On What Could Chinese Mining Enterprises Achieve High-Level Environmental Performance?—Based on the fsQCA Method

Abstract

:1. Introduction

2. Study Design

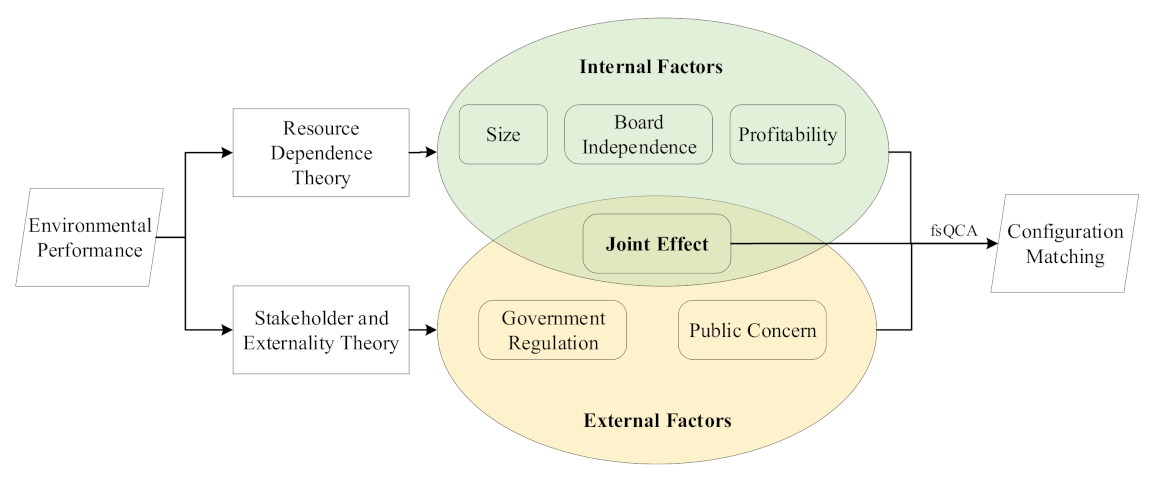

2.1. Theoretical Background

2.2. Methodology

2.3. Variable Design

2.4. Case Selection

2.5. Data Calibration

3. Results

3.1. Single-Factor Necessity Analysis

3.2. Multi-Factor Combination Analysis

3.3. Robustness Test

4. Discussion

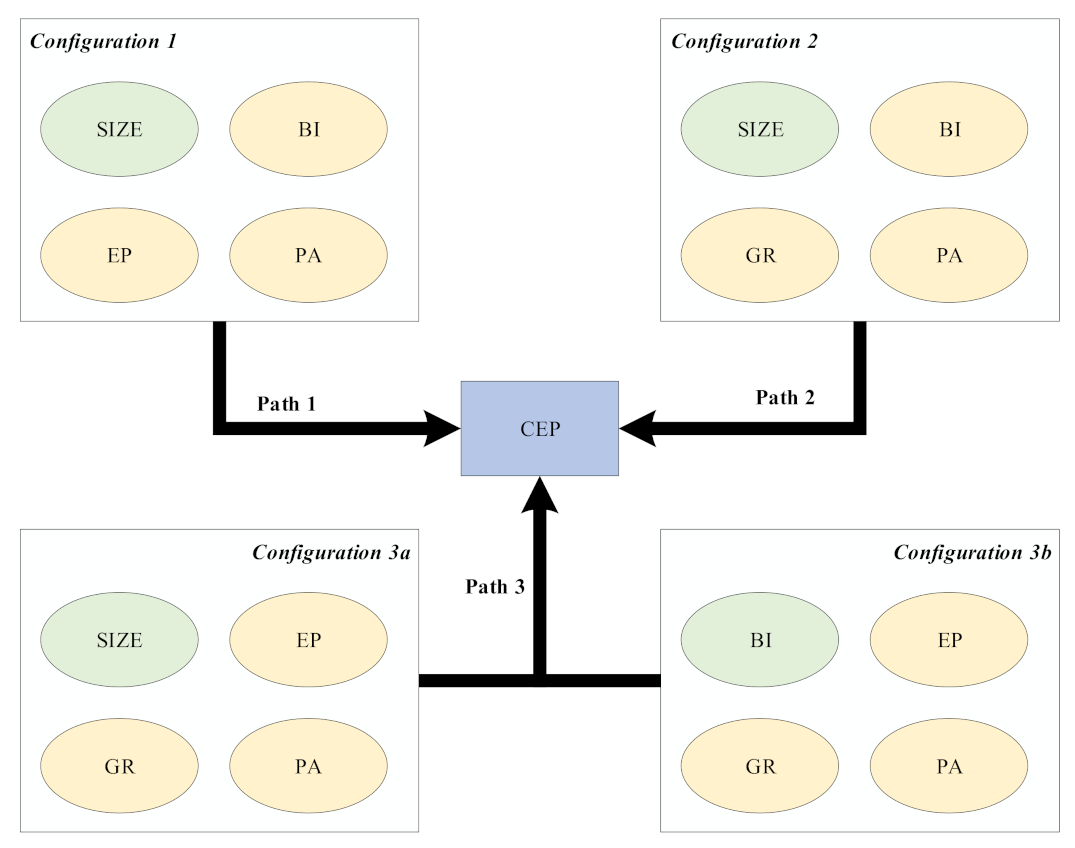

4.1. Three Paths for Mining Enterprises to Achieve High Environmental Performance

4.2. Relationship between Conditions

5. Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Li, H. A survey on environmental regulation’s influence on the optimization of industrial structure. China Min. 2020, 29, 21–25. [Google Scholar]

- Gao, W. Research on Green Mining Development under the Environmental Regulation in China. Ph.D. Thesis, China University of Geosciences, Beijing, China, 2018. [Google Scholar]

- Ma, F.; Guo, X.; Cha, N. The study on the impact of environmental regulation on technological innovation performance: Empirical test based on resource-based enterprises. Sci. Sci. Technol. Manag. 2011, 32, 87–92. [Google Scholar]

- Xepapadeas, A.; de Zeeuw, A. Environmental policy and competitiveness: The Porter hypothesis and the composition of capital. J. Environ. Econ. Manag. 1999, 37, 165–182. [Google Scholar] [CrossRef] [Green Version]

- Walley, N.; Whitehead, B. It’s not easy being green. Read. Bus. Environ. 1994, 36, 4. [Google Scholar]

- Palmer, K.; Oates, W.E.; Portney, P.R. Tightening environmental standards: The benefit-cost or the no-cost paradigm? J. Econ. Perspect. 1995, 9, 119–132. [Google Scholar] [CrossRef]

- Porter, M.E.; Linde, C.V.D. Green and competitive: Ending the stalemate. Harvard Business Review 1999, 28, 128–129. [Google Scholar]

- Schaltegger, S.; Figge, F. Environmental shareholder value: Economic success with corporate environmental management. Eco-Manag. Audit. J. Corp. Environ. Manag. 2000, 7, 29–42. [Google Scholar] [CrossRef]

- Jaggi, B.; Freedman, M. An examination of the impact of pollution performance on economic and market performance: Pulp and paper firms. J. Bus. Financ. Account. 1992, 19, 697–713. [Google Scholar] [CrossRef]

- Robaina, M.; Madaleno, M. The relationship between emissions reduction and financial performance: Are Portuguese companies in a sustainable development path? Corp. Soc. Responsib. Environ. Manag. 2020, 27, 1213–1226. [Google Scholar] [CrossRef]

- Lucato, W.C.; Costa, E.M.; de Oliveira Neto, G.C. The environmental performance of SMEs in the Brazilian textile industry and the relationship with their financial performance. J. Environ. Manag. 2017, 203, 550–556. [Google Scholar] [CrossRef]

- King, A.A.; Lenox, M.J. Does it really pay to be green? An empirical study of firm environmental and financial performance: An empirical study of firm environmental and financial performance. J. Ind. Ecol. 2001, 5, 105–116. [Google Scholar] [CrossRef] [Green Version]

- Bai, X. Research on the Relationship between Environmental Performace and Financial Performance of Coal Industry in China. Ph.D. Thesis, Beijing Jiaotong University, Beijing, China, 2019. [Google Scholar]

- Zhang, Y.; Wei, J.; Zhu, Y.; George-Ufot, G. Untangling the relationship between Corporate Environmental Performance and Corporate Financial Performance: The double-edged moderating effects of environmental uncertainty. J. Clean. Prod. 2020, 263, 121584. [Google Scholar] [CrossRef]

- Elsayed, K.; Paton, D. The impact of environmental performance on firm performance: Static and dynamic panel data evidence. Struct. Chang. Econ. Dyn. 2005, 16, 395–412. [Google Scholar] [CrossRef]

- De Beer, P.; Friend, F. Environmental accounting: A management tool for enhancing corporate environmental and economic performance. Ecol. Econ. 2006, 58, 548–560. [Google Scholar] [CrossRef] [Green Version]

- Yang, W. The dynamic environmetal performance of regional industry in China: an empirical analysis with DEA. J. Quant. Tech. Econ. 2009, 26, 87–98. [Google Scholar]

- Yamaguchi, K. Re-examination of stock price reaction to environmental performance: A GARCH application. Ecol. Econ. 2008, 68, 345–352. [Google Scholar] [CrossRef]

- Angelia, D.; Suryaningsih, R. The effect of environmental performance and corporate social responsibility disclosure towards financial performance (Case study to manufacture, infrastructure, and service companies that listed at Indonesia stock exchange). Procedia Soc. Behav. Sci. 2015, 211, 348–355. [Google Scholar] [CrossRef] [Green Version]

- Oeyono, J.; Samy, M.; Bampton, R. An examination of corporate social responsibility and financial performance. J. Glob. Responsib. 2011, 2, 100–112. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Yang, Y.; Liyu, X.; Shen, H. Green finacial policies, corporate governance and environmental disclosure: A case study of 502 listed firms in heavy polluiton industry. Financ. Trade Res. 2011, 5, 131–139. [Google Scholar]

- Liu, T.; Zhang, Y.; Liang, D. Can ownership structure improve environmental performance in Chinese manufacturing firms? The moderating effect of financial performance. J. Clean. Prod. 2019, 225, 58–71. [Google Scholar] [CrossRef] [Green Version]

- Nyborg, K.; Telle, K. Firms’ compliance to environmental regulation: Is there really a paradox? Environ. Resour. Econ. 2006, 35, 1–18. [Google Scholar] [CrossRef]

- Liu, B.; Yu, Q.; Bi, J.; Zhang, B. The driving force of improving corporate environmental performance baed on the stakeholder theory. China Popul. Resour. Environ. 2009, 19, 80–84. [Google Scholar]

- Li, W.; Chen, G. The relationship of external environment, green management and environmental performance. China Popul. Resour. Environ. 2010, 20, 84–88. [Google Scholar]

- Zeng, S.; Meng, X.; Zeng, R.; Tam, C.M.; Tam, V.W.; Jin, T. How environmental management driving forces affect environmental and economic performance of SMEs: A study in the Northern China district. J. Clean. Prod. 2011, 19, 1426–1437. [Google Scholar] [CrossRef]

- Xu, L.; Chen, L.; Zhang, S.; Liu, N. Tone at the top management, media attention and environmental performance. In East China Economic Management; Anhui College of Economics and Management: Hefei, China, 2018; Volume 32, pp. 114–123. [Google Scholar]

- He, L.; Hou, T. Determinants of Environmental Performance Information Disclosure in Chinese Listed Companies: Empirical Evidence Based on Social Responsibility Reports. China Popul. Resour. Environ. 2010, 8, 103–108. [Google Scholar]

- Lv, J.; Jiao, S. Empirical Study on the Relations among Environmental Disclosure, Environmental Performance and Financial Performance. J. Shanxi Univ. Financ. Econ. 2011, 1, 109–116. [Google Scholar]

- Villiers, C.D.; Naiker, V.; Staden, C. The Effect of Board Characteristics on Firm Environmental Performance. J. Manag. 2011, 37, 1636–1663. [Google Scholar] [CrossRef]

- Jin, J.; Du, J. Research on the Mechanism of Chinese FDI Enterprises’ Environmental Performance—Double Mediating Model of Different Environmental Behavior. Manag. Rev. 2021, 33, 68–79. [Google Scholar]

- Cui, Y.; Liu, X. Game analysis of the strategies of environmental pollution control among local governments in China. Theory Reform. 2009, 6, 62–65. [Google Scholar]

- Huang, Q. Game thinking and policy suggestions in environmental protection. Dev. Res. 2009, 1, 71–73. [Google Scholar]

- An, Z.; Ding, H.; Hou, H. Game analysis and Strategy Research on Stakeholders of environmental performance. Inq. Econ. Issues 2013, 3, 30–36. [Google Scholar]

- Xiong, Y. Analysis on the Influence of Government Environmental Regulation and Public Participation on Enterprises’ Pollution Behavior. Ph.D. Thesis, Nanjing Agricultural University, Nanjing, China, 2007. [Google Scholar]

- Wang, J.; Sun, R.; Pan, Y. Research on environmental performance influence mechanism and guiding policy of closed-loop supply chain. Ecol. Econ. 2020, 36, 175–181. [Google Scholar]

- Wang, C. Research on the Relationship between Economic Performance and Environmental Performance on the Firm Level. Ph.D. Thesis, Tianjin University of Technology, Tianjin, China, 2008. [Google Scholar]

- Zhang, M. The Research on the Influential Factors and Their Influence Mechanism of Iron and Steel Enterprise Green Production Behavior. Ph.D. Thesis, China University of Mining and Techology, Beijing, China, 2016. [Google Scholar]

- Du, Y.; Jia, L. Configurational perspective and quantitative comparative analysis (QCA)—A new path for management study. Manag. World 2017, 6, 155–167. [Google Scholar]

- Invernizzi, D.C.; Locatelli, G.; Brookes, N.; Davis, A. Qualitative comparative analysis as a method for project studies: The case of energy infrastructure. Renew. Sustain. Energy Rev. 2020, 133, 110314. [Google Scholar] [CrossRef]

- Pfeffer, J.; Salancik, G. External Control of Organizations—Resource Dependence Perspective; Routledge: London, UK, 2015. [Google Scholar]

- Friedman, A.L.; Miles, S. Developing stakeholder theory. J. Manag. Stud. 2002, 39, 1–21. [Google Scholar] [CrossRef]

- Shen, M.; Linqiao, H. The classification of externality and evolvement of externality theory. J. Zhejiang Univ. (Humanit. Soc. Sci.) 2002, 1, 152–160. [Google Scholar]

- Hillman, A.J.; Withers, M.C.; Collins, B.J. Resource dependence theory: A review. J. Manag. 2009, 35, 1404–1427. [Google Scholar] [CrossRef] [Green Version]

- Sharif, S.P.; Wei, K.K.; Phillip, S. Independent Directors’ Resource Provision Capability in Publicly-Listed Companies in Malaysia. Soc. Sci. Electron. Publ. 2016, 11, 113–121. [Google Scholar] [CrossRef]

- Phillips, R. Stakeholder Theory and Organizational Ethics; Berrett-Koehler Publishers: San Francisco, CA, USA, 2003. [Google Scholar]

- Freeman, R.E.; Harrison, J.S.; Wicks, A.C.; Parmar, B.L.; De Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: Cambridge, UK, 2010. [Google Scholar]

- Anderson, D.A. Environmental Exigencies and the Efficient Voter Rule. Economies 2020, 8, 100. [Google Scholar] [CrossRef]

- Du, B.; Zhang, P. Multi-concurrent causality and multi-paths of the policies for the transformation of scientific and technological achievements–QCA analysis based on the technology transfer polices in 22 regions in China. Sci. Sci. Manag. S T 2019, 40, 3–14. [Google Scholar]

- Cheng, C.; Zhong, H.; Guo, Y.; Li, G. Research on the driving pattern of firm’s online/off line innovation collaboration: Based on networking synergy and resource allocation. Stud. Sci. Sci. 2018, 36, 723–731. [Google Scholar]

- Rihoux, B.; Ragin, C.C. Configurational Comparative Methods: Qualitative Comparative Analysis (QCA) and Related Techniques; Sage Publications: Thousand Oaks, CA, USA, 2008; Volume 51. [Google Scholar]

- Fiss, P.C. Building Better Causal Theories: A Fuzzy Set Approach to Typologies in Organization Research. Acad. Manag. J. 2011, 54, 393–420. [Google Scholar] [CrossRef] [Green Version]

- Zhang, M.; Du, Y. Qualitative Competitive Analysis (QCA) in management and organization research: Position, tactics, and directions. Chin. J. Manag. 2019, 16, 1312–1323. [Google Scholar]

- Yong, T.; Park, C. A qualitative comparative analysis on factors affecting the deployment of electric vehicles. Energy Procedia 2017, 128, 497–503. [Google Scholar] [CrossRef]

- Kraus, S.; Ribeiro-Soriano, D.; Schüssler, M. Fuzzy-set qualitative comparative analysis (fsQCA) in entrepreneurship and innovation research—The rise of a method. Int. Entrep. Manag. J. 2018, 14, 15–33. [Google Scholar] [CrossRef]

- Schneider, C.Q.; Wagemann, C. Set-Theoretic Methods for the Social Sciences: A Guide to Qualitative Comparative Analysis; Cambridge University Press: Cambridge, UK, 2012. [Google Scholar]

- De Villiers, R. QCA in empirical marketing research: An experiment featuring Dorah Explorah, investigating celebrity endorsement’s effect on product selection. Australas. Mark. J. 2017, 25, 225–250. [Google Scholar] [CrossRef]

- Zhang, H.; Fan, Y.; Li, X. Research on corporate social responsibility investment strategy based on the application of fuzzy qualitative comparative analysis. Chin. J. Manag. 2018, 15, 1047–1055. [Google Scholar]

- Ragin, C.C. The Comparative Method: Moving beyond Qualitative and Quantitative Strategies; University of California Press: Berkeley, CA, USA, 2014. [Google Scholar]

- Ragin, C.C. Fuzzy sets: Calibration versus measurement. Methodol. Vol. Oxf. Handb. Political Sci. 2007, 2, 1–31. [Google Scholar]

- Pappas, I.O.; Kourouthanassis, P.E.; Giannakos, M.N.; Chrissikopoulos, V. Explaining online shopping behavior with fsQCA: The role of cognitive and affective perceptions. J. Bus. Res. 2016, 69, 794–803. [Google Scholar] [CrossRef]

- Zhang, H.; Zhou, Y.; Yin, H. A study of ESG green rating and green index. Financ. Forum 2017, 22, 3–14. [Google Scholar]

- Zhang, l.; Zhao, H. Does corporate environmental, social and corporate governance (ESG) performance affect corporate value?—Based on Empirical Research of A-Share Listed Companies. Wuhan Financ. 2019, 10, 36–43. [Google Scholar]

- Shi, Q. Qualitative Comparative Analysis in Time:The Development of TQCA and TSQCA. Comp. Politics Stud. 2016, 10, 40–58. [Google Scholar]

- Zhao, W.; Wang, N. Research on Performance Improvement Path of Chinese Returnees Enterprises Considering Ambidextrous Network:The Fuzzy-Set Qualitative Comparative Analysis. Sci. Sci. Manag. S T 2017, 38, 128–139. [Google Scholar]

- Yu, X.; Liu, G.; Liang, H. Kinship combinations and efficient governance patterns in family business: A qualitative comparative analysis of Chinese listed family firms. China Soft Sci. 2018, 38, 153–165. [Google Scholar]

- Shen, J.; Li, S.; Zhang, J. Research on influencing factors of big data industry development capability: Based on fsQCA. Sci. Technol. Manag. Res. 2019, 39, 140–147. [Google Scholar]

- Yan, J.; Wang, M. Rsearch on the path of high-level corporate social responsibility information disclosur under the coordination of stakeholders: A study based on the fsQCA mehtod. J. Dongguang Univ. Technol. 2020, 27, 74–81. [Google Scholar]

- Zhou, J.; Wang, M. How internet buzzwords spread in China: Crisp-set Qualitative Competitive Analysis (csQCA) of 12 public events. J. Commun. 2016, 38, 26–46. [Google Scholar]

- Mikalef, P.; Pateli, A.; van de Wetering, R. IT architecture flexibility and IT governance decentralisation as drivers of IT-enabled dynamic capabilities and competitive performance: The moderating effect of the external environment. Eur. J. Inf. Syst. 2020, 1–29. [Google Scholar] [CrossRef]

- Ordanini, A.; Parasuraman, A.; Rubera, G. When the recipe is more important than the ingredients: A qualitative comparative analysis (QCA) of service innovation configurations. J. Serv. Res. 2014, 17, 134–149. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Variable | Full-Membership Threshold | Crossover Point | Non-Membership Threshold |

|---|---|---|---|

| SIZE | 25.994 | 23.430 | 20.982 |

| BI | 0.430 | 0.355 | 0.333 |

| EP | 0.180 | 0.066 | 0.015 |

| GR | 70 | 60 | 40 |

| PA | 1000 | 600 | 314.867 |

| CEP | 8 | 6.9 | 4 |

| Condition Variables | High CEP | |

|---|---|---|

| Consistency | Coverage | |

| SIZE | 0.729 | 0.775 |

| ∼SIZE | 0.487 | 0.542 |

| BI | 0.569 | 0.716 |

| ∼ BI | 0.623 | 0.595 |

| GR | 0.562 | 0.737 |

| ∼GR | 0.576 | 0.534 |

| EP | 0.566 | 0.672 |

| ∼EP | 0.654 | 0.655 |

| PA | 0.721 | 0.711 |

| ∼PA | 0.442 | 0.535 |

| Configuration | Solution | |||

|---|---|---|---|---|

| 1 | 2 | 3a | 3b | |

| SIZE | • | • | • | |

| BI | ● | ● | • | |

| EP | ● | ● | ● | |

| GR | ● | ● | ● | |

| PA | ● | ● | ● | ● |

| consistency | 0.914 | 0.927 | 0.913 | 0.957 |

| raw coverage | 0.290 | 0.269 | 0.247 | 0.210 |

| unique coverage | 0.091 | 0.070 | 0.049 | 0.012 |

| overall solution consistency | 0.885 | |||

| overall solution coverage | 0.421 | |||

| Configuration | Solution | |||

|---|---|---|---|---|

| 1 | 2 | 3a | 3b | |

| SIZE | • | • | • | |

| BI | ● | ● | • | |

| EP | ● | ● | ● | |

| GR | ● | ● | ● | |

| PA | ● | ● | ● | ● |

| consistency | 0.945 | 0.942 | 0.951 | 0.976 |

| raw coverage | 0.295 | 0.269 | 0.254 | 0.211 |

| unique coverage | 0.096 | 0.069 | 0.054 | 0.011 |

| overall solution consistency | 0.913 | |||

| overall solution coverage | 0.430 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gao, Z.; He, D.; Niu, S. On What Could Chinese Mining Enterprises Achieve High-Level Environmental Performance?—Based on the fsQCA Method. Int. J. Environ. Res. Public Health 2021, 18, 7290. https://doi.org/10.3390/ijerph18147290

Gao Z, He D, Niu S. On What Could Chinese Mining Enterprises Achieve High-Level Environmental Performance?—Based on the fsQCA Method. International Journal of Environmental Research and Public Health. 2021; 18(14):7290. https://doi.org/10.3390/ijerph18147290

Chicago/Turabian StyleGao, Zhengjie, Dayi He, and Shuaifang Niu. 2021. "On What Could Chinese Mining Enterprises Achieve High-Level Environmental Performance?—Based on the fsQCA Method" International Journal of Environmental Research and Public Health 18, no. 14: 7290. https://doi.org/10.3390/ijerph18147290

APA StyleGao, Z., He, D., & Niu, S. (2021). On What Could Chinese Mining Enterprises Achieve High-Level Environmental Performance?—Based on the fsQCA Method. International Journal of Environmental Research and Public Health, 18(14), 7290. https://doi.org/10.3390/ijerph18147290