Nonlinear Stochastic Equation within an Itô Prescription for Modelling of Financial Market

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Economic Entropy

3. Phenomenological Itô Equation

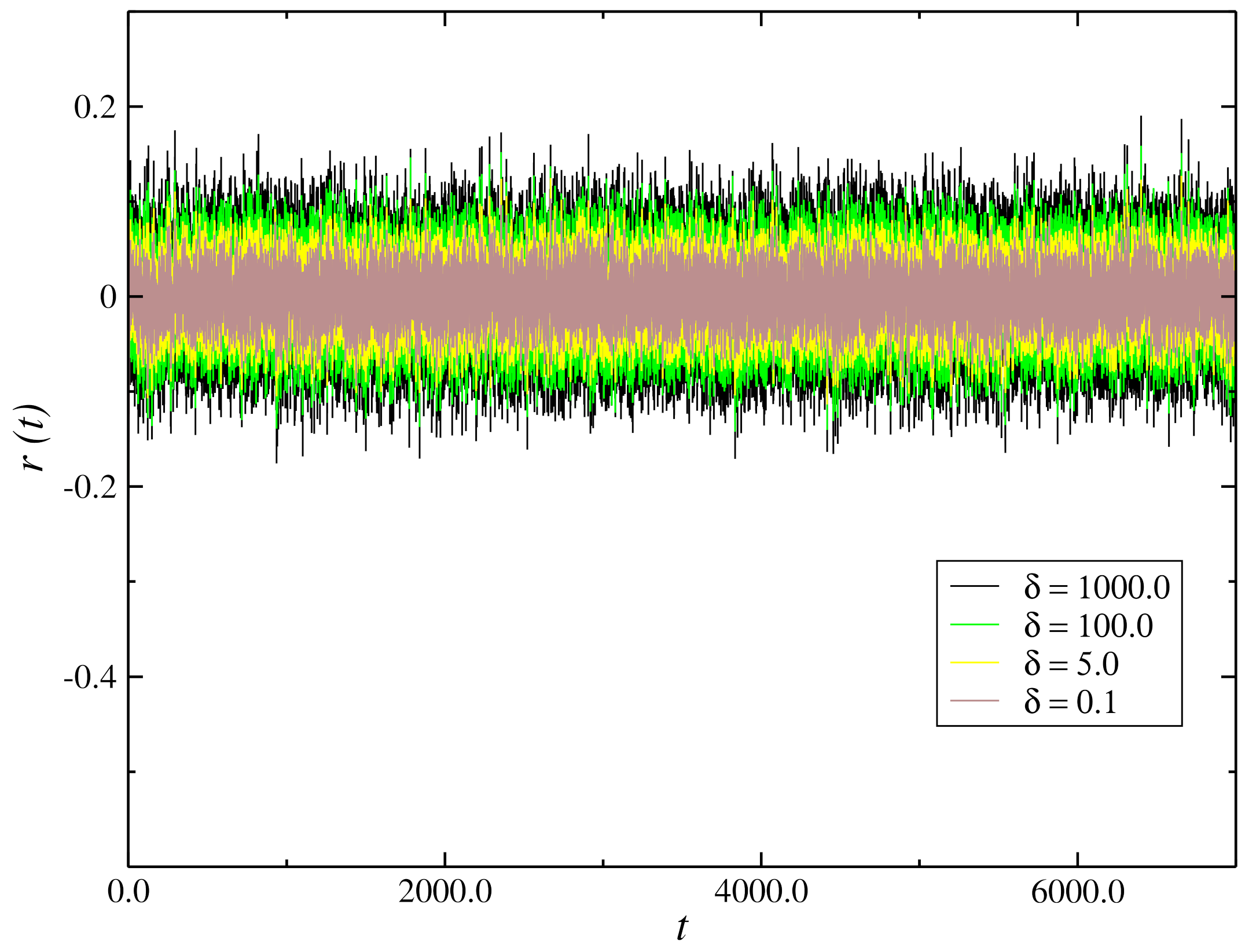

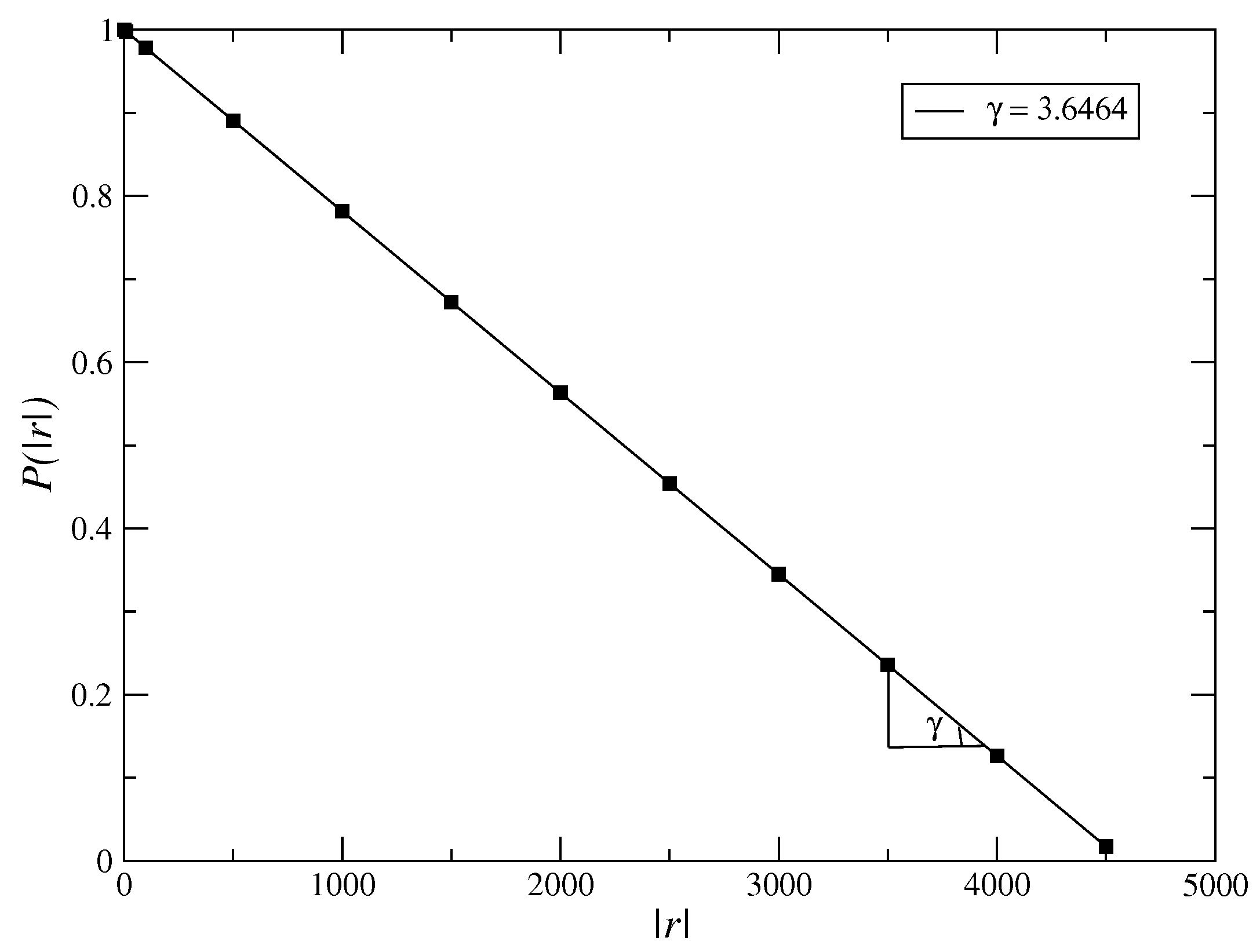

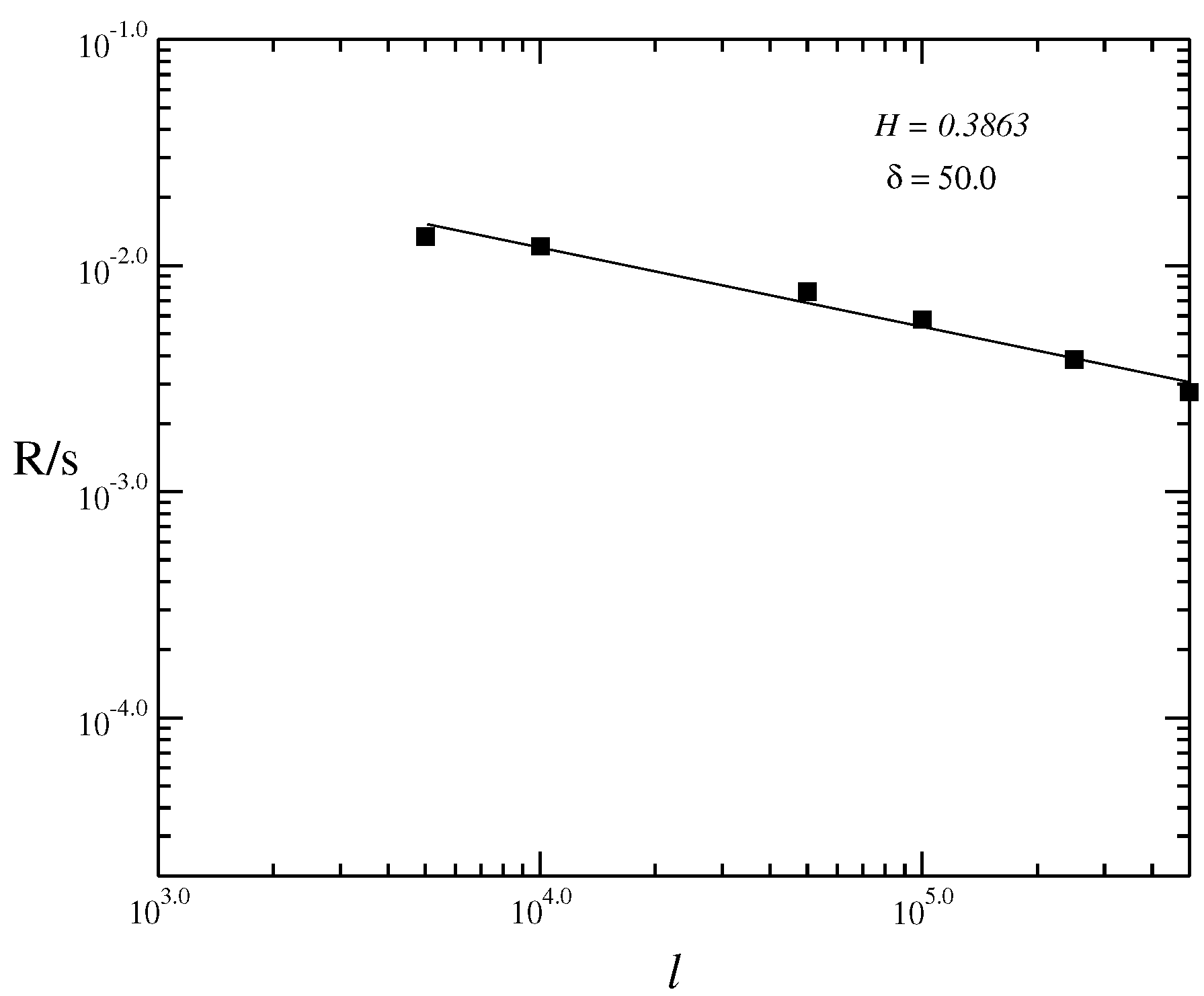

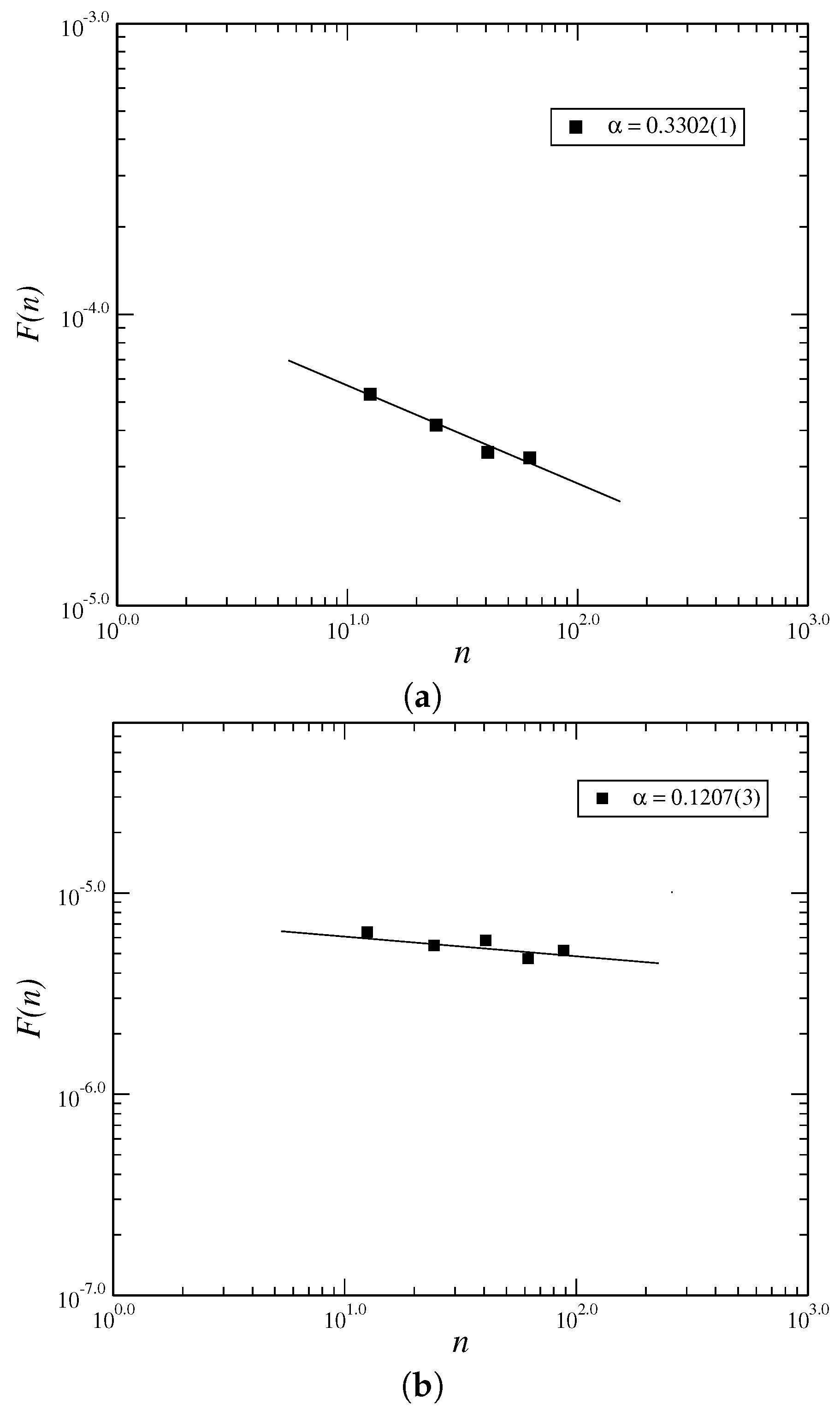

4. Numerical Results

5. Analysis by Fokker–Planck Equation

6. Conclusions

Funding

Conflicts of Interest

References

- Richmond, P.; Mimkes, J.; Hutzler, S. Econophysics and Physical Economics; Oxford University Press: Oxford, UK, 2013. [Google Scholar]

- Jacobs, K. Stochastic Processes for Physicists; Cambridge University Press: New York, NY, USA, 2013. [Google Scholar]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–659. [Google Scholar] [CrossRef]

- Mantegna, R.S.; Stanley, H.E. An Introduction to Econophysics, Correlations and Complexity in Finance, 4th ed.; Cambridge University Press: New York, NY, USA, 2007. [Google Scholar]

- Mike, S.; Farmer, J.D. An empirical behavioral model of liquidity and volatility. J. Econ. Dyn. Control 2008, 32, 200–234. [Google Scholar] [CrossRef]

- Gu, G.-F.; Zhou, W.-X. Emergence of long memory in stock volatility from a modified Mike-Farmer model. Europhys. Lett. 2009, 86, 48002. [Google Scholar] [CrossRef]

- Zhang, X.; Ping, J.; Zhu, T.; Li, Y.; Xiong, X. Are price limits effective? An examination of an artificial stock market. PLoS ONE 2016, 11, e0160406. [Google Scholar] [CrossRef]

- Sornette, D. Critical Phenomena in Natural Sicences—Chaos, Fractals, Self-Organization and Disorder: Concepts and Tools, 2nd ed.; Springer: Berlin/Heidelberg, Germany, 2004. [Google Scholar]

- Meng, H.; Ren, F.; Gu, G.-F.; Xiong, X.; Zhang, Y.-J.; Zhou, W.-X.; Zhang, W. Effects of long memory in the order submission process on the properties of recurrence intervals of large price fluctuations. Europhys. Lett. 2012, 98, 38003. [Google Scholar] [CrossRef][Green Version]

- Assenza, T.; Gatti, D.D.; Grazzini, J. Emergent dynamics of a macroeconomic agent based model with capital and credit. J. Econ. Dyn. Control 2015, 50, 5–28. [Google Scholar] [CrossRef]

- Diks, C.; Wang, J. Can a stochastic cusp catastrophe model explain housing market crashes? J. Econ. Dyn. Control 2016, 69, 68–88. [Google Scholar] [CrossRef]

- In’t Veld, D. Adverse effects of leverage and short-selling constraints in a financial market model with heterogeneous agents. J. Econ. Dyn. Control 2016, 69, 45–67. [Google Scholar] [CrossRef]

- Lima, L. Modeling of the financial market using the two-dimensional anisotropic Ising model. Phys. A Stat. Mech. Appl. 2017, 482, 544–551. [Google Scholar] [CrossRef]

- Gu, G.-F.; Zhou, W.-X. On the probability distribution of stock returns in the Mike-Farmer model. Eur. Phys. J. B 2009, 67, 585–592. [Google Scholar] [CrossRef]

- Zhou, W.-X.; Sornette, D. Self-organizing Ising model of financial markets. Eur. Phys. J. B 2007, 55, 175–181. [Google Scholar] [CrossRef]

- Sznajd-Weron, K.; Weron, R. A simple model of price formation. Int. J. Mod. Phys. C 2002, 13, 115–123. [Google Scholar] [CrossRef]

- Callen, E.; Shapero, D. A theory of social imitation. Phys. Today 1974, 27, 23. [Google Scholar] [CrossRef]

- Montroll, E.W.; Badger, W.W. Introduction to Quantitative Aspects of Social Phenomena; Gordon and Breach: New York, NY, USA, 1974. [Google Scholar]

- Orléan, A. Bayesian interactions and collective dynamics of opinion: Herd behavior and mimetic contagion. J. Econ. Behav. Organ. 1995, 28, 257–274. [Google Scholar] [CrossRef]

- Wang, F.; Yamasaki, K.; Havlin, S.; Stanley, H.E. Indication of multiscaling in the volatility return intervals of stock markets. Phys. Rev. E 2008, 77, 016109. [Google Scholar] [CrossRef]

- Gopikrishnan, P.; Meyer, M.; Amaral, L.N.; Stanley, H.E. Inverse cubic law for the distribution of stock price variations. Eur. Phys. J. B 1998, 3, 139–140. [Google Scholar] [CrossRef]

- Gopikrishnan, P.; Plerou, V.; Amaral, L.A.N.; Meyer, M.; Stanley, H.E. Scaling of the distribution of fluctuations of financial market indices. Phys. Rev. E 1999, 60, 5305. [Google Scholar] [CrossRef]

- Plerou, V.; Gopikrishnan, P.; Amaral, L.A.N.; Meyer, M.; Stanley, H.E. Scaling of the distribution of price fluctuations of individual companies. Phys. Rev. E 1999, 60, 6519. [Google Scholar] [CrossRef]

- Botta, F.; Moat, H.S.; Stanley, H.E.; Preis, T. Quantifying stock return distributions in financial markets. PLoS ONE 2015, 10, e0135600. [Google Scholar] [CrossRef]

- Zhou, J.; Gu, G.-F.; Jiang, Z.-Q.; Xiong, X.; Chen, W.; Zhang, W.; Zhou, W.-X. Computational experiments successfully predict the emergence of autocorrelations in ultra-high-frequency stock returns. Comput. Econ. 2017, 50, 579–594. [Google Scholar] [CrossRef]

- Karamé, F. A new particle filtering approach to estimate stochastic volatility models with Markov-switching. Econom. Stat. 2018, 8, 204–230. [Google Scholar] [CrossRef]

- Anzarut, M.; Mena, R.H. Harris process to model stochastic volatility. Econom. Stat. 2019, 10, 151–169. [Google Scholar] [CrossRef]

- Lima, L.S.; Miranda, L.L.B. Price dynamics of the financial markets using the stochastic differential equation for a potential double well. Phys. A Stat. Mech. Appl. 2018, 490, 828–833. [Google Scholar] [CrossRef]

- Lima, L.S.; Santos, G.K.C. Stochastic process with multiplicative structure for the dynamic behavior of the financial market. Phys. A Stat. Mech. Appl. 2018, 512, 222–229. [Google Scholar] [CrossRef]

- Lima, L.S.; Oliveira, S.C.; Abeilice, A.F. Modelling Based in Stochastic Non-Linear Differential Equation for Price Dynamics. Pioneer J. Math. Math. Sci. 2018, 23, 93–103. [Google Scholar]

- Lima, L.S.; Oliveira, S.C.; Abeilice, A.F.; Melgaço, J.H. Breaks down of the modeling of the financial market with addition of non-linear terms in the Itô stochastic process. Phys. A Stat. Mech. Appl. 2019, 526, 120932. [Google Scholar] [CrossRef]

- Shreve, S.E. Stochastic Calculus for Finance II: Continuous-Time Models; Springer: New York, NY, USA, 2004. [Google Scholar]

- Gardiner, C. Stochastic Methods, A Handbook for the Natural and Social Sciences, 4th ed.; Springer: Berlin/Heidelberg, Germany, 2009. [Google Scholar]

- Oksendal, B. Stochastic Differential Equations: An Introduction with Applications, 6th ed.; Springer: Berlin/Heidelberg, Germany, 2013. [Google Scholar]

- Xavier, P.O.; Atman, A.; de Magalhães, A.B. Equation-based model for the stock market. Phys. Rev. E 2017, 96, 032305. [Google Scholar] [CrossRef]

- He, J.-H. Some asymptotic methods for strongly nonlinear equations. Int. J. Mod. Phys. B 2006, 20, 1141–1199. [Google Scholar] [CrossRef]

- Tsallis, C. Economics and Finance: q-Statistical stylized features galore. Entropy 2017, 19, 457. [Google Scholar] [CrossRef]

- Ribeiro, M.S.; Nobre, F.D.; Curado, E.M. Classes of N-dimensional nonlinear Fokker–Planck equations associated to Tsallis entropy. Entropy 2011, 13, 1928–1944. [Google Scholar] [CrossRef]

- Tsallis, C. Possible generalization of Boltzmann-Gibbs statistics. J. Stat. Phys. 1988, 52, 479–487. [Google Scholar] [CrossRef]

- Yu, W.-T.; Chen, H.-Y. Herding and zero-intelligence agents in the order book dynamics of an artificial double auction market. Chin. J. Phys. 2018, 56, 1405–1414. [Google Scholar] [CrossRef]

- Mandelbrot, B. The Variation of Certain Speculative Prices. J. Bus. 1963, 35, 394. [Google Scholar] [CrossRef]

- Fama, E.F. Mandelbrot and the stable Paretian hypothesis. J. Bus. 1963, 36, 420–429. [Google Scholar] [CrossRef]

- Lux, T.; Marchesi, M. Scaling and criticality in a stochastic multi-agent model of a financial market. Nature 1999, 397, 498. [Google Scholar] [CrossRef]

- Bouchaud, J.-P.; Cont, R. A Langevin approach to stock market fluctuations and crashes. Eur. Phys. J. B 1998, 6, 543–550. [Google Scholar] [CrossRef]

- Kleinow, T. Testing Continuous Time Models in Financial Markets. Ph.D. Thesis, Humboldt University of Berlin, Berlin, Germany, 2002. [Google Scholar]

- Barbu, V.; Röckner, M. Nonlinear Fokker–Planck equations driven by Gaussian linear multiplicative noise. J. Differ. Equ. 2018, 265, 4993–5030. [Google Scholar] [CrossRef]

- Wang, P.; Zhang, W.; Li, X.; Shen, D. Trading volume and return volatility of Bitcoin market: Evidence for the sequential information arrival hypothesis. J. Econ. Interact. Coord. 2019, 14, 377–418. [Google Scholar] [CrossRef]

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

S. Lima, L. Nonlinear Stochastic Equation within an Itô Prescription for Modelling of Financial Market. Entropy 2019, 21, 530. https://doi.org/10.3390/e21050530

S. Lima L. Nonlinear Stochastic Equation within an Itô Prescription for Modelling of Financial Market. Entropy. 2019; 21(5):530. https://doi.org/10.3390/e21050530

Chicago/Turabian StyleS. Lima, Leonardo. 2019. "Nonlinear Stochastic Equation within an Itô Prescription for Modelling of Financial Market" Entropy 21, no. 5: 530. https://doi.org/10.3390/e21050530

APA StyleS. Lima, L. (2019). Nonlinear Stochastic Equation within an Itô Prescription for Modelling of Financial Market. Entropy, 21(5), 530. https://doi.org/10.3390/e21050530