Forecasting Sales in Live-Streaming Cross-Border E-Commerce in the UK Using the Temporal Fusion Transformer Model

Abstract

1. Introduction

- Enhanced Temporal Fusion Transformer (TFT): The introduction of novel prediction position encodings optimizes the capture of long-term dependencies and local features in the data.

- Multi-feature data integration: This study presents a forecasting framework that integrates various data types—historical sales, KOL influence, user behavior, and seasonal features—resulting in improved prediction accuracy.

- Improved Model Interpretability: The model incorporates concepts of long-term, medium-term, and short-term predictions, significantly enhancing the model’s interpretative capabilities and facilitating more optimized decision-making throughout the entire life cycle management of cross-border e-commerce.

- Industry Relevance: The proposed model offers cross-border e-commerce businesses a more effective tool to navigate the volatile market environment and enhance operational efficiency.

2. Theoretical Analysis of E-Commerce Demand Fluctuations

2.1. Demand Forecasting

2.2. Factors Influencing E-Commerce Live-Streaming Sales

2.2.1. Historical Data

2.2.2. Influence of Key Opinion Leaders (KOLs)

2.2.3. Seasonal Features

2.2.4. Weekend and Holiday Effects

3. Methodology

3.1. Data

3.1.1. Data Description

- Basic product information: This section includes product name, category, and description.

- Live-streaming content: This section provides information on the live-streaming session, including the start time, end time, title, duration, price, and total number of viewers.

3.1.2. Data Cleaning

3.2. Key Factors Influencing Prediction

3.2.1. Live-Streaming Sales Features

- Original Sales (Sale): The historical sales data, denoted as Sale, serve as the primary indicator of fundamental sales trends over time.

- Log Sales (Log_sale): The natural logarithm of sales data (Log_sale) is employed to smooth fluctuations and reduce the influence of extreme values. To prevent computational issues with zero-valued sales, a small constant () is added.

- Average Sales by Product ID (Average_Sale_by_ID): The average sales performance for each product ID is calculated as shown in Equation (1):where represents the total number of records for product ID i, and denotes the sales value of the j-th record.

3.2.2. Key Opinion Leader (KOL) Features

- Live Streaming Price (Price): Prices are standardized using the exchange rate r, converting the original price p into USD, as shown in Equation (2):

- Number of Viewers (Views): Reflects the real-time audience size during a live stream, serving as a proxy for the KOL’s influence on sales.

3.2.3. Time Features

- Time Index (Time_idx): Represents the chronological sequence of records, ordered by time and product category.

- Relative Time Index (Relative_Time_idx): Denotes the position of the current time point relative to the sequence.

- Seasonality (Seasonality): Seasonal trends, particularly prominent for products such as sunscreen, are captured using the month of the transaction as shown in Equation (6):

3.2.4. Weekend and Holiday Effects

- Weekend Effect (Weekend): Indicates whether a record corresponds to a weekend:

- Holiday Effect (Holiday): Captures the effects of national and cultural holidays:

3.3. Model Design

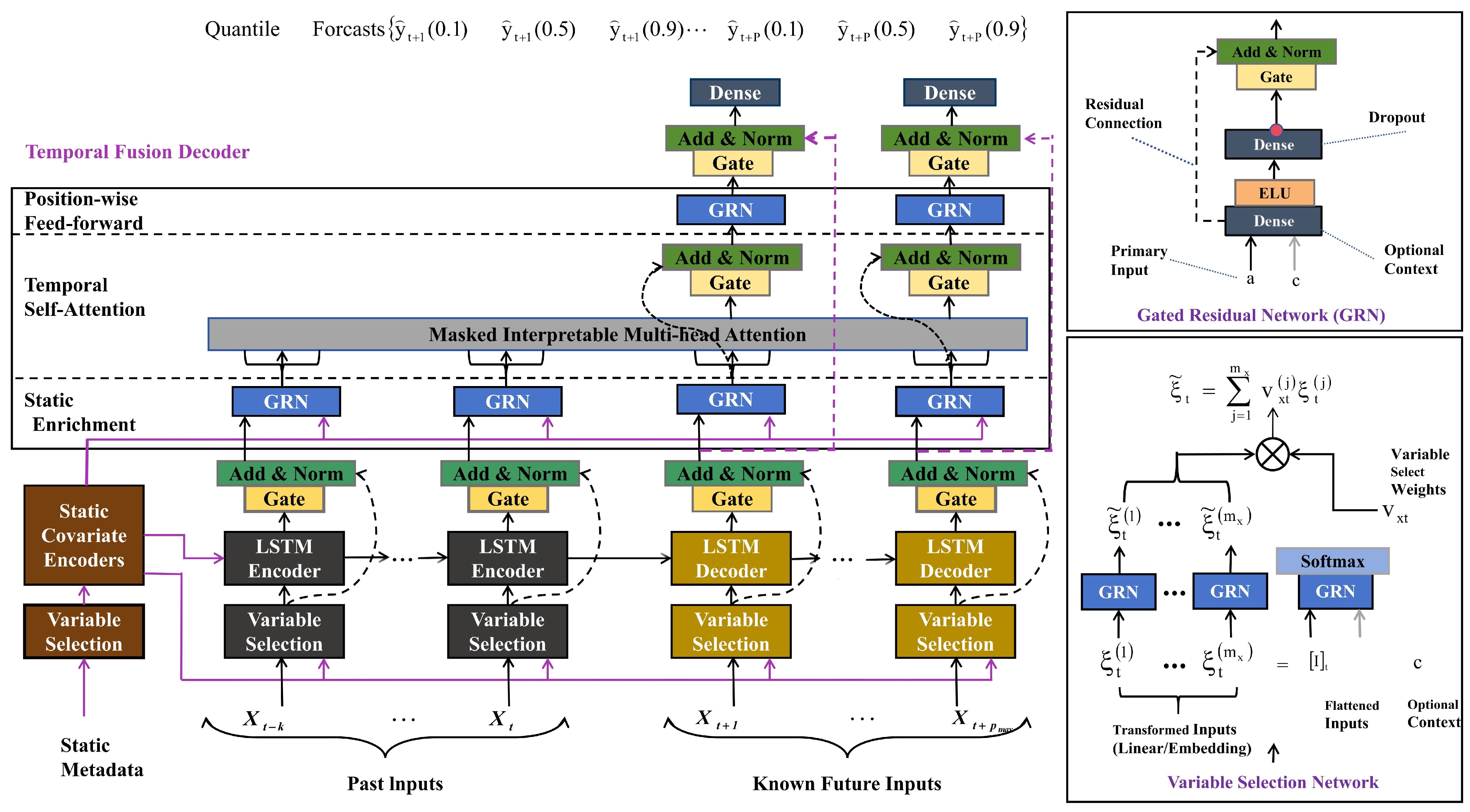

3.3.1. Temporal Fusion Transformer (TFT) Model

- A fixed-length look-back window k, capturing historical target values ;

- Known inputs , spanning both retrospective and prospective intervals;

- Observed inputs , constrained to measurements preceding the forecast time t.

- Identity behavior: When

- Saturated constant output: When , inducing linear projection

- Locality enhancement with sequence-to-sequence layer: In a time series, the value of a point is closely related to its surrounding values. This study uses a sequence-to-sequence model to capture local dependencies. The gated skip connection is used as the input layer of the temporal fusion decoder as shown in Equation (24), where t is the time point and n is the position index.We propose the application of a sequence-to-sequence layer to naturally handle these differences—feeding into the encoder and into the decoder. This then generates a set of uniform temporal features that serve as inputs into the temporal fusion decoder itself, denoted by with n being a position index.

- Static enrichment layer: Encodes the influence of static variables and generates context-enhanced static information (Equation (25)):where the weights of are shared across the entirelayer, and is a context vector from a static covariateencoder.

- Temporal self-attention layer: Temporal features learn long- and short-term dependencies through the self-attention mechanism, with the addition of a gating layer as shown in Equations (26) and (27):All static-enriched temporal features are first grouped into a single matrix—i.e., —and interpretable multi-head attention is applied at each forecast time (with ). The attention dimensions are set as , where is the number of heads.

- Position-wise feed-forward layer: Integrates multi-layer outputs to generate the final prediction as shown in Equations (28)–(30):Let and denote the linear coefficients associated with quantile q. Forecasts are generated for future horizons . The parameters of are shared across the layer.

3.3.2. Forecasting Framework

3.4. Comparative Model

3.4.1. LSTM Model

- Forget Gate: This gate determines how much past information should be forgotten at the current time step, as shown in Equation (32).

- Input Gate: The Input Gate determines the new information at the current moment, as shown in Equation (33).

- Output Gate: The Output Gate determines the output information (Equation (34)).and are weight parameters, and are bias parameters.

- denotes the predicted future sales volume;

- and denote the hidden and memory cell states at time step i.

3.4.2. GRU Model

3.4.3. CNN Model

- T represents the number of time steps (length of the time series).

- N represents the spatial dimension of product features (such as sales volume, price, kol, etc.).

- is the feature map from the previous layer, initially set as the input data .

- is the convolution kernel of layer l.

- is the bias term.

- is the nonlinear activation function, such as ReLU.

- transforms the feature map into a one-dimensional vector.

- represents the weight matrix of the fully connected layer.

- is the bias term of the fully connected layer.

- denotes the final activation function, which can be a linear mapping or a nonlinear function such as ReLU.

- This layer integrates the extracted features and learns complex relationships between them to generate the final sales prediction output.

3.4.4. ARIMA Model

- p: Order of the autoregressive component, representing the number of lagged observations.

- d: Degree of difference required to achieve stationarity.

- q: Order of the moving average component, reflecting the influence of past forecast errors.

3.5. Model Hyperparameter Tuning

3.6. Evaluation Metrics

4. Experimental Results

4.1. Performance Evaluation

4.1.1. Temporal Fusion Transformers (TFT)

- Attention Mechanism: Effectively captures long-term and short-term temporal dependencies, adapting to complex time series patterns.

- Multivariate Capability: Adept at handling the combined influence of multiple factors such as promotional activities, seasonal variations, and user behavior, which are prevalent in cross-border e-commerce.

- Stability: Demonstrates robust performance with minimal error fluctuations across different prediction periods.

4.1.2. Long Short-Term Memory (LSTM) and Gated Recurrent Units (GRU)

4.1.3. Convolutional Neural Networks (CNN)

4.1.4. Autoregressive Integrated Moving Average (ARIMA)

- Linear Assumption: ARIMA assumes linear relationships in time series, failing to capture non-linear fluctuations in live stream sales (e.g., sudden traffic surges, user interactions).

- Insufficient Multivariate Support: Supports only univariate predictions, limiting its ability to integrate multidimensional features.

4.2. Model Metrics and Risk Early Warning

4.2.1. Practical Implications of MAE in Predictive Modeling

4.2.2. Practical Implications of RMSE in Predictive Modeling

4.2.3. Practical Implications of MSE in Predictive Modeling

4.3. Model Prediction Results

4.4. Model Interpretability

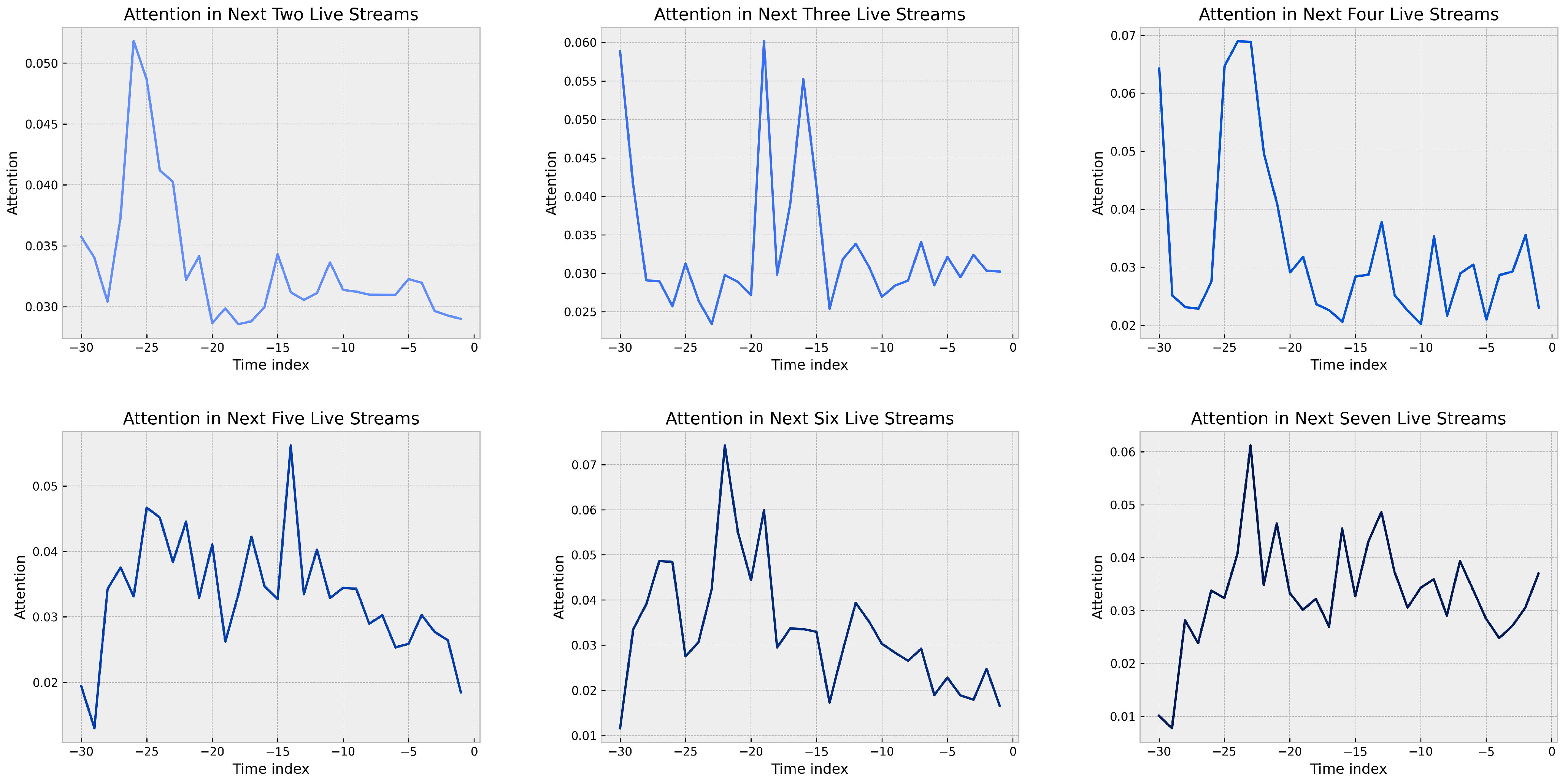

4.4.1. Attention

- Short-term forecast (2–3 steps): The model places more emphasis on older historical data (−30 to −25 periods) to capture long-term trends that are critical for short-term forecasts. The focus on recent data is reduced, reflecting the model’s reliance on established patterns rather than immediate fluctuations.

- Medium-term forecast (4–5 steps): The attention weights are more evenly distributed, peaking between −15 and −10 periods while remaining sensitive to earlier trends. This balance suggests that the model considers short-term fluctuations and broader sales trends.

- Long-term forecast (steps 6–7): The shift in focus to the −25 to −20 period shows that the model focuses on medium-term trends and reduces reliance on recent data. This highlights the model’s ability to capture cyclical patterns and maintain long-term sales forecasts.

4.4.2. Importance of Static Variables

- Product Category (ID): The importance of this feature varies across different forecast horizons. A higher value indicates a stronger influence on the prediction.

- Encoder Length (Encoder_Length): The length of the input time series significantly impacts prediction accuracy. The varying importance across different forecast horizons suggests that the relevance of historical data changes with the prediction time frame.

- Sales Center (Sale_Center): Representing the central tendency of historical sales data (e.g., mean or median), this feature’s importance fluctuates, indicating its varying contribution to predictions at different horizons.

- Sales Scale (Sale_Scale): This feature reflects the range or dispersion of historical sales data and its influence on the target variable prediction.

4.4.3. Dynamic Feature Weights in Multi-Horizon Forecasting

4.4.4. Importance of Different Features

4.5. Commercial Applications of Model Interpretability

4.5.1. Spatiotemporal Optimization of Marketing Budgets

4.5.2. Three-Tier Responsive Mechanism for Dynamic Inventory Management

- Execute capacity framework agreements aligned with long-term trends while adjusting overseas warehouse baseline inventory through seasonality indices;

- Initiate prelaunch phases 6–7 weeks preceding major promotional seasons (e.g., Christmas/Black Friday), with inventory replenishment timelines determined through backward scheduling from customs clearance cycles.

4.5.3. Feedback Control System for Real-Time Decision-Making

5. Conclusions

- Static Features: The importance of static features varies significantly in different forecast periods. This result inspires subsequent research. The weight changes of static features in different prediction periods should be fully considered when constructing a cross-border e-commerce live broadcast prediction model.

- KOL Features: In contrast, the duration of live streams has a weaker impact on sales forecasting because consumers pay more attention to the quality and interactivity of the live stream content. This study further enriches the theoretical explanation of the spillover effects of KOLs on live marketing [45,49], revealing the critical role of KOLs from a new perspective of the product marketing cycle and utilizing the interpretability of TFT models to make the mechanism of influence of KOLs more straightforward.

- Time-Series Features: Time index (Time_idx) and periodic features (e.g., Week_sin, Week_cos) contribute significantly to the prediction of medium and short-term sales, indicating that periodic factors have a significant impact in the short term. In contrast, seasonal features and relative time index become significantly more important in long-term forecasting, showing the key role of seasonal variations and long-term trends in long-term sales forecasting. This conclusion further verifies the importance of time features (such as seasonal factors) in sales forecasting [51,52,54].

- Short-term forecasting (step size = 2 to 3): The model primarily relies on static features such as the average product ID sales and the sequential time series information.

- Medium-term forecasting (step size = 4 to 5): The model depends more on the volatility of historical sales data, periodic features, and the impact of holidays and weekends.

- Long-term forecasting (step size = 6 to 7): In the long-term forecast, the importance of smoothed sales data (Log_sale) and seasonal features increases significantly, indicating that the model relies more on stable signals in capturing long-term trends.

6. Limitations and Future Research

6.1. Limitations

6.2. Future Directions

6.2.1. Enhanced Modeling of KOL Features

6.2.2. Integration of Regional Features

6.2.3. Integration of Category Features

6.2.4. Extension to Multimodal Data Integration

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Zhang, X.; Zha, X.; Dan, B.; Liu, Y.; Sui, R. Logistics Mode Selection and Information Sharing in a Cross-Border e-Commerce Supply Chain with Competition. Eur. J. Oper. Res. 2024, 314, 136–151. [Google Scholar] [CrossRef]

- Chen, S.; Ke, S.; Han, S.; Gupta, S.; Sivarajah, U. Which Product Description Phrases Affect Sales Forecasting? An Explainable AI Framework by Integrating WaveNet Neural Network Models with Multiple Regression. Decis. Support Syst. 2024, 176, 114065. [Google Scholar] [CrossRef]

- APAC Regulatory & Legal Salary Guide. Available online: https://www.larsonmaddox.com/regulatory-and-legal-salary-guide-compensation-benchmarking-in-key-industries-across-APAC (accessed on 1 January 2024).

- Derindag, O.F.; Yasar, Z.R.; Aslan, C.; Parmaksiz, S. Analyzing the differential effects of COVID-19 on export flows: A focus on customs procedures. Empirica 2024, 51, 977–1000. [Google Scholar] [CrossRef]

- Aslan, C.; Derindag, O.F.; Parmaksiz, S. Effects of cross-border E-commerce customs declaration ceiling increase on export performance under COVID-19 conditions. Kybernetes 2024, 53, 3348–3364. [Google Scholar] [CrossRef]

- Roscoe, S.; Skipworth, H.; Aktas, E.; Habib, F. Managing Supply Chain Uncertainty Arising from Geopolitical Disruptions: Evidence from the Pharmaceutical Industry and Brexit. Int. J. Oper. Prod. Manag. 2020, 40, 1499–1529. [Google Scholar] [CrossRef]

- Queiroz, M.M.; Fosso Wamba, S.; Chiappetta Jabbour, C.J.; Machado, M.C. Supply Chain Resilience in the UK during the Coronavirus Pandemic: A Resource Orchestration Perspective. Int. J. Prod. Econ. 2022, 245, 108405. [Google Scholar] [CrossRef]

- Ma, J.; Chen, J.; Zhang, G.; Chen, S. Online Opinion Leadership Styles and Purchase Intention in Livestreaming E-Commerce. Serv. Ind. J. 2024, 1–27. [Google Scholar] [CrossRef]

- Pappas, N. UK Outbound Travel and Brexit Complexity. Tour. Manag. 2019, 72, 12–22. [Google Scholar] [CrossRef]

- Trade, Migration and Brexit. Available online: https://ukandeu.ac.uk/trade-migration-and-brexit/ (accessed on 25 October 2022).

- Qian, L. The Global Imperative: Chinese Cross-Border E-Commerce and Its Political-Economic Implications in a Deglobalising World. Asian Stud. Rev. 2024, 48, 828–846. [Google Scholar] [CrossRef]

- Xu, Y.; Zeng, K.; Guo, J.; Li, X.; Dong, L.; Jiang, W. Whether Live Streaming Has a Better Performance? An Examination of Product Presentation Modes on Cross-Border E-Commerce Platform. Int. J. Hum.-Comput. Interact. 2023, 41, 69–84. [Google Scholar] [CrossRef]

- Gong, H.; Zhao, M.; Ren, J.; Hao, Z. Live Streaming Strategy under Multi-Channel Sales of the Online Retailer. Electron. Commer. Res. Appl. 2022, 55, 101184. [Google Scholar] [CrossRef]

- Zhang, W.; Liu, C.; Ming, L.; Cheng, Y. The sales impacts of traffic acquisition promotion in live-streaming commerce. Prod. Oper. Manag. 2022, 10591478231224938. [Google Scholar] [CrossRef]

- Xu, W.; Cao, Y.; Chen, R. A multimodal analytics framework for product sales prediction with the reputation of anchors in live streaming e-commerce. Decis. Support Syst. 2024, 177, 114104. [Google Scholar] [CrossRef]

- Lu, B.; Chen, Z. Live streaming commerce and consumers’ purchase intention: An uncertainty reduction perspective. Inf. Manag. 2021, 58, 103509. [Google Scholar] [CrossRef]

- Frontiers | How Live Streaming Features Impact Consumers’ Purchase Intention in the Context of Cross-Border E-Commerce? A Research Based on SOR Theory. Available online: https://www.frontiersin.org/journals/psychology/articles/10.3389/fpsyg.2021.767876/full (accessed on 4 January 2025).

- Alabdulrazzaq, H.; Alenezi, M.N.; Rawajfih, Y.; Alghannam, B.A.; Al-Hassan, A.A.; Al-Anzi, F.S. On the Accuracy of ARIMA Based Prediction of COVID-19 Spread. Results Phys. 2021, 27, 104509. [Google Scholar] [CrossRef]

- Wang, X.; Kang, Y.; Hyndman, R.J.; Li, F. Distributed ARIMA models for ultra-long time series. Int. J. Forecast. 2023, 39, 1163–1184. [Google Scholar] [CrossRef]

- Lu, S. Research on GDP forecast analysis combining BP neural network and ARIMA model. Comput. Intell. Neurosci. 2021, 2021, 1026978. [Google Scholar] [CrossRef]

- Kim, S.; Choi, C.Y.; Shahandashti, M.; Ryu, K.R. Improving accuracy in predicting city-level construction cost indices by combining linear ARIMA and nonlinear ANNs. J. Manag. Eng. 2022, 38, 04021093. [Google Scholar] [CrossRef]

- He, Q.Q.; Wu, C.; Si, Y.W. LSTM with particle swarm optimization for sales forecasting. Electron. Commer. Res. Appl. 2022, 51, 101118. [Google Scholar] [CrossRef]

- Wu, H. Predicting e-commerce product prices through the integration of variational mode decomposition and deep neural networks. PeerJ Comput. Sci. 2024, 10, e2353. [Google Scholar] [CrossRef]

- Lim, B.; Arık, S.Ö.; Loeff, N.; Pfister, T. Temporal fusion transformers for interpretable multi-horizon time series forecasting. Int. J. Forecast. 2021, 37, 1748–1764. [Google Scholar] [CrossRef]

- Wang, Y.; Jia, F.; Schoenherr, T.; Chen, L. Cross-border e-commerce firms as supply chain integrators: The management of three flows. Ind. Mark. Manag. 2020, 89, 72–88. [Google Scholar] [CrossRef]

- Lin, Q.; Jia, N.; Chen, L.; Zhong, S.; Yang, Y.; Gao, T. A two-stage prediction model based on behavior mining in livestream e-commerce. Decis. Support Syst. 2023, 174, 114013. [Google Scholar] [CrossRef]

- Wu, H.; Qiao, Y.; Luo, C. Cross-border e-commerce, trade digitisation and enterprise export resilience. Financ. Res. Lett. 2024, 65, 105513. [Google Scholar] [CrossRef]

- Koutsandreas, D.; Spiliotis, E.; Petropoulos, F.; Assimakopoulos, V. On the selection of forecasting accuracy measures. J. Oper. Res. Soc. 2022, 73, 937–954. [Google Scholar] [CrossRef]

- Muthukalyani, A.R. Unlocking accurate demand forecasting in retail supply chains with AI-driven predictive analytics. Inf. Technol. Manag. 2023, 14, 48–57. [Google Scholar]

- Cheba, K.; Kiba-Janiak, M.; Baraniecka, A.; Kołakowski, T. Impact of external factors on e-commerce market in cities and its implications on environment. Sustain. Cities Soc. 2021, 72, 103032. [Google Scholar] [CrossRef]

- Daniel, C.; Hernandez, T. What retail apocalypse? A Delphi forecast of commercial space demand in the Toronto region. J. Retail. Consum. Serv. 2024, 77, 103670. [Google Scholar] [CrossRef]

- Cai, W.; Song, Y.; Wei, Z. Multimodal Data Guided Spatial Feature Fusion and Grouping Strategy for E-Commerce Commodity Demand Forecasting. Mob. Inf. Syst. 2021, 2021, 5568208. [Google Scholar] [CrossRef]

- Li, Z.; Zhang, N. Short-Term Demand Forecast of E-Commerce Platform Based on ConvLSTM Network. Comput. Intell. Neurosci. 2022, 2022, 5227829. [Google Scholar] [CrossRef]

- Zhang, B.; Tseng, M.L.; Qi, L.; Guo, Y.; Wang, C.H. A comparative online sales forecasting analysis: Data mining techniques. Comput. Ind. Eng. 2023, 176, 108935. [Google Scholar] [CrossRef]

- Suryawan, I.G.T.; Putra, I.K.N.; Meliana, P.M.; Sudipa, I.G.I. Performance Comparison of ARIMA, LSTM, and Prophet Methods in Sales Forecasting. Sink. J. Tek. Inform. 2024, 8, 2410–2421. [Google Scholar] [CrossRef]

- Dhankhar, S.; Dhankhar, N.; Sandhu, V.; Mehla, S. Forecasting Electric Vehicle Sales with ARIMA and Exponential Smoothing Method: The Case of India. Transport. Dev. Econ. 2024, 10, 32. [Google Scholar] [CrossRef]

- Elalem, Y.K.; Maier, S.; Seifert, R.W. A machine learning-based framework for forecasting sales of new products with short life cycles using deep neural networks. Int. J. Forecast. 2023, 39, 1874–1894. [Google Scholar] [CrossRef]

- Xie, L.; Liu, J.; Wang, W. Predicting sales and cross-border e-commerce supply chain management using artificial neural networks and the Capuchin search algorithm. Sci. Rep. 2024, 14, 13297. [Google Scholar] [CrossRef]

- Chen, Y.; Xie, X.; Pei, Z.; Yi, W.; Wang, C.; Zhang, W.; Ji, Z. Development of a Time Series E-Commerce Sales Prediction Method for Short-Shelf-Life Products Using GRU-LightGBM. Appl. Sci. 2024, 14, 866. [Google Scholar] [CrossRef]

- Bhatt, S.; Ghazanfar, M.; Amirhosseini, M. Machine learning based cryptocurrency price prediction using historical data and social media sentiment. Comput. Sci. Inf. Technol. 2023, 13, 1–11. [Google Scholar]

- Pongdatu, G.A.N.; Putra, Y.H. Seasonal time series forecasting using sarima and holt winter’s exponential smoothing. IOP Conf. Ser. Mater. Sci. Eng. 2018, 407, 012153. [Google Scholar] [CrossRef]

- Zhuang, Q.; Zhang, X.; Wang, P.; Deng, B.; Pan, H. A neural network model for China B2C e-commerce sales forecast based on promotional factors and historical data. In Proceedings of the 2019 International Conference on Economic Management and Model Engineering (ICEMME), Malacca, Malaysia, 6–8 December 2019; pp. 307–312. [Google Scholar]

- Liu, J.; Liu, C.; Zhang, L.; Xu, Y. Research on sales information prediction system of e-commerce enterprises based on time series model. Inf. Syst. e-Bus. Manag. 2020, 18, 823–836. [Google Scholar] [CrossRef]

- Chen, J.; Lan, Y.C.; Chang, Y.W. Consumer behaviour in cross-border e-commerce: Systematic literature review and future research agenda. Int. J. Consum. Stud. 2023, 47, 2609–2669. [Google Scholar] [CrossRef]

- He, P.; Shang, Q.; Pedrycz, W.; Chen, Z.S. Short video creation and traffic investment decision in social e-commerce platforms. Omega 2024, 128, 103129. [Google Scholar] [CrossRef]

- Niu, B.; Yu, X.; Dong, J. Could AI livestream perform better than KOL in cross-border operations? Transp. Res. Part E Logist. Transp. Rev. 2023, 174, 103130. [Google Scholar] [CrossRef]

- Zhang, H.; Sui, R.; Zha, X. The key opinion leader introduction and pricing strategy for live streaming e-commerce platforms considering the impact of network effects. J. Retail. Consum. Serv. 2025, 82, 104077. [Google Scholar] [CrossRef]

- He, W.; Jin, C. A study on the influence of the characteristics of key opinion leaders on consumers’ purchase intention in live streaming commerce: Based on dual-systems theory. Electron. Commer. Res. 2024, 24, 1235–1265. [Google Scholar] [CrossRef]

- Lin, X.; Gui, L.; Lu, Y. Managing sales via livestream commerce: Implications of price negotiation and consumer price search. Prod. Oper. Manag. 2024, 10591478231224930. [Google Scholar] [CrossRef]

- Xiong, L.; Cho, V.; Law, K.M.Y.; Lam, L. A study of KOL effectiveness on brand image of skincare products. Enterp. Inf. Syst. 2021, 15, 1483–1500. [Google Scholar] [CrossRef]

- Moorthi, K.; Srihari, K.; Karthik, S. Improving business process by predicting customer needs based on seasonal analysis: The role of big data in e-commerce. Int. J. Bus. Excell. 2020, 20, 561–574. [Google Scholar] [CrossRef]

- Liu, X.; Zhou, Y.W.; Shen, Y.; Ge, C.; Jiang, J. Zooming in the impacts of merchants’ participation in transformation from online flash sale to mixed sale e-commerce platform. Inf. Manag. 2021, 58, 103409. [Google Scholar] [CrossRef]

- Fathalla, A.; Salah, A.; Li, K.; Li, K.; Francesco, P. Deep end-to-end learning for price prediction of second-hand items. Knowl. Inf. Syst. 2020, 62, 4541–4568. [Google Scholar] [CrossRef]

- Kharfan, M.; Chan, V.W.K.; Firdolas Efendigil, T. A data-driven forecasting approach for newly launched seasonal products by leveraging machine-learning approaches. Ann. Oper. Res. 2021, 303, 159–174. [Google Scholar] [CrossRef]

- Zhao, Y. Research on E-Commerce Retail Demand Forecasting Based on SARIMA Model and K-means Clustering Algorithm. Acad. J. Sci. Technol. 2024, 10, 226–231. [Google Scholar] [CrossRef]

- Tran, D.T.; Huh, J.H. Forecast of seasonal consumption behavior of consumers and privacy-preserving data mining with new S-Apriori algorithm. J. Supercomput. 2023, 79, 12691–12736. [Google Scholar] [CrossRef]

- Deng, L.; Ye, Q.; Xu, D.; Sun, F. The “holiday effect” in consumer satisfaction: Evidence from review ratings. Inf. Manag. 2023, 60, 103863. [Google Scholar] [CrossRef]

- Bir, C.L.; Widmar, N.J.O.; Davis, M.K.; Erasmus, M.A.; Zuelly, S. Willingness to pay for whole turkey attributes during Thanksgiving holiday shopping in the United States. Poult. Sci. 2020, 99, 2798–2810. [Google Scholar] [CrossRef]

- Zane, D.M.; Reczek, R.W.; Haws, K.L. Promoting pi day: Consumer response to special day-themed sales promotions. J. Consum. Psychol. 2022, 32, 652–663. [Google Scholar] [CrossRef]

- Namin, A.; Dehdashti, Y. A “hidden” side of consumer grocery shopping choice. J. Retail. Consum. Serv. 2019, 48, 16–27. [Google Scholar] [CrossRef]

- Ahlbom, C.P.; Roggeveen, A.L.; Grewal, D.; Nordfält, J. Understanding how music influences shopping on weekdays and weekends. J. Mark. Res. 2023, 60, 987–1007. [Google Scholar] [CrossRef]

- Du, J.; Zhu, L.; Ma, Y.; Zhang, Y. Beyond weekdays: The impact of the weekend effect on eWOM of hedonic product. J. Retail. Consum. Serv. 2024, 77, 103624. [Google Scholar] [CrossRef]

- Agarwal, S.; Bubna, A.; Lipscomb, M. Timing to the statement: Understanding fluctuations in consumer credit use. Manag. Sci. 2021, 67, 5124–5144. [Google Scholar] [CrossRef]

- West, C.; Mogilner, C.; DeVoe, S.E. Happiness from treating the weekend like a vacation. Soc. Psychol. Personal. Sci. 2021, 12, 346–356. [Google Scholar] [CrossRef]

- Xie, V.; Bagchi, R. How duration of storage affects food waste behavior. J. Consum. Psychol. 2024, 34, 570–587. [Google Scholar] [CrossRef]

- Soukhovolsky, V.; Kovalev, A.; Pitt, A.; Shulman, K.; Tarasova, O.; Kessel, B. The cyclicity of coronavirus cases: “Waves” and the “weekend effect”. Chaos Solitons Fractals 2021, 144, 110718. [Google Scholar] [CrossRef] [PubMed]

- Akiba, T.; Sano, S.; Yanase, T.; Ohta, T.; Koyama, M. Optuna: A next-generation hyperparameter optimization framework. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, Anchorage, AK, USA, 4–8 August 2019; pp. 2623–2631. [Google Scholar]

- Vaswani, A. Attention is all you need. Adv. Neural Inf. Process. Syst. 2017, 30. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Field | Example |

|---|---|

| Country | British |

| Id | 1729399984946253384 |

| Category | Beauty and skincare |

| Price | USD 19.11 |

| KOL name | @adaslifestyleb |

| Number of fans | 12,000 |

| Sale | 36 |

| Live streaming start time | 1 June 2024 14:05:11 |

| Live streaming end time | 1 June 2024 17:55:53 |

| Live streaming title | Time to do my nails |

| Live streaming duration | 3 h 50 m |

| Number of viewers | 17,906 |

| Product Description | L’Oreal Skincare & Comfort Revitalift Filler |

| Hyaluronic Acid & Caffeine Revitalift Eye Serum, | |

| Filler Plumping Water Cream, Anti-Wrinkle Dropper | |

| Serum Paradise Glotion Glow, Select your Type |

| Horizon Size | Learning Rate | Dropout Rate | Gradient Clip | Hidden Size | Continuous Size | Attention Heads |

|---|---|---|---|---|---|---|

| Live T2 | 0.02799 | 0.21330 | 0.01109 | 17 | 9 | 4 |

| Live S3 | 0.00414 | 0.13253 | 0.07409 | 53 | 8 | 4 |

| Live S4 | 0.01403 | 0.13951 | 0.07803 | 47 | 10 | 3 |

| Live S5 | 0.00107 | 0.21212 | 0.78937 | 83 | 47 | 2 |

| Live S6 | 0.00466 | 0.13864 | 0.78735 | 44 | 15 | 2 |

| Live S7 | 0.00409 | 0.13725 | 0.01586 | 36 | 8 | 2 |

| Short-Term Forecast | Medium-Term Forecast | Long-Term Forecast | Mean | |||||

|---|---|---|---|---|---|---|---|---|

| Size 2 | Size 3 | Size 4 | Size 5 | Size 6 | Size 7 | |||

| MAE | TFT | 2.371 | 2.420 | 2.949 | 2.747 | 2.798 | 2.323 | 2.704 |

| LSTM | 4.701 | 4.852 | 4.954 | 5.258 | 3.978 | 4.985 | 4.794 | |

| GRU | 4.701 | 4.027 | 3.871 | 4.269 | 4.313 | 4.426 | 4.120 | |

| CNN | 4.456 | 4.295 | 5.333 | 5.175 | 4.803 | 5.648 | 5.240 | |

| ARIMA | 18.90 | 17.45 | 17.80 | 15.70 | 14.78 | 14.33 | 15.65 | |

| RMSE | TFT | 2.944 | 2.571 | 3.650 | 3.130 | 3.269 | 2.941 | 3.248 |

| LSTM | 8.901 | 8.960 | 9.434 | 10.20 | 8.194 | 9.284 | 9.278 | |

| GRU | 9.412 | 7.344 | 7.579 | 8.098 | 8.139 | 8.678 | 20.46 | |

| CNN | 7.878 | 6.787 | 9.336 | 8.660 | 8.897 | 10.44 | 9.333 | |

| ARIMA | 20.33 | 20.93 | 21.39 | 19.43 | 18.31 | 17.81 | 19.24 | |

| MSE | TFT | 8.669 | 6.611 | 13.32 | 9.798 | 10.68 | 8.652 | 10.61 |

| LSTM | 79.23 | 80.28 | 89.00 | 104.0 | 67.14 | 86.19 | 86.58 | |

| GRU | 88.58 | 53.94 | 57.44 | 65.59 | 66.26 | 75.30 | 51.65 | |

| CNN | 62.07 | 46.07 | 87.16 | 75.00 | 79.15 | 109.0 | 87.58 | |

| ARIMA | 921.7 | 734.3 | 681.2 | 555.2 | 488.0 | 467.4 | 548.0 | |

| Variables | Short-Term Forecast | Medium-Term Forecast | Long-Term Forecast | |||

|---|---|---|---|---|---|---|

| Size 2 | Size 3 | Size 4 | Size 5 | Size 6 | Size 7 | |

| Sale | 4.58% | 54.30% | 37.87% | 41.99% | 2.27% | 4.17% |

| Log_sale | 3.02% | 1.46% | 2.62% | 0.66% | 30.00% | 35.90% |

| Avg_sale_by_id | 46.77% | 2.55% | 1.18% | 7.32% | 5.67% | 2.12% |

| Time_idx | 19.84% | 2.77% | 6.28% | 4.43% | 11.08% | 1.15% |

| Relative_Time_idx | 2.42% | 1.93% | 2.82% | 4.87% | 3.27% | 5.04% |

| Weekday_cos | 0.92% | 2.82% | 6.42% | 3.93% | 2.51% | 1.91% |

| Weekday_sin | 1.70% | 3.05% | 1.44% | 3.85% | 2.41% | 4.83% |

| Week_cos | 1.86% | 1.50% | 9.27% | 3.34% | 9.49% | 4.17% |

| Week_sin | 1.36% | 6.17% | 6.27% | 4.37% | 5.24% | 7.00% |

| Seasonality | 0.98% | 8.43% | 5.34% | 0.88% | 1.26% | 17.56% |

| Holidays | 4.62% | 1.39% | 5.75% | 4.59% | 11.50% | 3.33% |

| Weekend | 2.21% | 1.17% | 7.11% | 10.53% | 3.14% | 1.70% |

| Price | 4.12% | 2.88% | 2.61% | 5.84% | 3.47% | 2.81% |

| Duration | 1.56% | 7.38% | 1.73% | 1.00% | 4.11% | 2.29% |

| Views | 4.03% | 2.21% | 3.27% | 2.40% | 4.57% | 6.03% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, Q.; Li, X.; Gao, P. Forecasting Sales in Live-Streaming Cross-Border E-Commerce in the UK Using the Temporal Fusion Transformer Model. J. Theor. Appl. Electron. Commer. Res. 2025, 20, 92. https://doi.org/10.3390/jtaer20020092

Zhang Q, Li X, Gao P. Forecasting Sales in Live-Streaming Cross-Border E-Commerce in the UK Using the Temporal Fusion Transformer Model. Journal of Theoretical and Applied Electronic Commerce Research. 2025; 20(2):92. https://doi.org/10.3390/jtaer20020092

Chicago/Turabian StyleZhang, Qi, Xue Li, and Pengbin Gao. 2025. "Forecasting Sales in Live-Streaming Cross-Border E-Commerce in the UK Using the Temporal Fusion Transformer Model" Journal of Theoretical and Applied Electronic Commerce Research 20, no. 2: 92. https://doi.org/10.3390/jtaer20020092

APA StyleZhang, Q., Li, X., & Gao, P. (2025). Forecasting Sales in Live-Streaming Cross-Border E-Commerce in the UK Using the Temporal Fusion Transformer Model. Journal of Theoretical and Applied Electronic Commerce Research, 20(2), 92. https://doi.org/10.3390/jtaer20020092