The Nexus between Formal Credit and E-Commerce Utilization of Entrepreneurial Farmers in Rural China: A Mediation Analysis

Abstract

1. Introduction

2. Theoretical Framework

3. Methodology

3.1. Data Collection

3.2. Variables and Summary Statistics

3.2.1. Dependent Variables

3.2.2. Independent Variables

3.2.3. Control Variables and Mediating Variables

3.3. Model specification

3.3.1. Propensity Score Matching

3.3.2. Mediation Analysis: Bootstrap Method

4. Results and Discussion

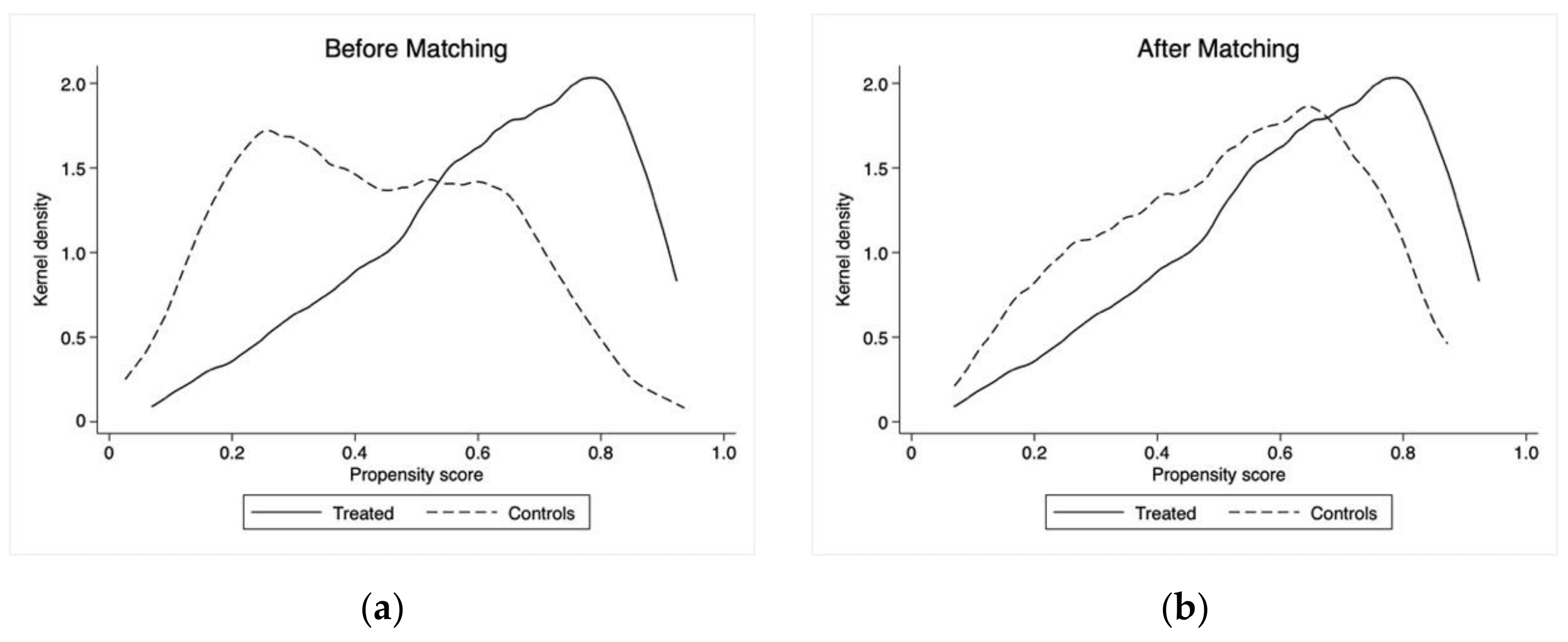

4.1. Common Support Domain and Balance Test

4.2. Treatment Effect Estimation

4.3. Heterogeneity Analysis

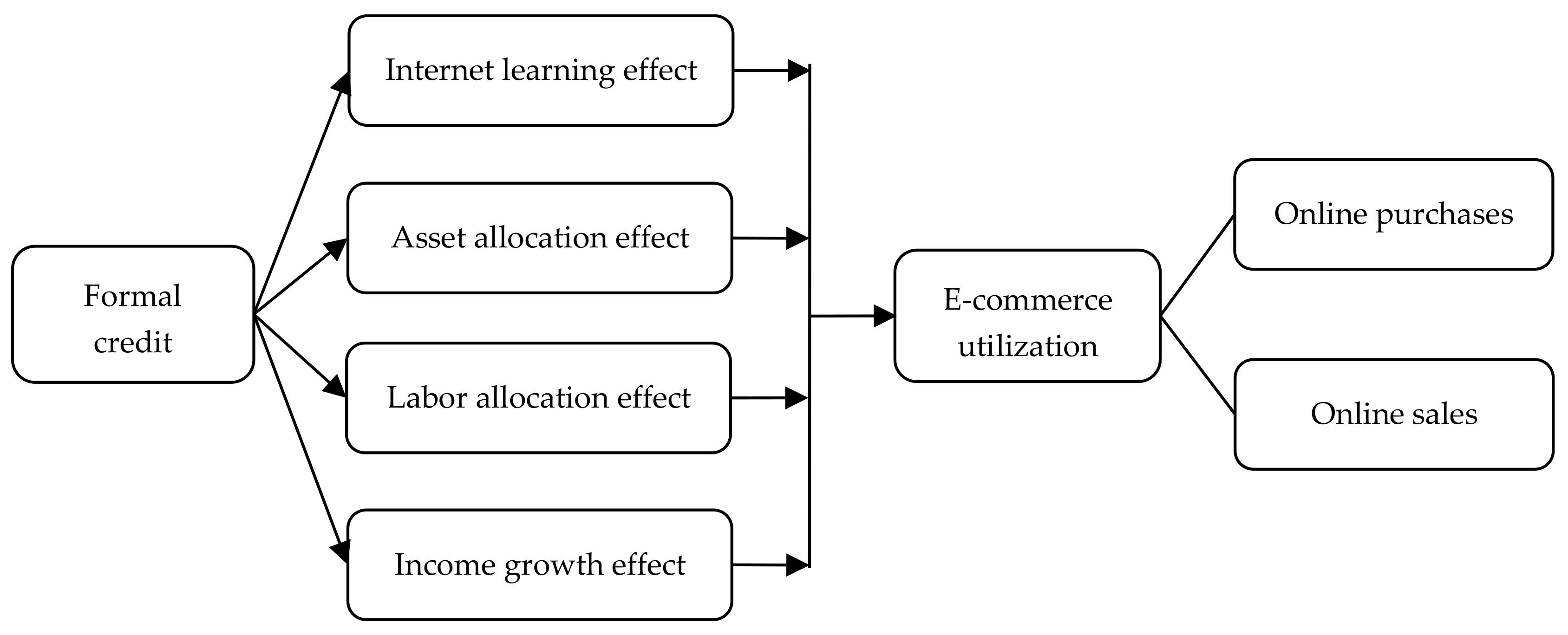

4.4. Mechanism Test Analysis

5. Conclusions and Policy Implications

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variables | Mean | Median | Std | Min | Max |

|---|---|---|---|---|---|

| E-commerce utilization | 0.42 | 0 | 0.49 | 0 | 1.00 |

| Online purchases | 0.23 | 0 | 0.42 | 0 | 1.00 |

| Online sales | 0.35 | 0 | 0.48 | 0 | 1.00 |

| Formal credit participation | 0.51 | 1.00 | 0.50 | 0 | 1.00 |

| Gender | 0.78 | 1.00 | 0.42 | 0 | 1.00 |

| Age | 44.45 | 46.00 | 9.23 | 19.00 | 69.00 |

| Education | 8.94 | 9.00 | 3.28 | 0 | 16.00 |

| Cooperative | 0.36 | 0 | 0.48 | 0 | 1.00 |

| New agricultural business entity | 0.48 | 0 | 0.50 | 0 | 1.00 |

| Social Network | 0.15 | 0 | 0.35 | 0 | 1.00 |

| Distance | 5.50 | 3.50 | 3.66 | 0 | 17.50 |

| Mobile payment | 0.85 | 1.00 | 0.36 | 0 | 1.00 |

| Credit cognition | 3.43 | 4.00 | 1.55 | 1.00 | 5.00 |

| Fund demand | 0.69 | 1.00 | 0.46 | 0 | 1.00 |

| Institution support | 3.57 | 4.00 | 1.03 | 1.00 | 5.00 |

| Internet knowledge | 2.68 | 3.00 | 1.04 | 1.00 | 5.00 |

| Information access | 2.41 | 3.00 | 0.76 | 1.00 | 5.00 |

| Fixed asset | 7.76 | 10.31 | 5.60 | 0 | 17.91 |

| Working capital | 9.32 | 10.60 | 4.18 | 0 | 16.30 |

| Short-term employment | 11.65 | 1.00 | 37.58 | 0 | 500 |

| Long-term employment | 2.59 | 0 | 19.07 | 0 | 50 |

| Gross income | 11.37 | 11.70 | 2.98 | 0 | 18.42 |

| Net income | 10.05 | 10.82 | 3.38 | 0 | 16.12 |

| Observations | 831 |

| Covariate | Coefficient | Marginal Effect |

|---|---|---|

| Gender | 0.4472 *** (0.1342) | 0.0892 *** (0.0269) |

| Age | −0.0169 ** (0.0074) | −0.0033 ** (0.0015) |

| Education | −0.0412 (0.0299) | −0.0082 (0.0059) |

| Cooperative | 0.5188 ** (0.2032) | 0.1035 *** (0.0399) |

| New agricultural business entity | 0.4434 ** (0.2015) | 0.0885 ** (0.0399) |

| Social network | 0.0769 * (0.0463) | 0.0154 * (0.0092) |

| Distance | −0.0597 ** (0.0267) | −0.0119 ** (0.0053) |

| Mobile payment | 0.7005 ** (0.3094) | 0.1398 ** (0.0610) |

| Credit cognition | 0.2880 *** (0.0698) | 0.0575 *** (0.0133) |

| Fund demand | 0.9117 *** (0.2371) | 0.1819 *** (0.0448) |

| Institution support | 0.1232 * (0.0742) | 0.0248 * (0.0148) |

| Internet knowledge | 0.2677 ** (0.1132) | 0.0534 ** (0.0223) |

| Information access | 0.1028 (0.1374) | 0.0205 (0.0274) |

| Fixed asset | 0.0400 ** (0.0171) | 0.0080 ** (0.0034) |

| Working capital | 0.1991 *** (0.0741) | 0.0039 *** (0.0014) |

| Gross income | 0.0702 (0.0511) | 0.0140 (0.0101) |

| Net income | 0.0934 ** (0.0436) | 0.0186 ** (0.0087) |

| Pseudo R2 | 0.1552 | |

| Wald chi2 | 103.65 *** | |

| Log pseudolikelihood | −357.2713 | |

| Observations | 831 | |

References

- Wang, H.; Zhuo, Y. The Necessary Way for the Development of China’s Rural Areas in the New Era-Rural Revitalization Strategy. Open J. Soc. Sci. 2018, 6, 97–106. [Google Scholar] [CrossRef]

- Cai, D.; Song, Q.; Ma, S.; Dong, Y.; Xu, Q. The relationship between credit constraints and household entrepreneurship in China. Int. Rev. Econ. Financ. 2018, 58, 246–258. [Google Scholar] [CrossRef]

- Su, L.; Kong, R. Does Internet Use Improve Rural Households’ Entrepreneurial Performance? An Empirical Analysis Based on Endogenous Switching Regression. Chin. Rural Econ. 2020, 2, 62–88. [Google Scholar]

- Qi, J.; Zheng, X.; Guo, H. The formation of Taobao villages in China. China Econ. Rev. 2019, 53, 106–127. [Google Scholar] [CrossRef]

- Sousa, R.; Horta, C.; Ribeiro, R.; Rabinovich, E. How to serve online consumers in rural markets: Evidence-based recommendations. Bus. Horizons 2020, 63, 351–362. [Google Scholar] [CrossRef]

- Strzębicki, D. The Development of Electronic Commerce in Agribusiness—The Polish Example. Procedia Econ. Finance 2015, 23, 1314–1320. [Google Scholar] [CrossRef]

- Zhou, L.; Wang, W.; Xu, J.; Liu, T.; Gu, J. Perceived information transparency in B2C e-commerce: An empirical investigation. Inf. Manag. 2018, 55, 912–927. [Google Scholar] [CrossRef]

- Hallikainen, H.; Laukkanen, T. National culture and consumer trust in e-commerce. Int. J. Inf. Manag. 2018, 38, 97–106. [Google Scholar] [CrossRef]

- Kurnia, S.; Karnali, R.J.; Rahim, M. A qualitative study of business-to-business electronic commerce adoption within the Indonesian grocery industry: A multi-theory perspective. Inf. Manag. 2015, 52, 518–536. [Google Scholar] [CrossRef]

- Chae, H.-C.; Koh, C.E.; Park, K.O. Information technology capability and firm performance: Role of industry. Inf. Manag. 2018, 55, 525–546. [Google Scholar] [CrossRef]

- Zhang, X.; Zheng, X.; Wu, C.; Tian, D. B2B E-Marketplace Adoption in Agriculture. J. Softw. 2009, 4, 232–239. [Google Scholar] [CrossRef]

- Alavion, J.; Allahyari, M.S. An Overview of the Electronic Agricultural Studies in Trading and Marketing Sections. Agric. Manag. Lucr. Stiintifice Ser. I Manag. Agric. 2012, 14, 123–132. [Google Scholar]

- Lestari, D. Measuring e-commerce adoption behaviour among gen-Z in Jakarta, Indonesia. Econ. Anal. Policy 2019, 64, 103–115. [Google Scholar] [CrossRef]

- Chang, M.K.; Cheung, W.; Lai, V.S. Literature derived reference models for the adoption of online shopping. Inf. Manag. 2005, 42, 543–559. [Google Scholar] [CrossRef]

- Zeng, Y.; Guo, H.; Jin, S. Does E-commerce Increase Farmers’ Income? Evidence from Shuyang County, Jiangsu Province, China. Chin. Rural Econ. 2018, 2, 49–64. [Google Scholar]

- Phang, D.C.; Wang, K.; Wang, Q.; Kauffman, R.J.; Naldi, M. How to derive causal insights for digital commerce in China? A research commentary on computational social science methods. Electron. Commer. Res. Appl. 2019, 35, 100837. [Google Scholar] [CrossRef]

- Martín, S.S.; Camarero, C. How perceived risk affects online buying. Online Inf. Rev. 2009, 33, 629–654. [Google Scholar] [CrossRef]

- Behera, B.S.; Panda, B.; Behera, R.A.; Nayak, N.; Behera, A.C.; Jena, S.K. Information Communication Technology Promoting Retail Marketing in Agriculture Sector in India as a Study. Procedia Comput. Sci. 2015, 48, 652–659. [Google Scholar] [CrossRef]

- Paulson, A.L.; Townsend, R. Entrepreneurship and financial constraints in Thailand. J. Corp. Finance 2004, 10, 229–262. [Google Scholar] [CrossRef]

- Djankov, S.; Qian, Y.; Roland, G.; Zhuravskaya, E. Who Are China’s Entrepreneurs? Am. Econ. Rev. 2006, 96, 348–352. [Google Scholar] [CrossRef]

- Zhang, G. The choice of formal or informal finance: Evidence from Chengdu, China. China Econ. Rev. 2008, 19, 659–678. [Google Scholar] [CrossRef]

- Khoi, P.D.; Gan, C.; Nartea, G.V.; Cohen, D.A. Formal and informal rural credit in the Mekong River Delta of Vietnam: Interaction and accessibility. J. Asian Econ. 2013, 26, 1–13. [Google Scholar] [CrossRef]

- Turvey, C.G.; Kong, R. Informal lending amongst friends and relatives: Can microcredit compete in rural China? China Econ. Rev. 2010, 21, 544–556. [Google Scholar] [CrossRef]

- Wang, Y.; Yu, Z.; Jin, M. E-commerce supply chains under capital constraints. Electron. Commer. Res. Appl. 2019, 35, 100851. [Google Scholar] [CrossRef]

- Anshari, M.; Almunawar, M.N.; Masri, M.; Hamdan, M. Digital Marketplace and FinTech to Support Agriculture Sustainability. Energy Procedia 2019, 156, 234–238. [Google Scholar] [CrossRef]

- Warren, M. The digital vicious cycle: Links between social disadvantage and digital exclusion in rural areas. Telecommun. Policy 2007, 31, 374–388. [Google Scholar] [CrossRef]

- Karaivanov, A.; Kessler, A. (Dis)advantages of informal loans—Theory and evidence. Eur. Econ. Rev. 2018, 102, 100–128. [Google Scholar] [CrossRef]

- Naminse, E.Y.; Zhuang, J. Does farmer entrepreneurship alleviate rural poverty in China? Evidence from Guangxi Province. PLoS ONE 2018, 13, e0194912. [Google Scholar] [CrossRef]

- Zhao, D.; Jiang, J.; Yin, Z. Can entrepreneurship bring happiness? Evidence from China. Econ. Model. 2020, 91, 679–686. [Google Scholar] [CrossRef]

- Yin, Z.; Gong, X.; Guo, P.; Wu, T. What Drives Entrepreneurship in Digital Economy? Evidence from China. Econ. Model. 2019, 82, 66–73. [Google Scholar] [CrossRef]

- Parker, S.C. A Time Series Model of Self-employment under Uncertainty. Economica 1996, 63, 459. [Google Scholar] [CrossRef]

- Ma, H.; Barbe, F.T.; Zhang, Y.C. Can Social Capital and Psychological Capital Improve the Entrepreneurial Performance of the New Generation of Migrant Workers in China? Sustainability 2018, 10, 3964. [Google Scholar] [CrossRef]

- Cloete, E.; Doens, M. B2B e-marketplace adoption in South African agriculture. Inf. Technol. Dev. 2008, 14, 184–196. [Google Scholar] [CrossRef]

- Molla, A.; Peszynski, K.; Pittayachawan, S. The Use of E-Business in Agribusiness: Investigating the Influence of E-Readiness and OTE Factors. J. Glob. Inf. Technol. Manag. 2010, 13, 56–78. [Google Scholar] [CrossRef]

- Rahayu, R.; Day, J. Determinant Factors of E-commerce Adoption by SMEs in Developing Country: Evidence from Indonesia. Procedia Soc. Behav. Sci. 2015, 195, 142–150. [Google Scholar] [CrossRef]

- Wu, W.-Y.; Chang, M.-L. The role of risk attitude on online shopping: Experience, customer satisfaction, and repurchase intention. Soc. Behav. Pers. Int. J. 2007, 35, 453–468. [Google Scholar] [CrossRef]

- Hong, I.B. Understanding the consumer’s online merchant selection process: The roles of product involvement, perceived risk, and trust expectation. Int. J. Inf. Manag. 2015, 35, 322–336. [Google Scholar] [CrossRef]

- Walsh, G.; Schaarschmidt, M.; Ivens, S. Effects of customer-based corporate reputation on perceived risk and relational outcomes: Empirical evidence from gender moderation in fashion retailing. J. Prod. Brand Manag. 2017, 26, 227–238. [Google Scholar] [CrossRef]

- Aji, J.M.M. Exploring Farmer-supplier Relationships in the East Java Seed Potato Market. Agric. Agric. Sci. Procedia 2016, 9, 83–94. [Google Scholar] [CrossRef]

- Batte, M.T.; Ernst, S. Net Gains from ’Net Purchases? Farmers’ Preferences for Online and Local Input Purchases. Agric. Resour. Econ. Rev. 2007, 36, 84–94. [Google Scholar] [CrossRef]

- Smith, A.D.; Paul, C.J.M.; Goe, W.R.; Kenney, M. Computer and Internet Use by Great Plains Farmers. SSRN Electron. J. 2004, 29. [Google Scholar] [CrossRef]

- Briggeman, B.; Whitacre, B. Farming and the Internet: Reasons for Non-Use. Agric. Resour. Econ. Rev. 2010, 39, 571–583. [Google Scholar] [CrossRef]

- Mishra, A.K.; Williams, R.P.; Detre, J.D. Internet Access and Internet Purchasing Patterns of Farm Households. Agric. Resour. Econ. Rev. 2009, 38, 240–257. [Google Scholar] [CrossRef]

- Fecke, W.; Danne, M.; Musshoff, O. E-commerce in agriculture—The case of crop protection product purchases in a discrete choice experiment. Comput. Electron. Agric. 2018, 151, 126–135. [Google Scholar] [CrossRef]

- Zwass, V. Structure and Macro-Level Impacts of Electronic Commerce: From Technological Infrastructure to Electronic Marketplaces. In Emerging Information Technologies: Improving Decisions, Cooperation, and Infrastructure; Sage: Beverly Hills, CA, USA, 2014; pp. 289–316. [Google Scholar]

- Dinu, G.; Dinu, L. Using Internet as a Commercial Tool: A Case Study of E-Commerce in Resita. Procedia Eng. 2014, 69, 469–476. [Google Scholar] [CrossRef]

- Fruhling, A.; Digman, L. The impact of electronic commerce on business-level strategies. J. Electron. Commer. Res. 2000, 1, 13. [Google Scholar]

- Zapata, S.D.; Carpio, C.; Isengildina, O.; Lamie, D. The Economic Impact of Services Provided by an Electronic Trade Platform: The Case of MarketMaker. J. Agric. Resour. Econ. 2013, 38, 359–378. [Google Scholar] [CrossRef]

- Lin, H.; Li, R.; Hou, S.; Li, W. Influencing factors and empowering mechanism of participation in e-commerce: An empirical analysis on poor households from Inner Mongolia, China. Alex. Eng. J. 2021, 60, 95–105. [Google Scholar] [CrossRef]

- Korsgaard, S.; Müller, S.; Tanvig, H.W. Rural entrepreneurship or entrepreneurship in the rural—between place and space. Int. J. Entrep. Behav. Res. 2015, 21, 5–26. [Google Scholar] [CrossRef]

- Feder, G.; Just, R.E.; Zilberman, D. Adoption of Agricultural Innovations in Developing Countries: A Survey. Econ. Dev. Cult. Chang. 1985, 33, 255–298. [Google Scholar] [CrossRef]

- Porgo, M.; Kuwornu, J.K.; Zahonogo, P.; Jatoe, J.B.D.; Egyir, I.S. Credit constraints and cropland allocation decisions in rural Burkina Faso. Land Use Policy 2018, 70, 666–674. [Google Scholar] [CrossRef]

- Jamaluddin, N. Adoption of E-commerce Practices among the Indian Farmers, a Survey of Trichy District in the State of Tamilnadu, India. Procedia Econ. Finance 2013, 7, 140–149. [Google Scholar] [CrossRef]

- Ma, W.; Zhou, X.; Liu, M. What drives farmers’ willingness to adopt e-commerce in rural China? The role of Internet use. Agribusiness 2020, 36, 159–163. [Google Scholar] [CrossRef]

- Barnett, W.A.; Hu, M.; Wang, X. Does the utilization of information communication technology promote entrepreneurship: Evidence from rural China. Technol. Forecast. Soc. Chang. 2019, 141, 12–21. [Google Scholar] [CrossRef]

- Lokers, R.; Knapen, R.; Janssen, S.; Van Randen, Y.; Jansen, J. Analysis of Big Data technologies for use in agro-environmental science. Environ. Model. Softw. 2016, 84, 494–504. [Google Scholar] [CrossRef]

- Lin, J.-H.; Jou, R. Financial e-commerce under capital regulation and deposit insurance. Int. Rev. Econ. Finance 2005, 14, 115–128. [Google Scholar] [CrossRef]

- Tang, R.; Yang, L. Financing strategy in fresh product supply chains under e-commerce environment. Electron. Commer. Res. Appl. 2020, 39, 100911. [Google Scholar] [CrossRef]

- Carrer, M.J.; Maia, A.G.; Vinholis, M.D.M.B.; Filho, H.M.D.S. Assessing the effectiveness of rural credit policy on the adoption of integrated crop-livestock systems in Brazil. Land Use Policy 2020, 92, 104468. [Google Scholar] [CrossRef]

- Doherty, B.; Haugh, H.; Lyon, F. Social Enterprises as Hybrid Organizations: A Review and Research Agenda. Int. J. Manag. Rev. 2014, 16, 417–436. [Google Scholar] [CrossRef]

- Swaminathan, H.; Du Bois, R.S.; Findeis, J.L. Impact of Access to Credit on Labor Allocation Patterns in Malawi. World Dev. 2010, 38, 555–566. [Google Scholar] [CrossRef]

- Dias, C.S.; Rodrigues, R.G.; Ferreira, J.J. What’s new in the research on agricultural entrepreneurship? J. Rural. Stud. 2019, 65, 99–115. [Google Scholar] [CrossRef]

- Akhtar, S.; Li, G.-C.; Nazir, A.; Razzaq, A.; Ullah, R.; Faisal, M.; Naseer, M.A.U.R.; Raza, M.H. Maize production under risk: The simultaneous adoption of off-farm income diversification and agricultural credit to manage risk. J. Integr. Agric. 2019, 18, 460–470. [Google Scholar] [CrossRef]

- Li, X.; Guo, H.; Jin, S.; Ma, W.; Zeng, Y. Do farmers gain internet dividends from E-commerce adoption? Evidence from China. Food Policy 2021, 102024, 102024. [Google Scholar] [CrossRef]

- Ma, S.; Wu, X.; Gan, L. Credit accessibility, institutional deficiency and entrepreneurship in China. China Econ. Rev. 2019, 54, 160–175. [Google Scholar] [CrossRef]

- Wang, H.; Kong, R. Does Formal Lending Promote Rural Households’ Consumption? An Empirical Analysis based on PSM Method. Chin. Rural Econ. 2019, 08, 72–90. [Google Scholar]

- Su, L.; Kong, R. Does Farmland Mortgage Loans Promote Farmers’Entrepreneurial Decision? Deviation Test between the Expectation and Implementation Effect of Farmland Mortgage Loans Policy. China Soft Sci. 2018, 12, 140–156. [Google Scholar]

- Becerril, J.; Abdulai, A. The Impact of Improved Maize Varieties on Poverty in Mexico: A Propensity Score-Matching Approach. World Dev. 2010, 38, 1024–1035. [Google Scholar] [CrossRef]

- Rebonato, R. Mostly Harmless Econometrics: An Empiricist’s Companion; Mastering ‘Metrics: The Path from Cause to Effect. Quant. Finance 2015, 16, 1009–1013. [Google Scholar] [CrossRef]

- Caliendo, M.; Kopeinig, S. Some Practical Guidance for the Implementation of Propensity Score Mateching. J. Econ. Surv. 2008, 22, 31–72. [Google Scholar] [CrossRef]

- Stuart, E.A. Matching Methods for Causal Inference: A Review and a Look Forward. Stat. Sci. 2010, 25, 1–21. [Google Scholar] [CrossRef]

- Estifanos, T.K.; Polyakov, M.; Pandit, R.; Hailu, A.; Burton, M. The impact of protected areas on the rural households’ incomes in Ethiopia. Land Use Policy 2020, 91, 104349. [Google Scholar] [CrossRef]

- Balaine, L.; Dillon, E.J.; Läpple, D.; Lynch, J. Can technology help achieve sustainable intensification? Evidence from milk recording on Irish dairy farms. Land Use Policy 2020, 92, 104437. [Google Scholar] [CrossRef] [PubMed]

- Baron, R.; Kenny, D. The Moderator-Mediator Variable Distinction in Social Psychological Research. J. Personal. Soc. Psychol. 1987, 51, 1173–1182. [Google Scholar] [CrossRef]

- Preacher, K.J.; Hayes, A.F. SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behav. Res. Methods Instrum. Comput. 2004, 36, 717–731. [Google Scholar] [CrossRef]

- Dehejia, R.H.; Wahba, S. Propensity Score-Matching Methods for Nonexperimental Causal Studies. Rev. Econ. Stat. 2002, 84, 151–161. [Google Scholar] [CrossRef]

- Lechner, M. A Note on the Common Support Problem in Applied Evaluation Studies. SSRN Electron. J. 2001, 91–92. [Google Scholar] [CrossRef]

- Rosenbaum, P.R.; Rubin, D.B. The central role of the propensity score in observational studies for causal effects. Biometrika 1983, 70, 41–55. [Google Scholar] [CrossRef]

- Yang, H.; Miao, L.; Zhao, C. The credit strategy of a green supply chain based on capital constraints. J. Clean. Prod. 2019, 224, 930–939. [Google Scholar] [CrossRef]

- Mei, Y.; Mao, D.; Lu, Y.; Chu, W. Effects and mechanisms of rural E-commerce clusters on households’ entrepreneurship behavior in China. Growth Chang. 2020, 51, 1588–1610. [Google Scholar] [CrossRef]

- Armey, L.; Vladar, A.; Pereira, F. Are phones fun? Usage and barriers to adoption for wireless data services among the younger generation of Asians. Int. J. Electron. Bus. 2011, 9, 8. [Google Scholar] [CrossRef]

- Gerpott, T.J.; Thomas, S.; Weichert, M. Personal characteristics and mobile Internet use intensity of consumers with computer-centric communication devices: An exploratory empirical study of iPad and laptop users in Germany. Telemat. Inform. 2013, 30, 87–99. [Google Scholar] [CrossRef]

- Lin, Q.L.; Zhu, J. A Study on the Strategy of Developing New Agricultural Management Business Entity in North-west Poverty-stricken Area. In Proceedings of the 2nd International Conference on Economics and Management, Education, Humanities and Social Sciences (EMEHSS 2018), Wuhan, China, 29–30 March 2018. [Google Scholar]

- Yang, W.; Yan, W. Analysis on Function Orientation and Development Countermeasures of New Agricultural Business Entities. J. Northeast. Agric. Univ. 2016, 23, 82–88. [Google Scholar] [CrossRef]

- Lim, S.H.; Kim, D.J.; Hur, Y.; Park, K. An Empirical Study of the Impacts of Perceived Security and Knowledge on Continuous Intention to Use Mobile Fintech Payment Services. Int. J. Hum. Comput. Interact. 2019, 35, 886–898. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Park, J.; Ahn, J.; Thavisay, T.; Ren, T. Examining the role of anxiety and social influence in multi-benefits of mobile payment service. J. Retail. Consum. Serv. 2019, 47, 140–149. [Google Scholar] [CrossRef]

- Beck, T.; Lu, L.; Yang, R. Finance and Growth for Microenterprises: Evidence from Rural China. World Dev. 2015, 67, 38–56. [Google Scholar] [CrossRef]

| Variables | Description | Credit Group (n = 422) | Non-Credit Group (n = 409) | Differences |

|---|---|---|---|---|

| E-commerce utilization | =1 if they use the internet to purchase raw materials or sell agricultural products; =0 otherwise | 0.50 (0.50) | 0.34 (0.47) | 0.16 *** |

| Online purchases | =1 if they use the internet to purchase raw materials; =0 otherwise | 0.29 (0.46) | 0.18 (0.38) | 0.11 *** |

| Online sales | =1 if they use the internet to sell products; =0 otherwise | 0.41 (0.49) | 0.29 (0.46) | 0.12 *** |

| Gender | =1 if male; =0 if female | 0.84 (0.37) | 0.71 (0.45) | 0.13 *** |

| Age | Farmers’ age in years | 43.25 (8.84) | 45.68 (9.48) | −2.43 *** |

| Education | Farmers’ education in years | 9.19 (3.16) | 8.67 (3.38) | 0.52 *** |

| Cooperative | =1 if they joined a cooperative; =0 otherwise | 0.46 (0.50) | 0.27 (0.44) | 0.19 *** |

| New agricultural business entity | =1 if recognized as a new agricultural business entity; =0 otherwise | 0.56 (0.50) | 0.39 (0.49) | 0.17 *** |

| Social network | =1 if relatives or friends work in financial institutions; =0 otherwise | 0.18 (0.39) | 0.11 (0.32) | 0.07 *** |

| Distance | Distance from home to financial institution (Unit: kilometer) | 4.78 (3.53) | 5.24 (3.77) | −0.46 * |

| Mobile payment | =1 if they use mobile payment; =0 otherwise | 0.91 (0.28) | 0.78 (0.42) | 0.13 *** |

| Credit cognition | “I am very familiar with formal credit and related policies.” | 3.44 (1.52) | 3.42 (1.59) | 0.02 |

| Fund demand | =1 if have fund demand; 0 = otherwise | 0.78 (0.41) | 0.58 (0.59) | 0.20 *** |

| Institution support | “I think local financial institutions are highly motivated to handle loan business.” | 3.63 (1.00) | 3.52 (1.06) | 0.11 |

| Internet knowledge | “I know a great deal about the internet.” | 2.92 (0.97) | 2.41 (1.06) | 0.51 *** |

| Information access | “I often get valuable information from smartphones and the internet.” | 2.52 (0.69) | 2.29 (0.81) | 0.23 *** |

| Fixed asset | The natural logarithm of investment in fixed assets within past three years | 8.63 (5.47) | 6.87 (5.61) | 0.76 *** |

| Working capital | The natural logarithm of working capital annually | 9.71 (4.05) | 8.94 (4.28) | 0.77 *** |

| Short-term employment | Number of short-term employees in 2017 | 14.34 (39.20) | 8.85 (35.65) | 5.49 *** |

| Long-term employment | Number of long-term employees in 2017 | 3.77 (25.99) | 1.37 (6.14) | 2.40 *** |

| Gross income | The natural logarithm of entrepreneurship gross income in 2017 | 11.84 (2.84) | 10.82 (3.05) | 1.02 *** |

| Net income | The natural logarithm of entrepreneurship net income in 2017 | 10.30 (3.47) | 9.76 (3.26) | 0.54 *** |

| Method | Ps R2 | LR Chi2 | p > Chi2 | MeanBias | MedBias |

|---|---|---|---|---|---|

| Unmatched | 0.155 | 131.23 | 0.000 | 29.1 | 31.0 |

| Nearest neighbor matching | 0.020 | 18.49 | 0.359 | 6.5 | 6.0 |

| Caliper matching | 0.014 | 12.94 | 0.740 | 5.4 | 4.4 |

| Nearest neighbor matching with caliper | 0.019 | 16.75 | 0.472 | 6.1 | 4.4 |

| Kernel matching | 0.015 | 13.93 | 0.672 | 5.5 | 4.3 |

| Spline matching | 0.019 | 16.38 | 0.497 | 7.9 | 6.1 |

| Mahalanobis matching | 0.020 | 18.25 | 0.373 | 8.9 | 5.4 |

| Matching Method | Treated | Controls | ATT | S.E. | T-Stat |

|---|---|---|---|---|---|

| Nearest neighbor matching | 0.5138 | 0.3267 | 0.1871 *** | 0.0393 | 4.76 |

| Caliper matching | 0.5122 | 0.3216 | 0.1906 *** | 0.0392 | 4.86 |

| Nearest neighbor matching with caliper | 0.5122 | 0.3265 | 0.1857 *** | 0.0384 | 4.83 |

| Kernel matching | 0.5123 | 0.3334 | 0.1789 *** | 0.0379 | 4.72 |

| Spline matching | 0.5138 | 0.3265 | 0.1873 *** | 0.0387 | 4.83 |

| Mahalanobis matching | 0.5127 | 0.3376 | 0.1751 *** | 0.0390 | 4.49 |

| Average | 0.1841 | ||||

| Matching Method | Treated | Controls | ATT | S.E. | T-Stat |

|---|---|---|---|---|---|

| Nearest neighbor matching | 0.2883 | 0.1713 | 0.1170 *** | 0.0416 | 2.81 |

| Caliper matching | 0.2892 | 0.1809 | 0.1083 ** | 0.0468 | 2.31 |

| Nearest neighbor matching with caliper | 0.2892 | 0.1718 | 0.1174 *** | 0.0421 | 2.78 |

| Kernel matching | 0.2892 | 0.1803 | 0.1089 ** | 0.0459 | 2.37 |

| Spline matching | 0.2883 | 0.1806 | 0.1077 ** | 0.0457 | 2.35 |

| Mahalanobis matching | 0.2887 | 0.1792 | 0.1095 ** | 0.0459 | 2.39 |

| Average | 0.1115 | ||||

| Matching Method | Treated | Controls | ATT | S.E. | T-Stat |

|---|---|---|---|---|---|

| Nearest neighbor matching | 0.4202 | 0.2762 | 0.1440 ** | 0.0575 | 2.50 |

| Caliper matching | 0.4215 | 0.2769 | 0.1446 ** | 0.0571 | 2.53 |

| Nearest neighbor matching with caliper | 0.4218 | 0.2810 | 0.1408 *** | 0.0538 | 2.62 |

| Kernel matching | 0.4213 | 0.2649 | 0.1564 *** | 0.0523 | 2.99 |

| Spline matching | 0.4201 | 0.2775 | 0.1426 *** | 0.0549 | 2.60 |

| Mahalanobis matching | 0.4221 | 0.2694 | 0.1527 *** | 0.0569 | 2.69 |

| Average | 0.1469 | ||||

| Variables | Standard | E-Commerce | Online Purchases | Online Sales | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| ATT | S.E. | T-Stat | ATT | S.E. | T-stat | ATT | S.E. | T-Stat | ||

| [19,39) | 0.1399 * | 0.0796 | 1.76 | 0.1765 ** | 0.0744 | 2.37 | 0.0992 | 0.0808 | 1.23 | |

| Age | [40,54) | 0.1217 ** | 0.0507 | 2.40 | 0.0830 * | 0.0437 | 1.90 | 0.0595 | 0.0635 | 0.94 |

| [55,69) | 0.0268 | 0.1258 | 0.21 | 0.0362 | 0.0780 | 0.47 | 0.0207 | 0.0917 | 0.23 | |

| New agricultural | Yes | 0.2175 *** | 0.0585 | 3.72 | 0.1358 *** | 0.0521 | 2.60 | 0.1938 *** | 0.0575 | 3.37 |

| business entity | No | 0.0606 | 0.0675 | 0.09 | 0.0492 | 0.0575 | 0.86 | 0.0855 | 0.0531 | 1.61 |

| Mobile | Yes | 0.1522 *** | 0.0441 | 3.45 | 0.0944 ** | 0.0394 | 2.40 | 0.1106 ** | 0.0435 | 2.54 |

| payment | No | 0.0875 | 0.0773 | 1.13 | 0.0090 | 0.0410 | 0.22 | 0.0375 | 0.0611 | 0.61 |

| Channel | Variables | Direct Effect | p Value | Indirect Effect | LLCI | ULCI |

|---|---|---|---|---|---|---|

| Internet learning effect | Internet knowledge | 0.0382 | 0.0234 | 0.0114 | 0.0045 | 0.0213 |

| Information access | 0.0364 | 0.0096 | 0.0032 | −0.0027 | 0.0104 | |

| Asset allocation effect | Fixed asset | 0.0334 | 0.0154 | 0.0032 | 0.0005 | 0.0082 |

| Working capital | 0.0312 | 0.0250 | 0.0065 | 0.0021 | 0.0133 | |

| Labor allocation effect | Short-term employment | 0.0038 | 0.0148 | 0.0016 | −0.0016 | 0.0066 |

| Long-term employment | 0.0315 | 0.0233 | 0.0105 | 0.0014 | 0.0452 | |

| Income growth effect | Gross income | 0.0401 | 0.0160 | 0.0077 | 0.0022 | 0.0178 |

| Net income | 0.0420 | 0.0111 | 0.0059 | 0.0015 | 0.0133 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, S.; Wang, H.; Wang, Z.; Koondhar, M.A.; Ji, L.; Kong, R. The Nexus between Formal Credit and E-Commerce Utilization of Entrepreneurial Farmers in Rural China: A Mediation Analysis. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 900-921. https://doi.org/10.3390/jtaer16040051

Yang S, Wang H, Wang Z, Koondhar MA, Ji L, Kong R. The Nexus between Formal Credit and E-Commerce Utilization of Entrepreneurial Farmers in Rural China: A Mediation Analysis. Journal of Theoretical and Applied Electronic Commerce Research. 2021; 16(4):900-921. https://doi.org/10.3390/jtaer16040051

Chicago/Turabian StyleYang, Shaoxiong, Huiling Wang, Zhengxiao Wang, Mansoor Ahmed Koondhar, Linxue Ji, and Rong Kong. 2021. "The Nexus between Formal Credit and E-Commerce Utilization of Entrepreneurial Farmers in Rural China: A Mediation Analysis" Journal of Theoretical and Applied Electronic Commerce Research 16, no. 4: 900-921. https://doi.org/10.3390/jtaer16040051

APA StyleYang, S., Wang, H., Wang, Z., Koondhar, M. A., Ji, L., & Kong, R. (2021). The Nexus between Formal Credit and E-Commerce Utilization of Entrepreneurial Farmers in Rural China: A Mediation Analysis. Journal of Theoretical and Applied Electronic Commerce Research, 16(4), 900-921. https://doi.org/10.3390/jtaer16040051