4.3. Analysis of Research Results

We studied the effects of investor sentiment, information cognition, short-selling restrains, and their cross-variables on market liquidity. There are many factors that affect market liquidity: Mishkin [

46] indicated that an increase in interest rates and in uncertainty about the future direction of government policies promotes financial crises. Li and Peng [

47] proposed that investor sentiment and stock market liquidity are Granger reasons for economic growth. Ding [

48] showed that an M2 year-on-year growth rate had significant impact on the liquidity of China’s bond market. Therefore, we considered the following control variables: Riskfree interest rate, economic uncertainty index, CPI, economic sentiment index, and M2 year-on-year growth rate. All data came from the Wind database. The ADF test found that these variables were nonstationary, so we smoothed them with the methods of first-order difference, and named them

,

,

,

, and

, respectively. In addition, Yao [

16] showed two-way causality between investor sentiment and market liquidity. To prevent endogenous effects on the model results, hysteresis variable

was added, and variable

was standardized. The model was as follows:

The results showed that only two control variables were significant,

and

. It was found by the Ljung–Box test that there was autocorrelation of the residual sequence. Wooldridge pointed out the sequence correlation of the error of the dynamic model, usually due to the regression function not being completely set, and the hysteresis variable could be added at this time. Therefore, we modified the model to the following form:

Before the study, we performed an augmented Dickey–Fuller test (ADF for short) on the variables in the model. The results were shown in

Table 2:

The stationarity test of all variables was accepted. When we added

or

into the model, the model had multicollinearity. Therefore, the model was fitted through the sample data, and the results were shown in

Table 3:

In these models, the explanatory variables were independent because VIF values of the variables were less than 10, and the Ljung–Box test and ARCH-LM test showed that Residuals do not have autocorrelation, ARCH effect.

Model 1 shows that the coefficient of was significantly negative and the increase of investor sentiment enhanced market liquidity. The partial regression coefficient of to was significantly positive, implying that the faster the information perception is, the weaker the market liquidity. This is because perception of new information by noise investors is mostly insufficient in China’s stock market. At that time, high investor sentiment helped to promote transactions, and the improvement of investor information’s cognitive ability weakened stock market liquidity.

The margin-trading and short-selling business indicated that investors could borrow or sell short-term or short-selling transactions from other brokers, which directly affected the trading behavior of investors. In addition, investor-sentiment changes and information cognitive ability affect their expected returns and market liquidity through short-selling-restrained market behavior.

The results of Models 1 and 4 are similar, and we believed it was unlikely that the margin-trading and short-selling business had an impact on the relationship between investor sentiment and market liquidity.

Models 2, 3, and 5 show that the coefficient of in these models was significantly positive, contrary to the effect of on , which indicates that the margin-trading and short-selling business inhibits the positive impact of investor sentiment on market liquidity.

We needed to test the robustness and validity of the model. A different illiquidity measurement was used to test the robustness of the results. Here, we chose CSI 300 as the object, and the following indicators based on Huang and Yang [

12]. The price amplitude on the

i-th trading day of the

t-th week is:

where

is the open price of the day,

is the highest price of the day,

is the lowest price of the day,

is the trading price on the

i-th trading day of the

t-th week,

is the number of effective trading day for the

t-th week. If the price amplitude on the trading day is not zero, then it is a valid trading day. Then:

The probability of the ADF test for this

was 0.043, so it was stationary. We used the same control variables as above. When we only introduced

, if the residual had no autocorrelation, no higher-order lags were introduced.

could cause severe multicollinearity. After fitting the model with ordinary least squares, the residual had an ARCH effect; therefore, the ARCH equation must be constructed to eliminate conditional heteroscedasticity [

49]. The model results were in

Table 4, and there was no multicollinearity, residual autocorrelation, and conditional heteroscedasticity in these models.

The variable relationship reflected by the parameter results was consistent with Models 1–5. Investor sentiment had positive impact on market liquidity, while information cognitive ability had negative impact on market liquidity, and the development of margin trading curbed the positive impact of investor sentiment on market liquidity. Therefore, the results were robust.

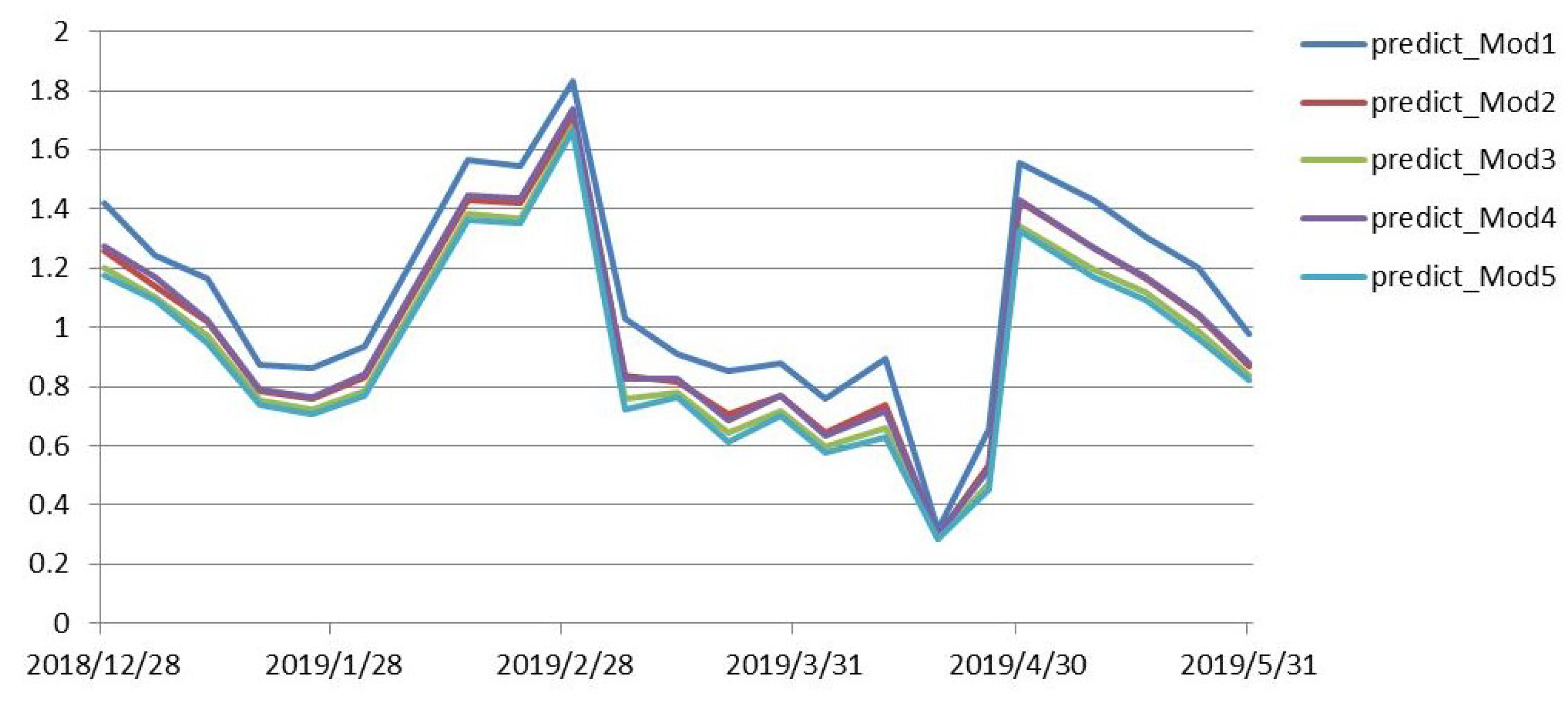

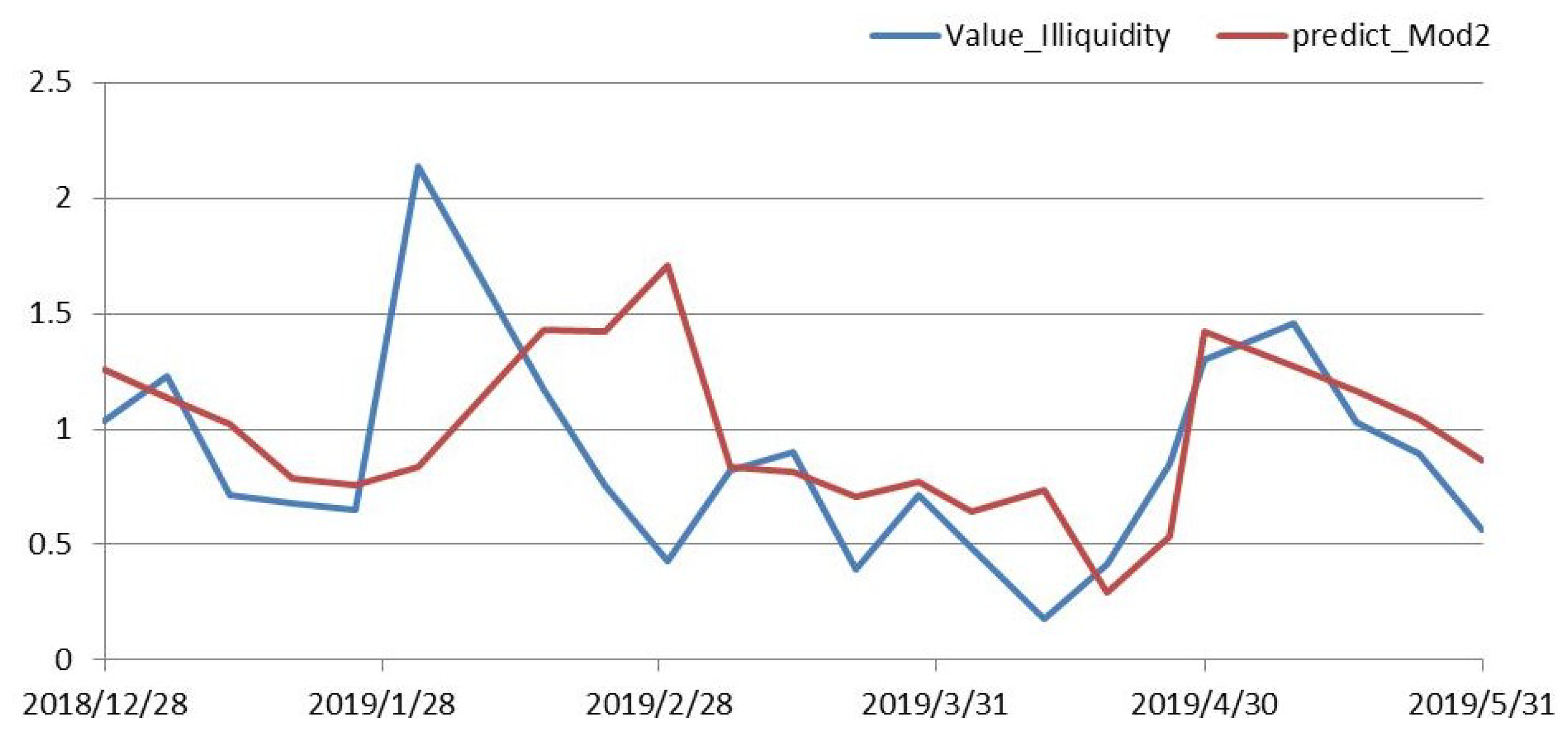

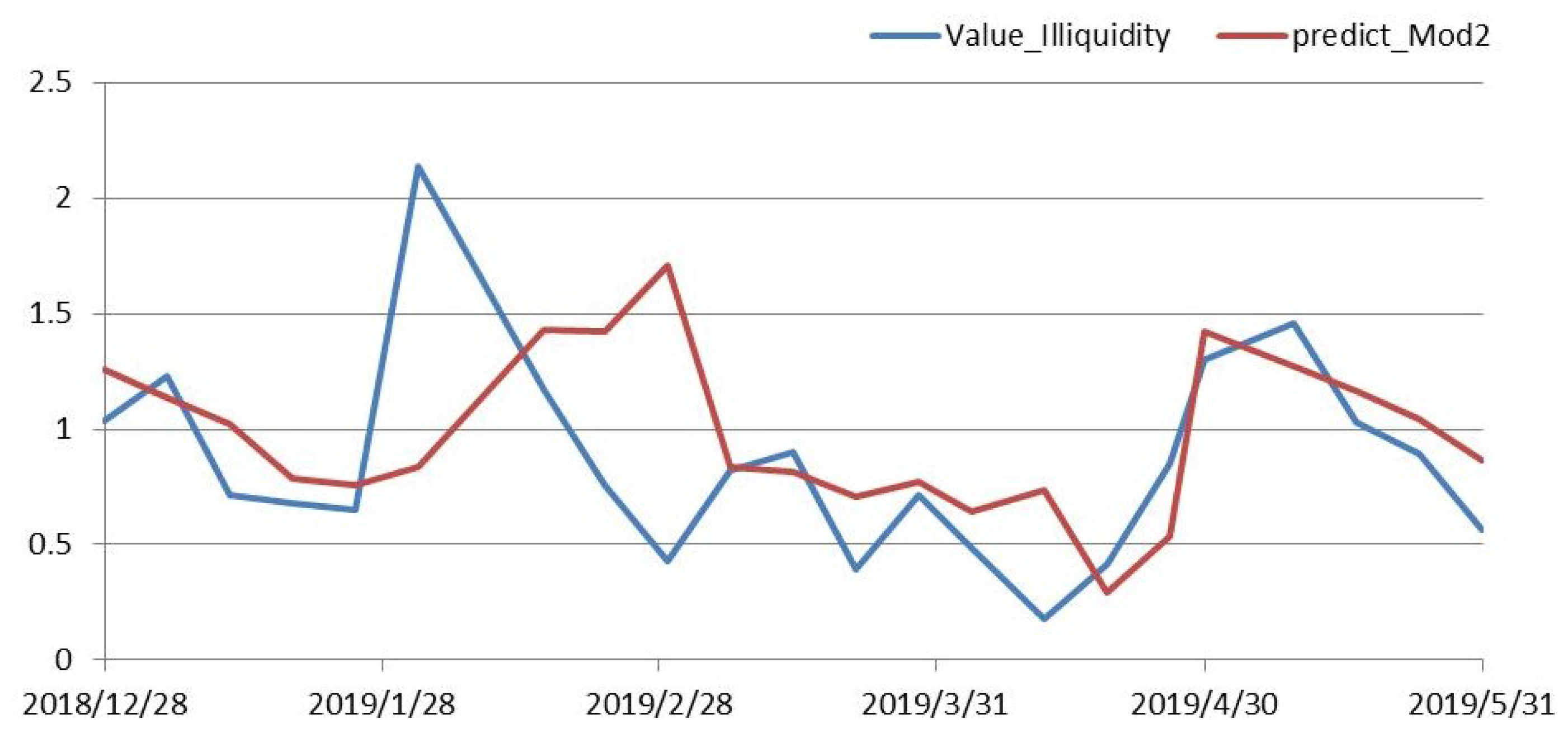

This was shown to determine the validity of the model, whether the predicted value of the model was consistent with the trend of the true value of illiquidity, and whether the predicted value fluctuated around the true-value data. In order to test the validity of the model, the illiquidity of the period was predicted based on market data from 24 December 2018 to 31 May 2019, and the predicted values and real-data charts were plotted as follows:

Figure 3 shows that the trend of the prediction results in the seven models was almost the same, except that the size of the predicted-value data was different. In all fitted models, Model 2 was significant with more variables. Comparing the results of Model 2 with the true value of illiquidity,

Figure 4 shows that the trend of the predicted-value data was similar with the true-value trends, and the predicted values fluctuated around the true value. It is obvious that the model had a good prediction effect, and could truly reflect the relationship between variables and market liquidity.

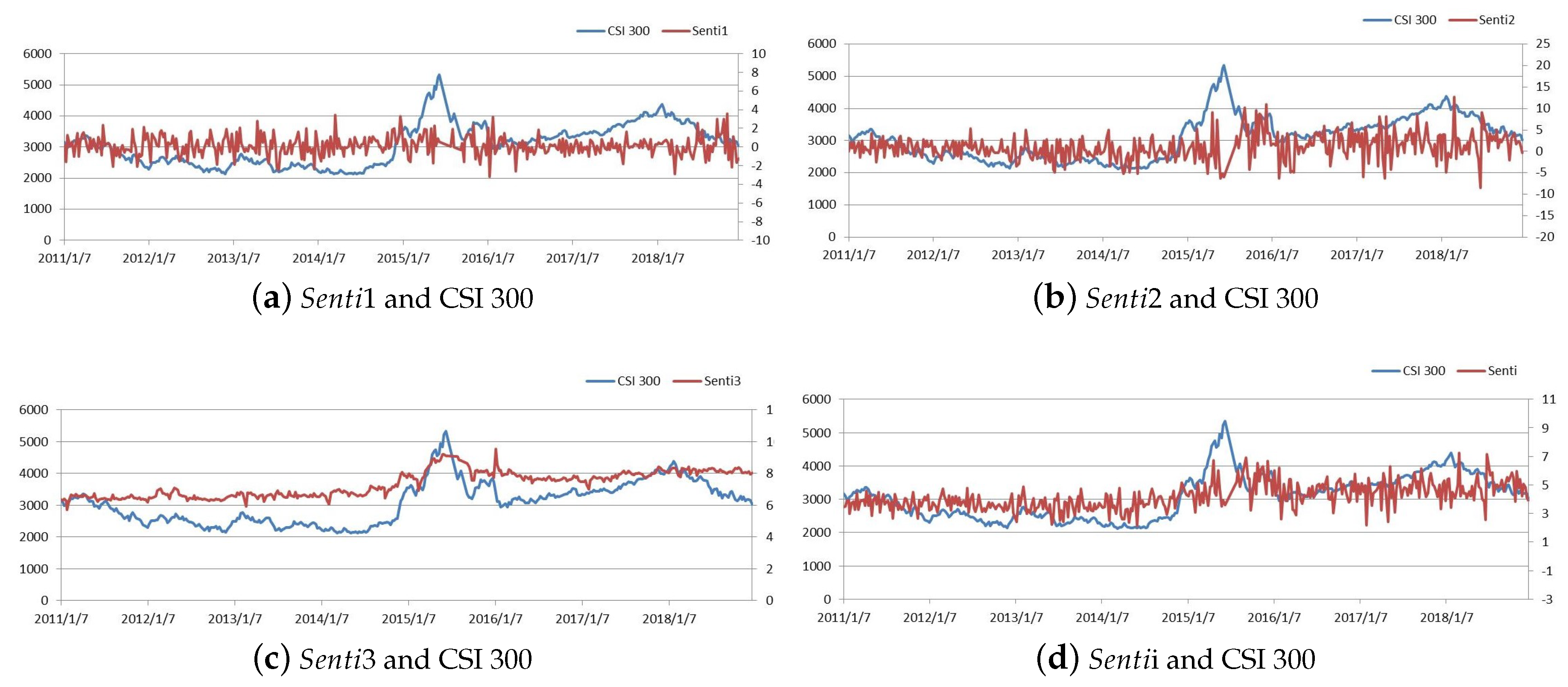

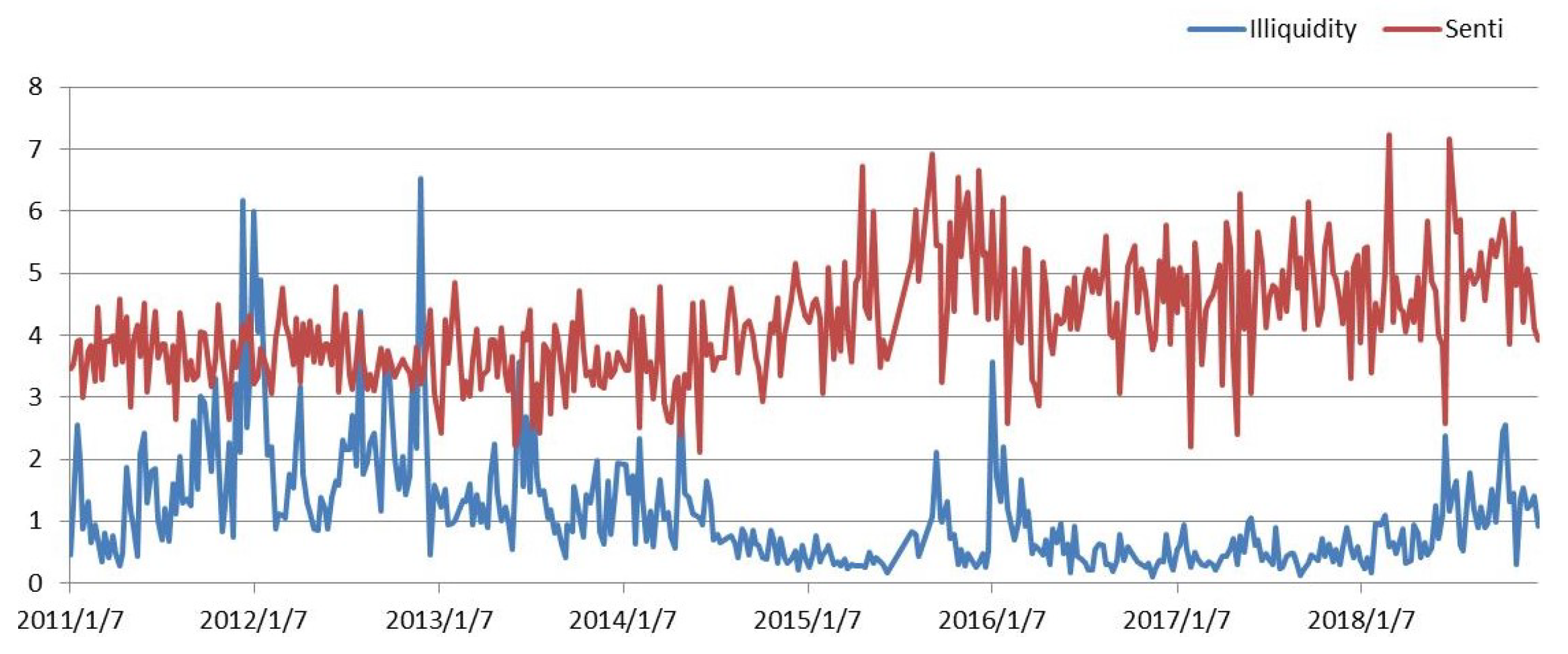

In the above, we used Baidu Index to construct investor sentiment index. In fact, Baidu Index was built by search-volume data of Baidu search engine, which can reflect the size of network information. Here, we use Baidu Index as the proxy variable of the amount of network information to study its impact on market liquidity,

was standardized. The empirical equation was as follows:

The ADF test for the cross-variables was in

Table 5. Results showed that they were all stationary:

The estimated results of the model are in

Table 6, and the VIF of the variables were less than 3, and the Ljung–Box test and ARCH-LM test were satisfied.

Nowadays, most people browse information from the network to grasp stock market dynamics, which affects their expectations and their investment decisions. Research shows that the coefficient is significantly negative, which indicates that explosive information volume of network information in bull market has a positive effect on stock market liquidity; the coefficient is significantly positive, indicating that there has a significant inhibitory effect in the bear market; the coefficient is not significant, meaning that there has no significant impact between the explosive information and market liquidity in the shock market. These results show that the amount of explosive information has an impact on the liquidity of the stock market, and this effect is heterogeneous. In the bull market, explosive-information volume is conducive to raising investment sentiment, thereby promoting market liquidity. In the bear market, it depresses investor sentiment and weakens market liquidity. There is no significant impact between them in the shock market.

We used a different illiquidity measurement for testing the robustness of the results. The results of the least-squares estimation had the ARCH effect, so an ARCH model was constructed. All models passed the Ljung–Box test and ARCH-LM test, and results were consistent with the above research results; the impact of explosive information on market liquidity was heterogeneous.

The empirical results in

Table 7 showed that investor sentiment had a positive impact on market liquidity. Investor perception of new information has negative impact on market liquidity, which indicates that most investors in the market are characterized by a lack of awareness and tend to generate follow-up trading behavior. As investor information cognitive ability increases, it lowers market liquidity. The margin-trading and short-selling business can restrain the positive impact of investor sentiment on market liquidity, and the impact of explosive information on market liquidity is heterogeneous.

{kind=link}

{kind=link}

{kind=link}

{kind=link}