COVID-19 Effects on the Relationship between Cryptocurrencies: Can It Be Contagion? Insights from Econophysics Approaches

Abstract

1. Introduction

2. Brief Literature Review

3. Data and Methods

4. Results and Discussion

4.1. Descriptive Statistics

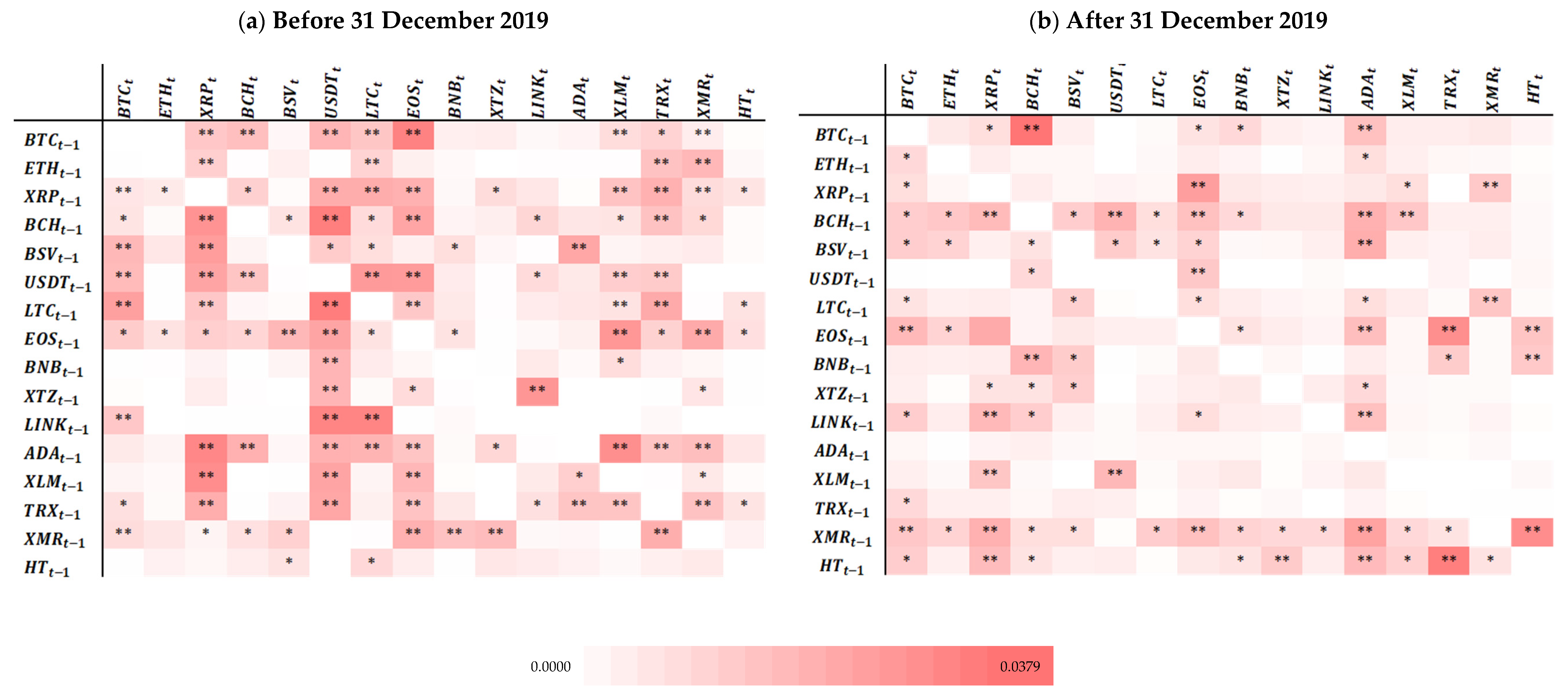

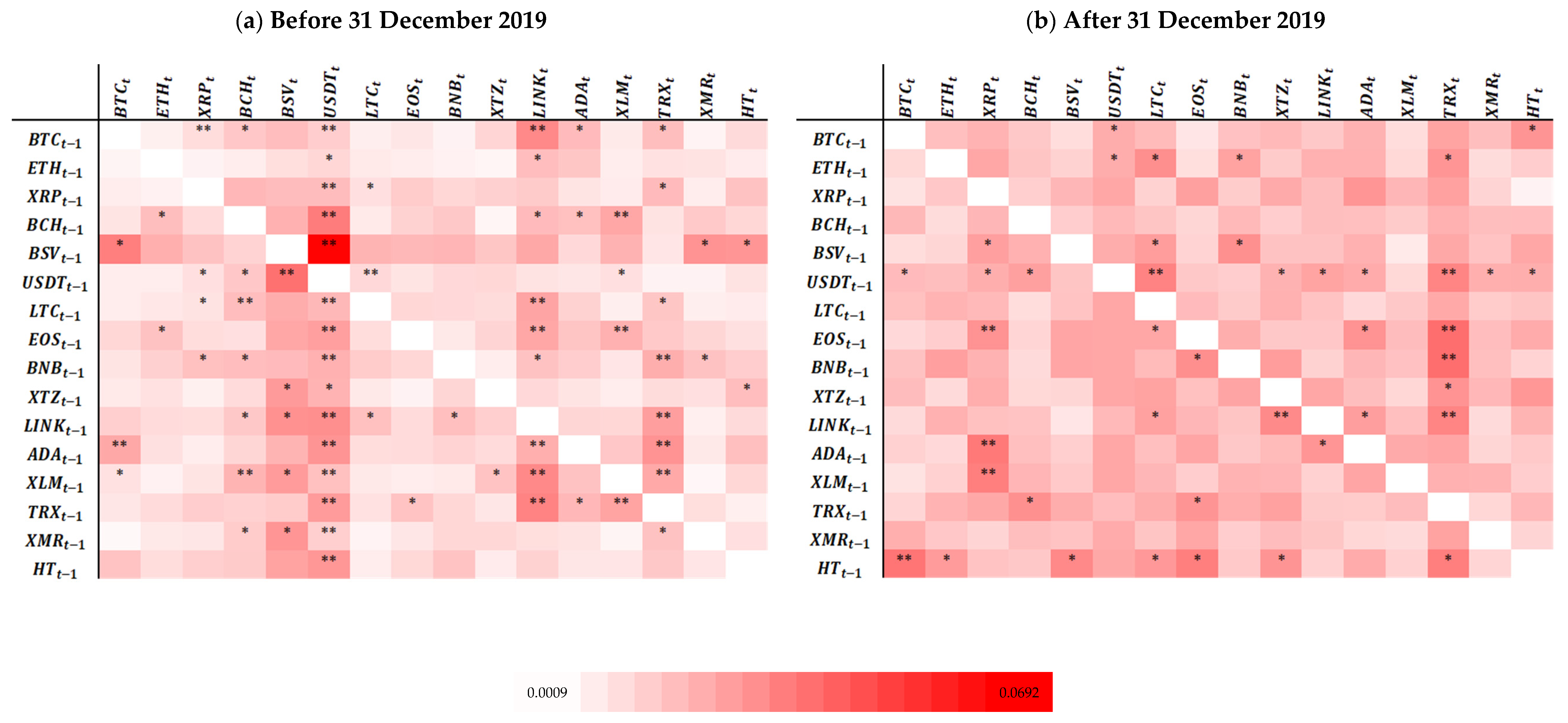

4.2. Mutual Information

4.3. Transfer Entropy Results

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Conflicts of Interest

References

- Bouri, E.; Shahzad, S.J.H.; Roubaud, D.; Kristoufek, L.; Lucey, B. Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. Q. Rev. Econ. Financ. 2020, 77, 156–164. [Google Scholar] [CrossRef]

- Neto, D. Are Google searches making the Bitcoin market run amok? A tail event analysis. N. Am. J. Econ. Financ. 2021, 57, 101454. [Google Scholar] [CrossRef]

- Leirvik, T. Cryptocurrency returns and the volatility of liquidity. Financ. Res. Lett. 2021, 44, 102031. [Google Scholar] [CrossRef]

- Mendoza, E.G.; Calvo, G.A. Rational contagion and the globalization of securities markets. J. Int. Econ. 2000, 51, 79–113. [Google Scholar]

- Seth, N.; Panda, L. Financial contagion: Review of empirical literature. Qual. Res. Financ. Mark. 2018, 10, 15–70. [Google Scholar] [CrossRef]

- Forbes, K.; Rigobon, R. No contagion, only interdependence: Measuring stock market comovements. J. Financ. 2002, 57, 2223–2261. [Google Scholar] [CrossRef]

- Bae, K.-H.; Karolyi, G.A.; Stulz, R.M. A New Approach to Measuring Financial Contagion. Rev. Financ. Stud. 2003, 16, 717–763. [Google Scholar] [CrossRef]

- Pericoli, M.; Sbracia, M. A primer on financial contagion. J. Econ. Surv. 2003, 17, 571–608. [Google Scholar] [CrossRef]

- Davidson, S.N. Interdependence or contagion: A model switching approach with a focus on Latin America. Econ. Model. 2020, 85, 166–197. [Google Scholar] [CrossRef]

- Le, T.H.; Do, H.X.; Nguyen, D.K.; Sensoy, A. COVID-19 pandemic and tail-dependency networks of financial assets. Financ. Res. Lett. 2021, 38, 101800. [Google Scholar] [CrossRef]

- Kristoufek, L. Tethered, or Untethered? On the interplay between stablecoins and major cryptoassets. Financ. Res. Lett. 2021, 43, 101991. [Google Scholar] [CrossRef]

- Park, S.; Jang, K.; Yang, J.-S. Information flow between bitcoin and other investment assets. Phys. A Stat. Mech. Its Appl. 2021, 566. [Google Scholar] [CrossRef]

- Mensi, W.; Rehman, M.U.; Maitra, D.; Al-Yahyaee, K.H.; Sensoy, A. Does bitcoin co-move and share risk with Sukuk and world and regional Islamic stock markets? Evidence using a time-frequency approach. Res. Int. Bus. Financ. 2020, 53, 101230. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Shahbaz, M.; Nasir, M.A.; Ullah, S. Financial modelling, risk management of energy instruments and the role of cryptocurrencies. Ann. Oper. Res. 2020, 313, 0123456789. [Google Scholar] [CrossRef]

- Vidal-Tomás, D.; Ibáñez, A.M.; Farinós, J.E. Herding in the cryptocurrency market: CSSD and CSAD approaches. Financ. Res. Lett. 2019, 30, 181–186. [Google Scholar] [CrossRef]

- Bouri, E.; Shahzad, S.J.H.; Roubaud, D. Co-explosivity in the cryptocurrency market. Financ. Res. Lett. 2019, 29, 178–183. [Google Scholar] [CrossRef]

- Ferreira, P.; Pereira, É. Contagion Effect in Cryptocurrency Market. J. Risk Financ. Manag. Commun. 2019, 12, 115. [Google Scholar] [CrossRef]

- Dionisio, A.; Menezes, R.; Mendes, D.A. Mutual information: A measure of dependency for nonlinear time series. Phys. A Stat. Mech. Its Appl. 2004, 344, 326–329. [Google Scholar] [CrossRef]

- Schreiber, T. Measuring information transfer. Phys. Rev. Lett. 2000, 85, 461–464. [Google Scholar] [CrossRef]

- Aslam, F.; Aziz, S.; Nguyen, D.K.; Mughal, K.S.; Khan, M. On the efficiency of foreign exchange markets in times of the COVID-19 pandemic. Technol. Forecast. Soc. Chang. 2020, 161, 120261. [Google Scholar] [CrossRef]

- Lee, K.-J.; Lu, S.-L.; Shih, Y. Contagion Effect of Natural Disaster and Financial Crisis Events on International Stock Markets. J. Risk Financ. Manag. 2018, 11, 16. [Google Scholar] [CrossRef]

- Nguyen, D.T.; Phan, D.H.B.; Ming, T.C.; Nguyen, V.K.L. An assessment of how COVID-19 changed the global equity market. Econ. Anal. Policy 2021, 69, 480–491. [Google Scholar] [CrossRef]

- Yousaf, I.; Ali, S. The COVID-19 outbreak and high frequency information transmission between major cryptocurrencies: Evidence from the VAR-DCC-GARCH approach. Borsa Istanb. Rev. 2020, 20, S1–S10. [Google Scholar] [CrossRef]

- Corbet, S.; Larkin, C.; Lucey, B. The contagion effects of the COVID-19 pandemic: Evidence from gold and cryptocurrencies. Financ. Res. Lett. 2020, 35, 101554. [Google Scholar] [CrossRef]

- Akhtaruzzaman, M.; Boubaker, S.; Nguyen, D.K.; Rahman, M.R. Systemic risk-sharing framework of cryptocurrencies in the COVID–19 crisis. Financ. Res. Lett. 2022, 47 Pt B, 102787. [Google Scholar] [CrossRef]

- James, N.; Menzies, M.; Chan, J. Changes to the extreme and erratic behaviour of cryptocurrencies during COVID-19. Phys. A Stat. Mech. Its Appl. 2021, 565, 125581. [Google Scholar] [CrossRef]

- Assaf, A.; Charif, H.; Demir, E. Information sharing among cryptocurrencies: Evidence from mutual information and approximate entropy during COVID-19. Financ. Res. Lett. 2022, 47, 102556. [Google Scholar] [CrossRef]

- Caferra, R.; Vidal-Tomás, D. Who raised from the abyss? A comparison between cryptocurrency and stock market dynamics during the COVID-19 pandemic. Financ. Res. Lett. 2021, 43, 101954. [Google Scholar] [CrossRef]

- Conlon, T.; Corbet, S.; McGee, R.J. Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Res. Int. Bus. Financ. 2020, 54, 101248. [Google Scholar] [CrossRef]

- Conlon, T.; McGee, R. Safe haven or risky hazard? Bitcoin during the COVID-19 bear market. Financ. Res. Lett. 2020, 35, 101607. [Google Scholar] [CrossRef]

- Goodell, J.W.; Goutte, S. Co-movement of COVID-19 and Bitcoin: Evidence from wavelet coherence analysis. Financ. Res. Lett. 2021, 38, 101625. [Google Scholar] [CrossRef] [PubMed]

- Yarovaya, L.; Matkovskyy, R.; Jalan, A. The effects of a “black swan” event (COVID-19) on herding behavior in cryptocurrency markets. J. Int. Financ. Mark. Inst. Money 2021, 75, 101321. [Google Scholar] [CrossRef]

- Cho, S.; Hyde, S.; Nguyen, N. Time-varying regional and global integration and contagion: Evidence from style portfolios. Int. Rev. Financ. Anal. 2015, 42, 109–131. [Google Scholar] [CrossRef]

- Ferreira, P. Portuguese and Brazilian stock market integration: A non-linear and detrended approach. Port. Econ. J. 2017, 16, 49–63. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Adewuyi, A.O.; Albulescu, C.T.; Wohar, M.E. Empirical evidence of extreme dependence and contagion risk between main cryptocurrencies. N. Am. J. Econ. Financ. 2020, 51, 101083. [Google Scholar] [CrossRef]

- Mensi, W.; Rehman, M.U.; Al-Yahyaee, K.H.; Al-Jarrah, I.M.W.; Kang, S.H. Time frequency analysis of the commonalities between Bitcoin and major Cryptocurrencies: Portfolio risk management implications. N. Am. J. Econ. Financ. 2019, 48, 283–294. [Google Scholar] [CrossRef]

- Qureshi, S.; Aftab, M.; Bouri, E.; Saeed, T. Dynamic interdependence of cryptocurrency markets: An analysis across time and frequency. Phys. A Stat. Mech. Its Appl. 2020, 559, 125077. [Google Scholar] [CrossRef]

- Koutmos, D. Return and volatility spillovers among cryptocurrencies. Econ. Lett. 2018, 173, 122–127. [Google Scholar] [CrossRef]

- Yi, S.; Xu, Z.; Wang, G.J. Volatility connectedness in the cryptocurrency market: Is Bitcoin a dominant cryptocurrency? Int. Rev. Financ. Anal. 2018, 60, 98–114. [Google Scholar] [CrossRef]

- Ji, Q.; Bouri, E.; Lau, C.K.M.; Roubaud, D. Dynamic connectedness and integration in cryptocurrency markets. Int. Rev. Financ. Anal. 2019, 63, 257–272. [Google Scholar] [CrossRef]

- Sensoy, A.; Silva, T.C.; Corbet, S.; Tabak, B.M. High-frequency return and volatility spillovers among cryptocurrencies. Appl. Econ. 2021, 53, 4310–4328. [Google Scholar] [CrossRef]

- Kakinaka, S.; Umeno, K. Asymmetric volatility dynamics in cryptocurrency markets on multi-time scales. Res. Int. Bus. Financ. 2022, 62, 101754. [Google Scholar] [CrossRef]

- Canh, N.P.; Wongchoti, U.; Thanh, S.D.; Thong, N.T. Systematic risk in cryptocurrency market: Evidence from DCC-MGARCH model. Financ. Res. Lett. 2019, 29, 90–100. [Google Scholar] [CrossRef]

- Huynh, T.L.D.; Nasir, M.A.; Vo, X.V.; Nguyen, T.T. “Small things matter most”: The spillover effects in the cryptocurrency market and gold as a silver bullet. N. Am. J. Econ. Financ. 2020, 54, 101277. [Google Scholar] [CrossRef]

- Guo, H.; Zhao, X.; Yu, H.; Zhang, X. Analysis of global stock markets’ connections with emphasis on the impact of COVID-19. Phys. A Stat. Mech. Its Appl. 2021, 569, 125774. [Google Scholar] [CrossRef]

- Szczygielski, J.J.; Brzeszczyński, J.; Charteris, A.; Bwanya, P.R. The COVID-19 storm and the energy sector: The impact and role of uncertainty. Energy Economics 2021, 109, 105258. [Google Scholar] [CrossRef]

- Shahzad, S.J.H.; Bouri, E.; Kang, S.H.; Saeed, T. Regime specific spillover across cryptocurrencies and the role of COVID-19. Financ. Innov. 2021, 7, 5. [Google Scholar] [CrossRef]

- Li, Z.; Wang, Y.; Huang, Z. Risk Connectedness Heterogeneity in the Cryptocurrency Markets. Front. Phys. 2020, 8, 243. [Google Scholar] [CrossRef]

- McKibbin, W.; Fernando, R. TheGlobalMacroeconomic Impacts ofCOVID-19:SevenScenarios Warwick. Asian Econ. Pap. 2021, 20, 1–21. [Google Scholar] [CrossRef]

- Naeem, M.A.; Bouri, E.; Peng, Z.; Shahzad, S.J.H.; Vo, X.V. Asymmetric efficiency of cryptocurrencies during COVID19. Phys. A Stat. Mech. Its Appl. 2021, 565, 125562. [Google Scholar] [CrossRef]

- Katsiampa, P.; Yarovaya, L.; Zięba, D. High-frequency connectedness between Bitcoin and other top-traded crypto assets during the COVID-19 crisis. J. Int. Financ. Mark. Inst. Money 2022, 79, 101578. [Google Scholar] [CrossRef]

- Sui, X.; Shi, G.; Hou, G.; Huang, S.; Li, Y. Impacts of COVID-19 on the Return and Volatility Nexus among Cryptocurrency Market. Complexity 2022, 2022, 5346080. [Google Scholar] [CrossRef]

- Balcilar, M.; Ozdemir, H.; Agan, B. Effects of COVID-19 on cryptocurrency and emerging market connectedness: Empirical evidence from quantile, frequency, and lasso networks. Phys. A Stat. Mech. Its Appl. 2022, 604, 127885. [Google Scholar] [CrossRef]

- Nguyen, A.P.N.; Mai, T.T.; Bezbradica, M.; Crane, M. The Cryptocurrency Market in Transition before and after COVID-19: An Opportunity for Investors? Entropy 2022, 24, 1317. [Google Scholar] [CrossRef]

- Yarovaya, L.; Zięba, D. Intraday volume-return nexus in cryptocurrency markets: Novel evidence from cryptocurrency classification. Res. Int. Bus. Financ. 2022, 60, 101592. [Google Scholar] [CrossRef]

- Rubbaniy, G.; Khalid, A.A.; Samitas, A. Are Cryptos Safe-Haven Assets during Covid-19? Evidence from Wavelet Coherence Analysis. Emerg. Mark. Financ. Trade 2021, 57, 1741–1756. [Google Scholar] [CrossRef]

- García-Medina, A.; Hernández, J.B.C. Network analysis of multivariate transfer entropy of cryptocurrencies in times of turbulence. Entropy 2020, 22, 760. [Google Scholar] [CrossRef]

- Ghorbel, A.; Jeribi, A. Investigating the relationship between volatilities of cryptocurrencies and other financial assets. Decis. Econ. Financ. 2021, 44, 817–843. [Google Scholar] [CrossRef]

- Wątorek, M.; Drożdż, S.; Kwapień, J.; Minati, L.; Oświęcimka, P.; Stanuszek, M. Multiscale characteristics of the emerging global cryptocurrency market. Phys. Rep. 2021, 901, 1–82. [Google Scholar] [CrossRef]

- Kwapień, J.; Wątorek, M.; Drożdż, S. Cryptocurrency market consolidation in 2020–2021. Entropy 2021, 23, 1674. [Google Scholar] [CrossRef]

- Raza, S.A.; Shah, N.; Guesmi, K.; Msolli, B. How does COVID-19 influence dynamic spillover connectedness between Cryptocurrencies? Evidence from non-parametric causality-in-quantiles techniques. Financ. Res. Lett. 2021, 47, 102569. [Google Scholar] [CrossRef] [PubMed]

- Drozdz, S.; Kwapień, J.; Oświecimka, P.; Stanisz, T.; Watorek, M. Complexity in economic and social systems: Cryptocurrency market at around COVID-19. Entropy 2020, 22, 1043. [Google Scholar] [CrossRef] [PubMed]

- Bariviera, A.F.; Merediz-Solà, I. Where Do We Stand in Cryptocurrencies Economic Research? a Survey Based on Hybrid Analysis. J. Econ. Surv. 2021, 35, 377–407. [Google Scholar] [CrossRef]

- Wątorek, M.; Kwapień, J.; Drożdż, S. Multifractal Cross-Correlations of Bitcoin and Ether Trading Characteristics in the Post-COVID-19 Time. Future Internet 2022, 14, 215. [Google Scholar] [CrossRef]

- Vidal-Tomás, D. Which cryptocurrency data sources should scholars use? Int. Rev. Financ. Anal. 2022, 81, 102061. [Google Scholar] [CrossRef]

- Shannon, C.E. A Mathematical Theory of Communication. Bell Syst. Tech. J. 1948, 27, 379–423, 623–656. [Google Scholar] [CrossRef]

- Rosser, J.B. Econophysics and the entropic foundations of economics. Entropy 2021, 23, 1286. [Google Scholar] [CrossRef]

- Kullback, S.; Leibler, R.A. On information and sufficiency. Ann. Math. Stat. 1951, 22, 79–86. [Google Scholar] [CrossRef]

- Sheraz, M.; Dedu, S.; Preda, V. Volatility Dynamics of Non-Linear Volatile Time Series and Analysis of Information Flow: Evidence from Cryptocurrency Data. Entropy 2022, 24, 1410. [Google Scholar] [CrossRef]

- Lizier, J.; Heinzle, J.; Horstmann, A.; Haynes, J.-D.; Prokopenko, M. Multivariate information-theoretic measures reveal directed information structure and task relevant changes in fMRI connectivity. J. Comput. Neurosci. 2011, 30, 85–107. [Google Scholar] [CrossRef]

- Dimpfl, T.; Peter, F.J. The impact of the financial crisis on transatlantic information flows: An intraday analysis. J. Int. Financ. Mark. Inst. Money 2014, 31, 1–13. [Google Scholar] [CrossRef]

- Barnett, L.; Barrett, A.B.; Seth, A.K. Granger Causality and Transfer Entropy Are equivalent for Gaussian Variables. Phys. Rev. Lett. 2009, 103, 238701. [Google Scholar] [CrossRef]

- Jizba, P.; Kleinert, H.; Shefaat, M. Rényi’s information transfer between financial time series. Phys. A Stat. Mech. Its Appl. 2012, 391, 2971–2989. [Google Scholar] [CrossRef]

- Dimpfl, T.; Peter, F.J. Using transfer entropy to measure information flows between financial markets. Stud. Nonlinear Dyn. Econom. 2013, 17, 85–102. [Google Scholar] [CrossRef]

- Behrendt, S.; Dimpfl, T.; Peter, F.J.; Zimmermann, D.J. RTransferEntropy—Quantifying information flow between different time series using effective transfer entropy. SoftwareX 2019, 10, 100265. [Google Scholar] [CrossRef]

- Dionísio, A.; Menezes, R.; Mendes, D.A. Entropy-based independence test. Nonlinear Dyn. 2006, 44, 351–357. [Google Scholar] [CrossRef]

- Gencer, A.E.; Basu, S.; Eyal, I.; van Renesse, R.; Sirer, E.G. Decentralization in Bitcoin and Ethereum Networks. In Financial Cryptography and Data Security. Lecture Notes in Computer Science. FC 2018; Meiklejohn, S., Sako, K., Eds.; Springer: Berlin/Heidelberg, Germany, 2018; Volume 10957. [Google Scholar] [CrossRef]

- Vidal-Tomás, D. Transitions in the cryptocurrency market during the COVID-19 pandemic: A network analysis. Financ. Res. Lett. 2021, 43, 101981. [Google Scholar] [CrossRef]

- Dimpfl, T.; Peter, F.J. Group transfer entropy with an application to cryptocurrencies. Phys. A Stat. Mech. Its Appl. 2019, 516, 543–551. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, Y.G.; Hu, Y.; Larkin, C.; Oxley, L. Any port in a storm: Cryptocurrency safe-havens during the COVID-19 pandemic. Econ. Lett. 2020, 194, 109377. [Google Scholar] [CrossRef]

- Marschinski, R.; Kantz, H. Analysing the information flow between financial time series. Eur. Phys. J. B 2002, 30, 275–281. [Google Scholar] [CrossRef]

- Maiti, M.; Kayal, P. Asymmetric Information Flow between Exchange Rate, Oil, and Gold: New Evidence from Transfer Entropy Approach. Risk Financ. Manag. 2023, 16, 2. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Cryptocurrency | Start Date | Market Capitalization (USD) | Observations | ||||

|---|---|---|---|---|---|---|---|

| Before 31 December 2019 | After 31 December 2019 | ||||||

| 1 | Bitcoin | BTC | 29 April 2013 | 162,684,945,903 | 61.77% | 2.437 | 396 |

| 2 | Ethereum | ETH | 07 August 2015 | 26,164,459,704 | 9.93% | 1.607 | 396 |

| 3 | Ripple | XRP | 04 August 2013 | 26,164,459,704 | 9.93% | 2.340 | 396 |

| 4 | Bitcoin Cash | BCH | 23 July 2017 | 6,059,789,428 | 2.30% | 891 | 396 |

| 5 | Bitcoin SV | BSV | 09 November 2018 | 4,290,029,659 | 1.63% | 417 | 396 |

| 6 | Tether | USDT | 25 February 2015 | 4,643,212,805 | 1.76% | 1.770 | 396 |

| 7 | Litecoin | LTC | 29 April 2013 | 3,889,681,824 | 1.48% | 2.437 | 396 |

| 8 | EOS | EOS | 01 July 2017 | 3,366,250,140 | 1.28% | 913 | 396 |

| 9 | BinanceCoin | BNB | 25 July 2017 | 3,138,663,736 | 1.19% | 889 | 396 |

| 10 | Tezos | XTZ | 02 October 2017 | 2,103,907,641 | 0.80% | 820 | 396 |

| 11 | ChainLink | LINK | 20 September 2017 | 1,520,607,569 | 0.58% | 832 | 396 |

| 12 | Cardano | ADA | 01 October 2017 | 1,268,987,677 | 0.48% | 821 | 396 |

| 13 | Stellar | XLM | 05 August 2014 | 1,183,231,787 | 0.45% | 1.974 | 396 |

| 14 | TRON | TRX | 13 September 2017 | 1,136,886,287 | 0.43% | 839 | 396 |

| 15 | Monero | XMR | 21 May 2014 | 1,143,443,765 | 0.43% | 2.050 | 396 |

| 16 | Huobi Token | HT | 03 February 2018 | 1,063,188,577 | 0.40% | 696 | 396 |

| Total | 249,821,746,206 | 94.86% | |||||

| Cryptocurrency | Before 31 December 2019 | After 31 December 2019 | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | Stdev. | Skewness | Kurtosis | Mean | Stdev. | Skewness | Kurtosis | |

| BTC | 0.0016 | 0.0427 | −0.1527 | 10.7409 | 0.0039 | 0.0414 | −3.4812 | 44.5290 |

| ETH | 0.0024 | 0.0714 | −3.4274 | 74.6109 | 0.0060 | 0.0551 | −2.5411 | 29.9171 |

| XRP | 0.0015 | 0.0727 | 2.0756 | 32.9133 | 0.0021 | 0.0660 | −0.3960 | 26.4318 |

| BCH | −0.0008 | 0.0794 | 0.6179 | 10.4098 | 0.0018 | 0.0603 | −1.8145 | 24.2868 |

| BSV | 0.0008 | 0.0901 | 0.8643 | 19.9132 | 0.0015 | 0.0814 | 2.8755 | 46.5471 |

| USDT | −0.0001 | 0.0211 | −12.2749 | 829.3628 | 0.0000 | 0.0055 | 0.1522 | 37.9746 |

| LTC | 0.0009 | 0.0645 | 1.7163 | 28.5632 | 0.0030 | 0.0540 | −1.5536 | 16.3358 |

| EOS | 0.0010 | 0.0827 | 2.2245 | 27.6377 | 0.0030 | 0.0545 | −2.0790 | 22.8957 |

| BNB | 0.0055 | 0.0787 | 1.3888 | 15.1944 | 0.0003 | 0.0502 | −3.3523 | 38.3843 |

| XTZ | −0.0004 | 0.0751 | 0.1255 | 10.5396 | 0.0019 | 0.0634 | −2.1090 | 24.3520 |

| LINK | 0.0027 | 0.0812 | 0.7048 | 7.1339 | 0.0065 | 0.0711 | −1.4227 | 18.0953 |

| ADA | 0.0003 | 0.0792 | 2.9094 | 29.3140 | 0.0061 | 0.0623 | −1.1089 | 14.6842 |

| XLM | 0.0015 | 0.0754 | 2.0089 | 19.6020 | 0.0050 | 0.0668 | 1.6195 | 21.9256 |

| TRX | 0.0023 | 0.0963 | 2.1343 | 19.3240 | 0.0022 | 0.0545 | −2.2636 | 24.9947 |

| XMR | 0.0016 | 0.0703 | 0.6497 | 9.6001 | 0.0029 | 0.0509 | −2.4056 | 26.4712 |

| HT | 0.0009 | 0.0518 | 0.6165 | 7.6063 | 0.0021 | 0.0431 | −3.5911 | 49.8863 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almeida, D.; Dionísio, A.; Vieira, I.; Ferreira, P. COVID-19 Effects on the Relationship between Cryptocurrencies: Can It Be Contagion? Insights from Econophysics Approaches. Entropy 2023, 25, 98. https://doi.org/10.3390/e25010098

Almeida D, Dionísio A, Vieira I, Ferreira P. COVID-19 Effects on the Relationship between Cryptocurrencies: Can It Be Contagion? Insights from Econophysics Approaches. Entropy. 2023; 25(1):98. https://doi.org/10.3390/e25010098

Chicago/Turabian StyleAlmeida, Dora, Andreia Dionísio, Isabel Vieira, and Paulo Ferreira. 2023. "COVID-19 Effects on the Relationship between Cryptocurrencies: Can It Be Contagion? Insights from Econophysics Approaches" Entropy 25, no. 1: 98. https://doi.org/10.3390/e25010098

APA StyleAlmeida, D., Dionísio, A., Vieira, I., & Ferreira, P. (2023). COVID-19 Effects on the Relationship between Cryptocurrencies: Can It Be Contagion? Insights from Econophysics Approaches. Entropy, 25(1), 98. https://doi.org/10.3390/e25010098