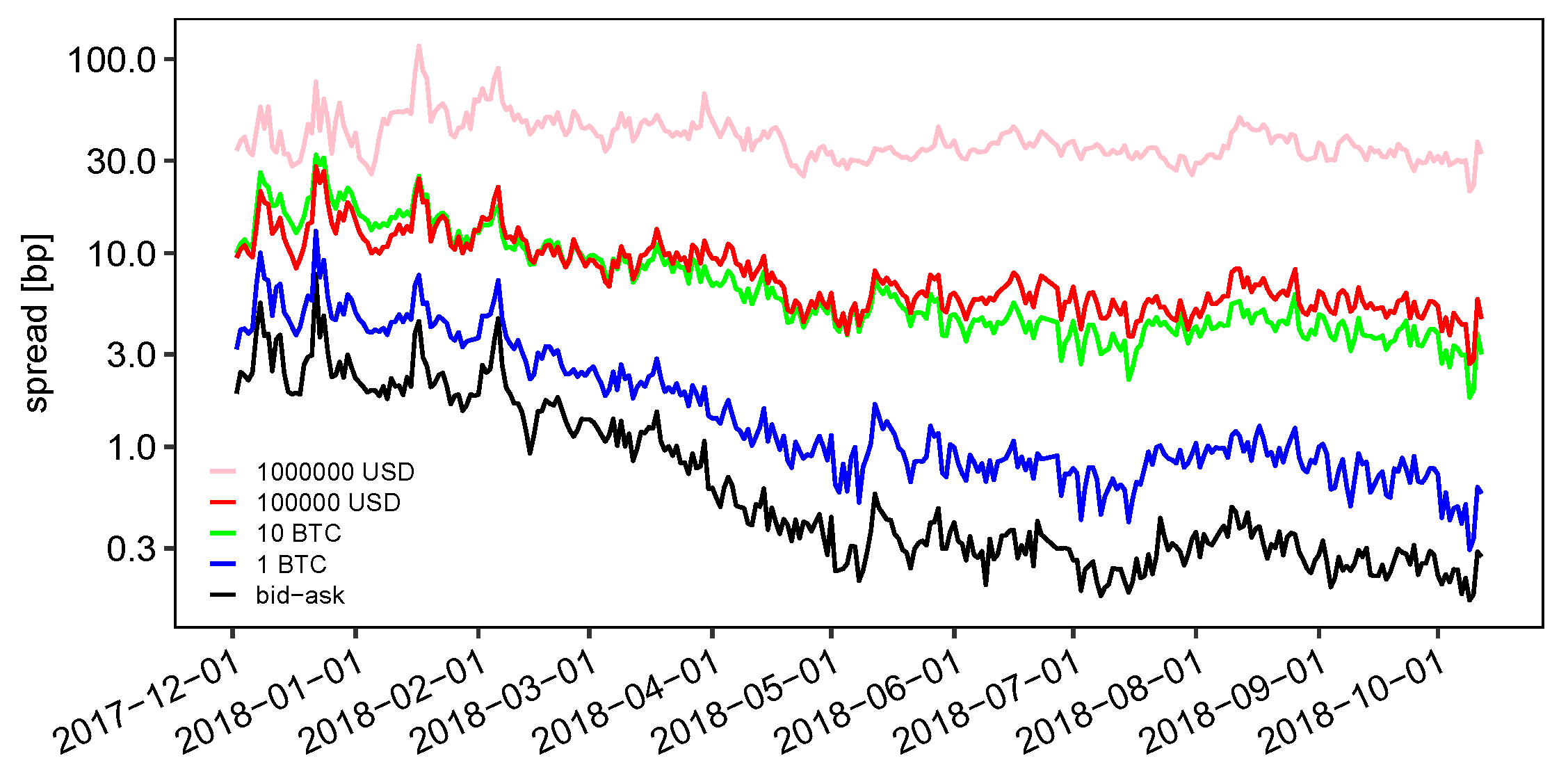

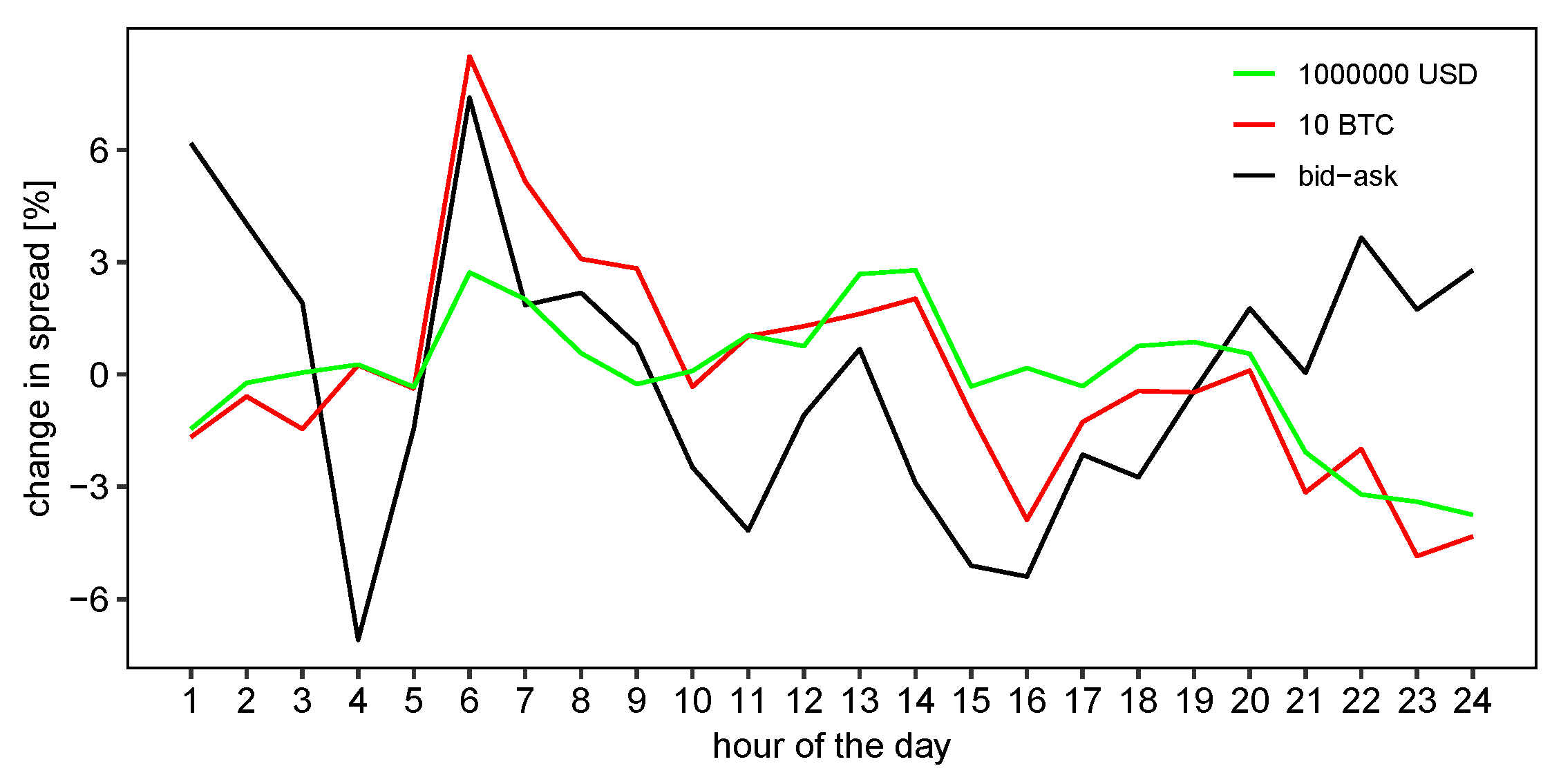

- Weak intraday patterns: Depending on the exchange, we observe either absent or weak intraday patterns in liquidity costs and weak patterns in trade frequency and size. Contrary to traditional markets, there is continuous trading at cryptocurrency exchanges, and our results might indicate a superposition of automated trading and worldwide market participation.

- Frequent minor trades: Many trades are of very small size, i.e., close to the minimum size increment. Unlike most traditional assets, Bitcoin can be traded in increments of with typical minimum order sizes in the order of . These two limits and the predominance of retail trading seems to explain the very broad empirical distribution of trade size with a minimum at the minimum size increment.

- Broad distribution of limit order prices: A large part of limit order volume and changes thereof is located very far away from the current price. Possible reasons are the unlimited lifetime of orders at cryptocurrency exchanges, the speculative placement of orders far away from the current price and the absence of regulatory limits such as price caps for submitted orders.

2. Cryptocurrency Exchange Market Structure

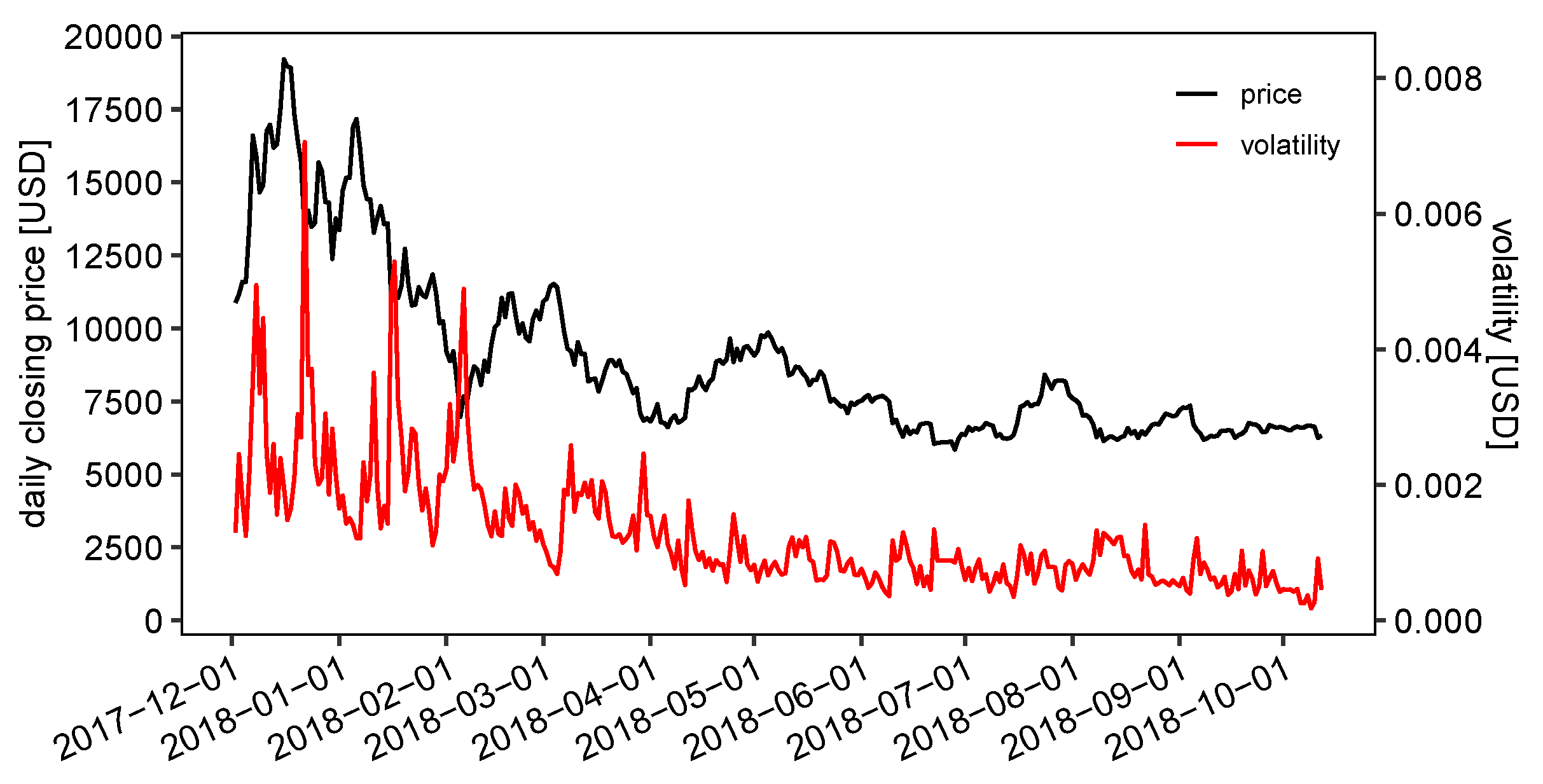

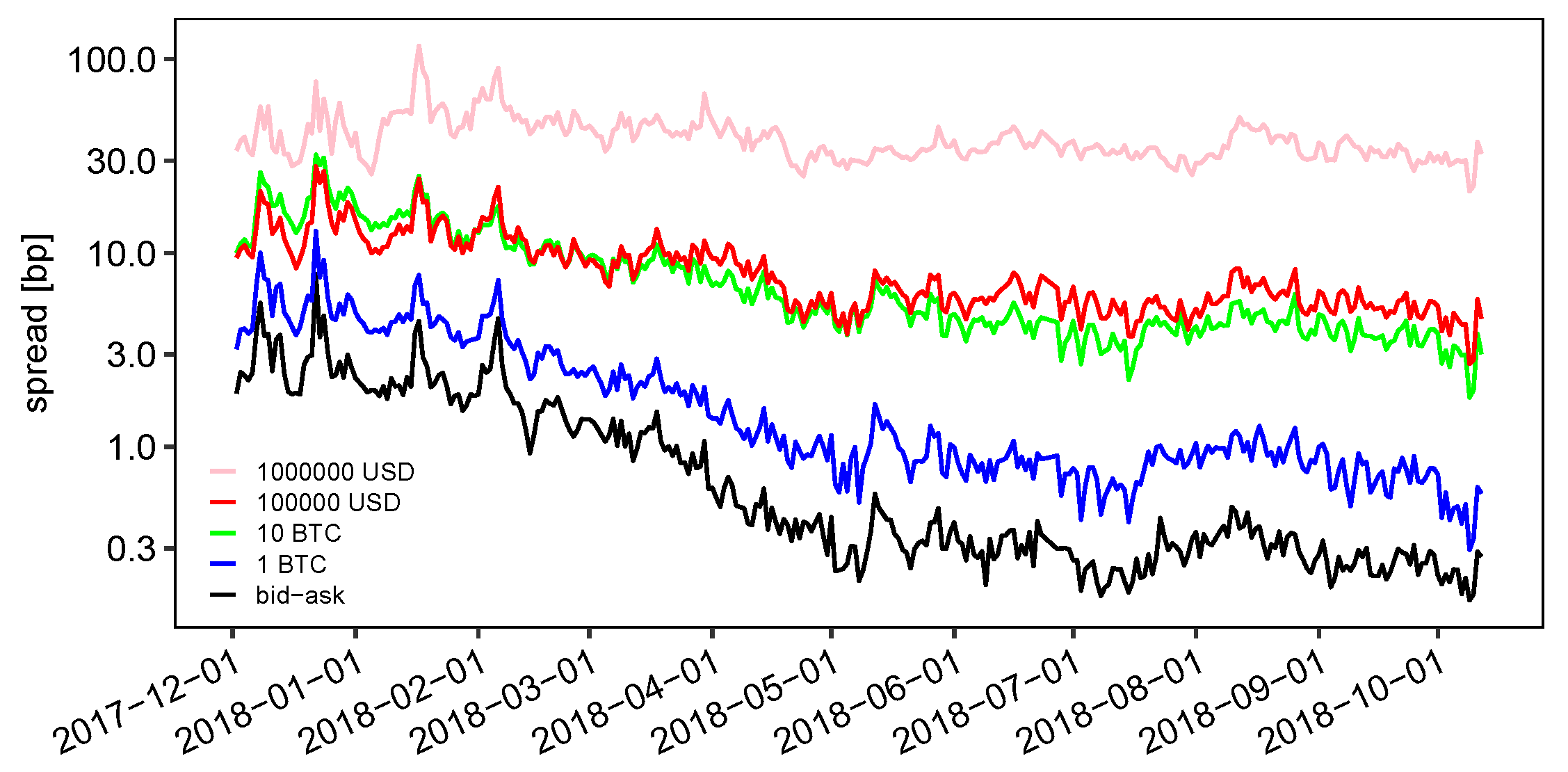

3. Data

4. Methodology

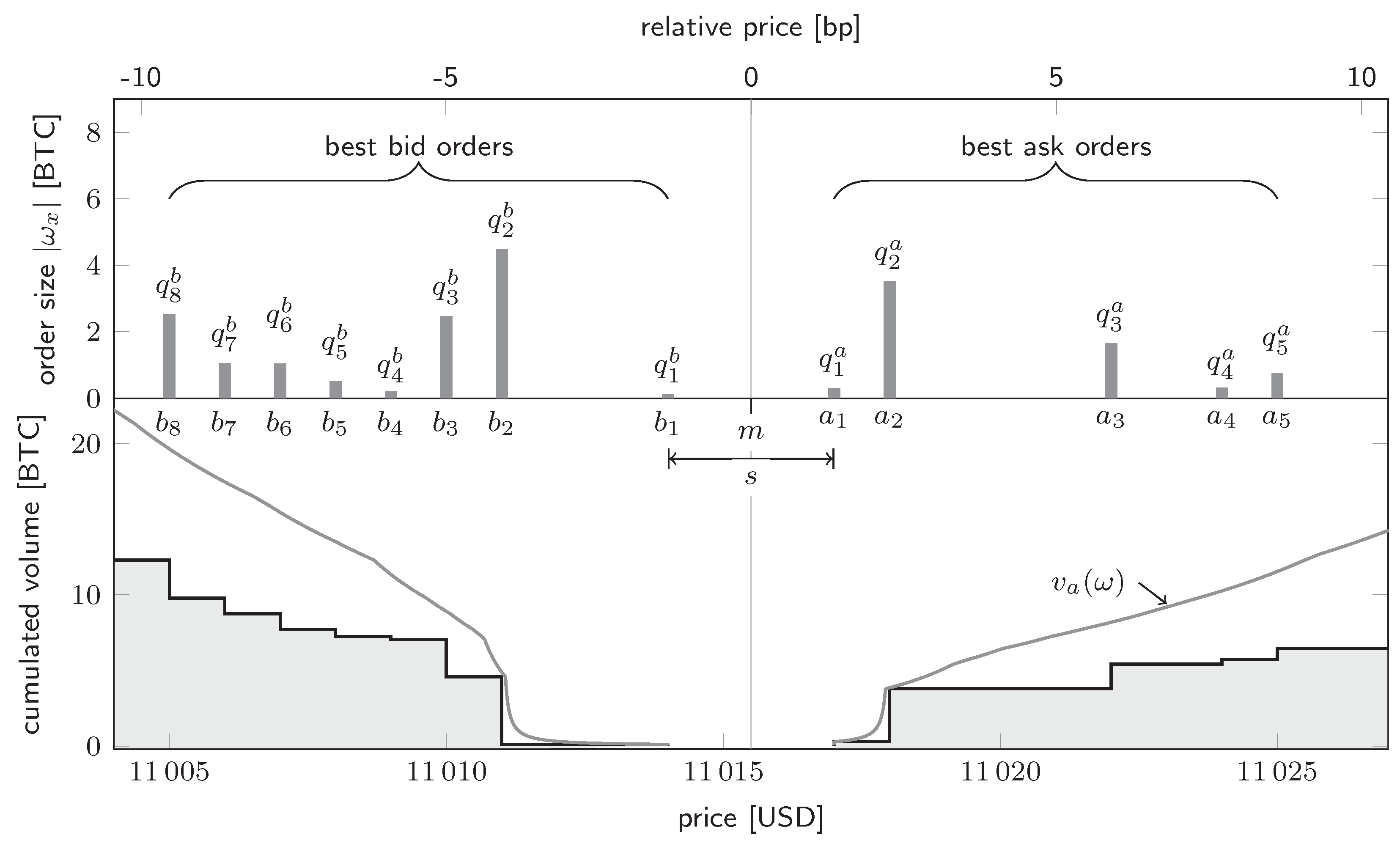

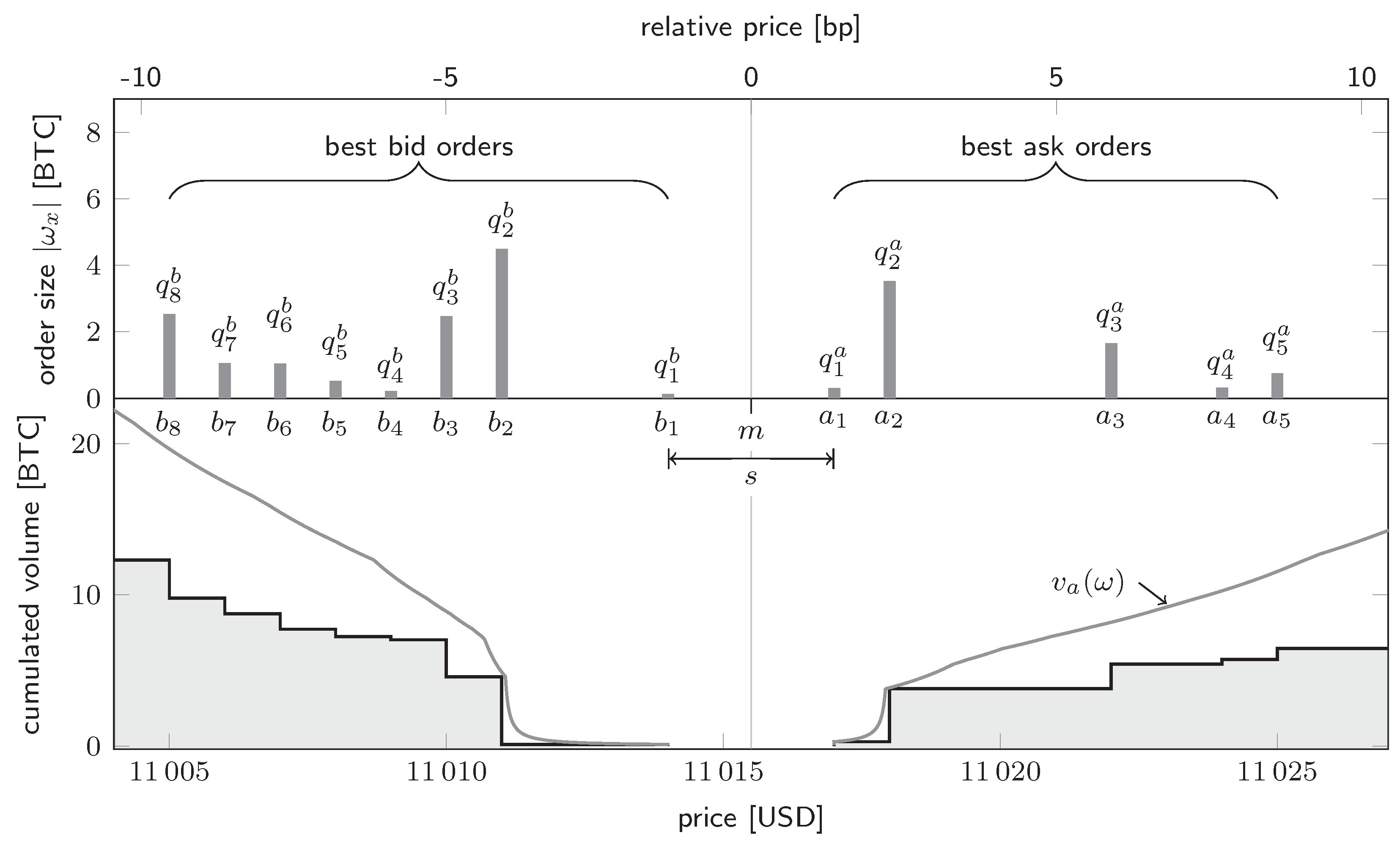

4.1. Basic Notation

4.2. Measures of the Static Limit Order Book

4.2.1. Descriptive Statistics of Unconditional Limit Order Book Measures

4.2.2. Time Series Properties of Limit Order Book Measures

4.2.3. Statistics of Conditional Limit Order Book Measures

4.3. Dynamics of the Limit Order Book: Order and Trade Flows

4.3.1. Descriptive Statistics of Unconditional Measures

4.3.2. Time Series Properties

4.3.3. Statistics of Conditional Trade Measures

5. Results

5.1. Analysis of the Static Limit Order Book

5.1.1. Descriptive Statistics of Unconditional Limit Order Book Measures

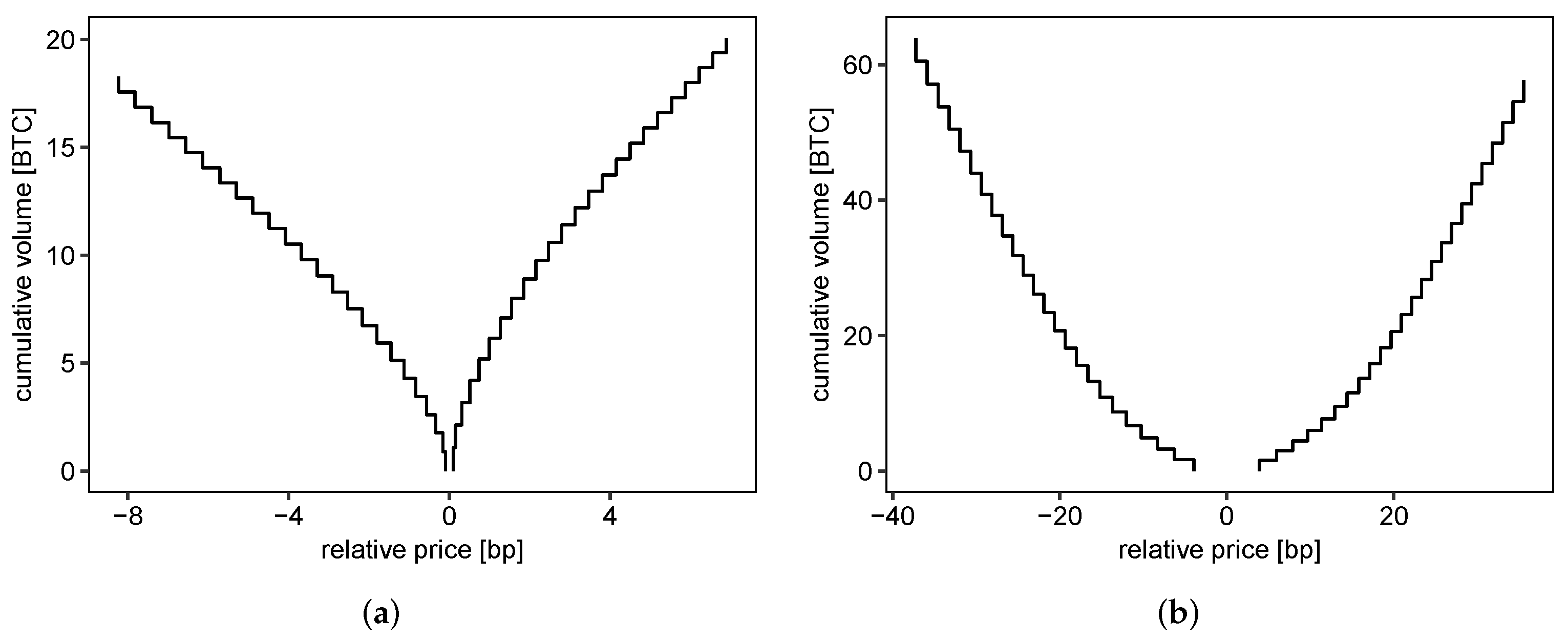

- Symmetry between bid and ask side: There is a high degree of symmetry in the average depth profile of the bid and the ask side: Average prices exhibit very similar absolute values, and depths agree surprisingly well at corresponding steps i. This symmetry is well-known for limit order stock markets (see, for example, Biais et al. (1995), Potters and Bouchaud (2003) and Cao et al. (2009)).

- Dispersion of liquidity: The liquidity provided at the best bid or the best ask price is only a very small part of overall liquidity, and the incremental liquidity provided by each level deeper in the LOB is comparably small. Biais et al. (1995) observe this pattern for equity data from the Paris Bourse, and we find that it is very pronounced in the Bitcoin market: The average level contributes an additional volume of (corresponding to roughly 20000 USD). These small depths may be driven by the fact that the cryptocurrency markets are still dominated by retail trading activity, and that there is still potential for further institutional market making activities—see Chaparro (2017) and Arnold (2018). Furthermore, we find that the average volume at the best ask/bid is triple the volume contributed by levels deeper in the book, which contrasts with Biais et al. (1995) who point out that it is slightly lower.

- Approximately linear price schedule: In agreement with Biais et al. (1995), we observe that the price schedule, i.e., the dependence of the price on demanded or offered quantity, can be approximated very well by linearity and is weakly concave. The concavity seems to be a consequence of an unequal spacing of average price levels rather than a consequence of increasing average volume at each price level. To analyze this in detail, Figure 2b displays the average relative spread between adjacent price levels (Equation (5)) as function of the level number i. The bid and the ask side of the LOB behave very similarly. The largest average difference in price is found directly after the best bid/best ask and amounts to roughly 1.2 bp, which is larger than the average bid-ask spread (0.97 bp). This value then declines to lower values and remains constant at roughly 0.7 bp for higher price levels ().6 The first 25 price levels in the static LOB are therefore denser further away from the bid-ask spread. We might interpret this observation as a consequence of the execution of market orders reducing the limit order volume at the center of the LOB. Orders deeper in the book are less likely to be executed, leading to more densely spaced price levels on average.

- Global maximum at (best) bid and ask: Consistent with the findings from the time-averaged cumulated depth profile, we find the global maximum of volume at the current bid or ask of the LOB. This structure resembles the finding by Potters and Bouchaud (2003) for the SPY exchange-traded fund at Island ECN, where maximum limit order volume is found at the best bid and ask.

- Maximum away from current price: There is a second, local maximum further away from the current bid (or ask), which we locate at relative prices in the order of 1%. We find the location of this maximum to be roughly symmetric between the ask and bid side of the order book. Both Bouchaud et al. (2002) and Gu et al. (2008) report a maximum in the average shape of the LOB located several ticks deep in the order book, yielding a hump-shaped average order book. In contrast to data from the Bitcoin exchange, this maximum is in relation closer to the current price.

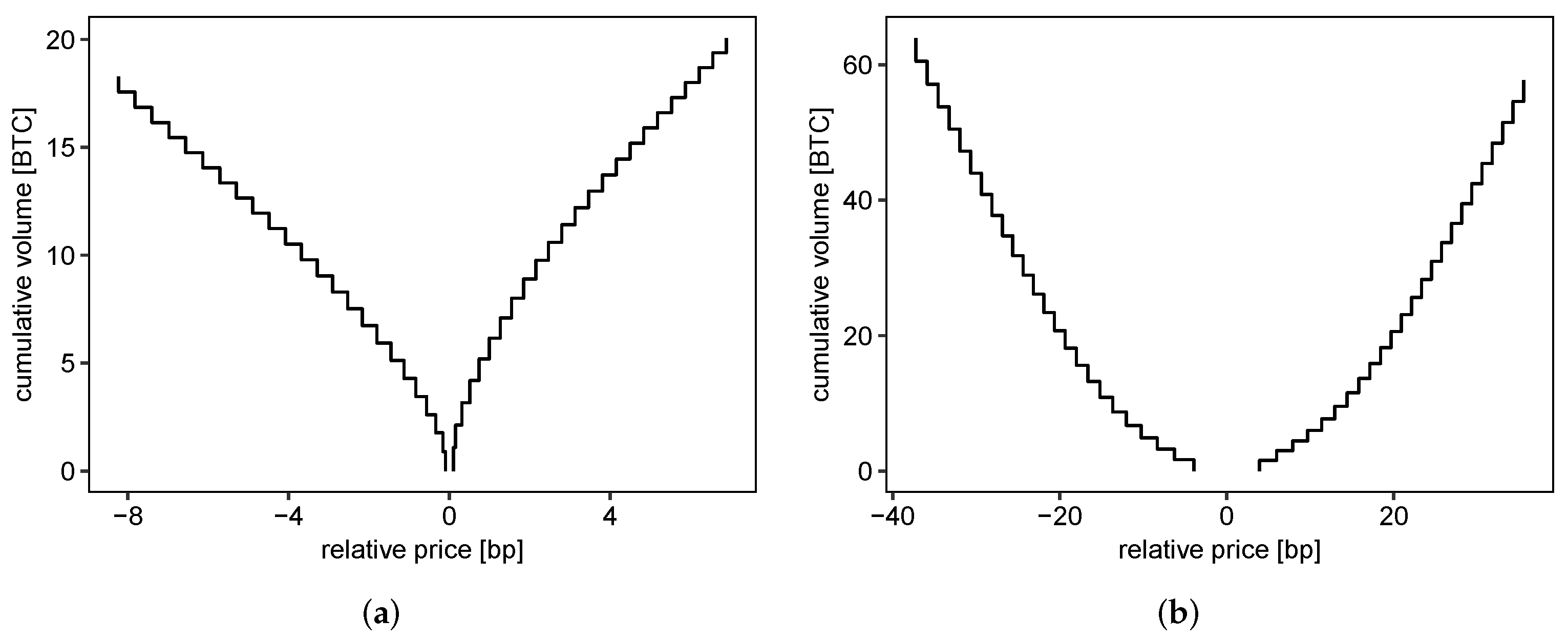

- Bouchaud et al. (2002, Broad distribution of time-averaged volume:) find that orders are placed as far as 50 percent away from the current mid price; however most limit order volume is located within the first 100 ticks surrounding the current price, consistent with the analyses of Potters and Bouchaud (2003) and Gu et al. (2008). In contrast, we find a very broad distribution of volume around the current mid price, which extends with significant shares of the total limit order volume to up to 100 percent of the current mid price, and for the case of ask orders even further.

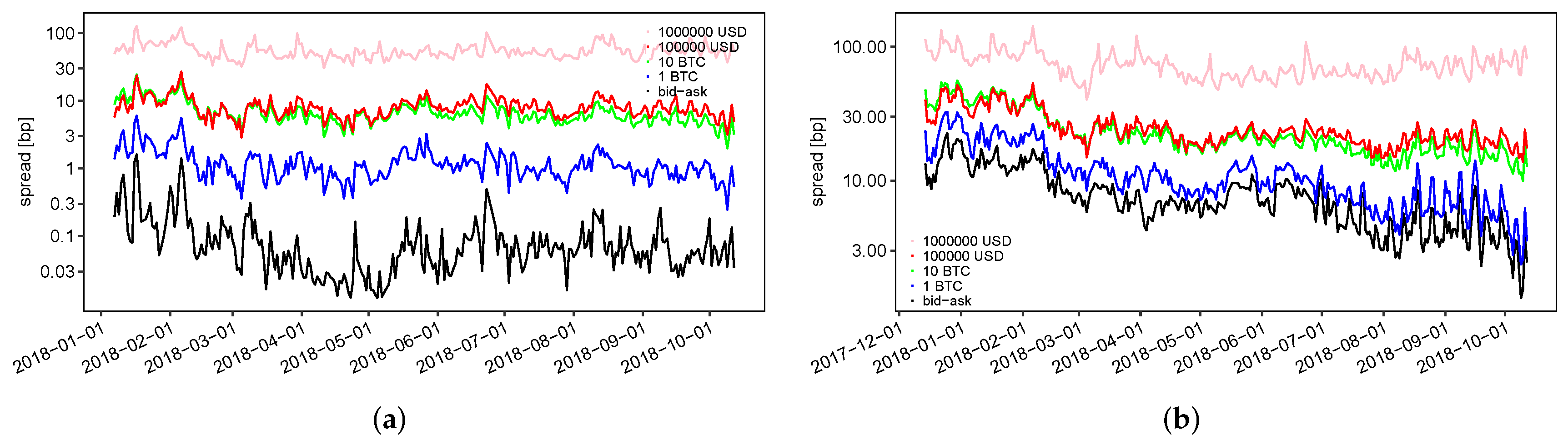

5.1.2. Time Series Characteristics of Statistics

5.1.3. Conditional Statistics of the Limit Order Book

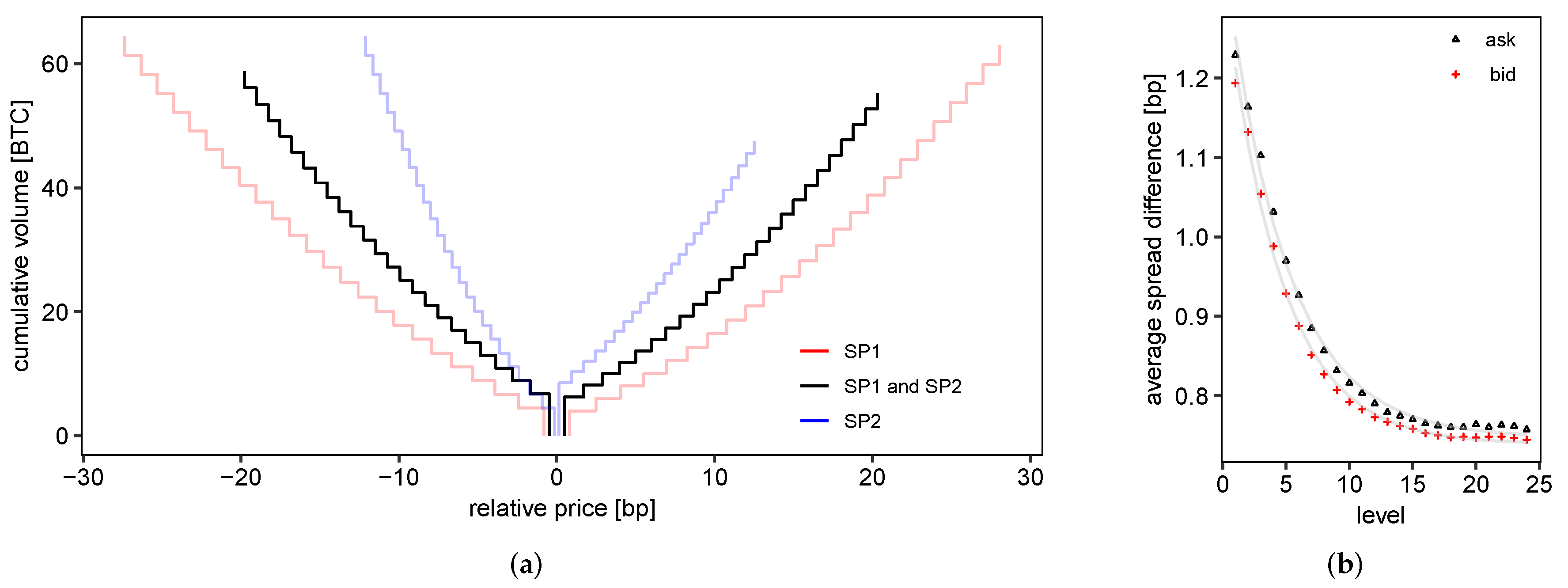

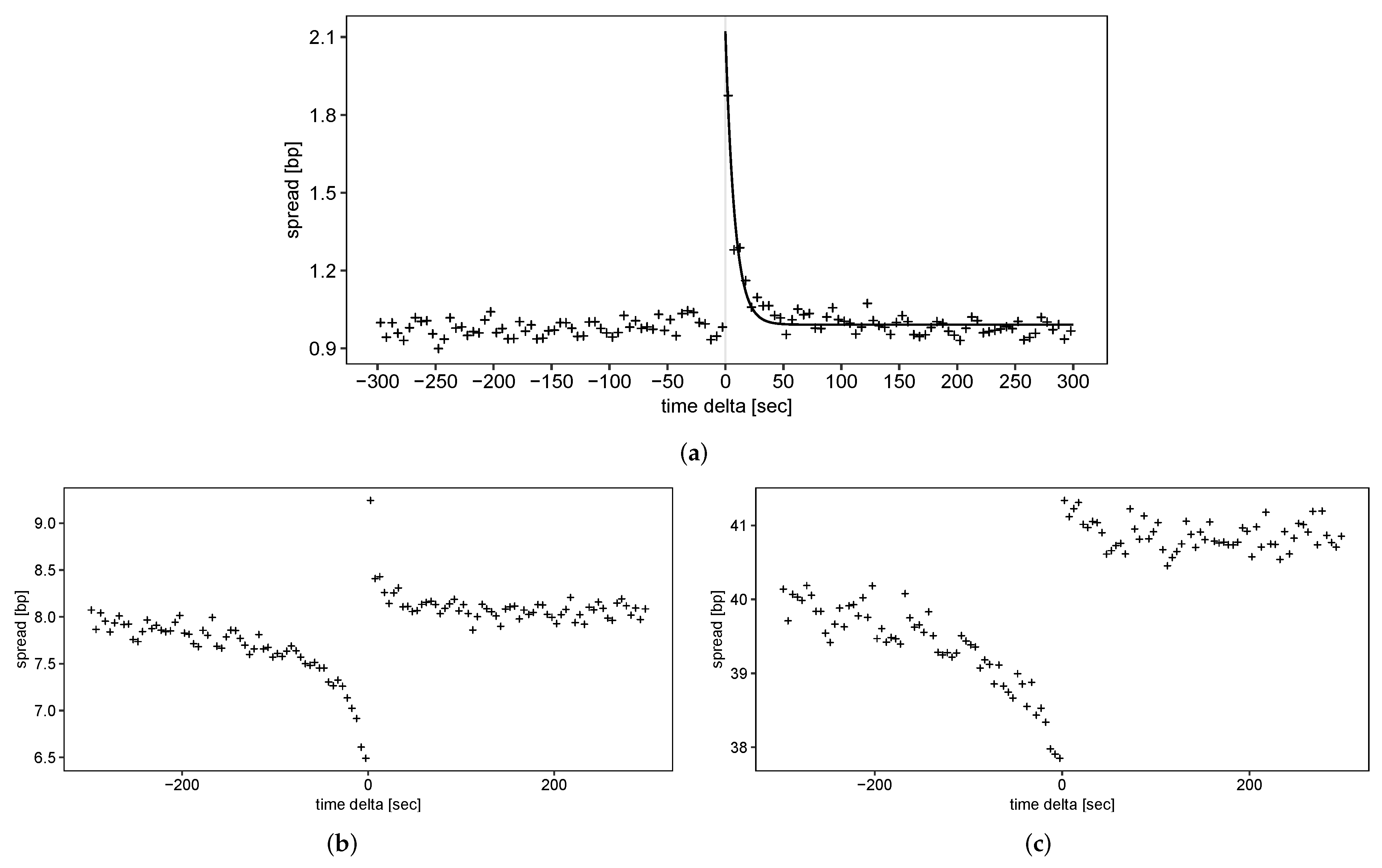

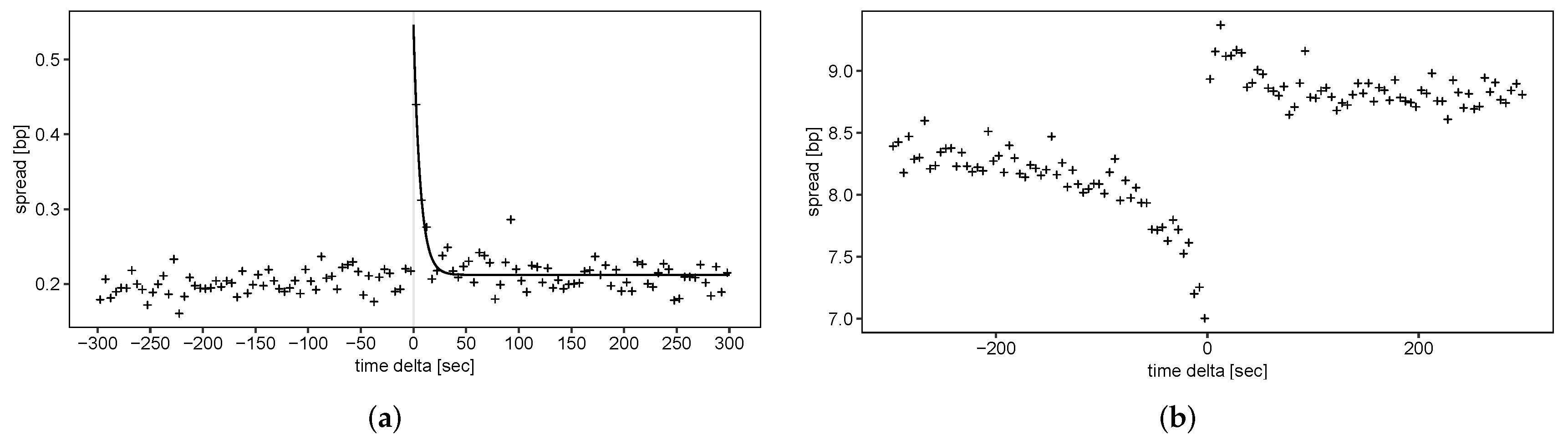

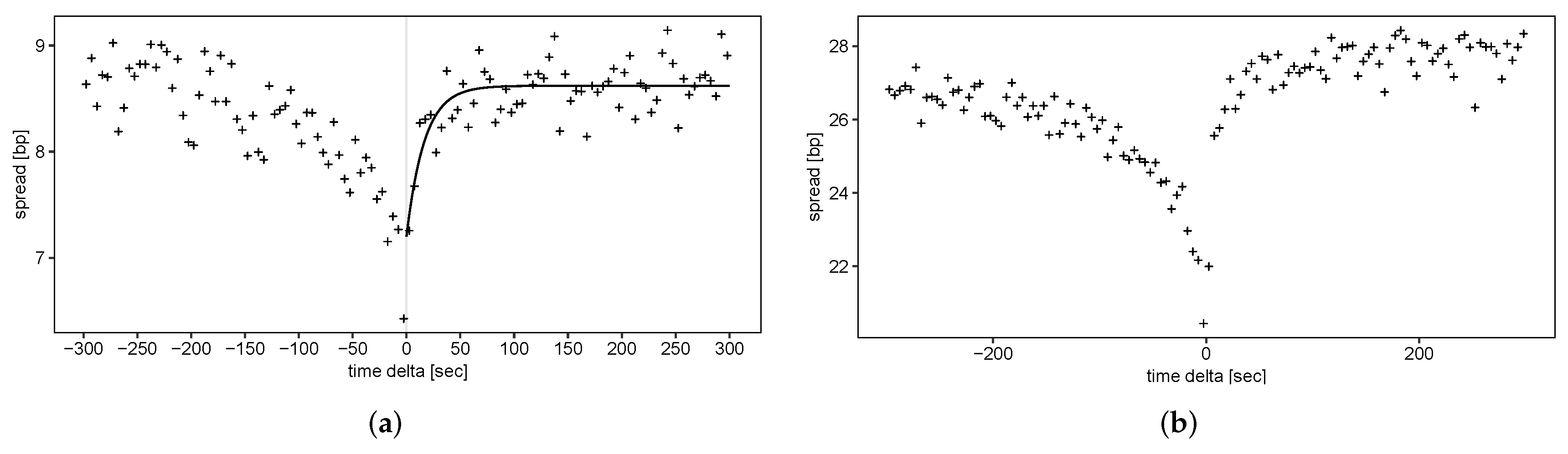

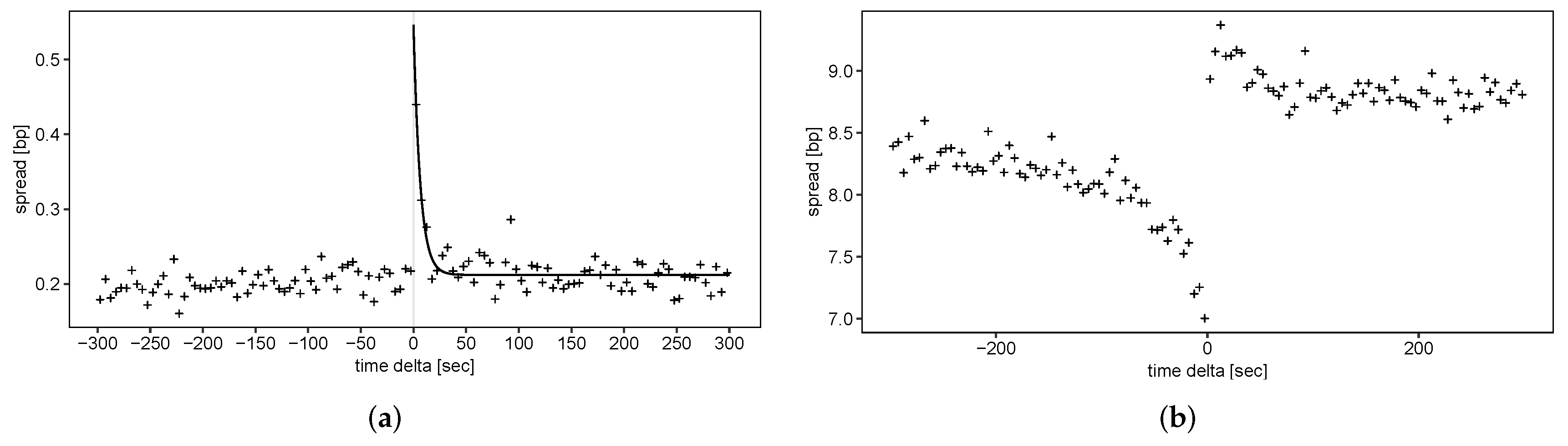

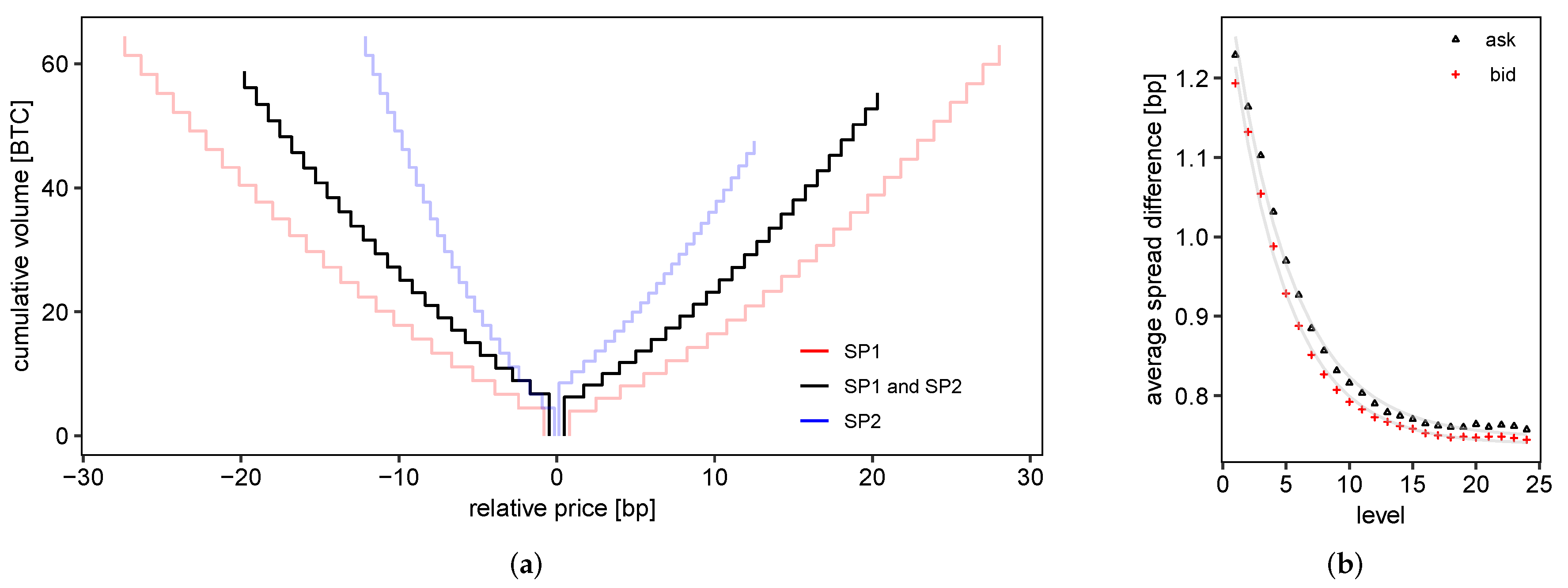

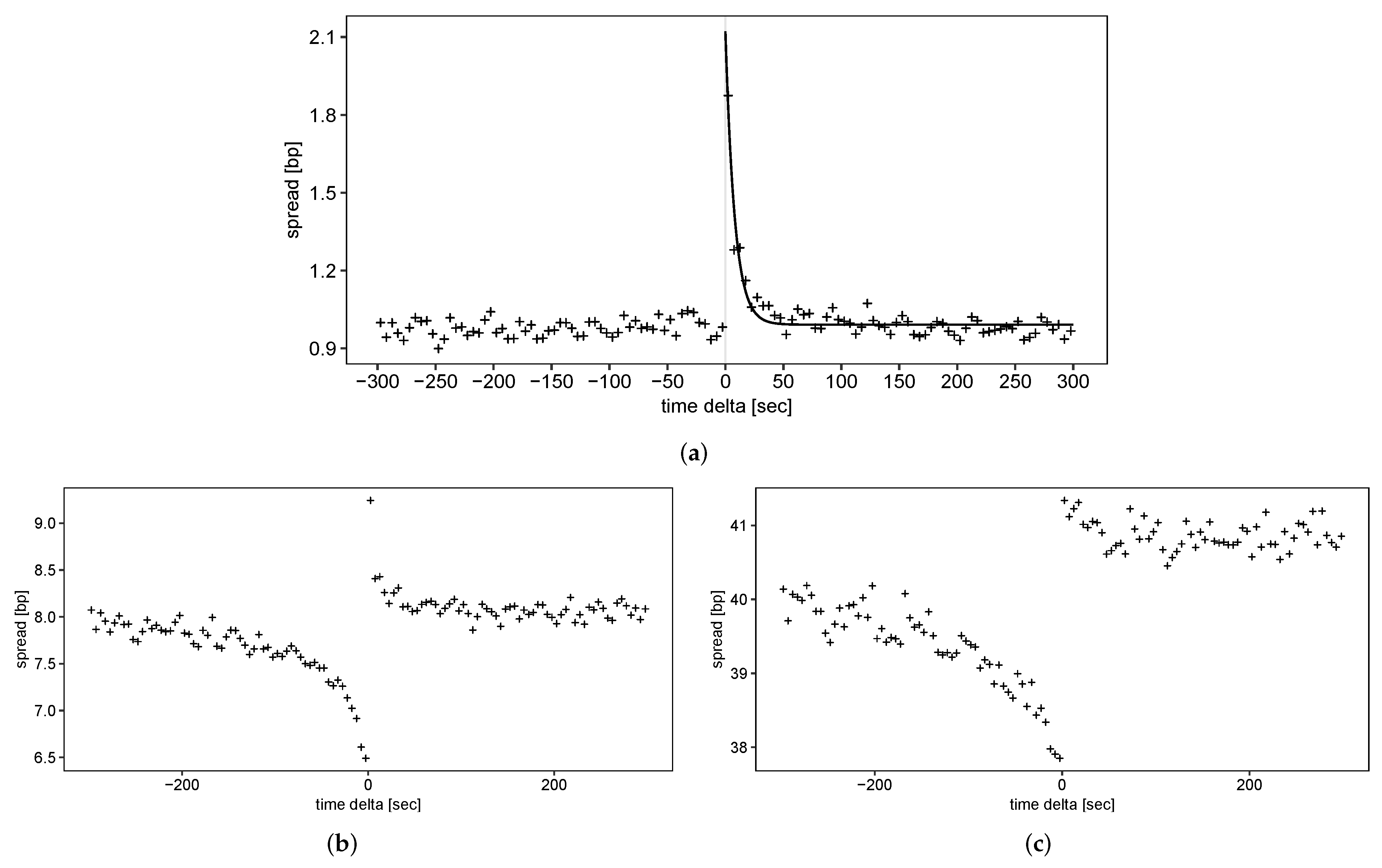

- Recovery of the bid-ask spread: We first consider the typical speed at which liquidity recovers after a large trade. We find that the average bid-ask spread increases to roughly 2 bp directly following the trade and subsequently recovers to its pre-event value of about 1 bp (Figure 8a). We fit an exponential decay function to estimate the decay time constant as s (corresponding to a half-life of s). Surprisingly, this is well in line with the finding of Cummings and Frino (2010) for large block trades of interest rate futures at the Sydney Futures Exchange: Considering only the largest block trades, they find that excess bid-ask spreads after the largest block purchases recover to a normal level on a time scale of approximately 7 s. They find that recovery is faster for the largest trades. Similarly, Large (2007) estimates a half-life time of about 20 s for a stock at the London Stock Exchange.

- Recovery of liquidity beyond the (best) bid and ask: For liquidity provided from deeper levels of the LOB, we find that liquidity does not quite recover to pre-event levels in the considered time window of 300 s (compare Figure 8b,c). Gomber et al. (2015) find that “it takes longer to restore large depth than to restore a small spread” (Gomber et al. 2015, p. 67). They estimate that it takes about four minutes to restore liquidity costs for EUR. For similar volumes (Figure 8b) we observe that average liquidity after the trade still differs slightly from pre-trade values.

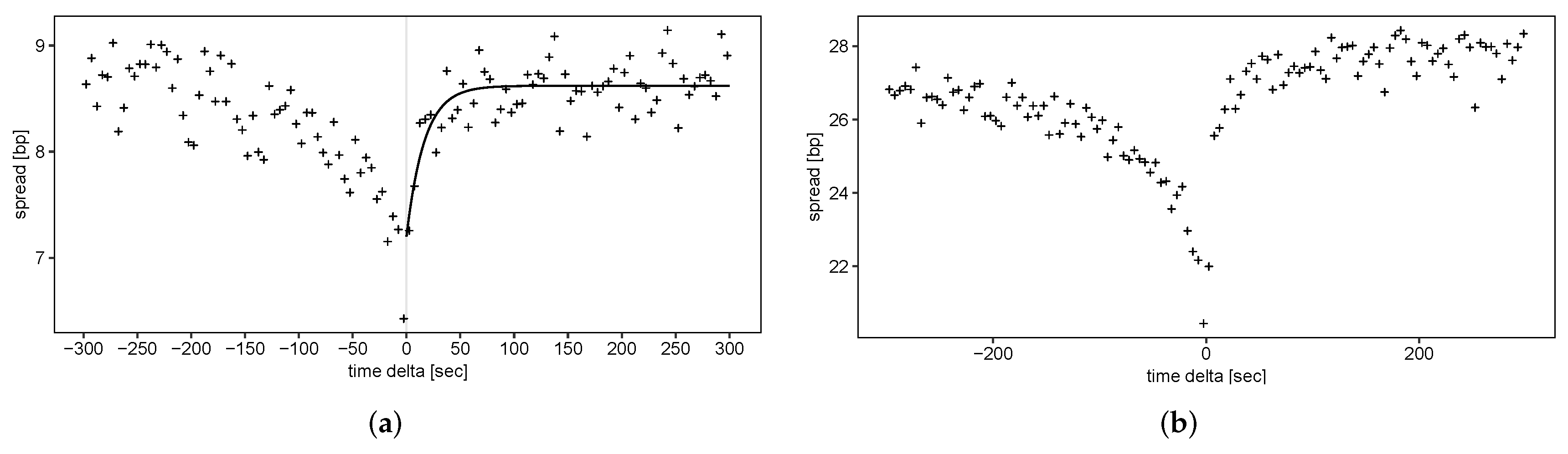

- Pre-trade liquidity increase and timing of large transactions: For average liquidity costs for USD and USD, we find—at first quite surprisingly—that liquidity increases prior to a large trade. This effect is observed in time windows of 2–3 min preceding the trade. Gomber et al. (2015) report a very similar finding for the evolution of the average exchange liquidity measure: Liquidity costs for EUR and DAX stocks decrease over an interval of about three minutes before large trades. Noticing that the increase in liquidity takes place on the side of the market where the trade occurs, they interpret this effect in terms of timed large transactions: Market participants prefer to execute large trades when liquidity is exceptionally high, and the execution of large trades relatively cheap. Our results indicate that the timing of large transactions is also present in Bitcoin markets.

5.2. Analysis of the Dynamics of the Limit Order Book: Order and Trade Flows

5.2.1. Unconditional Descriptive Statistics of Trades and Order Book Changes

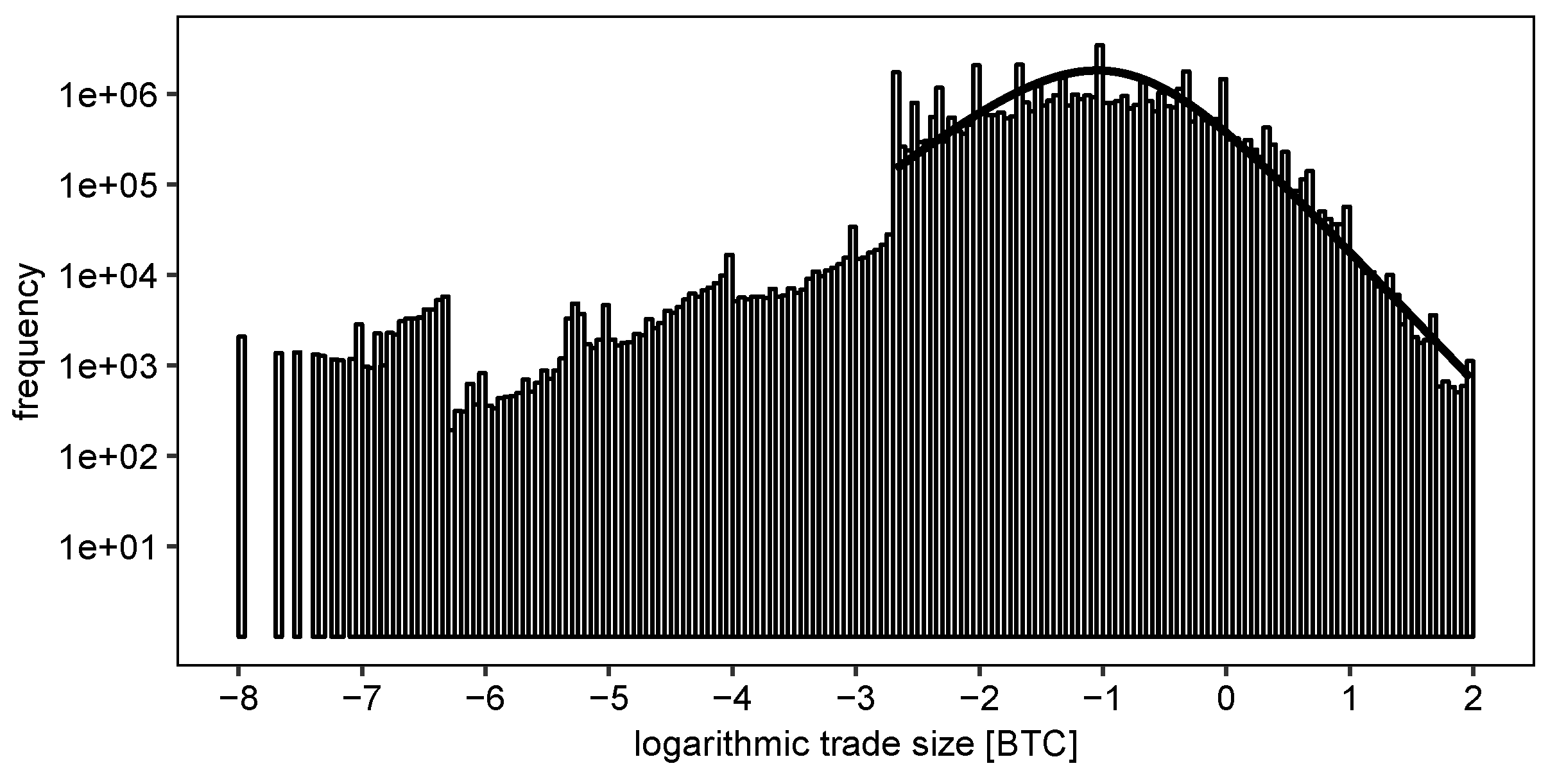

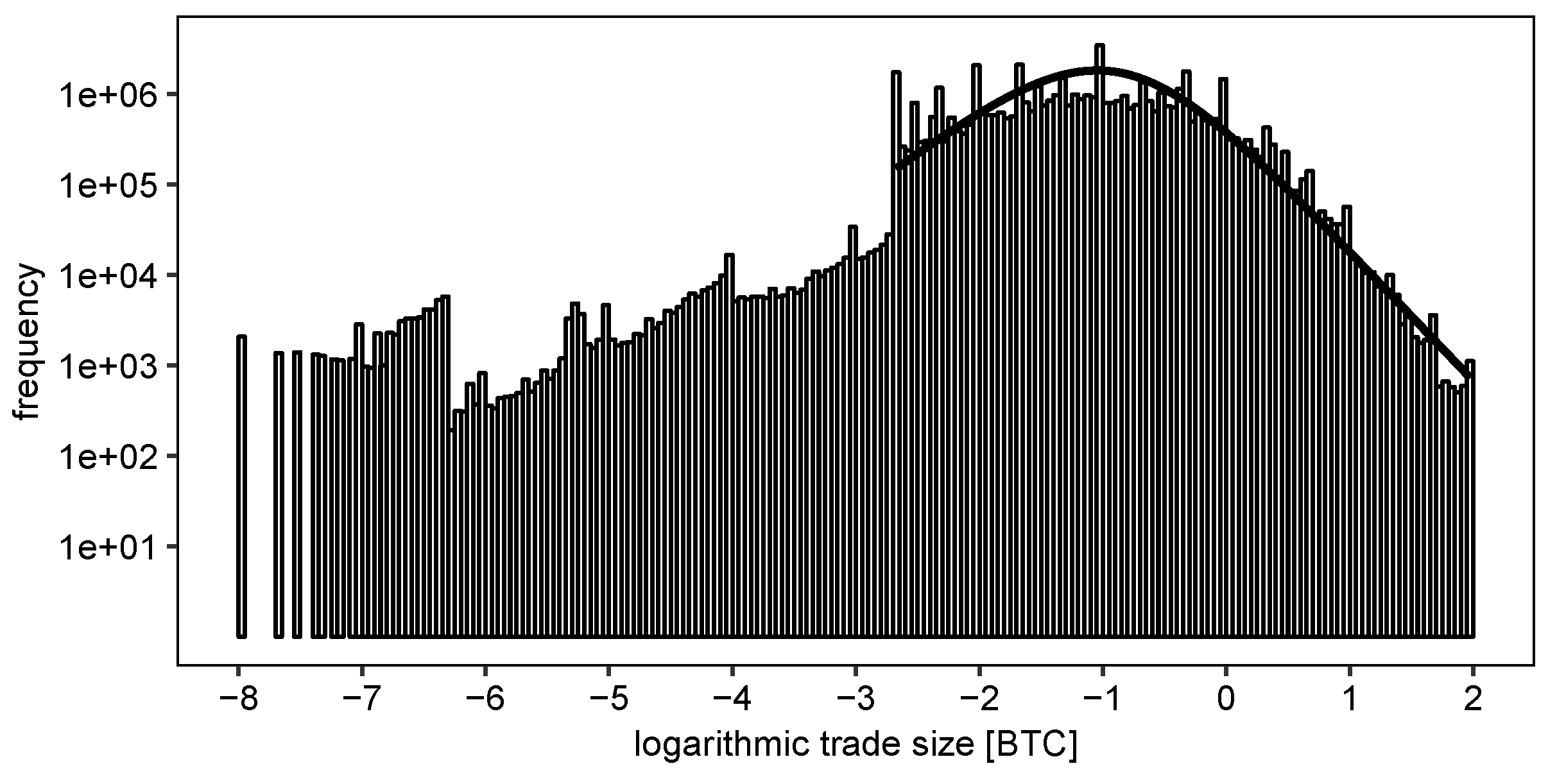

- Two regimes separated by the minimum order size: The distribution of trade size exhibits a large jump at the minimum order size of 0.002 BTC, and separates two regimes: For smaller trades, trade frequency increases with trade size, but exhibits discontinuities. For larger trade sizes, the distribution exhibits a convex plateau and a power tail for trades larger 1 BTC.

- Power-law dependence of volume for large trades: For trade sizes exceeding the minimum order size, the empirical distribution of trade size agrees well with results from the literature: Similar to the results of Mu et al. (2009), the empirical distribution of trade sizes larger than the minimum order size fits well to a q-Gamma distribution with parameters , and . The asymptotic tail exponent of this distribution is given by . Gopikrishnan et al. (2000) and Maslov and Mills (2001) find power tails with comparable values for US stock markets () and the NASDAQ ().

- Significant share of trades smaller than the minimum order size: A large share of trades has a size smaller than the minimum order size. We interpret these results in the light of a minimum order size increment ( BTC) much smaller than the minimum order size (0.002 BTC), leading to trade sizes much smaller than the minimum order size. For example, an ask order with initial volume 0.0021 BTC could be partially matched with a bid order of 0.002 BTC, leaving a small ask order active that could subsequently lead to a trade of size 0.0001 BTC.

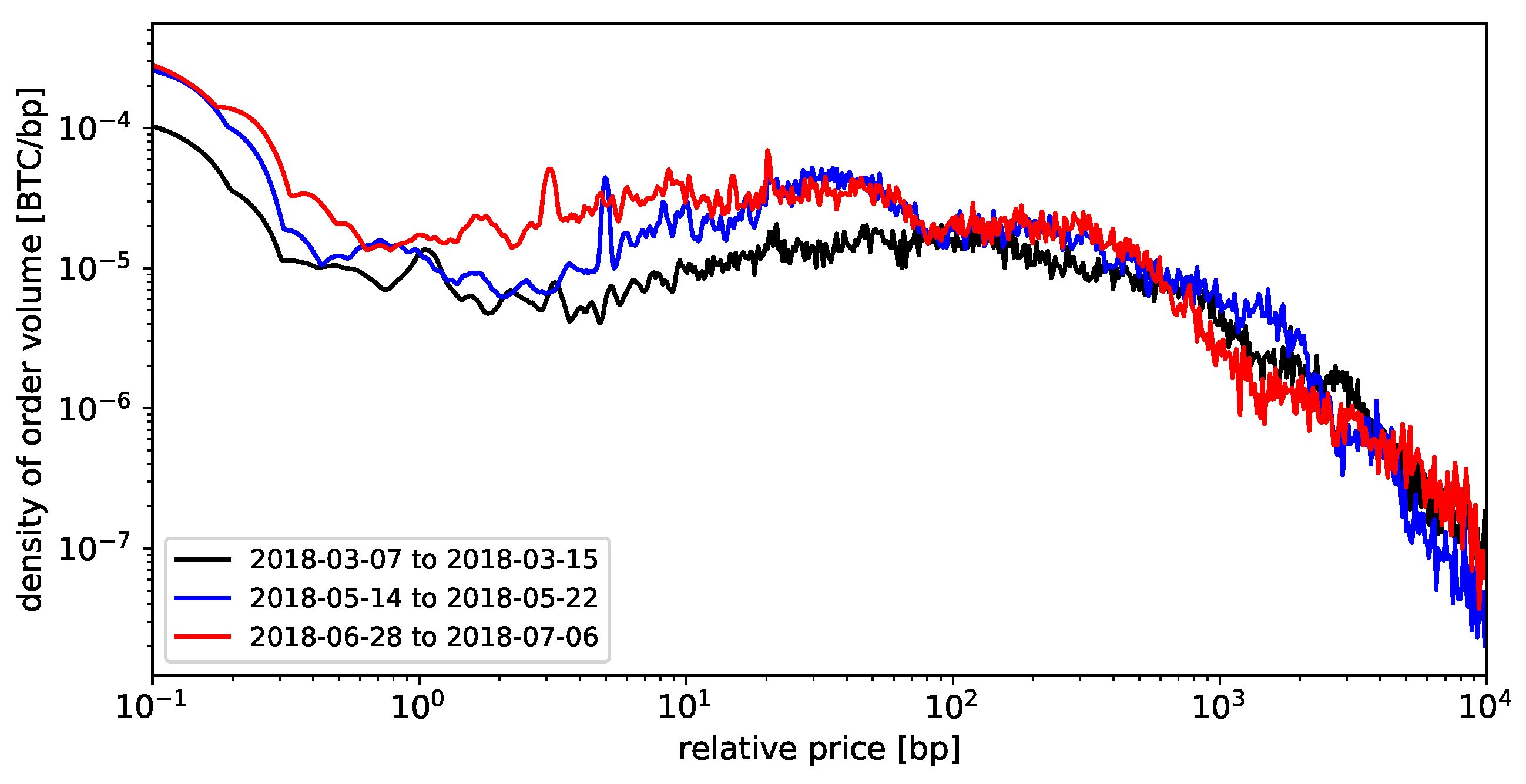

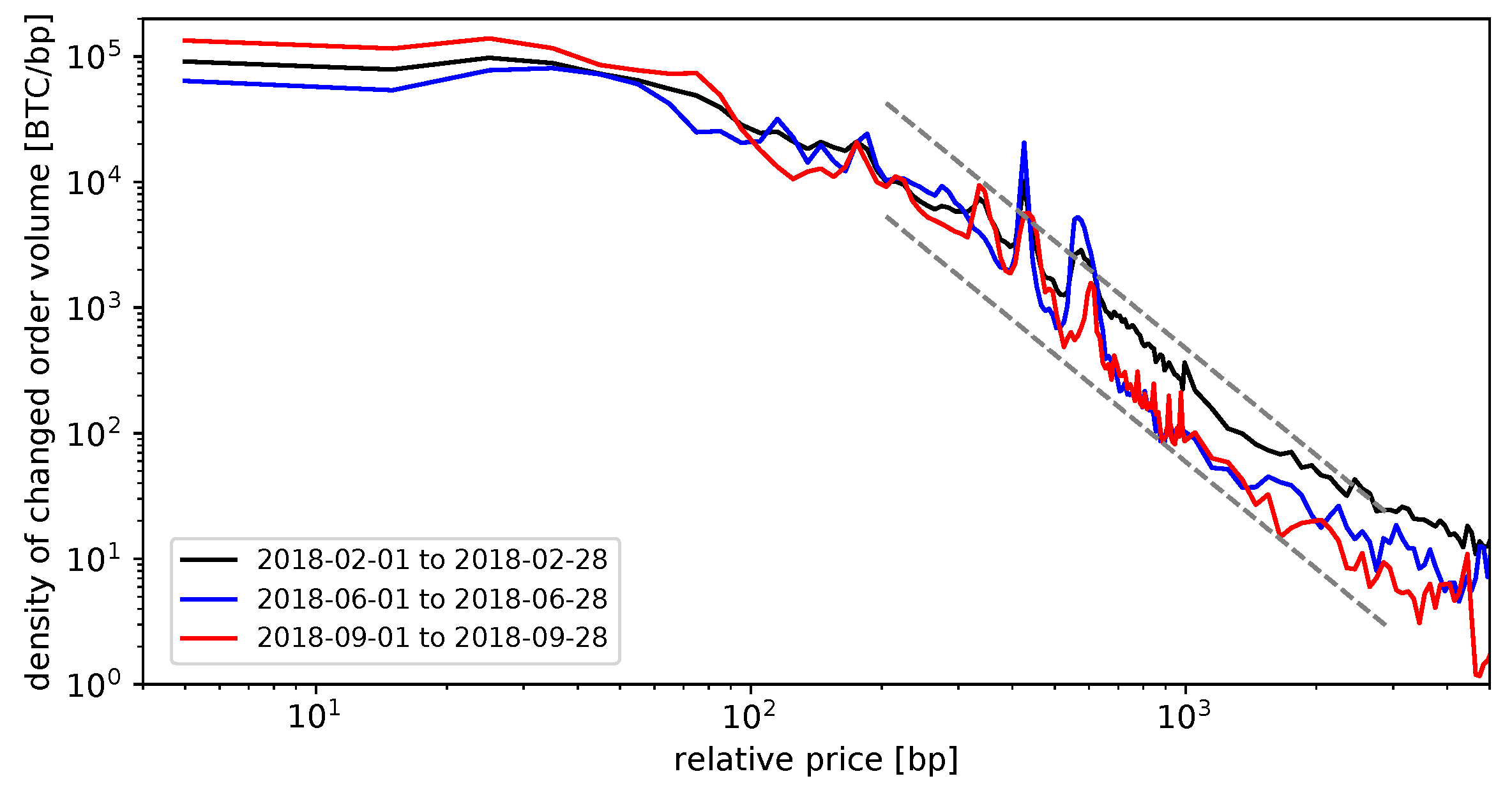

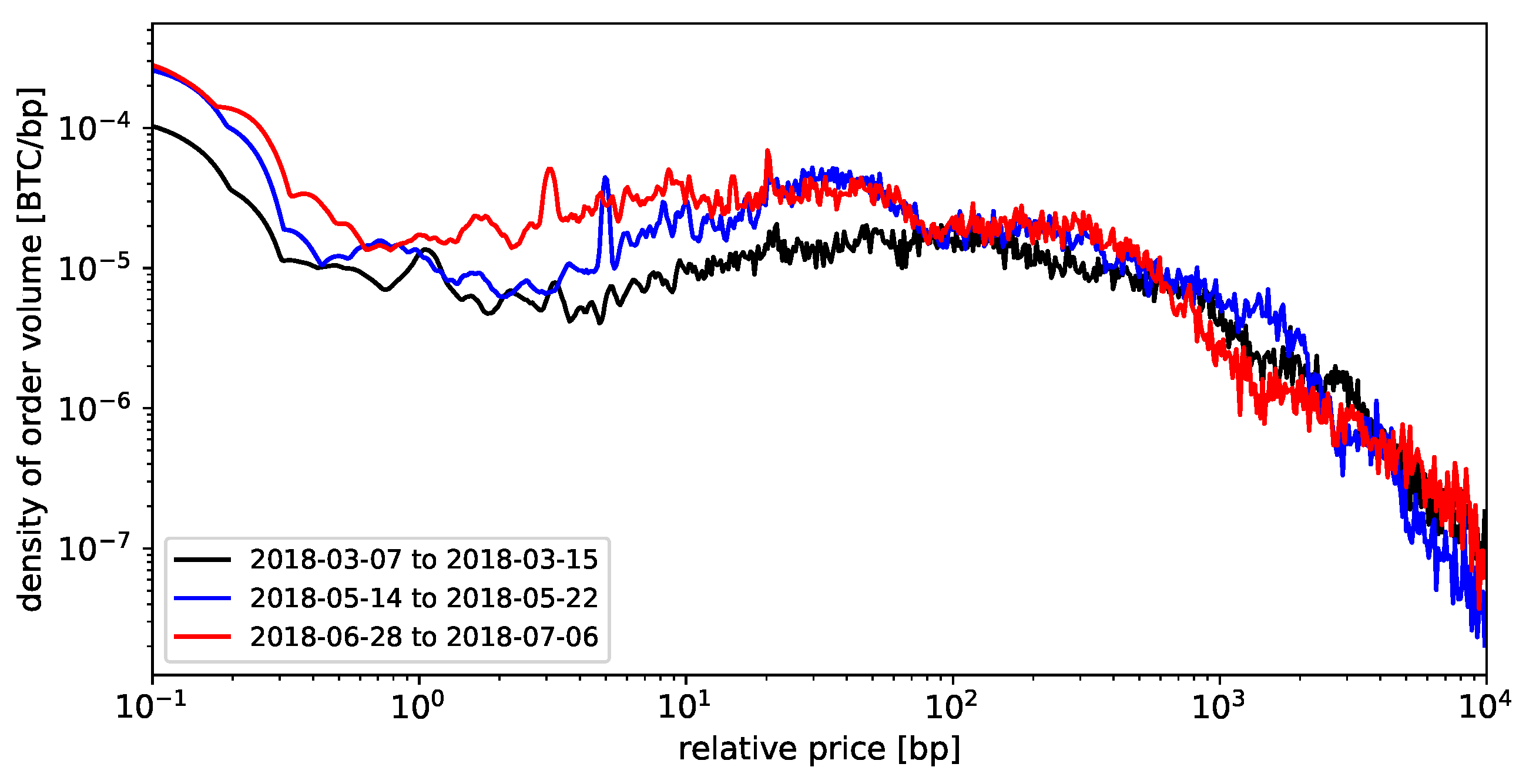

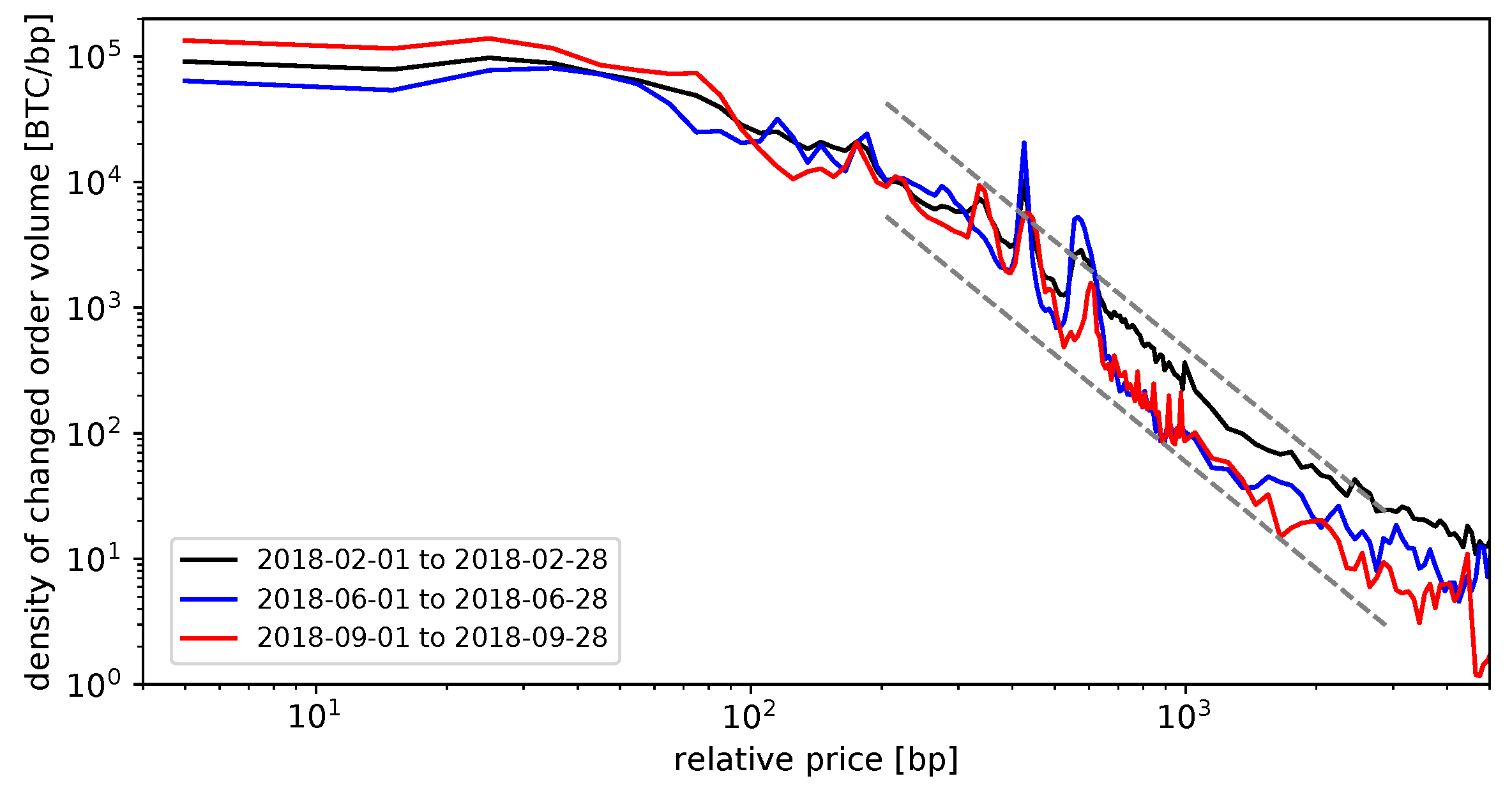

- Power tail away from the current price: Further away from the current mid price, the changed limit order volume declines rapidly. Figure 10 includes dashed straight lines with a slope of roughly −2.8, and the empirical density in log-log axes declines at a roughly similar rate. Power tails in the distribution of order frequency as a function of the difference to the price have been found before (compare, for example, Bouchaud et al. (2002), Zovko and Farmer (2002) and Potters and Bouchaud (2003). These analyses consider all incoming orders, whereas we consider the total change in depth in the LOB. Therefore, a different distribution close to the mid price would be expected.

- Constant changed order volume near the current price: We find a roughly constant density in changed limit order volume up to a relative price of 1 percent. We may cautiously conclude that this finding is still consistent with the literature: Several authors (for example, Bouchaud et al. (2002), Zovko and Farmer (2002) and Potters and Bouchaud (2003)) found that most orders arrive at the current bid or ask price. These orders are, however, executed immediately or with high profitability, and thus cannot be observed in our analysis, leading to the observed plateau in the distribution of changed limit order volume. Orders arriving further away from the current price are less likely executed and lead to persistent changes in limit order depth, which we observe in our analysis.

- Peaked activity away from the current price: Quite surprisingly, we see distinct peaks in changed order volume at relative prices of 4 and 6 percent. These could be the consequence of speculative order placement or the traders’ preference for certain round order prices.

5.2.2. Time Series Characteristics of Trade Properties

5.2.3. Conditional Statistics Across All Trades

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Results for Further Exchanges

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | |

|---|---|---|---|---|---|---|---|---|---|---|

| mean | 0.0992 | 0.1532 | 0.3097 | 0.5102 | 0.7390 | −0.0992 | −0.1638 | −0.3407 | −0.5685 | −0.8364 |

| sd | 9.4231 | 0.9120 | 1.3032 | 1.6700 | 2.0189 | 9.4231 | 0.9466 | 1.3670 | 1.7763 | 2.2484 |

| q25 | 0.0056 | 0.0057 | 0.0058 | 0.0060 | 0.0061 | −0.0076 | −0.0077 | −0.0078 | −0.0085 | −0.4824 |

| median | 0.0067 | 0.0068 | 0.0071 | 0.0074 | 0.0075 | −0.0067 | −0.0068 | −0.0070 | −0.0073 | −0.0075 |

| q75 | 0.0076 | 0.0077 | 0.0078 | 0.0085 | 0.3317 | −0.0056 | −0.0057 | −0.0058 | −0.0059 | −0.0060 |

| [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | |

| mean | 1.0937 | 1.0352 | 1.0407 | 1.0242 | 1.0012 | 0.8994 | 0.8716 | 0.8330 | 0.8478 | 0.8355 |

| sd | 3.5183 | 3.4218 | 3.5283 | 3.5174 | 3.5246 | 2.7554 | 2.7223 | 2.6287 | 2.7821 | 2.7304 |

| q25 | 0.0047 | 0.0029 | 0.0030 | 0.0025 | 0.0023 | 0.0077 | 0.0064 | 0.0060 | 0.0063 | 0.0063 |

| median | 0.1130 | 0.1000 | 0.0932 | 0.0800 | 0.0662 | 0.1200 | 0.1002 | 0.1000 | 0.1000 | 0.0958 |

| q75 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 1.0000 | 0.9725 | 0.9683 | 0.9460 |

| [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | |

|---|---|---|---|---|---|---|---|---|---|---|

| mean | 3.9306 | 5.9740 | 7.8983 | 9.6986 | 11.3785 | −3.9306 | −6.2516 | −8.3233 | −10.2498 | −12.0205 |

| sd | 3.6971 | 5.0798 | 5.9524 | 6.6103 | 7.1657 | 3.6971 | 5.2242 | 6.1008 | 6.7221 | 7.2437 |

| q25 | 1.3370 | 2.6456 | 3.9142 | 5.1897 | 6.5248 | −5.3879 | −7.9980 | −10.6020 | −12.8396 | −14.7508 |

| median | 3.1511 | 4.7447 | 6.4603 | 8.2124 | 9.8818 | −3.1511 | −4.9946 | −6.9114 | −8.8283 | −10.5893 |

| q75 | 5.3879 | 7.6499 | 10.1350 | 12.3066 | 14.2027 | −1.3370 | −2.8920 | −4.3039 | −5.7707 | −7.2550 |

| [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | |

| mean | 1.5771 | 1.4164 | 1.4532 | 1.5579 | 1.7032 | 1.6735 | 1.5641 | 1.6563 | 1.8360 | 1.9904 |

| sd | 6.7095 | 5.3325 | 4.6434 | 4.6641 | 4.7830 | 9.1645 | 6.3446 | 4.9995 | 5.1847 | 5.3419 |

| q25 | 0.0697 | 0.0380 | 0.0341 | 0.0350 | 0.0396 | 0.0855 | 0.0941 | 0.1000 | 0.1000 | 0.1000 |

| median | 0.5244 | 0.4200 | 0.4200 | 0.4440 | 0.5000 | 0.6273 | 0.6000 | 0.6691 | 0.8000 | 0.9397 |

| q75 | 1.4285 | 1.3380 | 1.4226 | 1.5000 | 1.5114 | 1.5000 | 1.5000 | 1.5146 | 1.6483 | 1.8762 |

| [BTC] | [USD] | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.5 | 1.0 | 2.0 | 5.0 | 10.0 | |||||

| A | mean | 0.1984 | 0.4565 | 0.8852 | 1.2585 | 1.9590 | 3.9038 | 6.9085 | 8.2644 | 55.9732 |

| sd | 18.8463 | 1.6903 | 3.0141 | 2.7074 | 3.3185 | 4.6643 | 6.2279 | 6.4667 | 72.2166 | |

| q25 | 0.0112 | 0.0116 | 0.0121 | 0.0124 | 0.0137 | 0.2657 | 2.5405 | 3.7401 | 42.1128 | |

| q50 | 0.0133 | 0.0142 | 0.0150 | 0.0155 | 0.3297 | 2.6565 | 5.7849 | 7.4037 | 51.9763 | |

| q75 | 0.0152 | 0.0157 | 0.4227 | 1.3888 | 2.8715 | 5.7636 | 9.5908 | 11.4203 | 63.9471 | |

| skew | 208.2537 | 9.5766 | 173.4533 | 5.0151 | 3.9150 | 2.8447 | 2.3831 | 2.0350 | 129.3065 | |

| kurt | 43464.80 | 228.58 | 69382.36 | 63.09 | 37.55 | 19.99 | 14.23 | 12.14 | 21011.61 | |

| B | mean | 7.8612 | 9.0643 | 10.5030 | 11.6672 | 13.7398 | 18.2892 | 23.5749 | 24.9565 | 73.5508 |

| sd | 7.3941 | 7.9357 | 8.7012 | 9.3081 | 10.0856 | 11.6074 | 13.0441 | 11.7406 | 21.6807 | |

| q25 | 2.6739 | 3.6618 | 4.7017 | 5.4402 | 6.9664 | 10.7988 | 15.4833 | 17.8222 | 58.9856 | |

| q50 | 6.3022 | 7.4225 | 8.6849 | 9.6938 | 11.7622 | 16.0878 | 20.7755 | 22.8481 | 69.9553 | |

| q75 | 10.7758 | 12.2041 | 13.8400 | 15.1248 | 17.3629 | 22.0618 | 27.1251 | 28.6737 | 83.7376 | |

| skew | 2.2649 | 2.1057 | 2.0129 | 1.9788 | 1.9183 | 1.8158 | 1.7826 | 1.7740 | 1.7231 | |

| kurt | 17.3872 | 14.8690 | 11.7922 | 10.3188 | 8.9804 | 6.9622 | 5.8785 | 7.1700 | 7.5178 | |

References

- Arnold, Andrew. 2018. How Institutional Investors Are Changing The Cryptocurrency Market. Forbes. Available online: https://www.forbes.com/sites/andrewarnold/2018/10/19/how-institutional-investors-are-changing-the-cryptocurrency-market/ (accessed on 17 January 2019).

- Bacon, Carl R. 2008. Practical Portfolio Performance Measurement and Attribution. The Wiley Finance Series. Hoboken: Wiley & Sons. [Google Scholar]

- Balanda, Kevin P., and Helen L. MacGillivray. 1990. Kurtosis and spread. Canadian Journal of Statistics 18: 17–30. [Google Scholar] [CrossRef]

- Bariviera, Aurelio F., María José Basgall, Waldo Hasperué, and Marcelo Naiouf. 2017. Some stylized facts of the Bitcoin market. Physica A: Statistical Mechanics and Its Applications 484: 82–90. [Google Scholar] [CrossRef]

- Biais, Bruno, Pierre Hillion, and Chester Spatt. 1995. An empirical analysis of the limit order book and the order flow in the Paris Bourse. The Journal of Finance 50: 1655–89. [Google Scholar] [CrossRef]

- Black, Fischer. 1971. Toward a fully automated stock exchange, part I. Financial Analysts Journal 27: 28–35. [Google Scholar] [CrossRef]

- Bouchaud, Jean-Philippe. 2009. Price Impact. arXiv, arXiv:0903.2428. [Google Scholar]

- Bouchaud, Jean-Philippe, Marc Mézard, and Marc Potters. 2002. Statistical properties of stock order books: Empirical results and models. Quantitative Finance 2: 251–56. [Google Scholar] [CrossRef]

- Brandvold, Morten, Peter Molnár, Kristian Vagstad, and Ole C. A. Valstad. 2015. Price discovery on Bitcoin exchanges. Journal of International Financial Markets, Institutions and Money 36: 18–35. [Google Scholar] [CrossRef]

- Böhme, Rainer, Nicolas Christin, Benjamin Edelman, and Tyler Moore. 2015. Bitcoin: Economics, technology, and governance. Journal of Economic Perspectives 29: 213–38. [Google Scholar] [CrossRef]

- Büning, Herbert. 1991. Robuste und Adaptive Tests. Berlin: De Gruyter. [Google Scholar]

- Cao, Charles, Oliver Hansch, and Xiaoxin Wang. 2009. The information content of an open limit-order book. Journal of Futures Markets 29: 16–41. [Google Scholar] [CrossRef]

- Chan, Stephen, Jeffrey Chu, Saralees Nadarajah, and Joerg Osterrieder. 2017. A statistical analysis of cryptocurrencies. Journal of Risk and Financial Management 10: 12. [Google Scholar] [CrossRef]

- Chaparro, Frank. 2017. A small band of trading specialists are taking calls about $50 million bitcoin deals. Business Insider Deutschland. Available online: https://www.businessinsider.de/bitcoin-trading-matures-as-institutions-pour-in-2017-11 (accessed on 17 January 2019).

- Chu, Jeffrey, Stephen Chan, Saralees Nadarajah, and Joerg Osterrieder. 2017. GARCH modelling of cryptocurrencies. Journal of Risk and Financial Management 10: 17. [Google Scholar] [CrossRef]

- Cont, Rama. 2001. Empirical properties of asset returns: Stylized facts and statistical issues. Quantitative Finance 1: 223–36. [Google Scholar] [CrossRef]

- Cont, Rama, Arseniy Kukanov, and Sasha Stoikov. 2014. The Price Impact of Order Book Events. Journal of Financial Econometrics 12: 47–88. [Google Scholar] [CrossRef]

- Cummings, James Richard, and Alex Frino. 2010. Further analysis of the speed of response to large trades in interest rate futures. Journal of Futures Markets 30: 705–24. [Google Scholar] [CrossRef]

- Danielsson, Jon, Lerby M. Ergun, Laurens de Haan, and Casper G. de Vries. 2016. Tail Index Estimation: Quantile Driven Threshold Selection. SSRN Scholarly Paper ID 2717478. Rochester: Social Science Research Network. [Google Scholar]

- Danielsson, Jon, and Richard Payne. 2001. Measuring and Explaining Liquidity on an Electronic Limit Order Book: Evidence from Reuters D2000-2. SSRN Scholarly Paper ID 276541. Sochester: Social Science Research Network. [Google Scholar]

- Degryse, Hans, Frank De Jong, Maarten Van Ravenswaaij, and Gunther Wuyts. 2005. Aggressive orders and the resiliency of a limit order market. Review of Finance 9: 201–42. [Google Scholar] [CrossRef]

- Dimpfl, Thomas. 2017. Bitcoin Market Microstructure. SSRN Scholarly Paper ID 2949807. SSochester: Social Science Research Network. [Google Scholar]

- Donier, Jonathan, and Julius Bonart. 2015. A million metaorder analysis of market impact on the Bitcoin. Market Microstructure and Liquidity 1: 1550008. [Google Scholar] [CrossRef]

- Donier, Jonathan, and Jean-Philippe Bouchaud. 2015. Why do markets crash? Bitcoin data offers unprecedented insights. PLoS ONE 10: e0139356. [Google Scholar] [CrossRef] [PubMed]

- Dyhrberg, Anne H., Sean Foley, and Jiri Svec. 2018. How investible is Bitcoin? Analyzing the liquidity and transaction costs of Bitcoin markets. Economics Letters 171: 140–43. [Google Scholar] [CrossRef]

- Easwaran, Soumya, Manu Dixit, and Sitabhra Sinha. 2015. itcoin dynamics: The inverse square law of price fluctuations and other stylized facts. In Econophysics and Data Driven Modelling of Market Dynamics. Edited by Frédéric Abergel, Hideaki Aoyama, Bikas K. Chakrabarti, Anirban Chakraborti and Asim Ghosh. New Economic Windows. Cham: Springer International Publishing, pp. 121–28. [Google Scholar]

- Foucault, Thierry, Ohad Kadan, and Eugene Kandel. 2005. Limit order book as a market for liquidity. The Review of Financial Studies 18: 1171–217. [Google Scholar] [CrossRef]

- Gomber, Peter, Uwe Schweickert, and Erik Theissen. 2015. Liquidity dynamics in an electronic open limit order book: An event study approach. European Financial Management 21: 52–78. [Google Scholar] [CrossRef]

- Gopikrishnan, Parameswaran, Vasiliki Plerou, Xavier Gabaix, and Harry E. Stanley. 2000. Statistical properties of share volume traded in financial markets. Physical Review E 62: R4493. [Google Scholar] [CrossRef]

- Gould, Martin D., Mason A. Porter, Stacy Williams, Mark McDonald, Daniel J. Fenn, and Sam D. Howison. 2013. Limit order books. Quantitative Finance 13: 1709–42. [Google Scholar] [CrossRef]

- Gu, Gao-Feng, Wei Chen, and Wei-Xing Zhou. 2008. Empirical shape function of limit-order books in the Chinese stock market. Physica A: Statistical Mechanics and its Applications 387: 5182–88. [Google Scholar] [CrossRef]

- Hill, Bruce M. 1975. A simple general approach to inference about the tail of a distribution. The Annals of Statistics 3: 1163–74. [Google Scholar] [CrossRef]

- Interactive Brokers. 2019. Order Handling Using Price Capping. Available online: https://www.interactivebrokers.com/en/index.php?f=14186 (accessed on 17 January 2019).

- Kelly, Bryan, and Hao Jiang. 2014. Tail risk and asset prices. The Review of Financial Studies 27: 2841–71. [Google Scholar] [CrossRef]

- Kyle, Albert S. 1985. Continuous auctions and insider trading. Econometrica 53: 1315–35. [Google Scholar] [CrossRef]

- Large, Jeremy. 2007. Measuring the resiliency of an electronic limit order book. Journal of Financial Markets 10: 1–25. [Google Scholar] [CrossRef]

- Ljung, Greta M., and George E. P. Box. 1978. On a measure of lack of fit in time series models. Biometrika 65: 297–303. [Google Scholar] [CrossRef]

- Lux, Thomas, and Michele Marchesi. 2000. Volatility clustering in financial markets: A microsimulation of interacting agents. International Journal of Theoretical and Applied Finance 3: 675–702. [Google Scholar] [CrossRef]

- Maslov, Sergei, and Mark Mills. 2001. Price fluctuations from the order book perspective—Empirical facts and a simple model. Physica A: Statistical Mechanics and its Applications 299: 234–46. [Google Scholar] [CrossRef]

- McInish, Thomas H., and Robert A. Wood. 1992. An analysis of intraday patterns in bid/ask spreads for NYSE stocks. The Journal of Finance 47: 753–64. [Google Scholar] [CrossRef]

- Mu, Guo-Hua, Wei Chen, János Kertész, and Wei-Xing Zhou. 2009. Preferred numbers and the distributions of trade sizes and trading volumes in the Chinese stock market. The European Physical Journal B 68: 145–52. [Google Scholar] [CrossRef]

- Potters, Marc, and Jean-Philippe Bouchaud. 2003. More statistical properties of order books and price impact. Physica A: Statistical Mechanics and its Applications 324: 133–40. [Google Scholar] [CrossRef]

- Ranaldo, Angelo. 2004. Order aggressiveness in limit order book markets. Journal of Financial Markets 7: 53–74. [Google Scholar] [CrossRef]

- Roşu, Ioanid. 2009. A dynamic model of the limit order book. The Review of Financial Studies 22: 4601–41. [Google Scholar] [CrossRef]

- Russell, Jeffrey R., and Robert F. Engle. 2010. Analysis of high-frequency data. In Handbook of Financial Econometrics: Tools and Techniques. Edited by Yacine Ait-Sahalia and Lars Peter Hansen. San Diego: North-Holland, vol. 1, pp. 383–426. [Google Scholar]

- Zargar, Faisal N., and Dilip Kumar. 2019. Long range dependence in the Bitcoin market: A study based on high-frequency data. Physica A: Statistical Mechanics and its Applications 515: 625–40. [Google Scholar] [CrossRef]

- Zhang, Wei, Pengfei Wang, Xiao Li, and Dehua Shen. 2018. Some stylized facts of the cryptocurrency market. Applied Economics 50: 5950–65. [Google Scholar] [CrossRef]

- Zovko, Ilija, and J. Doyne Farmer. 2002. The power of patience: A behavioural regularity in limit-order placement. Quantitative Finance 2: 387–92. [Google Scholar] [CrossRef]

| 1 | Formerly called GDAX. |

| 2 | Two-sided in this case refers to both the bid and the ask side of the order book, and is used for comparability to the (two-sided) bid-ask spread. Please note that this is equal to the exchange liquidity measure (XLM) of Gomber et al. (2015). |

| 3 | To keep the three groups canonical, the third group is limited to conditions other than the own past of the data, i.e., the time series, which was already addressed in the second group. |

| 4 | There are theoretical-based methods and heuristics. For an overview about the different methods see Danielsson et al. (2016). |

| 5 | Whenever possible, results for subperiods are shown alongside main results. Omitted results are available on request. |

| 6 | The question arises whether these results are a consequence of the limited price increment of the exchange. With average mid prices in the order of 10,000 USD and a price increment of 0.1 USD, we obtain a technical limit for relative price differences of 0.1 bp, which is still one order of magnitude larger than the observed average price differences. |

| 7 | The reported VWAP spreads are upper bounds as BitFinex allows hidden limit orders which might provide further liquidity. |

| 8 | There is only weak skewness (Table 6) giving no indication that the symmetry assumption underlying the metric is violated. |

| 9 | We obtain a p-value of 0.6340. Given the large sample sizes for minutely and hourly data, applying the Ljung-Box test is not meaningful, because even the smallest estimated autocorrelation is significant (Lux and Marchesi 2000). |

| 10 | Following McInish and Wood (1992), we additionally perform a regression of the bid-ask spread on dummy variables for each hour of the day. In line with previous results, regression results do not yield a significant pattern. |

| 11 | As for BitFinex, we run a dummy variable regression which supports the existence of the U-shaped pattern. |

| Exchange | Order Type | Fees | Resolution | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Market | Stop | FOK | IOC | Hidden | Taker [bp] | Maker [bp] | Deposit | Withdrawal | Tick Size(USD) | Min. OrderSize (BTC) | |

| BitFinex | ✓ | ✓ | ✓ | ✓ | ✓ | 20–5.5 | 10–0 | 10 bp/20 USD | 10 bp/20 USD | ||

| BitStamp | ✓ | ✓ | 25–10 | 25–10 | 5 bp/7.5 USD | 9 bp/15 USD | ≈ | ||||

| Bittrex | ✓ | 25 | 25 | NA | NA | ||||||

| Coinbase/GDAX | ✓ | ✓ | ✓ | ✓ | 30–10 | 0 | 10 USD | 25 USD | |||

| Gemini | ✓ | ✓ | ✓ | 100–10 | 100–0 | none | none | ||||

| Kraken | ✓ | ✓ | 26–10 | 16–0 | 5 USD | 5 USD | |||||

| Poloniex | ✓ | 20–10 | 10–0 | none | 10 bp/50 USD | ||||||

| Common Fact | Measure Considered for Analysis | Key References | Type |

|---|---|---|---|

| Symmetric mean cumulative depth profiles | Time-averaged depth profile (Equations (3) and (4)) and time-averaged relative price differences between adjacent steps of the LOB (Equation (5)) | Biais et al. (1995), Cao et al. (2009) and Potters and Bouchaud (2003) | U |

| Gamma-distributed depth at best bid and best ask | Unconditional empirical distribution of the total volume (depth) at the best bid (or ask), i.e., and | Bouchaud et al. (2002) | U |

| Hump-shaped mean depth profile | Empirical distribution of the time-averaged volume from the depth profile ( and ) as a function of the (relative) price difference to the ask or bid price | Bouchaud et al. (2002), Potters and Bouchaud (2003) and Gu et al. (2008) | U |

| Increase in liquidity costs beyond the best bid/ask | Unconditional distribution of the relative bid-ask spread and the relative VWAP spread | Gomber et al. (2015) | U |

| Heavy tails of mid-price returns | Unconditional distribution of mid-price returns analyzed with kurtosis estimates and Hill estimator (Equations (10) and (11)) | Hill (1975), Balanda and MacGillivray (1990) and Lux and Marchesi (2000) | TS |

| No autocorrelation of returns | Autocorrelation of logarithmic mid-price returns (Equation (8)) | Lux and Marchesi (2000) and Cont (2001) | TS |

| Volatility clustering | Autocorrelation of absolute or squared logarithmic mid-price returns, i.e., the functions and , respectively (Equation (9)) | Lux and Marchesi (2000) and Cont (2001) | TS |

| Non-constant liquidity costs | Average daily liquidity costs (i.e., the bid-ask spread and the VWAP spread ) | Dyhrberg et al. (2018) | TS |

| U-shaped intraday patterns of liquidity costs | Average liquidity costs (i.e., the bid-ask spread and the VWAP spread ) conditional on the hour of the day | McInish and Wood (1992) and Gomber et al. (2015) | C |

| Liquidity resiliency and timed large trades | Distribution of average liquidity costs (i.e., the bid-ask spread and the VWAP spread ) for large trades conditional on the event time of the trade (Equation (12)) | Cummings and Frino (2010) and Gomber et al. (2015) | C |

| Common Fact | Measure Considered for Analysis | Key References | Type |

|---|---|---|---|

| Number preference for trade sizes | Empirical distribution of trade size | Mu et al. (2009) | U |

| Power tail in the distribution of trade size | Empirical distribution of trade size | Gopikrishnan et al. (2000), Maslov and Mills (2001) and Mu et al. (2009) | U |

| Power-law decay of order frequency with relative price | Time-average of changed limit order volume, i.e., and (Equation (14)) | similar to Bouchaud et al. (2002) and Zovko and Farmer (2002) | U |

| Negative autocorrelation of trade prices (bid-ask bounce) | Autocorrelation of the series of trade price changes (Equation (15)) | Cont (2001) and Russell and Engle (2010) | TS |

| Autocorrelation of trade sizes | Autocorrelation in the series of trade sizes (Equation (16)) | TS | |

| Intraday patterns in trade frequency and volume | Average trade frequency and average trade size conditional on the hour of the day | Biais et al. (1995) and Danielsson and Payne (2001) | C |

| [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | |

|---|---|---|---|---|---|---|---|---|---|---|

| mean | 0.4831 | 1.7123 | 2.8763 | 3.9788 | 5.0104 | 5.9803 | 6.9070 | 7.7917 | 8.6484 | 9.4799 |

| sd | 1.2024 | 2.3147 | 2.9969 | 3.6133 | 4.1442 | 4.6576 | 5.1445 | 5.6122 | 6.0846 | 6.5424 |

| q25 | 0.0675 | 0.3759 | 1.0092 | 1.6425 | 2.3193 | 2.9572 | 3.5081 | 4.0941 | 4.6438 | 5.1234 |

| median | 0.0777 | 1.0470 | 2.0961 | 3.0733 | 3.9880 | 4.8294 | 5.5362 | 6.2500 | 6.9267 | 7.5638 |

| q75 | 0.4392 | 2.1786 | 3.7341 | 5.1103 | 6.4375 | 7.6628 | 8.8376 | 9.9623 | 11.0422 | 12.1047 |

| [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | [bp] | |

| mean | −0.4831 | −1.6766 | −2.8087 | −3.8629 | −4.8509 | −5.7797 | −6.6675 | −7.5188 | −8.3457 | −9.1531 |

| sd | 1.2024 | 2.2548 | 2.9204 | 3.4579 | 3.9502 | 4.4140 | 4.8690 | 5.3263 | 5.7785 | 6.2391 |

| q25 | −0.4392 | −2.1422 | −3.6505 | −5.0113 | −6.2035 | −7.3812 | −8.4742 | −9.5624 | −10.6170 | −11.6707 |

| median | −0.0777 | −1.0301 | −2.0679 | −3.0492 | −3.9324 | −4.7487 | −5.3844 | −6.0720 | −6.7132 | −7.3242 |

| q75 | −0.0675 | −0.3608 | −0.9902 | −1.6176 | −2.2711 | −2.9088 | −3.4496 | −4.0167 | −4.5456 | −5.0245 |

| [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | |

| mean | 6.2519 | 1.9335 | 1.8313 | 1.8295 | 1.8376 | 1.8579 | 1.8727 | 1.8916 | 1.8991 | 1.9668 |

| sd | 20.2119 | 14.0038 | 9.5268 | 9.3860 | 10.6332 | 9.5688 | 9.6347 | 10.2464 | 9.9094 | 17.8200 |

| q25 | 0.5049 | 0.1000 | 0.1000 | 0.1049 | 0.1093 | 0.1226 | 0.1270 | 0.1322 | 0.1300 | 0.1338 |

| median | 2.1400 | 0.5225 | 0.5008 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| q75 | 6.6157 | 1.6600 | 1.5000 | 1.4802 | 1.4634 | 1.4722 | 1.4860 | 1.4990 | 1.5000 | 1.5000 |

| [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | [BTC] | |

| mean | 6.7553 | 2.1255 | 2.0309 | 2.0423 | 2.0494 | 2.0255 | 1.9986 | 2.0195 | 2.0211 | 2.0247 |

| sd | 21.0636 | 10.3102 | 11.5825 | 12.0838 | 11.7907 | 12.6380 | 12.7130 | 12.8436 | 12.1750 | 10.6579 |

| q25 | 0.5972 | 0.1000 | 0.1000 | 0.1000 | 0.1000 | 0.1063 | 0.1121 | 0.1194 | 0.1270 | 0.1251 |

| median | 2.2928 | 0.5394 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 | 0.5000 |

| q75 | 6.8141 | 1.7280 | 1.5360 | 1.5000 | 1.4770 | 1.4512 | 1.4300 | 1.4440 | 1.4743 | 1.5000 |

| [BTC] | [USD] | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 0.1 | 0.5 | 1.0 | 2.0 | 5.0 | 10.0 | ||||

| min | 0.1000 | 0.1000 | 0.1000 | 0.1000 | 0.1000 | 0.1000 | 0.1000 | 0.1000 | 0.1291 |

| max | 327.2825 | 327.2825 | 327.2825 | 327.2825 | 327.2825 | 327.7916 | 330.2782 | 327.9760 | 381.7934 |

| mean | 0.9663 | 1.1993 | 1.6364 | 2.0350 | 2.7790 | 4.8564 | 7.8754 | 8.3667 | 39.6270 |

| sd | 2.4048 | 2.6776 | 3.1408 | 3.5267 | 4.1727 | 5.7297 | 7.6235 | 6.7230 | 14.9090 |

| q25 | 0.1350 | 0.1405 | 0.1488 | 0.1520 | 0.1604 | 1.0064 | 2.9504 | 4.0599 | 31.2217 |

| q50 | 0.1554 | 0.1591 | 0.4497 | 0.7421 | 1.2843 | 3.2525 | 5.8831 | 7.0778 | 37.0837 |

| q75 | 0.8783 | 0.9870 | 1.8381 | 2.5691 | 3.7175 | 6.5002 | 10.2739 | 10.8947 | 45.1485 |

| skew | 17.0203 | 13.9014 | 10.0866 | 8.2406 | 6.4527 | 4.2931 | 3.2508 | 3.4022 | 2.6558 |

| kurt | 1201.9088 | 831.4204 | 465.3095 | 309.4683 | 183.0332 | 74.8028 | 37.9242 | 49.7824 | 17.6048 |

| min | −363.0070 | −1273.4918 | −2039.0606 |

| max | 454.4009 | 1127.3911 | 2063.1761 |

| mean | −0.0219 | −0.6505 | −15.1541 |

| sd | 15.3572 | 115.6858 | 497.8412 |

| q25 | −3.4865 | −35.9549 | −232.2230 |

| q50 | 0.0000 | 1.2460 | 5.8898 |

| q75 | 3.5754 | 35.1836 | 187.2999 |

| skew | 0.1583 | 0.0309 | −0.0797 |

| SP1 and SP2 | SP1 | SP2 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Side | Both | Left | Right | Both | Left | Right | Both | Both | Both | Both |

| 44.3497 | 41.5939 | 47.3472 | 17.6771 | 18.0461 | 17.3392 | 32.219 | 11.6763 | 77.9707 | 30.7078 | |

| 0.6481 | 0.7975 | 0.6004 | 0.5784 | 0.4773 | 0.6922 | 0.3992 | 0.2830 | 0.5555 | 0.9727 | |

| 2.0521 | 1.9382 | 2.1681 | 2.2681 | 2.4375 | 2.1438 | 2.4160 | 2.6743 | 2.0854 | 1.8972 | |

| 2.4823 | 2.3919 | 2.5650 | 2.8674 | 2.8448 | 2.8233 | 2.8642 | 3.2549 | 2.3750 | 2.1826 | |

| 2.8954 | 2.8852 | 2.9079 | 3.2968 | 3.6668 | 2.9610 | 3.2203 | 3.7743 | 2.4933 | 2.7144 | |

| lag n | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| SP1 and SP2 | 1 | 0.0342 | 0.2847 | 0.4667 | −0.0722 | 0.1625 | 0.2962 | 0.0004 | 0.1443 | 0.1209 |

| 2 | −0.0172 | 0.2357 | 0.4295 | 0.0134 | 0.2028 | 0.3259 | 0.0179 | 0.0436 | 0.1205 | |

| 3 | −0.0055 | 0.2198 | 0.4121 | −0.0208 | 0.1690 | 0.3071 | 0.0107 | 0.0766 | 0.1681 | |

| 4 | −0.0015 | 0.2324 | 0.4041 | −0.0364 | 0.1366 | 0.2833 | −0.0862 | 0.2132 | 0.1960 | |

| 5 | −0.0074 | 0.2069 | 0.4005 | −0.0083 | 0.2034 | 0.3264 | 0.0441 | 0.0796 | 0.1203 | |

| 6 | −0.0093 | 0.2112 | 0.3961 | 0.0212 | 0.1386 | 0.2850 | 0.0174 | 0.0887 | 0.1428 | |

| 7 | −0.0169 | 0.1976 | 0.3885 | −0.0120 | 0.1785 | 0.3083 | −0.0201 | 0.0733 | 0.1395 | |

| 8 | −0.0097 | 0.1858 | 0.3835 | 0.0071 | 0.2399 | 0.3399 | 0.0531 | 0.1511 | 0.2352 | |

| 9 | −0.0068 | 0.1873 | 0.3784 | −0.0427 | 0.2007 | 0.3056 | −0.0229 | 0.0528 | 0.0892 | |

| 10 | −0.0055 | 0.1944 | 0.3801 | 0.0535 | 0.2099 | 0.2927 | −0.0307 | 0.1126 | 0.1503 | |

| SP1 | 1 | 0.0306 | 0.2706 | 0.4019 | −0.0900 | 0.1324 | 0.2084 | −0.0044 | 0.0678 | −0.0331 |

| 2 | −0.0186 | 0.2267 | 0.3683 | 0.0170 | 0.1793 | 0.2588 | 0.0071 | −0.0532 | −0.0188 | |

| 3 | −0.0066 | 0.2119 | 0.3523 | −0.0256 | 0.1432 | 0.2421 | 0.0116 | −0.0107 | 0.0539 | |

| 4 | −0.0001 | 0.2265 | 0.3452 | −0.0403 | 0.1067 | 0.2109 | −0.1007 | 0.1495 | 0.0927 | |

| 5 | −0.0080 | 0.1995 | 0.3432 | −0.0098 | 0.1822 | 0.2663 | 0.0533 | 0.0075 | 0.0164 | |

| SP2 | 1 | 0.0592 | 0.2883 | 0.3813 | 0.0157 | 0.0757 | 0.1497 | 0.0189 | −0.0040 | 0.0720 |

| 2 | −0.0076 | 0.1446 | 0.2933 | −0.0162 | 0.0029 | 0.0512 | 0.0613 | 0.0169 | 0.0044 | |

| 3 | 0.0019 | 0.1071 | 0.2538 | −0.0005 | 0.0342 | 0.0651 | −0.0042 | −0.0530 | −0.0213 | |

| 4 | −0.0112 | 0.0914 | 0.2339 | 0.0019 | −0.0044 | 0.0359 | −0.0424 | −0.0098 | −0.0080 | |

| 5 | −0.0033 | 0.0810 | 0.2190 | −0.0035 | −0.0073 | 0.0292 | 0.0132 | −0.0785 | −0.0848 | |

| [USD] | [USD] | [BTC] | |||||

|---|---|---|---|---|---|---|---|

| All | All | Ask-Initiated | Bid-Initiated | All | Ask-Initiated | Bid-Initiated | |

| count | 51,058,356 | 51,058,356 | 26,112,746 | 24,945,610 | 51,058,356 | 26,112,746 | 24,945,610 |

| mean | 8665.11 | 3053.87 | 3059.75 | 3047.72 | 0.3643 | 0.3658 | 0.3627 |

| sd | 2493.81 | 13,658.82 | 14,155.62 | 13,118.64 | 1.6686 | 1.7441 | 1.5857 |

| q25 | 6710.00 | 138.14 | 134.45 | 143.19 | 0.0170 | 0.0160 | 0.0180 |

| q50 | 8011.30 | 634.33 | 626.23 | 641.15 | 0.0752 | 0.0748 | 0.0760 |

| q75 | 9602.40 | 2431.44 | 2419.27 | 2440.93 | 0.2938 | 0.2906 | 0.2970 |

| skew | 1.52 | 89.51 | 97.32 | 78.79 | 94.84 | 92.21 | 97.75 |

| lag n | All | All | |||||

|---|---|---|---|---|---|---|---|

| SP1 and SP2 | 1 | 0.1225 | 0.1398 | 0.1176 | −0.1759 | −0.0790 | −0.0833 |

| 2 | 0.1045 | 0.1106 | 0.1128 | −0.0529 | −0.0204 | −0.0234 | |

| 3 | 0.0926 | 0.0995 | 0.0946 | −0.0302 | −0.0110 | −0.0147 | |

| 4 | 0.1092 | 0.1219 | 0.1061 | −0.0107 | −0.0001 | −0.0033 | |

| 5 | 0.0743 | 0.0775 | 0.0796 | −0.0128 | −0.0059 | −0.0066 | |

| 6 | 0.0893 | 0.0947 | 0.0931 | −0.0032 | 0.0059 | 0.0045 | |

| 7 | 0.0672 | 0.0728 | 0.0694 | −0.0091 | −0.0018 | −0.0018 | |

| 8 | 0.0890 | 0.1013 | 0.0832 | −0.0020 | 0.0048 | 0.0036 | |

| SP1 | 1 | 0.1024 | 0.1314 | 0.0854 | −0.1775 | −0.0787 | −0.0831 |

| 2 | 0.0675 | 0.0718 | 0.0773 | −0.0532 | −0.0204 | −0.0236 | |

| 3 | 0.0611 | 0.0644 | 0.0665 | −0.0294 | −0.0101 | −0.0140 | |

| 4 | 0.0596 | 0.0609 | 0.0671 | −0.0111 | −0.0006 | −0.0042 | |

| 5 | 0.0496 | 0.0505 | 0.0580 | −0.0114 | −0.0044 | −0.0054 | |

| SP2 | 1 | 0.1406 | 0.1464 | 0.1513 | −0.1378 | −0.0834 | −0.0871 |

| 2 | 0.1380 | 0.1419 | 0.1501 | −0.0468 | −0.0207 | −0.0205 | |

| 3 | 0.1211 | 0.1278 | 0.1239 | −0.0483 | −0.0276 | −0.0276 | |

| 4 | 0.1541 | 0.1713 | 0.1469 | −0.0024 | 0.0099 | 0.0121 | |

| 5 | 0.0965 | 0.0993 | 0.1021 | −0.0458 | −0.0320 | −0.0288 | |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Schnaubelt, M.; Rende, J.; Krauss, C. Testing Stylized Facts of Bitcoin Limit Order Books. J. Risk Financial Manag. 2019, 12, 25. https://doi.org/10.3390/jrfm12010025

Schnaubelt M, Rende J, Krauss C. Testing Stylized Facts of Bitcoin Limit Order Books. Journal of Risk and Financial Management. 2019; 12(1):25. https://doi.org/10.3390/jrfm12010025

Chicago/Turabian StyleSchnaubelt, Matthias, Jonas Rende, and Christopher Krauss. 2019. "Testing Stylized Facts of Bitcoin Limit Order Books" Journal of Risk and Financial Management 12, no. 1: 25. https://doi.org/10.3390/jrfm12010025

APA StyleSchnaubelt, M., Rende, J., & Krauss, C. (2019). Testing Stylized Facts of Bitcoin Limit Order Books. Journal of Risk and Financial Management, 12(1), 25. https://doi.org/10.3390/jrfm12010025