Diversification of Time-Varying Tangency Portfolio under Nonlinear Constraints through Semi-Integer Beetle Antennae Search Algorithm

Abstract

:1. Introduction

- We define and explore the TV-TPNC problem as a NLP problem.

- To tackle NLP problems with cardinality constraints, a hybrid algorithm, called SIBAS, is proposed.

- We present the SIBAS efficiency against particle swarm optimization (PSO), differential evolution (DE) and slime mould algorithm (SMA) on a financial NLP problem.

2. Tangency Portfolio Optimization

| maxp | |

| subject to | |

| subject to | |

3. The Semi-Integer Beetle Antennae Search Model

3.1. The SIBAS Algorithm

3.2. SIBAS Approach on the TV-TPNC Problem and the Complete Process

| Algorithm 1: The complete process to solve the TV-TPNC problem of (9)–(12) using SIBAS. |

| Require: The market dataset M; the delays number ; the initial portfolio and the value of parameter . |

|

| Ensure: The optimal solution of the TV-TPNC problem of (9)–(12). |

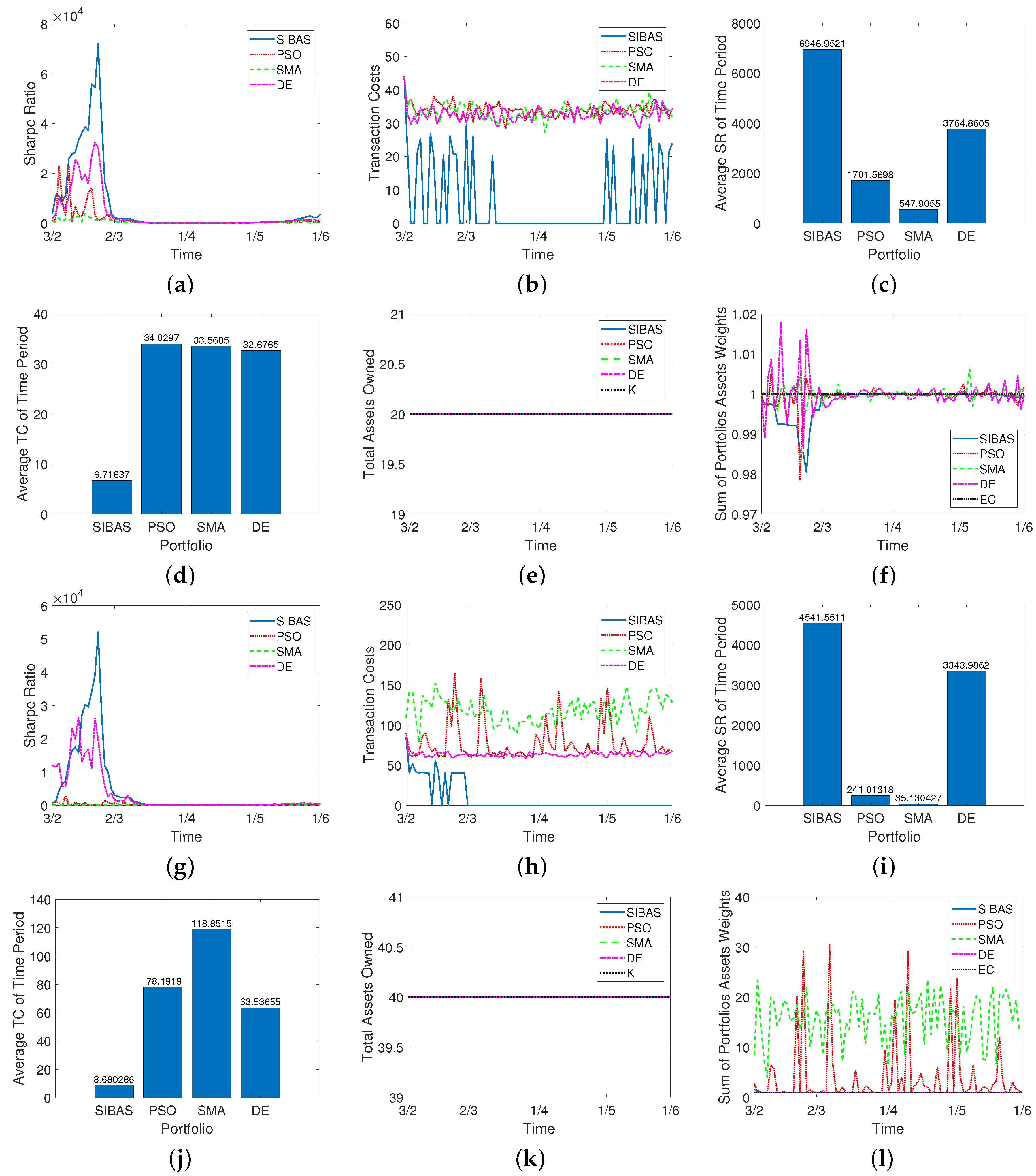

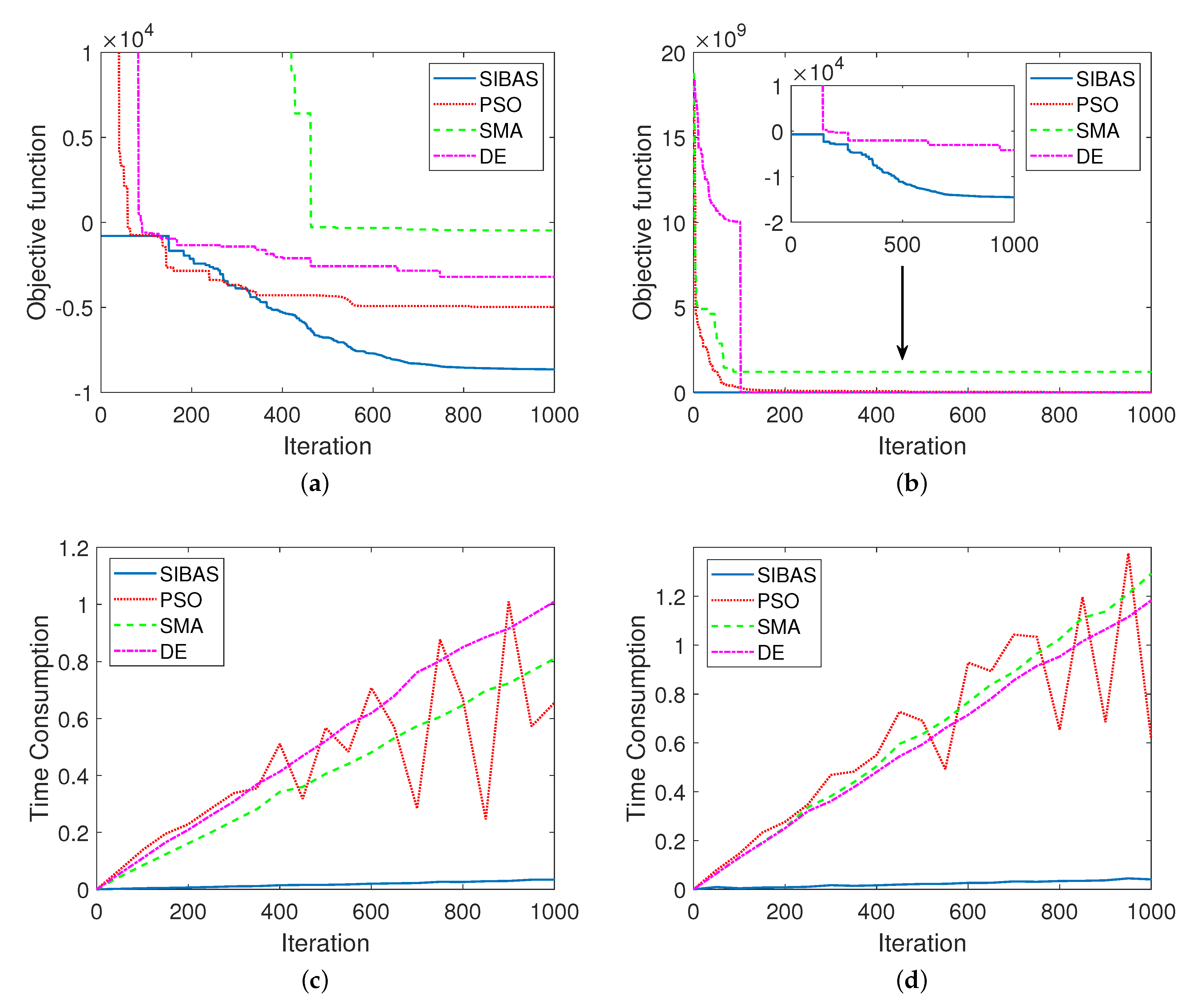

4. Applications

4.1. Real-World Data Portfolio Cases

4.2. MATLAB Repository

5. Conclusions

- The SIBAS could be compared to other popular meta-heuristics approaches in larger portfolios and other financial portfolio optimization problems.

- The use of SIBAS in constraint optimization problems in different scientific domains.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Simos, T.E.; Mourtas, S.D.; Katsikis, V.N. Time-varying Black–Litterman portfolio optimization using a bio-inspired approach and neuronets. Appl. Soft Comput. 2021, 112, 107767. [Google Scholar] [CrossRef]

- Katsikis, V.N.; Mourtas, S.D. Computational Management; Modeling and Optimization in Science and Technologies, Chapter Portfolio Insurance and Intelligent Algorithms; Springer: Cham, Switzerland, 2021; Volume 18, pp. 305–323. [Google Scholar] [CrossRef]

- Katsikis, V.N.; Mourtas, S.D.; Stanimirović, P.S.; Li, S.; Cao, X. Time-Varying Mean-Variance Portfolio Selection under Transaction Costs and Cardinality Constraint Problem via Beetle Antennae Search Algorithm (BAS). Oper. Res. Forum 2021, 2, 18. [Google Scholar] [CrossRef]

- Mourtas, S.D.; Katsikis, V.N. V-Shaped BAS: Applications on Large Portfolios Selection Problem. Comput. Econ. 2021. [Google Scholar] [CrossRef]

- Ye, K.; Parpas, P.; Rustem, B. Robust portfolio optimization: A conic programming approach. Comp. Opt. Appl. 2012, 52, 463–481. [Google Scholar] [CrossRef] [Green Version]

- Konno, H.; Akishino, K.; Yamamoto, R. Optimization of a Long-Short Portfolio under Nonconvex Transaction Cost. Comp. Opt. Appl. 2005, 32, 115–132. [Google Scholar] [CrossRef]

- Ogryczak, W.; Sliwinski, T. On solving the dual for portfolio selection by optimizing Conditional Value at Risk. Comp. Opt. Appl. 2011, 50, 591–595. [Google Scholar] [CrossRef]

- Katsikis, V.N.; Mourtas, S.D. A heuristic process on the existence of positive bases with applications to minimum-cost portfolio insurance in C[a, b]. Appl. Math. Comput. 2019, 349, 221–244. [Google Scholar] [CrossRef]

- Katsikis, V.N.; Mourtas, S.D. ORPIT: A Matlab Toolbox for Option Replication and Portfolio Insurance in Incomplete Markets. Comput. Econ. 2019, 56, 711–721. [Google Scholar] [CrossRef]

- Jiang, X.; Li, S. BAS: Beetle Antennae Search Algorithm for Optimization Problems. arXiv 2017, arXiv:1710.10724. [Google Scholar] [CrossRef]

- Medvedeva, M.A.; Katsikis, V.N.; Mourtas, S.D.; Simos, T.E. Randomized time-varying knapsack problems via binary beetle antennae search algorithm: Emphasis on applications in portfolio insurance. Math. Methods Appl. Sci. 2020, 44, 2002–2012. [Google Scholar] [CrossRef]

- Khan, A.H.; Cao, X.; Katsikis, V.N.; Stanimirovic, P.; Brajevic, I.; Li, S.; Kadry, S.; Nam, Y. Optimal Portfolio Management for Engineering Problems Using Nonconvex Cardinality Constraint: A Computing Perspective. IEEE Access 2020, 8, 57437–57450. [Google Scholar] [CrossRef]

- Katsikis, V.N.; Mourtas, S.D.; Stanimirović, P.S.; Li, S.; Cao, X. Time-varying minimum-cost portfolio insurance under transaction costs problem via Beetle Antennae Search Algorithm (BAS). Appl. Math. Comput. 2020, 385, 125453. [Google Scholar] [CrossRef]

- Khan, A.T.; Cao, X.; Li, S.; Hu, B.; Katsikis, V.N. Quantum Beetle Antennae Search: A Novel Technique for The Constrained Portfolio Optimization Problem. Sci. China Inf. Sci. 2021, 64, 152204. [Google Scholar] [CrossRef]

- Wu, Q.; Ma, Z.; Xu, G.; Li, S.; Chen, D. A Novel Neural Network Classifier Using Beetle Antennae Search Algorithm for Pattern Classification. IEEE Access 2019, 7, 64686–64696. [Google Scholar] [CrossRef]

- Khan, A.H.; Cao, X.; Li, S.; Katsikis, V.N.; Liao, L. BAS-ADAM: An ADAM based approach to improve the performance of beetle antennae search optimizer. IEEE/CAA J. Autom. Sin. 2020, 7, 461–471. [Google Scholar] [CrossRef]

- Fan, Y.; Shao, J.; Sun, G. Optimized PID controller based on beetle antennae search algorithm for electro-hydraulic position servo control system. Sensors 2019, 19, 2727. [Google Scholar] [CrossRef] [Green Version]

- Yue, Z.; Li, G.; Jiang, X.; Li, S.; Cheng, J.; Ren, P. A Hardware Descriptive Approach to Beetle Antennae Search. IEEE Access 2020, 8, 89059–89070. [Google Scholar] [CrossRef]

- Chen, D.; Li, X.; Li, S. A Novel Convolutional Neural Network Model Based on Beetle Antennae Search Optimization Algorithm for Computerized Tomography Diagnosis. IEEE Trans. Neural Netw. Learn. Syst. 2021, 1–12. [Google Scholar] [CrossRef]

- Tobin, J. Liquidity Preference as Behavior Towards Risk. Rev. Econ. Stud. 1958, 25, 65–86. [Google Scholar] [CrossRef]

- Maringer, D.G. Portfolio Management with Heuristic Optimization, 1st ed.; Advances in Computational Management Science; Springer: Berlin/Heidelberg, Germany, 2005; Volume 8. [Google Scholar] [CrossRef]

- Jansen, R.; van Dijk, R. Optimal Benchmark Tracking with Small Portfolios. J. Portf. Manag. 2002, 28, 33–39. [Google Scholar] [CrossRef]

- Lobo, M.S.; Fazel, M.; Boyd, S. Portfolio optimization with linear and fixed transaction costs. Ann. Oper. Res. 2007, 152, 341–365. [Google Scholar] [CrossRef]

- Deb, K. Optimization for Engineering Design: Algorithms and Examples, 2nd ed.; PHI: Delhi, New Delhi, India, 2013. [Google Scholar]

- Yang, X.S. Nature-Inspired Optimization Algorithms, 1st ed.; Elsevier Insights, Elsevier: Amsterdam, The Netherlands, 2014. [Google Scholar]

- Li, S.; Chen, H.; Wang, M.; Heidari, A.A.; Mirjalili, S. Slime mould algorithm: A new method for stochastic optimization. Future Gener. Comput. Syst. 2020, 111, 300–323. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Portfolio | SIBAS | PSO | SMA | DE |

|---|---|---|---|---|

| Case 1 (40 Stocks) | s | s | s | s |

| Case 2 (80 Stocks) | s | s | s | s |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Katsikis, V.N.; Mourtas, S.D. Diversification of Time-Varying Tangency Portfolio under Nonlinear Constraints through Semi-Integer Beetle Antennae Search Algorithm. AppliedMath 2021, 1, 63-73. https://doi.org/10.3390/appliedmath1010005

Katsikis VN, Mourtas SD. Diversification of Time-Varying Tangency Portfolio under Nonlinear Constraints through Semi-Integer Beetle Antennae Search Algorithm. AppliedMath. 2021; 1(1):63-73. https://doi.org/10.3390/appliedmath1010005

Chicago/Turabian StyleKatsikis, Vasilios N., and Spyridon D. Mourtas. 2021. "Diversification of Time-Varying Tangency Portfolio under Nonlinear Constraints through Semi-Integer Beetle Antennae Search Algorithm" AppliedMath 1, no. 1: 63-73. https://doi.org/10.3390/appliedmath1010005