Sustainable Knowledge Creation and Corporate Outcomes: Does Corporate Data Governance Matter?

Department of Accounting and Finance, Cyprus International University, Via Mersin 10, Lefkosa 0090, Northern Cyprus, Turkey

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(20), 5575; https://doi.org/10.3390/su11205575

Submission received: 23 September 2019

/

Revised: 5 October 2019

/

Accepted: 7 October 2019

/

Published: 10 October 2019

(This article belongs to the Section Economic and Business Aspects of Sustainability)

Abstract

:It has been recognized that data curation and governance can equip firms with the capability to generate sustainable knowledge. However, the antecedent and consequences of sustainable knowledge creation have not been systematically explored. The model in this study describes how sustainable knowledge creation enhances corporate information transparency, innovation, and financial and market performance. In addition, we also show how corporate data governance fosters sustainable knowledge creation among corporations listed in the Amman Stock exchange. Using survey data from (n = 180) publicly listed corporations and a judgmental sampling technique, we applied partial least squares structural equation modeling (PLS–SEM). Results from PLS–SEM show that corporate data governance is a predictor for sustainable knowledge creation, and sustainable knowledge creation is also a predictor for corporate information transparency and innovative, financial, and market performance. The study offers guidelines for corporate managers to effectively manage and use corporate data responsibly to attain sustainable knowledge creation which in turn results in greater corporate performance and desired outcomes. Implications for practice and theory are discussed.

1. Introduction

Inquiries about how likely it is that large corporate data governance can help firms gain a competitive advantage are still very scarce. Emerging research commentaries echoed the possible contributions of corporate data governance through internalized and institutionalized practices, strategic flexibility, and the acquisition of external knowledge in adapting to the ecosystem [1,2]. According to Otto [3] “any corporatewide framework designed to determine decision-related rights and duties associated with data management as a corporate resource” is data governance (p. 47). Raymond et al. [2] and Alhassan, Sammon and Daly [4] stated that the concept of data governance equates to corporate assets that have value or potential value. Tallon, Ramirez and Short [5] claimed that corporate data governance can significantly contribute to enhanced decision-making. According to Loebbecke and Picot [6], corporate data governance practices allowed airlines to acquire, store, analyze, and interpret data, and then assimilate it with real-time data for decision-making purposes. In this regard, such practices are bound to create and generate pools of knowledge which are necessary for data-driven decision-making and/or insight generation.

Sustainable knowledge and its management emerged as a critical intangible asset for corporations [7]; more specifically, knowledge creation processes help to attain a long-term competitive advantage [8]. In their influential work, Nonaka and Von Krogh [9] stated that knowledge creation entails making available and developing knowledge generated by corporate entities and crystallizing and merging it with the corporate knowledge system. To create new knowledge, “new conceptual artifacts and structures for interaction must be assembled, which provide possibilities as well as constrain the entities in consequent knowledge-creation cycles” [10]. In the context of this study, corporate data governance is an important artifact. The capability to create and utilize knowledge is the most significant challenge managers are facing. It appears that the literature is still yet to unveil the process in which a corporation creates and utilizes knowledge. Mao et al. [11] asserted that the associations between various types of information technology and/or governance resources with knowledge creation are unclear, which calls for additional inquiry. In the context of this study, how corporate data governance contributes to sustainable corporate knowledge creation.

There are conflicting and incoherent findings in the literature. For instance, Zack, McKeen and Singh [12] showed that knowledge management (KM) practices, e.g., knowledge creation, have a direct effect on organizational performance and not on financial performance. They argued that organizational performance can later be translated to financial performance. In contrast, Cohen and Olsen [13] found a direct association between KM activities and financial and market performance. In his review, Inkinen [14] argued that KM activities can result in both financial and nonfinancial outcomes (e.g., process efficiency, innovation coordination, responsiveness, etc.), insinuating that innovative performance is an inclusive category. Past studies have underpinned several competing theoretical and empirical evidence on the impact of KM activities on performance [15,16]. However, there is lack of distinction on the type of performance measure. To provide insights from Arabian corporations with oriental cultures, this study consolidates three types of performance, namely innovative, financial, and market performance, in a single model, and observes how sustainable knowledge creation resulting from corporate data governance influences these performance measures.

Nevertheless, our understanding of corporate data governance is limited for several reasons. Firstly, Mao et al. [11] recommend further inquiry into the association between Information and communications technology (ICT) capabilities and KM because it is still vague. Secondly, Daily et al. [17] and Kamioka et al. [18] urged researchers to explain the mechanism by which data governance can be translated into a competitive advantage. In this study, we seek to answer this question from a corporate data governance perspective, and further, we bridged the connection using sustainable knowledge creation and performance variables. Lastly, the mixed results concerning the association between KM practices and performance arise from the fact “that some of the previously used corporate performance metrics have included different performance measures, financial ratios, customer satisfaction and employee satisfaction” [13] (p. 233). To provide clarity on these measures, this paper conceptualizes each performance measure independently.

2. Literature Review and Hypotheses

The theme “governance” has been an important research area for decades. Scholars have investigated the processes and approaches by which corporations organize, control, and direct resources to attain strategic goals [19]. Accordingly, governance in corporation, popularly known as corporate governance, gained an audience due antisocial behavior among corporations, collapse and bankruptcy, hostile takeovers, and the belief that corporate governance can improve firm’s performance and market share [20]. In their influential work, Rossi et al. [20] highlighted that corporate characteristics as a subcomponent of corporate governance can shape financial decisions and activities of firms. On the other hand, corporate governance ensures that counterproductive actions and activities of individuals are detected and subsequently prevented [21]. For instance, corporate governance ensures voluntary financial disclosure [22] and boosts competitive advantage, and competitive advantage is best harvested via data and/or knowledge management. In this sense, corporate governance functions as a control and support mechanism for knowledge. Henceforth, governance that focus on data may serve as a stepping stone toward competitive advantage for corporations.

Data governance refers to the “collection of capabilities or practices for the creation, capture, valuation, storage, usage, control, access, archival, and deletion of information over its life cycle” [5]. Corporate data governance is the capability of a corporation to mobilize relevant resources to maximize the value of information [1]. According to Weber et al. [23], corporate data governance is a triad phenomenon that subsumes activities spanning from structural practices (i.e., decision-making and the appropriation of roles to governance of data), procedural or operational practices (decision-making of data usage), and relational practices (i.e., inter-relational development and responsibilities). Structural practices are designed to pivot specific corporate data and non-data decision makers alongside given responsibilities and roles in terms of data control, ownership, analysis, value, and expenditure management, e.g., explicit declarations of data usage and protection policies, and the establishment of committees to audit compliance to internal data policies [1].

The second subcomponent of corporate data governance, procedural or operational practices, determines the processes and approaches by which corporations execute data [23]. These practices include corporate data access rights, usage and retention policies, analytic policies, and cost allocation. Operational practices may vary according to the type of data analyzed and the type of knowledge explored [1]. The third subcomponent of corporate data governance, relational practices, deals with formalized links between entities in different business units, e.g., alignments of strategic plans, sharing knowledge and insights, and educating and training each other [1,24]. Corporate data governance has been shown to be a critical component of business value [25]. According to Wu, Straub, and Liang [26], corporate information governance can indirectly enhance firm performance through strategic alignment. Kathuria et al. [27] showed that data governance is an effective mechanism for developing and managing information-related artifacts, e.g., in the healthcare industry. It has also been shown to provide comprehensive information that can be analyzed to provide detailed knowledge about patient health [28].

Theories such as the resource-based view (RBV) and knowledge-based view (RBV) see resources as an important and valuable engine for corporations. In this sense, corporate data governance is a valuable resource because it allows corporations to control, save, and use knowledge and data internally. Knowledge management (KM) is the ability of an organization to mobilize and deploy knowledge-based resources to gain a competitive advantage [15]. KM entails practices that unleash a firm’s intellectual potential through its management of knowledge resources. In the context of KM, knowledge creation is considered as a continuous process resulting from the interactions between individuals and their environment [29], which leads to the generation of new knowledge in the corporation to be used by individuals and the corporation.

The literature conceptualized knowledge creation as a bidimensional concept with ontological and epistemological dimensions [30]. The ontological abstraction states that sustainable knowledge creation is a spiral process spanning from the individual level, and moving up across sectional, departmental, divisional, and organizational boundaries [30], while the epistemological abstraction states that four types of knowledge conversion occur when tacit and explicit knowledge interact. More subtly, sustainable knowledge creation evolves through socialization, externalization, combination, and internalization, also known as the “SECI” process [7].

Sustainable knowledge creation begins with socialization—a systematic means by which new tacit knowledge is shared through direct daily social interaction. Formalizing knowledge is challenging, therefore spending time together, sharing a work-space, and a sort of apprenticeship ensures that individuals have hands-on experiences [10]. Next is the externalization phase, where individuals start articulating tacit knowledge through dialogue and reflection. More specifically, entities use their “discursive consciousness and try to rationalize and articulate the world that surrounds them” [10] (p. 96). Combination is the third phase, where explicit knowledge is obtained from inside or outside the organization. The knowledge is then processed, e.g., edited, combined, and organized, in a systematic manner that can be shared between entities in the corporation. Internalization process is the last phase, where the created and shared knowledge is practically applied and used as a base for new routines within the corporation [10].

This simply means that sustainable knowledge creation is a social process between entities that is not confined within the entities. Practically, sustainable knowledge creation is generally associated with environment, people, and processes, e.g., human skills, organizational culture, infrastructure, strategy, interactions, and trust between individuals and groups [29]. Past studies have shown knowledge creation is influenced by varying factors, e.g., information cultures [31], distributed leadership [32], organizational and environmental factors [29], and social networks and support [33]. In line with this study proposition, data analytics capability was found to be associated with knowledge generation for firms [34]. Strangely, limited attention has been paid to how corporate data governance can foster and facilitate sustainable knowledge creation culture in corporations. Mikalef et al. [35] claimed that firms can leverage data analytics capability to generate strategic value in form of knowledge that can further be processed into performance. This can take several forms, e. g., marketing, technological, and operational capabilities [36]. Pappas et al. [37] proposes big data and business analytics as important sources of empirical evidence for sustainable knowledgeable societies. This study theorizes that corporate data governance can also be a source for sustainable knowledge creation in corporations.

H1.

Corporate data governance has a positive impact on sustainable knowledge creation.

According to Donaldson and Preston’s [38] conceptualization of stakeholder theory, corporations’ benefits and leverage on collective ideas, skills, and resources come from various entities, e.g., stakeholders. In this article, stakeholder theory was adopted to expound how sustainable knowledge creation enhances perceived information transparency. According to McManus et al. [39], corporate information transparency denotes “openness and access to information, the free flow of information, and the right to own some information”. In other words, corporate information transparency delineates an employee’s ability to access the required information and data for business decisions [40]. In the context of this study, corporate information transparency reflects financial data transparency such as financial disclosures, governance transparency, and disclosures of activities within and outside the corporation [41]. Bushman et al. [41] further categorized corporate information transparency into two categories, namely internal transparency, which mirrors employees’ access to internal information across units within the corporation for business decisions (e.g., knowledge sharing between a superior and a subordinate in the same unit, and between units’ heads or employees in different units), and external transparency, which mirrors employees’ access to information belonging to external stakeholders (e.g., partners, suppliers etc.) for business decisions. The Internet has eased the process by which information can be accessed, used, and distributed across individuals, teams, and organizations. Past researches have illustrated the vital role knowledge management processes. For instance, Alavi and Leidner [42] and Al-Jabri and Roztocki [43] asserted that IT systems facilitates transparency through information sharing at an individual, team, and corporate level. This has also received empirical evidence from the public sector [44,45]. Moreover, the purpose of sustainable knowledge creation is to allow the users/employees to make and reach informed decisions [15,46]. There seems to be a dearth of research linking sustainable knowledge creation and corporate information transparency. This paper theorizes that sustainable knowledge creation, e.g., access, usage, and distribution of data among corporate entities, may result in higher levels of corporate information transparency, which in turn may lead to better decisions and subsequent competitive advantage. Thus, this paper theorizes the following:

H2.

Sustainable knowledge creation has a positive impact on corporate information transparency.

There is a growing recognition that the nature of the relationship between KM processes and corporate performance is changing [11,14]). Traditionally, corporate performance has been viewed as one component, however, practitioners and contemporary scholars have begun to recognize the need to categorize corporate performance based on segmental criteria, e.g., market, financial and innovative. For instance, dominant research findings showed that intellectual property (explicit knowledge) can foster firm performance through the creation of new patentable technologies [9]. A research on Spanish and Colombian firms found that KM practices can boost innovation performance [47,48]. Knowledge creation appears to exert an indirect effect on organizational performance through organizational learning [49]. Other researches showed that KM management and processes boosted high-tech Chinese enterprises’ operational performance [50], operational performance of manufacturing firms in Malaysia [51], innovative performance [52], and market and financial performance of hospitality and service firms in South Africa [13] and Spain [47]. Recent studies found that KM practices have profound influences on innovative, quality, and operational performance [16]. KM is a corner stone for quality improvement through incremental innovative and market performance. Despite the voluminous research on the KM processes and performance, notably absent from this literature is an in-depth exploration of the mechanism by which sustainable knowledge creation affects the three main corporate performances (i.e., innovative, financial, and market). Additionally, prior work utilizes varying levels of metrics to measure corporate performance, in response to research call echoed by Inkinen [14] concerning inconsistency among the metrics. This paper conceptualized three important performances as corporate outcomes of sustainable knowledge creation. This abstraction will provide valuable insight for managers and answers to prior research calls. Thus, this paper theorizes the following:

H3.

Sustainable knowledge creation has a positive impact on (a) innovative performance, (b) financial performance, and (c) market performance.

3. Methods and Materials

3.1. Sample and Procedures

The survey items were originally in English. The researchers consulted two professional translators to back-translate the text from English to Arabic and vice versa. Consequently, a pretest was carried out to ensure and evade ambiguity, biases, and at the end no further changes were made. Next, the managements of the listed firms were contacted to participate in the survey. According to the information obtained from the Amman Stock Market (2019), there are 192 listed firms, and 189 firms agreed to participate in the study. Prior work showed that chief executive officers (CEOs) influence corporate policies by setting the tone at the top [53]. Thus, the researcher visited each firm and asked the chief financial officers (CFO) to respond to the survey. The CFOs were briefed about the purpose of the research and were subsequently assured that the information they provide will be used for research purposes only and will not be disclosed to third parties. Prior work showed that this strategy can mitigate social desirability and common method bias [54,55]. Five (5) CFOs withdrew their consent for participation due to meetings and other commitments, and four (4) stopped responding to the survey citing the level of information sensitivity. Thus, only 180 valid surveys were obtained.

3.2. Instruments

Corporate data governance is the capacity of corporations to acquire, store, and manipulate big data richness and combine it with real-time data to forecast future events such as demand, fluctuations, and price adjustments etc. As a triad dimensional construct with structural (SP1 to SP2), procedural (PP1 to PP5), and relational (RP1 to RP2) governance practices as subdimensions, the construct was operationalized with a 9-item scale [1]. Sustainable knowledge creation was operationalized with a 19-item scale (KC1 to KC19) that measured how corporations create sustainable knowledge. The items were borrowed from [8] studies. Corporate information transparency was operationalized with a 7-item scale (CIT1 to CIT7) borrowed from [43,46] studies.

Innovative performance was operationalized with a 5-item scale (IP1 to IP5) borrowed from [56] studies. Financial performance was operationalized with a 4-item scale (FP1 to FP4) borrowed from [57] studies. Market performance was operationalized with a 5-item scale (MP1 to MP5) borrowed from [58] studies. All the instruments were anchored on a 7-point scale spanning from “1” (Strongly disagree) to “7” (Strongly agree), except for market performance, which was anchored on a 7-point scale ranging from “1” (To an Extremely Small Extent) to “7” (To an Extremely Large Extent).

Demographic information, such as firm age, firm size measure by the number of employees, and the operational industry, was measured. Approximately 43.3% of the firms had more than 250 employees, 40.6% had between 51 and 250 Employees, and the rest had less than 50 employees. An overwhelming number of the firms (66.7%) were in the service industry, 25% operated in the manufacturing industry, 4.4% in the hotel and hospitality industry, 2.8% in the oil, gas, and mining industry, and the rest in the IT and telecommunication industry. Regarding firm age, 47.8% had been in operation for more than 10 years, 47.2% between 6 and 10 years, and the rest between 1 and 5 years.

3.3. Data Analysis and Results

For prior scholars [59,60], a covariance-based structural equation modeling (CB-SEM) was a better option for theory testing due to its capability to assess the goodness of fit of the data with the model based on parametric estimations. Secondly, partial least squares structural equation modeling (PLS-SEM) was a better option for examining theory foundation and predictions of outcome variables. Artificial intelligence techniques such as neural networks, Bayesian networks, etc., were better options for predictive models. The present study, for our aims to explore a relational presence among the variables under investigation, opted to use PLS-SEM.

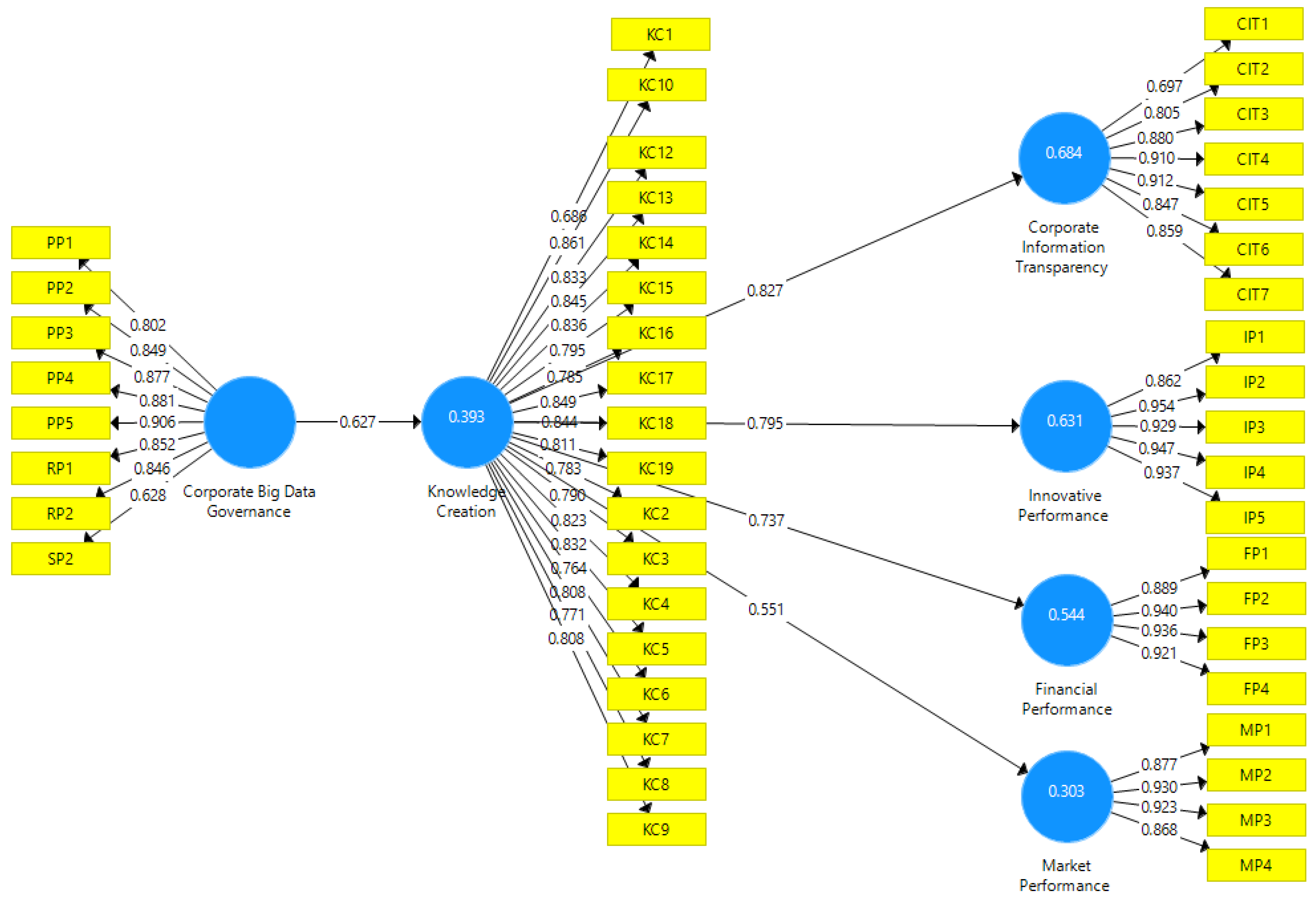

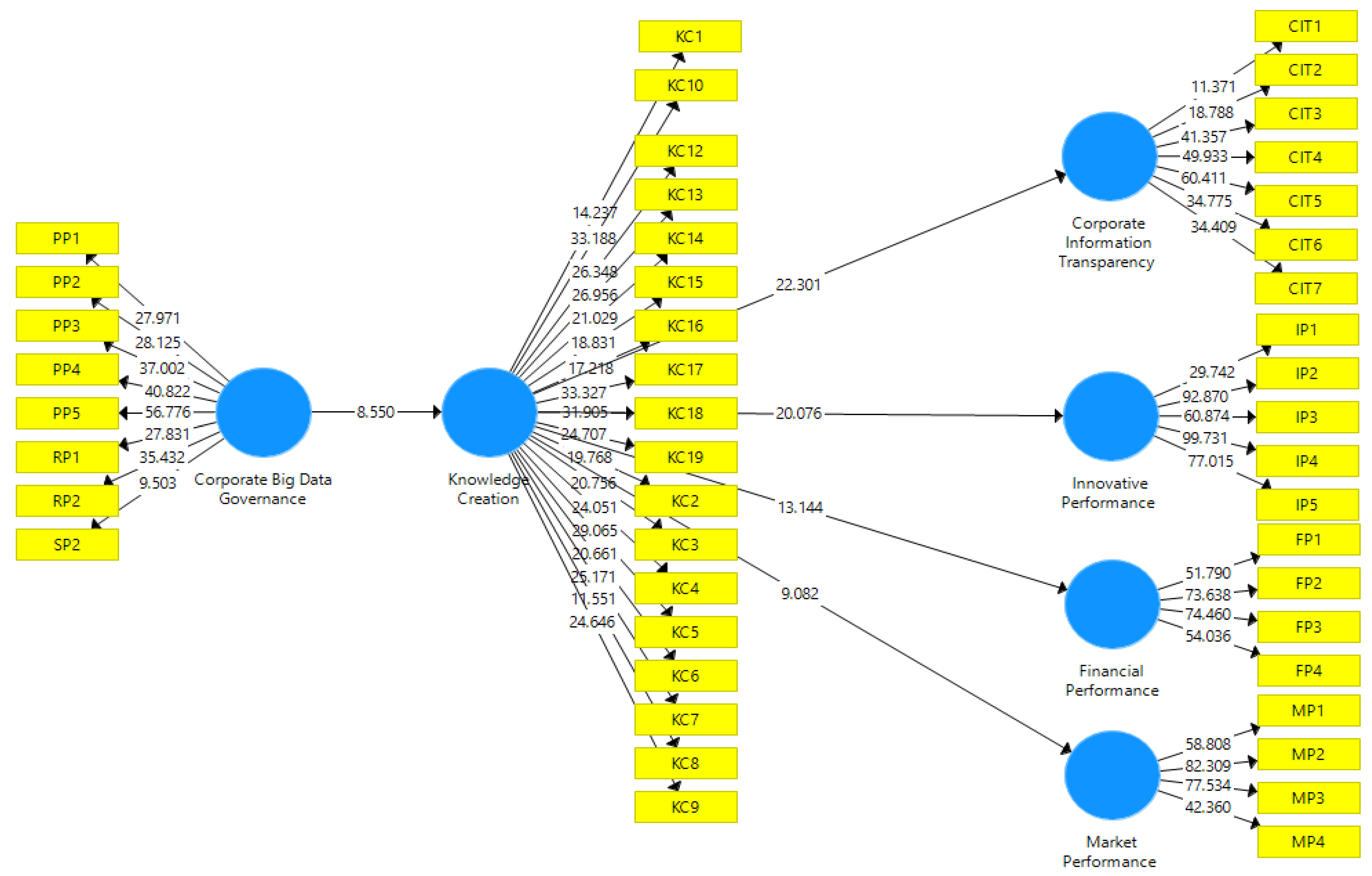

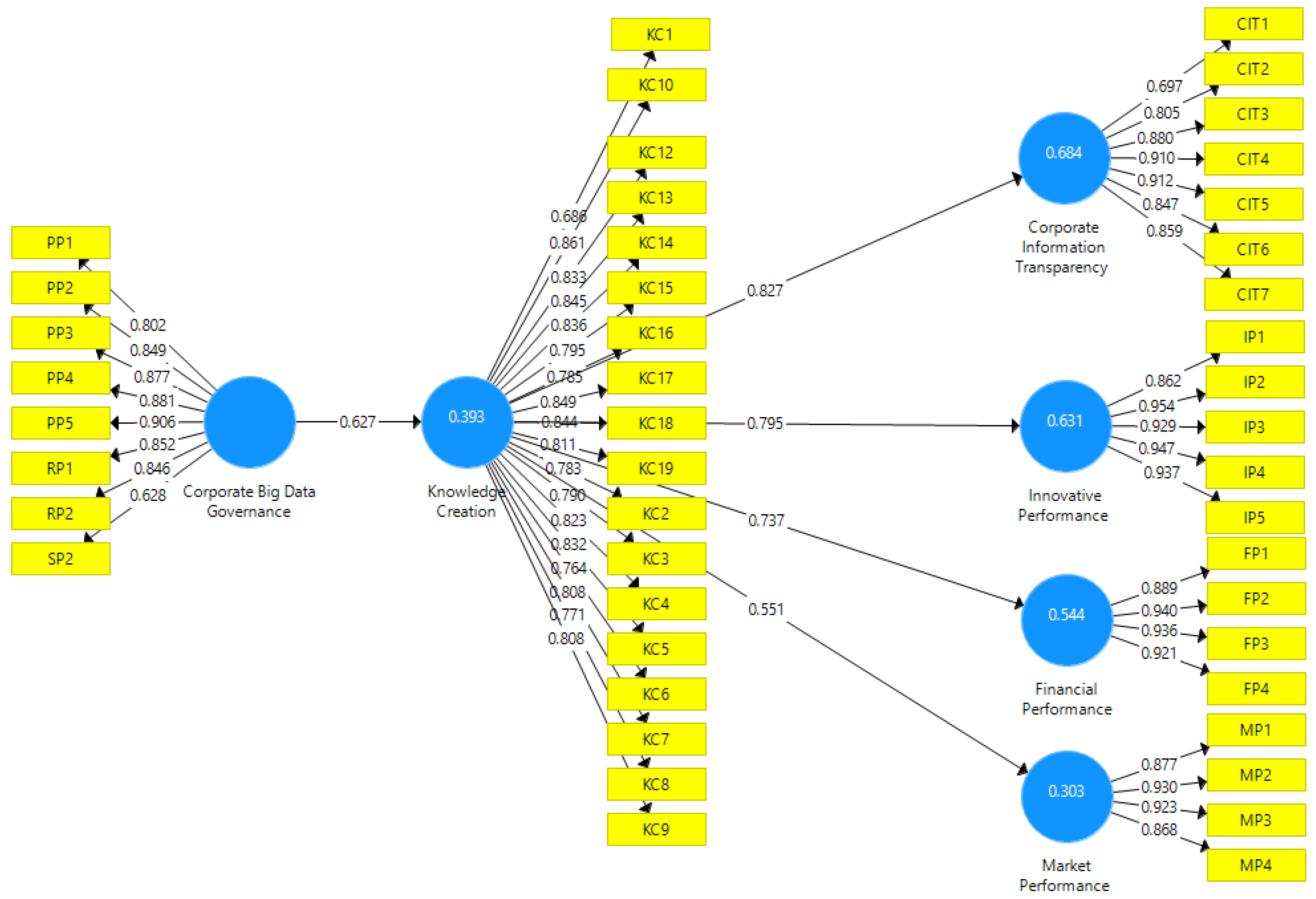

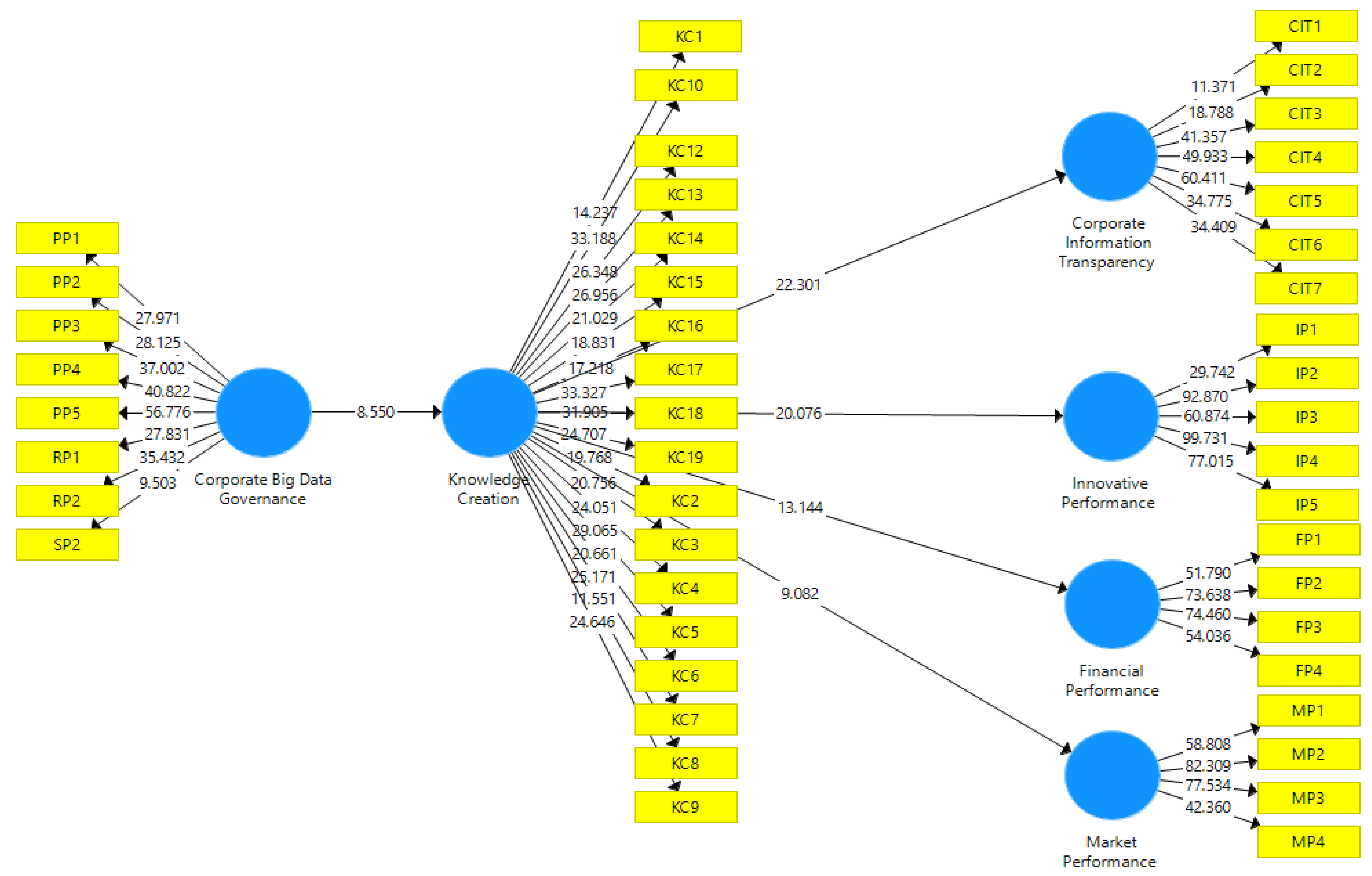

Prior to testing the relational associations between the variables, the researchers examined the measurement models’ construct reliability and convergent and divergent validity using SmartPLS Version 3 software. To ensure the presence of construct reliability and convergent validity, the coefficients of retained items’ outer loadings, the t-statistics, Cronbach’s alpha (α), composite reliability (CR), and average variance extracted (AVE) were measured. Scale items with low factor loadings were discarded, and the retained items’ outer loadings exceeded the threshold >0.50 (see Figure 1) and were statistically significant (see Figure 2). The constructs (α) and (CR) exceeded the threshold of 0.7, and AVE exceeded the threshold value of 0.5 [61]. To ensure the presence of discriminant validity, The Fornell–Larcker criterion was scrutinized. The AVE scores were higher than the squared interconstruct correlations [62]. In summation, these outcomes provided evidence of construct reliability and convergent and divergent validity (see Table 1).

Corporate data governance exerts a positive impact on sustainable knowledge creation (β = 0.63, ρ < 0.000) and explains 39% of the variance in sustainable knowledge creation. Data analysis suggests that sustainable knowledge creation exerts a positive impact on corporate information transparency (β = 0.83, ρ < 0.000) and sustainable knowledge creation explains 68% of corporate information transparency. Thus, hypothesis 1 and 2 received empirical support. Subsequently, sustainable knowledge creation exerted a positive impact on innovative performance, financial performance, and market performance, respectively (β = 0.80, ρ < 0.000), (β = 0.74, ρ < 0.000), and (β = 0.55, ρ < 0.000). Sustainable knowledge creation also explains 63%, 54%, and 30% of the variance in innovative performance, financial performance, and market performance, respectively. It appears that sustainable knowledge creation influences innovative performance more, financial performance comes second, and subsequently market performance. Simply a 1 unit increase in sustainable knowledge creation will result in a 0.80 unit increase in innovative performance, a 0.74 unit increase in financial performance, and a 0.55 unit increase in market performance. Thus, hypothesis 3a, b, and c received empirical support. See Figure 1 and Figure 2.

Although the mediating role of sustainable knowledge creation was not hypothesized, the present study tested for mediation effects using bootstrapping analysis with a bias corrected confidence interval with n = 5000 resamples. Bootstrapping uses computer intensive resampling to make inferences rather than making assumptions about the population. More subtly, bootstrapping treats a given sample as the population [63]. Results from bootstrapping analyses delineate that sustainable knowledge creation mediates the link between corporate data governance and corporate information transparency (β = 0.52, ρ < 0.000), with these intervals (Bias = 0.002; 2.5% = 0.37; 97.5% = 0.64). Sustainable knowledge creation mediates the link between corporate data governance and innovative performance (β = 0.49, ρ < 0.000), with these intervals (Bias = −0.001; 2.5% = 0.35; 97.5% = 0.63). Sustainable knowledge creation mediates the link between corporate data governance and financial performance (β = 0.46, ρ < 0.000), with these intervals (Bias = −0.001; 2.5% = 0.31; 97.5% = 0.59). Sustainable knowledge creation mediates the link between corporate data governance and market performance (β = 0.35, ρ < 0.000), with these intervals (Bias = 0.001; 2.5% = 0.22; 97.5% = 0.47). These results show that sustainable knowledge creation takes the role of a full mediator in the hypothesized relationship.

4. Discussion

The purpose of this research is to bring clarity and precision to the theoretical rationales and mechanisms involved in the associations between corporate data governance, sustainable knowledge creation, corporate information transparency, and innovative, financial, and market performance. More specifically, this study sought to provide evidence on how corporate data governance improves sustainable knowledge creation. The pruning and refining effort in this study hypothesized and unveiled the theoretical mechanisms in which sustainable knowledge creation further enhances corporate outcomes, such as corporate information transparency, innovative performance, financial performance, and market performance. In summation, this paper unveiled six important outcomes as follows:

- Corporate data governance emerged as a strong predictor of sustainable knowledge creation. By abstracting corporate data governance from a financial perspective and showing how it improves sustainable knowledge creation, this article answers the call for greater scholarly attention to antecedents for knowledge creation and its consequences [8,15]. Past work only showed the beneficial effects of data governance, IT management, and sustainable knowledge creation for firms without empirical evidence [3,10,11,17,23]. Even the studies that provided empirical evidence acknowledged incoherency by recommending future investigation [18]. Capitalizing on this line of reasoning, this study observed an incremental change in sustainable knowledge creation when corporate data governance was leveraged. Simply, corporate data governance can contribute to knowledge creation and enhance decision-making as it provides a framework for decision rights and accountabilities as part of corporate-wide strategy.

- Our expectation about the role of sustainable knowledge creation emerging as a predictor for corporate information transparency was supported. The outcome demonstrates that sustainable knowledge creation has the tendency to increase perceived corporate information transparency. This is consistent with the general KM literature’s conclusion that an individual’s involvement and participation in decision processes allows them to have an insight on what is going on within the corporation [42,43]. For example, the free flow of information and access to information ensures that individuals can access, use, update, and share knowledge with colleagues, superiors, and external stakeholders within the boundary of corporate regulations.

- The results of this study help address two needs in KM and performance research streams, more specifically, sustainable knowledge creation and three types of corporate performance. One, the mechanisms that link sustainable knowledge creation to firm performance have remained largely in a black box [15]. Two, KM researches mostly combined and considered performance as a single entity [48] and paid little attention to which corporate performance dimension benefited more from sustainable knowledge creation. Third, sustainable knowledge creation emerged as a strong predictor for corporate innovative performance. Our study also advances the corporate innovative performance literature, as prior studies focused on how shared knowledge can boost innovative performance [51]. In addition, prior work showed that explicit knowledge (organized) has more impact on innovation and financial performance, while tacit knowledge has more impact on operational performance. Our findings are in line with past empirical outcomes, sustainable knowledge creation impacted innovative performance the most. Our study extends these concepts to the domain of created knowledge through corporate data governance.

- Sustainable knowledge creation emerged as strong predictor for corporate financial performance. Prior work also found that KM initiatives have a positive influence on financial performance [47]. This study narrowed down the argument by specifically highlighting the incremental impact of sustainable knowledge creation on corporate financial performance. Contrariwise to our finding, Zack et al.’s [12] study among North American and Australian firms found that KM practices do not exert any effect on financial performance. Our results show that corporate financial performance was second in terms of effect size, however, prior work argued that KM practices in Spanish firms exerted more effect on financial performance compared to innovative and market performance [47]. The present outcome shows variation, and a plausible explanation for this might be in the geographic, economic, cultural, and country’s context. Similar arguments were echoed by [12]. Nonetheless, managers could rely on these findings to negotiate with and convince stakeholders concerning the importance of corporate data governance and sustainable knowledge creation in determining greater financial performance.

- Sustainable knowledge creation emerged as strong predictor for corporate market performance. Past research found that KM practices can enhance financial and market performance [13]. However, this paper argues that conceptualizing financial and market performance as one construct is misleading. Other field work revealed that the association between knowledge creation and performance was mediated by organizational learning [49]. In this study, we theorize that knowledge creation is itself a kind of learning. Using a Chinese sample Chen [50] revealed that KM practices amplified operational performance. In short, our result helps to clarify the role of knowledge creation in amplifying market performance, an area that has receive scant attention, mixed results, and inconsistent conceptualization.

- Sustainable knowledge creation assumes the role of a mediator in the association between the exogenous variable and endogenous variables. Our mediation results offer novel insights into the mechanistic processes in which corporate data governance drives sustainable knowledge creation, and subsequently results in corporate information transparency and innovative, financial, and market performance. Prior studies have examined the varying mechanisms underlying knowledge generation and its subsequent outcomes. For example, organizational and environmental factors [29], information cultures [31], and distributed leadership [32]. However, no study explores the interplay of corporate data governance with sustainable knowledge creation and their effects on corporate information transparency and innovative, financial, and market performance. In short, previous researches failed to acknowledge the chained relationships between the variables under investigation. Thus, our post hoc mediation analyses add insights into the potential effects of corporate data governance in a broader sense.

5. Practical and Theoretical Implications

This study extends the sustainable knowledge creation and corporate data governance literature in the setting of an emerging economy to highlight their importance. In particular, the study diagnoses whether corporate data governance implications are reflected in sustainable knowledge creation, and whether sustainable knowledge creation implications are reflected in corporate performance. Several insights emerged in line with these findings, and some theoretical and practical implications are set forth. First, the current paper advances the literature on the consequences of corporate data governance by explicating how it results in sustainable knowledge creation which further strengthens corporate performance (i.e., innovative, financial, and market) as well as information transparency. In other words, this paper provides insights into how corporate data governance, an important knowledge creation input, advances and accelerates favorable corporate outcomes. Second, this paper advances the literature on the determinants, mechanisms, and consequences of sustainable knowledge creation by specifying how corporations can stimulate knowledge creation which has long-term benefits through increased innovative, financial, and market performance, as well as transparency indices. In other word, this paper answers research calls to provide more conceptual and empirical specificity for corporate data governance and knowledge management echoed by [1,18,37]. Third, the present findings provide practical implications for corporate knowledge managers by highlighting the importance of corporate data management as an essential asset for sustainable knowledge creation. Thus, corporate leaders can increase knowledge creation by creating and fostering data governance policies. Fourth, corporations can foster an organizational climate in which individuals and team knowledge are assessed and governed by rules, where knowledge creation processes and activities are valued and rewarded. Doing this will not only enhance corporate performance but also its transparency policies. Fifth, our findings also suggest that corporations need to equip themselves with effective corporate data governance practices, and enhance knowledge generation, accounting, and reporting standards which is likely to improve performance in emerging economies, such as Jordan. Sixth, by using a structural equation modeling methodology to test the association between the variables under investigation, this paper provides clarity on how to measure and interpret first-hand accounts of the subject of interest. In doing so, future researchers can compare and contrast between first-hand accounts and secondary accounts (i.e., published corporate data) using proxy variables. In addition, researchers are encouraged to consider advanced methodological approaches such as artificial neural networks, Bayesian networks, and fuzzy sets due to their predictive validity [64,65].

6. Limitations and Future Research Direction

The findings should be interpreted within the context of a methodological challenge regarding the measures and data collection, e.g., a cross-sectional design, self-reported and single sourced data have the tendency to inhibit causal inference and increases the tendency of social desirability bias, and common method variance. Despite these shortcomings, this study utilized the procedural approach, e.g., assurance of confidentiality and the use of proximity approach (i.e., placing predictor and criterion variables in separate pages). To draw such concrete causal conclusions, longitudinal and experimental studies are needed. A positive outlook for the findings considering common method variance is that we assured respondents’ confidentiality, moreover, we utilized a proximity approach in which exogenous variables were placed in separate pages [55]. The outcome cannot be generalized to other cultural and/or natural settings with more infrastructures, affluent resources, and established legislations.

Author Contributions

R.A.I.A. and M.A. conceived and designed the experiments. R.A.I.A. contributed in writing and also analyzed the data. M.A. supervised the project.

Funding

This research received no funding support.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Mikalef, P.; Krogstie, J. Big Data Governance and Dynamic Capabilities: The Moderating Effect of Environmental Uncertainty. In Proceedings of the Twenty-Second Pacific Asia Conference on Information Systems, Yokohama, Japan, 26–30 June 2018. [Google Scholar]

- Raymond, L.; Bergeron, F.; Croteau, A.M.; Uwizeyemungu, S. Determinants and Outcomes of IT Governance in Manufacturing SMEs: A strategic IT management perspective. Int. J. Account. Inf. Syst. 2019, in press. [Google Scholar] [CrossRef]

- Otto, B. Organizing data governance: Findings from the telecommunications industry and consequences for large service providers. Commun. Assoc. Inf. Syst. 2011, 29, 45–66. [Google Scholar] [CrossRef]

- Alhassan, I.; Sammon, D.; Daly, M. Data Governance Activities: An Analysis of the Literature. J. Decis. Syst. 2016, 25, 64–75. [Google Scholar] [CrossRef]

- Tallon, P.P.; Ramirez, R.V.; Short, J.E. The Information Artifact in IT Governance: Toward a Theory of Information Governance. J. Manag. Inf. Syst. 2013, 30, 141–178. [Google Scholar] [CrossRef]

- Loebbecke, C.; Picot, A. Reflections on Societal and Business Model Transformation Arising From Digitization and Big Data Analytics: A Research Agenda. J. Strateg. Inf. Syst. 2015, 24, 149–157. [Google Scholar] [CrossRef]

- Nonaka, I. A Dynamic Theory of Organizational Knowledge Creation. Org. Sci. 1994, 5, 14–37. [Google Scholar] [CrossRef]

- Lee, H.; Choi, B. Knowledge Management Enablers, Processes and Organizational Performance: An Integrative View and Empirical Examination. J. Manag. Inf. Syst. 2003, 20, 20–179. [Google Scholar]

- Nonaka, I.; Von Krogh, G. Perspective—Tacit Knowledge and Knowledge Conversion: Controversy and Advancement in Organizational Knowledge Creation Theory. Org. Sci. 2009, 20, 635–652. [Google Scholar] [CrossRef]

- Nonaka, I.; Toyama, R. The Knowledge-Creating Theory Revisited: Knowledge Creation as a Synthesizing Process. In The Essentials of Knowledge Management; Edwards, J.S., Ed.; Palgrave Macmillan: London, UK, 2015. [Google Scholar]

- Mao, H.; Liu, S.; Zhang, J.; Deng, Z. Information Technology Resource, Knowledge Management Capability and Competitive Advantage: The Moderating Role of Resource Commitment. Int. J. Inf. Manag. 2016, 36, 1062–1074. [Google Scholar] [CrossRef]

- Zack, M.; McKeen, J.; Singh, S. Knowledge Management and Organizational Performance: An Exploratory Analysis. J. Knowl. Manag. 2009, 13, 392–409. [Google Scholar] [CrossRef]

- Cohen, J.F.; Olsen, K. Knowledge Management Capabilities and Firm Performance: A Test of Universalistic, Contingency and Complementarity Perspectives. Expert. Syst. Appl. 2015, 42, 1178–1188. [Google Scholar] [CrossRef]

- Inkinen, H. Review of Empirical Research on Knowledge Management Practices and Firm Performance. J. Knowl. Manag. 2016, 20, 230–257. [Google Scholar] [CrossRef]

- Abubakar, A.M.; Elrehail, H.; Alatailat, M.A.; Elçi, A. Knowledge Management, Decision-Making Style and Organizational Performance. J. Innov. Knowl. 2017, 4, 104–114. [Google Scholar] [CrossRef]

- Al Ahbabi, S.A.; Singh, S.K.; Balasubramanian, S.; Gaur, S.S. Employee Perception of Impact of Knowledge Management Processes on Public Sector Performance. J. Knowl. Manag. 2019, 23, 351–373. [Google Scholar] [CrossRef]

- Daily, C.M.; Dalton, D.R.; Cannella, A.A., Jr. Corporate Governance: Decades of Dialogue and Data. Acad. Manag. Rev. 2003, 28, 371–382. [Google Scholar] [CrossRef]

- Kamioka, T.; Luo, X.; Tapanainen, T. An Empirical Investigation of Data Governance: The Role of Accountabilities. In Proceedings of the Pacific Asia Conference on Information Systems, Chiayi, Taiwan, 27 June–1 July 2016. [Google Scholar]

- Leiblein, M.J.; Reuer, J.J.; Dalsace, F. Do Make or Buy Decisions Matter? The Influence of Organizational Governance on Technological Performance. Strategic. Manag. J. 2002, 23, 817–833. [Google Scholar] [CrossRef]

- Rossi, M.; Lombardi, R.; Siggia, D.; Oliva, N. The Impact of Corporate Characteristics on the Financial Decisions of Companies: Evidence on Funding Decisions by Italian SMEs. J. Innov. Entrep. 2015, 5. [Google Scholar] [CrossRef]

- Widyaningsih, I.U.; Gunardi, A.; Rossi, M.; Rahmawati, R. Expropriation by the Controlling Shareholders on Firm Value in the Context of Indonesia: Corporate Governance as Moderating Variable. Int. J. Manag. Finan. Acct. 2017, 9, 322–337. [Google Scholar] [CrossRef]

- Rouf, M.A. Firm-Specific Characteristics, Corporate Governance and Voluntary Disclosure in Annual Reports of Listed Companies in Bangladesh. Int. J. Manag. Finan. Acct. 2017, 9, 263–282. [Google Scholar]

- Weber, K.; Otto, B.; Österle, H. One Size does not fit all: A Contingency Approach to Data Governance. ACM J. Data Inf. Qual. 2009, 1, 4. [Google Scholar] [CrossRef]

- Kooper, M.N.; Maes, R.; Lindgreen, E.R. On the Governance of Information: Introducing a New Concept of Governance to Support the Management of Information. Int. J. Inf. Manag. 2011, 31, 195–200. [Google Scholar] [CrossRef]

- De Haes, S.; Van Grembergen, W.; Debreceny, R.S. COBIT 5 and Enterprise Governance of Information Technology: Building Blocks and Research Opportunities. J. Inf. Syst. 2013, 27, 307–324. [Google Scholar] [CrossRef]

- Wu, S.P.J.; Straub, D.W.; Liang, T.P. How Information Technology Governance Mechanisms and Strategic Alignment Influence Organizational Performance: Insights from a Matched Survey of Business and IT Managers. Mis Q. 2015, 39, 497–518. [Google Scholar] [CrossRef]

- Kathuria, A.; Saldanha, T.J.V.; Khuntia, J.; Andrade Rojas, M.G. How Information Management Capability Affects Innovation Capability and Firm Performance Under Turbulence: Evidence from India. In Proceedings of the International Conference on Information Systems, Dublin, Ireland, 11–14 December 2016. [Google Scholar]

- Murdoch, T.B.; Detsky, A.S. The Inevitable Application of Big Data to Health Care. JAMA 2013, 309, 1351–1352. [Google Scholar] [CrossRef] [PubMed]

- Little, T.A.; Deokar, A.V. Understanding Knowledge Creation in the Context of Knowledge-Intensive Business Processes. J. Knowl. Manag. 2016, 20, 858–879. [Google Scholar] [CrossRef]

- Nonaka, I.; Takeuchi, H. The Knowledge-Creating Company: How Japanese Companies Create the Dynamics of Innovation; Oxford University Press: New York, NY, USA, 1995. [Google Scholar]

- Vick, T.E.; Nagano, M.S.; Popadiuk, S. Information Culture and its Influences in Knowledge Creation: Evidence from University Teams Engaged in Collaborative Innovation Projects. Int. J. Inf. Manag. 2015, 35, 292–298. [Google Scholar] [CrossRef]

- Cannatelli, B.; Smith, B.; Giudici, A.; Jones, J.; Conger, M. An Expanded Model of Distributed Leadership in Organizational Knowledge Creation. Long Range Plann. 2017, 50, 582–602. [Google Scholar] [CrossRef]

- Smith, K.; Collins, C.; Clark, K. Existing Knowledge, Knowledge Creation Capability and the Rate of New Product Introduction in High-Technology Firms. Acad. Manag. J. 2005, 48, 346–357. [Google Scholar] [CrossRef]

- Gupta, M.; George, J.F. Toward the Development of a Big Data Analytics Capability. Inf. Manag. 2016, 53, 1049–1064. [Google Scholar] [CrossRef]

- Mikalef, P.; Boura, M.; Lekakos, G.; Krogstie, J. Big Data Analytics and Firm Performance: Findings from a Mixed-Method Approach. J. Bus. Res. 2019, 98, 261–276. [Google Scholar] [CrossRef]

- Mikalef, P.; Krogstie, J.; Pappas, I.O.; Pavlou, P. Exploring the Relationship Between Big Data Analytics Capability and Competitive Performance: The Mediating Roles of Dynamic and Operational Capabilities. Inf. Manag. 2019, in press. [Google Scholar] [CrossRef]

- Pappas, I.O.; Mikalef, P.; Giannakos, M.N.; Krogstie, J.; Lekakos, G. Big Data and Business Analytics Ecosystems: Paving the Way Towards Digital Transformation and Sustainable Societies. Inf. Syst. e-Business Manag. 2018, 16, 479–491. [Google Scholar] [CrossRef]

- Donaldson, T.; Preston, L.E. The Stakeholder Theory of the Corporation: Concepts, Evidence and Implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- McManus, T.; Holtzman, Y.; Lazarus, H.; Anderberg, J.; Lazarus, H. Transparency Guru: An Interview with Tom McManus. J. Manag. Devel. 2006, 25, 923–936. [Google Scholar] [CrossRef]

- Simon, C. Corporate Information Transparency: The Synthesis of Internal and External Information Streams. J. Manag. Devel. 2006, 25, 1029–1031. [Google Scholar] [CrossRef]

- Bushman, R.M.; Piotroski, J.D.; Smith, A.J. What Determines Corporate Transparency? J. Account. Res. 2004, 42, 207–252. [Google Scholar] [CrossRef]

- Alavi, M.; Leidner, D.E. Knowledge Management and Knowledge Management Systems: Conceptual Foundations and Research Issues. Mis Q. 2001, 25, 107–136. [Google Scholar] [CrossRef]

- Al-Jabri, I.M.; Roztocki, N. Adoption of ERP systems: Does Information Transparency Matter? Telemat. Inform. 2015, 32, 300–310. [Google Scholar] [CrossRef]

- Bonsón, E.; Royo, S.; Ratkai, M. Citizens’ Engagement on Local Governments’ Facebook sites. An Empirical Analysis: The Impact of Different Media and Content Types in Western Europe. Gov. Inf. Q. 2015, 32, 52–62. [Google Scholar]

- Venkatesh, V.; Thong, J.Y.; Chan, F.K.; Hu, P.J. Managing Citizens’ Uncertainty in e-Government Services: The Mediating and Moderating Roles of Transparency and Trust. Inf. Syst. Res. 2016, 27, 87–111. [Google Scholar] [CrossRef]

- Bertot, J.C.; Jaeger, P.T.; Grimes, J.M. Using ICTs to Create a Culture of Transparency: E-government and Social Media as Openness and Anti-Corruption Tools for Societies. Gov. Inf. Q. 2010, 27, 264–271. [Google Scholar] [CrossRef]

- López-Nicolás, C.; Meroño-Cerdán, Á.L. Strategic Knowledge Management, Innovation and Performance. Int. J. Inf. Manag. 2011, 31, 502–509. [Google Scholar]

- Saenz, J.; Aramburu, N.; Blanco, C.E. Knowledge Sharing and Innovation in Spanish and Colombian High-Tech Firms. J. Knowl. Manag. 2012, 16, 919–933. [Google Scholar] [CrossRef]

- Ramírez, A.M.; Morales, V.J.G.; Rojas, R.M. Knowledge Creation, Organizational Learning and Their Effects on Organizational Performance. Engin. Econ. 2011, 22, 309–318. [Google Scholar] [CrossRef]

- Chen, J.L. Effects of Knowledge Management on the Operational Performance of the B & B Industry. Int. J. Markt. Stud. 2016, 8, 67–76. [Google Scholar]

- Tan, L.P.; Wong, K.Y. Linkage Between Knowledge Management and Manufacturing Performance: A Structural Equation Modeling Approach. J. Knowl. Manag. 2015, 19, 814–835. [Google Scholar] [CrossRef]

- Iyer, D.N.; Sharp, B.M.; Brush, T.H. Knowledge Creation and Innovation Performance: An Exploration of Competing Perspectives on Organizational Systems. Univ. J. Manag. 2017, 5, 261–270. [Google Scholar] [CrossRef] [Green Version]

- Aliani, K.; Mhamid, I.; Rossi, M. Does CEO Overconfidence Influence Tax Planning? Evidence from Tunisian Context. Int. J Manag. Finan. Acct. 2016, 8, 197–208. [Google Scholar] [CrossRef]

- Jahmani, K.; Fadiya, S.O.; Abubakar, A.M.; Elrehail, H. Knowledge Content Quality, Perceived Usefulness, KMS Use for Sharing and Retrieval: A Flock Leadership Application. VINE J. Inf. Knowl. Manag. Syst. 2018, 48, 470–490. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Podsakoff, N.P. Sources of Method Bias in Social Science Research and Recommendations on How to Control it. Annu. Rev. Psychol. 2012, 63, 539–569. [Google Scholar] [CrossRef]

- Alpkan, L.; Bulut, C.; Gunday, G.; Ulusoy, G.; Kilic, K. Organizational Support for Intrapreneurship and its Interaction with Human Capital to Enhance Innovative Performance. Manag. Dec. 2010, 48, 732–755. [Google Scholar] [CrossRef]

- Drew, S.A. From Knowledge to Action: The Impact of Benchmarking on Organizational Performance. Long Range Plann. 1997, 30, 427–441. [Google Scholar] [CrossRef]

- Vorhies, D.W.; Morgan, N.A. Benchmarking Marketing Capabilities for Sustainable Competitive Advantage. J. Mark. 2005, 69, 80–94. [Google Scholar] [CrossRef]

- Abubakar, A.M. Linking Work-Family Interference, Workplace Incivility, Gender and Psychological Distress. J. Manag. Devel. 2018, 37, 226–242. [Google Scholar] [CrossRef]

- Henseler, J.; Ringle, C.M.; Sinkovics, R.R. The Use of Partial Least Squares Path Modelling in International Marketing. In New Challenges to International Marketing; Emerald Group Publishing: Bingley, UK, 2009. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Multivariate Data Analysis; Pearson: London, UK, 2014. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models With Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Behravesh, E.; Tanova, C.; Abubakar, A.M. Do High-Performance Work Systems Always Help to Retain Employees or is there a Dark Side? Serv. Ind. J. 2019, 1–21. [Google Scholar] [CrossRef]

- Abubakar, A.M.; Behravesh, E.; Rezapouraghdam, H.; Yildiz, S.B. Applying Artificial Intelligence Technique to Predict Knowledge Hiding Behavior. Int. J. Inf. Manag. 2019, 49, 45–57. [Google Scholar] [CrossRef]

- Fiss, P.C. Building Better Causal Theories: A Fuzzy Set Approach to Typologies in Organization Research. Acad. Manag. J. 2011, 54, 393–420. [Google Scholar] [CrossRef]

Figure 1.

Research model with factor loadings (outer indicators), beta values (inner indicators), and r squares (inside circles).

Figure 1.

Research model with factor loadings (outer indicators), beta values (inner indicators), and r squares (inside circles).

Figure 2.

Scale items’ t-statistics (outer indicators) and the significance of relationships (inner indicators).

Figure 2.

Scale items’ t-statistics (outer indicators) and the significance of relationships (inner indicators).

{kind=link}

{kind=link}

Table 1.

Reliability and convergent and divergent validity.

| Instruments | 1 | 2 | 3 | 4 | 5 | 6 | α | CR | AVE | R2 |

|---|---|---|---|---|---|---|---|---|---|---|

| Corporate data governance | 0.83 | 0.94 | 0.95 | 0.70 | ||||||

| Sustainable knowledge creation | 0.63 | 0.81 | 0.97 | 0.97 | 0.65 | 0.39 | ||||

| Corporate information transparency | 0.56 | 0.83 | 0.85 | 0.93 | 0.95 | 0.72 | 0.68 | |||

| Innovative performance | 0.46 | 0.80 | 0.72 | 0.93 | 0.96 | 0.97 | 0.86 | 0.63 | ||

| Financial performance | 0.41 | 0.74 | 0.71 | 0.82 | 0.92 | 0.94 | 0.96 | 0.85 | 0.54 | |

| Market performance | 0.54 | 0.55 | 0.48 | 0.49 | 0.55 | 0.90 | 0.92 | 0.94 | 0.81 | 0.30 |

Note: α, Cronbach’s alpha ≥0.70; CR, composite reliability ≥0.70; AVE, average variance extracted ≥0.50; Values below the diagonal in bold are squared interconstruct correlations for the Fornell–Larcker criterion.

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Abueed, R.A.I.; Aga, M. Sustainable Knowledge Creation and Corporate Outcomes: Does Corporate Data Governance Matter? Sustainability 2019, 11, 5575. https://doi.org/10.3390/su11205575

AMA Style

Abueed RAI, Aga M. Sustainable Knowledge Creation and Corporate Outcomes: Does Corporate Data Governance Matter? Sustainability. 2019; 11(20):5575. https://doi.org/10.3390/su11205575

Chicago/Turabian StyleAbueed, Raed A.I., and Mehmet Aga. 2019. "Sustainable Knowledge Creation and Corporate Outcomes: Does Corporate Data Governance Matter?" Sustainability 11, no. 20: 5575. https://doi.org/10.3390/su11205575

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.