Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China

by

, , and

, , and

Wei Tong Chen

1,

Adiqa Kausar Kiani

2,

Ming-Tsung Wu

3,

Hew Cameron Merrett

4,* and

Chih-Hsing Wang

5 1

Department of Civil & Construction Engineering, Graduate School of Engineering Science & Technology, National Yunlin University of Science & Technology, Yunlin 64002, Taiwan

2

Bachelor Program in International Management, College of Management, National Yunlin University of Science & Technology, Yunlin 64002, Taiwan

3

Chang Hong Construction Co., Ltd., Yunlin 64002, Taiwan

4

Centre for Emergency Response Information, National Yunlin University of Science & Technology, Yunlin 64002, Taiwan

5

Bachelor Program in Industrial Projects, National Yunlin University of Science & Technology, Yunlin 64002, Taiwan

*

Author to whom correspondence should be addressed.

Sustainability 2023, 15(2), 941; https://doi.org/10.3390/su15020941

Submission received: 6 October 2022

/

Revised: 9 December 2022

/

Accepted: 23 December 2022

/

Published: 4 January 2023

(This article belongs to the Special Issue Advances in Construction Performance Prediction Techniques: Perspectives for Sustainability)

Abstract

:A strong construction industry is critical to any country’s economic and infrastructural development. Facing declining business prospects in the domestic market, Taiwanese construction firms have sought new opportunities overseas, particularly in the mainland Chinese market. Without an adequate understanding of the market, making such investments involves significant risks. To better understand the differences in the markets, this study investigates the technical efficiency (TE) of the Taiwanese construction industry compared to mainland China. The focus was on TE values of construction companies across the two markets as well as the strengths and weaknesses to help inform the decision-making process. The TE evaluation was completed using the stochastic frontier approach (SFA) with a subinput efficiency model to evaluate three inputs (assets, costs, and labor) of 123 construction companies with 59 companies in mainland China and 64 companies in Taiwan. Results show that for the key asset investment factors in Taiwan’s construction industry, TE is lower than that in mainland China. However, Taiwan’s construction industry was found to have higher labor efficiency than mainland China. Relative to mainland Chinese companies, Taiwanese companies have advantages in both labor inputs and revenue outputs but are disadvantaged in terms of the firm and market size. This study shows that Taiwanese construction firms are positioned to pursue expansion into mainland China, ideally by establishing cooperative alliances. Results also show that government policy needs to ensure construction companies are supported by increased economic freedom and reduced restrictions, as these positively correlate with the revenue of local construction companies.

1. Introduction

A strong construction industry is critical to any country’s economic and infrastructural development [1]. The construction industry is highly interconnected with many supporting industries, including cement, steel, transportation, electrical machinery, etc. In 2009, Taiwan joined the World Trade Organization, opening the domestic construction market to foreign companies, which resulted in increased competition for local firms. With increased competition, many Taiwanese construction companies have sought growth opportunities overseas, particularly across the Taiwan Strait into mainland China [2,3]. Managing the risks involved in this international expansion during normal and unstable or challenging scenarios requires careful assessments of the target market to ensure financial viability. Research on the topic of construction industry efficiency is limited in relation to the COVID-19 pandemic. Research on small construction companies in Ghana showed that small construction firms are struggling to maintain pre-COVID efficiency due to several factors, including financial and workforce elements [4].

As a starting point, this study focuses on the efficiency of cross-Taiwan Strait construction firms between 2007 and 2017 as a normal baseline. Such assessments focus on achieving the greatest construction output from the available resources. This study investigates the technical efficiency (TE) of the Taiwanese construction industry compared to mainland China, where TE refers to the efficiency with which the available inputs are used to produce an effective output. In this case, the resources of interest are those required for a given construction project. Robust TE assessments will enable Taiwanese construction companies with limited international exposure to better target international construction opportunities with greater confidence. The assessment of the construction industry TE can also support the Taiwanese government in developing policies and incentives to assist construction enterprises to be competitive in the mainland Chinese construction market [5,6].

The Taiwanese Ministry of the Interior, Construction and Planning Agent’s records showed that the Taiwanese construction industry’s overall production outputs totaled USD $18.9 billion in 2018, a decrease of nearly $0.83 billion from 2015. As of 2020, the Taiwanese construction industry directly employed 138,847 people, of which, support staff in specialized technical and managerial roles accounted for 58.0% compared to 39.6% for construction workers (engineering technicians and general workers) [7]. Simultaneously, Taiwan’s construction industry has faced pressures from excessive price fluctuations and limited cost control along with increased prices for raw materials [8]. In response, construction firms appealed for government assistance in the form of controls on the prices of raw materials and other assistance to maintain the commercial viability of the construction sector. Initiatives such as the Sales Tax on Special Goods and Services Ordinance have been implemented to improve sector performance. However, Taiwan’s construction market is relatively small, and the imminent completion of large-scale programs of public work projects leaves many firms scrambling to find projects overseas. Such an expansion can be daunting for Taiwanese construction firms due to the limited information at an industry level on the competitive operating environments in other countries or regions [9]. This is further compounded by the limited number of Taiwanese construction companies with extensive experience in overseas construction operations.

At present, there is a lack of such supporting determinates to build an understanding of operating environments in other countries [10,11,12,13]. The successful overseas expansion of Taiwanese construction firms requires an accurate, effective, and viable evaluation of target markets under a stable market scenario and an objective assessment of the ability of domestic firms to effectively meet market demand while still being a commercially viable investment [14]. In the case of mainland China’s market, the primary questions many Taiwanese firms ask when entering the market include:

- What are the respective TE values for various operations aspects as well as the strengths and weaknesses of construction companies on both sides of the Taiwan Strait?

- What is the TE of selected Taiwanese construction companies, and how do they compare to mainland China?

The presented research study utilizes data reported from Taiwanese construction companies’ domestic operations and target market operational data as the basis for performance evaluations with TE. Such information is critical for companies to understand their strengths and weaknesses when evaluating potential opportunities for overseas expansion. The performance of Taiwan’s construction sector has changed radically over the last decade due to a combination of factors. To quantify the impact of these changes, current efficiency analysis of the industry is urgently needed along with comparisons of efficiency with construction companies in other countries. This study seeks to fill this gap by investigating the comparative TE values for Taiwan and mainland China using data envelopment analysis (DEA) and stochastic frontier analysis (SFA).

1.1. Approaches to Measuring Efficiency

Measurement of efficiency is an area of research in multiple industry sectors, especially during challenging times. Measurement of operational efficiency in the construction industry, especially between different enterprises across different countries, is fundamental to understanding performance factors when considering entering a new market. While there has been some investigation of the efficiency of the domestic market in Taiwan [15,16,17], further research is required to understand efficiency at the regional scale. There are numerous ways to measure the efficiency of a particular industrial sector; the most typically used methods are SFA and DEA, with many studies using one or both methods to estimate TE. This popularity is due to the flexibility of the approaches for a range of purposes. The following sections explore different applications of both SFA and DEA as well as relevant factors across the construction industry and related examples.

1.1.1. Stochastic Frontier Analysis

SFA provides a practical approach to understanding various market fluctuations and other influences on efficiency in construction and related industries [15]. Fernandez-Lopez and Coto-Millan [18] estimated TE for the construction industry in Spain between 1996 to 2011 to assess the influence of the 2008 financial crisis using SFA. Results showed that TE was lower at the beginning of the financial crisis than during the crisis when efficiency was essential to maintain financial viability. The study also found that firms with lower TE were more likely to experience difficulties before the fall of the housing market. Hendrawan and Utama [19] estimated the TE of listed construction companies in Indonesia from 2013 to 2017 using SFA. The findings showed that variable costs of revenue, capital expenditures, personnel expenses, and inflation rates had significantly affected TE values whereas net fixed assets and total equity showed insignificant effects on overall TE. Yin [20] examined spatial spillover effects based on total factor productivity (TFP) measurements for construction industry companies operating in China’s Yangtze River Delta. A significant spillover effect of TFP was found among local cities, showing that the promotion of the regional construction industry improved overall production levels for mainland China’s construction industry.

Outside of the construction field, SFA has been applied successfully in many complex scenarios, including energy efficiency [21,22]. For estimating the energy efficiency of the US manufacturing industry during 1987–2012, Boyd and Lee [21] applied SFA. A Malmquist index was also used to evaluate energy efficiency indices and frontier change after decomposition. The results showed that firms entering the industry were more efficient and closer to the frontier. Sayavong [23] estimated TE using SFA in the manufacturing industry in Laos using cross-sectional census data from 2012 to 2013. The findings showed that efficiency levels varied across subindustries with an average efficiency of 72.5%. The firm size, credit access, and accounting system were all critical factors for enhancing production efficiency. Using the SFA model’s CD function, [24] analyzed the effects of administrative class and city size on urban production efficiency in mainland China using data from 261 cities in 30 regions from 2000 to 2013. The results showed that the higher the city’s administrative level, the greater the inefficiency of urban production. Jin et al. [25] used SFA to evaluate land-use efficiency, ecological efficiency, and ecological performance of each county in mainland China’s Hubei Province in the face of rapid urbanization. Their findings provide a valuable reference for the development of new urban areas, the efficient utilization of available land, and the protection of ecological values.

Hsieh [26] used SFA to evaluate the operating efficiency of 23 Japanese security firms from 2010 to 2014 by categorizing different input factors. Total operating revenue was used as the output factor, and shareholder equity, operating expenses, and the number of employees were used as the input factors. Chang et al. [27] evaluated the input efficiency of 56 banks across the Taiwan Strait from 2007 to 2011 using the number of employees, total fixed assets, total capital as inputs, total lending, and total investment as outputs and group-specific macroeconomic variables. Chang [28] used randomized SFA to calculate the performance of 310 mutual funds in Taiwan from 2007 to 2012 using total asset net worth and expense ratio as input variables; using risk-adjusted returns as the output variable; and adding macroeconomic variables to support the analysis. Hu et al. [29] used Japan securities corporation itemized input efficiency SFA to calculate the decomposition input efficiency of 23 Japanese securities firms from 2010 to 2014. Chang [30] collected data on 57 Taiwanese securities firms from 2005 to 2011 using SFA to calculate their subinput efficiency performance. SFA was used to estimate the impact of macroeconomic variables on the efficiency values of individual input factors. The output variables used included the firms’ total proprietary incomes, brokerage incomes, and underwriting incomes while the input variables included total fixed assets, shareholder equity, number of employees, and operating expenses.

1.1.2. Data Envelope Analysis (DEA)

DEA is applied in economics to estimate production frontiers [31]. To evaluate the regional-level efficiency of the construction industry in 30 Chinese provincial administrative units from 2011 to 2016 covering mainland China’s eastern, central, and western regions, Yang et al. [32] applied the slacks-based measure of efficiency in the DEA model. Results showed declining average sustainable efficiency values of 0.64, 0.59, and 0.48, respectively, for the three regions. Furthermore, the technical equipment ratio and the external environmental factors were found to play vital roles in the sustainable efficiency of the construction industry.

At a multinational level, Park et al. [33] used DEA to compare the efficiency of the construction industries in China and the United States from 1990 to 2011. The United States’ construction industry was found to be significantly more efficient and stable while China depended mainly on scale efficiency to overcome technological disadvantages and overinvestment. In the wider Asian context, Park et al. [33] also compared the efficiency and productivity of Chinese, Japanese, and Korean construction firms between 2005 and 2011 using DEA and DEA-based Malmquist methods. The findings showed that the average efficiency score of Korean construction firms (0.861) was higher than those of Japanese construction firms (0.775) and even higher than Chinese construction firms (0.639). The comparison also found that the average Malmquist productivity index (MPI) of Chinese construction firms (5.5%) was higher than those of Korean construction firms (0.9%) and Japanese construction firms (−0.1%). This indicates that Korean construction firms need to focus more on improving productivity than efficiency to enhance their competitiveness in the construction industry.

The investigation of construction enterprise operating efficiency using DEA became a notable area of interest around the time of the 2008 financial crisis. Wong et al. [34] used DEA to analyze and compare the operating efficiency of construction projects in Iran, and Al-Malkawi and Pillai [35] compared the UAE construction industry’s financial performance before and after the global financial crisis. You and Zi [36] also used DEA to examine changes in operating efficiency, TE, and allocative efficiency in the Korean construction industry before and after the financial crisis. Kapelko and Lansink [37] calculated the TE of medium- and large-sized construction firms in Spain before and after the 2008 financial crisis. The analysis also included the impact of socioeconomic factors on TE using DEA with bootstrapping for the years 2000 to 2010. Their findings showed that efficiency was higher for firms with highly leveraged exports integrated into the form of joint stock companies located in Spanish regions with higher GDP (gross domestic product) per capita. In contrast, firms with high stock relative to turnover had lower TE values. TE increased with firm size for relatively small-sized construction firms but decreased beyond a critical firm size. In contrast, TE decreased with age for young firms but eventually increased for older firms.

A DEA-based analysis of the operating efficiency of 80 listed construction companies operating in Taiwan from 2002 to 2009 investigated operating and internal capital allocation structures and identified each firm’s respective competitive advantage [38]. In the work of Chen et al. [39], DEA was used as a performance evaluation model to analyze the operating efficiency of listed construction companies in Taiwan between 2004 and 2006 as well as to identify management factors affecting efficiency to assess the effectiveness of various competitive strategies before the 2008 financial crisis. To analyze operational performance, Huang et al. [40] used the common border input distance function to investigate the common border TE of two subsectors of construction and building companies with different business models. It is evident that analysis of the Taiwanese construction industry using both methods SFA and DEA has been limited, especially for those operating internationally. Supporting successful expansion into international markets requires exploring the insights of construction industries’ performances and their efficacy levels for mainland China and Taiwan.

Outside of the construction industry, Mujadad and Ahmed [41] analyzed TE for Pakistan’s large-scale manufacturing industries (LSMI) using a DEA truncated regression model. First, they applied the bootstrapped DEA technique to estimate bias-corrected TE scores. They found diseconomies in large firms and suggested reducing the firm size to improve operating efficiency. The wages of skilled workers were also found to have a significant and positive effect on TE; however, market size showed no significant impact. To estimate TE and total productivity growth for medium- and large-scale manufacturing subsectors using annual survey-based data for Ethiopia, Erena et al. [42] used DEA, MPI, and a Tobit regression model to identify potential impact factors. The results showed that, on average, medium- and large-scale manufacturing subsectors registered a 0.37 efficiency score over the postfinancial crisis study period from 2010 to 2017. This suggests that, on average, the sector could reduce input quantity by 63% without altering production levels or expand production by 63% without the input of additional resources. Moreover, productivity grew by 13% over the study period, which equates to less than 2% growth per annum. As productivity is the linear combination of catch-up and frontier shift, firms must balance these factors to improve productivity and profitability. In Ukraine, Goncharuk [43,44] used nonparametric techniques to estimate efficiency at the interindustry and intraindustry level using DEA. The results showed that high-tech industries display greater efficiency, particularly for durable goods; however, consumer goods, including light manufacturing and food production, showed much lower efficiency along with construction-related industries.

Research in the Taiwanese finance and insurance industry has seen the adoption of several novel and conventional methods for assessing operating efficiency. Investigating the cross-Strait life insurance industry, Hu et al. [45] found that the sector has itemized input efficiency. The study used a randomized border method to evaluate the operating efficiency of selected input factors for 90 life insurance companies operating across the Taiwan Strait from 2006 to 2011. The number of employees, shareholder equity capital, and liability capital were input factors, with operating income used as an output factor. Using randomized marginal analysis, Tsai [46] estimated the overall operating efficiency and itemized input efficiency of 187 domestic open-end mutual funds in Taiwan (2011 to 2015). The research assessed the impact of macroeconomic variables on the efficiency values, with the sample funds classified into two categories, general and professional, for comparison.

For Taiwanese construction companies, SFA and DEA are invaluable methods for assessing the impact of macroeconomic variables on a range of efficiency factors. Such information is needed to explore and develop a more concrete understanding of efficiency to contribute to the development of Taiwan’s economy.

2. Materials and Methods

A production function can be defined as either input-oriented or output-oriented. An input-oriented assessment refers to the minimum input demand for a certain quantitative output. In contrast, an output-oriented assessment refers to the maximum output produced with a certain quantitative input [47]. As a measurement of productivity, TE can be derived from a production function that uses the concept of “distance function” to measure the distance of output (ya) or input (xa) from the production boundary (y*, x*) at the observed sample point, where ya to y* is the output distance function and xa to x* is the input distance function. Calculating TE is completed through the radial expansion or contraction relationship produced by the distance function.

For simplicity, this study used the Cobb–Douglas production function (CD function) for analysis in the log form [48], as shown in Equation (1).

The parameter β is a fixed constant, and the production is a fixed return to scale. Also known as the CD function, the advantage of this production function is that it has a simple and well-defined numerical structure. Cobb–Douglas as a production function can be applied to analyzing property values in a long-term structure of changing size. The error between the observed and estimated values is minimized by regression to find the parameter values [49].

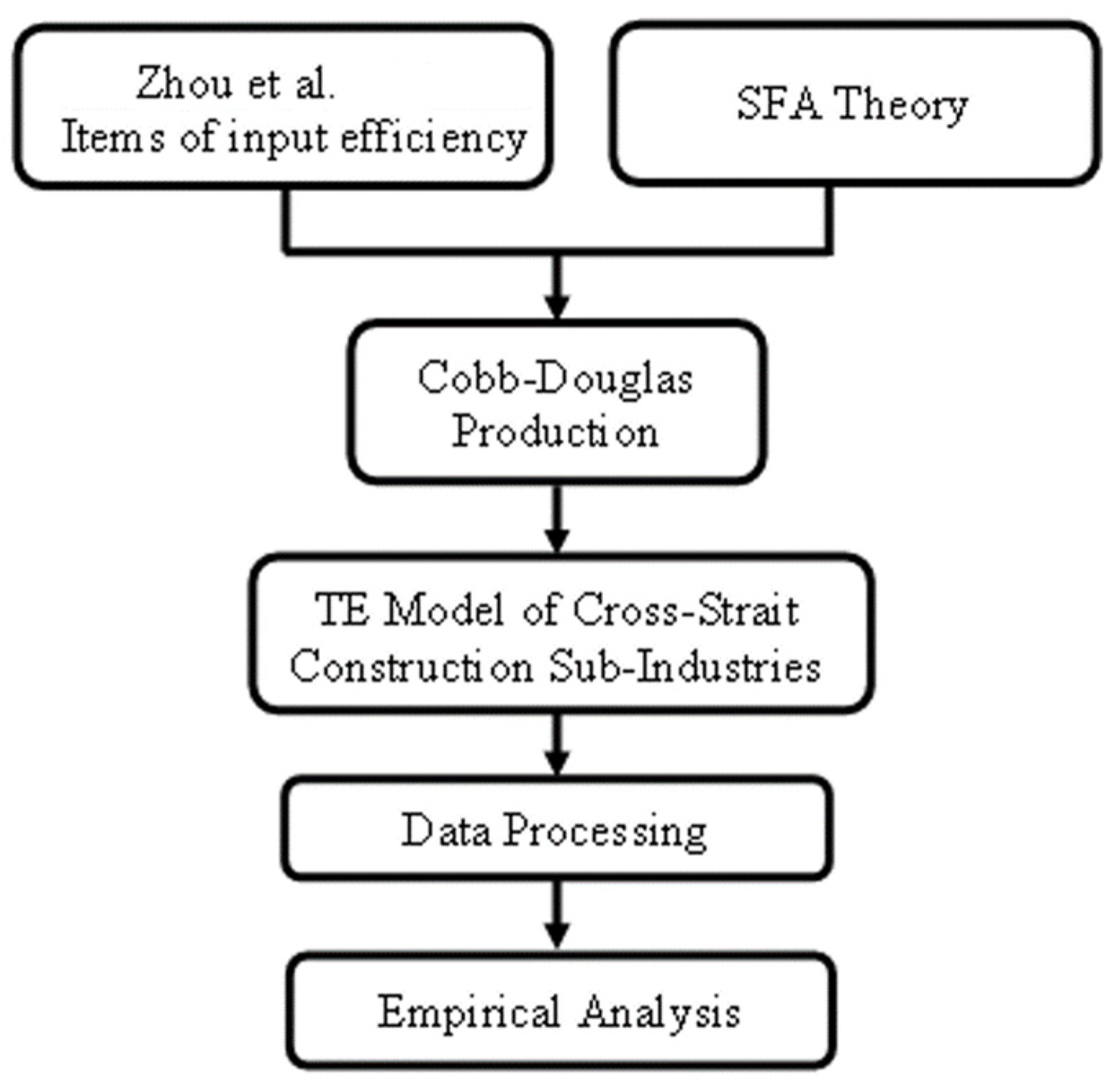

This study focuses on constructing a research model that applies the SFA theory of the randomized frontier method, combining the TE of each input and output following the methodology outlined in Zhou et al. [50] which uses the CD function to construct the TE of three inputs, one output, and selected macroeconomic variables. An overview of the research framework and processing steps is provided in Figure 1.

2.1. Research Model

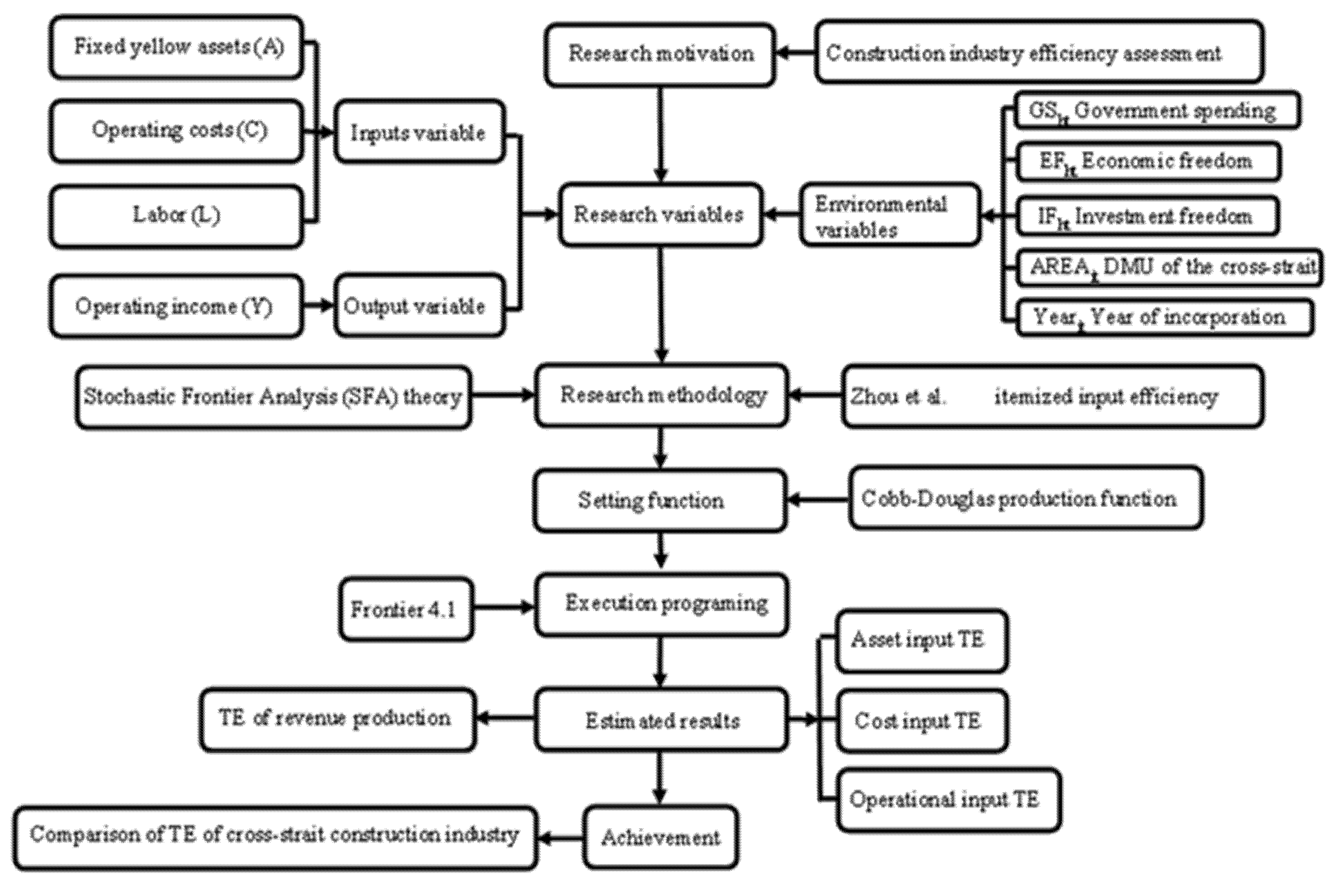

The TE research approach for the cross-Strait construction industry focuses on overall efficiency in relation to the individual efficiency of selected input factors [50]. This approach uses the chi-square of the distance function to create a stochastic boundary model to estimate the efficiency values of the subinput factors in a total factor framework. The final model estimates the itemized input efficiency of the three-input–one-output model, assuming that the production function is the CD function. The research steps are given in Figure 2.

In the total production framework, fixed assets (A), labor (L), and operating costs (C) are considered inputs, and operating revenues (Y) are considered outputs. The production technology is described in Equation (2):

T = {(A, C, L, Y): (A, C, L) can produce Y},

‘T’ consists of all feasible input–output vectors where ‘T’ is a convex and closed set with freely disposable inputs and outputs, i.e., (A′, C′, L′, Y′) ϵ T, when (A′, C′, L′) ≥ (A, C, L) and Y′ ≤ Y. Therefore, to calculate the TE of the fixed asset (A), the Shephard distance function of the fixed asset (A) is defined as shown in Equation (3):

DA (A, C, L, Y) = sup {α:(A/α, C, L, Y) ϵT},

Similarly, the Shephard’s distance functions for operating cost (C) and labor (L) are given in Equations (4) and (5):

DC (A, C, L, Y) = sup {α: (A, C/α, L, Y) ϵT},

DL (A, C, L, Y) = up {α:(A, C, L/α, Y) ϵT},

When applying the stochastic boundary method to estimate the distance function, the variables “observation” and “time” are included in the distance function. Therefore, assuming that there are n decision maker units (DMUs), the combination of input and output of the ith DMU in period t is (Ait, Cit, Lit, Yit); the set ‘T’ can be rewritten as shown in Equation (6).

T = {(Ait, Cit, Lit, Yit): (Ait, Cit, Lit) can produce Yit},

Fixed assets (A), operating costs (C), and labor force (L) could be converted using Equations (7)–(9), and the Shephard distance function is expressed as

DA (Ait, Cit, Lit, Yit),

DC (Ait, Cit, Lit, Yit),

DL (Ait, Cit, Lit, Yit),

The logarithm of the Cobb–Douglas production function is used to obtain Equation (10).

ln DA (Ait, Cit, Lit, Yit) = β0 + βA lnAit + βC lnCit + βL lnLit + βY lnYit + vit,

In this situation, vit is the variable of the external random disturbance term under the normal distribution, and using the property that the Shephard distance function has the coefficients, we obtain

DA (Ait, Cit, Lit, Yit) = Ait DA (1, Cit, Lit, Yit),

Incorporating Equation (11) into the algorithm obtains Equation (12).

−ln Ait = β0 + βC ln Cit + βL ln Lit + βY ln Yit + vit − ln DA (Ait, Cit, Lit, Yit),

Setting uit = ln DA (Ait, Cit, Lit, Yit), uit is the value of the degree of inefficiency and follows a non-negative distribution. The following Equation can be derived for the TE of asset inputs (Equation (13)).

where vit − uit is considered a combined error component. This study combines the methodology of Zhou, et al. [50] as well as Battese and Coelli [51] to analyze longitudinal and cross-sectional data, assuming uit ~ N + (uit, σit2) and vit ~ N + (0, σv2), to derive the TE model functions for each item of input and output as shown in Equations (14)–(16).

Asset input TE: −ln Ait =β0 + βL ln Lit + βC ln Cit + βY ln Yit + vit − uit,

Cost input TE: −ln Cit = β0 + βA ln Ait + βL ln Lit + βY ln Yit + vit − uit,

Labor input TE: −ln Lit = β0 + βA ln Ait + βC ln Cit + βY ln Yit + vit − uit,

Revenue output TE: ln Yit = β0 + βA ln Ait + βC ln Cit + βL ln Lit + vit − uit,

In this study, macroeconomic variables are also included to investigate the effect of macroeconomic variables on uit, as in Equation (17):

where h represents Taiwan or mainland China, GSht: government expenditure, EFht: economic freedom, IFht: investment freedom. In addition, the dummy variable AREAit is used to differentiate the DMU across the Taiwan Strait, which is “0” if the DMU belongs to Taiwan and “1” if it belongs to mainland China. Yearit stands for the number of years the company has been in operation.

uit = δ0 + δ1GSht + δ2EFht + δ3IFht + δ4AREAit + δ5YEARit + εit,

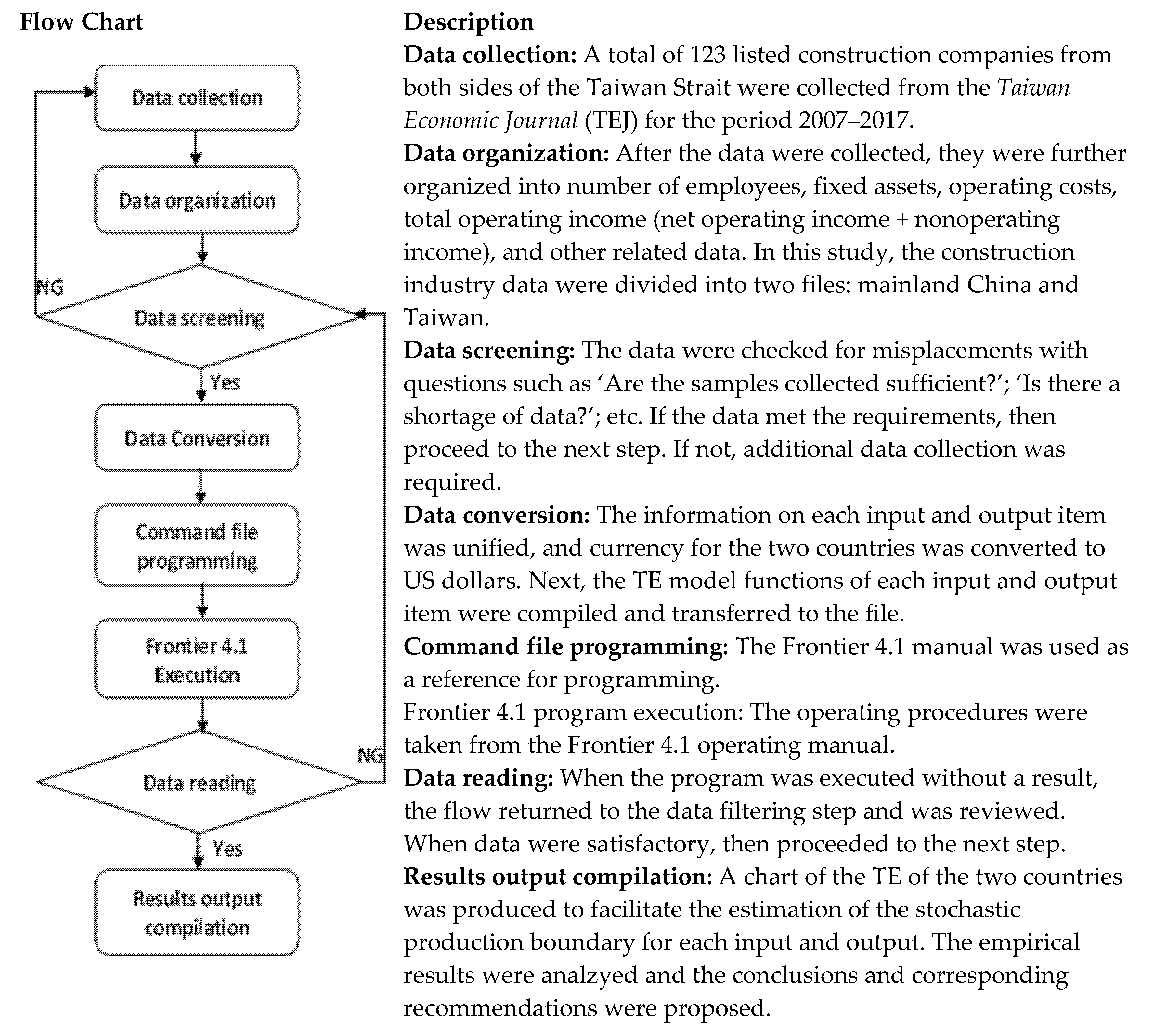

In this study, Equations (14) and (16) are estimated simultaneously to calculate the cost input efficiency of each construction company and analyze the impact of macroeconomic variables on the cost input efficiency. Figure 3 shows the data processing flow employed in this study with the implementation steps described in the right column.

2.2. Data Sources and Variables

Data were compiled from details of 123 listed construction companies published in the Taiwan Economic Journal (TEJ) for the period 2007–2017 with 59 companies in mainland China and 64 companies in Taiwan. This period was chosen as it represented the construction market under “typical conditions”. The data taken from the “Taiwan Economic Journal (TEJ)” were collected through different channels which are largely operated or supported by the Taiwanese government. For the selection of input and output items, this study considered the literature on efficiency evaluation relevant to construction firm operations. The review of the different input and output variables considered for the study is shown in Table 1.

Based on findings from the literature, the TE of inputs in the construction industry in the two regions was determined based on three variables: fixed assets (A), operating costs (C), and number of employees (L). The output variable selected was operating income (Y). The definitions of input and output variables are provided in Table 2.

Table 3 and Table 4 show the means and standard errors of the input and output variables in the construction industry across the Taiwan Strait from 2007–2017. Mainland China features a larger scale of operation along with significantly larger input and output variable values compared to Taiwanese companies.

Table 5 shows the significant differences in input and output variables with fixed assets (A), operating costs (C), number of employees (L), and operating income (Y) all reaching a significance level of p < 0.001.

Focusing on the three construction companies (two from Taiwan, one from mainland China), this study further analyzes the technical efficiency and macroeconomic variables of three inputs taken from previous studies: assets and labor [54], assets [16], and revenue. Key influential factors were also considered, including government expenditure, economic freedom, investment freedom, and years of establishment. As shown in Table 6, the three companies A, B, and C were comparatively analyzed in regard to performance of assets, costs, labor input factors, and TE of revenue production for construction companies in both regions.

3. Results

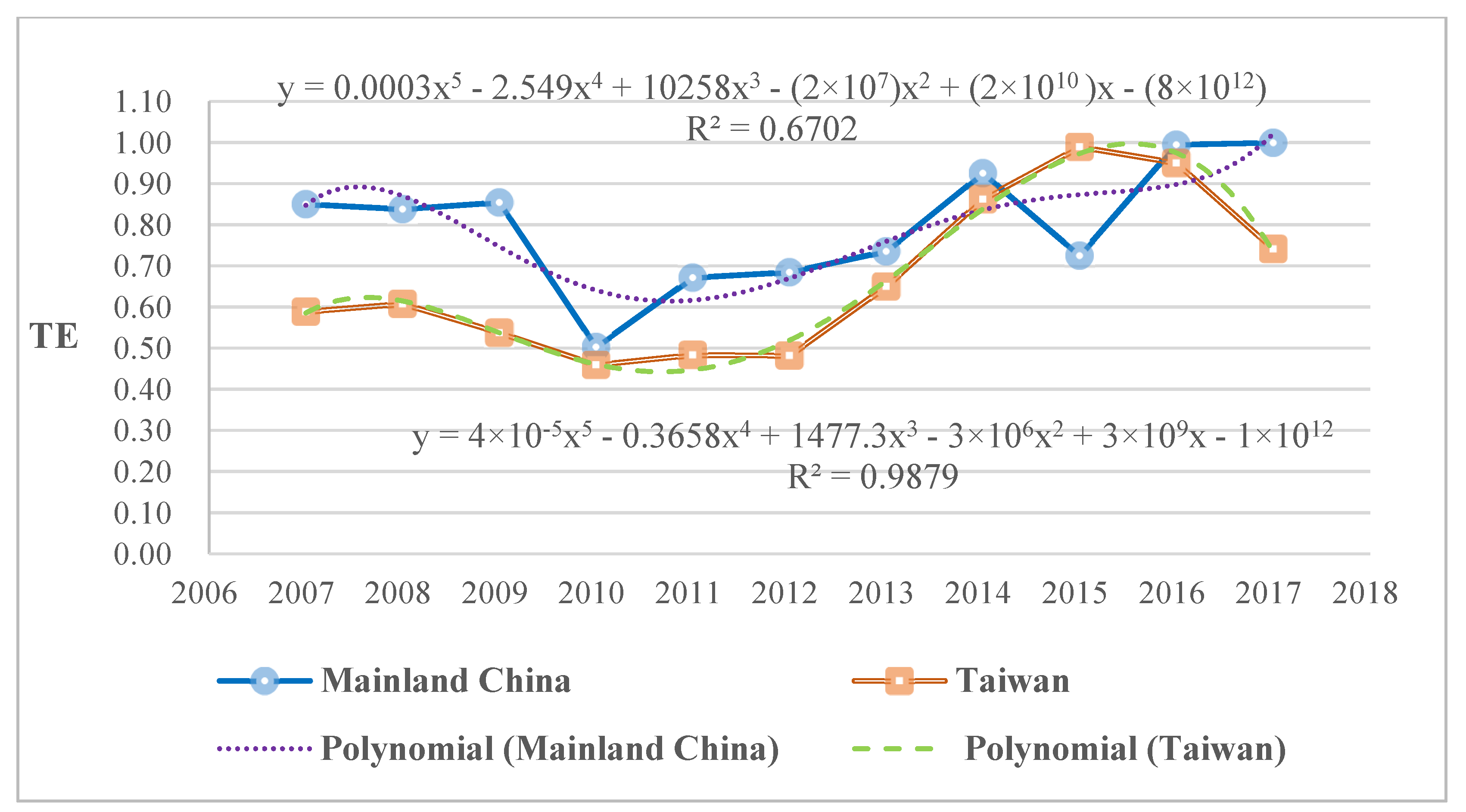

The results of the random production boundary estimation and average TE values are provided in the following section. A fifth-order polynomial regression was used to characterize the average TE trends between 2007 and 2017 for each country due to fluctuations in the TE values over time. The models were checked using the Bayesian information criterion (BIC) and R2 value.

3.1. Technical Efficiency (TE) Analysis of Asset Inputs

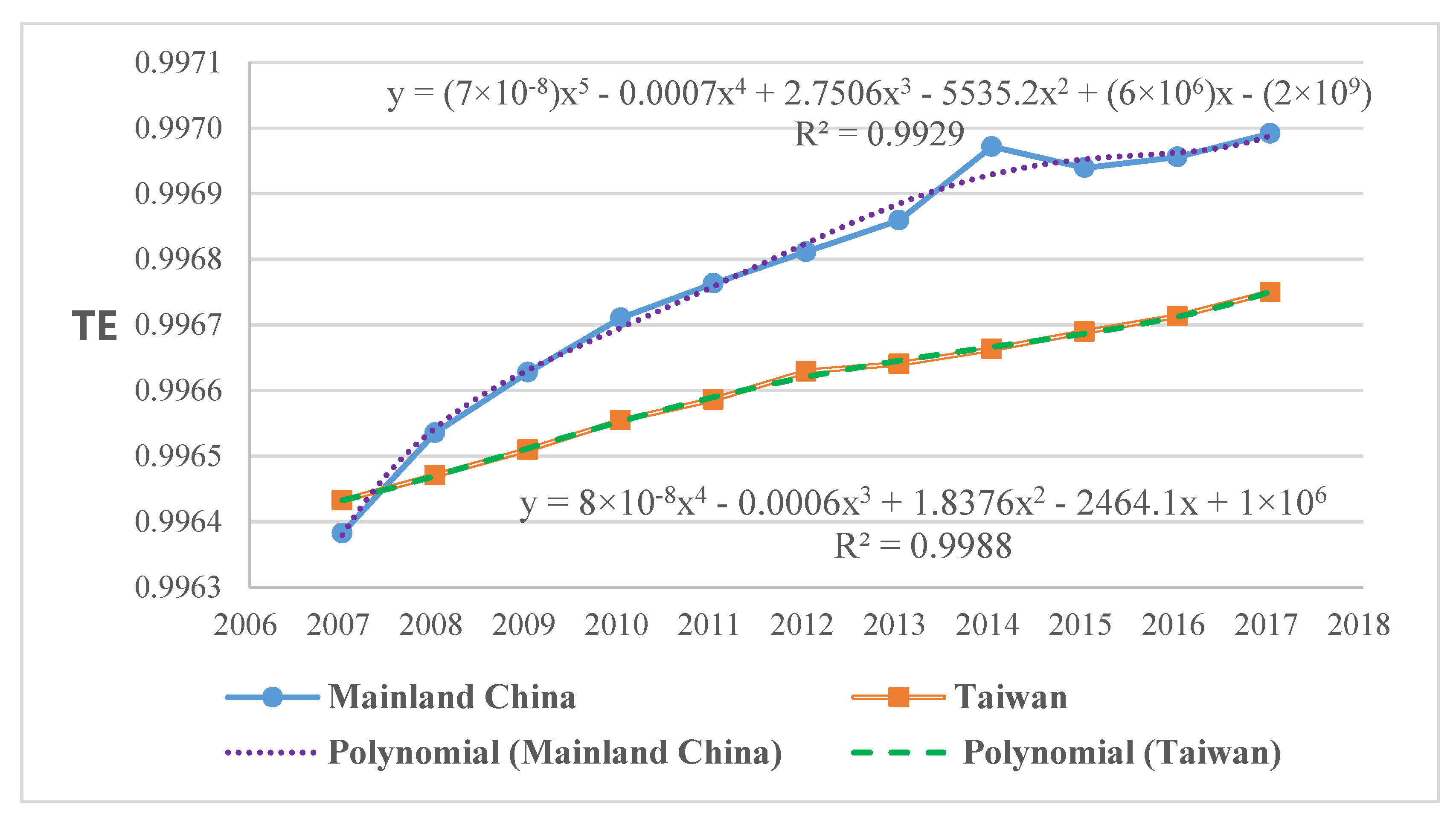

The stochastic production boundary estimation of the TE of asset inputs is provided in Table 7. The results illustrate that the TE of asset input factors for construction companies across the Taiwan Strait show notable differences in trends (Figure 4). The results also show that the TE of asset input factors in mainland China outperformed those in Taiwan. However, more importantly, the overall curvilinear trend shows that the gap across the Strait appears to be narrowing.

In mainland China, the asset input efficiency showed greater stability at the end of the 11th and 12th Five-Year Plan for National Economic and Social Development of the People’s Republic of China. After an initial period of decline, growth was observed between 2010 and 2015 and continued the following year onwards. For Taiwan, the most notable growth in asset input efficiency was observed from 2012 to 2015. This period of growth is attributed to Taiwan’s implementation of the Sales Tax on Special Goods and Services Ordinance, which came into effect on 1 June 2011, resulting in year-on-year growth in asset input efficiency.

Of the macroeconomic variables in Table 7, GSht stands for government expenditures, EFht stands for economic freedom, and IFht stands for investment freedom. Additionally, AREA is a dummy variable used to differentiate between DMUs on both sides of the Taiwan Strait, which is “0” if the DMU belongs to Taiwan and “1” if it belongs to mainland China; YEARit stands for the number of years a company has been in operation.

The macroeconomic variables show government expenditure has a significant positive correlation with the inefficiency index of the asset input factor. The results show that government influence at a macroeconomic level can negatively affect the overall TE of the construction industry. Increased government expenditure is shown to negatively affect the TE of the asset input factor. Where greater government expenditure is associated with a reduced TE value for the asset input factor of construction companies. Economic freedom was also found to have a significant negative correlation with the inefficiency index of asset input factors; that is, increased financial freedom is associated with improved TE values for the asset input factors of local construction companies, and the same holds true for investment freedom. Such results show that for Taiwanese construction companies to be competitive, the government needs to prioritize policy and regulatory-focused initiatives.

Interestingly, company longevity has a significant positive correlation with the inefficiency index of asset input factors, which means that the longer the company has been in operation, the lower the TE of asset input factors. The longer a company has been in operation, the greater the investments in assets, and thus the TE of the asset input of the construction company is reduced. The combination error (σ²) and γ inefficiency variance are shown to have a significant positive correlation with the inefficiency index of the asset input factor. Furthermore, the results of the random production boundary estimation of asset inputs show that the error is due to the variance of the inefficiency term, and the effect of the random interference term is nominal.

3.2. TE of Cost Inputs

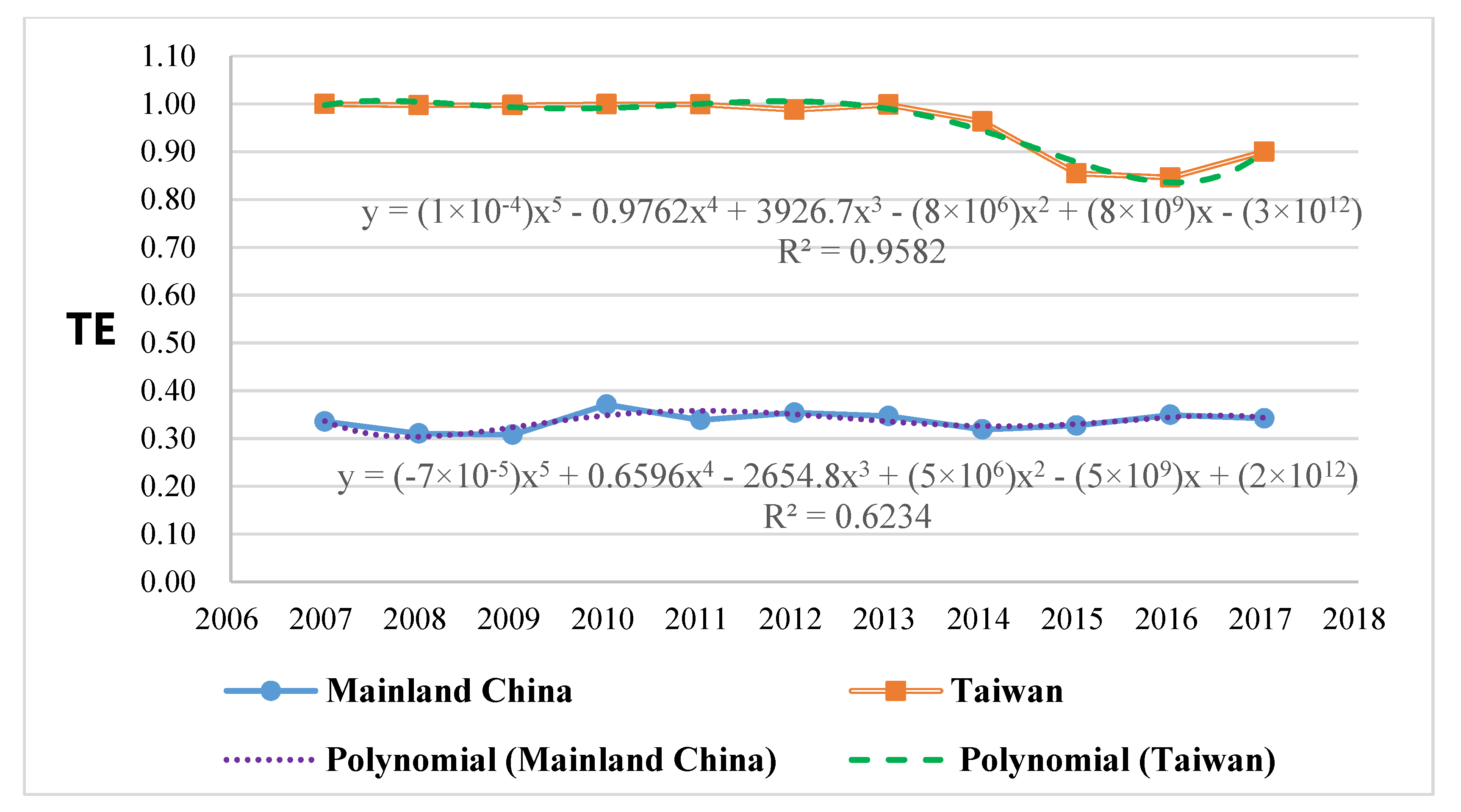

The analysis of efficiency for cost inputs shows the TE values of cost input factors; the mean TE value for cost inputs in Taiwan’s construction industry is, on average, less than mainland China’s (Figure 5).

The analysis of the macroeconomic variables shows that government expenditure has no significant effect on the inefficiency index of cost input factors, showing that, unlike asset inputs, government expenditure has no effect on the TE of cost input factors of Taiwanese construction companies. Economic freedom was also found to have no significant effect on the inefficiency index of cost input factors. Results show that economic freedom does not affect the TE of cost input factors for local Taiwanese construction companies. The degree of investment freedom was also found to have no significant effect on the inefficiency index of cost input factors, and therefore does not affect the TE of cost input factors of construction companies on both sides of the Taiwan Strait. The same was found for the effect of company longevity on the cost input factor inefficiency index, meaning it does not affect the TE of the cost input factor of cross-Strait construction companies.

In Table 8, the combination error (σ²) and γ inefficiency variance in the cost input random production boundary estimation results have a significant positive correlation with the cost input factor inefficiency index. That is, the cost input random production boundary estimation results show that the error mainly comes from the variation of the inefficiency term, and the random interference term has a very small impact.

3.3. TE of Labor Inputs

Results in Table 9 show a significant difference in the TE of labor input factors of construction companies across the Taiwan Strait. Furthermore, Figure 6 shows that the TE of labor input factors of construction companies in mainland China underperforms that of Taiwan. The polynomial linear trend analysis shows that construction firms on both sides of the Taiwan Strait have comparable gradients for the average TE value, but the linearity of the construction industry across the Taiwan Strait still has a segment gap. Such results show government expenditure also has a negative impact on the TE of labor input factors. Increased government expenditures correlate with companies having to invest more labor inputs, thus reducing their TE values. In addition, economic freedom has a significant positive correlation with the labor input factor inefficiency index, that is, greater economic freedom correlates with reduced TE values for the labor input factor of Taiwan’s construction companies. Essentially, the higher the overall investment freedom, the lower the labor input factor of TE for local construction.

Company longevity was found to have a significant positive correlation with the inefficiency index of labor input factors, showing that the longer the company has been in operation, the lower the TE value of labor input factors. Therefore, longevity has a negative effect on the TE of labor input factors for the construction industry on both sides of the Taiwan Strait. Results show that older companies with more labor invested and organizational inflexibility reduce the TE of labor inputs. The σ² combination error and γ inefficiency variance have a significant positive correlation (γ significant) with the labor input factor inefficiency index. The results of the labor input stochastic production boundary estimation show that the error is attributable to the variance of the inefficiency term.

3.4. TE Analysis of Revenue Production

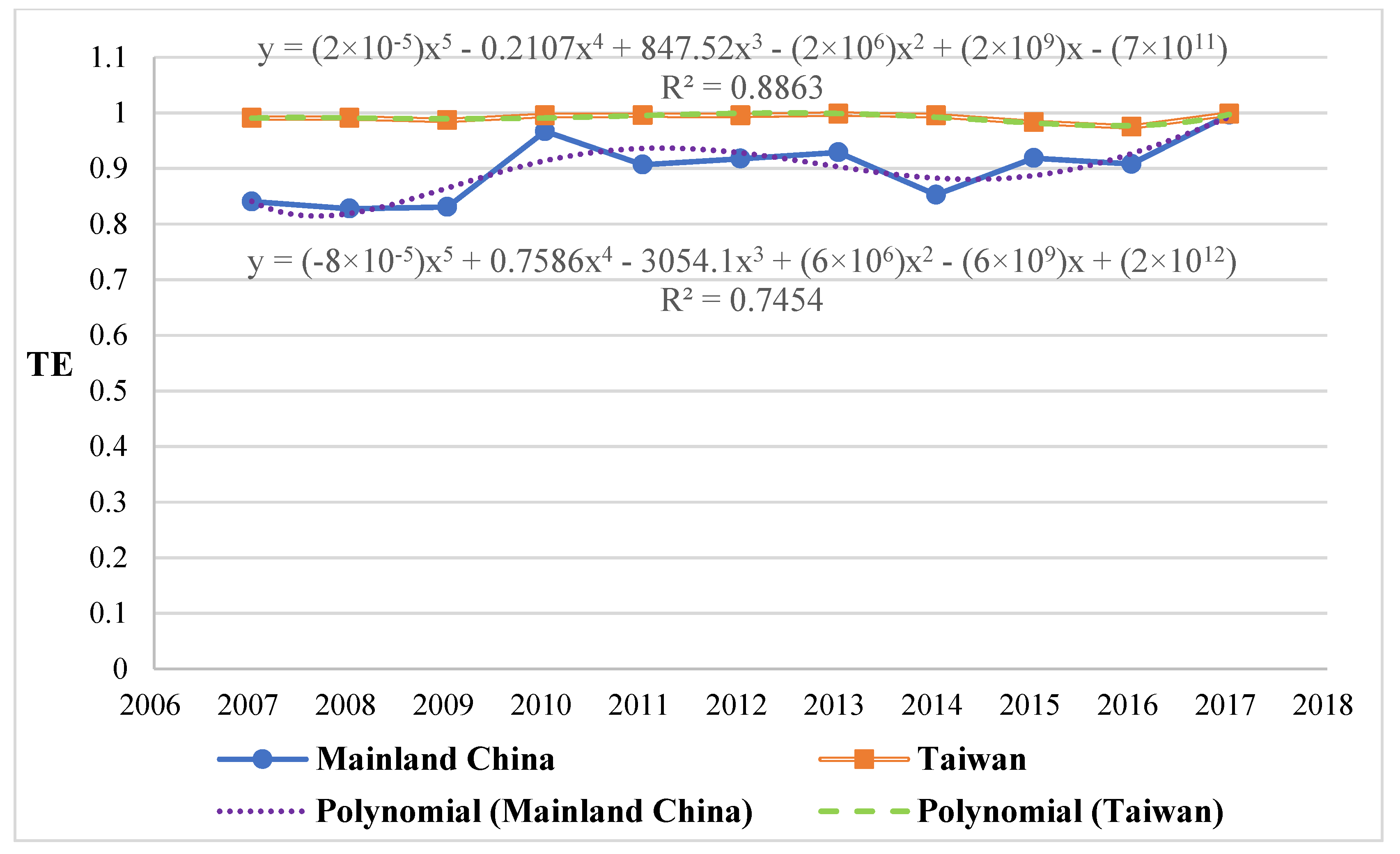

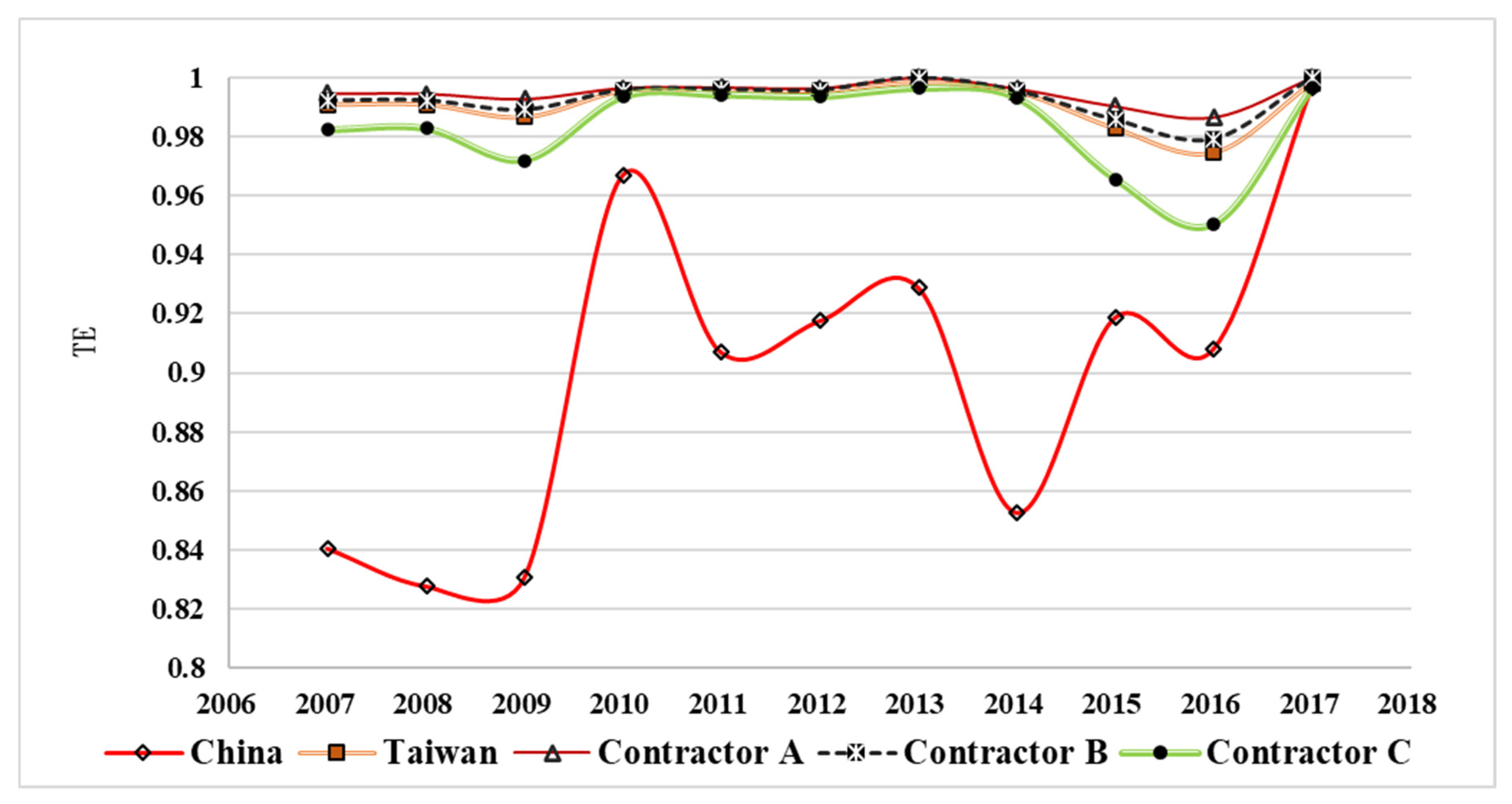

A significant difference was found between the TE of revenue and output factors of construction companies in the two regions (Table 10). The TE of revenue-generating factors in mainland China underperforms those in Taiwan, and the linear trend in Figure 7 shows that this gap is narrowing.

The macroeconomic variables in Table 10 show that government expenditures display a significant positive correlation with the inefficiency index of the revenue generation factor. An increase in government expenditures reduces the TE value of the revenue generation factor of local construction companies. These results highlight that government expenditure also has a negative effect on the TE of the revenue generation factor, showing that the greater the government expenditure, the lower the TE value of the revenue generation factor for a construction company. Economic freedom has a significant negative correlation with the inefficiency index of revenue-generating factors. The greater the economic freedom of the operating environment, the better the TE of revenue-generating factors of local construction companies. The higher the degree of investment freedom, the lower the TE of the revenue-generating factors of the local construction company.

As for the length of company operations, the duration of operations has a significant positive correlation with the inefficiency index of the revenue-generating factors. The longer the company is in operation, the lower the TE of the revenue-generating factors of the construction companies. The σ² combination error is significant, but γ has a positive effect on the revenue production factor inefficiency index. The results show that the error in the random production boundary estimates of revenue production is mainly due to the low degree of variation in the revenue production inefficiency items. The variation in revenue production among operating companies is mainly because of macroeconomic variables and random interference items.

4. Discussion

4.1. Company Comparison of Asset Inputs

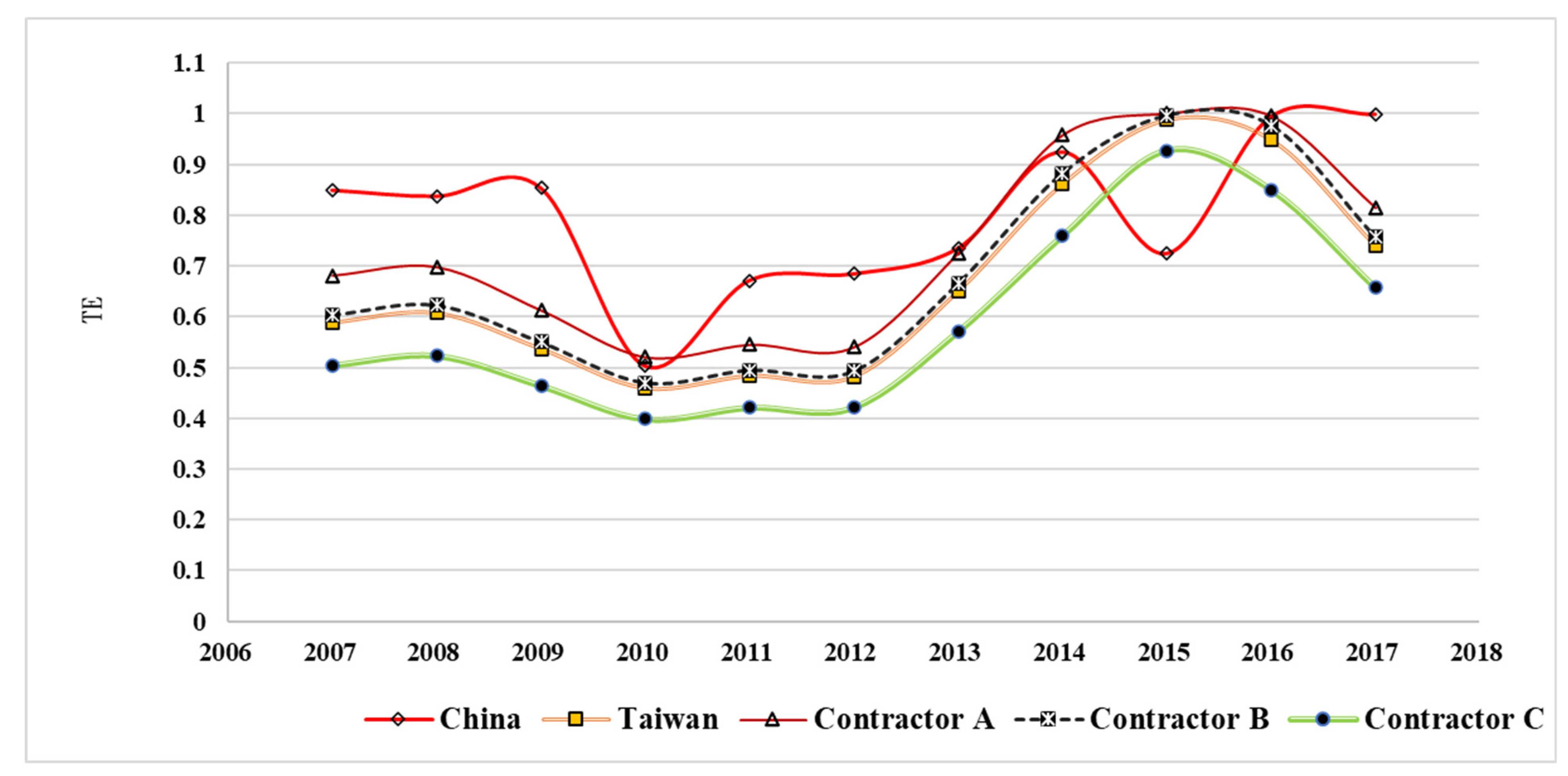

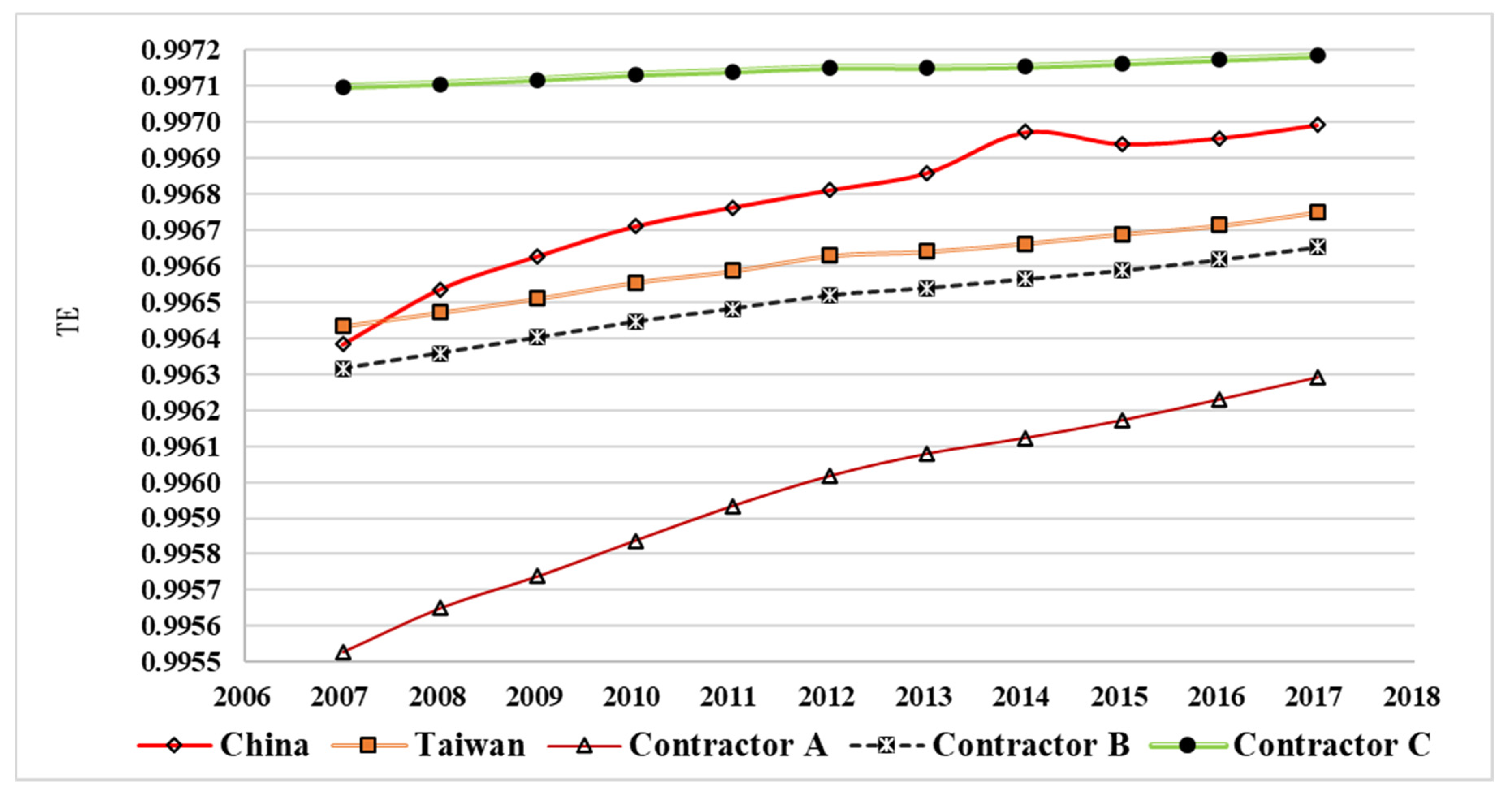

The TE values for the asset input factors for companies A, B, and C did not vary from their Taiwan counterparts, but a difference in the volatility efficiency of each company was observed (Figure 8). The TE values of the asset input factors of construction companies on both sides of the Taiwan Strait differ significantly. The TE of the asset input factors for mainland China outperforms those of Taiwan, and the TE of the asset input factors for Taiwan is lower than the average TE value for mainland China. There is still a partial gap between the target countries, but the trends show that the gap is gradually narrowing. Companies A, B, and C underperformed in comparison to the average value of mainland China TE for asset input factors. Companies A and B outperformed the average TE value of Taiwan for the asset input factors while B had the same performance as the average value for Taiwan. The TE value for A outperformed that of other domestic companies and showed a significant difference from the average TE value for Taiwan. Company C lagged behind the Taiwanese group average. Comparing the TE of the asset input factors (Figure 8), the performance of the TE value of the asset input factors for mainland China outperformed that of Company A, which in turn outperformed Company B, which outperformed the Taiwanese average, and Company C lagged behind the Taiwanese average: [mainland China > A > B ≒ Taiwan> C].

4.2. Comparison of TE of Cost Inputs

When comparing the TE of cost inputs, no significant difference (p = 0.01) was observed in the TE of the cost input factors of construction companies across the Taiwan Strait. For comparative analysis, the average value of TE of the cost input factors in mainland China was slightly lower than in Taiwan in 2007 (Figure 6) but has since fallen behind. As shown in Figure 9, Company C outperformed the Taiwan group average in terms of TE for cost input factors and outperformed the mainland China group average in terms of TE of the cost input factors. Companies A and B underperformed their peer group averages across the Taiwan Strait with Company A showing a significant performance drop in 2007. Company B similarly fell slightly behind the Taiwanese group average. All three companies have different TE performance for cost input factors, thus verifying the operating revenue/operating cost [C > B > A]. Comparing the TE of the cost input factors (Figure 5 and Figure 6), Company C outperformed mainland China, which in turn outperformed Taiwan’s peer average followed by Company B and Company A [C > mainland China > Taiwan > B > A].

4.3. Comparison of TE of labor inputs

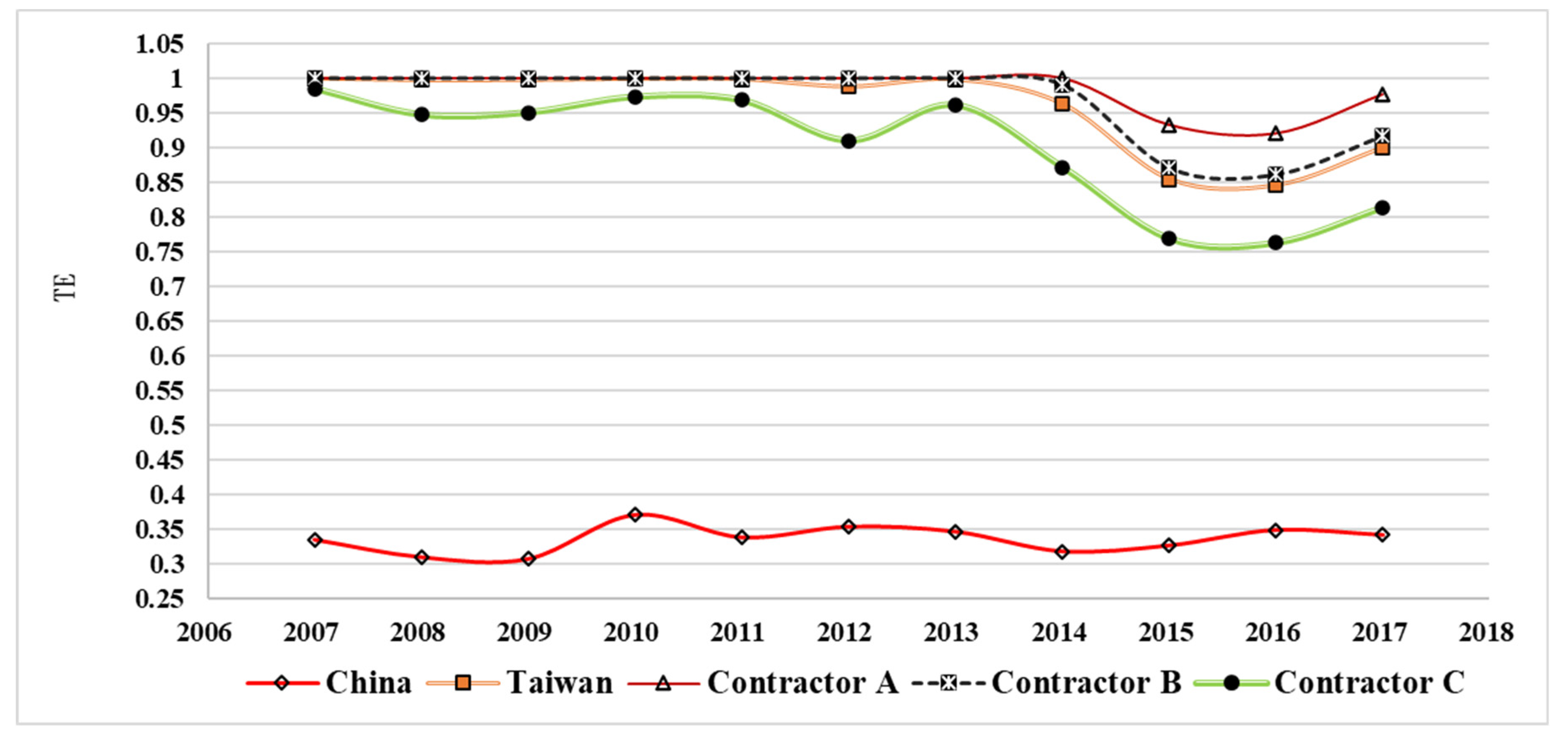

The TE values of labor input factors in the cross-Strait construction industry are shown in Figure 10. In this regard, construction companies in mainland China underperformed the companies in Taiwan. The slope of the average TE values of the construction companies on both sides of the Taiwan Strait is similar and still smooth, but some differences are found in the linearity. The TE value of the labor input factor of Company C falls behind the Taiwanese average value with a particularly wide gap from 2013 to 2017. A significant drop is observed in 2012 while the TE performance of the labor input factor of Company C still outperforms mainland China. Comparing the TE of labor input factors (Figure 10), Company A clearly outperforms Company B followed by Company B, the Taiwanese average, Company C, and the average for mainland China [A > B > Taiwan > C > mainland China].

4.4. Comparison of TE of Revenue Production

Figure 11 shows a significant difference in the TE of revenue production factors, where Companies A, B, and C show linear patterns like that of Taiwan with slight differences in terms of volatility from 2008 to 2010. No significant difference was found in volatility from 2010–2014, but significant differences emerged from 2014–2017. Taiwan’s 2009 economic recession was primarily caused by a drop in external demand following the international financial crisis. Given low domestic demand, unemployment rose sharply followed by deflation. Private investment, traditionally an important driver of Taiwan’s economic growth, remained sluggish. In 2015, multiple black swan events in international finance reduced global economic growth to 2.4% in the following year. Figure 8 shows the TE performance of revenue output factors of Company A is significantly better than that of Company B followed by the Taiwan average, Company C, and the mainland China average [A > B > Taiwan > C > mainland China].

5. Conclusions

The Taiwanese construction industry is relatively mature, but its construction market is becoming saturated. The results show that to obtain a competitive edge, Taiwan’s construction firms need to leverage their management and technical advantages in the construction industry in mainland China. Furthermore, the TE of the construction industry in other developed Asian markets outperforms that of mainland China [33]. Such context is an important consideration for Taiwanese companies planning on entering other markets within the Asian region.

The role of the government has a significant influence over TE and the success of the cross-Strait expansion. Government spending was shown to have a negative effect on the TE of the asset input factor, which is explained by the constant equation of GDP. With more economic freedom, there are fewer restrictions on construction companies (i.e., more freedom to invest), and thus the lower the asset investment, the higher the revenue output. Furthermore, companies that have been in operation longer typically have the resources to invest in more assets to obtain greater revenue. However, firm longevity has a negative impact on the TE of asset input factors in construction firms on both sides of the Taiwan Strait, which means that older companies show a greater deal of inflexibility and agility in making operational decisions.

Government spending negatively impacts the TE of the revenue production factor. Government policy needs to consider that increased economic freedom and reduced restrictions positively correlate with the revenue output performance of local construction companies, and economic freedom also has a positive effect on the TE of revenue-generating factors. Where there is greater government spending, construction companies need to invest more to maintain revenue output. Greater economic and investment freedom reduces government regulation, allowing for increased labor flows and therefore requiring additional labor investment to maintain relative revenue output.

The comparative analysis of the three selected companies in the cross-Strait region confirms that the market in mainland China is highly productive and has a positive impact on revenue and output. Taiwanese companies perform similarly to the average value of the construction industry in mainland China and have the scale and market conditions to successfully enter the construction market in mainland China. In terms of labor input, Taiwanese companies have a significant advantage over their counterparts in mainland China. This is attributed to the maturity and level of skill of Taiwan’s construction industry.

The findings of this research raise the following implications for future research regarding the international expansion of Taiwanese construction companies:

- Prior to the impacts of COVID-19, some Taiwanese companies had the scale and market advantages needed to enter the mainland Chinese market with obvious advantages in terms of labor input factors and revenue output. Further research on establishing cooperative alliances post-COVID-19 may be a practical strategy to consider for Taiwanese companies seeking to enter the mainland Chinese market.

- Changes in government policy are the key factor behind the large fluctuation of the cross-Strait construction industry’s asset investment. Before entering the construction market in mainland China, the policies in place need to allow the freedom and consistency required to effectively support construction companies operating across the Taiwan Strait.

- The impact of macroeconomic input and output variables for each item is not significant in the short term (<1 year). Where the impact becomes more pronounced is in the medium and long term, necessitating careful ongoing evaluation and planning.

- In line with current policies or plans (e.g., Taiwan’s Southbound Policy), these findings provide a useful reference for further exploration and analysis of potential new opportunities for Taiwan’s construction industry throughout the Asian region.

A further limitation to consider in future research is the limited sample size of companies. With a larger cross-section of the construction industry, it is possible to account for variations in the operational aspects of Taiwanese construction companies. While the method chosen for this analysis provides a good overview of the TE for the cross-Strait construction industry, it is not possible to investigate multiple outputs. With the research pointing to opportunities for the Taiwanese to expand into the mainland Chinese construction industry, further research on TE both before and after COVID-19 can be conducted to assist construction firms in understanding market changes.

Author Contributions

Conceptualization, W.T.C. and M.-T.W.; methodology, W.T.C. and M.-T.W.; software, M.-T.W.; validation, H.C.M.; formal analysis, A.K.K. and M.-T.W.; investigation, M.-T.W.; resources, C.-H.W.; data curation, M.-T.W.; writing—original draft preparation, W.T.C., A.K.K. and H.C.M.; writing—review and editing, W.T.C., A.K.K. and H.C.M.; visualization, C.-H.W.; supervision, W.T.C. and A.K.K.; project administration, C.-H.W. and H.C.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Not applicable.

Acknowledgments

The authors wish to thank the peer reviewers whose feedback helped to improve this paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Chen, W.T.; Merrett, H.C.; Huang, Y.H.; Bria, T.A.; Lin, Y.H. Exploring the relationship between safety climate and worker safety behavior on building construction sites in Taiwan. Sustainability 2021, 13, 3326. [Google Scholar] [CrossRef]

- Pan, N.H.; Lee, M.L. Enhancing construction companies’ marketing strategies: The construction industry in Taiwan. Int. J. Organ. Innov. 2017, 10, 143–164. [Google Scholar]

- Chien, H.J.; Barthorpe, S. The current state of information and communication technology usage by small and medium Taiwanese construction companies. J. Inf. Technol. Constr. 2009, 15, 75–85. [Google Scholar]

- Amoah, C.; Bamfo-Agyei, E.; Simpeh, F. The COVID-19 pandemic: The woes of small construction firms in Ghana. Smart Sustain. Built Environ. 2021, 11, 2046–6099. [Google Scholar] [CrossRef]

- Pao, H.W.; Wu, H.I.; Ho, S.P.; Lee, C.Y. From partner selection to trust dynamics: Evidence of the cross-country partnership of Taiwanese construction firms. J. Adv. Manag. Res. 2015, 12, 128–140. [Google Scholar] [CrossRef]

- Chen, T.T.; Wu, F.Y. Exploring critical factors for partnering in the Taiwanese construction industry. In Proceedings of the International Conference on Engineering, Project, and Production Management, Pingtung, Taiwan, 14–15 October 2010. [Google Scholar]

- The Construction and Planning Agent—Ministry of the Interior (CPAMI). Annual Report—2020; Ministry of the Interior: Taipei City, Taiwan, 2021. [Google Scholar]

- Fernandes, D.S.; Joseph, G. Organisational Strategies for Competitive Advantage in the Construction Industry: Chinese Dominance in Southern Africa. J. Constr. Dev. Ctries. 2020, 25, 1–38. [Google Scholar] [CrossRef]

- Lin, C.L.; Fan, C.; Chen, B.K. Hybrid Analytic Hierarchy Process–Artificial Neural Network Model for Predicting the Major Risks and Quality of Taiwanese Construction Projects. Appl. Sci. 2022, 12, 7790. [Google Scholar] [CrossRef]

- Public Construction Commission (PCC). Engineering Industry Globalization Promotion Plan (Policy White Paper)―Phase 2 (2018–2021); Executive Yuan: Taipei City, Taiwan, 2017.

- Public Construction Commission (PCC). Engineering Industry Globalization Promotion Plan (Policy Release)―Phase 3 (2022–2025); Executive Yuan: Taipei City, Taiwan, 2021.

- Chen, J.C. Strengthening the Scientific Research Institutions of the Ministry of Construction and Enhancing the International Competitiveness of the Construction Industry; The Storm Media: Taipei, Taiwan, 2021. [Google Scholar]

- Lin, B.J. The Development Status and Trend of Taiwan Construction Industry. Taiwan Econ. Outlook 2017, 174, 46–48. [Google Scholar]

- Hossain, M.U.; Ng, S.T.; Antwi-Afari, P.; Amor, B. Circular economy and the construction industry: Existing trends, challenges and prospective framework for sustainable construction. Renew. Sustain. Energy Rev. 2020, 130, 109948. [Google Scholar] [CrossRef]

- Dzeng, R.J.; Wu, J.S. Efficiency Measurement of the Construction Industry in Taiwan: A Stochastic Frontier Cost Function Approach. Constr. Manag. Econ. 2013, 31, 335–344. [Google Scholar] [CrossRef]

- Chen, J.H. Evaluation of operating performance of listed construction companies in Taiwan—Application of data envelopment analysis. J. Constr. 2018, 106, 17–29. [Google Scholar]

- Dzeng, R.J.; Wu, J.S. The Cost Efficiency of Construction Industry in Taiwan. Open Constr. Build. Technol. J. 2012, 6, 8–16. [Google Scholar] [CrossRef] [Green Version]

- Fernandez-Lopez, X.L.; Coto-Millan, P. From the boom to the collapse: A technical efficiency analysis of the Spanish construction industry during the financial crisis. Constr. Econ. Build. 2015, 15, 104–117. [Google Scholar] [CrossRef] [Green Version]

- Hendrawan, R.; Utama, P.P. Efficiency Measurement of Building Construction Sector Companies Listed on Indonesia Stock Exchange: Stochastic Frontier Analysis Approach. Asian J. Manag. Sci. Educ. 2020, 9, 1–15. [Google Scholar]

- Yin, T. Research on Spatial Spillover Effect of Total Factor Productivity in Construction Industry: Evidence from Yangtze River Delta Region in China. Am. J. Ind. Bus. Manag. 2021, 11, 1140–1152. [Google Scholar] [CrossRef]

- Boyd, G.A.; Lee, J.M. Measuring plant level energy efficiency and technical change in the U.S. metal-based durable manufacturing sector using stochastic frontier analysis. Energy Econ. 2019, 81, 159–174. [Google Scholar] [CrossRef] [Green Version]

- Wanke, P.; Tan, Y.; Antunes, J.; Hadi-Vencheh, A. Business environment drivers and technical efficiency in the Chinese energy industry: A robust Bayesian stochastic frontier analysis. Comput. Ind. Eng. 2020, 144, 10648. [Google Scholar] [CrossRef]

- Sayavong, V. Technical inefficiency of the manufacturing sector in Laos: A case study of the firm survey. J. Asian Bus. Econ. Stud. 2021; ahead-of-print. [Google Scholar]

- Jian, L.; Peng, L.; Shan, F.; Ping, W. Administrative hierarchy, city size, and urban productivity. Macro-Qual. Res. 2018, 1, 31–43. [Google Scholar]

- Jin, G.; Wu, F.; Li, Z.H.; Guo, B.S.; Zhao, X. Measurement and analysis of land use and ecological efficiency in rapidly urbanizing areas. J. Ecol. 2017, 37, 8048–8057. [Google Scholar]

- Hsieh, H.P. Study on the Operational Efficiency of Japanese Securities Firms. Master’s Thesis, Institute of Business Administration, School of Management, National Chiao Tung University, Hsinchu, Taiwan, 2016. [Google Scholar]

- Chang, T.P.; Hu, J.L.; Chiu, L.H. Application of stochastic common border analysis to explore the efficiency of cross-strait banking inputs. Appl. Econ. Ser. 2016, 100, 149–181. [Google Scholar]

- Chang, W.L. Itemized Input Efficiency of Mutual Funds in Taiwan. Master’s Thesis, Institute of Business Administration, School of Management National Chiao Tung University, Hsinchu, Taiwan, 2013. [Google Scholar]

- Hu, J.L.; Honma, S.; Hsieh, H.P. Input efficiency of Japanese securities firms: An application of Stochastic Frontier Analysis. J. Manag. Res. 2018, 18, 71–89. [Google Scholar]

- Chang, L.C. Study on the Efficiency of Sub-Inputs of Taiwan’s Securities Firms: Application of Stochastic Boundary Analysis. Master’s Thesis, Graduate School of Management, National Chiao Tung University, Hsinchu, Taiwan, 2013. [Google Scholar]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Yang, Z.; Fang, H.; Xue, X. Sustainable efficiency and CO2 reduction potential of China’s construction industry: Application of a three-stage virtual frontier SBM-DEA model. J. Asian Archit. Build. Eng. 2021, 21, 604–617. [Google Scholar] [CrossRef]

- Park, J.L.; Yoo, S.K.; Lee, J.S.; Kim, J.H.; Kim, J.J. Comparing the Efficiency and Productivity of Construction Firms in China, Japan, and Korea Using DEA and DEA-based Malmquist. J. Asian Archit. Build. Eng. 2015, 14, 57–64. [Google Scholar] [CrossRef] [Green Version]

- Wong, W.P.; Gholipour, H.F.; Bazrafshan, E. How Efficient Are Real Estate and Construction Companies in Iran’s Close Economy? Int. J. Strateg. Prop. Manag. 2012, 16, 392–413. [Google Scholar] [CrossRef] [Green Version]

- Al-Malkawi, H.A.N.; Pillai, R. The Impact of Financial Crisis on UAE Real Estate and Construction Sector: Analysis and Implications. Humanomics 2013, 29, 115–135. [Google Scholar] [CrossRef]

- You, T.; Zi, H. The economic crisis and efficiency change: Evidence from the Korean construction industry. Appl. Econ. 2007, 39, 1833–1842. [Google Scholar] [CrossRef]

- Kapelko, M.; Lansink, A.O. Technical efficiency and its determinants in the Spanish construction sector pre- and post-financial crisis. Int. J. Strateg. Prop. Manag. 2015, 19, 96–109. [Google Scholar] [CrossRef]

- Lee, S.M. Competitive Analysis of Taiwan’s Construction Industry. Master’s Thesis, Department of Civil and Disaster Prevention Engineering, National Union University, Miaoli, Taiwan, 2011. [Google Scholar]

- Chen, B.L.; Chou, K.H.; Cheng, Y.J.; Lin, C.C.; Dai, Y.C. Analysis of operating efficiency of listed construction companies in Taiwan. J. Constr. 2010, 1, 25–50. [Google Scholar]

- Huang, T.S.; Chang, P.K. A comparison of technical efficiency of common boundary in our construction industry. Manag. Syst. 2015, 22, 149–174. [Google Scholar]

- Mujaddad, H.G.; Ahmad, H.K. Measuring efficiency of Manufacturing Industries in Pakistan: An Application of DEA Double Bootstrap Technique. Pak. Econ. Soc. Rev. 2007, 54, 363–384. [Google Scholar]

- Erena, O.T.; Kalko, M.M.; Debele, S.A. Technical efficiency, technological progress and productivity growth of large and medium manufacturing industries in Ethiopia: A data envelopment analysis. Cogent Econ. Financ. 2021, 9, 1997160. [Google Scholar] [CrossRef]

- Goncharuk, A.G. Impact of political changes on industrial efficiency: A case of Ukraine. J. Econ. Stud. 2007, 34, 324–340. [Google Scholar] [CrossRef]

- Goncharuk, A.G. Using the DEA in efficiency management in industry. Int. J. Product. Qual. Manag. 2007, 2, 241–262. [Google Scholar] [CrossRef]

- Hu, J.L.; Chang, T.P.; Chu, H.H. Comparison of itemized input efficiency of cross-strait life insurance industry: Application of stochastic boundary analysis. Soochow J. Econ. Bus. 2014, 85, 41–46. [Google Scholar]

- Tsai, Y.Y. Efficiency of Itemized Inputs in Taiwan Regional Funds: An Application of Stochastic Boundary Analysis. Master’s Thesis, Institute of Business Administration, College of Management, National Chiao Tung University, Hsinchu, Taiwan, 2016. [Google Scholar]

- Huang, K.R.; Fu, C.T.; Huang, M.E. Performance Evaluation: Theory and Application of Efficiency and Productivity; Xin Lu Book Co.: Taipei, Taiwan, 2010. [Google Scholar]

- Xie, T.; Zhu, X. Research on the measurement of contribution value of scientific and technological talents in China’s mining industry—Innovative application based on “Cobb Douglas production function method”. In IOP Conference Series: Earth and Environmental Science; IOP Publishing: Bristol, UK, 2022; Volume 1087. [Google Scholar]

- McKenzie, T. Cobb-Douglas Production Function. 2022. Available online: https://inomics.com/terms/cobb-douglas-production-function-1456726 (accessed on 23 July 2022).

- Zhou, P.B.; Ang, W.; Zhou, D.Q. Measuring Economy-Wide Energy Efficiency Performance: A Parametric Frontier Approach. Appl. Energy 2012, 90, 196–200. [Google Scholar] [CrossRef]

- Battese, G.E.; Coelli, T.J. A Model for Technical Inefficiency Effects in a Stochastic Frontier Production Function for Panel Data. J. Product. Anal. 1995, 20, 325–332. [Google Scholar] [CrossRef] [Green Version]

- Coelli, T.J. A Guide to FRONTIER Version 4.1: A Computer Program for Stochastic Frontier Production and Cost Function Estimation; CPEA Working Papers: Armidale, Australia, 1996. [Google Scholar]

- Zhang, B.G.; Huang, T.X.; Guo, J.Y. Analysis of Productivity Changes at the Common Boundary of Listed Construction and Architecture Companies: Application of Input-Oriented Distance Function. Soochow J. Econ. Bus. 2014, 85, 1–40. [Google Scholar]

- Wu, J.H.; Ho, B.J.; Huang, Y.C. The Performances and Management Strategy for Taiwan’s Construction Industries. J. Archit. 2008, 64, 25–48. [Google Scholar]

- Wu, C.H. Application of the Random Boundary Method to the Cost Efficiency and Influence Factors of Construction Companies. Ph.D. Thesis, Department of Civil Engineering, National Chiao Tung University, Hsinchu, Taiwan, 2013. [Google Scholar]

- Wang, K.T. Performance Evaluation of Listed Cabinet-Building Companies in Taiwan-Application of the Random Production Boundary Method. Master’s Thesis, Ling Tung University of Science and Technology, Taichung, Taiwan, 2017. [Google Scholar]

- Zheng, X.; Chau, K.W.; Hui, E.C.M. Efficiency Assessment of Listed Real Estate Companies: An Empirical Study of China. Int. J. Strateg. Prop. Manag. 2011, 15, 91–104. [Google Scholar] [CrossRef]

Figure 1.

Overview of the research framework [50].

Figure 1.

Overview of the research framework [50].

Figure 2.

Technical Efficiency Model of Cross-Strait Construction Industry [50].

Figure 2.

Technical Efficiency Model of Cross-Strait Construction Industry [50].

Figure 3.

Data processing flow used with the description of the implementation steps in the right column. The Frontier 4.1 manual [52].

Figure 3.

Data processing flow used with the description of the implementation steps in the right column. The Frontier 4.1 manual [52].

Figure 4.

Average TE value of cross-Strait construction industry asset input factors of Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 4.

Average TE value of cross-Strait construction industry asset input factors of Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 5.

Average TE values of cost input factors in the cross-Strait construction industry for Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 5.

Average TE values of cost input factors in the cross-Strait construction industry for Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 6.

TE values of labor input factors in the cross-Strait construction industry for Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 6.

TE values of labor input factors in the cross-Strait construction industry for Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 7.

TE values of cross-Strait construction industry revenue and output factors for Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 7.

TE values of cross-Strait construction industry revenue and output factors for Taiwan (TW) and mainland China (MC) between 2007 and 2017.

Figure 8.

Comparison of TE of Cross-Strait Construction Industry 2007 to 2017.

Figure 9.

Comparison of TE of Cost Input Factors in the Cross-Strait Construction Industry 2007 to 2017.

Figure 9.

Comparison of TE of Cost Input Factors in the Cross-Strait Construction Industry 2007 to 2017.

Figure 10.

Comparison of TE of Labor Input Factors in Cross-Strait Construction Industry 2007 to 2017.

Figure 10.

Comparison of TE of Labor Input Factors in Cross-Strait Construction Industry 2007 to 2017.

Figure 11.

Comparison of TE of Revenue and Output Factors in the Cross-Strait Construction Industry 2007 to 2017.

Figure 11.

Comparison of TE of Revenue and Output Factors in the Cross-Strait Construction Industry 2007 to 2017.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Input and output variables related to construction industry efficiency evaluation.

| Items | Inputs and Outputs | Huang & Chang [40] | Zhang et al. [53] | Wong et al. [34] | Wu et al. [54] | Wu [55] | Wang [56] | Dzeng & Wu [17] | Dzeng & Wu [15] | Zheng et al. [57] | Chen [16] |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Inputs | Capital price | ● | |||||||||

| Labor price | ● | ||||||||||

| Equipment cost | ● | ||||||||||

| Equipment cost | ● | ||||||||||

| Total assets | ● | ● | ● | ||||||||

| Total liabilities | ● | ||||||||||

| Shareholders’ equity | ● | ||||||||||

| Capital stock | ● | ● | ● | ● | ● | ||||||

| Fixed assets | ● | ||||||||||

| Net fixed assets | ● | ● | ● | ||||||||

| Operating costs | ● | ● | ● | ● | ● | ● | ● | ||||

| Number of employees | ● | ● | ● | ● | ● | ● | ● | ● | ● | ||

| Outputs | Debt ratio | ● | |||||||||

| Gross profit from operations | ● | ● | |||||||||

| Net income after tax | ● | ||||||||||

| Operating income | ● | ● | ● | ● | |||||||

| Net income from operations | ● | ● | ● | ● | ● | ● | |||||

| Nonoperating income | ● | ● |

Table 2.

Definition of Input and output elements.

| Item | Input/output | Definition |

|---|---|---|

| Inputs | Fixed assets (A) | Cost of fixed assets and net of accumulated depreciation as of the end of the year. |

| Operating cost (C) | The income statement includes operating costs plus operating expenses, net of employment costs. | |

| Number of employees (L) | Total number of employees at the end of the fiscal year. | |

| Output | Operating income (Y) | “Net operating income” is total operating income annually, net of refunds and discounts, and “non-operating income” is total non-operating income in the income statement. Net operating income + nonoperating income is presented in this study. |

Table 3.

Inputs and Output Variables for Mainland China.

| Year | Inputs Variables | Output Variable | ||

|---|---|---|---|---|

| Fixed Assets (A) | Operating Costs (C) | Number of Employees (L) | Operating Income (Y) | |

| 2007 | 150,717 (57,327) | 1,284,813 (593,683) | 11,373 (5596) | 1,444,610 (665,312) |

| 2008 | 207,119 (81,728) | 1,756,323 (814,468) | 11,875 (5735) | 1,974,320 (911,420) |

| 2009 | 267,151 (107,176) | 2,588,635 (1,225,333) | 12,462 (6041) | 2,894,243 (1,360,869) |

| 2010 | 321,762 (130,229) | 3,542,627 (1,687,351) | 13,410 (6403) | 3,954,318 (1,869,421) |

| 2011 | 389,618 (149,902) | 4,034,773 (1,854,236) | 14,464 (6774) | 4,563,122 (2,086,602) |

| 2012 | 440,382 (163,840) | 4,532,648 (2,074,113) | 15,612 (7024) | 5,134,554 (2,339,479) |

| 2013 | 501,888 (183,962) | 5,483,698 (2,520,506) | 16,303 (7233) | 6,196,908 (2,829,566) |

| 2014 | 516,332 (195,272) | 6,072,390 (2,783,455) | 16,886 (7483) | 6,907,099 (3,153,419) |

| 2015 | 558,257 (205,911) | 6,305,863 (2,898,355) | 17,081 (7528) | 7,175,088 (3,286,399) |

| 2016 | 587,839 (206,890) | 6,513,967 (2,966,969) | 17,541 (7620) | 7,265,120 (3,281,260) |

| 2017 | 645,605 (221,718) | 6,969,090 (3,165,771) | 18,352 (7764) | 7,812,648 (3,517,100) |

Note: n = 649. The values in brackets are standard errors.

Table 4.

Inputs and Output Variables for Taiwan.

| Year | Inputs Variables | Outputs Variables | ||

|---|---|---|---|---|

| Fixed Assets (A) | Operating Costs (C) | Number of Employees (L) | Operating Income (Y) | |

| 2007 | 39,679 (8,979) | 96,686 (14,396) | 340 (77) | 124,596 (17,521) |

| 2008 | 47,513 (13,481) | 102,857 (16,936) | 338 (78) | 128,247 (19,796) |

| 2009 | 46,918 (13,470) | 96,016 (14,627) | 334 (78) | 125,336 (18,882) |

| 2010 | 51,545 (14,884) | 109,696 (17,745) | 370 (86) | 148,894 (23,951) |

| 2011 | 57,923 (17,439) | 114,407 (18,452) | 399 (97) | 159,119 (224,531) |

| 2012 | 66,471 (20,403) | 117,536 (18,761) | 379 (94) | 165,057 (23,965) |

| 2013 | 40,004 (13,904) | 140,617 (22,953) | 411 (102) | 200,759 (30,915) |

| 2014 | 39,992 (14,844) | 125,038 (22,768) | 402 (98) | 174,453 (29,844) |

| 2015 | 42,344 (15,077) | 114,432 (20,578) | 401 (98) | 156,252 (27,129) |

| 2016 | 39,507 (12,395) | 118,079 (21,294) | 365 (79) | 156,935 (27,267) |

| 2017 | 36,407 (8490) | 110,001 (15,356) | 359 (78) | 146,805 (20,010) |

Note: n = 704. The values shown in brackets are standard errors.

Table 5.

Average of input/output variables of cross-Strait construction industry.

| Variable | Mainland China Average | Taiwan Average | t Test (p-Value) |

|---|---|---|---|

| Fixed assets (A) | 416,970 | 46,209 | 7.4926 (p < 0.001) |

| Operating costs (C) | 4,462,256 | 113,215 | 6.4942 (p < 0.001) |

| Number of employees (L) | 15,033 | 372 | 7.1173 (p < 0.001) |

| Operating income (Y) | 5,029,275 | 153,314 | 6.4975 (p < 0.001) |

Table 6.

Efficiency Comparison Company Basic Information.

| Company | Capital (NTD *) | Ratio of the Main Products |

|---|---|---|

| A | 2,085,205 | Construction (99.6%), Engineering (0.4%) |

| B | 1,134,400 | Office Building (32.3%), Civil Engineering (24.6%), Other Projects (20.7%) |

| C | 3,475,274 | Engineering (100%) |

* NTD thousand dollars.

Table 7.

Asset input random production boundary estimation results.

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | −1.3646 | 0.3410 | −4.0017 *** |

| lnLit | −0.7965 | 0.0418 | −19.0331 *** |

| lnCit | 0.0782 | 0.0843 | 0.9273 |

| lnYit | −0.3435 | 0.0995 | −3.4533 *** |

| δ0 | 5.2670 | 1.2260 | 4.2963 *** |

| GSht | 3.2661 | 0.6345 | 5.1473 *** |

| EFht | −7.9755 | 1.2780 | −6.2407 *** |

| IFht | −3.7200 | 0.6250 | −5.9521 *** |

| AREAit | −3.1291 | 0.5086 | −6.1527 *** |

| YEARit | 0.1755 | 0.0381 | 4.6025 *** |

| σ² | 2.4375 | 0.1065 | 22.8777 *** |

| γ | 1 × 10−4 | 7 × 10−6 | 21.0489 *** |

| log likelihood function = −2527.15 | |||

| Total obs. 1353 | |||

Note: *** represents significance of 1%, respectively; σ² = σ²u + σ² v; γ = σ² u/σ².

Table 8.

Results of random production boundary estimation of cost inputs.

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | 1.2259 | 0.0891 | 13.7631 *** |

| lnAit | 0.0057 | 0.0083 | 0.6882 |

| lnLit | −0.0372 | 0.0141 | −2.6415 *** |

| lnYit | −1.0590 | 0.0122 | −86.8771 *** |

| δ0 | −0.0057 | 0.7377 | −0.0077 |

| GSht | −0.0055 | 0.7771 | −0.0071 |

| EFht | 0.0011 | 0.6788 | 0.0017 |

| IFht | 0.0030 | 0.5854 | 0.0051 |

| AREAit | −0.0214 | 0.4161 | −0.0515 |

| YEARit | −0.0283 | 0.1022 | −0.2765 |

| σ² | 0.2338 | 0.0112 | 20.9461 *** |

| γ | 0.0016 | 0.0015 | 1.0719 *** |

| log likelihood function = | −941.17 | ||

| Total obs. | 1353 | ||

Note: *** represents significance of 1%, respectively; σ² = σ²u + σ²v; γ = σ²u/σ².

Table 9.

Labor input random production boundary estimation results.

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | 3.0478 | 0.1756 | 17.3557 *** |

| lnAit | −0.2472 | 0.0138 | −17.9752 *** |

| lnCit | −0.1185 | 0.0492 | −2.4078 ** |

| lnYit | −0.4043 | 0.0558 | −7.2458 *** |

| δ0 | −4.4145 | 0.9773 | −4.5169 *** |

| GSht | 1.0798 | 0.2985 | 3.6177 *** |

| EFht | 2.8631 | 0.6725 | 4.2571 *** |

| IFht | 1.2688 | 0.2855 | 4.4447 *** |

| AREAit | 2.3278 | 0.2817 | 8.2648 *** |

| YEARit | 0.1500 | 0.0367 | 4.0897 *** |

| σ² | 0.7753 | 0.0291 | 26.6518 *** |

| γ | 2 × 10−5 | 8× 10−6 | 2.1515 ** |

| log likelihood function = | −1747.22 | ||

| Total obs. | 1353 | ||

Note: **, *** represents significance of 5% and 1%, respectively; σ² = σ²u + σ²v; γ = σ²u/σ².

Table 10.

Estimated results of revenue output stochastic production margins.

| Parameters | Relationship | Standard Deviation | t-Value |

|---|---|---|---|

| β0 | 1.7617 | 0.0469 | 37.5761 *** |

| lnAit | 0.0365 | 0.0072 | 5.0947 *** |

| lnCit | 0.8242 | 0.0073 | 112.1341 *** |

| lnLit | 0.0512 | 0.0080 | 6.3601 *** |

| δ0 | −1.4463 | 0.2328 | −6.2112 *** |

| GSht | 0.8719 | 0.3408 | 2.5584 ** |

| EFht | −1.2415 | 0.3051 | −4.0694 *** |

| IFht | 1.8899 | 0.6449 | 2.9308 *** |

| AREAit | 0.8029 | 0.2346 | 3.4227 *** |

| YEARit | 0.0547 | 0.0140 | 3.9140 *** |

| σ² | 0.1879 | 0.0070 | 26.8012 *** |

| γ | 0.0030 | 0.0018 | 1.6731 * |

| log likelihood function = | −747.05 | ||

| Total obs. | 1353 | ||

Note: *, **, *** represents significance of 10%, 5%, 1%, respectively; σ² = σ²u + σ²v; γ = σ²u/σ².

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Chen, W.T.; Kiani, A.K.; Wu, M.-T.; Merrett, H.C.; Wang, C.-H. Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China. Sustainability 2023, 15, 941. https://doi.org/10.3390/su15020941

AMA Style

Chen WT, Kiani AK, Wu M-T, Merrett HC, Wang C-H. Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China. Sustainability. 2023; 15(2):941. https://doi.org/10.3390/su15020941

Chicago/Turabian StyleChen, Wei Tong, Adiqa Kausar Kiani, Ming-Tsung Wu, Hew Cameron Merrett, and Chih-Hsing Wang. 2023. "Comparison of the Technical Efficiency of Construction Industries—A Case Study of Taiwan and Mainland China" Sustainability 15, no. 2: 941. https://doi.org/10.3390/su15020941

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.