Prevalence, Use Behaviors, and Preferences among Users of Heated Tobacco Products: Findings from the 2018 ITC Japan Survey

,

,  ,

,  and

and

Abstract

1. Introduction

2. Materials and Methods

2.1. Data Source

2.2. Measures

2.2.1. Sociodemographic Variables

2.2.2. Patterns of HTP Use and Cigarette Smoking

2.2.3. HTP Device Brand Preferences

2.2.4. HTP Flavor Preferences

2.3. Statistical Analysis

3. Results

3.1. Prevalence of HTP Use and User Characteristics

3.2. Patterns of HTP Use and Cigarette Smoking

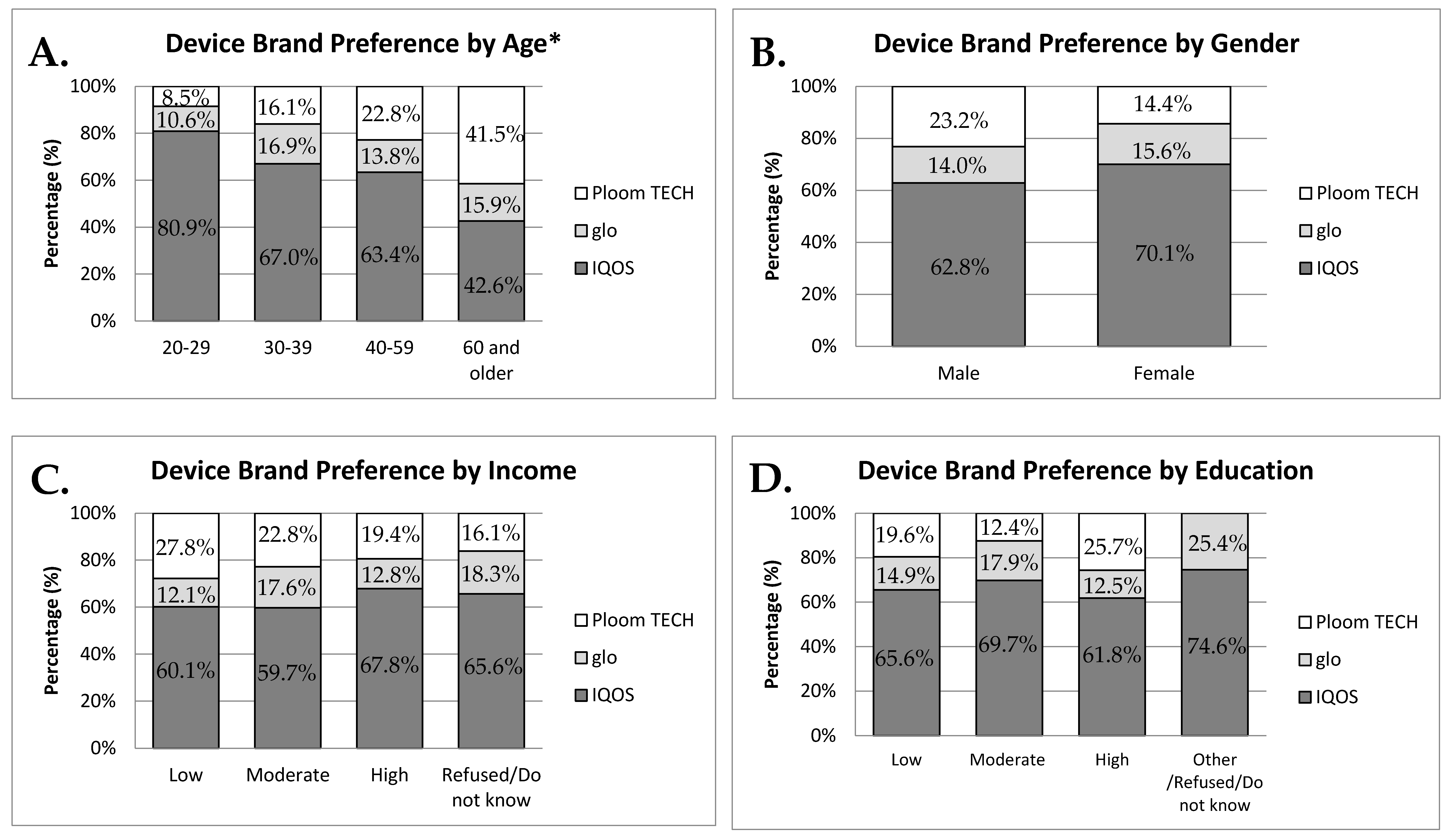

3.3. Device Brand Preference

3.4. Flavor Preference

4. Discussion

4.1. Prevalence and Pattern of HTP Use

4.2. Device Brand Preference

4.3. Flavor Preference

4.4. Study Limitations

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A. Survey Weighting for “Less than Weekly, but at Least Once a Month” HTP Users

Appendix B

{kind=link}

| No | Product Name | Device Brand | Flavor Category |

|---|---|---|---|

| 1 | Marlboro Heatstick Balanced | IQOS | Tobacco |

| 2 | Marlboro Heatstick Menthol | IQOS | Menthol |

| 3 | Marlboro Heatstick Mint | IQOS | Menthol |

| 4 | Marlboro Heatstick Purple Menthol | IQOS | Mentholated fruity |

| 5 | Marlboro Heatstick Regular | IQOS | Tobacco |

| 6 | Marlboro Heatstick Smooth | IQOS | Tobacco |

| 7 | Kent Neostick Bright Tobacco | glo | Tobacco |

| 8 | Kent Neostick Citrus Fresh * | glo | Mentholated fruity |

| 9 | Kent Neostick Dark Fresh * | glo | Mentholated fruity |

| 10 | Kent Neostick Fresh Mix | glo | Menthol |

| 11 | Kent Neostick Intense Fresh | glo | Menthol |

| 12 | Kent Neostick Refreshing Menthol | glo | Menthol |

| 13 | Kent Neostick Regular | glo | Tobacco |

| 14 | Kent Neostick Rich Tobacco * | glo | Tobacco |

| 15 | Kent Neostick Smooth Fresh | glo | Menthol |

| 16 | Kent Neostick Spark Fresh * | glo | Mentholated fruity |

| 17 | Kent Neostick Strong Menthol | glo | Menthol |

| 18 | Mevius for Ploom TECH Brown Aroma | Ploom TECH | Coffee |

| 19 | Mevius for Ploom TECH Cooler Green | Ploom TECH | Mentholated fruity |

| 20 | Mevius for Ploom TECH Cooler Purple | Ploom TECH | Mentholated fruity |

| 21 | Mevius for Ploom TECH Red Cooler | Ploom TECH | Mentholated fruity |

| 22 | Mevius for Ploom TECH Regular | Ploom TECH | Tobacco |

References

- Brose, L.S.; Simonavicius, E.; Cheeseman, H. Awareness and Use of “Heat-not-burn” Tobacco Products in Great Britain. Tob. Regul. Sci. 2018, 4, 44–50. [Google Scholar] [CrossRef]

- Simonavicius, E.; Mcneill, A.; Shahab, L.; Brose, L.S. Heat-not-burn tobacco products: A systematic literature review. Tob. Control 2019, 28, 582–594. [Google Scholar] [CrossRef] [PubMed]

- World Health Organization. Heated tobacco products (HTPs) market monitoring information sheet. 2018. Available online: http://www.who.int/tobacco/publications/prod_regulation/heated-tobacco-products/en/ (accessed on 24 October 2019).

- Bialous, S.A.; Glantz, S.A. Heated tobacco products: Another tobacco industry global strategy to slow progress in tobacco control. Tob. Control 2018, 27, s111–s117. [Google Scholar] [CrossRef] [PubMed]

- Tabuchi, T.; Kiyohara, K.; Hoshino, T.; Bekki, K.; Inaba, Y.; Kunugita, N. Awareness and use of electronic cigarettes and heat-not-burn tobacco products in Japan. Addiction 2016, 111, 706–713. [Google Scholar] [CrossRef] [PubMed]

- Kim, J.; Yu, H.; Lee, S.; Paek, Y.J. Awareness, experience and prevalence of heated tobacco product, IQOS, among young Korean adults. Tob. Control 2018, 27, s74–s77. [Google Scholar] [CrossRef]

- Liu, X.; Lugo, A.; Spizzichino, L.; Tabuchi, T.; Pacifici, R.; Gallus, S. Heat-not-burn tobacco products: Concerns from the Italian experience. Tob. Control 2019, 28, 113–114. [Google Scholar] [CrossRef]

- Nyman, A.L.; Weaver, S.R.; Popova, L.; Pechacek, T.F.; Huang, J.; Ashley, D.L.; Eriksen, M.P. Awareness and use of heated tobacco products among US adults, 2016–2017. Tob. Control 2018, 27, s55–s61. [Google Scholar] [CrossRef]

- Marynak, K.L.; Wang, T.W.; King, B.A.; Agaku, I.T.; Reimels, E.A.; Graffunder, C.M. Awareness and Ever Use of “Heat-Not-Burn” Tobacco Products Among U.S. Adults, 2017. Am. J. Prev. Med. 2018, 55, 551–554. [Google Scholar] [CrossRef]

- Tsugawa, Y.; Hashimoto, K.; Tabuchi, T.; Shibuya, K. What can Japan learn from tobacco control in the UK? Lancet 2017, 390, 933–934. [Google Scholar] [CrossRef]

- Tabuchi, T.; Gallus, S.; Shinozaki, T.; Nakaya, T.; Kunugita, N.; Colwell, B. Heat-not-burn tobacco product use in Japan: Its prevalence, predictors and perceived symptoms from exposure to secondhand heat-not-burn tobacco aerosol. Tob. Control 2017, 27, e25–e33. [Google Scholar] [CrossRef]

- Uranaka, T.; Ando, R. Philip Morris Aims to Revive Japan Sales with Cheaper Heat-Not-Burn Tobacco. Reuters. Tokyo. 2018. Available online: https://www.reuters.com/article/us-pmi-japan/philip-morris-aims-to-revive-japan-sales-with-cheaper-heat-not-burn-tobacco-idUSKCN1MX06E (accessed on 29 August 2019).

- Uranaka, T.; Shimizu, R. Japan Tobacco to cut heated tobacco prices in battle with Philip Morris. Reuters. Tokyo. 2018. Available online: https://www.reuters.com/article/us-japan-tobacco/japan-tobacco-to-cut-heated-tobacco-prices-in-battle-with-philip-morris-idUSKCN1IW0XH (accessed on 12 November 2019).

- Kumamaru, H. Update of Current Status in Japan on Tobacco Harm Reduction. 2019. Available online: https://gfn.net.co/downloads/2019/presentations/Hiroya_Kumamaru.pdf (accessed on 12 November 2019).

- Uranaka, T.; Geller, M. British American Tobacco to test tobacco e-cigarette in Japan. Reuters. Tokyo. 2016. Available online: https://www.reuters.com/article/us-brit-am-tobacco-ecigarettes-idUSKBN1330AG (accessed on 12 November 2019).

- Japan Tobacco Inc. JT Applies to Amend Retail Prices of Tobacco Products in Japan in Response to a Planned Excise Increase. 2018. Available online: https://www.jt.com/media/news/2018/pdf/20180814_E01.pdf (accessed on 12 November 2019).

- Sternbach, N.; Annunziata, K.; Fukuda, T.; Yirong, C.; Stankus, A. Smoking Trends in Japan From 2008–2017: Results From The National Health and Wellness Survey. Value Heal. 2018, 21, S105. [Google Scholar] [CrossRef]

- Assunta, M.; Chapman, S. A “clean cigarette” for a clean nation: A case study of Salem Pianissimo in Japan. Tob. Control 2004, 13 (Suppl. 2), 58–62. [Google Scholar] [CrossRef] [PubMed]

- McKelvey, K.; Popova, L.; Kim, M.; Chaffee, B.W.; Vijayaraghavan, M.; Ling, P.; Halpern-Felsher, B. Heated tobacco products likely appeal to adolescents and young adults. Tob. Control 2018, 27, s41–s47. [Google Scholar] [CrossRef] [PubMed]

- Hair, E.C.; Bennett, M.; Sheen, E.; Cantrell, J.; Briggs, J.; Fenn, Z.; Vallone, D. Examining perceptions about IQOS heated tobacco product: Consumer studies in Japan and Switzerland. Tob. Control 2018, 27, s70–s73. [Google Scholar] [CrossRef] [PubMed]

- Pollay, R.W. Targeting youth and concerned smokers: Evidence from Canadian tobacco industry documents. Tob. Control 2000, 9, 136–147. [Google Scholar] [CrossRef]

- Wakefield, M.; Morley, C.; Horan, J.K.; Cummings, K.M. The cigarette pack as image: New evidence from tobacco industry documents. Tob. Control 2002, 11 (Suppl. 1), 73–80. [Google Scholar] [CrossRef]

- Carpenter, C.M.; Wayne, G.F.; Pauly, J.L.; Koh, H.K.; Connolly, G.N. New cigarette brands with flavors that appeal to youth: Tobacco marketing strategies. Health Aff. 2005, 24, 1601–1610. [Google Scholar] [CrossRef]

- Hafez, N.; Ling, P.M. Finding the Kool Mixx: How Brown and Williamson used music marketing to sell cigarettes. Tob. Control 2006, 15, 359–366. [Google Scholar] [CrossRef]

- Cruz, T.B.; Wright, L.T.; Crawford, G. The menthol marketing mix: Targeted promotions for focus communities in the United States. Nicotine Tob. Res. 2010, 12 (Suppl. 2), 147–153. [Google Scholar] [CrossRef] [PubMed]

- Ministry of Health, Labour and Welfare. Report on National Health and Nutritional Survey, Japan 2016. Ministry of Health, Labour and Welfare; 2018. Available online: http://www.mhlw.go.jp/bunya/kenkou/eiyou/h28-houkou.html (accessed on 8 September 2019).

- Japan Tobacco Inc. JT’s Annual Survey Finds 21.1 Percent of Japanese Adults Are Smokers. 2018. Available online: https://www.jt.com/investors/media/press_releases/2012/0730_01.html (accessed on 1 September 2019).

- Berry, K.M.; Fetterman, J.L.; Benjamin, E.J.; Bhatnagar, A.; Barrington-Trimis, J.L.; Leventhal, A.M.; Stokes, A. Association of Electronic Cigarette Use With Subsequent Initiation of Tobacco Cigarettes in US Youths. JAMA Netw. Open 2019, 2, e187794. [Google Scholar] [CrossRef] [PubMed]

- Soneji, S.; Barrington-Trimis, J.L.; Wills, T.A.; Leventhal, A.M.; Unger, J.B.; Gibson, L.A.; Spindle, T.R. Association Between Initial Use of e-Cigarettes and Subsequent Cigarette Smoking Among Adolescents and Young Adults: A Systematic Review and Meta-analysis. JAMA Pediatr. 2017, 171, 788–797. [Google Scholar] [CrossRef] [PubMed]

- Hwang, J.H.; Ryu, D.H.; Park, S. Heated tobacco products: Cigarette complements, not substitutes. Drug Alcohol Depend. 2019, 204, 107576. [Google Scholar] [CrossRef] [PubMed]

- Roulet, S.; Chrea, C.; Kanitscheider, C.; Kallischnigg, G.; Magnani, P.; Weitkunat, R. Potential predictors of adoption of the Tobacco Heating System by U.S. adult smokers: An actual use study. F1000Res. 2019, 8, 214. [Google Scholar] [CrossRef] [PubMed]

- Dyer, O. E-cigarette makers under fire for marketing to young people. BMJ 2019, 365, 2261. [Google Scholar] [CrossRef] [PubMed]

- St Helen, G.; Jacob, P.; Nardone, N.; Benowitz, N.L. IQOS: Examination of Philip Morris International’s claim of reduced exposure. Tob. Control 2018, 27 (Suppl. 1), s30–s36. [Google Scholar] [CrossRef] [PubMed]

- Mallock, N.; Pieper, E.; Hutzler, C.; Henkler-Stephani, F.; Luch, A. Heated Tobacco Products: A Review of Current Knowledge and Initial Assessments. Front Public Health 2019, 7, 287. [Google Scholar] [CrossRef]

- Freedman, K.S.; Nelson, N.M.; Feldman, L.L. Smoking initiation among young adults in the United States and Canada, 1998–2010: A systematic review. Prev. Chronic Dis. 2012, 9, E05. [Google Scholar] [CrossRef]

- Connolly, G.N.; Behm, I.; Osaki, Y.; Wayne, G.F. The impact of menthol cigarettes on smoking initiation among non-smoking young females in Japan. Int. J. Environ. Res. Public Health 2011, 8, 1–14. [Google Scholar] [CrossRef]

- WHO Study Group on Tobacco Product Regulation (TobReg). Banning Menthol in Tobacco Products. World Health Organization. 2016. Available online: https://apps.who.int/iris/bitstream/handle/10665/205928/9789241510332_eng.pdf (accessed on 12 September 2019).

- Lee, Y.O.; Glantz, S.A. Menthol: Putting the pieces together. Tob. Control 2011, 20 (Suppl. 2), 1–7. [Google Scholar] [CrossRef]

- Villanti, A.C.; Collins, L.K.; Niaura, R.S.; Gagosian, S.Y.; Abrams, D.B. Menthol cigarettes and the public health standard: A systematic review. BMC Public Health 2017, 17, 1–13. [Google Scholar] [CrossRef]

- Ahijevych, K.; Garrett, B.E. The role of menthol in cigarettes as a reinforcer of smoking behavior. Nicotine Tob. Res. 2010, 12 (Suppl. 2), 110–116. [Google Scholar] [CrossRef] [PubMed]

| IQOS | Glo | Ploom TECH | |

|---|---|---|---|

| Device picture |  |  |  |

| Manufacturer | Philip Morris International (PMI) | British American Tobacco (BAT) | Japan Tobacco International (JTI) |

| First launched | November 2014 | December 2016 | March 2016 |

| Type of tobacco inserts | Stick | Stick | Capsule |

| Device generations | 1st: IQOS 2nd: IQOS 2.4 3rd: IQOS 3 and IQOS 3 Multi | 1st: glo 2nd: glo Series 2 and glo Series 2 Mini | 1st: Ploom TECH 2nd: Ploom TECH+ and Ploom S * |

| Brand name of inserts | Marlboro Heatsticks | Kent Neostick | Mevius for Ploom TECH |

| Flavor variety of inserts | Balanced, Menthol, Mint, Purple Menthol, Regular, Smooth | Bright Tobacco, Citrus Fresh, Dark Fresh, Fresh Mix, Intense Fresh, Refreshing Menthol, Regular, Rich Tobacco, Smooth Fresh, Spark Fresh, Strong Menthol | Brown Aroma, Cooler Green, Cooler Purple, Red Cooler, Regular |

| Price † | IQOS 2.4: ¥7980 [13] IQOS 3 Multi: ¥8980 [14] Marlboro Heatsticks: ¥500 [12] | glo: ¥2980 [13] glo Series 2: ¥2980 [14] glo Series 2 Mini: ¥3980 [14] Kent Neostick: ¥420 [15] | Ploom TECH: ¥2980 [14] Ploom TECH+: ¥4980 [14] Ploom S: ¥7980 [14] Mevius for Ploom TECH: ¥490 [16] |

| Variable | Category | Current HTP User (n = 859) | Exclusive HTP User (n = 170) | HTP User by Smoking Status * | ||

|---|---|---|---|---|---|---|

| Current Smokers (n = 689) | Former Smokers (n = 115) | Never Smokers (n = 7) | ||||

| Weighted % (95% Confidence Interval) | ||||||

| Prevalence | 2.7 (2.4–3.0) | 0.9 (0.7–1.1) | 1.8 (1.6–2.1) | 0.7 (0.5–0.9) | 0.02 (0.01–0.06) | |

| Demographics | ||||||

| Gender | Male | 76.0 (72.0–79.7) | 71.8 (63.5–78.8) | 78.1 (73.3–82.2) | 72.8 (62.9–80.8) | 62.7 (23.0–90.4) |

| Female | 24.0 (20.3–28.0) | 28.2 (21.2–36.4) | 21.9 (17.8–26.7) | 27.2 (19.1–37.1) | 37.3 (9.5–77.0) | |

| F(1.93, 1551.85) = 0.91; p = 0.400 † | ||||||

| Age (years) | 20–29 | 16.6 (13.2–20.7) | 12.9 (7.1–22.3) | 18.4 (14.5–22.9) | 14.8 (7.7–26.6) | - |

| 30–39 | 26.1 (22.6–29.8) | 22.6 (16.2–30.5) | 27.7 (23.8–32.0) | 21.8 (14.4–31.4) | 47.6 (15.6–81.7) | |

| 40–59 | 44.0 (39.7–48.3) | 55.7 (46.4–64.6) | 38.4 (34.0–43.0) | 54.4 (43.3–65.2) | 52.4 (18.3–84.4) | |

| 60 and older | 13.3 (10.6–16.7) | 8.8 (4.7–15.8) | 15.5 (12.2–19.5) | 9.0 (4.3–17.9) | - | |

| F(5.23, 4200.06) = 1.72; p = 0.122 | ||||||

| Annual Household Income | Low | 15.8 (13.0–19.0) | 14.3 (9.3–21.3) | 16.5 (13.4–20.1) | 14.9 (8.9–23.7) | 11.9 (1.6–53.5) |

| Moderate | 22.6 (18.2–26.3) | 19.3 (13.2–27.2) | 24.1 (20.3–28.4) | 19.6 (12.5–29.4) | 10.3 (1.3–49.5) | |

| High | 51.0 (46.6–55.3) | 60.6 (51.6–68.9) | 46.5 (41.8–51.2) | 61.3 (50.4–71.1) | 60.4 (24.0–88.0) | |

| Refused/Do not know | 10.6 (7.9–14.1) | 5.8 (3.1–10.6) | 12.9 (9.4–17.6) | 4.2 (1.8–9.8) | 17.3 (2.4–64.1) | |

| F(5.42, 4351.58) = 2.18; p = 0.048 | ||||||

| Education | Low | 25.9 (22.6–29.5) | 24.6 (18.3–32.2) | 26.5 (22.9–30.5) | 21.9 (15.1–30.8) | - |

| Moderate | 21.4 (17.8–25.3) | 22.1 (16.3–29.1) | 21.0 (16.7–26.0) | 18.7 (12.6–26.7) | 65.0 (28.2–89.7) | |

| High | 51.9 (47.6–56.3) | 52.9 (43.9–61.7) | 51.5 (46.7–56.2) | 58.9 (48.3–68.6) | 35.0 (10.2–71.8) | |

| Other/Refused/Do not know | 0.8 (0.4–1.7) | 0.4 (0.1–2.9) | 1.0 (0.4–2.3) | 0.5 (0.1–3.8) | - | |

| F(5.53, 4439.27) = 1.63; p = 0.140 | ||||||

| Product Use Pattern | ||||||

| Frequency of HTP Use | Daily | 63.4 (58.9–67.6) | 88.3 (80.5–93.2) | 51.5 (46.7–56.3) | 86.9 (77.2–92.9) | 100.0 |

| Weekly | 16.1 (13.5–19.1) | 9.9 (5.7–16.7) | 19.1 (16.1–22.5) | 10.8 (5.8–19.3) | - | |

| Monthly | 20.5 (16.7–24.9) | 1.8 (0.2–11.6) | 29.4 (24.4–34.9) | 2.3 (0.3–14.6) | - | |

| F(3.03, 2432.26) = 9.56; p < 0.001 | ||||||

| Time to first HTP use | 5 min or less | 15.4 (12.8–18.5) | 17.5 (12.0–24.8) | 14.4 (11.7–17.6) | 15.1 (9.1–23.9) | 42.0 (13.0–77.8) |

| 6–30 min | 33.8 (29.7–38.1) | 40.9 (32.2–50.1) | 30.4 (62.0–35.1) | 42.6 (32.1–53.7) | 25.4 (3.9–74.1) | |

| 31–60 min | 15.5 (12.5–19.0) | 18.9 (12.5–27.6) | 13.9 (11.0–17.3) | 19.8 (12.2–30.5) | 10.4 (1.3–49.5) | |

| More than 60 min | 32.8 (28.9–37.1) | 20.9 (14.2–29.6) | 38.5 (33.9–43.3) | 20.2 (12.5–31.1) | 22.2 (5.1–60.4) | |

| Refused/Do not know | 2.5 (1.3–4.6) | 1.8 (0.2–11.6) | 2.8 (1.6–5.0) | 2.3 (0.3–14.6) | - | |

| F(6.27, 5038.00) = 1.91; p = 0.071 | ||||||

| Tobacco-containing inserts per day ‡ | 10.0 (2.8–15.0) | 10.0 (5.0–18.0) | 7 (1.4–15.0) | 10.0 (5.0–18.0) | 15.0 (3.0–20.0) | |

| Device Brand Preferences | ||||||

| Device Brand | IQOS | 64.5 (60.3–68.6) | 74.0 (65.3–81.1) | 60.1 (55.3–64.7) | 74.8 (64.1–83.2) | 100.0 |

| glo | 14.4 (11.7–17.5) | 8.2 (4.6–14.2) | 17.2 (13.9–21.2) | 8.9 (4.6–16.5) | - | |

| Ploom TECH | 21.1 (17.8–24.8) | 17.8 (11.8–25.9) | 22.7 (18.9–26.9) | 16.3 (9.5–26.4) | - | |

| F(3.68, 2921.15) = 2.69; p = 0.033 | ||||||

| Flavor Preferences | ||||||

| Flavor | Tobacco | 33.7 (29.8–37.7) | 29.3 (21.8–38.1) | 35.7 (31.5–40.2) | 26.8 (18.1–37.6) | 35.0 (10.2–71.8) |

| Menthol | 41.5 (37.2–45.9) | 47.5 (38.5–56.7) | 38.6 (34.2–43.3) | 49.2 (38.4–60.2) | 65.0 (28.2–89.7) | |

| Mentholated fruity § | 20.0 (16.4–24.1) | 20.3 (13.8–28.9) | 19.8 (15.7–24.5) | 21.0 (13.2–31.7) | - | |

| Coffee | 3.1 (1.9–4.9) | 0.9 (0.2–3.9) | 4.1 (2.5–6.7) | 0.8 (0.1–5.5) | - | |

| Refused/Do not know | 1.8 (0.9–3.4) | 2.0 (0.6–6.1) | 1.7 (0.7–3.7) | 2.2 (0.6–7.8) | - | |

| F(7.47, 5995.58) = 1.16; p = 0.319 | ||||||

| HTP Device Brand | p-Value * | ||||

|---|---|---|---|---|---|

| Weighted % (95% Confidence Interval) | |||||

| IQO (n = 547) | Glo (n = 131) | Ploom TECH (n = 172) | |||

| Product Use Pattern | |||||

| Frequency of HTP Use | Daily | 69.6 (63.9–74.7) | 60.1 (48.2–70.9) | 49.1 (39.9–58.3) | 0.004 |

| Weekly | 14.8 (11.7–18.7) | 16.0 (10.3–24.1) | 20.2 (14.6–27.3) | ||

| Monthly | 15.6 (11.1–21.3) | 23.9 (14.0–37.5) | 30.7 (22.4–40.5) | ||

| Time to first HTP use | 5 min or less | 19.2 (15.4–23.6) | 13.9 (8.7–21.4) | 6.2 (3.4–11.2) | 0.001 |

| 6–30 min | 36.6 (31.3–42.3) | 26.6 (18.9–36.1) | 29.6 (21.5–39.3) | ||

| 31–60 min | 15.8 (12.1–20.4) | 15.2 (8.5–25.7) | 16.3 (10.3–24.8) | ||

| More than 60 min | 26.5 (21.9–31.6) | 40.3 (29.6–52.0) | 46.5 (37.4–55.8) | ||

| Refused/Do not know | 1.9 (0.6–5.4) | 4.0 (1.3–11.4) | 1.4 (0.4–4.2) | ||

| Tobacco-containing inserts per day † | 10.0 (5.0–18.0) | 10.0 (5.0–15.0) | 1.0 (0.7–5.0) | <0.001 | |

| Device Brand | |||||

| Reason for choosing specific device brand ‡ | Perceived reduction in health risk compared to smoking | 64.7 (59.2–69.8) | 59.2 (48.4–69.2) | 68.4 (59.2–76.4) | 0.364 |

| Price | 18.2 (14.0–23.3) | 37.2 (27.8–47.6) | 35.4 (26.9–44.9) | 0.001 | |

| Taste | 43.3 (37.8–49.0) | 36.3 (27.0–46.7) | 48.4 (39.2–57.7) | 0.223 | |

| Design | 37.6 (32.1–43.4) | 29.4 (20.1–39.4) | 39.3 (30.7–48.6) | 0.768 | |

| Time to heat | 21.7 (17.8–26.2) | 42.0 (31.5–53.3) | 54.0 (44.6–63.1) | <0.001 | |

| Advertising | 24.9 (20.8–29.5) | 23.1 (13.6–36.5) | 16.9 (11.4–24.3) | 0.703 | |

| Availability | 56.5 (50.7–62.1) | 53.2 (42.1–64.0) | 34.5 (26.4–43.6) | 0.002 | |

| Used by friends | 68.1 (62.8–73.0) | 41.4 (31.4–52.2) | 25.8 (18.5–34.8) | <0.001 | |

| Endorsement in media | 22.9 (18.2–28.5) | 8.3 (4.8–14.1) | 5.9 (2.9–11.3) | <0.001 | |

| Flavor | |||||

| Flavor | Tobacco | 37.0 (32.0–42.3) | 28.1 (20.5–37.7) | 29.2 (21.9–37.8) | <0.001 |

| Menthol | 52.6 (47.0–58.2) | 51.8 (41.0–62.4) | - | ||

| Mentholated fruity § | 9.5 (5.9–15.0) | 19.0 (12.4–28.0) | 54.6 (45.3–63.5) | ||

| Coffee | - | - | 15.0 (9.5–22.9) | ||

| Refused/Do not know | 0.9 (0.3–3.1) | 1.1 (0.3–4.5) | 1.2 (0.4–3.0) | ||

| IQOS * | Glo † | Ploom TECH ‡ | ||

|---|---|---|---|---|

| aOR (95% CI) | aOR (95% CI) | aOR (95% CI) | ||

| Gender | Male | Ref | Ref | Ref |

| Female | 1.14 (0.73–1.78) | 0.96 (0.58–1.60) | 0.84 (0.47–1.51) | |

| Age (years) | 20–29 | Ref | Ref | Ref |

| 30–39 | 0.46 (0.24–0.86) | 1.62 (0.78–3.35) | 2.26 (0.90–5.67) | |

| 40–59 | 0.36 (0.20–0.66) | 1.35 (0.67–2.71) | 3.79 (1.61–8.92) | |

| 60 and older | 0.20 (0.09–0.43) | 1.53 (0.55–4.21) | 6.52 (2.44–17.44) | |

| Annual Household Income | Low | Ref | Ref | Ref |

| Moderate | 0.95 (0.51–1.76) | 1.49 (0.69–3.18) | 0.83 (0.39–1.75) | |

| High | 1.49 (0.85–2.61) | 1.10 (0.59–2.08) | 0.55 (0.27–1.11) | |

| Refused/Do not know | 1.22 (0.58–2.59) | 1.48 (0.60–3.66) | 0.56 (0.22–1.46) | |

| Education | Low | Ref | Ref | Ref |

| Moderate | 1.26 (0.76–2.09) | 1.16 (0.61–2.21) | 0.58 (0.32–1.07) | |

| High | 0.84 (0.54–1.31) | 0.83 (0.49–1.44) | 1.42 (0.83–2.45) | |

| Other/Refused/Do not know | 1.28 (0.16–9.91) | 1.66 (0.16–17.18) | - § | |

| Frequency of HTP Use | Daily | Ref | Ref | Ref |

| Weekly | 0.61 (0.39–0.95) | 1.08 (0.61–1.93) | 1.89 (1.12–3.17) | |

| Monthly | 0.49 (0.29–0.83) | 1.26 (0.62–2.56) | 2.12 (1.19–3.76) |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sutanto, E.; Miller, C.; Smith, D.M.; O’Connor, R.J.; Quah, A.C.K.; Cummings, K.M.; Xu, S.; Fong, G.T.; Hyland, A.; Ouimet, J.; et al. Prevalence, Use Behaviors, and Preferences among Users of Heated Tobacco Products: Findings from the 2018 ITC Japan Survey. Int. J. Environ. Res. Public Health 2019, 16, 4630. https://doi.org/10.3390/ijerph16234630

Sutanto E, Miller C, Smith DM, O’Connor RJ, Quah ACK, Cummings KM, Xu S, Fong GT, Hyland A, Ouimet J, et al. Prevalence, Use Behaviors, and Preferences among Users of Heated Tobacco Products: Findings from the 2018 ITC Japan Survey. International Journal of Environmental Research and Public Health. 2019; 16(23):4630. https://doi.org/10.3390/ijerph16234630

Chicago/Turabian StyleSutanto, Edward, Connor Miller, Danielle M. Smith, Richard J. O’Connor, Anne C. K. Quah, K. Michael Cummings, Steve Xu, Geoffrey T. Fong, Andrew Hyland, Janine Ouimet, and et al. 2019. "Prevalence, Use Behaviors, and Preferences among Users of Heated Tobacco Products: Findings from the 2018 ITC Japan Survey" International Journal of Environmental Research and Public Health 16, no. 23: 4630. https://doi.org/10.3390/ijerph16234630

APA StyleSutanto, E., Miller, C., Smith, D. M., O’Connor, R. J., Quah, A. C. K., Cummings, K. M., Xu, S., Fong, G. T., Hyland, A., Ouimet, J., Yoshimi, I., Mochizuki, Y., Tabuchi, T., & Goniewicz, M. L. (2019). Prevalence, Use Behaviors, and Preferences among Users of Heated Tobacco Products: Findings from the 2018 ITC Japan Survey. International Journal of Environmental Research and Public Health, 16(23), 4630. https://doi.org/10.3390/ijerph16234630