Advancing Sustainability Through Industrial Symbiosis: A Technoeconomic Approach Using Material Flow Cost Accounting and Cost–Benefit Analysis

, , , , , , and

, , , , , , and

Abstract

:1. Introduction

2. MFCA, CAPEX, and OPEX Within Industrial Symbiosis: State of the Art

3. Scope of the Current Work and Strategy Planned

3.1. Model Background

3.2. Model Description and Adaptation for IS Assessment

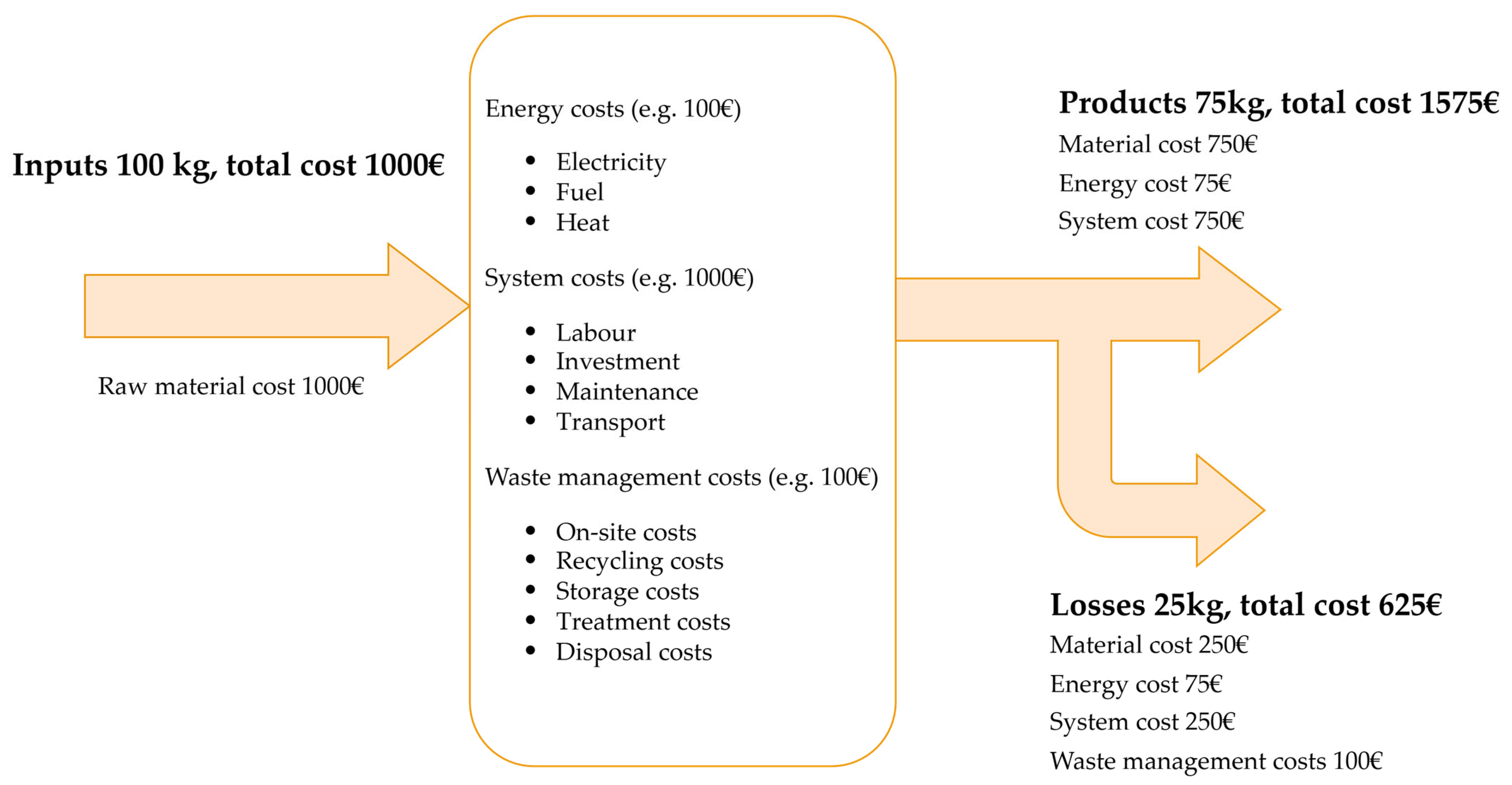

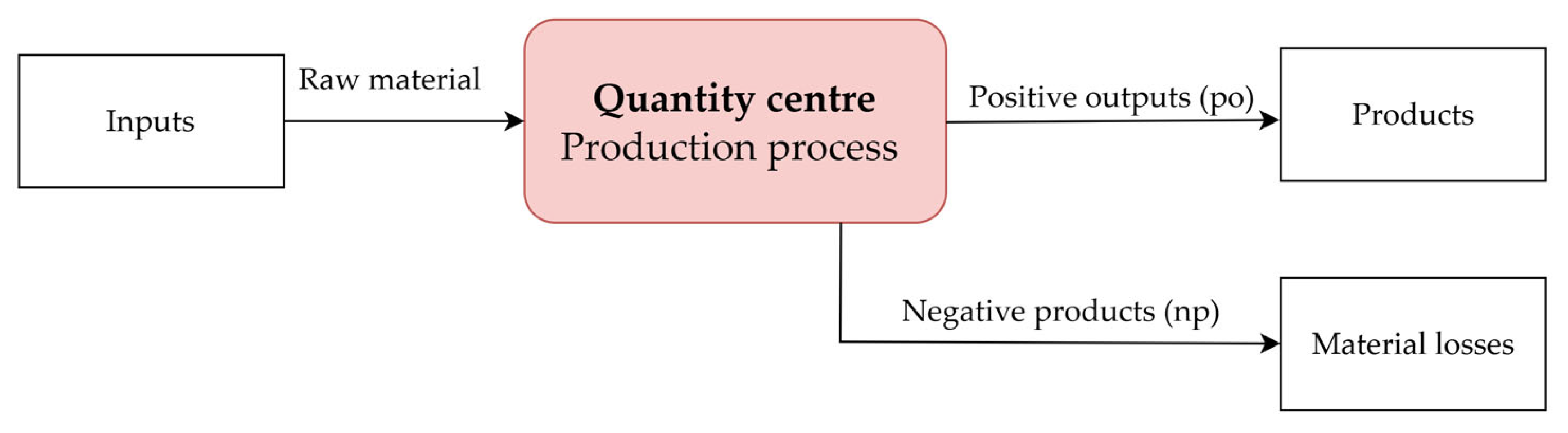

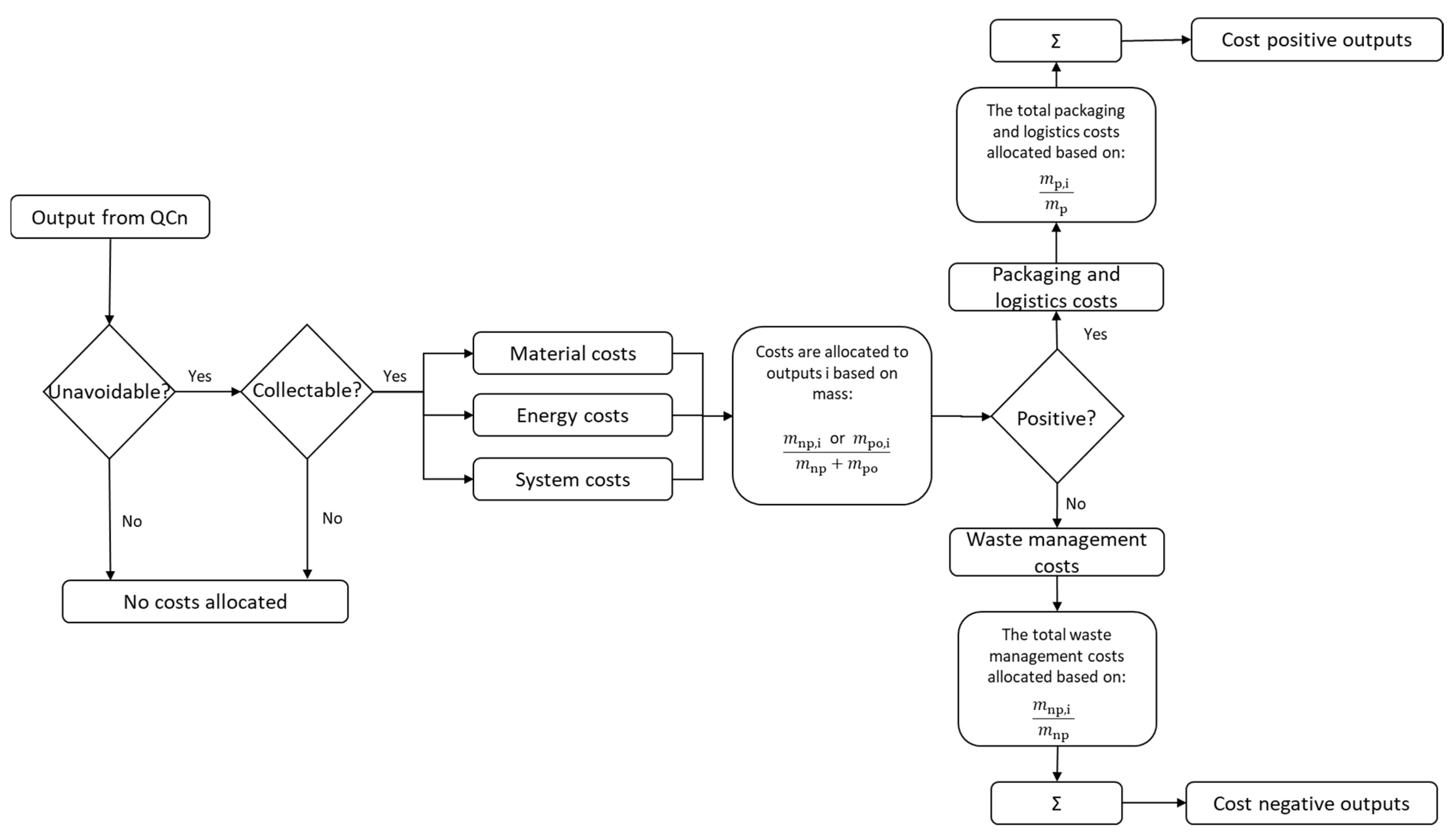

3.2.1. Quantity Centres

3.2.2. Allocation Methods

3.2.3. From Material and Energy Balance to Cost Balance

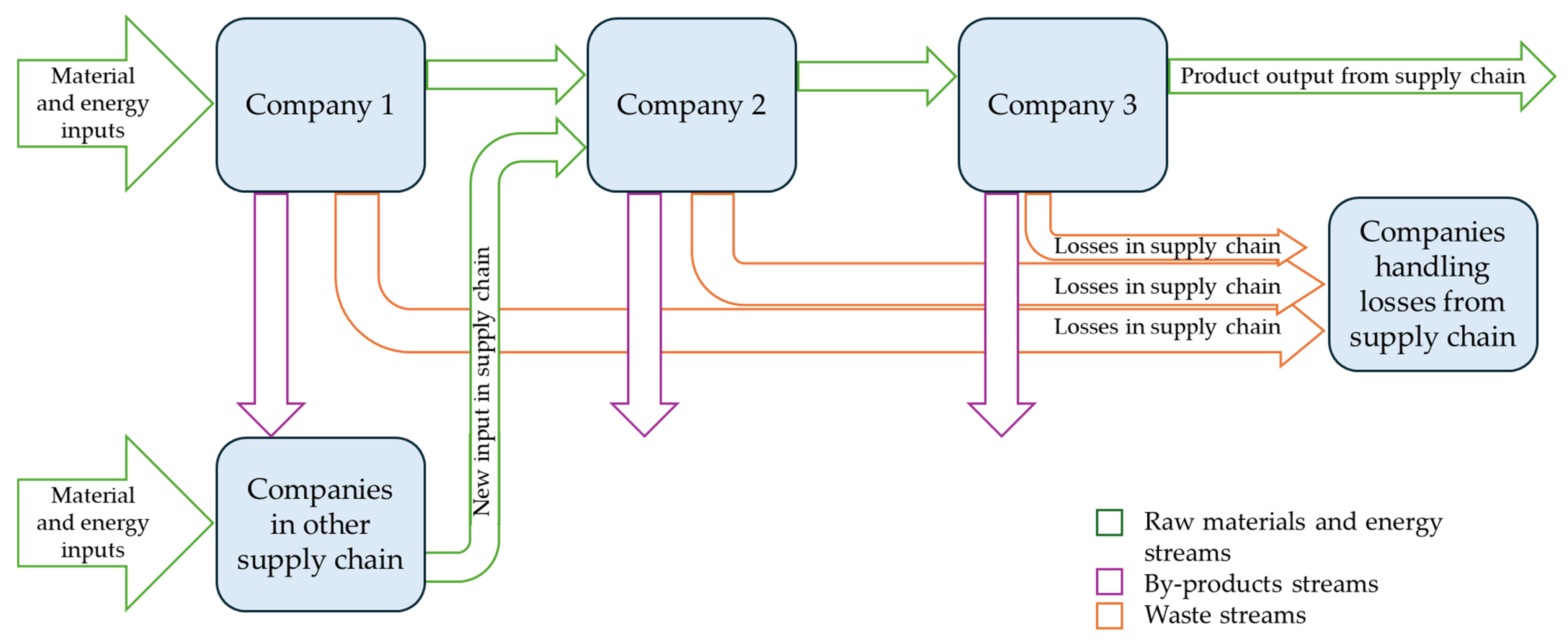

3.2.4. Expanding from Single Organisations to Interlinked Systems

4. MFCA Methodology on IS

- Definition of the baseline configurations: identify the targeted processes impacted by IS actions at each demo site. For Escombreras, this includes processes within the fertiliser production chain, while, in Frövi, the focus is on utilising residual heat from the pulp and paper industry for heating a tomato greenhouse to reduce fossil fuel consumption. Check existing piping and instrumentation diagrams (P&IDs) for current processes and collect historical data where available. Set process boundaries to limit the scope of analysis to processes affected by IS upgrades. Characterise target streams in terms of material and energy flows, composition, temperature, and pressure.

- Establishment of a block diagram: develop a diagram that includes all relevant process units and the material and energy flow connections between them. This will serve as the foundation for both demo sites to visualise their unique process interconnections.

- Definition of quantity centres (QC): group process units into QCs that represent specific roles in the overall process. In Escombreras, QCs may include fertiliser production units, while, in Frövi, they may involve heat recovery systems and greenhouse operations.

- Matching of flows, units, and streams characterisation: develop a matching matrix linking inflows and outflows to their corresponding processes or control units. This matrix allows for calculating losses and inefficiencies in each process stage, tailored to the operational characteristics of each demo site.

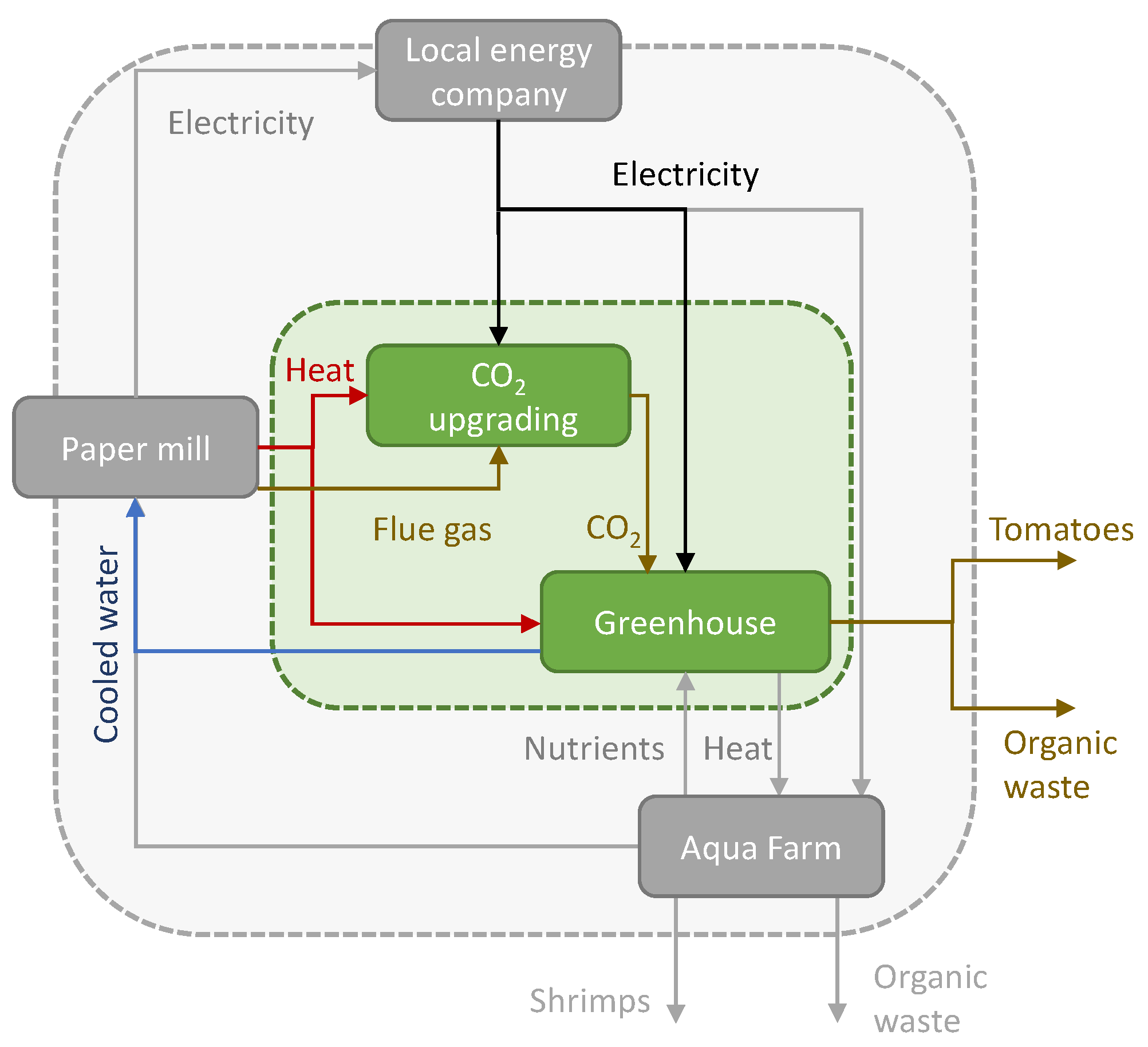

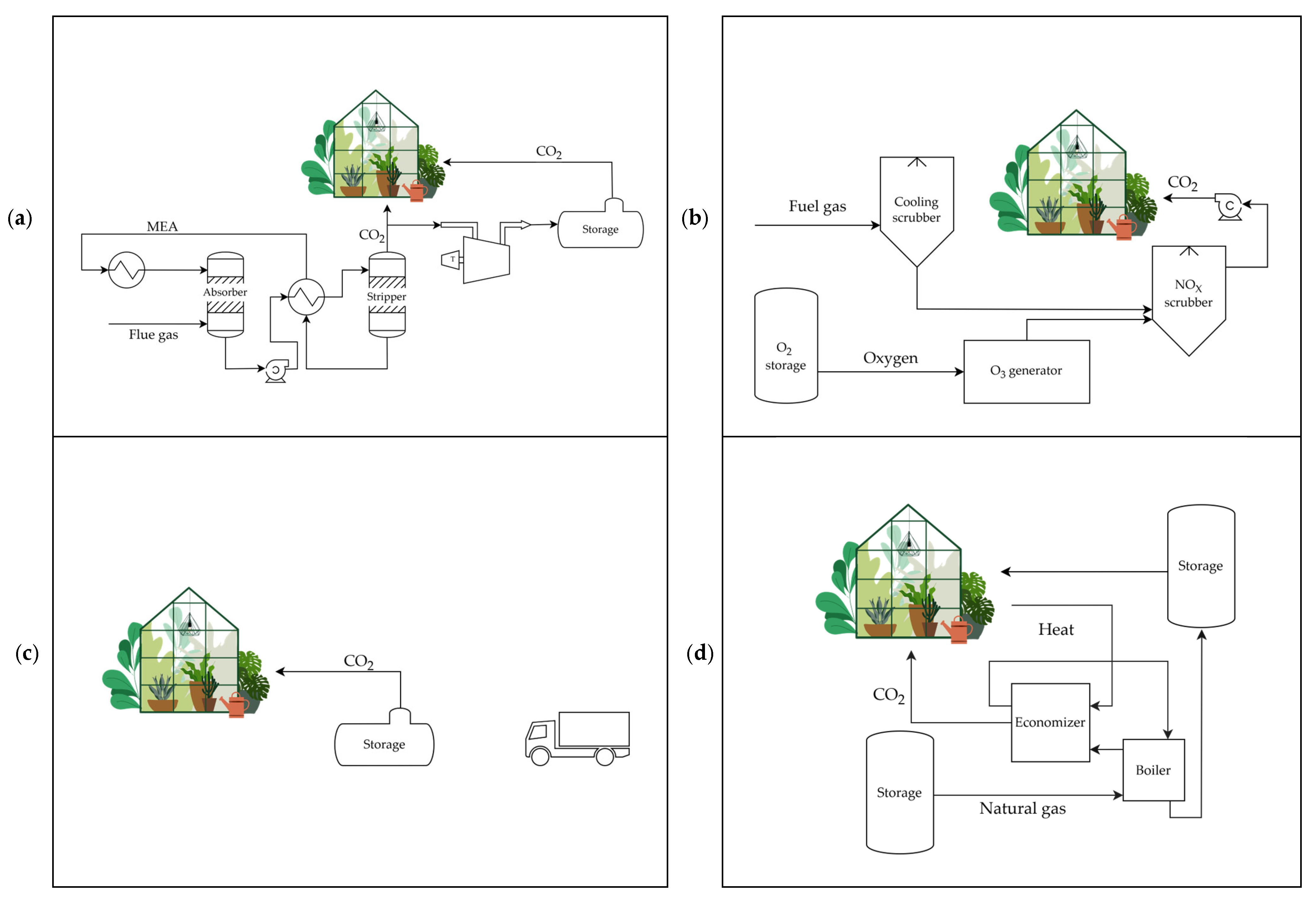

- Identification of waste streams: use the matching matrix to identify two key outputs: (a) material losses, calculated through mass balances for each substance in a control unit. (b) Energy balances, including electrical contributions (e.g., pumping and stirring) and thermal contributions (e.g., heating and refrigeration). In Frövi, this step focused on capturing the thermal energy flow from industrial processes to the greenhouse.

- Transformation of material loss and energy inputs into monetary units: convert material losses and energy consumption into monetary values. For Escombreras, this may include electricity costs for fertiliser production, while, in Frövi, it involves calculating the monetary value of residual heat compared to the cost of fossil fuels that would otherwise be required for greenhouse heating.

- Characterisation of the IS solution: repeat steps 1 to 6 for the proposed IS scenarios, incorporating necessary assumptions. In Escombreras, this might involve optimising fertiliser by-products, while, in Frövi, it focuses on integrating residual heat into the greenhouse heating systems, considering potential investments in heat transfer infrastructure.

- Reporting of MFCA results: present results using Sankey diagrams to visualise material and energy flows and their associated costs. The diagrams will highlight the cost proportions for QCs, material losses, and energy flows, aiding stakeholders in understanding process efficiency improvements.

- Calculation of CAPEX and OPEX for the processes involved in both current and IS solutions: assess the capital and operational expenditures for both the baseline and IS scenarios. In Escombreras, this might include only partially amortised equipment, whereas, in Frövi, new investments in heat exchange and transfer systems could be evaluated.

- Establishment of guidelines for waste materials and energy exchange pricing: couple MFCA results with traditional cost–benefit analyses (CBA) to establish pricing guidelines for waste and energy exchanges. For Frövi, this step includes evaluating the economic benefits of residual heat utilisation versus conventional fossil fuel heating costs, ensuring mutually beneficial agreements for all stakeholders involved.

5. Overview of IS Case Studies

5.1. Spanish Demo-Site Description

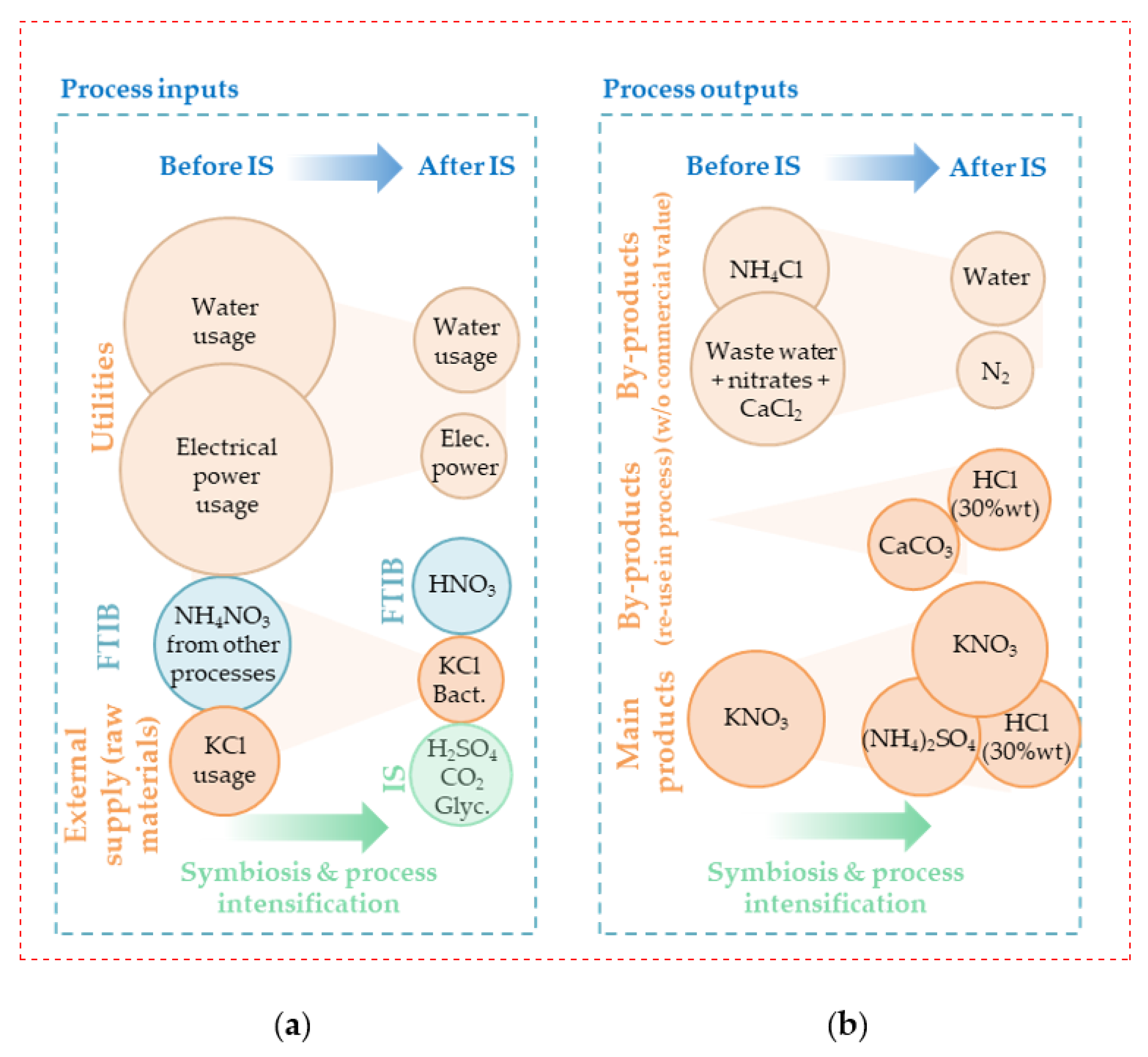

- High aqueous dilution requirements: the process requires a significant dilution ratio of KNO3 to H2O (1:5), which hinders efficiency.

- Elevated energy consumption: the pumping and cooling of the highly diluted product stream demand substantial energy input, mainly for the separation of KNO3 from the by-product (NH4Cl).

- Generation of a low-value by-product: ammonium chloride (NH4Cl) is produced as a by-product of the reaction of ammonium nitrate (NH4NO3) and potassium chloride (KCl), offering little to no commercial value.

- Wastewater challenges: the production of strontium salts generates calcium chloride (CaCl2) as a secondary by-product due to the use of hydrochloric acid (HCl) in leaching operations. This CaCl2 is partially discharged in wastewater, where it interacts with sulphate salts from neighbouring industries, forming calcium sulphate (CaSO4) and causing clogging issues in the general wastewater discharge system.

5.2. Swedish Demo-Site Description

6. MFCA Results

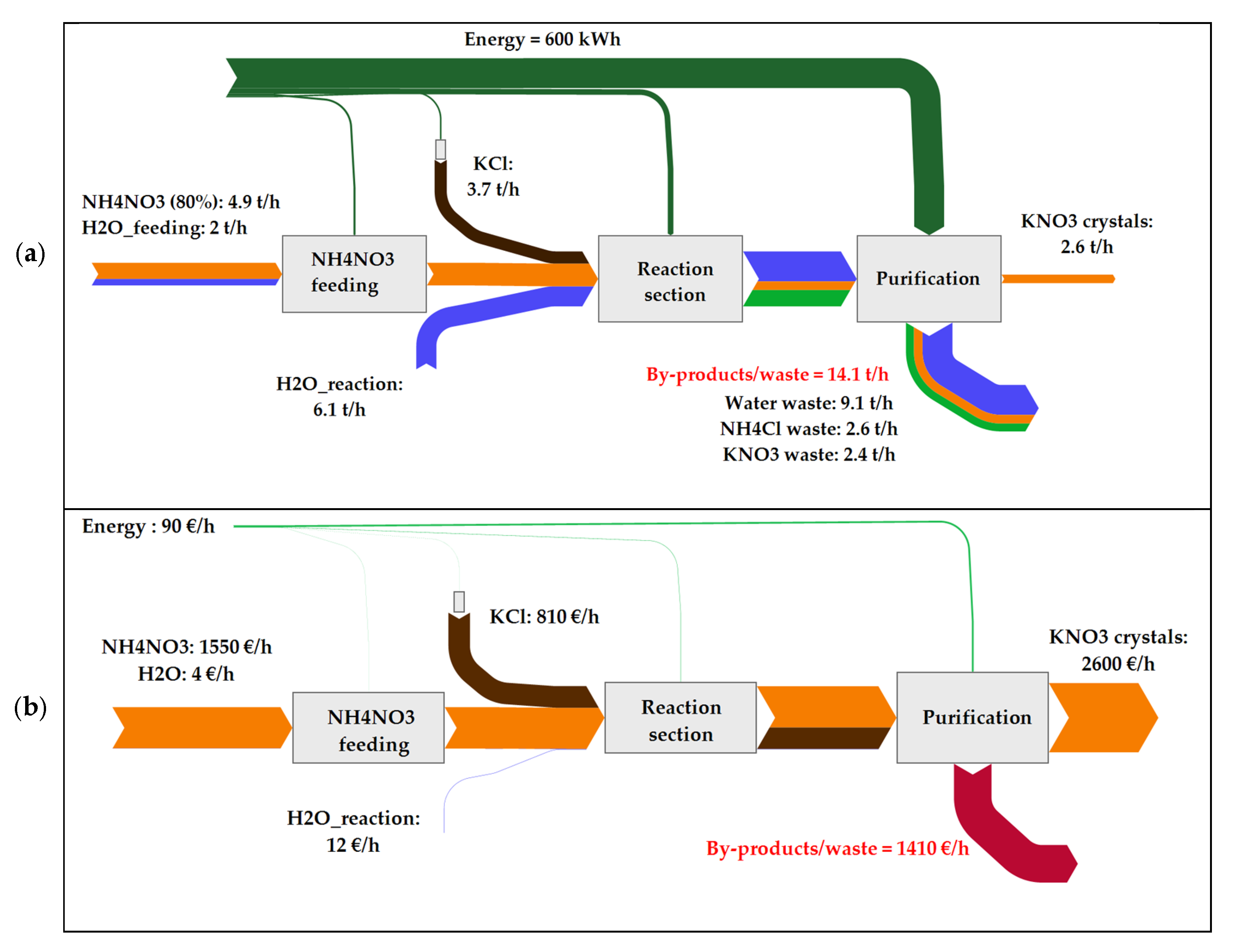

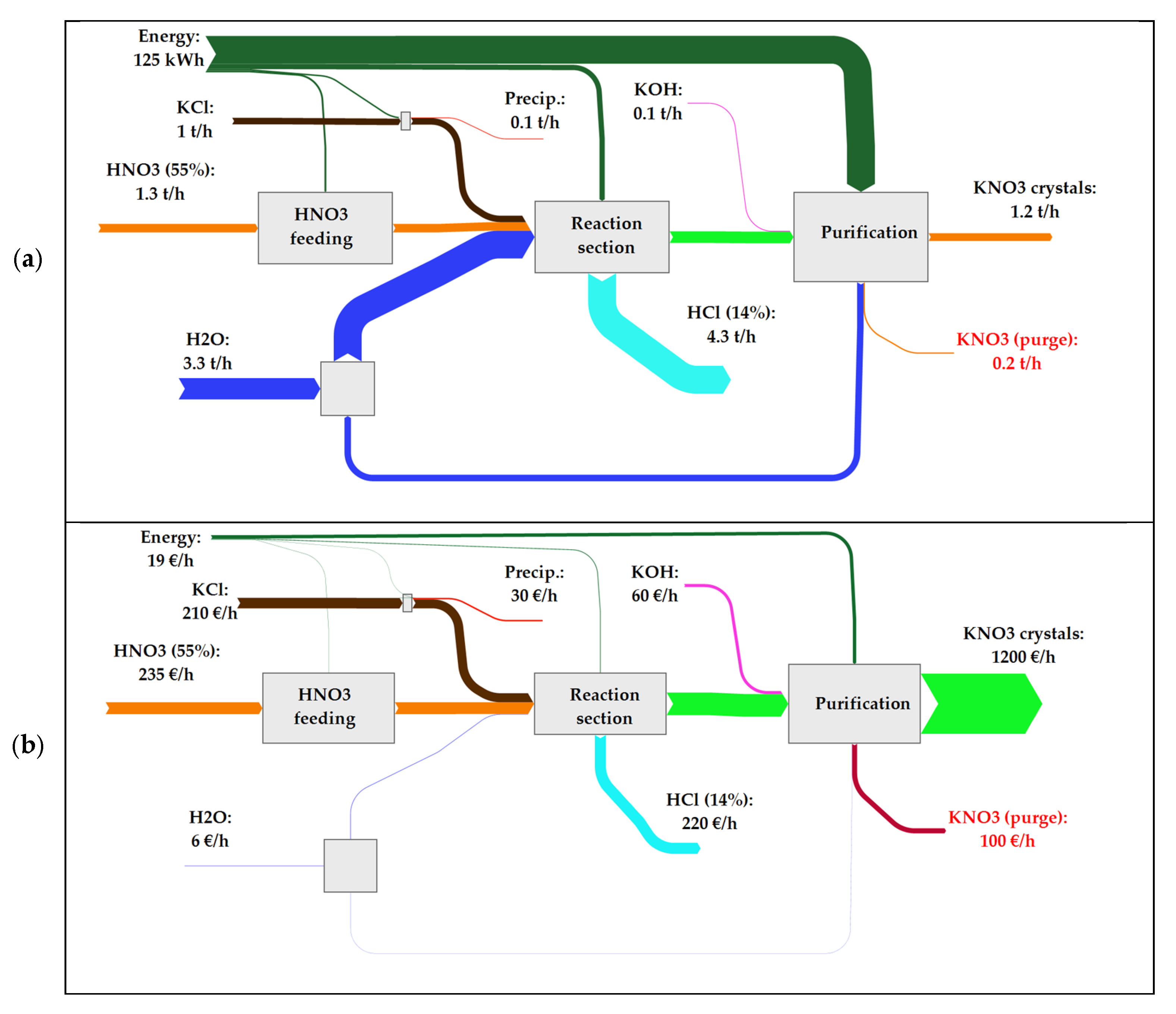

6.1. Baseline: Spanish Pre-IS Scenario

6.2. CORALIS: Spanish Post-IS Scenario

6.3. CORALIS Swedish Demo Site

7. Conclusions

7.1. General

- Holistic resource flow management: MFCA applied across interconnected supply chains enables a comprehensive understanding of how resource inputs, waste outputs, and costs are distributed across multiple companies in a symbiotic network. This fosters shared accountability for resource efficiency.

- Dynamic cost and resource modelling: integrating MFCA with IS requires new models to dynamically track how changes in one company (e.g., raw material quality or process efficiency) ripple across the network, influencing costs and performance at different points.

- Redefinition of quantity centres: quantity centres in MFCA would expand beyond processes or departments to include entire companies or clusters of companies, requiring new frameworks to map and manage these broader interactions.

- Collaborative decision making: IS layers demand collective strategies for resource sharing, waste valorisation, and cost distribution, supported by MFCA insights that highlight mutual benefits and shared risks.

- Alignment with circular economy goals: by identifying opportunities to reuse waste, reduce virgin material use, and optimise shared resources, this integration positions MFCA and ISO 14052 as critical tools for achieving circular economy objectives.

7.2. On This Work

7.3. Practical Recommendations and Future Research Directions

7.3.1. Practical Recommendations for Policymakers and Industry Practitioners

7.3.2. Future Research Directions Beyond MFCA and ISO 14052

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Abbreviations

| MFCA | Material Flow Cost Accounting |

| CBA | Cost–Benefit Analysis |

| CAPEX | Capital Expenditures |

| OPEX | Operational Expenditures |

| LCA | Life Cycle Assessment |

| IS | Industrial Symbiosis |

| EIPs | Eco-Industrial Parks |

| CO2 | Carbon Dioxide |

| SDGs | Sustainable Development Goals |

| P&IDs | Piping and Instrumentation Diagrams |

| NPO | Non-Product Output |

| QC | Quantity Centres |

| ROI | Return on Investment |

| PBP | Payback Period |

References

- Ghisellini, P.; Cialani, C.; Ulgiati, S. A review on circular economy: The expected transition to a balanced interplay of envi-ronmental and economic systems. J. Clean Prod. 2016, 114, 11–32. [Google Scholar] [CrossRef]

- Shi, L.; Chertow, M. Organizational Boundary Change in Industrial Symbiosis: Revisiting the Guitang Group in China. Sustainability 2017, 9, 1085. [Google Scholar] [CrossRef]

- Haskins, C. Multidisciplinary investigation of eco-industrial parks. Syst. Eng. 2006, 9, 313–330. [Google Scholar] [CrossRef]

- Cervo, H.; Ogé, S.; Maqbool, A.S.; Mendez Alva, F.; Lessard, L.; Bredimas, A.; Ferrasse, J.-H.; Van Eetvelde, G. A Case Study of Industrial Symbiosis in the Humber Region Using the EPOS Methodology. Sustainability 2019, 11, 6940. [Google Scholar] [CrossRef]

- Chertow, M.; Park, J. Scholarship and Practice in Industrial Symbiosis: 1989–2014. In Taking Stock of Industrial Ecology; Clift, R., Druckman, A., Eds.; Springer International Publishing: Cham, Switzerland, 2016; pp. 87–116. [Google Scholar] [CrossRef]

- Veugelers, R.; Tagliapietra, S.; Trasi, C. Green Industrial Policy in Europe: Past, Present, and Prospects. J. Ind. Compet. Trade 2024, 24, 4. [Google Scholar] [CrossRef]

- Huang, B.; Yong, G.; Zhao, J.; Domenech, T.; Liu, Z.; Chiu, S.F.; McDowall, W.; Bleischwitz, R.; Liu, J.; Yao, Y. Review of the development of China’s Eco-industrial Park standard system. Resour. Conserv. Recycl. 2019, 140, 137–144. [Google Scholar] [CrossRef]

- Mendez-Alva, F.; Cervo, H.; Krese, G.; Van Eetvelde, G. Industrial symbiosis profiles in energy-intensive industries: Sectoral insights from open databases. J. Clean. Prod. 2021, 314, 128031. [Google Scholar] [CrossRef]

- Demartini, M.; Tonelli, F.; Govindan, K. An investigation into modelling approaches for industrial symbiosis: A literature review and research agenda. Clean. Logist. Supply Chain. 2022, 3, 100020. [Google Scholar] [CrossRef]

- Yadav, V.S.; Majumdar, A. Mitigating the barriers of industrial symbiosis for waste management: An integrated decision-making framework for the textile and clothing industry. Waste Manag. Res. 2024, 42, 544–555. [Google Scholar] [CrossRef]

- Boom-Cárcamo, E.; Peñabaena-Niebles, R. Analysis of the Development of Industrial Symbiosis in Emerging and Frontier Market Countries: Barriers and Drivers. Sustainability 2022, 14, 4223. [Google Scholar] [CrossRef]

- Cárcamo, E.A.B.; Peñabaena-Niebles, R. Opportunities and challenges for the waste management in emerging and frontier countries through industrial symbiosis. J. Clean. Prod. 2022, 363, 132607. [Google Scholar] [CrossRef]

- Mazzanti, M.; Zoboli, R. Waste generation, waste disposal and policy effectiveness: Evidence on decoupling from the European Union. Resour. Conserv. Recycl. 2008, 52, 1221–1234. [Google Scholar] [CrossRef]

- Mishra, M.; Desul, S.; Santos, C.A.G.; Mishra, S.K.; Kamal, A.H.M.; Goswami, S.; Kalumba, A.M.; Biswal, R.; Goswami, S.; Baral, K. A bibliometric analysis of sustainable development goals (SDGs): A review of progress, challenges, and opportunities. Environ. Dev. Sustain. 2024, 26, 11101–11143. [Google Scholar] [CrossRef]

- Salvador, R.W.; Doong, R.-A. Simultaneous achievement of energy recovery and carbon sequestration through municipal solid waste management: A review. Chemosphere 2024, 361, 142478. [Google Scholar] [CrossRef]

- Gautam, M.; Agrawal, M. Greenhouse Gas Emissions from Municipal Solid Waste Management: A Review of Global Scenario. In Carbon Footprint Case Studies: Municipal Solid Waste Management, Sustainable Road Transport and Carbon Sequestration; Muthu, S.S., Ed.; Springer: Singapore, 2021; pp. 123–160. [Google Scholar] [CrossRef]

- United Nations Environment Programme and International Solid Waste Association, Beyond an Age of Waste Turning Rubbish into a Resource. 2024. Available online: https://wedocs.unep.org/20.500.11822/44939 (accessed on 10 March 2025).

- Ellen Macarthur Foundation. How the Circular Economy Tackles Climate Change. 2021. Available online: https://www.ellenmacarthurfoundation.org/completing-the-picture (accessed on 10 March 2025).

- Smith, A. Systemic Analysis of Circular Economy Principles in Agricultural Waste Management and Their Synergy with National Sustainable Development Objectives. 2025. Available online: https://neobibliotheca.com/index.php/TASCCDC/article/view/n-2025-02-07 (accessed on 10 March 2025).

- Cottes, M.; Mainardis, M.; Simeoni, P. Assessing the Techno-Economic Feasibility of Waste Electric and Electronic Equipment Treatment Plant: A Multi-Decisional Modeling Approach. Sustainability 2023, 15, 16248. [Google Scholar] [CrossRef]

- Geng, Y.; Doberstein, B. Developing the circular economy in China: Challenges and opportunities for achieving ‘leapfrog development. Int. J. Sustain. Dev. World Ecol. 2008, 15, 231–239. [Google Scholar] [CrossRef]

- Henriques, J.; Ferrão, P.; Castro, R.; Azevedo, J. Industrial Symbiosis: A Sectoral Analysis on Enablers and Barriers. Sustainability 2021, 13, 1723. [Google Scholar] [CrossRef]

- Cisi, M.; Napoli, R. Economic evaluation framework for Industrial Symbiosis through network lenses: A systematic literature review. Eur. J. Soc. Impact Circ. Econ. 2024, 5, 1–27. [Google Scholar] [CrossRef]

- Lawal, M.; Alwi, S.R.W.; Manan, Z.A.; Ho, W.S. Industrial symbiosis tools—A review. J. Clean. Prod. 2021, 280, 124327. [Google Scholar] [CrossRef]

- Ramírez-Rodríguez, L.C.; Ormazabal, M.; Jaca, C. Mapping sustainability assessment methods through the industrial symbiosis life cycle for a circular economy. Sustain. Prod. Consum. 2024, 50, 253–267. [Google Scholar] [CrossRef]

- Sacchi, R.; Ramsheva, Y.K. The effect of price regulation on the performances of industrial symbiosis: A case study on district heating. Int. J. Sustain. Energy Plan. Manag. 2017, 14, 39–56. [Google Scholar] [CrossRef]

- Mishan, E.Q.E.J. Cost-Benefit Analysis, 6th ed.; Routledge: London, UK, 2020; Available online: https://www.taylorfrancis.com/books/mono/10.4324/9781351029780/cost-benefit-analysis-euston-quah-mishan (accessed on 16 January 2025).

- Hansjürgens, B. Economic valuation through cost-benefit analysis—Possibilities and limitations. Toxicology 2004, 205, 241–252. [Google Scholar] [CrossRef] [PubMed]

- Reniers, G.; Talarico, L.; Paltrinieri, N. Chapter 16—Cost-Benefit Analysis of Safety Measures. In Dynamic Risk Analysis in the Chemical and Petroleum Industry; Paltrinieri, N., Khan, F., Eds.; Butterworth-Heinemann: Oxford, UK, 2016; pp. 195–205. [Google Scholar] [CrossRef]

- Loizidou, M. Waste Management and Symbiosis for Waste Valorization. Waste Biomass Valoriz. 2015, 6, 623–624. [Google Scholar] [CrossRef]

- Tsagkari, M.; Couturier, J.-L.; Kokossis, A.; Dubois, J.-L. Early-Stage Capital Cost Estimation of Biorefinery Processes: A Comparative Study of Heuristic Techniques. ChemSusChem 2016, 9, 2284–2297. [Google Scholar] [CrossRef]

- Environmental Industries Office. Material Flow Cost Accounting: MFCA Case Examples; Ministry of Economy, Trade and Industry: Tokyo, Japan, 2010. [Google Scholar]

- ISO 14051:2011; Environmental Management—Material Flow Cost Accounting—General Framework. International Organization for Standardization: Geneva, Switzerland, 2011.

- Kokubu, K.; Tachikawa, H. Material Flow Cost Accounting: Significance and Practical Approach∗. In Handbook of Sustainable Engineering; Kauffman, J., Lee, K.-M., Eds.; Springer: Dordrecht, The Netherlands, 2013; pp. 351–369. [Google Scholar] [CrossRef]

- Kasemset, C.; Chernsupornchai, J.; Palaud, W. Application of MFCA in waste reduction: Case study on a small textile factory in Thailand. J. Clean Prod. 2015, 108, 1342–1351. [Google Scholar] [CrossRef]

- Christ, K.L.; Burritt, R.L. ISO 14051: A new era for MFCA implementation and research. Rev. De Contab.-Span. Account. Rev. 2016, 19, 1–9. [Google Scholar] [CrossRef]

- Faria, E.; Caldeira-Pires, A.; Barreto, C. Social, economic, and institutional configurations of the industrial symbiosis process: A comparative analysis of the literature and a proposed theoretical and analytical framework. Sustainability 2021, 13, 7123. [Google Scholar] [CrossRef]

- Jacobsen, N.B. Applications and Implementation Industrial Symbiosis in Kalundborg, Denmark. A Quantitative Assessment of Economic and Environmental Aspects. 2006. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1162/108819806775545411 (accessed on 10 March 2025).

- ISO 14052:2017; Environmental Management—Material Flow Cost Accounting—Guidance for Practical Implementation in a Supply Chain. International Organization for Standardization: Geneva, Switzerland, 2017.

- Schaltegger, S.; Christ, K.L.; Wenzig, J.; Burritt, R.L. Corporate sustainability management accounting and multi-level links for sustainability—A systematic review. Int. J. Manag. Rev. 2022, 24, 480–500. [Google Scholar] [CrossRef]

- Huang, S.Y.; Chiu, A.A.; Chao, P.C.; Wang, N. The Application of Material Flow Cost Accounting in Waste Reduction. Sus-tainability 2019, 11, 1270. [Google Scholar] [CrossRef]

- Walz, M.; Guenther, E. What effects does material flow cost accounting have for companies?: Evidence from a case studies analysis. J. Ind. Ecol. 2021, 25, 593–613. [Google Scholar] [CrossRef]

- Qu, L.; Wang, Z.; Sun, C.; Yin, L. Application of ABB in environmental management accounting: Incorporating MFCA into the budget process. Front. Environ. Sci. 2022, 10, 963903. [Google Scholar] [CrossRef]

- Lütje, A.; Leber, S.; Scholten, J.; Wohlgemuth, V. Web Tool for the Identification of Industrial Symbioses in Industrial Parks. In Advances and New Trends in Environmental Informatics; Kamilaris, A., Wohlgemuth, V., Karatzas, K., Athanasiadis, I.N., Eds.; Springer International Publishing: Cham, Switzerland, 2021; pp. 19–34. [Google Scholar]

- Yazdanpanah, V.; Yazan, D.M.; Zijm, W.H.M. Dynamics and Allocation of Transaction Cost in Multiagent Industrial Symbiosis. CoRR 020. Available online: https://arxiv.org/abs/2010.01361 (accessed on 10 March 2025).

- Dekamin, M.; Sadeghimofrad, T.; Ahmadloo, A. Energy, economic, and environmental (3E) assessment of the major greenhouse crops: MFCA-LCA approach. Environ. Sci. Pollut. Res. 2024, 31, 21894–21912. [Google Scholar] [CrossRef] [PubMed]

- Amicarelli, V.; Roe, B.E.; Bux, C. Measuring Food Loss and Waste Costs in the Italian Potato Chip Industry Using Material Flow Cost Accounting. Agriculture 2022, 12, 523. [Google Scholar] [CrossRef]

- Zeng, H.; Zhou, Z.; Xiao, X. MFCA extension from a life cycle perspective: Methodical refinements and use case. Resour. Policy 2021, 74, 101507. [Google Scholar] [CrossRef]

- Wagner, B. A report on the origins of Material Flow Cost Accounting (MFCA) research activities. J. Clean Prod. 2015, 108, 1255–1261. [Google Scholar] [CrossRef]

- Nishitani, K.; Kokubu, K.; Wu, Q.; Kitada, H.; Guenther, E.; Guenther, T. Material flow cost accounting (MFCA) for the circular economy: An empirical study of the triadic relationship between MFCA, environmental performance, and the economic performance of Japanese companies. J. Environ. Manag. 2022, 303, 114219. [Google Scholar] [CrossRef]

- Montag, L. Roadmap to a Circular Economy by 2030: A Comparative Review of Circular Business Model Visions in Germany and Japan. Sustainability 2023, 15, 5374. [Google Scholar] [CrossRef]

- Schmidt, M. The interpretation and extension of Material Flow Cost Accounting (MFCA) in the context of environmental material flow analysis. J. Clean Prod. 2015, 108, 1310–1319. [Google Scholar] [CrossRef]

- ISO 14053:2021; Environmental Management—Material Flow Cost Accounting—Guidance for Phased Implementation in Organizations. International Organization for Standardization: Geneva, Switzerland, 2021.

- Lütje, A.; Möller, A.; Wohlgemuth, V. A Preliminary Concept for an IT-Supported Industrial Symbiosis (IS) Tool Using Extended Material Flow Cost Accounting (MFCA)—Impulses for Environmental Management Information Systems (EMIS). In Advances and New Trends in Environmental Informatics; Bungartz, H.-J., Kranzlmüller, D., Weinberg, V., Weismüller, J., Wohlgemuth, V., Eds.; Springer International Publishing: Cham, Switzerland, 2018; pp. 167–181. [Google Scholar]

- Walls, C.; Putri, A.R.K.; Beck, G. Material Flow Cost Accounting as a Resource-Saving Tool for Emerging Recycling Technologies. Clean Technol. 2023, 5, 652–674. [Google Scholar] [CrossRef]

- Maulana, Y.; Dendi, P.; Rahmawati, T. Material Flow Cost Accounting to Enhance Sustainable Development: A Green Accounting Perspective. J. Ris. Akunt. Terpadu 2024, 17. [Google Scholar] [CrossRef]

- Christ, K.L.; Burritt, R.L. Water management accounting: A framework for corporate practice. Clean Prod. 2017, 152, 379–386. [Google Scholar] [CrossRef]

- Patricio, J.; Kalmykova, Y.; Rosado, L.; Cohen, J.; Westin, A.; Gil, J. Method for identifying industrial symbiosis opportunities. Resour. Conserv. Recycl. 2022, 185, 106437. [Google Scholar] [CrossRef]

- Rieckhof, R.; Bergmann, A.; Guenther, E. Interrelating material flow cost accounting with management control systems to introduce resource efficiency into strategy. J. Clean Prod. 2015, 108, 1262–1278. [Google Scholar] [CrossRef]

- Zion Market Research. Potassium Nitrate Market Industry Perspective. Available online: https://www.zionmarketresearch.com/report/potassium-nitrate-market (accessed on 6 December 2024).

- Trädgårdsproduktion, J. The Swedish Board of Agriculture. 2020. Available online: https://jordbruksverket.se/om-jordbruksverket/jordbruksverkets-officiella-statistik/jordbruksverkets-statistikrapporter/statistik/2021-06-29-tradgardsproduktion-2020 (accessed on 16 January 2025).

- Iacovidou, E.; Velenturf, A.P.M.; Purnell, P. Quality of resources: A typology for supporting transitions towards resource efficiency using the single-use plastic bottle as an example. Sci. Total Environ. 2019, 647, 441–448. [Google Scholar] [CrossRef]

- Velenturf, A.P.M.; Purnell, P.; Tregent, M.; Ferguson, J.; Holmes, A. Co-Producing a Vision and Approach for the Transition towards a Circular Economy: Perspectives from Government Partners. Sustainability 2018, 10, 1401. [Google Scholar] [CrossRef]

- Eurostat. Electricity Prices for Non-Household Consumers. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Electricity_price_statistics#Electricity_prices_for_non-household_consumers (accessed on 16 January 2025).

- Indexmundi. Commodity Price Indices: Potassium Chloride. 2022. Available online: https://www.indexmundi.com/commodities/?commodity=potassium-chloride&months=60¤cy=eur (accessed on 16 January 2025).

- AHDB. Fertiliser Prices. Available online: https://ahdb.org.uk/GB-fertiliser-prices (accessed on 16 January 2025).

- Procurement Resource. Hydrochloric Acid Price Trend. Available online: https://www.procurementresource.com/resource-center/hydrochloric-acid-price-trends (accessed on 16 January 2025).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Methodology | Focus Areas | Limitations | Remarks |

|---|---|---|---|---|

| [42] | Meta-analysis of 73 MFCA case studies | Effects and challenges of MFCA implementation in companies | Limited data availability may affect reliability; potential reporting bias in case study selection | Provides a broad synthesis of MFCA applications, highlighting common benefits and challenges. Offers practical insights for companies considering MFCA adoption and serves as a foundation for further research. |

| [43] | MFCA-ABB (Activity-Based Budgeting) | Integration of MFCA into budgeting for forecasting resource use, product output, and waste generation in manufacturing | Primarily applied to a single case study (liquor production), limiting generalisability; MFCA is traditionally ex-post, requiring further validation for predictive use | Expands MFCA from reporting to proactive planning, enabling environmental–economic budgeting. Demonstrates the potential for adapting conventional management accounting tools to sustainability-focused decision making. |

| [44] | Development of a web tool for identifying industrial symbiosis | Identification of potential synergies in industrial parks | Focuses on the development phase; lacks extensive field application | Introduces a web-based tool aimed at facilitating the discovery of industrial symbiosis opportunities, potentially integrating MFCA data for enhanced decision making. |

| [45] | Multiagent simulation of transaction costs in industrial symbiosis | Analysis of transaction cost dynamics in symbiotic networks | Theoretical model; requires empirical validation | Provides insights into the economic interactions within industrial symbiosis networks, which could be complemented by MFCA for a comprehensive economic assessment. |

| [46] | Integration of LCA and MFCA | Economic, energy, and environmental (3E) sustainability of greenhouse crop production (cucumber, tomato, and bell pepper) | LCA alone does not account for economic losses from resource inefficiencies; reliance on subsidies may distort economic feasibility | MFCA complements LCA by quantifying the economic impact of waste and inefficiencies |

| [47] | MFCA | Economic and environmental impacts of food loss and waste in the Italian salty snack sector before and during COVID-19 | Focuses on a specific food sector (potato chips), limiting generalisability | Demonstrates MFCA’s potential to quantify economic losses from waste and inefficiencies, supporting circular economy strategies and food waste management policies |

| [48] | MFCA-LCA integrated model | Lifecycle extension of MFCA, integrating environmental damage valuation and cost accounting | Lacks empirical validation beyond the case study; theoretical framework still developing | Expands MFCA applicability by incorporating lifecycle assessment, offering a more comprehensive sustainability evaluation for decision making in enterprises. |

| Option | Allocated Production Cost for Tomatoes | Allocated Production Cost for Plant Residues |

|---|---|---|

| A | 1.30 EUR/kg | 1.33 EUR/kg |

| B | 1.04 EUR/kg | 1.07 EUR/kg |

| C | 1.07 EUR/kg | 1.10 EUR/kg |

| D | 1.23 EUR/kg | 1.26 EUR/kg |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Leiva, H.; Julian, I.; Ventura, L.; Wallin, E.; Vendt, M.; Fornell, R.; Galindo Paniagua, F.; Ascaso, S.; Gomez-Perez, M. Advancing Sustainability Through Industrial Symbiosis: A Technoeconomic Approach Using Material Flow Cost Accounting and Cost–Benefit Analysis. Sustainability 2025, 17, 2730. https://doi.org/10.3390/su17062730

Leiva H, Julian I, Ventura L, Wallin E, Vendt M, Fornell R, Galindo Paniagua F, Ascaso S, Gomez-Perez M. Advancing Sustainability Through Industrial Symbiosis: A Technoeconomic Approach Using Material Flow Cost Accounting and Cost–Benefit Analysis. Sustainability. 2025; 17(6):2730. https://doi.org/10.3390/su17062730

Chicago/Turabian StyleLeiva, Héctor, Ignacio Julian, Lucía Ventura, Elin Wallin, Marcus Vendt, Rickard Fornell, Francisca Galindo Paniagua, Sonia Ascaso, and Manuel Gomez-Perez. 2025. "Advancing Sustainability Through Industrial Symbiosis: A Technoeconomic Approach Using Material Flow Cost Accounting and Cost–Benefit Analysis" Sustainability 17, no. 6: 2730. https://doi.org/10.3390/su17062730

APA StyleLeiva, H., Julian, I., Ventura, L., Wallin, E., Vendt, M., Fornell, R., Galindo Paniagua, F., Ascaso, S., & Gomez-Perez, M. (2025). Advancing Sustainability Through Industrial Symbiosis: A Technoeconomic Approach Using Material Flow Cost Accounting and Cost–Benefit Analysis. Sustainability, 17(6), 2730. https://doi.org/10.3390/su17062730