Impact of COVID-19 Movement Restrictions on Mobile Financing Services (MFSs) in Bangladesh

Abstract

:1. Introduction

2. Literature Review

Structure of MFSs in Bangladesh

3. Methodology

Data and Variable Selection

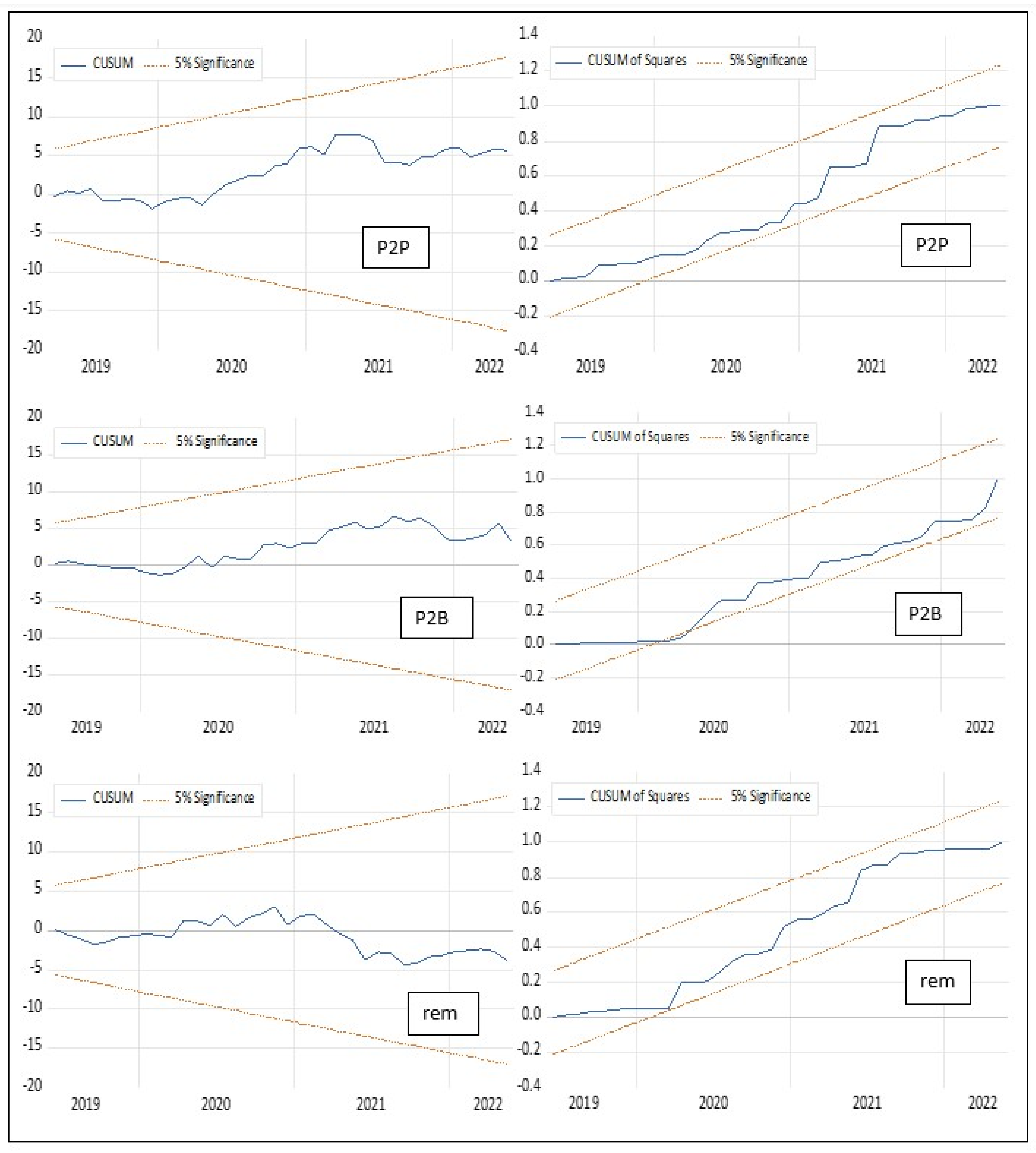

4. Empirical Results

5. Conclusions

Limitations

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Serial No | Name of the Business Entity | Name of the MFS Service |

|---|---|---|

| 1 | Dutch Bangla Bank Ltd. | ROCKET |

| 2 | bKash Ltd. | bKash |

| 3 | Mercantile Bank Ltd. | MYCash |

| 4 | Islami Bank Bangladesh Ltd. | Islami Bank mCash |

| 5 | Trust Axiata Digital Ltd. | Trust Axiata pay:tap |

| 6 | First Security Islami Bank Ltd. | FSIBL FirstPay |

| 7 | UCB Fintech Company Ltd. | Upay (উপায়) |

| 8 | One Bank Ltd. | OK Wallet |

| 9 | Rupali Bank Ltd. | Rupali Bank |

| 10 | Southeast Bank Ltd. | TeleCash |

| 11 | Al-Arafah Islami Bank Ltd. | Islamic Wallet |

| 12 | Meghna Bank Ltd. | Meghna Bank |

| 13 | Bangladesh Post Office (with interim approval of Bangladesh Bank) | Nagad |

| Series | Level | First Difference |

|---|---|---|

| −0.931 | −15.502 *** | |

| −1.070 | −9.804 *** | |

| −0.889 | −7.939 *** | |

| −0.084 | −9.488 *** | |

| −0.865 | −9.581 *** | |

| 1.072 | −4.276 *** | |

| −2.356 | −11.196 *** |

| Models | Dependent Variable | F-Statistics | Cointegration |

|---|---|---|---|

| Model 1 | P2Pt | F = 3.862 t = −2.895 | Yes |

| lnM2t | F = 9.608 t = −4.918 | Yes | |

| IPIt | F = 10.582 t = −4.900 | Yes | |

| Model 2 | P2Bt | F = 8.214 t = −4.556 | Yes |

| lnM2t | F = 2.272 t = −2.072 | No | |

| IPIt | F = 12.126 t = −5.306 | Yes | |

| Model 3 | remt | F = 4.272 t = −2.898 | Yes |

| lnM2t | F= 2.658 t = −2.172 | No | |

| IPIt | F = 11.497 t = −5.798 | Yes |

References

- Demirgüç-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S. The Global Findex Database 2021: Financial Inclusion, Digital Payments, and Resilience in the Age of COVID-19; World Bank: Washington, DC, USA, 2022; Available online: https://openknowledge.worldbank.org/bitstream/handle/10986/37578/9781464818974.pdf (accessed on 15 December 2022).

- Medhi, I.; Ratan, A.; Toyama, K. Mobile-Banking Adoption and Usage by Low-Literate, Low-Income Users in the Developing World. In Proceedings of the International Conference on Internationalization, Design and Global Development, San Diego, CA, USA, 19–24 July 2009; Springer: Berlin/Heidelberg, Germany, 2009; pp. 485–494. [Google Scholar] [CrossRef]

- Nabi, M.G.; Talukder, M.S.; Saha, P.P.; Sutradhar, R.R.; Ayesha-E-Fahmida; Chen, G.; Banerjee, S. Mobile Financial Services in Bangladesh: An Overview of Market Development; Bangladesh Bank: Dhaka, Bangladesh, 2012; Available online: https://www.bb.org.bd/pub/research/policypaper/pp072012.pdf (accessed on 12 January 2023).

- Siddik, M.N.; Sun, G.; Yanjuan, C.U.; Kabiraj, S. Financial inclusion through mobile banking: A case of Bangladesh. J. Appl. Financ. Bank. 2014, 4, 109–136. [Google Scholar]

- Okeleke, K. Achieving Mobile-Enabled Digital Inclusion in Bangladesh; GSMA: London, UK, 2021; Available online: https://www.gsma.com/mobilefordevelopment/wp-content/uploads/2021/03/Achieving-mobile-enabled-digital-inclusion-in-Bangladesh.pdf (accessed on 3 August 2023).

- Ouma, S.A.; Odongo, T.M.; Were, M. Mobile financial services and financial inclusion: Is it a boon for savings mobilization? Rev. Dev. Financ. 2017, 7, 29–35. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, A.; Klapper, L.F. Measuring Financial Inclusion: The Global Findex Database; Volume Policy Research Working Paper 6025; World Bank: Washington, DC, USA, 2012. [Google Scholar]

- Demirgüç-Kunt, A.; Singer, D. Financial Inclusion and Inclusive Growth: A Review of Recent Empirical Evidence; World Bank Policy Research Working Paper 8040; World Bank: Washington, DC, USA, 2017. [Google Scholar]

- Kanobe, F.; Alexander, P.M.; Bwalya, K.J. Policies, Regulations and Procedures and their Effects on Mobile Money Systems in Uganda. Electron. J. Inf. Syst. Dev. Ctries. 2017, 83, 1–15. [Google Scholar] [CrossRef]

- Ministry of Finance. Financial Institutions Division: National Financial Inclusion Strategy-Bangladesh (NFIS-B); Ministry of Finance, Government of Bangladesh: Dhaka, Bangladesh, 2021. Available online: https://fid.portal.gov.bd/sites/default/files/files/fid.portal.gov.bd/notices/43182ae2_205c_417f_919f_172c5cb60566/Final-Submitted%20to%20FID_NFIS-B-v2.doc (accessed on 10 September 2022).

- BTRC. Annual Report 2020–2021; Bangladesh Telecommunication Regulatory Commission: Dhaka, Bangladesh, 2021. Available online: http://www.btrc.gov.bd/site/view/annual_reports/Annual-Report (accessed on 12 December 2022).

- Rohanifar, Y.; Sultana, S.; Nandy, S.; Saha, P.; Chowdhury, M.J.H.; Al-Ameen, M.N.; Ahmed, S.I. The Role of Intermediaries, Terrorist Assemblage, and Re-skilling in the Adoption of Cashless Transaction Systems in Bangladesh. In Proceedings of the ACM SIGCAS/SIGCHI Conference on Computing and Sustainable Societies (COMPASS), Seattle, WA, USA, 29 June–1 July 2022; pp. 266–279. [Google Scholar] [CrossRef]

- Pieal, J.; Hossain, M. ‘Cashless Dhaka’ Still a Far Cry. The Business Standard, 3 July 2023. Available online: https://www.tbsnews.net/features/panorama/cashless-dhaka-still-far-cry-659026 (accessed on 5 July 2023).

- Hossain, M.; Chowdhury, T. COVID-19, Fintech, and the Recovery of Micro, Small, and Medium-Sized Enterprises: Evidence from Bangladesh; ADBI Working Paper 1305; Asian Development Bank Institute: Chiyoda-ku, Japan, 2022; Available online: https://www.adb.org/publications/covid-19-fintech-and-the-recovery-of-micro-small-and-medium-sized-enterprises-evidence-from-bangladesh (accessed on 12 July 2023).

- Deloitte. Impact of the COVID-19 Crisis on Short-and Medium-Term Consumer Behavior; Deloitte: London, UK, 2020; Issue 06/2020; Available online: https://www2.deloitte.com/content/dam/Deloitte/de/Documents/consumer-business/Impact%20of%20the%20COVID-19%20crisis%20on%20consumer%20behavior.pdf (accessed on 8 July 2021).

- Bangladesh Bank. Mobile Financial Services (MFS) Comparative Summary Statement of March 2021 and April 2021. Available online: https://www.bb.org.bd/fnansys/paymentsys/mfsdata.php (accessed on 10 September 2022).

- Andersson-Manjang, S.K.; Nika, N. The State of the Industry Report on Mobile Money 2021; GSMA: London, UK, 2021; Available online: https://www.gsma.com/mobilefordevelopment/wp-content/uploads/2021/03/GSMA_State-of-the-Industry-Report-on-Mobile-Money-2021_Full-report.pdf (accessed on 12 December 2022).

- Demirguc-Kunt, A.; Klapper, L.; Singer, D.; Ansar, S.; Hess, J. The Global Findex Database 2017: Measuring Financial Inclusion and the Fintech Revolution; World Bank: Washington, DC, USA, 2018. [Google Scholar]

- Ahmad, A.H.; Green, C.; Jiang, F. Mobile Money, Financial Inclusion and Development: A Review with Reference to African Experience. J. Econ. Surv. 2020, 34, 753–792. [Google Scholar] [CrossRef]

- Loh, X.-M.; Lee, V.-H.; Hew, T.-S.; Lin, B. The cognitive-affective nexus on mobile payment continuance intention during the COVID-19 pandemic. Int. J. Bank Mark. 2022, 40, 939–959. [Google Scholar] [CrossRef]

- Ramasamy, S.; Guru, B.K.; Nair, M.; Vaithilingam, S. Development of E-Money in Malaysia. Econ. Bull. 2006, 8, 135–148. [Google Scholar]

- Lee, Y.-K.; Park, J.-H.; Chung, N.; Blakeney, A. A unified perspective on the factors influencing usage intention toward mobile financial services. J. Bus. Res. 2012, 65, 1590–1599. [Google Scholar] [CrossRef]

- Chemingui, H.; Ben Lallouna, H. Resistance, motivations, trust and intention to use mobile financial services. Int. J. Bank Mark. 2013, 31, 574–592. [Google Scholar] [CrossRef]

- Shakouri, G.H.; Kazemi, A. Selection of the best ARMAX model for forecasting energy demand: Case study of the residential and commercial sectors in Iran. Energy Effic. 2015, 9, 339–352. [Google Scholar] [CrossRef]

- Ozili, P.K. Financial Inclusion and Fintech during COVID-19 Crisis: Policy Solutions. Co. Lawyer J. 2020, 8. [Google Scholar] [CrossRef]

- Yamada, E.; Satoshi, S.; Enerelt, M. The COVID-19 pandemic, remittances and financial inclusion in the Philippines. Philipp. Rev. Econ. 2021, 57, 18–41. [Google Scholar] [CrossRef]

- Pesaran, M.H.; Shin, Y.; Smith, R.J. Bounds testing approaches to the analysis of level relationships. J. Appl. Econom. 2001, 16, 289–326. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Alamoudi, H.; Alharthi, M.; Glavee-Geo, R. Advances in mobile financial services: A review of the literature and future research directions. Int. J. Bank Mark. 2022, 41, 1–33. [Google Scholar] [CrossRef]

- Fernandes, C.; Borges, M.R.; Caiado, J. The contribution of digital financial services to financial inclusion in Mozambique: An ARDL model approach. Appl. Econ. 2020, 53, 400–409. [Google Scholar] [CrossRef]

- Abdul Mannan, K.; Farhana, K.M. Digital Financial Inclusion and Remittances: An Empirical Study on Bangladeshi Migrant Households. FinTech 2023, 2, 680–697. [Google Scholar] [CrossRef]

- Morawczynski, O. Examining the Usage and Impact of Transformational M-Banking in Kenya; Springer: Berlin/Heidelberg, Germany, 2009; pp. 495–504. [Google Scholar]

- Kim, M.; Zoo, H.; Lee, H.; Kang, J. Mobile financial services, financial inclusion, and development: A systematic review of academic literature. Electron. J. Inf. Syst. Dev. Ctries. 2018, 84, e12044. [Google Scholar] [CrossRef]

- Blaise, N.; Kosgei, M. Mobile Banking and Financial Inclusion in Burundi. IOSR J. Econ. Financ. 2021, 12, 60–68. [Google Scholar]

- Lee, J.N.; Morduch, J.; Ravindran, S.; Shonchoy, A.; Zaman, H. Poverty and Migration in the Digital Age: Experimental Evidence on Mobile Banking in Bangladesh. Am. Econ. J. Appl. Econ. 2021, 13, 38–71. [Google Scholar] [CrossRef]

- Noyon, A.U. The Digital Money Magic in Rural Economy. The Business Standard, 9 December 2023. Available online: https://www.tbsnews.net/economy/digital-money-magic-rural-economy-754058 (accessed on 10 December 2023).

- Parvez, J.; Islam, A.; Woodard, J. Mobile Financial Services in Bangladesh: A Survey of Current Services, Regulations, and Usage in Select USAID Projects; mStar: Dhaka, Bangladesh, 2015; Available online: https://www.marketlinks.org/sites/default/files/resource/files/MFSinBangladesh_April2015.pdf (accessed on 12 July 2022).

- Bangladesh Bank. List of MFS Providers; Bangladesh Bank: Dhaka, Bangladesh, 2023; Available online: https://www.bb.org.bd/fnansys/paymentsys/mfs_provider.pdf (accessed on 30 July 2023).

- Sayilgan, G.; Yildirim, O. Determinants of profitability in Turkish banking sector: 2002–2007. Int. Res. J. Financ. Econ. 2009, 28, 207–214. [Google Scholar]

- Cheung, Y.W.; Lai, K.S. Lag Order and Critical Values of the Augmented Dickey-Fuller Test. J. Bus. Econ. Stat. 1995, 13, 277–280. [Google Scholar]

- Sanz, F.P.; Mersland, R.; de Lima, P. The uptake of mobile financial services in the Middle East and North Africa region. Enterp. Dev. Microfinance 2013, 24, 295–310. [Google Scholar] [CrossRef]

- Narayan, P.K. Fiji’s Tourism Demand: The ARDL Approach to Cointegration. Tour. Econ. 2016, 10, 193–206. [Google Scholar] [CrossRef]

- World Bank. Financial Inclusion. 2017. Available online: https://www.worldbank.org/en/topic/financialinclusion/overview#1 (accessed on 1 August 2023).

- Honohan, P. Financial Development, Growth, and Poverty: How Close are the Links? World Bank: Washington, DC, USA, 2004; Available online: http://hdl.handle.net/10986/14439 (accessed on 5 August 2022).

- Sarma, M. Index of Financial Inclusion; Indian Council for Research on International Economic Relations (ICRIER): New Delhi, India, 2008; Working Paper No. 215; Available online: http://hdl.handle.net/10419/176233 (accessed on 12 December 2022).

- Rashid, S. Impact of COVID-19 on Selected Criminal Activities in Dhaka, Bangladesh. Asian J. Criminol. 2021, 16, 5–17. [Google Scholar] [CrossRef] [PubMed]

- Adhitya, A.; Sembel, H.R. The impacts of mobile banking technology adoption on the financial performance and stock performance of big banks in Indonesia. South East Asia J. Contemp. Bus. Econ. Law 2020, 22, 63–73. [Google Scholar]

- Nkoro, E.; Uko, A.K. Autoregressive Distributed Lag (ARDL) cointegration technique: Application and interpretation. J. Stat. Econom. Methods 2016, 5, 63–91. [Google Scholar]

- Aziz, A.; Naima, U. Rethinking digital financial inclusion: Evidence from Bangladesh. Technol. Soc. 2021, 64. [Google Scholar] [CrossRef]

- Brown, R.; Durbin, J.; Evans, J. Techniques for testing the constancy of regression relationships over time. J. R. Stat. Soc. Ser. B (Methodol.) 1975, 37, 149–163. [Google Scholar] [CrossRef]

- Bangladesh Bank. Bangladesh Mobile Financial Services (MFS) Regulations, 2022. Available online: https://www.bb.org.bd/mediaroom/circulars/psd/feb152022psd04e.pdf (accessed on 27 December 2022).

- United Nations. Evidence-Based E-Government Policies for Advancing Governmental Service Delivery and Accountability in Support of the Sustainable Development Goals; United Nations Department of Economic and Social Affairs (UN DESA): New York, NY, USA, 2019; Available online: https://capacity.desa.un.org/node/3160 (accessed on 28 September 2022).

- Changchit, C.; Lonkani, R.; Sampet, J. Mobile banking: Exploring determinants of its adoption. J. Organ. Comput. Electron. Commer. 2017, 27, 239–261. [Google Scholar] [CrossRef]

- Ortega, D. Cash or Bytes? Garment Workers’ Payment Preferences; BRAC Institute of Governance & Development: Dhaka, Bangladesh, 2021; Available online: https://bigd.bracu.ac.bd/cash-or-bytes-garment-workers-payment-preferences/ (accessed on 12 December 2022).

- UNCDF. Inclusive Digital Payments Solutions for the Garment Sector Workers in Bangladesh; Women’s World Banking: New York, NY, USA, 2020; Available online: https://www.womensworldbanking.org/insights/inclusive-digital-payments-solutions-for-the-garment-sector-workers-in-bangladesh/ (accessed on 5 August 2023).

- Ali, S. Global Findex 2021: How Digital Wages Empower Bangladeshi Women; Bill & Melinda Gates Foundation: Seattle, WA, USA, 2022; Available online: https://www.gatesfoundation.org/ideas/articles/2021-findex-report-financial-inclusion-benefits-bangladeshi-women (accessed on 25 September 2022).

- Hasan, M.T. Digital Financial Inclusion of Marginalised People. 2022. Available online: https://a2i.gov.bd/digital-financial-inclusion-of-marginalised-people/ (accessed on 14 January 2023).

- TBS Report. MFS Accelerated Financial Inclusion in Pandemic. The Business Standard, 12 March 2022. Available online: https://www.tbsnews.net/economy/banking/mfs-accelerated-financial-inclusion-pandemic-383911 (accessed on 12 December 2022).

- McCaffrey, M. Does Mobile Money Improve Financial Inclusion? United Nations Capital Development Fund (UNCDF): New York, NY, USA,, 2022; Available online: https://www.uncdf.org/article/7809/does-mobile-money-improve-financial-inclusion (accessed on 8 October 2022).

- TBS Report. Cenbank Doubles Limit for Sending Remittances to MFS Accounts. The Business Standard, 6 December 2023. Available online: https://www.tbsnews.net/economy/bangladesh-bank-doubles-limit-sending-remittances-through-mfs-752826 (accessed on 7 December 2023).

- Khan, B. Govt to Set up Expats’ Centres in 36 Countries. The Daily Star, 15 December 2023. Available online: https://www.thedailystar.net/news/bangladesh/news/govt-set-expats-centres-36-countries-3494771 (accessed on 16 December 2023).

| Variable | Definition, Mean and Standard Deviation for the Period December 2016 to May 2022 | Source | |

|---|---|---|---|

| Dependent variable for Model 1 | Natural log of the person-to-person transaction (in million BDT) in month t Mean (S.D): 11.15 (0.5473) | Bangladesh Bank | |

| Natural log of utility payments (in million BDT) in month t Mean (S.D): 8.219 (0.558) | Bangladesh Bank | ||

| Natural log of inward remittances (in million BDT) in month t Mean (S.D): 5.612 (1.185) | Bangladesh Bank | ||

| Dependent variable for Model 2 | atmVt | Natural log of monthly volume of ATM transactions throughout the country. Mean (S.D): 7.313 (0.616) | Bangladesh Bank |

| Control variables for Models 1 and 2 | Natural log of money supply (M2) (in million BDT) in month t Mean (S.D): 16.286 (0.139) | Bangladesh Bank | |

| Labor Wage Index in month t Mean (S.D): 161.88 (12.84) | Bangladesh Bureau of Statistics (BBS) | ||

| Natural log of the number of total agents providing MFSs in month t Mean (S.D): 13.695 (0.126) | Bangladesh Bank | ||

| General industrial production index for the month t. Mean (S.D): 406.57 (72.12533) | Bangladesh Bureau of Statistics (BBS) | ||

| A dummy variable with a value of 1 for the month when the nationwide lockdown was in place, and 0 otherwise. Mean (S.D): 0.226 (0.126) | N/A | ||

| A dummy variable taking the value 1 for a month if the month contains any major religious and cultural festivals like Eid and Puja festivals in that year and is 0 otherwise. Mean (S.D): 0.226 (0.126) | N/A | ||

| The number of observations. N = 66 | |||

| Variables | |||

|---|---|---|---|

| Industrial Production Index (IPI) | 0.000456 (0.22) | 0.00163 * (0.67) | −0.0117 (−1.48) |

| Money supply (lnM2) | 4.644 ** (2.03) | 7.232 ** (2.62) | −0.5233 (−0.59) |

| Agents | −3.193 ** (−2.26) | −1.463 (−0.62) | 7.9126 * (0.85) |

| Wage Index | 0.0271 (1.01) | 0.02682 (0.96) | 0.0390 (0.15) |

| Movement restriction (dummy) | 0.175 ** (2.05) | 0.06232 * (0.66) | 0.1473 (1.14) |

| Festivals (dummy) | 0.1308 (1.36) | 0.1643 (1.82) | 0.2413 (0.61) |

| Variable | |||

|---|---|---|---|

| −0.4669 *** (−3.31) | |||

| 0.001227 *** (3.01) | 0.00108 (1.44) | 0.00755 (0.46) | |

| 0.00044 (1.25) | 0.000245 (0.19) | ||

| 1.7631 (1.02) | 1.413 (0.56) | ||

| −1.8158 (−1.20) | |||

| 0.8042 (0.76) | 1.887 (0.82) | ||

| 0.2888 (0.31) | 1.4332 (0.71) | ||

| 0.0751 * (1.43) | −0.20078 ** (−2.15) | ||

| −0.0327 (−1.25) | −0.2408 *** (−3.99) | ||

| 0.06778 *** (2.66) | 0.1458 (0.96) | 0.11305 * (1.08) | |

| 0.09998 ** (2.06) | 0.199 ** (2.39) | ||

| −0.383 ** (−2.23) | −0.635 *** (−3.11) | −0.2385 ** (−2.60) | |

| Constant | 9.4709 (0.68) | −57.575 ** (−2.52) | −45.976 (−1.16) |

| Adj R2 | 0.6861 | 0.6252 | 0.5628 |

| Log likelihood | 81.0178 | 46.362 | 31.5729 |

| DW test | 2.1808 | 2.092 | 1.985 |

| 61.84 | 62.05 | 58.24 |

| Dependent Variable: Volume of ATM Transactions (in Log) | |||

|---|---|---|---|

| Model 1 | Model 2 | Model 3 | |

| P2P | 0.0634 * (0.2228) | ||

| P2B | 0.38005 *** (0.13094) | ||

| Rem | 0.07719 * (0.04463) | ||

| DC19 | −4.3469 * (1.6272) | −3.0521 *** (1.1118) | −1.0389 *** (0.37756) |

| P2P*DC19 | 0.3993 *** (0.14117) | ||

| P2B*DC19 | 0.3852 *** (0.1283) | ||

| Rem*DC19 | 0.21756 *** (0.059063) | ||

| IPI | 0.00187 *** (0.000577) | 0.001922 *** (0.000586) | 0.000906 * (0.0005208) |

| Dfest | 0.000723 (0.04153) | 0.01322 (0.03936) | 0.01024 (0.03478) |

| Agents | 3.1939 * (1.2115) | −2.567 ** (1.0525) | 2.901 *** (1.020) |

| wageIndex | 0.0453 (0.0123) | 0.05839 *** (0.01322) | 0.04053 *** (0.0102) |

| M2(log) | 1.4817 (1.8895) | −1.9855 (1.5985) | 2.3933 * (1.1990) |

| Constant | 19.447 * (9.836) | 61.3557 *** (20.4287) | 1.4658 (14.940) |

| N | 66 | 66 | 66 |

| Adj-R2 | 0.9411 | 0.9834 | 0.9569 |

| F-statistic | 125.09 *** | 130.78 *** | 181.28 *** |

| Root MSE | 0.12803 | 0.15283 | 0.14965 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Rashid, S. Impact of COVID-19 Movement Restrictions on Mobile Financing Services (MFSs) in Bangladesh. FinTech 2024, 3, 1-16. https://doi.org/10.3390/fintech3010001

Rashid S. Impact of COVID-19 Movement Restrictions on Mobile Financing Services (MFSs) in Bangladesh. FinTech. 2024; 3(1):1-16. https://doi.org/10.3390/fintech3010001

Chicago/Turabian StyleRashid, Sungida. 2024. "Impact of COVID-19 Movement Restrictions on Mobile Financing Services (MFSs) in Bangladesh" FinTech 3, no. 1: 1-16. https://doi.org/10.3390/fintech3010001

APA StyleRashid, S. (2024). Impact of COVID-19 Movement Restrictions on Mobile Financing Services (MFSs) in Bangladesh. FinTech, 3(1), 1-16. https://doi.org/10.3390/fintech3010001