Enterprise Risk Management: Improving Embedded Risk Management and Risk Governance

Abstract

1. Introduction

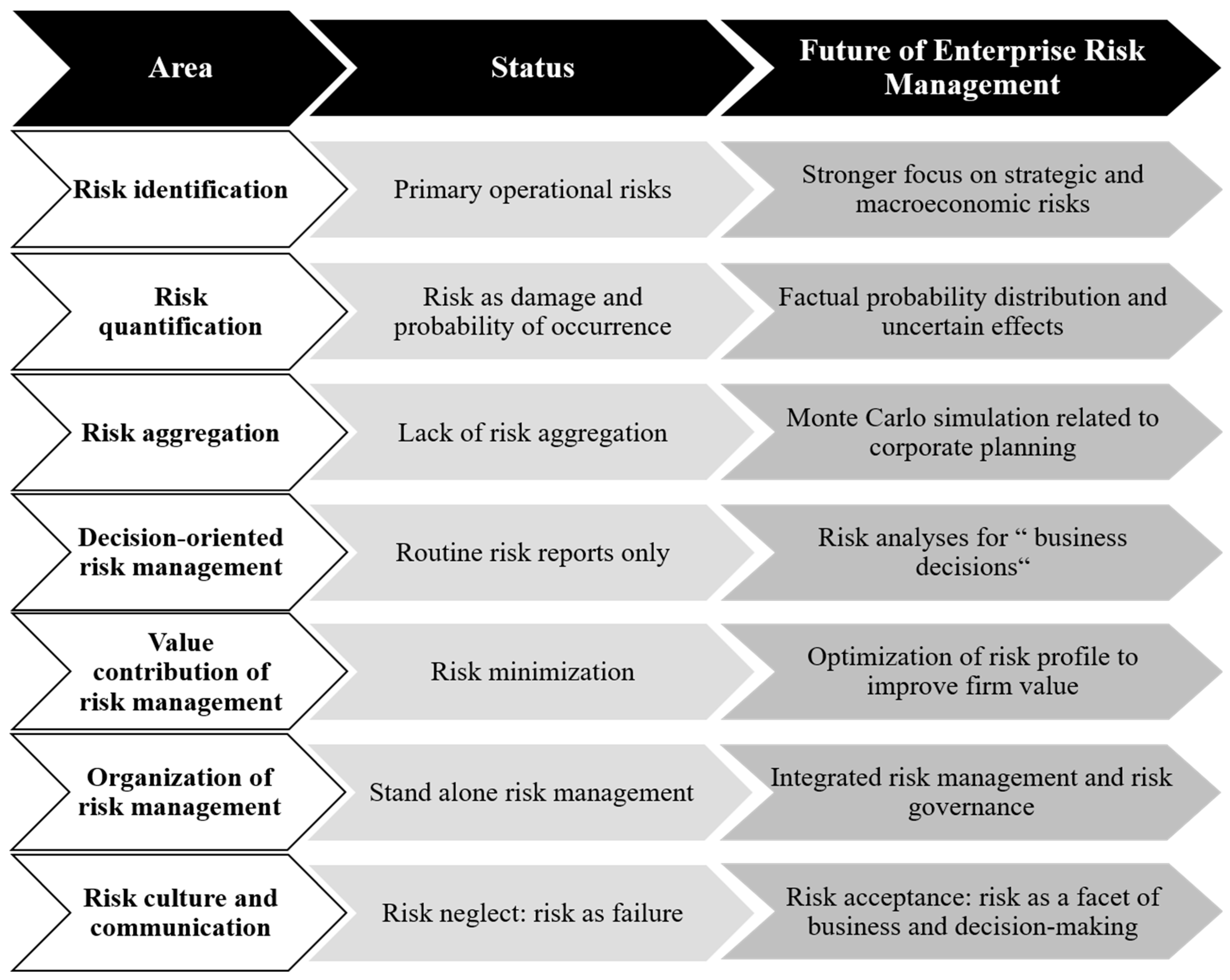

- Risk identification;

- Risk quantification;

- Risk aggregation;

- Decision orientation;

- Value contribution of risk management;

- Integrative risk management;

- Risk culture and communication.

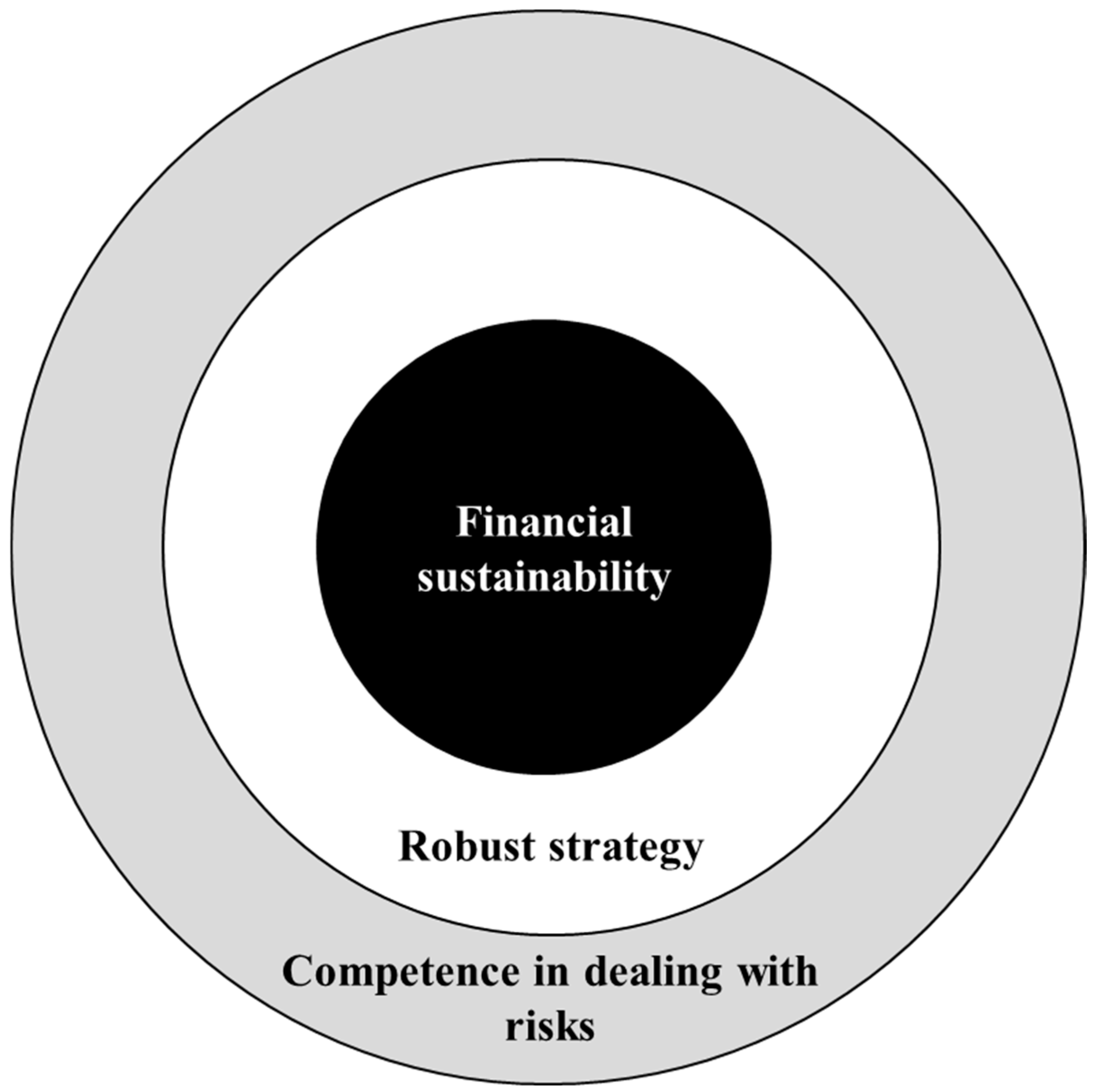

2. Robust Enterprise Framework

- Financial sustainability at the core, aiming at a stable rating and/or low earnings risk;

- A robust strategy focusing on stable strategic potential for success driving future financial performance and enterprise value;

- High competence in managing risks (both opportunities and threats), especially in decision-making.

2.1. Financial Sustainability

- (1)

- The enterprise at least matches the growth of the industry, in real terms and over the long term;

- (2)

- The risk-dependent probability of insolvency (p) is low;

- (3)

- The earnings risk, expressed by the coefficient of variation (V) of profits, is acceptable to the owners;

- (4)

- Capital returns exceed the risk-based cost of capital.

2.2. Robust Strategies

2.3. Competence in Managing Risks

3. Sound Risk Governance

3.1. Risk Identification

- Threats to individual success potentials or the business strategy as a whole, often arising from technological or societal trends;

- Changes in competitive forces in the industry environment (e.g., removal of barriers to entry, increasing dependence on customers or suppliers, availability of substitutes);

- The macroeconomic environment.

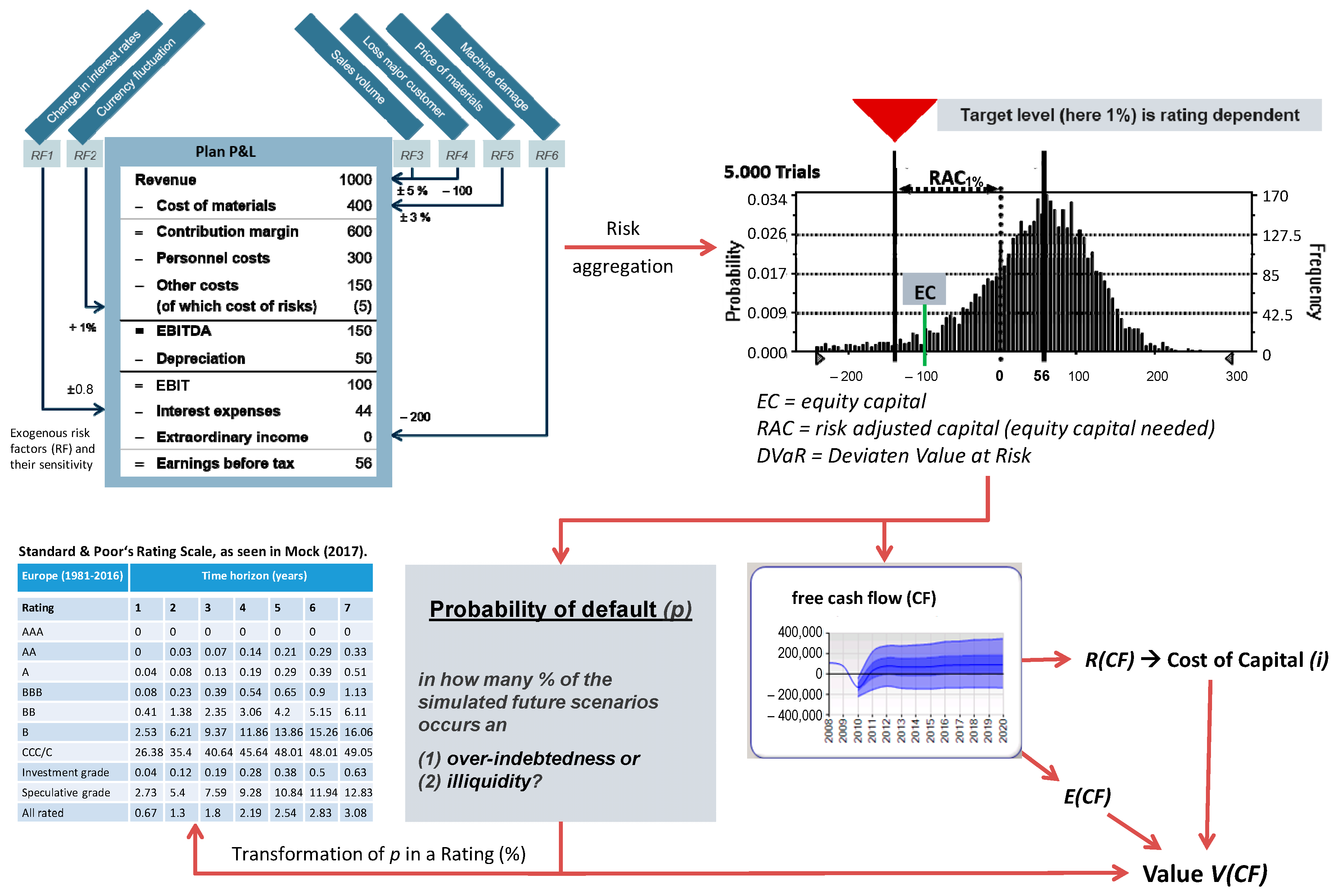

3.2. Risk Quantification

3.3. Risk Aggregation

3.4. Decision Orientation

3.5. Value Contribution of Risk Management

3.6. Organization-Wide Integrative Risk Management

- (a)

- Planned values and budgets are based on assumptions (e.g., raw material prices). Every uncertain assumption is a risk. Therefore, it is efficient to explicitly record all assumptions as part of the planning process and to share this information for risk management.

- (b)

- A new risk is identified whenever a deviation from the plan is caused by an as-yet unrecorded risk.

- (c)

- Strategic management and control systems (e.g., the balanced scorecard) are used to implement corporate strategy by clearly describing strategic objectives, expressed as key performance indicators (KPIs), and assigning measures and responsibilities. Assigning risks to key indicators reveals whether they can trigger deviations from the plan, augmenting the traditional scorecard approach. Those responsible for a particular metric then monitor the associated risks, which incentivizes employees to identify risks that can cause deviations. Moreover, deviation analysis makes it possible to assign responsibility for deviations that have occurred according to their cause. As a rule, the effects of exogenous risks cannot be attributed to those responsible for the performance indicator in the performance assessment.

3.7. Risk Culture and Communication

4. Literature Analysis

- Risk identification: Do the authors include strategic and macroeconomic risks?

- Risk quantification: Do the authors mention risk quantification?

- Risk aggregation: Do the authors stress that risks must be aggregated via simulations?

- Decision orientation: Do the authors stipulate that risk analysis must be linked to business decisions?

- Value contribution: Do the authors mention how risk management can improve firm value?

- Integrative risk management: Do the authors view risk management integratively?

- Risk culture and communication: Are risk culture and communication referenced?

5. Conclusions

- (a)

- Decision orientation and links to value-oriented corporate management: risk management should reveal how the risk scope changes before a decision is made and how this change should factor into the decision calculus.

- (b)

- Risk quantification, including commonly disregarded risk areas such as economic, geopolitical, and non-financial sustainability risks.

- (c)

- Risk aggregation procedures that link corporate planning to risk analysis using Monte Carlo simulations, facilitating decision-oriented risk management.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

| 1 | |

| 2 | We did not limit the analysis to the below-mentioned exact terms but used similar terms for the respective categories or truncated search terms such as “strateg*”, “cultur*”, or “quanti*”. To identify strategic and macroeconomic risks, we use these two terms and their truncated forms. For risk quantification, we used “metric”, “assessment”, “modelling”, “evaluation”, “quantification” and their truncated versions. For aggregation, we used aggregation (and a truncated form) as well as “portfolio”, “collective”, “simulat*”, and “dependenc*”. For decision orientation, we used “decisio*”; for value contribution, we used “value*”; for organization, we used “integrat*”, “holistic”, and “ERM”; and for risk culture, we used “cultur*”. We then related these terms to the context of their usage and assigned the respective grades. |

References

- Ai, Jing, Vickie Bajtelsmit, and Tianyang Wang. 2016. The Combined Effect of Enterprise Risk Management and Diversification on Property and Casualty Insurer Performance. Journal of Risk and Insurance 85: 513–43. [Google Scholar] [CrossRef]

- Amit, Raphael, and Birger Wernerfelt. 1990. Why Do Firms Reduce Business Risk? Academy of Management Journal 33: 520–33. [Google Scholar] [CrossRef]

- Annamalah, Sanmugam, Murali Raman, Govindan Marthandan, and Aravindan Kalisri Logeswaran. 2018. Implementation of Enterprise Risk Management (ERM) Framework in Enhancing Business Performances in Oil and Gas Sector. Economies 6: 4. [Google Scholar] [CrossRef]

- Anton, Sorin. 2018. The Impact of Enterprise Risk Management on Firm Value: Empirical Evidence from Romanian Non-financial Firms. Engineering Economics 29: 151–57. [Google Scholar] [CrossRef]

- Arrfelt, Mathias, Michael Mannor, Jennifer Nahrgang, and Amanda Christensen. 2018. All Risk-Taking Is Not the Same: Examining the Competing Effects of Firm Risk-Taking with Meta-Analysis. Review of Management Science 12: 621–60. [Google Scholar] [CrossRef]

- Ayyub, Bilal. 2014. Systems Resilience for Multihazard Environments: Definition, Metrics, and Valuation for Decision Making. Risk Analysis 34: 340–55. [Google Scholar] [CrossRef]

- Bao, Chunbing, Dengsheng Wu, Jie Wan, Jianping Li, and Jianming Chen. 2017. Comparison of Different Methods to Design Risk Matrices from the Perspective of Applicability. Procedia Computer Science 122: 455–62. [Google Scholar] [CrossRef]

- Baxter, Ryan, Jean Bedard, Rani Hoitash, and Andrew Yezegel. 2013. Enterprise Risk Management Program Quality: Determinants, Value Relevance, and the Financial Crisis. Contemporary Accounting Research 30: 1264–95. [Google Scholar] [CrossRef]

- Beasley, Mark, and Bruce Branson. 2022. 2022 Global State of Enterprise Risk Oversight. Enterprise Risk Management Initiative. September 27. Available online: https://erm.ncsu.edu/library/article/2022-global-state-of-enterprise-risk-oversight (accessed on 24 October 2024).

- Beasley, Mark, Don Pagach, and Richard Warr. 2008. Information Conveyed in Hiring Announcements of Senior Executives Overseeing Enterprise-Wide Risk Management Processes. Journal of Accounting, Auditing and Finance 23: 311–32. [Google Scholar] [CrossRef]

- Beasley, Mark, Richard Clune, and Dana Hermanson. 2005. Enterprise Risk Management: An Empirical Analysis of Factors Associated with the Extent of Implementation. Journal of Accounting and Public Policy 24: 521–31. [Google Scholar] [CrossRef]

- Berger, Thomas, and Werner Gleißner. 2018. Integrated Management Systems: Linking Risk Management and Management Control Systems. International Journal of Risk Assessment and Management 21: 215–31. [Google Scholar] [CrossRef]

- Berger, Thomas, Ignace Hooge, and Pankaj Trivedi. 2022. Processing of Information from Risk Maps in India and Germany: The Influence of Cognitive Reflection, Numeracy, and Experience. Asia-Pacific Journal of Risk and Insurance 17: 63–85. [Google Scholar] [CrossRef]

- Bohnert, Alexander, Nadine Gatzert, Robert Hoyt, and Philipp Lechner. 2018. The Drivers and Value of Enterprise Risk Management: Evidence from ERM Ratings. The European Journal of Finance 25: 234–55. [Google Scholar] [CrossRef]

- Bowman, Edward. 1980. A Risk/Return Paradox for Strategic Management. Sloan Management Review 21: 17–33. [Google Scholar]

- Buchner, Markus, Michael Kuttner, Christine Mitter, and Petra Sommerauer. 2021. Resilienz von Familienunternehmen—Eine systematische Literaturanalyse. Betriebswirtschaftliche Forschung und Praxis 73: 225–52. [Google Scholar]

- Budd, James. 1993. Characterizing Risk from the Strategic Management Perspective. Ph.D. dissertation, Kent State University, Kent, OH, USA. [Google Scholar]

- Callahan, Carolyn, and Jared Soileau. 2017. Does Enterprise Risk Management Enhance Operating Performance? Advances in Accounting 37: 122–39. [Google Scholar] [CrossRef]

- Campbell, John, Jens Hilscher, and Jan Szilagyi. 2008. In Search of Distress Risk. Journal of Finance 63: 2899–939. [Google Scholar] [CrossRef]

- Chen, Yu-Lun, Yi-Wie Chuang, Hong-Gia Huang, and Jhuan-Yu Shih. 2020. The Value of Implementing Enterprise Risk Management: Evidence from Taiwan’s Financial Industry. The North American Journal of Economics and Finance 54: 100926. [Google Scholar] [CrossRef]

- Committee of Sponsoring Organizations of the Treadway Commission (COSO), ed. 2017. Enterprise Risk Management—Integrating with Strategy and Performance. Durham: Committee of Sponsoring Organizations of the Treadway Commission (COSO). [Google Scholar]

- Dempsey, Mike. 2013. The Capital Asset Pricing Model (CAPM): The History of a Failed Revolutionary Idea in Finance? Abacus 49: 7–23. [Google Scholar] [CrossRef]

- Dorfleitner, Gregor, and Werner Gleißner. 2018. Valuing Streams of Risky Cashflows with Risk-Value Models. Journal of Risk 20: 1–27. [Google Scholar] [CrossRef]

- Eckles, David, Robert Hoyt, and Steve Miller. 2014. The Impact of Enterprise Risk Management on the Marginal Cost of Reducing Risk: Evidence from the Insurance Industry. Journal of Banking and Finance 49: 409–23. [Google Scholar] [CrossRef]

- El Ghoul, Sadok, Omrame Guedhami, Hakkon Kim, and Kwangwoo Park. 2018. Corporate Environmental Responsibility and the Cost of Capital: International Evidence. Journal of Business Ethics 149: 335–361. [Google Scholar] [CrossRef]

- Ernst, Dietmar. 2022. Simulation-Based Business Valuation: Methodical Implementation in the Valuation Practice. Journal of Risk and Financial Management 15: 200. [Google Scholar] [CrossRef]

- Fama, Eugene, and Kenneth French. 2015. A Five-Factor Asset Pricing Model. Journal of Financial Economics 116: 1–22. [Google Scholar] [CrossRef]

- Farrell, Mark, and Ronan Gallagher. 2015. The Valuation Implications of Enterprise Risk Management Maturity. Journal of Risk and Insurance 82: 625–57. [Google Scholar] [CrossRef]

- Farrell, Mark, and Ronan Gallagher. 2019. Moderating Influences on the ERM Maturity-Performance Relationship. Research in International Business and Finance 47: 616–28. [Google Scholar] [CrossRef]

- Fernández, Pablo. 2019. Is It Ethical to Teach That Beta and CAPM Explain Something? S&P Global Market Intelligence. Available online: https://dx.doi.org/10.2139/ssrn.2980847 (accessed on 24 October 2024).

- Florio, Cristina, and Giulia Leoni. 2017. Enterprise Risk Management and Firm Performance: The Italian Case. The British Accounting Review 49: 56–74. [Google Scholar] [CrossRef]

- Fraser, John, Rob Quail, and Betty Simkins, eds. 2021. Enterprise Risk Management: Today’s Leading Research and Best Practices for Tomorrow’s Executives, 2nd ed. Hoboken: Wiley. [Google Scholar]

- Froot, Kenneth, David Scharfstein, and Jeremy Stein. 1993. Risk Management: Coordinating Corporate Investment and Financing Policies. The Journal of Finance 48: 1629–58. [Google Scholar] [CrossRef]

- Garcia-Retamero, Rocio, and Edward Cokely. 2013. Communicating Health Risks with Visual Aids. Current Directions in Psychological Science 22: 392–99. [Google Scholar] [CrossRef]

- Gleißner, Werner. 2019. Cost of Capital and Probability of Default in Value-Based Risk Management. Management Research Review 42: 1243–58. [Google Scholar] [CrossRef]

- Gleißner, Werner. 2020. Integratives Risikomanagement – Schnittstellen zu Controlling, Compliance und Interner Revision. Controlling 32: 23–29. [Google Scholar] [CrossRef]

- Gleißner, Werner. 2023. Uncertainty and Resilience in Strategic Management: Profile of a Robust Company. International Journal of Risk Assessment and Management 26: 75–94. [Google Scholar] [CrossRef]

- Gleißner, Werner, and Dietmar Ernst. 2023. The Simulation-Based Valuation of Companies and Their Strategies–Classification, Methodology and Case Study. EBVM–The European Business Valuation Magazine 2: 4–16. [Google Scholar]

- Gleißner, Werner, Thomas Günther, and Christian Walkshäusl. 2022. Financial Sustainability: Measurement and Empirical Evidence. Journal of Business Economics 92: 467–516. [Google Scholar] [CrossRef]

- Golshan, Nargess, and Siti Zaleha Abdul Rasid. 2012. Determinants of Enterprise Risk Management Adoption: An Empirical Analysis of Malaysian Public Listed Firms. International Journal of Social and Human Sciences 6: 119–26. [Google Scholar]

- Gordon, Lawrence, Martin Loeb, and Chih-Yang Tseng. 2009. Enterprise Risk Management and Firm Performance: A Contingency Perspective. Journal of Accounting and Public Policy 28: 301–27. [Google Scholar] [CrossRef]

- Grace, Martin, Tyler Leverty, Richard Phillips, and Prakash Shimpi. 2014. The Value of Investing in Enterprise Risk Management. Journal of Risk and Insurance 82: 289–316. [Google Scholar] [CrossRef]

- Gupta, Kartick. 2018. Environmental Sustainability and Implied Cost of Equity: International Evidence. Journal of Business Ethics 147: 343–65. [Google Scholar] [CrossRef]

- Hanggraeni, Dewi, Beata Ślusarczyk, Liyu Sulung, and Athor Subroto. 2019. The Impact of Internal, External, and Enterprise Risk Management on the Performance of Micro, Small, and Medium Enterprises. Sustainability 11: 2172. [Google Scholar] [CrossRef]

- Hardy, Mary, and David Saunders. 2022. Quantitative Enterprise Risk Management. Cambridge: Cambridge University Press. [Google Scholar]

- Hargreaves, Jane. 2021. Quantitative Risk Assessment in ERM. In Enterprise Risk Management: Today’s Leading Research and Best Practices for Tomorrow’s Executives, 2nd ed. Edited by John Fraser, Rob Quail and Betty Simkins. Hoboken: Wiley, pp. 441–57. [Google Scholar]

- Holton, Glyn. 2004. Defining Risk. Financial Analysts Journal 60: 19–25. [Google Scholar] [CrossRef]

- Horvey, Sylvester, and Jacob Ankamah. 2020. Enterprise Risk Management and Firm Performance: Empirical Evidence from Ghana Equity Market. Cogent Economics and Finance 8: 1840102. [Google Scholar] [CrossRef]

- Horvey, Sylvester, and Jones Odei-Mensah. 2023. The Measurements and Performance of Enterprise Risk Management: A Comprehensive Literature Review. Journal of Risk Research 26: 778–800. [Google Scholar] [CrossRef]

- Hoyt, Robert, and Andre P. Liebenberg. 2011. The Value of Enterprise Risk Management. Journal of Risk and Insurance 78: 795–822. [Google Scholar] [CrossRef]

- Hunziker, Stefan. 2019. Enterprise Risk Management: Modern Approaches to Balancing Risk and Reward. Wiesbaden: Springer Gabler. [Google Scholar]

- International Organization for Standardization (ISO). 2018. Risk Management—Guidelines. ISO Standard No. 31000:2018. Geneva: International Organization for Standardization (ISO).

- Joyce, Chuck, and Kimball Mayer. 2012. Profits for the Long Run: Affirming the Case for Quality. GMO White Paper. June. Available online: http://csinvesting.org/wp-content/uploads/2012/06/gmo_wp_-_2012_06_-_profits_for_the_long_run_-_affirming_quality.pdf (accessed on 24 October 2024).

- Kaplan, Robert, and Anette Mikes. 2012. Managing Risks: A New Framework. Harvard Business Review 90: 48–60. [Google Scholar]

- Kaplan, Robert, and Anette Mikes. 2016. Risk Management—The Revealing Hand. Journal of Applied Corporate Finance 28: 8–18. [Google Scholar] [CrossRef]

- Kataoka, Shinji. 1963. A Stochastic Programming Model. Econometrica 31: 181–96. [Google Scholar] [CrossRef]

- Khan, Majid, Dildar Hussain, and Waqar Mehmood. 2016. Why Do Firms Adopt Enterprise Risk Management (ERM)? Empirical Evidence from France. Management Decision 54: 1886–907. [Google Scholar] [CrossRef]

- Krause, Timothy, and Yiuman Tse. 2016. Risk Management and Firm Value: Recent Theory and Evidence. International Journal of Accounting and Information Management 24: 56–81. [Google Scholar] [CrossRef]

- Kunz, Jennifer, and Mathias Heitz. 2021. Banks’ Risk Culture and Management Control Systems: A Systematic Literature Review. Journal of Management Control 32: 439–93. [Google Scholar] [CrossRef]

- Lechner, Philipp, and Nadine Gatzert. 2018. Determinants and Value of Enterprise Risk Management: Empirical Evidence from Germany. The European Journal of Finance 24: 867–87. [Google Scholar] [CrossRef]

- Li, Xun, and Zhenyu Wu. 2009. Corporate Risk Management and Investment Decisions. The Journal of Risk Finance 10: 155–68. [Google Scholar] [CrossRef]

- Liebenberg, André, and Robert Hoyt. 2003. The Determinants of Enterprise Risk Management: Evidence from the Appointment of Chief Risk Officers. Risk Management and Insurance Review 6: 37–52. [Google Scholar] [CrossRef]

- Lin, Yijia, Min-Ming Wen, and Jifeng Yu. 2012. Enterprise Risk Management: Strategic Antecedents, Risk Integration, and Performance. North American Actuarial Journal 16: 1–28. [Google Scholar] [CrossRef]

- Malik, Muhammad, Mahbub Zaman, and Sherrena Buckby. 2020. Enterprise Risk Management and Firm Performance: Role of the Risk Committee. Journal of Contemporary Accounting and Economics 16: 100178. [Google Scholar] [CrossRef]

- Mardessi, Sana, and Sonda Ben Arab. 2018. Determinants of ERM Implementation: The Case of Tunisian Companies. Journal of Financial Reporting and Accounting 16: 443–63. [Google Scholar] [CrossRef]

- McShane, Michael. 2017. Enterprise Risk Management: History and a Design Science Proposal. The Journal of Risk Finance 19: 137–53. [Google Scholar] [CrossRef]

- McShane, Michael, Anil Nair, and Elzotbek Rustambekov. 2011. Does Enterprise Risk Management Increase Firm Value? Journal of Accounting, Auditing, and Finance 26: 641–58. [Google Scholar] [CrossRef]

- Miloš Sprčić, Danijela, Marina Mešin Žagar, Zeljko Sevic, and Mojca Marc. 2016. Does Enterprise Risk Management Influence Market Value—A Long-Term Perspective. Risk Management 18: 65–88. [Google Scholar] [CrossRef]

- Mthiyane, Zodwa, Huibrecht van der Poll, and Makgopa Tshehla. 2022. A framework for risk management in small medium enterprises in developing countries. Risks 10: 173. [Google Scholar] [CrossRef]

- Nair, Anil, Elzotbek Rustambekov, Michael McShane, and Stav Fainshmidt. 2014. Enterprise Risk Management as a Dynamic Capability: A Test of Its Effectiveness During a Crisis. Managerial and Decision Economics 35: 555–66. [Google Scholar] [CrossRef]

- Nasr, Arash, Saideh Alaei, Fateme Bakhshi, Farzin Rasoulyan, Hojat Tayaran, and Mohammad Farahi. 2019. How Enterprise Risk Management (ERM) Can Affect on Short-Term and Long-Term Firm Performance: Evidence from the Iranian Banking System. Entrepreneurship and Sustainability Issues 7: 1387–405. [Google Scholar] [CrossRef] [PubMed]

- Nguyen, Duc, and Dinh-Tri Vo. 2020. Enterprise Risk Management and Solvency: The Case of the Listed EU Insurers. Journal of Business Research 113: 360–69. [Google Scholar] [CrossRef]

- Nocco, Brian, and René Stulz. 2022. Enterprise Risk Management: Theory and Practice. Journal of Applied Corporate Finance 34: 81–94. [Google Scholar] [CrossRef]

- Novak, David, Zhaohui Wu, and Kevin Dooley. 2021. Whose Resilience Matters? Addressing Issues of Scale in Supply Chain Resilience. Journal of Business Logistics 42: 323–35. [Google Scholar] [CrossRef]

- Orlando, Albina. 2021. Cyber risk quantification: Investigating the role of cyber value at risk. Risks 9: 184. [Google Scholar] [CrossRef]

- Otero González, Luís, Pablo Santomil, and Aracely Herrera. 2020. The Effect of Enterprise Risk Management on the Risk and the Performance of Spanish Listed Companies. European Research on Management and Business Economics 26: 111–20. [Google Scholar] [CrossRef]

- Pagach, Don, and Richard Warr. 2011. The Characteristics of Firms That Hire Chief Risk Officers. Journal of Risk & Insurance 78: 185–211. [Google Scholar]

- Pan, Yihui, Stephan Siegel, and Tracy Wang. 2020. The Cultural Origin of CEOs’ Attitudes Toward Uncertainty: Evidence from Corporate Acquisitions. The Review of Financial Studies 33: 2977–3030. [Google Scholar] [CrossRef]

- Ping, Ai Teoh, and Rajendran Muthuveloo. 2015. The Impact of Enterprise Risk Management on Firm Performance: Evidence from Malaysia. Asian Social Science 11: 149–59. [Google Scholar] [CrossRef]

- Quon, Tony, Daniel Zeghal, and Michel Maingot. 2012. Enterprise Risk Management and Business Performance During the Financial and Economic Crises. Problems and Perspectives in Management 10: 95–103. [Google Scholar]

- Rossi, Matteo. 2016. The Capital Asset Pricing Model: A Critical Literature Review. Global Business and Economics Review 18: 604–17. [Google Scholar] [CrossRef]

- S&P Global. 2005. Evaluating the Enterprise Risk Management Practices of Insurance Companies. Standard and Poor’s RatingsDirect, October 17. [Google Scholar]

- Saeidi, Parvaneh, Sayyedeh Saeidi, Leonardo Gutierrez, Dalia Streimikiene, Melfi Alrasheedi, Sayedeh Saeidi, and Abbas Mardani. 2021. The Influence of Enterprise Risk Management on Firm Performance with the Moderating Effect of Intellectual Capital Dimensions. Economic Research-Ekonomska Istraživanja 34: 122–51. [Google Scholar] [CrossRef]

- Saha, Anatu, and Burton Malkiel. 2012. DCF Valuation with Cash Flow Cessation Risk. Journal of Applied Finance 22: 175–85. [Google Scholar]

- Shleifer, Andrei, and Robert Vishny. 1997. The Limits of Arbitrage. The Journal of Finance 52: 35–55. [Google Scholar] [CrossRef]

- Silva, Juliano, Aldy da Silva, and Betty Chan. 2019. Enterprise Risk Management and Firm Value: Evidence from Brazil. Emerging Markets Finance and Trade 55: 687–703. [Google Scholar] [CrossRef]

- Stein, Volker, and Arnd Wiedemann. 2016. Risk Governance: Conceptualization, Tasks, and Research Agenda. Journal of Business Economics 86: 813–36. [Google Scholar] [CrossRef]

- Stein, Volker, Arnd Wiedemann, and Christiane Bouten. 2019. Framing Risk Governance. Management Research Review 42: 1224–42. [Google Scholar]

- Telser, Lester. 1955. Safety First and Hedging. Review of Economic Studies 23: 1–16. [Google Scholar] [CrossRef]

- Vose, David. 2008. Risk Analysis: A Quantitative Guide, 3rd ed. Hoboken: Wiley. [Google Scholar]

- Weigel, Christine, Martin Hiebl, and Arnd Wiedemann. 2018. Vom Risk Management zur Risk Governance. Controlling and Management 62: 34–40. [Google Scholar] [CrossRef]

- Wiedemann, Arnd, Volker Stein, and Mark Fonseca. 2022. Risk Governance in Organizations: Future Perspectives. Siegen: Universitätsverlag Siegen. [Google Scholar]

- Zou, Xiang, Che Isa, and Mahfuzur Rahman. 2019. Valuation of Enterprise Risk Management in the Manufacturing Industry. Total Quality Management and Business Excellence 30: 1389–410. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Authors | Identification | Quantification | Aggregation | Decision Orientation | Value Contribution | Organization | Risk Culture |

|---|---|---|---|---|---|---|---|

| (Ai et al. 2016) | YES | Partly | NO | Partly | Partly | YES | Partly |

| (Annamalah et al. 2018) | Partly | NO | NO | Partly | NO | Partly | Partly |

| (Anton 2018) | NO | NO | NO | Partly | Partly | Partly | Partly |

| (Baxter et al. 2013) | NO | Partly | NO | NO | Partly | Partly | NO |

| (Beasley et al. 2005) | NO | Partly | NO | NO | Partly | YES | NO |

| (Beasley et al. 2008) | YES | YES | YES | Partly | YES | YES | Partly |

| (Bohnert et al. 2018) | NO | NO | NO | NO | YES | YES | NO |

| (Callahan and Soileau 2017) | NO | NO | NO | NO | YES | Partly | NO |

| (Chen et al. 2020) | NO | Partly | NO | NO | Partly | YES | Partly |

| (Eckles et al. 2014) | Partly | YES | YES | YES | YES | YES | YES |

| (Farrell and Gallagher 2015) | NO | NO | YES | YES | YES | YES | YES |

| (Farrell and Gallagher 2019) | YES | Partly | NO | Partly | YES | YES | Partly |

| (Florio and Leoni 2017) | NO | NO | NO | NO | NO | YES | NO |

| (Golshan and Rasid 2012) | NO | Partly | NO | NO | Partly | YES | NO |

| (Gordon et al. 2009) | Partly | YES | Partly | YES | YES | YES | Partly |

| (Grace et al. 2014) | NO | Partly | NO | YES | NO | YES | NO |

| (Hanggraeni et al. 2019) | NO | NO | NO | NO | Partly | YES | NO |

| (Horvey and Ankamah 2020) | NO | NO | NO | Partly | YES | YES | NO |

| (Hoyt and Liebenberg 2011) | NO | Partly | NO | NO | Partly | YES | NO |

| (Khan et al. 2016) | NO | Partly | NO | NO | YES | YES | YES |

| (Lechner and Gatzert 2018) | NO | NO | NO | YES | YES | YES | NO |

| (Liebenberg and Hoyt 2003) | NO | Partly | Partly | NO | YES | YES | Partly |

| (Lin et al. 2012) | NO | NO | NO | YES | YES | YES | YES |

| (Malik et al. 2020) | YES | YES | NO | NO | Partly | YES | Partly |

| (Mardessi and Arab 2018) | Partly | NO | YES | YES | YES | YES | Partly |

| (McShane et al. 2011) | NO | NO | YES | YES | YES | YES | Partly |

| (Miloš Sprčić et al. 2016) | NO | NO | NO | YES | Partly | NO | YES |

| (Nair et al. 2014) | NO | NO | NO | NO | Partly | YES | NO |

| (Nasr et al. 2019) | NO | NO | NO | NO | NO | Partly | NO |

| (Nguyen and Vo 2020) | NO | Partly | YES | Partly | Partly | YES | NO |

| (Otero González et al. 2020) | NO | Partly | NO | NO | Partly | YES | NO |

| (Pagach and Warr 2011) | NO | YES | NO | NO | Partly | YES | NO |

| (Ping and Muthuveloo 2015) | YES | Partly | NO | Partly | Partly | Partly | NO |

| (Quon et al. 2012) | NO | Partly | Partly | Yes | Partly | YES | NO |

| (Saeidi et al. 2021) | NO | Partly | NO | Partly | Partly | YES | YES |

| (Silva et al. 2019) | NO | Partly | NO | Partly | Partly | YES | Partly |

| (Zou et al. 2019) | NO | NO | NO | Partly | Partly | YES | NO |

| Share “Yes” | 13.5% | 13.5% | 16.2% | 27.0% | 37.8% | 81.1% | 16.2% |

| Share “No” | 75.7% | 43.2% | 75.7% | 43.2% | 10.8% | 2.7% | 51.4% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gleißner, W.; Berger, T.B. Enterprise Risk Management: Improving Embedded Risk Management and Risk Governance. Risks 2024, 12, 196. https://doi.org/10.3390/risks12120196

Gleißner W, Berger TB. Enterprise Risk Management: Improving Embedded Risk Management and Risk Governance. Risks. 2024; 12(12):196. https://doi.org/10.3390/risks12120196

Chicago/Turabian StyleGleißner, Werner, and Thomas B. Berger. 2024. "Enterprise Risk Management: Improving Embedded Risk Management and Risk Governance" Risks 12, no. 12: 196. https://doi.org/10.3390/risks12120196

APA StyleGleißner, W., & Berger, T. B. (2024). Enterprise Risk Management: Improving Embedded Risk Management and Risk Governance. Risks, 12(12), 196. https://doi.org/10.3390/risks12120196