Value-Based Health Care: Long-Term Care Insurance for Out-of-Pocket Medical Expenses and Self-Rated Health

Abstract

1. Introduction

2. Literature Review

2.1. Long-Term Care Insurance Policy Context

2.2. Long-Term Care Insurance and Medical Expenses

2.3. Long-Term Care Insurance and Health

2.4. Reasons for the Controversy

3. Materials and Methods

3.1. Data Source

3.2. Variable Definition and Data Description

3.3. Identification Strategy and Model Setting

4. Results

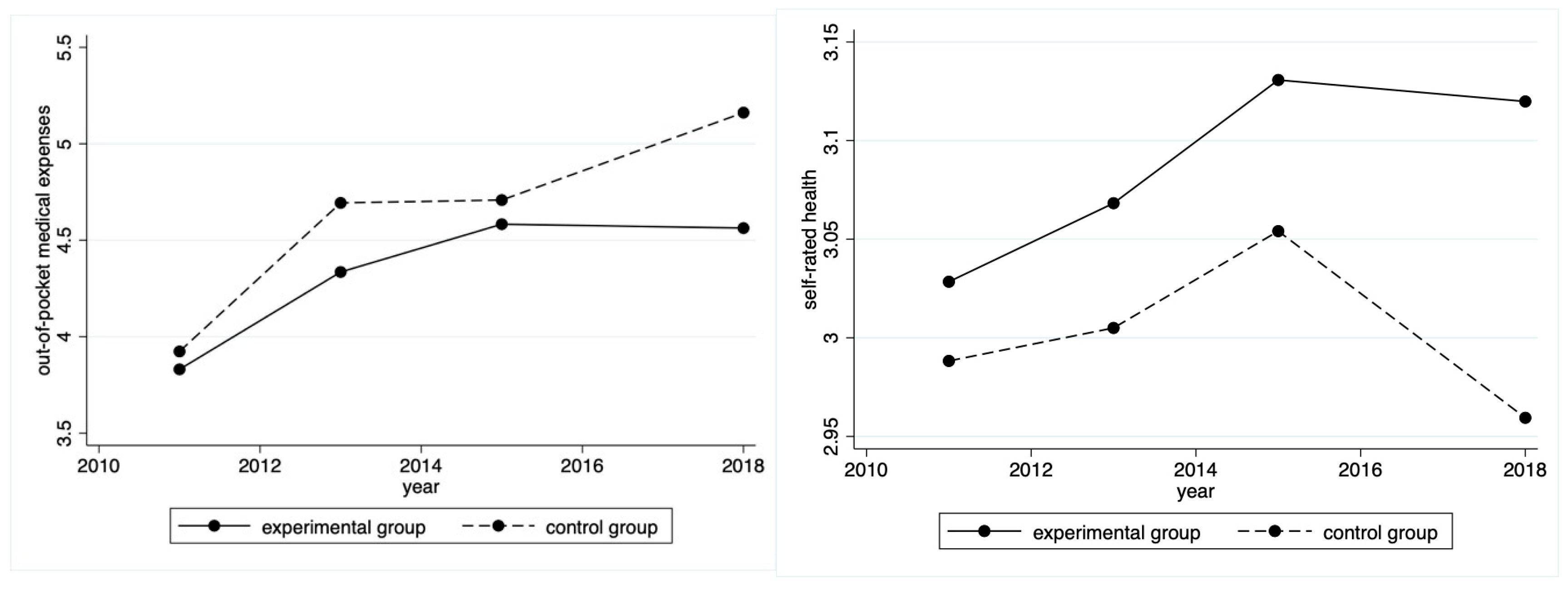

4.1. Time Trends in Out-of-Pocket Medical Expenses and Self-Rated Health

4.2. The Balance Test

4.3. DID Results Based on the Matched Samples

4.4. Robustness Test

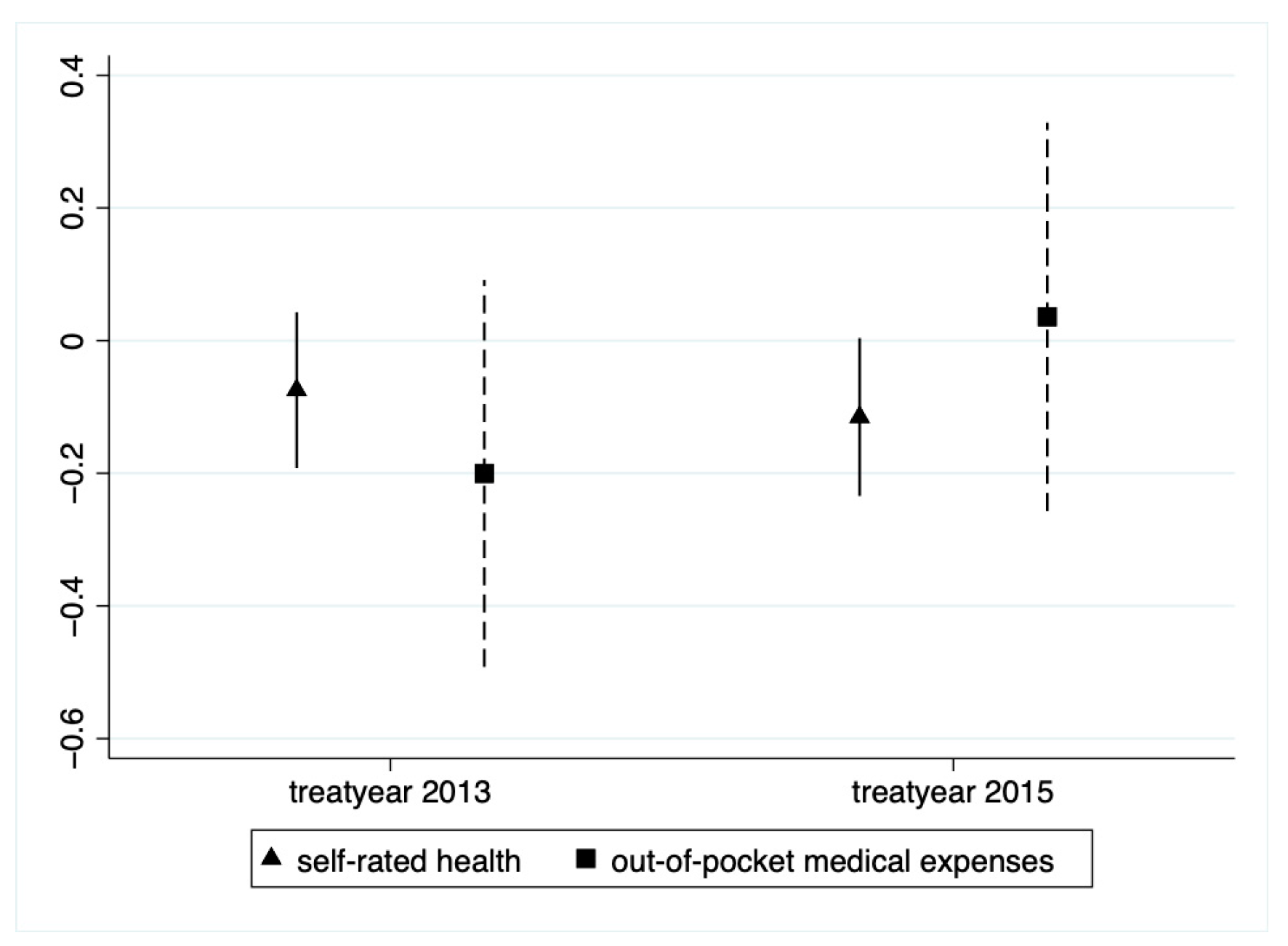

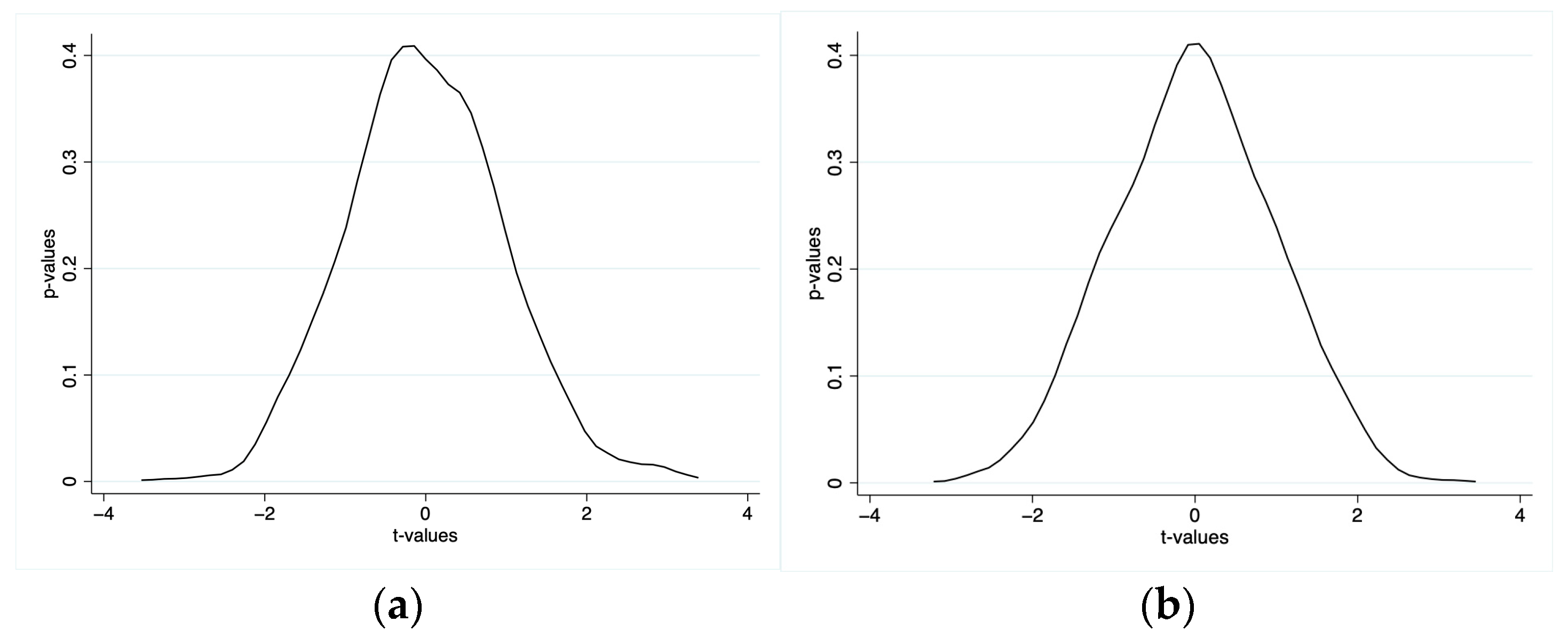

4.4.1. Parallel Trend Test

4.4.2. Placebo Effect

4.4.3. Tail-Curtailing

4.4.4. Change the PSM Matching Mode

4.5. Heterogeneity Test

4.5.1. Urban and Rural Heterogeneity Analysis

4.5.2. Disabled and Non-Disabled Heterogeneity Analysis

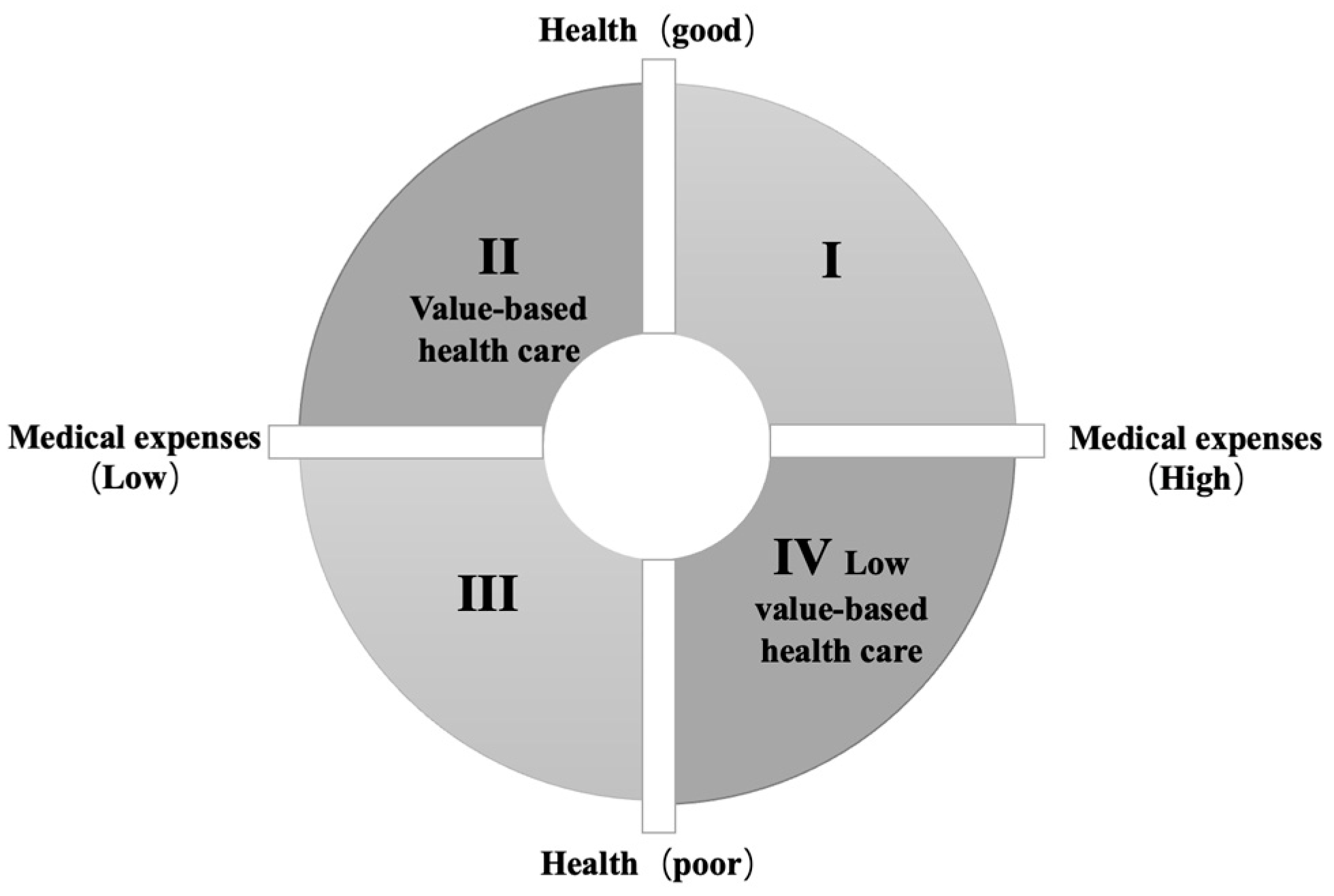

5. A Brief Discussion on Cost-Benefit Analysis

6. Conclusions and Implications

7. Limitations and Future Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Wei, J.; Zhang, J.; Deng, Y.; Sun, L.; Guo, P. Suicidal ideation among the Chinese elderly and its correlates: A comparison between the rural and urban populations. Int. J. Environ. Res. Public Health 2018, 15, 422. [Google Scholar] [CrossRef] [PubMed]

- Teng, E.J.; Friedman, L.C. Increasing mental health awareness and appropriate service use in older Chinese Americans: A pilot intervention. Patient Educ. Couns. 2009, 76, 143–146. [Google Scholar] [CrossRef] [PubMed]

- Han, Y.; Shen, T. Long-term care insurance pilot programme in China: Policy evaluation and optimization options—Taking the pilot programme in the Northeast of China as an Example. Int. J. Environ. Res. Public Health 2022, 19, 4298. [Google Scholar] [CrossRef] [PubMed]

- Fang, H. Population aging, retirement income security, and asset markets in China. NBER Rep. 2018, 2, 18–22. [Google Scholar]

- Jin, H.; Wang, H.; Li, X.; Zheng, W.; Ye, S.; Zhang, S.; Zhou, J.; Pennington, M. Economic burden of COVID-19, China, January–March, 2020: A cost-of-illness study. Bull. World Health Organ. 2021, 99, 112–114. [Google Scholar] [CrossRef]

- Yip, W.; Fu, H.; Chen, A.T.; Zhai, T.; Jian, W.; Xu, R.; Pan, J.; Hu, M.; Zhou, Z.; Chen, Q.; et al. 10 years of health-care reform in China: Progress and gaps in universal health coverage. Lancet 2019, 394, 1192–1204. [Google Scholar] [CrossRef] [PubMed]

- Zhou, R.; Cheng, J.; Wang, S.; Yao, N. A qualitative study of home health care experiences among Chinese homebound adults. BMC Geriatr. 2021, 21, 309. [Google Scholar] [CrossRef]

- Anderson, G. The challenge of financing care for individuals with multimorbidities. Medicine 2011, 81–107. [Google Scholar]

- Hofmarcher, M.M.; Oxley, H.; Rusticelli, E. Improved Health System Performance through better Care Coordination; OECD Health Working; OECD Publishing: Paris, France, 2007. [Google Scholar]

- Costa-font, J.; Courbage, C.; Swartz, K. Financing long-term care: Ex ante, ex post or both? Health Econ. 2015, 24, 45–57. [Google Scholar] [CrossRef]

- Wang, Q.; Zhou, Y.; Ding, X.; Ying, X. Demand for long-term care insurance in China. Int. J. Environ. Res. Public Health 2018, 15, 6. [Google Scholar] [CrossRef]

- Dai, W. Is China facing the social risks associated with reliance on hospitalization for the care of the elderly with chronic diseases? Int. J. Health Plan. Manag. 2019, 34, 794–805. [Google Scholar] [CrossRef] [PubMed]

- Forder, J. Long-term care and hospital utilisation by older people: An analysis of substitution rates. Health Econ. 2009, 18, 1322–1338. [Google Scholar] [CrossRef] [PubMed]

- Gaughan, J.; Gravelle, H.; Siciliani, L. Testing the bed-blocking hypothesis: Does nursing and care home supply reduce delayed hospital discharges? Health Econ. 2015, 24, 32–44. [Google Scholar] [CrossRef] [PubMed]

- Porter, M.E. What is value in health care. New Engl. J. Med. 2010, 363, 2477–2481. [Google Scholar] [CrossRef] [PubMed]

- Bermejo, F.; Del Pozo, R.; Moya, P. Main factors determining the economic production sustained by public long-term care spending in Spain. Int. J. Environ. Res. Public Health 2021, 18, 9199. [Google Scholar] [CrossRef] [PubMed]

- Chernew, M.E.; Rosen, A.B.; Fendrick, A.M. Value-Based Insurance Design: By abandoning the archaic principle that all services must cost the same for all patients, we can move to a high-value health system. Health Aff. 2007, 26 (Suppl. 2), w195–w203. [Google Scholar] [CrossRef]

- Anderson, G.F.; Frogner, B.K. Health spending in OECD countries: Obtaining value per dollar. Health Aff. 2008, 27, 1718–1727. [Google Scholar] [CrossRef]

- McGinnis, J.M.; Stuckhardt, L.; Saunders, R.; Smith, M. Best Care at Lower Cost: The Path to Continuously Learning Health Care in America; National Academies Press: Washington, DC, USA, 2013. [Google Scholar]

- Macinko, J.; Starfield, B.; Shi, L. The contribution of primary care systems to health outcomes within Organization for Economic Cooperation and Development (OECD) countries, 1970–1998. Health Serv. Res. 2003, 38, 831–865. [Google Scholar] [CrossRef]

- Anderson, G.F.; Hussey, P.S.; Frogner, B.K.; Waters, H.R. Health spending in the United States and the rest of the industrialized world. Health Aff. 2005, 24, 903–914. [Google Scholar] [CrossRef]

- Papanicolas, I.; Woskie, L.; Jha, A.K. Health care spending in the United States and other high-income countries. J. Am. Med. Assoc. 2018, 319, 1024–1039. [Google Scholar] [CrossRef]

- Choi, J.W.; Park, E.-C.; Lee, S.G.; Park, S.; Ryu, H.-G.; Kim, T.H. Does long-term care insurance reduce the burden of medical costs? A retrospective elderly cohort study. Geriatr. Gerontol. Int. 2018, 18, 1641–1646. [Google Scholar] [CrossRef] [PubMed]

- Feng, J.; Wang, Z.; Yu, Y. Does long-term care insurance reduce hospital utilization and medical expenditures? Evidence from China. Soc. Sci. Med. 2020, 258, 113081. [Google Scholar] [CrossRef]

- Kim, H.B.; Lim, W. Long-term care insurance, informal care, and medical expenditures. J. Public Econ. 2015, 125, 128–142. [Google Scholar] [CrossRef]

- Al-Hanawi, M.K.; Mwale, M.L.; Qattan, A.M.N. Health insurance and out-of-pocket expenditure on health and medicine: Heterogeneities along income. Front. Pharmacol. 2021, 12, 638035–638048. [Google Scholar] [CrossRef] [PubMed]

- Sperber, N.R.; Voils, C.I.; Coe, N.B.; Konetzka, R.T.; Boles, J.; Van Houtven, C.H. How can adult children influence parents’ long-term care insurance purchase decisions? Gerontologist 2017, 57, 292–299. [Google Scholar] [CrossRef] [PubMed]

- Mosca, I.; Van Der Wees, P.J.; Mot, E.S.; Wammes, J.J.; Jeurissen, P.P. Sustainability of long-term care: Puzzling tasks ahead for policy-makers. Int. J. Health Policy Manag. 2017, 6, 195–205. [Google Scholar] [CrossRef]

- Fang, H.; Eggleston, K.; Hanson, K.; Wu, M. Enhancing financial protection under China’s social health insurance to achieve universal health coverage. Br. Med. J. 2019, 365, l2378. [Google Scholar] [CrossRef]

- Gade, G.; Venohr, I.; Conner, D.; McGrady, K.; Beane, J.; Richardson, R.H.; Williams, M.P.; Liberson, M.; Blum, M.; Della Penna, R. Impact of an inpatient palliative care team: A randomized controlled trial. J. Palliat. Med. 2008, 11, 180–190. [Google Scholar] [CrossRef]

- Di Pollina, L.; Guessous, I.; Petoud, V.; Combescure, C.; Buchs, B.; Schaller, P.; Kossovsky, M.; Gaspoz, J.-M. Integrated care at home reduces unnecessary hospitalizations of community-dwelling frail older adults: A prospective controlled trial. BMC Geriatr. 2017, 17, 53. [Google Scholar] [CrossRef]

- Hyun, K.-R.; Kang, S.; Lee, S. Does long-term care insurance affect the length of stay in hospitals for the elderly in Korea? A difference-in-difference method. BMC Health Serv. Res. 2014, 14, 630. [Google Scholar] [CrossRef]

- Bailey, M.J.; Goodman-Bacon, A. The War on Poverty’s experiment in public medicine: Community health centers and the mortality of older Americans. Am. Econ. Rev. 2015, 105, 1067–1104. [Google Scholar] [CrossRef] [PubMed]

- Deraas, T.S.; Berntsen, G.R.; Hasvold, T.; Førde, O.H. Does long-term care use within primary health care reduce hospital use among older people in Norway? A national five-year population-based observational study. BMC Health Serv. Res. 2011, 11, 287. [Google Scholar] [CrossRef]

- Costa-Font, J.; Jimenez-Martin, S.; Vilaplana, C. Does long-term care subsidization reduce hospital admissions and uti-lization? J. Health Econ. 2018, 58, 43–66. [Google Scholar] [CrossRef] [PubMed]

- Wooldridge, J.; Schore, J. The evaluation of the National Long Term Care Demonstration. 7. The effect of channeling on the use of nursing homes, hospitals, and other medical services. Health Serv. Res. 1988, 23, 119–127. [Google Scholar] [PubMed]

- McKnight, R. Home care reimbursement, long-term care utilization, and health outcomes. J. Public Econ. 2006, 90, 293–323. [Google Scholar] [CrossRef]

- Bak, E.; Dobrzyn-Matusiak, D.; Marcisz, C.; Kulik, H.; Marcisz, E. Physical and mental health aspects of elderly in social care in Poland. Clin. Interv. Aging 2014, 9, 1793–1802. [Google Scholar] [CrossRef]

- Na, L.; Streim, J.E. Psychosocial well-being associated with activity of daily living stages among community-dwelling older adults. Gerontol. Geriatr. Med. 2017, 3, 2333721417700011. [Google Scholar] [CrossRef]

- Choi, J.; Joung, E. The association between the utilization of long-term care services and mortality in elderly Koreans. Arch. Gerontol. Geriatr. 2016, 65, 122–127. [Google Scholar] [CrossRef]

- Spiers, G.; Matthews, F.E.; Moffatt, S.; Barker, R.O.; Jarvis, H.; Stow, D.; Kingston, A.; Hanratty, B. Impact of social care supply on healthcare utilisation by older adults: A systematic review and meta-analysis. Age Ageing 2019, 48, 57–66. [Google Scholar] [CrossRef]

- Rodrigues, R.; Ilinca, S.; Schmidt, A.E. Income-rich and wealth-poor? The impact of measures of socio-economic status in the analysis of the distribution of long-term care use among older people. Health Econ. 2018, 27, 637–646. [Google Scholar] [CrossRef]

- Tenand, M.; Bakx, P.; Van Doorslaer, E. Equal long-term care for equal needs with universal and comprehensive coverage? An assessment using Dutch administrative data. Health Econ. 2020, 29, 435–451. [Google Scholar] [CrossRef] [PubMed]

- García-Gómez, P.; Hernández-Quevedo, C.; Jiménez-Rubio, D.; Oliva-Moreno, J. Inequity in long-term care use and unmet need: Two sides of the same coin. J. Health Econ. 2015, 39, 147–158. [Google Scholar] [CrossRef] [PubMed]

- Newhouse, J.P. Medical care costs: How much welfare loss? J. Econ. Perspect. 1992, 6, 3–21. [Google Scholar] [CrossRef] [PubMed]

- Rice, T.; Thomas, K.; Weissert, W. The effect of owning private long-term care insurance policies on out-of-pocket costs. Health Serv. Res. 1991, 25, 907–933. [Google Scholar] [PubMed]

- Tang, Y.; Chen, T.; Zhao, Y.; Taghizadeh-Hesary, F. The Impact of the Long-Term Care Insurance on the Medical Expenses and Health Status in China. Front. Public Health 2022, 10, 876–888. [Google Scholar] [CrossRef]

- Palumbo, M.G. Uncertain medical expenses and precautionary saving near the end of the life cycle. Rev. Econ. Stud. 1999, 66, 395–421. [Google Scholar] [CrossRef]

- Yi, J.-J.; Yoo, W.-K.; Kim, S.-Y.; Kim, K.-K.; Yi, S.-W. Medical expenses by site of cancer and survival time among cancer patients in the last one year of life. J. Prev. Med. Public Health 2005, 38, 9–15. [Google Scholar]

- Scanlon, W.J. Possible reforms for financing long-term care. J. Econ. Perspect. 1992, 6, 43–58. [Google Scholar] [CrossRef]

- Brown, J.R.; Finkelstein, A. Why is the market for long-term care insurance so small? J. Public Econ. 2007, 91, 1967–1991. [Google Scholar] [CrossRef]

- Ko, A. An equilibrium analysis of the long-term care insurance market. Rev. Econ. Stud. 2022, 89, 1993–2025. [Google Scholar] [CrossRef]

- Kim, H.; Kwon, S. A decade of public long-term care insurance in South Korea: Policy lessons for aging countries. Health Policy 2021, 125, 22–26. [Google Scholar] [CrossRef]

- Tsutsui, T.; Muramatsu, N. Care-needs certification in the long-term care insurance system of Japan. J. Amer-Ican Geriatr. Soc. 2005, 53, 522–527. [Google Scholar] [CrossRef]

- Budnick, A.; Hering, C.; Eggert, S.; Teubner, C.; Suhr, R.; Kuhlmey, A.; Gellert, P. Informal caregivers during the COVID-19 pandemic perceive additional burden: Findings from an ad-hoc survey in Germany. BMC Health Serv. Res. 2021, 21, 353. [Google Scholar] [CrossRef] [PubMed]

- Kim, H.; Mitra, S. The Economic and Health Effects of Long-term Care Insurance: New Evidence from Korea. J. Econ. Ageing 2022, 23, 100412. [Google Scholar] [CrossRef]

- Aloisio, L.D.; Coughlin, M.; Squires, J.E. Individual and organizational factors of nurses’ job satisfaction in long-term care: A systematic review. Int. J. Nurs. Stud. 2021, 123, 104073. [Google Scholar] [CrossRef] [PubMed]

- Kwon, H.J.; Cho, Y.U.; Ko, J.Y. The effects of long-term care insurance on the life satisfaction and satisfaction in family relationships-The DD method combined with propensity score matching. Korean J. Soc. Welf. 2011, 63, 301–326. [Google Scholar]

- Feng, T.; Du, H.; Coffman, D.; Qu, A.; Dong, Z. Clean heating and heating poverty: A perspective based on cost-benefit analysis. Energy Policy 2021, 152, 112205–112238. [Google Scholar] [CrossRef]

- Lei, X.; Bai, C.; Hong, J.; Liu, H. Long-term care insurance and the well-being of older adults and their families: Evidence from China. Soc. Sci. Med. 2022, 296, 114745. [Google Scholar] [CrossRef]

- Andersen, R.M.; McCutcheon, A.; A Aday, L.; Chiu, G.Y.; Bell, R. Exploring dimensions of access to medical care. Health Serv. Res. 1983, 18, 49–74. [Google Scholar]

- Wade, D.; Collin, C. The Barthel ADL Index: A standard measure of physical disability? Int. Disabil. Stud. 1988, 10, 64–67. [Google Scholar] [CrossRef]

- Strauss, J.; Lei, X.; Park, A.; Shen, Y.; Smith, J.P.; Yang, Z.; Zhao, Y. Health outcomes and socio-economic status among the elderly in China: Evidence from the CHARLS Pilot. J. Popul. Ageing 2010, 3, 111–142. [Google Scholar] [CrossRef]

- Liu, H.; Hu, T. Evaluating the long-term care insurance policy from medical expenses and health security equity perspec-tive: Evidence from China. Arch. Public Health 2022, 80, 1–15. [Google Scholar] [CrossRef] [PubMed]

- D’Agostino, R.B., Jr. Propensity score methods for bias reduction in the comparison of a treatment to a non-randomized control group. Stat. Med. 1998, 17, 2265–2281. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Bio-Metr. 1983, 70, 41–55. [Google Scholar] [CrossRef]

- Yang, Y.; Zhang, Y. The Impact of the Green Credit Policy on the Short-Term and Long-Term Debt Financing of Heavily Polluting Enterprises: Based on PSM-DID Method. Int. J. Environ. Res. Public Health 2022, 19, 11287. [Google Scholar] [CrossRef] [PubMed]

- Shipman, J.E.; Swanquist, Q.T.; Whited, R.L. Propensity score matching in accounting research. Account. Rev. 2017, 92, 213–244. [Google Scholar] [CrossRef]

- Agarwal, S.; Qian, W. Consumption and debt response to unanticipated income shocks: Evidence from a natural experiment in Singapore. Am. Econ. Rev. 2014, 104, 4205–4230. [Google Scholar] [CrossRef]

- Roth, J. Pretest with caution: Event-study estimates after testing for parallel trends. Am. Econ. Rev. Insights 2022, 4, 305–322. [Google Scholar] [CrossRef]

- Deng, X.; Liao, J.; Peng, R.; Chen, J. The impact of long-term care insurance on medical utilization and expenditures: Evidence from Jingmen, China. Int. J. Environ. Res. Public Health 2022, 19, 12275. [Google Scholar] [CrossRef]

- Liu, Q.; Lu, Y. Firm investment and exporting: Evidence from China’s value-added tax reform. J. Int. Econ. 2015, 97, 392–403. [Google Scholar] [CrossRef]

- Yang, X.; Rice, R. An equilibrium model endogenizing the emergence of a dual structure between the urban and rural sec-tors. J. Urban Econ. 1994, 35, 346–368. [Google Scholar] [CrossRef]

- Olden, A.; Møen, J. The triple difference estimator. Econom. J. 2022, 25, 531–553. [Google Scholar] [CrossRef]

- Zhang, Y.; Goza, F.W. Who will care for the elderly in China?: A review of the problems caused by China’s one-child policy and their potential solutions. J. Aging Stud. 2006, 20, 151–164. [Google Scholar] [CrossRef]

- De la Maisonneuve, C.; Oliveira Martins, J. A Projection Method for Public Health and Long-Term Care Expenditures; OECD: Paris, France, 2013. [Google Scholar]

- Arai, Y. and S.H. Zarit, Exploring strategies to alleviate caregiver burden: Effects of the National Long-Term Care insurance scheme in Japan. Psychogeriatrics 2011, 11, 183–189. [Google Scholar] [CrossRef] [PubMed]

- Kumamoto, K.; Arai, Y.; Zarit, S.H. Use of home care services effectively reduces feelings of burden among family care-givers of disabled elderly in Japan: Preliminary results. Int. J. Geriatr. PsychiatryA J. Psychiatry Late Life Allied Sci. 2006, 21, 163–170. [Google Scholar] [CrossRef]

- Fu, R.; Noguchi, H.; Kawamura, A.; Takahashi, H.; Tamiya, N. Spillover effect of Japanese long-term care insurance as an employment promotion policy for family caregivers. J. Health Econ. 2017, 56, 103–112. [Google Scholar] [CrossRef]

- Van Houtven, C.H.; Coe, N.; Skira, M.M. The effect of informal care on work and wages. J. Health Econ. 2013, 32, 240–252. [Google Scholar] [CrossRef]

- Byrne, D.; Goeree, M.S.; Hiedemann, B.; Stern, S. Formal home health care, informal care, and family decision making. Int. Econ. Rev. 2009, 50, 1205–1242. [Google Scholar] [CrossRef]

- Rice, J.B.; Kasper, J.D.; Pezzin, L.E. A comparative analysis of Medicaid long-term care policies and their effects on elderly dual enrollees. Health Econ. 2009, 18, 275–290. [Google Scholar] [CrossRef]

- Schmitz, H.; Westphal, M. Short-and medium-term effects of informal care provision on female caregivers’ health. Jour-Nal Health Econ. 2015, 42, 174–185. [Google Scholar] [CrossRef]

- Feng, Z.; Glinskaya, E.; Chen, H.; Gong, S.; Qiu, Y.; Xu, J.; Yip, W. Long-term care system for older adults in China: Policy landscape, challenges, and future prospects. Lancet 2020, 396, 1362–1372. [Google Scholar] [CrossRef] [PubMed]

- Zhu, Y.; Österle, A. China’s policy experimentation on long-term care insurance: Implications for access. Int. J. Health Plan. Manag. 2019, 34, e1661–e1674. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Pilot City | Implementation Time | Coverage Objects |

|---|---|---|

| Chengde City Hebei province | November 2016 | Employee health insurance participants |

| Changchun City Jilin province | May 2015 | Medical insurance for employees and medical insurance for non-working urban residents |

| Qiqihar City Heilongjiang province | October 2017 | Employee health insurance participants |

| Shanghai City | January 2017 | Medical insurance for employees and medical insurance for urban and rural residents |

| Nantong City Jiangsu province | January 2016 | Medical insurance for employees and medical insurance for urban and rural residents |

| Suzhou City Jiangsu province | June 2017 | Medical insurance for employees and medical insurance for urban and rural residents |

| Ningbo City Zhejiang province | December 2017 | Employee health insurance participants |

| Anqing City Anhui province | January 2017 | Employee health insurance participants |

| Shangrao City Jiangxi province | January 2017 | Employee health insurance participants |

| Qindao City Shandong province | July 2012 | Medical insurance for employees and medical insurance for non-working urban residents |

| Jingmen City Hubei province | November 2016 | Medical insurance for employees and medical insurance for urban and rural residents |

| Guangzhou City Guangdong province | August 2017 | Employee health insurance participants |

| Chongqing City | December 2017 | Employee health insurance participants |

| Chengdu City Sichuan province | July 2017 | Employee health insurance participants |

| Shihezi City Xinjiang Production and Construction Corps | January 2017 | Medical insurance for employees and medical insurance for urban and rural residents |

| Variables | Definition |

|---|---|

| Explained variable | |

| Out-of-pocket medical expenses | Past year out-of-pocket medical expenses were logarithmized |

| Self-rated health | Poor = 1; fair = 2; good = 3; very good = 4; excellent = 5 |

| Main explanatory variables | |

| After | After 2016 = 1; others = 0 |

| Treat | Cities covered by long-term care insurance = 1; others = 0 |

| Control variable | |

| Age | Age of the elderly |

| Gender | Female= 1; male= 0 |

| Residence | Rural = 1; urban = 0 |

| Married | Living with a spouse = 1; others = 0 |

| Education | Uneducated = 0; primary school = 6; junior high school = 9; high school and technical secondary school = 12; junior college = 15; undergraduate = 16; Master’s degree or above = 19 |

| Chronic disease | Having a chronic disease = 1; others = 0 |

| Activities of daily living score | Scores range from 0 to 6, with higher scores indicating poorer health |

| Center for Epidemiological Studies-Depression score | Scores range from 0 to 30, with higher scores indicating a higher level of depression |

| Retirement | Formal retirement = 1; others = 0 |

| Child | Number of living children |

| Total income | Total household income was logarithmized |

| Pension | Have a pension = 1; others = 0 |

| Variables | Number | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|

| Out-of-pocket medical expenses | 35,215 | 4.5796 | 3.8288 | 0 | 14.6220 |

| Self-rated health | 35,215 | 3.0159 | 0.9463 | 1 | 5 |

| Age | 35,215 | 60.8659 | 8.8558 | 45 | 108 |

| Gender | 35,215 | 0.4715 | 0.4992 | 0 | 1 |

| Education | 35,215 | 4.7524 | 4.6087 | 0 | 19 |

| Marriage | 35,215 | 0.8372 | 0.3692 | 0 | 1 |

| Residence | 35,215 | 0.6448 | 0.4786 | 0 | 1 |

| Activities of daily living score | 35,215 | 0.3459 | 0.9232 | 0 | 6 |

| Child | 35,215 | 2.6535 | 1.2797 | 0 | 10 |

| Total income | 35,215 | 9.4615 | 2.2245 | 0 | 14.8589 |

| Retirement | 35,215 | 0.1346 | 0.3413 | 0 | 1 |

| Pension | 35,215 | 0.3434 | 0.4749 | 0 | 1 |

| Center for Epidemiological Studies-Depression score | 35,215 | 8.1108 | 6.1135 | 0 | 30 |

| Chronic disease | 35,215 | 0.7636 | 0.4249 | 0 | 1 |

| Variables | Unmatched | Mean | %Bias | %Reduct Bias | t-Test | ||

|---|---|---|---|---|---|---|---|

| Matched | Treated | Control | t | p > t | |||

| Age | U | 61.294 | 60.732 | 6.4 | 80.1 | 4.02 | 0.000 |

| M | 61.294 | 61.405 | −1.3 | −0.62 | 0.537 | ||

| Gender | U | 0.470 | 0.471 | −0.3 | −305.1 | −0.17 | 0.869 |

| M | 0.470 | 0.465 | 1.1 | 0.51 | 0.610 | ||

| Education | U | 4.673 | 4.750 | −1.7 | 94.4 | −1.06 | 0.291 |

| M | 4.673 | 4.669 | 0.1 | 0.04 | 0.965 | ||

| Marriage | U | 0.852 | 0.836 | 4.2 | 90.3 | 2.63 | 0.008 |

| M | 0.852 | 0.850 | 0.4 | 0.20 | 0.840 | ||

| Residence | U | 0.565 | 0.661 | −19.8 | 94.5 | −12.71 | 0.000 |

| M | 0.565 | 0.560 | 1.1 | 0.51 | 0.608 | ||

| ADL score | U | 0.298 | 0.348 | −5.5 | 88.7 | −3.43 | 0.001 |

| M | 0.298 | 0.304 | −0.6 | −0.31 | 0.754 | ||

| Child | U | 2.439 | 2.671 | −18.1 | 93.6 | −11.72 | 0.000 |

| M | 2.439 | 2.454 | −1.2 | −0.56 | 0.575 | ||

| Total income | U | 9.702 | 9.436 | 12.2 | 93.6 | 7.65 | 0.000 |

| M | 9.702 | 9.685 | 0.8 | 0.39 | 0.697 | ||

| Retirement | U | 0.186 | 0.121 | 18.2 | 95.1 | 12.30 | 0.000 |

| M | 0.186 | 0.189 | −0.9 | −0.40 | 0.692 | ||

| Pension | U | 0.355 | 0.342 | 2.8 | 71.7 | 1.77 | 0.077 |

| M | 0.355 | 0.359 | −0.8 | −0.38 | 0.706 | ||

| CESD score | U | 7.391 | 8.173 | −12.9 | 96.4 | −8.17 | 0.000 |

| M | 7.391 | 7.419 | −0.5 | −0.23 | 0.819 | ||

| Chronic diseases | U | 0.763 | 0.762 | 0.1 | −359.7 | 0.08 | 0.938 |

| M | 0.763 | 0.765 | −0.6 | −0.27 | 0.784 | ||

| Variables | Out-of-Pocket Medical Expenses | Self-Rated Health | ||

|---|---|---|---|---|

| Treat *After | −0.4031 *** (0.0007) | −0.3716 *** (0.0017) | 0.0660 ** (0.0128) | 0.0573 *** (0.0281) |

| Age | 0.0227 (0.8538) | −0.0444 (0.1007) | ||

| Marriage | −0.0102 (0.9169) | −0.0198 (0.3539) | ||

| ADL score | 0.2882 *** (0.0000) | −0.0883 *** (0.0000) | ||

| Child | 0.1545 *** (0.0024) | 0.0071 (0.5246) | ||

| Total income | 0.0265 ** (0.0114) | 0.0036 (0.1141) | ||

| Retirement | −0.1245 (0.3894) | 0.0417 (0.1900) | ||

| Pension | 0.0497 (0.3814) | 0.0137 (0.2713) | ||

| CESD score | 0.0614 *** (0.0000) | −0.0228 *** (0.0000) | ||

| Chronic diseases | 0.6881 *** (0.0000) | −0.1420 *** (0.0000) | ||

| Constant | 3.8997 *** (0.0000) | 0.9217 (0.8965) | 3.0004 *** (0.0000) | 5.8189 *** (0.0002) |

| Time fixed effect | YES | YES | YES | YES |

| Individual fixed effect | YES | YES | YES | YES |

| Number | 35215 | 35215 | 35215 | 35215 |

| R-squared | 0.0237 | 0.0395 | 0.0035 | 0.0375 |

| Variables | Out-of-Pocket Medical Expenses | Self-Rated Health | ||

|---|---|---|---|---|

| Treat *After | −0.4028 *** (0.0007) | −0.3713 *** (0.0017) | 0.0660 ** (0.0128) | 0.0573 ** (0.0280) |

| Age | 0.0247 (0.8400) | −0.0444 (0.1007) | ||

| Marriage | −0.0102 (0.9158) | −0.0198 (0.3543) | ||

| ADL score | 0.2856 *** (0.0000) | −0.0883 *** (0.0000) | ||

| Child | 0.1549 *** (0.0023) | 0.0071 (0.5250) | ||

| Total income | 0.0271 *** (0.0096) | 0.0037 (0.1056) | ||

| Retirement | −0.1229 (0.3940) | 0.0416 (0.1904) | ||

| Pension | 0.0505 (0.3720) | 0.0137 (0.2732) | ||

| CESD score | 0.0608 *** (0.0000) | −0.0228 *** (0.0000) | ||

| Chronic diseases | 0.6880 *** (0.0000) | −0.1420 *** (0.0000) | ||

| Constant | 3.8971 *** (0.0000) | 0.7982 (0.9100) | 3.0004 *** (0.0000) | 5.8182 *** (0.0002) |

| Time fixed effect | YES | YES | YES | YES |

| Individual fixed effect | YES | YES | YES | YES |

| Number | 35215 | 35215 | 35215 | 35215 |

| R-squared | 0.0236 | 0.0393 | 0.0035 | 0.0375 |

| Variables | Mahalanobis Distance Matching | Nearest Neighbor Matching | ||

|---|---|---|---|---|

| Out-of-Pocket Medical Expenses | Self-Rated Health | Out-of-Pocket Medical Expenses | Self-Rated Health | |

| Treat *After | −0.3716 *** (0.0017) | 0.0573 ** (0.0281) | −0.3716 *** (0.0017) | 0.0576 ** (0.0272) |

| Age | 0.0227 (0.8538) | −0.0444 (0.1007) | 0.0227 (0.8539) | −0.0436 (0.1074) |

| Marriage | −0.0102 (0.9169) | −0.0198 (0.3539) | −0.0102 (0.9169) | −0.0198 (0.3541) |

| ADL score | 0.2882 *** (0.0000) | −0.0883 *** (0.0000) | 0.2883 *** (0.0000) | −0.0884 *** (0.0000) |

| Child | 0.1545 *** (0.0024) | 0.0071 (0.5246) | 0.1545 *** (0.0024) | 0.0071 (0.5248) |

| Total income | 0.0265 ** (0.0114) | 0.0036 (0.1141) | 0.0265 ** (0.0114) | 0.0036 (0.1134) |

| Retirement | −0.1245 (0.3894) | 0.0417 (0.1900) | −0.1245 (0.3894) | 0.0416 (0.1904) |

| Pension | 0.0497 (0.3814) | 0.0137 (0.2713) | 0.0496 (0.3825) | 0.0137 (0.2715) |

| CESD score | 0.0614 *** (0.0000) | −0.0228 *** (0.0000) | 0.0614 *** (0.0000) | −0.0228 *** (0.0000) |

| Chronic diseases | 0.6881 *** (0.0000) | −0.1420 *** (0.0000) | 0.6881 *** (0.0000) | −0.1421 *** (0.0000) |

| Constant | 0.9217 (0.8965) | 5.8189 *** (0.0002) | 0.9221 (0.8965) | 5.7715 *** (0.0002) |

| Time fixed effect | YES | YES | YES | YES |

| Individual fixed effect | YES | YES | YES | YES |

| Number | 35215 | 35215 | 35213 | 35213 |

| R-squared | 0.0395 | 0.0375 | 0.0395 | 0.0375 |

| Variables | Out-of-Pocket Medical Expenses | Self-Rated Health | ||

|---|---|---|---|---|

| Urban | Rural | Urban | Rural | |

| Treat *After | −0.4091 *** (0.0027) | −0.2427 (0.3778) | 0.0550 * (0.0738) | 0.0430 (0.4230) |

| Age | −0.0731 (0.5951) | 0.4680 (0.1200) | −0.0416 (0.1803) | −0.0703 (0.2310) |

| Marriage | −0.0324 (0.7642) | −0.0378 (0.8870) | 0.0119 (0.6260) | −0.2023 *** (0.0001) |

| ADL score | 0.2915 *** (0.0000) | 0.1698 * (0.0609) | −0.0854 *** (0.0000) | −0.0843 *** (0.0000) |

| Child | 0.1606 *** (0.0047) | 0.2184 (0.1062) | 0.0056 (0.6613) | 0.0214 (0.4166) |

| Total income | 0.0290 ** (0.0118) | 0.0158 (0.6118) | 0.0047 * (0.0698) | 0.0048 (0.4289) |

| Retirement | −0.1668 (0.4755) | 0.0042 (0.9847) | 0.0461 (0.3825) | 0.0486 (0.2506) |

| Pension | 0.0363 (0.5799) | 0.2186 (0.1621) | 0.0125 (0.3981) | 0.0353 (0.2477) |

| CESD score | 0.0583 *** (0.0000) | 0.0781 *** (0.0000) | −0.0220 *** (0.0000) | −0.0300 *** (0.0000) |

| Chronic diseases | 0.6670 *** (0.0000) | 0.7580 *** (0.0008) | −0.1406 *** (0.0000) | −0.1260 *** (0.0041) |

| Constant | 6.3403 (0.4217) | −25.0523 (0.1563) | 5.5914 *** (0.0017) | 7.5903 ** (0.0277) |

| Time fixed effect | YES | YES | YES | YES |

| Individual fixed effect | YES | YES | YES | YES |

| Number | 27894 | 6320 | 27894 | 6320 |

| R-squared | 0.0414 | 0.0349 | 0.0359 | 0.0513 |

| Variables | Out-of-Pocket Medical Expenses | Self-Rated Health | ||

|---|---|---|---|---|

| Non-Disabled | Disabled | Non-Disabled | Disabled | |

| Treat *After * Dis | −0.4588 (0.2135) | −0.4002 *** (0.0031) | −0.0726 (0.4074) | 0.0685 ** (0.0191) |

| Age | 0.2978 (0.4255) | −0.0828 (0.5593) | −0.0520 (0.5582) | −0.0204 (0.5057) |

| Marriage | −0.3799 (0.2290) | 0.0592 (0.5976) | −0.0450 (0.5488) | −0.0234 (0.3346) |

| Child | 0.1971 (0.1977) | 0.1262 ** (0.0321) | −0.0380 (0.2955) | 0.0108 (0.3951) |

| Total income | 0.0279 (0.3775) | 0.0265 ** (0.0286) | 0.0047 (0.5284) | 0.0034 (0.1967) |

| Retirement | 1.2741 ** (0.0353) | −0.1856 (0.2389) | −0.0687 (0.6327) | 0.0366 (0.2830) |

| Pension | 0.1623 (0.3068) | 0.0408 (0.5428) | 0.0103 (0.7848) | 0.0201 (0.1656) |

| CESD score | 0.0500 *** (0.0000) | 0.0651 *** (0.0000) | −0.0213 *** (0.0000) | −0.0230 *** (0.0000) |

| Chronic diseases | 0.2945 (0.4229) | 0.6427 *** (0.0000) | 0.0456 (0.6013) | −0.1479 *** (0.0000) |

| Constant | −14.0457 (0.5370) | 6.8173 (0.3984) | 5.9572 (0.2704) | 4.4901 ** (0.0101) |

| Time fixed effect | YES | YES | YES | YES |

| Individual fixed effect | YES | YES | YES | YES |

| Number | 28959 | 6256 | 28959 | 6256 |

| R-squared | 0.0275 | 0.0324 | 0.0412 | 0.0245 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ma, G.; Xu, K. Value-Based Health Care: Long-Term Care Insurance for Out-of-Pocket Medical Expenses and Self-Rated Health. Int. J. Environ. Res. Public Health 2023, 20, 192. https://doi.org/10.3390/ijerph20010192

Ma G, Xu K. Value-Based Health Care: Long-Term Care Insurance for Out-of-Pocket Medical Expenses and Self-Rated Health. International Journal of Environmental Research and Public Health. 2023; 20(1):192. https://doi.org/10.3390/ijerph20010192

Chicago/Turabian StyleMa, Guangbo, and Kun Xu. 2023. "Value-Based Health Care: Long-Term Care Insurance for Out-of-Pocket Medical Expenses and Self-Rated Health" International Journal of Environmental Research and Public Health 20, no. 1: 192. https://doi.org/10.3390/ijerph20010192

APA StyleMa, G., & Xu, K. (2023). Value-Based Health Care: Long-Term Care Insurance for Out-of-Pocket Medical Expenses and Self-Rated Health. International Journal of Environmental Research and Public Health, 20(1), 192. https://doi.org/10.3390/ijerph20010192