Customers’ Satisfaction of E-Banking in Bangladesh: Do Service Quality and Customers’ Experiences Matter?

Abstract

:1. Introduction

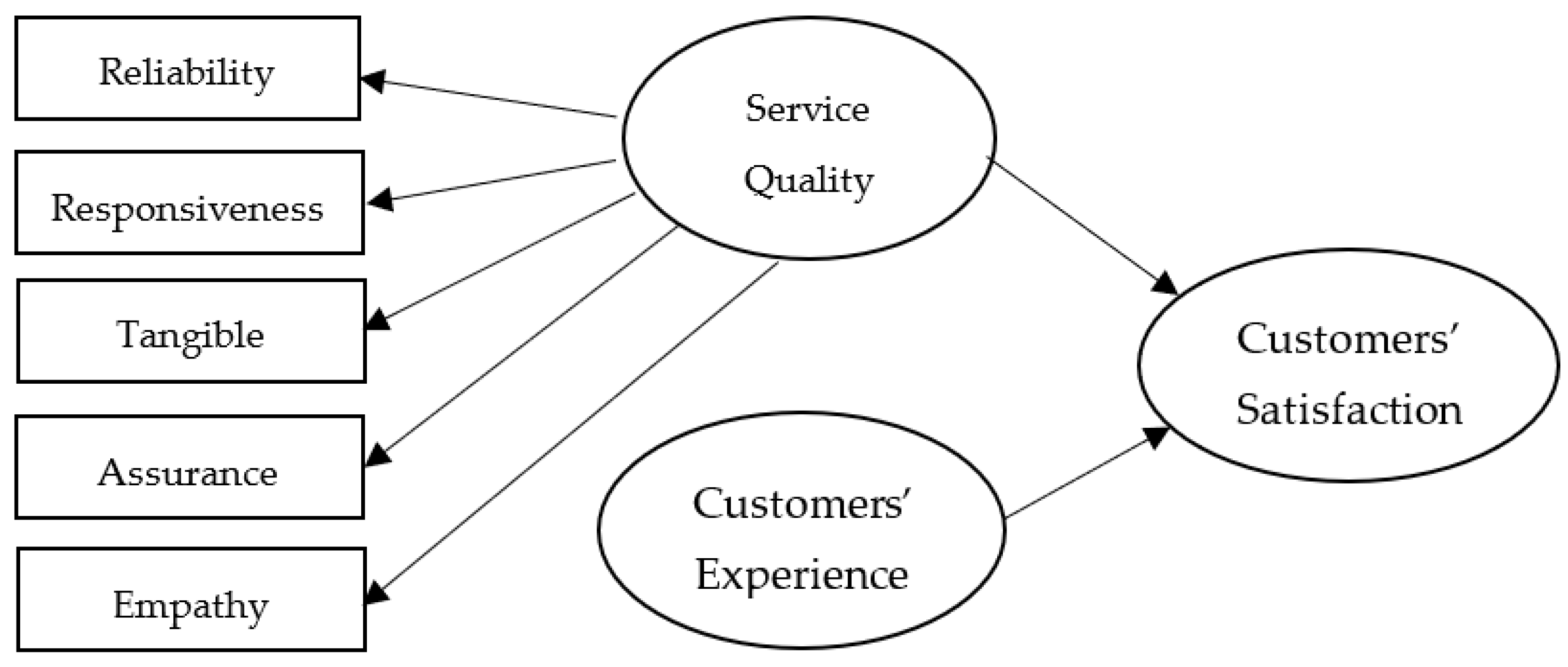

2. Research Framework and Development of Hypotheses

3. Research Methodology

3.1. Sampling Technique and Sample Size

3.2. Research Variables with Sources

3.3. Statistical Tools

4. Analyses and Findings

4.1. Preliminary Analysis

4.2. Demographic and Descriptive Findings

4.2.1. Demographic Findings

4.2.2. Descriptive Findings

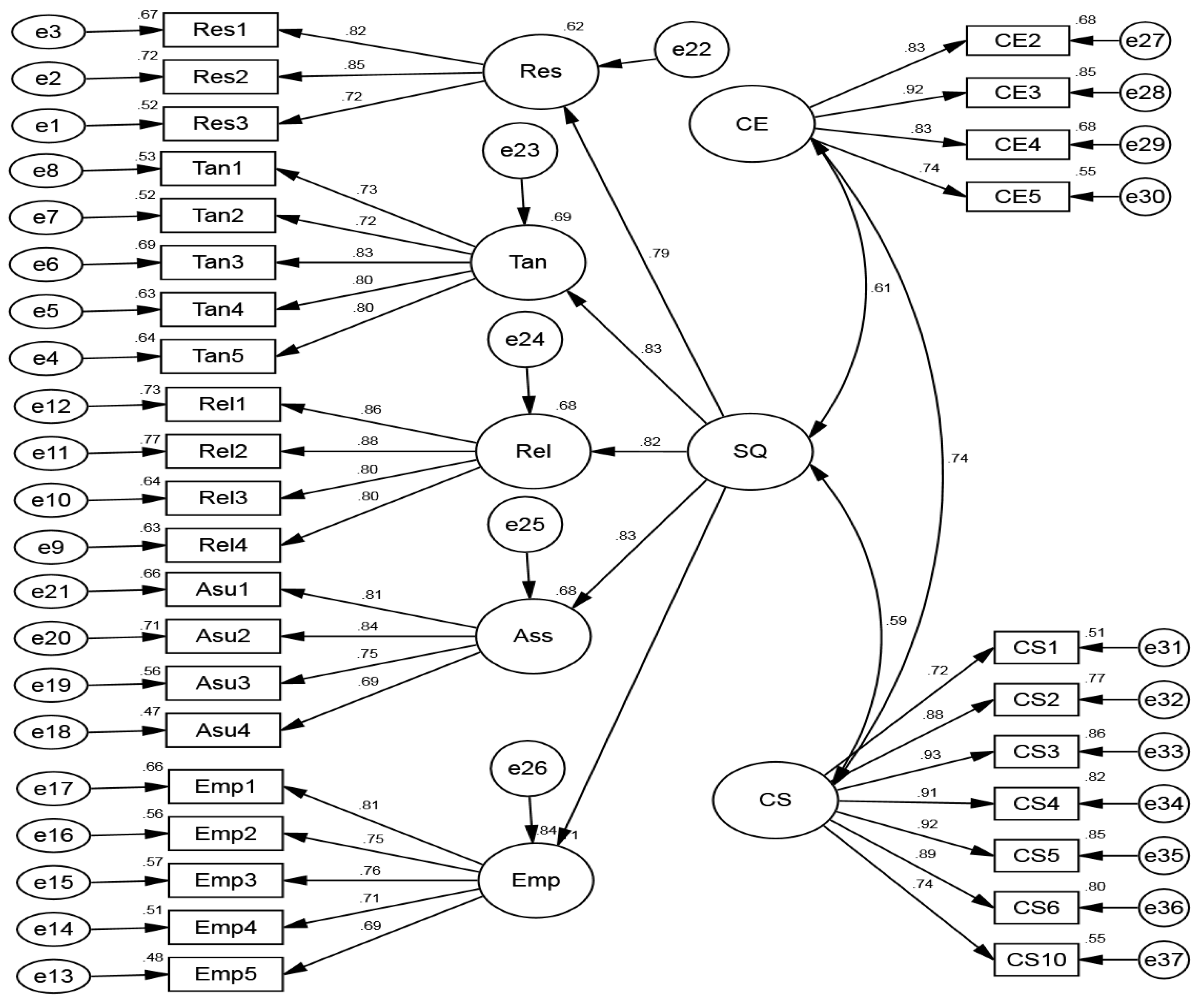

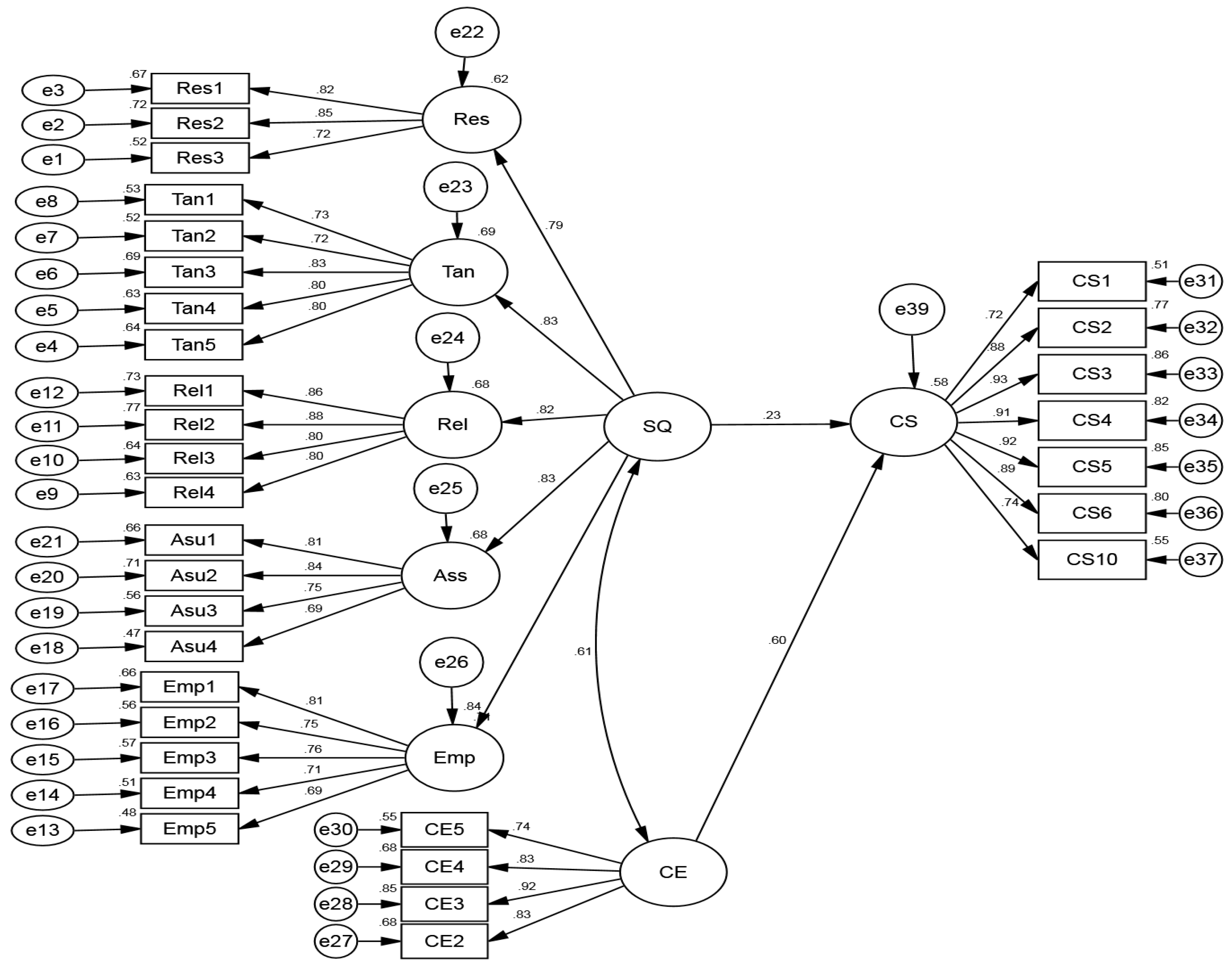

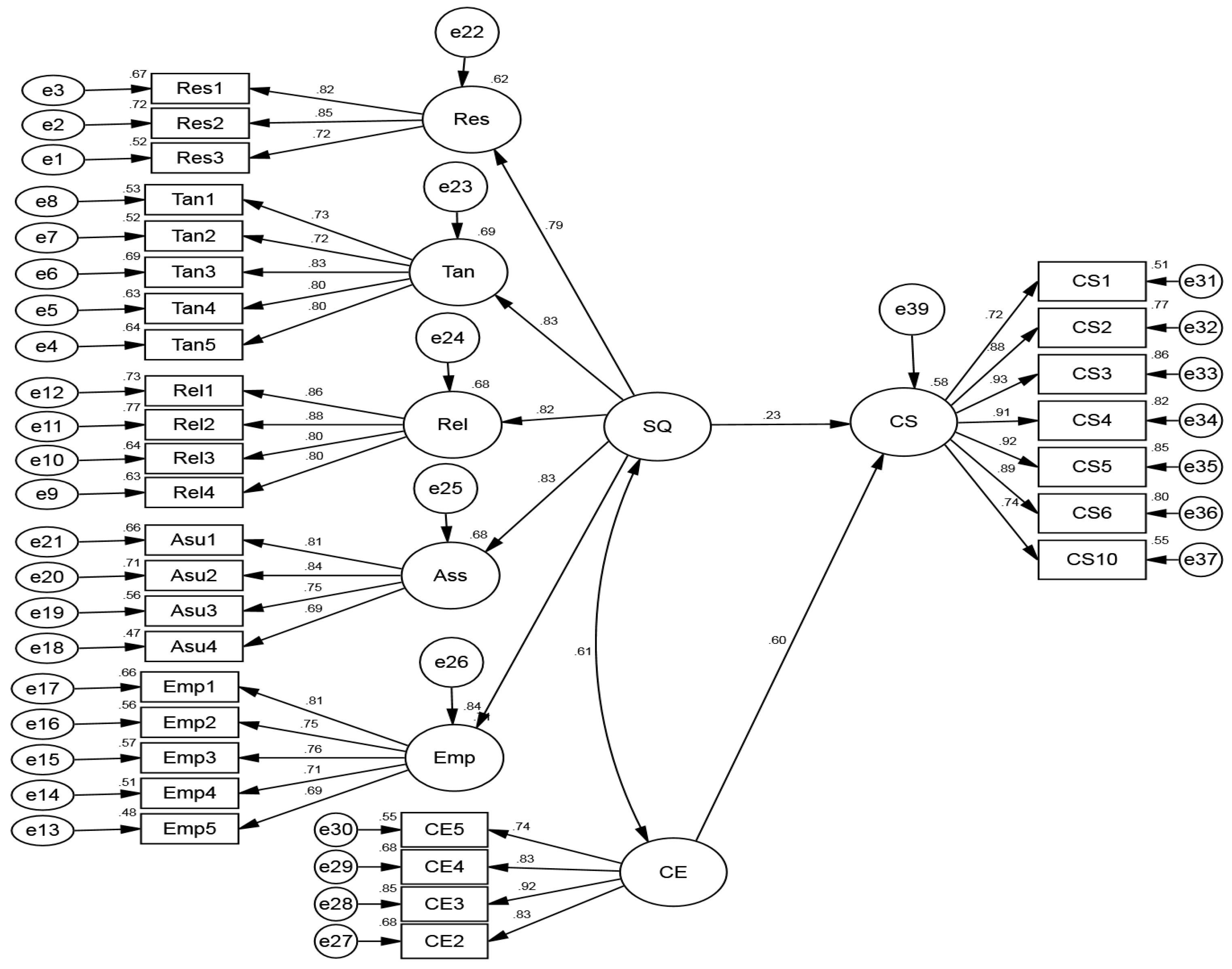

4.3. Measurement and Structural Models

4.3.1. Measurement Model

4.3.2. Structural Model

5. Discussion of the Findings

6. Contributions

6.1. Theoretical Contributions

6.2. Practical Contributions

7. Conclusions and Areas for Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Khan, M.R.; Rana, S.; Hosen, M.I. Impact of trustworthiness on the usage of m-banking apps: A study on Bangladeshi consumers. Bus. Perspect. Res. 2022, 10, 234–250. [Google Scholar] [CrossRef]

- Bangladesh Bank. 2022. Available online: https://www.bb.org.bd/en/index.php/financialactivity/bankfi (accessed on 22 March 2022).

- Rahaman, M.S.; Uddin, M.J.; Rahman, M.M.; Samuel, A.B. Commercial bank employees’ job burnout: Hope or hype? Int. J. Bus. Glob. 2023, 33, 444–467. [Google Scholar] [CrossRef]

- Rahaman, M.S.; Rahman, M.M. Effects of burnout on intention to leave by public banking sector in Bangladesh. Int. J. Public Sect. Perform. Manag. 2023, 11, 108–122. [Google Scholar] [CrossRef]

- Anjum, N.; Rahaman, M.S.; Choudhury, M.I.; Rahman, M.M. An Insight into Green HRM Practices for Sustainable Workplace in the Banking Sector of Bangladesh: The Role of Electronic HRM. J. Bus. Strategy Financ. Manag. 2022, 4, 66. [Google Scholar] [CrossRef]

- Rahman, M.M.; Abdul, M.; Ali, N.A.; Uddin, M.J.; Rahman, M.S. Employees’ Retention Strategy on Quality of Work Life (QWL) Dimensions of Private Commercial Banks in Bangladesh. Pertanika J. Soc. Sci. Humanit. 2017, 25, 647–662. [Google Scholar]

- Business Standard. Available online: https://www.tbsnews.net/economy/bankingIU=Internetusers;IBU=Internetbanking-uses (accessed on 2 February 2023).

- Bashir, M.A.; Ali, M.H.; Reaz, M. Customer’s satisfaction towards E-banking in Bangladesh. Int. J. Adm. Gov. 2015, 1, 37–44. [Google Scholar]

- Ali, M.H.; Bashir, M.A.; Rahman, M.M.; Wai, L.M.; Rahman, M.A.; Hamid, A.B.A. Relationships between Service Quality, Customer Experience and Customer Satisfaction of E-Banking In Bangladesh. J. Adv. Res. Bus. Manag. Stud. 2019, 15, 23–32. [Google Scholar]

- Sadowska, B. Management accounting as an element of the integrated information system of an economic entity. Zesz. Teoretyczne Rachun. 2018, 98, 225–246. [Google Scholar] [CrossRef]

- Kaur, B.; Kiran, S.; Grima, S.; Rupeika-Apoga, R. Digital Banking in Northern India: The Risks on Customer Satisfaction. Risks 2021, 9, 209. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Al-Sartawi, A.; Hannoon, A.; Khalid, A.A. Information technology governance and online banking in Bahrain. In Proceedings of the Artificial Intelligence for Sustainable Finance and Sustainable Technology: Proceedings of ICGER, 1 January 2022; Springer International Publishing: Cham, Switzerland, 2022; pp. 611–618. [Google Scholar]

- Kumar, H.; Sofat, R. Digital payment and consumer buying behaviour-an empirical study on Uttarakhand, India. Int. J. Electron. Bank. 2022, 3, 337–357. [Google Scholar] [CrossRef]

- Bashir, M.A.; Ali, M.H.; Wai, L.M.; Hossain, M.I.; Rahaman, M.S. Mediating effect of customer perceived value on the relationship between service quality and customer satisfaction of E-Banking in Bangladesh. Int. J. Adv. Sci. Technol. 2020, 29, 3590–3606. [Google Scholar]

- Roy, S.K.; Khan, M.R.; Hossain, S.M.K. Determinants of users’ satisfaction regarding mobile operators in Bangladesh: An exploratory factor analysis approach on university students. Eur. J. Bus. Manag. 2016, 8, 31–39. [Google Scholar]

- Bhambra, R.K. Adoption of online banking in Goa amidst the pandemic. Int. J. Electron. Bank. 2022, 3, 163–175. [Google Scholar] [CrossRef]

- Kavitha, K. Mobile banking supervising system-issues, challenges and suggestions to improve mobile banking services. Adv. Comput. Sci. Int. J. 2015, 4, 65–67. [Google Scholar]

- Raza, S.A.; Shah, N.; Ali, M. Acceptance of mobile banking in Islamic banks: Evidence from. Modified UTAUT model. J. Islam. Mark. 2019, 10, 357–376. [Google Scholar] [CrossRef]

- Al Amin, M.; Arefin, M.S.; Alam, M.S.; Rasul, T.F. Understanding the predictors of rural customers’ continuance intention toward mobile banking services applications during the COVID-19 pandemic. J. Glob. Mark. 2022, 35, 324–347. [Google Scholar] [CrossRef]

- Prakash, A.; Mahajan, Y.; Gadekar, A. Adoption of mobile money among internal migrant workers during the corona pandemic in India: A study focused on moderation by mode of payments. Int. J. Electron. Bank. 2022, 3, 144–162. [Google Scholar] [CrossRef]

- Raji, A.A.; Zameni, A.; Mansur, M. Effect of Electronic Banking on Customer Satisfaction in Kwara State, Nigeria. Soc. Sci. 2021, 11, 1571–1585. [Google Scholar] [CrossRef]

- Bashir, M.A.; Ali, M.H. An integrative model of customer experience in Malaysia E-banking service delivery. Glob. Manag. Lit. 2015, 57–68. [Google Scholar]

- Al-Sartawi, A.; Al-Okaily, M.; Hannoon, A.; Khalid, A.A. Financial technology: Literature review paper. Artif. Intell. Sustain. Financ. Sustain. Technol. Proc. ICGER 2022, 2021, 194–200. [Google Scholar]

- Hossain, M.A.; Jahan, N.; Kim, M. A multidimensional and hierarchical model of banking services and behavioral intentions of customers. Int. J. Emerg. Mark. 2023, 18, 845–867. [Google Scholar] [CrossRef]

- Naeem, M.; Ozuem, W. The role of social media in internet banking transition during COVID-19 pandemic: Using multiple methods and sources in qualitative research. J. Retail. Consum. Serv. 2021, 60, 102483. [Google Scholar] [CrossRef]

- Gupta, N. Influence of demographic variables on synchronisation between customer satisfaction and retail banking channels for customers of public sector banks of India. Int. J. Electron. Bank. 2019, 1, 206–219. [Google Scholar] [CrossRef]

- Haque, M.A.; Urmee, G.; Ahsan, M.K. Credit Card: Changing the Buying Attitudes regarding Luxury Goods and Maintaining Quality of Living Standard, Asian Account. Audit. Adv. 2022, 13, 16–24. [Google Scholar]

- Czaja-Cieszyńska, H.; Lulek, A.; Sadowska, B. Informational Function of Accounting from the Perspective of Corporate Social Responsibility; Scientific Publishing House of the University of Szczecin: Szczecin, Poland, 2021. [Google Scholar]

- Parasuraman, A.; Zeithaml, V.; Berry, L. A conceptual model of service quality and its implications for future research. J. Mark. 1985, 49, 41–50. [Google Scholar] [CrossRef]

- Jahan, N.; Shahria, G. Factors effecting customer satisfaction of mobile banking in Bangladesh: A study on young users’ perspective. South Asian J. Mark. 2022, 3, 60–76. [Google Scholar] [CrossRef]

- Feng, L.; Hui, L.; Meiqian, H.; Kangle, C.; Mehdi, D. Customer satisfaction with bank services: The role of cloud services, security, e-learning and service quality. Technol. Soc. 2021, 64, 101487. [Google Scholar]

- Alam, M.J.; Jesmin, J.; Faruk, M.; Nur-Al-Ahad, M. Development of E-banking in Bangladesh: A Survey Study. Financ. Mark. Inst. Risks 2021, 5, 42–51. [Google Scholar] [CrossRef]

- Sarker, B.; Sarker, B.; Podder, P.; Robel, M.R.A. Progression of Internet Banking System in Bangladesh and its Challenges. Int. J. Comput. Appl. 2020, 177, 11–15. [Google Scholar] [CrossRef]

- Karim, M.M.; Bhuiyan, M.Y.A.; Nath, S.K.D.; Latif, W.B. Conceptual Framework of Recruitment and Selection Process. Int. J. Bus. Soc. Res. 2021, 11, 18–25. [Google Scholar]

- Munir, M.M.M.; Bishwas, P.C. Security: Challenge of E-banking Service Practice in Bangladesh. Jahangirnagar J. Bus. Stud. 2019, 8, 185–196. [Google Scholar]

- Davis, F.D. A Technology Acceptance Model for Empirically Testing New End-User Information Systems: Theory and Results. Ph.D. Thesis, Massachusetts Institute of Technology, Cambridge, MA, USA, 1985. [Google Scholar]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. 1989, 13, 319–339. [Google Scholar] [CrossRef]

- Venkatesh, V.; Davis, F.D. A model of the antecedents of perceived ease of use: Development and test. Decis. Sci. 1996, 27, 451–481. [Google Scholar] [CrossRef]

- Bitkina, O.V.; Park, J.; Kim, H.K. Measuring user-perceived characteristics for banking services: Proposing a methodology. Int. J. Environ. Res. Public Health 2022, 19, 2358. [Google Scholar] [CrossRef] [PubMed]

- Parasuraman, A.; Zeithaml, V.A.; Berry, L.L. SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. J. Retail. 1988, 64, 12–40. [Google Scholar]

- Khan, N.; Kadir, S.L.S.A. The impact of perceived value dimension on satisfaction and behavior intention: Young-adult consumers in banking industry. Afr. J. Bus. Manag. 2011, 5, 7055–7067. [Google Scholar]

- Obeng-Ayisi, E.; Quansah, C.; Mensah, R.O.; Acquah, A. An Investigation into Factors Impacting on Customer Decision to Adopt E-Banking: Viewpoints of GCB Customers. Tech. Soc. Sci. J. 2022, 33, 357–371. [Google Scholar] [CrossRef]

- Zeleke, S.; Chauhan, S. The Effect of Electronic Banking Service on Customer Satisfaction: Evidence From Commercial Banks Of Ethiopia Operating In Hawassa City Administration. J. Posit. Sch. Psychol. 2022, 6, 3228–3246. [Google Scholar]

- Torabi, M.; Bélanger, C.H. Influence of Online Reviews on Student Satisfaction Seen through a Service Quality Model. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 3063–3077. [Google Scholar] [CrossRef]

- Zeithaml, V.A. Services Marketing: Integrating Customer; Tata Mcgraw Hill: New York, NY, USA, 2011. [Google Scholar]

- Dam, S.M.; Dam, T.C. Relationships between Service Quality, Brand Image, Customer Satisfaction, and Customer Loyalty. J. Asian Financ. Econ. Bus. 2021, 8, 585–593. [Google Scholar]

- Begenau, J.; Landvoigt, T. Financial regulation in a quantitative model of the modern banking system. Rev. Econ. Stud. 2022, 89, 1748–1784. [Google Scholar] [CrossRef]

- Siddiqi, K.O. Interrelations between service qualities attributes, customer satisfaction and customer loyalty in the retail banking sector in Bangladesh. Int. J. Bus. Manag. 2011, 6, 12–25. [Google Scholar] [CrossRef]

- George, A.; Kumar, G.G. Impact of service quality dimensions in internet banking on customer satisfaction. Decision 2014, 41, 73–85. [Google Scholar] [CrossRef]

- Mamat, M.; Haron, M.S.; Razak, N.S.A. Personal interaction encounter, customer involvement, familiarity and customer service experience in Malaysian public universities. Procedia-Soc. Behav. Sci. 2014, 130, 293–298. [Google Scholar] [CrossRef]

- Kushwaha, A.K.; Kumar, P.; Kar, A.K. What impacts customer experience for B2B enterprises on using AI-enabled chatbots? Insights from Big data analytics. Ind. Mark. Manag. 2021, 98, 207–221. [Google Scholar] [CrossRef]

- Nguyen, H.V.; Vu, T.D.; Nguyen, B.K.; Nguyen, T.M.N.; Do, B.; Nguyen, N. Evaluating the Impact of E-Service Quality on Customer Intention to Use Video Teller Machine Services. J. Open Innov. Technol. Mark. Complex. 2022, 8, 167. [Google Scholar] [CrossRef]

- Peña-García, N.; Losada-Otálora, M.; Juliao-Rossi, J.; Rodríguez-Orejuela, A. Co-Creation of Value and Customer Experience: An Application in Online Banking. Sustainability 2021, 13, 10486. [Google Scholar] [CrossRef]

- Masum, M.H.; Rahman, M.; Islamc, K.Z. E-banking Performance of Commercial Banks in Bangladesh: A Study on its Efficiency, Fulfillment, and Trust as the predictors. J. Bus. Dev. Stud. 2022, 1, 15–29. [Google Scholar]

- Narteh, B.; Kuada, J. Customer satisfaction with retail banking services in Ghana. Thunderbird Int. Bus. Rev. 2014, 56, 353–371. [Google Scholar] [CrossRef]

- Rahman, M.M.; Tabash, M.I.; Salamzadeh, A.; Abduli, S.; Rahaman, M.S. Sampling techniques (probability) for quantitative social science researchers: A conceptual guidelines with examples. Seeu Rev. 2022, 17, 42–51. [Google Scholar] [CrossRef]

- Zafar, F.; Kamran, A.; Salman, S. Influence of E-commerce and Emerging Innovative Technological Advancements in the Banking Sector in Pakistan. Int. Conf. Manag. Sci. Eng. Manag. 2022, 193–206. [Google Scholar]

- Rahman, M.M. Sample Size Determination for Survey Research and Non-Probability Sampling Techniques: A Review and Set of Recommendations. J. Entrep. Bus. Econ. 2023, 11, 42–62. [Google Scholar]

- MohdThasThaker, H.; MohdThasThaker, M.A.; Khaliq, A.; Allah Pitchay, A.; Iqbal Hussain, H. Behavioural intention and adoption of internet banking among clients’ of Islamic banks in Malaysia: An analysis using UTAUT2. J. Islam. Mark. 2022, 13, 1171–1197. [Google Scholar] [CrossRef]

- Fornell, C.; Johnson, M.D.; Anderson, E.W.; Cha, J.; Bryant, B.E. The American customer satisfaction index: Nature, purpose, and findings. J. Mark. 1996, 60, 7–18. [Google Scholar] [CrossRef]

- Johnson, M.D.; Gustafsson, A.; Andreassen, T.W.; Lervik, L.; Cha, J. The evolution and future of national customer satisfaction index models. J. Econ. Psychol. 2001, 22, 217–245. [Google Scholar] [CrossRef]

- Rahman, M.M.; Adedeji, S.B.; Bashir, M.A.; Islam, J.; Reaz, M.; Khan, A.M. Mediation using covariance based-structural equation modeling (CB-SEM): The why and how? Asian J. Empir. Res. 2018, 4, 434–442. [Google Scholar] [CrossRef]

- Rahman, M.M.; Ali, N.A.; Jantan, A.H.; Samuel, A.B.; Rahaman, M.S. Mediation using CB-SEM: A practical guideline. Int. J. Technol. Transf. Commer. 2021, 18, 195–206. [Google Scholar] [CrossRef]

- Mahajan, R. Advancements in Technology and Customer’s Satisfaction with online banking services. Turk. J. Comput. Math. Educ. TURCOMAT 2021, 12, 2314–2319. [Google Scholar]

- Gayathri, S. The mediating effect of customer satisfaction on the relationship between service quality and customer loyalty in Digital Banking. J. Contemp. Issues Bus. Gov. 2022, 28, 20–31. [Google Scholar]

- Das, S.A.; Ravi, N. A Study on the Impact of E-Banking Service Quality on Customer Satisfaction. Asian J. Econ. Financ. Manag. 2021, 48–56. [Google Scholar]

- Omofowa, M.S.; Omofowa, S.; Nwachukwu, C.; Le, V. E-Banking Service Quality and Customer Satisfaction: Evidence from Deposit Money Bank in South-South Nigeria. Management 2021, 18, 288–302. [Google Scholar] [CrossRef]

- Khan, M.M.; Fasih, M. Impact of service quality on customer satisfaction and customer loyalty: Evidence from banking sector. Pak. J. Commer. Soc. Sci. 2014, 8, 331–354. [Google Scholar]

- Kabir, M.A.; Al Poddar, S.C. E-banking and customer satisfaction in Bangladesh. Eur. J. Bus. Manag. 2015, 7, 47–55. [Google Scholar]

- Dauda, Y.; Santhapparaj, A.S.; Asirvatham, D.; Raman, R. The impact of e-commerce security, and national environment on consumer adoption of internet banking in Malaysia and Singapore. J. Internet Bank. Commer. 2007, 12, 1–20. [Google Scholar]

- Mbama, C.I.; Ezepue, P.O. Digital banking, customer experience and bank financial performance: UK customers’ perceptions. Int. J. Bank Mark. 2018, 36, 230–255. [Google Scholar] [CrossRef]

- Malik, S.U. Customer satisfaction, perceived service quality and mediating role of perceived value. Int. J. Mark. Stud. 2012, 4, 68–76. [Google Scholar] [CrossRef]

- Berraies, S.; Hamouda, M. Customer empowerment and firms’ performance: The mediating effects of innovation and customer satisfaction. Int. J. Bank Mark. 2018, 36, 336–356. [Google Scholar] [CrossRef]

- Andotra, N.; Lal, T. Investigating occupation-wise perception of customers towards access to cooperative banking services. Int. J. Cust. Relat. 2016, 4, 5–11. [Google Scholar] [CrossRef]

- Arshad Khan, M.; Alhumoudi, H.A. Performance of E-Banking and the Mediating Effect of Customer Satisfaction: A Structural Equation Model Approach. Sustainability 2022, 14, 7224. [Google Scholar] [CrossRef]

- Jolović, N.; Đuričin, S. Analysis of the Role of VCFs as Non-banking Financial Institutions in Financing Women’s Entrepreneurship. J. Women’s Entrep. Educ. 2019, 3–4, 33–52. [Google Scholar]

- Kyewaalabye, M.; Mayanja, J.B.; Nnyanzi, J.B. The Growth Effects of Electronic Banking: Evidence from Eastern Africa. J. Entrep. Bus. Econ. 2022, 10, 294–325. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Authors | Independent Variable | Dependent Variable |

|---|---|---|

| [31] | Service quality, web design and content, security and privacy, convenience, and speed | Customer satisfaction |

| [32] | Review paper | |

| [24] | E-banking services | Financial performance |

| [33] | Review paper | |

| [34] | Conceptual paper | Conceptual paper |

| [35] | Security and loyalty | E-Banking practices |

| Variable | Dimensions | Measures | Sources | Reliability |

|---|---|---|---|---|

| Service Quality | 5 | 25 | [25,29] | 0.89 |

| Customers’ Experience | 1 | 7 | [25,29] | 0.91 |

| Customers’ Satisfaction | 1 | 10 | [60,61] | 0.90 |

| Demographic Information | Findings |

|---|---|

| Gender | Male = 59% Female = 41% |

| Age | 18–25 = 15% 26–33 = 75% Above 34 = 10% |

| Level of education | High school and college = 5% Undergraduate = 14% Postgraduate = 70% Other = 11% |

| Occupation | Government employees = 14% Private employees = 55% Businessmen = 15% Housewife = 6% Students = 10% |

| Maritalstatus | Married = 35% Unmarried = 65% |

| Income (per month) | Less than BDT 20,000 = 5% Between BDT 20,000 to 30,000 = 8% Between BDT 30,000 to 50,000 = 69% Between BDT 50,000 to 80,000 = 11% Above BDT 80,000 = 7% |

| Mean | SD | A_CS | A_Sev_Qul | A_CE | Collinearity Statistics | ||

|---|---|---|---|---|---|---|---|

| Tolerance | VIF | ||||||

| A_CS | 3.7093 | 0.90202 | 1 | ||||

| A_Sev_Qul | 3.7664 | 0.73055 | 0.556 ** | 1 | 0.718 | 1.392 | |

| A_CE | 3.1556 | 1.05766 | 0.690 ** | 0.531 ** | 1 | 0.718 | 1.392 |

| Absolute Fit | Incremental Fit | Parsimonious Fit | |||

|---|---|---|---|---|---|

| RMSEA | GFI | AGFI | CFI | Chisq/df | |

| Measurement Model | 0.056 | 0.844 | 0.819 | 0.940 | 2.00 |

| Variables | Variables | Estimate | S.E. | C.R. | p | |

|---|---|---|---|---|---|---|

| SQ | --- | CS | 0.23 | 0.057 | 4.834 | ***(significant) |

| CE | --- | CS | 0.60 | 0.043 | 10.261 | *** (significant) |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bashir, M.A.; Haque, M.A.; Salamzadeh, A.; Rahman, M.M. Customers’ Satisfaction of E-Banking in Bangladesh: Do Service Quality and Customers’ Experiences Matter? FinTech 2023, 2, 657-667. https://doi.org/10.3390/fintech2030036

Bashir MA, Haque MA, Salamzadeh A, Rahman MM. Customers’ Satisfaction of E-Banking in Bangladesh: Do Service Quality and Customers’ Experiences Matter? FinTech. 2023; 2(3):657-667. https://doi.org/10.3390/fintech2030036

Chicago/Turabian StyleBashir, Md. Abdul, Md. Alaul Haque, Aidin Salamzadeh, and Md. Mizanur Rahman. 2023. "Customers’ Satisfaction of E-Banking in Bangladesh: Do Service Quality and Customers’ Experiences Matter?" FinTech 2, no. 3: 657-667. https://doi.org/10.3390/fintech2030036

APA StyleBashir, M. A., Haque, M. A., Salamzadeh, A., & Rahman, M. M. (2023). Customers’ Satisfaction of E-Banking in Bangladesh: Do Service Quality and Customers’ Experiences Matter? FinTech, 2(3), 657-667. https://doi.org/10.3390/fintech2030036