1. Introduction

Gold and stock exchange have always been pivotal for investors. Cryptocurrency has also attracted the attention of investors (and researchers too) as an alternative investment. This paper aims to compare three different investment options: the Bitcoin cryptocurrency price, the gold price, and the Dow Jones stock index level examining three periods. The first period, from October 2014 to September 2018, marked the initiation of the official cryptocurrency price data. The second period, from October 2018 to May 2022, aimed to capture more recent trends before the effects of COVID-19 were fully embedded, and the third period, from January 2020 to December 2023, is the whole COVID-19 period with the initiation, embedded, and terminal phases.

Ref. [

1] used cryptographic proof to solve the double-spending issue when he introduced modern blockchain technology. Nakamoto’s creative application, as noted by [

2,

3] sets the stage for an electronic payment system based on cryptographic proof rather than trust, allowing decentralized transactions without the need for a middleman. Cryptographic techniques are used by cryptocurrencies, a subset of digital currencies, to achieve consensus [

4]. They are classified as non-legal tender by the World Bank, European Banking Authority (EBA), and European Securities and Markets Authority (ESMA), but are legal tender in El Salvador [

4]. Cryptocurrency is defined by the FATF as a digital representation of value that serves as a store of value, an accounting unit, and a medium of exchange but does not have the legal standing of a national currency [

4].

By providing a thorough understanding of the complex world of cryptocurrencies, this multifaceted exploration aims to set the stage for future research. Electronic money is different from digital currency in that it is a digital form of legal tender, whereas digital or virtual currency is a more general term that includes electronic money to some degree [

5]. Digital currencies were defined as forms of digital money without a specific legal status by the European Central Bank (ECB) in 2012 as part of a comprehensive report aimed at classifying and regulating them (ECB, 2015). The International Monetary Fund (IMF) further classified cryptocurrencies as a subset of digital currencies, which include Bitcoin and other cryptocurrencies as well as simpler IOUs and those linked to physical assets, like gold [

4]. Digital currencies or digital debt systems are what the Committee on Payments and Market Infrastructures (CPMI), a division of the Bank for International Settlements (BIS), refers to as cryptocurrencies. Even though the Bretton Woods agreement was abandoned in 1973, gold has become less important in the global monetary system. The IMF is one of the world’s biggest official holders of gold [

6]. Over time, the legal status of gold ownership in the United States has changed. President Roosevelt outlawed it in 1933, and President Ford reversed the decision in 1974. An important turning point was the removal of barriers and discrimination against private ownership of gold with the liberalization of global markets, especially in China in 2005 and in India in 1991 [

7].

A variety of products and services are available for investing in gold, including gold coins, bars, mutual funds, tradable securities, gold derivatives, gold accounts, and shares in gold mining firms. Sovereigns and Krugerrands are examples of physical gold coins that have inherent value. Gold bars are larger quantities of pure gold that are usually kept for investment purposes. They are usually cast or minted. Exchange-traded funds (ETFs) and bonds backed by gold are examples of tradable gold securities that give investors exposure to gold without requiring physical possession. Gold mutual funds invest in a diverse portfolio of gold-related assets by pooling the contributions of several investors. Like futures contracts, gold derivatives let investors make predictions about gold prices in the future. Banks and other financial institutions can provide gold accounts that let people buy and sell gold electronically. Finally, purchasing stock in gold mining firms gives investors a tangential exposure to gold, as the dynamics of the gold market impact the performance of these stocks [

8,

9]. Every type of gold investment has advantages and disadvantages of its own, enabling investors to customize their portfolios according to their risk tolerance and financial objectives.

The historical demands associated with economic advancement that have changed over time on a global scale are the foundation for the creation of stock exchanges. Technology led to a global economic boom in the middle of the 20th century and the emergence of contemporary stock exchange operating frameworks. The earliest exchanges were encouraged by early economies and agrarian societies in Europe, while resource-rich nations like Africa and Canada witnessed an increase in exchanges due to the mineral trade. The market began in the 17th century, and the Industrial Revolution in the 19th century proved to be crucial. Early 18th-century government bond markets gave rise to stock exchanges, which saw a turning point in 1773 when London traders formalized their domain. The New York Stock Exchange, established in 1792, was impacted by innovations in technology, such as the telegraph, and was instrumental in the post-Civil War era. The transatlantic cable link established in 1866 and the electronic market established by Nasdaq in 1971 both had revolutionary effects. The London Stock Exchange leads in issuers and variety, while the New York Stock Exchange currently holds the title of the largest in the world. The London Stock Exchange, Euronext, Norex, Nasdaq, Easdaq, and Nasdaq represent the evolution of global markets. Since 1885, the Dow Jones Industrial Average has evaluated the stock performance of thirty major American companies. Because of its small size, some people view it as an incomplete representation when compared to indices like the S&P 500. The index, calculated using a divisor of approximately 0.1474, is 6.7843 times greater than the total of the component values.

The paper is organized as follows. First, a review of the relevant literature is provided. An analysis of the data used follows. Then, the statistical methods (descriptive, correlations, multiple linear regression) as well as the time series analysis methods (autocorrelation, cross correlation, granger causality tests, ARIMA modeling) used to analyze the data and the relative results are presented and analyzed. Following this, the main conclusions drawn are evaluated and the study’s practical implications are highlighted. Finally, the main limitations of the study are discussed, and potential future research is indicated.

2. Literature Review

A thorough examination of several factors is included in research on cryptocurrencies and their economic ramifications, which sheds light on their intricate dynamics and wider economic consequences. Using statistical methods based on rescaled range analysis, Ref. [

10] investigate the spread and fractal structure of the dynamic relationship between gold and silver prices. In comparison to straightforward wait-and-see and moving average strategies, this analysis shows the efficacy of trading rules over a range of holding periods. By utilizing an asymmetric GARCH methodology. Ref. [

11] evaluate Bitcoin’s risk-hedging capabilities against gold, highlighting the cryptocurrency’s potential as a short-term hedge against stocks. Similarly to this, Ref. [

12] fits parametric distributions to examine the statistical characteristics of popular cryptocurrencies. To identify cryptocurrencies with lower risk, Ref. [

13] focuses on the tail behavior of returns in five major cryptocurrencies. It does this by estimating risk measures and applying extreme value analysis. Blockchains as distributed ledgers in peer-to-peer networks are examined in detail in [

14], which models the blockchain proof-of-work protocol as a stochastic game and examines the equilibrium strategies of rational miners. Ref. [

15] have developed a new research avenue in which they thoroughly examine transaction histories within the cryptocurrency complex. They achieve this by using an empirically oriented approach that aims to explain the mechanics of cryptocurrencies and suggest possible avenues for future research. The economic characteristics of digital assets are evaluated by [

16], who propose that because cryptocurrencies have weak cross-correlations with traditional assets, they are appropriate for economic diversification. Angerer and colleagues (2021) underscore the significance of consolidating understanding in reaction to swiftly accumulating empirical data regarding cryptocurrencies. Through a thorough meta-analysis, Ref. [

17] fills in knowledge gaps regarding the factors influencing cryptocurrency usage intention. To investigate correlations in cryptocurrency contexts, Ref. [

18] presents a dual-stage analysis methodology that combines artificial neural networks (ANN) and partial least squares structural equation modeling (PLS-SEM). Ref. [

19] make a second contribution in which they conduct a systematic literature analysis and identify three areas of promising future research: non-standardized financial risks, the adoption of innovative cryptocurrencies, and subjective risk perception. Ref. [

20] criticize the narrow focus of fintech research and offer a framework that supports a more expansive understanding of user needs in cryptocurrency research. In their analysis of the intricacies of a dual economy, Refs. [

21,

22] highlight the importance of equivalent nominal interest rates and a risk-adjusted martingale exchange rate in the context of international cryptocurrencies.

The relationship between global energy commodities and the stock markets of China, India, South Africa, and Brazil was investigated by [

23]. They analyzed this relationship using wavelet techniques and discovered that positive co-movements become stronger over time. They also found that this relationship is significantly impacted by volatilities, especially those derived from the US Volatility Index. The authors concluded that investors looking to manage portfolio risks in energy commodities and the stock markets of the nations can benefit from these insights. Using an asymmetric approach, Ref. [

24] investigated how susceptible sustainable Islamic stock returns were to implied market volatilities. They discovered that most volatilities had an impact on these returns that is inversely related. The writers stressed how crucial it is to build portfolios using appropriate volatility indices to efficiently manage risk in a variety of market scenarios. Ref. [

25] carried out a study within the framework of the COVID-19 pandemic. They looked at the connection between gold and different cryptocurrencies using frequency-dependent asymmetric and causality analysis technologies. According to the research, gold primarily serves as a diversifier and safe haven for most cryptocurrencies over a range of investment horizons. Significant short- and medium-term hedging benefits for Dogecoin, Ripple, and Bitcoin were also found in the study. Ref. [

26] examined the short- and long-term relationships between three cryptocurrencies and twenty-one stock exchanges using the VAR/VEC Model. These variables showed cointegration, short-term relationships, and causality, according to their analysis. The Stock Exchange series showed signs of cryptocurrency influence as well, with an average impact of 16, 15, and 16 periods for Bitcoin, Litecoin, and Ripple, respectively. Ref. [

27] used the reduction method in a different research project to determine important factors that influence Bitcoin returns and volatility. After conducting an analysis, they concluded that the reduced set of explanatory variables influencing Bitcoin returns includes market capitalization, Bitcoin mining difficulty, gold return, Euro/USD exchange rate return, US Nasdaq stock exchange index return, and Twitter-based economic uncertainty. The authors also discovered that the volume of the cryptocurrency and the lag terms of the ARCH effect have the biggest effects on Bitcoin volatility. Ref. [

28] investigated the interactions between Bitcoin to euro, gold, and STOXX50 during the period of COVID-19 and showed that the COVID-19 cases and gold hurt the exchange rate of Bitcoin to euro, while there was great volatility regarding the response of Bitcoin to a shock of STOXX50. Ref. [

29] examined the existence of interdependencies between specific stock market indices (namely RTSI, Eurostoxx, and S&P 500), exchange rates (EUR/USD and RUB/USD) and crude oil for the period January 2021 to July 2022 with daily data, applying a wavelet coherence approach, and revealed the existence of strong correlations between all variables, during different time periods and for different frequencies during the period reviewed.

3. Data Analysis

Three time periods comprise the research period: October 2014–September 2018, October 2019–September 2022, and January 2020–December 2023. The availability of data had a significant impact on the choice of the study period. The sub-periods we have chosen have a duration of four years. The first studied period was chosen to represent the time leading up to the Greek economy’s recovery from the severe financial crisis that began in 2010. The second period is continuous with the first period. The third period has a period of overlap with the second. The third period is the period from the appearance until the complete disappearance of the pandemic crisis COVID-19. The data available are the closing prices of gold, the DWJ index, and Bitcoin. These data are examined for the abovementioned three different periods, to compare whether the influencing mechanisms between the time series are kept unchanged over time. Time series data are daily values. The key descriptive statistics of Bitcoin, gold, and the DWJ for each period are presented in

Table 1 below.

The key research question is whether there is a causal effect of gold and DWJ on Bitcoin. Furthermore, an additional research question is if there are changes over time to the possible causal effects found in the research question. R-language v.4.3.2 and IBM SPSS v.24.0 software were used to analyze the data and to provide the answer to the research question. We applied time series analysis techniques along with traditional descriptive and inductive statistics techniques. Time plots, multiple scatter dot plot matrices, autocorrelation functions, Granger causality tests, the Pearson’s R correlation coefficient, ordinary multiple regression analysis, and cross-correlation time series analysis were specifically used. In particular, initially the simple descriptive indicators for the three time series for each period were calculated, such as the mean, median, standard deviation, skewness, kurtosis, K’S normality, and stationarity tests. Then, the time plot graphs were constructed, which give us a visual overview of the dependence of the three time series. Pearson’s correlation coefficient was then implemented for a rough overview of correlation and the corresponding multiple scatter dot plot matrices were produced. Multiple linear regression (non-time series approximation) was applied for an initial estimate of the weighted effects of gold and the DWJ on Bitcoin. Then, all the necessary transformations were implemented such as time lags, time differences, log transformations etc. Next, the autocorrelation and partial autocorrelation functions and relevant graphs were implemented, from which, among other things, the time lag depth of the dependencies is derived. Finally, time series regression models (ARIMA, etc.) were implemented to accurately capture the impact mechanisms of gold and DTC on Bitcoin.

4. Results

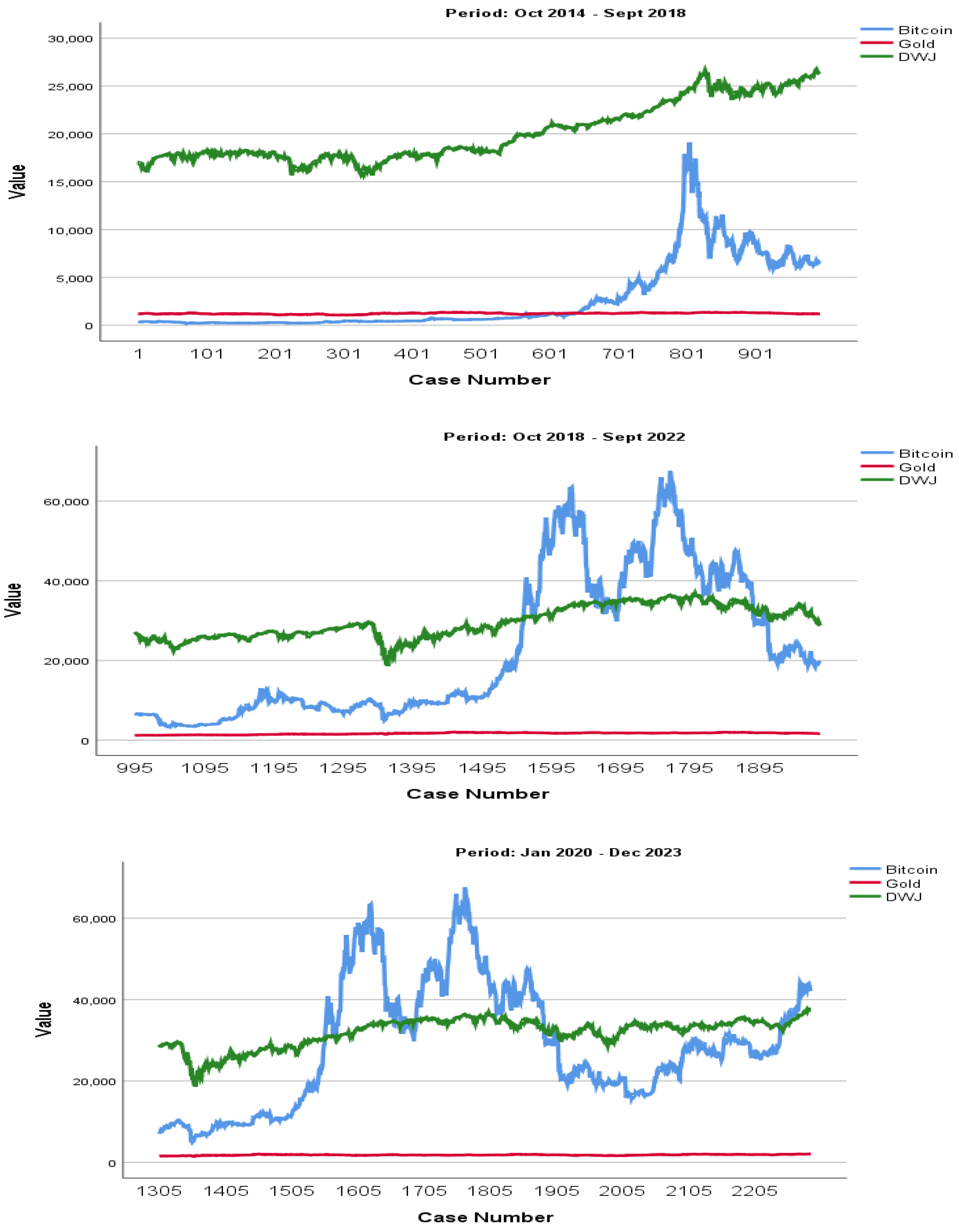

Figure 1 below shows time plot graphs for gold, the DWJ, and Bitcoin over three time periods. The overview of the time plot shows that there is a weak visual co-variation in the three sets of times series.

The Pearson’s R correlation coefficient was then calculated between the three time series and for the three merged periods (thus, the Pearson coefficient applied to the whole period from 2014 to 2023), resulting in a statistically significant strong positive correlation between all three time series: R

Bitcoin & Gold = 0.779,

p < 0.001; R

Bitcoin & DWJ = 0.863,

p < 0.001 and R

Gold & DWJ = 0.875,

p < 0.001. It is worth noting that there was no significant correlation between gold and the DWJ during the first data period.

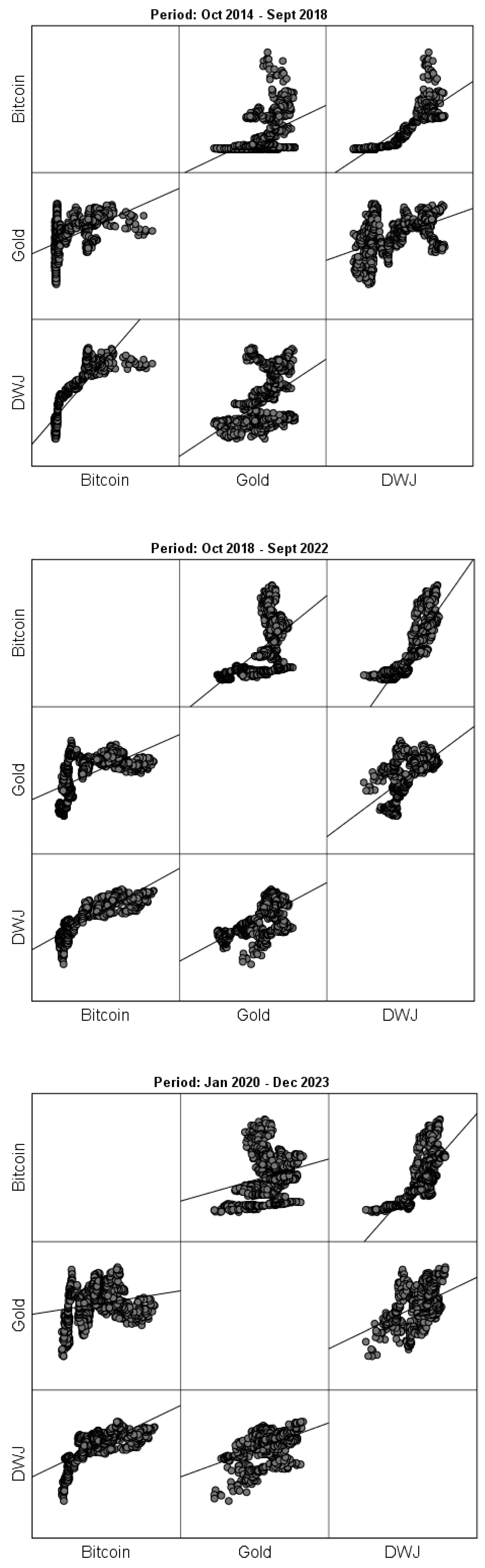

Figure 2 below depicts a multiple scatter dot matrix that shows a strong positive correlation.

Following the analysis, a multiple linear regression analysis was applied with the price of Bitcoin as the dependent variable; the predictive variables were the prices of gold and the DWJ, with the “enter” method. This analysis—like the previous ones—is applied as an initial and descriptive exploration of the relationship between the three variables. The regression results are presented in

Table 2 below. The regression results show a statistically significant effect (

p < 0.05) of gold and the DWJ on Bitcoin. The data in this regression cover the whole time period, since this regression analyses only simultaneous values without taking time lags into account.

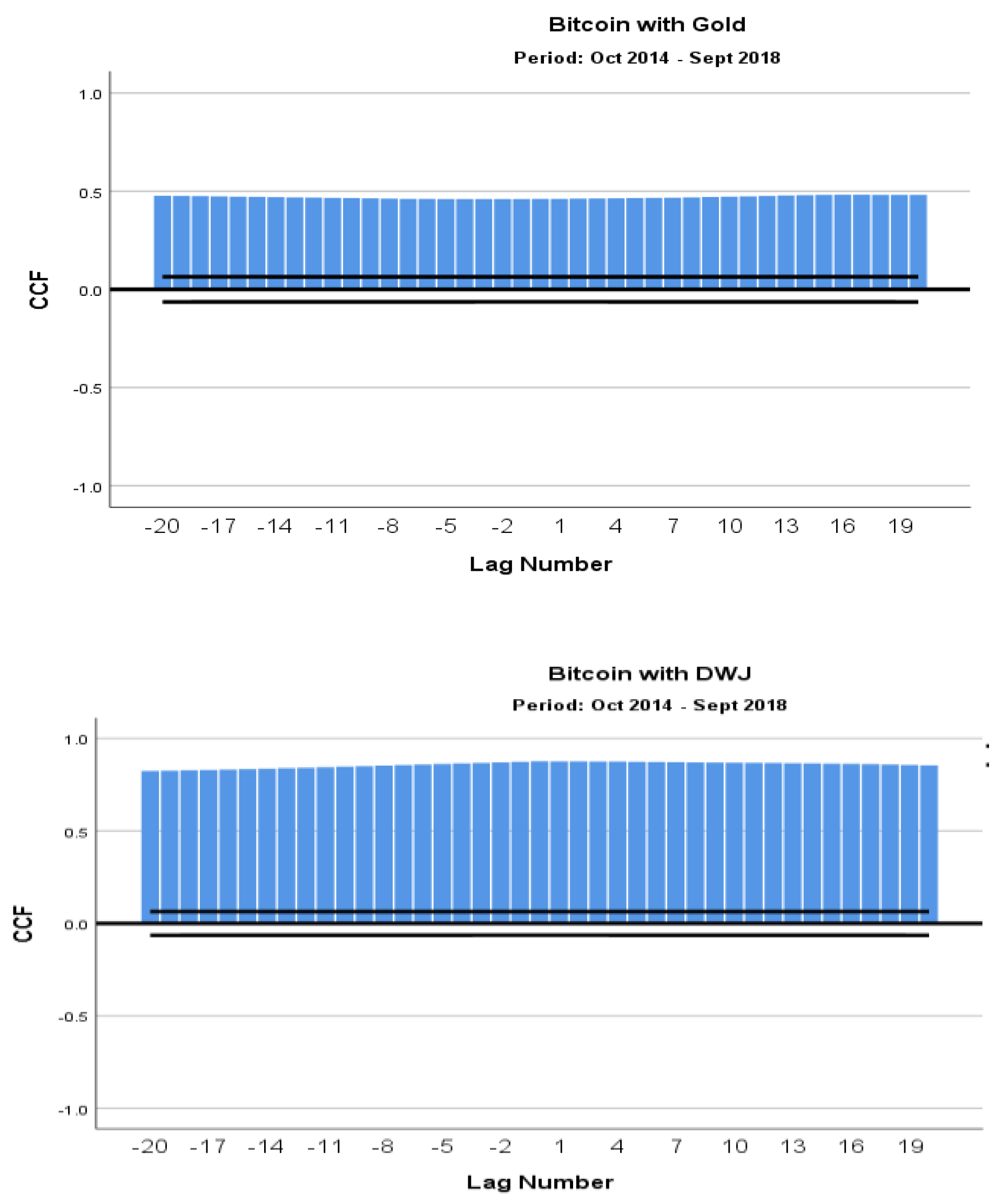

Τhen, the partial autocorrelation function (PACF) and cross-correlation function (CCF) was estimated for the three time series for the three periods. From the results of the CCF, it follows that there is an effect of the first time order lag on gold and bitcoin, while there is more complicated structure of lag influence to the DWJ, which consists of lags with orders of 1, 2, 3, and 8. Furthermore, a time series cross correlation analysis was performed. The visual results of the cross-correlation coefficients are presented in

Figure 3 below, from which it is evident that the existing influence over Bitcoin is stronger in the case of gold than in the case of DWJ. In

Figure 3, there are presenting only some indicative graphs, due to the large number of all possible variable and period combinations. Furthermore, it seems that the structure of these influences is differentiated between the three periods studied.

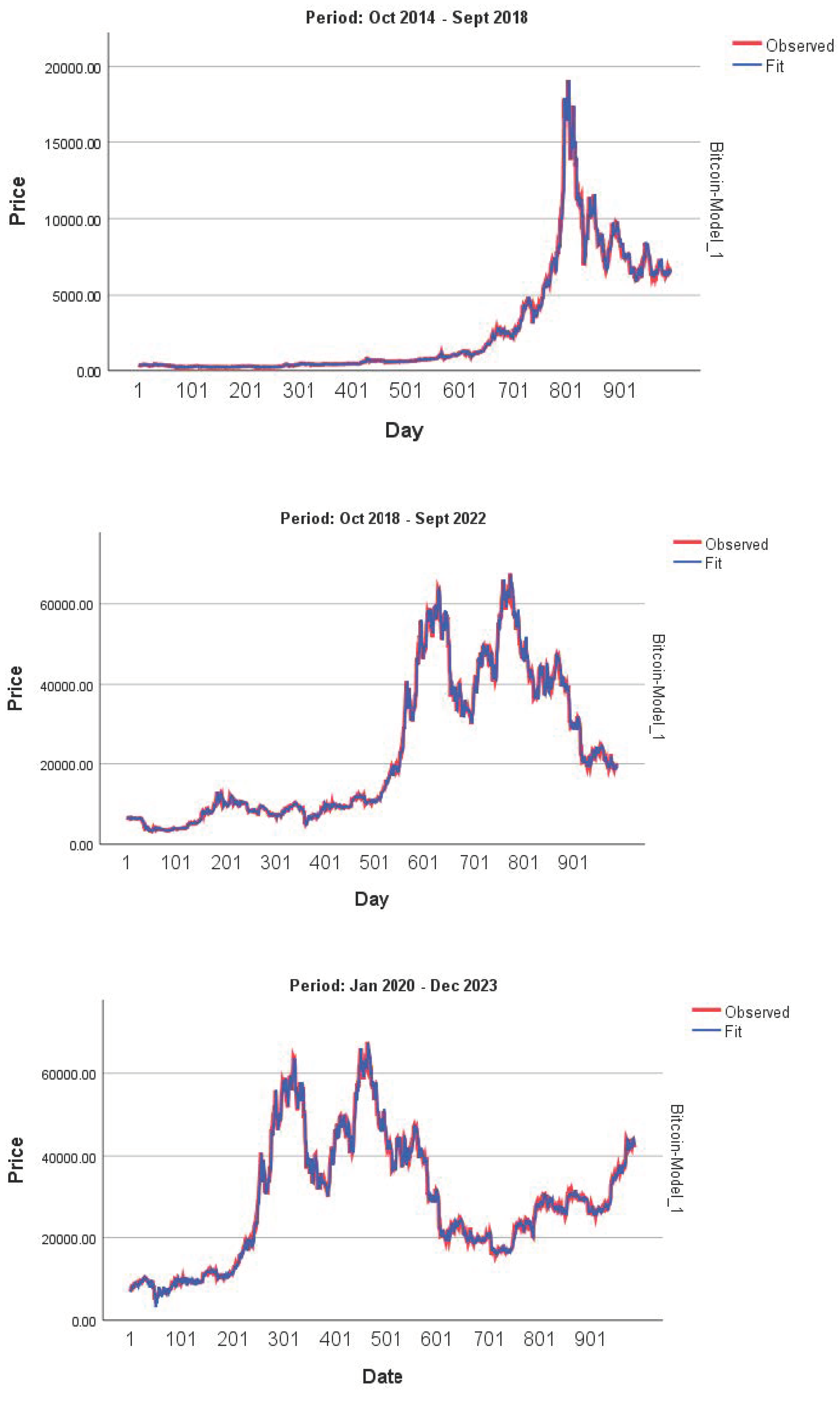

Given the information obtained from the above analyses, several ARIMA models were performed to test the forecasting ability of gold and DWJ over Bitcoin. We selected the optimum model based on the goodness of fit tests, and the results are presented in

Table 3 below, from which it is evident that a different ARIMA model fits each of the three periods best; in particular, the model is differentiated between the COVID-19 period (third period) versus the pre-COVID periods.

The comparisons between the predicted and observed values are given in

Figure 4 below and it seems to be slightly satisfactory. The distribution of the residuals was tested with the KS test and marginally found to be in compliance with the normal distribution (

p = 0.048).

Finally, a Granger causality test was performed to examine if a cause–effect relationship exists between Bitcoin (effect) and Gold and the DWJ. To perform this, we constructed the LAG time series and the difference time series for gold and the DWJ. The definitions of the two functions are as follows:

After constructing these variables, a multiple linear regression was applied with Bitcoin as the dependent variable and all the first to fourth order LAGS and DIFF functions of Gold and DWJ were used as predictors. Because of the large number of predictors, we applied a backward stepwise method of regression, which automatically test–retested and rejected predictors based on their explanatory contribution. The results are given in

Table 4 below, from which it is evident that a Granger causality exists. This means that gold and DWJ can in fact predict the values of the Bitcoin, although a set of more complex interactions between the three variables may exist, described by many other variables that are not used in the model.

5. Discussion and Conclusions

In this study, three alternative investment options were compared: Bitcoin cryptocurrency price, gold price, and the Dow Jones stock index level. Daily data from three distinct periods are utilized, with each period spanning four years. The first period, from October 2014 to September 2018, marked the initiation of official cryptocurrency price data. The second period, from October 2018 to May 2022, aimed to capture more recent trends before the effects of COVID-19 were fully embedded, and the third period, from January 2020 to December 2023, is the whole COVID-19 period with the initiation, embedded and terminal phases. Classical inductive statistical methods (descriptive, correlations, multiple linear regression) as well as time series analysis methods (autocorrelation, cross-correlation, Granger causality tests, ARIMA modeling) were used to analyze the data.

From the various analyses carried out, we found a causal effect from the DWJ and gold on Bitcoin. The intensity of the effect relationship is sensitive and varies depending on the type of analysis and the chosen statistical model. It is noted that the meaning given to causality is not causality in general (“x causes y”; this is a philosophical question) but a causality in the sense of Granger causality (“x forecasts y”). Differences are also observed both in the intensity of the effects and in the model of the effects between the three time periods of the examined data, especially between the COVID-19 period and the other two periods. In the first period of study, the effects acquire a more complex character with the participation and effects from the DWJ, demonstrating that Bitcoin acquires a character of a stock market product. In the second period, the predictive effects on Bitcoin mainly come from gold, demonstrating that in that period Bitcoin had a more monetary character. In the third period, the main characteristic of the prediction model is the short-term time prediction window; this means that the regression model mainly consists of short-term lags and differences. To sum-up, gold and the DWJ can forecast Bitcoin in a time horizon of some days, and the possible addition of more predictive variables (model enriching) may extend the goodness of fit of such predictions. Our finding regarding the effects of gold and the time-dependent asymmetry of these effects are in accordance with [

30,

31], in terms of the gold effects.

When discussing the limitations and practical implications of a predictive ARIMA model for Bitcoin using gold and the DWJ as predictors, it is important to consider both the theoretical aspects of the model and the real-world applicability of the findings. Hence, in light of the findings of the present study, the following considerations should be noted. (a) Data sensitivity and volatility: Bitcoin and other cryptocurrencies are known for their high volatility, which can be influenced by factors not traditionally associated with financial markets, such as technological changes, regulatory news, and social media. The inclusion of gold and the DWJ as predictors might not capture the full scope of variables affecting Bitcoin. (b) Stationarity assumption: ARIMA models require the time series to be stationary. While differentiation and integration can help achieve stationarity, the dynamic and evolving nature of cryptocurrency markets might make it challenging to maintain this assumption over time. (c) External factors and black swan events: The model might not account for unexpected ‘black swan’ events or sudden changes in external factors (e.g., geopolitical events, sudden regulatory changes) that can significantly impact Bitcoin. Therefore, further research could focus on further enhancing the predictive model using financial, technological, etc., variables to meet these considerations. Furthermore, future research could also extend to comparing the findings of this model to alternative ones (i.e., like DCC-GARCH employed by [

32]) for the same time periods).

Given the interconnectedness found in the model, the results may imply that investors wishing to diversify their holdings should consider Bitcoin in addition to more conventional assets, like stocks and gold. In this instance, the diversification strategy of the portfolio incorporates Bitcoin. Investors and portfolio managers can more effectively manage risk and protect themselves from market downturns by having a better understanding of the relationship between Bitcoin prices and traditional financial markets (through gold and the DWJ). Furthermore, the relationship between the price of Bitcoin and conventional assets may function as a gauge for overall market sentiment, offering insights into investor confidence and risk tolerance under various market circumstances. Traders may enhance trade execution and profitability by utilizing the model’s insights to create algorithmic trading strategies that take advantage of gold and the DWJ’s predictive power over Bitcoin prices. Finally, the findings might inform policymakers and regulators about the interconnectedness of digital and traditional financial markets, guiding the development of policies that ensure market stability and protect investors.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}