1. Introduction

Compositional time series, in which observations are vectors of proportions constrained to sum to one, arise in a wide range of applications. For instance, market researchers track evolving shares of competing products [

1] ecologists monitor species composition over time, and sociologists or political scientists follow shifting demographic or budgetary profiles [

2]. In each case, the data lie within a simplex, making the Dirichlet model a common starting point [

3,

4]. However, when temporal dependence is also present—for example, today’s composition influences tomorrow’s—the Dirichlet framework must be extended to account for dynamics in a way that respects the simplex constraints.

Several approaches have emerged to handle dynamic compositional data, notably by coupling the Dirichlet with Auto-Regressive Moving Average (ARMA)-like structures [

5], by using a logistic-normal representation [

6], or by adopting new families of innovation distributions [

7]. Others have adapted the model to cope with zeros [

8] or extreme heavy-tailed behaviors. In particular, the Bayesian Dirichlet Auto-Regressive Moving Average (B-DARMA) model [

9] addresses key compositional modeling challenges by introducing Vector Auto-Regression (VAR) and Vector Moving Average (VMA) terms for multivariate compositional data. Under B-DARMA, each day’s, or time point’s, composition is Dirichlet-distributed with parameters that evolve with a VARMA process in the additive log-ratio space, capturing both compositional constraints and serial correlation.

Although B-DARMA provides a flexible foundation, practitioners must still specify priors for potentially high-dimensional parameter spaces, which can be prone to overfitting or omitted-lag bias. The growing literature on Bayesian shrinkage priors offers numerous solutions, from global–local shrinkage frameworks [

10] to hierarchical approaches [

11], along with classic spike-and-slab [

12,

13] and Laplace priors [

14]. These priors can encourage sparsity and suppress extraneous lags in over-parameterized models, a crucial feature for many real-world compositional applications in which the number of possible lags or covariates exceeds the sample size. The horseshoe prior [

15,

16] has shown particular promise in forecasting studies where only a minority of parameters matter and many are effectively zero. At the same time, hierarchical shrinkage [

11] facilitates partial pooling across related coefficient blocks, an appealing property when working with multi-sector or multi-species compositions.

In this paper, we systematically investigate how five different prior families—informative normal, horseshoe, Laplace, spike-and-slab, and hierarchical shrinkage—affect parameter recovery and predictive accuracy in the B-DARMA model. We compare their performance across three main scenarios using simulated data: (i) correct specification, where the model order matches the true process; (ii) overfitting, where extraneous VAR/VMA terms inflate model dimensionality; and (iii) underfitting, where key VAR/VMA terms are missing altogether. Our findings confirm that shrinkage priors—especially horseshoe and hierarchical variants—can successfully rein in overfitting, providing more robust parameter estimates and improved forecasts. Conversely, no amount of shrinkage compensates for omitted terms, highlighting the need for careful model specification.

To demonstrate the practical impact, we also apply B-DARMA to daily S&P 500 sector trading data, a large-scale compositional time series characterized by multiple seasonalities and long-lag behavior. Consistent with the simulation insights, we find that more aggressive shrinkage priors significantly reduce spurious complexity and improve forecast accuracy, especially for volatile sectors. These outcomes reinforce that while B-DARMA provides a natural scaffolding for compositional dependence, judicious prior selection and meaningful lag choices are pivotal.

In the remainder of this paper, we first review the B-DARMA model (

Section 2) and outline how our five prior families (informative, horseshoe, Laplace, spike-and-slab, and hierarchical) encode distinct shrinkage behaviors. We then present the design and results of three simulation studies (

Section 3 and

Section 4) before turning to the empirical S&P 500 application (

Section 5). We conclude with recommendations for practitioners modeling compositional time series with complex temporal dynamics and large parameter counts.

2. Background

2.1. Compositional Data and the Dirichlet Distribution

Compositional data consist of vectors of proportions, each strictly between zero and one and summing to unity [

3]. Formally, let

where each

and

The vector

resides in the

-dimensional simplex.

A natural choice for modeling such compositional vectors is the

Dirichlet distribution. In its basic form, a Dirichlet random vector

is parameterized by a concentration vector

with

. The probability density function is

where

and

is the Gamma function. This parameterization captures both the support of compositional data (the simplex) and the potential correlation structure among components.

2.2. B-DARMA Model

To capture temporal dependence in compositional data, the Bayesian Dirichlet Auto-Regressive Moving Average (B-DARMA) model [

9] augments the Dirichlet framework with VAR and VMA dynamics. Specifically, for each time

, let

be the observed composition. We assume

with density

, where

’ is the mean composition and

is a precision parameter. Both

and

may vary with time.

Because each

lies in the simplex, we map it to an unconstrained

-dimensional vector via the

additive log-ratio transform

We denote

To incorporate serial dependence, we assume that

follows a vector VARMA process in the transformed space

for

, where

. In this notation,

and

are each

coefficient matrices;

is a known

covariate matrix, including any intercepts, trends, or seasonality; and

is a vector of regression coefficients shared across the

components.

The Dirichlet precision

can also evolve over time. For an

-vector of covariates

, we set

with

. In the absence of covariates, we simply have

for all

t, so

becomes a constant.

We gather all unknown parameters into a vector of length

C,

where

,

, and

, and

is the j-th element of

. The total number of free parameters is thus

Bayesian inference begins by positing a prior distribution

over the model parameters

. Bayes’ theorem updates this prior to form the posterior

where

and

is the normalizing constant obtained by integrating over

. Each

follows the Dirichlet likelihood (

1).

Next, to generate predictions for the subsequent

S time points,

, we construct the joint predictive distribution

In practice, analysts often summarize this distribution at future time points

by reporting measures such as the posterior mean or median.

2.3. Bayesian Shrinkage Priors for B-DARMA Coefficients

In a fully Bayesian approach, all unknown parameters in the B-DARMA model—including the VARMA coefficients in and , the regression vector , and the precision-related parameters —require prior distributions. Different shrinkage priors can produce significantly different outcomes, particularly in high-dimensional or sparse settings where many coefficients may be small. This section discusses five popular priors (normal, horseshoe, Laplace, spike-and-slab, and hierarchical), highlighting how each encodes shrinkage or sparsity assumptions.

An informative normal prior serves as a straightforward baseline. We model each coefficient by . The mean a often defaults to zero unless prior knowledge indicates a different center. The variance determines the shrinkage strength; smaller yields tighter concentration around a. In B-DARMA applications, it may be sensible to set for the VARMA parameters if they are believed to be small on average, whereas for covariates , a smaller prior variance such as can reflect stronger beliefs that regression effects are modest.

The

horseshoe prior [

15] is well-suited for sparse problems. We model each coefficient

as

, with a global scale

and local scales

. Large local scales allow some coefficients to remain sizable, whereas most are heavily shrunk. This can be beneficial if the B-DARMA model includes many possible lags or covariates, only a small subset of which are expected to matter for compositional forecasting.

A

Laplace (double-exponential) prior [

14] employs the density

. This enforces an

-type penalty that can drive many coefficients close to zero while still allowing moderate signals to persist. The scale

b can be chosen a priori or assigned its own hyperprior, such as a half-Cauchy, so that the data adaptively determine the shrinkage level. In a B-DARMA context, choosing a smaller

b for high-dimensional VARMA terms can prevent spurious estimates from inflating the parameter space.

A

spike-and-slab prior [

12] can introduce explicit sparsity by placing a point mass at zero. Let

be the mixing parameter for the

jth coefficient. Then, each coefficient

follows the mixture

where

is the Dirac measure at zero. Coefficients drawn from the spike component remain exactly zero, effectively excluding them from the model, while coefficients from the slab remain freely estimated. This setup allows the B-DARMA specification to adapt by discarding irrelevant lags or covariates.

A

hierarchical shrinkage prior [

17] can encourage partial pooling across groups of coefficients. We model each coefficient

by

and then place a half-Cauchy prior on

. In B-DARMA, one could assign separate group scales to the AR, MA, and regression blocks, thereby allowing the model to learn an appropriate overall variability for each group of parameters.

These priors differ in how strongly they push coefficients toward zero and whether they favor a few large coefficients or moderate shrinkage for all. The normal prior provides a baseline continuous shrinkage, the horseshoe prior excels when only a minority of parameters are truly large, the Laplace prior induces an -type penalty that can zero out many coefficients, the spike-and-slab prior explicitly discards some parameters, and the hierarchical prior alternative enables group-level learning of shrinkage scales. The next sections illustrate how these choices affect both parameter recovery and compositional forecasting in various simulation and real-data scenarios.

2.4. Posterior Computation

All B-DARMA models are fit with STAN [

18] in R using Hamiltonian Monte Carlo. We run 4 chains, each with 500 warm-up and 750 sampling iterations, yielding

posterior draws. The sampler uses

adapt_delta = 0.85,

max_treedepth = 11, and random initial values drawn uniformly from [−0.25, 0.25].

2.5. Stationarity and Structural Considerations

Open theoretical gap. B-DARMA inherits the difficulty noted by Zheng and Chen [

5]: after the additive-log-ratio (ALR) link, the innovation is

not a martingale-difference sequence (MDS). Consequently, classical stationarity results for VARMA (p,q) processes do not transfer directly, and a full set of strict- or weak-stationarity conditions remains an open problem ([

9] [IJF, §2.2]).

Why Bayesian inference remains valid. Bayesian estimation proceeds via the joint posterior

, which does not require the likelihood-error sequence to be an MDS [

19]. We therefore regard B–DARMA as a flexible likelihood-based filter for compositional time series rather than assume that the fitted parameters represent a strictly stationary data-generating process.

3. Simulation Studies

We conduct three simulation studies to investigate how different priors affect parameter inference and forecasting in a B-DARMA model. All studies use the same sparse DARMA(2,1) data-generating process (DGP) but vary the fitted model to be correctly specified, deliberately overfitted, or underfitted. We first describe the DGP and the priors considered, and then outline the study designs and performance metrics.

3.1. Data-Generating Process

We simulate a six-dimensional compositional time series

, each component constrained to sum to one. The true process is DARMA(2,1) with fixed precision

,

, and

, a

identity matrix. We set our VAR and VMA matrices to

We initialize

and

from

, simulate

observations, and replicate this procedure 50 times. We focus on posterior inference for

and

, as well as forecasting accuracy.

3.2. Prior Distributions and Hyperparameters

We specify five candidate priors for the coefficient vectors: normal (mean 0, variance 1), horseshoe (global and local scales), Laplace (scale ), spike-and-slab (with local mixing parameters ), and hierarchical normal (with a half-Cauchy prior on the group-level scale). Although these priors remain the same across simulations, they are applied to different sets of coefficients: and in Simulation 1; –– and in Simulation 2; and and in Simulation 3. For the Dirichlet precision parameter, we use . The normal prior on is , and the Laplace and hierarchical normal versions adopt smaller scales to impose stronger shrinkage on intercepts.

3.3. Study Designs

We fit three B-DARMA specifications to the same DARMA(2,1) data:

Study 1 (Correct Specification): B-DARMA(2,1) matches the true DGP.

Study 2 (Overfitting): B-DARMA(4,2) includes extraneous higher-order VAR and VMA terms.

Study 3 (Underfitting): B-DARMA(1,0) omits the second VAR lag and the MA(1) term.

Each configuration is paired with each of the five priors, yielding 15 total fitted models. We repeat the simulation for 50 synthetic datasets of length T.

3.4. Evaluation Metrics

We assess both parameter recovery and forecasting performance. Let

be a true parameter and

be the posterior mean from simulation

s. We compute

along with 95% credible-interval coverage and interval length. If a parameter is omitted (as in underfitting), we exclude it from these summaries.

For forecasting, we use the first 80 points for training and the remaining 20 points for testing. Let

be the posterior mean forecast at time

t in simulation

s. We define

where

denotes the true composition in the test set for the

s-th simulation. Each of the three study designs is then evaluated under each of the five priors, illuminating how prior choice interacts with model misspecification.

5. Application to S&P 500 Sector Trading Values

5.1. Motivation and Data Description

A fixed daily trading value in the S&P 500 is allocated across different sectors, giving rise to compositional data that captures how investors distribute their capital each day. Tracking these proportions over time can reveal macroeconomic trends, sector rotation, and shifts in investor sentiment. In our analysis, we examined the daily proportions of eleven S&P 500 sectors from January 2021 to December 2023. These sectors include the following:

Technology: software, hardware, and related services.

Healthcare: pharmaceuticals, biotechnology, and healthcare services.

Financial Services: banking, insurance, and investment services.

Consumer Discretionary: non-essential goods and services.

Industrials: manufacturing, aerospace, defense, and machinery.

Consumer Staples: essential goods, such as food and household items.

Energy: oil, gas, and renewable resources.

Utilities: public services such as electricity and water.

Real Estate: REITs and property management.

Materials: chemicals, metals, and construction materials.

Communication Services: media, telecommunication, and internet services.

Let

denote the dollar trading value executed in sector

k on trading day

t for

(

sectors). The market-wide total is

and the composition we analyze is the vector of sector shares

The stationarity (or non-stationarity) of the compositional time series

is independent of that of the gross total

:

may drift without affecting the stationarity of the shares, and, conversely, the shares could be non-stationary even if

is itself stationary.

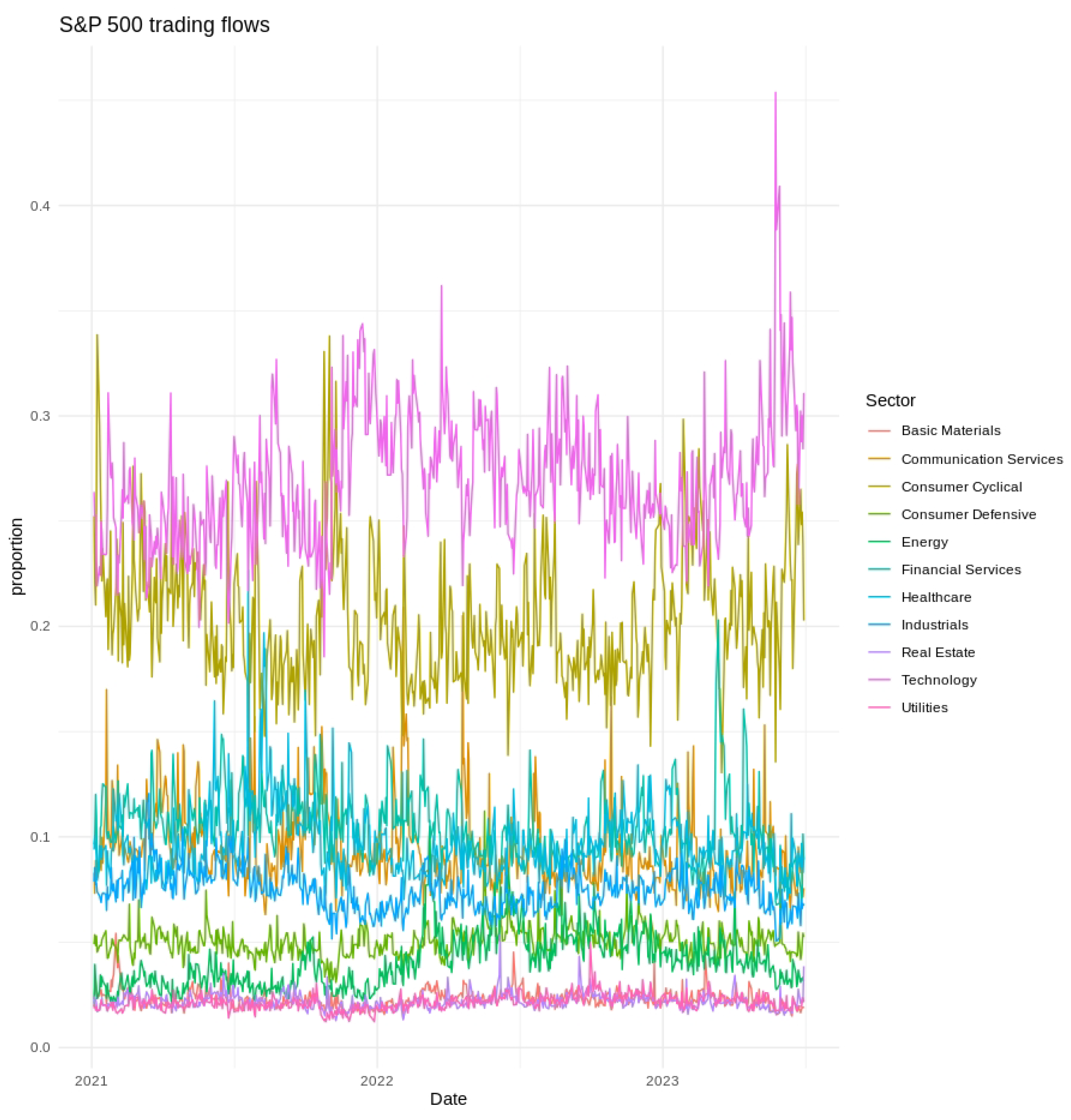

We used data from 1 January 2021 to 30 June 2023, for training, as shown in

Figure 1. The forecast evaluation was conducted on 126 trading days, spanning 1 July through 31 December 2023.

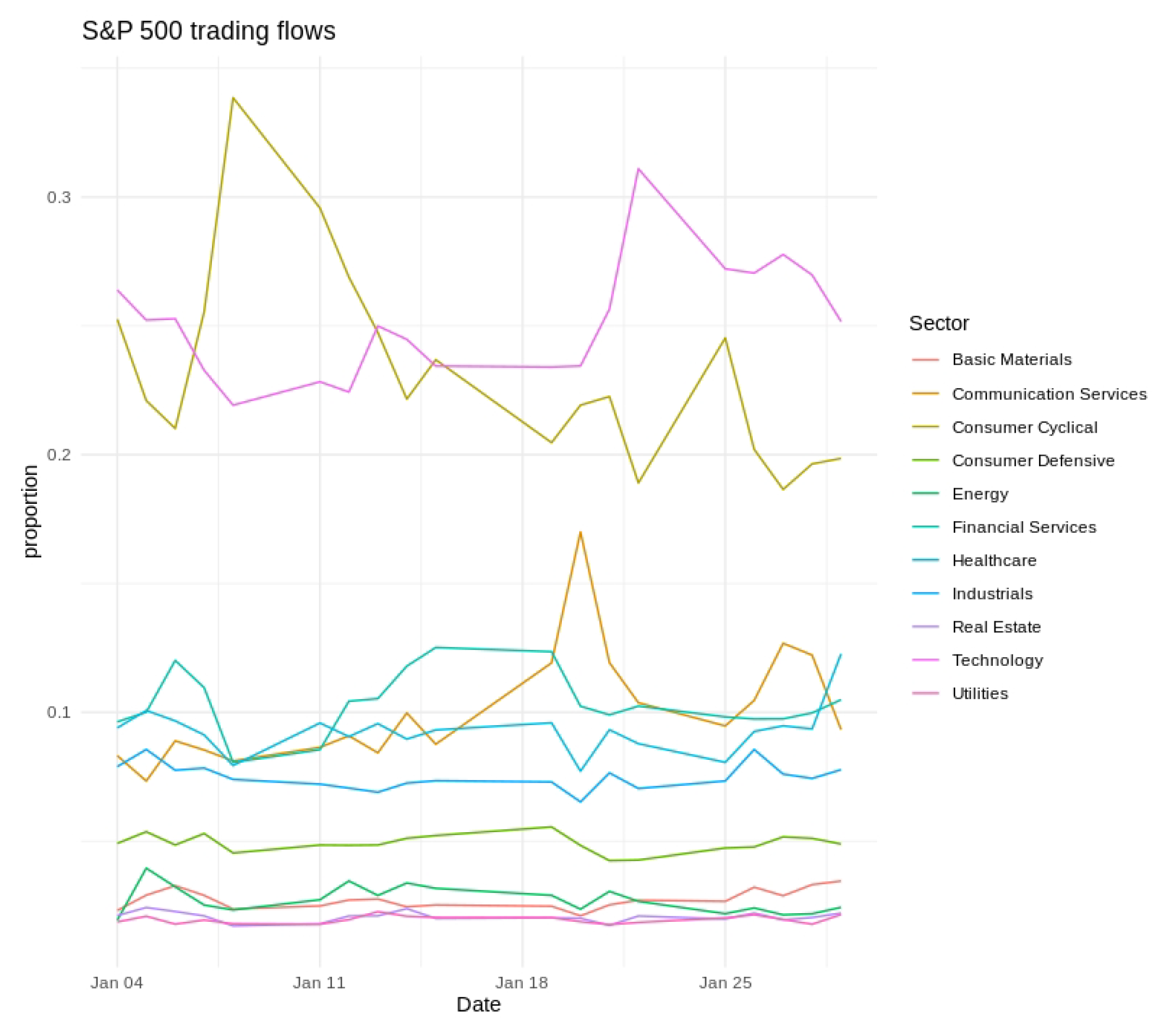

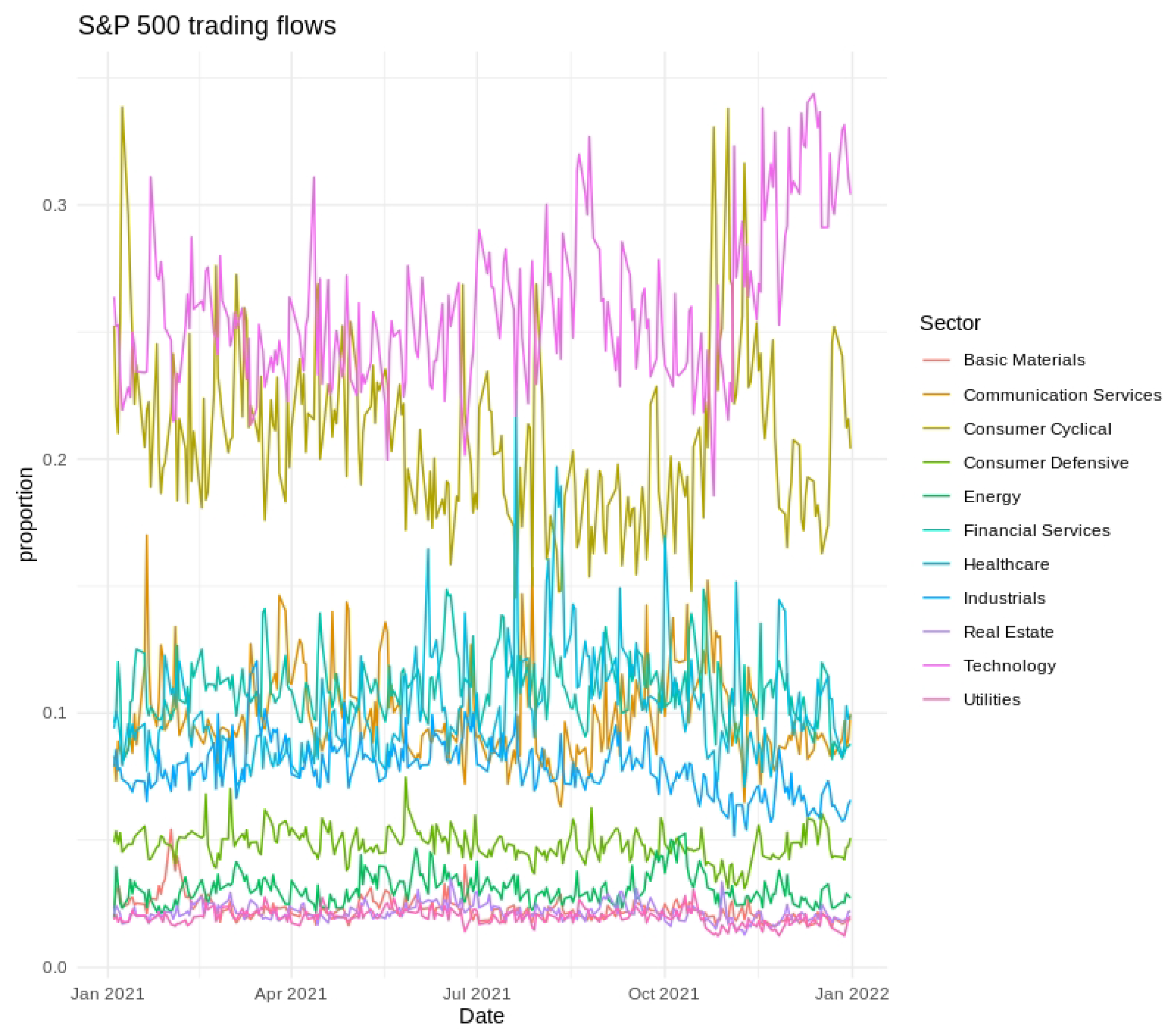

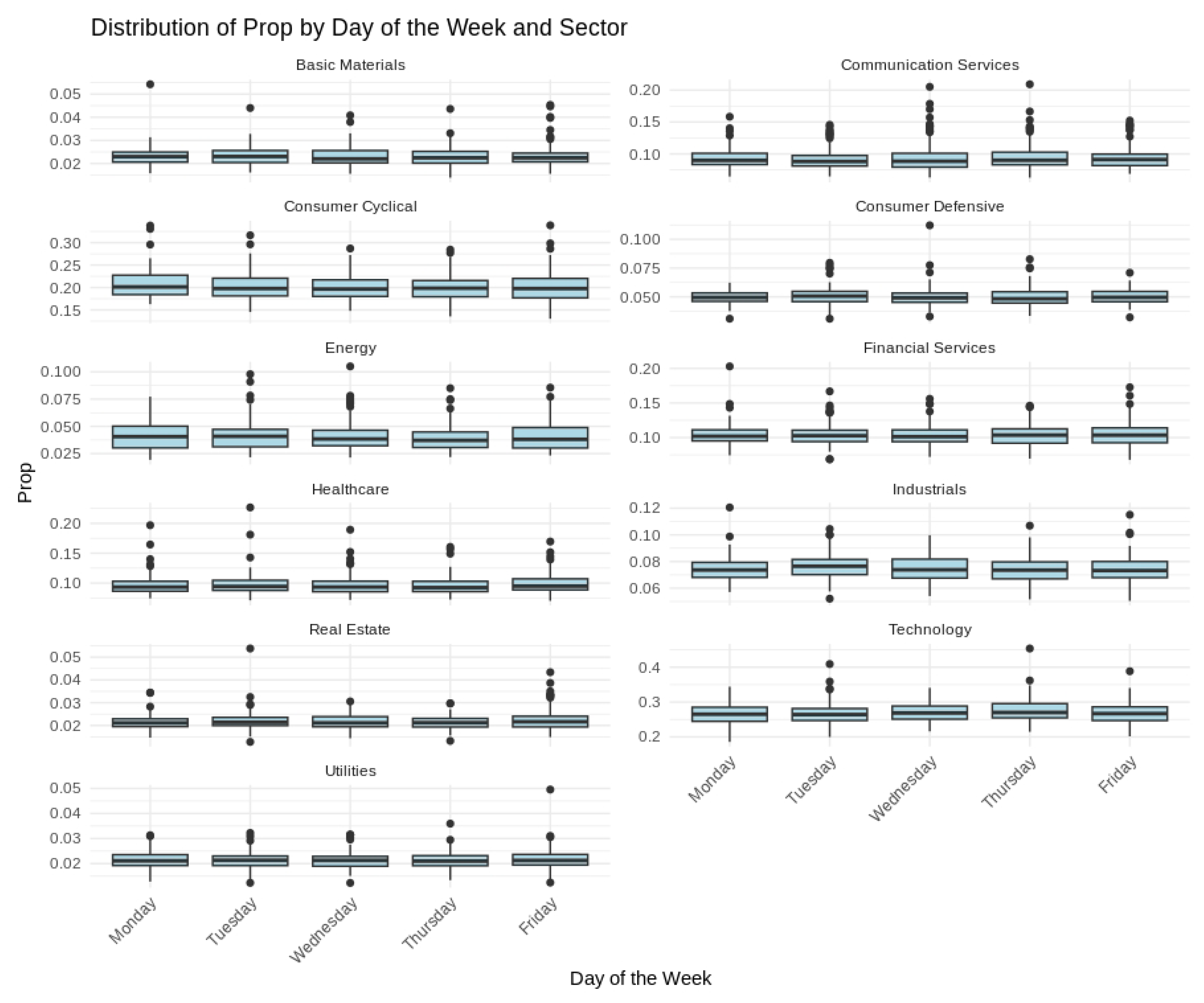

Short-term variability, cyclical tendencies, and gradual long-term shifts emerged across the series. Technology and Financial Services consistently held the largest fractions of the fixed daily trading value, whereas Utilities and Real Estate occupied much smaller shares. Day-to-day fluctuations tended to be more pronounced in Consumer Discretionary and Communication Services, indicating greater sensitivity to rapidly changing market conditions. Seasonal patterns and moderate differences across weekdays were also evident, as illustrated in

Figure 2,

Figure 3 and

Figure 4, further underscoring the multifaceted nature of sector-level trading dynamics.

Model specification (purposeful over-parameterization). A model is fitted by design with a lag order that exceeds the horizon over which sector reallocations are generally thought to propagate. Ten trading days (≈ two calendar weeks), therefore, represent a deliberate overfit, allowing us to evaluate how strongly the global–local shrinkage priors suppress redundant dynamics. Each sector’s additive-log-ratio is regressed on its own composition at lags , yielding VAR coefficients in the matrices .

Seasonality is modeled with Fourier bases that are fixed regardless of the chosen lag: two sine–cosine pairs capture the 5-day trading cycle (Monday–Friday), and five pairs capture the annual cycle of roughly 252 trading days. These 14 terms, together with a sector-specific intercept, form the design matrix for the linear predictor; the same seasonal structure enters the model for the Dirichlet precision .

In total, the specification estimates 1165 parameters: 1000 VAR coefficients, 140 seasonal coefficients, 10 intercepts, and 15 precision-related terms. The intentionally generous lag order thus functions as a stress test.

5.2. Priors and Hyperparameters

For all priors, the intercept in is given an prior, and all seasonal Fourier terms in receive .

Under the informative normal prior, every element of is modeled with an prior, and each element of has an prior.

The

Laplace prior [

14] is implemented via an exponential mixture: each coefficient

satisfies

with

, leading to an overall Laplace

prior. We set

and

for

and

, respectively.

For the

spike-and-slab prior [

12], each coefficient

is drawn from a mixture:

with probability

or

with probability

, where

is the mixing weight.

The

horseshoe prior [

15] introduces one global scale parameter

and local scales

, all drawn from

. Each coefficient

then follows

.

Finally, under the

hierarchical prior [

17], the coefficients are partitioned into three groups: (i) the elements of

, (ii) the diagonal entries of each lag matrix

, and (iii) the off-diagonal entries of each

. Then, the coefficients in

are modeled as

, while for each lag

p in

, the diagonal entries follow

and the off-diagonal entries follow

.

5.3. Evaluation Metrics and Forecasting

A B-DARMA(10,0) model was fit with each of the five priors using the training data. A 126-day forecast was then generated for the test period using the mean of the joint predictive distribution. Mean absolute error (MAE) was used as a measure of average discrepancy between the predicted and observed shares, while root mean squared error (RMSE) weighs larger deviations more explicitly.

5.4. Results

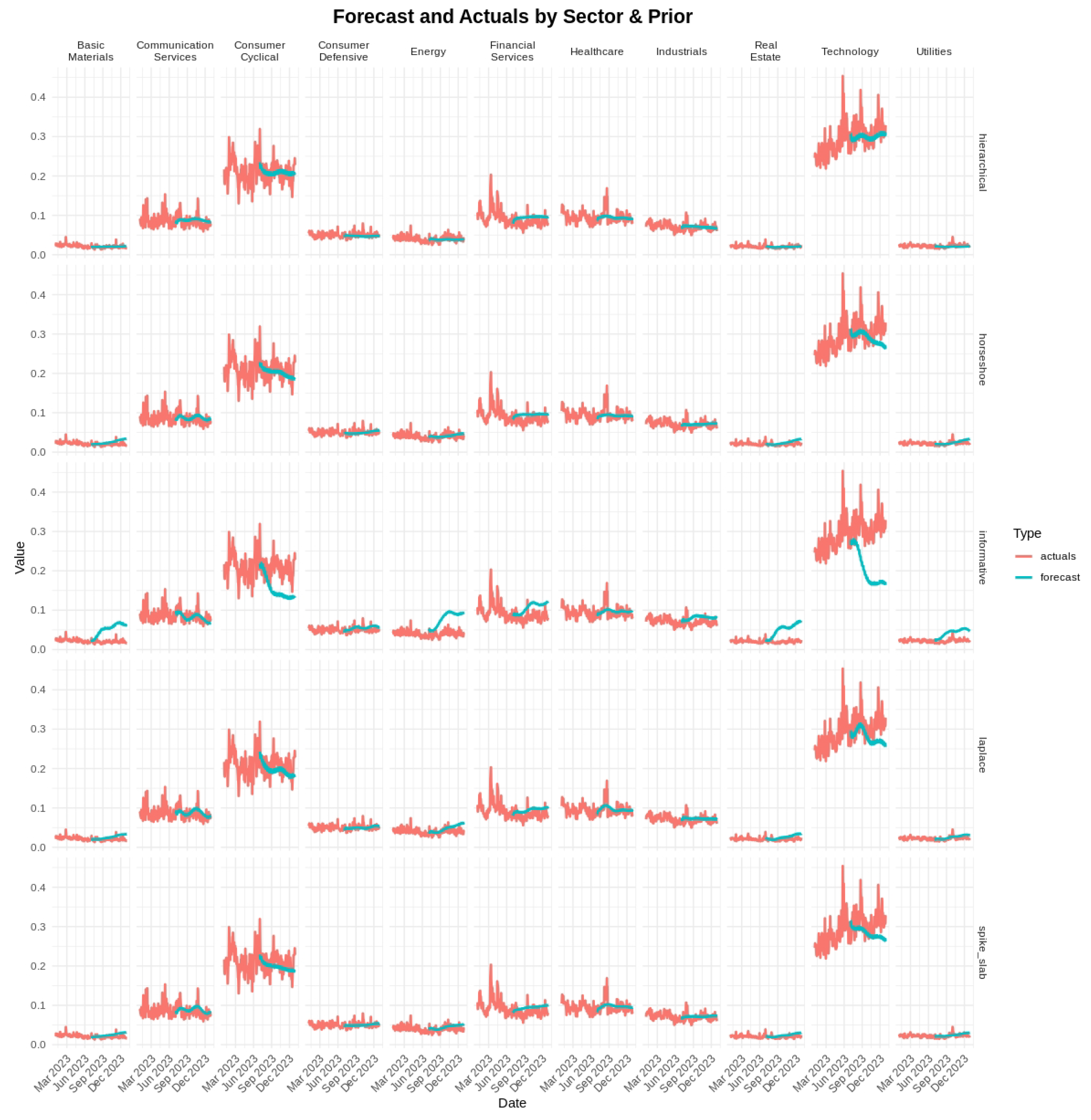

In

Figure 5, the forecasts (in turquoise) are shown together with the actual daily proportions (in red) for each sector over the 126-day test interval. The hierarchical and horseshoe priors led to predictions that aligned more closely with the observed values than the informative prior, particularly in volatile sectors such as Energy and Technology. Under the spike-and-slab prior, smaller signals were at times set to zero, which occasionally delayed responses to abrupt shifts in sector composition.

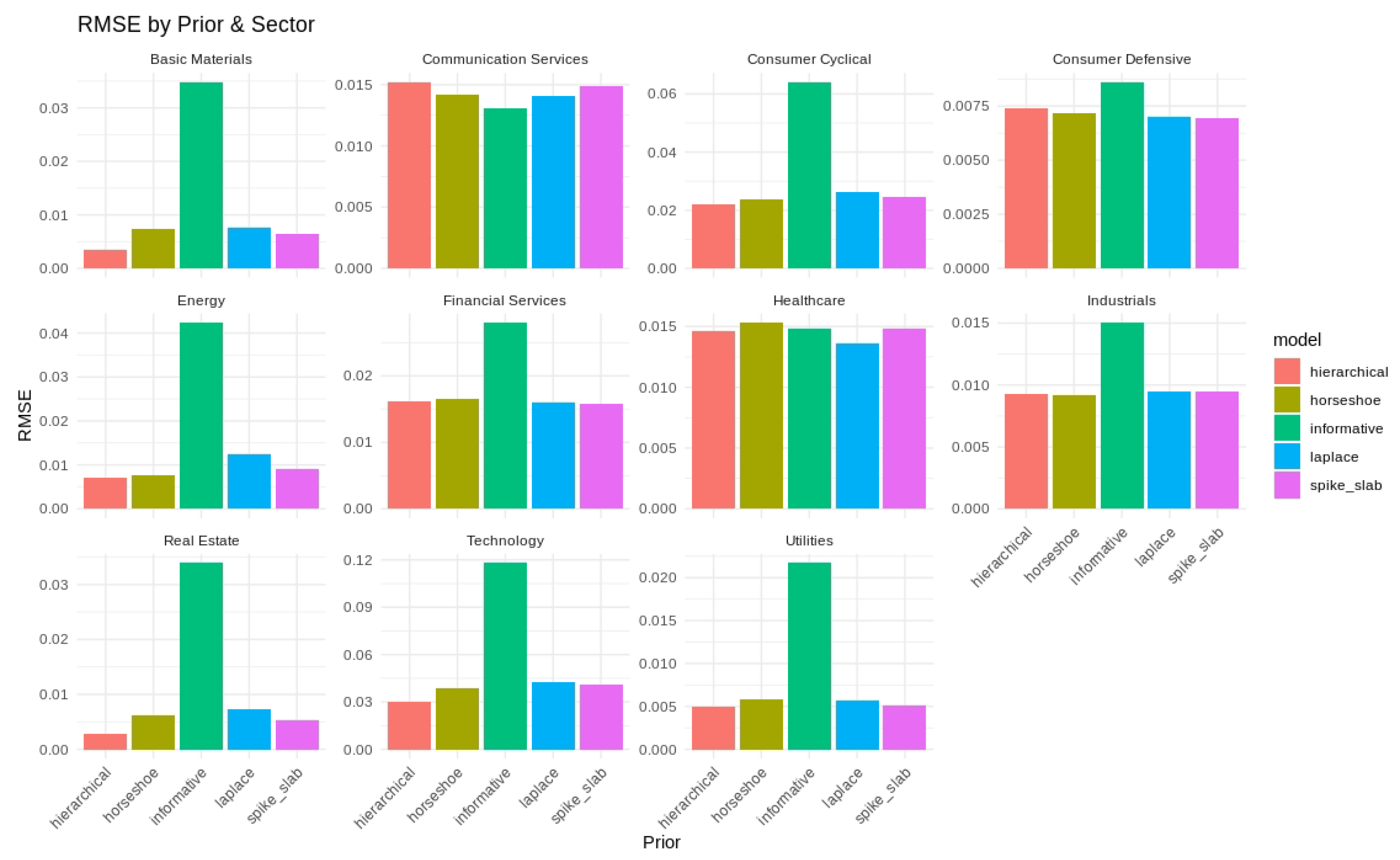

The sector-level RMSE values under each prior are shown in

Figure 6, and the average RMSE and MAE values are listed in

Table 7. The hierarchical and spike-and-slab priors yielded the smallest RMSE in multiple sectors, and horseshoe priors were found to be effective for larger fluctuations in the Consumer Cyclical and Financial Services sectors. The informative prior generally had higher errors, reflecting the value of regularization in a high-dimensional parameter space.

Summary of Findings

The findings in this real-data application align with our earlier simulation results. In the large-scale B-DARMA model, shrinkage priors reduced extraneous complexity and lowered forecast errors. The horseshoe, Laplace, and spike-and-slab priors limited the number of active coefficients and delivered stable predictions. Hierarchical priors performed similarly, in part because they partially pool information across related parameters, shrinking them toward a common distribution while still allowing differences where the data support them. Sectors with higher volatility, such as Technology, Communication Services, and Consumer Cyclical, appeared to benefit most from strong shrinkage, whereas more stable sectors like Utilities and Basic Materials performed comparably under all priors. Overall, these outcomes highlight the value of effective regularization in models with multiple lags and complex seasonality, especially in markets that experience rapid fluctuations.

6. Discussion

6.1. Comparisons Across Simulations and Real Data

Our three simulation studies demonstrated how prior selection interacts with model specification in B-DARMA. When the model order matched the true data-generating process (DARMA(2,1)), all priors yielded acceptable results, although the horseshoe and hierarchical priors produced slightly lower RMSE and better interval coverage. Overfitting by fitting B-DARMA(4,2) confirmed that strong shrinkage—particularly the horseshoe—helps suppress spurious higher-order coefficients and avoids inflating forecast errors. Conversely, underfitting remains impervious to prior choice, as omitting critical AR(2) and MA(1) terms led to uniformly higher biases and coverage shortfalls across all priors. All four shrinkage priors neutralized redundant lags, and any of them is preferable to an under-specified alternative.

These lessons translate directly to real data, where we intentionally specified a large-lag B-DARMA model for S&P 500 sector trading. Just as in the overfitting simulation, the horseshoe, Laplace, and spike-and-slab priors effectively shrank extraneous parameters and preserved forecast accuracy. Hierarchical priors provided comparably strong performance through partial pooling, whereas the informative prior yielded higher forecast errors in volatile sectors such as Energy and Technology. These empirical patterns mirror the simulation findings, reinforcing that the combination of a potentially over-parameterized model and minimal shrinkage can lead to unstable estimates and suboptimal forecasts.

Computation time. Using identical Stan settings (four chains, 1250 iterations, 500 warm-ups), the informative prior completed the fastest in about 10 min per chain and served as our baseline. Laplace added roughly 20 % to the wall-clock time (12 min), reflecting the heavier double-exponential tails that require more leapfrog steps. The horseshoe and hierarchical priors were slower by 40 % (14–15 min) because their global–local scale hierarchies force smaller step sizes during HMC integration. Spike-and-slab was the clear outlier, nearly doubling run-time (20 min) owing to the latent inclusion indicators that create funnel-shaped geometry. Practitioners with tight computational budgets might prefer the Laplace prior, while more aggressive sparsity (horseshoe, hierarchical, and spike-and-slab) simply warrants proportionally longer runs.

6.2. Implications and Guidelines

Overall, our results underscore three main points relevant to both simulated and real-world compositional time-series modeling:

Shrinkage priors mitigate overfitting. Horseshoe priors are especially adept at handling sparse dynamics and large parameter spaces, as shown by the minimal performance degradation in both the simulated and real overfitting scenarios.

Hierarchical priors offer robust partial pooling. They attain performance comparable to the horseshoe prior while retaining smooth shrinkage across correlated parameters, making them a flexible choice for multi-sector or multi-component series.

Model misspecification overshadows prior advantages. Underfitting in simulations, or failing to include essential lags in practice, leads to systematic bias and reduced coverage that shrinkage alone cannot remedy. Model identification and appropriate lag selection remain critical for accurate inference.

The S&P 500 data analysis underscores these points: the shrinkage priors consistently outperformed the informative prior in managing a high-dimensional model, yet sector-specific volatility still caused reduced accuracy. Sectors with greater day-to-day variability, such as Technology or Consumer Cyclical, benefited more from aggressive regularization than stable ones (e.g., Utilities and Basic Materials).

Incorporating a dynamic selection of lag structures or exploring alternative priors may further improve compositional forecasting in settings with complex seasonalities or extremely large parameter spaces. Meanwhile, practitioners should pair robust prior modeling with careful model diagnostics (e.g., residual checks and information criteria) to ensure that underfitting and overfitting are detected early.

Overall, these findings reinforce the need for carefully chosen priors, especially in high-dimensional compositional time-series contexts. The horseshoe, Laplace, and hierarchical priors successfully protect against overfitting while preserving essential signals, as illustrated by both the simulation and real-data (S&P 500) analyses. Nonetheless, fundamental model adequacy remains paramount, as even the best prior cannot rescue a structurally under-specified model. We recommend that analysts combine thorough sensitivity checks of priors with well-informed decisions about lag order, covariate inclusion, and potential seasonal effects in B-DARMA applications.

Code Availability

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}