Abstract

COVID-19 has undeniably impacted the retail industry sectors; we are now witnessing the emergence of a large body of research on the effects of the pandemic in retailing. However, few of these studies provide a clear picture of this topic from prior to and after COVID-19. This research sheds light on whether large retailers have adapted their channels by offering integrated and digital services amid the new conditions forced on them. This study assesses indicators of channel integration and digital transformation of all large clothing and apparel retailers in Spain—before and after COVID-19—and analyzes the differences by means of McNemar’s test and one-way repeated-measures ANOVA. The analysis suggests that large retailers were moderately prepared to provide multichannel and omnichannel services and that they focused on integrating quick and easy-to-implement services, such as omnichannel gift cards, or communicating via WhatsApp for customer care services. The study also identifies elements in which large clothing brands should prioritize on after the pandemic to effectively deploy omnichannel strategies.

1. Introduction

The coronavirus disease 2019 (COVID-19) outbreak, caused by severe acute respiratory syndrome coronavirus-2 (SARS-CoV-2), has changed our lifestyles, including consumer shopping behaviors. Soft and hard lockdowns across the globe have had an impact on how people work, socialize, and shop. Due to the pandemic, the use of digital technologies during shopping experiences has become prevalent. Digital channels are now being intensively used; companies are rethinking their strategies—they are accelerating their use of digital strategies, for example, increasing their digital service offerings to remain competitive [1,2].

COVID-19 has had a substantial impact on Europe in 2020 and 2021. European countries, in attempt to alleviate the dramatic consequences of the pandemic, adopted various lockdown measures, ranging from partial to total population confinement [3]. In Spain, these measures included severe mobility restrictions as well as school and retail closures (except for supermarkets, pharmacies, and banks) [4]. As cases began to decrease, Spanish authorities progressively allowed the reopening of businesses, which helped lead to activity volumes similar to what they were like from before the pandemic. Some European countries (e.g., Belgium, Germany, France, the Netherlands, Finland, and Sweden) have already recovered and even surpassed previous activity, whereas in Spain, activity levels are still 3–5% down compared to pre-pandemic levels [5]. The role of electronic commerce in preventing further abrupt sales declines is critical for retailers. Even with internet sales increasing prior to the pandemic, digital channels have grown at faster rates (approximately, 25% on average) compared to pre-pandemic levels [5,6], with notable increases in clothing and apparel (63%), furniture (29%), food delivery (28%), computers, and smartphones (26%) [7].

The post-pandemic acceleration of the pre-pandemic changes seen in consumer behaviors (i.e., consumers using physical and online channels freely and at their convenience) and in companies’ attitudes toward digital channels (that were developing slowly prior to COVID-19), suggest that “going back to normal” is not a realistic scenario [8] and that we are now heading into what many are calling “the new normal”. For instance, consumers who have never used digital channels, or only used them occasionally, have been forced to change their shopping habits, i.e., they now use online shops and mobile apps to pay for goods and services; they pay using credit cards or other digital payment systems and the products are delivered to their homes [9,10,11].

Therefore, the digital transformation of retail is no longer an option but an obligation [12]. Retailers were pressured to implement digital technologies, almost overnight, to survive in the post-pandemic environment. They were forced to adapt their infrastructures, processes, and even their cultures within a span of a few months; effective digital transformation took anywhere from three to seven years prior to COVID-19, considering internal (e.g., back-office, operations, R&D) and external (e.g., interactions with customers, supply chain) processes [13]. Although this transformation has impacted all industries and sectors, the depth of this change differ, as consumer goods have been less affected than other industries, such as healthcare, finance, and banking [13].

The integrated management of physical and digital services in retail, as a fundamental part of the digital transformation of a company, is essential to maintain a competitive advantage and ensure the survival of a business [10]. Shopping processes that seamlessly integrated various sales channels (omnichannel commerce) helped improve customer satisfaction during the lockdown, when mobility restrictions were implemented [14,15]. While channel integration strategies have gained significant interest among academics in recent years, regarding consumers (e.g., [16,17]) and retailers (e.g., transformation of supply chains and logistics [18,19], digital technology strategic implementations [20], and business model innovations [21]), few studies have adopted intermediate positions or investigated how consumers perceive the integration of retail service offerings across different channels (e.g., [22,23,24,25]). Although the effects of the COVID-19 pandemic on retailing have attracted scholarly interest in the past two years, many questions need to be answered. For example, will retailers undergo long-term shifts in the balance of online and offline retailing [10]? How will service organizations recover from challenges created by lockdowns and quarantines [26]?

This study explores these questions by comparing changes in channel integration and the digital transformation of customer services across top clothing and apparel firms in Spain from before and after COVID-19 (note that, while COVID-19 is still considered a global pandemic by the World Health Organization, in this study, “after COVID-19” refers to the period after which all restrictions were lifted in Spain regarding the activities involving clothing and apparel retailers). In this study, we observe the extent to which the pandemic has accelerated the digital transformation of retailers, and what aspects of omnichannel retailing have been most affected by the changing conditions imposed by the COVID-19 outbreak. The study introduces a conceptual framework to analyze the channel integration and digital transformation of retailing, followed by a review of the main changes in consumer behaviors and in retail caused by the pandemic. Then, the analysis compares the changes experienced by clothing and apparel firms during the pandemic. Finally, the study discusses the results of the analysis and presents the main implications for theory and practice.

2. Background

2.1. The Digital Transformation of Retail and Channel Integration

2.1.1. Digital Transformation of Retail

While the definition of digital transformation is multifaceted, it highlights the transforming abilities of digital technologies for businesses, especially large brick-and-mortar firms [27]. From a customer-centric perspective, digital transformation encompasses the digitization of sales and communication channels to provide novel ways to effectively interact and engage with customers [27,28]; it also involves replacing or enhancing the physical offerings of a firm’s products and services. Digital transformation builds on digital technologies, such as the Internet of Things (IoT), mobility, cloud-based services, big data, augmented and virtual reality, blockchain, and social media to improve a company’s performance and maximize value creation for consumers [29] through enhanced customer experiences and optimization of commercial and logistics processes [23]. Companies provide different customer touchpoints (e.g., website, mobile app), build digital services (e.g., online billing, customer data management), and open new communication channels (e.g., email, chats, instant messaging, social media) with their customers to adapt to their needs and establish bidirectional communication. Digitization of these services shows a company’s inclination to provide consumers with multichannel and omnichannel services.

2.1.2. Channel Integration and Omnichannel Commerce

Channel integration takes the digitization of services one step further by encompassing marketing and sales processes. Channel integration, or integrated channel management, refers to the combination of services associated with sales channels, to enhance the shopping experiences of customers [30]. The main objective of channel integration is to provide seamless customer experiences across all channels by offering alternative routes to the same information and products [31], fostering loyalty [30].

While researchers have focused on channel integration in their studies, research on how to measure channel integration has been greatly neglected thus far, even though it has gained notable interest in past years [32]. Approaches to measure the levels of channel integration may involve different aspects, such as retailer–supplier relationships [33], the analysis of logistics processes [19], customer experiences [34], supply chain performances [35], or an analysis of the service offerings across channels [22,24], which is the perspective we take in this study.

An analysis of service offerings generally identifies elements associated with the different stages of the shopping process (prepurchase, purchase, and post-purchase). For example, Oh et al. [22] focused on informational elements and differentiated among integrated promotion, integrated transaction information management, integrated product and pricing information management, integrated information access, integrated order fulfillment, and integrated customer service, an approach also adopted in [36]. Building on [22], Acquila-Natale and Chaparro-Peláez [37] (later refined in [24]) identified six dimensions, placing emphasis on (but not limited to) the prepurchase stage: customer touchpoints, channel consistency, integrated promotion, integrated access to information, integrated fulfilment, and integrated customer care services.

2.2. Pandemics, COVID-19, and Consumer Behavior

The COVID-19 pandemic was not the first world pandemic of the century (although, thus far, it was the most lethal and contagious). With severe acute respiratory syndrome-associated coronavirus (SARS-CoV or SARS-CoV-1), which was first detected in China in November 2002 and lasted until 2004, there were 8469 cases and 916 deaths (case fatality rate of 11%) [38]. Middle East respiratory syndrome-related coronavirus (MERS-CoV) was first detected in 2012 in Saudi Arabia and is still active, with 2468 reported cases and 851 deaths (case fatality rate of 34.5%) confirmed as of September 2019 [39].

While the magnitude of COVID-19 highly surpasses that of SARS and MERS (we are currently sitting at nearly 400 million cases and almost 6 million deaths [40]), changes in consumer behavior caused by the latter two may help better understand the impact of COVID-19 on shopping behavior. For example, prior research observed that lower spending in physical channels during the MERS pandemic, due to fear of contagion, was only partially balanced by an increase in online sales [11,41]. This partial balance was not uniform across sectors and was highly dependent on the type of product; for example, in consumer electronics, the increase in online sales was similar to the decrease in physical sales, while in luxury products, the increase in online sales did not compensate for the drop in physical sales. Other retail industries, such as groceries, remained largely unaffected, because individuals were allowed (albeit with some limitations) to shop offline [42].

There is another differentiating element between COVID-19 and previous pandemics. There have been significant developments in electronic commerce since the apparition of SARS and MERS [43], facilitating the transition from physical to online channels [44]. For example, the number of online shoppers grew from 60% to 73% in Europe in 2017–2021, with higher growth in the past two years [45]. In Spain, the number of internet users who shopped online grew from 41.5% to 79.4% in 2020, and 6.8% of online shoppers made their first purchase online in 2020 [46,47]. These figures are in line with those in other countries; for instance, internet shopping grew more in the 2019–2020 period (10%) than in the previous decade [13]. To summarize, the main difference between COVID-19 and previous pandemics—while they share common elements—involves the digital transformation in the retail industry, including new services that combine physical and online channels, as well as in changes in shopping behaviors of newer generations, who are more inclined to incorporate digital technologies in their lives [48].

2.3. COVID-19 and Retailing

Due to state-mandated lockdowns and subsequent closures of nonessential physical stores, consumers have shifted to online shopping [11]. As mentioned above, this measure translated into large sales drops for retailers; in some sectors, retailers were unable to make up for these losses via online sales. For example, the textile industry had their worst results in 15 years, with a 40% decrease in sales in the 2019–2020 period [49].

The effects of the COVID-19 pandemic have generally led to two different situations for retailers. The first situation involves the temporary (or permanent) closures of physical stores and, in the worst case scenario, the complete closure of businesses as part of business restructuring. An example that illustrates the reduction of physical stores (in clothing and apparel retailing) is that of Façonnable Spain, which closed all but three of its physical stores. The second situation encompasses the need for rapid adoption of digital strategies; for example, food and restaurant industries incorporated store pick-up (BOPIS) and delivery services as they were unable to open their physical stores during the pandemic [2].

Many brick-and-mortar retailers introduced their own online stores or transformed their product offerings to remain competitive against digital platforms, such as Amazon or Alibaba, among others. Retailers were forced to implement solutions that they were previously reluctant to adopt, changing the ways they conducted their businesses [43] and providing unique experiences to customers through integrated services across various channels [2,48]. Such services include contacting store employees (via virtual phone calls or chats), online product displays in virtual showrooms, timely and secure deliveries, real-time purchase information, and secure online transactions.

One final consideration regarding channel integration and the digital transformation of retail involves a shift in the expectations of consumers. Prior to the pandemic, experts advocated for the need for retailers to go one step beyond digitization by incorporating omnichannel strategies into their businesses [30,50]. The pandemic has intensified the societal dependence of online channels, while raising shoppers’ expectations about shopping experiences; in this regard, many are speaking about the need to ingrain digital transformation processes within shopping processes, particularly in channel integration, to enhance consumer experiences in the post-pandemic “new normal” [8,11,12,48]. Retailers are ”forced” to integrate management of their sales channels to meet these expectations through consistent brand experiences, synchronizing product offerings across channels, unifying purchase histories or discount coupons that could be redeemed on any of the channels offered [36,51].

Based on the above, it can be argued that the decrease in sales and increased costs owing to the incorporation of new services have led to lower retail revenues; although retailers have been forced to adapt to multichannel operations. Therefore, we propose the following hypotheses, in the context of clothing and apparel retailing:

Hypothesis 1 (H1).

The number of large clothing and apparel retailers decreased after the COVID-19 pandemic.

Hypothesis 2 (H2).

The number of large clothing and apparel retailers that have adopted multichannel strategies (e.g., incorporated digital touchpoints) increased after the COVID-19 pandemic.

Hypothesis 3 (H3).

Large clothing and apparel retailers increased their channel integration levels after the COVID-19 pandemic.

Regarding digitized services, it is worth considering that, in the last decade, the fast growth of social media has helped the development of omnichannel operations, initially as information, communication, and information channels [52]. The use of social networks has increased from 29% to 54% globally [53,54,55]. In Spain, 80% of the population have active accounts on social networking sites, compared to 47% in 2015 [53,54,55]. However, the evolutions of various social networks are dissimilar; for example, Facebook, Twitter, and YouTube seem to have stabilized in the past two years, while other social networking sites, such as Instagram, continue to experience steady growth (Appendix A.3), particularly due to the daily use of individuals under 40 years old [56]. Based on this trend, we can propose the following:

Hypothesis 4 (H4).

Large clothing and apparel retailers have maintained or augmented their offers of digitized services for communication purposes to adapt to changes in consumer habits (regarding social media use).

While the formulation of H3 is general, this study will analyze channel integration as a whole, and will also investigate the individual dimensions and indicators of channel integration.

3. Materials and Methods

3.1. Sample

The study included large clothing and apparel brands (with revenues higher than EUR 3 million), excluding specialized brands (e.g., sports, luxury brands). Brands were required to operate in Spain, regardless of whether they were based in Spain or international brands, and offer services in two or more channels (e.g., physical, web, mobile).

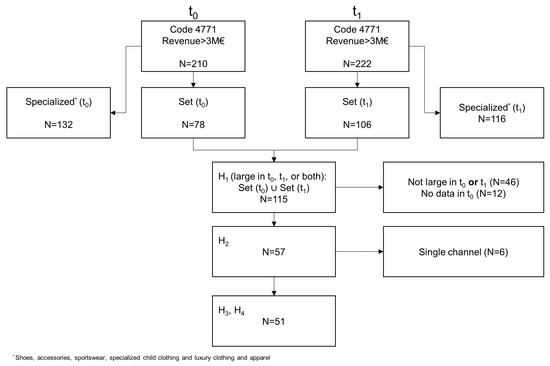

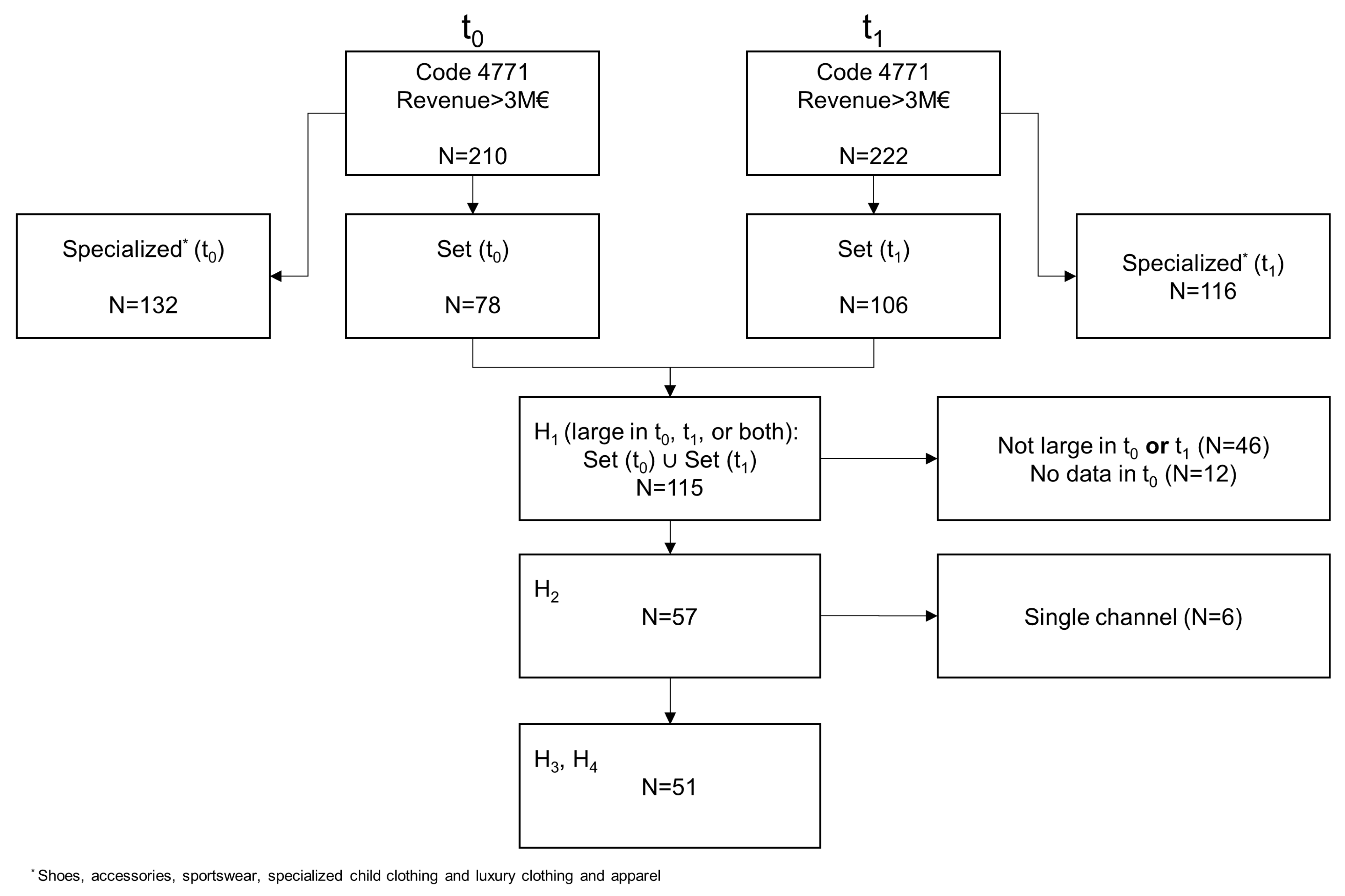

Data were collected at two different times to test the research hypotheses and analyze the effects of COVID-19; the first wave of data collections (t0) covered the period between September and November 2019 (before the COVID-19 pandemic), while the second wave (t1) extended from November 2021 to January 2022 (during the sixth wave of the pandemic, months after most restrictions affecting retail had been lifted). For t0, we used the data sets elaborated by Acquila-Natale et al. [37] and Iglesias-Pradas et al. [24], whereas data collection in t1 followed the systematic procedure outlined in [24]. Figure 1 summarizes the data collection process:

Figure 1.

Data analysis and hypotheses testing procedures.

- Development of an initial list of candidate brands from the ranks of Spanish companies, by revenue, from the eInforma database [57], filtered by sector (code 4771, “Retailing of clothing and apparel in specialized stores”), as well as revenue (more than EUR 3 million). This first search returned 210 (t0) and 222 results (t1), respectively.

- Data purge: after manual inspection of each brand, two independent coders identified brands that met the criteria for exclusion (retailers that only sold shoes, accessories, sportswear, specialized children’s clothing, and luxury clothing and apparel). The list after removal of records included 78 (t0) and 106 (t1) brands, respectively.

To test H1, we considered the union of the two data sets resulting from the second step (i.e., clothing and apparel retailers, excluding specialized and luxury brands, with revenues higher than EUR 3 million at any of the two data collection periods; NH1 = 115). To test H2 with comparable sample sets only including large companies, we excluded companies that were not considered large in either period from the previous data set (N = 46); because there were no data available in the pre-COVID data set for 12 companies that operated in single physical locations (i.e., no data points for t0), they were also excluded from the data set; thus, NH2 = 57. Testing of hypotheses H3 and H4 excluded single-channel companies of the previous data set, to only include those that operated as multichannel retailers (NH3–H4 = 51).

3.2. Measurement Instrument

The measurement instrument (Appendix A.1 and Appendix A.2) used for the research was the same as the one proposed in [24], comprising the six dimensions of channel integration detailed in Section 2.1.2 (six dimensions, 27 indicators) and the digital transformation in Section 2.1.1 (12 indicators, even though the analysis focuses on digital communication services). Similar to [24], all indicators of channel integration were assigned a value of 1 if the service was offered by the brand, and 0 if not. Regarding indicators of digital transformation, this study introduced a novelty when assigning value to a brand’s presence on different social media networks: whereas [24] only considered binary values (1 if the brand had an official account on a social media networking site, 0 otherwise); this study offers a more nuanced analysis of these indicators, with values ranging from 0 to 1 to identify social media network presence as well as frequency of updates; in other words, when a brand was present on a social media network but had no activity in the two years prior to t1, a value of 0.1 was assigned, with values in increments of 0.1 depending on the date of the last update. The final channel integration level measurement was calculated as a percentage, assigning equal weights to each indicator. As noted in [24], indicators related to customer touchpoints, customer service, or digital transformation, although similar, do not refer to the same observed service (for example, having a website but not selling via the website, or having a presence on a social network but not using it to provide customer care service, would render different values in the indicators of channel integration and digital transformation).

3.3. Data Collection Procedure

The data were collected by two independent coders and revised by a third independent coder. Data collections included observations of brand information publicly available on websites or mobile apps and a mystery shopping approach [58]. Mystery shopping involves investigating the transactions between customers and service providers to measure service delivery [59]. With mystery shopping, researchers gather data directly from companies and brands to evaluate the services provided by a company, acting as “mystery shoppers” (i.e., not revealing the nature of the research) by visiting the stores (and, in this case, visiting the web store and mobile app), collecting data using preset scripts. Whenever necessary, the observed data were completed by interacting with the company via different channels, such as telephone, chat, e-mail, social networks, and instant messaging platforms. The use of mystery shopping in this study does not delve into the quality of the services provided; it was used to confirm whether the brand offered a service from those included in the measurement instrument, to alleviate subjectivity in data collection [60].

3.4. Analysis Technique

Hypotheses testing involves the analysis of matched-pairs data with a binary response; therefore, we used McNemar’s test to compare marginal proportions [61], which is appropriate to determine whether there is a significant change in nominal data before and after an event, as in this case. Because the sum of the status changes in the contingency tables is lower than 10, in all cases, we used the mcnemar.exact and mcnemarExactDP functions from the exact2x2 R package to calculate the exact version of McNemar’s test. The exact version is based on the binomial distribution on one of the off-diagonal values conditioned on the total of both off-diagonal values [62].

H3 may be tested by performing a paired-samples (repeated measures) t-test (or non-parametric equivalent if t-test assumptions are not met). Because the study only involved two groups, one-way repeated-measures ANOVA provided the same results as the t-test. ANOVA was the analysis procedure used in this study, as there were tools available to provide both numerical and graphical result outputs; in this case, we used the R function ggwithinstats from the ggstatsplot package [63]. For comparison of each indicator, we performed McNemar’s test.

For H4, we tested for differences across each digitized communication service (D.1.3 through D.1.10 in Table A2) using ggwithinstats, because variables could be non-binary; additionally, we tested for differences across the rest of the digital transformation indicators (i.e., mobile app, web page, customer data management, and online billing) using McNemar’s test to enrich the interpretation of results.

4. Results

Table 1 shows the number of large clothing and apparel retailers found in the data before and after the COVID-19 pandemic. McNemar’s exact test (p-value < 0.001) shows significant changes in the number of large retailers before and after the pandemic, but in the opposite direction of the expected result, which suggests that there were more large clothing and apparel companies after the pandemic than prior to COVID-19. Therefore, H1 is rejected.

Table 1.

Clothing and apparel retailers classified as large companies.

Table 2 includes the number of large companies that had multichannel operation before and after COVID-19. Again, McNemar’s exact test (p-value = 1) suggests that, contrary to H2, single-channel operating retailers did not change their channel strategies in response to the pandemic. All large retailers maintained their channel strategies during the pandemic. Of the six retailers that continued to operate in only one channel, five of them were multilabel retailers that had a digital presence oriented toward driving consumers to their physical stores; the remaining one (Nekane) was a pure online player (and the only large clothing and apparel retailer without a physical footprint).

Table 2.

Single-channel and multichannel operations of large clothing and apparel retailers before and after COVID-19.

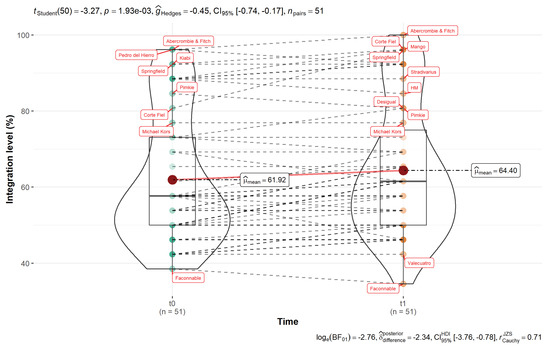

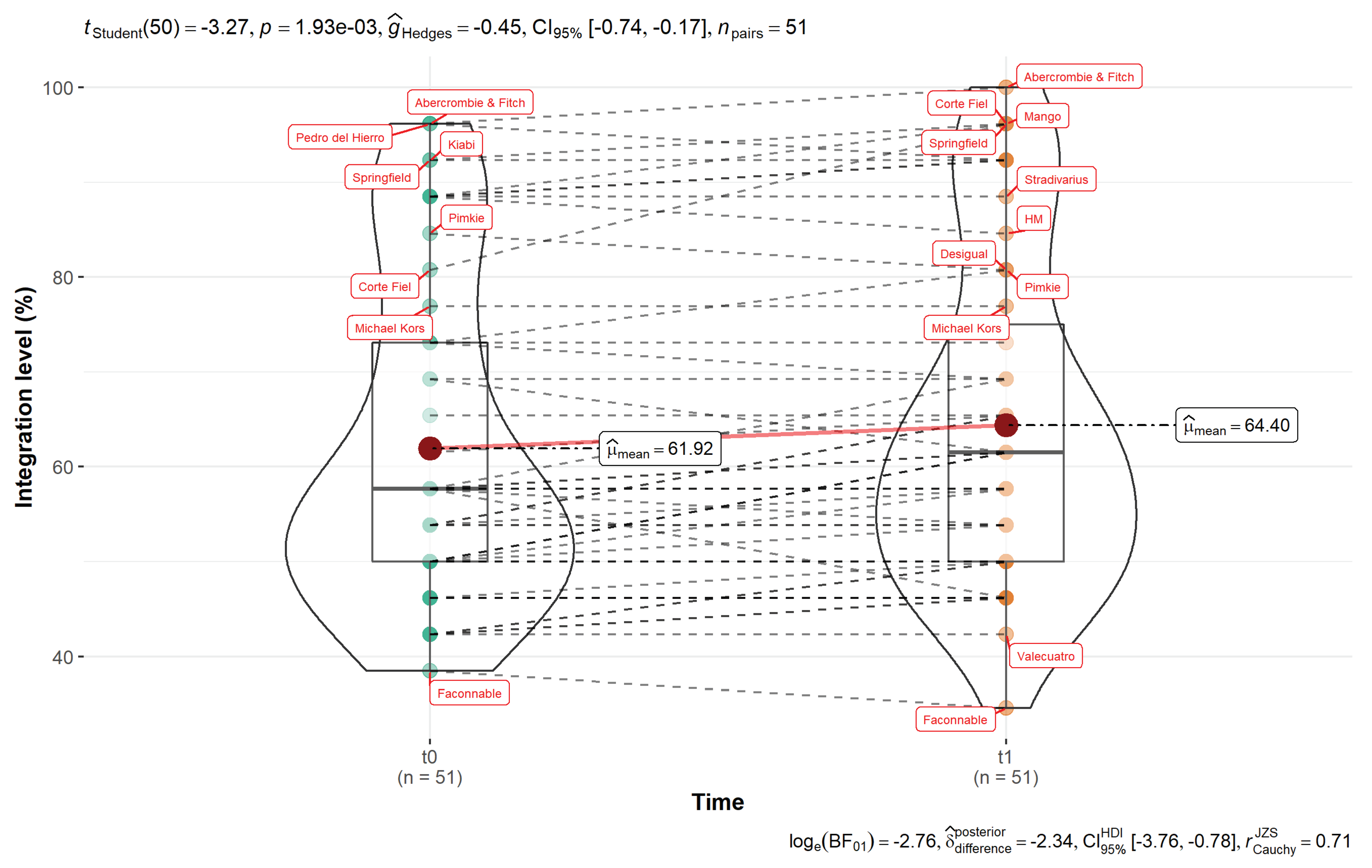

Figure 2 shows the main results of the channel integration analysis. From Figure 2, we observe a significant increase of 2.5 points in channel integration levels across large clothing and apparel retailers, in support of H3. This means that, on average, retailers integrated one new service in their omnichannel offerings. Figure 2 shows that, despite the global trend in improving multichannel and omnichannel services, a few retailers decreased their service offerings; the most notable change was that of Façonnable, mentioned earlier, which closed most of their physical stores during the pandemic.

Figure 2.

Comparison of global channel integration levels across large clothing and apparel retailers: (a) Before COVID-19 (t0). (b) After COVID-19 (t1).

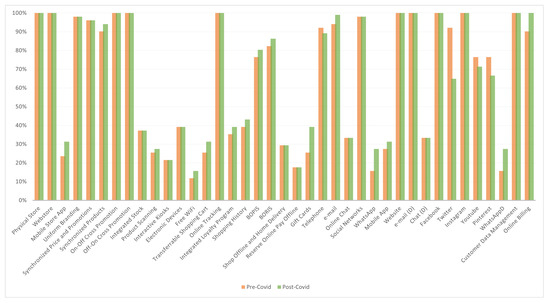

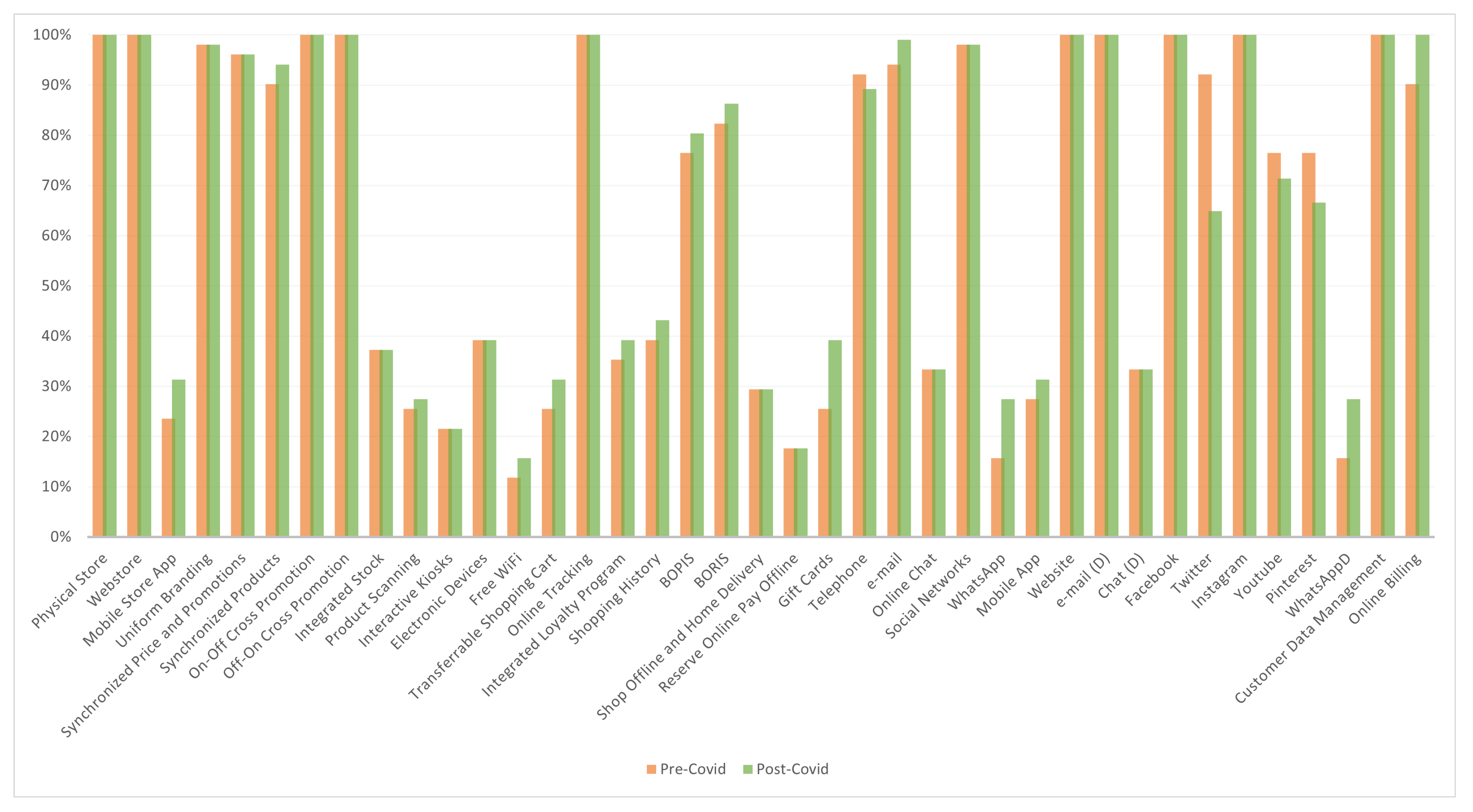

McNemar’s test for individual indicators (with option alternative = “greater” as a parameter in mcnemarExactDP) reveals that the degree of integration of specific services did not significantly change (p-value > 0.05), except for (a) the availability of cross-channel gift cards (p-value = 0.008), with seven retailers incorporating this integrated service, and (b) integrated customer care services offered via WhatsApp (p-value = 0.035), with one retailer ceasing to offer the service but seven retailers adding it. It is also worth pointing out that the analysis failed to find significant differences in the services that already had high integration levels prior to the pandemic, such as cross-channel promotion, online tracking, or social networks, and that the data show that none of the channel integration services experienced a decrease on average (Figure 3).

Figure 3.

Channel services—integrated and digital services implemented before (t0) and after (t1) COVID-19.

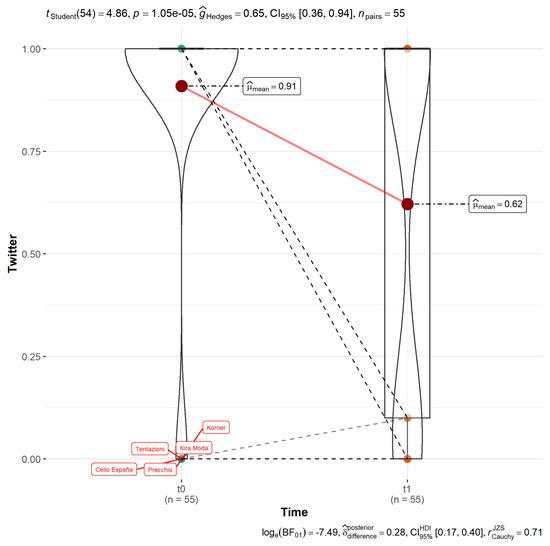

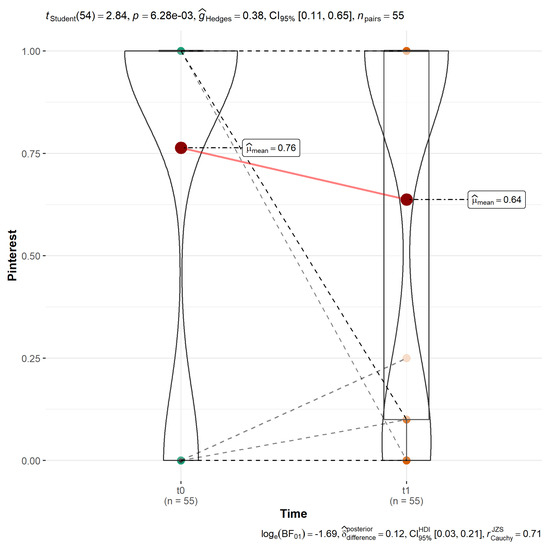

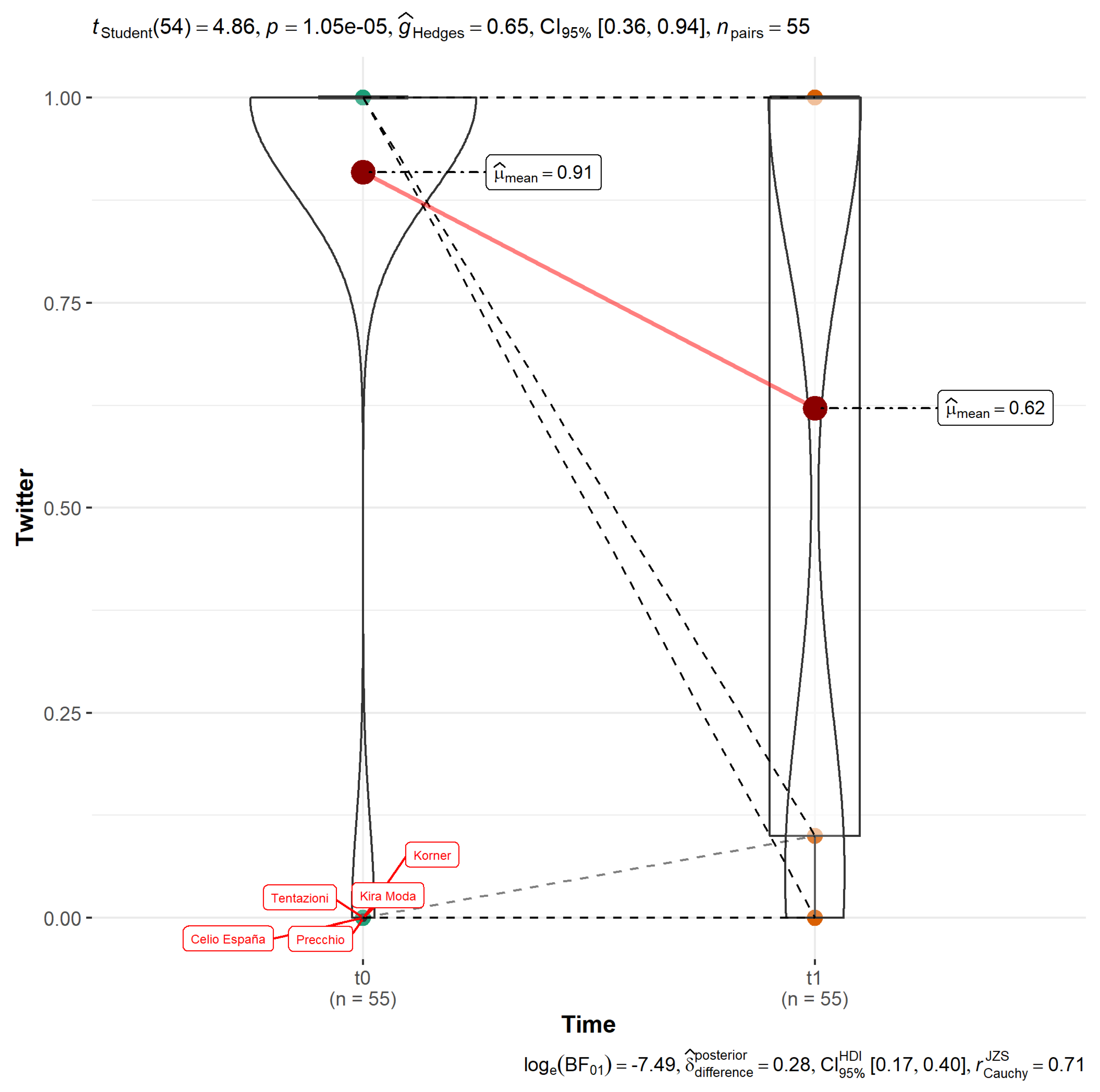

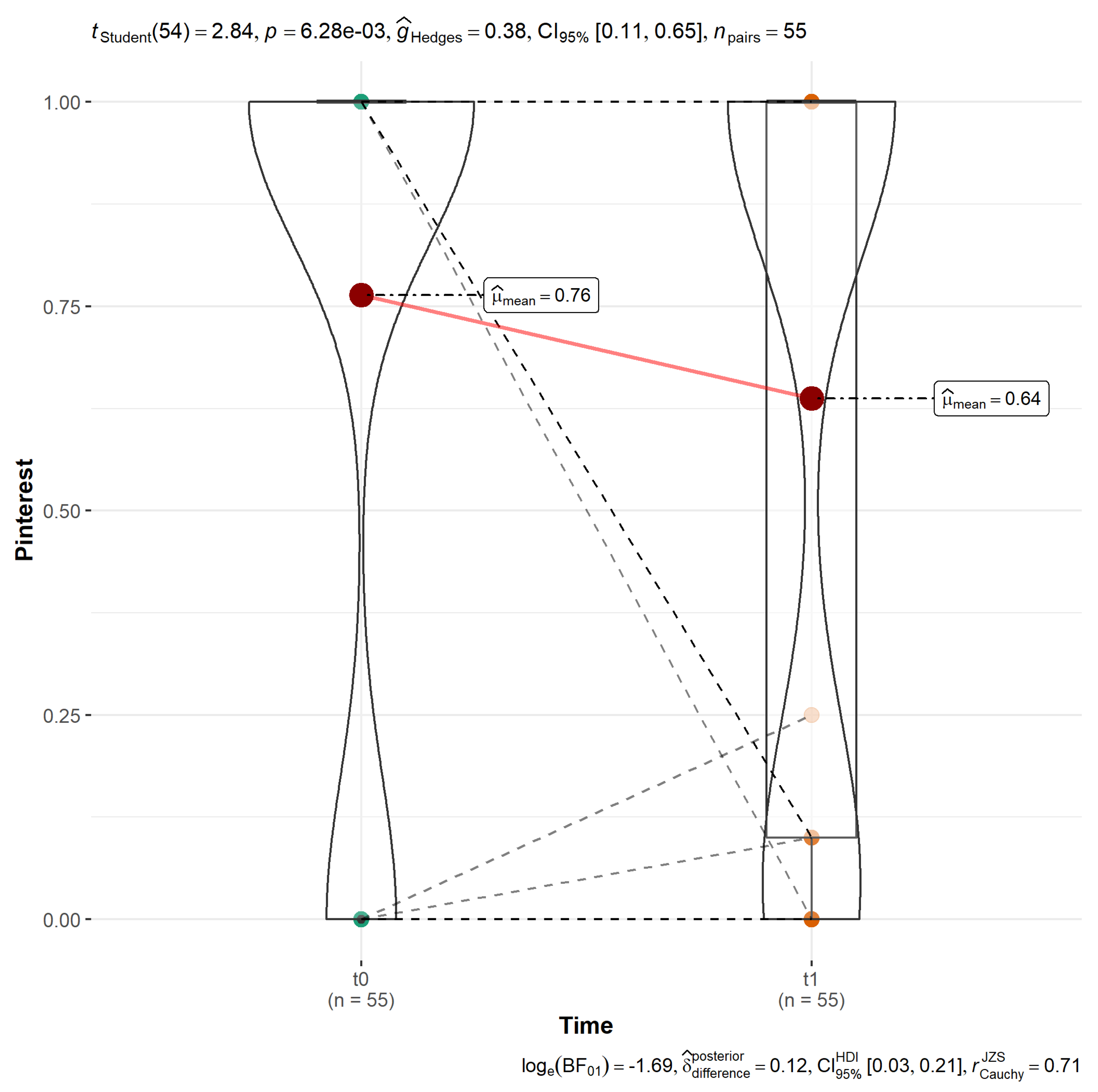

Finally, the analysis showed significant drops in the use of some social networks, such as Pinterest and Twitter (Figure 4 and Figure 5), and we observed a significant increase in the use of WhatsApp. While the formulation of H4 would suggest that an increase in the use of Instagram might be expected, the analysis shows no significant differences, but this result is conditioned by the fact that all companies were already using this communication channel before the pandemic. Regarding other digital services, McNemar’s test shows a significant increase in the use of online billing services (p-value = 0.031), a service that 46 retailers offered before the pandemic, but is now offered by all 51 retailers included in the data set. We also observed differences in the implementation of WhatsApp as a communication channel, but its significance is only marginal (p-value < 0.05, one-sided; p-value = 0.07, two-sided) as no direction of change was proposed.

Figure 4.

Changes in the implementation and use of Twitter.

Figure 5.

Changes in the implementation and use of Pinterest.

5. Discussion

5.1. Large Clothing and Apparel Retailers and the COVID-19 Pandemic

In light of the results, the study shows that the number of large clothing and apparel retailers did not decrease during the pandemic, as expected, but rather experienced a significant increase. A total of 9 out of 78 companies (11.5%) had to be excluded from the list of large clothing and apparel retailers based on the criteria detailed in Section 3.1; of these, 5 saw their revenues fall below EUR 3 million, 2 were in liquidation, and 2 changed their main sectors of activity. Furthermore, a total of 37 companies that did not reach EUR 3 million in revenue prior to COVID-19 increased their sales over this figure during the pandemic.

This finding is contrary to our hypothesis and suggests that the pandemic struck SMEs more heavily (especially the smallest of them, such as mom-and-pop stores). Indeed, additional data also confirm that, while the number of clothing and apparel retailers decreased 11% in the past two years, the national market of clothing and apparel retailing stores in Spain increased by 12% [57]. It is likely that large multichannel retailers have seized a large market share that was filled by smaller retailers before the pandemic, as the latter struggled to compete in a multichannel context. The results then point to the existence of a gap between large and small retailers, in line with Chaparro-Peláez et al.’s [64] analysis of the retail electricity market, highlighting that large retailers are better prepared for transitions to digital customer-centric strategies and omnichannel retailing.

The analysis supports the idea that large clothing and apparel retailers did not suffer from the devastating effects of the pandemic that affected other sectors, such as tourism and hospitality [65], likely due to their high e-commerce readiness and multichannel development before the outbreak, compared to other retailing industries [24]. Recent reports back the idea that clothing and apparel retailers have managed to offset the losses in physical sales during the pandemic with internet sales: clothing was the area of activity with the highest percentage of e-commerce turnover in 2021 in Spain, especially due to transactions from foreign locations, and the market value of internet clothing and apparel retail in Spain experienced an increase of 48% in 2020 [66].

Regarding the effects of COVID-19 on the implementation of multichannel strategies across large clothing and apparel retailers—the analysis revealed that the large retailers did not change their strategies during the COVID-19 pandemic. While we expected that all 51 retailers that already had multichannel strategies in place before the pandemic would continue their strategies, it came as a surprise that the remaining 6 large retailers that operated in a single-channel before the pandemic did not embrace multichannel operations to overcome the restrictions (e.g., lack of activity in physical stores due to the lockdown) to remain competitive. While the result merits further scrutiny, one possible explanation is that the impact of the pandemic was severe only during the lockdown phase (two months, from March to May 2020) and that there was a recovery stage in May–July, after which, sales were stabilized—an approximate 20% decrease in the “new normal” [67]. Physical single-channel retailers may have endured the lockdown stage with heavy losses, focusing on strengthening their physical channels during the recovery stage, but not being able to invest further in multichannel operations due to financial stress.

5.2. Channel Integration and Digital Transformation of Clothing and Apparel Retail in Spain

The results offer interesting insights into the effects of the COVID-19 pandemic, concerning how large clothing and apparel retailers reacted to overcome the imposed restrictions (e.g., a complete lockdown in Spain). The analysis shows that most large retailers already had multichannel strategies in place, especially regarding digital presence (all retailers had previously implemented web stores, social network accounts, and cross-channel promotion strategies), as well as some outbound logistics processes (e.g., online tracking).

The analysis also suggests that during the pandemic retailers prioritized easy-to-implement, low-cost, short-term, and high-return solutions, such as redeemable gift cards valid on any channel (omnichannel gift cards), which increase customer dissatisfaction with the service when not properly integrated [68]. This decision makes sense when observing other services with low overall degrees of integration across brands that refer to the digitalization of a physical store (e.g., product scanning, interactive kiosks, or free Wi-Fi), have non-negligible costs (e.g., integrated stock), pivot around the physical stores, and are largely limited by restrictions (e.g., buy-online-pickup-in-store, buy-online-return-in-store, reserve-online-pay-offline, shop-offline-home-delivery). Nonetheless, a few brands did integrate these services, and it is expected that they will be given higher priority when the virus may no longer be considered a problem.

Figure 3 shows an increase in the implementation of mobile store applications. While the change in the number of brands incorporating mobile store apps was not significant, we expect that this trend will generalize in the near future, as most retailers are leveraging the capabilities of mobile apps [69]. Brands should be aware about the potential of mobile apps to foster consumers’ intention to engage in purchasing [70] and for value creation, for both shoppers and the companies: companies may obtain enriched and fine-grained data about their customers, and in turn, they can provide personalized services, offers, and recommendations [24,70].

There is a significant change in the implementation of WhatsApp for customer care services. There may be two fundamental reasons for this change, which may be highly specific to Spain, although it may be extrapolated to other instant messaging applications in other countries. First, WhatsApp is the most used digital communication application in Spain: nine out of ten people use it daily (Table A3); second, the mobile version of WhatsApp for businesses (https://www.whatsapp.com/business (accessed on 15 February 2022)) makes it easier for retailers to integrate different services (e.g., online chat, product catalog, or automated messages) at a central point, and provides integration with the digital touchpoints (e.g., websites, mobile applications) and other systems (e.g., customer relationship management software).

Finally, we observed a shift in how brands manage their digital services that deserves further investigation. On the one hand, the pandemic seems to have forced all retailers to introduce online billing systems (all brands that did not offer this service prior to the pandemic now do). On the other hand, brands have started to decrease their presence on social networks; while the use of Instagram and Facebook (the leading social platforms) is generalized, some brands are moving away from social networking sites that have reached a plateau in the number of total users or that are in decline (e.g., Twitter, Pinterest), and from those that are more resource-intensive, such as YouTube. This finding seems to confirm that clothing and apparel brands—pioneers in embracing social media as marketing communication channels [71]—react rather quickly to changes in consumer trends and behaviors.

5.3. Implications for Practice

The managerial implications derived from this study are manifold. First, the study highlights the relevance of digital transformation for retailers to be competitive. As the results show, large clothing and apparel retailers were able to endure the hardships associated with the pandemic and lockdown because they were already well prepared to provide multichannel services. In this sense, the results also hint at the existence of a digital breach between large and SME retailers. Same as electricity retailers, small clothing and apparel retailers face additional barriers regarding digital transformation, especially those related to limited capital availability [64]. The effects of the pandemic may have broadened this gap, as the results suggest that the decrease in sales has had more of an impact on smaller retailers, and may be a wake-up call for national policy makers to focus on plans that help small retailers implement their digital transformation. However, this interpretation must be investigated in more detail with accurate data from small and medium-sized retailers, which were not captured by this study.

Second, the analysis seems to confirm that omnichannel operation strategies are being implemented in different phases. Iglesias-Pradas et al. [24] suggest that retailers adapt their day-to-day operations to multiple channel configurations and then implement IT-supported services to improve customer shopping experiences, as seen in this study (e.g., relatively slow levels of integrated stock and shopping history services). However, the study shows that the implementation of some services may have been disrupted by the pandemic; for example, there was a trend in retailing to provide a wider range of fulfilment options before the pandemic, but companies have mostly maintained their delivery and return options; this is largely due to the decrease in activity in physical stores, which made it risky to invest in these services (e.g., BORIS, BOPIS) at the time, despite these services being well-received and extensively used by shoppers [72].

Third, and related to the previous point, the logical next step for large retailers in the “new normal” is to take advantage of the physical store to provide unique shopper experiences [73,74]. Our analysis identifies many areas of improvement that could be attended to, in order to fully grasp the potential benefits of omnichannel operations, such as the use of electronic devices by sales associates [17], product scanning, integrated loyalty programs, or even some aspects that were not included in this study due to their relative novelty, such as augmented reality systems.

Fourth, the study highlights the importance of having multichannel operations (only 5 of the 57 large retailers operate solely as traditional retailers) and of the physical channel (only 1 brand operates solely online). This result seems to confirm that retailers that do not incorporate both online and offline channels are at peril [75].

Finally, the research focuses on three sales channels for multichannel and omnichannel operations (physical, web store, and mobile app store). While social media has traditionally been seen as a communication and marketing channel, social networking sites are now extending their functionalities to provide shopping options for users (e.g., Instagram Shopping) [76]. In future studies on channel integration using the conceptual framework analyzed in this study, researchers might want to expand our classification to include these new sales channels.

6. Conclusions

This study analyzed the impacts of the COVID-19 pandemic on the multichannel and omnichannel strategies of large clothing and apparel retailers in Spain, focusing on service channel integration and implementation of digital communication and customer service. The study complements current research on the changing habits of shopping behaviors owing to the COVID-19 pandemic, with customer-oriented perspectives (e.g., [77]), by analyzing retailers’ response to the pandemic regarding their multichannel services offering. Therefore, the research contributes toward further understanding of channel integration, the most promising area for future research in the omnichannel domain [78], in the context of changes caused by the pandemic. Channel integration connects both the consumer and company perspectives and is key to seamlessness, superior customer value and creation of long-term sustainable business models [78].

From an academic perspective, the study sets apart from cross-sectional studies on the impacts of the pandemic; it offers a longitudinal view that facilitates the assessment of its effects and helps contextualize the results of the analysis. Even though we may assume that the results are similar to those in other European countries, the findings of the research may not be generalized to other sectors or countries and, therefore, this research calls for further confirmation (or highlighting of differences) in different cultural contexts and industries. The application of the conceptual framework for the assessment of channel integration and digitalization of services also addresses the issues related to research design and data collection due to omnichannel complexities [78].

From a practitioner view, the study is a diagnostic tool that provides a clearer picture of the current state of multichannel and omnichannel clothing and apparel retailing, as well as of the effects of COVID-19 in the industry. The analysis suggests that large brands in the sector are steadily progressing towards achieving omnichannel status and, thus, increasing their resilience. However, when confronting the results with industry reports, while large retailers seem to have managed to ‘ride the wave’ and survive (or even grow) during the pandemic, small traditional brick-and-mortar retailers (less prepared to transition toward multichannel operations) have taken a hit that has threatened their own survival; failing to embrace the digital transformation will, in most cases, lead to their disappearance.

The analysis found areas of improvement that companies have failed to address so far, such as offering a complete variety of purchasing, delivery and return options, and the integration of digital services in physical stores to appeal to omnichannel consumers and improve overall shopping experiences. Additionally, the data suggest that digital presence strategies in social networking sites are experiencing a ’reset’ process, whereby brands are abandoning their ideas of being active in all possible platforms (which is time and resource consuming) and instead are carefully planning their social network marketing strategies to adapt to new consumer habits.

To conclude, we would like to address a shortcoming of this study regarding the financial information on companies used for classification as large retailers. Only financial data up until 2020 were available for the study, as the period for reporting the companies’ results in 2021 was not complete by the time the study ended. Even though the overwhelming evidence of the analysis suggests otherwise, this limitation might introduce a slight bias in singular cases that might affect the testing of H1.

Author Contributions

Conceptualization, E.A.-N. and J.C.-P.; methodology, E.A.-N, J.C.-P. and L.D.-R.-C.; validation, J.C.-P., L.D.-R.-C. and C.C.-E.; formal analysis, E.A.-N. and J.C.-P.; investigation, E.A.-N. and C.C.-E.; resources, L.D.-R.-C. and C.C.-E.; data curation, E.A.-N. and C.C.-E.; writing—original draft preparation, E.A.-N. and J.C.-P.; writing—review and editing, L.D.-R.-C. and C.C.-E.; visualization, C.C.-E.; supervision, E.A.-N.; project administration, E.A.-N. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data that support the findings of this study are available on request from the authors.

Acknowledgments

The authors would like to thank Ángel Hernández-García for his feedback in earlier versions of this work.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Appendix A.1. Channel Integration

Table A1.

Dimensions and indicators of channel integration.

Table A1.

Dimensions and indicators of channel integration.

| Dimension | Description | Indicators |

|---|---|---|

| 1. Customer touchpoints | Channels available for company–consumer interaction | 1.1. Physical store |

| 1.2 Web store | ||

| 1.3. Mobile app | ||

| 2. Channel consistency | Consistency of brand image, products, and prices across channels | 2.1. Uniform branding |

| 2.2. Synchronized price and promotions | ||

| 2.3. Synchronized products | ||

| 3. Integrated promotion | Existence or absence of cross-channel promotion | 3.1. On–off promotion |

| 3.2. Off–on promotion | ||

| 4. Integrated access to information | Consistent access to data and information across channels | 4.1. Integrated stock |

| 4.2. Product scanning | ||

| 4.3. Interactive kiosks | ||

| 4.4. Electronic devices | ||

| 4.5. Free Wi-Fi | ||

| 4.6. Transfer shopping cart | ||

| 4.7. Order tracking | ||

| 4.8. Integrated loyalty programs | ||

| 4.9. Shopping history | ||

| 5. Integrated fulfilment | Synchronized outbound logistics processes across channels (e.g., delivery and return options) | 5.1. Buy Online, Pick-up In Store (BOPIS) |

| 5.2. Buy Online, Return In Store (BORIS) | ||

| 5.3. Shop offline and home delivery | ||

| 5.4. Reserve online and pay offline | ||

| 5.5. Gift cards | ||

| 6. Integrated customer service | Integrated communication channels during purchasing process | 6.1. Telephone |

| 6.2. E-mail | ||

| 6.3. Chat | ||

| 6.4. Social networks | ||

| 6.5. WhatsApp |

Appendix A.2. Digital Services

Table A2.

Dimensions and indicators of digital services.

Table A2.

Dimensions and indicators of digital services.

| Dimension | Indicators |

|---|---|

| D.1. Digital transformation | D1.1. D-Mobile app |

| D1.2. Web page | |

| D1.3. E-mail | |

| D1.4. Chat | |

| D1.5. Facebook | |

| D1.6. Twitter | |

| D1.7. Instagram | |

| D1.8. YouTube | |

| D1.9. Pinterest | |

| D1.10. WhatsApp | |

| D1.11. Customer data management | |

| D1.12. Online billing |

Appendix A.3. Evolution of Social Network Use in Spain

Table A3.

Evolution of the use of social networking sites in Spain, as a percentage of the population [79].

Table A3.

Evolution of the use of social networking sites in Spain, as a percentage of the population [79].

| Social Network | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|---|

| 33.0% | 44.0% | 71.0% | 69.0% | 82.0% | 79.0% | 79.2% | |

| 17.0% | 24.0% | 44.0% | 39.0% | 49.0% | 53.0% | 52.6% | |

| 10.0% | 15.0% | 37.0% | 40.0% | 54.0% | 65.0% | 69.0% | |

| 7.0% | 9.0% | 23.0% | 22.0% | 28.0% | 35.0% | 33.7% | |

| YouTube | 74.0% | 73.0% | 89.0% | 89.0% | 89.3% | ||

| 42.0% | 45.0% | 65.0% | 73.0% | 87.0% | 86.0% | 89.5% |

References

- Donthu, N.; Gustafsson, A. Effects of COVID-19 on business and research. J. Bus. Res. 2020, 117, 284–289. [Google Scholar] [CrossRef] [PubMed]

- Soto-Acosta, P. COVID-19 Pandemic: Shifting Digital Transformation to a High-Speed Gear. Inf. Syst. Manag. 2020, 37, 260–266. [Google Scholar] [CrossRef]

- ACAPS. #COVID-19 Government Measures Dataset. 2020. Available online: https://www.acaps.org/covid-19-government-measures-dataset (accessed on 10 February 2022).

- Ministerio de la Presidencia Relaciones con las Cortes y Memoria Democrática. Real Decreto 463/2020, de 14 de marzo, por el que se declara el estado de alarma para la gestión de la situación de crisis sanitaria ocasionada por el COVID-19. Boletín Estado 2020, 67, 25390–25400. [Google Scholar]

- Eurostat. Impact of COVID-19 Crisis on Retail Trade. Technical Report; Eurostat: Luxembourg, 2021. [Google Scholar]

- Eurostat. E-Commerce Statistics; Technical Report; Eurostat: Luxembourg, 2022. [Google Scholar]

- Eurostat. E-Commerce Statistics for Individuals; Technical Report; Eurostat: Luxembourg, 2022. [Google Scholar]

- Beckers, J.; Weekx, S.; Beutels, P.; Verhetsel, A. COVID-19 and retail: The catalyst for e-commerce in Belgium? J. Retail. Consum. Serv. 2021, 62, 102645. [Google Scholar] [CrossRef]

- Chou, X.; Pietri, N.O.; Loske, D.; Klumpp, M.; Montemanni, R. Optimization Strategies for In-Store Order Picking in Omnichannel Retailing. IFIP Adv. Inf. Commun. Technol. 2021, 631, 603–611. [Google Scholar] [CrossRef]

- Das, G.; Jain, S.P.; Maheswaran, D.; Slotegraaf, R.J.; Srinivasan, R. Pandemics and marketing: Insights, impacts, and research opportunities. J. Acad. Mark. Sci. 2021, 49, 835–854. [Google Scholar] [CrossRef]

- Pantano, E.; Pizzi, G.; Scarpi, D.; Dennis, C. Competing during a pandemic? Retailers’ ups and downs during the COVID-19 outbreak. J. Bus. Res. 2020, 116, 209–213. [Google Scholar] [CrossRef]

- Willems, K.; Verhulst, N.; Brengman, M. How COVID-19 Could Accelerate the Adoption of New Retail Technologies and Enhance the (E-)Servicescape. In The Future of Service Post-COVID-19 Pandemic; Lee, J., Han, S.H., Eds.; Springer: Singapore, 2021; Volume 2, Chapter 6; pp. 103–134. [Google Scholar] [CrossRef]

- LaBerge, L.; O’Toole, C.; Schneider, J.; Smaje, K. How COVID-19 Has Pushed Companies over the Technology Tipping Point and Transformed Business Forever. July 2020. Available online: https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/how-covid-19-has-pushed-companies-over-the-technology-tipping-point-and-transformed-business-forever (accessed on 7 February 2022).

- Fortuna, F.; Risso, M.; Musso, F. Omnichannelling and the Predominance of Big Retailers in the post-Covid Era. Symphonya Emerg. Issues Manag. 2021, 2, 142–157. [Google Scholar] [CrossRef]

- Chatterjee, S.; Chaudhuri, R.; Vrontis, D. Examining the global retail apocalypse during the COVID-19 pandemic using strategic omnichannel management: A consumers’ data privacy and data security perspective. J. Strateg. Mark. 2021, 29, 617–632. [Google Scholar] [CrossRef]

- Chen, Y.; Chi, T. How does channel integration affect consumers’ selection of omni-channel shopping methods? An empirical study of u.s. consumers. Sustainability 2021, 13, 8983. [Google Scholar] [CrossRef]

- Swoboda, B.; Winters, A. Effects of the most useful offline-online and online-offline channel integration services for consumers. Decis. Support Syst. 2021, 145, 113522. [Google Scholar] [CrossRef]

- Ishfaq, R.; Davis-Sramek, E.; Gibson, B. Digital supply chains in omnichannel retail: A conceptual framework. J. Bus. Logist. 2021, 1–20. [Google Scholar] [CrossRef]

- Liu, X.; Lan, H.; Song, G. An evaluation model of omni-channel retail logistics service integration level. In Proceedings of the 2018 4th International Conference on Industrial and Business Engineering, Macau, Macao, 24–26 October 2018. [Google Scholar] [CrossRef]

- Mugge, P.; Abbu, H.; Michaelis, T.L.; Kwiatkowski, A.; Gudergan, G. Patterns of Digitization: A Practical Guide to Digital Transformation. Res. Technol. Manag. 2020, 63, 27–35. [Google Scholar] [CrossRef]

- Do Vale, G.; Collin-Lachaud, I.; Lecocq, X. Micro-level practices of bricolage during business model innovation process: The case of digital transformation towards omni-channel retailing. Scand. J. Manag. 2021, 37, 101154. [Google Scholar] [CrossRef]

- Oh, L.; Teo, H.; Sambamurthy, V. The effects of retail channel integration through the use of information technologies on firm performance. J. Oper. Manag. 2012, 30, 368–381. [Google Scholar] [CrossRef]

- Acquila-Natale, E.; Iglesias-Pradas, S. A matter of value? Predicting channel preference and multichannel behaviors in retail. Technol. Forecast. Soc. Chang. 2021, 162, 120401. [Google Scholar] [CrossRef]

- Iglesias-Pradas, S.; Acquila-Natale, E.; Del-Río-Carazo, L. Omnichannel retailing: A tale of three sectors. Ekon. Istraz. 2021, 1–32. [Google Scholar] [CrossRef]

- Kleinlercher, K.; Emrich, O.; Herhausen, D.; Verhoef, P.C.; Rudolph, T. Websites as Information Hubs: How Informational Channel Integration and Shopping Benefit Density Interact in Steering Customers to the Physical Store. J. Assoc. Consum. Res. 2018, 3, 330–342. [Google Scholar] [CrossRef]

- Kabadayi, S.; O’Connor, G.E.; Tuzovic, S. Viewpoint: The impact of coronavirus on service ecosystems as service mega-disruptions. J. Serv. Mark. 2020, 34, 809–817. [Google Scholar] [CrossRef]

- Haffke, I.; Kalgovas, B.; Benlian, A. The role of the CIO and the CDO in an Organization’s Digital Transformation. In Proceedings of the 2016 International Conference on Information Systems, ICIS, Dublin, Ireland, 11–14 December 2016. [Google Scholar]

- Reis, J.; Amorim, M.; Melão, N.; Matos, P. Digital Transformation: A Literature Review and Guidelines for Future Research. In Trends and Advances in Information Systems and Technologies. WorldCIST’18 2018. Advances in Intelligent Systems and Computing; Rocha, A., Adeli, H., Reis, L.P., Costanzo, S., Eds.; Springer International Publishing: Cham, Switzerland, 2018; pp. 411–421. [Google Scholar] [CrossRef]

- McDonald, M.P.; Rowsell-Jones, A. The Digital Edge: Exploiting Information & Technology for Business Advantage; Gartner, Inc.: Stamford, CT, USA, 2012. [Google Scholar]

- Cao, L.; Li, L. The Impact of Cross-Channel Integration on Retailers’ Sales Growth. J. Retail. 2015, 91, 198–216. [Google Scholar] [CrossRef]

- Peltola, S.; Vainio, H.; Nieminen, M. Key Factors in Developing Omnichannel Customer Experience with Finnish Retailers; Springer International Publishing: Cham, Switzerland, 2015; Volume 9191, pp. 335–346. [Google Scholar] [CrossRef]

- Domański, R. How to measure omnichannel? Marketing indicator-based approach—Theory fundamentals. Logforum 2021, 17, 373–385. [Google Scholar] [CrossRef]

- Ailawadi, K.L.; Farris, P.W. Managing Multi- and Omni-Channel Distribution: Metrics and Research Directions. J. Retail. 2017, 93, 120–135. [Google Scholar] [CrossRef]

- Patti, C.H.; van Dessel, M.M.; Hartley, S.W. Reimagining customer service through journey mapping and measurement. Eur. J. Mark. 2020, 54, 2387–2417. [Google Scholar] [CrossRef]

- Adivar, B.; Hüseyinoğlu, I.Ö.Y.; Christopher, M. A quantitative performance management framework for assessing omnichannel retail supply chains. J. Retail. Consum. Serv. 2019, 48, 257–269. [Google Scholar] [CrossRef]

- Lee Yohn, D. The Pandemic Is Rewriting the Rules of Retail. Harvard Business Review. July 2020. Available online: https://hbr.org/2020/07/the-pandemic-is-rewriting-the-rules-of-retail (accessed on 7 February 2022).

- Acquila-Natale, E.; Chaparro-Peláez, J. The long road to omni-channel retailing: An assessment of channel integration levels across fashion and apparel retailers. Eur. J. Int. Manag. 2020, 14, 1049–1069. [Google Scholar] [CrossRef]

- Chan-Yeung, M.; Xu, R.H. SARS: Epidemiology. Respirology 2003, 8, S9–S14. [Google Scholar] [CrossRef]

- World Health Organization. MERS Situation Update. September 2019. Available online: http://www.emro.who.int/pandemic-epidemic-diseases/mers-cov/mers-situation-update-september-2019.html (accessed on 7 February 2022).

- World Health Organization. WHO Coronavirus (COVID-19) Dashboard. Available online: https://covid19.who.int/ (accessed on 7 February 2022).

- Jung, H.; Park, M.; Hong, K.; Hyun, E. The Impact of an epidemic outbreak on consumer expenditures: An empirical assessment for MERS Korea. Sustainability 2016, 8, 454. [Google Scholar] [CrossRef] [Green Version]

- Jung, E.; Sung, H. The influence of the Middle East respiratory syndrome outbreak on online and offline markets for retail sales. Sustainability 2017, 9, 411. [Google Scholar] [CrossRef] [Green Version]

- Brem, A.; Viardot, E.; Nylund, P.A. Implications of the coronavirus (COVID-19) outbreak for innovation: Which technologies will improve our lives? Technol. Forecast. Soc. Chang. 2021, 163, 120451. [Google Scholar] [CrossRef]

- Zwanka, R.J.; Buff, C. COVID-19 Generation: A Conceptual Framework of the Consumer Behavioral Shifts to Be Caused by the COVID-19 Pandemic. J. Int. Consum. Mark. 2021, 33, 58–67. [Google Scholar] [CrossRef]

- Lone, S.; Harboul, N.; Weltevreden, J.W.J. European E-Commerce Report; Technical Report; Amsterdam University of Applied Sciences & Ecommerce Europe: Amsterdam, The Netherlands; Brussels, Belgium, 2021. [Google Scholar]

- Urueña, A.; Ballestero, M.P.; Castro, R.; Cadenas, S.; Maira, M.; Prieto, E. El Comercio Electrónico B2C en España 2019; Technical Report; Secretaría General Técnica, Centro de Publicaciones: Madrid, Spain, 2020. [Google Scholar] [CrossRef]

- Velasco, L.; Urueña, A.; Ballestero, M.P. Compras Online en España; Technical Report; Ministerio de Asuntos Económicos y Transformación Digital, Secretaría General Técnica: Madrid, Spain, 2021. [Google Scholar] [CrossRef]

- Jiang, Y.; Stylos, N. Triggers of consumers’ enhanced digital engagement and the role of digital technologies in transforming the retail ecosystem during COVID-19 pandemic. Technol. Forecast. Soc. Chang. 2021, 172, 121029. [Google Scholar] [CrossRef]

- Statista. Ventas del Comercio de la Moda España 2007–2020. 2020. Available online: https://es.statista.com/estadisticas/478927/variacion-interanual-de-las-ventas-del-comercio-de-la-moda-espana/ (accessed on 7 February 2022).

- Rigby, D. The Future of Shopping. Harv. Bus. Rev. 2011, 89, 65–76. [Google Scholar]

- Shi, S.; Wang, Y.; Chen, X.; Zhang, Q. Conceptualization of omnichannel customer experience and its impact on shopping intention: A mixed-method approach. Int. J. Inf. Manag. 2020, 50, 325–336. [Google Scholar] [CrossRef]

- Yumurtacı Hüseyinoğlu, I.Ö.; Galipoğlu, E.; Kotzab, H. Social, local and mobile commerce practices in omni-channel retailing. Int. J. Retail Distrib. Manag. 2017, 45, 711–729. [Google Scholar] [CrossRef]

- We Are Social. Digital 2015: Spain. 2015. Available online: https://datareportal.com/reports/digital-2015-spain (accessed on 7 February 2022).

- We Are Social. Digital 2015: Global Digital Overview. 2015. Available online: https://datareportal.com/reports/digital-2015-global-digital-overview (accessed on 7 February 2022).

- We Are Social. Digital 2021: Spain. 2021. Available online: https://datareportal.com/reports/digital-2021-spain (accessed on 7 February 2022).

- Acebes, B.; Montanera, R. Estudio de Redes Sociales; Technical Report; IAB Spain: Madrid, Spain, 2020. [Google Scholar]

- elEconomista.es. Ranking de Empresas del Sector Comercio al por Menor de Prendas de Vestir en Establecimientos Especializados. 2022. Available online: https://ranking-empresas.eleconomista.es/sector-4771.html (accessed on 15 February 2022).

- Wilson, A.M. The Use of Mystery Shopping in the Measurement of Service Delivery. Serv. Ind. J. 1998, 18, 148–163. [Google Scholar] [CrossRef]

- Peterman, K.; Young, D. Mystery Shopping: An Innovative Method for Observing Interactions With Scientists During Public Science Events. Visit. Stud. 2015, 18, 83–102. [Google Scholar] [CrossRef]

- Mckechnie, D.S.; Grant, J.; Bagaria, V. Observation of listening behaviors in retail service encounters. Manag. Serv. Qual. Int. J. 2007, 17, 116–133. [Google Scholar] [CrossRef]

- Agresti, A. An Introduction to Categorical Data Analysis; JohnWiley & Sons, Inc.: Hoboken, NJ, USA, 2007; p. 373. [Google Scholar]

- Fay, M.P.; Hunsberger, S.A.; Nason, M.; Gabriel, E.; Lumbard, K. exact2x2: Exact Tests and Confidence Intervals for 2x2 Tables Version. 2021. Available online: https://cran.r-project.org/web/packages/exact2x2/exact2x2.pdf (accessed on 11 February 2022).

- Patil, I. Visualizations with statistical details: The ’ggstatsplot’ approach. J. Open Source Softw. 2021, 6, 3167. [Google Scholar] [CrossRef]

- Chaparro-Peláez, J.; Acquila-Natale, E.; Hernández-García, A.; Iglesias-Pradas, S. The Digital Transformation of the Retail Electricity Market in Spain. Energies 2020, 13, 2085. [Google Scholar] [CrossRef] [Green Version]

- Banco de España. Informe Anual 2020; Technical Report; Banco de Espña: Madrid, Spain, 2021. [Google Scholar]

- The Spanish National Markets and Competition Commission. E-Commerce Statistics in Spain via Means-of-Payment Entities; Technical Report; Comisión Nacional de los Mercados y la Competencia: Madrid, Spain, 2022. [Google Scholar]

- EY. Informe Sector Moda en España. Análisis del Impacto de la Crisis del COVID-19; Technical Report; Ernst & Young, S.L.: Madrid, Spain, 2020. [Google Scholar]

- Rosenmayer, A.; McQuilken, L.; Robertson, N.; Ogden, S. Omni-channel service failures and recoveries: Refined typologies using Facebook complaints. J. Serv. Mark. 2018, 32, 269–285. [Google Scholar] [CrossRef]

- Akter, S.; Hossain, T.M.; Strong, C. What omnichannel really means? J. Strateg. Mark. 2021, 29, 567–573. [Google Scholar] [CrossRef]

- Kang, J.Y.M. What drives omnichannel shopping behaviors?: Fashion lifestyle of social-local-mobile consumers. J. Fash. Mark. Manag. 2019, 23, 224–238. [Google Scholar] [CrossRef]

- Ananda, A.S.; Hernández-García, A.; Acquila-Natale, E.; Lamberti, L. What makes fashion consumers “click”? Generation of eWoM engagement in social media. Asia Pac. J. Mark. Logist. 2019, 31, 398–418. [Google Scholar] [CrossRef]

- Enderle, G.; Farsi, A.; Pensky, R.; Stallmann, F. The King is Dead, Long Live the King! Technical Report; EY-Parthenon: Düsseldorf, Germany, 2018. [Google Scholar]

- von Briel, F. The future of omnichannel retail: A four-stage Delphi study. Technol. Forecast. Soc. Chang. 2018, 132, 217–229. [Google Scholar] [CrossRef]

- Bell, D.R.; Gallino, S.; Moreno, A. The store is dead—Long live the store. MIT Sloan Manag. Rev. 2018, 59, 1–8. [Google Scholar]

- Acquila-Natale, E.; Hernández-García, A.; Iglesias-Pradas, S.; Chaparro-Peláez, J. Stay or switch? Investigating lock-in effect in multi-channel apparel retailing. Econ. Bus. Lett. 2020, 9, 298–305. [Google Scholar] [CrossRef]

- Qiu, C.M.; Yang, L. COVID 19’s Impacts on Omni Channel Operations. In The Impact of COVID-19 on E-Commerce; Mazaheri, E., Ed.; Proud Pen: London, UK, 2020. [Google Scholar] [CrossRef]

- Georgiadou, E.; Koopmann, A.; Müller, A.; Leménager, T.; Hillemacher, T.; Kiefer, F. Who Was Shopping More During the Spring Lockdown 2020 in Germany? Front. Psychiatry 2021, 12, 1–9. [Google Scholar] [CrossRef]

- Salvietti, G.; Ziliani, C.; Teller, C.; Ieva, M.; Ranfagni, S. Omnichannel retailing and post-pandemic recovery: Building a research agenda. Int. J. Retail. Distrib. Manag. 2022. [Google Scholar] [CrossRef]

- DataReportal. Global Digital Insights. 2022. Available online: https://datareportal.com/reports/digital-2022-global-overview-report (accessed on 10 February 2022).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).