Intelligent Decision Support in Proportional–Stop-Loss Reinsurance Using Multiple Attribute Decision-Making (MADM)

Abstract

:1. Introduction

1.1. Background

- The optimal reinsurance form, under given criteria;

- Given the reinsurance form, the choice of reinsurance parameters. (e.g., optimal retention portion for proportional reinsurance, optimal retention limit for stop-loss reinsurance, etc.)

1.2. Paper Development

2. Literature Review

3. Methodology

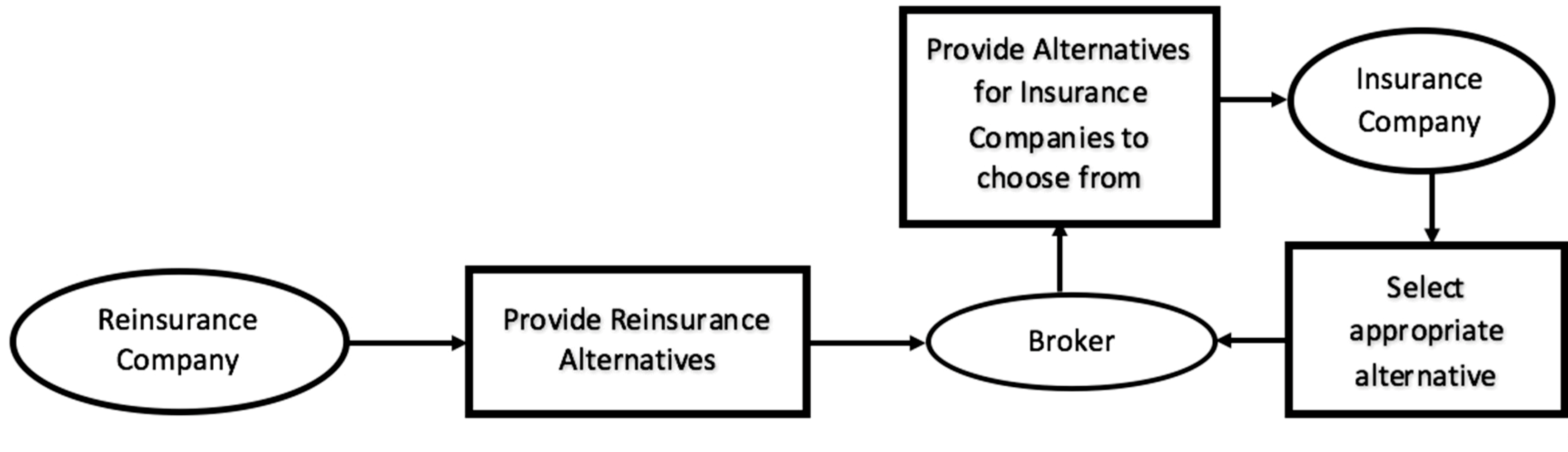

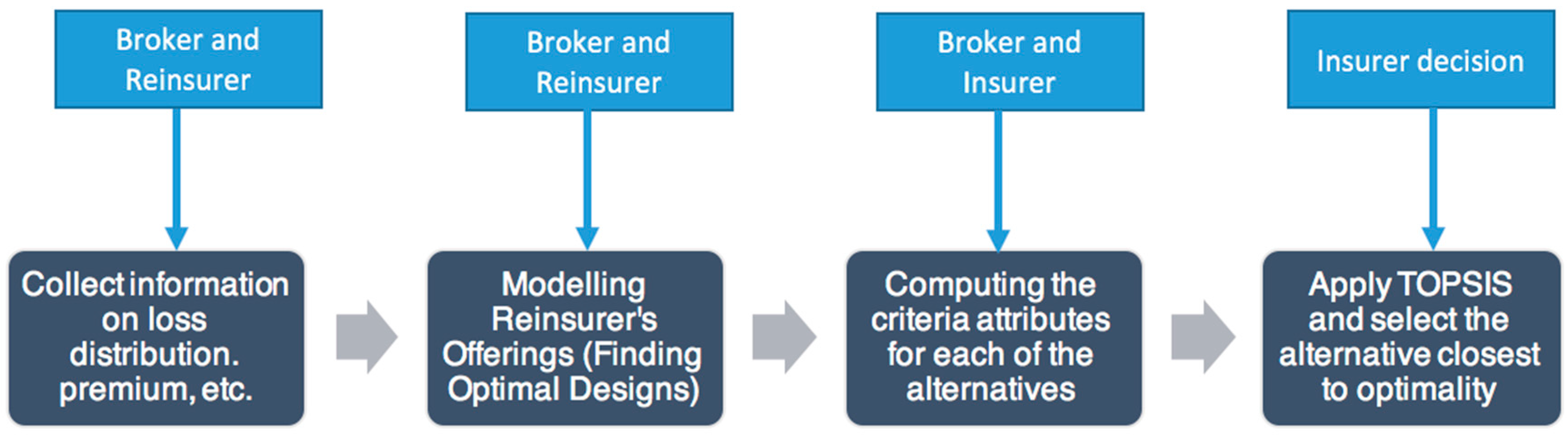

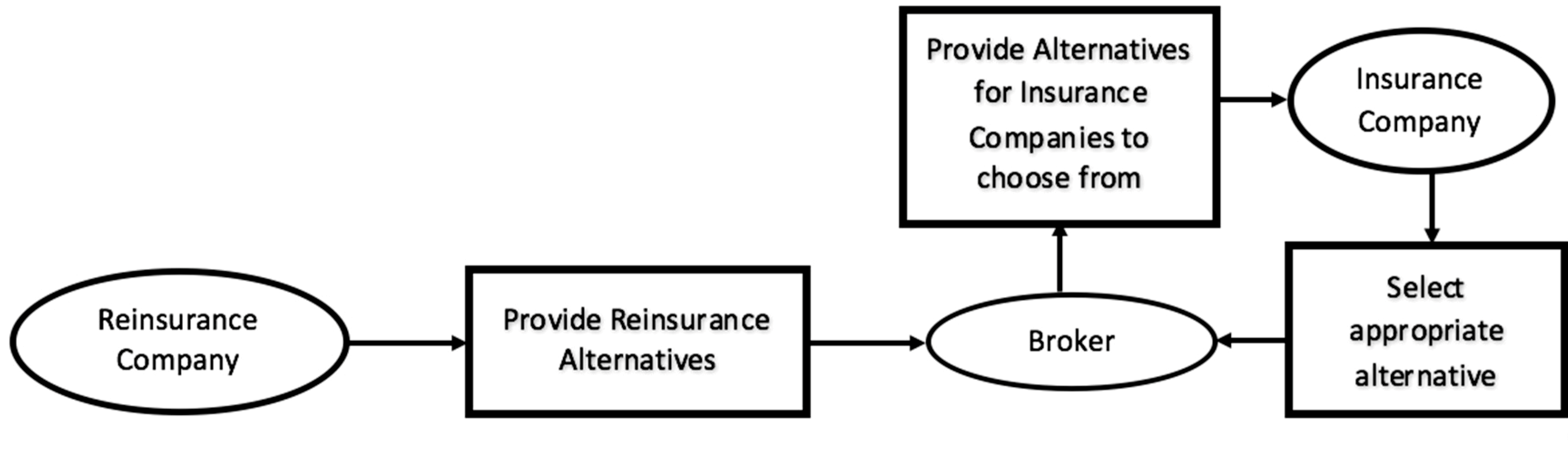

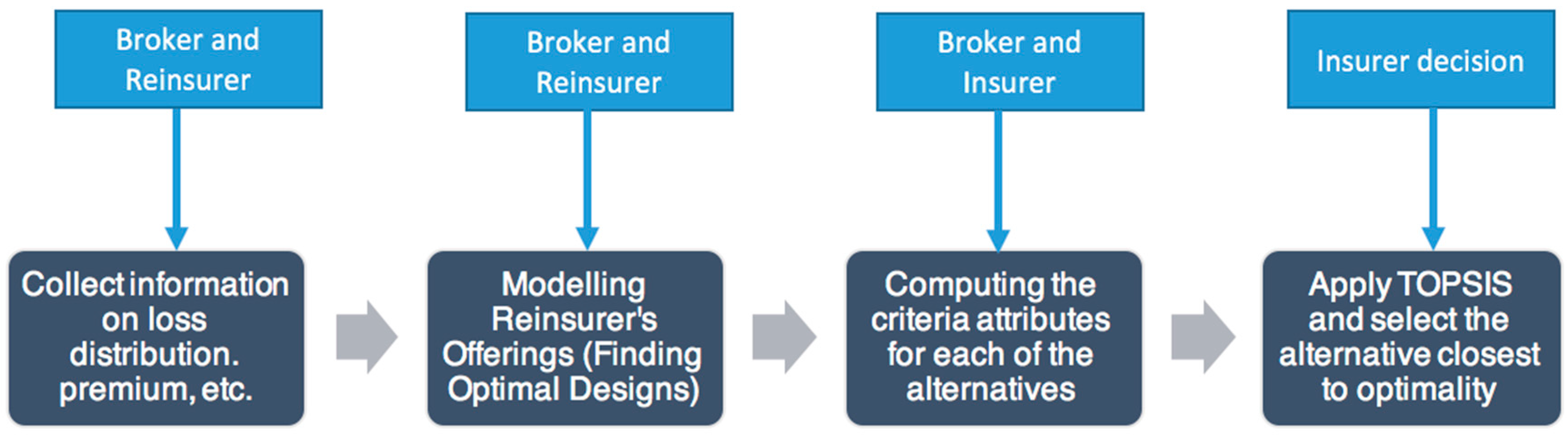

3.1. Decision Flow

3.2. The Proportional–Stop-Loss Reinsurance Model

3.3. Variable Definition

3.4. Simulating Alternatives Using MODM

3.5. Calculating Decision Criteria

3.5.1. Expected Profit of the Insurance Company (Reinsured Party):

3.5.2. Expected Shortfall

3.5.3. Ruin Probability

3.5.4. Expected Utility

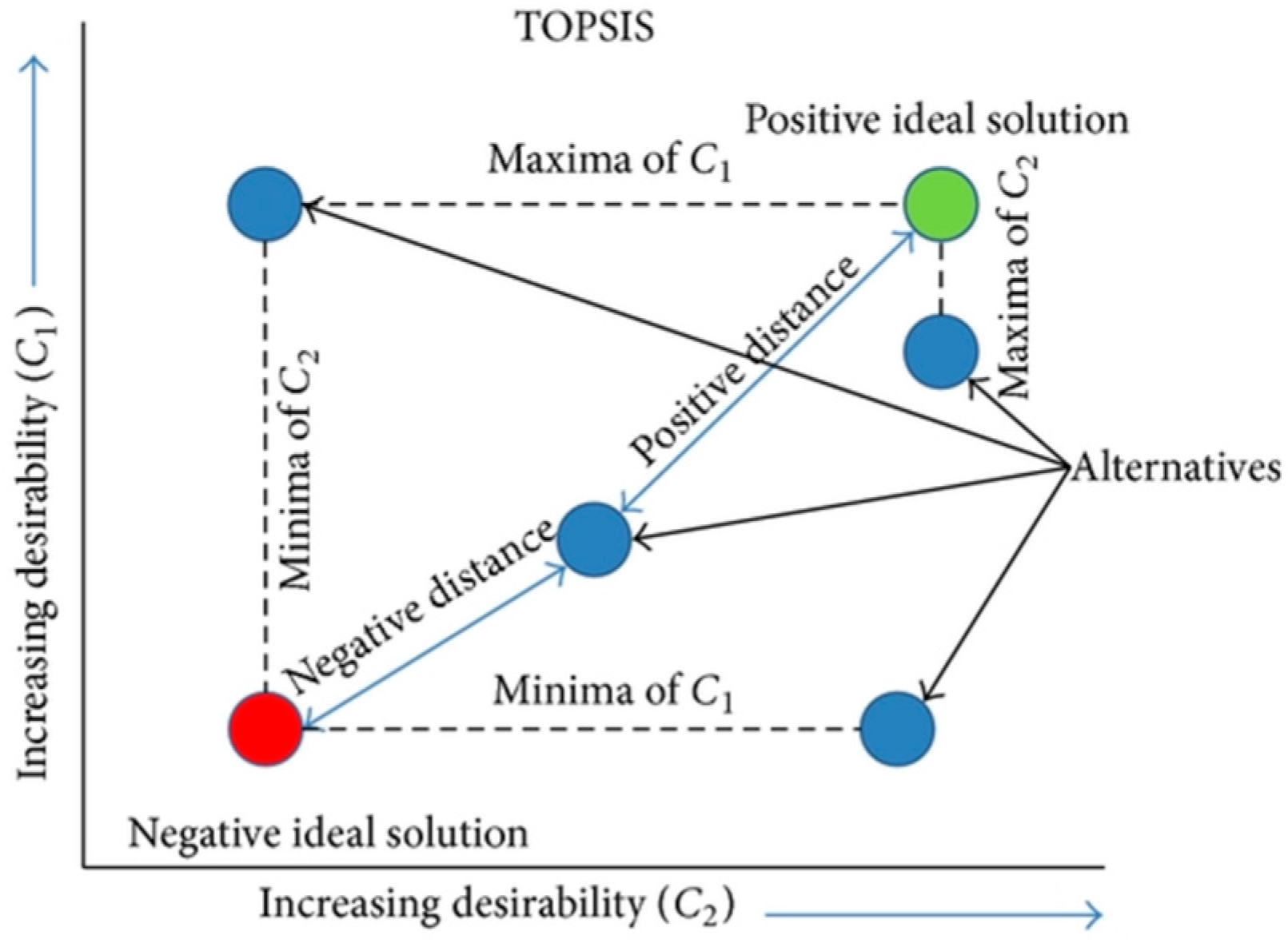

3.6. Selecting the Best Alternative Using MADM

- Formulate decision matrix with alternatives and decision criteria . The attribute value of on for and is represented as .

- Calculate weight of the criteria using entropy technique as follows:

- Normalize the decision matrix using the following formula:One may notice that by scaling the criteria (multiplying a constant to ), the decision will not change. However, it will not necessarily return same decision for different utility functions that generate the same decision under expected utility measurement, as adding a constant to in the formula will change the resulting .

- Calculate the weighted normalized decision matrix by using the normalized decision matrix parameter and weight vector ) to return the weighted normalized decision matrix parameter . If criteria are given same weight, .

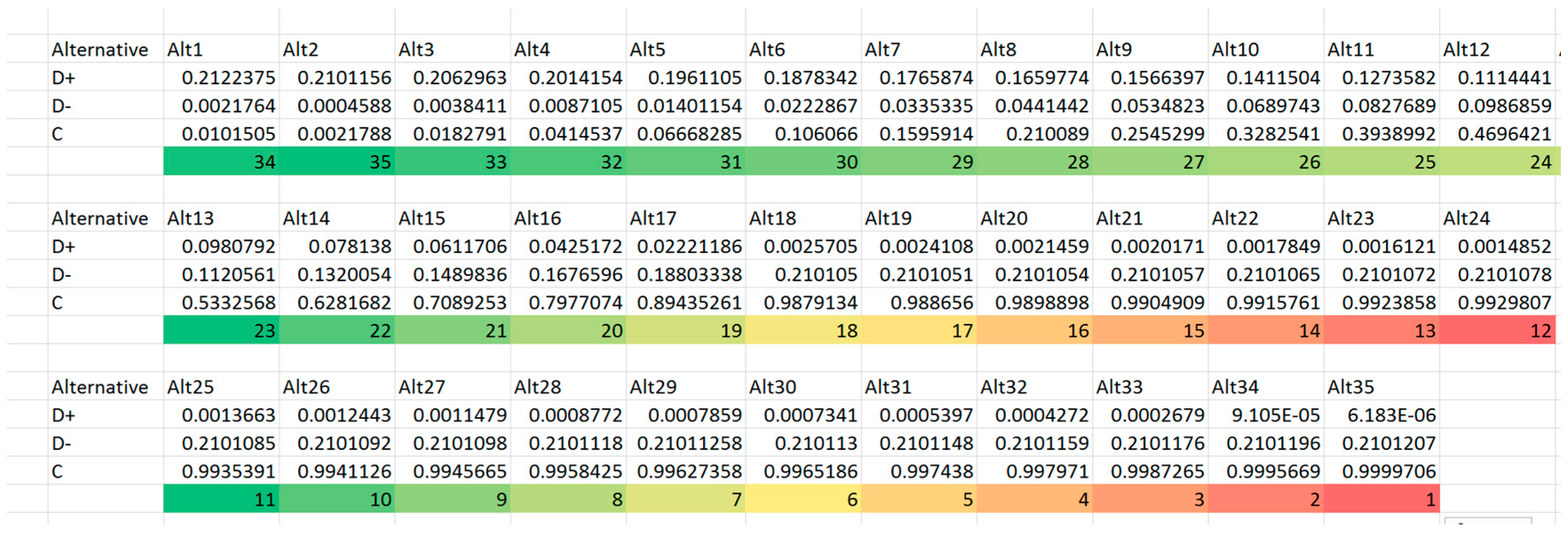

- Compute the vectors of positive ideal solutions and the negative ideal solutions, denoted by:

- Calculate the distance between each alternative and the positive and negative ideal points. The distance between alternative and the positive ideal points is:The distance between alternative and the negative ideal solutions are:

- Calculate the relative closeness coefficient of each alternative represented as:

- Rank the alternatives according to . The alternative with higher value is preferred over lower alternatives.

4. Case Study

4.1. Loss Distribution Modeling

4.2. Generating Alternatives from the Viewpoints of Reinsurers

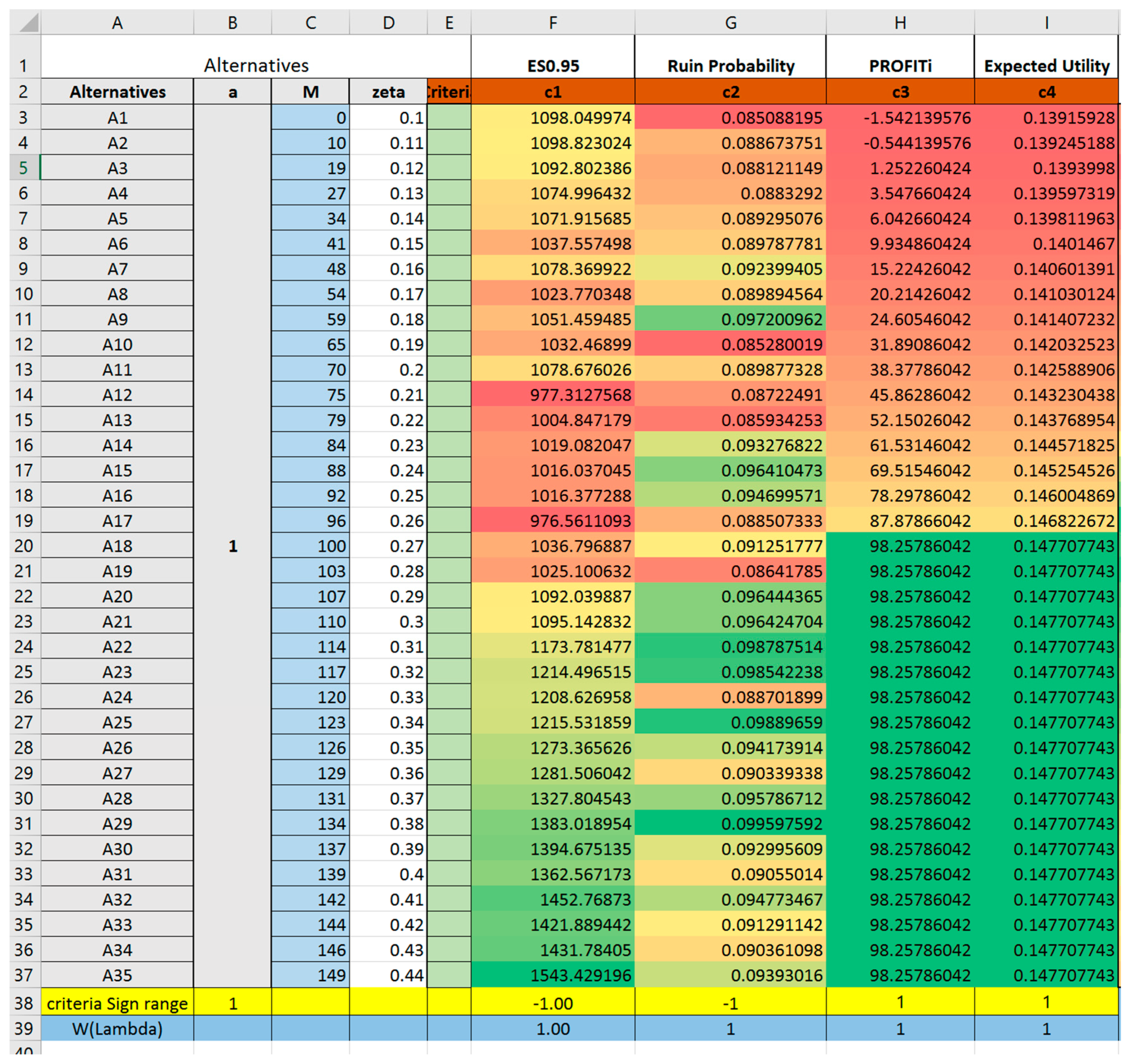

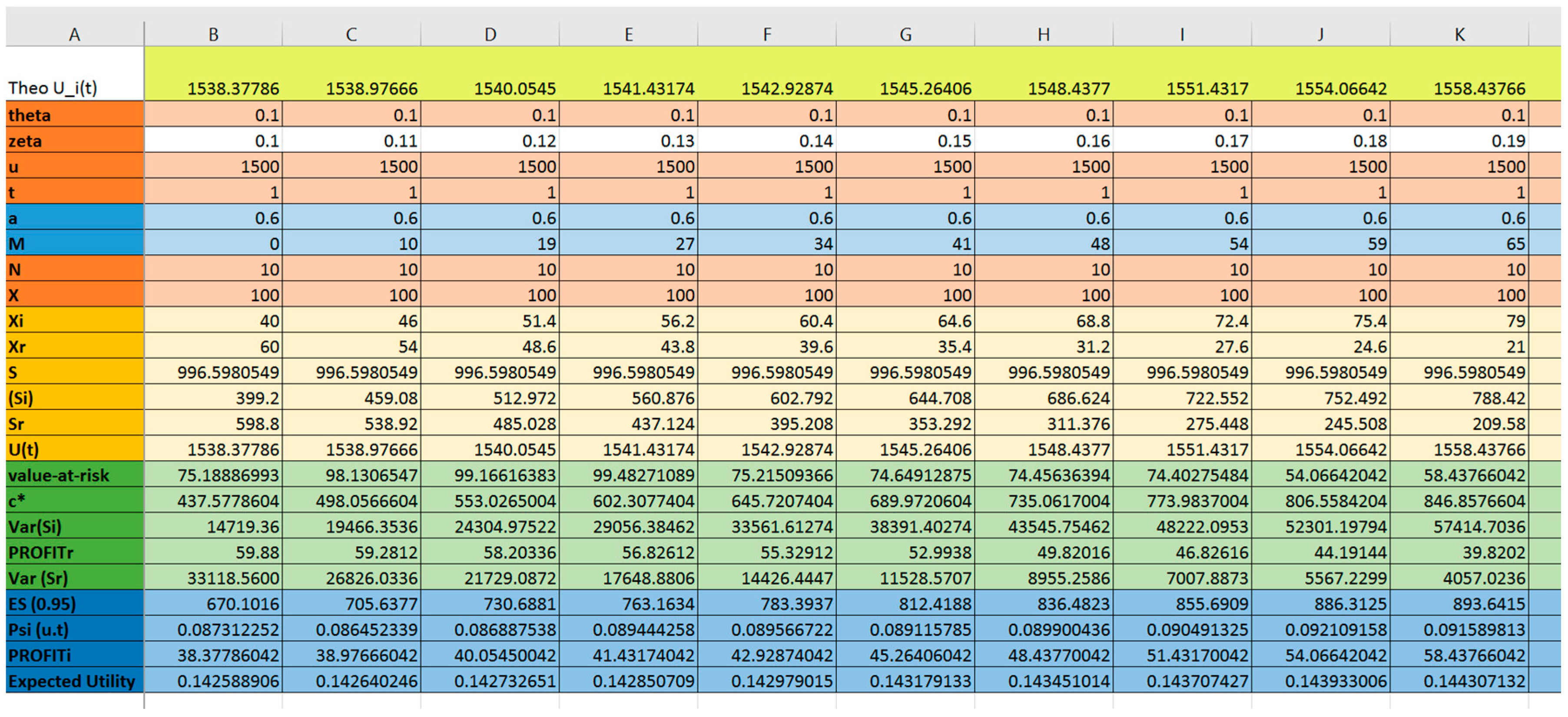

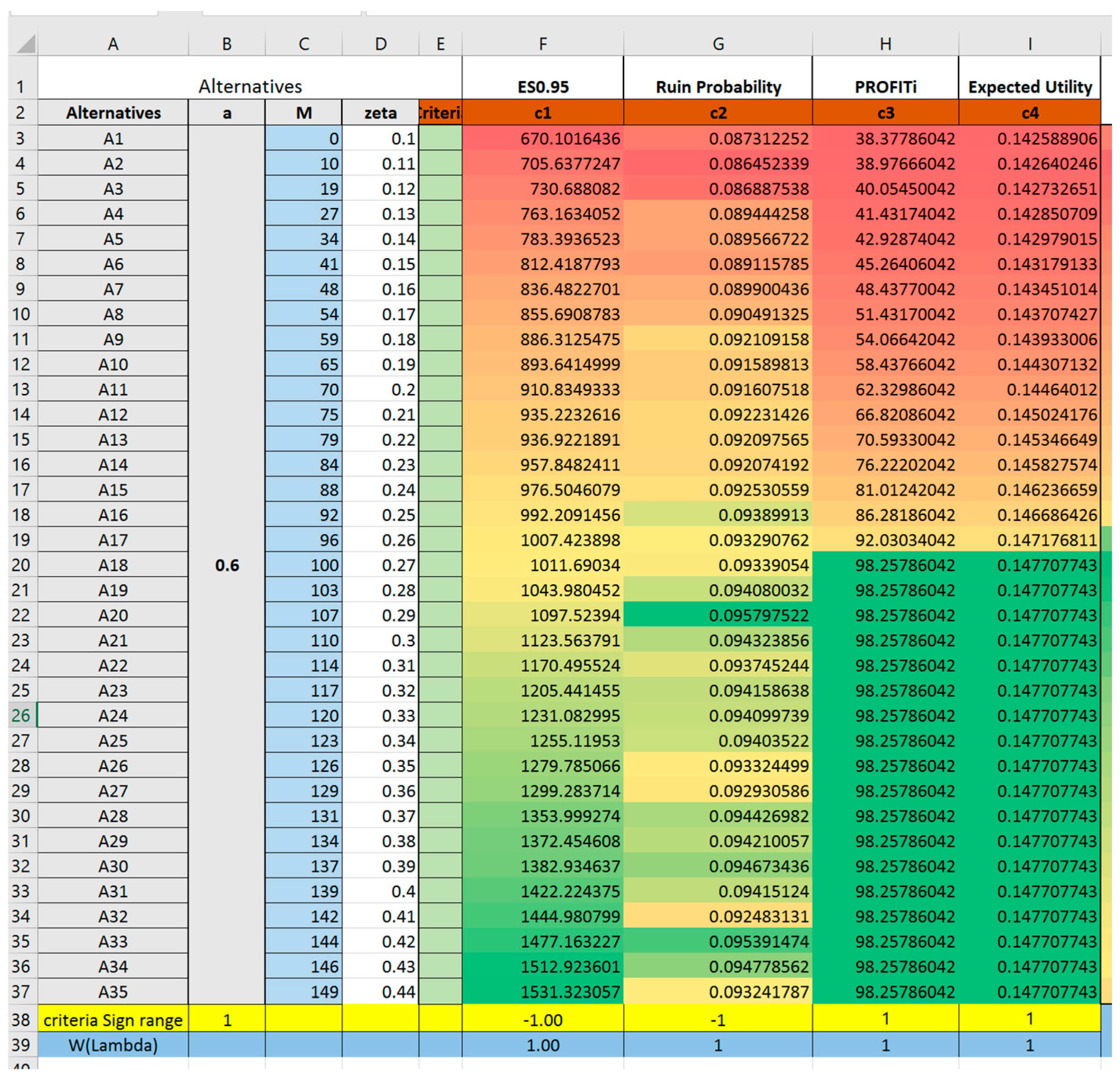

4.3. Constructing Decision Matrix

4.4. Selecting Alternatives Using TOPSIS

| topsis (decisionMakingMatrix,lambdaWeight,criteriaSign) |

5. Managerial Implications

- The best alternative suggested by TOPSIS does not necessarily optimize any one single criterion, rather, it has an overall highest ranking due to its relative weighted closeness to all four criteria. In reality, if reinsurance is chosen merely according to expected profit, the insurance company may suffer from a high probability of financial crisis. On the other hand, if the decision merely considers constraining higher shortfalls, the insurance company may appear to have poor performance based on their profit and loss statement due to the low profits obtained.By increasing the ceding amount from a = 0.6 to a = 0.75, 0.9, one result from Trial 1,2,3,4 (Trial 2–4 are reported in Appendix A) suggests that the ranking of alternatives is different when parameters are changed. When the ceding portions are fixed at relatively lower level (such as a = 0.6 to a = 0.75) the best alternative to choose will have the retention limit equaling to mean value of loss. Thus, if the given reinsurance parameters (either , or ) are altered, it is recommended for the insurance company to evaluate once again the reinsurance plans instead of extrapolating conclusions from previous experiences.

- In addition, Trial 4 with a = 1 models an excess-of-loss reinsurance form where . Accordingly, results from Trial 4 are in accordance with previous knowledge on excess-of-loss reinsurance. Under excess-of-loss reinsurance, the best form is given at , which is in correspondence with Section 2 in Payandeh-Najafabadi and Panahi-Bazaz (2017).

- In each trial, the Alternative 1 M = 0 simulates the scenario of pure proportional reinsurance. Trial 5 attempts to model different retention level under proportional reinsurance () with fixed reinsurance premium loading factor . The result shows that given same premium loading factor, retention level of 0.6 would be most preferable.

- By setting (a, M) to (0, 0), we could also model the scenario of no reinsurance. The results show that with no reinsurance, the expected shortfall of insurance company will be significantly higher than all other alternatives, and the ruin probability will be higher as well. This suggests that insurance company without reinsurance is more likely to become bankrupt if large losses are incurred. As compensation, the expected profit and utility will increase by a small amount for the insurance company due to high profit from insurance premium and low probability of large losses. However, noting the high ruin probability, which suggests a much higher risk of bankruptcy, the insurance company will often seek for reinsurance to keep ruin probability low.

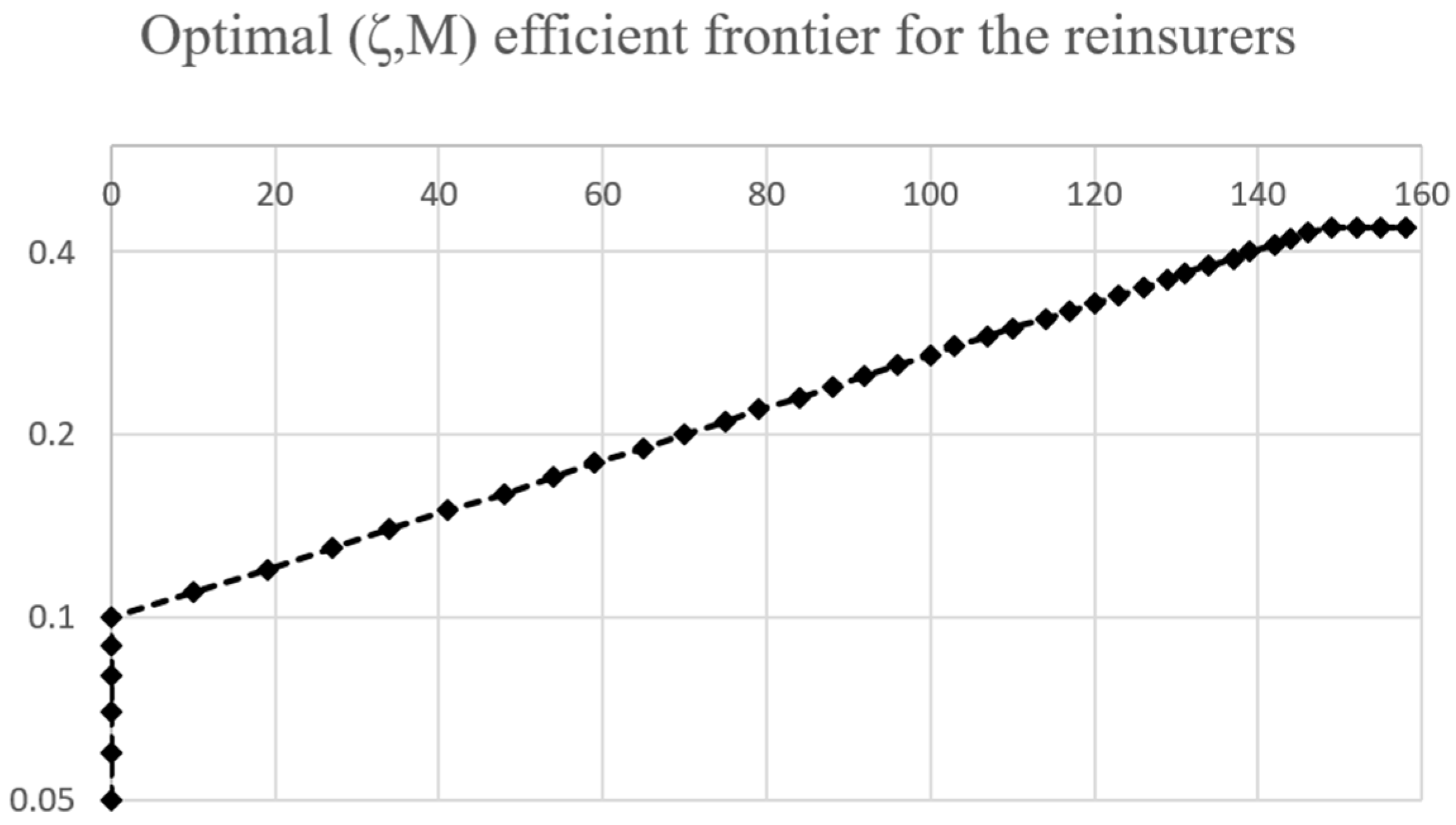

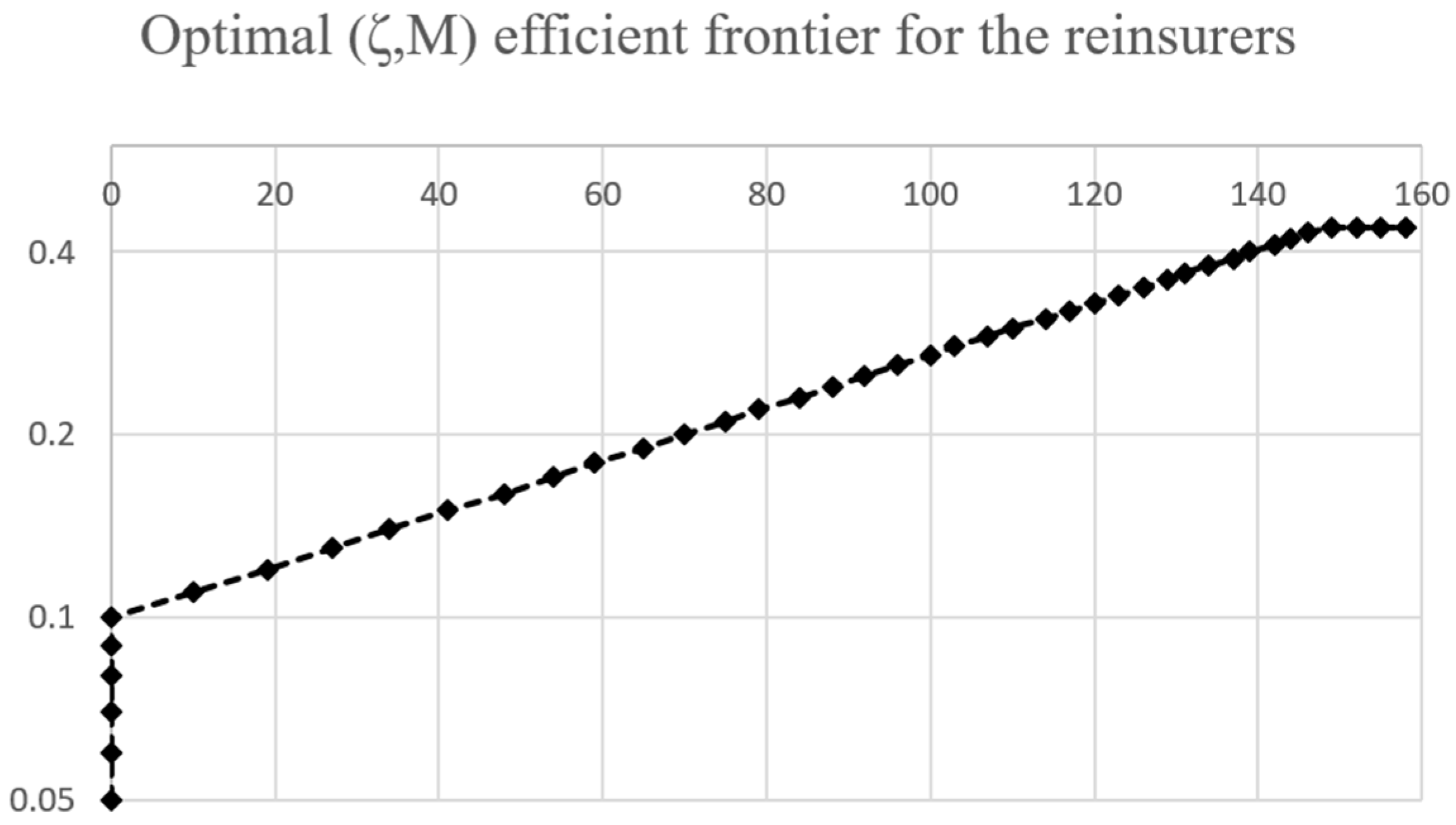

- Furthermore, through the simulation process, the variance and profitability of the reinsurer are also being observed and calculated (as can be seen from Figure 9). The result was in correspondence with our previous argument that by scaling the ceding portion a to larger values, both the variance and the profitability of the reinsurer will increase, suggesting that there is a trade-off between high profit and high risk of large losses. Thus, this supports our previous assumption that the reinsurer is ambiguous towards a design that only differs with respect to parameter a.

6. Conclusions

6.1. Contributions

- To the best of our knowledge, this is the first theoretical study using MADM to approach proportional–stop-loss reinsurance model, though there are a few recent studies using MADM in designing either pure proportional or pure stop-loss reinsurance contracts;

- This is one of the few studies taking a non-discriminatory position considering both the insurance and the reinsurance company in designing an optimal reinsurance contract, and the study made significant contribution by incorporating existing MODM models and the promising MADM model into one decision flow process to arrive at a robust decision for reinsurance design;

- This study demonstrates the feasibility of incorporating intelligent decision supporting systems in reinsurance deal-making. As observed by the author through industry experiences, @Risk has grown its popularity recently for actuarial study in modeling risk and claims. The prototype of TOPSIS implemented through Matlab suggests that a software of multi-criteria decision support would be promising.

- As previous research suggested (Bazaz and Najafabadi 2015), MADM is not likely to address finding of optimal type of reinsurance. However, with the generic formulation of proportional–stop-loss reinsurance, we would be able to model proportional reinsurance and stop-loss reinsurance as special cases of proportional–stop-loss, thus the choice between proportional and non-proportional reinsurance using MADM could be possible under this formulation of reinsurance.

6.2. Limitations

- In terms of the scope of study, due to time and resource constraints the study only considers proportional-stop-loss treaty reinsurance, while basing the decision process on ruin probability, CVaR, and expected utility criteria. Other types of reinsurance and decision measurements have not been elaborated and tested.

- In terms of methodology, this study attempts to utilize the simulation software @Risk to model the loss and claim distribution and to use numerical TOPSIS model in modeling decisions from the insurance company, without reaching to a close-form solution. Thus, the conclusions were drawn based on simulation result rather than robust theoretical derivation.

- In terms of model implementation, due to resource constraints, this study only includes a numerical made-up case instead of existing cases to conduct archival research in addressing the decision process in the reinsurance purchase decisions.

6.3. Future Directions

Author Contributions

Conflicts of Interest

Appendix A. TOPSIS Trials #2, #3 and #4

References

- Ameri Sianaki, Omid. 2015. Intelligent Decision Support System for Energy Management in Demand Response Programs and Residential and Industrial Sectors of the Smart Grid. Doctoral dissertation, Curtin University, Bentley, Western Australia, Australia. [Google Scholar]

- Bazaz, Ali Panahi, and Amir T Payandeh Najafabadi. 2015. An Optimal Reinsurance Contract from Insurer’s and Reinsurer’s Viewpoints. Applications & Applied Mathematics 10: 970–982. [Google Scholar]

- Borch, Karl. 1960. Reciprocal Reinsurance Treaties Seen as a Two-Person Co-Operative Game. Scandinavian Actuarial Journal 1960: 29–58. [Google Scholar] [CrossRef]

- Borck, Karl. 1960. An Attempt to Determine the Optimum Amount of Stop Loss Reinsurance. Brussels: Brussels, pp. 597–610. [Google Scholar]

- Cai, Jun, Haiyan Liu, and Ruodu Wang. 2017. Pareto-optimal reinsurance arrangements under general model settings. Insurance: Mathematics and Economics. [Google Scholar] [CrossRef]

- Carter, R. L. 1979. Reinsurance. Berlin: Springer. [Google Scholar]

- Chauhan, Aditya, and Rahul Vaish. 2013. Fluid Selection of Organic Rankine Cycle Using Decision Making Approach. Journal of Computational Engineering 2013. [Google Scholar] [CrossRef]

- Hürlimann, Werner. 2011. Optimal Reinsurance Revisited–point of View of Cedent and Reinsurer. Astin Bulletin 41: 547–74. [Google Scholar]

- Hwang, Ching-Lai, Young-Jou Lai, and Ting-Yun Liu. 1993. A new approach for multiple objective decision making. Computers and Operational Research 20: 889–99. [Google Scholar] [CrossRef]

- Hwang, Ching-Lai, and Kwangsun Yoon. 1981. Multiple Attribute Decision Making: Methods and Applications. New York: Springer. [Google Scholar]

- Karageyik, Başak Bulut, and David Dickson. 2016. Optimal reinsurance under multiple attribute decision making. Annals of Actuarial Science 10: 65–86. [Google Scholar] [CrossRef]

- Karageyik, Başak Bulut, and Şule Şahin. 2017. Determination of the Optimal Retention Level Based on Different Measures. Journal of Risk and Financial Management 10: 4. [Google Scholar] [CrossRef]

- Liang, Haiming. 2014. Research on Methods for Two-Sided Trade Matching Decision-Making Based on the Broker. Ph.D. Thesis, Northeastern University, Boston, MA, USA. [Google Scholar]

- Payandeh-Najafabadi, Amir T, and Ali Panahi-Bazaz. 2017. An Optimal Combination of Proportional and Stop-Loss Reinsurance Contracts from Insurer’s and Reinsurer’s Viewpoints. arXiv Preprint, arXiv:1701.05450. [Google Scholar]

- Samson, Danny, and Howard Thomas. 1983. Reinsurance Decision Making and Expected Utility. The Journal of Risk and Insurance 50: 249–64. [Google Scholar] [CrossRef]

- Samson, Danny, and Howard Thomas. 1985. Decision analysis models in reinsurance. European Journal of Operational Research 19: 201–11. [Google Scholar] [CrossRef]

- Vajda, Stefan. 1962. Minimum Variance Reinsurance. Astin Bulletin 2: 257–60. [Google Scholar] [CrossRef]

- Wang, Gang. 2003. Reinsurance Optimization Models. Ph.D. Thesis, Hunan University, Changsha, China. [Google Scholar]

- Yoon, Kwangsun. 1987. A reconciliation among discrete compromise situations. Journal of Operational Research Society 38: 277–86. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variable | Variable Explanation |

|---|---|

| the time period of one contract, in our case study ; | |

| the number of claims incurred in period t (during one contract); | |

| the wealth held by insurance company at time t; | |

| the loading factor of the reinsurance premium paid to the reinsurer; | |

| the loading factor of the premium paid to the reinsured party; | |

| the claim amount of one single loss; | |

| the claim amount payable by the insurance company (the reinsured party); | |

| the claim amount payable by the reinsurance company (the reinsurer); | |

| the aggregate loss of an insurance portfolio; | |

| the aggregate claim (loss) incurred to insurance company (the reinsured party); | |

| the aggregate claim (loss) incurred to the reinsurance company (reinsurer); | |

| the cumulative distribution function of S; | |

| the survival distribution function of S; | |

| the proportional–stop-loss reinsurance parameter,; | |

| the total premium per unit time; | |

| the premium gained by the insurance company; | |

| the premium payable to the reinsurer; | |

| the expected shortfall with a confidence level of ; | |

| the expected profit gained by insurance company; | |

| the ruin probability of insurance company’s wealth ; | |

| the utility of insurance company at the end of period t; |

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, S.J.X.; Poh, K.L. Intelligent Decision Support in Proportional–Stop-Loss Reinsurance Using Multiple Attribute Decision-Making (MADM). J. Risk Financial Manag. 2017, 10, 22. https://doi.org/10.3390/jrfm10040022

Wang SJX, Poh KL. Intelligent Decision Support in Proportional–Stop-Loss Reinsurance Using Multiple Attribute Decision-Making (MADM). Journal of Risk and Financial Management. 2017; 10(4):22. https://doi.org/10.3390/jrfm10040022

Chicago/Turabian StyleWang, Shirley Jie Xuan, and Kim Leng Poh. 2017. "Intelligent Decision Support in Proportional–Stop-Loss Reinsurance Using Multiple Attribute Decision-Making (MADM)" Journal of Risk and Financial Management 10, no. 4: 22. https://doi.org/10.3390/jrfm10040022

APA StyleWang, S. J. X., & Poh, K. L. (2017). Intelligent Decision Support in Proportional–Stop-Loss Reinsurance Using Multiple Attribute Decision-Making (MADM). Journal of Risk and Financial Management, 10(4), 22. https://doi.org/10.3390/jrfm10040022